rc 163170 - cornerstone annual... · 5 corporate information contd. 2016 annual report &...

TRANSCRIPT

21, Water Corporation Drive, Off Ligali Ayorinde Street, Victoria Island, Lagos.

Tel: 012806500 Web: www.cornerstone.com.ng

Email: [email protected]

RC 163170

2016ANNUAL REPORT & ACCOUNTS

PROFESSIONALISM

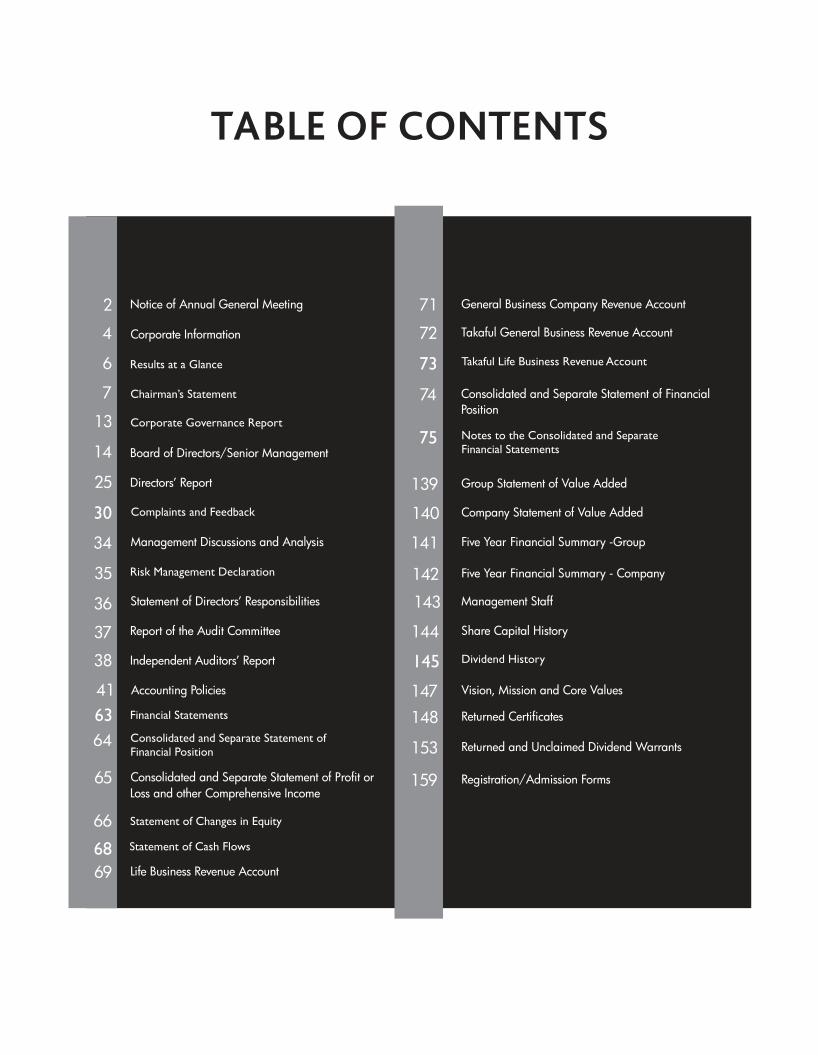

30

Risk Management Declaration

Financial Statements63Consolidated and Separate Statement of Financial Position

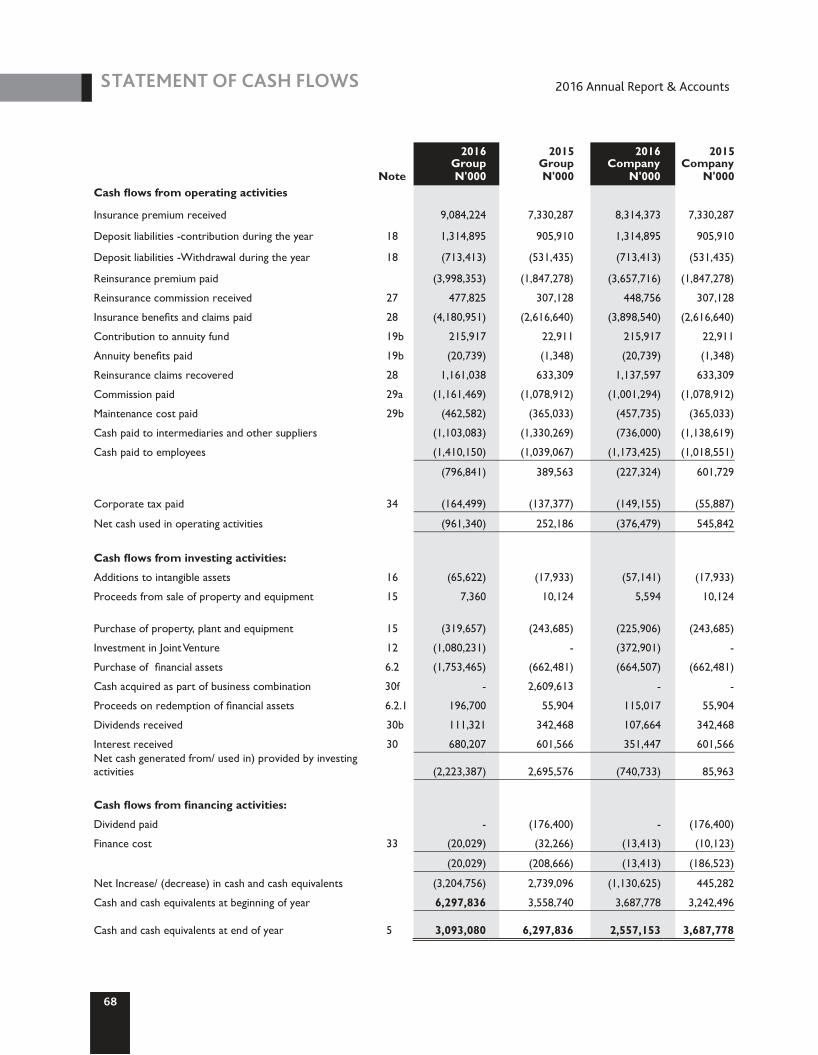

Statement of Cash Flows68

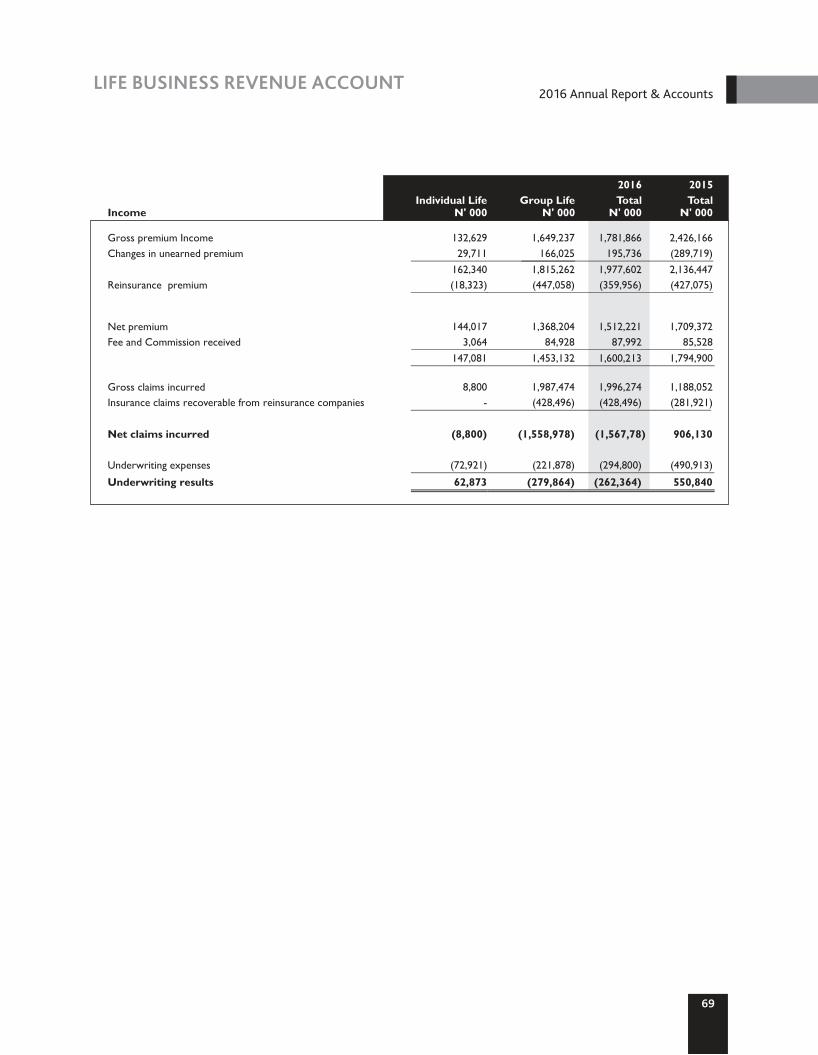

Takaful Life Business Revenue Account73

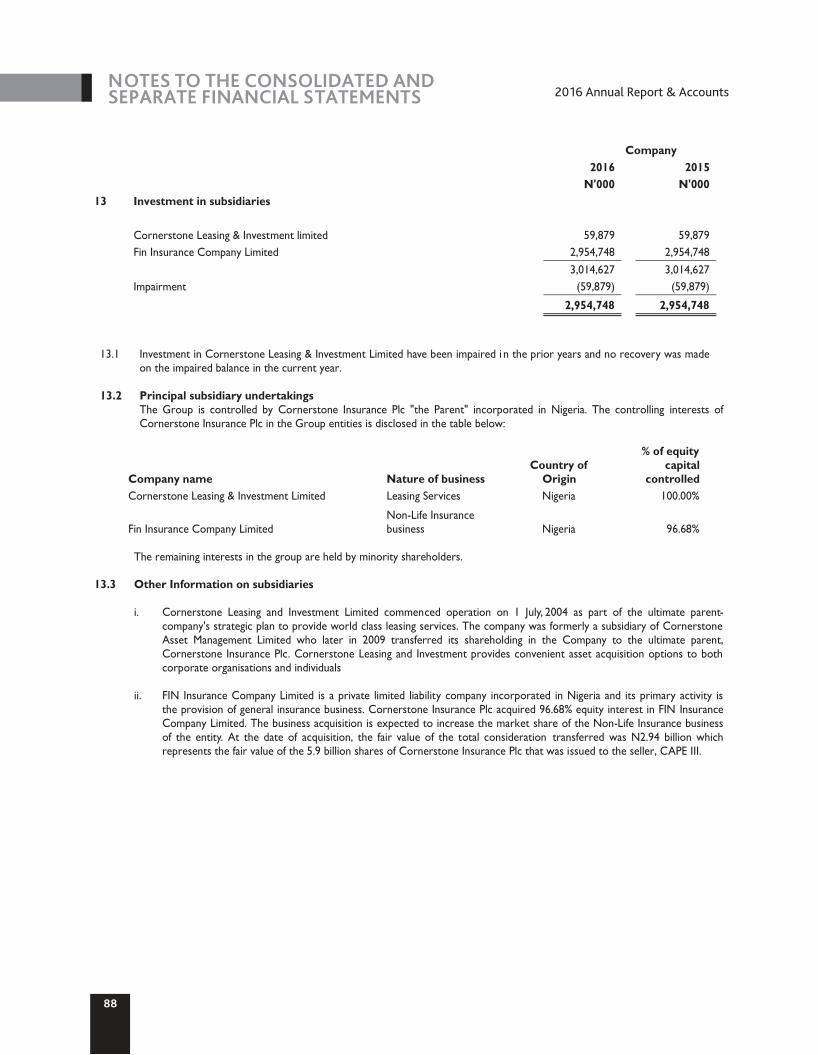

Notes to the Consolidated and Separate Financial Statements

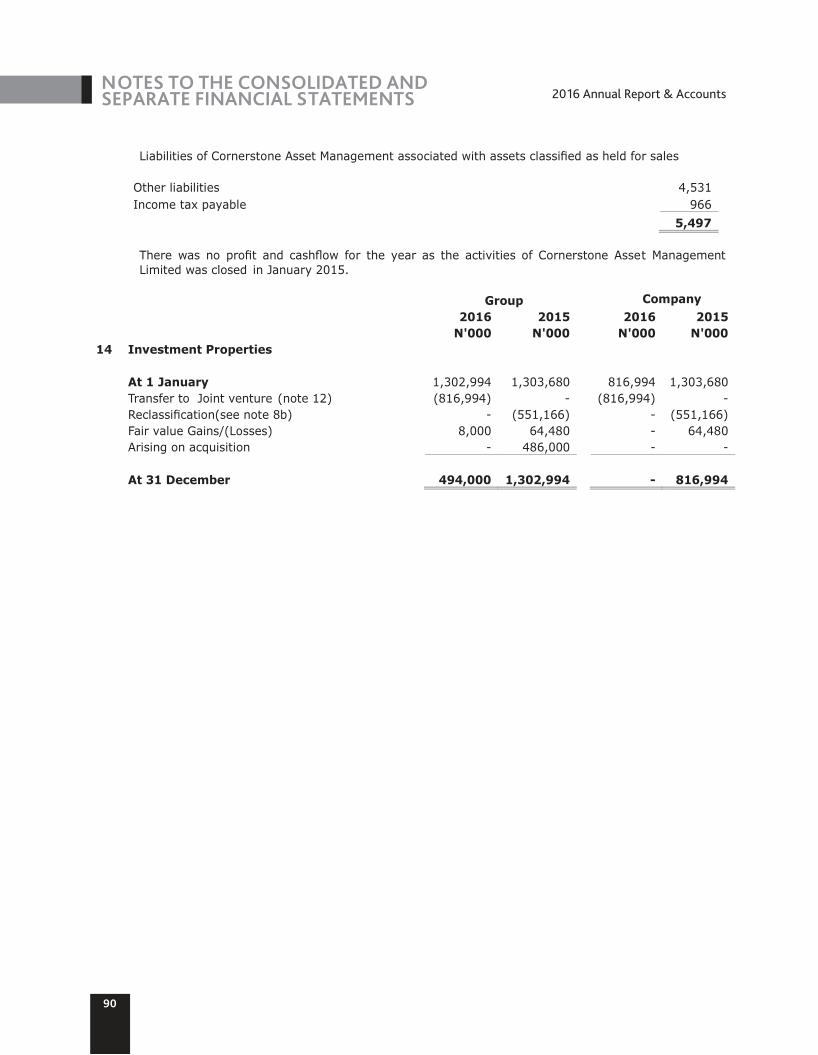

75

Dividend History145

Results at a Glance

Chairman’s Statement

Corporate Governance Report

Complaints and Feedback

Statement of Changes in Equity

2

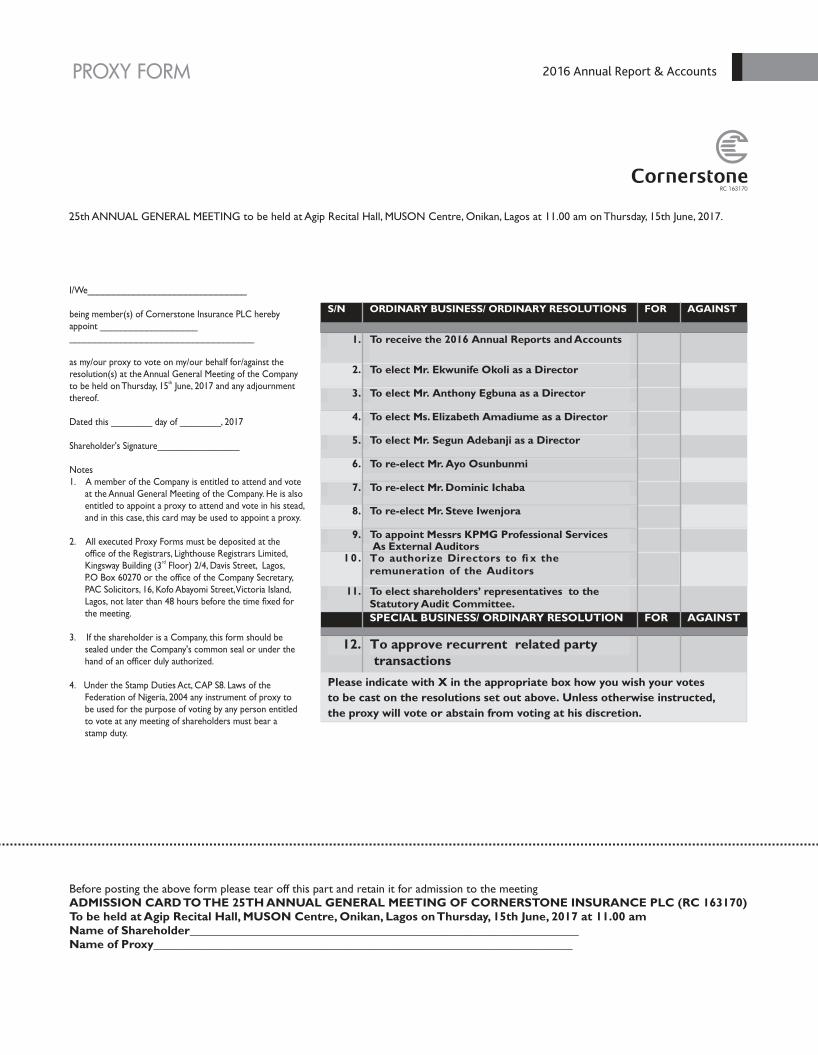

NOTICE OF ANNUAL GENERAL MEETING 2016 Annual Report & Accounts

ORDINARY BUSINESS

1. To receive the Audited Financial Statements of the Company for the year ended December 31, 2016 together with the Reports of the Directors, Auditors and Audit Committee thereon;

2. To elect and re-elect Directors;

3. To authorise the Directors to fix the remuneration of the Auditors;

4. To elect shareholders' representatives to the Audit Committee; and

5. To consider and if thought fit, pass the following resolution as an ordinary resolution of which Special Notice has been given in accordance with Section 364 (1) (a) of the Companies and Allied Matters Act, CAP C20, LFN, 2004:

“that Messrs. Akintola Williams Deloitte, shall retire as Auditors of the Company in line with Section 8 (iii) of the NAICOM Code of Corporate Governance and in their stead, Messrs, KPMG Professional Services be and are hereby appointed as Auditors of the Company.

SPECIAL BUSINESS

6. To consider and if thought fit, pass the following as an ordinary resolution:

Approval of Related Party Transactions

“That a General Mandate be and is hereby given to the Company to enter into recurrent transactions with related parties for the Company's day-to-day operations, including the procurement of goods and services, on normal commercial terms in compliance with the Nigerian Stock Exchange Rules Governing Transactions with Related Parties or Interested Persons.”

PROXY A member entitled to attend and vote at the Annual General Meeting may appoint a proxy to attend and vote in his/her stead. A proxy need not be a member of the Company. A form of proxy is attached to the Annual Report and if intended to be used, it must be executed and returned to the office of the Registrars, Lighthouse Registrars Limited, Kingsway Building (3rd Floor) 2/4, Davis Street, Lagos or the office of the Company Secretary, PAC Solicitors, 16, Kofo Abayomi Street, Victoria Island, Lagos, not later than 48 hours before the time fixed for the meeting.

NOTES

1. CLOSURE OF REGISTER OF MEMBERS AND TRANSFER BOOKS

The Register of Members and Transfer Books of the Company will be closed from June 5 to June 9, 2017 (both days inclusive) to enable the Registrar update the Register of members.

2. AUDIT COMMITTEE• Pursuant to Section 359(5) of the Companies and

Allied Matters Act 2004, any Shareholder may nominate another shareholder for appointment to the Audit Committee by giving notice in writing of such nomination to the Company Secretary at least Twenty One (21) days before the Annual General Meeting.

• Please note that The Code of Corporate Governance for Public Companies issued by the Securities and Exchange Commission provides that members of the Audit Committee should be financially literate and able to read financial statements. We therefore request that all nominations to the Audit Committee should be accompanied with the Curriculum Vitae of the Nominees.

3. ELECTION/RE-ELECTION OF DIRECTORS

3.1. Election of Directorsi. To elect Mr. Ekwunife Okoli as a non-executive

independent Director with effect from 22 July, nd

2016;ii. To elect Ms. Elizabeth Amadiume as a non-

executive independent Director with effect from 21 October, 2016;st

iii. To elect Mr. Anthony Egbuna as a non-executive Director with effect from 21 October, 2016;st

