randon s.a. implementos e participaÇÕes automotive … challenge 2013... · autometal sa 5.9x 11x...

TRANSCRIPT

Universidade Federal de Santa Catarina Marco Arruda, Gustavo Busnardo, Richard Schnorrenberger, Evelin Silva, Thais Pabis São Paulo, November 2013

RANDON S.A. IMPLEMENTOS E PARTICIPAÇÕES Automotive Industry

Introduction Investment Case Risks Conclusion

INTRODUTION

Introduction Investment Case Risks Conclusion

INTRODUTION

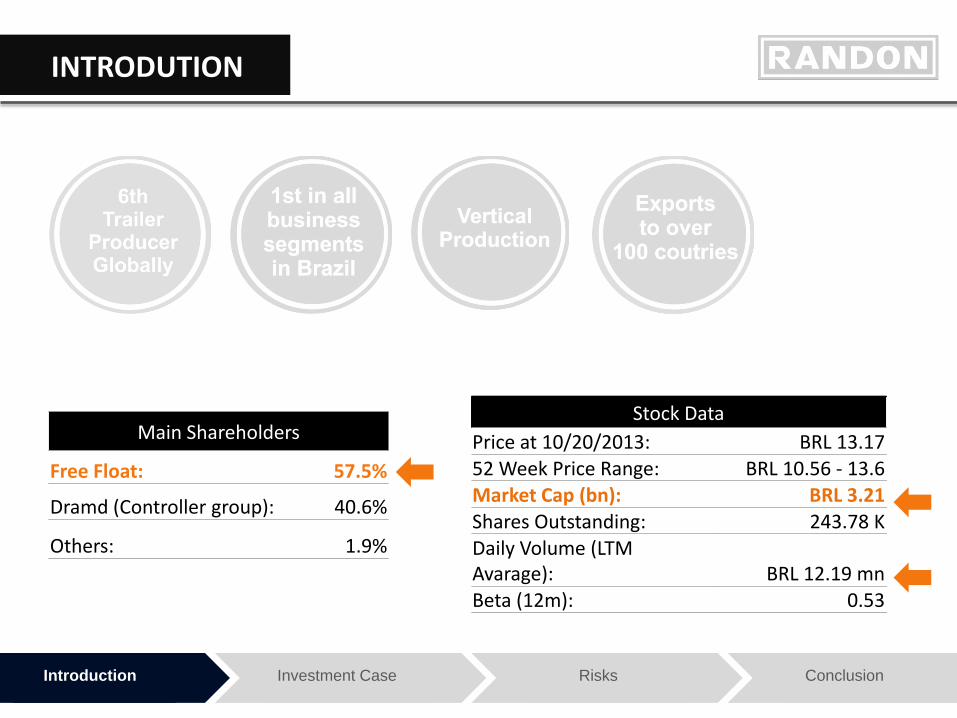

Main Shareholders

Free Float: 57.5%

Dramd (Controller group): 40.6%

Others: 1.9%

Stock Data Price at 10/20/2013: BRL 13.17 52 Week Price Range: BRL 10.56 - 13.6 Market Cap (bn): BRL 3.21 Shares Outstanding: 243.78 K Daily Volume (LTM Avarage): BRL 12.19 mn Beta (12m): 0.53

Main Shareholders

Free Float: 57.5%

Dramd (Controller group): 40.6%

Others: 1.9%

Stock Data Price at 10/20/2013: BRL 13.17 52 Week Price Range: BRL 10.56 - 13.6 Market Cap (bn): BRL 3.21 Shares Outstanding: 243.78 K Daily Volume (LTM Avarage): BRL 12.19 mn Beta (12m): 0.53

Stock Data Price at 10/20/2013: BRL 13.17 52 Week Price Range: BRL 10.56 - 13.6 Market Cap (bn): BRL 3.21 Shares Outstanding: 243.78 K Daily Volume (LTM Avarage): BRL 12.19 mn Beta (12m): 0.53

Introduction Investment Case Risks Conclusion

INTRODUTION

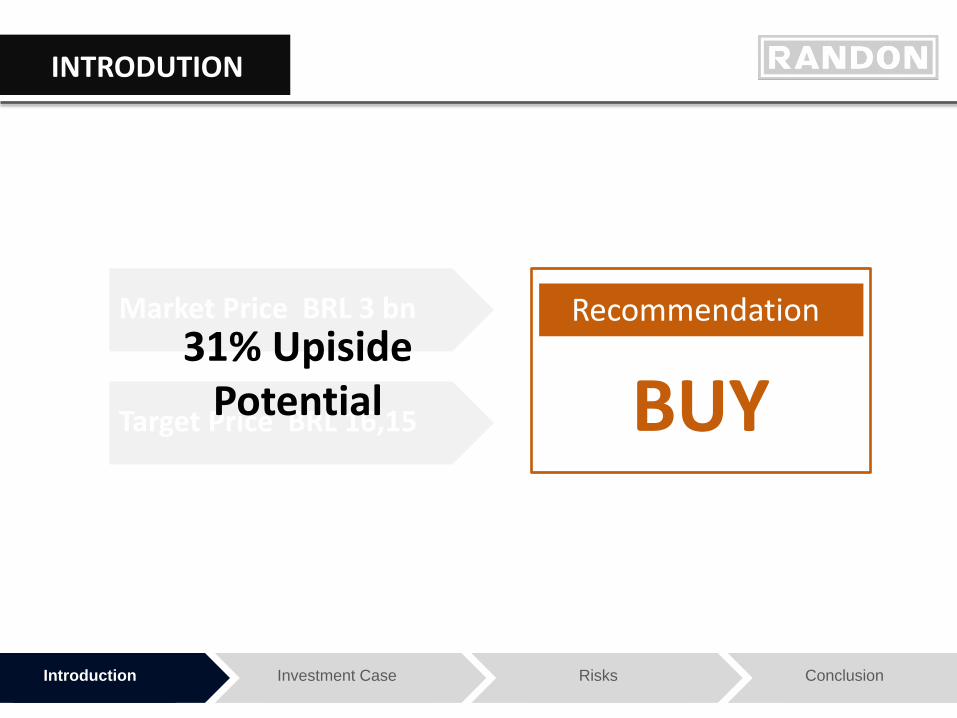

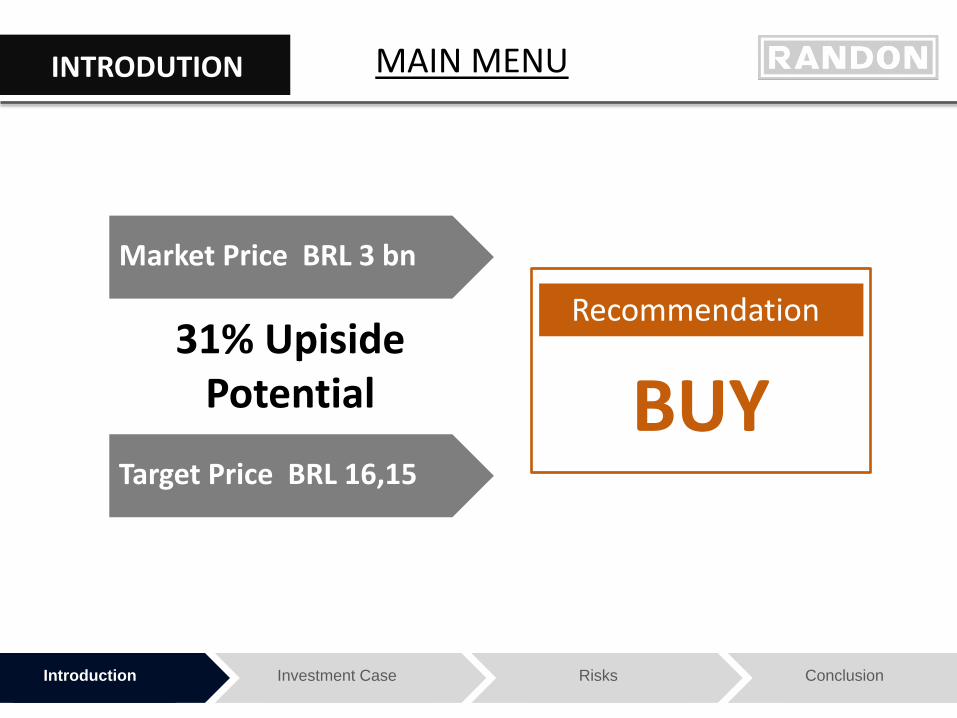

Market Price BRL 3 bn

Target Price BRL 16,15 BUY Recommendation

31% Upiside Potential

Net revenue per segment

Introduction Investment Case Risks Conclusion

BUSINESS DESCTIPTION

Vehicles and

trailers 51%

Auto parts 47%

Financial services

2%

Truck trailers

83%

Special vehicles

10%

Rail Wagons 7%

Suspension Systems

36%

Friction materials

34%

Air Brakes 21%

Castings 9%

Introduction Investment Case Risks Conclusion

WHY BUY?

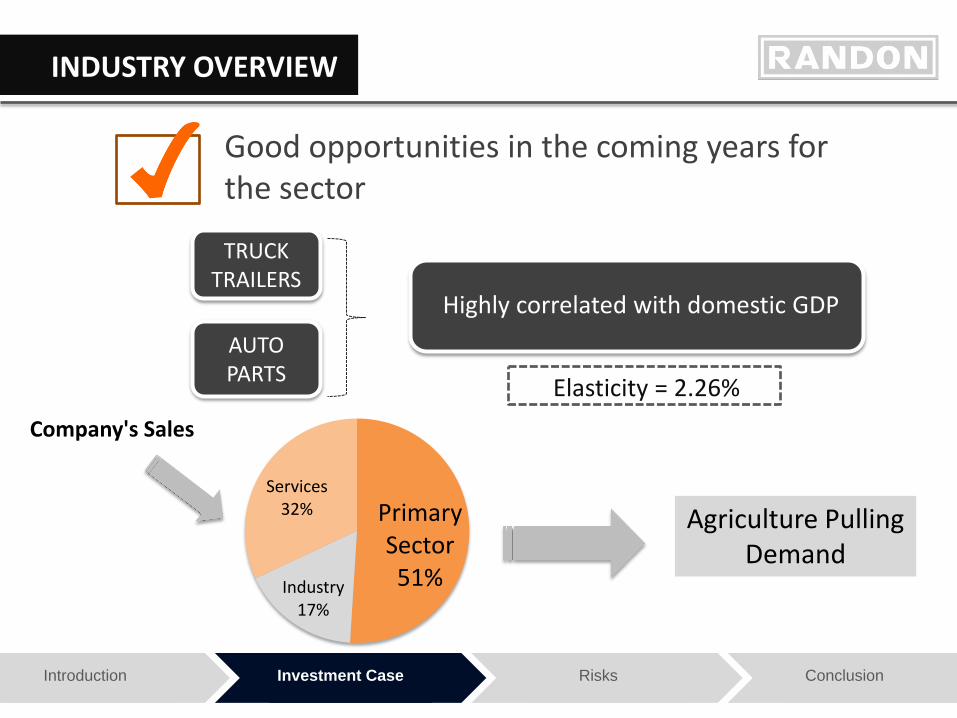

Good opportunities in the coming years for the sector

Confirmative Valuation

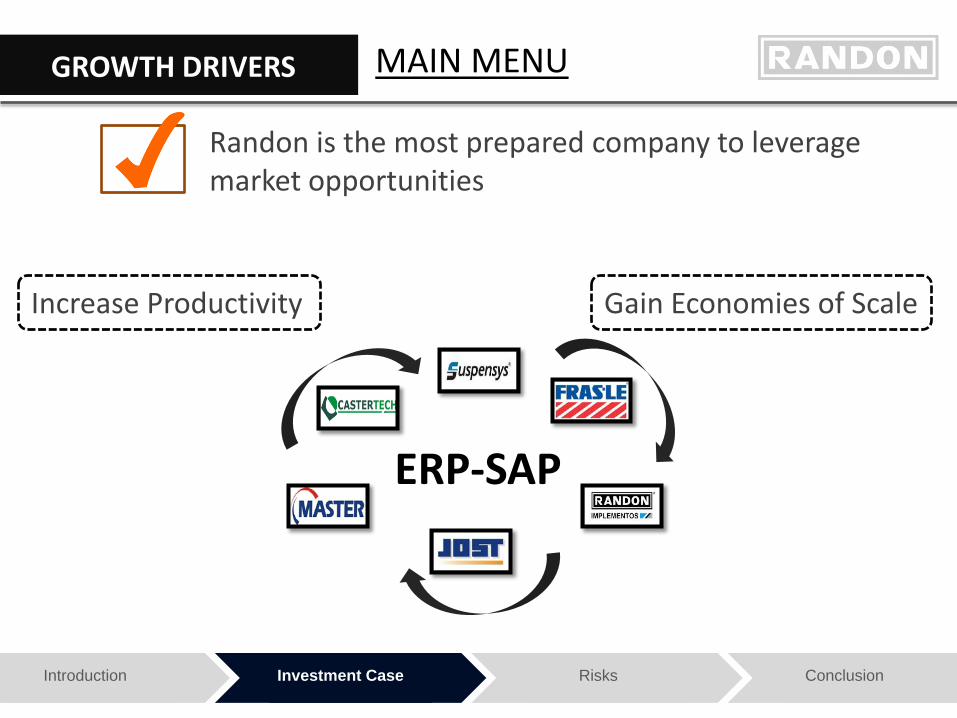

Randon is the most prepared company to leverage market opportunities

Introduction Investment Case Risks Conclusion

INDUSTRY OVERVIEW

TRUCK TRAILERS

AUTO PARTS

Highly correlated with domestic GDP

Elasticity = 2.26%

Primary Sector 51% Industry

17%

Services 32%

Company's Sales

Agriculture Pulling Demand

Good opportunities in the coming years for the sector

Introduction Investment Case Risks Conclusion

INDUSTRY OVERVIEW

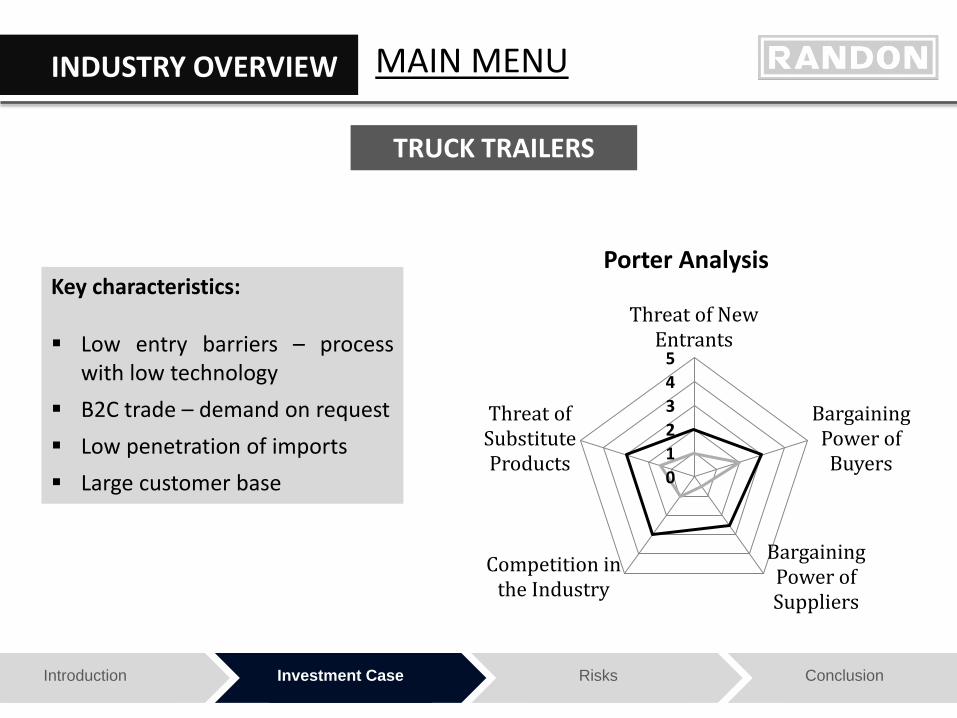

Porter Analysis Key characteristics:

Low entry barriers – process

with low technology

B2C trade – demand on request

Low penetration of imports

Large customer base 0 1 2 3 4 5

Threat of New Entrants

Bargaining Power of Buyers

Bargaining Power of Suppliers

Competition in the Industry

Threat of Substitute Products

TRUCK TRAILERS

Introduction Investment Case Risks Conclusion

INDUSTRY OVERVIEW

Porter Analysis Key characteristics: High entry barriers – requires

high technology processes

B2B trade – concentrated customer base

Joint engineering strategy - integration between subsidiaries

Drivers: domestic and international automotive production and aftermarket needs.

