recent dynamics in the rare-earth sector and their effects …€¦ · · 2017-11-22their effects...

TRANSCRIPT

Los Angeles Convention Center, Los Angeles, California, USA!

Recent Dynamics in the Rare-Earth Sector and their Effects on the Motion-Control Supply Chain

Gareth P Hatch, PhD!Founding Principal, Technology Metals Research, LLC!

Motion Control 2013!October 15-17, 2013!

A note about Technology Metals Research (TMR)!

2!Technology Metals Research!

TMR provides market intelligence, commentary and analysis on critical & strategic materials such as the rare earths and other technology metals & materials

We help companies, investors, government agencies & individuals do their homework on the challenges and opportunities associated with these materials

Disclaimer & Cautionary Statement!

The information contained in this presentation is provided by Technology Metals Research, LLC (“TMR”) and the author, for general educational purposes only. Certain information herein is based on third-party sources that are believed to be reliable, but whose accuracy is not guaranteed. It may also contain statements that could constitute forward-looking statements, describing expectations, opinions or guidance that are not statements of fact. Forward-looking statements may include, among others, statements regarding future market supply and demand, government policies, and other market dynamics, or the assumptions underlying any of the foregoing. In this presentation, words such as "may", "could", "would", "will", "likely", "believe", "expect", "anticipate", "intend", "plan", “goal”, "estimate" and similar words and the negative forms thereof are used to identify forward-looking statements.

Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that are beyond TMR's control, and which may cause actual results, level of activity, performance or achievements to be materially different from those expressed or implied by such forward-looking statements.

This presentation is provided on an “as is” basis, and neither TMR nor the author make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the third-party information, data or charts contained herein, for any purpose. Use of all information herein is voluntary, and reliance on it should only be undertaken after an independent review of its accuracy, completeness, efficacy and timeliness. Any reliance placed on such information is therefore strictly at the risk of the user.

In no event will TMR or the author be held liable for any loss or damage including without limitation, indirect or consequential loss or damage, or any loss or damage whatsoever arising from loss of data or profits arising out of, or in connection with, the use of this presentation or the information contained within it.

Overview!

Introduction Rare-Earth Demand Current Rare-Earth Supply Chinese Mining & Export Quotas Effects of Price Volatility The Politics of Rare Earths Other Supply & Demand Issues Future Sources of Rare-Earth Supply Final Thoughts

Introduction

Recent Dynamics in the Rare-Earth Sector and!their Effects on the Motion-Control Supply Chain!

Permanent magnets!

Forces generated by permanent magnets are proportional to the square of the magnetic induction (B)

Rare-earth permanent magnets (REPMs) produce the highest B of any magnet material

The so-called light rare earths present “channel” the magnetism of ferromagnetic transition metals (Fe, Co)

Resistance to demagnetization (coercivity) in Nd-Fe-B magnets can be enhanced by adding so-called heavy rare earths

Coercivity is important at higher operating temperatures and when demagnetizing fields are present in the motor

6!Introduction!

Many motors use permanent magnets!

Wide variety of motor topologies Wide variety of magnets for permanent-magnet motors

• Hard ferrite • Bonded Nd-Fe-B (rare-earth-based) • Sintered Nd-Fe-B (rare-earth-based) • Sm-Co (rare-earth-based)

Of course COST is a major factor Certain motor applications require the power / torque

density that rare-earth-based magnets can bring Focus is on the rare earths that go into such magnets

7!Introduction!

What are the rare earths?!

A group of chemical elements that exhibit special magnetic, electronic, catalytic and optical properties

Rare earths are enablers – they can have a profound effect on the performance of a wide range of complex engineered systems and hi-tech devices

8!Introduction!

Which are the 17 rare-earth elements?!

9!Introduction!!

Source: Technology Metals Research!

The rare-earth industry focuses on 15 elements!

10!Introduction!!

Source: Technology Metals Research!

The rare earths can be divided into sub-groups!

Definitions relate to the processing of concentrates Used by metallurgists & flow-sheet engineers Not always used elsewhere in the industry

• Sm, Eu & Gd as lights on the basis of electronic structure • Eu & Gd frequently grouped with the heavies

Be sure to know which convention is being used • Make sure to compare “apples to apples”

11!Introduction!

Source: Technology Metals Research!

The magnet-related rare earths!

