recent changes and controversial … changes and controversial issues by ca puloma d. dalal on ......

TRANSCRIPT

RECENT CHANGES

AND CONTROVERSIAL

ISSUES

BY

CA PULOMA D. DALAL

ON

06TH DECEMBER, 2017

PDD6TH December, 2017

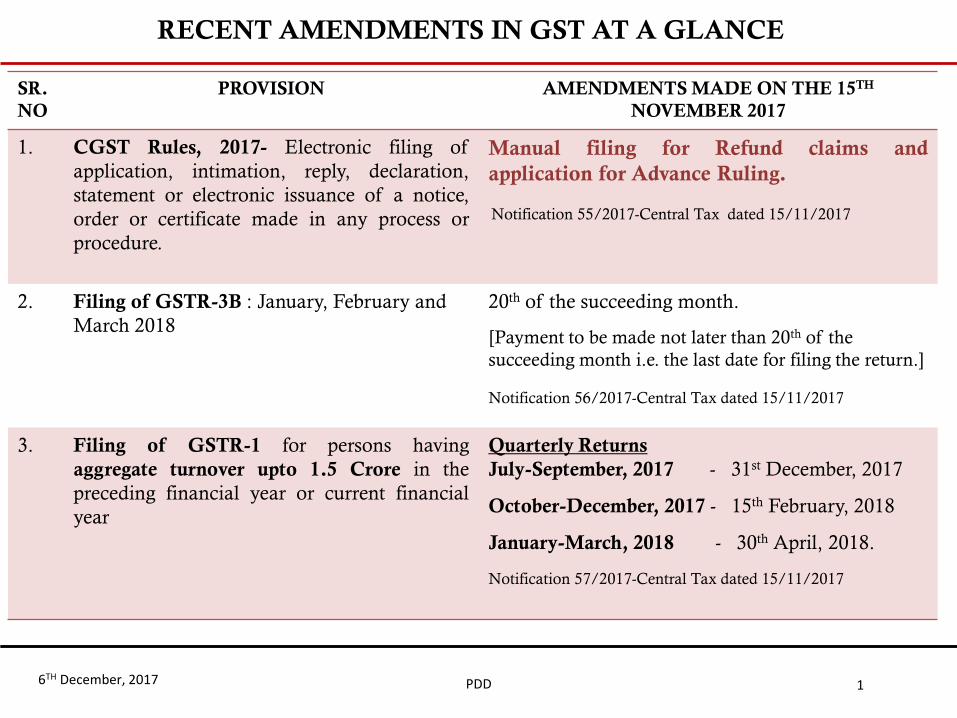

RECENT AMENDMENTS IN GST AT A GLANCE

SR.

NO

PROVISION AMENDMENTS MADE ON THE 15TH

NOVEMBER 2017

1. CGST Rules, 2017- Electronic filing of

application, intimation, reply, declaration,

statement or electronic issuance of a notice,

order or certificate made in any process or

procedure.

Manual filing for Refund claims and

application for Advance Ruling.

2. Filing of GSTR-3B : January, February and

March 2018

20th of the succeeding month.

[Payment to be made not later than 20th of the

succeeding month i.e. the last date for filing the return.]

3. Filing of GSTR-1 for persons having

aggregate turnover upto 1.5 Crore in the

preceding financial year or current financial

year

Quarterly Returns

July-September, 2017 - 31st December, 2017

October-December, 2017 - 15th February, 2018

January-March, 2018 - 30th April, 2018.

Notification 55/2017-Central Tax dated 15/11/2017

Notification 56/2017-Central Tax dated 15/11/2017

Notification 57/2017-Central Tax dated 15/11/2017

6TH December, 2017 PDD 1

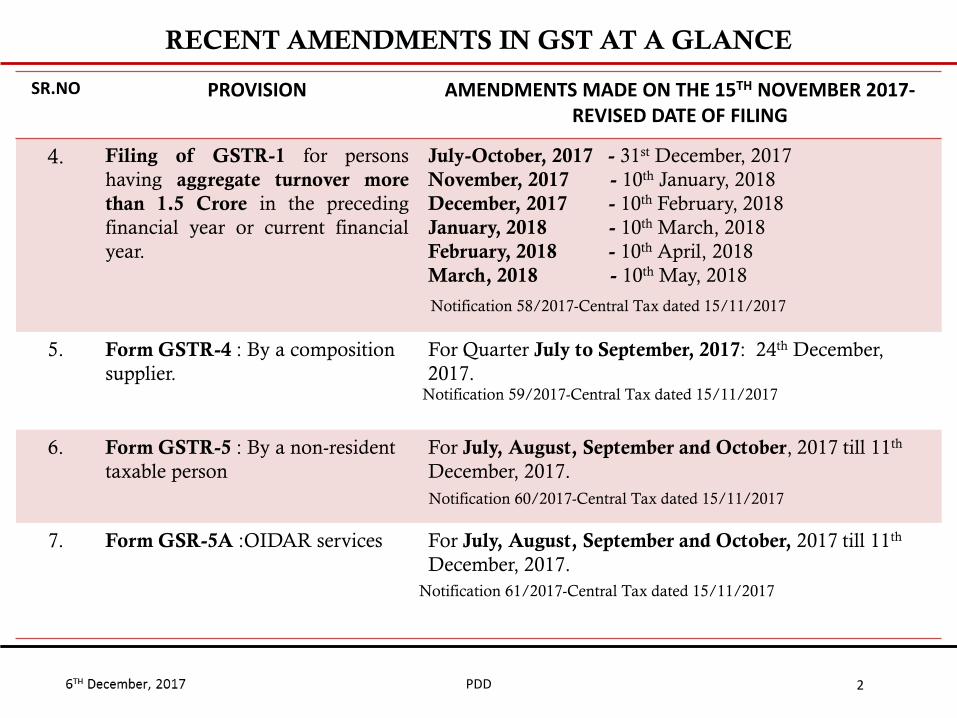

RECENT AMENDMENTS IN GST AT A GLANCE

SR.NO PROVISION AMENDMENTS MADE ON THE 15TH NOVEMBER 2017-REVISED DATE OF FILING

4. Filing of GSTR-1 for persons

having aggregate turnover more

than 1.5 Crore in the preceding

financial year or current financial

year.

July-October, 2017 - 31st December, 2017

November, 2017 - 10th January, 2018

December, 2017 - 10th February, 2018

January, 2018 - 10th March, 2018

February, 2018 - 10th April, 2018

March, 2018 - 10th May, 2018

5. Form GSTR-4 : By a composition

supplier.

For Quarter July to September, 2017: 24th December,

2017.

6. Form GSTR-5 : By a non-resident

taxable person

For July, August, September and October, 2017 till 11th

December, 2017.

7. Form GSR-5A :OIDAR services For July, August, September and October, 2017 till 11th

December, 2017.

