rating: buy the site paramount gold nevada corp (pzg ... · gold and silver corp. (pzg; buy)....

TRANSCRIPT

Initiating CoverageMetals and Mining

April 27, 2015

Paramount Gold Nevada Corp (PZG)Rating: Buy

Heiko F. Ihle, CFA212-356-0510

[email protected] Sekelsky212-356-0511

Awakening the Sleeping Giant; Initiating with a Buy

Stock Data 04/24/2015Price $1.71Exchange NYSEPrice Target $3.7052-Week High $2.0052-Week Low $1.40Enterprise Value (MM) $5Market Cap (MM) $15Shares Outstanding (MM) 8.5Short Interest (MM) 10.18Balance Sheet MetricsCash (MM) $10.0Total Debt (MM) $0.0Total Cash/Share $1.18

EPS DilutedFull Year - Dec 2014A 2015E 2016EFY 0.00 0.00 0.00Revenue ($M)Full Year - Dec 2014A 2015E 2016EFY 0.00 (0.34) (0.28)

1.6

1.4

1.2

1

0.8

0.6

0.4APR-14 AUG-14 DEC-14 APR-15

20

15

10

5

0

Vol. (mil) Price

Paramount Gold Nevada is a mining exploration companyfocused on its wholly-owned Sleeper Project. The new companyis a spin-out from the "old" Paramount Gold and Couer Mining (CDE;not rated) transaction, which closed on April 17, 2015. As a part of thetransaction, Paramount Gold and Silver's non-Mexican assets werespun-off into a new entity, Paramount Gold Nevada. The new entitywas seeded with $10.0 million in cash minus transaction expenses,in addition to the advanced exploration stage Sleeper asset and twoearly-stage exploration properties. We believe additional exploratorywork could aid in restarting production from the past producing, large-scale Sleeper Project. We are initiating coverage on Paramount GoldNevada with a Buy recommendation and a $3.70 price target.

The Sleeper Project is located approximately 25 miles fromWinnemucca, NV and reachable in about 3 hours by car fromReno, NV. We toured the property on April 22, 2015 and walkedaway with a good feeling about the future potential of the site. Wespent substantial time with Nancy Wolverson, the consulting geologistfor the site and left with a good impression of the exploration anddevelopment potential at the site.

The Sleeper Project has a history of past production. The sitewas first mined by Amax Gold from 1986 to 1996 and produced atotal of 1.6 million ounces of gold over the life of the mine. We notethat the property has been reclaimed with a Preliminary EconomicAssessment (PEA) completed by Paramount on the property in 2012and additional priority exploration targets. Given that initial capitalexpenditures at the site are expected to be approximately $350 million,coupled with the lower-grade nature of the deposit, we ultimatelycontend that higher gold prices are warranted before the Sleeperproject is advanced towards production unless a large high-gradedeposit is found.

We expect management to take an acquisitive stance. In ouropinion, management could choose to acquire or take a position in anadvanced exploration project that could provide the firm with near-termcash flow potential. We believe this strategy would be prudent giventhe fact that the firm's only material property at present may requirehigher gold prices and has a longer-term nature to first production.

We are initiating on Paramount Gold Nevada with a Buyrecommendation and a $3.70 per share price target. Our valuationis based on a DCF of anticipated operations at the Sleeper Project,in addition to the $10.0 million in cash on the firm's balance sheet.Given that we do not anticipate first production at Sleeper until 2020,coupled with the large CapEx required at the site, we utilize a 15%discount rate in our model. While we note that this discount rate couldbe lowered as the firm expands its material asset base beyond Sleeperand further de-risks the project.

Risks. 1) Gold price risk; 2) future funding requirements risk; 3)technical risk; 4) permitting risk and 5) political risk.

For definitions and the distribution of analyst ratings, analyst certifications, and other disclosures, please refer to pages 19 - 20 of this report.

Paramount Gold Nevada Summary

Paramount Gold Nevada is an exploration stage mining company located in Winnemucca, Nevada.

The firm was recently spun-out of the merger between Coeur Mining (CDE; not rated) and Paramount

Gold and Silver Corp. (PZG; Buy). Coeur’s interest in the acquisition related to Paramount’s San Miguel

Project in Chihuahua, Mexico. The asset owned by the “old” Paramount, San Miguel, covers

approximately 121,000 hectares surrounding Coeur’s Palmarejo mine complex, in addition to the Don Ese

deposit. We believe Don Ese played a large factor in the Coeur acquisition. Given’s Coeur’s sole

immediate interest San Miguel, Paramount’s non-Mexican assets and $10.0 million in cash were spun off

into a new entity, Paramount Gold Nevada, with Coeur retaining a 4.9% interest in the new company.

