recognition of information value

TRANSCRIPT

1 | P a g e | R e c o g n i t i o n o f I n f o r m a t i o n V a l u e

Recognition of Information Value

Introduction

For information to be recognized as an asset, it must have a measurable value. Value for information

comes from its use in achieving a value proposition, just like a patent facilitates a product to enjoy some

level of value. Information asset valuation must be able to withstand the scrutiny of an external audit,

requiring a value recognition process being highly predictable and repeatable.

The primary role of the Chief Data Officer (CDO) is the accountability of the organization’s information

assets, which, if done properly, will have a measurable positive influence on the overall achieved

revenue of the organization. It is a primary responsibility of the CDO to optimize the value associated

with information within an organization. This value will only be achieved when the information

catalyzes a value proposition. The purpose of this writing is to provide a framework for measuring the

revenue influence achievable by the activities of the CDO, as well as the interplay with the other leaders

accountable for driving value from information assets.

How Information is linked to organizational value

Information is a facilitator for the identification and determination of strategies and tactics as described

in the value propositions of the organization. When value is captured, created, extended or protected, a

portion of the achieved value is attributable to the information that facilitated its capture. The CDO is

responsible for ensuring the optimal use of the information available. The value of the information is

computed based on its participation in delivering organizational value in a way similar to other

intangible assets of the organization such as patents, trademarks and other intangible assets. There are

some key concepts that must be addressed prior to providing the process for determining of the

effectiveness of the CDO.

2 | P a g e | R e c o g n i t i o n o f I n f o r m a t i o n V a l u e

Figure 1 | Business Model Canvas as presented in Value Proposition Design, Strategyzer, 2014

The business models that drive organizational strategies and tactics are comprised of several

processes, each of which consume information. The graphical representation of the business

model is the Business Model Canvas, which is described in the Value Proposition Design

(Strategyzer, Osterwalder, 2014).

Each business model is driven by a storyboard which describes how value will be obtained from

the successful execution of a business model (InfoSight Partners, 2016).

Figure 2 | Vision Storytelling Canvas, InfoSight Partners, LLC, 2016

3 | P a g e | R e c o g n i t i o n o f I n f o r m a t i o n V a l u e

Rivers of information flow through the vision as depicted in the storytelling canvas, and when

collaborated amongst the actors participating in a specific strategy or tactic, influences the

success or failure of a value proposition. This influence is the measurable value of the intangible

information asset. The recognition of value achievable for information will be computed as a

percentage of the value proposition as negotiated by the Chief Data Officer and computed

similarly to royalties.

The value of information is enhanced when it is used in critical situations. For example,

information that helps Apple thwart off the next great competitor to the iPhone is worth much

more than information used to produce a standard analysis. Generally, the more critical

situation presented, the shorter the life span of the increased value for information. In the

equity markets, there is high value for information that is immediate and very little value for

information that is fifteen minutes old.

The CDO Revenue Recognition Road Map

There are several core activities which a CDO must drive to recognize value from information. Some of

these key activities, which we will discuss more fully are:

Driving a map which links the intersections of processes, actors and information. These

intersections are opportunities for achieving value from information, or potential information,

and can be similarly be considered as the relation between potential and kinetic energy. If the

intersection of information, process and actors is not utilized, actual value is not achieved. In

the digital economy, the intersections change more regularly than they have in the past, and it is

incumbent upon the CDO to maintain the current potential value opportunities.

Resistance is a measure of not using information in business processes for one reason or

another, similar to the flow of electricity avoiding resistance. If information is too difficult to

use, then it may not be requested even though it was available for a process. Possible

resistance reasons are

o information clutter,

o lack of information context and scope,

o accessibility of information and

o trustworthiness of information.

Figure 2 | Vision Storytelling Canvas, InfoSight Partners, LLC, 2016

4 | P a g e | R e c o g n i t i o n o f I n f o r m a t i o n V a l u e

Figure 3| Eradicating Resistance to using information, InfoSight Partners, 2016

The CDO in concert with the governance organization should be relentless in eradicating

information usage resistance.