0 1 2 3 4 5

Threat of New Entrants

Bargaining Power of Buyers

Bargaining Power of Suppliers

Competition in the Industry

Threat of Substitute Products

AUTO PARTS

Introduction Investment Case Risks Conclusion

INDUSTRY OVERVIEW

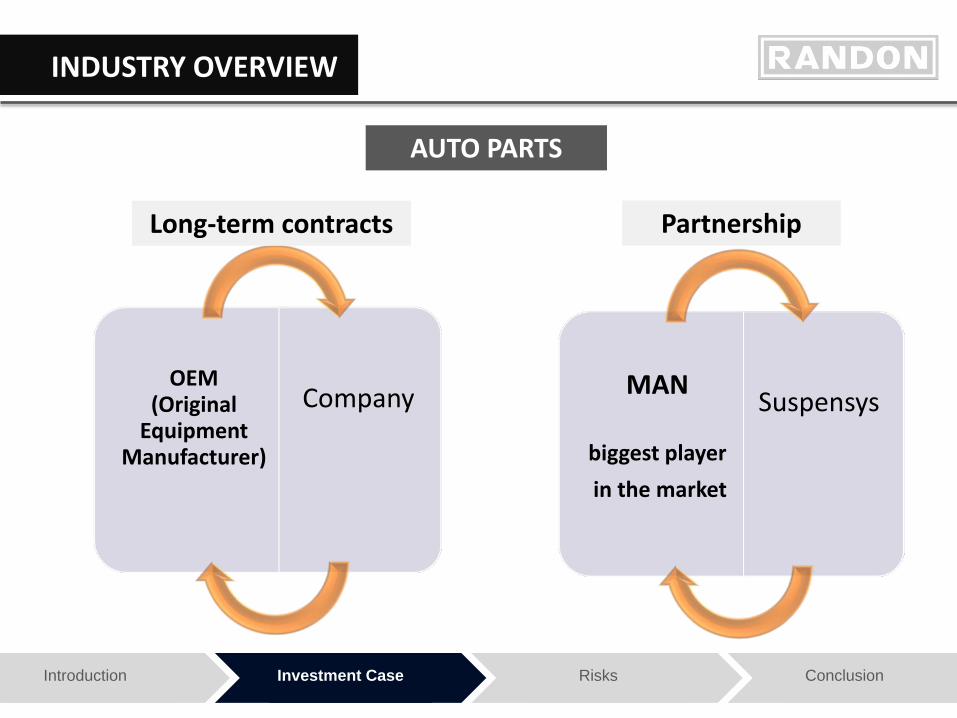

AUTO PARTS

OEM

(Original Equipment

Manufacturer)

Company

Long-term contracts

MAN

biggest player in the market

Suspensys

Partnership

Introduction Investment Case Risks Conclusion

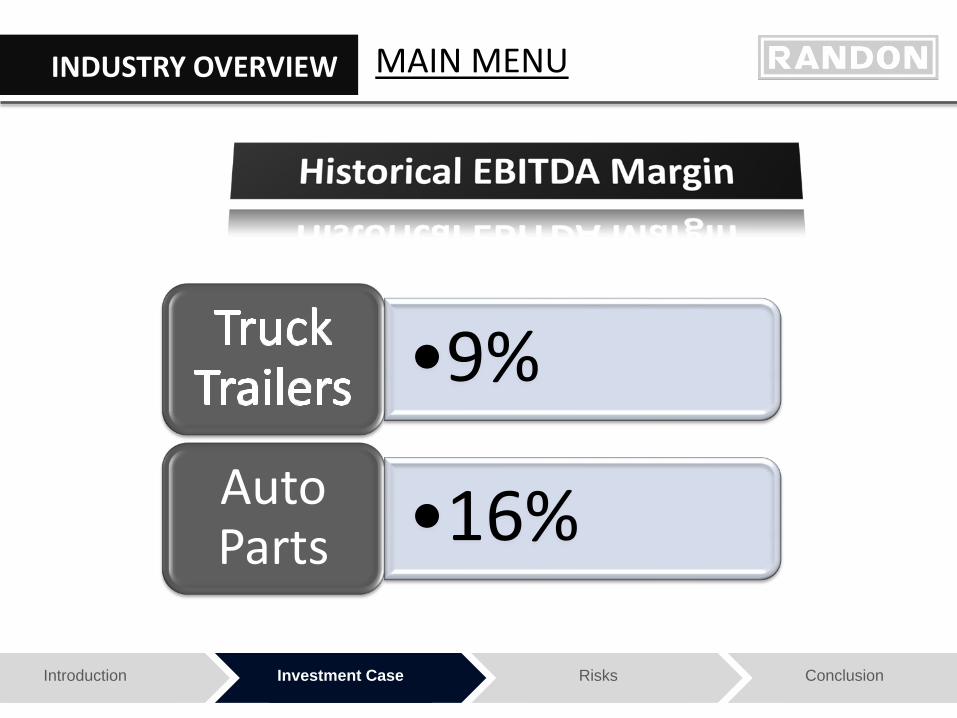

INDUSTRY OVERVIEW

•9%

•16% Auto Parts

Introduction Investment Case Risks Conclusion

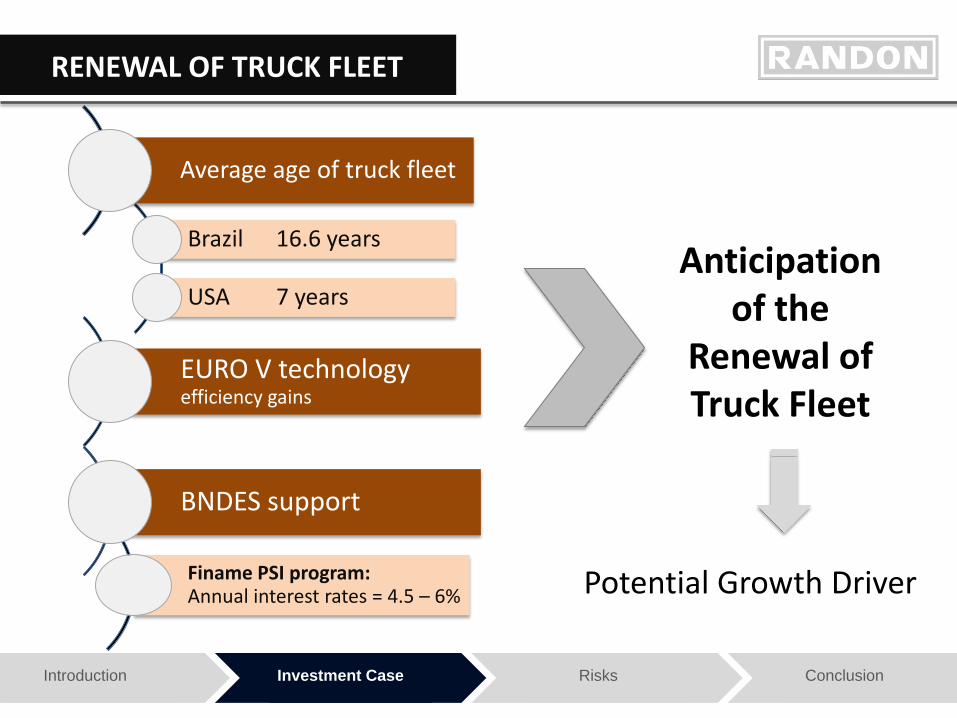

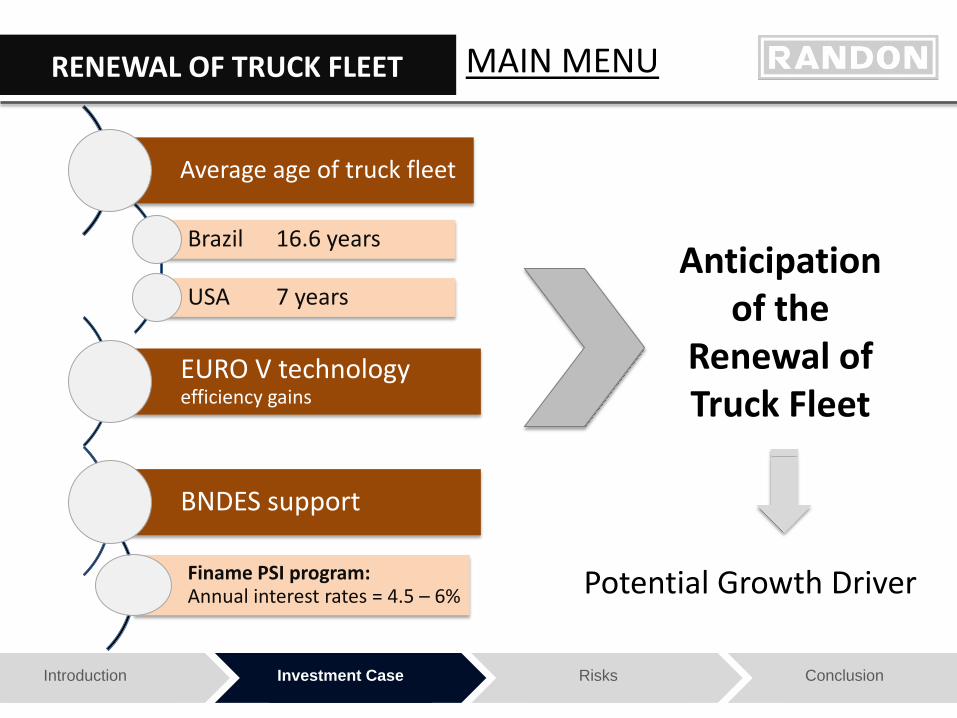

RENEWAL OF TRUCK FLEET

Brazil 16.6 years

USA 7 years

EURO V technology efficiency gains

Average age of truck fleet

Finame PSI program: Annual interest rates = 4.5 – 6%

Anticipation of the

Renewal of Truck Fleet

Potential Growth Driver

BNDES support

Introduction Investment Case Risks Conclusion

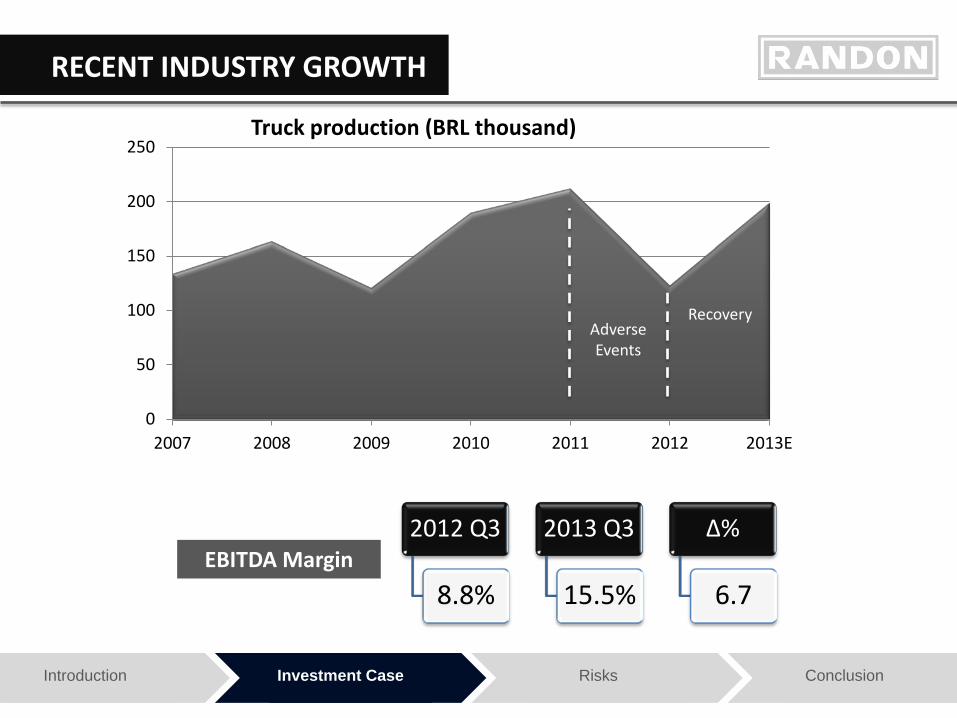

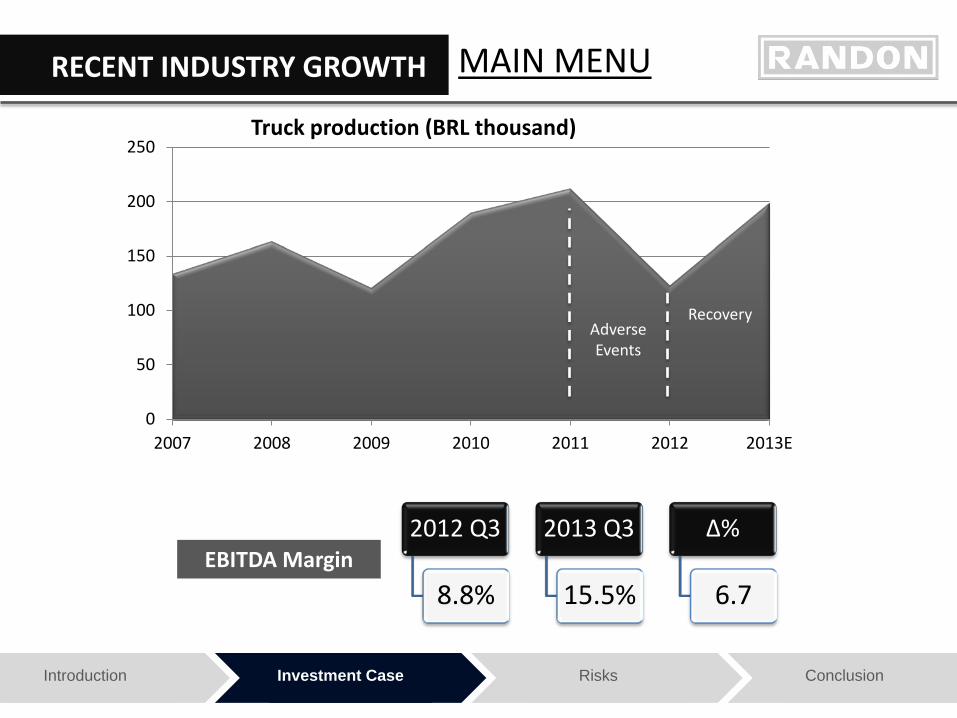

RECENT INDUSTRY GROWTH

2012 Q3

8.8%

2013 Q3

15.5%

Δ%

6.7 EBITDA Margin

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012 2013E

Truck production (BRL thousand)

Adverse Events

Recovery

Introduction Investment Case Risks Conclusion

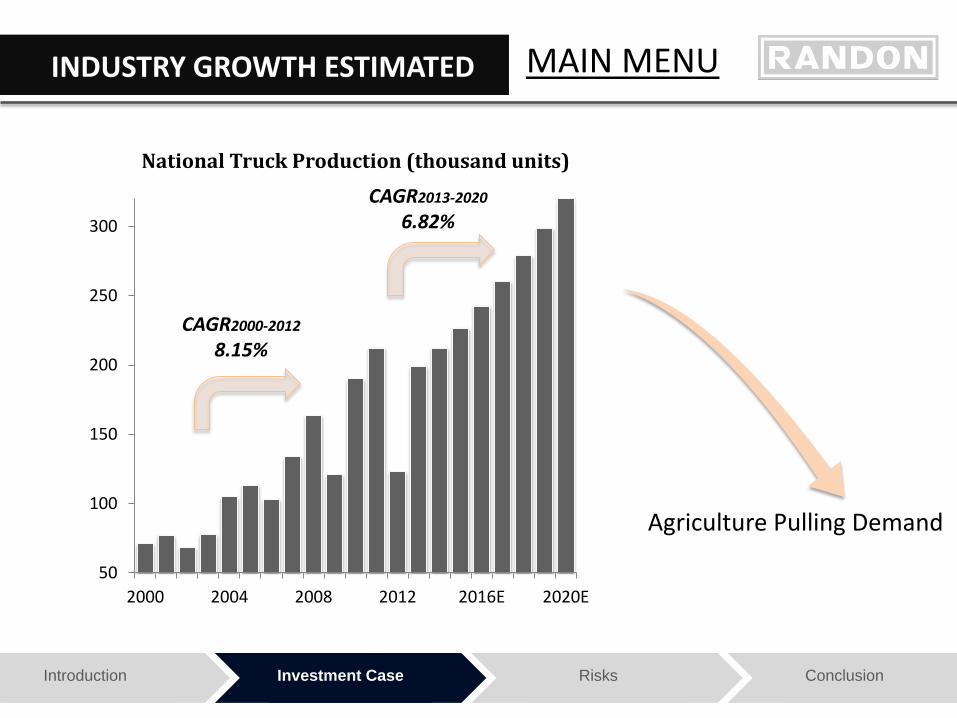

INDUSTRY GROWTH ESTIMATED

50

100

150

200

250

300

2000 2004 2008 2012 2016E 2020E

National Truck Production (thousand units)

