recession keepshouse prices in the dumps in most european markets

TRANSCRIPT

Economic Research:

Recession Keeps House Prices In TheDumps In Most European Markets

Credit Market Services:

Sophie Tahiri, Economist, Paris (33) 1-4420-6788; [email protected]

Jean-Michel Six, EMEA Chief Economist, Paris (33) 1-4420-6705;

Media Contact:

Mark Tierney, London (44) 20-7176-3504; [email protected]

Table Of Contents

Belgium: Growth Is Cooling As Transactions Slow

France: Home Price Declines Appear To Be Gaining Momentum

Germany: Rising Prices Are Still Bucking The European Trend

Ireland: Starting A Long Road To Recovery

Italy: Economic Woes Are Dragging House Prices Down Further

The Netherlands: House Prices Are Under Pressure As Consumer

Confidence Declines

Portugal: The Market Still Sliding Despite Attempts To Revive It

Spain: A Glut Of Unsold Homes Will Keep The Market Depressed

U.K.: Mortgage Relief May Help Lift The Market

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 1

1123007 | 301015591

Economic Research:

Recession Keeps House Prices In The Dumps InMost European Markets

The bearish tendency in most of Europe's housing markets looks set to continue this year as the recession bites.

Standard & Poor's forecasts that house prices in most countries will stay on a downward path through the year, and

that declines will only slow or stabilize in 2014. Spanish households are feeling the pain most severely. We predict

prices will fall by 8% this year and by another 5% in 2014, as precarious economic conditions deter buyers and as

swathes of unsold housing stock drag on prices.

House prices in France also appear to be undergoing a protracted correction after decades of double-digit growth.

Tight fiscal policies, the anticipation of higher taxes over the coming 18 months, and a likely continued rise in

unemployment will keep the market declining by 5% this year and next year, according to our forecasts. What's more,

indicators show that residential real estate in France remains expensive by historical standards, with prices to incomes

still 30% above their long-term average at the end of 2012. In The Netherlands, Italy, Portugal, too, we expect that

falling household incomes in addition to mortgage lending constraints will continue to depress home prices.

Overview

• We forecast that residential real estate prices will keep falling in most European markets this year.

• Spain's housing market will likely suffer the heaviest year-on-year price falls of 8%, followed by the

Netherlands (5.5%) and France (5.0%).

• The German market, though, should still see moderate 3% price rises, and we predict U.K. prices will also rise

by 1.5% overall.

• The long-term prospects for many markets are more positive, however, as affordability ratios, measuring prices

to income, gradually rebalance.

Only in Germany and the U.K, are housing markets strengthening. The German residential property market is an

outlier in Europe. We forecast prices will appreciate by 3% this year and by another 3% next year, after much steeper

rises in 2011 and in the first half of 2012. We nevertheless see this as normalization rather than overheating given that

Germany's housing market didn't experience the boom over recent decades that many others saw. The

price-to-income ratio still finds the German housing market undervalued by 20%. In the U.K., supportive mortgage

measures will help foster a house-price rise of 1.5% this year after strengthening 2.3% last year.

Beyond the economic crisis, though, the prospects for most of Europe's housing markets appear more positive, in our

view. A shortage of housing supply, coupled with rising demographics in the Netherlands, France, and the U.K., to

name just three, should underpin prices over the longer run.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 2

1123007 | 301015591

Table 1

European Nominal House Prices (% change, quarter on quarter)

2009 2010 2011 2012 2013f 2014f

Belgium* 1.1 5.9 2.0 1.8 0.5 1.5

France (4.2) 7.7 3.7 (1.6) (5.0) (5.0)

Germany 1.6 2.7 6.8 3.5 3.0 3.0

Ireland (19.1) (11.0) (15.8) (6.1) (0.9) 0.0

Italy* (3.4) (1.4) (2.8) (4.0) (3.0) (1.0)

Netherlands (5.0) (1.0) (3.4) (7.3) (5.5) (1.0)

Portugal (0.6) 1.6 (0.8) (2.7) (1.5) 0.0

Spain (6.6) (3.3) (7.1) (10.5) (8.0) (5.0)

U.K. 0.3 3.8 (0.5) 2.3 1.5 1.0

Sources: S&P, OECD. *For these countries, 2012 nominal house prices are estimates. F--Forecast.