A process can have three usage models, each of which impact the achievable value of

information. A process can be executed:

o For business-as-usual (BAU) conditions, in which the information is used to maintain

course,

o For non-business-as-usual (NBAU) conditions, in which the information is used to either

detect or navigate conditions which do not fit one or more expectations as specified in

the business storytelling canvas,

o Or for disruptive conditions, in which information is used to either detect or recast a

business model due to a sufficiently significant departure from the expectations as

specified in the business storytelling canvas.

Information carries a premium value for disruptive and NBAU business conditions, which a CDO

should map.

Orchestrating the recognition of information value

5 | P a g e | R e c o g n i t i o n o f I n f o r m a t i o n V a l u e

Information is a non-tangible asset of the organization. As such, it must pass the scrutiny of an audit as

must other assets of the organization. This mandates an orchestration layer which can stand the

scrutiny of an outside auditor. The orchestration process must use the potential value map as specified

by the CDO, the recorded requests for information for use in business processes and the information

valuation computations (similar to royalty computations). The orchestration layer must have controls

similar to other production processes, in this case the orchestration layer is secured for use by the data

asset manager (the data asset manager has similar responsibilities to other asset managers).

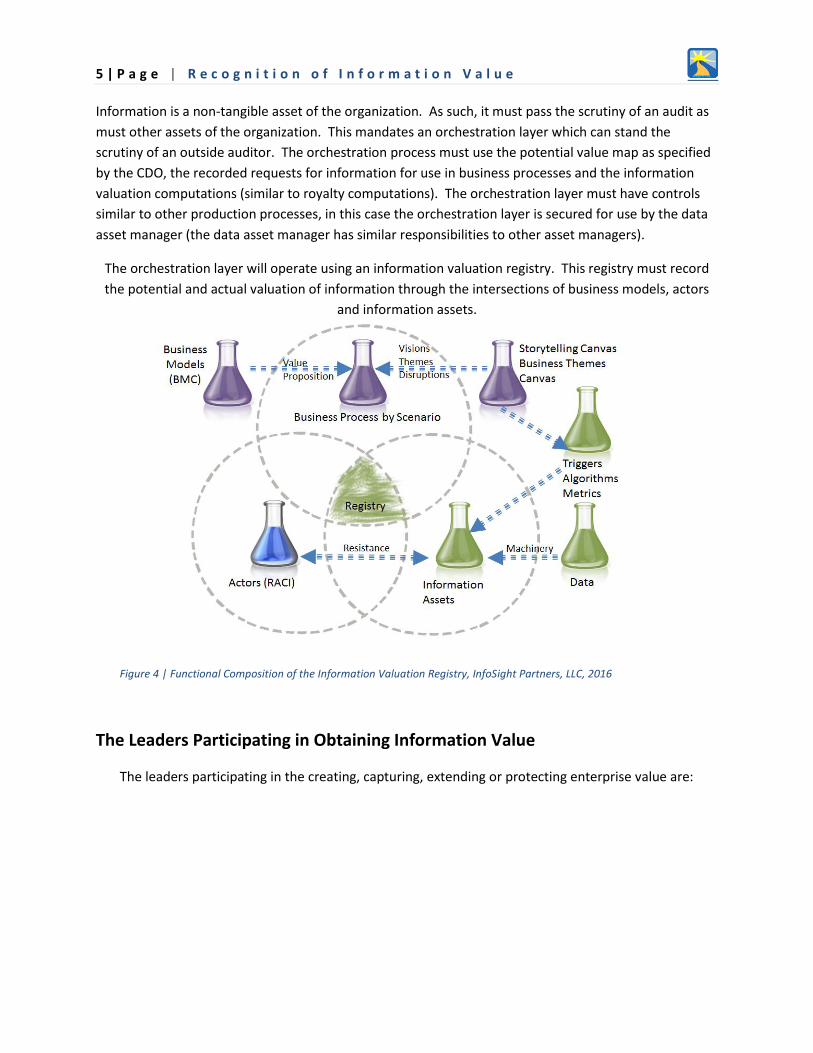

The orchestration layer will operate using an information valuation registry. This registry must record

the potential and actual valuation of information through the intersections of business models, actors

and information assets.