Notification 58/2017-Central Tax dated 15/11/2017

Notification 59/2017-Central Tax dated 15/11/2017

Notification 60/2017-Central Tax dated 15/11/2017

Notification 61/2017-Central Tax dated 15/11/2017

PDD 2

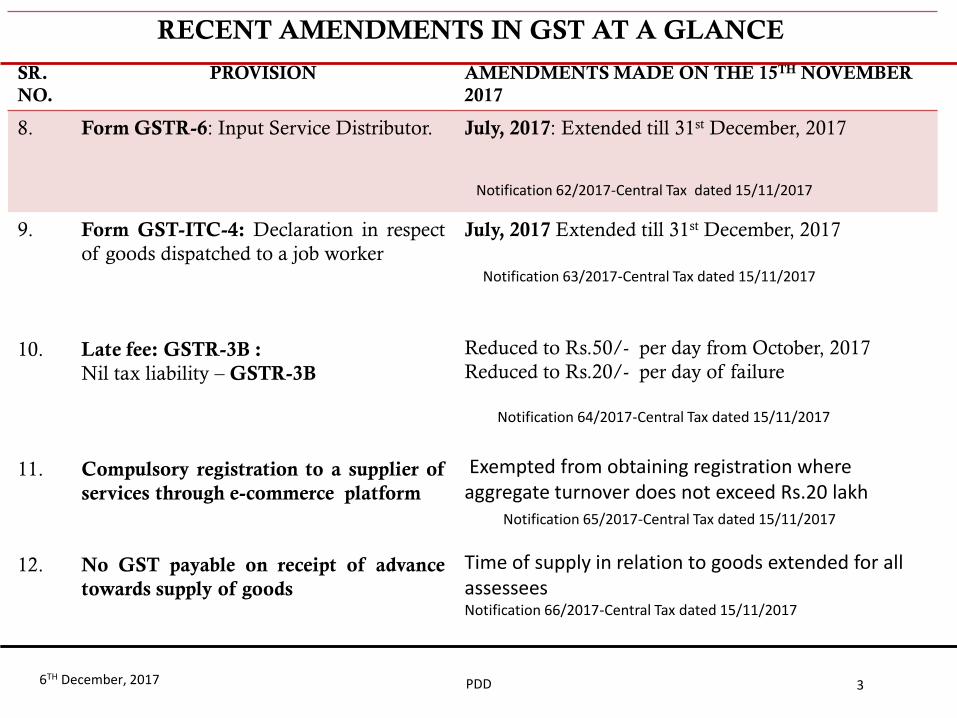

RECENT AMENDMENTS IN GST AT A GLANCE

SR.

NO.

PROVISION AMENDMENTS MADE ON THE 15TH NOVEMBER

2017

8. Form GSTR-6: Input Service Distributor. July, 2017: Extended till 31st December, 2017

9.

10.

11.

12.

Form GST-ITC-4: Declaration in respect

of goods dispatched to a job worker

Late fee: GSTR-3B :

Nil tax liability – GSTR-3B

Compulsory registration to a supplier of

services through e-commerce platform

No GST payable on receipt of advance

towards supply of goods

July, 2017 Extended till 31st December, 2017

Notification 63/2017-Central Tax dated 15/11/2017

Reduced to Rs.50/- per day from October, 2017

Reduced to Rs.20/- per day of failure

Notification 64/2017-Central Tax dated 15/11/2017

Exempted from obtaining registration where aggregate turnover does not exceed Rs.20 lakh

Notification 65/2017-Central Tax dated 15/11/2017

Time of supply in relation to goods extended for all assesseesNotification 66/2017-Central Tax dated 15/11/2017

Notification 62/2017-Central Tax dated 15/11/2017

6TH December, 2017 PDD 3

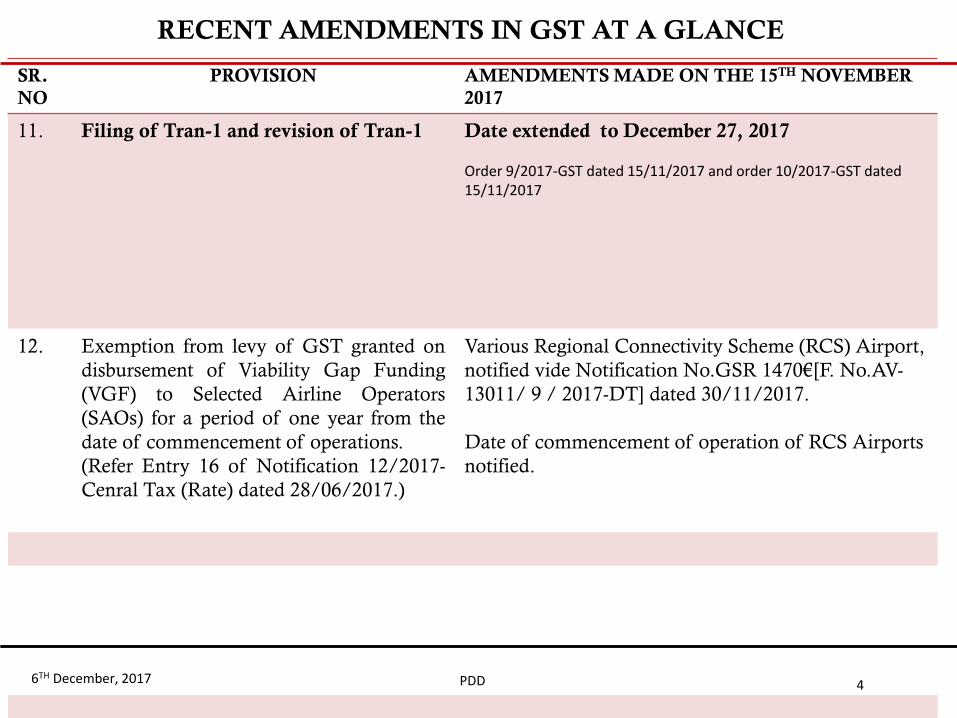

RECENT AMENDMENTS IN GST AT A GLANCE

SR.

NO

PROVISION AMENDMENTS MADE ON THE 15TH NOVEMBER

2017

11. Filing of Tran-1 and revision of Tran-1 Date extended to December 27, 2017

Order 9/2017-GST dated 15/11/2017 and order 10/2017-GST dated 15/11/2017

12. Exemption from levy of GST granted on

disbursement of Viability Gap Funding

(VGF) to Selected Airline Operators

(SAOs) for a period of one year from the

date of commencement of operations.

(Refer Entry 16 of Notification 12/2017-

Cenral Tax (Rate) dated 28/06/2017.)

Various Regional Connectivity Scheme (RCS) Airport,

notified vide Notification No.GSR 1470€[F. No.AV-

13011/ 9 / 2017-DT] dated 30/11/2017.

Date of commencement of operation of RCS Airports

notified.

6TH December, 2017 PDD 4

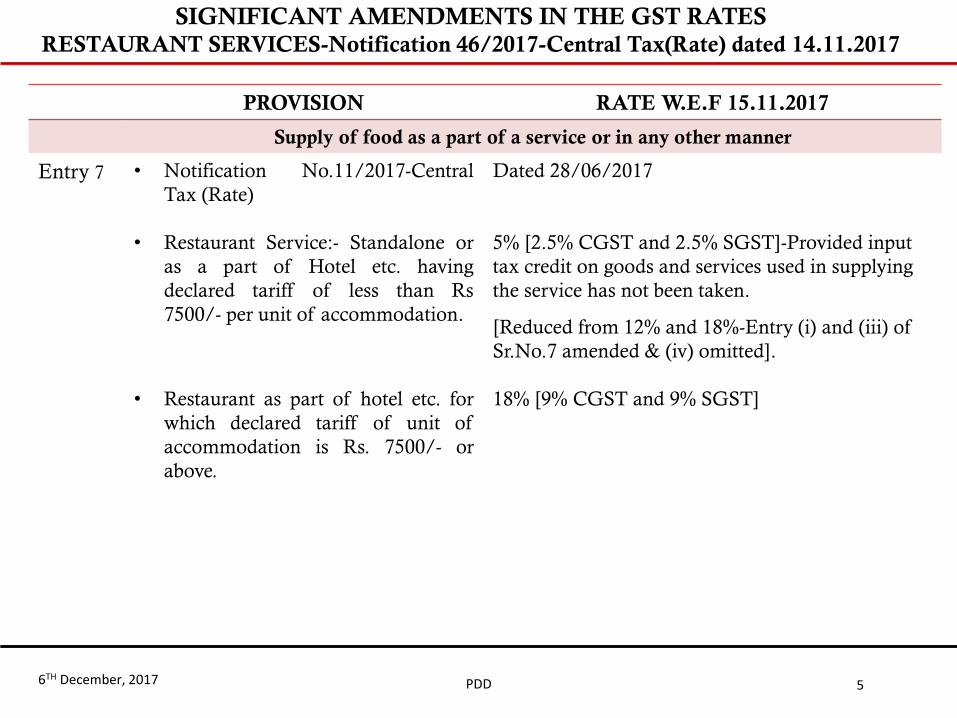

SIGNIFICANT AMENDMENTS IN THE GST RATESRESTAURANT SERVICES-Notification 46/2017-Central Tax(Rate) dated 14.11.2017

PROVISION RATE W.E.F 15.11.2017

Supply of food as a part of a service or in any other manner

Entry 7 • Notification No.11/2017-Central

Tax (Rate)

• Restaurant Service:- Standalone or

as a part of Hotel etc. having

declared tariff of less than Rs

7500/- per unit of accommodation.

