real estate trends in central ohio - uli...

TRANSCRIPT

Real Estate Trends in Central Ohio

Presentation by Jung Kim | December 3, 2015

The National Picture: Highlights from ULI’s Emerging Trends in Real Estate

4.02 3.98

3.85 3.81 3.80

3.70 3.67 3.67 3.61 3.61 3.55 3.52

3.44

1.00 2.00 3.00 4.00 5.00

Real estate brokers Private real estate owners/developers

Institutional real estate owners/developers Real estate investment managers

Commercial builders Homebuilders/land developers

Architects/designers REITS

Insurance company RE lenders Real estate consultants

Commercial bank RE lenders CMBS lenders/issuers

Property managers

2016 2015 2014 2013 2012

Prospects by real estate industry Abysmal Fair Excellent

Top 10 issues for real estate in 2016 No

importance Moderate

importance Great

importance

4.56 4.13 4.10

4.03 3.95

3.83 3.78

3.57 3.53 3.51

1.00 2.00 3.00 4.00 5.00

Job growth Construction costs

Income and wage growth Land costs

Interest rates Infrastructure funding/development

Vacancy rates Transportation funding

Global economic growth Refinancing

Underwriting standards in 2016

DEBT

EQUITY

35.4% 45.7%

43.3% 19.6%

31.9% 29.8%

51.7% 44.7%

39.4% 41.5%

35.1% 29.2%

12.9% 9.6%

17.4% 39.1%

33.0% 41.0%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2016 2015 2014 2013 2012 2011

Less rigorous Remain the same More rigorous

34.0% 41.4%

30.7% 19.6% 22.8%

26.6%

52.4% 47.5%

50.8% 50.7% 46.7% 40.6%

13.6% 11.1%

18.5% 29.7% 30.5%

32.8%

2016 2015 2014 2013 2012 2011

Equity availability in 2016 Very large

decline Stay the

same Very large increase

3.90

3.60

3.60

3.50

3.31

3.26

1.00 2.00 3.00 4.00 5.00

Foreign investors

Institutional investors/pension funds

Private equity/opportunity/hedge funds

Private local investors

Private REITs

Public equity REITs

Debt availability in 2016 Very large

decline Stay the

same Very large increase

3.65

3.59

3.58

3.48

3.44

3.33

2.91

1.00 2.00 3.00 4.00 5.00

Securitized lenders/CMBS

Nonbank financial institutions

Mezzanine lenders

Insurance companies

Commercial banks

Mortgage REITs

Government-sponsored enterprises

Real estate capital market balance

38% 44%

48% 46%

14% 11%

2015 2016

Oversupplied In balance Undersupplied

14%

35%

56%

55%

30%

10%

2015

2016

20%

25%

51%

52%

30%

23%

2015

2016

55%

64%

33%

29%

12%

8%

2015

2016

Debt capital for acquisitions Debt capital for refinancing Debt capital for development Equity capital for investing

Next stop: the suburbs?

