rationale of consumer behavior in organized retail...

TRANSCRIPT

Chapter 5

Rationale of Consumer Behavior in Organized

Retail Outlets

5.1 Introduction

5.2 Factors Affecting Consumer Decision Making

5.3 Indian Retail Sector and Changing Consumer Behavior

5.4 Retail Consumer Behavior and Role of Services in Retailing

5.5 Theories of Consumer Behavior

5.6 Primary Data Analysis of Dimension of Consumer Behavior

5.7 Summary of the Observation

5.8 Testing of the Hypotheses

5.9 Conclusion

219

Chapter 5

Rationale of Consumer Behavior in Organized

Retail Outlets

5.1 Introduction

The retail sector in India is witnessing a huge revamping exercise as traditional

markets make way for new formats such as departmental stores, hypermarkets,

supermarkets and specialty stores. Western-style malls have begun appearing in

metros and second-rung cities alike introducing the Indian consumer to a shopping

experience like never before. The sector is at an inflexion point where the growth of

organized retailing and growth in the consumption by the Indian population is going

to take a higher growth trajectory. The Indian population is witnessing a significant

change in its demographics. Organized retail is on all time high in India. The growth

is boosted by various factors such as availability of professional practices, media

proliferation, various brands which are gaining value thereby enhancing industry

growth, availability of various funding options, regulations like VAT implementation

to make processes simple, sea change in demographics of country and international

exposure.

The retail sector is one of the fastest growing ones in India, catering to the world's

second largest consumer market. The Indian consumer market is estimated to grow at

13 percent annually from $322 billion in 2006-07 to $590 billion in 2011-12.

Organized retail, which constituted a low 4 percent of total retail in 2006-07, is

220

estimated to grow at 45-50 percent per annum and attain a 16 percent share of the

total retail market by 2011-12302

.

Consumer behavior is defined as “The dynamic interaction of affect and cognition,

behavior and the environment into which human beings conduct the exchange aspects

of lives”. IT means that the buying habits of the consumer are greatly affected by their

thought process and their feelings experienced. Human beings are greatly influenced

in their buying actions by various factors like opinion of others, marketing stimuli like

product, advertising, packaging and product appearance.

Consumer buying behavior refers to the buying behavior of the ultimate consumer.

Consumer behavior is the understanding of how consumers make decision to use their

resources such as time money and effort for buying using and disposing goods and

services .the behavior of humans as consumers is complex. Marketers understanding

of the drivers of consumers buying behavior will help them to service their customer

effectively and efficiently and attract new customers. It is very important and required

to understand customers shopping behavior with regards to retailing this includes

decision variables regarding brand selection shopping timing and choice of retail

format and store.

Traditional demographic variables cannot clearly identify the complete characteristics

of an evolutionary retail market, as consumers in the same demographic group have

diverse psychographic makeup. Therefore, psychographic factors influencing

consumer behavior have to be understood more closely by organized retailers.

Further, organized retailing itself has a tremendous influence on consumer behavior.

Thus, consumer behavior and organized retailing have reciprocal influences on each

other.

So far, the prominent organized retail sector players have been largely restricted to

urban areas. In fact, their emergence and growth has been phenomenal in metropolitan

cities and in other large cities. However, of late, organized retail has started making

302

Ghosh Dastidar Surajit and Datta Biplab., Demographic Differences in Consumer Exploratory

Tendencies: An Empirical Examination, IIMB Management Review, Vol. 21, No.4, pp. 297-312

2009.

221

inroads even into smaller cities. Infrastructure constraints, huge distribution costs

owing to large geographical area, fragmented market, and absence of national

distribution nodes and networks, are the main limitations faced by organized retailers

today in India.

5.1.1 Indian Consumer Behavior

The Indian consumer has undergone a remarkable transformation. Just a decade or

two ago, the Indian consumer saved most of his income, purchased the bare

necessities and rarely indulged himself. Today, armed with a higher income, credit

cards, exposure to the shopping culture of the west and a desire to improve his

standard of living, the Indian consumer is spending like never before. Organized retail

with its variety of products and multitude of malls and supermarkets is fueling his

addiction. His new mentality, in turn, is fueling the growth of organized retail in

India.

Some of the features characteristic of these consumers is their tendency to borrow

money in order to buy the upscale items – contrary to the traditional line of thought

that Indian consumers are indisposed to credit. But these consumers not only have

price and quality on their minds but also the fact that their brands effectively reflect

their local environment and are consonant with their life style. And this is where the

foreign multinationals coming into the Indian consumer market has to pay attention.

Selling global brands in India at global prices is a road to perdition. Companies who

have tailored their products to the Indian environment and customer have reaped high

rewards.

At the same time, Indians will find it hard to give up their old habits of shopping at

the local corner-store or buying goods from the street-vendor. The next section

describes the unorganized and organized retail sectors in detail. It is critical to

understand these sectors individually to speculate about possible the nature of

interaction between them. While the traditional form of retail in India is sure to suffer

a setback from the entry of large organized retailers, it is possible for both forms to

222

co-exist serving the new personality and old-habits of the Indian consumer

simultaneously.

The retailer in order to stay in the market and face the competition he should

understand consumer shopping behavior. This is possible by analyzing the factors that

affect behavior. These factors could be demographic, psychological, environmental or

related to the lifestyle of the customer. The retailer also needs to identify the various

stages in the customer decision making process and the major influence stage. To

understand the concept from the 1950s to 1980 Indian shoppers were used to shop at

Haat, Mandis, Melas and at small family run stores kirana shops. After liberalization,

privatization and globalization Indian government lifted the restrictions from private

companies and Indian economy slowly progressed from being state-led to market

friendly. This was the beginning of modern India. The growth of middle and higher

middle class, growing trend of call centers and BPO, increasing number o dual

income nuclear families, convenience of shopping from one place to another,

reasonable pricing and a good place to pass the time fuelled the growth of

supermarket, hypermarkets and concepts of organized retailing in India.

223

Figure 5.1

Consumer Behavior Model in Changing Retail Scenario

5.1.2 The Need for Studying Consumer Behavior

The key challenge faced by the retailer is creating products and services which would

be successful in the market. An accurate understanding of consumer need helps the

retailer create product that is likely to be successful in the market. Understanding

consumer buying behavior is the starting point of strategy creation. The understanding

helps in determining the channels of communication, proving consumer knowledge

which can help a firm assess how well it has achieved its product positioning goals.

The firm with the help of studying consumer behavior tries to see how its products are

perceived, whether there is a good match or not and then to consider the positioning

strategy deemed a success.

224

The retailer should know the consumers, because it is imported to know how, when

and where the customers use the product or service that the retailers sell. When the

retailer understands consumer behavior he is able to make an objective analysis of

internal strengths and weakness. This analysis may reveal certain startling facts and

provide direction for future differentiation strategies.

5.2 Factors Influencing the Behavior of the Consumer

The behavior of retail consumer is a subject of study across the world.

In India retailers and retail formats are evolving on a great extent. Understanding the

reasons for consumer‟s behavior is very important for retailer. Following are the

factors which influence the customer‟s decision making process.

1. Range of Merchandise: The range of merchandise is perhaps the most important

reason for customers to patronize a particular outlet. The initial curiosity of the

store may draw a consumer to a retail store, but converting him into a buyer and

retailing him over a period of time is largely dependent on the quality and the

range of merchandise offered by the store. The range of merchandise offered

plays an important role in case of categories like devalues, books and music.

2. Convenience of Shopping at a particular outlet: The element of convenience is a

fast gaining promises in the world of organized retail. This is especially true in

case of items like grocery/fruits and chemists. For example, while buying

medicines, most patients would prefer the buy from the chemist near the doctor

clinic or near the hospital.

3. Time to travel: The time required to reach a particular retail location is again

fast becoming critical. This is very much relevant in cities or metros like

Mumbai, where travel time is high. This has resulted in many local areas

developing in terms of shopping to facilitate buying.