• Restaurant as part of hotel etc. for

which declared tariff of unit of

accommodation is Rs. 7500/- or

above.

Dated 28/06/2017

5% [2.5% CGST and 2.5% SGST]-Provided input

tax credit on goods and services used in supplying

the service has not been taken.

[Reduced from 12% and 18%-Entry (i) and (iii) of

Sr.No.7 amended & (iv) omitted].

18% [9% CGST and 9% SGST]

6TH December, 2017 PDD 5

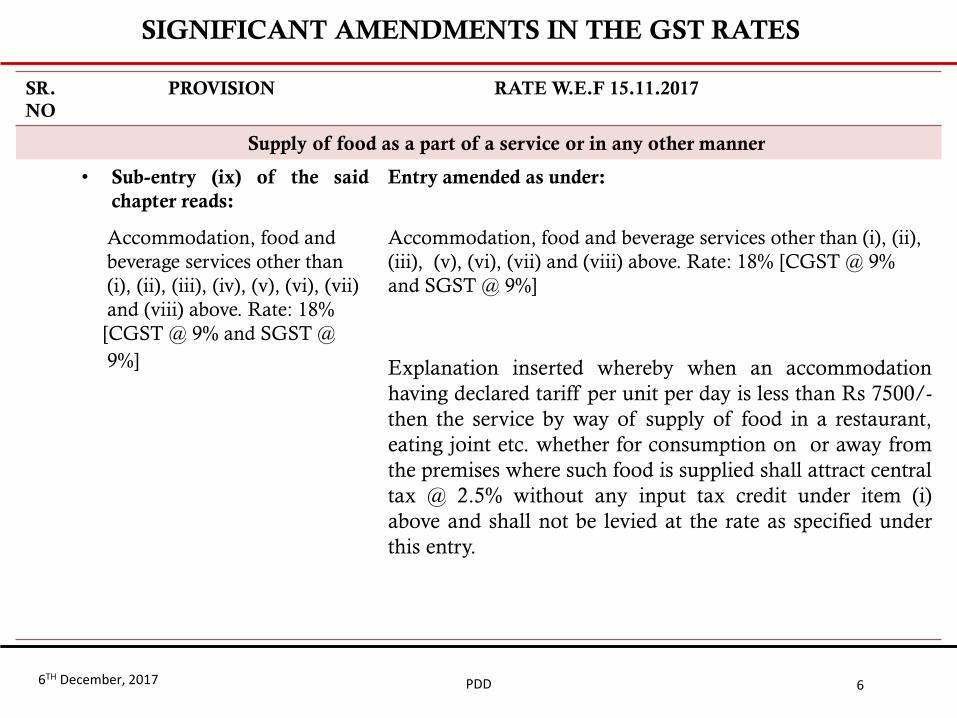

SIGNIFICANT AMENDMENTS IN THE GST RATES

SR.

NO

PROVISION RATE W.E.F 15.11.2017

Supply of food as a part of a service or in any other manner

• Sub-entry (ix) of the said

chapter reads:

Accommodation, food and

beverage services other than

(i), (ii), (iii), (iv), (v), (vi), (vii)

and (viii) above. Rate: 18%

[CGST @ 9% and SGST @

9%]

Entry amended as under:

Accommodation, food and beverage services other than (i), (ii),

(iii), (v), (vi), (vii) and (viii) above. Rate: 18% [CGST @ 9%

and SGST @ 9%]

Explanation inserted whereby when an accommodation

having declared tariff per unit per day is less than Rs 7500/-

then the service by way of supply of food in a restaurant,

eating joint etc. whether for consumption on or away from

the premises where such food is supplied shall attract central

tax @ 2.5% without any input tax credit under item (i)

above and shall not be levied at the rate as specified under

this entry.

PDD6TH December, 2017 6

ISSUES

A] Whether the GST rate of 5% is mandatory to be followed by all restaurants?

B] Determine the GST rate in the following situations:

(i) Restaurants located in hotels having a seasonal tariff exceeding Rs 7500/- in some months.

(ii) Free home delivery of a 500gm Ice-Cream pack from an ice-cream parlour.

C] How would a Restaurant avail input tax credit for the of month of November, 2017 the effective

date of amendment being 15.11.2017.

D] Implications of passing on inadequate or no benefit of reduced rate to the consumers.

PDD6TH December, 2017 7

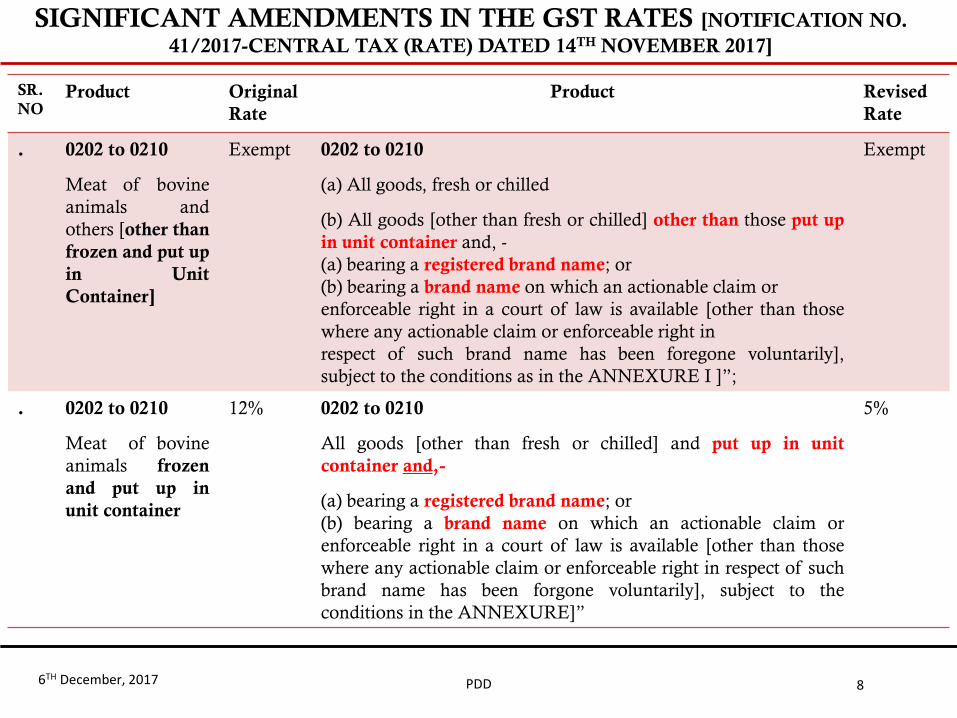

SIGNIFICANT AMENDMENTS IN THE GST RATES [NOTIFICATION NO.

41/2017-CENTRAL TAX (RATE) DATED 14TH NOVEMBER 2017]

SR.