iv. To elect Mr. Segun Adebanji as a non-executive Director with effect from 28 April, 2017th

The profiles of the Directors are contained in the Annual Report and Accounts.

3.2. Re-election of Directors Pursuant to Section 259 (1) of the Companies and

Allied Matters Act, CAP C20, LFN, 2004, the Directors to retire by rotation are Mr. Ayo Osunbunmi, Mr. Dominic Ichaba and Mr. Steve Iwenjora.

Their profiles are contained in the Annual Reports and Accounts and are also available for viewing on www.cornerstone.com.ng

NOTICE IS HEREBY GIVEN that the Twenty Fifth Annual General Meeting of Cornerstone Insurance PLC will hold at ththe Agip Recital Hall, MUSON Centre, Onikan, Lagos on Thursday, June 15 , 2017 at 11.00am to transact the following

businesses:

3

TABLE OF CONTENT2016 Annual Report & AccountsNOTICE OF ANNUAL GENERAL MEETING CONTD.

4. RIGHTS OF SECURITIES’ HOLDERS TO ASK QUESTIONS

Any member attending the meeting has the right to ask questions at the meeting and in writing prior to the meeting. Any questions to be asked prior to the meeting must reach the Company not later than 48 hours before the time fixed for the meeting.

5. WEBSITE A copy of this Notice and other information relating to the

meeting can be accessed via the Company's website at www.cornerstone.com.ng

thDated this 8 day of May, 2017By Order Of the Board

Elizabeth I. Uba-Onubogu PAC Solicitors (Company Secretary) FRC/2015/NBA/0000000/6266

16, Kofo Abayomi Street Victoria Island, Lagos Tel: 0909 929 8887, 0806 348 0070Website: www.cornerstone.com.ng

2016 Annual Report & Accounts

TABLE OF CONTENTCORPORATE INFORMATION

BOARD OF DIRECTORS Mr. Segun AdebanjiMr. Paul KokorichaMr. Adedotun Sulaiman (MFR) Mr. Richard IkiebeMr. Ganiyu Musa Mr. Oladapo EgbeyemiAlhaji Hussaini AbdulrahmanMr. Peter Ameadaji (Alternate)Mr. Dominic IchabaMr Steve IwenjoraMrs. Ndidi Okonkwo Nwuneli (MFR) Mr. Ekwunife OkoliMs. Elizabeth AmadiumeMr. Anthony EgbunaMr. Tokunbo BelloMr. Ayo Osunbunmi

Group Chairman( From April 28, 2017)Group Chairman( From October, 2016 to April 2017)Group Chairman( Retired September, 2016)Vice Chairman( Retired March 2016)Group Managing Director/CEONon-executive Director( Retired March, 2016)Non-executive Director( Retired March, 2016)Non-executive Director( Retired March, 2016)Non-Executive DirectorNon-Executive DirectorIndependent Director(Resigned December 2016)Independent Director( Appointed July 22, 2016)Independent Director( Appointed October 21, 2016)Non-Executive Director(appointed October 21, 2016)Executive DirectorExecutive Director

LEGAL ADVISER Ifeoma Utah21, Water Corporation Drive, Off Ligali Ayorinde Street, Victoria Island, Lagos

COMPANY SECRETARY PAC Solicitors16 Kofo Abayomi Street, Victoria Island, Lagos.Tel: +234-805-056-9557, +234(01)7611191, +234(01) 2701121,+234(01)8980746

REGISTERED OFFICE: 136, Lewis Street, Lagos. Tel:01-0126332863, 2630722,2631832 (Lagos Island Office)Website: www.cornerstone.com.ng

CORPORATE HEAD OFFICE: 21, Water Corporation Drive, Off Ligali Ayorinde Street, Victoria Island, LagosTel: 01-2806500 Website: www.cornerstone.com.ngEmail: [email protected]

1) 136, Lewis Street, Lagos. Tel:01-2632863,2630722,2631832(Lagos Island Office)2) 79, Allen Avenue(Samsung House) Ikeja, Lagos. Tel: 0802306981,01-81829843) Polysonic Mall(2nd Floor)42/44, Warehouse Road, Apapa, Lagos. Tel: 08033911435,070288565894) 191, Herbert Macaulay Street, Yaba.5) Idowu Tailor, Victoria Island Lagos

LAGOS BRANCHES:

OTHER BRANCHES 1) KM 20, Constitution Road, Kaduna Tel:070292341552) 67, Aboderin Layout, Oni& Sons Area, Ring Road, Ibadan Tel:02-87356493) 180, Aba Express Road, Port Harcourt Tel: 07029325494, 080569384544) Plot 487, Adetokunbo Ademola Str., Wuse II, Abuja Tel: 09-87766611,070284155415) Suite 7, No.5, Bank Road, Kano Tel:064-913241,064-9255786) 57, Effurun / Sapele Road, Effurun-Warri, Delta State Tel:070290663137) 110, Muritala Muhammed Highway, Calabar Municipality, Calabar, Cross Rivers State. Tel: 087-845147,080569384548) Agbeloba Buildin. 56, Quarry Road, Abeokuta, Ogun State. Tel:01-73630429) 3, Sokoto Road, Sabo Oke, Ilorin, Kwara State. Tel: 080595581032

4

2016 Annual Report & Accounts

5

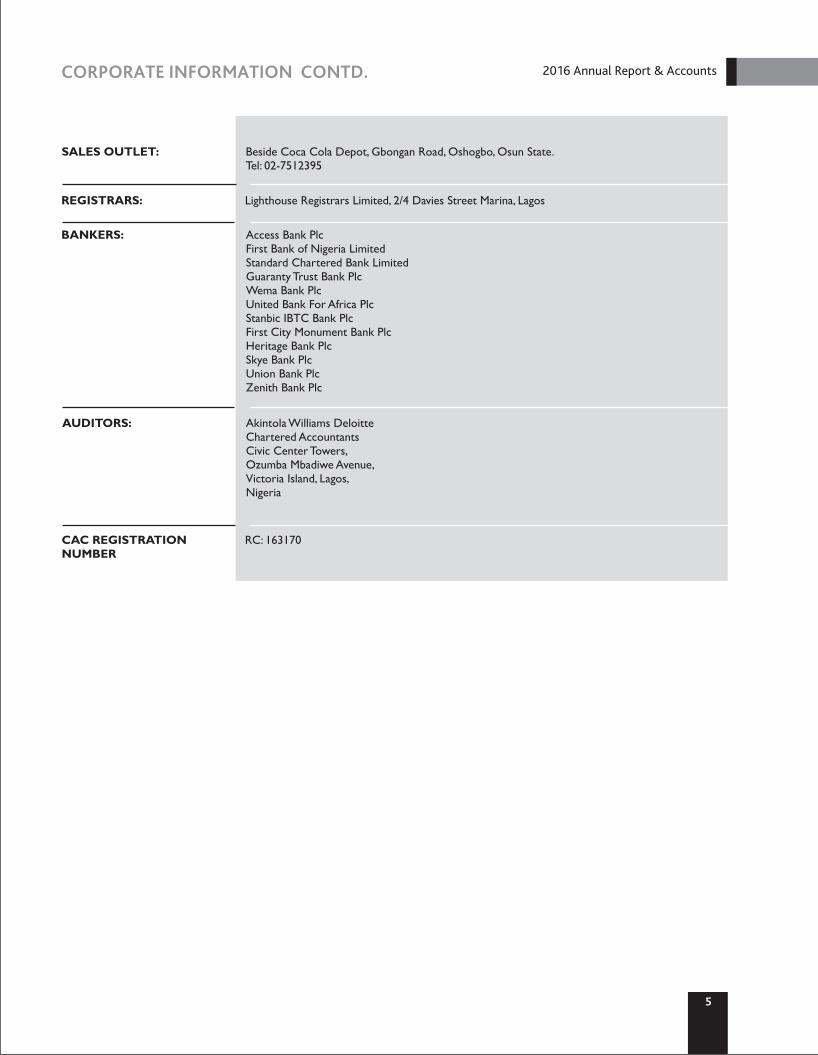

CORPORATE INFORMATION CONTD. 2016 Annual Report & Accounts

SALES OUTLET: Beside Coca Cola Depot, Gbongan Road, Oshogbo, Osun State. Tel: 02-7512395