Paramount Gold Nevada’s principal asset is the Sleeper Gold Project in Nevada. The project is

located approximately 25 miles from Winnemucca, Nevada. The overall land package at Sleeper contains

roughly 34,000 acres. Notably, the vast land package extends to Newmont’s (NEM; not rated) Sandman

project, which Newmont acquired in the acquisition of Fronteer Gold in 2011 for approximately $2.3

billion. We highlight Sleeper’s vicinity to a major producer, which gives Sleeper the potential to possibly

be a joint-venture or acquisition target in the future—much like San Miguel.

Exhibit 1: Sleeper Mine Claims

Source: SRK NI 43-101 Technical Report Dated April 17, 2015.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 2

Sleeper Project Overview

The Sleeper Project has a history of past production. The site was first mined by Amax Gold from

1986 to 1996, and produced a total of 1.6 million ounces of gold. In fact, during the first year of production

the average cost was only $60 per ounce, which made Sleeper one of the lowest-cost gold mines in the

world. Notably, AMAX expected the asset to produce around 40,000 ounces of gold, but due to much

higher-than-anticipated grades at the site, the asset significantly outperformed expectations. While in

operation, AMAX processed higher grade ore (> 0.1 oz/t) through the on-site mill with lower grade ore

(0.006-0.1 oz/t) through a heap leach.

Exhibit 2: Location of Sleeper Project

Source: Paramount Gold.

Due to past production at the site, infrastructure, access to water and a large skilled labor pool is

available. The project is connected to a regional electrical grid and possesses road access to two major

highways. The town of Winnemucca, NV has a population of approximately 8,000 people, and currently

supports existing mining operations in the area. Given the large number of mining operations in Nevada

as a whole, we do not expect the sourcing of labor to be a major hindrance at Sleeper.

While power and water remain on site, all previous facilities and mining infrastructure have been

removed. Following the mine closure in 1996, the project’s facilities, including waste dumps, tailings,

leach pads, roads and open pits, were all reclaimed. While all previous mining equipment has been

removed from the site, the project still retains access to both power and water, in addition to the access

road. Currently Sleeper possesses access to power through power lines at the site while water can be

accessed through two wells located at the site.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 3

Reclamation efforts from past production at Sleeper have been successful. We highlight that the

reclamation efforts have received various awards, which we believe demonstrates to the surrounding

communities that safe sustainable mining can and does occur. Given this, we do not expect the firm to

have environmental or regulatory difficulty in bringing the project back into production in the future. We

note that while various permits are still required, including water, air quality, mine plan, and reclamation,

the firm has been taking baseline measures since closure of the mine, which could accelerate the

permitting process in the future.

The three open-pits at the site have since merged into one and accumulated water, which must be

pumped before mining can resume. While we don’t expect the de-watering to be a hindrance to

advancing the asset, we note that management expects the process to take about 6 months once

permitting is received, at a cost of approximately $1.0-2.0 million. Although the pits have not yet been

pumped out, Paramount conducted various drilling campaigns around the pit since 2010. (see Exhibit 3).

Exhibit 3: Drill-Hole Locations Outside Sleeper Pit

Source: Paramount Gold.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 4

The Sleeper Project Under Paramount’s Ownership

Paramount Gold and Silver began drilling the project in 2010. The drilling campaigns continued

through early 2013 with a total of 39 diamond core holes and 36 exploration holes drilled for a total of

24,282 meters. Further, 65 shallow RC holes were drilled for a total of 2,674 meters within the waste

dumps in an effort to determine the gold content of the dumps. While the initial program focused on the

West Wood and Facilities area of the project (see Exhibit 4), further exploration drilling uncovered the

South Sleeper and Pad mineralization at site.

Exhibit 4: West Wood and Facilities Areas

Source: SRK NI 43-101 Technical Report Dated April 17, 2015.

A Preliminary Economic Assessment (PEA) was completed on the property on June 30, 2012. The

study identified a 17-year mine life, with 29.2 million tonnes per year, or approximately 81,000 tonnes per

day, being processed through heap leach methodology. Further, the study estimates annual production of

172,000 ounces of gold and 263,000 ounces of silver. Given the lower-grade nature of mining operations

at Sleeper, as well as Nevada in general, we believe a heap leach scenario remains the most economical

method of operation. Under this scenario, cash costs at the project are expected to be approximately

$767 per ounce of gold equivalent produced.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 5

An updated resource estimate was released on the Sleeper Project on April 17, 2015. The updated

estimate outlined a large-tonnage, somewhat low-grade project. We highlight the increase in overall

resources at the site as the cutoff grade is lowered, providing the project is large optionality with respect

to higher future gold prices. We note that the project does have a large amount of Inferred resources, and

we believe these resources could be upgraded through future drilling at the site.

Exhibit 5: In-Pit Sleeper Resources

Source: SRK NI 43-101 Technical Report Dated April 17, 2015.