Belgium: Growth Is Cooling As Transactions Slow

Growth in Belgium's housing market looks set slow over the coming quarters as conditions for buyers become tighter.

Yet, prices and household debt are still moderate compared with the rest of Europe, which should prevent a downturn.

We now forecast that prices will rise by just 0.5% this year and by 1.5% in 2014 (see table 2).

Recent trends.

Home prices already cooled in the fourth quarter of 2012, with growth estimated at 1.6%, below the inflation rate.

Reflecting this weakness, house purchase transactions also slowed. Only 123,000 units changed hands in 2012

compared with more than 128,000 in 2011, reflecting a 4.2% fall, according to Belgium Statistics (see chart 1). The fall

in transactions was less marked in the Brussels region than in the rest of the country. Yet, consumer confidence

remains as depressed as during the 2008-2009 global financial crisis as austerity measures and rising unemployment

are cutting household incomes.

Future trends.

We expect only very little growth in house prices in nominal terms, and negative growth in real terms over the next

few years. Factors that have underpinned prices over the past decade will become less supportive, in our view. First,

we believe interest rates on loans, now at a historical low, will stabilize over the next few quarters as credit standards

tighten. We also expect borrowing capacity to be less supportive. Second, lower household incomes are unlikely to be

offset by a drop in the savings rate. In past years, Belgian households and investors were able to make larger down

payments to keep up with house price increases. The average down payment on residences rose significantly from

23% in 2004 to 37% of the property value in 2011. But it now seems to have reached a limit, and stabilized in 2012 at

over 36%. Furthermore, a fall in transactions is most often an early sign of cooling prices. Early indications available

for the first quarter of 2013 strongly suggest to us that the decline in transactions is gaining momentum.

However, we don't believe these negatives will add up to a downturn in Belgium's housing market. Home prices and

household debt are still moderate compared with other countries. What's more, the economy should start to recover

gradually in the second half of 2013, taking advantage to some extent the recovery in world trade.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 3

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Table 2

Belgian Housing Market Statistics

2009 2010 2011 2012e 2013f 2014f

Nominal house prices (% change year on year) 1.1 5.9 2.0 1.8 0.5 1.5

Real GDP (% change) (2.8) 2.4 1.8 (0.2) (0.1) 0.8

CPI inflation (%) 0.0 2.3 3.5 2.6 2.0 1.5

Unemployment rate 7.9 8.3 7.2 7.4 7.9 7.9

Sources: S&P, Eurostat, Banque Nationale de Belgique, OECD, Statistics Belgium. e--Estimated. f--Forecast.

Chart 1

Sources: Statistics Belgium, ECB, Organization for Economic Co-operation and Development (OECD), National Bank

of Belgium.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 4

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

France: Home Price Declines Appear To Be Gaining Momentum

We forecast that home prices will fall by 5% both this year and again next year as France undergoes a price correction

after decades of double-digit growth (see table 3).

Recent trends

Transactions on the French residential market fell significantly in 2012 by 12% (see chart 2), although prices appeared

still to show some resilience. Data for the final quarter of last year, however, suggest the downturn in transactions is

now starting to affect prices. The solicitors federation reported that prices in the greater Paris area (Ile de France)

dropped by 1.4% in the fourth quarter. Early indications for the first four months of 2013 also strongly suggest that the

price decline is gaining momentum.

We believe this downturn would likely have materialized sooner had it not been for favorable financial and fiscal

conditions that continued to support the housing market through most of 2012. As of February 2013, interest rates on

housing loans were still very low historically, at 3.13% on average. However, more fundamental factors have

progressively gained the upper hand. For the first time since 1984, household purchasing power fell in 2012 by 0.2%,

while unemployment rose from a year earlier. GDP growth last year was flat and indications for 2013 point to another

year of contraction in economic activity, by 0.2% according to our forecast, as fiscal tightening weakens domestic

demand. Meanwhile, some fiscal incentives ended during 2012, such as zero-interest rate loans for first-time buyers.