4. Socio economic factors: Socio economic factors are seen as a fundamental to

development. India is a nation which has a large middle class a youth population

225

which is happy spending and a steady rate of growth of G.D.P. The Socio-

economic background of the consumer largely determines his lifestyle.

Consumer buying behavior varies from market to market and is largely

influenced by the culture of the region. This can be explained with the help of an

example. That is a culture of Asia is different than Western Culture, therefore

accordingly consumer behavior also shifts. The retailer needs to understand that

the need hierarchy is different for each market.

It is important for the retailer to consider socio economic change in a geographic

region over a period of time as it is indicator of the facilities available at various

levels and the quality of life of the population this would indirectly be related to the

spread of organized retail. The primary indication of socio economic change is the

increase in life expectancy from 58 years in the year 1991-92, to an average of 66

years in 2006-07. India aims to achieve 100 percent literacy (within the age group of

15-35) by the year 2006-07, there also likely hood that the basic amenities like

drinking water and electricity will be available and this will result in the improvement

in the basic quality of life of an average Indian citizens and when basic necessities are

being taken care there is good change that the demand for other products and services

may increase.

The researcher in order to understand whether the developments of organized retail

outlets have changed the consumer behavior conducted a primary research of 723

consumers in Mumbai and categorized them into different age group. The results are

put up in the table 5.1 and also the graphical representation in Graph 5.1.

Table 5.1

Organized Retail outlets and change in consumer behavior

Sr.No Age

Total 15-25 25-35 35-45 45-55 > 55

1 Yes, very much 188 74 23 10 5 300

2 Yes, to some extent 155 111 65 34 5 370

3 No not at all 25 8 5 13 2 53

Total 368 193 93 57 12 723

Source: Compiled from Primary data.

226

Graph 5.1

Organized Retail outlets and change in consumer behavior

Table 5.1 and Graph 5.1 give a clear indication that the development of organized

retail outlets in Mumbai has changed the behavior to a great extent. Major impact

could be seen in the age group of 15-25 with 188 respondent having a feel of very

much and 155 feeling that the impact has been to some extent, further it has been seen

that respondents between the age group of 25-35 also feel the same but the number

differing 74 respondent feel the impact is very much and 111 respondent feel the

impact is to some extent. The analysis states that the young and middle a consumers

are greatly influenced by the growth of organized outlets.

5.2.1 Stage of the Family Life Cycle

The stage of the family life cycle that customer belongs to and also it largely

influences his needs. For example, the needs of a young bachelor will be different

from the needs of an elderly retired couple. Therefore the retailers need to be clear

about the market that he is catering to as he cannot be everything to everybody.

Demographic factors

Demographic factors are unique to a person. It involves identification of who is

responsible for the decision making or buying and who is the ultimate consumer. All

stores have focused themselves on respective segments based on factors such as age,

income, family, size, gender, occupation, etc.

227

Psychological factors

Psychological factors refer to the inner aspects of an individual. An understanding of

consumer‟s psychology guides the retailers segmentation strategy consumers respond

differently towards the same retail marketing due to their respective motives,

personality, level of involvement and attitude.

Motives : motivation is prerequisite for any action which includes buying .it

stimulates the need

Perception: perception is the process by which consumers attach meaning to

incoming stimulate by forming mental pictures of persons, place and objects.

Stimulates reception is accomplished though the fire senses that is sight,

sound, taste, touch and smell. The consumer feels that what he/she sees hear,

feel , taste and small is what they get

Learning: learning is the process of acquiring knowledge through past

experience. When a consumer visits a store and the treatment he receives will

be criteria for repeat visits to the store. if the experience with the sales team

was good then the consumer may visit the store even if the goods are slightly

expensive.

Tree sampling/ treats are also ways of making the consumer learn about a

product and its attributes. A retailer must encourage a consumer to touch and

feel the product so that his visit could turn in to a buying experience. It‟s been

seen that most new format retailers have benefited on touch, feel, and

experience concept which results in real learning process.

Environmental factors: Environmental factors are both physical and social

factors. This includes physical objects (goods and outlets) spatial relationship

(location of shopping center and merchandising stores) and social factors

(reference groups and opinion leaders). The environmental factors influence

consumer attitude learning motives etc. which in turn influence affective and

cognitive responses and therefore shopping behavior and the individual.

228

Social class: social class is referred to as the classification of members of

society into a hurrah of distinct status and class. Social class is measured by

variables such as education occupation, wealth and ownership of assets.

Market research has established a link between social class and consumer

attitudes concerning shopping behavior. Middle class and higher sections of

society prefer to shop for grocery items once a month from a particular shop.

They usually prefer stores offering variety and range of choice perplex sectors

of society usually purchase on a daily bases. Social statues of an individual

play an important role even in determining the frequency of purchase. It‟s

been seen that majority of the middle class consumers prefer to buy vegetables

in the morning for their freshness despite the prices being on the higher side

on the contrary the louder end sections of the society prefer to buy at late

evening to get benefits of low prices

Lifestyle: lifestyle refers to an individual‟s way/style of living as determined

by his/her activities, interests and opinions. Lifestyle is considered to be

highly correlated with consumer‟s values and personality traits. An

individual‟s lifestyles is influenced by the social group be belongs to and his

occupation.

5.2.2 The Customer Decision Making Process

The need for a product or services starts generally at the time when the need for the

particular product or service is recognized. The need may be psychological or

fictional. Psychological needs are associated with personal satisfaction that the

customer may get from purchasing or using the product. The functional need is

directly related to the function of product. The functional need is directly related to

the function of product. Then comes a stage where consumers seek information about

the product and the place where he can make the purchase.

Therefore it is seen that in the world of relating consumer passes through five distinct

stages to complete his buying process which are as follows.

229

Figure 5.2

Customer’s decision making process

Depending on the criteria important to consumer he evaluates the various options

available and narrows down the choice to a few stores where he may make the

purchase. He also to make sure his buying decision may visit couple of stores

Stage: I Identification of need for the product or service

The buying process begins when the consumer becomes aware or realizes that

they have some unsatisfied needs. The unsatisfied need arises when the customers

desired level of satisfaction. The consumer through his previous life‟s experience

knows how well he can satisfy these unmet needs like hunger, thirst and shortage of

clothing.

Need recognition in most cases is straight forward when individuals find shortage of

something or goods required are of daily use. For example, there is no wheat/milk in

the kitchen. A need may be aroused by an external. Stimulus such as deserve to visit a

part of a store while purchasing other usual items.

230

Stage: II Information search

The 2nd

stage is gathering information on how to solve the problem is the consumer

look for the possible options to resolve the need in consideration. Information search

is a process where the prospective buyers examine their environment for appropriate

information to make a sound decision .this search may be external (from memory) or

external (through friends, family, published sources salespersons, and the internet) an

individual usually drives or acquires information from the sources namely internal

and external. Persons past experience accompanied with shopping exposure might

provide him with substantial guidelines to make the correct decision with the help of

his or her internal memory. Consumers invest time in information search in

preparation to the perceived risk associated with the particular purchase and

importance of purchase.

Stage: III Evaluation of alternatives

After information search for the required product the consumer is expected to take a

final decision on one of the choices. The search also helps the consumer to acquire

knowledge about the criterion to be used to evaluate the various alternatives involved

at the information stage. To justify this point in gurgoan some management students

in order tie find out best option enlisted the following restaurants for entering friends

a) Haldi ram

b) Nirulas

c) Mc Donald‟s

d) Pizza hut.

The alternatives which are actively considered during the consumer decision making

process constitute the individual‟s evoked set. The evoked set comprised retail outlets

already in the memory and distinctly added from the retail environment (i.e. mass

media, friend) with respect to a particular product purchase.

It is essential for all the retailers or marketers to ensure that their brand finds place in

the consideration set of the target segment retailers require an effective marketing

231

programme, especially in terms of their communication strategy in order to informed

position the store as per the needs of the target segment. At the same time retailers

need to revise its offering and attributes as per the changing preferences of their target

segment. After evaluating or rating various alternatives or importance attributes an

individual can shortlist the best possible retail outlet (an eating joint for taking his

friends out for a treat).

