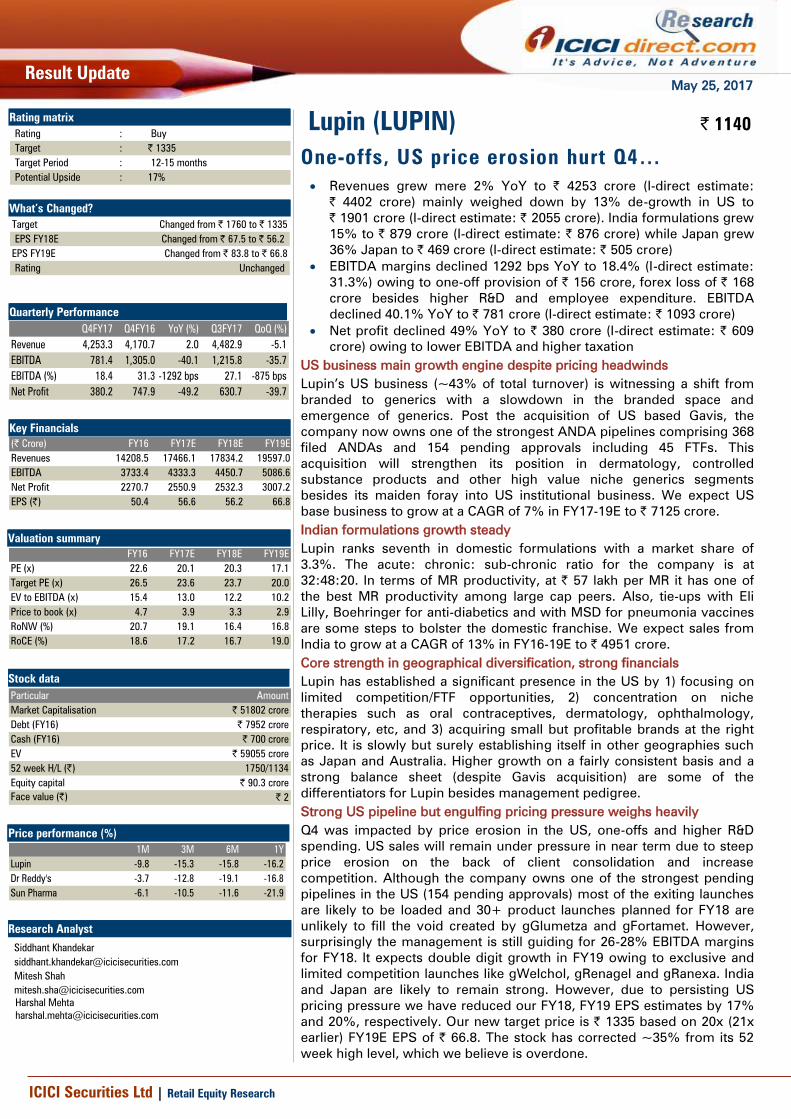

rating mat lupin (lupin) |...

TRANSCRIPT

May 25, 2017

ICICI Securities Ltd | Retail Equity Research

Result Update

One-offs, US price erosion hurt Q4…

Revenues grew mere 2% YoY to | 4253 crore (I-direct estimate:

| 4402 crore) mainly weighed down by 13% de-growth in US to

| 1901 crore (I-direct estimate: | 2055 crore). India formulations grew

15% to | 879 crore (I-direct estimate: | 876 crore) while Japan grew

36% Japan to | 469 crore (I-direct estimate: | 505 crore)

EBITDA margins declined 1292 bps YoY to 18.4% (I-direct estimate:

31.3%) owing to one-off provision of | 156 crore, forex loss of | 168

crore besides higher R&D and employee expenditure. EBITDA

declined 40.1% YoY to | 781 crore (I-direct estimate: | 1093 crore)

Net profit declined 49% YoY to | 380 crore (I-direct estimate: | 609

crore) owing to lower EBITDA and higher taxation

US business main growth engine despite pricing headwinds

Lupin’s US business (~43% of total turnover) is witnessing a shift from

branded to generics with a slowdown in the branded space and

emergence of generics. Post the acquisition of US based Gavis, the

company now owns one of the strongest ANDA pipelines comprising 368

filed ANDAs and 154 pending approvals including 45 FTFs. This

acquisition will strengthen its position in dermatology, controlled

substance products and other high value niche generics segments

besides its maiden foray into US institutional business. We expect US

base business to grow at a CAGR of 7% in FY17-19E to | 7125 crore.

Indian formulations growth steady

Lupin ranks seventh in domestic formulations with a market share of

3.3%. The acute: chronic: sub-chronic ratio for the company is at

32:48:20. In terms of MR productivity, at | 57 lakh per MR it has one of

the best MR productivity among large cap peers. Also, tie-ups with Eli

Lilly, Boehringer for anti-diabetics and with MSD for pneumonia vaccines

are some steps to bolster the domestic franchise. We expect sales from

India to grow at a CAGR of 13% in FY16-19E to | 4951 crore.

Core strength in geographical diversification, strong financials

Lupin has established a significant presence in the US by 1) focusing on

limited competition/FTF opportunities, 2) concentration on niche

therapies such as oral contraceptives, dermatology, ophthalmology,

respiratory, etc, and 3) acquiring small but profitable brands at the right

price. It is slowly but surely establishing itself in other geographies such

as Japan and Australia. Higher growth on a fairly consistent basis and a

strong balance sheet (despite Gavis acquisition) are some of the

differentiators for Lupin besides management pedigree.

Strong US pipeline but engulfing pricing pressure weighs heavily

Q4 was impacted by price erosion in the US, one-offs and higher R&D

spending. US sales will remain under pressure in near term due to steep

price erosion on the back of client consolidation and increase

competition. Although the company owns one of the strongest pending

pipelines in the US (154 pending approvals) most of the exiting launches

are likely to be loaded and 30+ product launches planned for FY18 are

unlikely to fill the void created by gGlumetza and gFortamet. However,

surprisingly the management is still guiding for 26-28% EBITDA margins

for FY18. It expects double digit growth in FY19 owing to exclusive and

limited competition launches like gWelchol, gRenagel and gRanexa. India

and Japan are likely to remain strong. However, due to persisting US

pricing pressure we have reduced our FY18, FY19 EPS estimates by 17%

and 20%, respectively. Our new target price is | 1335 based on 20x (21x

earlier) FY19E EPS of | 66.8. The stock has corrected ~35% from its 52

week high level, which we believe is overdone.

Rating matrix

Rating : Buy

Target : | 1335

Target Period : 12-15 months

Potential Upside : 17%

What’s Changed?