For commercial permanent-magnet materials: • Sm-Co type: Sm (Gd, Pr) • Nd-Fe-B type: Nd, Pr, Dy, Tb • Sm-Fe-N type: Sm

12!Introduction!

Source: Technology Metals Research!

The “alphabet soup” of rare-earth acronyms!

Rare-earth element – REE Rare-earth oxide – REO Light REE / REO – LREE / LREO Medium REE / REO – MREE / MREO Heavy REE / REO – HREE / HREO Critical REE / REO – CREE / CREO Total REE / REO – TREE / TREO Rare-earth permanent magnet - REPM

13!Introduction!

Why should I care about non-magnet-related REEs?!

REEs are chemically very similar to each other – thus: • They are always found together • They have to be mined together

They are very difficult to separate from each other • They require complex processing routes, e.g. solvent extraction • Facilities require significant capital & operational expenditures

Their supply and demand dynamics are intertwined • The dynamics for any one REE indirectly affects them all • Magnet production can ∴ be affected by non-magnet REEs

14!Introduction!

Applications for REEs!

Significant growth in end-use demand • New hi-tech products and devices in addition to new markets • Increased market penetration of clean-energy platforms

Magnets in electric motors are a KEY driver Clean-energy applications require significant quantities

• Wind turbines: approx. 150-200 kg REEs per MW produced • Hybrid electric vehicles (HEVs): approx. 2-3 kg REEs per vehicle

15!Introduction!

Applications for REEs!

Beware of the hype • E.g. only a fraction of wind turbines use REE-based magnets • E.g. older estimates for REEs in HEVs were exaggerated

But – be aware of the potential impact of legislation • E.g. bans on incandescent light bulbs

Specific efficiency regulations on electric motors • EU: 2005 Directive on Eco-design • USA: 2007 Energy Independence and Security Act (EISA) • EU: Commission Regulation 640/2009 – IE3 by 2015-2017

16!Introduction!

Rare-Earth Demand

Recent Dynamics in the Rare-Earth Sector and!their Effects on the Motion-Control Supply Chain!

From where does the demand originate?!

18!Rare-Earth Demand!!

Sources: IMCOA, Technology Metals Research!

From where does the demand originate?!

19!Rare-Earth Demand!!

Sources: IMCOA, Technology Metals Research!

From where does the demand originate?!

20!Rare-Earth Demand!!

Sources: IMCOA, Technology Metals Research!

From where does the demand originate?!

21!Rare-Earth Demand!!

Sources: IMCOA, Technology Metals Research!

Future demand!

22!Rare-Earth Demand!!

Sources: IMCOA, Technology Metals Research!

65%

35%

69%

31%

China Rest of World

2012e Demand 115 kt TREO

2016f Demand 163 kt TREO

Future demand!

23!Rare-Earth Demand!!

Sources: IMCOA, Technology Metals Research!

Future demand!

24!Rare-Earth Demand!!

Source: IMCOA!

End Use China USA Japan & SE Asia Others Total Market

Share

Permanent Magnets 28,000 2,000 4,500 1,500 36,000 22%

Metal Alloys 20,000 2,000 2,500 1,500 26,000 16%

Catalysts 14,500 6,500 2,500 1,500 25,000 15%

Polishing Powders 19,000 3,000 2,000 1,000 25,000 15%

Phosphors 9,000 1,000 2,000 500 12,500 8%

Glass Additives 6,000 1,000 1,000 1,000 9,000 6%

Ceramics 4,000 2,000 2,000 1,000 9,000 6%

Other 6,500 8,000 3,500 2,000 20,000 12%

Total Demand 107,000 25,500 20,000 10,000 162,500 100%

Market Share 66% 16% 12% 7% 100%

Forecast for global rare-earth demand in 2016 (t REO ± 20%) !

Current Rare-Earth Supply

Recent Dynamics in the Rare-Earth Sector and!their Effects on the Motion-Control Supply Chain!

Where are REEs currently mined?!

26!Current Rare-Earth Supply!!

Source: Technology Metals Research!

From where does the supply originate?!

27!Current Rare-Earth Supply!!

Sources: IMCOA, Chinese State Council Information Office, Technology Metals Research!

91%

9%

China Rest of World

2012e Supply 106 kt TREO

65%

35%

2016f Supply 178 kt TREO

Future supply!

Significant future supply will come from outside of China

28!Current Rare-Earth Supply!