Stage: IV Purchase decision

After evaluating various alternatives an individual is in a position to focus on the

preferred product category, good retail outlet or brand. This followed by a purchase

decision by the consumer final choice from multiple alternatives leads to the purchase

stage or decision. This involves an exchange of cash or credit note for the ownership

or usage of offering. It is this purchase stage that generates revenue for the retailers

and the marketers in the value chain.

In the retailing content the purchase stage plays the most important role in consumer

decision making with regard to place of shopping. in the Indian context one can

obtain many products from multiple retail outlets or formats.

Stage V: Post Purchase Dissonance

After purchasing a particular good or service or visiting outlet consumers evaluate its

performance against their expected level of satisfaction on account of important

attributes.

Example: When a consumer visits a multiplex theatre he/she is expected to examine

the experience on account of sound effect, air conditioning efficiency, other consumer

behavior, etc.

This kind of evaluation is likely to lead to three possible outcomes:

1. Actual performance meets expectations leading to a neutral response. Hence

the individual may like to evaluate it further.

232

2. Performance exceeds expected levels, resulting in satisfaction. This may lead

to repeated purchase and positive word-of-mouth publicity.

3. Performance may fall short of the expectations, resulting in dissatisfaction.

This may lead to discontinuation of purchase of the particular good or from

the retail outlet.

Therefore in case of Post Purchase evaluation, the basic concern of the consumer is to

reassure himself that he or she has opted for the best available option from amongst

various alternatives. This helps the consumer to minimize the Post Purchase cognitive

dissonance.

5.2.3 Emerging Patterns in Organized Retailing in Relation to Consumer

Behavior

The patterns of organized retailing in India and their consequential reciprocal

relationship with consumer behavior can be observed through a deeper insight into the

Indian market there exists two type of shopping which analyses the consumer

behavior as mentioned below:

1. The hedonic shopping value differs across product categories and also in case

of consumables and durables.

2. Utilitarian shopping has started giving way to hedonic shopping'! With the

emergence of organized retailing. Yet, the majority still prefers utilitarian

shopping.

3. Add-on features in modem retail stores have an insignificant impact on actual

sales conversion, as majority of the consumers still prefer 'value for money'

while shopping.

4. Retail service quality has assumed the central role in shaping the consumers'

perception, sales conversion rate, and repeat sales and overall shopping

satisfaction.

233

5. Socio-cultural differences, coupled with other demographic and psychographic

factors, are influencing buying behavior and choice of the store even after the

emergence of egalitarian shopping malls.

5.3 Indian Retail Sector and Changing Consumer Behavior

The Indian retail sector is still predominantly unorganized. However, organized retail

units are fast emerging and becoming the preferred choice of consumers, especially in

urban areas. This development is attributed to a number of factors. Firstly, economic

liberalization has facilitated the entry of multinationals into the cash-and-carry

business and single brand retailing.

Multinational companies are also taking advantage of India's low-cost labor and raw

materials to make India a sourcing hub, as well as a market for their products.

Secondly, increasing income levels and a growing sense of brand consciousness

among India's middle and higher income groups have led to increased popularity of

organized retail units.

The changing consumer behavior is increasingly shaping organized retailing and is, in

turn, evolving with new found options and opportunities. On the socio-cultural side,

the growing number of nuclear families, general improvement in education levels and,

most importantly, continuous rise in women's economic independence through jobs,

as well as entrepreneurship, has made women play a more proactive role in shopping

for the family. This has led to an increasing number of customers availing of

convenience options such as super markets, where most of the shopping for daily

necessities can be done under one roof.

Changing income levels and occupation have resulted in a change in the consumer‟s

buying behavior. More urban women are seeking employment resulting in dual

income families. This results in more disposable income that in turn spawns

consumerism. Moreover, in households with working women there is greater work

pressure and increased commuting time resulting in adjustments being made to the

food habits (cooking vs. ready to eat) as well as clothing. The focus shifts to

234

convenience and comfort. The size and composition of the shopping basket has

changed over time. Today‟s consumers are looking for shopping convenience and

want to have all their requirements under one roof, coupled with speed in the retail

store operations. Due to time constraints, families are now looking for

„shoppertainment‟ – combining shopping with entertainment. This is one of the causes

of increased footfalls at malls with multiplexes.

As India moves into modern retailing with several changes with regard to its markets,

bands and consumers there are unique challenges that a multinational company

entering India has to cope up with, whether it is a fast moving consumer goods

(FMCG) company or a multinational retail chain like Tesco or Wal-Mart. There are

unique retailing aspects that need to be studied in detail by these companies. While

the world over the retail density (number of shops per 1000 consumers) is on the

decline, the retail density in India is on the increase. This is because of the fact that

small neighborhood shops called kirana shops about eleven million in India.

They have been a part of the Indian shopping culture for several decades and even

toady organized retailing (modern retail outlets) contribute just 2-3 percent of the

total retail sale in the country. Point of Purchase (POP) materials are used both by

kirana shops and by organized supermarket retail outlets. This study investigates the

impact of POP materials on kirana shop purchases and the purchases of consumers

from supermarkets. Given the importance of POP material on the purchase of FMCG

purchases, the authors feel that this study will be useful to bridge the gap between

theory and practice and will provide valuable insights to managers involved in

retailing.

Reciprocal Influence of Organized Retailing on Consumer Behavior

Consumer choices and preferences and overall consumer behavior have always played

an important role in shaping market trends and have thus influenced the evolution of

organized retailing in India. However, after reaching a specific stage of development,

organized retailing has also started influencing the way the consumers look at the

market, not only in terms of choice of products and services, but also in terms of the

235

overall shopping experience. Enhanced shopping experience, better packaging,

hygienic environment and value added services rendered by organized retail stores

have raised the expectations of even those consumers who frequent traditional kirana

stores. In response, many of the traditional stores in the unorganized sector have

reinvented themselves and adopted better practices in product packaging, visual

merchandizing and display, etc. In turn, many organized retailers are resorting to

selling below the maximum retail price, providing home delivery and implementing

loyalty programs, as strategies for survival.

While unorganized retailers have started reinventing themselves due to the inroads

made by organized retailers, the organized retailers on their part have realized the

importance of the personal touch provided by traditional kirana merchants and have

begun offering personalized services, trying to strike a lasting relationship with their

customers through membership cards, and intimation regarding bargain offers through

SMS, etc.

The dramatic changes in consumer behavior have necessitated made it imperative for

marketers to have in-depth knowledge about various dimensions which link retailing

and consumer behavior. For instance, McDonald's found that a sizeable percentage of

its customers decide about eating and the choice of restaurant at the last moment. It is,

therefore, opening small outlets in popular shopping areas and malls, in places with

high traffic density and at airports. It is also providing play areas to ensure that

families visit its outlets along with children.

McKinsey Global Institute, in association with the Indian Council for Research on

International Economic Relations (ICRIER), brought out a study report titled, "The

Bird of Gold, The Rise of India's Consumer Market". This study attempted to analyze

the rise of the Indian consumer market and its influence on consumer spending, their

buying behavior and the overall economic development of the country. ICRIER also

conducted a comprehensive study titled, "Impact of Organized Retailing on the

Unorganized Sector". This study brought out the emerging patterns of organized

retailing and identified the possible impact on consumers, intermediaries and

manufacturers. It also made some policy prescriptions in this regard. It can be

236

summarized that a precise understanding of consumer's choices and preferences is the

key to success in the changing milieu.

Redefining Retailing and Consumer Behavior

During recent years, the entire concept of retailing has been redefined in terms of both

its structure and also the fundamental changes in consumer behavior on account of

demographic, psychographic and socioeconomic factors. The changing pattern of

consumer behavior is influencing retailing in India, especially organized retailing. As

a matter of fact, personal and social factors such as needs, perceptions, attitudes,

interests, opinions, activities and lifestyles mostly influence consumer behavior in a

rapidly changing retail environment. Traditional demographic variables cannot

identify the complete characteristics of an evolutionary retail market, as consumers in

the same demographic group have diverse psychographic makeup. Therefore,

psychographic factors influencing consumer behavior have to be understood more

closely by organized retailers.

