rbs round up - 060810 brought to you be egol.com.au

TRANSCRIPT

8/9/2019 RBS Round Up - 060810 brought to you be egol.com.au

http://slidepdf.com/reader/full/rbs-round-up-060810-brought-to-you-be-egolcomau 1/10

Equity Structured Products and Warrants

This material has been produced by RBS sales and trading staff and should not be considered independent.

The Round Up

6 August 2010 Issue No. 382

The Round Up is a comprehensive

daily note produced by the RBS

Warrants team providing an overview

of market movements along with

quality ideas for warrant traders and

investors.

Equities

Move Last % Move Range Volume

ASX 200 +24.4 4566.5 +0.5% u.c to +38 $5.0 bn(A)

SPI - yesterday +18.0 4537.0 +0.4% +8 to +31 18,194(L)

Dow Jones -5.5 10675.0 -0.1% -68 to -1 LowS&P 500 -1.4 1125.8 -0.1% -8 to -1 LowNasdaq -10.5 2293.1 -0.5% -22 to -5 LowFTSE -20.4 5365.8 -0.4% -29 to +31 Avg

Commodities Move Last % Today % Past Month

Oil-WTI spot -0.41 82.06 -0.5% +13.8%Gold Spot +0.75 1195.70 +0.1% -1.1% Nickel (LME) -3.45 989.25 -0.3% +17.2%Aluminium (LME) -1.19 99.39 -1.2% +14.7%Copper (LME) -4.83 334.35 -1.4% +14.5%Zinc (LME) -1.03 93.85 -1.1% +16.6%Silver +0.05 18.35 +0.3% +3.0%Sugar -0.59 18.29 -3.1% +9.5%

Global Market Action Scoreboard, commentary

Aussie Market Action SPI Comment, Events & Dividends

RIO Tinto (RIOKZG) MINI Trading Buy – Iron Clad Results

Macquarie Group(MQGKZD) MINI Trading Buy – When the going gets tough....

Origin Energy (ORGKZC) MINI Trading Buy – Offtake and set for NSW

privatisation sale

Australian Strategy Monthly Market Review - May 2010

8/9/2019 RBS Round Up - 060810 brought to you be egol.com.au

http://slidepdf.com/reader/full/rbs-round-up-060810-brought-to-you-be-egolcomau 2/10

Equity Structured Products and Warrants

Dual Listed Companies (DLC’s) Move %Move Last AUD Terms Diff to Aus

NWS (US) +0.35 +2.2% 15.93 17.40 -24.2 c

RIO (UK) +18.0 p +0.5% £34.30 59.54 -1346.5 c

BLT (BHP UK) +16.0 p +0.8% £20.250 35.15 -568.6 c

American Depository Receipts (ADR’s) Move %Move Last AUD Terms Diff to Aus

BHP (US) +0.02 +0.0% 75.05 40.98 +14.4 c

AWC (US) +0.02 +0.3% 5.96 1.63 -1.3 c

ANZ (US) -0.30 -1.4% 21.05 22.99 -21.7 c

WBC (US) -0.83 -0.8% 108.66 23.74 -11.5 c

NAB (US) -0.09 -0.4% 22.85 24.96 -23.4 c

LGL (US) +0.57 +1.5% 39.05 4.26 -0.5 c

RMD (US) +0.34 +0.5% 68.03 7.43 +6.0 c

JHX (US) -0.45 -1.5% 28.60 6.25 -0.3 c

PDN (CAN) +0.13 +3.6% 3.75 4.03 -6.4 c

Overnight Commentary United States Commentary

Stocks fell and Treasuries rallied as an unexpected jump in American jobless claims fueled concern the economic rebound is slowing.

The yen strengthened and wheat jumped to a 23-month high.

The thought of a potential upside breakout ahead of Friday's payroll number appears to be derailed by a soft jobless claims report. In

the overnight session, the headline index futures have traded in tight ranges near the top of this week's range but post jobless claims,

prices have retraced to the midpoints of yesterday's range. The majority of the past three trading sessions, S&P futures have remained

in a tight range between 1124.50 (100 day moving average) and 1112.00 (200 day moving average). This week's market profile (see

chart) shows a stronger bottom and a less convincing high giving greater probability to a move higher later in the week but today's price

action may follow a similar pattern of the previous three sessions and stay in between the two key moving averages. Beyond the

recent trading range, 1103.00 continues to be key support while 1127.50 remains the next big hurdle.