REGISTRARS: Lighthouse Registrars Limited, 2/4 Davies Street Marina, Lagos

BANKERS: Access Bank PlcFirst Bank of Nigeria LimitedStandard Chartered Bank LimitedGuaranty Trust Bank PlcWema Bank PlcUnited Bank For Africa PlcStanbic IBTC Bank PlcFirst City Monument Bank PlcHeritage Bank PlcSkye Bank PlcUnion Bank PlcZenith Bank Plc

AUDITORS: Akintola Williams DeloitteChartered AccountantsCivic Center Towers,Ozumba Mbadiwe Avenue, Victoria Island, Lagos,Nigeria

CAC REGISTRATION NUMBER

RC: 163170

TABLE OF CONTENT

6

RESULTS AT A GLANCE 2016 Annual Report & Accounts

Group

2016

N'000

9,190,634

8,456,458

(1,264,660)

(470,563)

(1,735,223)

Group

2015

N'000

7,331,633

7,119,632

1,843,054

(212,300)

1,630,754

Company

2016

N'000

8,389,950

7,768,850

(1,516,213)

(373,574)

(1,889,787)

Company

2015

N'000

7,331,633

7,119,632

(332,139)

(203,374)

(535,513)

Gross Premium Written

Gross Premium Income

(Loss)/Profit Before Taxation

Taxation

(Loss)/Profit After Taxation

CHAIRMAN’SSTATEMENT

CHAIRMAN’S STATEMENT 2016 Annual Report & Accounts

28

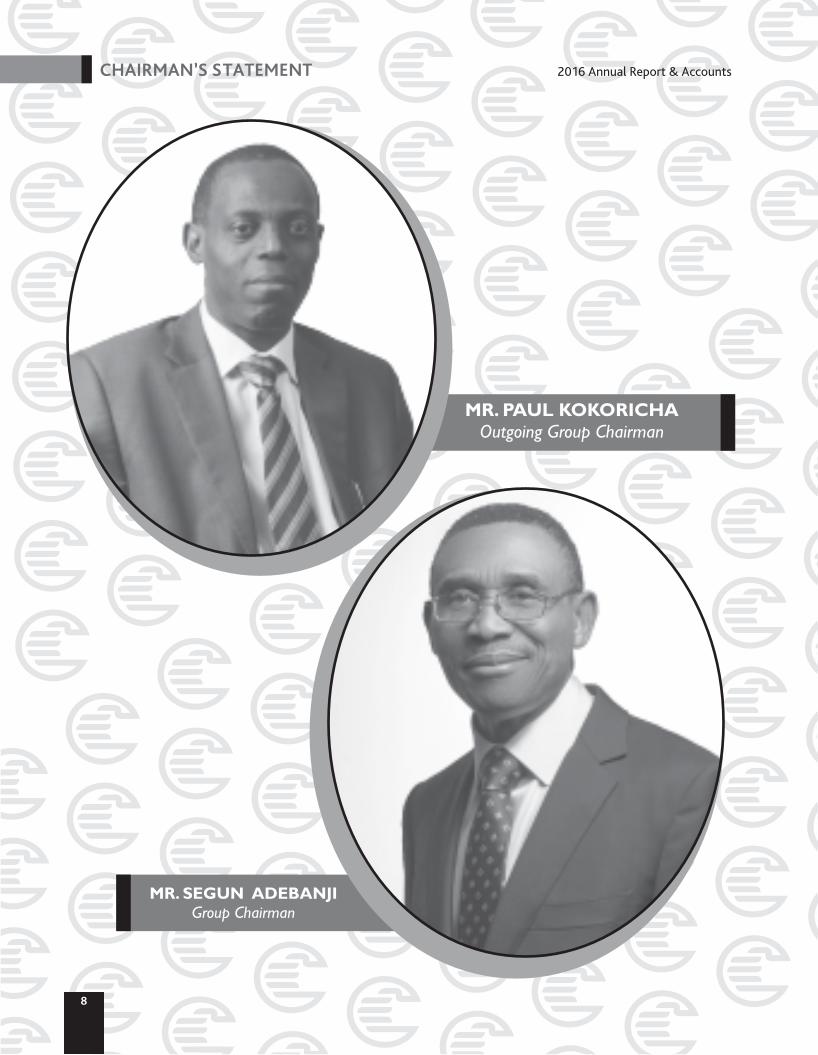

MR. PAUL KOKORICHA Outgoing Group Chairman

MR. SEGUN ADEBANJIGroup Chairman

TABLE OF CONTENT

9

CHAIRMAN’S STATEMENT CONTD. 2016 Annual Report & Accounts

Distinguished shareholders, members of the Board of Directors, thinvited guests, ladies and gentlemen. I welcome you all to the 25

Annual General Meeting of our Company, Cornerstone Insurance PLC (“the Company”). I hereby present to you the Annual Report and accounts for the financial year ended 31 December, 2016 as well as an overview of the major developments that shaped our financial results.

The Global EconomyPerhaps two of the most significant socio-political events of the year occurred in the United Kingdom (UK) and the United States (US). A referendum on European Union (EU) membership resulted in a 52% vote in favour of the UK leaving the EU while Donald Trump emerged winner of the US Presidential election.

The “Brexit” vote created immediate economic shocks that reverberated globally, as the UK currency experienced an initial 11% drop in value; the largest in the era of free-floating currencies and over USD$2 trillion in value was lost in stocks globally. Later in the year, President Trump's nationalist posture signified possible changes to the Trans-Pacific Partnership Agreement (TPPA) which would have accounted for a third of global trade. This development altered the dynamics of the economic and political landscape in Asia. The eventual withdrawal of the US from the TPPA is expected to provide China a great opportunity to consolidate its influence in the region and bolster its economic recovery.

A number of African countries saw their currencies weaken as the US Federal Reserve raised interest rates by 0.25% to 1% late in the year. With significant dollar-denominated bonds and high debt to GDP ratios, countries like Ghana, South Africa, Kenya and Tunisia face tough economic challenges.

Despite the volatility however, the world economy still grew by an estimated 3.1%, a slight reduction from the 3.2% achieved in 2015 due mainly to weaker-than-expected growth in the United States and uncertainties regarding the institutional and trade arrangements between the European Union and post-Brexit United Kingdom. Growth in emerging markets and developing economies remained subdued as commodity exporters struggled. Whilst emerging Asia continued to register strong growth and slight improvements recorded in recession-hit Brazil and Russia, activity weakened in sub-Saharan Africa as South Africa continued to grapple with severe unemployment while resource-rich Nigeria faced severe economic and security challenges.

Macroeconomic ReviewBefore the start of the year, analysts and macroeconomic commentators alike were largely unanimous in projecting a negative outlook for the Nigerian economy in 2016. Indeed, the first quarter of the year ended with a GDP contraction of -0.36%. This was off the back of lower economic activity and depressed foreign exchange (forex) earnings caused in part by a 22% drop in the average price of Bonny Light compared to the previous quarter (US$34.39 per barrel from US$44.08 per barrel).

Moreover, renewed militancy in large parts of some oil producing states, characterized by the destruction of pipelines and other related infrastructures, further lowered the country's output and earning capacity. Crude oil production dropped by 3.7% in Q1 2016 from 1.89 million barrels per day in the previous quarter to

1.82 million barrels per day. By the end of the second quarter, Nigeria had recorded two consecutive quarters of contraction (-2.06% in Q2) and for the first time in 29 years, the economy was officially in a recession.

Among other factors, the sharp drop in forex income, in an import dependent economy, played a major role in the decline of the value of the Naira. With increasing pressure on forex reserves, the Central Bank of Nigeria (CBN) resorted to controlling demand for forex through multiple exchange rates and a series of circulars to market operators while also attempting to checkmate nefarious activities in the forex markets.

With the gap between the official and parallel exchange rates widening to as much as N50 in Q2, a devaluation of the currency was inevitable and in June 2016, the CBN announced a new forex policy which was effectively a devaluation. The start of the managed float regime saw the official rate of the Naira plummet by 29% from the peg of N197/US$1 to N254/US$1 within 24 hours. By the end of the second half of the year and after periodic interventions, the official exchange rate stood at N304/US$1 while the parallel market rate continued to rise and closed the year at N490/US$1, creating a gap of N186 or 61%. Higher rates of forex and higher costs of importation dovetailed into rising prices. The Consumer Price Index (CPI), which started the year in single digits, at 9.62%, inched upwards month on month and ended the year at 18.55%, an 11-year high. The key drivers of the almost 100% rise in the inflation rate (Year on Year) were electricity, fuel prices and road transportation.

Amidst the harsh economic climate, the President presented an expansionary 2016 budget of N6.07 trillion with a 30% allocation towards capital expenditure and N200 billion allocated to special intervention programmes at the grass root level.

In summary, the macroeconomic environment was characterised by thinner margins for most corporations in the manufacturing and FMCG industries. It was a year characterised more by incremental growth and cost control measures than by capacity expansion projects. For the average Nigerian, the year was one of shrinking disposable incomes caused by sharp price increases of imported and locally produced household items. Asset acquisition gave way to asset consolidation and reduced discretionary expenses.

The magnitude of the economic downturn had a significant adverse impact on insurance. The rapid rise in prices of goods and services was particularly detrimental to the insurance industry. Not only did this affect the ability of customers to pay premiums, the claims ratios increased astronomically as replacement costs for items lost or damaged were disproportionate to the premiums collected for contracts written in the prior 12 months.

The Insurance IndustryNotwithstanding the overall macroeconomic outlook, there was justifiable reason for cautious optimism for the insurance industry at the beginning of the year. An expansionary budget focused on infrastructure spending could open additional insurance opportunities whilst a business friendly regulatory and consultative regulatory framework would create an enabling environment for innovation and growth.

10

CHAIRMAN’S STATEMENT CONTD. 2016 Annual Report & Accounts

During the year, the Insurance regulator, the National Insurance Commission (NAICOM) announced that guidelines were being drafted for new alternative distribution channels. NAICOM, through the Nigerian Bar Association and members of the Nigerian Stock Exchange commenced discussions with stakeholders to design structures for the distribution of Insurance products. It is expected that the new channels will act as referral channels only and will not be involved in the actual sale of insurance products. Nonetheless, when launched, the new channels are expected to have a significant impact by increasing insurance penetration in the country. A l so i n t h e distribution space, there were a number of regulatory interventions that addressed breaches in commission payments to unlicensed intermediaries. The Commission suspended all distribution partnerships with banks, telco's, airlines and web-based aggregators that were in violation of Section 34 of the Insurance Act 2003.

Company Financial PerformanceThe harsh economic climate notwithstanding, your Company has sustained its growth trajectory by growing Gross Premium Written by 25% to N9.1 billion from N7.3 billion in 2015. Sales to retail customers accounted for 25% of premiums while Special Risks products to the Oil & Gas and Engineering sectors contributed the second highest proportion at 23%. The increased financial strength from the conclusion of the acquisition of Fin Insurance and their growing reputation as a credible partner is now opening the opportunity for leadership position on major transactions as well as provide support for our retail expansion.

However, high claims inflation and the security challenges in the North East and South-South zones of the country led to a significant deterioration in the claims experience during the year under review. Gross claims for the year totalled N4.5 billion representing an increase of 61% from the previous year of N2.8 billion, driven largely by death claims from the group life, credit life and third party motor classes of insurance. The company has since carried out a comprehensive portfolio review and corrective actions have been taken to improve terms and conditions, reduce participation or exit the business as appropriate.

Net investment income increased by 98%, from N.74 billion to N1.47 billion, mainly due to the consolidation of the investment income of the subsidiary. The unlisted equities portfolio suffered significant impairment while the financial commitment on our new head office building constrained the liquidity that would have benefited from attractive yields on short term instruments. Similarly, the rising cost of goods and services, coupled with the first-time consolidation of the operations of the subsidiary led to a 45% increase in management expenses. Significant investments are being made in improving the technology and distribution infrastructure to support the company's retail strategy. Indeed, the agency network almost doubled from 832 to 1,600 agents while a robust platform has been built for the rollout of the bancassurance channel. While these costs are being accounted for in the current financial statements, we expect the benefits to accrue over several accounting periods.

As a result, despite the modest growth in revenue, the combined effects of the harsh macroeconomic environment, high claims cost, rising inflation and benign investment income have led to a

reported Loss before Tax of N1.26 billion (2015: N1.52billion). Understandably, this is a matter of much disappointment for all our shareholders, the Board and management.