NOProduct Original

Rate

Product Revised

Rate

. 0202 to 0210

Meat of bovine

animals and

others [other than

frozen and put up

in Unit

Container]

Exempt 0202 to 0210

(a) All goods, fresh or chilled

(b) All goods [other than fresh or chilled] other than those put up

in unit container and, -

(a) bearing a registered brand name; or

(b) bearing a brand name on which an actionable claim or

enforceable right in a court of law is available [other than those

where any actionable claim or enforceable right in

respect of such brand name has been foregone voluntarily],

subject to the conditions as in the ANNEXURE I ]”;

Exempt

. 0202 to 0210

Meat of bovine

animals frozen

and put up in

unit container

12% 0202 to 0210

All goods [other than fresh or chilled] and put up in unit

container and,-

(a) bearing a registered brand name; or

(b) bearing a brand name on which an actionable claim or

enforceable right in a court of law is available [other than those

where any actionable claim or enforceable right in respect of such

brand name has been forgone voluntarily], subject to the

conditions in the ANNEXURE]”

5%

6TH December, 2017 PDD 8

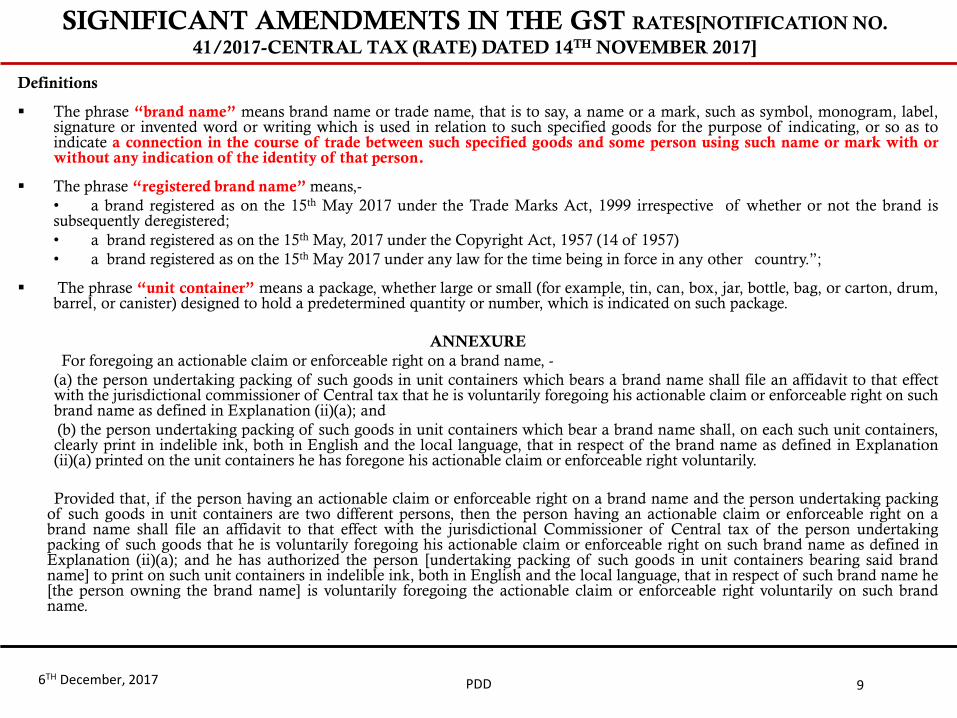

SIGNIFICANT AMENDMENTS IN THE GST RATES[NOTIFICATION NO.

41/2017-CENTRAL TAX (RATE) DATED 14TH NOVEMBER 2017]

Definitions

The phrase “brand name” means brand name or trade name, that is to say, a name or a mark, such as symbol, monogram, label,signature or invented word or writing which is used in relation to such specified goods for the purpose of indicating, or so as toindicate a connection in the course of trade between such specified goods and some person using such name or mark with orwithout any indication of the identity of that person.

The phrase “registered brand name” means,-

• a brand registered as on the 15th May 2017 under the Trade Marks Act, 1999 irrespective of whether or not the brand issubsequently deregistered;

• a brand registered as on the 15th May, 2017 under the Copyright Act, 1957 (14 of 1957)

• a brand registered as on the 15th May 2017 under any law for the time being in force in any other country.”;

The phrase “unit container” means a package, whether large or small (for example, tin, can, box, jar, bottle, bag, or carton, drum,barrel, or canister) designed to hold a predetermined quantity or number, which is indicated on such package.

ANNEXURE

For foregoing an actionable claim or enforceable right on a brand name, -

(a) the person undertaking packing of such goods in unit containers which bears a brand name shall file an affidavit to that effectwith the jurisdictional commissioner of Central tax that he is voluntarily foregoing his actionable claim or enforceable right on suchbrand name as defined in Explanation (ii)(a); and

(b) the person undertaking packing of such goods in unit containers which bear a brand name shall, on each such unit containers,clearly print in indelible ink, both in English and the local language, that in respect of the brand name as defined in Explanation(ii)(a) printed on the unit containers he has foregone his actionable claim or enforceable right voluntarily.

Provided that, if the person having an actionable claim or enforceable right on a brand name and the person undertaking packingof such goods in unit containers are two different persons, then the person having an actionable claim or enforceable right on abrand name shall file an affidavit to that effect with the jurisdictional Commissioner of Central tax of the person undertakingpacking of such goods that he is voluntarily foregoing his actionable claim or enforceable right on such brand name as defined inExplanation (ii)(a); and he has authorized the person [undertaking packing of such goods in unit containers bearing said brandname] to print on such unit containers in indelible ink, both in English and the local language, that in respect of such brand name he[the person owning the brand name] is voluntarily foregoing the actionable claim or enforceable right voluntarily on such brandname.

6TH December, 2017 PDD 9

JUDICIAL PRONOUNCEMENTS

Commissioner of C.Ex.,Hyderabad-IV Vs. Stangen Immuno Diagnostics [2015 (318) ELT 585 (S.C.)]

Held: The central idea contained in the aforesaid definition is that the mark is used with the purpose to showconnection of the said goods with some person who is using the name or mark. Therefore, in order to qualifyas “brand name” or “trade name” it has to be established that such a mark, symbol, design or name etc. hasacquired the reputation of the nature that one is able to associate the said mark etc. with themanufacturer.

Commissioner of Central Excise Vs. Sanghi Threads [2015 (321) ELT 180 (SC)]

Held: Symbol/Monogram used on packing material by all units of the manufacturer and is also used on theletterpads of the respective units-Such monogram only a housemark for identification of group and not abrand name for identification of the product as it is followed by the name of the particular unit of themanufacturer.

Circular No. 52/52/94-CX dated 01.09.94

Para 3: "Perusal of the said explanation (Explanation IX to the notification No. 1/93-CE) will show that tosatisfy the requirement of brand name or trade name, it is necessary that the trade name must indicate aconnection in the course of trade between such specified goods and some person using such name or markwith or without any indication or identity of that person. Unless connection between the trade name andthe person with whom that trade name is to be identified can be established, the requirement of brand nameor trade name as provided for in the the said notification will not be satisfied. It is an admitted case of theDepartment that in respect of locks, the units are making locks bearing the same name of mark eventhough there is no person who claims ownership to that mark or name. The names being used in themanufacture of locks by these small scale units do not belong to any particular manufacturer and any unitis free to use any name. Therefore, in our view, without the issue of Notification of 4th / 11th May, 1994units which are using trade name or brand name, which does not belong to any person, were eligible forexemption under the said notification because of explanation IX in the said notification. Admittedly, thenotification dated 4th /11th May, 1994, is classificatory in nature and the purpose could have been achievedby issuing a clarification to the field formations."

6TH December, 2017 PDD 10

ISSUES

(a) Determine the GST rates for the following:

(i) meat products packed in Unit containers of 20kg each with a stamp “SW” on the package for

the purpose of identification of the product for sale.

(ii) frozen meat sold by weight off the counter packed in containers for the purpose of delivery.

(iii) frozen meat – unbranded sold in unit container

6TH December, 2017 PDD 11

AMENDMENT: MERCHANT EXPORTERS-NOTIFICATION 40/2017-CENTRAL TAX (RATE) DATED

23RD OCTOBER 2017 AND NOTIFICATION 41/2017-INTEGRATED TAX (RATE) DATED 23RD OCTOBER 2017

Intra-State and inter-state supply by a registered supplier to a registered recipient for export liable for GST

@ 0.1% subject to the fulfillment of the following conditions:

(a) Registered Supplier:

(i) to supply the goods to the registered recipient on a tax invoice;

(b) Registered Recipient:

(i) to export the goods within ninety days from the date of issue of invoice;

(ii) to indicate the GSTIN and the tax invoice number of the supplier of the said goods in the shipping bill or

bill of export, as the case may be;

(iii) is registered with an Export Promotion Council or a Commodity Board recognised by the Department of

Commerce;

(iv) to place an order on for procuring goods at concessional rate and a copy to be provided to the

jurisdictional tax officer of the registered supplier;

(v) to move the said goods from place of registered supplier –

(a) directly to the Port, ICD, Airport or Land Customs Station from where the said goods are to be

exported; or

(b) directly to a registered warehouse from where the said goods have to move to the Port, ICD etc. from

where the said goods are to be exported;

(vi) if intends to aggregate supplies from multiple registered suppliers and then export, the goods shall move

to a registered warehouse and after the aggregation, goods shall move to the Port, ICD, Customs Station

etc. from where they shall be exported.