Outlook for the Sleeper Project for the Remainder of 2015

The firm expects to spend approximately $1.4 million at Sleeper over the next year. It is expected

that the majority of the exploration budget is to be focused on consulting, material modeling, and

metallurgical testing. Once the metallurgical testing at the site is complete, we expect management to

review the possibility of producing an updated PEA for the project. If Paramount decides to move forward

with a PEA at Sleeper, we expect the April 2015 updated resource estimate to be included in the revised

mine plan. The estimated cost for an updated PEA is approximately $300,000.

Assuming the project enters production, initial capital costs for the project are estimated to be

$346.2 million. Further, total CapEx throughout the mine life is estimated to be $687.8 million, including

$278.1 million in sustaining capital and $63.5 million in contingency capital. Given the somewhat large

amount of capital required to bring Sleeper into production, we believe a higher gold price may be

warranted in order to secure the necessary financing for the project.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 6

H.C. Wainwright Site Visit on April 21 - 22, 2015

On April 21, 2015, we had dinner in Reno, NV with Nancy Wolverson, a consulting geologist for the

Sleeper Project. This was followed by a visit to the project outside of Winnemucca, NV on April 22. At

dinner, we discussed further steps required to move Sleeper into production, in addition to progress made

at the site over the past year.

The “old” Paramount had primarily focused on the San Miguel project. Given that Sleeper is the sole

asset of the “new Paramount,” we expect continued focus on Sleeper going forward. Further, we note that

over the past year there has been some meaningful progress in reclamation work and additional work on

the updated resource and geologic model, which we expect to be released in 2015.

We spoke further about additional plans for the site for the remainder of 2015. The main goal of the

firm is to issue the updated resource, followed by an updated PEA. At present, the 2015 budget of $1.4

million is comprised of consulting, geological modelling and metallurgical testing.

After a 3.5 hour drive to site from Reno, mostly across I-80, a divided 4-lane road, we reached the

site. Although we did not drive through many cities, there is an ample supply of food, gasoline and other

essentials on the way and in Winnemucca. We highlight that the entire drive was on paved and state

maintained roads, with the exception of the last 5 miles, which were on a graded gravel road.

Exhibit 6: Five Mile Graded Gravel Road Accessing Sleeper

Source: H.C. Wainwright Sleeper Site Visit April 21-22, 2015.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 7

Although somewhat remote from major towns, we highlight that various projects are located

between Reno and Winnemucca, en-route to the Sleeper project. They include Coeur Mining’s

Rochester Mine 10 miles outside of Lovelock, Pershing Gold’s (PGLC; Buy) Relief Canyon project and a

variety of Rye Patch Gold (RPM; not rated) projects. There are also numerous small, privately-held mines

around. Further, we note that the Spring Valley deposit jointly owned by Barrick and Midway is located

close to the Rochester Mine.

Exhibit 7: The Florida Canyon Mine Owned by Jipangu (private) as Seen from I-80

Source: H.C. Wainwright Sleeper Site Visit April 21-22, 2015.