CAGR2000-2012

8.15%

CAGR2013-2020

6.82%

Agriculture Pulling Demand

Randon is the most prepared company to leverage market opportunities

ERP-SAP

GROWTH DRIVERS

Increase Productivity Gain Economies of Scale

Introduction Investment Case Risks Conclusion

Introduction Investment Case Risks Conclusion

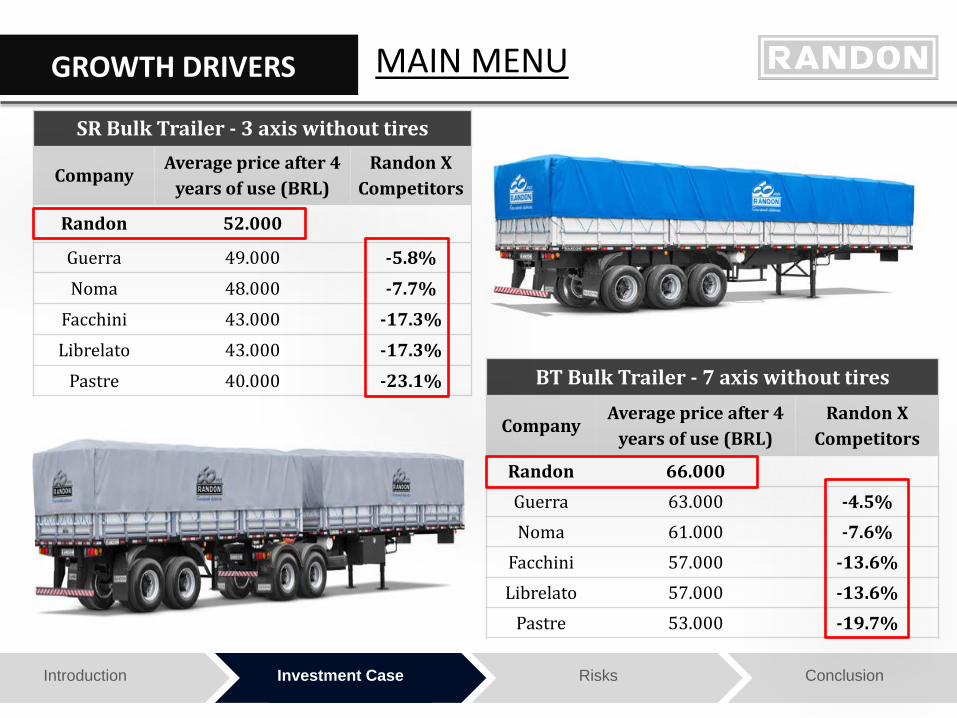

GROWTH DRIVERS

SR Bulk Trailer - 3 axis without tires

Company Average price after 4

years of use (BRL) Randon X

Competitors

Randon 52.000

Guerra 49.000 -5.8%

Noma 48.000 -7.7%

Facchini 43.000 -17.3%

Librelato 43.000 -17.3%

Pastre 40.000 -23.1% BT Bulk Trailer - 7 axis without tires

Company Average price after 4

years of use (BRL) Randon X

Competitors

Randon 66.000 Guerra 63.000 -4.5%

Noma 61.000 -7.6%

Facchini 57.000 -13.6%

Librelato 57.000 -13.6%

Pastre 53.000 -19.7%

Durability

Quality

Introduction Investment Case Risks Conclusion

GROWTH DRIVERS

Investments in R&D

E-coat painting system

Proving ground

Introduction Investment Case Risks Conclusion

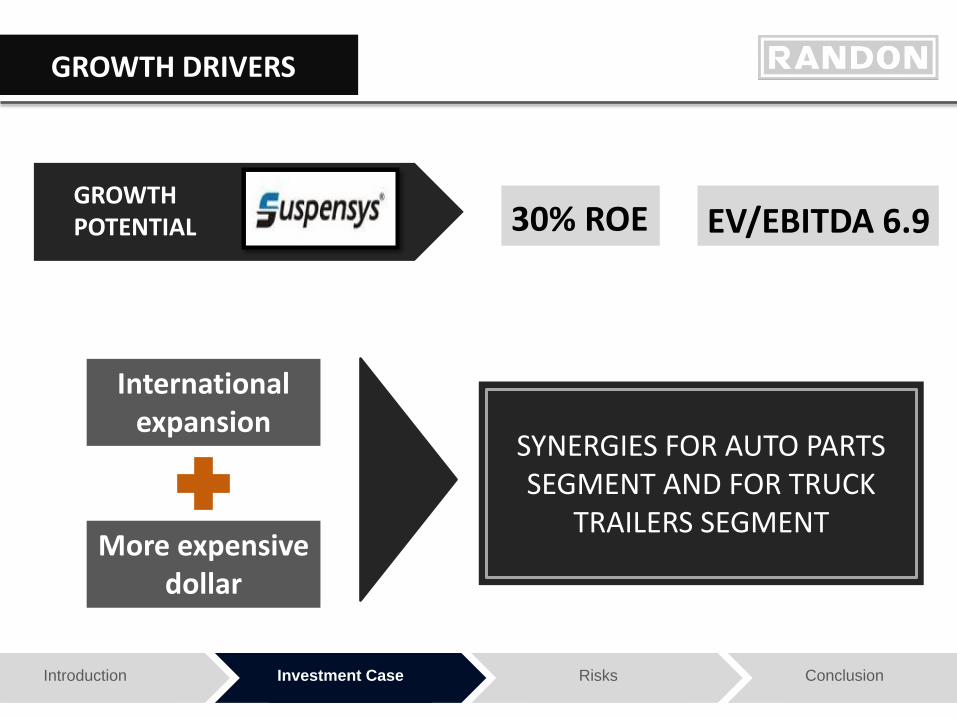

GROWTH DRIVERS

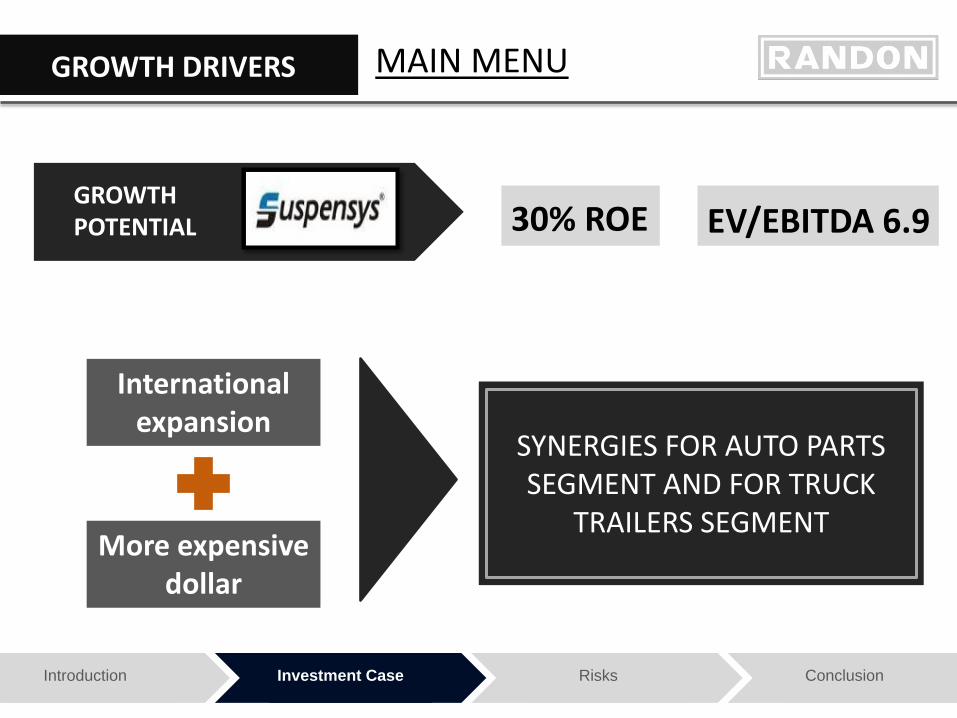

GROWTH POTENTIAL 30% ROE EV/EBITDA 6.9

More expensive dollar

International expansion

SYNERGIES FOR AUTO PARTS SEGMENT AND FOR TRUCK

TRAILERS SEGMENT

Introduction Investment Case Risks Conclusion

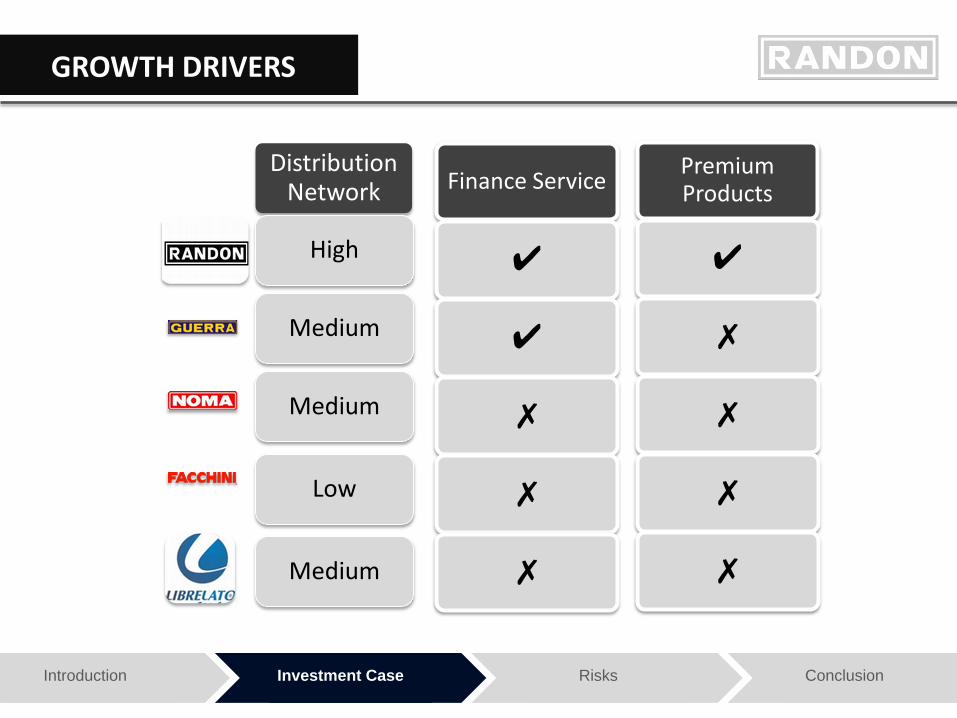

GROWTH DRIVERS

Distribution Network

High

Medium

Medium

Low

Medium

Finance Service

✔

✔

✗

✗

✗

Premium Products

✔

✗

✗

✗

✗

Introduction Investment Case Risks Conclusion

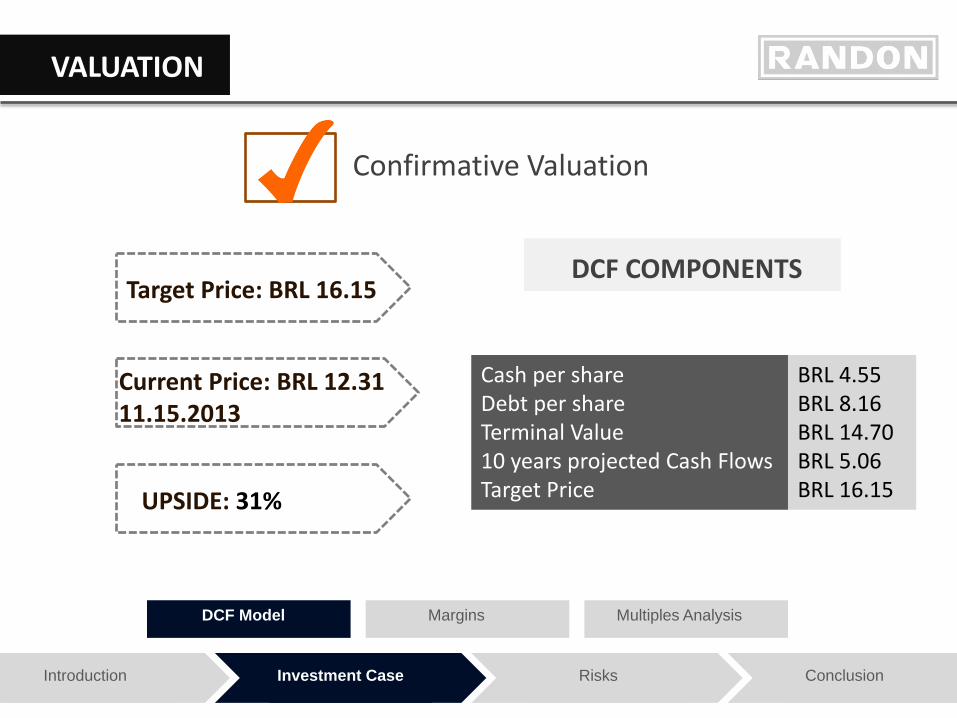

VALUATION

UPSIDE: 31%

Target Price: BRL 16.15

Current Price: BRL 12.31 11.15.2013

DCF COMPONENTS

DCF Model Multiples Analysis Margins

Cash per share Debt per share Terminal Value 10 years projected Cash Flows Target Price

BRL 4.55 BRL 8.16 BRL 14.70 BRL 5.06 BRL 16.15

Confirmative Valuation

Introduction Investment Case Risks Conclusion

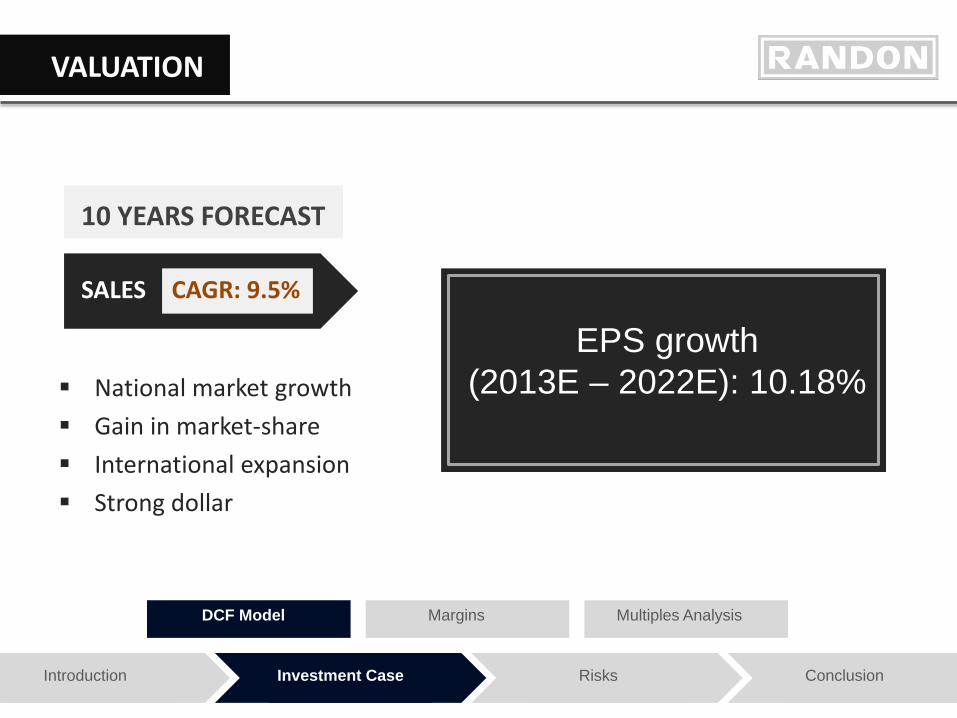

VALUATION

DCF Model Multiples Analysis Margins

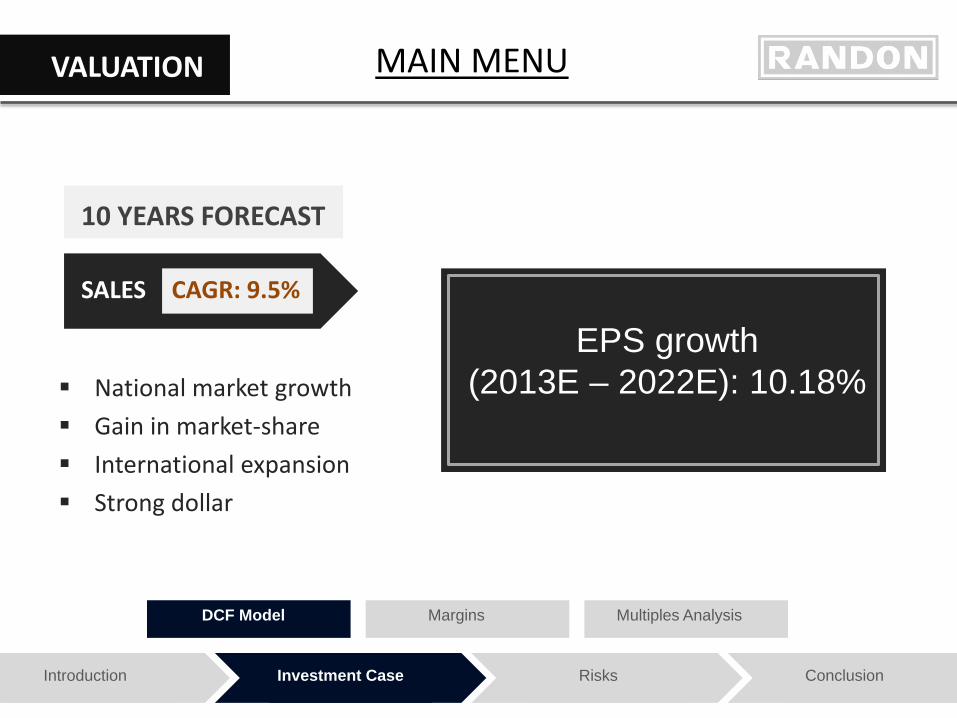

National market growth Gain in market-share International expansion Strong dollar