2012e 2016f

LREO MREO HREO LREO MREO HREO

China 85,000 t 3,750 t 6,925 t 105,000 t 4,650 t 6,250 t

Rest of World 10,000 t 250 t 75 t 60,000 t 1,350 t 750 t

TOTAL 95,000 t 4,000 t 7,000 t 165,000 t 6,000 t 7,000 t

Global rare-earth supply in 2012 (estimate ± 15%) and 2016 (forecast ± 20%) !

Source: IMCOA!

Chinese Mining & Export Quotas

Recent Dynamics in the Rare-Earth Sector and!their Effects on the Motion-Control Supply Chain!

Rare-earth mining production in China!

30!Chinese Mining & Export Quotas!

YUNNAN

SICHUAN

SHANDONG

JIANGXI

INNER MONGOLIA

HUNAN

GUANGXI GUANGDONG

FUJIAN

Sources: Technology Metals Research, Chinese Ministry of Land & Resources, Chinese State Council Information Office!

Chinese Ministry of Land & Resources allocates mining quotas to nine different provinces and regions

Type of REE production depends on the geology of the province or region

In 2012: • 93,800 t of REO quotas • 96,000e t of actual production

2013 saw similar quotas

Rare-earth mining production in China!

31!Chinese Mining & Export Quotas!

Sources: Technology Metals Research, Chinese Ministry of Land & Resources, Chinese State Council Information Office!

YUNNAN

SICHUAN

SHANDONG

JIANGXI

INNER MONGOLIA

HUNAN

GUANGXI GUANGDONG

FUJIAN

Province / Region 2013 Mining Quota

LREOs (t) HREOs (t)

Fujian 0 2,000

Guangdong 0 2,200

Guangxi 2,500 0

Hunan 2,000 0

Inner Mongolia 50,000 0

Jiangxi 0 9,000

Shandong 1,500 0

Sichuan 24,400 0

Yunnan 0 200

Sub-totals 80,400 13,400

Total Quota 93,800

Actual Production TBD

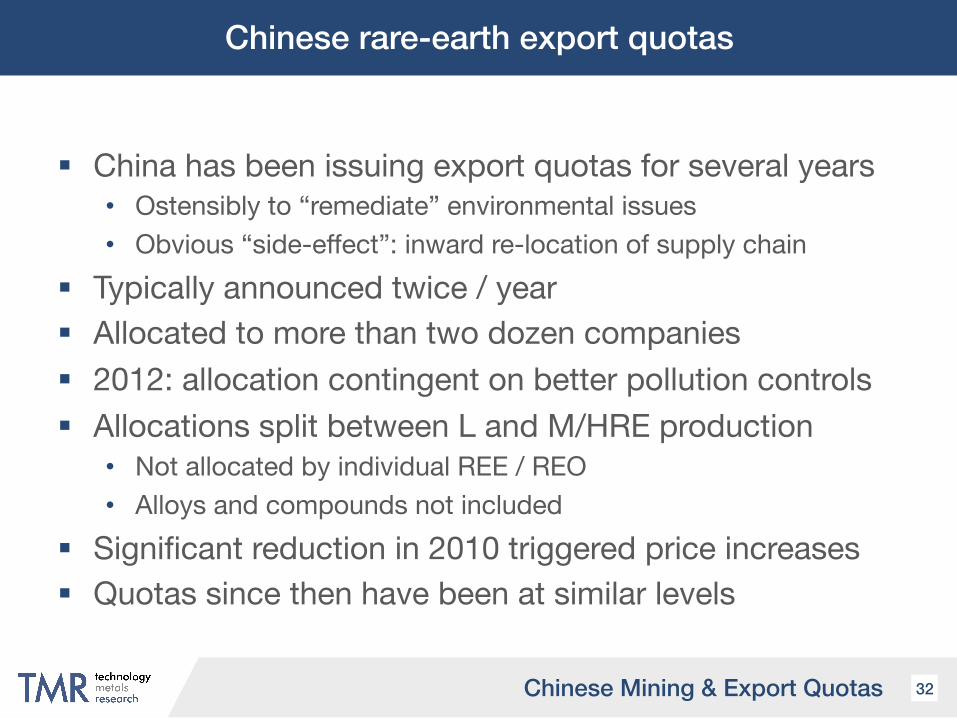

Chinese rare-earth export quotas!