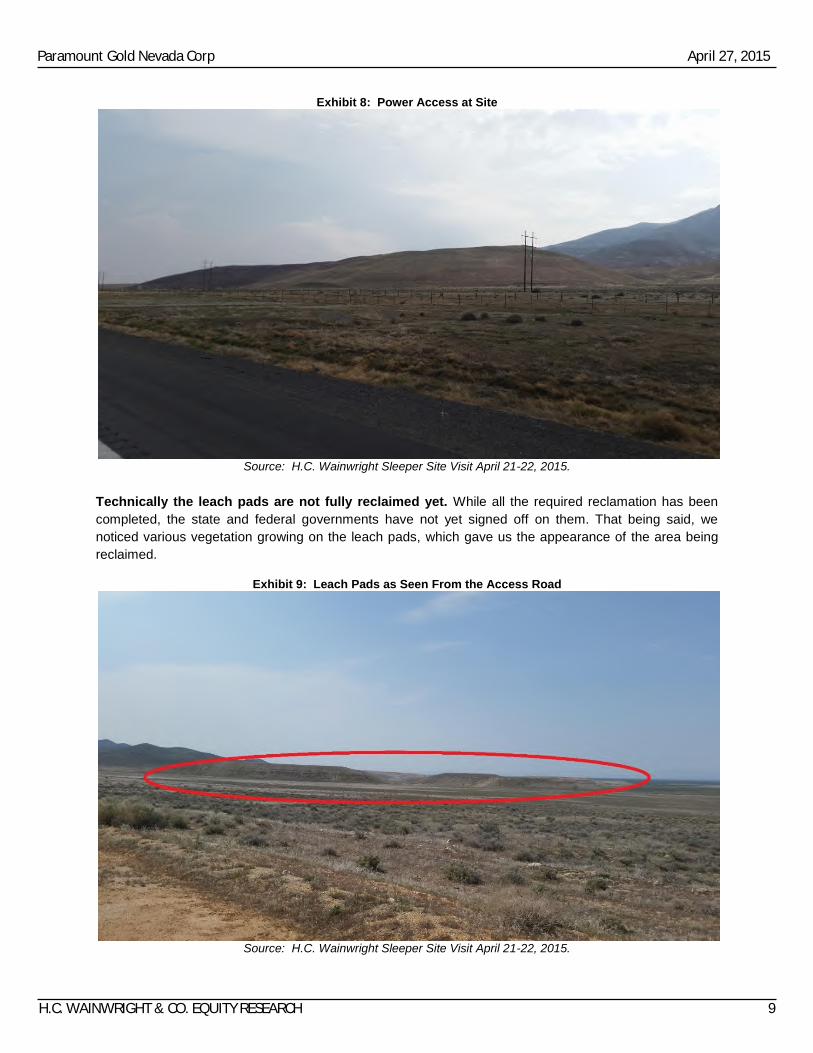

Upon entering the site, we immediately noticed the power lines and the decent condition of the

gravel road. While Paramount helps with the maintenance of the road, technically the county is

responsible for all maintenance work allowing for meaningful cost savings. The access road to site,

formally known as Sod House Road, has the width to comfortably fit two trucks, while there are still active

power lines from the days Sleeper was in operation.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 8

Exhibit 8: Power Access at Site

Source: H.C. Wainwright Sleeper Site Visit April 21-22, 2015.

Technically the leach pads are not fully reclaimed yet. While all the required reclamation has been

completed, the state and federal governments have not yet signed off on them. That being said, we

noticed various vegetation growing on the leach pads, which gave us the appearance of the area being

reclaimed.

Exhibit 9: Leach Pads as Seen From the Access Road

Source: H.C. Wainwright Sleeper Site Visit April 21-22, 2015.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 9

After arriving at site, we toured the machinery shop, which currently houses a large amount of

core in addition to some of the equipment kept at site. While the shop is starting to show its age, we

highlight that its large size allows for additional core or equipment to be stored on the property. The shop

has grid power and various fuel tanks for diesel and gasoline.

Exhibit 10: Core Located in the Machinery Shop

Source: H.C. Wainwright Sleeper Site Visit April 21-22, 2015.

Following the tour of the machinery shop, we proceeded to drive around the Sleeper Pit. The

length of the lake is currently approximately 1.2 kilometers by 500 meters. This pit includes the new South

Sleeper, the facilities oxide zone that is above the waterline, and the West Wood area. We also received

an overview of the various discoveries located below the pit.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 10

Exhibit 11: Various Areas Around the Sleeper Pit

Source: H.C. Wainwright Sleeper Site Visit April 21-22, 2015 and Nancy Wolverson, Geologist.

After touring the project, we drove about 45 minutes to the company’s Winnemucca office. While

relatively small, the office was well organized and had a number of maps and some of the higher-grade

core samples from the site. We note that some of these core samples were polished while most were in

their sawn, natural state.

Exhibit 12: Core Samples at Paramount Gold Nevada’s Winnemucca Office

Source: H.C. Wainwright Sleeper Site Visit April 21-22, 2015.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 11