United Kingdom & Europe Commentary

Eurostoxx: -0.2% FTSE: -0.38% DAX: +0.04% CAC: +0.09%

Eurostoxx traded with no real conviction overnight. Opened flattish, traded up for most of the morning before grinding lower over the

afternoon. Closed not far off the lows.

Earnings news:

Aviva (+7%), Rio Tinto (+0.5%), Deutsche Tel (-2.8%), Ferrexpo (+0.03%), Givaudan (+1.7%) and Millennium & Copthorne (+7%)

were all strong ...

Unilever (-5%) still managed to disappoint despite most people expecting weak numbers given what we have seen otherwise out of the

HPC space.... Barclays (-4.7%) caused some disappointment as they missed their cost targets but Inv Bank biz better than peers. ...

Commerzbank (-2%) said that they were actually going to make a profit this year... Generali (-0.25%) reported in line.

Otherwise it was quite a day for macro in Europe... we started with a v strong Spanish Bond auction with 3.5bln issued (top of range),

1.9 x bid to cover. 2.276% yield (vs 3.32% when issued June 10). Saw more positives for the peripheral soverign space with a

Statement issued by EC, ECB & IMF post the first review mission to Greece was pretty positive....

In non- peripheral, German Factory orders came in better at 3.2% vs 1.4%, in line with recent strength of data. Worth noting Elga'

Batch's note this morning raising GDP forecasts for the eurozone, although she doesn't believe this strength will last due to a

weakening consumer (again the higher food inflation factor playing some part). ECB & MPC leave rates unchanged as expected.

8/9/2019 RBS Round Up - 060810 brought to you be egol.com.au

http://slidepdf.com/reader/full/rbs-round-up-060810-brought-to-you-be-egolcomau 3/10

Equity Structured Products and Warrants

Commodities Commentary

Oil-0.5%,Gold+0.1%,Nickel-0.3%,Aluminium-1.2%,Copper-1.4%,Zinc-1.1%,Silver+0.3%.

GOLD

Gold extended its gains to settle higher for a seventh straight day on Thursday as physical buying on China's decision to expand itsmarket for the metal and old extended its gains to settle higher for a seventh straight day on Thursday

OIL

Oil declined Thursday, tracking a slump in equities and as the start of contract rollover put some pressure on the front-month contract.

The National Hurricane Centre released its latest forecast for the Atlantic hurricane season, which cut down the number of named

storms expected even though it reaffirmed an active hurricane season.

Currencies Commentary

The U.S. dollar declined modestly against the euro and other major rivals on Thursday as traders hesitated to make large bets aheadof Friday's U.S. jobs report, which is expected to show private employers hired while overall payrolls dropped.

The euro had been higher after European Central Bank President Jean-Claude Trichet gave a positive spin to second-quartereconomic numbers and stress tests of the European banks.

SPI Commentary

The SPI traded up 13pts to 4537. Open at 4524 with a high of 4553 and a low of 4503. Volume 21,540. Overnight the SPI traded down

5pts to 4532.

SPI Intraday SPI Daily

*SPI report taken from the 9:50am open to the 4:30pm close on the previous trading day. Charts taken from IRESS

8/9/2019 RBS Round Up - 060810 brought to you be egol.com.au

http://slidepdf.com/reader/full/rbs-round-up-060810-brought-to-you-be-egolcomau 4/10