Target Changed from | 1760 to | 1335

EPS FY18E Changed from | 67.5 to | 56.2

EPS FY19E Changed from | 83.8 to | 66.8

Rating Unchanged

Quarterly Performance

Q4FY17 Q4FY16 YoY (%) Q3FY17 QoQ (%)

Revenue 4,253.3 4,170.7 2.0 4,482.9 -5.1

EBITDA 781.4 1,305.0 -40.1 1,215.8 -35.7

EBITDA (%) 18.4 31.3 -1292 bps 27.1 -875 bps

Net Profit 380.2 747.9 -49.2 630.7 -39.7

Key Financials

(| Crore) FY16 FY17E FY18E FY19E

Revenues 14208.5 17466.1 17834.2 19597.0

EBITDA 3733.4 4333.3 4450.7 5086.6

Net Profit 2270.7 2550.9 2532.3 3007.2

EPS (|) 50.4 56.6 56.2 66.8

Valuation summary

FY16 FY17E FY18E FY19E

PE (x) 22.6 20.1 20.3 17.1

Target PE (x) 26.5 23.6 23.7 20.0

EV to EBITDA (x) 15.4 13.0 12.2 10.2

Price to book (x) 4.7 3.9 3.3 2.9

RoNW (%) 20.7 19.1 16.4 16.8

RoCE (%) 18.6 17.2 16.7 19.0

Stock data

Particular

Market Capitalisation

Debt (FY16)

Cash (FY16)

EV

52 week H/L (|) 1750/1134

Equity capital

Face value (|) | 2

| 90.3 crore

Amount

| 51802 crore

| 59055 crore

| 7952 crore

| 700 crore

Price performance (%)

1M 3M 6M 1Y

Lupin -9.8 -15.3 -15.8 -16.2

Dr Reddy's -3.7 -12.8 -19.1 -16.8

Sun Pharma -6.1 -10.5 -11.6 -21.9

Research Analyst

Siddhant Khandekar

Mitesh Shah

Harshal Mehta

Lupin (LUPIN) | 1140

ICICI Securities Ltd | Retail Equity Research Page 2

Variance analysis

(| crore) Q4FY17 Q4FY17E Q4FY16 Q3FY17 YoY (%) QoQ (%) Comments

Revenue 4,253.3 4,401.6 4,170.7 4,482.9 2.0 -5.1 YoY growth in India and Japan largely offset by decline in US

Raw Material Expenses 1,185.1 1,320.5 1,101.0 1,301.6 7.6 -8.9 147 bps YoY contraction in gross margins to 72.1% mainly on the back of

adverse product mix

Employee Expenses 707.8 682.3 577.9 731.2 22.5 -3.2 Increased mainly due to new recruitments at expanded Somerset (Gavis)

facility in the US

Other Expenditure 1,579.1 1,306.2 1,186.8 1,234.3 33.0 27.9 Increased mainly due to higher R&D expenses and | 156 crore of product

related provision. R&D expenses increased 31% YoY to | 671 crore

EBITDA 781.4 1,092.7 1,305.0 1,215.8 -40.1 -35.7

EBITDA (%) 18.4 24.8 31.3 27.1 -1292 bps -875 bps YoY decline in margin mainly due to one-off provision, forex loss of | 168

crore against forx gain of | 26.7 crore in Q4FY16, higher R&D and employee

expenditure. Miss vis-à-vis I-direct estimates mainly due to higher R&D

expenses, one-off provision and forex loss

Interest 40.6 40.1 21.3 45.9 90.9 -11.6

Depreciation 267.4 230.9 148.7 230.9 79.8 15.8 YoY increase in depreciation mainly due to Gavis amortisation

Other Income 45.3 27.8 34.9 103.6 30.0 -56.2

PBT 518.7 849.5 1,169.9 1,042.6 -55.7 -50.3

Tax 136.7 237.9 418.8 409.5 -67.4 -66.6 YoY, QoQ decline mainly due to higher deferred tax. Normalised tax rate was

24%

PAT before MI 382.0 611.7 751.1 633.1 -49.1 -39.7

Minority Interest 1.8 2.3 3.3 2.4 -45.4 -24.6

Net Profit 380.2 609.4 747.9 630.7 -49.2 -39.7 YoY decline mainly due to weak operational performance and higher taxation

Key Metrics

India 878.8 875.7 761.5 991.2 15.4 -11.3

Japan 468.7 505.3 344.2 449.2 36.2 4.3 Strong sales mainly due to sales from 21 acquired products from Shionogi

US 1,900.7 2,055.3 2,187.1 2,175.5 -13.1 -12.6 YoY decline mainly due to price erosion in base business and gGlumetza. Miss

vis-à-vis I-direct expectations was mainly due to higher-than-expected price

erosion in base business

Europe 135.5 137.9 125.4 142.8 8.0 -5.1 Constant currency sales in Germany decline 9.6% YoY to €6.5 million

South Africa 165.8 135.7 113.5 112.7 46.0 47.1 Beat vis-à-vis estimates mainly due to higher-than-expected constant

currency growth. Constant currency growth was 26%

ROW markets 331.0 317.2 275.8 265.1 20.0 24.9 YoY growth mainly due to 37% YoY growth in LATAM to | 127 crore

API 281.5 298.0 283.8 268.4 -0.8 4.9

Change in estimates

(| Crore) Old New % Change Old New % Change

Revenue 19,526.2 17,834.2 -8.7 22,065.0 19,597.0 -11.2 Changed mainly due to higher-than-expected price erosion in the US

EBITDA 5,020.5 4,450.7 -11.3 6,004.2 5,086.6 -15.3

EBITDA Margin (%) 25.7 25.0 -76 bps 27.2 26.0 -126 bps Changed mainly due to adverse product mix

PAT 3,029.2 2,532.3 -16.4 3,768.3 3,007.2 -20.2

EPS (|) 67.2 56.2 -16.4 83.6 66.8 -20.2 Changed mainly due to reduced revenue and EBITDA margins assumptions

FY18E FY19E

Assumptions

Current Comments

(| crore) FY16 FY17E FY18E FY19E FY18E FY19E

India 3,406.4 3,797.1 4,308.9 4,890.4 4,305.3 4,951.1

Japan 1,364.2 1,777.3 2,408.6 2,697.6 2,408.6 3,134.7

US 5,913.2 8,262.6 7,168.8 7,667.1 8,876.6 9,642.1 Change mainly due to higher-than-expected price erosion in base business

Europe 455.4 529.4 582.3 640.5 585.0 643.5

South Africa 399.7 482.2 550.4 633.0 518.4 596.2 Change mainly due to better-than-expected sales in Q4FY17

ROW markets 947.0 1,114.3 1,281.5 1,473.7 1,265.6 1,455.4

API 1,214.9 1,128.7 1,151.3 1,174.3 1,168.1 1,191.5

Earlier

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 3

Company Analysis

From a global leader in anti-tuberculosis (TB) and other infectious

diseases to one of the fastest growing prescription companies in the US,

Lupin has come a long way to emerge as a leading Indian generic

exporter. Established in 1968, the company adapted well as per the

changed industry dynamics like other peers such as Sun, Dr Reddy’s,

Ranbaxy and Cipla. During this journey, it changed focus in therapies -

from acute to chronic and also geographies, from domestic driven to

export oriented. It received USFDA approvals for two facilities-

Ankaleshwar and Mandideep way back in 1989. Besides this, the

company has been fairly active on the global M&A front. It has acquired

companies in Japan (significant acquisitions), Australia, Philippines and

South Africa. Similarly, the company also acquired small ticket but

lucrative brands in the US (Suprax, Antara, Locoid lotion, Inspira Chamber

and Alinia). Its latest acquisition, however, has been a complex injectable

technology based company (Nanomi) in the Netherlands. Infrastructure -

11 manufacturing facilities including two in Japan – seven formulations

(three USFDA approved) and four APIs (two USFDA approved).

