receivables powerpoint slides to accompany fundamental accounting principles, 14ce prepared by joe...

TRANSCRIPT

ReceivablesReceivables

PowerPoint Slides to accompanyFundamental Accounting Principles, 14ce

Prepared byJoe Pidutti, Durham College

CHAPTER

9

© 2013 McGraw-Hill Ryerson Limited.

1. Describe accounts receivable and how they occur and are recorded. (LO1)

2. Apply the allowance method to account for uncollectible accounts receivable. (LO2)

3. Estimate uncollectible accounts receivable using approaches based on sales and accounts receivable. (LO3)

2 © 2013 McGraw-Hill Ryerson Limited.

Learning ObjectivesLearning Objectives

4. Describe and record a short-term note receivable and calculate its maturity date and interest. (LO4)

5. Explain how receivables can be converted to cash before maturity. (Appendix 9A) (LO5)

6. Calculate accounts receivable turnover and days’ sales uncollected to analyze liquidity. (Appendix 9B) (LO6)

3 © 2013 McGraw-Hill Ryerson Limited.

Learning ObjectivesLearning Objectives

• Arise from credit sales to customers.• Often referred to as Trade Receivables.• Other receivables include interest

receivable, rent receivable, tax refund receivable.

4 © 2013 McGraw-Hill Ryerson Limited.

Accounts ReceivableAccounts Receivable

LO 1

Companies selling on account need to:• Maintain a separate account for each

customer.• Account for bad debts.

5 © 2013 McGraw-Hill Ryerson Limited.

Accounts ReceivableAccounts Receivable

LO 1

Example: TechCom has the following Accounts Receivable balances at June 30:

6© 2013 McGraw-Hill Ryerson Limited.

General Ledger A/R Subledger

Accounts Receivable RDA Electronics

bal. 3,000 bal. 1,000

CompStore

bal. 2,000

Total 3,000

Control account balances with total of subledger balances.

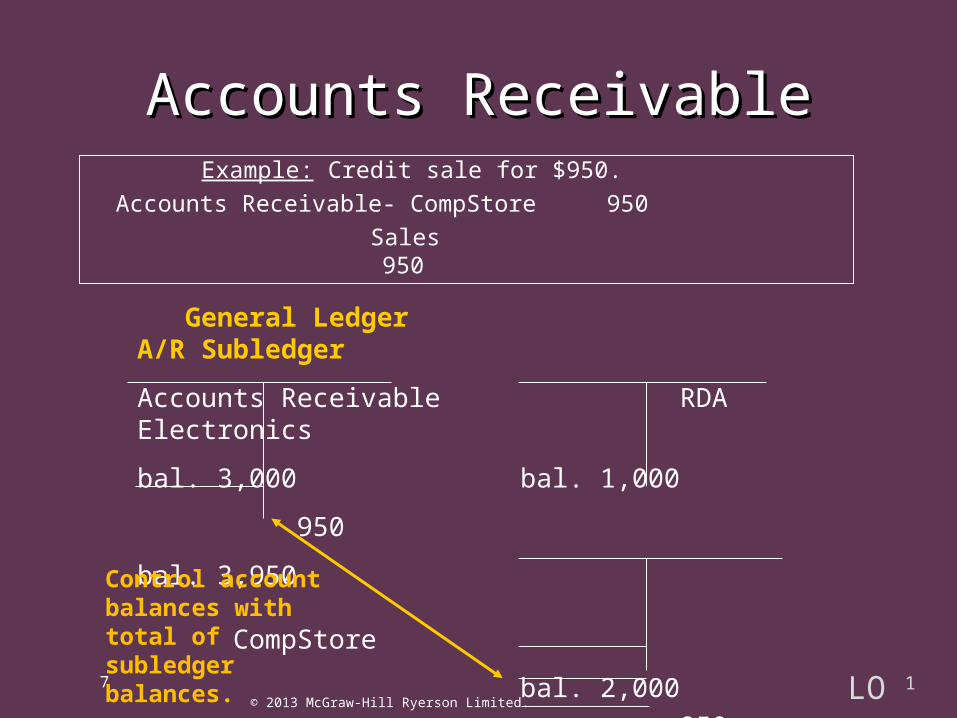

Accounts ReceivableAccounts Receivable

LO 1

General Ledger A/R Subledger

Accounts Receivable RDA Electronics

bal. 3,000 bal. 1,000

950

bal. 3,950 CompStore

bal. 2,000

950

bal. 2,950 Total 3,950

Control account balances with total of subledger balances.