Authorities also withdrew special fiscal incentives for buy-to-let investors, causing a retreat in the number of

investment-based transactions. According to a large private real estate company, the percentage of buy-to-let investors

among total buyers had fallen to 12% at the start of 2013 from 22% a year ago.

Future trends

The recent price declines in France are likely not just a temporary phenomenon, but rather the harbinger of a more

protracted correction, in our opinion. We forecast the French economy overall will stay weak this year and into next

year. Domestic demand will continue to suffer from tight fiscal policies, and households are likely to protect their

savings in anticipation of higher taxes over the coming 18 months. A likely continued rise in unemployment will add to

overall uncertainties. Furthermore, fundamental housing market indicators show that residential real estate in France

remains expensive by historical standards. The affordability ratio (measuring prices to incomes) was still 30% above its

long-term average at the end of 2012. Although this indicator offers only a partial view of market conditions, we think

it highlights that France hasn't experienced a house-price correction observed elsewhere in Europe, and particularly in

the U.K., since 2007. France is also on the brink of a demographic shift as baby-boomers approach retirement age. This

will likely gradually change the market balance in favor of buyers, so adding downward pressure on prices.

That said, we don't expect a genuine collapse in prices. Our unchanged forecast of a 5% drop this year and again in

2014, appears to us a moderate correction after years of double-digit growth. We also think low interest rates will

continue to support prices over the next few years. A lack of attractive alternative long-term investment opportunities

is also likely to continue to provide a degree of support to residential real estate.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 5

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Table 3

French Housing Market Statistics

2009 2010 2011 2012 2013f 2014f

Nominal house prices (% change year on year) (4.2) 7.7 3.7 (1.6) (5.0) (5.0)

Real GDP (% change) (3.1) 1.7 1.7 (0.0) (0.2) 0.6

CPI inflation (%) 0.1 1.7 2.3 2.2 1.5 1.7

Unemployment rate 9.5 9.7 9.6 10.5 10.9 11.2

Sources: S&P, Eurostat, OECD, INSEE. f--Forecast.

Chart 2

Sources: Ministère de l'Ecologie du Développement et de l'Aménagement du Territoire, ECB, OECD, INSEE (Institut

National de la Statistique et des Etudes Economiques), ECB.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 6

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Germany: Rising Prices Are Still Bucking The European Trend

Although it has lost the growth momentum it showed in 2011 and in the first half of 2012, residential real estate in

Germany is still appreciating modestly. After changing the sample of properties included in its calculations, the OECD

has revised downward its previous price estimate for 2012. The market increased by 3.5% year on year last year in

nominal terms and by 1.8% when adjusted by inflation. Despite this revision, we maintain our forecasts for nominal

price growth of 3% this year and another 3% next year, owing to positive economic fundamentals such as a resilient

labor market (see table 4). We nevertheless see this as normalization rather than overheating given that Germany's

housing market didn't experience the boom over recent decades that many others saw.

Recent trends.

After recording a marked increase in the first part of 2012, housing construction growth calmed at the end of the year.

Total dwelling permits rose by only 4.8% (to 239,465 units) in 2012, after nearly 22% in 2011 (see chart 3). The

expansion of the housing supply reflects a surge in demand due to strong immigration and the attraction of the

property market as an investment. A more flexible supply is likely to reduce house-price volatility over time.

Historically low financing costs and good income prospects continued to stimulate growth in mortgage lending last

year. Loans for housing purchases rose by 2.1% in February, which is the same rate registered in mid-2006 before the

financial crisis.

Future trends.

As reflected in a recent bank lending survey that showed a perceptible tightening in credit standards for housing loans,

and given banks' conservative practices, we believe that house-price rises will stay contained. We expect that the

Bundesbank will remain vigilant and will implement effective and prudent supervision should prices become very

volatile. Nonetheless, fundamentals continue to support a further rise in the residential market, in our view. Surveys by

the consumer researcher GFK ("Gesellschaft für Konsumforshung") point to a highly optimistic consumer climate. This

rests not least on the positive labor market situation and strong rise in earnings. We forecast that unemployment will

fall slightly to 5.7% in 2013 and to 5.6% in 2014 (see table 4). We also project that wages will continue to rise in

Germany, as signaled by the wage agreements for the steel industry in March. The affordability index, measured as

price to income, also finds the German housing market undervalued by 20%. The ratio is well below the long-term

average for the index (chart 3). The price-to-rent ratio similarly points in this direction.