Figure 4 | Functional Composition of the Information Valuation Registry, InfoSight Partners, LLC, 2016

The Leaders Participating in Obtaining Information Value

The leaders participating in the creating, capturing, extending or protecting enterprise value are:

6 | P a g e | R e c o g n i t i o n o f I n f o r m a t i o n V a l u e

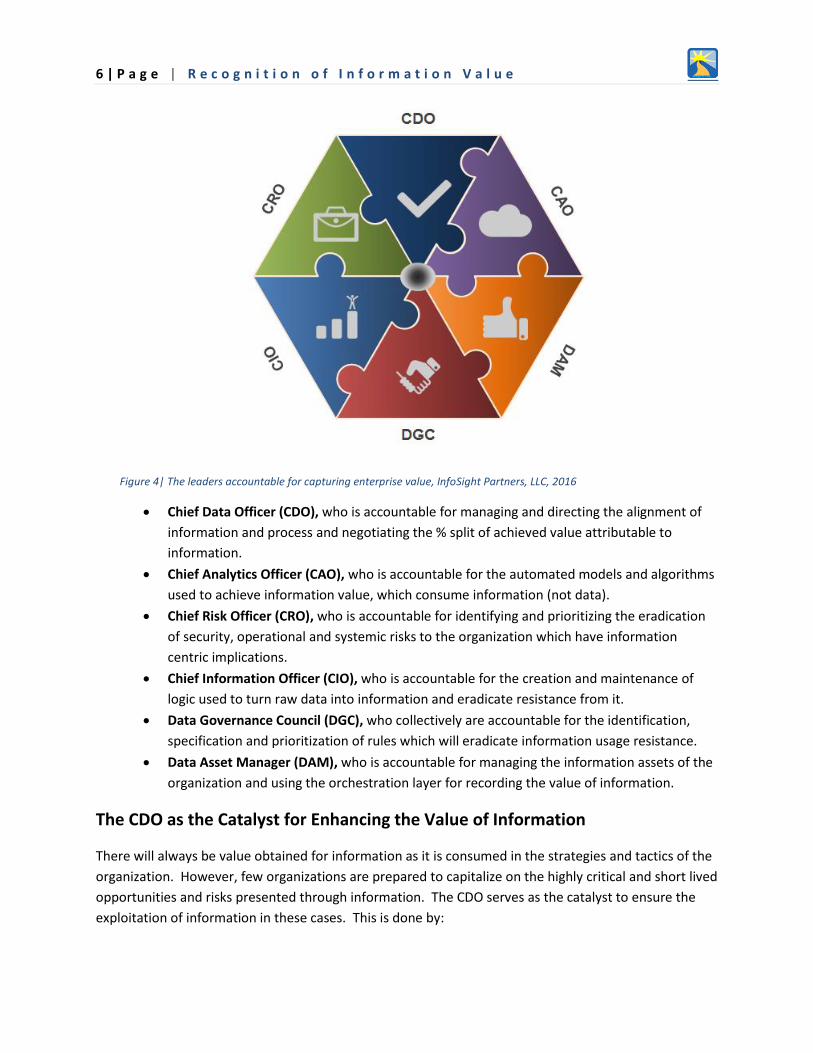

Figure 4| The leaders accountable for capturing enterprise value, InfoSight Partners, LLC, 2016

Chief Data Officer (CDO), who is accountable for managing and directing the alignment of

information and process and negotiating the % split of achieved value attributable to

information.

Chief Analytics Officer (CAO), who is accountable for the automated models and algorithms

used to achieve information value, which consume information (not data).

Chief Risk Officer (CRO), who is accountable for identifying and prioritizing the eradication

of security, operational and systemic risks to the organization which have information

centric implications.