Exhibit 1: Return ratios to improve further

25.4 25.4

19.1

21.9 21.6

18.6

26.5

29.8

22.5

27.1

20.7

26.3

26.6

35.7 35.1

17.2

0

5

10

15

20

25

30

35

40

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

(%

)

RoNW RoCE

Source: Company, ICICIdirect.com Research

Exhibit 2: R&D spend likely to remain at elevated level

465.95 500.64

681.8

929.4

1099

1604

6.0

7.37.7

9.2

13.5 13.5

6.6

5.2

0

300

600

900

1200

1500

1800

2100

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

3

5

7

9

11

13

15

R & D cost (| crore) R & D cost % revenues

Source: Company, ICICIdirect.com Research

The current financial health of the company is the culmination of prudent

business decisions in the past. Over the last 10 years, revenues, EBITDA

and PAT have grown at a CAGR of 20%, 26% and 21%, respectively.

Considering more recent numbers, in FY12-17, the revenue, EBITDA and

PAT have grown at a CAGR of 20%, 17% and 13% to | 14466 crore,

| 4333 crore and | 2551 crore, respectively. Similarly, during the same

period, the R&D spend as a percentage of sales, has gone up from 6.6%

in FY12 to 9.2% in FY17.

Going ahead, in the near term, we expect revenues, EBITDA and PAT to

grow at a CAGR of 6%, 8% and 9%, respectively, in FY17-19E. However,

from a long term perspective, we believe the company is well poised to

grow at a healthy rate given the strong US pipeline, vast experience and

good understanding of the US market, continued traction in Indian

branded formulations with higher chronic focus and improvement in the

Japanese market, which is perhaps the only geography where there is a

scope for improvement. On the R&D front, we see the composition spend

tilting towards NDDS, NCEs, biosimilars from the current ANDA/NDA

albeit gradually to prepare for the scenario beyond 2020.

ICICI Securities Ltd | Retail Equity Research Page 4

Exhibit 3: Revenues to grow at CAGR of 6% in FY17-19E

7082.9

9641.3

11286.6

12770.0

14208.5

17466.1 17834.2

19597.0

0

3000

6000

9000

12000

15000

18000

21000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

(|

crore)

Source: Company, ICICIdirect.com Research

Exhibit 4: US base business pricing pressure, higher base to percolate into negative CAGR

2079.8

3769.5

4887.1

5659.35913.2

8262.6

7168.87667.1

0.0

2000.0

4000.0

6000.0

8000.0

10000.0

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

US (| crore)

Source: Company, ICICIdirect.com Research

Exhibit 5: Indian formulation sales to grow at CAGR of 14% in FY17-19E

1350.01573.5

2479.6

2968.0

3406.4

3797.1

4308.9

4890.4

0.0

1100.0

2200.0

3300.0

4400.0

5500.0

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

India (| crore)

Source: Company, ICICIdirect.com Research

Revenues to grow at a CAGR of 6% in FY17-19E to

| 19597 crore driven by 14% growth in the India business,

23% in Japan, 15% in RoW markets, 15% in South Africa,

10% in European markets and 4% de-growth in US

formulations business

Lupin is the fifth largest generics player in the US in terms

of prescriptions. It owns a healthy product pipeline

(including Gavis) in the US (368 ANDAs filed, 154

pending approvals and 214 approvals), which includes

some limited competition products and 45 FTFs

opportunities. It is planning to launch more than 150 (100

owns and 50 from GAVIS) products in the US market in

the next four or five years. Acquisition of Gavis will also

strengthen its position in dermatology, controlled

substance products and other high value niche generics

segments besides its maiden foray into US institutional

business. Lupin is one of the few generic companies that

has a presence in the branded business. Currently, it is

marketing four branded products in the US market,

including two that were in-licensed in the last 12 months.

However, with continued pricing pressure in the US base

business due to buyers consolidation, we expect sales

from the US market to decline at a CAGR of 3.7% in FY17-

19E to | 7667 crore

Lupin is ranked seventh in domestic formulations with a

market share of 3.3%. The company is adding more drugs

in chronic therapies, which would drive growth in the

domestic market. We expect sales from India to grow at a

CAGR of 14% in FY17-19E to | 4890 crore

19.8% CAGR

5.9% CAGR

31.8% CAGR

-3.7% CAGR

23% CAGR

13.5% CAGR

ICICI Securities Ltd | Retail Equity Research Page 5

Exhibit 6: Japanese revenue to grow at CAGR of 23% in FY17-19E

860.8

1304.0 1295.4 1323.9 1364.2

1777.3

2408.6

2697.6

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Japan (| crore)

Source: Company, ICICIdirect.com Research

Exhibit 7: EBITDA to grow at CAGR of 8% in FY17-19E

1959

2270

2899

3620 3733

4333 4451

5087

27.7

23.5

25.7

28.3

26.3

24.8 25.0

26.0

0

1000

2000

3000

4000

5000

6000

7000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

(|

crore)

15

17

19

21

23

25

27

29

(%

)

EBITDA EBITDA Margins (%)

Source: Company, ICICIdirect.com Research

Exhibit 8: Net profit to grow at CAGR of 9% in FY17-19E

1382.11314.1

1836.4

2403.22270.7

2550.9

3007.2

2532.3

19.5

13.6

16.3

18.8

14.614.2

15.3

16.0

0

500

1000

1500

2000

2500

3000

3500

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

5

7

9

11

13

15

17

19

Net Profit Net Profit Margins (%)

Source: Company, ICICIdirect.com Research

The Japanese acquisitions i.e. Kyowa and I’rom are yet to

achieve expected critical mass both in terms of

scalability and profitability. While Kyowa profitability is

expected to improve on the back of back-ended

integration by sourcing of APIs from Goa, the I’rom

business remains challenging due to the lumpy nature of

the CRAMS business. Kyowa has acquired 21 branded

products from Shionogi. Recently acquired 21 products

from Shionogi will add to the company’s overall growth.