Table 4

German Housing Market Statistics

2009 2010 2011 2012 2013f 2014f

Nominal house prices (% change year on year) 1.6 2.7 6.8 3.5 3.0 3.0

Real GDP, % change (5.08) 4.2 3.0 0.7 0.8 1.5

CPI inflation (%) 0.2 1.2 2.5 2.1 1.8 1.7

Unemployment rate 7.8 7.1 6.0 5.5 5.7 5.6

Sources: S&P, Eurostat, OECD, Deutsche Bundesbank. e--Estimate. f--Forecast.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 7

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Chart 3

Sources: ECB, OECD, Deutsche Bundesbank.

Ireland: Starting A Long Road To Recovery

The heavy slump in the Irish housing market appears to have bottomed out. House prices posted their first

quarter-on-quarter increase in 22 quarters in December 2012 and we forecast that prices will stabilize this year and

next, after falling 6.1% in 2012 (see table 5). But even if prices are no longer in free fall, we think a recovery is still a

long way off. Tight credit supply, and excess capacity suggest that prices in Ireland may recover only slowly.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 8

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Recent trends.

Limited new construction is helping the market stabilize. New construction contracted by 19% in 2012, with only 8,488

new units completed compared with 10,480 in 2011. This is well below the 2006 peak of 90,000 units, and below

potential demand. This suggests to us that the overhang of unoccupied properties should slowly erode. Some larger

conurbations where there is no large supply overhang, such as Dublin, Galway, or Cork, have even registered price

rises. Another sign of improvement was an upturn in transactions. The Property Services Regulatory Authority

indicates that transactions rose significantly in 2012, although they abated somewhat in the first quarter of 2013--they

were up 37.1% last year, but decreased by 1.1% in March 2013 year on year. This is because home buyers wanted to

benefit from the mortgage interest relief that ended on Jan. 1, 2013. Similarly, lending for house purchases increased

by 5.4% in February from the previous year (see chart 4). In particular, outstanding housing loans surged by nearly 8%

in December 2012 from the previous month.

Future trends.

The Irish property market will likely continue to stabilize for the next two years, in our view. Price-to-income and

price-to-rent ratios have returned to their long-term average (see chart 4), indicating that prices have reached an

equilibrium. Economic recovery in 2013 and 2014 should also support demand for housing. We expect real GDP to

rise 1.2% this year and 2.2% next year, while unemployment should slowly decline to 14.1% in 2014 from 14.9% in

2012 (see table 5).

Still, while momentum appears to be building in the housing market, the rate of increase in transactions and house

lending this year may not exceed 2012, as mortgage interest relief has ended. What's more, a new local property tax

coming into force later this year may also drag on the price upturn.

Table 5

Irish Housing Market Statistics

2009 2010 2011 2012 2013f 2014f

Nominal house prices (% change year on year) (19.1) (11.0) (15.8) (6.1) (0.9) 0.0

Real GDP (% change) (5.5) (0.8) 1.4 0.4 1.2 2.2

CPI inflation (%) (1.7) (1.6) 1.1 2.1 1.7 1.8

Unemployment rate 11.9 13.7 14.4 14.9 14.6 14.1

Sources: S&P, Eurostat, OECD, Central Statistics Office. f--Forecast.

Chart 4

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 9

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Sources: Property Services Regulatory Authority, ECB, OECD, Central Statistics Office Ireland.