10 YEARS FORECAST

SALES CAGR: 9.5%

EPS growth (2013E – 2022E): 10.18%

Introduction Investment Case Risks Conclusion

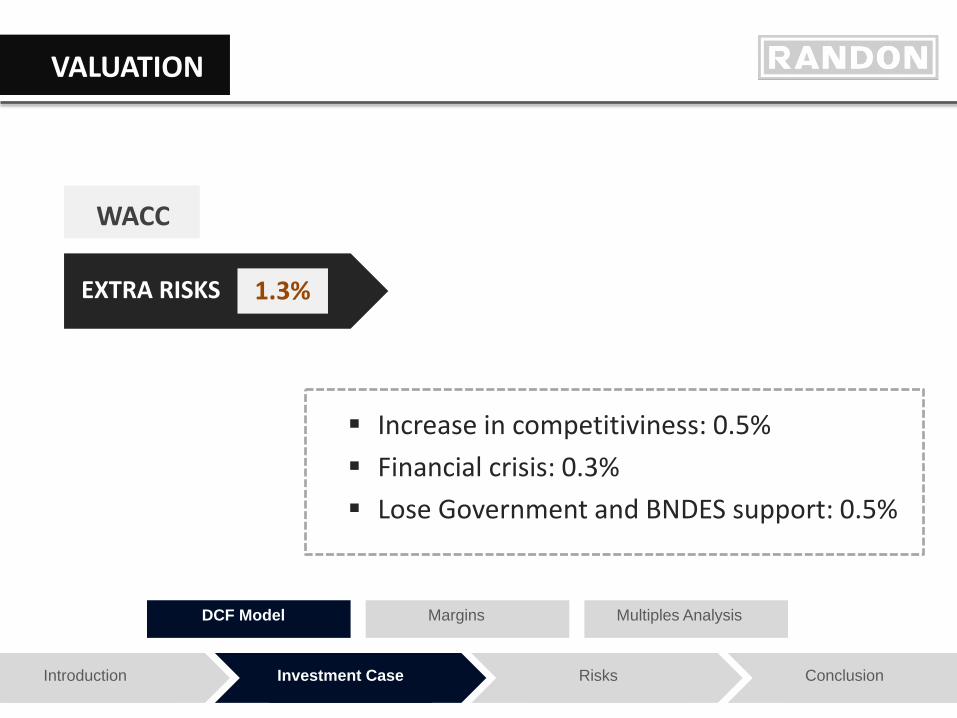

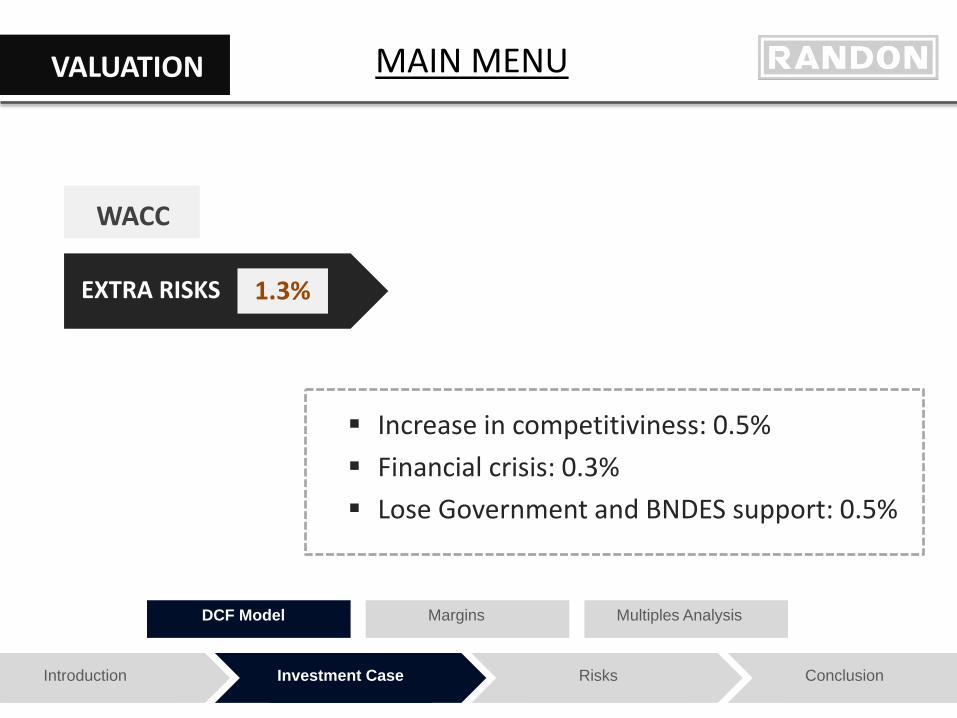

VALUATION

DCF Model Multiples Analysis Margins

WACC

Increase in competitiviness: 0.5% Financial crisis: 0.3% Lose Government and BNDES support: 0.5%

EXTRA RISKS 1.3%

Introduction Investment Case Risks Conclusion

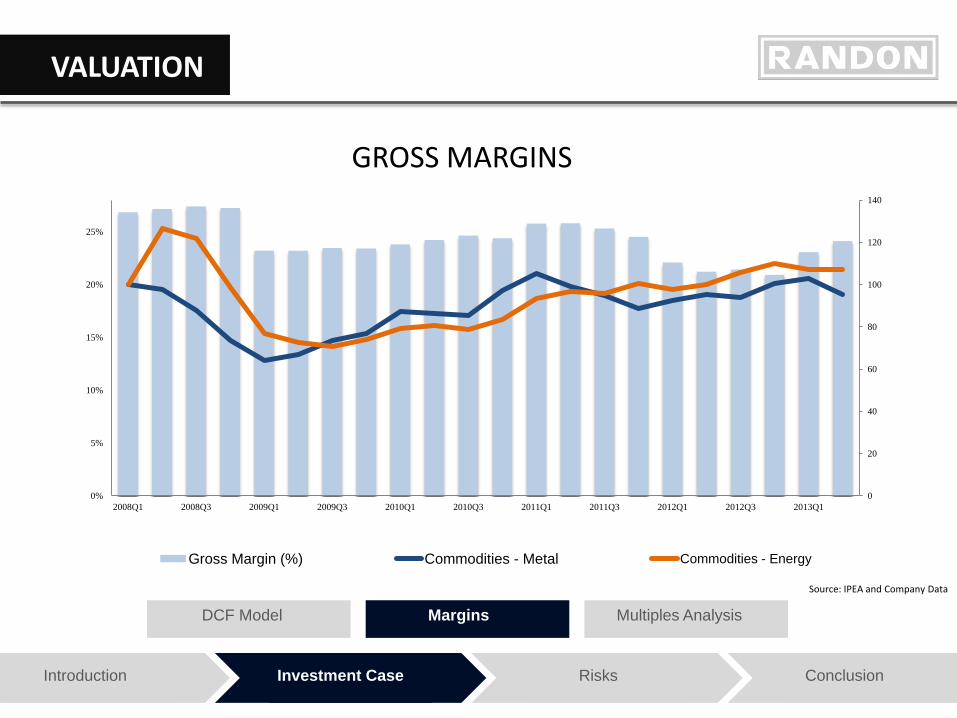

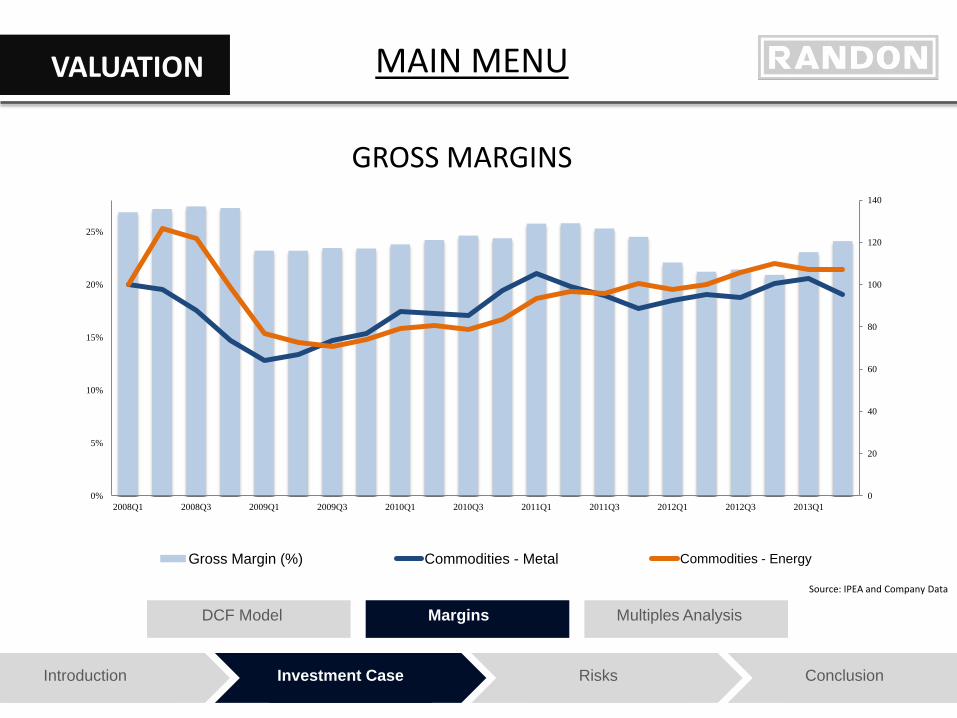

VALUATION

DCF Model Multiples Analysis Margins

0

20

40

60

80

100

120

140

0%

5%

10%

15%

20%

25%

2008Q1 2008Q3 2009Q1 2009Q3 2010Q1 2010Q3 2011Q1 2011Q3 2012Q1 2012Q3 2013Q1

Gross Margin (%) Commodities - Metal Commodities - Energy

Source: IPEA and Company Data

GROSS MARGINS

Introduction Investment Case Risks Conclusion

VALUATION

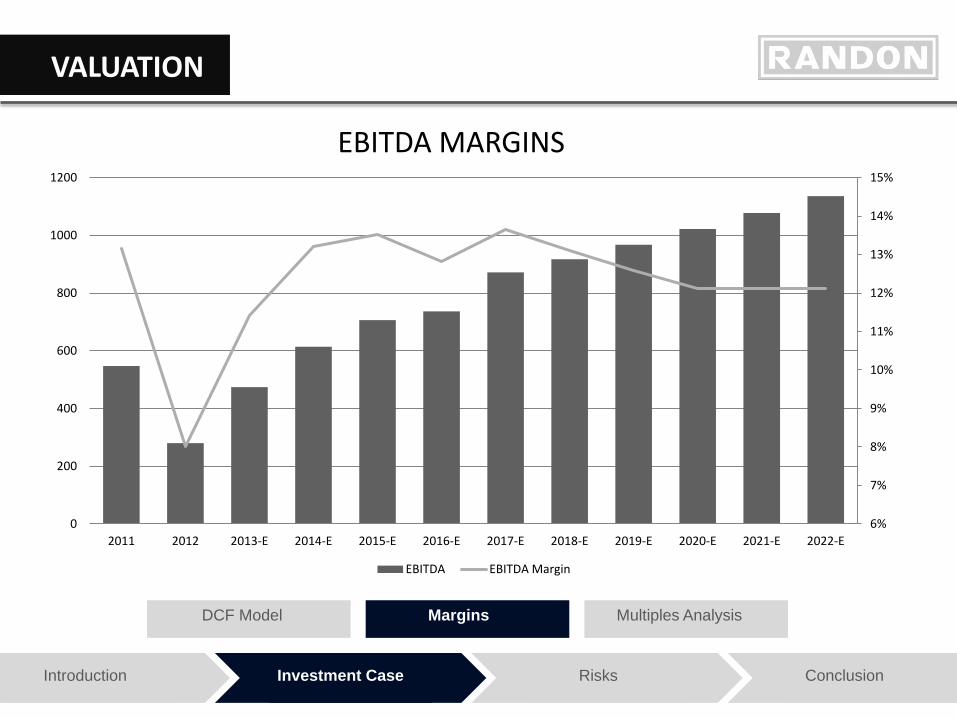

DCF Model Multiples Analysis Margins

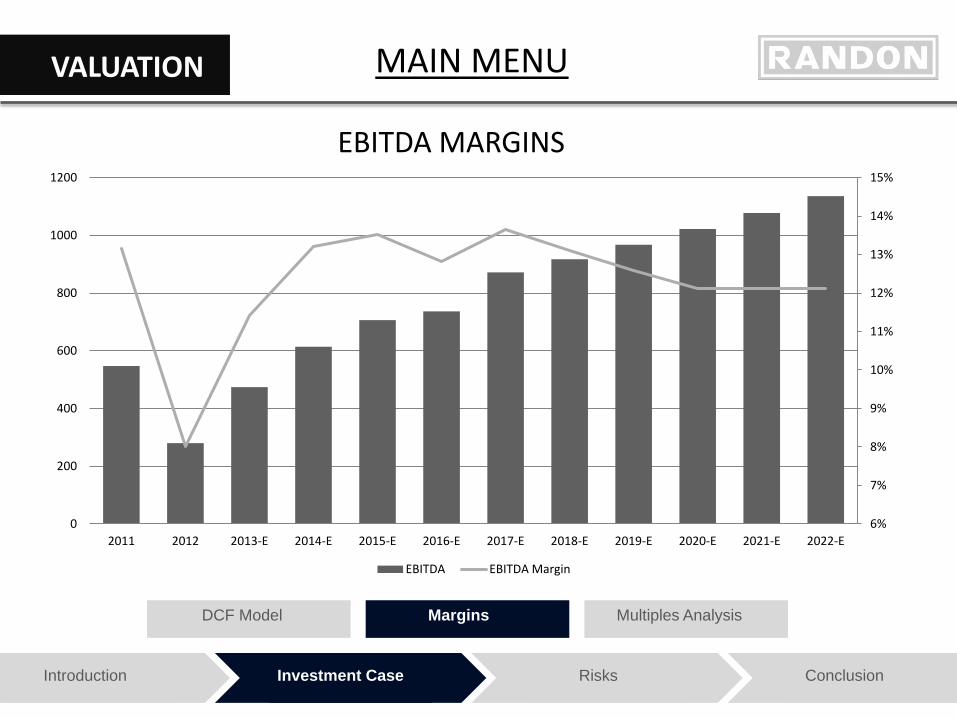

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

0

200

400

600

800

1000

1200

2011 2012 2013-E 2014-E 2015-E 2016-E 2017-E 2018-E 2019-E 2020-E 2021-E 2022-E

EBITDA EBITDA Margin

EBITDA MARGINS

Introduction Investment Case Risks Conclusion

VALUATION

DCF Model Multiples Analysis Margins

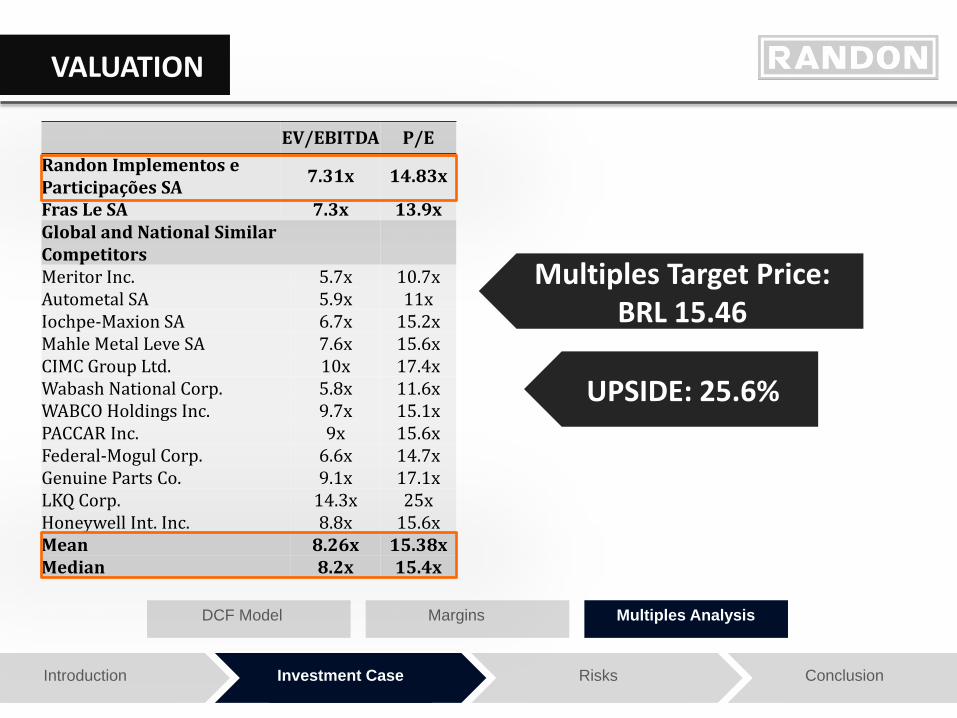

Multiples Target Price: BRL 15.46

UPSIDE: 25.6%

EV/EBITDA P/E Randon Implementos e Participações SA 7.31x 14.83x

Fras Le SA 7.3x 13.9x Global and National Similar Competitors Meritor Inc. 5.7x 10.7x Autometal SA 5.9x 11x Iochpe-Maxion SA 6.7x 15.2x Mahle Metal Leve SA 7.6x 15.6x CIMC Group Ltd. 10x 17.4x Wabash National Corp. 5.8x 11.6x WABCO Holdings Inc. 9.7x 15.1x PACCAR Inc. 9x 15.6x Federal-Mogul Corp. 6.6x 14.7x Genuine Parts Co. 9.1x 17.1x LKQ Corp. 14.3x 25x Honeywell Int. Inc. 8.8x 15.6x Mean 8.26x 15.38x Median 8.2x 15.4x