Today, retailing is much more than mere merchandising. It is about reflecting

customer desires and aspirations, and forging long-lasting relationships with them. As

the Indian consumers evolve, they expect much more each time they step into a store.

The concept of shopping has undergone a change in terms of format and consumer

buying behavior, ushering in a revolution in shopping. Retailing is going through a

transition, not only in India, but the world over. For a long time, the comer grocery

store was the only choice available to the consumer.

This has given way to international formats of retailing. The traditional food and

grocery segment has seen the emergence of supermarkets and grocery chains. The

non-food segment in organized retailing has extended itself into various formats and

categories where it has been largely successful.

The research showed that today‟s savvy consumers demand increasingly creative and

more importantly interactive strategies, to entice them into stores. Discovering what

makes consumers tick and buy from certain stores can perhaps be achieved by

returning to more traditional retail methods that allow the consumer to participate or

237

interactive with the seller on a more personal level or implement new technology that

streamlines the purchasing process as smooth and painless as possible.

Staffing is also an area that can make or break consumers‟ retail experiences.

Obtaining the right balance between being overbearing and non-existent staff is

difficult but vital to creating a good store image and something that consumers

believe is still not being got right. Personal service and not being held in a queue is

something that we have gotten used to on the internet. Self-service options, which are

becoming standard in many of the major supermarkets, go somewhere toward

achieving this.

Influence of situational variables on shopping behavior

A shopping situation is a particular act of Buying Behaviour occurring at a specific

point in space and time. This can be explained with the help of following examples:

A customer seeking service at the Lakme beauty parlours – these parlours are open to

customers on all the seven days of a week, from 10 am to around 7 pm, in the midst of

soft lights while the strains of sarange and sarod soothe the customers frayed nerves

which is simply a behavior setting. The situation serves as an interface between the

person (salon consumer) and the stimulates object (beauty treatment such as facial

pedicure etc) and all those factors defining that interface constituting situational

variables.

Situational variables refers to all those factors particular to a time and place of

observation which do not follow from a knowledge of personal (intra-individual) and

stimulus (choice alternatives) attributes.

These attributes range from store location and layout to time of day and the presence

or absence of others.

These are classified into four distinct dimensions of situational influence.

238

Figure 5.3

Dimensions of Situational Influence

1. Physical Setting: The physical setting covers geographical location of the retail

but might equally be seen in terms of the environment in which the consumer

reads a catalogue or access a shopping centre and a particular store.

Shoppers are categorized in the following manner:

1. The shoppers who travel for half an hour or more are considered – Far

shoppers.

2. The shoppers who travel for less than half an hour are considered – near

shoppers.

3. The shoppers who usually shop before 3 pm are designated as – early

shoppers.

4. The shoppers who usually shop after 3 pm are designated as – late shoppers.

It is also seen that there is influences on consumer behavior resulting from

environmental conditions such as weather or climate, placement of merchandise,

access to information in a store and background music or color scheme.

2. Social Setting: The social setting describes the presence or absence of others

together with their social role attributes and opportunities for interaction.

Therefore it encapsulates everything – security staff in the shopping centre or

239

store, opportunities for interaction with sales staff, friends or relatives

accompanying the consumer on the shopping trip and even to proximity of other

customer present in the store or service scope. The shoppers who are accompanied

by other people are considerate to be social shoppers; those who are

unaccompanied are designated solitary shoppers.

3. Temporal Aspects: Temporal aspects are very important elements that affect the

situational variables. Time of day and constraints upon time available for

shopping are variables with very obvious effects on buyer behavior.

For example: Milk is purchased from vendor or retail outlets by most of the

people in India in morning hours or evening hours.

Women prefer shopping in post lunch hours after attending to their children and

returning before the rest of the family reaches home.

They‟re taking into consideration the above factors, the retailers open their shops

in accordance to shopping hours of their target segments. Shoppers who spent

hours less than an hour was considered were considered to be “quick shoppers”

and those who spent more than one hour or more were designated as “slow

shoppers”.

4. Task Definition: Task definition is more individual specific and encompasses

cognitive and motivational indications of the shopping situation, effectively

capturing situational influences on the task definition, information search and

evaluation stages depicted in traditional consumer decision making models. The

difference in the degree of information processing behavior varies for practical or

hedonistic products, products for self consumption versus gift purchases for others

etc.

Therefore the sound understanding and importance that is given to the influence of

situational variables in devising the retail marketing mix will ensure the effective and

profitable output to the retailers. It is also seen that the consumer image of a retail

outlet plays an important role in determining the nature of shopping behavior, it is

240

also important to understand the factors that affect the image formation of retail store

along with the process of its formation.

5.4 Retail Customer Behavior and Role of Services in Retailing

In marketing there exists both the customer and the shopper. Customer is someone

who buys from the retailers and the shoppers are the ones who buy from the retailer.

Example: Window shoppers who spend time in the retail outlets just looking at the

products but with or without any real intention for buying.

It‟s a belief that consumer has time constraints and therefore wants everything at his

disposal and in spite of internal making inroads in the shift of shopping behavior but

majority of the consumers still prefers to purchase through stores.

Stores remain popular because of the following basic reasons:

1. Need to touch and feel the product prior to buying

2. It allows social interaction and the opportunity to compare brands at one place.

3. It initiates impulse buying by the look and physical feel of the product such as

chocolates snacks and

4. Consumers also look for ambience and convenience in shopping.

5. Customer‟s money drives the economy and retail is where consumers spend

their money such as in boutiques, restaurants discounts stores and e tailors.

6. Consumer shopping behavior can be understood analyzing factors such as

demographic, psychological or the lifestyle of the consumer.

Retailers are required to have better understanding of consumer benefits their

perceptions and attitudes and how they influence the development of successful retail

marketing strategies. Effective retailing requires an appreciation of the buying

behavior of consumer.

241

It‟s important that retailers must understand their consumers better so that they can

both respond to and anticipate their needs proactively.

The following are some major criteria for the right approach to a customer‟s

requirements:

1. Creating the right environment.

2. Listening to customers

3. Providing rewards to frequent buyers.

4. Realizing the lifetime value of a customer and ensuring loyalty. The concept

of life time value customers is employed in relationship building and

marketing.

5.5 Theories of Consumer Behavior

The most fruitful approach to an understanding of retail demand is to identify and

evaluate the broader theories of consumer behavior linked to purchase behavior. The

discipline of consumer behavior has borrowed a range of concepts from the

quantitative and behavioural sciences in order to generate integrated models of action.

Theories can only be assessed on the contribution they make to our understanding of

the purchase process.

Models of behavior are useful means of organizing dispatch bodies of knowledge

regarding social action on somewhat arbitrary yet plausible process of intervening

psychological, social economic and behavioral variables. The early models were;

1. The Engel-Kollat Blackwell (EKB) model (1986)

2. Howlard and Sheth (1969)

3. Nicosia (1966)

These models can be found to share several commonalities:

242

1. They all exhibit consumer behavior as a decision process.

2. They provide a comprehensive model for focusing mainly on the behavior of

the individual consumer.

3. They share the belief that behavior is rational and hence can in principle be

explained.

4. They view buying behavior as purposive, with the consumer as an active

information seeker- both of information stored internally and of information

available in the external environment. Thus the search and evaluation of

information is a key component of the decision process.

5. They believe that consumers limit the amount of information taken in and

more over time from general notions to more specific criteria and preference

for alternatives.

6. They all include a notion of feedback that is outcomes from purchases will

affect future purchases.

I. The Engel-Kollat-Blackwell (EKB) model

The Engel-Kollat-Blackwell (EKB) model has been widely referenced and is

acknowledged as one of the most comprehensive explanations of consumer behavior.

The original model has undergone three major revisions since 1968 and the current

model. While retaining some of the fundamentals has become more sophisticated in

definitional and explanatory aspects and therefore varies from the original version.