Example: Credit sale for $950.

Accounts Receivable- CompStore 950

Sales 950

7© 2013 McGraw-Hill Ryerson Limited.

Accounts ReceivableAccounts Receivable

LO 1

General Ledger A/R Subledger

Accounts Receivable RDA Electronics

bal. 3,000 bal. 1,000 720

950 720 bal. 280

bal. 3,230 CompStore

bal. 2,000

950

bal. 2,950 Total 3,230

Control account balances with total of subledger balances.

Example: Collection of accountCash 720

Accounts Receivable-RDA 720

8© 2013 McGraw-Hill Ryerson Limited.

Accounts ReceivableAccounts Receivable

LO 1

• Some customers who are granted credit do not pay what they promised.

• The accounts of these customers are called uncollectible accounts or bad debts.

9 © 2013 McGraw-Hill Ryerson Limited.

Valuing Accounts ReceivableValuing Accounts Receivable

LO 1

Methods for accounting for uncollectible accounts:

1. Direct method (does not satisfy GAAP)

2. Allowance method (satisfies GAAP)a) Income statement approach (percent of sales)

b) Balance sheet approach (calculates the required balance in AFDA)

10 © 2013 McGraw-Hill Ryerson Limited.

Valuing Accounts ReceivableValuing Accounts Receivable

LO 2

• The matching principle requires that bad debts expense be matched and reported in the same period as the sale that generated the receivable.

• The allowance method satisfies the matching principle by matching expected bad debts losses (expenses) with revenues that produced the losses.

11 © 2013 McGraw-Hill Ryerson Limited.

Allowance MethodAllowance Method

LO 2

• Adjustments for bad debts are made at the end of the accounting period.

• Adjustments use a contra-asset account called Allowance for Doubtful Accounts.

12 © 2013 McGraw-Hill Ryerson Limited.

Recording Estimated Bad Debt Recording Estimated Bad Debt ExpenseExpense

LO 2

Example: The estimated bad debts for TechCom is $1,500.

The period end entry to record bad debts is:

Bad Debts Expense 1,500

Allowance for Doubtful Accounts 1,500

An allowance account is used since we do not know which accounts will be uncollectible.

13 © 2013 McGraw-Hill Ryerson Limited.

Recording Estimated Bad Debt Expense - Allowance Method

LO 2

Example: A specific customer’s account (Jack Kent) is considered uncollectible.

The entry to record the write-off is:

Allowance for Doubtful Accounts 520

Accounts Receivable - Jack Kent 520

Note that there is no expense recorded when the account is written off. The estimated expense was previously recorded.

14 © 2013 McGraw-Hill Ryerson Limited.

Writing Off a Bad Debt - Allowance Method

LO 2

General Ledger BalancesBad Debts Expense 1,500 Allowance for Doubtful Accounts 1,500To record estimated bad debts

Allowance for Doubtful Accounts 520 Accounts Receivable - Jack Kent 520To write off an uncollectible account

Accounts Receivable Allow. For Doubtful Accts.

bal. 20,000 1,500

520 520

bal. 19,480 bal. 980

15 © 2013 McGraw-Hill Ryerson Limited. LO 2

16 © 2013 McGraw-Hill Ryerson Limited.

Realizable Value Before and After Write-off

Before Write-off

After Write-off

Accounts Receivable $20,000 $19,480

Less: Allowance for Doubtful Accounts 1,500 980

Est. Realizable Accounts Receivable $18,500 $18,500

Accounts Receivable Allow. For Doubtful Accts.

bal. 20,000 1,500

520 520

bal. 19,480 bal. 980

LO 2

Example: Jack Kent pays his account in full after the account had been written off. Entries are needed to record the reinstatement of the account and the subsequent collection.

The entries are: Accounts Receivable-Jack Kent 520 Allowance for Doubtful Accounts 520 To reinstate customer’s account.