Introduction Investment Case Risks Conclusion

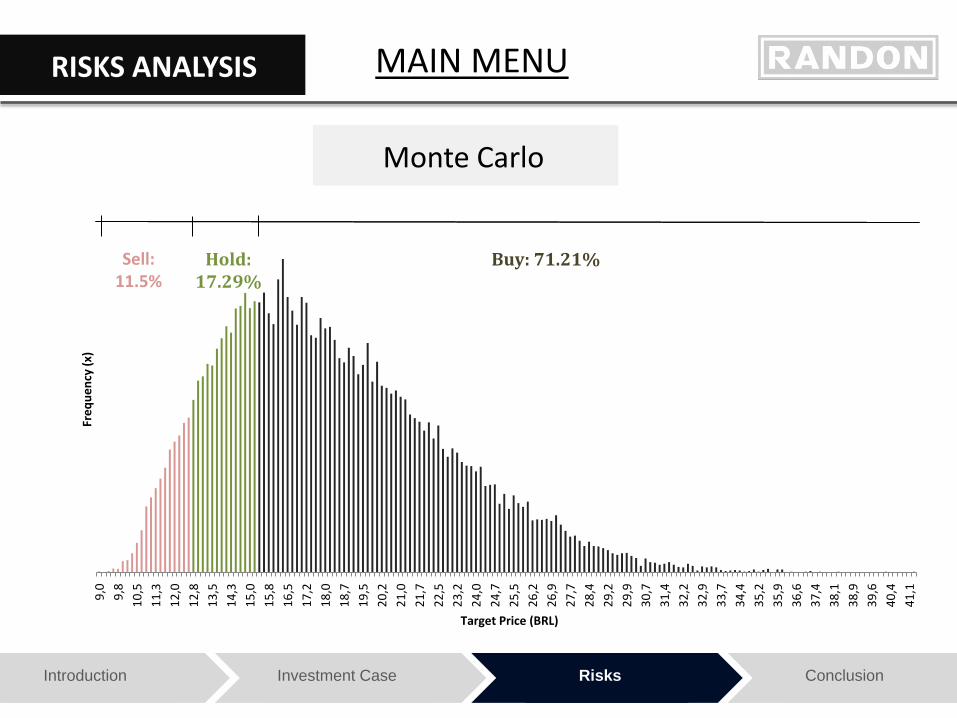

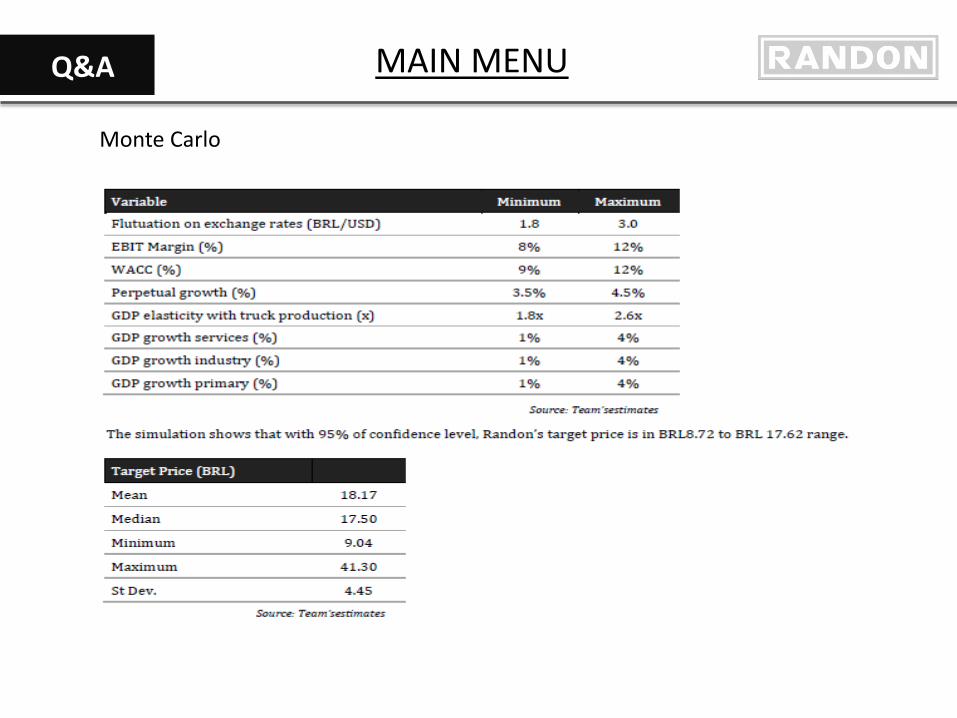

RISKS ANALYSIS 9

,0

9,8

1

0,5

1

1,3

1

2,0

1

2,8

1

3,5

1

4,3

1

5,0

1

5,8

1

6,5

1

7,2

1

8,0

1

8,7

1

9,5

2

0,2

2

1,0

2

1,7

2

2,5

2

3,2

2

4,0

2

4,7

2

5,5

2

6,2

2

6,9

2

7,7

2

8,4

2

9,2

2

9,9

3

0,7

3

1,4

3

2,2

3

2,9

3

3,7

3

4,4

3

5,2

3

5,9

3

6,6

3

7,4

3

8,1

3

8,9

3

9,6

4

0,4

4

1,1

Freq

uenc

y (x

)

Target Price (BRL)