Chief Information Officer (CIO), who is accountable for the creation and maintenance of

logic used to turn raw data into information and eradicate resistance from it.

Data Governance Council (DGC), who collectively are accountable for the identification,

specification and prioritization of rules which will eradicate information usage resistance.

Data Asset Manager (DAM), who is accountable for managing the information assets of the

organization and using the orchestration layer for recording the value of information.

The CDO as the Catalyst for Enhancing the Value of Information

There will always be value obtained for information as it is consumed in the strategies and tactics of the

organization. However, few organizations are prepared to capitalize on the highly critical and short lived

opportunities and risks presented through information. The CDO serves as the catalyst to ensure the

exploitation of information in these cases. This is done by:

7 | P a g e | R e c o g n i t i o n o f I n f o r m a t i o n V a l u e

Ensuring the inclusion of high value uses of information in the strategies and tactics of the

organization.

Devising a mechanism to measure the contribution of information to the strategies and tactics

of the organization.

There are several barriers to the successful use of information in high value circumstances, described in

this writing as the information value levers. The CDO, in concert with the other leaders of the

information assets of the organization, ensure that the information value levers facilitate the optimal

use of information in these high value circumstances. The CDO should own a scorecard that measures

the continued improvement of the information value levers, as the improvement of the information

value levers is a key measurement in the effectiveness of the CDO.

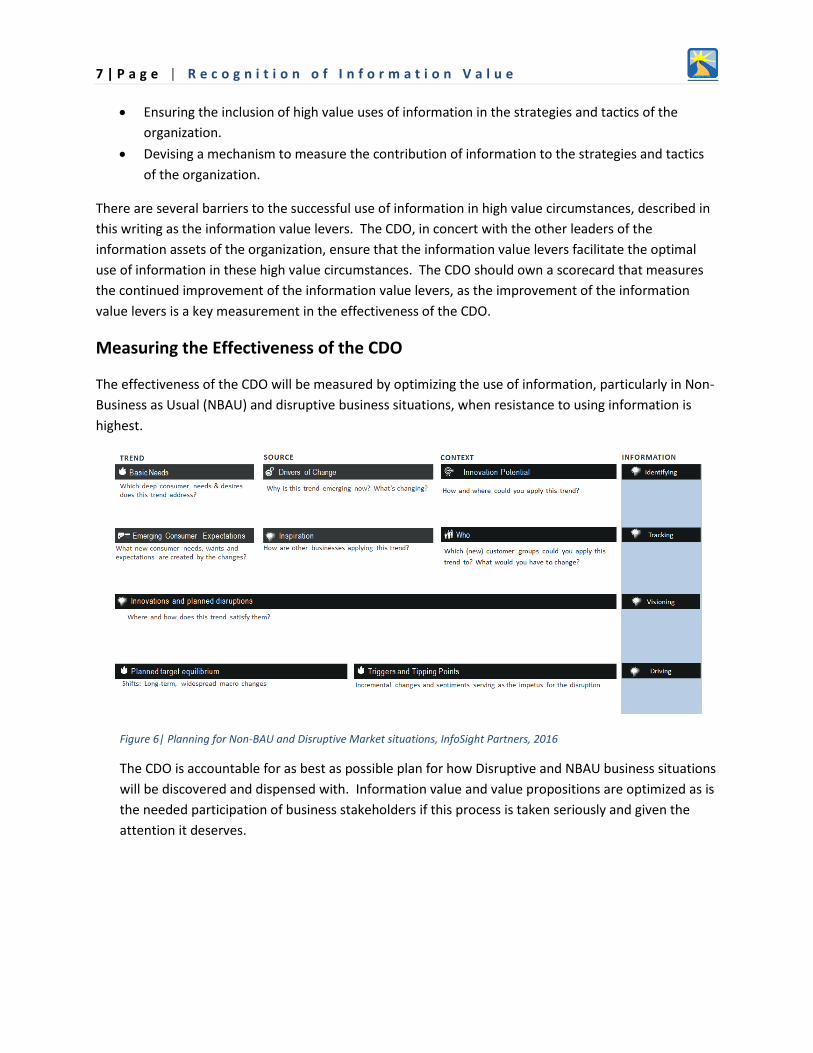

Measuring the Effectiveness of the CDO

The effectiveness of the CDO will be measured by optimizing the use of information, particularly in Non-

Business as Usual (NBAU) and disruptive business situations, when resistance to using information is

highest.