The EKB model takes a broad view, incorporating inputs such as perception and

learning. A key feature of the EKB model is its incorporation of the differences

between high and low involvement as part of the buying process.

High involvement is normally present in the decision making process when the

perceived risk in the purchase is high. This element of risk is higher when the

consumer is unsure about the outcome of his or her purchase decision. This arises

when:

243

a. Information is limited

b. The buyer has low confidence.

c. The price relative to income is high

This has obvious connections to demand Engel, Blackwell and Miniard (EBM) in

1986 stated that limited problem solving (LPS) activity takes place when there is little

perceived risk that a wrong decision will be made.

The EKB model has the decision process as pathways of convergence passing through

various stages of processing prior to any choice being made.

II. Sheth’s family model of behavior

The Purchase decision process quite often is investigated in terms of the individual. It

is clear that for the purchase of high price items the decision process involves a high

level of risk that the decision may be a poor one. It also often involves the preference

resolution of more than one individual. This creates a complex situation whereby,

more often than not, the purchase has to satisfy the divergent needs of the group.

Within the theory of family buying behavior there is a concept of role structure, that is

among individual members of the family takes on roles such that collecting

information, deciding on the available budget etc. the family can make any ways its

final decision but it has to be realized that the dealing is with a homogenous unit, but

with a collection of individuals with different roles, needs modules and interest.

The Sheth model of the family decision process provides one of the few examples of

an attempt to replicate the behavior of group decision making. There exists a problem

with Sheth model and that is every aspect of search modules, believes and

prepositions occurs in tandem with each member of the group prior to their being a

resolution of the group to a final decision and thereby a joint or autonomous outcomes

occur.

244

5.6 Primary Survey of Consumer Behavior

Indian consumer markets are becoming increasingly complex and competitive. The

internationally known brands, modern retail outlets, and increasingly discerning

consumers have made the markets very sophisticated. Demands for goods and

services are changing very rapidly these days. The higher income, socio-economic

changes, and the growing national population are the most important trends that will

affecting the market in this decade. Also, consumer life styles and preferences are

changing, which have created a wide diversity of consumer demand. With these

changes, retailers will have to redefine their marketing strategies in order to compete

and preserve market share. Consumers are now exposed not only to higher levels of

information about the offerings of competing supermarkets, but they are also faced

with a larger number of choices from which to pick out their “best buy”. Therefore, it

is necessary for the retailers of supermarkets to know about consumers‟ choice

processes and to understand the major determinants of store patronage. The primary

question before the retailer is: How do consumers make store choice decisions? A

retailer‟s success is said to be tied to his focus in customers. Retailers need to

understand which factors influence the customers to purchase in their stores. They

must give these customers a legitimate reason to shop in one particular store over

another, and one of the ways to do this is to look at the customer‟s needs and wants.

Retailers need to examine such basics as what they offer the customers in the way of

time, service, selection, quality, value and confidence. A deluge of research reports

and diverse data appearing on the changing consumer behavior in globalised India in

newspaper, magazines, journals and also the views of various academicians have been

expressed in various seminars and conferences. This raised a curiosity in the mind of

the researcher to study the volatile consumer behavior. The researcher selected

Mumbai region because of the rapidly changing face of the urban market,

mushrooming of malls in this metropolitan city, the researcher also understood the

fact that changes take place first in Mumbai being a commercial capital of India.

Retail executives are increasingly aware of the diversity in the patterns of shopping

behavior among consumers. This diversity has been accompanied by a shift in the

channel power relationships in the distribution of goods and services. Both the

245

diversity in the pattern of shopping behavior and the power shift has encouraged

researchers to focus more attention on patronage behavior in an effort to understand

the consumer better.

The study basically focuses on the organized retail outlets and its impact on the

consumer behavior. The term consumer behavior has wide connotations and the study

covered broad areas related to consumer‟s perception, consumer‟s preference their

buying behavior etc. The researcher in order to find out this targeted few categories

such as age status, marital status, employment status and gender. The main objective

was to find out the changing consumer behavior their familiarity with regards to

organized retail outlets and the impact of these outlets on their budget and on the

unorganized retail outlets. Since Mumbai metropolitan city has a huge population

therefore the researcher took limited sample size of the population. The researcher in

spite of taking limited sample size tried to show the necessary impact on consumer

behavior in the near future.

Profile of the respondents

The total number of respondents selected was seven hundred twenty three for the

entire Mumbai region. The detail of the sample is as below which is distributed age

wise.

Employment status of the respondents

The researcher made an attempt to ascertain the employment status of the respondents

first. A total of four categories were made, namely, business, service, self

employment (which included people associated with professions like health and

beauty parlors classes) none employed, this category mainly included housewives and

students. Since the researcher selected the sample on random basis, it became

essential to ascertain the employment status and on the basis of which the responses

of the respondents could be categorized.

246

Table 5.2

Employment Status of the respondents

Sr.No. Categories Respondents Percent

1 Self Employed 62 8.6

2 Service 331 45.8

3 Business 64 8.9

4 Retired 51 7.1

5 Not Employed Currently 169 23.4

6 Housewife 46 6.4

Source: Compiled from Primary data.

Graph 5.2

Employment Status of the respondents

Table 5.2 and Graph 5.2 give a clear indication of the category of population residing

in Mumbai. Out of the 723 respondents it‟s been found that maximum population

belongs to the service class, sixty two belongs to the self employed group sixty four

belongs to the business class and further there has been evoked a category who are not

employed currently with forty six respondents . This category mainly consisted

children and housewives. Therefore it could be seen that it is service class employees

with regular monthly income who gets influential with organized retail outlets.

247

Profile according to the Annual Income of the respondents

Another area that was keen to study by the researcher was that annual family income

of the people. This was divided in the ranges, from Rs. one lakh to Rs. ten lakh and

above as given in the table. The researcher conducted this study to understand the

category of people visiting the organized outlets in Mumbai.

Table 5.3

Annual Income of the respondents

Source: Compiled from Primary data.

Sr.No. Categories Respondents Percent

1 1-3 Lakh 289 40.0

2 3-5 178 24.6

3 5-7 74 10.2

4 7-9 49 6.8

5 10 & above 133 18.4

Total 723 100.0

248

Graph 5.3

Annual Income of the respondents

Table 5.3 and Graph 5.3 project information about annual income of the respondent.

Since maximum population belong to salaried class and followed by a combination of

self employed and business class it has been seen that there is a tilt between one and

five lakh there also has been an increase in the income range from ten lakh and above

with one hundred thirty three respondents falling into the category.

Visit to Organized Retail Outlets

The researcher in order to understand the shift in consumer behavior was keen in

knowing their visit to the organized retail outlets. In order to get a clear view the

researcher further divided it in the categories of age, marital status, gender and

annual family income. The results found gave an interesting scenario of the Mumbai

based consumers.

249

Table 5.4

Visit to Organized retail outlets as per age group

Sr.No Age Number of Respondent

yes No

1 15-25 264 104

2 25-35 165 28

3 35-45 86 7

4 45-55 52 5

5 > 55 7 5

Total 574 149

Source: Compiled from Primary data.

Graph 5.4

Visit to Organized retail outlets as per age group

Table 5.4 and Graph 5.4 give a clear view of the respondent belonging to the different

age group visiting to organized retail outlets. The researcher was keen in knowing the

age group who visit the organized retail outlets maximum. The results put up gives a

clear view that 264 respondent of the age group 15-25 165 respondent of the age

group 25-35 and 86 respondents of the age group 35-45 visit the organized retail

250

outlets the maximum stating that it is the teenagers and the young adults who prefer

organized retail outlets the maximum. Further the senior citizens with 7 respondents

still prefer to visit the traditional outlets. Therefore it is seen from the research that

gradually the organized retail outlets have started pulling the maximum population

resulting in changing consumer behavior.

Table 5.5

Visit to Organized retail outlets as per Gender

Source: Compiled from Primary data.