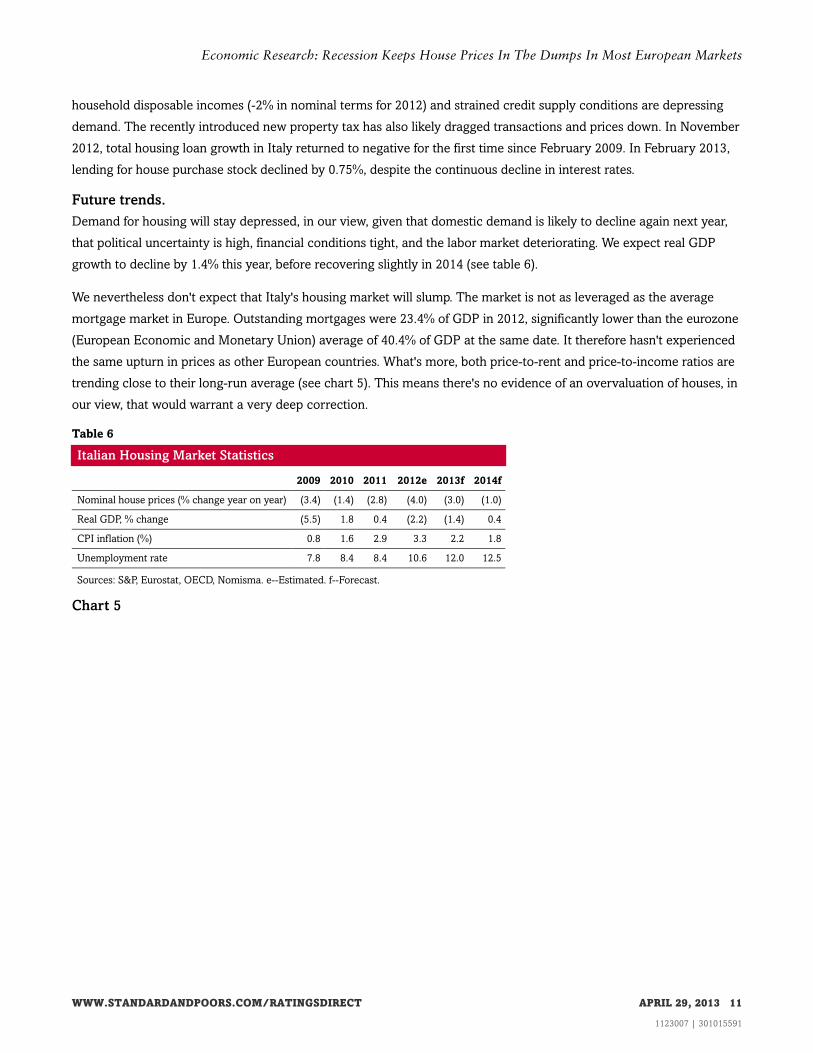

Italy: Economic Woes Are Dragging House Prices Down Further

After revising our forecasts for the Italian economy downward, we anticipate that housing prices will also dip further

this year, by 3% (see table 6). We don't envisage any recovery before 2015.

Recent trends.

"Agenzia del Territorio", the public agency providing cadaster-related and land registry services, revised downward its

estimates of house sales for 2012 to about 444,000 units. This is only half that of 2006, when transactions peaked. It is

also down by 26% on last year (see chart 5). This was accompanied by a 4% fall in prices last year. Contracting

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 10

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

household disposable incomes (-2% in nominal terms for 2012) and strained credit supply conditions are depressing

demand. The recently introduced new property tax has also likely dragged transactions and prices down. In November

2012, total housing loan growth in Italy returned to negative for the first time since February 2009. In February 2013,

lending for house purchase stock declined by 0.75%, despite the continuous decline in interest rates.

Future trends.

Demand for housing will stay depressed, in our view, given that domestic demand is likely to decline again next year,

that political uncertainty is high, financial conditions tight, and the labor market deteriorating. We expect real GDP

growth to decline by 1.4% this year, before recovering slightly in 2014 (see table 6).

We nevertheless don't expect that Italy's housing market will slump. The market is not as leveraged as the average

mortgage market in Europe. Outstanding mortgages were 23.4% of GDP in 2012, significantly lower than the eurozone

(European Economic and Monetary Union) average of 40.4% of GDP at the same date. It therefore hasn't experienced

the same upturn in prices as other European countries. What's more, both price-to-rent and price-to-income ratios are

trending close to their long-run average (see chart 5). This means there's no evidence of an overvaluation of houses, in

our view, that would warrant a very deep correction.