6TH December, 2017 PDD 12

AMENDMENT: MERCHANT EXPORTERS-NOTIFICATION 40/2017-CENTRAL TAX (RATE) DATED

23RD OCTOBER 2017 AND NOTIFICATION 41/2017-INTEGRATED TAX (RATE) DATED 23RD OCTOBER 2017

Intra-State and inter-state supply by a registered supplier to a registered recipient for export liable for GST

@ 0.1% subject to the fulfillment of the following conditions:

Registered Recipient

(vii) to endorse receipt of goods on the tax invoice and also obtain acknowledgement of receipt of goods in

the registered warehouse in the situation referred to in (vi) above from the warehouse operator and shall

provide the same to the supplier as well as to the jurisdictional tax officer of such supplier; and

(viii) on exporting the goods to provide copy of shipping bill or bill of export having GSTIN and tax invoice

of the supplier along with proof of export general manifest or export report having been filed to the

supplier as well as his jurisdictional tax officer.

6TH December, 2017 PDD 13

AMENDMENT: MERCHANT EXPORTERS-NOTIFICATION 40/2017-CENTRAL TAX (RATE) DATED

23RD OCTOBER 2017 AND NOTIFICATION 41/2017-INTEGRATED TAX (RATE) DATED 23RD OCTOBER 2017

Issues:

(i) What is a “Registered Warehouse”?

(ii) Whether one to one correlation is required to be maintained for the goods procured from a registered supplier at

a concessional rate and the goods exported?

(iii) Whether the said benefit of concessional rate is available to manufacturers purchasing raw materials for the

purpose of export?

(iv) Whether the registered supplier is entitled for refund on account of an inverted duty structure?

Proviso to Section 54(3) of the CGST Act

Provided that no refund of unutilized input tax credit shall be allowed in cases other than-

(i) ……………….

(ii) Where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on

output supplies (other than nil rated or fully exempt supplies), except supplies of goods or services or both as may be

notified by the Government on the recommendations of the Council:

[Refer - Notification for goods-5/2017-Central Tax(Rate) dated 28.06.2017 (As amended mainly in respect of

woven fabrics in chapter 50 to 55, 60 and railways, tramways, coaches, wagons etc. in chapter 86.

- Also refer to Rule 89(2)(h) of CGST Rules, 2017 and Rule 89(5)].

6TH December, 2017 PDD 14

REVERSE CHARGE MECHANISM

• Section 9(3) of the CGST Act: The Government may, on the recommendations of the Council, by notification,

specify categories of supply of goods or services or both, the tax on which shall be paid on reverse charge basis

by the recipient of such goods or services or both and all the provisions of this Act shall apply to such recipient

as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

• Section 9(4) of the CGST Act: The central tax in respect of the supply of taxable goods or services or both by a

supplier, who is not registered, to a registered person shall be paid by such person on reverse charge basis as

the recipient and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying

the tax in relation to the supply of such goods or services or both. [Deferred till 31.03.2018 vide notification no.

38/2017-Central Tax (Rate) dated 13th October, 2017]

• Section 31(3)(f) of the CGST Act : A registered person who is liable to pay tax under sub-section (3) or sub-

section (4) of section 9 shall issue an invoice in respect of goods or services or both received by him from the

supplier who is not registered on the date of receipt of goods or services or both;

• Rule 36 of the CGST Rules, 2017: Documentary requirements and conditions for claiming input tax credit

(b) an invoice issued in accordance with the provisions of clause (f) of sub-section (3) of section 31, subject to

the payment of tax;

6TH December, 2017 PDD 15

POSERS

1) Whether GST paid under reverse charge mechanism is available as input tax credit in the same month?

2) Determine whether tax is to be paid on reverse charge mechanism in respect of the following services:

a) Mr. A. has bought stationery from a local shop who is not registered in GST on the 5th October, 2017

-Payment made on the 5th October, 2017

- Payment made at the end of month on the 31st October, 2017

b) Mr. B. has received legal services from a lawyer on the 17th October, 2017

c) Mr. C has received security services from an unregistered supplier in the month of August 2017. The

invoice dated 10th September, 2017 for the said service is received on the 15th September, 2017.

d) Will RCM be triggered for security service received from Mr. C during the month of October,2017. Will the

implications change if advance is paid to C on 9th October, 2017 for the said services provided during October,

2017.

e) RCM is applicable on specified services under notification 13/2017-Central Tax (Rate) dated 28.06.2017. No

definitions provided for business entity, insurance agent, insurance business under the said notification. In

absence of definitions of specified service / service recipient under the notifications, what are the implications?

6TH December, 2017 PDD 16

Sr.

No

Particulars Rate

TRANSPORT OF GOODS BY VESSEL

1. Transport of Goods by vessel 5% [With ITC of input services]

2. Transport of Goods by vessel by a person located in non-

taxable territory to a person located in non-taxable territory

for transportation of goods from a place outside India upto

the customs station of clearance in India.

Corrigendum on the 30th June, 2017 to Notification

8/2017-Integrated Tax(Rate): Where the value of taxable

service provided by a person located in non-taxable territory to

a person located in non-taxable territory by way of

transportation of goods by a vessel from a place outside India

up to the customs station of clearance in India is not available

with the person liable for paying integrated tax, the same shall

be deemed to be 10 % of the CIF value (sum of cost, insurance

and freight) of imported goods.”;

5% [With ITC of input services[

Person liable to pay: Importer

[As defined in section 2(26) of the

Customs Act, 1962-Notification 10/2017-

Integrated Tax (Rate) dated 28.06.2017]

FREIGHT-HEADING 9965: GOODS TRANSPORT SERVICES

6TH December, 2017 PDD 17

Sr.No Particulars Rate

TRANSPORT OF GOODS BY ROAD

3.

Services of goods transport agency in relation to

transportation of goods

“goods transport agency” means any person who

provides service in relation to transport of goods by

road and issues consignment note, by whatever name

called.

[Notification 20/2017-Central Tax (Rate) dated 22.08.2017]

5% [With No ITC]

12% [with full ITC]

To be applied on all services of GTA

4. Services by way of transportation of goods-

(a) by road except the services of –

(i) a goods transport agency

[Notification 12/2017-Central Tax (Rate) dated 28.06.2017]

Exempt

FREIGHT-HEADING 9965: GOODS TRANSPORT SERVICES

6TH December, 2017 PDD 18

ISSUES

Import of goods has already suffered IGST on the value determined by custom valuation rule to includecost of transportation, handling and insurance related to importation. Whether 5% GST amounts todouble.

• Rule 10(2) of the Customs Valuation (Determination of Value of imported goods) Rules, 2007

The value of imported goods shall be the value of such goods, for delivery at the time and place of

importation and shall include-

(a) the cost of transport of the imported goods to the place of importation;

(b) loading, unloading and handling charges associated with the delivery of the imported goods at theplace of importation; and

(c) the cost of insurance.

• Section 7(2) of IGST Act: Supply of goods imported into the territory of India, till they cross thecustoms frontiers of India, shall be treated to be supply of goods in the course of inter-State trade orcommerce.

• Section 7(4) of the IGST Act: Supply of services imported into the territory of India shall be treated tobe supply of services in the course of inter-State trade or commerce.

• Section 2(30) of CGST Act: “Composite supply means a supply made by a taxable person to arecipient consisting of two or more taxable supplies of goods or services or both or any combinationthereof, which are naturally bundled and supplied in conjunction with each other in the ordinary courseof business, one of which is a principal supply”.