Figure 6| Planning for Non-BAU and Disruptive Market situations, InfoSight Partners, 2016

The CDO is accountable for as best as possible plan for how Disruptive and NBAU business situations

will be discovered and dispensed with. Information value and value propositions are optimized as is

the needed participation of business stakeholders if this process is taken seriously and given the

attention it deserves.

8 | P a g e | R e c o g n i t i o n o f I n f o r m a t i o n V a l u e

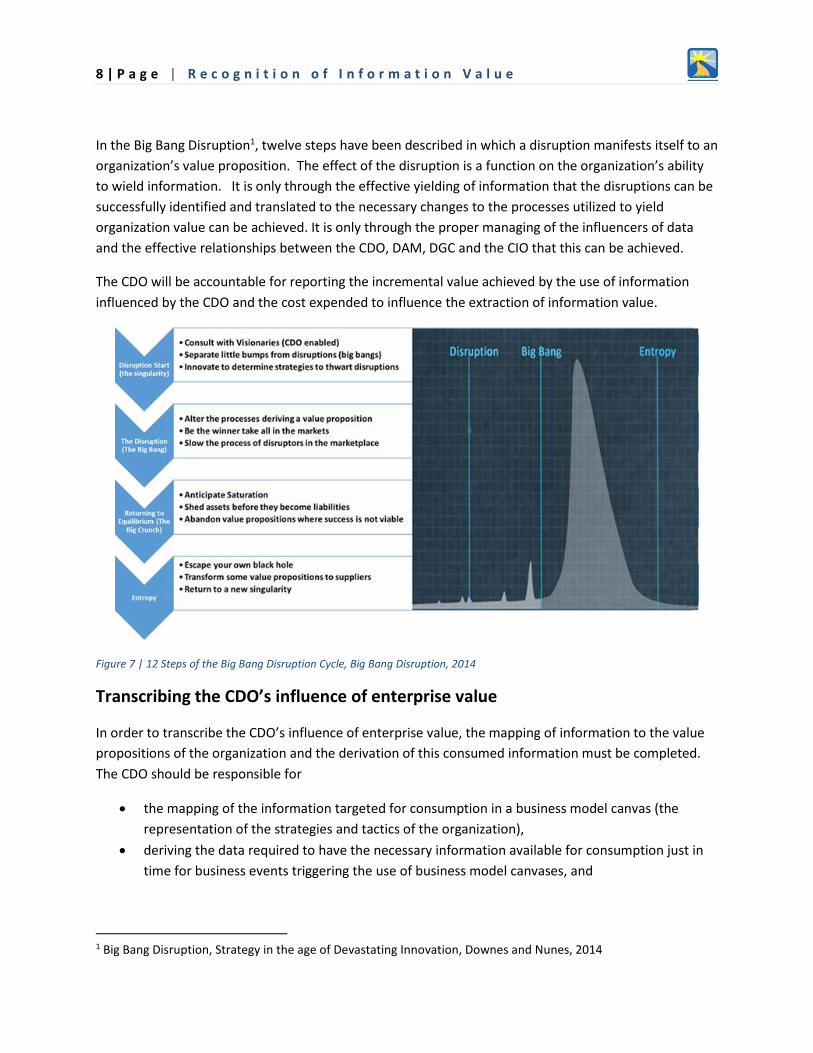

In the Big Bang Disruption1, twelve steps have been described in which a disruption manifests itself to an

organization’s value proposition. The effect of the disruption is a function on the organization’s ability

to wield information. It is only through the effective yielding of information that the disruptions can be

successfully identified and translated to the necessary changes to the processes utilized to yield

organization value can be achieved. It is only through the proper managing of the influencers of data

and the effective relationships between the CDO, DAM, DGC and the CIO that this can be achieved.