Cash 520 Accounts Receivable-Jack Kent 520 To record collection of account.

17 © 2013 McGraw-Hill Ryerson Limited.

Recovery of a Bad Debt- Allowance Method

LO 2

Acceptable Methods:

1. Percent of Sales Approach

2. Accounts Receivable Approach

18 © 2013 McGraw-Hill Ryerson Limited.

Estimating Bad Debts ExpenseEstimating Bad Debts Expense

LO 3

• Also referred to as the Income Statement Approach.

• Based on idea that a percentage of a company’s credit sales are uncollectible.

• The primary focus is on matching bad debts expense with credit sales.

19 © 2013 McGraw-Hill Ryerson Limited.

Percent of Sales ApproachPercent of Sales Approach

LO 3

Current Period Salesx Estimated Bad Debt %= Estimated Bad Debts Expense

Percent of Sales ApproachPercent of Sales Approach

20 © 2013 McGraw-Hill Ryerson Limited.

Under this approach, bad debts expense is computed as follows:

LO 3

Example: MusicLand has credit sales of $400,000 and estimates 0.6% of those sales will not be collectible. Estimated Bad Debts Expense is calculated as $2,400 ($400,000 x .6%).

The period end adjusting entry would be:

Percent of Sales ApproachPercent of Sales Approach

21 © 2013 McGraw-Hill Ryerson Limited.

Bad Debts Expense 2,400 Allowance for Doubtful Accounts 2,400To record estimated bad debts

LO 3

• This method assumes that a percentage of Accounts Receivable is uncollectible.

• Using this method, we compute the estimate of the Allowance for Doubtful Accounts as:

22 © 2013 McGraw-Hill Ryerson Limited.

Year-end Accounts Receivable x Est. Bad Debt %

Percent of Accounts Receivable Percent of Accounts Receivable Approach Approach

LO 3

Percent of Accounts Receivable Percent of Accounts Receivable ApproachApproach

23 © 2013 McGraw-Hill Ryerson Limited.

Bad Debts Expense is computed as:

Estimated adjusted balance in Allowance for Doubtful Accounts

- Unadjusted year-end balance in Allowance for Doubtful Accounts

= Estimated Bad Debts Expense

The objective for the entry is to make the Allowance account balance equal to the portion of outstanding Accounts Receivable estimated to be uncollectible.

LO 3

Assumes that the older the Account Receivable the more likely is will become uncollectible.

Steps:1. Group accounts based on how much time has

passed since they were created.2. Estimate rates of uncollectibility for each group.3. Apply rate to each group to get the required

balance for the Allowance account.

24 © 2013 McGraw-Hill Ryerson Limited.