Cities 46%

Cities 37%

Suburbs 24%

Suburbs 29%

Rural/small towns 30%

Rural/small towns 32%

Current

Desired

Millennials current and desired location

Big city 46%

Big city 61%

Medium-sized city 54%

Medium-sized city 39%

Current

Desired

Suburbs <20 min. 70%

Suburbs <20 min. 76%

Suburbs >20 min. 30%

Suburbs >20 min. 24%

Current

Desired

The Local Picture: Real Estate Trends in Central Ohio

Respondents by field

Private Developer

32%

Builder 3%

Lender 8% Institutional

Investor 8%

Brokerage 3%

Professional Service Firm

30%

Government 8%

University 3%

Other 5%

Respondents by title

Owner 32%

President/CEO 13%

EVP/COO/CFO 10%

Vice President 8%

Director/ Manager

26%

Associate 8%

Other 3%

Respondents by sector

64% 58%

47% 28% 28%

25% 25%

22%

0% 20% 40% 60% 80% 100%

Residential - rental

Office

Retail

Residential - for sale

Industrial/distribution

Hospitality

Niche/alternative

Institutional/public

Expected profitability of own business

Excellent

Good

Fair

Poor

Abysmal

Excellent Good Fair Poor Abysmal

3.68 4.02 4.05

4.27 3.89 3.91 4.06

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

2013 2014 2015 2016

Expectations Actual

Expected profitability of own business

Excellent

Good

Fair

Poor

Abysmal

Excellent Good Fair Poor Abysmal

3.98 4.06 4.28 4.09 4.27 4.14

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Cleveland Columbus Indiana

2015 2016

Central Ohio relative to other markets

3.30

3.42

3.75

3.50

3.30

3.30

3.46

3.46

3.39

3.42

3.22

3.21

3.09

3.29

3.42

3.23

3.27

3.43

3.22

3.09

3.26

3.54

3.58

3.35

1.00 2.00 3.00 4.00 5.00

REITs

Real estate investment management

Private local real estate owners

Commercial bank real estate lenders

CMBS lenders/issuers

Insurance company real estate lenders

Real estate brokers

Architects, designers

Real estate consultants

Commercial developers

Multifamily developers

Homebuilders/residential land developers

2016 2015

Much worse

Somewhat better

Much better

About the same

Somewhat worse

Central Ohio relative to other markets "Overall, Columbus is healthy and doing well compared to its peers."

"Columbus across the board is good. For industrial, we are top 5 in second tier markets in rent growth, absorption, and delivery."

Central Ohio compares “very, very favorably, especially with the technology industry."

Central Ohio 2016 issues: Economy

Excellent

Good

Fair

Poor

Abysmal

4.22

4.03

4.00

3.51

3.19

3.38

3.95

3.95

3.65

3.10

3.30

3.18

1.00 2.00 3.00 4.00 5.00

Job growth

Income and wage growth

Interest rates

Inflation

Energy prices

State and local budget problems

2016 2015

No importance Great

importance Moderate

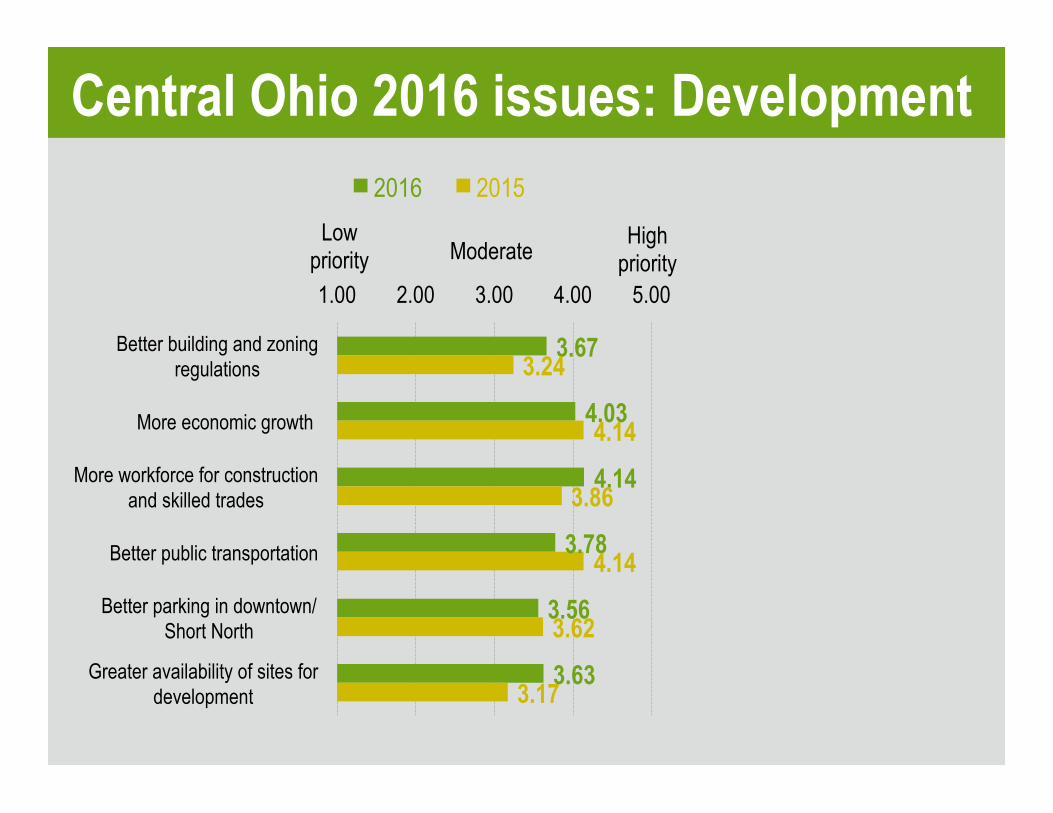

Central Ohio 2016 issues: Development

Excellent

Good

Fair

Poor

Abysmal

3.67

4.03

4.14

3.78

3.56

3.63

3.24

4.14

3.86

4.14

3.62

3.17

1.00 2.00 3.00 4.00 5.00

Better building and zoning regulations

More economic growth

More workforce for construction and skilled trades

Better public transportation

Better parking in downtown/Short North

Greater availability of sites for development

2016 2015 Low

priority High

priority Moderate

Central Ohio 2016 issues "Every sub trade has the same issue of finding qualified workforce."