Equity Structured Products and Warrants

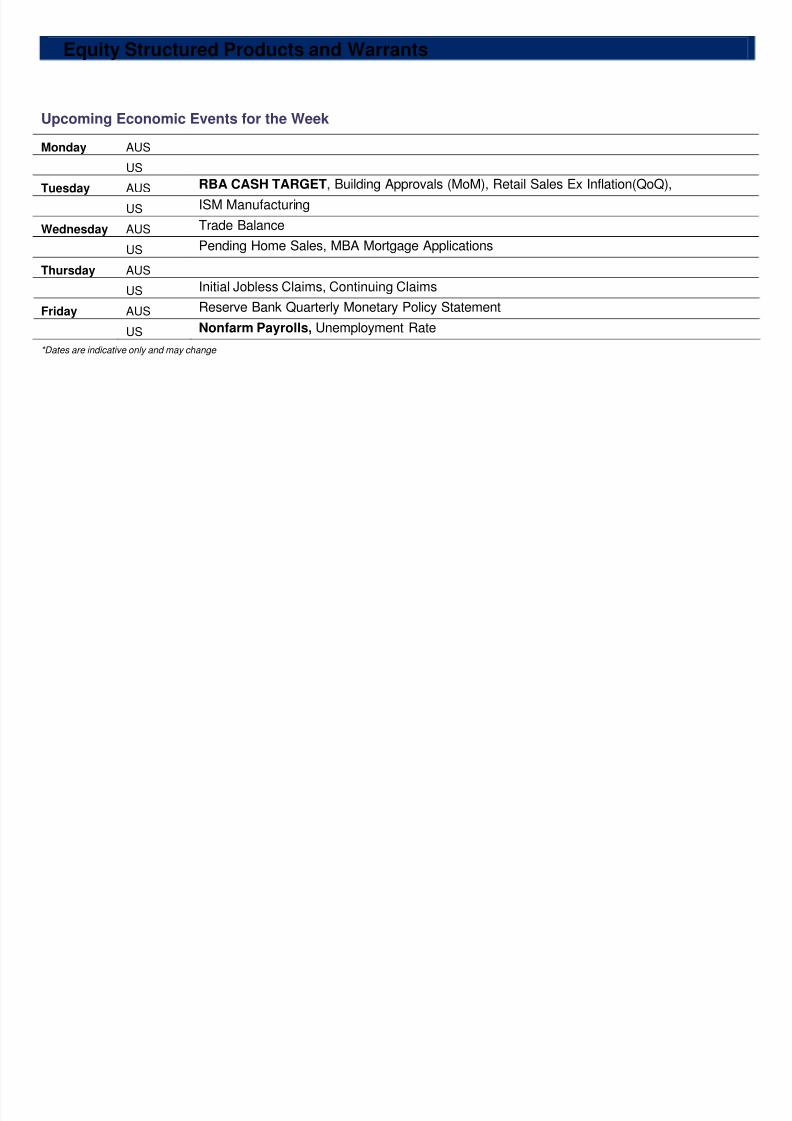

Upcoming Economic Events for the Week

Monday AUS

US

Tuesday AUS RBA CASH TARGET, Building Approvals (MoM), Retail Sales Ex Inflation(QoQ),

US ISM Manufacturing

Wednesday AUS Trade Balance

US Pending Home Sales, MBA Mortgage Applications

Thursday AUS

US Initial Jobless Claims, Continuing Claims

Friday AUS Reserve Bank Quarterly Monetary Policy Statement

US Nonfarm Payrolls, Unemployment Rate

*Dates are indicative only and may change

8/9/2019 RBS Round Up - 060810 brought to you be egol.com.au

http://slidepdf.com/reader/full/rbs-round-up-060810-brought-to-you-be-egolcomau 5/10

Equity Structured Products and Warrants

MINI Trading Buy: RIO Tinto (RIOKZG) – Iron Clad Result

RBS MINIs over RIO

Stock: Rio Tinto Ticker: RIO Share price: A$73.01 Target price: A$83.20 NPV: A$83.20 Rec. Buy

Summary

RIO reported underlying earnings of US$5.8bn, ahead of consensus at US$5.5bn and well above our forecast US$5.2bn.The difference related to iron ore where RIO achieved better prices than we had expected (we took a conservative view

on price realisations in light of the move from benchmark to quarterly contracts). A dividend of US$0.45ps was declared,inline with our forecast. Net debt at the end of the period stands at US$12bn (US$19bn YE2010), with gearing at 19%.Overall a strong result in our view.

Underlying NPAT by division

Divisional NPAT (US$m) 1H10E Consensus Actual Diff vs RBS Diff vs RBS Iron Ore 3,420 3676 4108 688 20%

Aluminium 387 348 358 -29 -7%

Copper 1,185 1153 1062 -123 -10%

Energy 620 793 642 22 4%

Diamond and Minerals 83 81 121 38 45%

Other Operations 4 -61 -2 -6 -148%

Underlying NPAT (US$m) 5,188 5,515 5,767 579 11%

Iron ore remains the key swing factor for RIO, with 2/3rds of earnings coming from the division. 3Q10 iron ore prices willbe the average of the March to May spot price, implying US$147/t FOB (above the spot price of US$134/t). Thisrepresents another gain qoq, which will see positive earnings momentum continue.