We expect sales from Japan to grow at a CAGR 23% in

FY17-19E to | 2698 crore mainly due to increase growth

in existing business and consolidation of Shionogi’s

portfolio

15.6% CAGR

23.2% CAGR

ICICI Securities Ltd | Retail Equity Research Page 6

Exhibit 9: Trends in quarterly financial performance

(| crore) Q4FY14 Q1FY15 Q2FY15 Q3FY15 Q4FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17 Q3FY17 Q4FY17 YoY (%) QoQ (%)

US 1469.9 1605.5 1271.6 1404.3 1377.9 1190.6 1155 1380.5 2187.1 2188.6 1997.8 2175.5 1900.7 -13.1 -12.6

Europe 79.5 69.0 87.6 80.5 89.1 100.3 115.8 113.9 125.4 128.0 123.1 142.8 135.5 8.0 -5.1

Japan 321.8 341.5 345.9 342.2 294.3 323.1 323.4 373.5 344.2 422.6 436.8 449.2 468.7 36.2 4.3

India 576.3 761.5 799.0 743.8 663.7 885.1 873.8 886.0 761.5 931.3 995.8 991.2 878.8 15.4 -11.3

South Africa 106.7 86.9 105.7 107.0 122.2 81.6 99.8 104.8 113.5 91.4 112.4 112.7 165.8 46.0 47.1

RoW 205.9 127.1 188.7 191.3 199.3 174.5 288.6 208.1 275.8 264.8 253.4 265.1 331.0 20.0 24.9

API 291.4 292.5 318.3 275.8 307.5 325.7 321.9 283.5 283.8 286.9 291.9 268.4 281.5 -0.8 4.9

Net Sales 3051.6 3284.0 3116.8 3144.9 3054.0 3080.9 3192.6 3357.7 4082.3 4313.6 4211.2 4404.9 4161.9 1.9 -5.5

OOI 69.0 56.9 56.6 32.7 24.1 75.2 137.1 198.2 88.4 125.9 79.3 77.9 91.4 3.4 17.3

Revenues 3120.5 3340.8 3173.4 3177.6 3078.2 3156.1 3329.7 3555.8 4170.7 4439.4 4290.5 4482.9 4253.3 2.0 -5.1

RM Cost 980.4 1107.4 1069.8 1023.6 956.4 983.5 1124.9 1123.0 1101.0 1271.9 1242.9 1301.6 1185.1 7.6 -8.9

% of Revenue 31.4 33.1 33.7 32.2 31.1 31.2 33.8 31.6 26.4 28.7 29.0 29.0 27.9

Gross Profit 2140.1 2233.5 2103.6 2154.1 2121.8 2172.6 2204.8 2432.8 3069.8 3167.5 3047.7 3181.3 3068.2 -0.1 -3.6

GPM (%) 68.6 66.9 66.3 67.8 68.9 68.8 66.2 68.4 73.6 71.3 71.0 71.0 72.1 -147 117

Employee Cost 389.6 410.4 438.9 415.9 482.2 497.3 532.8 528.4 577.9 705.9 712.4 731.2 707.8 22.5 -3.2

% of Revenue 12.5 12.3 13.8 13.1 15.7 15.8 16.0 14.9 13.9 15.9 16.6 16.3 16.6 278.4 33.1

Other expenditure 873.6 708.4 832.2 855.3 850.2 850.5 1009.4 1027.3 1186.8 1153.5 1307.2 1234.3 1579.1 33.0 27.9

% of Revenue 28.0 21.2 26.2 26.9 27.6 26.9 30.3 28.9 28.5 26.0 30.5 27.5 37.1

Total Expenditure 2243.6 2226.1 2340.9 2294.7 2288.8 2331.2 2667.1 2678.7 2865.7 3131.4 3262.4 3267.0 3471.9 21.2 6.3

% of Revenue 71.9 66.6 73.8 72.2 74.4 73.9 80.1 75.3 68.7 70.5 76.0 72.9 81.6 1291.9 875.1

EBITDA 876.9 1114.8 832.5 882.9 789.4 824.8 662.6 877.2 1305.0 1308.0 1028.1 1215.8 781.4 -40.1 -35.7

EBITDA Margin (%) 28.1 33.4 26.2 27.8 25.6 26.1 19.9 24.7 31.3 29.5 24.0 27.1 18.4 -1291.9 -875.1

Other income 5.2 28.9 110.2 83.4 17.2 75.7 57.8 65.3 34.9 82.6 27.1 103.6 45.3 30.0 -56.2

Interest 12.2 2.6 2.1 2.7 2.5 7.0 24.1 9.2 21.3 32.0 26.3 45.9 40.6 90.9 -11.6

Depreciation 74.3 108.6 108.7 110.3 107.2 101.4 115.5 111.4 148.7 202.7 211.2 230.9 267.4 79.8 15.8

PBT 794.7 1031.5 831.0 852.4 696.0 791.1 579.9 820.9 1168.9 1155.0 816.7 1041.6 517.7 -55.7 -50.3

Tax 232.7 402.9 192.6 238.7 136.2 225.8 159.1 290.9 418.8 273.4 158.9 409.5 136.7 -67.4 -66.6

Tax rate (%) 29.3 39.1 23.2 28.0 19.6 28.5 27.4 35.4 35.8 23.7 19.5 39.3 26.4

PAT 562.0 628.6 638.4 613.7 559.7 565.3 420.8 530.0 750.1 881.6 657.8 632.1 381.0 -49.2 -39.7

PAT Margin (%) 18.0 18.8 20.1 19.3 18.2 17.9 12.6 14.9 18.0 19.9 15.3 14.1 9.0 -902.8 -514.3

Minority Interest 10.0 4.8 9.4 13.3 13.7 -2.2 2.7 1.3 3.3 0.6 0.8 2.4 1.8 -45.4 -24.6

PAT After MI 552.0 623.7 629.0 600.5 546.0 567.6 418.1 528.8 746.9 881.0 657.0 629.7 379.2 -49.2 -39.8

Source: Company, ICICIdirect.com Research

Lupin - SWOT Analysis

Strengths - Prudent geographical mix covering high opportunity

emerging markets as well as developed markets. Formidable US presence

with highest rank among Indian peers in the US generic prescriptions

space. One of the best working capital management in the industry with

strong return ratios and ever improving margins.

Weakness - The Japanese market still remains a low margin business.

Opportunities - In the US generics space, a lot of opportunities are

panning out in the oral contraceptives and respiratory space.

Threats - Increased USFDA scrutiny across the globe regarding cGMP

issues, pricing pressure due to client consolidation in the US, pricing

probe by the Department of Justice (DoJ) in the US, proposed tightening

by the new regime by adapting to the bidding process and imposition of

border adjustment tax on imported drugs in the US. Gavis like costly

acquisitions can stretch the balance sheet further if the product pipeline

fails to deliver the expected payback.