China has been issuing export quotas for several years • Ostensibly to “remediate” environmental issues • Obvious “side-effect”: inward re-location of supply chain

Typically announced twice / year Allocated to more than two dozen companies 2012: allocation contingent on better pollution controls Allocations split between L and M/HRE production

• Not allocated by individual REE / REO • Alloys and compounds not included

Significant reduction in 2010 triggered price increases Quotas since then have been at similar levels

32!Chinese Mining & Export Quotas!

Chinese rare-earth export quotas!

33!Chinese Mining & Export Quotas!

Sources: Chinese Ministry of Commerce, Chinese Ministry of Industry & Information Technology, Asian Metal!

* rare-earth oxides only – other materials may constitute approx. 2-3,000 t / year!

Effects of Price Volatility

Recent Dynamics in the Rare-Earth Sector and!their Effects on the Motion-Control Supply Chain!

What caused the recent REE price spike?!

Triggered by significant reduction in 2010 export quotas Led to disconnect between internal & export pricing Inflection point in Feb 2011 for internal China prices

• Internal stockpiling / speculation • Siphoning to black market for export – arbitrage opportunity

Prices peaked in Jul-Aug 2011 Significant reduction in volumes of official exports Apparent increase in smuggling of rare-earth materials

• Chinese authorities claim 20% of all 2011 exports were illegal • Likely to actually be much higher via deliberate mislabeling

35!Effects of Price Volatility!

Recent REO prices!

36!Effects of Price Volatility!

Sources: Technology Metals Research, Metal Pages!

Recent REO prices!

37!Effects of Price Volatility!

Sources: Technology Metals Research, Metal Pages!

Recent REO prices!

38!Effects of Price Volatility!

Sources: Technology Metals Research, Metal Pages!

Recent REO prices!

39!Effects of Price Volatility!

Sources: Technology Metals Research, Metal Pages!

Be aware of the limitations of published rare-earth prices!

40!Effects of Price Volatility!

Sources: Asian Metal, Metal Pages!

Bonded Nd-Fe-B motor magnets!

41!Effects of Price Volatility!

Source: TDK!

Compression molded Nd-Fe-B bonded magnets typically used in motors

Based on Magnequench MQP material or similar Little to no heavy REEs such as Dy or Tb

Bonded Nd-Fe-B motor magnets!

42!Effects of Price Volatility!

Source: Technology Metals Research!

Bonded Nd-Fe-B motor magnets!

43!Effects of Price Volatility!

Source: Technology Metals Research!

Sintered Nd-Fe-B magnets!

Hard-disk drives (HDD) are major user of REPMs 581M HDD units shipped in 2012 (Coughlin Associates)

• 2M 1.8” drives, 298M 2.5” drives & 281M 3.5” drives HDDs contain two sets of Nd-based REPMs:

• Spindle motor – bonded isotropic MQP-B type material • Voice-coil motor (VCM) – sintered anisotropic material

Size of spindle motor has not seen too much change Not so for the VCM magnets

• 1986: 70 g / HDD; 1996: 15-20 g / HDD; 2002: 7-15g / HDD

44!Effects of Price Volatility!

Sintered Nd-Fe-B magnets!

In July 2011, Magnequench looked at REPMs in VCMs Acquired a number of new HDDs and disassembled them

• Mix of Seagate & Western Digital HDDs • Mix of 2.5” & 3.5” HDDs

Determined mass and composition of VCM REPMs A number of surprises:

• #1 (to me) - these magnets contain HREEs • #2 (to me) - the magnets these days are tiny! • #3 - significant variation in compositions • #4 - some paired REPMs had significant compositional differences

45!Effects of Price Volatility!

Sintered Nd-Fe-B magnets!

46!Effects of Price Volatility!

Source: Magnequench!

!!

!

Sintered Nd-Fe-B magnets!

Based on the data, determined an average composition • Nd - 22% : Pr - 5.3% : Tb - 0.25% : Dy – 1.4% (by weight)

Determined mass of REEs per magnet

47!Effects of Price Volatility!

HDD size Magnets (g) Nd (g) Pr (g) Tb (g) Dy (g) TREE (g)

2.5” 2.7 0.59 0.14 0.007 0.038 0.78

3.5” 5.0 1.10 0.27 0.013 0.070 1.45

Average mass of REEs contained in 2011 model HDD VCM magnets!

Source: Magnequench, Technology Metals Research!

Case study: hard-disk drive magnets!

48!Effects of Price Volatility!

Source: Technology Metals Research!

Case study: hard-disk drive magnets!

49!Effects of Price Volatility!

Source: Technology Metals Research!