Corporate items

RIO is about to enter a growth phase which is positive for production growth, however a significant amount of capexneeds to be spent.

+ Net debt reduced to US$12bn from US$39bn at 30 June 2009 + Full year 2010 capex to approach US$6bn (RBS US$5.7bn)

+ Full year 2011 capex to be approx US$9bn (RBS US$5.9bn) + Impairment charge of US$403m, related to Alcan Engineered Products

Security ExPrc Stop Loss CP ConvFac Delta Description

NCMKZG 51.2382 56.31 Long 1 1 MINI Long

8/9/2019 RBS Round Up - 060810 brought to you be egol.com.au

http://slidepdf.com/reader/full/rbs-round-up-060810-brought-to-you-be-egolcomau 6/10

Equity Structured Products and Warrants

MINI Trading Buy: Macquarie Group (MQG.AX): When the going gets tough.... MQG's 1Q10 update highlighted that key divisions have been impacted by weak market conditions. RBSResearch have lowered FY11F EPS by 4% and 1% in forward years to account for these near term impacts. We

believe that underlying market conditions will improve in 2H11 rendering MQG good value at current levels.Maintain a Buy.

Buy Long MINI MQGKZD for short/medium term trade to $45 or hold for the long term.

Source: IRESS

First quarter ahead of pcp but outlook cautious MQG announced that its 1Q11 earnings were slightly ahead of a subdued pcp. As expected, the key divisions, MacquarieSecurities, Macquarie Capital and FICC, were impacted by weak market conditions. MQG's revised outlook states thatthese divisions are unlikely to beat FY10 results in FY11F if 1Q11 conditions do not improve over the remainder of theyear. However, we believe that conditions in 1Q11 were particularly weak with global equity indices off 10-12% and seethis as unlikely to be repeated over the remainder of FY11.

Changes to forecasts - FY11 EPS reduced by 4% and FY12/13 reduced by 1% RBS Research have lowered FY11F EPS by 4% to account for the cautious outlook for Macquarie Capital, MacquarieSecurities and FICC business. FY12/13F EPS are lowered by 1% as we believe that the investment banking cycle has just been pushed back six to 12 months, and with the transaction pipeline building, it is a matter of markets stabilising toreach execution.

Investment view - retain Buy recommendation, TP trimmed to A$54 MQG's balance sheet remains strong and the firm continues to capitalise on the market downturn by acquiringbusinesses and portfolios from distressed sellers. Whilst the current operating conditions are clearly subdued, theinvestment banking cycle appears to have been pushed back rather than cancelled altogether, and we see near-termearnings supported by lower impairments and recent acquisitions. With the stock still trading below 10x RBS Research’sreduced FY11F EPS, we retain a Buy recommendation.

RBS MINIs over MQG

Security ExPrc Stop Loss CP ConvFac Delta Description

MQGKZB 22.3002 24.33 Long 1 1 MINI Long

MQGKZD 26.1646 28.59 Long 1 1 MINI Long

8/9/2019 RBS Round Up - 060810 brought to you be egol.com.au

http://slidepdf.com/reader/full/rbs-round-up-060810-brought-to-you-be-egolcomau 7/10

Equity Structured Products and Warrants

MINI Trading Buy: Origin Energy (ORGKZC) – Offtake and set for NSW privatisation sale ORG's share price has come under pressure of late. In addition to general market jitters, we believeconcerns over the outlook for APLNG and the potential for an earnings downgrade have also weighed

on sentiment. In our view, the longer-term outlook hasn't changed, and we are buyers on thisweakness. Buy maintained with RBS Target Price of $18.25

Source: IRESS

Earnings should hold up in FY10... A few things have gone against ORG since the interim result in February (eg, Contact, Cooper flooding, lower oil price,weaker APLNG gas sales), but we still expect the company to meet its c15% NPAT guidance (RBS +15.3% vs market+16.6%). The key positive driver over the last half has been particularly weak electricity spot prices, which should help theretail business deliver a solid FY10 result.

... and the outlook for FY11 looks pretty robust As shown in this note, next year seems to be loaded with a range of positive earnings drivers, so we find it hard to seeORG being unable to deliver solid profit growth. In our view, the biggest risk revolves around how the Darling Downspower station will interact with ORG's retail business. In isolation, the near-term outlook for the generator would be pretty

ugly, but we are hoping that any downside is offset by improved retail margins.