6TH December, 2017 PDD 19

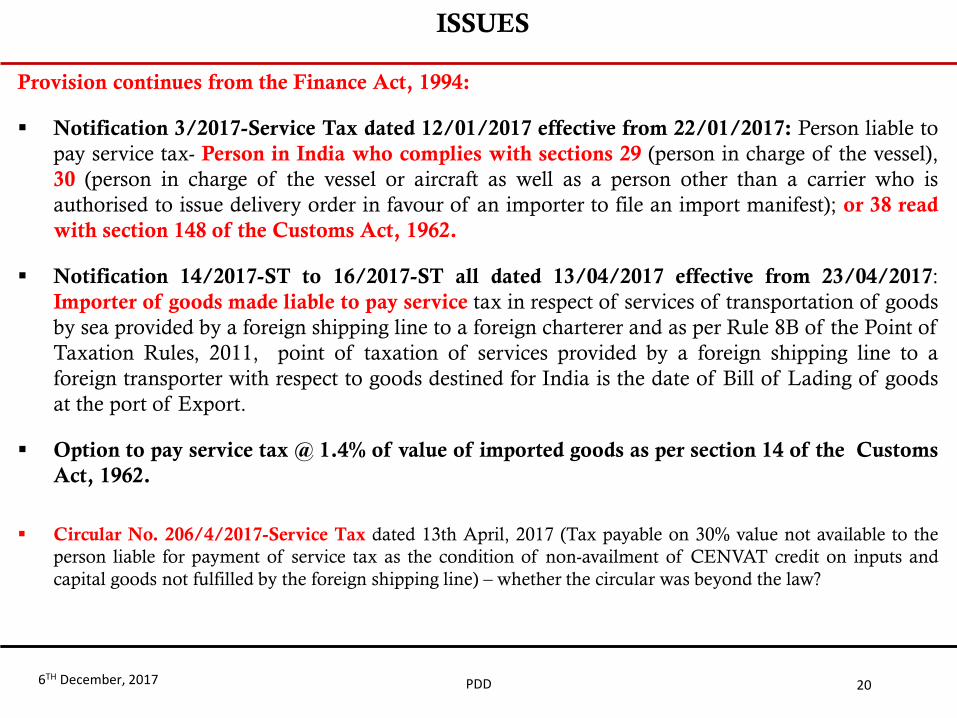

ISSUES

Provision continues from the Finance Act, 1994:

Notification 3/2017-Service Tax dated 12/01/2017 effective from 22/01/2017: Person liable to

pay service tax- Person in India who complies with sections 29 (person in charge of the vessel),

30 (person in charge of the vessel or aircraft as well as a person other than a carrier who is

authorised to issue delivery order in favour of an importer to file an import manifest); or 38 read

with section 148 of the Customs Act, 1962.

Notification 14/2017-ST to 16/2017-ST all dated 13/04/2017 effective from 23/04/2017:

Importer of goods made liable to pay service tax in respect of services of transportation of goods

by sea provided by a foreign shipping line to a foreign charterer and as per Rule 8B of the Point of

Taxation Rules, 2011, point of taxation of services provided by a foreign shipping line to a

foreign transporter with respect to goods destined for India is the date of Bill of Lading of goods

at the port of Export.

Option to pay service tax @ 1.4% of value of imported goods as per section 14 of the Customs

Act, 1962.

Circular No. 206/4/2017-Service Tax dated 13th April, 2017 (Tax payable on 30% value not available to the

person liable for payment of service tax as the condition of non-availment of CENVAT credit on inputs and

capital goods not fulfilled by the foreign shipping line) – whether the circular was beyond the law?

6TH December, 2017 PDD 20

ISSUES

A customs house agent (CHA) has received the services of a goods transport agency who has

charged GST @ 12% to the agent. Determine the GST rate to be charged in the following

scenarios by the CHA billing the shipper:

a) The transport charges are billed to the shipper at cost;

b) The transport charges are billed with profit margin;

6TH December, 2017 PDD 21

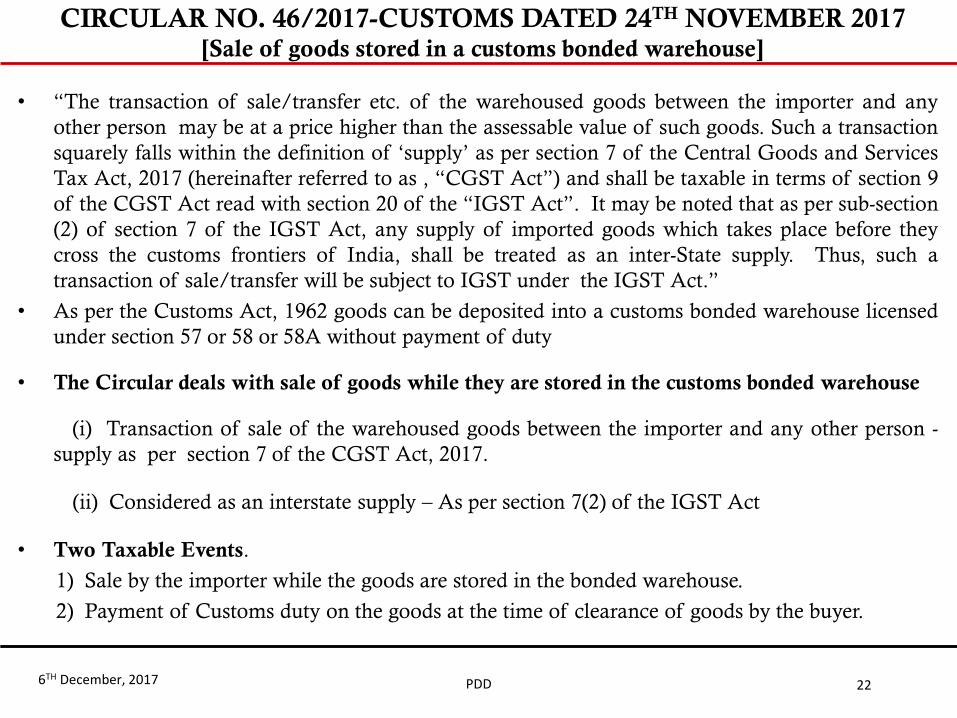

CIRCULAR NO. 46/2017-CUSTOMS DATED 24TH NOVEMBER 2017[Sale of goods stored in a customs bonded warehouse]

• “The transaction of sale/transfer etc. of the warehoused goods between the importer and any

other person may be at a price higher than the assessable value of such goods. Such a transaction

squarely falls within the definition of ‘supply’ as per section 7 of the Central Goods and Services

Tax Act, 2017 (hereinafter referred to as , “CGST Act”) and shall be taxable in terms of section 9

of the CGST Act read with section 20 of the “IGST Act”. It may be noted that as per sub-section

(2) of section 7 of the IGST Act, any supply of imported goods which takes place before they

cross the customs frontiers of India, shall be treated as an inter-State supply. Thus, such a

transaction of sale/transfer will be subject to IGST under the IGST Act.”

• As per the Customs Act, 1962 goods can be deposited into a customs bonded warehouse licensed

under section 57 or 58 or 58A without payment of duty

• The Circular deals with sale of goods while they are stored in the customs bonded warehouse

(i) Transaction of sale of the warehoused goods between the importer and any other person -

supply as per section 7 of the CGST Act, 2017.

(ii) Considered as an interstate supply – As per section 7(2) of the IGST Act

• Two Taxable Events.

1) Sale by the importer while the goods are stored in the bonded warehouse.

2) Payment of Customs duty on the goods at the time of clearance of goods by the buyer.