Aging of Accounts Receivable Aging of Accounts Receivable ApproachApproach

LO 3

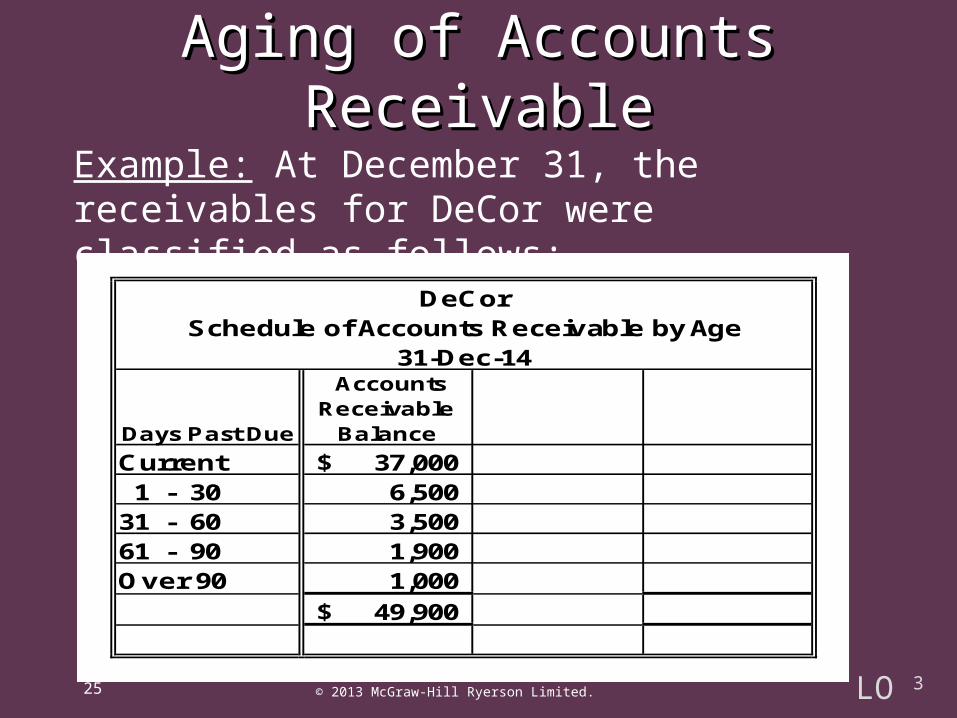

Example: At December 31, the receivables for DeCor were classified as follows:

Aging of Accounts ReceivableAging of Accounts Receivable

25 © 2013 McGraw-Hill Ryerson Limited.

DeCorSchedule of Accounts Receivable by Age

31-Dec-14

Days Past Due

Accounts Receivable

Balance

Current 37,000$ 1 - 30 6,500 31 - 60 3,500 61 - 90 1,900 Over 90 1,000

49,900$

LO 3

Using estimated bad debt percentages, DeCor would calculate the estimated uncollectible amount as follows:

Aging of Accounts ReceivableAging of Accounts Receivable

26 © 2013 McGraw-Hill Ryerson Limited.

DeCorSchedule of Accounts Receivable by Age

31-Dec-14

Days Past Due

Accounts Receivable

Balance

Estimated Bad Debts

Percent

Estimated Uncollectible

Amount

Current 37,000$ 2% 740$ 1 - 30 6,500 5% 325 31 - 60 3,500 10% 350 61 - 90 1,900 25% 475 Over 90 1,000 40% 400

49,900$ 2,290$

LO 3

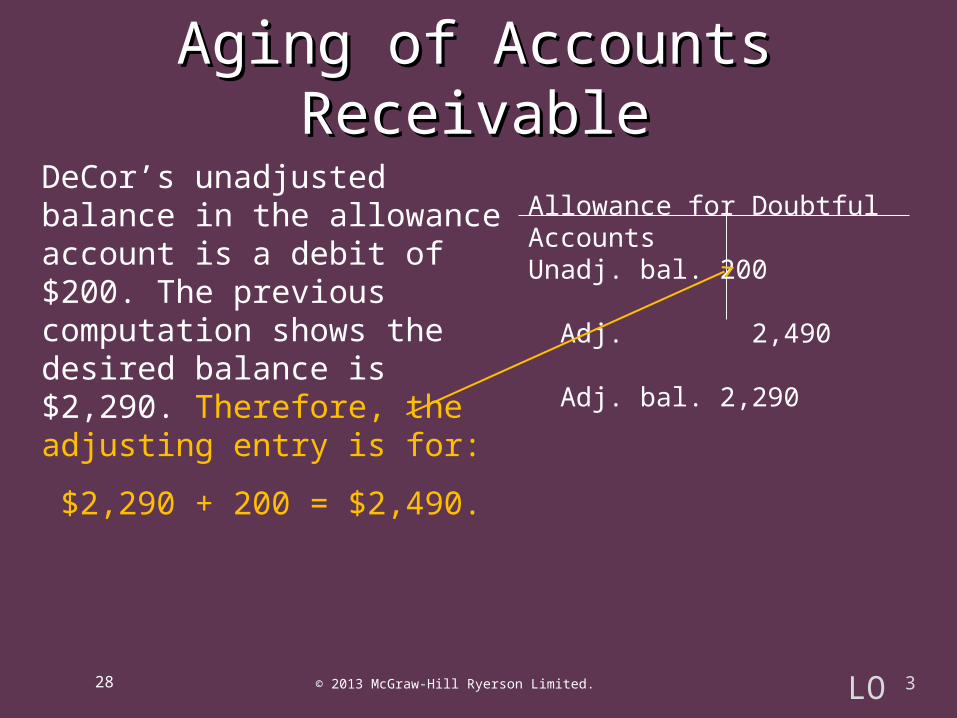

Allowance for Doubtful AccountsUnadj. bal. 200 Adj. bal. 2,290

DeCor’s unadjusted balance in the allowance account is a debit of $200. The previous computation shows the desired balance is $2,290.