Table 6

Italian Housing Market Statistics

2009 2010 2011 2012e 2013f 2014f

Nominal house prices (% change year on year) (3.4) (1.4) (2.8) (4.0) (3.0) (1.0)

Real GDP, % change (5.5) 1.8 0.4 (2.2) (1.4) 0.4

CPI inflation (%) 0.8 1.6 2.9 3.3 2.2 1.8

Unemployment rate 7.8 8.4 8.4 10.6 12.0 12.5

Sources: S&P, Eurostat, OECD, Nomisma. e--Estimated. f--Forecast.

Chart 5

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 11

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Sources: Agenzia del Territorio, Nomisma, ECB, OECD.

The Netherlands: House Prices Are Under Pressure As Consumer ConfidenceDeclines

The Dutch housing market is still in the doldrums because a deteriorating labor market and uncertainty surrounding

pensions is putting off buyers. We still forecast home price declines of 5.5% for 2013, but only a 1% decline for 2014

(see table 7). Over the longer view, however, we anticipate that the economy will improve, and housing will become

more affordable, leading to a stabilization of prices. The agreement between the government and social partners on

postponing €4.3 billion worth of spending cuts may also positively affect household incomes and consumer

confidence.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 12

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Recent trends.

Housing transactions spiked in the fourth quarter of 2012 as many first-time buyers took advantage of more

advantageous fiscal treatment that ended in December 2012. As of Jan. 1, 2013, new mortgage holders are obliged to

pay off their mortgages on an annuity basis to be eligible for mortgage interest relief. As a result, prices only declined

by 0.2% on a quarterly basis, while house sales rose by 55% in the fourth quarter of 2012. For the full year, prices

declined by 7.3% while transactions fell by 2.9% (see chart 8).

Households have remained cautious because economic uncertainty and austerity measures are cutting their

purchasing power. This is limiting their borrowing capacity, although interest rates on mortgages continue to slowly

decline and are at about 4.0% (see chart 6). In our view, the 7.4% increase in housing loans in February 2013 is

misleading. When including mortgage loans transferred by monetary financial institutions and special-purpose

vehicles, the yearly growth rate trended downward to 1.4% in that month.

Future trends.

We expect prices to keep falling this year because economic growth in the Netherlands will remain anemic in 2013 and

unemployment will rise to 6.3%. Both the decline in purchasing power and rise in unemployment will keep households

very cautious. In the longer term, though, we believe prices should bottom out as the economy turns more positive.

Among the more fundamental factors, supply shortage continues to worsen because construction output has for some

years been below the rate before the financial crisis. Permits for residential building fell by 35% in 2012 on the previous

year and were 60% lower than their 2006 peak. The fall in the supply of new homes, in addition to the steady increase

in the number of households, should help to stabilize the market. Added to this, the price-to-income ratio is

approaching its long-term average, making houses more affordable.

Table 7

Dutch Housing Market Statistics

2009 2010 2011 2012 2013f 2014f

Nominal house price (% change year on year) (5.0) (1.0) (3.4) (7.3) (5.5) (1.0)

Real GDP (% change) (3.7) 1.6 1.0 (0.9) (0.5) 0.8

CPI inflation (%) 1.0 0.9 2.5 2.8 2.0 1.4

Unemployment rate 3.7 4.5 4.4 5.3 6.3 6.5

Sources: S&P, Eurostat, Kadaster, OECD, CBS Statistics Netherlands. F--forecast.

Chart 6

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 13

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Sources: Central Bureau of Statistics Netherlands (CBS), ECB, OECD, Kadaster.

Portugal: The Market Still Sliding Despite Attempts To Revive It

The Portuguese housing market is continuing to slide gradually as demand falters. Households are unwilling to buy

homes because consumer confidence is falling, unemployment looks set to rise to 18% this year, and earnings are

declining. We now forecast that house prices will fall by 1.5% before stabilizing in 2014 (see table 8).

Recent trends.