Graph 5.5

Visit to Organized retail outlets as per Gender

Sr.No Response Details Sex Total

Male Female Male

1. Yes Total

Respondents 260 314 260

2. No Total

Respondents 109 40 109

Total

Respondents 369 354 369

251

Table 5.5 and Graph 5.5 give a clear view of the respondents visiting to organized

retail outlets. The results put up gives a clear view of the respondent belonging to the

different age group weather married or male or female and earning any annual income

of family. On being asked about their visits to organized retail outlets it was absorbed

that a total of 79 percent of respondents gave an affirmative reply of their visit and the

21 percent gave a negative reply this shows that the visiting population outnumbered

the non visitors. Further it is also seen from the research that gradually the organized

retail outlets have started pulling the maximum population resulting in changing

consumer behavior.

Table 5.6

Visit to Organized retail outlets as per Annual Family Income

Sr.

No.

Response Details

Annual Family Income

Total % 1-3 Lakh 3-5 Lakh 5-7 Lakh 7-9 Lakh 10 & above

1 Yes Respondents 77% 62% 89% 92% 97% 79%

2 No Respondents 23% 38% 11% 8% 3% 21%

Source: Compiled from Primary data.

Graph 5.6

Visit to Organized retail outlets as per Annual Family Income

252

Table 5.6 and Graph 5.6 give a clear view of the respondents visiting to organized

retail outlets. The results put up gives a clear view of the respondent belonging to the

different age group weather married or male or female and earning any annual income

of family. On being asked about their visits to organized retail outlets it was absorbed

that a total of 79 percent of respondents gave an affirmative reply of their visit and the

21 percent gave a negative reply this shows that the visiting population outnumbered

the non visitors. Further it is also seen from the research that gradually the organized

retail outlets have started pulling the maximum population resulting in changing

consumer behavior.

Frequency of Visit to Organized Retail Outlets

Seven hundred twenty three respondents from different suburbs of Mumbai were

selected for the purpose of data collection. The research was divided into various

categories and the researcher basically concentrated on marital status wise. To

understand the changing behavior of consumers it is very much important to analyze

the frequency of their visits. The results are put up in tabular form below.

Table 5.7

Visit to Organized Retail Outlets as per Marital Status

Source: Compiled from Primary data.

Sr.No Frequency of the

Visit

Marital Status

Total Married Unmarried

1 Daily Total Respondents 6 27 33

2 3-4/week Total Respondents 9 18 27

3 Weekly Total Respondents 91 93 184

4 1-2/month Total Respondents 120 144 264

5 Occasionally Total Respondents 26 40 66

Total 252 322 574

253

Graph 5.7

Visits to Organized Retail Outlets as per Marital Status

From the Table 5.7 and graph 5.7 it is pertinent that it is unmarried people who visit

the malls more with three hundred twenty two respondents visiting .Further a deep

survey showed that the frequency varied but all of them visited the organized outlets.

27 percent respondent visited daily, 18 visited in three to four weeks 29 percent

visiting weekly 45 percent visiting in one to two months and forty percent visiting

occasionally. The respondents also gave the list of most chosen destination by them

which were only the preferences they included:

i. Globus, ii) Inorbit Mall, iii) Growells iv) V Mall v) Shoppers Stop vi)

Nirmal Lifestyle vii) The Hub viii) Megha Mall ix) Lifestyle.

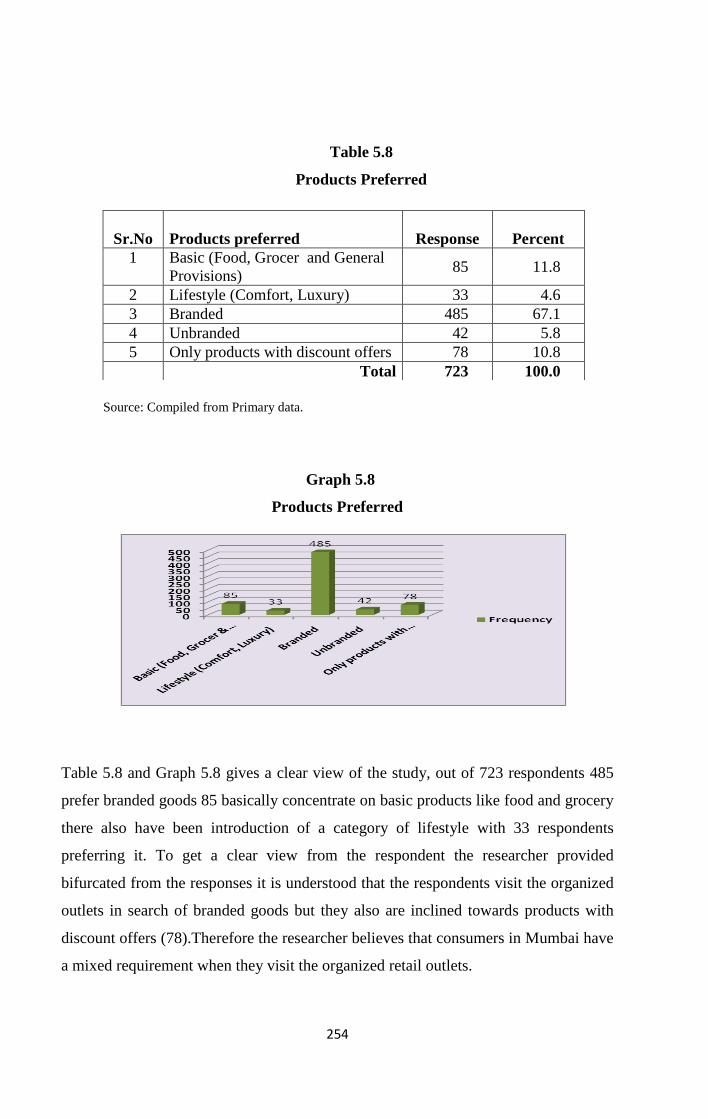

Products preferred

Malls basically termed as Multi Brand Outlets. The organized retail outlets are very

much popular in Mumbai because of the fact that they offer variety of choices and

again they provide a unique experience of see feel touch and posses. The shops in

these outlets have unique blend of various merchandise which include basic, comfort,

lifestyle branded and unbranded therefore the researcher made an attempt to find out

the preferences of Mumbai based on consumers and this throws a light on the shift of

behavior of consumers.

254

Table 5.8

Products Preferred

Source: Compiled from Primary data.

Graph 5.8

Products Preferred

Table 5.8 and Graph 5.8 gives a clear view of the study, out of 723 respondents 485

prefer branded goods 85 basically concentrate on basic products like food and grocery

there also have been introduction of a category of lifestyle with 33 respondents

preferring it. To get a clear view from the respondent the researcher provided

bifurcated from the responses it is understood that the respondents visit the organized

outlets in search of branded goods but they also are inclined towards products with

discount offers (78).Therefore the researcher believes that consumers in Mumbai have

a mixed requirement when they visit the organized retail outlets.

Sr.No

Products preferred Response Percent

1 Basic (Food, Grocer and General

Provisions) 85 11.8

2 Lifestyle (Comfort, Luxury) 33 4.6

3 Branded 485 67.1

4 Unbranded 42 5.8

5 Only products with discount offers 78 10.8

Total 723 100.0

255

Table 5.9

Products Preferred as per Age

Sr.

No.

Products Preferred Age

Total 15-25 25-35 35-45 45-55 > 55

1 Basic (Food, Grocer

and General Provisions) 43 34 6 2 0 85

2 Lifestyle (Comfort,

Luxury) 19 7 4 2 1 33

3 Branded 230 132 68 48 7 485

4 Unbranded 41 1 0 0 0 42

5 Only products with

discount offers 35 19 15 5 4 78

Total 368 193 93 57 12 723

Source: Compiled from Primary data.

Graph 5.9

Products Preferred as per Age

The respondent tried to find out the type of products purchased by the consumers of

different age groups which are put up below.