Aging of Accounts ReceivableAging of Accounts Receivable

27 © 2013 McGraw-Hill Ryerson Limited. LO 3

DeCor’s unadjusted balance in the allowance account is a debit of $200. The previous computation shows the desired balance is $2,290. Therefore, the adjusting entry is for:

$2,290 + 200 = $2,490.

Aging of Accounts ReceivableAging of Accounts Receivable

28 © 2013 McGraw-Hill Ryerson Limited.

Allowance for Doubtful AccountsUnadj. bal. 200 Adj. 2,490 Adj. bal. 2,290

LO 3

DeCor’s unadjusted balance in the allowance account is a debit of $200. The previous computation shows the desired balance is $2,290. Therefore, the adjusting entry is for:

$2,290 + 200 = $2,490.

Aging of Accounts ReceivableAging of Accounts Receivable

29 © 2013 McGraw-Hill Ryerson Limited.

Bad Debts Expense 2,490 Allowance for Doubtful Accounts 2,490To record estimated bad debts

Allowance for Doubtful AccountsUnadj. bal. 200 2,490 Adj. bal. 2,290

LO 3

• Sometimes used as an alternative to the Allowance method when uncollectible accounts are not material.

• The loss from an uncollectible account is recorded when it is determined to be uncollectible.

• This method does not satisfy the principles of prudence and matching.

30 © 2013 McGraw-Hill Ryerson Limited.

Direct Write-off MethodDirect Write-off Method

LO 3

Example: A specific customer’s account (Jack Kent) is considered uncollectible. The entry to record the write-off is:

Bad Debts Expense 520

Accounts Receivable—Jack Kent 520

31 © 2013 McGraw-Hill Ryerson Limited.

Writing Off a Bad Debt - Writing Off a Bad Debt - Direct Write-off MethodDirect Write-off Method

LO 3

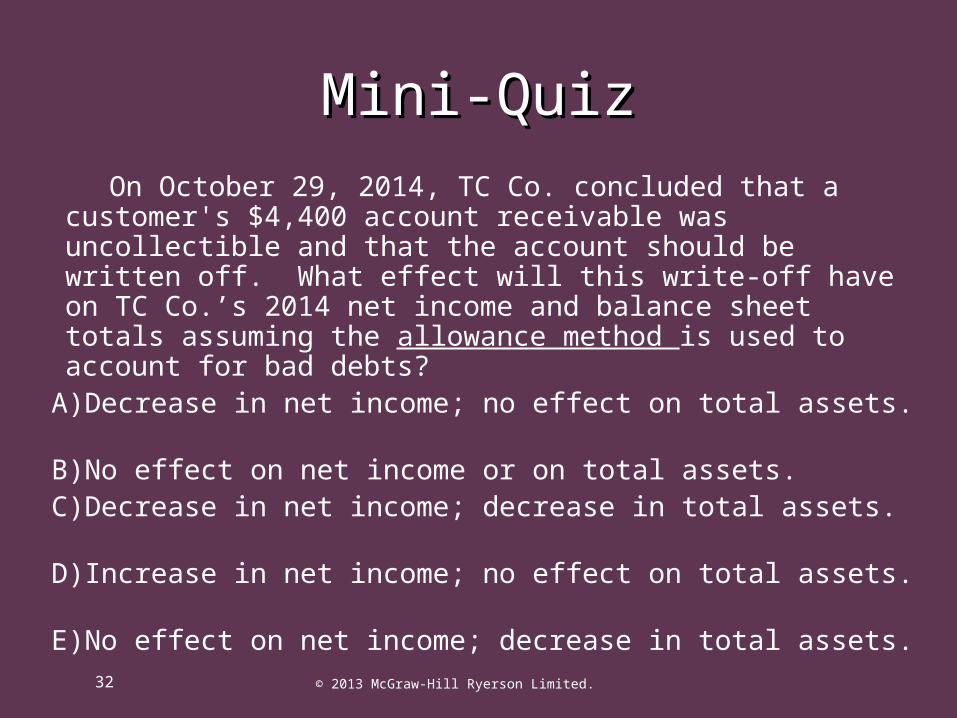

On October 29, 2014, TC Co. concluded that a customer's $4,400 account receivable was uncollectible and that the account should be written off. What effect will this write-off have on TC Co.’s 2014 net income and balance sheet totals assuming the allowance method is used to account for bad debts?