In 2012, residential retail prices dropped by 2.7% on the previous year. Activity in Portugal's residential construction

sector has continued to weaken, as shown by a 35% year-on-year decline in permits issued for residential buildings last

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 14

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

year (see chart 7). Given mortgage lending constraints, loan growth continued to plunge, even though interest rates fell

to historic lows of 3.28% in February 2013 (see chart 7). In the same month, total housing loans in Portugal dropped by

3.6% to €109.9 billion from a year earlier (see chart 7). The bank lending survey for the first quarter of 2013 pointed

again to further tightening in mortgage lending, owing to the increasing cost of funding, balance-sheet constraints, and

less favorable expectations regarding general economic activity. The decline in demand for house purchases induced

some Portuguese banks to offer thousands of repossessed homes at reduced prices to revive demand. The Portuguese

government is also trying to attract foreign buyers to the country's property market. It announced last year it would

grant special resident permits to non-EU citizens who invest more than €500,000 in real estate.

Future trends.

In spite of bank and government initiatives, we still expect that the housing market will stay depressed in the short

term, owing to deteriorating labor market conditions, lower confidence, adjustment of permanent incomes, and tight

access to credit. Portuguese household debt is still very high, both in historical terms and in comparison with other

eurozone countries. We therefore expect it to keep declining.

Nevertheless, we believe Portugal's property price declines will stay relatively limited. Unlike Spain or Ireland, Portugal

doesn't have an oversupply of housing, owing to sluggish economic performance and decades of rent controls. Prices

have barely increased in real terms since the 1990s. What's more, the price-to-rent ratio is trending downward and is

nearly 12% below its long-term average. The price-to-income ratio, on the other hand, has been increasing since 2011,

suggesting that incomes are falling at a more rapid pace than prices.

Table 8

Portuguese Housing Market Statistics

2009 2010 2011 2012 2013f 2014f

Nominal house prices (% change year on year) (0.6) 1.6 (0.8) (2.7) (1.5) 0.0

Real GDP, % change (2.9) 1.4 (1.6) (3.2) (1.5) 0.9

CPI inflation (%) (0.9) 1.4 3.6 1.5 1.5 1.8

Unemployment rate 10.6 12.0 12.9 16.0 18.0 15.0

Source: S&P, Eurostat, BIS/private sector. f--forecast.

Chart 7

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 15

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Source: OECD, ECB.

Spain: A Glut Of Unsold Homes Will Keep The Market Depressed

We see no signs of improvement in Spain's housing market given the precarious economic conditions and the heavy

weight of unsold housing stock. Adding to this oversupply, Spain's "bad bank" SAREB has revealed plans to sell 45,500

housing units over the next five years, representing one-half of the housing stock in its portfolio. Considering the bank's

large stock--it owns about 30% of all new homes for sale--this asset liquidation will very likely determine the pace of

price declines. Assuming SAREB's disinvestment is gradual, we forecast that house prices in Spain will fall by 8.0% this

year and by another 5% in 2014 (see table 9).

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 16

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Recent trends.

Home prices plunged by 10.5% in 2012 from a year earlier and have now fallen 28% from their peak in March 2008.

The rapid increase in unemployment--expected to reach nearly 27% in 2013--alongside severe fiscal consolidation and

tight financial market conditions are hitting households' purchasing power and weakening their borrowing capacity.

What's more, high indebtedness will continue to drain funds from household budgets, leaving little room for saving.

Indeed, household investments have halved over the past five years.

Transactions, meanwhile, have stayed very low: 325,000 homes exchanged hands in January for the last 12 months,

down by 6.4% from January last year (see chart 8). The Spanish market is still saddled with an excess supply of about

680,000 units, according to the Spanish housing ministry's official estimates for 2011. The number of new homes

completed last year dropped to 133,000 from a peak of about 760,000 units in 2006, suggesting that the adjustment

process is still under way.

Future trends.

We see little opportunity for Spanish households to become much more solvent given that prices are still falling,

purchasing power is declining, and interest rates are stabilizing. This should keep demand very depressed. The sizable

chunk of idle housing stock will also prevent an early recovery in residential property prices. Price-to-income and

price-to-rent ratios lead us to expect a further 20% drop in housing prices over the next four years. Yet, given serial

correlation, there could be some degree of overshooting in house prices before they return to their long-term

equilibrium, in our view.