256

Table 5.9 and Graph 5.9 throws light on the information about the product preference

by the different age groups. The detailed analysis shows that consumers of all the age

group prefer branded goods. The proportion is very high in the young age group of

15-25 with 230 respondents preferring branded followed by age group 25-35 with 132

respondents. Therefore the analysis shows that according to the young generation

perception it is organized retail outlets where branded goods are sold because as seen

in the earlier table the young generation visit organized outlets.

Table 5.10

Products preferred as per Annual Family Income

Source: Compiled from Primary data.

Sr.

No.

Annual Family Income

Total

1-3

Lakh

3-5

Lakh

5-7

Lakh

7-9

Lakh

10 &

above

1

Basic (Food, Grocer

and General

Provisions)

Total

Respondents 43 34 4 3 1 85

2

Lifestyle (Comfort,

Luxury) Total

Respondents 13 14 2 1 3 33

3 Branded Total

Respondents 159 115 61 39 111 485

4 Unbranded Total

Respondents 41 1 0 0 0 42

5

Only products with

discount offers Total

Respondents 33 14 7 6 18 78

Total 289 178 74 49 133 723

257

Graph 5.10

Products preferred as per Annual Family Income

The respondent tried to find out the type of products purchased by the consumers of

different age groups which are put up below.

Table 5.10 and graph 5.10 throws light on the information about the product

preference as per the Annual family Income. The detailed analysis shows that

consumers belonging to any income group prefer branded goods. The proportion is

very high in the income range of 1-3 lakh with 289 respondents opting for organized

retail outlets for purchasing basic (food grocery and general provisions) with 43

respondents, lifestyle goods with 13 respondents and with 159 respondents for

branded goods. It is also seen that 485 respondents belonging to any income range

prefer to go to organized outlets basically for branded goods. This shows that in

Mumbai no matter to which income group the respondent belongs to but for opting

branded goods they go to organized outlets.

The researcher was keen in knowing the preference of married and unmarried

respondents in buying the products. There was a belief that it is unmarried who visit

more to the organized outlets. To understand this analysis was done and the compiled

data is put in a tabular form below.

258

Table 5.11

Products preferred as per Marital Status

Source: Compiled from Primary data.

Graph 5.11

Products preferred as per Marital Status

Table 5.11 and Graph 5.11, shows that out of 723 respondents, it is 286 married and

437 unmarried respondents who visit malls for fulfillment of their requirement.

Further it is also seen that both married and unmarried prefer branded goods but it is

Sr.

No.

Types of Products

Preferred

Marital Status

Total

Married Unmarried

1 Basic (Food, Grocer and

General Provisions)

Total Respondents 33 52 85

2 Lifestyle (Comfort,

Luxury)

Total Respondents 9 24 33

3 Branded Total Respondents 208 277 485

4 Unbranded Total Respondents 0 42 42

5 Only products with

discount offers

Total Respondents 36 42 78

Total 286 437 723

259

unmarried respondents (277) who visit malls with an intention to purchase branded

goods.

Therefore the researcher believes that organized outlets offer number of options to the

consumers to make choices. Consumers also prefer visiting these outlets because here

they not only get goods of their choice but they can touch feel and also see and

thereby giving them a unique experience. The researcher tried to explore this fact and

find out the result.

Impact of Organized Outlets on Budgetary Spending

There has been an assumption that growth of organized retail outlets have increased a

impact on the budget of the consumers visiting them to find out this the researcher

framed a question asking the respondents randomly about the impact these outlets

have created on their monthly budgets and to analyze the researcher conducted study

under two categories employment status and annual family income.

Table 5.12

Impact on Budgetary Spending as per Employment Status

Sr.

No.

Response Employment Status Total

Self

Employed Service Business Retired

Not Employed

Currently Housewife

1 Yes, Higher

spending 28 162 36 8 95 31 360

2 Yes, Lower

spending 15 65 6 1 51 13 151

3 No 19 104 22 42 23 2 212

Total 62 331 64 51 169 46 723

Source: Compiled from Primary data.

260

Graph 5.12

Impact on Budgetary Spending as per Employment Status

Table 5.12 and Graph 5.12 show that there has been a significant impact on the

budgetary spending of the respondent belonging to different employment status, with

360 respondent accepting the fact that there has been higher spending and 151 saying

spending has increased but little lower there has been 212 respondent who felt that

there is no impact on their budgetary spending. Further as per analyze it‟s been

observer that there has been drastic change in the budgetary spending specially in

service oriented respondents with 162 respondent reciprocating, that development of

organized retail outlets have initiated them in higher spending.

Table 5.13 and Graph 5.13 shows the budgetary impact as per annual family income

out of total 723 respondents 360 respondents feel that there has been higher spending

and 151 respondent feel that increase is there but little low and 212 respondents feel

there has been no significant impact on the budgetary spending. Further classification

shows that respondent in income slab of 1-3 lakhs are the ones who viewed more

about the impact on budgetary spending.

0 50 100 150 200

Self Employed

Service

Business

Retired

Not Employed Currently

Housewife

Emp

loym

en

t St

atu

s

28

162

36

8

95

31

15

65

6

1

51

13

19

104

22

42

23

2

No

Yes, Lower spending

Yes, Higher spending

261

Table 5.13

Impact on Budgetary Spending as per Annual Family Income

Source: Compiled from Primary data.

Graph 5.13

Impact on Budgetary Spending as per Annual Family Income

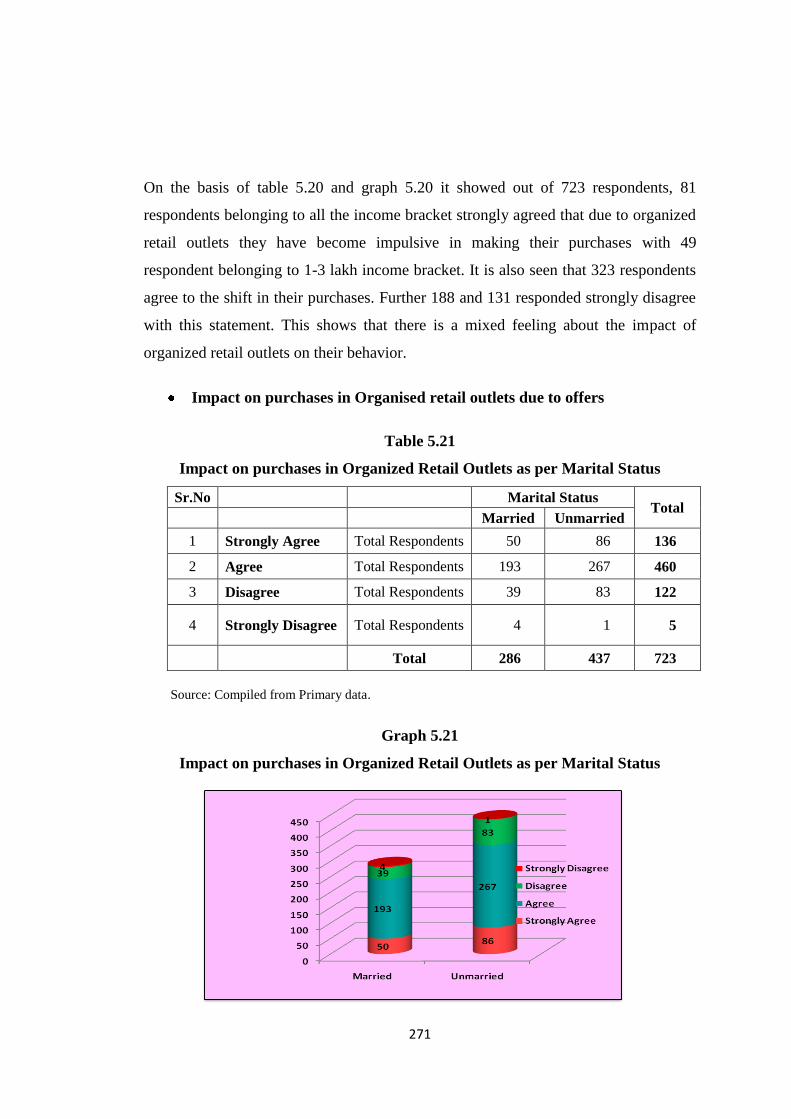

Preference of visit to organized retail outlets than unorganized retail outlets

There has been long debate on the popularity of both the retail outlets and also to

know which outlets the consumers prefer to visit the more. The researcher in order to

find out the preferences of the respondents between organized and unorganized tried

to ask certain questions. The main objective was to understand the shift in their

Sr.