A)Decrease in net income; no effect on total assets. B)No effect on net income or on total assets. C)Decrease in net income; decrease in total assets. D)Increase in net income; no effect on total assets. E)No effect on net income; decrease in total assets.

32 © 2013 McGraw-Hill Ryerson Limited.

Mini-QuizMini-Quiz

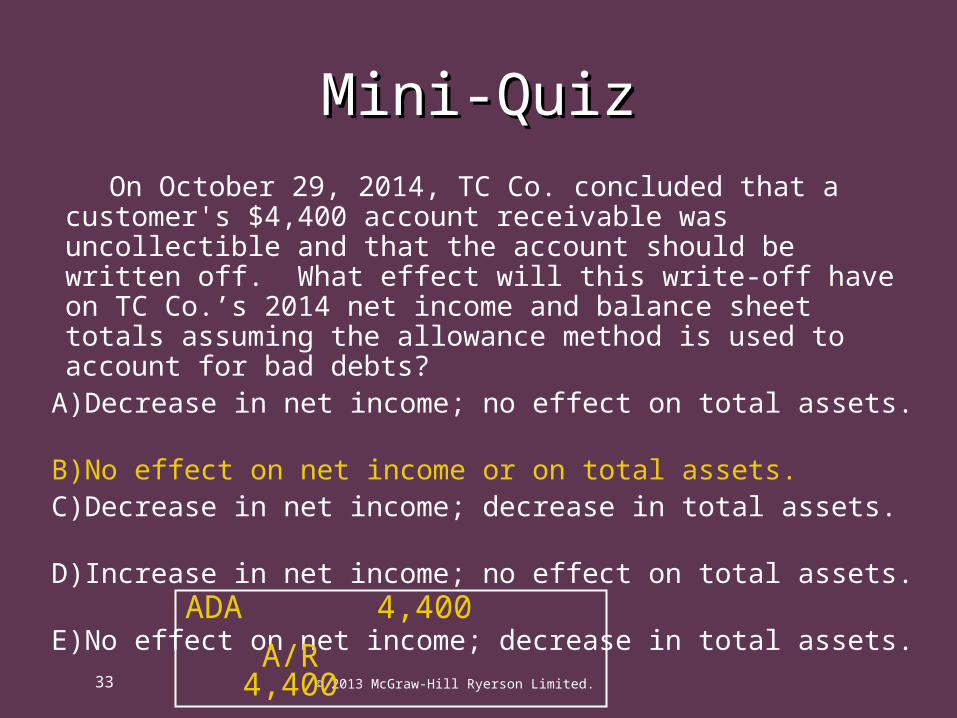

On October 29, 2014, TC Co. concluded that a customer's $4,400 account receivable was uncollectible and that the account should be written off. What effect will this write-off have on TC Co.’s 2014 net income and balance sheet totals assuming the allowance method is used to account for bad debts?

A)Decrease in net income; no effect on total assets. B)No effect on net income or on total assets. C)Decrease in net income; decrease in total assets. D)Increase in net income; no effect on total assets. E)No effect on net income; decrease in total assets.

33 © 2013 McGraw-Hill Ryerson Limited.

ADA 4,400

A/R 4,400

Mini-QuizMini-Quiz

Promissory Note A written promise to pay a specified amount

of money either on demand or at a definite future date.

Short-Term Note Receivable A promissory note that becomes due within

12 months or within the firm’s operating cycle.

34 © 2013 McGraw-Hill Ryerson Limited.

Short-Term Notes ReceivableShort-Term Notes Receivable

LO 4

• Usually interest bearing.• Interest rates are stated on an annual

basis.

Interest is calculated as follows:

35 © 2013 McGraw-Hill Ryerson Limited.