Table 9

Spanish Housing Market Statistics

2009 2010 2011 2012 2013f 2014f

Nominal house prices (% change year on year) (6.6) (3.3) (7.1) (10.5) (8.0) (5.0)

Real GDP (% change) (3.7) (0.3) 0.4 (1.4) (1.5) 0.6

CPI inflation (%) (0.2) 2.0 3.1 2.4 2.0 1.0

Unemployment rate 18.0 20.1 21.7 25.1 26.8 26.5

Sources: S&P, Eurostat, Banco de Espana, OECD. F--Forecast.

Chart 8

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 17

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Sources: Instituto Nacional de Estadistica (INE), ECB, OECD, Banco de Espana.

U.K.: Mortgage Relief May Help Lift The Market

Prospects for the U.K. housing market are improving, in our opinion, thanks to government mortgage relief measures

to support homebuyers, as well as tight housing supply. Yet, price-to-income ratios suggest homes are still overvalued.

On balance, therefore, we forecast house prices will rise by a moderate 1.5% this year and by 1% in 2014 (see table

10).

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 18

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Recent trends.

In 2012, prices rose by 2.3% across the U.K., according to OECD estimates. Yet, this represented a 0.4% decline in real

terms, when adjusted for inflation. Nationwide statistics also mask a widely divergent picture across the country.

London and the south of England have seen positive house price growth over the past year, while prices have

weakened in the midlands and the north.

Transactions, meanwhile, were up 4.9% in February on a last-12-months basis (see chart 9). But although sales are

trending upward, they are still 45% below 2007. Housing starts in the U.K. dropped by 11% to 98,290 units in 2012.

This is well below the 233,000 new homes per year that housing experts say the U.K. needs to meet the predicted

expansion in the number of households. The gap between demand and supply will therefore continue to widen.

Mortgage approvals were up slightly by 0.7% in February this year from a year ago. Yet, home mortgage lending is still

40% below figures before the financial crisis. This is because mortgage providers are limiting the volume of mortgages

available, particularly to first-time buyers, by reducing loan-to-value ratios. That said, the Bank of England's

funding-for-lending scheme has made it cheaper for households that previously had access to credit to obtain loans.

Future trends.

We believe the government's new mortgage support measures are likely to help revive the market. The new scheme

offers buyers with a deposit of at least 5% an interest-free loan of up to 20% of the value of most new homes. A second

measure that targets first-time buyers consists of a government mortgage guarantee that assists buyers of homes worth

up to £600,000.

Strong demand for housing should also help lift the U.K. housing market over the coming years. There is unlikely to be

a substantial increase in housing supply in the near term. Furthermore, government and Bank of England measures are

pushing down interest rates and increasing buyer solvency.

Still, the house price-to-income ratio suggests that prices 20% above their long-term average. This is why we expect

that prices will only rise moderately.

Table 10

U.K. Housing Market Statistics

2009 2010 2011 2012 2013f 2014f

Nominal house prices (% change year on year) 0.3 3.8 (0.5) 2.3 1.5 1.0

Real GDP (% change) (4.0) 1.8 0.9 (0.0) 0.6 1.3

CPI inflation (%) 2.2 3.3 4.5 2.8 2.8 2.5

Unemployment rate 7.5 7.9 8.0 8.0 8.5 8.0

Sources: S&P, Eurostat, OECD, Department for Communities and Local Government. f--Forecast.

Chart 9

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 19

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

Sources: HM Revenue & Customs, Bank of England, OECD, Department for Communities and Local Government.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 20

1123007 | 301015591

Economic Research: Recession Keeps House Prices In The Dumps In Most European Markets

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P

reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,

www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription) and www.spcapitaliq.com

(subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information

about our ratings fees is available at www.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective

activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established

policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain

regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion. S&P

Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any

damage alleged to have been suffered on account thereof.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and

not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase,

hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to

update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment

and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does

not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be

reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part

thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval

system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be

used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or

agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not

responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for

the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL

EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR

A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING

WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no

event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential

damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by

negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Copyright © 2013 by Standard & Poor's Financial Services LLC. All rights reserved.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 29, 2013 21

1123007 | 301015591