No.

Details

frequency of

visits

Annual Family Income Total

1-3 Lakh 3-5 Lakh 5-7 Lakh 7-9 Lakh 10 & above

1 Yes, Higher

spending 114 69 42 31 104 360

2 Yes, Lower

spending 74 28 18 6 25 151

3 No 101 81 14 12 4 212

Total 289 178 74 49 133 723

262

behavior after the development of these outlets. The replies gave a clear idea about

the trends that will be followed in the future. The researcher categorized two basic

areas (Gender wise and age wise) to know the preference.

Table 5.14

Preference of visit to organized retail outlets than unorganized retail outlets as

per Gender

Source: Compiled from Primary data.

Graph 5.14

Preference of visit to organized retail outlets than unorganized retail outlets as

per Gender

An attempt was made by the researcher to understand the preferences made by the

respondents as per gender Table 5.14 and Graph 5.14 shows that in all 723

respondents were surveyed and 498 respondent gave an affirmative response of

visiting the organized retail outlets further analysation showed that the female

Sr.No Preference Sex

Total Male Female

1 Yes Total Respondents 237 261 498

2 No Total Respondents 132 93 225

Total 369 354 723

263

population in Mumbai are more inclined towards organized outlets with 261

respondents confirming yes as their visit and 237 male respondents confirming of

their visit. It was also seen that about 225 respondents, denied their visits to organized

outlets and in this category it was male population with 132 respondents who

outnumbered female population with 93 numbers.

Table 5.15

Frequency of the Visit as per Gender Wise

Source: Compiled from Primary data.

Graph 5.15

Frequency of the Visit as per Gender Wise

Graph 5.15

Sr.No. Frequency of

visit

Sex

Total Male Female

1 Up to 25% Total Respondents 47 71 118

2 Up to 50% Total Respondents 129 115 244

3 Up to 75% Total Respondents 52 72 124

4 Up to 100% Total Respondents 9 3 12

Total 237 261 498

264

The researcher was keen in knowing the frequency of the visits made by the

respondents, Table 5.15 and Graph 5.15 shows the results, when both male and

female respondents were questioned about their frequency of visit around 244

respondents confirmed it to be about 50 percent with male (129 ) outnumbered female

(115). Further 124 respondent confirmed their frequency up to 75 percent in this

category it was female (72) who outnumbered male (52). This analysis made by the

researcher therefore shows that with the development of malls in Mumbai region the

frequency of visits by both male and female have increased.

Table 5.16

Preference of visit to organized retail outlets as per Age

Source: Compiled from Primary data.

Sr.No. Preference Age

Total 15-25 25-35 35-45 45-55 > 55

1 Yes Total

Respondents 224 149 79 39 7 498

2 No Total

Respondents 144 44 14 18 5 225

Total 368 193 93 57 12 723

100% 100% 100% 100% 100% 100%

265

Graph 5.16

Preference of visit to organized retail outlets as per Age

The researcher further made an attempt to understand the preferences made by the

respondents as per age Table 5.16 and Graph 5.16 shows that in all 723 respondents

were surveyed and 498 respondent gave an affirmative response of visiting the

organized retail outlets it has also been absorbed that respondents of all the age group

are inclined towards organized retail outlets but the young respondents in the age

bracket 15 to 25 (224) and 25 to 35 (149) are maximum who visit the outlets and

respondents above the age bracket 55(7) hardly do visit the outlets, this shows the

Mumbai with young generation is slowly moving towards change. It was also seen

that about 225 respondent, denied their visits to organized outlets and in this category

with the consumers in age bracket of 15-25 (144) outnumbering the list.

266

Table 5.17

Frequency of the Visit as per Age Wise

Sr.

No.

Frequency

of visit

Age Total

15-25 25-35 35-45 45-55 > 55

1 Up to

25%

Total

Respondents

77 30 5 6 0 118

2 Up to

50%

Total

Respondents

100 74 40 26 4 244

3 Up to

75%

Total

Respondents

41 43 31 7 2 124

4 Up to

100%

Total

Respondents

6 2 3 0 1 12

Total 224 149 79 39 7 498

Source: Compiled from Primary data.

Graph 5.17

Frequency of the Visit as per Age Wise

267

Table 5.17 and Graph 5.17 shows the results of survey, when the respondents were

questioned about their frequency of visit around 244 respondents belonging to

different age group confirmed it to be about 50 percent with maximum respondents

being in the age bracket of 15-25 (100), 25-35 (74), 35-45 (40) and 45-55(26) and the

lowest being respondent in the age bracket of above 55 (4).Further the response has

been move of the respondents in the age brackets of 15-25 (218) and 25-35 (147), this

shows that Mumbai has the young generation who are the reason for this change.

Change in Buying Behavior due organized retail outlets

There was requirement to understand the change in the consumer behavior due to the

setting of the organized retail outlets. The researcher also was keen in knowing the

impact created by these outlets in a city like Mumbai that keeps accepting the changes

gracefully. To understand this researcher concentrated on one category basically

namely gender wise and while doing so she tried to find out the frequency also.

Table 5.18

Change in Buying Behaviour as per Gender

Sr.No. Response Sex

Total Male Female

Yes, very much Total Respondents 207 93 300

Yes, to some extent Total Respondents 138 232 370

No not at all Total Respondents 24 29 53

369 354 723

Source: Compiled from Primary data.

268

Graph 5.18

Change in Buying Behaviour as per Gender

Table 5.18 and Graph 5.18 give a clear analization of the changing buying habit of

consumers. Total 300 respondents were of the opinion that due to organized retail

outlets their behavior has changed very much with male respondents (207)

outnumbering female respondents (93). Further 370 respondents were of the opinion

that their behavior has changed but to some extent with female respondents (232)

being more than male (138). Around 53 respondents were of the opinion that their

behavior is stable and there has been no change.

Table 5.19

Frequency in Change in Buying Behaviour as per Gender

Sr.No Response Sex

Total Male Female

1 25% Total Respondents 144 95 239

2 50% Total Respondents 148 185 333

3 75% Total Respondents 47 45 92

4 100% Total Respondents 6 0 6

Total 345 325 670

Source: Compiled from Primary data.

269

Graph 5.19

Frequency in Change in Buying Behaviour as per Gender

Table 5.19 and Graph 5.19 give the frequency of the changing behavior. The

respondents agreed that this shift in the buying behavior is due to the offers and

facilities being given by them. The researcher also tried to find the frequency in this

change in behavior the result is with 333 respondents responding to 50 percent with

male (148) and female (185). The result also showed that there are few respondents

numbering to 53 who felt that the development of these organized retail outlets have

not changed their buying behavior.

Changes in Buying Behavior

Organised retail outlets resulting in Impulsive Purchases

There is a general assumption that the malls attract people and even when they

go for window shopping they end up in making impulsive purchases. The

researcher therefore wanted to test this on the basis of the following

parameters and categories. Since the researcher wanted to have a clear idea

about the impulsive purchases with respect to annual family income and age

group wise.

270

Table 5.20

Impulsive purchases in Organised Retail Outlets as per Annual Family Income

Source: Compiled from Primary data.

Graph 5.20

Impulsive purchases in Organised Retail Outlets as per Annual Family Income

Sr

No

Annual Family Income

Total 1-3 Lakh

3-5

Lakh

5-7

Lakh

7-9

Lakh

10 &

above

1 Strongly

Agree

Total

Respondents 49 13 7 5 7 81

2 Agree Total

Respondents 135 124 25 18 21 323

3 Disagree Total