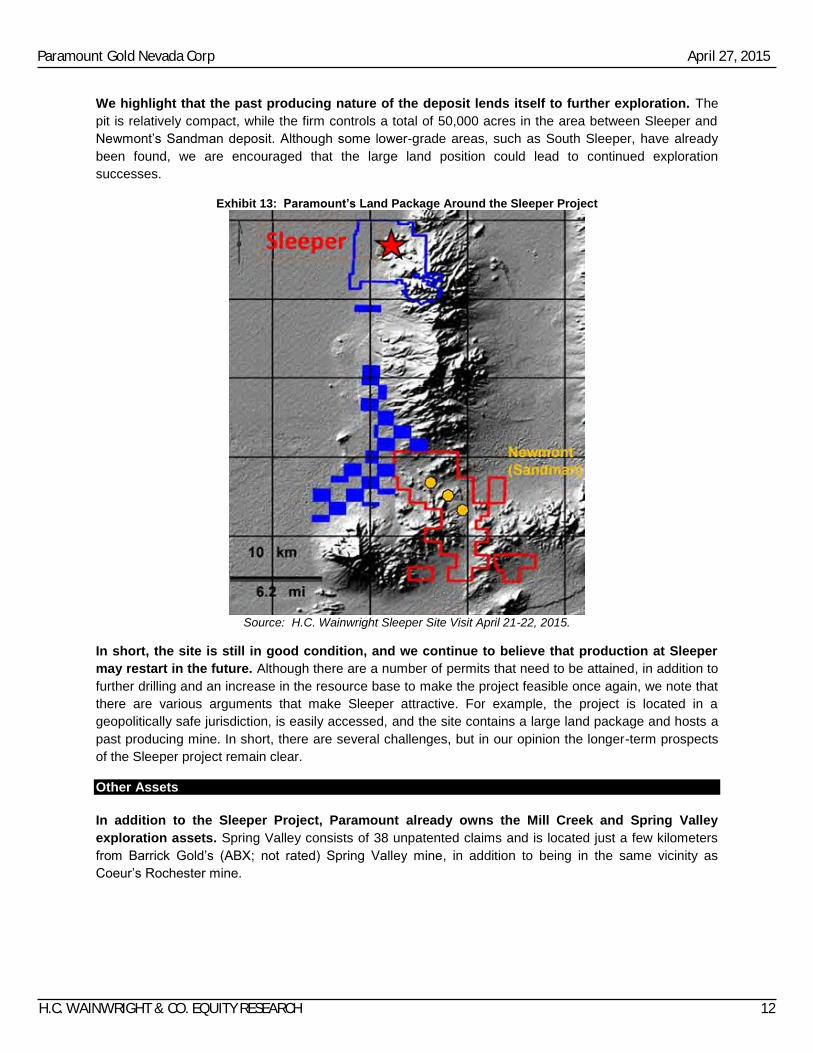

We highlight that the past producing nature of the deposit lends itself to further exploration. The

pit is relatively compact, while the firm controls a total of 50,000 acres in the area between Sleeper and

Newmont’s Sandman deposit. Although some lower-grade areas, such as South Sleeper, have already

been found, we are encouraged that the large land position could lead to continued exploration

successes.

Exhibit 13: Paramount’s Land Package Around the Sleeper Project

Source: H.C. Wainwright Sleeper Site Visit April 21-22, 2015.

In short, the site is still in good condition, and we continue to believe that production at Sleeper

may restart in the future. Although there are a number of permits that need to be attained, in addition to

further drilling and an increase in the resource base to make the project feasible once again, we note that

there are various arguments that make Sleeper attractive. For example, the project is located in a

geopolitically safe jurisdiction, is easily accessed, and the site contains a large land package and hosts a

past producing mine. In short, there are several challenges, but in our opinion the longer-term prospects

of the Sleeper project remain clear.

Other Assets

In addition to the Sleeper Project, Paramount already owns the Mill Creek and Spring Valley

exploration assets. Spring Valley consists of 38 unpatented claims and is located just a few kilometers

from Barrick Gold’s (ABX; not rated) Spring Valley mine, in addition to being in the same vicinity as

Coeur’s Rochester mine.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 12

Exhibit 14: Spring Valley Project Location

Source: Paramount Gold.

The firm’s Mill Creek property consists of 36 unpatented mining claims and is easily accessible by

all-weather roads. The property is within 35km of three mines, two of which are owned by Barrick. In

2005, a technical report was completed on the property, highlighting results from 26 drill holes. Due to the

results of the study, there remains a possibility that the mineralization met during the drilling is related to

major north, northwest, and northeast mineralized structures in the area.

We note the proximity of both Mill Creek and Spring Valley to “major” precious metals producers

in the area. Should mineralization from one of the surrounding properties extend to Mill Creek or Spring

Valley, the assets could be targets for additional drilling programs. Given the current capital market

sentiment towards non-producing, under-explored assets, we currently assign a zero dollar valuation to

these assets in our model. Further, we do not expect the firm to focus on advancing either asset in 2015.

While we are not expecting exploratory activities to occur at either property, we highlight the negligible

claim fees (approximately $11,000 per year) and believe the company should continue to maintain the

claims at both sites.

Valuation and Sensitivity Analysis

We currently value the Sleeper Project at $21.2 million, or $2.49 per share. We arrive at this

valuation based on a reasonably conservative discount rate of 15.0%, with construction at the site

estimated to begin in 2019. We utilize long-term gold and silver prices of $1,200 and $17.50 per ounce,

respectively. We note that we are currently anticipating first production at Sleeper in 2020, with production

of 254,000 ounces of gold and 576,000 ounces of silver for a total of 263,000 gold equivalent. While this

is higher than the expected annual production at Sleeper, our model currently assumes a higher-grade

scenario during the early years of production.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 13

Exhibit 15: Sleeper DCF Valuation

Source: H.C. Wainwright estimates.

Paramount currently holds $1.17 per share in cash. Given that the firm was seeded with $10.0 million

in cash prior to the spinout and currently has an enterprise value of approximately $4.5 million, we believe

the market is not only underpricing the potential of the Sleeper asset, but also management’s ability to

create shareholder value. As seen with the previous iteration of the “old” Paramount, the management

team including current Paramount Gold Nevada executives Glen Van Treek (President) and Carlo

Buffone (CFO), were able to successfully advance and ultimately transform San Miguel into an acquisition

target.