RSPT shouldn't have a significant impact on long-term fundamentals We still don't expect the current proposal to get up with no changes (eg, the uplift rate) but, even if it does, we don't see itmaking a material dent in our ORG valuation. RBS Research base-case valuation for APLNG would fall only 10% underthe RSPT, using RBS Research conservative forecasts for capex and an LNG sales price. At any rate, we believe themarket is underestimating ORG's fall-back plans if the LNG project is delayed materially (we have pushed back thetimeline by 12 months to mid 2015) or even shelved.

Buy maintained; we think current weakness provides a good opportunity It may be difficult to pinpoint a precise catalyst for Origin's share price to re-rate but, in our view, there is no question thestock is loaded up with positive optionality that can be exercised at any time. The NSW trade sale (fingers crossed) lookspromising and we believe ORG is well positioned to make an accretive acquisition.

BUY ORGKZC for 1-for-1 upside towards RBS Target Price of $18.25

RBS MINIs over ORG Security ExPrc Stop Loss CP ConvFac Delta Description

ORGKZC 1095.88 1198 Call 1 1 MINI Long

8/9/2019 RBS Round Up - 060810 brought to you be egol.com.au

http://slidepdf.com/reader/full/rbs-round-up-060810-brought-to-you-be-egolcomau 8/10

Equity Structured Products and Warrants

RBS Round Up Corner: Monthly Market Review - July 2010

The focus for markets in July was on the European bank stress tests. Despite some commentators questioning

how 'stressful' the tests really were, the market reacted positively to the outcome. Strong company results in theUS and a more tame than expected outcome from Basel also helped investor sentiment.

Australia's performance vs the world In local currency, the All Ordinaries (+4.2%) underperformed the US S&P 500 (+6.9%), the World MSCI ex AustraliaIndex (+7.9%) and the regional MSCI ex Japan Index (+7.1%).

The best- and worst-performing sectors The best performers for the month were Industrials (+7.2%), Financials ex Property (+6.5%) and Materials (+4.9%). Theworst performers were Information Technology (-4.0%), Telecommunication Services (-0.5%) and Health Care (+0.9%).

The top-five and bottom-five performing S&P/ASX 200 stocks The top-five performers from the S&P/ASX 200 (price) Index for the month were Linc Energy (+56.4%), Intoll Group(+41.3%), Lynas Corporation (+39.4%), Downer EDI (+38.1%) and Kagara (+34.0%). The bottom-five performers wereNufarm (-29.1%), Aquarius Platinum (-19.8%), Eldorado Gold (-14.8%), iSoft Group (-14.7%) and St Barbara (-14.3%).

Consensus earnings revisions The top-five upgrades were Iluka Resources (+23.8%), Intoll Group (+23.4%), Newcrest Mining (+7.2%), Lihir Gold(+6.2%) and OZ Minerals (+2.7%). The top-five downgrades were Nufarm (-31.0%), Aquarius Platinum (-24.3%), Boral (-18.8%), AWE (-14.6%) and Paladin Energy (-10.6%).

8/9/2019 RBS Round Up - 060810 brought to you be egol.com.au

http://slidepdf.com/reader/full/rbs-round-up-060810-brought-to-you-be-egolcomau 9/10

Equity Structured Products and Warrants

Global growth and valuation appeal to drive equities

Global pressure points manageable and global economic growth to progress further We have reviewed the key macro pressure points for global equity markets and are confident the gradual economicrecovery will be sustained. The market appears to be excessively discounting the prevailing structural and cyclical risks,as serious as they are. The global markets are being forced to confront many unresolved issues, creating pockets ofopportunity. In our view, this is one such opportunity. We see corporate investment as the next global growth driver andglobal corporate health is now supportive of investment resumption, following a period of capex neglect. Corporateprofitability should not be underestimated and in time is likely to be the micro issue that takes centre stage, pushingmacro issues to the background.

We believe resumed confidence in earnings will drive markets forwardAnalysts are often thought to be perennially bullish at the outset. However, following two years of savage declines inexpectations and given the fact we are entering the first year of synchronised positive global economic growth, Australianequity consensus estimates appear both defensible and achievable to us, at 24% growth forecast for FY11.