6TH December, 2017 PDD 22

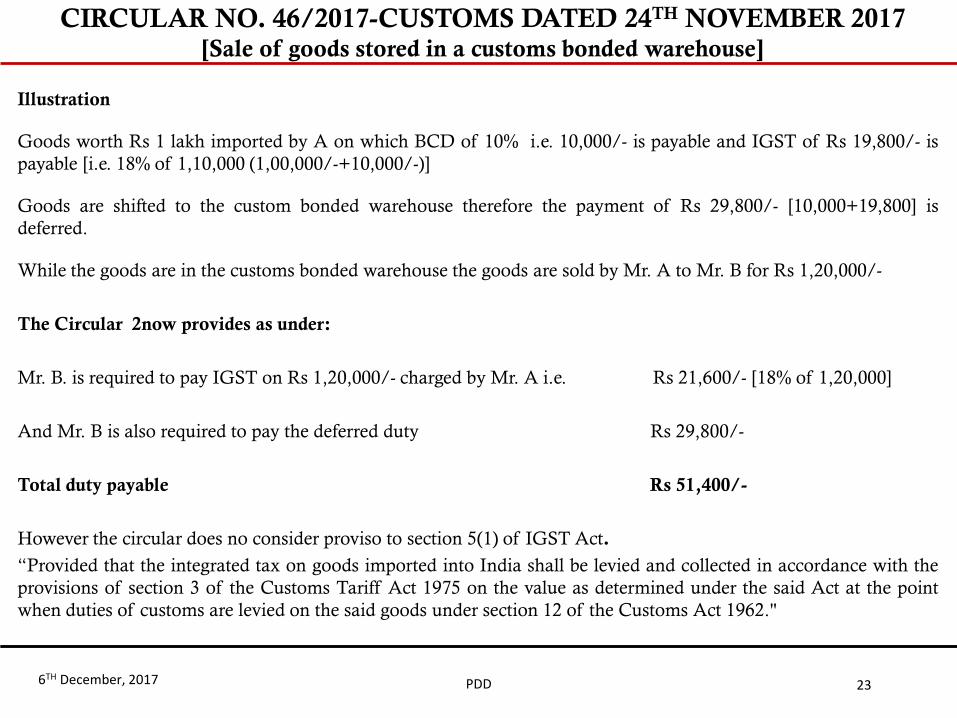

CIRCULAR NO. 46/2017-CUSTOMS DATED 24TH NOVEMBER 2017[Sale of goods stored in a customs bonded warehouse]

Illustration

Goods worth Rs 1 lakh imported by A on which BCD of 10% i.e. 10,000/- is payable and IGST of Rs 19,800/- is

payable [i.e. 18% of 1,10,000 (1,00,000/-+10,000/-)]

Goods are shifted to the custom bonded warehouse therefore the payment of Rs 29,800/- [10,000+19,800] is

deferred.

While the goods are in the customs bonded warehouse the goods are sold by Mr. A to Mr. B for Rs 1,20,000/-

The Circular 2now provides as under:

Mr. B. is required to pay IGST on Rs 1,20,000/- charged by Mr. A i.e. Rs 21,600/- [18% of 1,20,000]

And Mr. B is also required to pay the deferred duty Rs 29,800/-

Total duty payable Rs 51,400/-

However the circular does no consider proviso to section 5(1) of IGST Act.

“Provided that the integrated tax on goods imported into India shall be levied and collected in accordance with the

provisions of section 3 of the Customs Tariff Act 1975 on the value as determined under the said Act at the point

when duties of customs are levied on the said goods under section 12 of the Customs Act 1962."

6TH December, 2017 PDD 23

CIRCULAR NO. 46/2017-CUSTOMS DATED 24TH NOVEMBER 2017[Sale of goods stored in a customs bonded warehouse]

Circular No. 33/2017-Cus dated 01.08.2017- High Seas Sale

The council has decided that IGST on high sea sale (s) transactions of imported goods,

whether one or multiple, shall be levied and collected only at the time of importation i.e.

when the import declarations are filed before the Customs authorities for the customs

clearance purposes for the first time. Further, value addition accruing in each such high

sea sale shall form part of the value on which IGST is collected at the time of

clearance.

Whether the Circular No.46/2017-Customs resulting in two taxable events is

challengeable?

Whether any provision exists in law either for refund or for credit of IGST paid twice?

6TH December, 2017 PDD 24

CIRCULAR NO. 46/2017-CUSTOMS DATED 24TH NOVEMBER 2017

• Section 2(11) of the Customs Act, 1962: "customs area" means the area of a customs

station 12[or a warehouse] and includes any area in which imported goods or export goods are

ordinarily kept before clearance by Customs Authorities;

• Section 2(25) of the Customs Act, 1962 :"imported goods" means any goods brought into India

from a place outside India but does not include goods which have been cleared for home

consumption;

• Section 7(2) of the IGST Act: Supply of goods imported into the territory of India, till they cross

the customs frontiers of India, shall be treated to be supply of goods in the course of inter-state

trade or commerce.

• Section 2(56) of the CGST Act “India” means the territory of India as referred to in article 1 of

the Constitution, its territorial waters, seabed and sub-soil underlying such waters, continental

shelf, exclusive economic zone or any other maritime zone as referred to in the Territorial Waters,

Continental Shelf, Exclusive Economic Zone and other Maritime Zones Act, 1976, and the air

space above its territory and territorial waters

6TH December, 2017 PDD 25

CIRCULAR NO. 46/2017-CUSTOMS DATED 24TH NOVEMBER 2017

M/s Hotel Ashoka Vs. Assistant Commissioner of Commercial Taxes & ANR [ 2012 (03) VIL

(SC)]

Issue: Sale made by duty free shops at the Bengaluru International Airport

Held: "When the goods are kept in the bonded warehouses, it cannot be said that the said goods had crossed

the customs frontiers. The goods are not cleared from the customs till they are brought in India by crossing

the customs frontiers. When the goods are lying in the bonded warehouses, they are deemed to have been

kept outside the customs frontiers of the country and as stated by the learned senior counsel appearing for

the appellant, the appellant was selling the goods from the duty free shops owned by it at Bengaluru

International Airport before the said goods had crossed the customs frontiers [para 18].

Though the transaction might take place within India but technically, looking to the provisions of Section

2(11) of the Customs Act and Article 286 of the Constitution, the said transaction would be said to have

taken place outside India. In other words, it cannot be said that the goods are imported into the territory

of India till the goods or the documents of title to the goods are brought into India. Admittedly, in the

instant case, the goods had not been brought into the customs frontiers of India before the transaction of

sales had taken place and, therefore, in our opinion, the transactions had taken place beyond or outside the

custom frontiers of India.[para 30]

6TH December, 2017 PDD 26

WORKS CONTRACT SERVICES

Section (119) of the CGST Act: “works contract” means a contract for building, construction,

fabrication, completion, erection, installation, fitting out, improvement, modification, repair,

maintenance, renovation, alteration or commissioning of any immovable property wherein transfer

of property in goods (whether as goods or in some other form) is involved in the execution of such

contract.

Section 17(5) of the CGST Act:

(c) Works contract services when supplied for construction of an immovable property (other than

plant and machinery) except where it is an input service for further supply of works contract service.

(d) Goods or services or both received by a taxable person for construction of an immovable property

(other than plant and machinery) on his own account including when such goods or services or both

are used in the course or furtherance of business.

Explanation-for the purposes of clauses (c) and (d) the expression “construction” includes re-construction,

renovation, additions or alterations or repairs to the extent of capitalisation, to the said immovable property;

6TH December, 2017 PDD 27

ISSUES

(a) Whether Transferable Development Rights (TDR) purchased by a developer from a land owner is

liable for GST?