How did the magnet industry respond to price spikes?!

Major efforts to reduce Nd-Fe-B usage in 2011-2012 • Switch from REPM to induction motors • Switch from surface-mounted to interior REPMs • Switch back to ferrite where possible • Higher HREE-containing REPMs – some switched to Sm-Co

Also efforts to “drop down” a grade or two (or three) • Reducing Dy & Tb = significant cost savings

Various funding initiatives for reducing REE usage Mag REO demand: 2010: 26 kt; 2011: 21 kt; 2012: 22.5 kt

• Rebounded further in 2013 – though end users are still wary At least one bankruptcy of a magnet company…

50!Effects of Price Volatility!

How did the magnet industry respond?!

Development and sale of lower HREE Nd-based materials • Grain-boundary diffusion – putting HREEs where needed

Dr. Sagawa / Intermetallics press-less sintered REPMs • No / low HREEs – reduced grain size for increased coercivity • JV with Molycorp, Daido Steel & Mitsubishi • Limited form factors – further development needed

Renewed interest in enhanced Magnequench powders • No HREEs – nanoscale grain size for increased coercivity

51!Effects of Price Volatility!

The Politics of Rare Earths

Recent Dynamics in the Rare-Earth Sector and!their Effects on the Motion-Control Supply Chain!

Was there a REE embargo in 2010?!

Sep 2010: Chinese fishing boat collides with Japanese patrol boats near Senkaku Islands in East China Sea • Also known as Diaoyu (China) or Diaoyutai Islands (Taiwan)

Chinese fishing-boat captain arrested by Japanese China accused of suspending REE shipments to Japan China denies the accusations Senior politicians have their say… Japan releases fishing-boat captain Alleged suspension of shipments “lifted”

53!The Politics of Rare Earths!

The WTO rare-earth trade dispute!

March 2012: USA, EU & Japan initiate WTO action • File simultaneous complaints against China • Related to exports of rare earths, tungsten & molybdenum

Covers wide range of rare-earth-containing materials • Ores, metals, oxides and other compounds • Phosphorescent powders • Magnetic powders and alloys

June 2012: State Council publishes REE white paper • Sets out position on various topics without tying into WTO case

July 2012: Dispute resolution panel set up

54!The Politics of Rare Earths!

The WTO rare-earth trade dispute!

The WTO complaints allege: • Unfair treatment of foreign entities via export restrictions • Discriminatory commercial operating rules within China • The setting of unofficial minimum export prices • Overall lack of transparency concerning implementation

China likely to cite two GATT Article XX exceptions: • “necessary to protect human, animal or plant life or health” • “relating to the conservation of exhaustible natural resources” BUT - cannot be “a disguised restriction on international trade”

• China recently lost a similar case • BUT – could it all be moot?

55!The Politics of Rare Earths!

Might we see the end of export quotas?!

Dec 2011: China divides quotas into LRE & M/HRE Aug 2012: industry leaders discuss the end of quotas

• Reported to have made the suggestion to government • As new ROW LREE sources come online – no longer relevant?

Might lead to elimination of LREE export quotas Few new sources of HREEs – so those would remain?

• Stronger case relating to “exhaustible natural resources” Significant internal discussion in China on the topic Backdrop of REE industry consolidation

56!The Politics of Rare Earths!

More recent goings-on!

Renewed antagonism between China & Japan Conveniently timed, fanciful / dubious stories

• REEs found in the Pacific Ocean • REEs found in Jamaican red mud • Let’s mine REEs on asteroids…

Dubious export stats from the Chinese authorities • For 2011: one minute it was 18,600 t, the next it was 16,855 t • Regurgitated verbatim by even the specialist media

Formation of Association of Chinese Rare-Earth Industry Companies cease production because of lower prices Launch of rare-earth exchange – more stable pricing?

57!The Politics of Rare Earths!

Other Supply & Demand Issues

Recent Dynamics in the Rare-Earth Sector and!their Effects on the Motion-Control Supply Chain!

Determination that some REEs are critical!

59!Other Supply & Demand Issues!

Sources: US Department of Energy, Technology Metals Research!

Is China running out of rare earths?!

Few doubt that there are ample reserves of LREEs Chinese State Council Information Office on M/HREEs:

• 1992 – 50 years of reserves in southern mining areas • 2012 – 15 years of reserves left at current extraction rates

60!Other Supply & Demand Issues!

Source: Technology Metals Research!