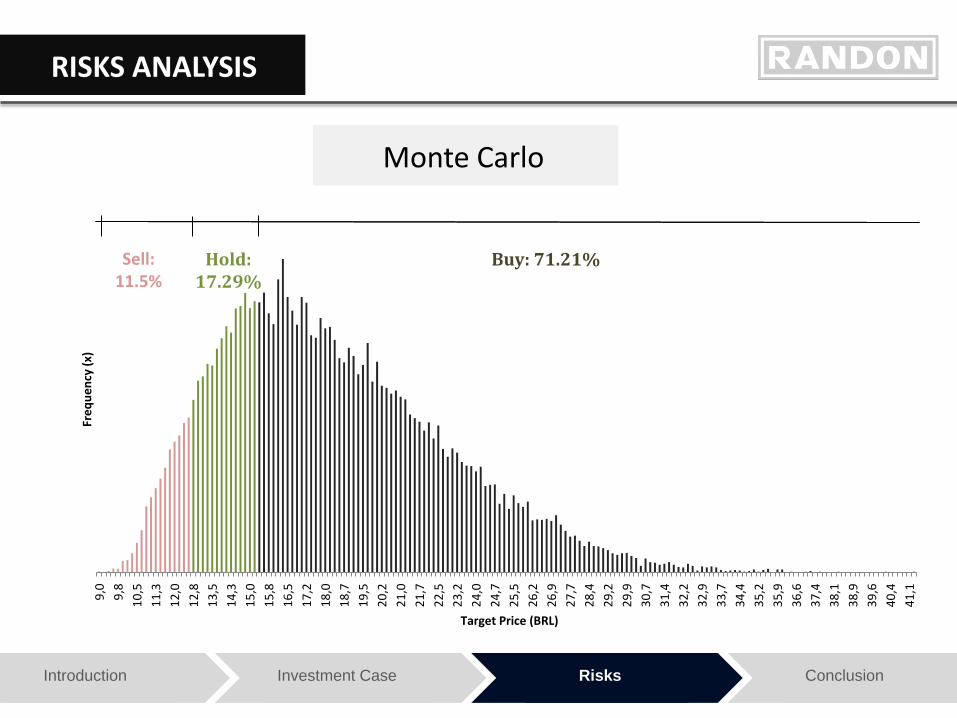

Buy: 71.21% Hold: 17.29%

Sell: 11.5%

Monte Carlo

Introduction Investment Case Risks Conclusion

CONCLUSION

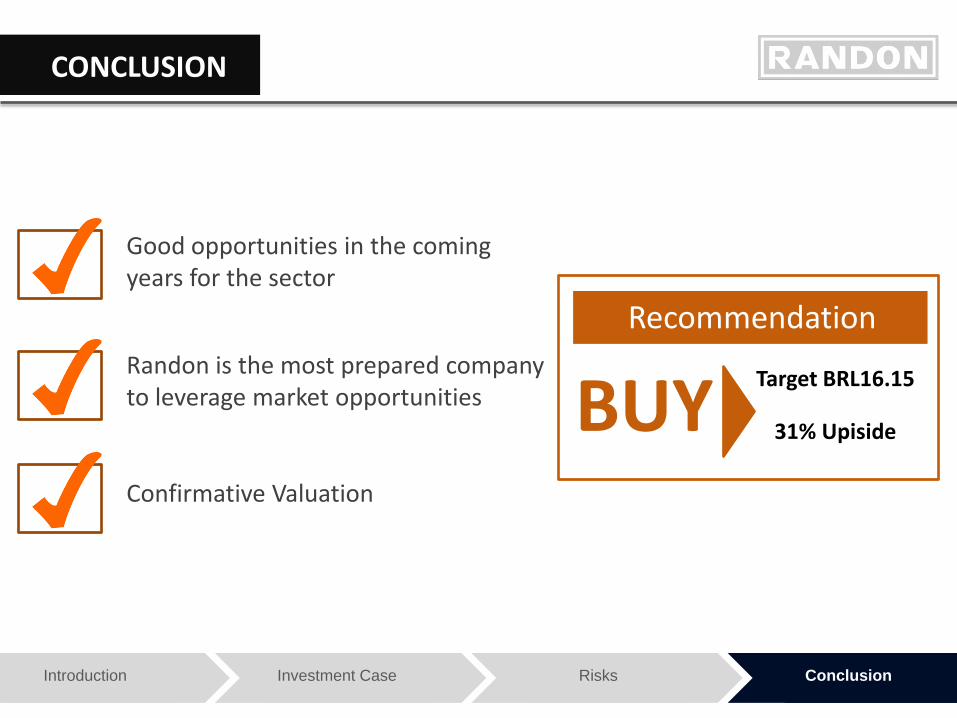

Good opportunities in the coming years for the sector

Confirmative Valuation

Randon is the most prepared company to leverage market opportunities BUY

Recommendation

31% Upiside

Target BRL16.15

Q&A THANK YOU Q&A

Q&A

Company Data

Income Statement 1

FCFF

WACC 1

Key Financial Ratios 1

Key Financial Ratios 2

Multiples 2

Balance sheet 1 Balance sheet 2

Multiples 1

Income Statement 2

WACC 2

DuPont Elasticity Randon’s Suppliers

Corporate Governance Graphic

Other information

SWOT

Truck components

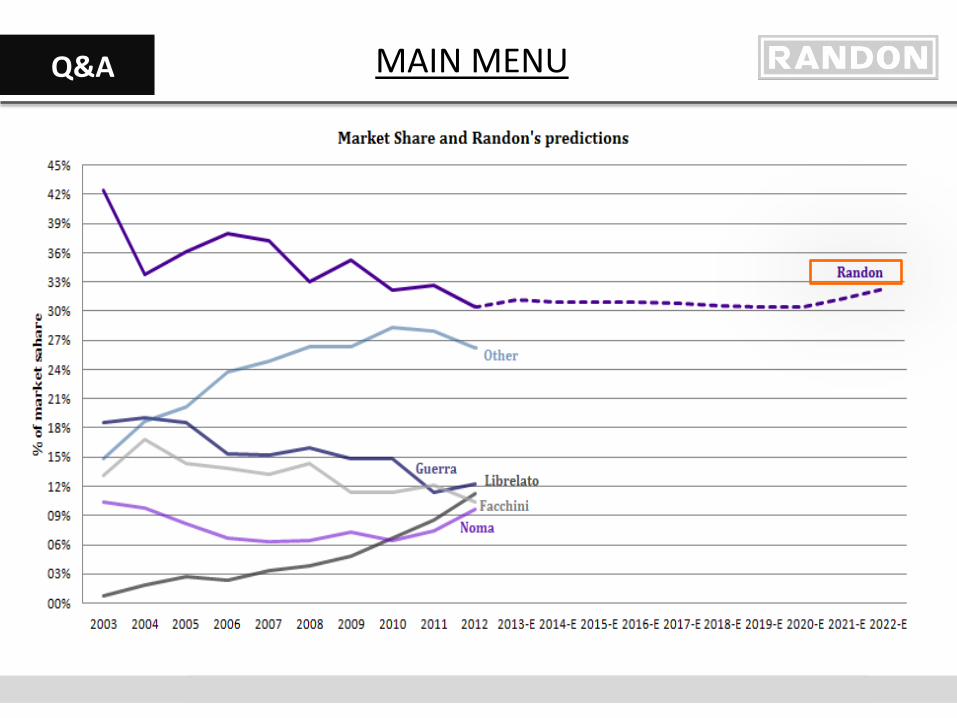

Market share

Rail Lines

Road Network

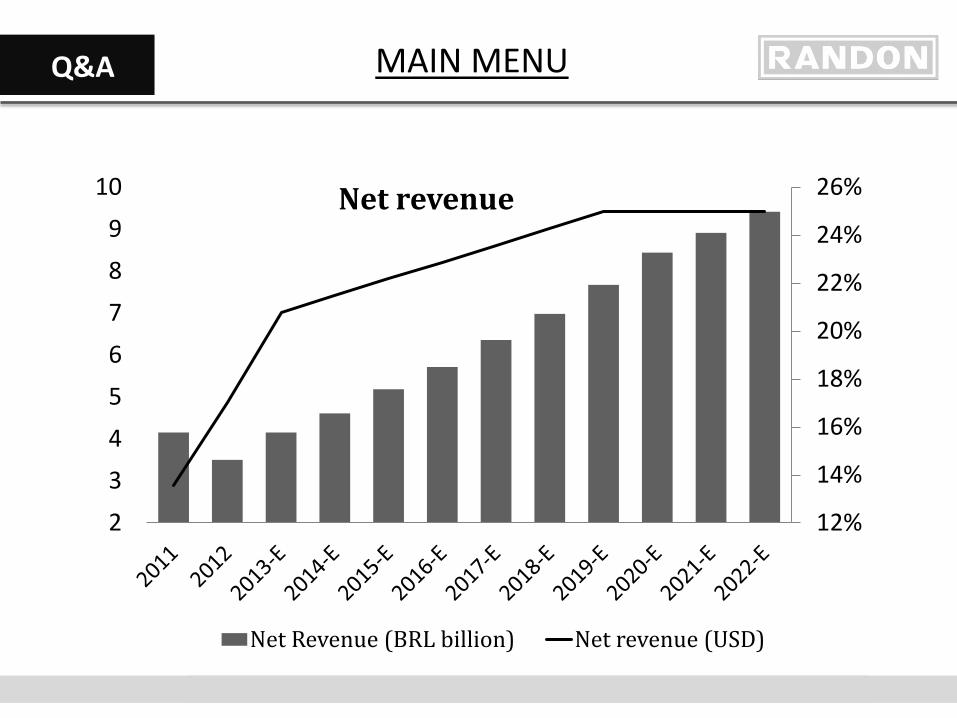

Net Revenue

Companies factories Corporate structure

Synerges

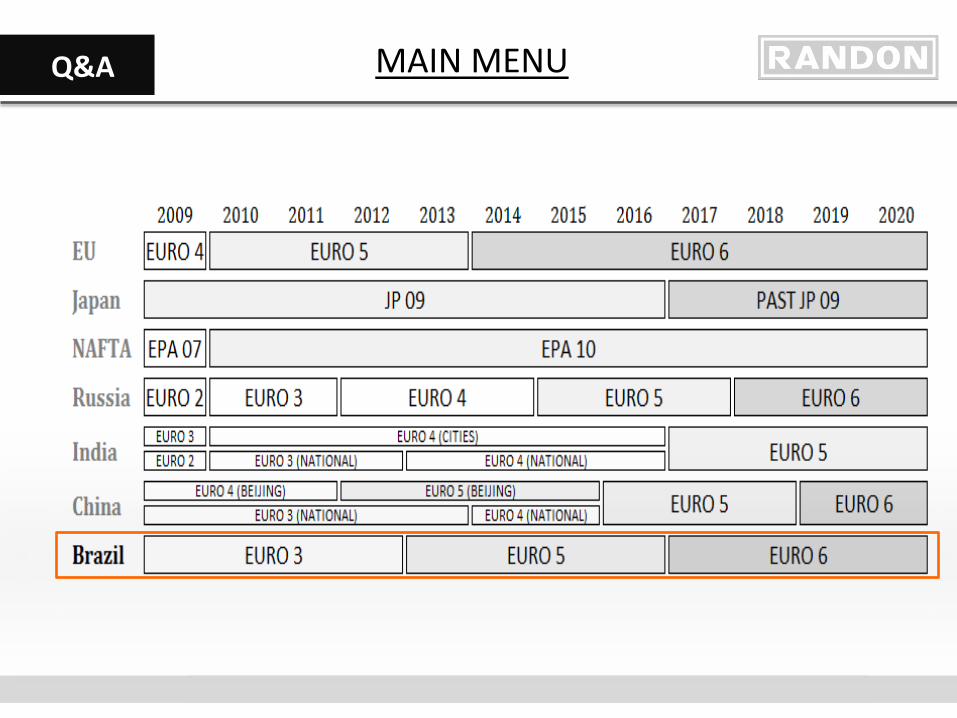

EURO

Global trailers producers

Distribution centers Auto parts market share World truck production

Bullish case Bearish case Domestic sale / exports

BNDES Company’s strategy

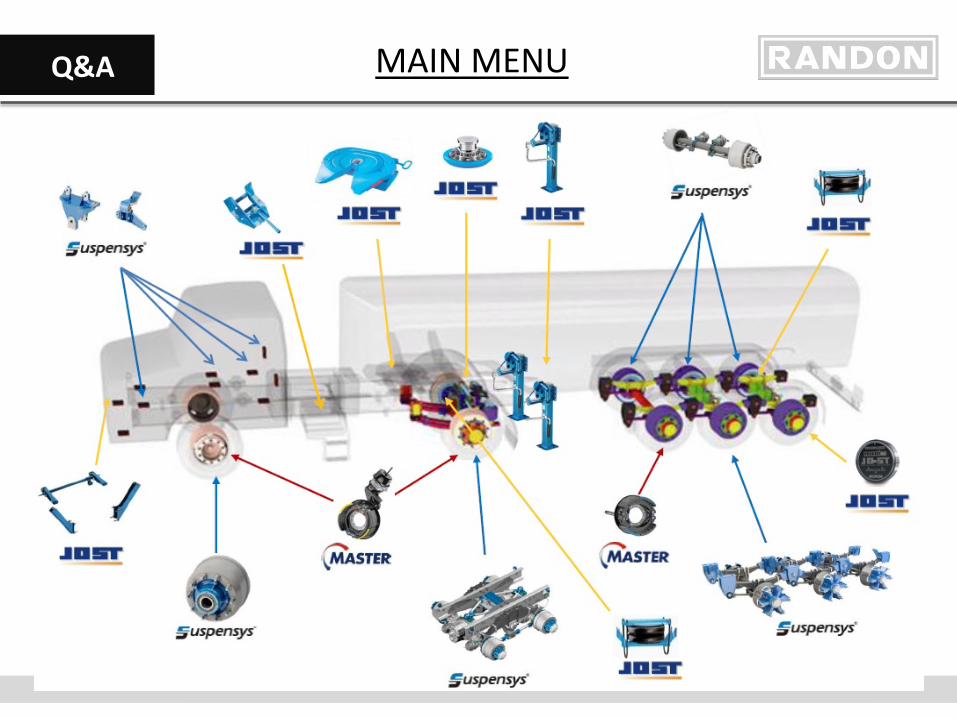

Suspensys Jost Master

Fras-le Raw materials Main events

Agribusiness Distribution synergies

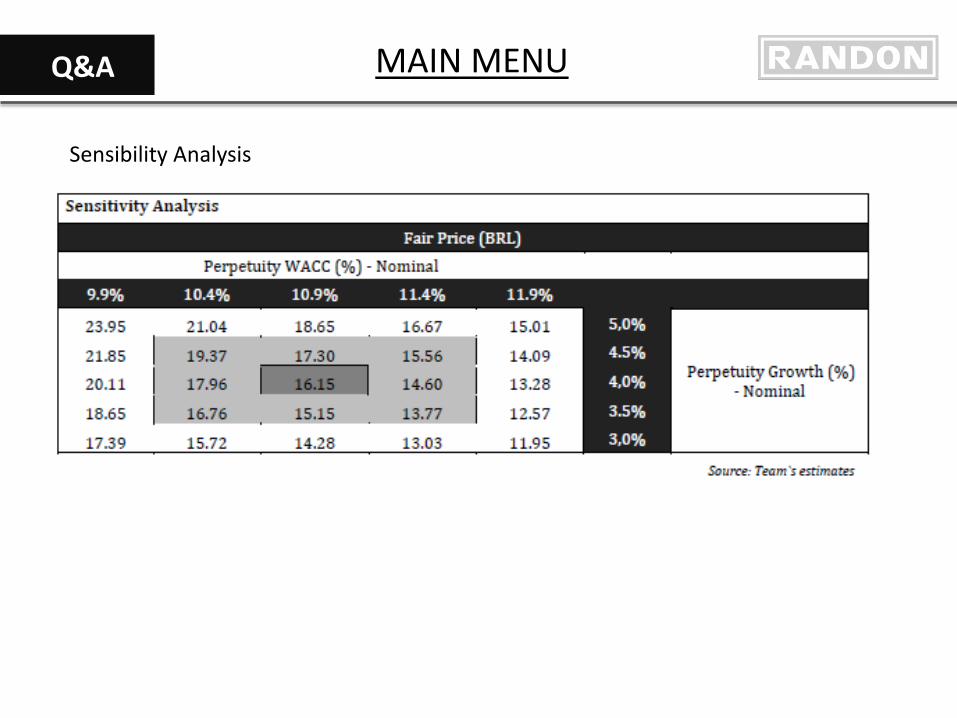

Sensibility Analysis Risk Matrix

Q&A

Introduction

Recommendation

Net revenue Investment Case Truck trailers Porter Auto parts Porter Auto parts contracts Historical EBITDA margins

Renew of truck fleet

Recent Industry growth

Bulk trailers

Industry growth estimated

ERP-SAP

R&D

Suspensys growth

Competitors DCF Components

DCF Model 1

DCF Model 2

Gross Margins EBITDA margins Multiples target price

Monte Carlo 1

Monte Carlo 2

Q&A

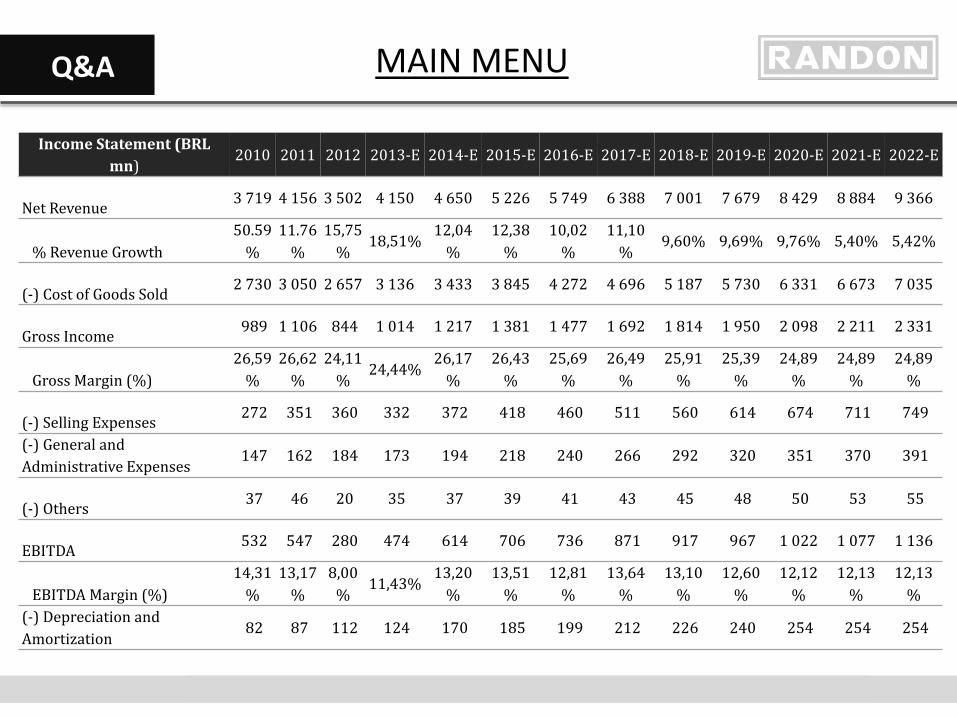

Income Statement (BRL mn)

2010 2011 2012 2013-E 2014-E 2015-E 2016-E 2017-E 2018-E 2019-E 2020-E 2021-E 2022-E

Net Revenue 3 719 4 156 3 502 4 150 4 650 5 226 5 749 6 388 7 001 7 679 8 429 8 884 9 366

% Revenue Growth 50.59

% 11.76

% 15,75

% 18,51%

12,04%

12,38%

10,02%

11,10%

9,60% 9,69% 9,76% 5,40% 5,42%

(-) Cost of Goods Sold 2 730 3 050 2 657 3 136 3 433 3 845 4 272 4 696 5 187 5 730 6 331 6 673 7 035

Gross Income 989 1 106 844 1 014 1 217 1 381 1 477 1 692 1 814 1 950 2 098 2 211 2 331

Gross Margin (%) 26,59

% 26,62

% 24,11

% 24,44%

26,17%

26,43%

25,69%

26,49%

25,91%

25,39%

24,89%

24,89%

24,89%

(-) Selling Expenses 272 351 360 332 372 418 460 511 560 614 674 711 749

(-) General and Administrative Expenses

147 162 184 173 194 218 240 266 292 320 351 370 391

(-) Others 37 46 20 35 37 39 41 43 45 48 50 53 55

EBITDA 532 547 280 474 614 706 736 871 917 967 1 022 1 077 1 136

EBITDA Margin (%) 14,31

% 13,17

% 8,00

% 11,43%

13,20%

13,51%

12,81%

13,64%

13,10%

12,60%

12,12%

12,13%

12,13%

(-) Depreciation and Amortization

82 87 112 124 170 185 199 212 226 240 254 254 254

MAIN MENU

Q&A

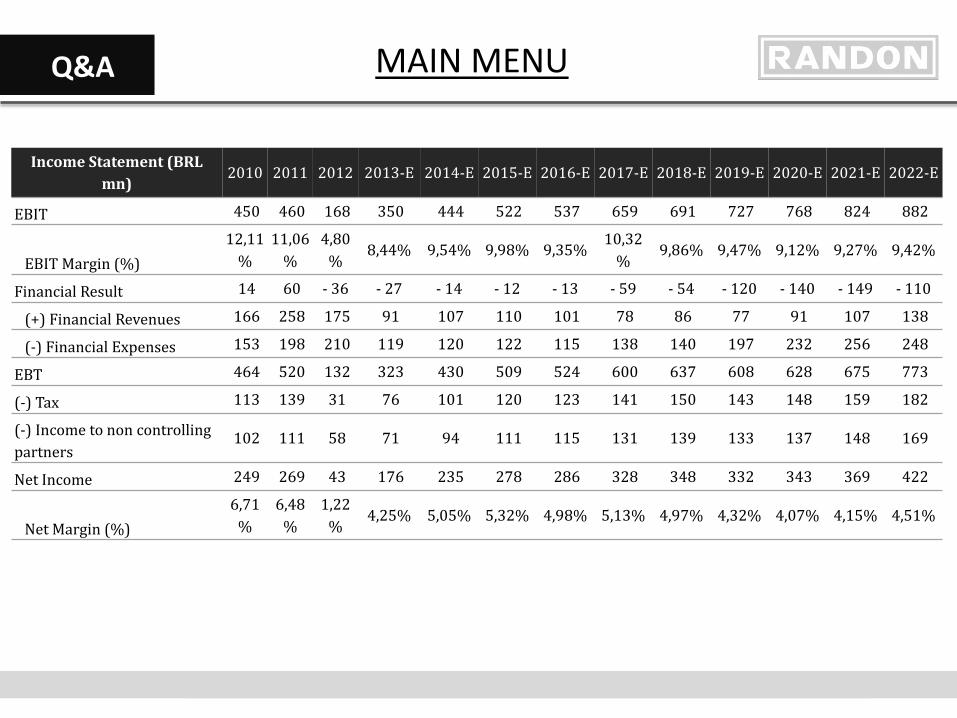

Income Statement (BRL mn)

2010 2011 2012 2013-E 2014-E 2015-E 2016-E 2017-E 2018-E 2019-E 2020-E 2021-E 2022-E

EBIT 450 460 168 350 444 522 537 659 691 727 768 824 882

EBIT Margin (%) 12,11

% 11,06

% 4,80

% 8,44% 9,54% 9,98% 9,35%

10,32%

9,86% 9,47% 9,12% 9,27% 9,42%

Financial Result 14 60 - 36 - 27 - 14 - 12 - 13 - 59 - 54 - 120 - 140 - 149 - 110

(+) Financial Revenues 166 258 175 91 107 110 101 78 86 77 91 107 138

(-) Financial Expenses 153 198 210 119 120 122 115 138 140 197 232 256 248

EBT 464 520 132 323 430 509 524 600 637 608 628 675 773

(-) Tax 113 139 31 76 101 120 123 141 150 143 148 159 182

(-) Income to non controlling partners

102 111 58 71 94 111 115 131 139 133 137 148 169

Net Income 249 269 43 176 235 278 286 328 348 332 343 369 422

Net Margin (%) 6,71

% 6,48

% 1,22

% 4,25% 5,05% 5,32% 4,98% 5,13% 4,97% 4,32% 4,07% 4,15% 4,51%

MAIN MENU

Q&A

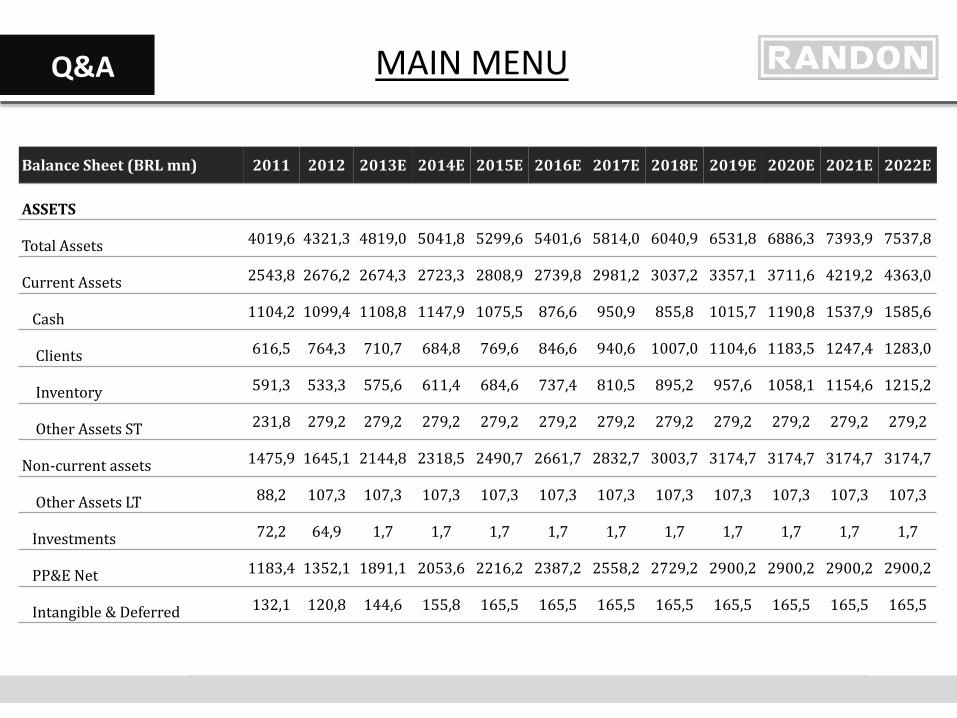

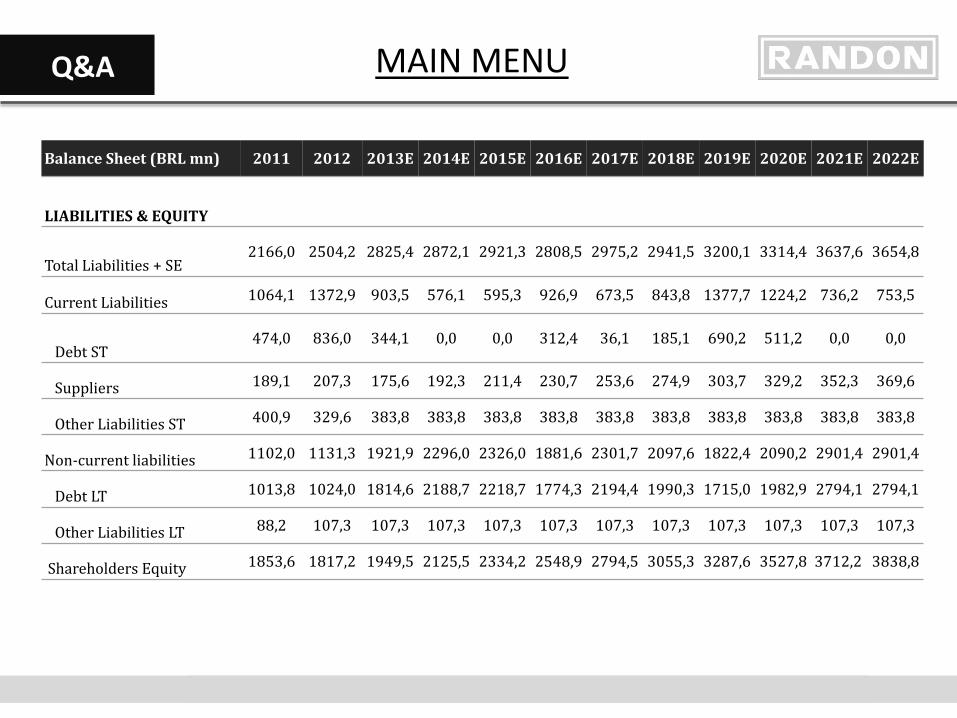

Balance Sheet (BRL mn) 2011 2012 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E

ASSETS

Total Assets 4019,6 4321,3 4819,0 5041,8 5299,6 5401,6 5814,0 6040,9 6531,8 6886,3 7393,9 7537,8

Current Assets 2543,8 2676,2 2674,3 2723,3 2808,9 2739,8 2981,2 3037,2 3357,1 3711,6 4219,2 4363,0

Cash 1104,2 1099,4 1108,8 1147,9 1075,5 876,6 950,9 855,8 1015,7 1190,8 1537,9 1585,6

Clients 616,5 764,3 710,7 684,8 769,6 846,6 940,6 1007,0 1104,6 1183,5 1247,4 1283,0

Inventory 591,3 533,3 575,6 611,4 684,6 737,4 810,5 895,2 957,6 1058,1 1154,6 1215,2

Other Assets ST 231,8 279,2 279,2 279,2 279,2 279,2 279,2 279,2 279,2 279,2 279,2 279,2

Non-current assets 1475,9 1645,1 2144,8 2318,5 2490,7 2661,7 2832,7 3003,7 3174,7 3174,7 3174,7 3174,7

Other Assets LT 88,2 107,3 107,3 107,3 107,3 107,3 107,3 107,3 107,3 107,3 107,3 107,3