The CDO will be accountable for reporting the incremental value achieved by the use of information

influenced by the CDO and the cost expended to influence the extraction of information value.

Figure 7 | 12 Steps of the Big Bang Disruption Cycle, Big Bang Disruption, 2014

Transcribing the CDO’s influence of enterprise value

In order to transcribe the CDO’s influence of enterprise value, the mapping of information to the value

propositions of the organization and the derivation of this consumed information must be completed.

The CDO should be responsible for

the mapping of the information targeted for consumption in a business model canvas (the

representation of the strategies and tactics of the organization),

deriving the data required to have the necessary information available for consumption just in

time for business events triggering the use of business model canvases, and

1 Big Bang Disruption, Strategy in the age of Devastating Innovation, Downes and Nunes, 2014

9 | P a g e | R e c o g n i t i o n o f I n f o r m a t i o n V a l u e

measuring the impediments to ensuring the just in time availability of information and timely

execution of the enterprise strategies and tactics.

An effective CDO will be measured by their ability to influence the high value uses of information. The

net profit achieved by the CDO’s activities are the difference between the value achieved by the

intangible information assets of the organization and the cost of ensuring the usability of this

information through governance, data quality, metadata, lineage and other programs which mitigate

the challenges that thwart use of information in high profile circumstances.

Some examples of real high profile circumstances are

The valuation risk associated with negative international press coverage caused by a

manufacturing defect in automotive ignition switches.

The successful market capture of a large block of cell phone customers by eliminating their

contractual obligations to obtain device discounts.

The successful thwarting of an SEC audit and associated press coverage caused by undetected

trade irregularities not surfaced in compliance reporting.

Each of these examples require swift use of information to either capitalize on market opportunities or

thwart risks exposed through the successful use of information.

There are several activities all of which will be new to the organization which should be tracked to

determine if the measurement of information influence on the processes that derive organizational

value are effective. These new activities are require a coordination of the processes used to capture,

create, extend and protect organizational value, the information used to derive this organizational value

and the data transformed to serve as the consumed information. There are four organizational roles,

some of which may exist in today’s organization, these being the Chief Data Officer (CDO), the Data

Asset Manager (DAM), the Data Governance Council (DGC) and the Chief Information Officer (CIO).

Metrics should be created on the factors that limit the use of information and the effective coordination

of the CDO, the DAM, the DGC and the CIO.

Furthermore, the recording of value influenced by information and the resultant revenue must be

recorded for the entire justification of the investment made to ensure the optimal use of information

through the efforts of the CDO, DAM, DGC and CIO. Metrics to measure the revenue attributable to

information use as a percentage of organizational revenue should be created to measure the effective

participation of the CDO and the recording of revenue attributable to the efforts of the CDO.