Board of DirectorsOn the 2 of April, 2017, I assumed the role of Chairman of the th8Board of Directors. This follows the retirement of the erstwhile Chairman, Mr. Paul Kokoricha who took over as Chairman from Mr. Adedotun Sulaiman. Mr. Adedotun Sula iman and Mr. Paul Kokoricha retired in line with the Code of Corporate Governance issued by NAICOM. As Mr. Sulaiman informed you at the last Annual General Meeting, four other members of the Board of Directors (Mr. Richard Ikiebe who served as Vice Chairman, Mr. Peter Ameadaji, Alhaji Hussaini Abdulrahman and Mr. Oladapo Egbeyemi) had also retired in line with the NAICOM Code of Corporate Governance.

In December 2016, Mrs. Ndidi Okonkwo Nwuneli resigned as an Independent Non-Executive Director to pursue other interests and attend to other commitments.

I would like to express my thanks to each of them for the professionalism and dedication they have demonstrated throughout the time they served on the Board and the contribution that they have made to the Company. I wish them the best in their future endeavours.

On July 22 2016, Mr. Ekwunife Okoli was appointed as an nd

Independent Non-Executive Director. He has proved a strong and positive fit to the Board, bringing new perspective to Board deliberations.

On October 2 2016, Ms. Elizabeth Amadiume and Mr. Anthony st1Egbuna joined the Board as Independent Non-Executive Director and Non-Executive Director respectively. They are all highly qualified and seasoned professionals and their appointments will bring a renewed dynamism to the Board. They will be presented to you for election at this Annual General Meeting.

OutlookEven though the country is not out of recession yet, the early signs give cause for cautious optimism that the worst may be over and economic activity may begin to improve. The rise in international crude oil prices above the US$50 per barrel mark bolstered foreign exchange reserves more than US$30 billion towards the tail end of Q1 2017. The CBN has directed an ample proportion of the reserves towards defending the Naira.

The proposed 2017 Federal budget of N7.29 trillion is a strong indication that President Buhari is committed to turning the economy around during the year. As in 2016, 30% (N2.24 trillion) of the expenditure will go towards capital projects of which N791 billion will be allocated to infrastructure projects in the Power, Works Housing and Transport sectors.

In a bid to address the root causes of the economic downturn, the Federal Government also unveiled a 4-year Economic Recovery and Growth Plan with one of its objectives being to achieve macroeconomic stability and economic diversification. The plan projects a 2.19% growth in GDP in 2017, reaching 7% by 2020. The full effects of the government's plans would have trickled down by

the second half of the year and economic activity is expected to pick up by then.

We have also seen early signs of greater collaboration amongst the financial services regulators which should lead to the satisfactory resolution of impediments in the areas of new products and distribution channels, especially bancassurance and annuity. Overall, I would say that the prospects for the Insurance industry are slightly positive with potential for moderate growth.

The Board of Directors and the management of your Company have also put in place additional cost management and revenue enhancement measures to ensure a quick return to profitability. Strict cost control measures on management expenses have been put in place and will be closely monitored as the year progresses.

There are also ongoing efforts to diversify sources of revenue into allied industries with higher profit margins. The Company made significant progress on our new Head Office under construction. When completed, we will operate from a complex befitting our status as a leading insurance player as well as obtain investment income from lettable floors.

I would like to conclude by appreciating our valued customers and their intermediaries for their continued patronage, as we hope to continue to provide effective solutions to your financial needs.

May God bless Cornerstone Insurance plc.

MR. SEGUN ADEBANJIGroup Chairman

CHAIRMAN’S STATEMENT CONTD. 2016 Annual Report & Accounts

11

REPORT

CORPORATE GOVERNANCEAs at 31st December, 2016

14

BOARD OF DIRECTORS 2016 Annual Report & Accounts

SEGUN ADEBANJIGROUP CHAIRMAN

Mr. Segun Adebanji, has had over 35 years working experience in blue chip companies. Prior to joining Africa Capital Alliance in January 2011, Mr. Segun Adebanji was the Executive Vice Chairman of Alvac Company Limited. Mr. Segun Adebanji's working experience includes UAC and Unilever PLC London and South Africa. He has served as Financial Director of Nigerian Breweries PLC and later Managing Director, Heineken Ghana Breweries and Namibia Breweries. Mr. Adebanji is a non-Executive Director of Nigerian Breweries Plc and Chairman, Bevpak Nigeria Limited. He is a Fellow of both the Chartered Association of Certified Accountants and the Institute of Chartered Accountants of Nigeria.

* thMr. Segun Adebanji was appointed as Chairman of the Board effective 28 April, 2017.

PAUL KOKORICHANON-EXECUTIVE DIRECTOR

Mr. Paul Kokoricha is an Executive Partner at African Capital Alliance and has over Thirty Years' experience in the financial services industry.

Mr. Paul Kokoricha holds a Bachelor of Science Degree, Second Class Upper Division in Economics and won the Departmental Prize for the Best Graduating Student in Economics in 1982 from the University of Nigeria, Nsukka. He is a Fellow of the Institute of Chartered Accountants of Nigeria.

* rdMr. Paul Kokoricha resigned from the Board as Chairman effective 23 April, 2017.

GANIYU MUSAMANAGING DIRECTOR

Mr. Ganiyu Musa worked at African Reinsurance Corporation for 19 years in various capacities including Director of Finance & Accounts/Chief Financial Officer for 10 years and Deputy Managing Director, Services for 5 years.

Mr. Ganiyu Musa is a highly experienced management professional with diversified experience in insurance, reinsurance, audit, consulting and financial management. He has over 27 years working experience and has served in different capacities at Pannell Kerr Forster, a firm of Chartered Accountants, Arthur Andersen and African Reinsurance Corporation.

He holds a Bachelor of Science degree in Business Administration and a Masters in Banking and Finance degree, both from the University of Lagos. He is a Fellow of the Institute of Chartered Accountants of Nigeria. He is also a Member of the Chartered Insurance Institute of London and a Senior Member of the Chartered Insurance Institute of Nigeria.

DOMINIC ICHABANON – EXECUTIVE DIRECTOR

Mr. Dominic Ichaba a former Managing Director of Cornerstone Insurance PLC, is a Legal Practitioner and a Chartered Stockbroker. He has experience in Banking, Insurance, Strategy development and Human Resources Management.

He is a graduate of the Ahmadu Bello University, Zaria and the Nigerian Law School and holds a Masters Degree in Business Administration. He is also an alumnus of the London Business School, the I.E.S.E Business School, Barcelona and the Wharton School, USA.

15

BOARD OF DIRECTORS’ PROFILE 2016 Annual Report & Accounts

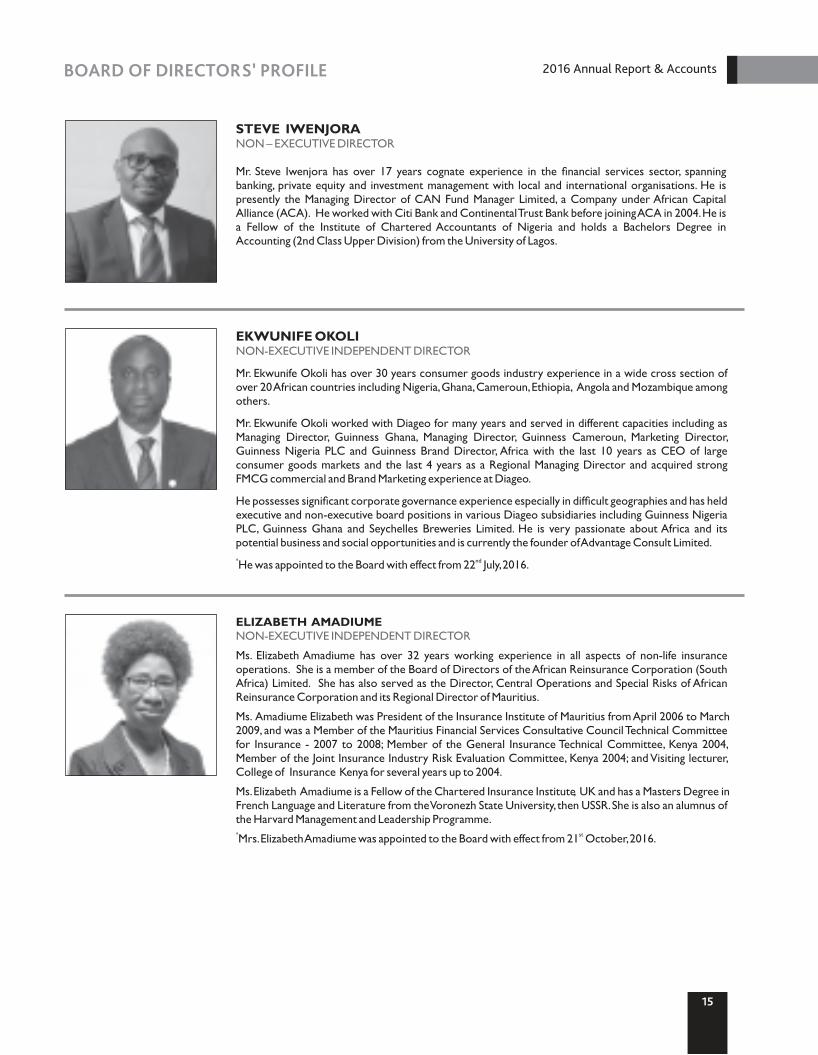

STEVE IWENJORANON – EXECUTIVE DIRECTOR

Mr. Steve Iwenjora has over 17 years cognate experience in the financial services sector, spanning banking, private equity and investment management with local and international organisations. He is presently the Managing Director of CAN Fund Manager Limited, a Company under African Capital Alliance (ACA). He worked with Citi Bank and Continental Trust Bank before joining ACA in 2004. He is a Fellow of the Institute of Chartered Accountants of Nigeria and holds a Bachelors Degree in Accounting (2nd Class Upper Division) from the University of Lagos.

EKWUNIFE OKOLINON-EXECUTIVE INDEPENDENT DIRECTOR

Mr. Ekwunife Okoli has over 30 years consumer goods industry experience in a wide cross section of over 20 African countries including Nigeria, Ghana, Cameroun, Ethiopia, Angola and Mozambique among others.

Mr. Ekwunife Okoli worked with Diageo for many years and served in different capacities including as Managing Director, Guinness Ghana, Managing Director, Guinness Cameroun, Marketing Director, Guinness Nigeria PLC and Guinness Brand Director, Africa with the last 10 years as CEO of large consumer goods markets and the last 4 years as a Regional Managing Director and acquired strong FMCG commercial and Brand Marketing experience at Diageo.

He possesses significant corporate governance experience especially in difficult geographies and has held executive and non-executive board positions in various Diageo subsidiaries including Guinness Nigeria PLC, Guinness Ghana and Seychelles Breweries Limited. He is very passionate about Africa and its potential business and social opportunities and is currently the founder of Advantage Consult Limited. * ndHe was appointed to the Board with effect from 22 July, 2016.

ELIZABETH AMADIUMENON-EXECUTIVE INDEPENDENT DIRECTOR

Ms. Elizabeth Amadiume has over 32 years working experience in all aspects of non-life insurance operations. She is a member of the Board of Directors of the African Reinsurance Corporation (South Africa) Limited. She has also served as the Director, Central Operations and Special Risks of African Reinsurance Corporation and its Regional Director of Mauritius.

Ms. Amadiume Elizabeth was President of the Insurance Institute of Mauritius from April 2006 to March 2009, and was a Member of the Mauritius Financial Services Consultative Council Technical Committee for Insurance - 2007 to 2008; Member of the General Insurance Technical Committee, Kenya 2004, Member of the Joint Insurance Industry Risk Evaluation Committee, Kenya 2004; and Visiting lecturer, College of Insurance Kenya for several years up to 2004.

Ms. Elizabeth Amadiume is a Fellow of the Chartered Insurance Institute, UK and has a Masters Degree in French Language and Literature from the Voronezh State University, then USSR. She is also an alumnus of the Harvard Management and Leadership Programme. * stMrs. Elizabeth Amadiume was appointed to the Board with effect from 21 October, 2016.

16

BOARD OF DIRECTORS 2016 Annual Report & Accounts

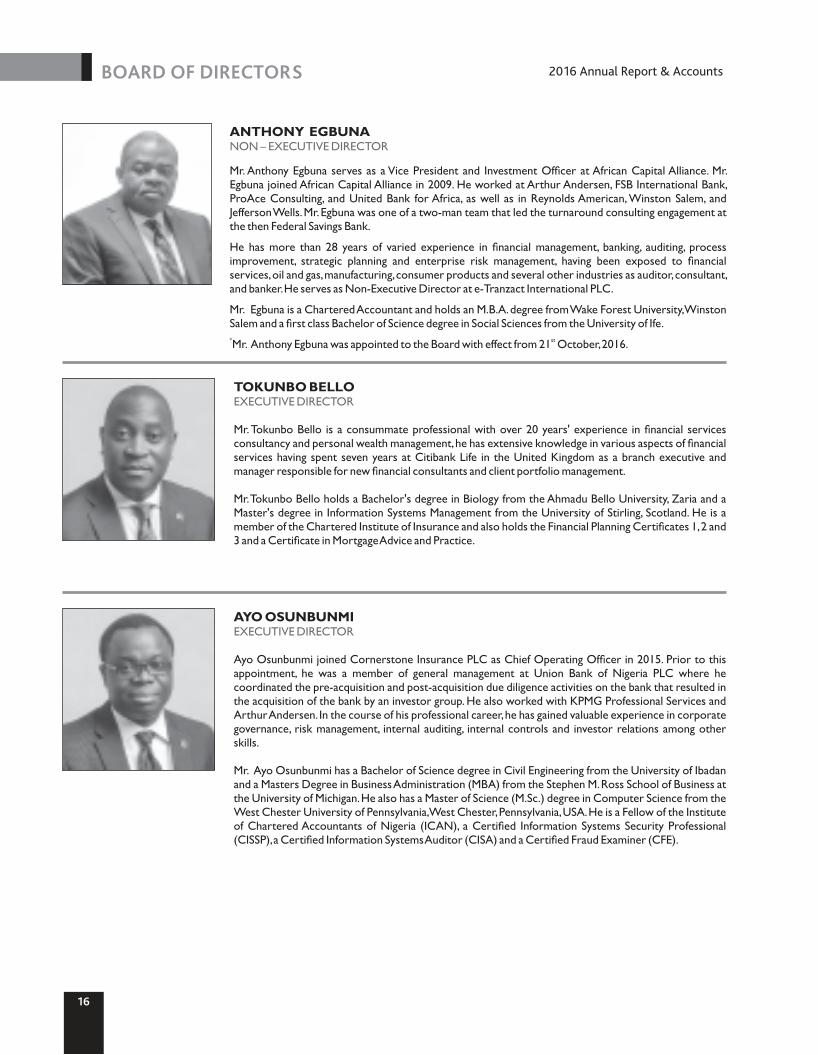

TOKUNBO BELLOEXECUTIVE DIRECTOR

Mr. Tokunbo Bello is a consummate professional with over 20 years' experience in financial services consultancy and personal wealth management, he has extensive knowledge in various aspects of financial services having spent seven years at Citibank Life in the United Kingdom as a branch executive and manager responsible for new financial consultants and client portfolio management.