Investments 72,2 64,9 1,7 1,7 1,7 1,7 1,7 1,7 1,7 1,7 1,7 1,7

PP&E Net 1183,4 1352,1 1891,1 2053,6 2216,2 2387,2 2558,2 2729,2 2900,2 2900,2 2900,2 2900,2

Intangible & Deferred 132,1 120,8 144,6 155,8 165,5 165,5 165,5 165,5 165,5 165,5 165,5 165,5

MAIN MENU

Q&A

Balance Sheet (BRL mn) 2011 2012 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E

LIABILITIES & EQUITY

Total Liabilities + SE 2166,0 2504,2 2825,4 2872,1 2921,3 2808,5 2975,2 2941,5 3200,1 3314,4 3637,6 3654,8

Current Liabilities 1064,1 1372,9 903,5 576,1 595,3 926,9 673,5 843,8 1377,7 1224,2 736,2 753,5

Debt ST 474,0 836,0 344,1 0,0 0,0 312,4 36,1 185,1 690,2 511,2 0,0 0,0

Suppliers 189,1 207,3 175,6 192,3 211,4 230,7 253,6 274,9 303,7 329,2 352,3 369,6

Other Liabilities ST 400,9 329,6 383,8 383,8 383,8 383,8 383,8 383,8 383,8 383,8 383,8 383,8

Non-current liabilities 1102,0 1131,3 1921,9 2296,0 2326,0 1881,6 2301,7 2097,6 1822,4 2090,2 2901,4 2901,4

Debt LT 1013,8 1024,0 1814,6 2188,7 2218,7 1774,3 2194,4 1990,3 1715,0 1982,9 2794,1 2794,1

Other Liabilities LT 88,2 107,3 107,3 107,3 107,3 107,3 107,3 107,3 107,3 107,3 107,3 107,3

Shareholders Equity 1853,6 1817,2 1949,5 2125,5 2334,2 2548,9 2794,5 3055,3 3287,6 3527,8 3712,2 3838,8

MAIN MENU

Q&A

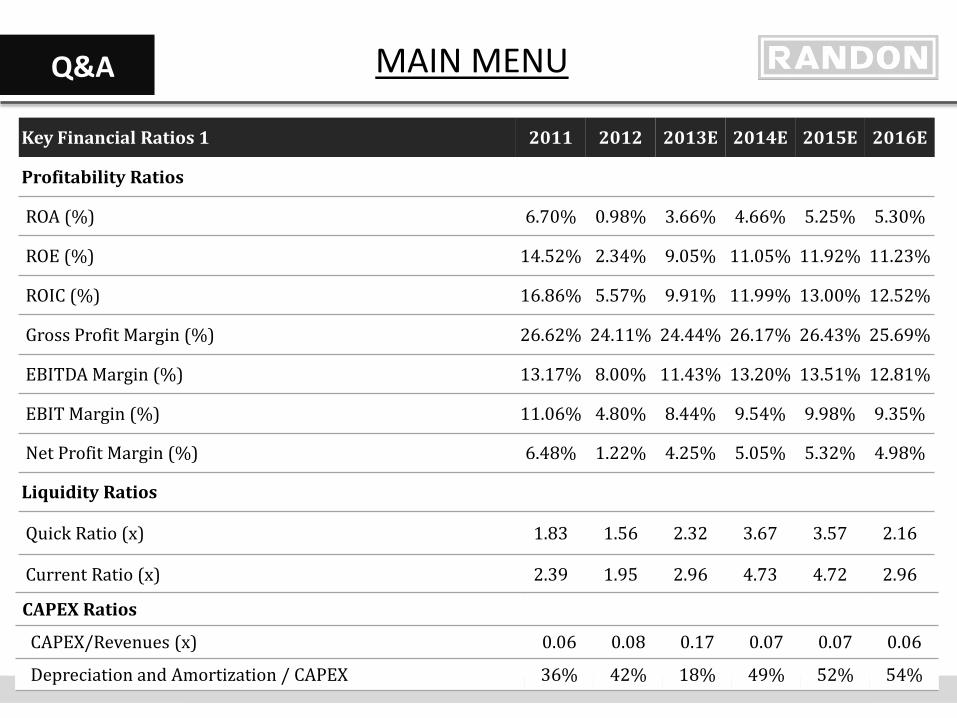

Key Financial Ratios 1 2011 2012 2013E 2014E 2015E 2016E

Profitability Ratios

ROA (%) 6.70% 0.98% 3.66% 4.66% 5.25% 5.30%

ROE (%) 14.52% 2.34% 9.05% 11.05% 11.92% 11.23%

ROIC (%) 16.86% 5.57% 9.91% 11.99% 13.00% 12.52%

Gross Profit Margin (%) 26.62% 24.11% 24.44% 26.17% 26.43% 25.69%

EBITDA Margin (%) 13.17% 8.00% 11.43% 13.20% 13.51% 12.81%

EBIT Margin (%) 11.06% 4.80% 8.44% 9.54% 9.98% 9.35%

Net Profit Margin (%) 6.48% 1.22% 4.25% 5.05% 5.32% 4.98%

Liquidity Ratios

Quick Ratio (x) 1.83 1.56 2.32 3.67 3.57 2.16

Current Ratio (x) 2.39 1.95 2.96 4.73 4.72 2.96

CAPEX Ratios

CAPEX/Revenues (x) 0.06 0.08 0.17 0.07 0.07 0.06

Depreciation and Amortization / CAPEX 36% 42% 18% 49% 52% 54%

MAIN MENU

Q&A

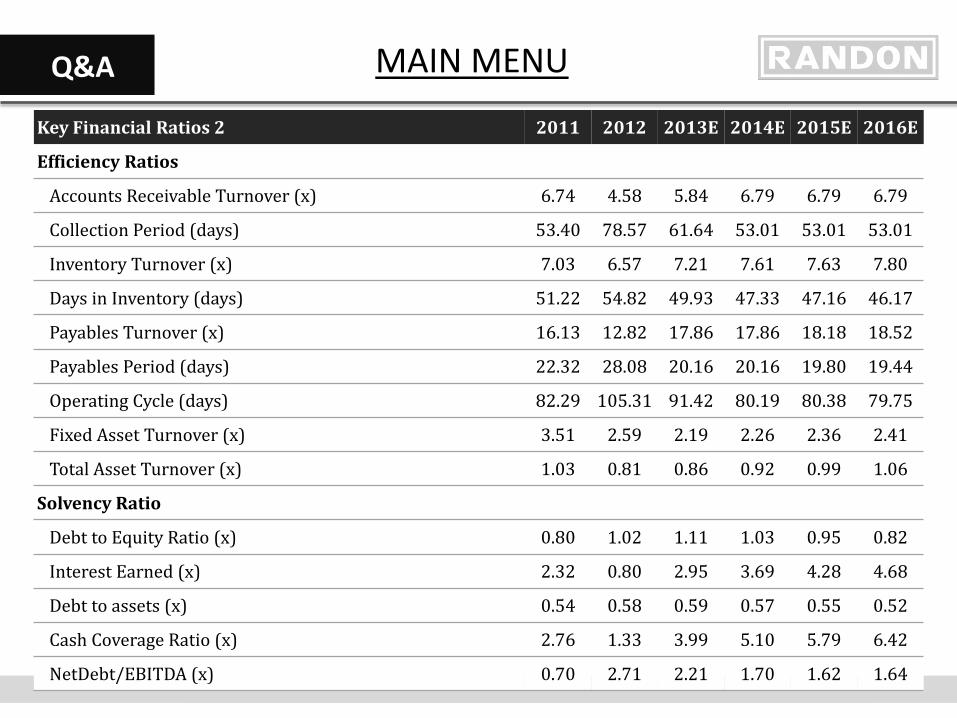

Key Financial Ratios 2 2011 2012 2013E 2014E 2015E 2016E

Efficiency Ratios

Accounts Receivable Turnover (x) 6.74 4.58 5.84 6.79 6.79 6.79

Collection Period (days) 53.40 78.57 61.64 53.01 53.01 53.01

Inventory Turnover (x) 7.03 6.57 7.21 7.61 7.63 7.80

Days in Inventory (days) 51.22 54.82 49.93 47.33 47.16 46.17

Payables Turnover (x) 16.13 12.82 17.86 17.86 18.18 18.52

Payables Period (days) 22.32 28.08 20.16 20.16 19.80 19.44

Operating Cycle (days) 82.29 105.31 91.42 80.19 80.38 79.75

Fixed Asset Turnover (x) 3.51 2.59 2.19 2.26 2.36 2.41

Total Asset Turnover (x) 1.03 0.81 0.86 0.92 0.99 1.06

Solvency Ratio

Debt to Equity Ratio (x) 0.80 1.02 1.11 1.03 0.95 0.82

Interest Earned (x) 2.32 0.80 2.95 3.69 4.28 4.68

Debt to assets (x) 0.54 0.58 0.59 0.57 0.55 0.52

Cash Coverage Ratio (x) 2.76 1.33 3.99 5.10 5.79 6.42

NetDebt/EBITDA (x) 0.70 2.71 2.21 1.70 1.62 1.64

MAIN MENU

Q&A

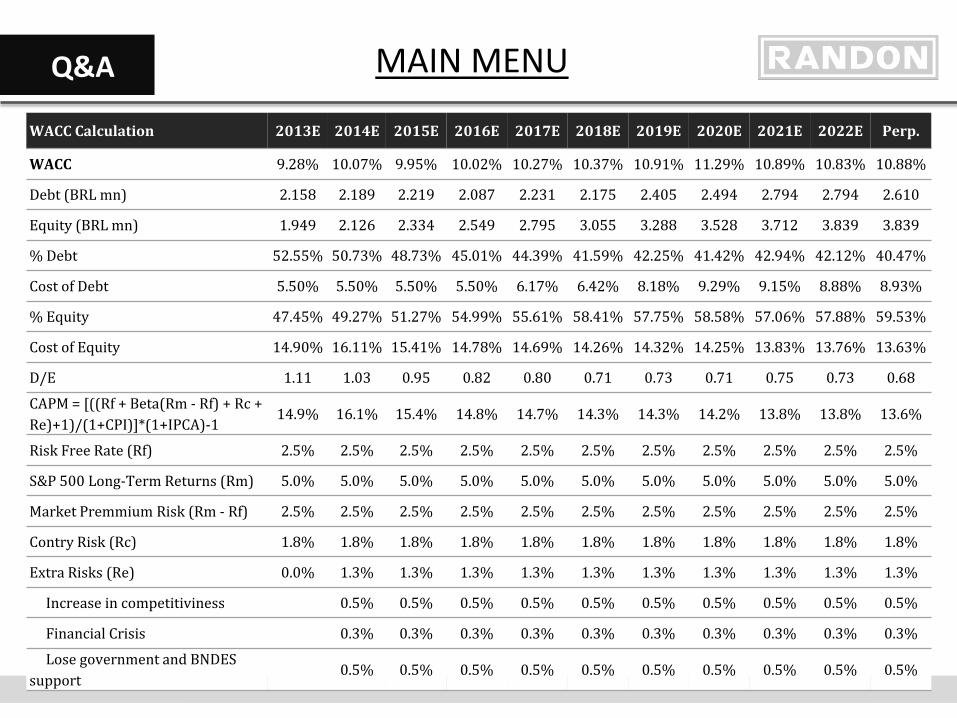

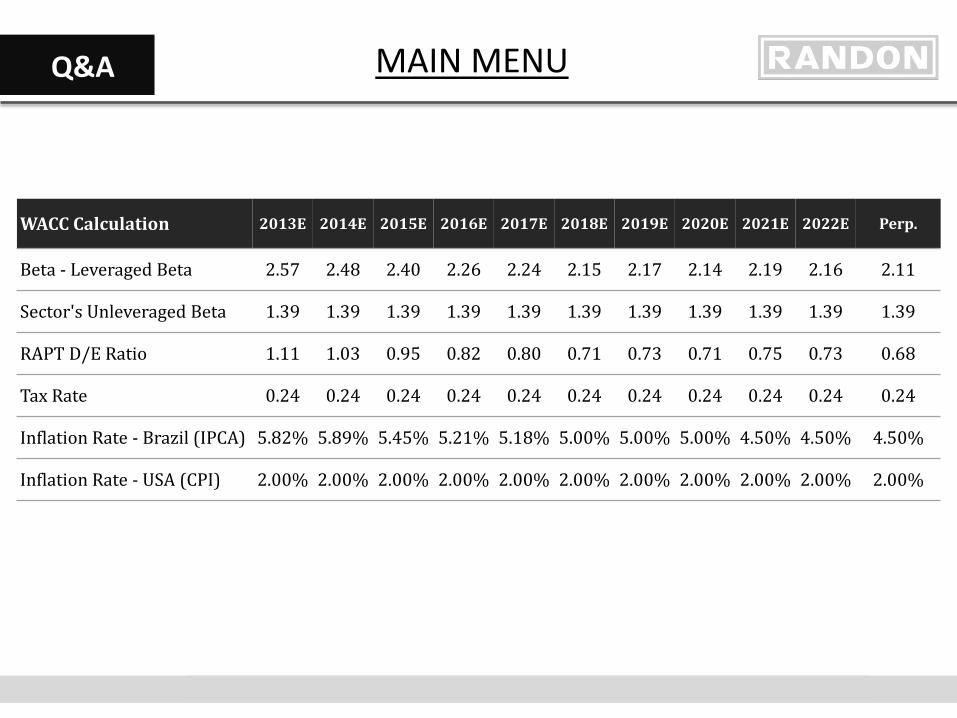

WACC Calculation 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E Perp.

WACC 9.28% 10.07% 9.95% 10.02% 10.27% 10.37% 10.91% 11.29% 10.89% 10.83% 10.88%

Debt (BRL mn) 2.158 2.189 2.219 2.087 2.231 2.175 2.405 2.494 2.794 2.794 2.610

Equity (BRL mn) 1.949 2.126 2.334 2.549 2.795 3.055 3.288 3.528 3.712 3.839 3.839

% Debt 52.55% 50.73% 48.73% 45.01% 44.39% 41.59% 42.25% 41.42% 42.94% 42.12% 40.47%

Cost of Debt 5.50% 5.50% 5.50% 5.50% 6.17% 6.42% 8.18% 9.29% 9.15% 8.88% 8.93%

% Equity 47.45% 49.27% 51.27% 54.99% 55.61% 58.41% 57.75% 58.58% 57.06% 57.88% 59.53%

Cost of Equity 14.90% 16.11% 15.41% 14.78% 14.69% 14.26% 14.32% 14.25% 13.83% 13.76% 13.63%

D/E 1.11 1.03 0.95 0.82 0.80 0.71 0.73 0.71 0.75 0.73 0.68

CAPM = [((Rf + Beta(Rm - Rf) + Rc + Re)+1)/(1+CPI)]*(1+IPCA)-1

14.9% 16.1% 15.4% 14.8% 14.7% 14.3% 14.3% 14.2% 13.8% 13.8% 13.6%

Risk Free Rate (Rf) 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5%

S&P 500 Long-Term Returns (Rm) 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0%

Market Premmium Risk (Rm - Rf) 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5%

Contry Risk (Rc) 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8%

Extra Risks (Re) 0.0% 1.3% 1.3% 1.3% 1.3% 1.3% 1.3% 1.3% 1.3% 1.3% 1.3%

Increase in competitiviness 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5%

Financial Crisis 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3%

Lose government and BNDES support

0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5%

MAIN MENU

Q&A

WACC Calculation 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E Perp.