We note that our valuation of Sleeper is very sensitive to long-term gold prices as well as discount

rate utilized in our model. At Sleeper, for every $50 change in the price of gold our NAV for the asset

changes by $2.07-$3.82 per share. Further, our NAV estimate is impacted by $0.12-$1.26 per share for

every 0.50% change in discount rate. We note that due to the limited amount of silver estimated to be at

the site, variances in silver prices have a limited impact on our overall valuation of the asset.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 14

Exhibit 16: Sleeper Sensitivity Analysis

Source: H.C. Wainwright estimates.

The development of Sleeper continues to depend on precious metals prices. As seen in Exhibit 7,

our assessment of operations at Sleeper becomes negative below $1,150 per ounce gold at a 15%

discount rate. While we remain cognizant that our 15% discount rate may be conservative, we believe it is

warranted due to the fact that it is Paramount’s only material asset at the present time. Should the

company’s portfolio of assets continue to grow, perhaps through an outside acquisition, we believe the

possibility of lowering our discount rate remains. We think the company should have a more reasonable

time raising the required capital for Sleeper as a potentially larger company or with a revenue-generating

asset in the firm’s project portfolio.

Conclusion

We are initiating coverage on Paramount Gold Nevada with a Buy rating and $3.70 price target.

Our valuation is based on a DCF of anticipated operations at the Sleeper Project, in addition to the $10.0

million in cash on the firm's balance sheet. Given that we do not anticipate first production at Sleeper until

2020, coupled with the large capital expenditures required at the site, we utilize a 15% discount rate in

our model. We note that this discount rate could be lowered as the firm expands its material asset base

beyond Sleeper and further de-risks the project.

We expect management to take an acquisitive stance. While we expect the firm to continue to

advance the Sleeper Project with the potential release of an updated PEA in 2015, we believe

management is continuing to evaluate external growth opportunities. The firm set forth the strategic goal

of evaluating and potentially acquiring assets within the United States that are located near established

mining camps. Moreover, we think Paramount’s management could utilize its past success, as seen with

the sale of San Miguel, as a model for future projects. Ultimately, we believe the firm could attempt to

acquire an exploration stage asset and advance the asset to the PEA of full Feasibility Study level with

the goal of selling or entering into a joint-venture agreement prior to construction.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 15

Risk Factors

Paramount might face funding issues. Given the non-producing nature of the firm’s assets, Paramount

currently receives no cash flow from any of its properties. Thus, management may need to either raise

capital or sell assets in order to fund current operations.

Sleeper has a long lead-time until first production. We believe bringing Sleeper into production could

take several years. Given the current market sentiment regarding mining stocks, we note that some

investors may prefer projects with a more near-term production date.

The company may be forced into an unfavorable joint-venture with a major mining firm. Sleeper is

located near larger firms’ assets, which may make the project a candidate for a joint-venture agreement

or takeover altogether. If the firm faces funding issues in the future, management may be forced into

entering into a disadvantageous joint-venture or partnership.

Commodity price risk. Nearly all commodity-related equities are exposed to changes in the underlying

commodity. Investors may seek this exposure for the upside potential, but must recognize that the

exposure cuts both ways. Lower commodity prices could undoubtedly make attractive projects less

economically viable.

Cautionary Note to U.S. Investors: Estimates of Measured, Indicated and Inferred Resources “Measured Mineral Resources” and “Indicated Mineral Resources.” U.S. investors are advised that while those terms are recognized and required by Canadian regulations, the U.S. Securities and Exchange Commission (SEC) does not recognize them, and describes the equivalent as “Mineralized Material.” U.S. investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into mineral reserves. “Inferred Mineral Resources.” U.S. Investors are advised that while those terms are recognized and required by Canadian regulations, the SEC does not recognize it. “Inferred Mineral Resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. In accordance with Canadian rules, estimates of inferred mineral resources cannot form the basis of feasibility or other economic studies. U.S. investors are cautioned not to assume that part or all of the inferred mineral resource exists, or that it is economically or legally mineable.

Appendix A: Management Team

Glen van Treek, President: Mr. Van Treek is the President and a director of Paramount Gold Nevada

Corp. since February 2015. He was formerly the Chief Operating Officer and V.P. Exploration of

Paramount Gold and Silver Corp and served in this role from January 2011 through the April 2015 merger

with Coeur Mining, Inc. He has over 25 years of progressive global experience in all stages of mineral

exploration. Prior to joining Paramount, for ten years he held various senior positions at Teck Resources

Ltd. (TCK; not rated) and most recently he managed the production geology, resource modeling and

exploration programs at Teck’s Quebrada Blanca mine in Chile.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 16

Carlo Buffone, CFO: Mr. Buffone is the Chief Financial Officer of Paramount Gold Nevada Corp. He was

formerly the Chief Financial Officer of Paramount Gold and Silver Corp. and had served in this role since

February 2010 through the merger with Coeur Mining, Inc. in April 2015. Prior to joining Paramount, from

2005 to January 2010 Mr. Buffone founded a private company named Mama’s Boy Wines, which

developed sales channels for Italian artisanal wine makers. From 1995 to 2005, he held various senior

financial management positions including his employment as a corporate development specialist for CMA

Holdings Group, a wealth management firm with over $23 billion in assets under administration where he

was responsible for mergers and acquisitions. Mr. Buffone is a Certified Management Accountant (CMA)

and received his Bachelor of Commerce Degree from the University of Ottawa in 1993 and studied

mergers and acquisitions at the Kellogg School of Management at Northwestern University in 2004.