Mr. Tokunbo Bello holds a Bachelor's degree in Biology from the Ahmadu Bello University, Zaria and a Master's degree in Information Systems Management from the University of Stirling, Scotland. He is a member of the Chartered Institute of Insurance and also holds the Financial Planning Certificates 1, 2 and 3 and a Certificate in Mortgage Advice and Practice.

AYO OSUNBUNMIEXECUTIVE DIRECTOR

Ayo Osunbunmi joined Cornerstone Insurance PLC as Chief Operating Officer in 2015. Prior to this appointment, he was a member of general management at Union Bank of Nigeria PLC where he coordinated the pre-acquisition and post-acquisition due diligence activities on the bank that resulted in the acquisition of the bank by an investor group. He also worked with KPMG Professional Services and Arthur Andersen. In the course of his professional career, he has gained valuable experience in corporate governance, risk management, internal auditing, internal controls and investor relations among other skills.

Mr. Ayo Osunbunmi has a Bachelor of Science degree in Civil Engineering from the University of Ibadan and a Masters Degree in Business Administration (MBA) from the Stephen M. Ross School of Business at the University of Michigan. He also has a Master of Science (M.Sc.) degree in Computer Science from the West Chester University of Pennsylvania, West Chester, Pennsylvania, USA. He is a Fellow of the Institute of Chartered Accountants of Nigeria (ICAN), a Certified Information Systems Security Professional (CISSP), a Certified Information Systems Auditor (CISA) and a Certified Fraud Examiner (CFE).

ANTHONY EGBUNANON – EXECUTIVE DIRECTOR

Mr. Anthony Egbuna serves as a Vice President and Investment Officer at African Capital Alliance. Mr. Egbuna joined African Capital Alliance in 2009. He worked at Arthur Andersen, FSB International Bank, ProAce Consulting, and United Bank for Africa, as well as in Reynolds American, Winston Salem, and Jefferson Wells. Mr. Egbuna was one of a two-man team that led the turnaround consulting engagement at the then Federal Savings Bank.

He has more than 28 years of varied experience in financial management, banking, auditing, process improvement, strategic planning and enterprise risk management, having been exposed to financial services, oil and gas, manufacturing, consumer products and several other industries as auditor, consultant, and banker. He serves as Non-Executive Director at e-Tranzact International PLC.

Mr. Egbuna is a Chartered Accountant and holds an M.B.A. degree from Wake Forest University, Winston Salem and a first class Bachelor of Science degree in Social Sciences from the University of Ife. * stMr. Anthony Egbuna was appointed to the Board with effect from 21 October, 2016.

217

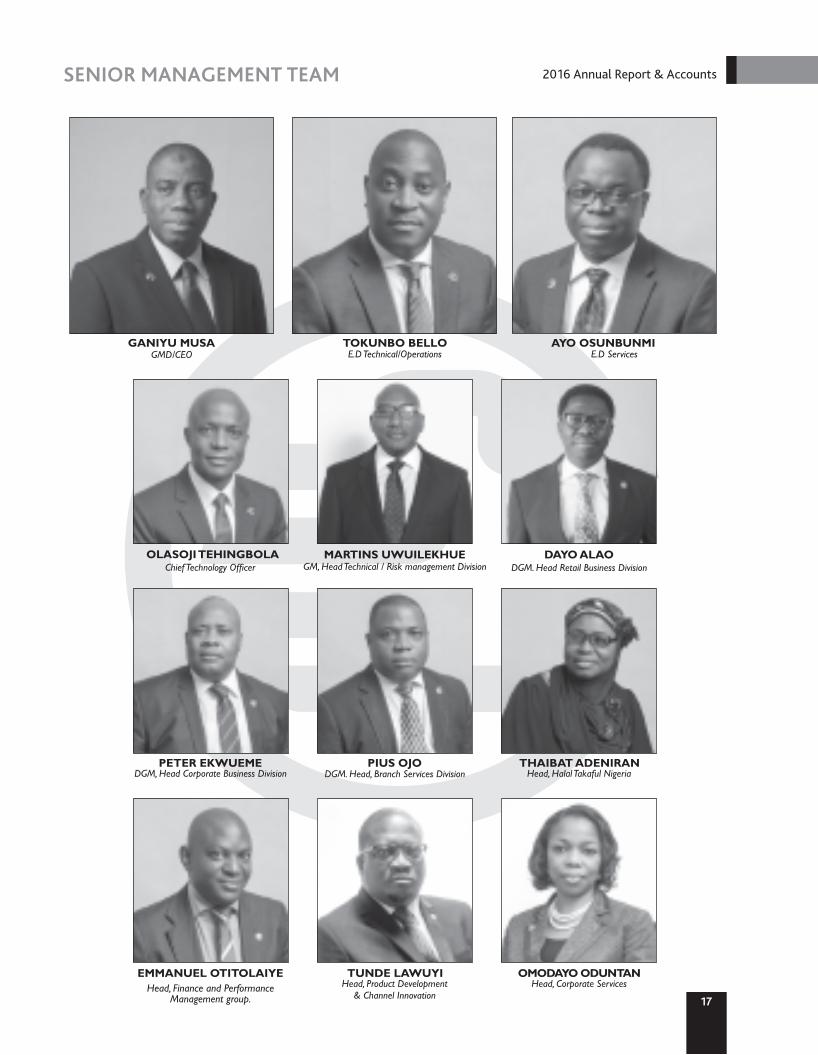

SENIOR MANAGEMENT TEAM 2016 Annual Report & Accounts

Head, Finance and Performance Management group.

GANIYU MUSA GMD/CEO

TOKUNBO BELLO E.D Technical/Operations

AYO OSUNBUNMI E.D Services

OLASOJI TEHINGBOLA Chief Technology Officer

MARTINS UWUILEKHUE GM, Head Technical / Risk management Division

DAYO ALAO DGM. Head Retail Business Division

PETER EKWUEME DGM, Head Corporate Business Division

PIUS OJO DGM. Head, Branch Services Division

THAIBAT ADENIRAN Head, Halal Takaful Nigeria

EMMANUEL OTITOLAIYE TUNDE LAWUYI Head, Product Development

& Channel Innovation

OMODAYO ODUNTAN Head, Corporate Services

18

CORPORATE GOVERNANCE REPORT 2016 Annual Report & Accounts

CORPORATE GOVERNANCE COMPLIANCE STATEMENTGovernance is central to the operations and structure of Cornerstone Insurance PLC and good corporate governance is an essential part of the spirit of the Board. Our Company's governance structures and practices align with applicable local legislation and international best practices including compliance with the Code of Corporate Governance issued by the National Insurance Commission (NAICOM) for the Insurance Industry in Nigeria and the Code of Corporate Governance for Public Companies issued by the Securities and Exchange Commission. Further, we ensure continuous review of our governance approach and practices to promote accountability and transparency.

The Board also ensures that its governance approach is reflected throughout the organisation and has developed a culture where managers at every level are accountable and stakeholder views are taken seriously. The Board determines the governance culture of the organisation and ensures that it leads by example by exhibiting responsible behaviour which is expected from every stakeholder in the organisation.

At the beginning of 2017, NAICOM issued a statement to the industry highlighting its regulatory priorities for the year 2017 part of which was monitoring the behavioural aspects of corporate governance. In furtherance of this objective, NAICOM subsequently issued a circular dated 25 August, 2016 clarifying th

some provisions of its Code of Corporate Governance. The circular, among other things, compressed the existing committees of insurance companies to three namely:

a. Finance, Investment and General Purposesb. Audit and Compliancec. Enterprise Risk Management and Governance

In compliance with this circular, the Board reviewed its committee structure and approved changes to the committees' Terms of Reference.

Some of the key initiatives which the Board embarked on in 2016 to strengthen its corporate governance processes include but are not limited to the following:

1. Appointment of the firm of J.K Randle as external consultants to conduct the annual Board evaluation of the Board in line with the provisions of the NAICOM Code of Corporate Governance;

2. Extensive review of the Company's Code of Business Ethics to guide employees, Directors and other stakeholders who transact with the Company. The Code contains clear provisions and guidelines on anti-bribery, conflict of interest situations, whistle blowing and ethical conduct;

3. Codification of the Company's Anti-money Laundering (AML) and Combating the Financing of Terrorism (CFT) policies;

4. Peer Review of the Company's compensation and remuneration levels to ensure that the Company remains competitive and can attract, motivate and retain skilled and qualified persons needed to manage the business of the organisation;

5. Constant monitoring of corporate governance regulations

and best practices to ensure that the Company is compliant at all times. The Board conducted a company-wide corporate governance audit to gauge the Company's compliance with extant regulations and best practices and devised action plans to address gaps which were identified;

6. The Company improved its interaction and engagement with various regulators as well as its stakeholders and has put in place measures to continue to strengthen these relationships.

7. The Company has a policy of zero tolerance for non-compliance and has developed a robust Compliance Framework to ensure compliance at all levels.

Governance StructureThe governance of the Company resides with the Board of Directors who are accountable to shareholders for creating and delivering sustainable value through the management of the Company's business.

The Board is responsible for the efficient operation of the Company and ensures the Company fully discharges its legal, financial and regulatory responsibilities. These oversight functions of the Board of Directors are exercised through its various Committees.

The matters which are more specifically reserved for the Board to ensure that it maintains full and effective control over appropriate strategic, financial, operational and compliance issues are:

• Maintenance of clear investment objectives and risk management policies;

• Formulation and Monitoring of the Group's Strategy and Implementation of that Strategy;

• Monitoring all business activities of the Company from analysis of investment performance to review of quarterly management accounts;

• Capital raising and Budget Allocation• Accounting policies, and financial reporting • Internal Control• Approval of material acquisitions and disposal of assets• Consideration and approval of Board and Senior

Management appointments or removals• Shareholder communication• Authorisation of Directors' conflicts or possible conflicts of

interest;• Review of terms of reference and membership of Board

Committees;

The Board delegates the operational management of the Group's businesses to the Group Chief Executive who reports to the Board and who can sub-delegate any of his powers as appropriate.

Board CompositionThe Board of Directors of Cornerstone Insurance PLC is comprised of experienced people with significant achievements in their respective professions.

As at December 31, 2016, there were Nine (9) members on the Board of Directors comprising Four (4) Non-Executive Directors, one of whom is the Chairman, Two (2) Independent Directors and Three (3) Executive Directors, one of whom is the Managing Director.

19

CORPORATE GOVERNANCE REPORT CONTD. 2016 Annual Report & Accounts

Changes to the Board

Resignations• Messrs. Richard Ikiebe, Oladapo In March, 2016,

Egbeyemi, Alhaji Hussaini Abdulrahman and Peter Ameadaji (alternate) retired as Directors from the Board in line with the NAICOM Code of Corporate Governance on tenure of Directors. The Chairman made this announcement to shareholders in his statement at the 2016 AGM of the Company.

• Mr. Adedotun SulaimanIn September, 2016, retired from the Board in compliance with the provisions of the NAICOM Code of Corporate Governance on tenure of Directors. The Board subsequently appointed Mr. Paul Kokoricha to replace him as Chairman.

• Mrs. Ndidi Okonkwo NwuneliIn December, 2016, resigned from the Board as a non-executive independent Director in order to pursue other interests and commitments.

Appointments/Election of Directors• In July 2016, the Board strengthened its composition with the

appointment of as a non-executive Mr. Ekwunife Okoliindependent Director. Details of his experience can be found on page 4.

The Board hereby presents the appointment of Mr. Ekwunife Okoli as a non-executive independent Director for approval at this Annual General Meeting.

• The Board through the ERM and Governance Committee reviewed its composition and recognised the need for greater diversity on the Board. In October, 2016, the Board appointed

Ms. Elizabeth Amadiume as a non-executive Independent Director. Details of her experience can be found on Page 4.

Ms. The Board hereby presents the appointment of Elizabeth Amadiume as a non-executive independent Director for approval at this Annual General Meeting.

• Mr. Anthony In October, 2016, the Board appointed Egbuna as a non-executive Director. Details of his experience can be found on Page 4.

Mr. The Board hereby presents the appointment of Anthony Egbuna as a non-executive Director for approval at this Annual General Meeting.

Post Y ear End Events• Mr. Segun Adebanji replaced Mr. Paul Kokoricha who

rdresigned from the Board as Chairman effective from 23 April, 2017. Details of his experience can be found on Page 2.