ICICI Securities Ltd | Retail Equity Research Page 7

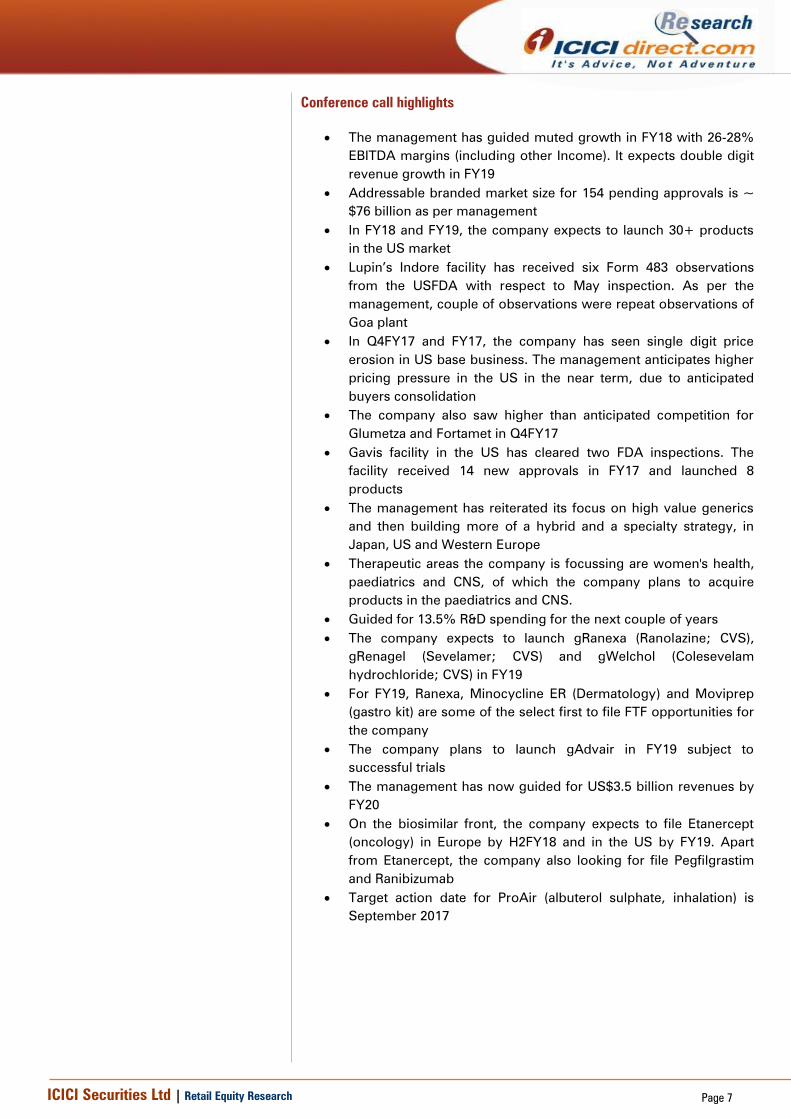

Conference call highlights

The management has guided muted growth in FY18 with 26-28%

EBITDA margins (including other Income). It expects double digit

revenue growth in FY19

Addressable branded market size for 154 pending approvals is ~

$76 billion as per management

In FY18 and FY19, the company expects to launch 30+ products

in the US market

Lupin’s Indore facility has received six Form 483 observations

from the USFDA with respect to May inspection. As per the

management, couple of observations were repeat observations of

Goa plant

In Q4FY17 and FY17, the company has seen single digit price

erosion in US base business. The management anticipates higher

pricing pressure in the US in the near term, due to anticipated

buyers consolidation

The company also saw higher than anticipated competition for

Glumetza and Fortamet in Q4FY17

Gavis facility in the US has cleared two FDA inspections. The

facility received 14 new approvals in FY17 and launched 8

products

The management has reiterated its focus on high value generics

and then building more of a hybrid and a specialty strategy, in

Japan, US and Western Europe

Therapeutic areas the company is focussing are women's health,

paediatrics and CNS, of which the company plans to acquire

products in the paediatrics and CNS.

Guided for 13.5% R&D spending for the next couple of years

The company expects to launch gRanexa (Ranolazine; CVS),

gRenagel (Sevelamer; CVS) and gWelchol (Colesevelam

hydrochloride; CVS) in FY19

For FY19, Ranexa, Minocycline ER (Dermatology) and Moviprep

(gastro kit) are some of the select first to file FTF opportunities for

the company

The company plans to launch gAdvair in FY19 subject to

successful trials

The management has now guided for US$3.5 billion revenues by

FY20

On the biosimilar front, the company expects to file Etanercept

(oncology) in Europe by H2FY18 and in the US by FY19. Apart

from Etanercept, the company also looking for file Pegfilgrastim

and Ranibizumab

Target action date for ProAir (albuterol sulphate, inhalation) is

September 2017

ICICI Securities Ltd | Retail Equity Research Page 8

Exhibit 10: Major Facilities

Location Segment Regulatory Approvals Type

Inspection

Date Outcome

` Formulations USFDA, TGA Australia, WHO GMP, MCC SA Tablets, Capsules, Liquids Jan-16 483 with 3 observations

Ankaleshwar (India) APIs UKMHRA, WHO GMP, ANVISA Brazil, EDQM, KFDA Intermediates and APIs

Mandideep (India) Formulations / APIs USFDA, UKMHRA,WHO GMP, TGA Auatralia APIs- CVS and Ciphalosporins Feb-16 483 with 4 observations

Tarapur (India) APIs USFDA, UKMHRA, WHO GMP APIs Aug-16 No observations

Goa (India) Formulations USFDA, UKMHRA, WHO GMP Solid orals Mar-16 Received EIR

Jammu (India) Formulations WHO GMP, ANVISA Brazil Formulations

Vadodara (India) APIs WHO GMP Intermediates and APIs

Indore (India) Formulations / APIs USFDA, UKMHRA,TGA Auatralia APIs and Formulations Jan-16 483 with 6 observations

Nagpur (India) Formulations WHO and USFDA Formulations

Kyowa (Japan) Formulations PMDA Orals

I' rom (Japan) Formulations PMDA Injectables

Vishakapatnam, AP APIs Under Initiation

Pune (India) R&D Aug-16 No observations

Oldenzaal, Netherlands R&D

Coral Springs, FL R&D

Somerset, NJ Formulations & R&D

Mexico City, Mexico Formulations & R&D

Minas Gerias, Brazil Formulations & R&D

Source: Company, ICICIdirect.com Research

Exhibit 11: Complex generics/speciality updates

Focus Areas FY16 R&D Update Filed Development

NDDDs Continue development (10 NCEs) NA NA

Biosimilars 10 under development; Etanercept started PhIII in Japan; NA 19.1

Respiratory 2 filings; Clinical trials started for 1 MDI; DPI clinical trials to commence in FY17 0.3 17.2

Injectables Nanomi-complex depot injectable development ongoing; LRP injectables development Ongoing NA 12.8

Controlled Subst. Gavis 9 products in market; 12 filings; Further Development ongoing 4.1 7.8

Dermatology Gavis 1 product in market; 24 filings; Development ongoing 3 2.7

Ophthalmology 2 in market; 7 filings; Continue development 3.1 1.8

OC’s 21 products in market; 10 pending approval 1.2 NA

Total 11.7 61.4

Targeted market Size (US$ billion)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 9

Valuation

Q4 was impacted by price erosion in the US, one-offs and higher R&D

spending. US sales will remain under pressure in the near term due to

steep price erosion on the back of client consolidation and increase

competition. Although the company owns one of the strongest pending

pipelines in the US (154 pending approvals) most existing launches are

likely to be loaded and 30+ product launches planned for FY18 are

unlikely to fill the void created by gGlumetza and gFortamet. However,

surprisingly the management is still guiding for 26-28% EBITDA margins

for FY18. It expects double digit growth in FY19 owing to exclusive and

limited competition launches like gWelchol, gRenagel and gRanexa. India

and Japan are likely to remain strong. However due to persisting US

pricing pressure, we have reduced our FY18, FY19 EPS estimates by 17%

and 20%, respectively. Our new target price is | 1335 based on 20x (21x

earlier) FY19E EPS of | 66.8. The stock has corrected ~35% from its 52

week high level, which we believe is overdone.