"Material costs for the most part have stayed pretty level, but labor costs are going up quite a bit."

"Sites are going to be a challenge due to zoning regulations."

Investment Recommendation: INDUSTRIAL

"Industrial is huge for us right now" and "will continue to stay strong."

Industrial is "very attractive on a national scale," but Central Ohio performs well "even as it relates to other markets around the country."

0% 50% 100%

All industrial

Bulk/distribution space

General industrial

R&D industrial

Self-storage

Sell Hold Buy

Cleveland

Columbus

Indiana

Investment Recommendation: OFFICE

"The number of people per square foot has changed and are downsizing."

"Trend of people wanting to locate in an urban area for their workforce, more so than we have seen over the past 20 or 30 years."

0% 50% 100%

All office

CBD office

Suburban office

Medical office

Sell Hold Buy

Cleveland

Columbus

Indiana

Investment Recommendation: RETAIL

Development "very flat," but "financially, retail is very strong."

"Downsizing and consolidation of tenants caused by online distribution channels."

With omnichannel, stores are "trying to do more or the same in smaller spaces."

0% 50% 100%

All retail

Regional malls

Power centers

Neighborhood/community

Sell Hold Buy

Cleveland

Columbus

Indiana

Investment Recommendation: RENTAL

"I don't see anything on the horizon slowing the activity down."

"Multifamily might slow down a little bit, but the demand is still out there."

"There is a really strong push to downsize and want the quality of life downtown can provide."

0% 50% 100%

All apartments

Luxury apartments

Moderate apartments

Tax credit apartments

Student housing

Sell Hold Buy

Cleveland

Columbus

Indiana

"The market is hot for residential for sale." "Residential sales have been very good." "Land is getting tougher and tougher to find."

"I don’t think the for-sale model will be as frothy as the early 2000’s, but we are seeing a growing demand for buyers."

Investment Recommendation: FOR SALE

Interest rates

Fall Moderately 3%

Remain Stable 19%

Increase Moderately

75%

Increase Substantially

3%

Expected change next 3 years Response to rate rise

0% 20% 40% 60% 80% 100%

Obtain financing or refinancing now

Adjust portfolio

Reduce development activity

Scale back risk

Cleveland Columbus Indiana

"Certainly, interest rates have not gone up as soon as people thought they would, but hopefully it will happen in a thoughtful manner."

"Slight increases – 50 to 75 basis points." Financing strategies include "putting in hedges and interest rate caps and swaps" and "locking our rates for existing assets at sub-5% rates."

Interest rates

Capital availability

Oversupplied 18%

In Balance 55%

Undersupplied 24%

Substantially Undersupplied

3%

Availability through 2016 Expected change in availability

Some Increase 35%

No Change 56%

Some Decline 9%

"The banks have been more aggressive than they were even in 2013 and 2014, so that has freed up capital to get deals done."

"For every dollar of equity needed, there are $4 or $5 chasing deals."

"Blocking and tackling is more difficult" as investors "require evidence that there is a market for the projects they are financing."

Capital availability

Prospects for Central Ohio submarkets

Powell 3.80 (+0.03) Polaris

3.94 (+0.02)

Dublin 4.21 (+0.21)

New Albany 4.12 (-0.15)

UA/Grandview 4.27 (+0.39)

Downtown4.33 (+0.12)

Easton 4.26 (-0.11)

Hilliard 3.41 (-0.18)

Gahanna/CMH 3.66 (+0.22)

Cbus North 3.50 (-0.32)

Cbus West 2.72 (+0.22)

Cbus East 2.81 (+0.17)

Worthington 3.75 (+0.33)

Westerville 3.73 (+0.08)

Cbus South 2.44 (+0.12)

Reynoldsburg 2.91 (+0.26)

Groveport/Obetz 3.13 (-0.06)

Grove City 3.34 (+0.15)

North Delaware 3.50 (+0.08)

Union 3.34 (+0.06)

Madison 2.74 (-0.06)

Pickaway 2.70 (-0.10)

Licking 3.07 (+0.31)

Fairfield 3.07 (+0.23)

Color Score

5 = Excellent

4.0 to 4.5

4 = Good

3.5 to 4.0

3.0 to 3.5

3 = Fair

2.5 to 3.0

2.0 to 2.5

2 = Poor

1 = Abysmal

Prospects for Central Ohio submarkets "Downtown is at a place it’s probably never been. Tremendous amount of momentum and on its way to becoming a great neighborhood."