Mr. Segun The Board hereby presents the appointment of Adebanji as a non-executive Director for approval at this Annual General Meeting.

Re-Election of DirectorsIn accordance with Section 259(1) of the Companies and Allied Matters Act, CAP C20, LFN, 2004, the following Directors retiring by rotation in accordance with Section 259 of the Companies and Allied Matters Act being eligible are presenting themselves for re-election:a. Mr. Ayo Osunbunmib. Mr. Dominic Ichabac. Mr. Steve Iwenjora

Their profiles are contained in the section for Directors' Profiles.

stThe composition of the Board as at 31 December, 2016 to date is presented as follows:

Mr. Ganiyu Musa

Mr. Ayo Osunbunmi

Mr. Tokunbo Bello

Managing Director/CEO

Executive Director

Executive Director

1Mr. Segun Adebanji2Mr. Paul Kokoricha3Mr. Adedotun Sulaiman

Mr. Dominic Ichaba

Mr. Steve Iwenjora4Ms. Elizabeth Amadiume5Mr. Anthony Egbuna6Mr. Ekwunife Okoli7Mrs. Ndidi Okonkwo Nwuneli

Chairman

Non-Executive Director

Non-Executive Director

Non-Executive Director

Non-Executive Director

Independent Director

Non-Executive Director

Independent Director

Independent Director

Non – Executive Directors

Executive Directors

1 thAppointed as Chairman of the Board effective 28 April, 2017.2 rdResigned as Chairman effective 23 April, 20173 thResigned from the Board effective 13 September, 20164 stAppointed effective from 21 October, 20165 stAppointed effective from 21 October, 20166 ndAppointed effective 22 July, 20167 thResigned effective 13 December, 2016

2

CORPORATE GOVERNANCE REPORT CONTD. 2016 Annual Report & Accounts

20

Board Appointment, Induction and TrainingThe Board through the Enterprise Risk Management (ERM) and Governance Committee is responsible for determining the required knowledge, skills and experience, required for the Board as a whole and for individual members. Members are expected to meet the standard requirements set by the Board and should also possess expertise and insights in the industry and other areas relevant to the Company.

All new non-executive Directors appointed to the Board are issued a letter of appointment which contains their fiduciary duties as Directors, their roles and responsibilities, remuneration and information on Board meetings among other things. On appointment, Directors receive information about Cornerstone Insurance including financial data and key policies supporting the Company's business practices. They also receive copies of the Terms of Reference of the Board and committees to which they have been appointed and the Company's Memorandum and Articles of Association. All new Directors are required to disclose their memberships on other Boards and any real or potential conflict of interest situations which they are aware of.

Directors are encouraged to update their skills and knowledge and the Board and individual Directors receive ongoing training as required. In 2016, Board members were trained and tested on AML and CFT regulations and processes. Directors also partook in the Fiduciary Awareness Certification Test (FACT) organised by the Nigerian Stock Exchange (NSE) in collaboration with the Centre for Business (CBI) Integrity as part of the Corporate Governance Rating System for companies listed on the Nigerian Stock Exchange.

Meetings of the BoardThe Board formally met Six (6) times in 2016. The Board meets at least once every quarter to perform its oversight function and to monitor the performance of management. Special Board meetings are scheduled whenever business exigencies arise which require the urgent attention of the Board. Between meetings, the Board maintains regular contact with Management.

Details of attendance by each of the Directors at Board meetings are shown in the table below.

stAttendance Register of the Members of the Board for the year ended 31 December, 2016

Annual Board EvaluationIn compliance with the NAICOM Code of Corporate Governance, the Company appointed the firm of J.K Randle to conduct the annual Board Evaluation exercise for the year ended 31 December, 2016. The report of the Board Evaluation is contained on page of the Annual st 24Report. At the Annual General Meeting of the Company held 21 July, 2015, the Company's shareholders approved the appointment of JK st Randle Professional Services to facilitate the evaluation of the Board. The Board is confident that JK Randle Professional Services will continue to deliver value to the Board.

During the year, the ERM and Governance Committee considered the report of the Board Evaluation carried out for the year ended 31 st

December 2015, identified areas of specific focus and developed action plans to address those areas.

1 2 3 4 5 6MEETINGS

NAMES

Mr. Adedotun Sulaiman

Mr. Paul Kokoricha

Mr. Segun Adebanji

Mr. Ganiyu Musa

Mr. Dominic Ichaba

Mr. Anthony Egbuna

Mr. Steve Iwenjora

Mr.Ekwunife Okoli

Mr. Ndidi O. Nwuneli

Ms. Elizabeth Amadiume

Mr. Tokunbo Bello

Mr. Ayo Osunbunmi

26/01/16 16/03/16 26/04/16 22/07/16 21/10/16 15/12/16Strategy Session

✓

✓

NYA

✓

✓

NYA

✓

NYA

✗

NYA

✗

✓

NLD

✓

✓

✓

✓

✓

✗

✓

✓

✓

✓

✓

Key: ✓-Present ✗-Absent NYA-Not Yet Appointed NLD- No Longer Director

✓

✓

NYA

✓

✓

NYA

✓

NYA

✓

NYA

✓

✓

✓

✓

NYA

✓

✓

NYA

û

NYA

✓

NYA

û

✓

✓

✓

NYA

✓

✓

NYA

✓

NYA

✓

NYA

✓

✓

NLD

✓

NYA

✓

✓

NYA

✓

✓

✓

NYA

✓

✓

21

CORPORATE GOVERNANCE REPORT CONTD. 2016 Annual Report & Accounts

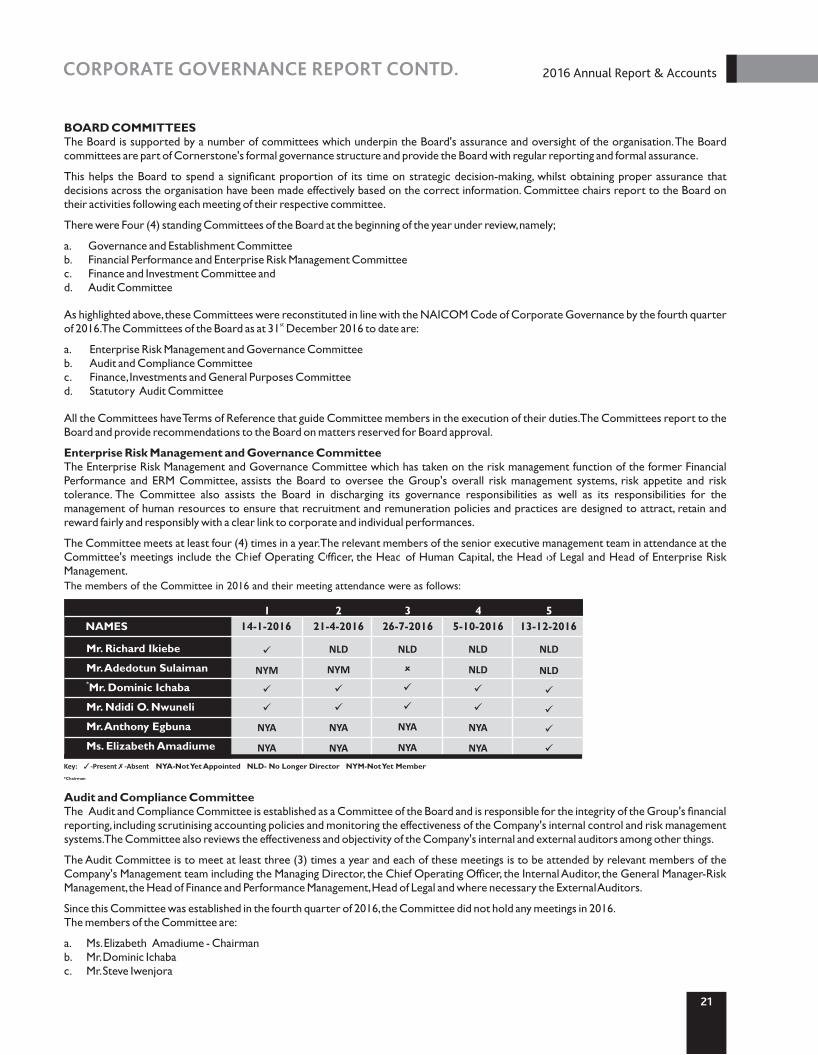

BOARD COMMITTEESThe Board is supported by a number of committees which underpin the Board's assurance and oversight of the organisation. The Board committees are part of Cornerstone's formal governance structure and provide the Board with regular reporting and formal assurance.

This helps the Board to spend a significant proportion of its time on strategic decision-making, whilst obtaining proper assurance that decisions across the organisation have been made effectively based on the correct information. Committee chairs report to the Board on their activities following each meeting of their respective committee.

There were Four (4) standing Committees of the Board at the beginning of the year under review, namely;

a. Governance and Establishment Committee b. Financial Performance and Enterprise Risk Management Committeec. Finance and Investment Committee and d. Audit Committee

As highlighted above, these Committees were reconstituted in line with the NAICOM Code of Corporate Governance by the fourth quarter of 2016. The Committees of the Board as at 31 December 2016 to date are:st

a. Enterprise Risk Management and Governance Committeeb. Audit and Compliance Committeec. Finance, Investments and General Purposes Committeed. Statutory Audit Committee

All the Committees have Terms of Reference that guide Committee members in the execution of their duties. The Committees report to the Board and provide recommendations to the Board on matters reserved for Board approval.

Enterprise Risk Management and Governance CommitteeThe Enterprise Risk Management and Governance Committee which has taken on the risk management function of the former Financial Performance and ERM Committee, assists the Board to oversee the Group's overall risk management systems, risk appetite and risk tolerance. The Committee also assists the Board in discharging its governance responsibilities as well as its responsibilities for the management of human resources to ensure that recruitment and remuneration policies and practices are designed to attract, retain and reward fairly and responsibly with a clear link to corporate and individual performances.

The Committee meets at least four (4) times in a year. The relevant members of the senior executive management team in attendance at the Committee's meetings include the Chief Operating Officer, the Head of Human Capital, the Head of Legal and Head of Enterprise Risk Management.The members of the Committee in 2016 and their meeting attendance were as follows:

Key: ✓-Present✗ -Absent NYA-Not Yet Appointed NLD- No Longer Director NYM-Not Yet Member*Chairman

1 2 3 4 5NAMES

Mr. Richard Ikiebe

Mr. Adedotun Sulaiman*Mr. Dominic Ichaba

Mr. Ndidi O. Nwuneli

Mr. Anthony Egbuna

Ms. Elizabeth Amadiume

21-4-201614-1-2016 26-7-2016 5-10-2016 13-12-2016

ü

NYM

ü

ü

NYA

NYA

NLD

NYM

ü

ü

NYA

NYA

NLD

û

ü

ü

NYA

NYA

NLD

NLD

ü

ü

NYA

NYA

NLD

NLD

ü

ü

ü

ü

Audit and Compliance CommitteeThe Audit and Compliance Committee is established as a Committee of the Board and is responsible for the integrity of the Group's financial reporting, including scrutinising accounting policies and monitoring the effectiveness of the Company's internal control and risk management systems. The Committee also reviews the effectiveness and objectivity of the Company's internal and external auditors among other things.

The Audit Committee is to meet at least three (3) times a year and each of these meetings is to be attended by relevant members of the Company's Management team including the Managing Director, the Chief Operating Officer, the Internal Auditor, the General Manager-Risk Management, the Head of Finance and Performance Management, Head of Legal and where necessary the External Auditors.

Since this Committee was established in the fourth quarter of 2016, the Committee did not hold any meetings in 2016.The members of the Committee are:

a. Ms. Elizabeth Amadiume - Chairmanb. Mr. Dominic Ichabac. Mr. Steve Iwenjora

22

CORPORATE GOVERNANCE REPORT CONTD. 2016 Annual Report & Accounts

ü

NYM

ü

ü

ü

ü

NYM

ü

NYM

ü

✗

NLD

ü

NYM

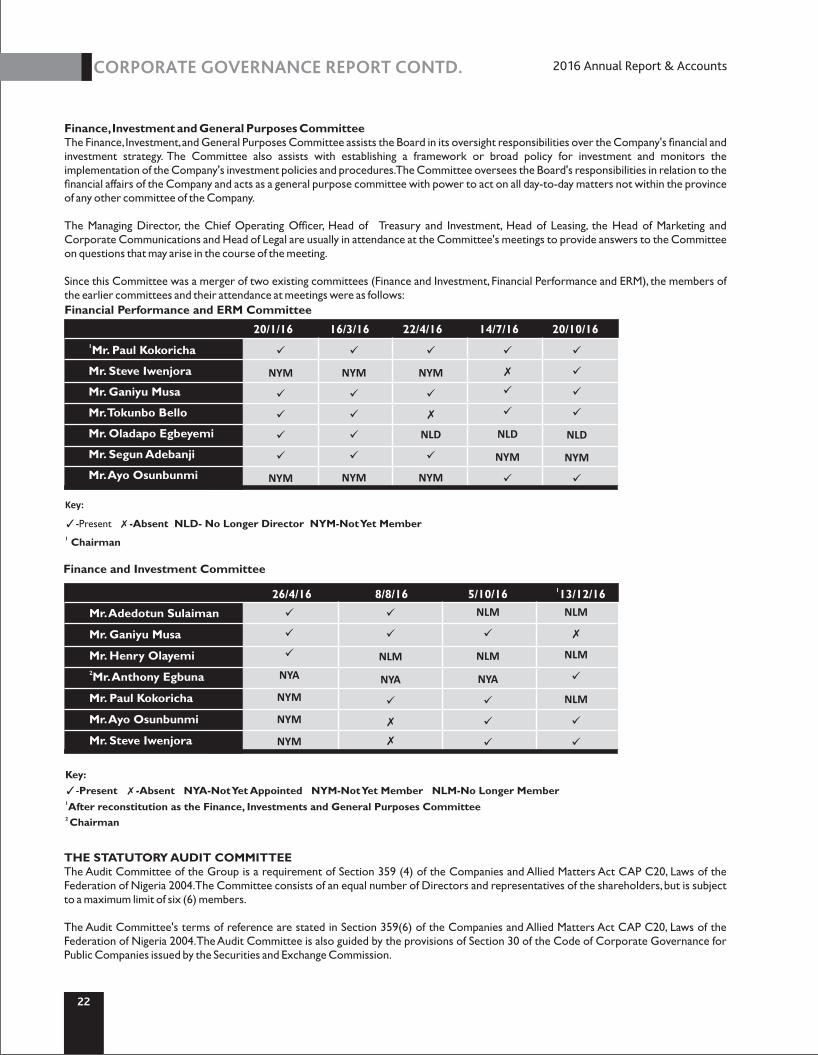

Financial Performance and ERM Committee

20/1/16 16/3/16 22/4/16 14/7/16 20/10/161Mr. Paul Kokoricha

Mr. Steve Iwenjora

Mr. Ganiyu Musa

Mr. Tokunbo Bello

Mr. Oladapo Egbeyemi

Mr. Segun Adebanji

Mr. Ayo Osunbunmi

ü

NYM

ü

ü

ü

ü

NYM

ü

✗

ü

ü

NLD

NYM

ü

ü

ü

ü

ü

NLD

NYM

ü

Key:

✓-Present ✗-Absent NLD- No Longer Director NYM-Not Yet Member 1 Chairman

Finance and Investment Committee

ü

ü

ü

NYA

NYM

NYM

NYM

NLM

ü

NLM

NYA

ü

ü

ü

ü

ü

NLM

NYA

ü

✗

✗

NLM

✗

NLM

ü

NLM

ü

ü

Mr. Adedotun Sulaiman

Mr. Ganiyu Musa

Mr. Henry Olayemi2Mr. Anthony Egbuna

Mr. Paul Kokoricha

Mr. Ayo Osunbunmi

Mr. Steve Iwenjora

126/4/16 8/8/16 5/10/16 13/12/16

Key:✓-Present ✗-Absent NYA-Not Yet Appointed NYM-Not Yet Member NLM-No Longer Member1After reconstitution as the Finance, Investments and General Purposes Committee2 Chairman

THE STATUTORY AUDIT COMMITTEEThe Audit Committee of the Group is a requirement of Section 359 (4) of the Companies and Allied Matters Act CAP C20, Laws of the Federation of Nigeria 2004. The Committee consists of an equal number of Directors and representatives of the shareholders, but is subject to a maximum limit of six (6) members.

The Audit Committee's terms of reference are stated in Section 359(6) of the Companies and Allied Matters Act CAP C20, Laws of the Federation of Nigeria 2004. The Audit Committee is also guided by the provisions of Section 30 of the Code of Corporate Governance for Public Companies issued by the Securities and Exchange Commission.

Finance, Investment and General Purposes CommitteeThe Finance, Investment, and General Purposes Committee assists the Board in its oversight responsibilities over the Company's financial and investment strategy. The Committee also assists with establishing a framework or broad policy for investment and monitors the implementation of the Company's investment policies and procedures. The Committee oversees the Board's responsibilities in relation to the financial affairs of the Company and acts as a general purpose committee with power to act on all day-to-day matters not within the province of any other committee of the Company.

The Managing Director, the Chief Operating Officer, Head of Treasury and Investment, Head of Leasing, the Head of Marketing and Corporate Communications and Head of Legal are usually in attendance at the Committee's meetings to provide answers to the Committee on questions that may arise in the course of the meeting.

Since this Committee was a merger of two existing committees (Finance and Investment, Financial Performance and ERM), the members of the earlier committees and their attendance at meetings were as follows:

23

CORPORATE GOVERNANCE REPORT CONTD. 2016 Annual Report & Accounts

Information Flow and Access to ManagementComprehensive Board papers are circulated electronically and in print to the Directors before each meeting of the Board and Board Committees. The Board papers highlight and address the agenda items on which the Managing Director will report and areas requiring approvals and decisions of the Board.

The Board has a good line of communication with Management and can request the presence of any senior Management staff to provide information when required at its meetings.

The Company Secretary is available to advise individual Directors on corporate governance matters.

Directors' RemunerationThe remuneration of Non-Executive Directors is competitive and comprises an annual fee and a meeting attendance allowance. The Board, through the ERM and Governance Committee, periodically reviews the remuneration package for Directors which is structured in a manner that does not compromise a Director's independence. The Company does not provide personal loans or credits to its Non-Executive Directors and publicly discloses the remuneration of each Director on an annual basis. In addition, the Company does not provide stock options to its Non-Executive Directors unless approved by shareholders at a general meeting.

The remuneration of Executive Directors including entitlements, benefits and share option schemes are adequately disclosed in the Financial Statements. However, no share option schemes were exercised in 2016.

Securities Trading PolicyIn compliance with the Investments & Securities Act, 2007, the Consolidated Rules and Regulations of the Securities and Exchange Commission and other relevant regulatory provisions, the Group has established a Securities Trading Policy which prohibits Directors, senior management, employees, professional advisers and every insider as described therein from abusing or placing themselves under the suspicion of abusing price sensitive information in relation to the Company's securities during closed periods. The policy is also available for viewing on https://cornerstone.com.ng/.

ü

ü

ü

ü

NYA

✗

ü

NYA

ü

ü

NLD

NLD

ü

NLM

ü

ü

21-1-2016 16-3-2016 21-4-2016 14-7-2016 20-10-20161Mr. Henry Olayemi

Mr. Chibuzor Eke

Mr. Lazarus Onwuka

Mr. Peter Ameadaji

Mr. Ariyo A. Olugbosun

Mr. Paul Kokoricha

Mrs. Ndidi O. Nwuneli

Mr. Dominic Ichaba

ü

ü

ü

ü

NYA

ü

ü

NYA

ü

ü

ü

NLD

NYA

ü

ü

NYA

✗

ü

NLD

NLD

NYA

✗

ü

ü

Key:✓-Present ✗-Absent NYA-Not Yet Appointed NLD- No Longer Director NLM-No Longer Member 1 Chairman

The members of the Statutory Audit Committee in 2016 and their attendance at meetings are as follows:

The Audit Committee meets at least three (3) times a year and each of these meetings are attended by relevant members of the Company's Management team including the Managing Director, the Chief Operating Officer, the Internal Auditor, the General Manager-Risk Management, the Head of Finance and Performance Management, Head of Legal and where necessary the External Auditors.

The roles and responsibilities of the Audit Committee include to:• Ascertain whether the accounting and reporting policies of the Company are in accordance with legal requirements and agreed ethical

practices;• Review the scope and planning of audit requirements;• Review the findings on Management matters in conjunction with the external auditor and departmental responses thereon;• Keep under review the effectiveness of the Company's system of accounting and internal control;• Make recommendations to the Board with regard to the appointment, removal and remuneration of the external auditors of the

company; • Authorise the internal auditor to carry out investigations into any activities of the Company which may be of interest or concern to the

committee.• Review the Company's whistle-blowing policy• Monitor and review the effectiveness of the Company's internal audit function in the context of the Company's overall risk management

system.

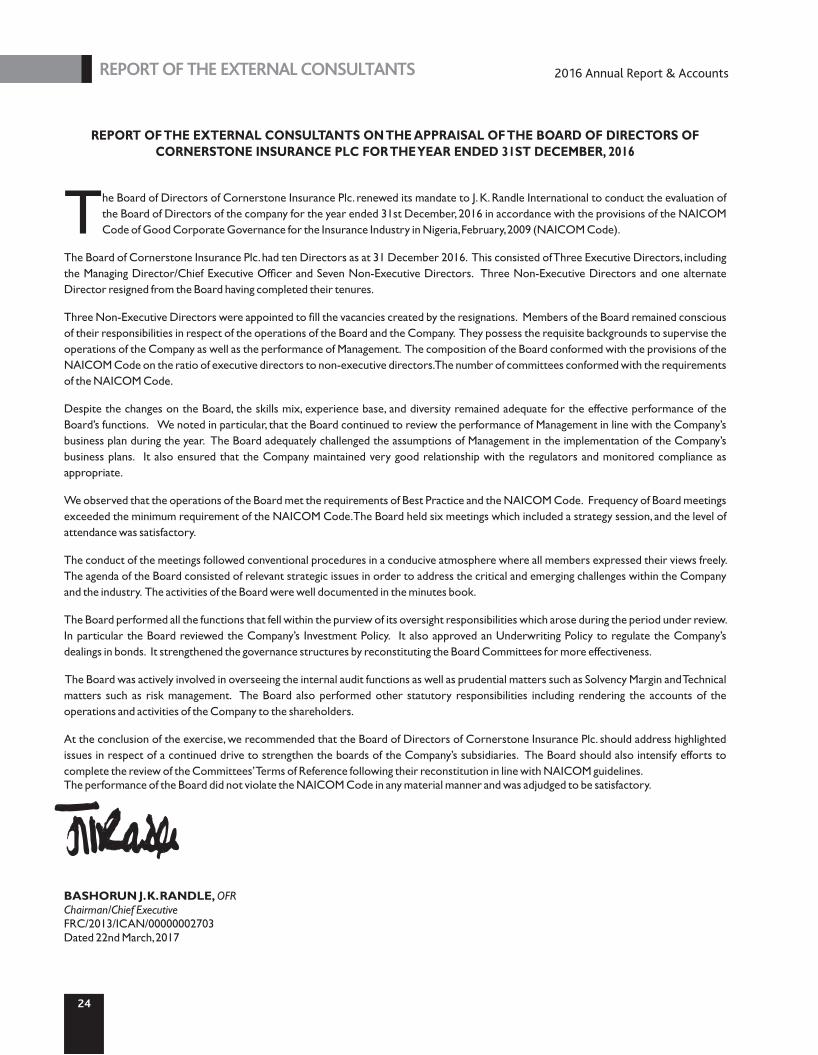

REPORT OF THE EXTERNAL CONSULTANTS 2016 Annual Report & Accounts

he Board of Directors of Cornerstone Insurance Plc. renewed its mandate to J. K. Randle International to conduct the evaluation of Tthe Board of Directors of the company for the year ended 31st December, 2016 in accordance with the provisions of the NAICOM Code of Good Corporate Governance for the Insurance Industry in Nigeria, February, 2009 (NAICOM Code).

The Board of Cornerstone Insurance Plc. had ten Directors as at 31 December 2016. This consisted of Three Executive Directors, including the Managing Director/Chief Executive Officer and Seven Non-Executive Directors. Three Non-Executive Directors and one alternate Director resigned from the Board having completed their tenures.

Three Non-Executive Directors were appointed to fill the vacancies created by the resignations. Members of the Board remained conscious of their responsibilities in respect of the operations of the Board and the Company. They possess the requisite backgrounds to supervise the operations of the Company as well as the performance of Management. The composition of the Board conformed with the provisions of the NAICOM Code on the ratio of executive directors to non-executive directors. The number of committees conformed with the requirements of the NAICOM Code.

Despite the changes on the Board, the skills mix, experience base, and diversity remained adequate for the effective performance of the Board’s functions. We noted in particular, that the Board continued to review the performance of Management in line with the Company’s business plan during the year. The Board adequately challenged the assumptions of Management in the implementation of the Company’s business plans. It also ensured that the Company maintained very good relationship with the regulators and monitored compliance as appropriate. We observed that the operations of the Board met the requirements of Best Practice and the NAICOM Code. Frequency of Board meetings exceeded the minimum requirement of the NAICOM Code. The Board held six meetings which included a strategy session, and the level of attendance was satisfactory.

The conduct of the meetings followed conventional procedures in a conducive atmosphere where all members expressed their views freely. The agenda of the Board consisted of relevant strategic issues in order to address the critical and emerging challenges within the Company and the industry. The activities of the Board were well documented in the minutes book.

The Board performed all the functions that fell within the purview of its oversight responsibilities which arose during the period under review. In particular the Board reviewed the Company’s Investment Policy. It also approved an Underwriting Policy to regulate the Company’s dealings in bonds. It strengthened the governance structures by reconstituting the Board Committees for more effectiveness.

The Board was actively involved in overseeing the internal audit functions as well as prudential matters such as Solvency Margin and Technical matters such as risk management. The Board also performed other statutory responsibilities including rendering the accounts of the operations and activities of the Company to the shareholders.

At the conclusion of the exercise, we recommended that the Board of Directors of Cornerstone Insurance Plc. should address highlighted issues in respect of a continued drive to strengthen the boards of the Company’s subsidiaries. The Board should also intensify efforts to complete the review of the Committees’ Terms of Reference following their reconstitution in line with NAICOM guidelines.The performance of the Board did not violate the NAICOM Code in any material manner and was adjudged to be satisfactory.

BASHORUN J. K. RANDLE, OFRChairman/Chief ExecutiveFRC/2013/ICAN/00000002703Dated 22nd March, 2017

REPORT OF THE EXTERNAL CONSULTANTS ON THE APPRAISAL OF THE BOARD OF DIRECTORS OFCORNERSTONE INSURANCE PLC FOR THE YEAR ENDED 31ST DECEMBER, 2016

24

Directors' shareholding: The Directors of the Company who held office during the year together with their direct and indirect interest in the issued share capital of the Company as recorded in the Register of Directors shareholding and as notified by the Directors in line with section 275 and 276 of the Company and Allied Matters Act and the Listing requirements of the Nigeria Stock Exchange are as follows:

The Directors of Cornerstone Insurance PLC (“Cornerstone'' or the “Company”) present their Report on the affairs of Cornerstone and its subsidiaries (together referred to as “the Group”), together with the Audited consolidated and separate financial statements and the Auditor's report for the year ended December 31 2016. st

LEGAL FORM AND PRINCIPAL ACTIVITYThe Company was incorporated on 26 July, 1991 as a private limited liability company and converted to a public limited company on 17 June, 1997.