Is China running out of rare earths?!

Early Feb 2013 – announcement on 6 new HREE mines Likely to be “replacements” for illegal mines

• China has clamped down strongly on illegal mining • Better for the environment AND tax coffers

Export quota still in place so unlikely to affect ROW Chinese won’t allow pricing to collapse Recent Chinese announcements on stockpiling Good for both ends of the ROW supply chain…

61!Other Supply & Demand Issues!

Non-Chinese HREE-rich mineral deposits!

Interest not just because of risks to Chinese sourcing Demand profile of each REE vs. natural occurrence:

• Ratio Dy + Tb : Pr + Nd ≈ 1:50 – 1:2 for permanent magnets • Ratio Dy + Tb : Pr + Nd ≈ 1:100 – 1:50 in typical LREE minerals

Growing demand for HREEs for lighting Most HREE-rich minerals are “challenging” to process

• Very few have been commercially exploited • Core reason for time it takes to develop HREE-rich deposits

62!Other Supply & Demand Issues!

The balance between REE surplus and deficit!

Specific REE production not independent of other REEs Even HREE-rich minerals contain significant LREEs Will likely lead to oversupply of non-critical LREEs

63!Other Supply & Demand Issues!

Source: IMCOA!

CeO2 Nd2O3 Eu2O3 Tb4O7 Dy2O3 Y2O3

Demand @ 150-170 kt/yr TREO 70 kt 25-30 kt 350-400 t 450-500 t 0.8-0.9 kt 9-10 kt

Supply @ 180-210 kt/yr TREO 80 kt 30-35 kt 400-450 t 250-300 t 1.0 kt 7-8 kt

Forecast for global supply and demand for select rare earths in 2016!

Future Sources of Rare-Earth Supply

Recent Dynamics in the Rare-Earth Sector and!their Effects on the Motion-Control Supply Chain!

Non-Chinese REE projects!

As of September 2013, TMR was monitoring: • 450+ REE projects in 37 countries outside of China • BUT - 85%+ at early stages of exploration & development

Currently 50 advanced projects on the TMR Index • 16 countries outside of China • Many of these are critical REE-rich deposits • All have code-compliant mineral-resource estimates

E.g. NI 43-101 / CIM, JORC, SAMREC • Several have completed feasibility and pre-feasibility studies • Some even have mineral reserves • Full list is available at www.RareEarths.org

65!Future Sources of Rare-Earth Supply!

Current and future sources of REE supply!

66!Future Sources of Rare-Earth Supply!!

Source: Technology Metals Research!

Future sources of REE supply outside of China!

67!Future Sources of Rare-Earth Supply!!

Source: Technology Metals Research!

Next challenge: producing separated REE products!

A particular issue for projects with HREE-rich deposits Many such companies plan to produce concentrates only But end users can’t use REE concentrates!

• NO independent separation facilities outside of China • Very few other such facilities either

One solution: a centralized REE separation facility • Innovation Metals Corp. (IMC) plans to provide low-cost tolling • IMC Consortium: mining companies, end users & traders • Looking to build a facility in Quebec, Canada by 2016 • Focused on critical REEs

68!Future Sources of Rare-Earth Supply!

Final Thoughts

Recent Dynamics in the Rare-Earth Sector and!their Effects on the Motion-Control Supply Chain!

Final thoughts!

We are unlikely to see a price spike like 2011 again Plenty of new projects coming online soon Bear in mind the contradiction for such projects:

• Producers need high REE prices, to finance their projects • End users need low prices to sell their products • Hopefully we will see a “happy medium”

Prices are unlikely to return to historical levels • China’s environmental stance means higher operating costs • Some prices were slowly trending up because of demand

Don’t be afraid to use devices containing REEs!

70!Final Thoughts!

Acknowledgements!

My thanks to the following for discussions & assistance: • Dave Brown (Molycorp Magnequench) • Zhanheng Chen (Chinese Society of Rare Earths) • Tom Coughlin (Coughlin Associates) • Dudley Kingsnorth (IMCOA & Curtin University) • Boris Saje (Kolektor) • Art Wagner (Consultant) • Jim Wise (Wise Magnet Applications)

Thank You!

Gareth P Hatch, PhD!Founding Principal!

Technology Metals Research, LLC!!

180 S. Western Ave #150!Carpentersville, IL 60110!United States of America!

!+1-847-867-3091!

[email protected]!www.techmetalsresearch.com!