Exhibit 12: One year forward PE

0

500

1000

1500

2000

2500

Feb-0

7

Aug-0

7

Feb-0

8

Aug-0

8

Feb-0

9

Aug-0

9

Feb-1

0

Aug-1

0

Feb-1

1

Aug-1

1

Feb-1

2

Aug-1

2

Feb-1

3

Aug-1

3

Feb-1

4

Aug-1

4

Feb-1

5

Aug-1

5

Feb-1

6

Aug-1

6

Feb-1

7

Price 29.4x 21.8x 19.3x 9.2x 4.1x

[

Source: Company, ICICIdirect.com Research

Exhibit 13: One year forward PE of company vs. CNX Pharma

0

5

10

15

20

25

30

35

40

45

Feb-07

Aug-07

Feb-08

Aug-08

Feb-09

Aug-09

Feb-10

Aug-10

Feb-11

Aug-11

Feb-12

Aug-12

Feb-13

Aug-13

Feb-14

Aug-14

Feb-15

Aug-15

Feb-16

Aug-16

Feb-17

(x)

Lupin CNX Pharma

3.9% Premium

Source: Company, ICICIdirect.com Research

Exhibit 14: Valuation

Revenues Growth EPS Growth P/E EV/EBITDA RoNW RoCE

(| crore) (%) (|) (%) (x) (X) (%) (%)

FY16 14209 11.3 50.4 -5.5 22.6 15.4 20.7 18.6

FY17E 17466 22.9 56.6 12.3 20.1 13.0 19.1 17.2

FY18E 17834 2.1 56.2 -0.7 20.3 12.2 16.4 16.7

FY19E 19597 9.9 66.8 18.8 17.1 10.2 16.8 19.0

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 10

Recommendation history vs. Consensus

0

500

1,000

1,500

2,000

2,500

Jan-17Nov-16Aug-16Jun-16Mar-16Jan-16Oct-15Aug-15Jun-15Mar-15Jan-15

(|

)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

(%

)

Price Idirect target Consensus Target Mean % Consensus with BUY

Source: Reuters, Company, ICICIdirect.com Research

Key events

Date Event

Sep-11 Receives USFDA approval for its first oral contraceptive drug norethindrone tablets

Nov-11 Japanese subsidiary Kyowa acquires specialty injectables company I’rom Pharmaceutical

Aug-13 Signs an agreement with Romark Laboratories, which provides exclusive rights to Lupin to promote, distribute and market Alinia (nitazoxanide) oral suspension

brand in the US market

Feb-14 Acquires Dutch firm Nanomi B.V. for an undisclosed amount, foraying into the technology intensive complex injectables space.

Mar-14 Acquires Mexico-based ophthalmic drugs maker Laboratories Grin

Apr-15 Consolidated Pharma Dynamics business in South Africa

May-15 Lupin acquires Brazil's Medquimica Industria Farmaceutica SA

Jul-15 Lupin's Goa facility recieves nine Form 483 observations

Jul-15 Lupin acquires Gavis Pharmaceuticals for US$ 880 million to strengthen its US portfolio

Jul-15 Closes Temmler acquisition in Germany

Mar-16 Completes Gavis acquisition

Jul-16 Goa facility receives establishment inspection report (EIR) from USFDA for July 2015 inspectation

Aug-16 Acquires 21 generic brands from Japan’s Shionogi for $150 million

Nov-16 Goa facility receives establishment inspection report (EIR) from USFDA for March 2016 inspectation

Apr-17 Lupin's Goa facility receives three Form 483 observations from USFDA

May-17 Lupin's Aurangabad facility receives nine Form 483 observations from USFDA

May-17 Opens 100,000 square foot expansion of its manufacturing facilities in Somerset, New Jersey

May-17 Indore facility receives six Form 483 observations from USFDA

Source: Company, ICICIdirect.com Research

Top 10 Shareholders Shareholding Pattern

Rank Investor Name Latest Filing Date % O/S Position Position Change

1 Zyma Laboratories, Ltd. 31-Mar-17 12.32 55.7m 0.0m

2 Rahas Investments Pvt. Ltd. 31-Mar-17 10.20 46.1m 0.0m

3 Visiomed Investments Pvt. Ltd. 31-Mar-17 9.77 44.1m 0.0m

4 Lupin Marketing Pvt. Ltd. 31-Mar-17 9.04 40.8m 0.0m

5 Lupin Investments Pvt. Ltd. 31-Mar-17 3.41 15.4m 0.0m

6 Stewart Investors 31-Mar-17 2.60 11.8m 0.2m

7 First State Investments (HK) Ltd. 31-Mar-17 2.43 11.0m 9.7m

8 National Westminster Bank Plc 31-Dec-16 2.43 11.0m 0.0m

9 Capital World Investors 31-Dec-16 1.75 7.9m 0.0m

10 Jhunjhunwala (Rakesh Radheshyam) 31-Mar-17 1.73 7.8m -0.5m

(in %) Mar-16 Jun-16 Sep-16 Dec-16 Mar-16

Promoter 46.5 46.8 46.8 46.7 46.7

Others 53.5 53.2 53.2 53.3 53.3

Source: Reuters, ICICIdirect.com Research

Recent Activity

Investor name Value ($) Shares Investor name Value ($) Shares

First State Investments (HK) Ltd. 216.5m 9.7m Capital International Investors -134.2m -6.0m

Capital International, Inc. 10.2m 0.5m Lupin International Pvt. Ltd. -40.8m -1.9m

ICICI Prudential Asset Management Co. Ltd. 7.6m 0.3m Abu Dhabi Investment Authority -21.6m -1.0m

DSP BlackRock Investment Managers Pvt. Ltd. 5.5m 0.2m Lyxor Asset Management -18.7m -0.8m

UTI Asset Management Co. Ltd. 4.4m 0.2m Jhunjhunwala (Rakesh Radheshyam) -11.1m -0.5m

Buys Sells

Source: Reuters, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 11

.