The Company's principal activity continues to be the provision of risk underwriting and related financial services to its customers. Such services include provision of life and non-life insurance services for both corporate and individual customers.

The Company has two wholly owned subsidiaries – Cornerstone Leasing and Investment Limited and Fin Insurance Company Limited. Cornerstone Leasing and Investment Limited commenced operations on 1 July 2004 and provides convenient asset acquisition options to

both corporate organizations and individuals. FIN Insurance Company Limited is a private limited liability company incorporated in Nigeria and its primary activity is the provision of general insurance business. Fin Insurance Company Limited was acquired in the year 2015. Cornerstone Insurance Plc acquired 96.68% equity interest in Fin Insurance Company Limited thereby qualifying Fin Insurance Company Limited as a subsidiary. The Company prepares consolidated financial statements. The financial results of all its subsidiaries have been consolidated in this Annual Report and Accounts.

2016 Annual Report & AccountsFor the year ended 31st December, 2016DIRECTORS’ REPORT

* These Directors represent the interest of Banc-Assure Limited and Capasure Limited on the Board of the Company

Operating Results: The following is a summary of the operating results:

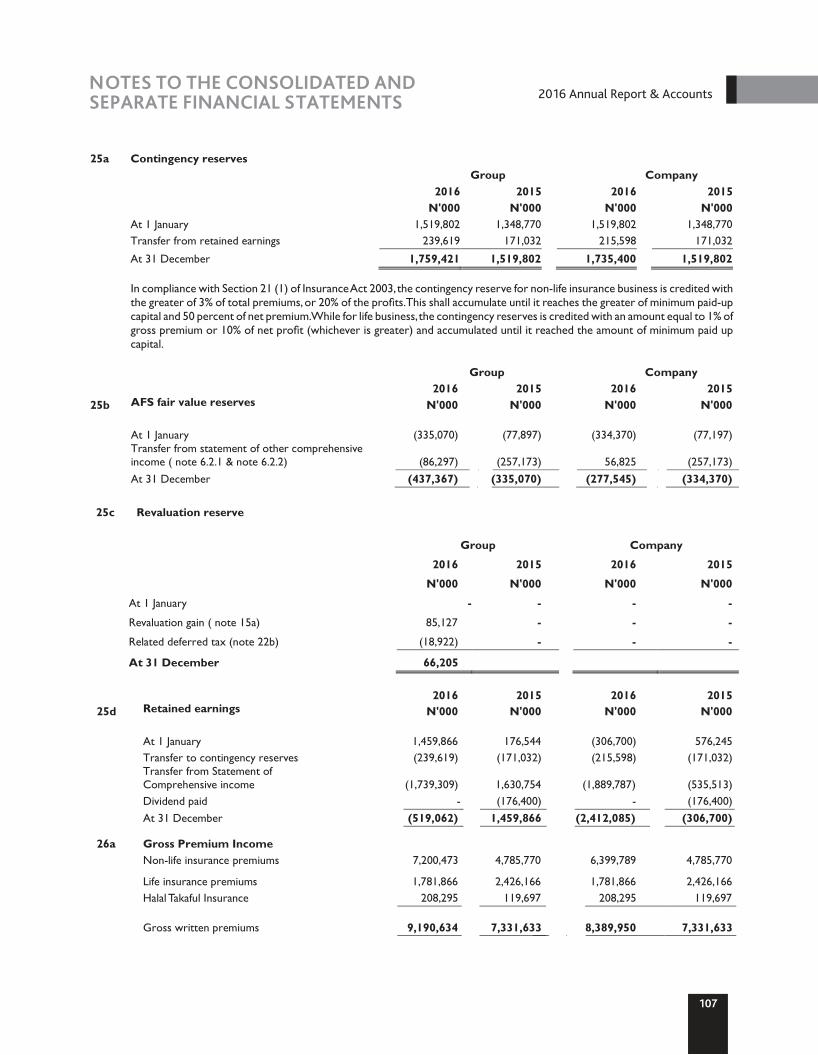

Group Group Company Company Group Company 2016 2015 2016 2015 YOY % YOY % N’000 N’000 N’000 N’000 Growth Growth

Gross Premium Written 9,190,634 7,331,633 8,389,950 7,331,633 25% 14%

Gross Premium Income 8,456,458 7,119,632 7,768,850 7,119,632 19% 9% (Loss)/Profit before taxation (1,264,660) 1,843,054 (1,516,213) (332,139) -169% 356% Taxation charge (470,563) (212,300) (373,574) (203,374) 122% 84%

(Loss)/Profit after taxation (1,735,223) 1,630,754 (1,889,787) (535,513) -206% 253%

Mr. -

NA

-

-

-

-

NA

-

NA

2,239,000

-

-

-

503,360

NA

DIRECT INDIRECT TOTAL

-

NA

2,239,000

-

-

503,360

NA

NAMES OF DIRECTORS

Mr. Paul Kokoricha *Ganiyu Musa

Mr. Dominic Ichaba

Mr. Anthony Egbuna *Mr. Steve Iwenjora *Mr. Ekwunife Okoli

Ms. Elizabeth Amadiume

Mr. Segun Adebanji *

Mr. Tokunbo Bello

Mr. Ayo Osunbunmi

25

26

2016 Annual Report & AccountsFor the year ended 31st December, 2016DIRECTORS’ REPORT

ANALYSIS OF SHAREHOLDING Shareholding Structure as at 31 December 2016 The analysis of the distribution of the shares of the Company at the end of the financial year was as follows:

The free float of shares as at the year ended 2016 stands at 46.4%. Property and Equipment Information relating to changes in property and equipment is given in Note 15 to the financial statements.

HUMAN CAPITALThe Company's Human Capital unit is responsible for driving and enhancing the performance of the organisation as well as attracting high potential professionals. All Human Capital policies of the Company are subject to local laws and regulations in Nigeria. One of the objectives of the unit is to provide a work environment that is conducive for both personal and professional growth and ensure that Management aligns with global best practice.

Employment of Physically Challenged Persons The Group operates a non-discriminatory policy in the consideration of applications for employment, including those received from physically challenged persons. The Group's policy is that the most qualified and experienced persons are recruited for appropriate job levels irrespective of an applicant's state of origin, ethnicity, religion or physical condition. In the event that an employee becomes physically challenged in the course of employment, the Group is in a position to arrange appropriate training to ensure the continuous employment of such a person without subjecting him/her to any disadvantage in his/ her career development. As at 31 December 2016, the Group had no physically challenged persons in its employment.

Range Number of shareholders

Number of shares held

1 -500

501 -1 ,000

1,001 -5 ,000

5 ,001 -10 ,000

10,001 -20,000

20,001 -50,000

50,001 -1,00 ,000

1,00,001 -5, 00,000

5,00,001 -1 ,000,000

1,000,001 -ABOVE

TOTAL

1,007

1,185

7,764

5,382

3,934

4,075

2,092

1,520

219

213

27,391

% of number of shares held

0.00

0.01

0.19

0.32

0.44

0.99

1.16

2.30

1.20

93.40

100

% of number of shareholders

3.68

4.33

28.35

19.65

14.36

14.88

7.64

5.55

0.80

0.78

100

277,293

1,088,001

28,038,546

46,479,215

64,504,551

145,733,030

170,930,503

339,083,286

176,515,413

13,756,948,770

14,729,598,613

SUBSTANTIAL INTEREST IN SHAREHOLDING AS AT 31 DECEMBER, 2016

BANC-ASSURE LIMITED 7,143,885,379 49 CAPASURE LIMITED 4,498,205,285 31

NAME SHAREHOLDING % OF SHAREHOLDING

Name Of Director Interest In Company Name Of Company Services

Mr. Dominic Ichaba Director/Shareholder Pac Solicitors Legal Services

DIRECTORS' INTEREST IN CONTRACTS In accordance with section 277 of the companies and Allied Matters Act of Nigeria, The Board received a declaration from the following Director in respect of the services set against his name.

27

2016 Annual Report & AccountsFor the year ended 31 December, 2016DIRECTORS’ REPORT

Gender Equality in Employment Cornerstone is an equal opportunity employer that adheres strictly to the principles of equality in all employment decisions and interventions. In order to provide equal employment opportunities to all individuals, employment decisions are based on merit, available vacancies and organizational priority.

Health, Safety and Welfare of Employees The Group continues to maintain strict health and safety rules and practices in the work environment which are reviewed periodically. Health, safety and fire drills are regularly organised to keep employees alert at all times. Employees are adequately insured against occupational hazards. In addition, the Group provides health insurance for its employees and their immediate families at its expense.

Employee Involvement and Training The Company places considerable value on the involvement of its employees and has continued the practice of keeping them informed on matters affecting them as employees and on various factors affecting the performance of the Company. Employee representatives are consulted regularly on a wide range of matters affecting their current and future interests. Management decisions are communicated to employees on matters that are of concern to them by utilising various means of internal communication, including internal memoranda, email, Intranet Portal, companywide team building interactions, management meetings and business performance sessions among others. The Company encourages the involvement of employees in the Company's performance through: • Reward & Recognition schemes such as staff promos; awards for the best performing staff in different areas of the organization

(Marketing & Support teams); • Profit sharing; • No Accident Bonus for Company drivers; and • Performance Pay (variable pay) for Middle to Senior Management Staff

For the year 2016 Financial Year, trainings were conducted using the following methods: • E-learning • Knowledge Sharing Sessions • Class room based trainings • Product Knowledge Trainings • Open programmes • International & Local Seminars • Health, Safety and Environment Training

Staff breakdown for 2016

28

2016 Annual Report & AccountsFor the year ended 31st December, 2016DIRECTORS’ REPORT

ENTERPRISE RISK MANAGEMENT

OverviewCornerstone's Enterprise Risk Management (ERM) model originates from a compendium of International risk standards. Foremost of the three (3) models is the ISO 31000 - Risk Management - Principles and Guidelines. The definition of risk represents the foundation of Cornerstone's risk management philosophy as contained in the ERM framework document. Corresponding supporting frameworks include:

• The COSO integrated framework and• The three (3) lines of risk defense model - Risk owners, ERM

& Internal Control/Audit

In addition to developing veritable structures in responding to the traditional Insurance Industry risks of claims management and underwriting risks among others, the Board of Directors and Management appreciate the dynamism risk portends for the business. For this reason, risk management structures have been instituted to administer material changes in the corporate risk management framework. These risks include: compliance/ regulatory, health and safety, strategic, reputational, operational and financial risks.

The Board is vested with the overall responsibility of overseeing the Group's risk management and internal control mechanism. The Group's internal Audit/Control function is instituted to strategically manage risks in the overall rather than exclude material risks in relation to the attainment of corporate objectives. The Group promotes the culture of risk awareness through policy directives, communication and training. Management is responsible for identifying, assessing and addressing material risks, and designing internal controls accordingly. Standard operating procedures and inherent controls are subject to periodic reviews by the Enterprise Risk Management unit, Management and Board Committees. The key financial and non-financial risks and uncertainties faced by the Group, have been considered during the year, and our approaches to managing them, are described in this report.

The Cornerstone Enterprise Risk Management (ERM) Programme

The Group's Enterprise Risk Management (ERM) Programme comprises instituted structures designed to manage a myriad of uncertainties and threats and equally explore opportunities in enhancing the Group's performance standards. The Group's ERM practice involves a cross-functional and multi-dimensional approach to corporate risk management. An ERM unit has been specifically charged with the function of identifying, evaluating, monitoring and reporting uncertainties (risks and opportunities) that may impact on corporate objectives (ISO: 31000) using the RAG (Red, Amber and Green) rating methodology.

The Group's risk context delineates the scope of the risk management process and sets the standards against which risks will be assessed in accordance with the Group's primary objective to be the leading insurance based financial services Group that transforms. The Group appreciates the myriad of uncertainties inherent in underwriting insurance and managing ancillary risks and how such risks potentially impact achievement of business objectives if left unaddressed via a structured /multi-dimensional risk management approach. It is to this end that the Group's ethics, philosophy and risk culture are embodied in our integrated risk management and control function.

Enterprise Risk Management (ERM) Governance A system of risk governance is realised by establishing standards related to organisational structure, risk strategy, written policies, limit systems, documentation and reporting. These structures ensure the timely movement of risk-related information and a s t ructured approach towards dec i s ion-mak ing and implementation.

Risk Management PhilosophyThe key elements of the Group's risk management philosophy are as follows:

• The Group considers sound risk management as the foundation of a long lasting financial institution.

• The Group shall continue to adopt a holistic and integrated approach to risk management.

• Risk officers shall be empowered to perform their duties professional ly and independently without undue interference.

• Risk management shall be governed by policies which are well defined and clearly communicated Group-wide.

• Risk management represents a shared responsibility. Therefore, the Group aims to build a shared -perspective on risks that is grounded on consensus.

Risk CultureThe Board and Senior management set the tone-at-the-top, by promoting accountable approaches to risks which are targeted at ensuring that the long-term rewards and the reputation of the Group is not jeopardized in a bid to achieve set objectives.

• The apex responsibility for risk management and control is fully vested in the Board of Directors.

• The Group's Management shall promote risk awareness and risk management practice across the enterprise.

• The Group advocates risk event reporting and whistle blowing, in order to properly monitor incidences of unethical practices.

• The Group shall maintain a firm obligation to ethical principles, which shall be demonstrated in the ethical performance of staff and in the decision making process.