Appendix B: Terms

Ag Silver NI National Instrument

Au Gold NN Nearest Neighbor

cfm Cubic foot per minute NSR Net smelter return

cm Centimeters OK Ordinary Kriging

COG Cut-off grade oz Troy ounce

Cu Copper oz/t Troy ounce per tonne

g Grams ppm Parts per million

g/t Grams per tonne Pb Lead

ha Hectares QAQC Quality assurance/Quality control

kg Kilograms RMR Rock Mass Rating

km Kilometers RQD Rock Quality Designation

kg/t Kilogram per tonne t Metric tonne

lbs Pounds t/m3 Metric tonnes per cubic meter

m Meters tpd Metric tonnes per day

Ma Millions of years yr Year

masl Meters above sea level Zn Zinc

Moz Million troy ounces $US/t United States dollars per tonne

Mn Manganese $US/g US dollars per gram

Mt Million metric tonnes $US/% US dollars per percent

Acronym Description

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 17

Paramount Gold Nevada

Sleeper Project

2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E 2031E 2032E 2033E 2034E 2035E 2036ETonnes Processed (000's) - - - - - 29,200 29,200 29,190 29,200 29,200 29,200 29,190 29,200 29,250 24,610 29,200 29,200 29,200 29,200 29,200 29,200 29,200Gold grade (g/t) - - - 0.43 0.27 0.31 0.33 0.28 0.29 0.28 0.25 0.27 0.22 0.23 0.23 0.23 0.23 0.23 0.23 0.23Gold Recovery - - - 63% 81% 77% 67% 74% 73% 71% 86% 77% 87% 82% 82% 82% 82% 82% 82% 82%Annual gold production - - - - - 254 205 224 208 195 199 187 202 196 151 177 177 177 177 177 177 177 Gold sales price 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$ 1,200$

Silver grade (g/t) - - 5.1 5.0 4.6 3.2 2.6 3.0 3.1 1.9 3.7 2.8 3.9 3.9 3.9 3.9 3.9 3.9 3.9 Silver Recovery - - 11% 11% 10% 10% 11% 10% 10% 10% 10% 11% 12% 12% 12% 12% 12% 12% 12%Annual silver production - - - - - 576 567 478 325 299 309 321 198 377 269 476 476 476 476 476 476 476 Silver sales price 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ 17.5$ Gold:Silver ratio 69 69 69 69 69 69 69 69 69 69 69 69 69 69 69 69 69 69 69 69 69 69Total gold equivalent produced - - - - - 263 214 231 212 199 203 191 205 201 155 184 184 184 184 184 184 184

Total gold cash cost - - - (750) (750) (750) (750) (750) (750) (750) (750) (750) (750) (750) (750) (750) (750) (750) (750) (750) Gross profit (in 000's) - - - - - 118,219 96,108 103,940 95,540 89,495 91,461 86,063 92,125 90,449 69,914 82,797 82,797 82,797 82,797 82,797 82,797 82,797 CapEx (in 000's) (2,500) (2,500) (2,500) (10,000) (346,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) (25,000) Tax (in 000's) 30% 750 750 750 3,000 103,800 (27,966) (21,332) (23,682) (21,162) (19,348) (19,938) (18,319) (20,137) (19,635) (13,474) (17,339) (17,339) (17,339) (17,339) (17,339) (17,339) (17,339)

Operating cash flow (1,750) (1,750) (1,750) (7,000) (242,200) 65,253 49,775 55,258 49,378 45,146 46,522 42,744 46,987 45,815 31,440 40,458 40,458 40,458 40,458 40,458 40,458 40,458

Cash flow discount rate 15% 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21PV of operating cash flow (1,750) (1,522) (1,323) (4,603) (138,479) 32,442 21,519 20,773 16,142 12,833 11,500 9,188 8,782 7,446 4,443 4,972 4,324 3,760 3,269 2,843 2,472 2,150

Total current cash flow 21,182 Fully diluted shares 8,518Project NAV per share $2.49