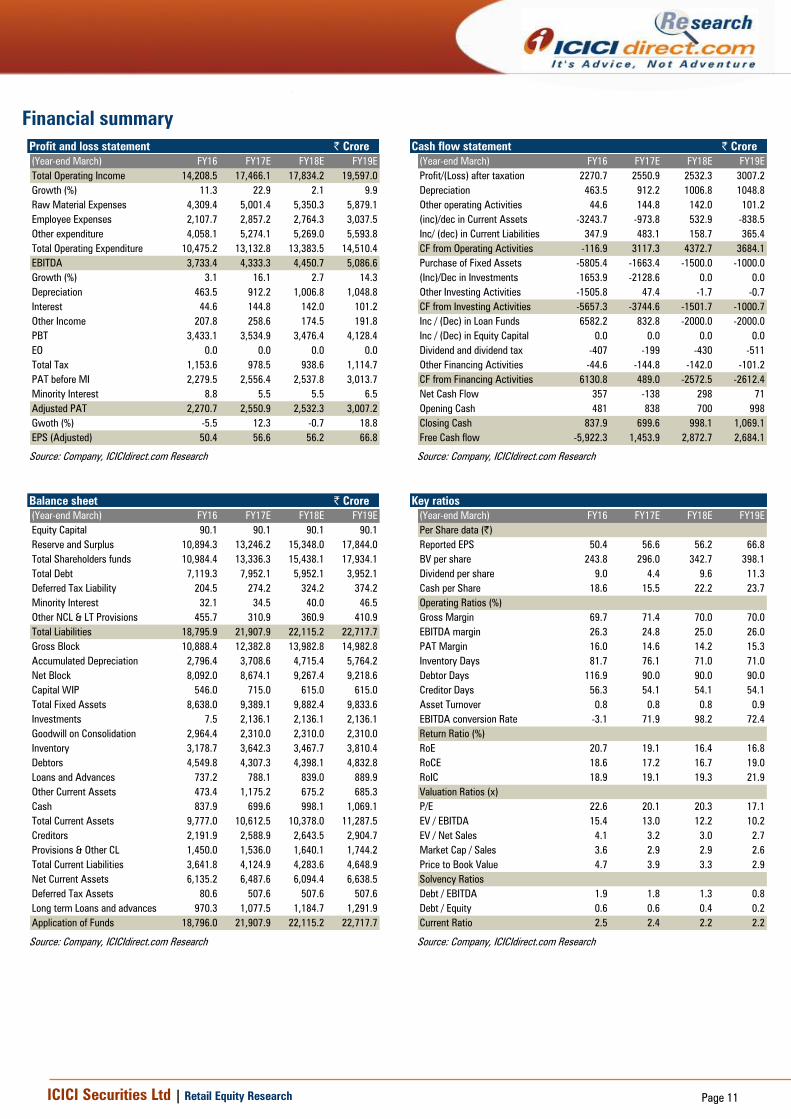

Financial summary

Profit and loss statement | Crore

(Year-end March) FY16 FY17E FY18E FY19E

Total Operating Income 14,208.5 17,466.1 17,834.2 19,597.0

Growth (%) 11.3 22.9 2.1 9.9

Raw Material Expenses 4,309.4 5,001.4 5,350.3 5,879.1

Employee Expenses 2,107.7 2,857.2 2,764.3 3,037.5

Other expenditure 4,058.1 5,274.1 5,269.0 5,593.8

Total Operating Expenditure 10,475.2 13,132.8 13,383.5 14,510.4

EBITDA 3,733.4 4,333.3 4,450.7 5,086.6

Growth (%) 3.1 16.1 2.7 14.3

Depreciation 463.5 912.2 1,006.8 1,048.8

Interest 44.6 144.8 142.0 101.2

Other Income 207.8 258.6 174.5 191.8

PBT 3,433.1 3,534.9 3,476.4 4,128.4

EO 0.0 0.0 0.0 0.0

Total Tax 1,153.6 978.5 938.6 1,114.7

PAT before MI 2,279.5 2,556.4 2,537.8 3,013.7

Minority Interest 8.8 5.5 5.5 6.5

Adjusted PAT 2,270.7 2,550.9 2,532.3 3,007.2

Gwoth (%) -5.5 12.3 -0.7 18.8

EPS (Adjusted) 50.4 56.6 56.2 66.8

Source: Company, ICICIdirect.com Research

Cash flow statement | Crore

(Year-end March) FY16 FY17E FY18E FY19E

Profit/(Loss) after taxation 2270.7 2550.9 2532.3 3007.2

Depreciation 463.5 912.2 1006.8 1048.8

Other operating Activities 44.6 144.8 142.0 101.2

(inc)/dec in Current Assets -3243.7 -973.8 532.9 -838.5

Inc/ (dec) in Current Liabilities 347.9 483.1 158.7 365.4

CF from Operating Activities -116.9 3117.3 4372.7 3684.1

Purchase of Fixed Assets -5805.4 -1663.4 -1500.0 -1000.0

(Inc)/Dec in Investments 1653.9 -2128.6 0.0 0.0

Other Investing Activities -1505.8 47.4 -1.7 -0.7

CF from Investing Activities -5657.3 -3744.6 -1501.7 -1000.7

Inc / (Dec) in Loan Funds 6582.2 832.8 -2000.0 -2000.0

Inc / (Dec) in Equity Capital 0.0 0.0 0.0 0.0

Dividend and dividend tax -407 -199 -430 -511

Other Financing Activities -44.6 -144.8 -142.0 -101.2

CF from Financing Activities 6130.8 489.0 -2572.5 -2612.4

Net Cash Flow 357 -138 298 71

Opening Cash 481 838 700 998

Closing Cash 837.9 699.6 998.1 1,069.1

Free Cash flow -5,922.3 1,453.9 2,872.7 2,684.1

Source: Company, ICICIdirect.com Research

Balance sheet | Crore

(Year-end March) FY16 FY17E FY18E FY19E

Equity Capital 90.1 90.1 90.1 90.1

Reserve and Surplus 10,894.3 13,246.2 15,348.0 17,844.0

Total Shareholders funds 10,984.4 13,336.3 15,438.1 17,934.1

Total Debt 7,119.3 7,952.1 5,952.1 3,952.1

Deferred Tax Liability 204.5 274.2 324.2 374.2

Minority Interest 32.1 34.5 40.0 46.5

Other NCL & LT Provisions 455.7 310.9 360.9 410.9

Total Liabilities 18,795.9 21,907.9 22,115.2 22,717.7

Gross Block 10,888.4 12,382.8 13,982.8 14,982.8

Accumulated Depreciation 2,796.4 3,708.6 4,715.4 5,764.2

Net Block 8,092.0 8,674.1 9,267.4 9,218.6

Capital WIP 546.0 715.0 615.0 615.0

Total Fixed Assets 8,638.0 9,389.1 9,882.4 9,833.6

Investments 7.5 2,136.1 2,136.1 2,136.1

Goodwill on Consolidation 2,964.4 2,310.0 2,310.0 2,310.0

Inventory 3,178.7 3,642.3 3,467.7 3,810.4

Debtors 4,549.8 4,307.3 4,398.1 4,832.8

Loans and Advances 737.2 788.1 839.0 889.9

Other Current Assets 473.4 1,175.2 675.2 685.3

Cash 837.9 699.6 998.1 1,069.1

Total Current Assets 9,777.0 10,612.5 10,378.0 11,287.5

Creditors 2,191.9 2,588.9 2,643.5 2,904.7

Provisions & Other CL 1,450.0 1,536.0 1,640.1 1,744.2

Total Current Liabilities 3,641.8 4,124.9 4,283.6 4,648.9

Net Current Assets 6,135.2 6,487.6 6,094.4 6,638.5

Deferred Tax Assets 80.6 507.6 507.6 507.6

Long term Loans and advances 970.3 1,077.5 1,184.7 1,291.9

Application of Funds 18,796.0 21,907.9 22,115.2 22,717.7

Source: Company, ICICIdirect.com Research

Key ratios

(Year-end March) FY16 FY17E FY18E FY19E

Per Share data (|)