"Anything urban is hot."

"It will be interesting to see the willingness of further out suburban communities to urbanize."

Hot Topics: Housing Affordability To what extent do you agree or disagree with the following statements?

0% 20% 40% 60% 80% 100%

Development is in line with demographic trends and

market demand

There has been too much focus on high-end rental units

Much of the new rental product is too small to continue to be competitive in the market as

millennials age

Strongly disagree Disagree Neutral Agree Strongly agree "Vacancy rate downtown is pretty low, so I think the market is able to satisfy the creation of these luxury apartments."

"No better time to mix in affordable housing as you are doing larger scale developments."

"Affordable works, but only with subsidies. We need more focus on how to do that."

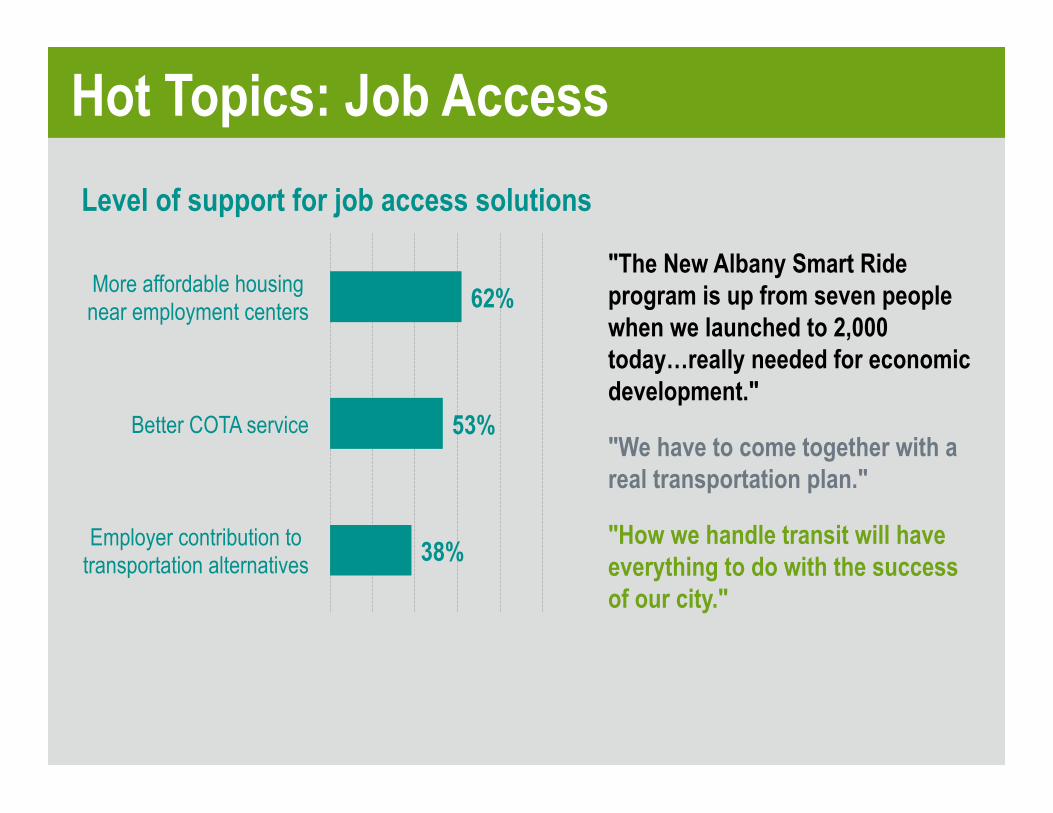

Hot Topics: Job Access Level of support for job access solutions

62%

53%

38%

More affordable housing near employment centers

Better COTA service

Employer contribution to transportation alternatives

"The New Albany Smart Ride program is up from seven people when we launched to 2,000 today…really needed for economic development."

"We have to come together with a real transportation plan."

"How we handle transit will have everything to do with the success of our city."

Five Takeaways for 2016 1. Great expectations: 2016 business prospects at highest score

ever in Real Estate Trends in Central Ohio.

2. O skilled tradesman, where art thou?: Workforce shortages a major pain point, leading to higher development costs and prices.

3. Doing more with less (space): Retail, office, and rental housing maximizing value with smaller spaces.

4. Fed said dovish, so did our survey: Small and gradual rises in interest rates.

5. Downtown takes the reins: Downtown Columbus ranks as top Central Ohio submarket for 2016.