S&P/ASX 200 targets – 5300 by end-2010, 5600 by mid-2011For the market as a whole, we derive our S&P/ASX 200 targets by applying a 12-month forward PE of 12.8x (about 1standard deviation cheap) to the RBS top-down assumptions for net income growth of 23% in FY11F and 14.6% inFY12F. On this basis, we forecast S&P/ASX 200 returns of 22% from 4354 currently to 5300 by year-end 2010 and afurther 5% appreciation to 5600 by mid-2011.

Our view is that there will be no default in Europe but that resolution of the crisis may still be some time off. We showbelow that while debt markets have deteriorated this is certainly no GFC event. With the Australian market trading on a12.2x forward market PE, some good buying opportunities are emerging on any sort of medium-term view.

8/9/2019 RBS Round Up - 060810 brought to you be egol.com.au

http://slidepdf.com/reader/full/rbs-round-up-060810-brought-to-you-be-egolcomau 10/10

Equity Structured Products and Warrants

For further information please do not hesitate to contact us on the details below

Equities Structured Products & Warrants

Toll free 1800 450 005 www.rbs.com.au/warrants

Trading Products Team

Ben Smoker 02 8259 2085 [email protected]

Ryan Corrigan 02 8259 2425 [email protected]

Investment Products Team

Elizabeth Tian 02 8259 2017 [email protected]

Tania Smyth 02 8259 2023 [email protected]

Robert Deutsch 02 8259 2065 [email protected]

Mark Tisdell 02 8259 6951 [email protected]

Disclaimer

The information contained in this report has been prepared by RBS Equities (Australia) Limited (“RBS Equities”) (ABN 84 002 768 701) (AFS Licence No 240530) and hasbeen taken from sources believed to be reliable. RBS Equities does not make representations that the information is accurate or complete and it should not be relied on assuch. Any opinions, forecasts and estimates contained in this report are the views of RBS Equities at the date of issue and are subject to change without notice. RBSEquities and its affiliated companies may make markets in the securities discussed. RBS Equities, its affiliated companies and their employees from time to time may holdshares, options, rights and warrants on any issue contained in this report and may, as principal or agent, sell such securities. RBS Equities may have acted as manager orco-manager of a public offering of any such securities in the past three years. RBS Equities’ affiliates may provide, or have provided banking services or corporate finance tothe companies referred to in this report. The knowledge of affiliates concerning such services may not be reflected in this report. This report does not constitute an offer orinvitation to purchase any securities and should not be relied upon in connection with any contract or commitment. RBS Equities, in preparing this report, has not taken intoaccount an individual client’s investment objectives, financial situation or particular needs. Before a client makes an investment decision, a client should consider whether anyadvice contained in this report is appropriate in light of their particular investment needs, objectives and financial circumstances. It is unreasonable to rely on anyrecommendation without first having consulted with your advisor for a personal securities recommendation. The information contained in this report is general advice only.RBS Equities, its officers, directors, employees and agents accept no liability for any loss or damage arising out of the use of all or any part of the information contained in thisreport. This Information is not intended for distribution to, or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to locallaw or regulation. If you are located outside Australia and use this Information, you are responsible for compliance with applicable local laws and regulation. This report may

not be taken or distributed, directly or indirectly into the United States, or to any U.S. person (as defined in Regulation S under the U.S. Securities Act of 1993, as amended).The warrants contained in this report are issued by RBS Group (Australia) Pty Limited (“RBS”) (ABN 78 000 862 797, AFS Licence No. 247013). The Product DisclosureStatements relating to these warrants are available upon request from RBS Equities or on our website www.rbs.com.au/warrants

RBS Group (Australia) Pty Limited is not an Authorised Deposit-Taking Institution and these products do not form deposits or other liabilities of The Royal Bank of ScotlandN.V. or The Royal Bank of Scotland plc. The Royal Bank of Scotland plc does not guarantee the obligations of RBS Group (Australia) Pty Limited.

© Copyright 2009. RBS Equities. A Participant of the ASX Group.

Explanation of Warrant Tables

Security – refers to the code ascribed to the warrant, ExDate – refers to the date on which the warrant expires or is reset, ExPrc – refers to the exercise price, or second

instalment payment, CP – tells you whether the warrant is a call or a put, ConvFac – the conversion factor of the warrant which tells you how many warrants you need to

exercise in order to take possession of 1 share, Delta – tells you how much the warrant will move for a 1c move in the underlying security, Description – Tells you the typeof warrant.

All charts taken from IRESS unless indicated otherwise