Reported EPS 50.4 56.6 56.2 66.8

BV per share 243.8 296.0 342.7 398.1

Dividend per share 9.0 4.4 9.6 11.3

Cash per Share 18.6 15.5 22.2 23.7

Operating Ratios (%)

Gross Margin 69.7 71.4 70.0 70.0

EBITDA margin 26.3 24.8 25.0 26.0

PAT Margin 16.0 14.6 14.2 15.3

Inventory Days 81.7 76.1 71.0 71.0

Debtor Days 116.9 90.0 90.0 90.0

Creditor Days 56.3 54.1 54.1 54.1

Asset Turnover 0.8 0.8 0.8 0.9

EBITDA conversion Rate -3.1 71.9 98.2 72.4

Return Ratio (%)

RoE 20.7 19.1 16.4 16.8

RoCE 18.6 17.2 16.7 19.0

RoIC 18.9 19.1 19.3 21.9

Valuation Ratios (x)

P/E 22.6 20.1 20.3 17.1

EV / EBITDA 15.4 13.0 12.2 10.2

EV / Net Sales 4.1 3.2 3.0 2.7

Market Cap / Sales 3.6 2.9 2.9 2.6

Price to Book Value 4.7 3.9 3.3 2.9

Solvency Ratios

Debt / EBITDA 1.9 1.8 1.3 0.8

Debt / Equity 0.6 0.6 0.4 0.2

Current Ratio 2.5 2.4 2.2 2.2

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 12

ICICIdirect.com coverage universe (Healthcare)

Company I-Direct CMP TP Rating M Cap

Code (|) (|) (| Cr) FY16 FY17E FY18E FY19E FY16 FY17E FY18E FY19E FY16 FY17E FY18E FY19E FY16 FY17E FY18E FY19E

Ajanta Pharma AJAPHA 1616 1,880 Buy 14222.9 45.4 58.5 61.7 72.4 35.6 27.6 26.2 22.3 42.9 40.6 33.8 31.7 34.2 32.6 27.0 25.2

Alembic Pharma ALEMPHA 570 615 Hold 10752.9 38.2 21.4 23.4 30.2 14.9 26.7 24.4 18.9 51.5 26.1 22.3 24.7 44.9 21.4 20.0 21.8

Apollo Hospitals APOHOS 1205 1,440 Buy 16768.1 26.7 20.9 24.2 35.6 45.1 57.7 49.9 33.8 9.2 7.5 8.4 11.4 10.8 7.9 8.4 11.2

Aurobindo Pharma AURPHA 526 965 Buy 30791.1 33.9 38.7 39.5 49.1 15.5 13.6 13.3 10.7 23.3 23.6 20.9 22.6 28.1 24.6 20.3 20.5

Biocon BIOCON 934 1,020 Hold 18680.0 23.1 31.0 25.5 40.8 40.4 30.1 36.6 22.9 9.1 11.4 10.4 15.3 11.4 13.5 10.2 14.5

Cadila Healthcare CADHEA 427 425 Hold 43683.1 15.0 12.2 16.9 21.5 28.5 34.9 25.2 19.9 26.7 15.2 20.1 23.0 28.6 19.9 22.9 23.8

Cipla CIPLA 504.1 575 Hold 40557.3 18.5 17.2 24.3 31.4 27.3 29.3 20.7 16.0 12.0 10.5 13.9 16.4 12.5 10.6 13.2 14.9

Divi's Lab DIVLAB 550 700 Hold 14594.1 41.8 41.1 42.8 47.8 13.2 13.4 12.8 11.5 30.7 26.8 24.4 23.7 25.9 21.6 19.3 18.6

Dr Reddy's Labs DRREDD 2428 2,610 Hold 40221.1 141.4 68.6 106.1 137.3 17.2 35.4 22.9 17.7 17.3 6.3 10.8 13.7 20.6 9.4 13.0 14.7

Glenmark Pharma GLEPHA 612 910 Buy 17265.9 32.2 46.9 47.0 49.4 19.0 13.0 13.0 12.4 16.2 20.6 19.5 18.9 21.2 25.9 20.8 18.1

Indoco Remedies INDREM 192.4 235 Hold 1772.5 9.4 8.7 12.7 15.6 20.5 22.0 15.1 12.3 12.9 9.5 13.9 16.1 14.8 12.4 15.8 16.8

Ipca Laboratories IPCLAB 489 560 Hold 6172.3 10.0 15.0 24.1 31.1 48.8 32.5 20.3 15.7 5.7 9.8 12.7 14.8 5.5 7.8 11.3 13.0

Jubilant Life JUBLIF 709.9 810 Buy 11307.4 26.0 36.1 48.8 66.0 27.3 19.7 14.6 10.8 12.0 13.3 15.1 18.4 14.2 16.8 18.7 20.4

Lupin LUPIN 1140 1,760 Buy 51499.5 50.4 61.7 67.2 83.6 22.6 18.5 17.0 13.6 18.6 20.2 20.8 23.9 20.7 20.9 19.2 19.9

Natco Pharma NATPHA 889.9 870 Buy 15510.8 8.5 25.3 14.8 18.2 104.9 35.2 60.3 48.9 16.0 33.0 17.6 19.2 11.9 27.2 14.0 15.0

Sun Pharma SUNPHA 592 765 Buy 141986.5 23.4 30.4 30.1 35.5 25.2 19.4 19.7 16.7 18.6 19.3 17.2 17.9 18.0 19.5 16.6 16.9

Syngene Int. SYNINT 458 515 Hold 9152.0 11.1 14.3 14.4 18.4 40.5 31.2 31.0 24.3 13.2 16.8 16.0 18.1 21.0 21.9 18.4 19.1

Torrent Pharma TORPHA 1220 1,475 Buy 20645.3 107.8 57.0 62.1 77.4 11.3 21.4 19.7 15.8 46.7 21.5 23.7 26.4 53.8 23.5 21.4 22.2

Unichem Lab UNILAB 251.5 285 Hold 2286.2 12.3 12.9 17.4 23.5 20.4 19.5 14.5 10.7 13.8 14.3 16.1 18.8 11.7 11.1 13.3 15.6

RoE (%)EPS (|) PE(x) RoCE (%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 13

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless

specified and the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

m

ICICIdirect.com Research

Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional

target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities Ltd | Retail Equity Research Page 14

ANALYST CERTIFICATION

We /I, Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta MTech (Biotechnology) Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views

expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the

specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has its

various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are

available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and

other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their

relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant

solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior

written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also,

there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and

such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other

circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances.

The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial

positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The

value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind

arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before

investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in

the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in

the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta MTech (Biotechnology) Research Analysts of this report have not received any compensation from the companies

mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta MTech (Biotechnology) Research Analysts do not serve as an officer, director or employee of the companies

mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to

observe such restriction.

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances.

The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial

positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The

value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind

arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before

investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in

the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in

the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its analysts did not receive any compensation or

other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts have any material

conflict of interest at the time of publication of this report.

It is confirmed that Siddhant Khandekar CA-INTER Mitesh Shah MS (Finance), Harshal Mehta MTech (Biotechnology) Research Analysts of this report have not received any compensation from the companies

mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.