Annual gold production - - - - - 254 205 224 208 195 199 187 202 196 151 177 177 177 177 177 177 177 Annual silver production - - - - - 576 567 478 325 299 309 321 198 377 269 476 476 476 476 476 476 476 Total gold equivalent - - - - - 263 214 231 212 199 203 191 205 201 155 184 184 184 184 184 184 184

Total PV of operating cash flow (1,750) (1,522) (1,323) (4,603) (138,479) 32,442 21,519 20,773 16,142 12,833 11,500 9,188 8,782 7,446 4,443 4,972 4,324 3,760 3,269 2,843 2,472 2,150 Current value of cash flow 21,182 2.49$ per share

Plus cash & equivalents 10,000 1.17$ per share

Plus exploratory assets 0

Less debt 0

Total current value 31,182

Common shares 8,518

Warrant 0

Options 0

Fully diluted shares 8,518

PZG share price in $ 1.70$

PZG NAV in US$ 3.66 53.6% discount to NAV

NAV Premium for target price 0%

Rounded Price Target 3.70 54.1% discount to NAV

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 18

Important Disclaimers

H.C. WAINWRIGHT & CO, LLC RATING SYSTEM: H.C. Wainwright employs a three tier rating system for evaluating boththe potential return and risk associated with owning common equity shares of rated firms. The expected return of any givenequity is measured on a RELATIVE basis of other companies in the same sector. The price objective is calculated to estimatethe potential movements in price that a given equity could reach provided certain targets are met over a defined time horizon.Price objectives are subject to external factors including industry events and market volatility.

RETURN ASSESSMENT

Market Outperform (Buy): The common stock of the company is expected to outperform a passive index comprised of all thecommon stock of companies within the same sector.Market Perform (Neutral): The common stock of the company is expected to mimic the performance of a passive indexcomprised of all the common stock of companies within the same sector.Market Underperform (Sell): The common stock of the company is expected to underperform a passive index comprised ofall the common stock of companies within the same sector.

Investment Banking Services include, but are not limited to, acting as a manager/co-manager in the underwriting or placementof securities, acting as financial advisor, and/or providing corporate finance or capital markets-related services to a companyor one of its affiliates or subsidiaries within the past 12 months.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 19

Distribution of Ratings TableIB Service/Past 12 Months

Ratings Count Percent Count PercentBuy 107 93.86% 43 40.19%Neutral 7 6.14% 1 14.29%Sell 0 0.00% 0 0.00%Under Review 0 0.00% 0 0.00%Total 114 100% 44 38.60%

H.C. Wainwright & Co, LLC (the “Firm”) is a member of FINRA and SIPC and a registered U.S. Broker-Dealer.

I, Heiko F. Ihle, CFA and Jake Sekelsky , certify that 1) all of the views expressed in this report accurately reflect my personalviews about any and all subject securities or issuers discussed; and 2) no part of my compensation was, is, or will be directlyor indirectly related to the specific recommendation or views expressed in this research report; and 3) neither myself nor anymembers of my household is an officer, director or advisory board member of these companies.

None of the research analysts or the research analyst’s household has a financial interest in the securities of ParamountGold Nevada Corp and Pershing Gold Corporation (including, without limitation, any option, right, warrant, future, long or shortposition).As of March 31, 2015 neither the Firm nor its affiliates beneficially own 1% or more of any class of common equity securitiesof Paramount Gold Nevada Corp and Pershing Gold Corporation .Neither the research analyst nor the Firm has any material conflict of interest in Paramount Gold Nevada Corp and PershingGold Corporation of which the research analyst knows or has reason to know at the time of publication of this research report.

The research analyst principally responsible for preparation of the report does not receive compensation that is based upon anyspecific investment banking services or transaction but is compensated based on factors including total revenue and profitabilityof the Firm, a substantial portion of which is derived from investment banking services.

The Firm or its affiliates did not receive compensation from Paramount Gold Nevada Corp and Pershing Gold Corporation forinvestment banking services within twelve months before, but will seek compensation from the companies mentioned in thisreport for investment banking services within three months following publication of the research report.

The Firm does not make a market in Paramount Gold Nevada Corp and Pershing Gold Corporation as of the date of thisresearch report.

The information contained herein is based on sources which we believe to be reliable but is not guaranteed by us as beingaccurate and does not purport to be a complete statement or summary of the available data on the company, industry or securitydiscussed in the report. All opinions and estimates included in this report constitute the analyst’s judgment as of the date ofthis report and are subject to change without notice.

The securities of the company discussed in this report may be unsuitable for investors depending on their specific investmentobjectives and financial position. Past performance is no guarantee of future results. This report is offered for informationalpurposes only, and does not constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdictionwhere such would be prohibited. No part of this report may be reproduced in any form without the expressed permission ofH.C. Wainwright & Co, LLC. Additional information available upon request.

Paramount Gold Nevada Corp April 27, 2015

H.C. WAINWRIGHT & CO. EQUITY RESEARCH 20