Interest =Principal of the note

Annual interest

rate

Time expressed

in yearsX X

Short-Term Notes ReceivableShort-Term Notes Receivable

LO 4

or I=Prt

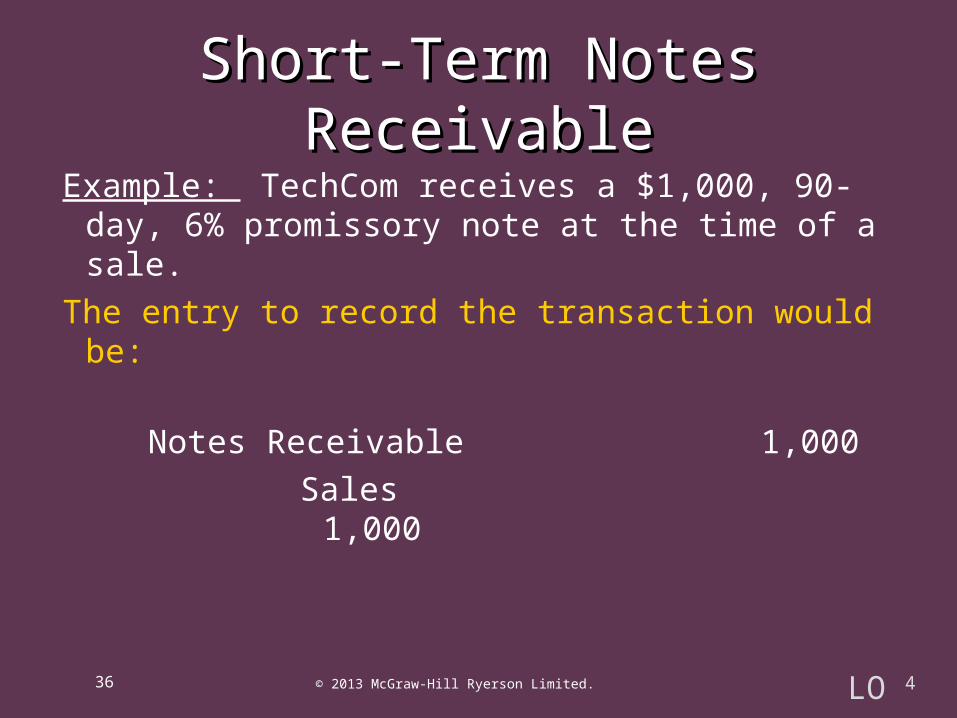

Short-Term Notes ReceivableShort-Term Notes Receivable

Example: TechCom receives a $1,000, 90-day, 6% promissory note at the time of a sale.

The entry to record the transaction would be:

Notes Receivable 1,000

Sales 1,000

36 © 2013 McGraw-Hill Ryerson Limited. LO 4

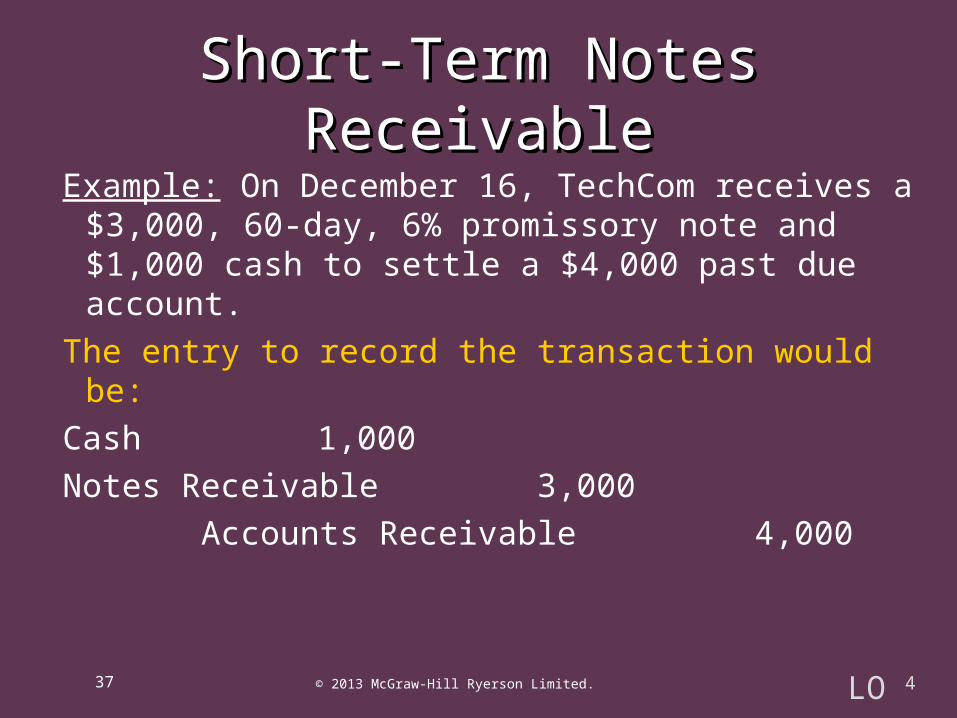

Short-Term Notes ReceivableShort-Term Notes Receivable

Example: On December 16, TechCom receives a $3,000, 60-day, 6% promissory note and $1,000 cash to settle a $4,000 past due account.

The entry to record the transaction would be:

Cash 1,000

Notes Receivable 3,000

Accounts Receivable 4,000

37 © 2013 McGraw-Hill Ryerson Limited. LO 4

Short-Term Notes ReceivableShort-Term Notes Receivable On December 31, 15 days after the note is issued, an accrual for

interest earned on the note is made. The entry to record the accrual would be:

Interest Receivable 7.40 Interest Revenue 7.40 (3,000 x 6% x 15/365) On February 14, the 60-day note matures. The entry to record the honouring of the note would be:

Cash 3,029.59 Interest Revenue 22.19 Interest Receivable 7.40 Notes Receivable 3,000.00 (3,000 x 6% x 60/365)= 29.59

38 © 2013 McGraw-Hill Ryerson Limited. LO 4

Short-Term Notes ReceivableShort-Term Notes Receivable

• Sometimes the maker of a note does not pay the note at maturity. This is known as dishonouring the note.

• The payee should use every legitimate means to collect.

• If the note was made to replace an AR then it should be removed from Notes Receivable and reinstated as an Account Receivable.

39 © 2013 McGraw-Hill Ryerson Limited. LO 4

ReviewReview

Explain why the allowance method satisfies the generally accepted principles of prudence and matching.

• The allowance method ensures that the asset, accounts receivable, and the reported net income are not overstated. In this way it accomplishes the requirements of the prudence principle.

• The allowance method recognizes the bad debts expense in the same period in which the related credit sales were recognized. In this way it accomplishes the required matching of expenses with the period in which the revenue was recognized.

40 © 2013 McGraw-Hill Ryerson Limited.

ReviewReview

Explain how to record the receipt of a note receivable.

• A note is recorded by entering the total amount borrowed (principal) as a debit to Notes Receivable and as a credit to the account representing the asset or service exchanged for the note.

41 © 2013 McGraw-Hill Ryerson Limited.

Receivables are sometimes converted into cash before maturity since:

1. Companies may need the cash.

2. Companies do not want to be involved in the collection activities.

42 © 2013 McGraw-Hill Ryerson Limited.

Converting Receivables to Cash Converting Receivables to Cash Before Maturity- Appendix 9ABefore Maturity- Appendix 9A

LO 5

Conversion of receivables into cash is accomplished by either:

1. Selling them to a factor

2. Pledging them as loan security.

43 © 2013 McGraw-Hill Ryerson Limited. LO 5

Converting Receivables to Cash Converting Receivables to Cash Before Maturity- Appendix 9ABefore Maturity- Appendix 9A

The quality (likelihood of collection) and liquidity (speed of collection) of a company’s receivables may be assessed by calculating:

1. Accounts receivable turnover ratio

2. Days’ sales uncollected

Using the Information Using the Information Appendix 9BAppendix 9B

44 © 2013 McGraw-Hill Ryerson Limited. LO 6

Accounts receivable turnover = Net Sales

Average accounts receivable

Days’ sales

Uncollected = Accounts receivable

Net salesx 365

45 © 2013 McGraw-Hill Ryerson Limited. LO 6

Using the Information Using the Information Appendix 9BAppendix 9B

End of Chapter End of Chapter

46 © 2013 McGraw-Hill Ryerson Limited.