(b) Whether a developer is entitled to avail input tax credit of inputs and input services used for

construction of a commercial complex in the following scenarios:

(i) The shops in the commercial complex are meant for sale;

(ii) The shops are to be given on rent

Schedule III: Activities or transactions which shall be treated neither as supply of goods nor as

supply of services

5. Sale of land and, subject to clause(b) of paragraph 5 of Schedule II, sale of building.

6TH December, 2017 PDD 28

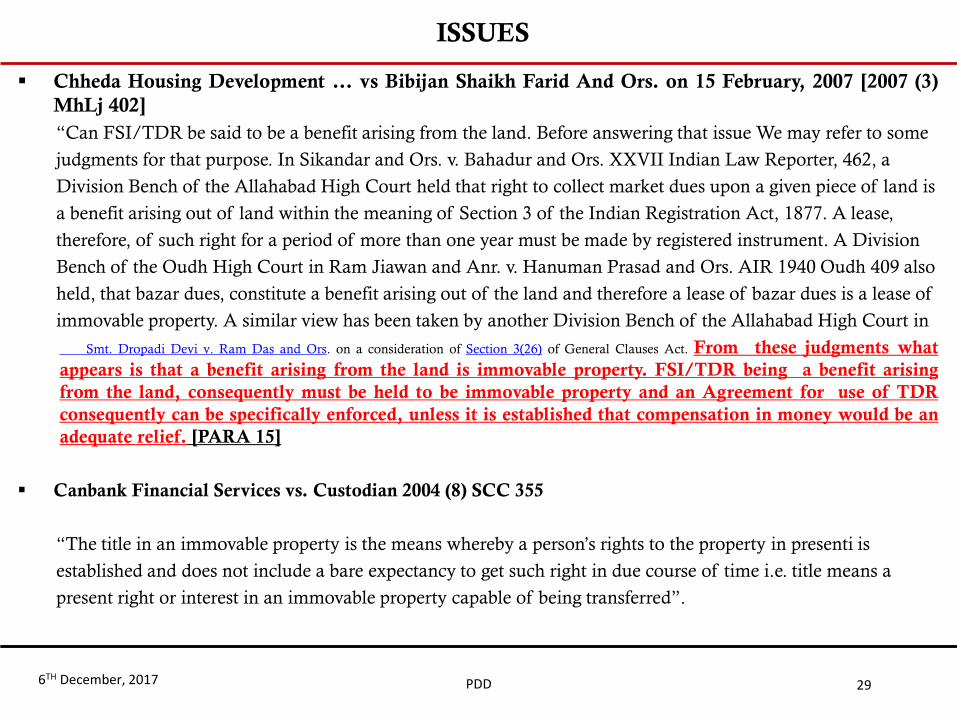

ISSUES

Chheda Housing Development ... vs Bibijan Shaikh Farid And Ors. on 15 February, 2007 [2007 (3)

MhLj 402]

“Can FSI/TDR be said to be a benefit arising from the land. Before answering that issue We may refer to some

judgments for that purpose. In Sikandar and Ors. v. Bahadur and Ors. XXVII Indian Law Reporter, 462, a

Division Bench of the Allahabad High Court held that right to collect market dues upon a given piece of land is

a benefit arising out of land within the meaning of Section 3 of the Indian Registration Act, 1877. A lease,

therefore, of such right for a period of more than one year must be made by registered instrument. A Division

Bench of the Oudh High Court in Ram Jiawan and Anr. v. Hanuman Prasad and Ors. AIR 1940 Oudh 409 also

held, that bazar dues, constitute a benefit arising out of the land and therefore a lease of bazar dues is a lease of

immovable property. A similar view has been taken by another Division Bench of the Allahabad High Court in

Smt. Dropadi Devi v. Ram Das and Ors. on a consideration of Section 3(26) of General Clauses Act. From these judgments what

appears is that a benefit arising from the land is immovable property. FSI/TDR being a benefit arising

from the land, consequently must be held to be immovable property and an Agreement for use of TDR

consequently can be specifically enforced, unless it is established that compensation in money would be an

adequate relief. [PARA 15]

Canbank Financial Services vs. Custodian 2004 (8) SCC 355

“The title in an immovable property is the means whereby a person’s rights to the property in presenti is

established and does not include a bare expectancy to get such right in due course of time i.e. title means a

present right or interest in an immovable property capable of being transferred”.

6TH December, 2017 PDD 29

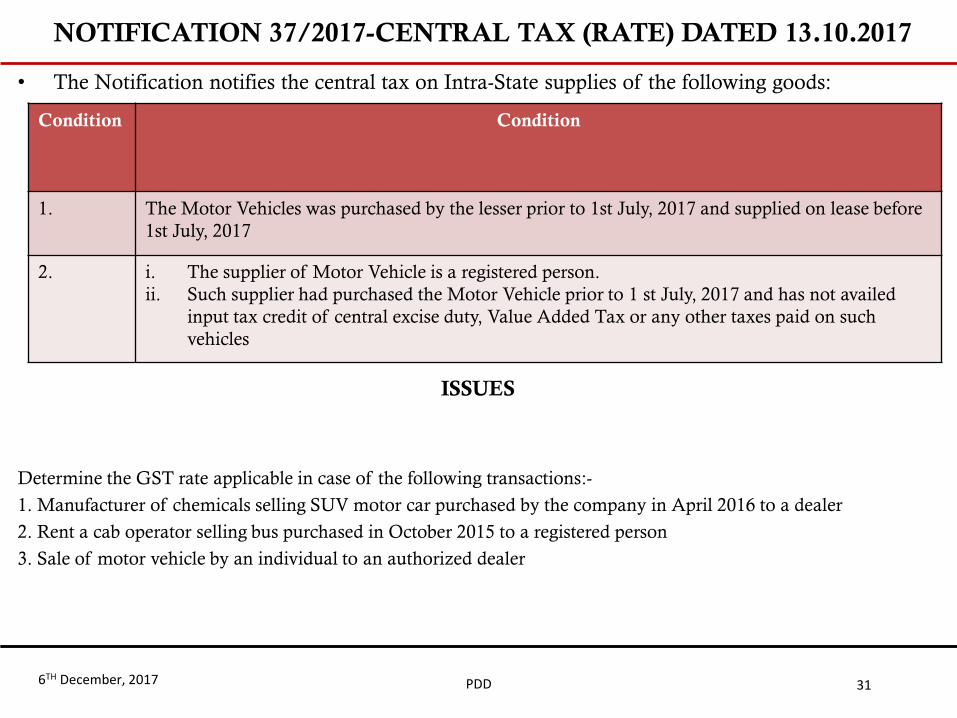

NOTIFICATION 37/2017-CENTRAL TAX (RATE) DATED 13.10.2017

• The Notification notifies the central tax on Intra-State supplies of the following goods:

6TH December, 2017 PDD 30

Sr.

No.

Chapter

Heading, Sub

Heading or

Tariff item

Description

of Goods

Rate Condition

1 87 Motor

Vehicles

65% of central tax applicable otherwise on such goods

under Notification No. 1/2017-Central Tax (Rate) dated,

28th June, 2017 published in the Gazette of India,

Extraordinary, Part II, Section 3, Sub Section (i), vide

G.S.R. 673 (E) dated the 28th June, 2017.

1

2 87 Motor

Vehicles

65% of central tax applicable otherwise on such goods

under Notification No. 1/2017-Central Tax (Rate) dated,

28th June, 2017 published in the Gazette of India,

Extraordinary, Part II, Section 3, Sub Section (i), vide

G.S.R. 673 (E) dated the 28th June, 2017

2

NOTIFICATION 37/2017-CENTRAL TAX (RATE) DATED 13.10.2017

• The Notification notifies the central tax on Intra-State supplies of the following goods:

ISSUES

Determine the GST rate applicable in case of the following transactions:-

1. Manufacturer of chemicals selling SUV motor car purchased by the company in April 2016 to a dealer

2. Rent a cab operator selling bus purchased in October 2015 to a registered person

3. Sale of motor vehicle by an individual to an authorized dealer

6TH December, 2017 PDD 31

Condition Condition

1. The Motor Vehicles was purchased by the lesser prior to 1st July, 2017 and supplied on lease before

1st July, 2017

2. i. The supplier of Motor Vehicle is a registered person.

ii. Such supplier had purchased the Motor Vehicle prior to 1 st July, 2017 and has not availed

input tax credit of central excise duty, Value Added Tax or any other taxes paid on such

vehicles

GST marches for its evolution on a journey uphill with task manifold.Do not whine or see bends, see only GOOD of the road ahead.For a CA can practice more with cobwebs to make a day Till the final destination arrives to see so SIMPLE a TAX.

May Good Luck go with you!!!

THANK YOU