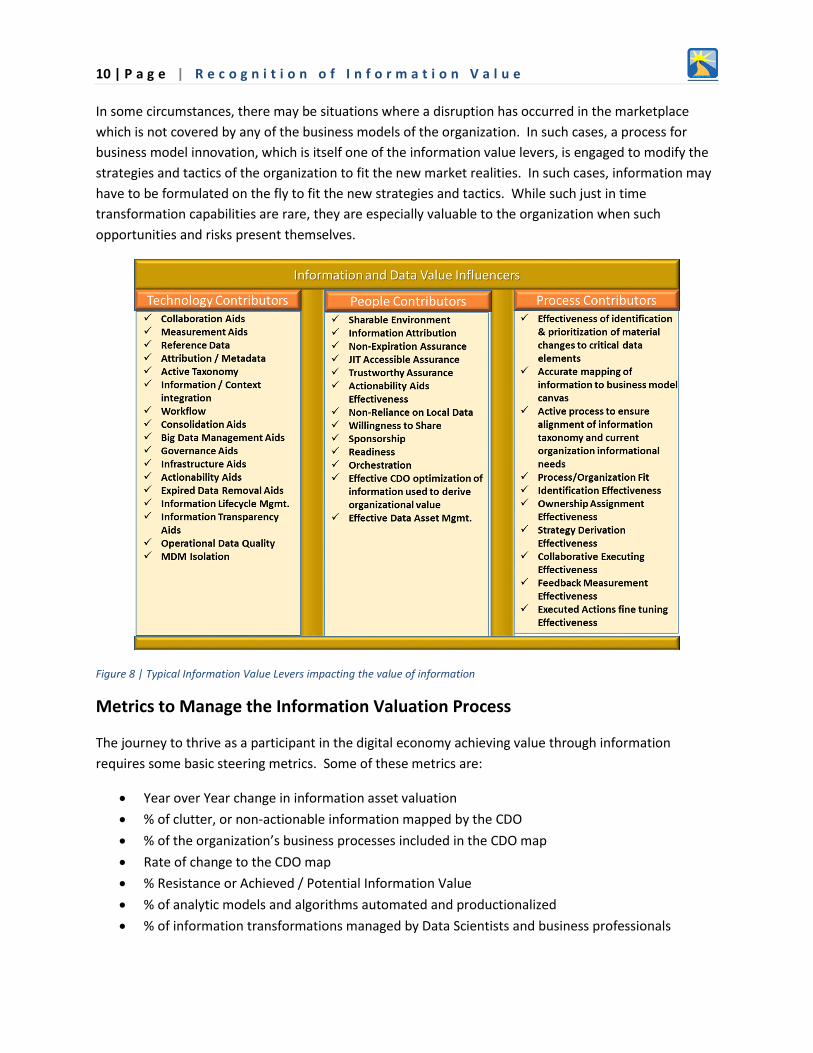

Improving the Information Value Levers

There are technology, people and process contributors that influence the valuation of information. All

of them are vehicles that, when successfully implemented, facilitate the use of information just in time

for the execution of strategies and tactics of the organization and the successful identification and

capitalization of opportunities and risks associated with the strategies and tactics of the organization.

10 | P a g e | R e c o g n i t i o n o f I n f o r m a t i o n V a l u e

In some circumstances, there may be situations where a disruption has occurred in the marketplace

which is not covered by any of the business models of the organization. In such cases, a process for

business model innovation, which is itself one of the information value levers, is engaged to modify the

strategies and tactics of the organization to fit the new market realities. In such cases, information may

have to be formulated on the fly to fit the new strategies and tactics. While such just in time

transformation capabilities are rare, they are especially valuable to the organization when such

opportunities and risks present themselves.

Figure 8 | Typical Information Value Levers impacting the value of information

Metrics to Manage the Information Valuation Process

The journey to thrive as a participant in the digital economy achieving value through information

requires some basic steering metrics. Some of these metrics are:

Year over Year change in information asset valuation

% of clutter, or non-actionable information mapped by the CDO

% of the organization’s business processes included in the CDO map

Rate of change to the CDO map

% Resistance or Achieved / Potential Information Value

% of analytic models and algorithms automated and productionalized

% of information transformations managed by Data Scientists and business professionals

11 | P a g e | R e c o g n i t i o n o f I n f o r m a t i o n V a l u e

% disruptive index (fraud, external forces, etc.) requiring alterations to business models and/or

the vision storytelling canvasses

About the Author

Mark Albala is the President of InfoSight Partners, LLC, a business consultancy which provides

financial and technology advisory services devised to facilitate focus into the value of information

assets. InfoSight Partners is lead by Mark Albala, who has served in technology and thought

leadership roles and serves as an advisor to analyst organizations and Lynn Albala, an officer of

the NJ State Society of CPAs (who leads the financial advisory services offered by InfoSight

Partners, LLC). Mark can be reached at [email protected].