Beta - Leveraged Beta 2.57 2.48 2.40 2.26 2.24 2.15 2.17 2.14 2.19 2.16 2.11

Sector's Unleveraged Beta 1.39 1.39 1.39 1.39 1.39 1.39 1.39 1.39 1.39 1.39 1.39

RAPT D/E Ratio 1.11 1.03 0.95 0.82 0.80 0.71 0.73 0.71 0.75 0.73 0.68

Tax Rate 0.24 0.24 0.24 0.24 0.24 0.24 0.24 0.24 0.24 0.24 0.24

Inflation Rate - Brazil (IPCA) 5.82% 5.89% 5.45% 5.21% 5.18% 5.00% 5.00% 5.00% 4.50% 4.50% 4.50%

Inflation Rate - USA (CPI) 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00%

MAIN MENU

Q&A

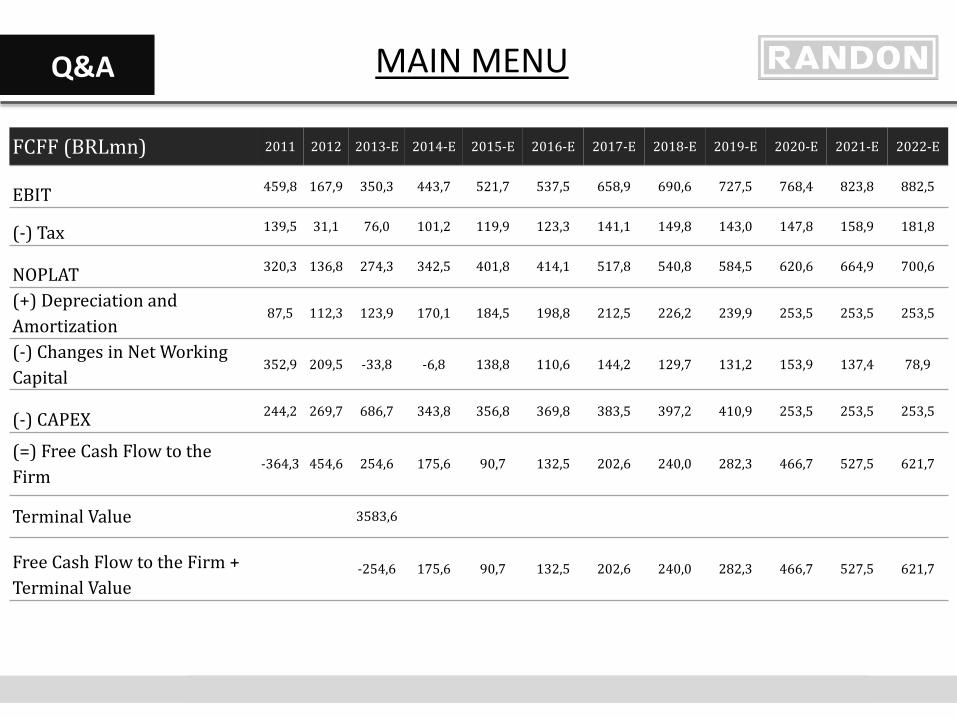

FCFF (BRLmn) 2011 2012 2013-E 2014-E 2015-E 2016-E 2017-E 2018-E 2019-E 2020-E 2021-E 2022-E

EBIT 459,8 167,9 350,3 443,7 521,7 537,5 658,9 690,6 727,5 768,4 823,8 882,5

(-) Tax 139,5 31,1 76,0 101,2 119,9 123,3 141,1 149,8 143,0 147,8 158,9 181,8

NOPLAT 320,3 136,8 274,3 342,5 401,8 414,1 517,8 540,8 584,5 620,6 664,9 700,6

(+) Depreciation and Amortization

87,5 112,3 123,9 170,1 184,5 198,8 212,5 226,2 239,9 253,5 253,5 253,5

(-) Changes in Net Working Capital

352,9 209,5 -33,8 -6,8 138,8 110,6 144,2 129,7 131,2 153,9 137,4 78,9

(-) CAPEX 244,2 269,7 686,7 343,8 356,8 369,8 383,5 397,2 410,9 253,5 253,5 253,5

(=) Free Cash Flow to the Firm

-364,3 454,6 254,6 175,6 90,7 132,5 202,6 240,0 282,3 466,7 527,5 621,7

Terminal Value 3583,6

Free Cash Flow to the Firm + Terminal Value

-254,6 175,6 90,7 132,5 202,6 240,0 282,3 466,7 527,5 621,7

MAIN MENU

Q&A

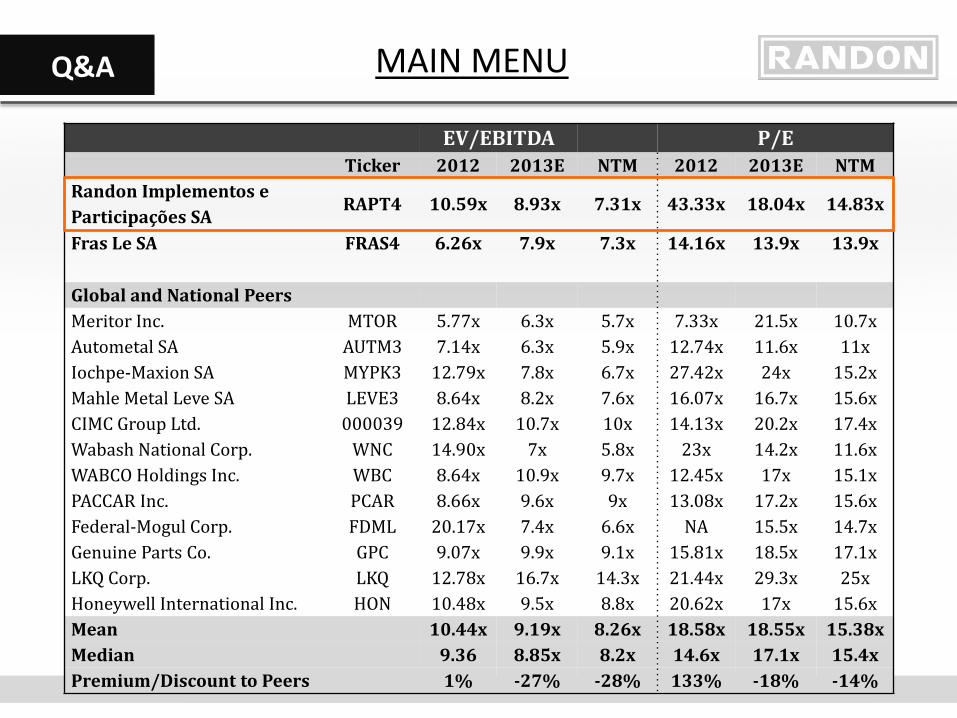

EV/EBITDA P/E Ticker 2012 2013E NTM 2012 2013E NTM

Randon Implementos e Participações SA

RAPT4 10.59x 8.93x 7.31x 43.33x 18.04x 14.83x

Fras Le SA FRAS4 6.26x 7.9x 7.3x 14.16x 13.9x 13.9x

Global and National Peers Meritor Inc. MTOR 5.77x 6.3x 5.7x 7.33x 21.5x 10.7x Autometal SA AUTM3 7.14x 6.3x 5.9x 12.74x 11.6x 11x Iochpe-Maxion SA MYPK3 12.79x 7.8x 6.7x 27.42x 24x 15.2x Mahle Metal Leve SA LEVE3 8.64x 8.2x 7.6x 16.07x 16.7x 15.6x CIMC Group Ltd. 000039 12.84x 10.7x 10x 14.13x 20.2x 17.4x Wabash National Corp. WNC 14.90x 7x 5.8x 23x 14.2x 11.6x WABCO Holdings Inc. WBC 8.64x 10.9x 9.7x 12.45x 17x 15.1x PACCAR Inc. PCAR 8.66x 9.6x 9x 13.08x 17.2x 15.6x Federal-Mogul Corp. FDML 20.17x 7.4x 6.6x NA 15.5x 14.7x Genuine Parts Co. GPC 9.07x 9.9x 9.1x 15.81x 18.5x 17.1x LKQ Corp. LKQ 12.78x 16.7x 14.3x 21.44x 29.3x 25x Honeywell International Inc. HON 10.48x 9.5x 8.8x 20.62x 17x 15.6x Mean 10.44x 9.19x 8.26x 18.58x 18.55x 15.38x Median 9.36 8.85x 8.2x 14.6x 17.1x 15.4x Premium/Discount to Peers 1% -27% -28% 133% -18% -14%

MAIN MENU

Q&A

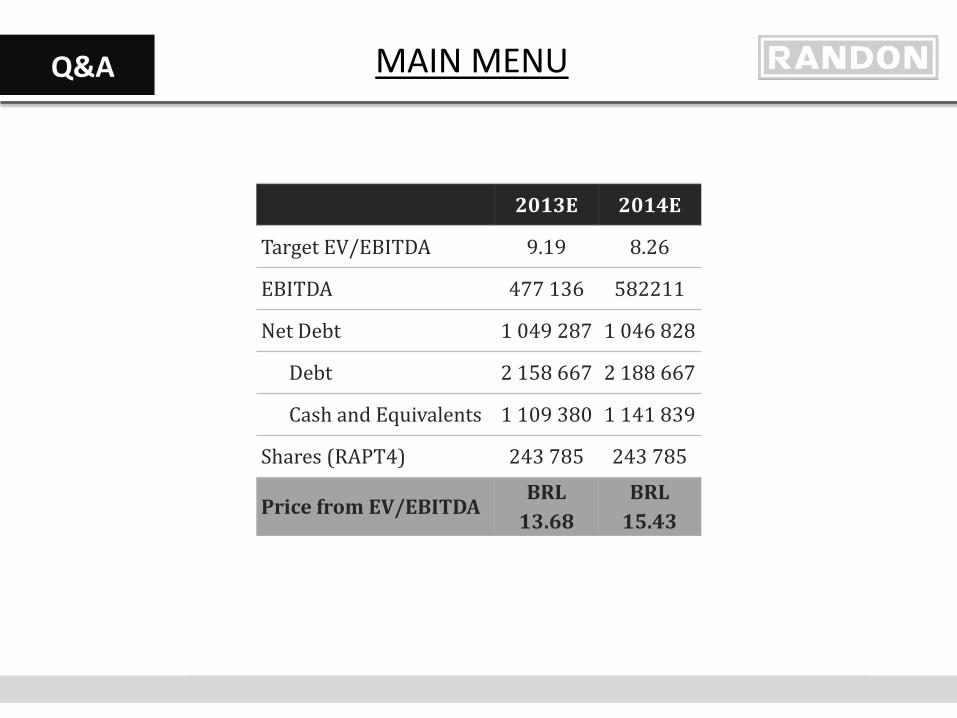

2013E 2014E

Target EV/EBITDA 9.19 8.26

EBITDA 477 136 582211

Net Debt 1 049 287 1 046 828

Debt 2 158 667 2 188 667

Cash and Equivalents 1 109 380 1 141 839

Shares (RAPT4) 243 785 243 785

Price from EV/EBITDA BRL

13.68 BRL

15.43

MAIN MENU

Q&A

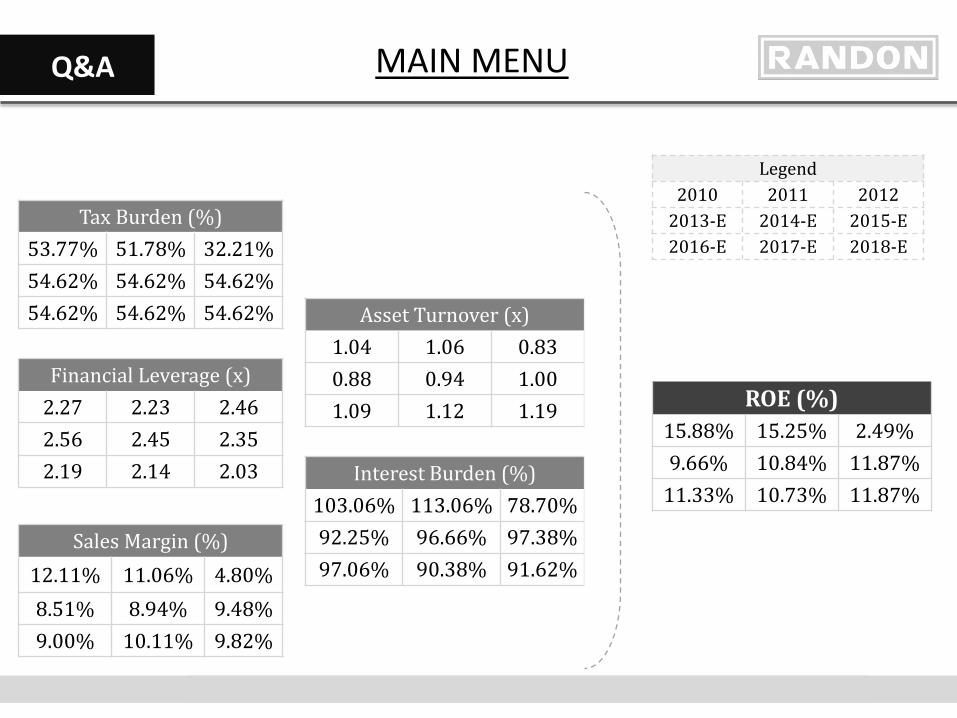

ROE (%) 15.88% 15.25% 2.49% 9.66% 10.84% 11.87%

11.33% 10.73% 11.87%

Tax Burden (%) 53.77% 51.78% 32.21% 54.62% 54.62% 54.62% 54.62% 54.62% 54.62%

Sales Margin (%)

12.11% 11.06% 4.80%

8.51% 8.94% 9.48% 9.00% 10.11% 9.82%

Asset Turnover (x) 1.04 1.06 0.83 0.88 0.94 1.00 1.09 1.12 1.19

Financial Leverage (x) 2.27 2.23 2.46 2.56 2.45 2.35 2.19 2.14 2.03 Interest Burden (%)

103.06% 113.06% 78.70% 92.25% 96.66% 97.38% 97.06% 90.38% 91.62%

Legend 2010 2011 2012

2013-E 2014-E 2015-E 2016-E 2017-E 2018-E

MAIN MENU

Q&A

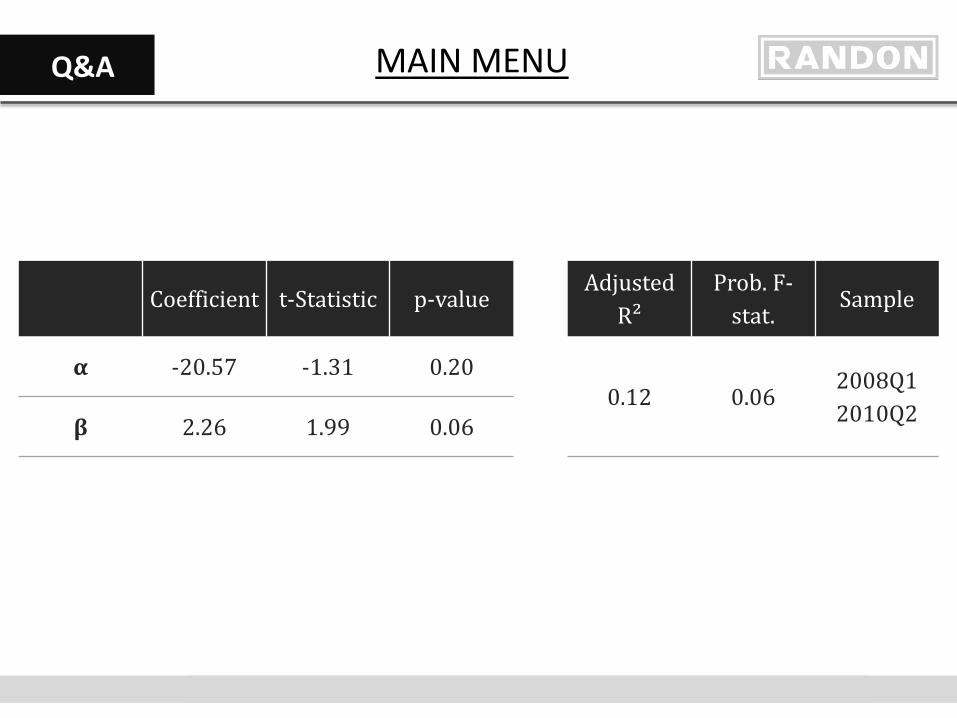

Coefficient t-Statistic p-value Adjusted

R² Prob. F-

stat. Sample

α -20.57 -1.31 0.20 0.12 0.06

2008Q1 2010Q2 β 2.26 1.99 0.06

MAIN MENU

Q&A

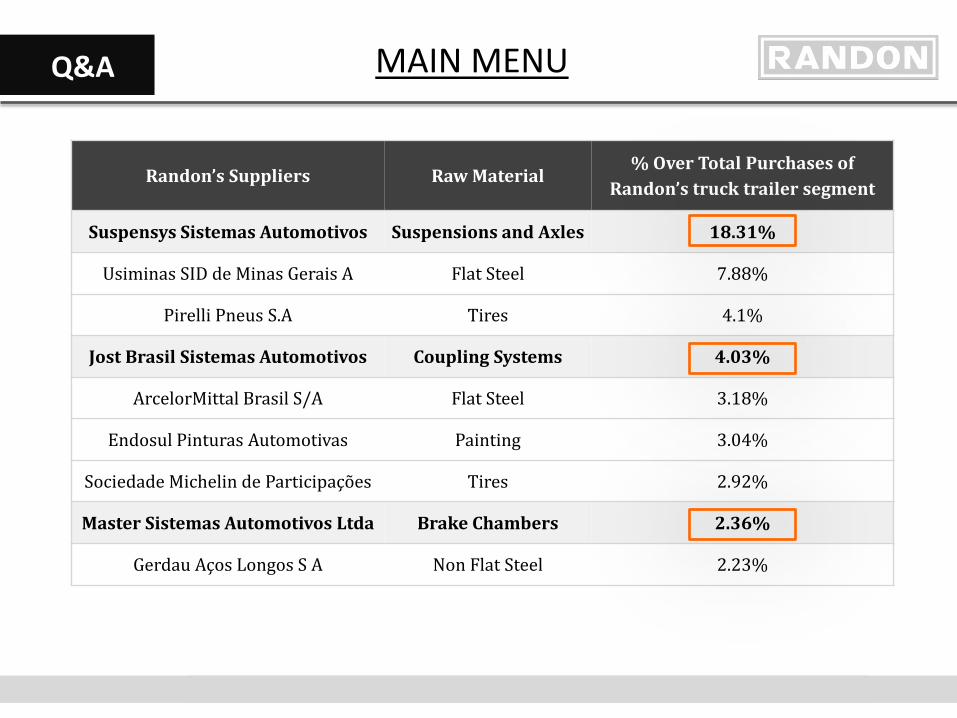

Randon’s Suppliers Raw Material % Over Total Purchases of

Randon’s truck trailer segment

Suspensys Sistemas Automotivos Suspensions and Axles 18.31%

Usiminas SID de Minas Gerais A Flat Steel 7.88%

Pirelli Pneus S.A Tires 4.1%

Jost Brasil Sistemas Automotivos Coupling Systems 4.03%

ArcelorMittal Brasil S/A Flat Steel 3.18%

Endosul Pinturas Automotivas Painting 3.04%

Sociedade Michelin de Participações Tires 2.92%

Master Sistemas Automotivos Ltda Brake Chambers 2.36%

Gerdau Aços Longos S A Non Flat Steel 2.23%

MAIN MENU

Q&A

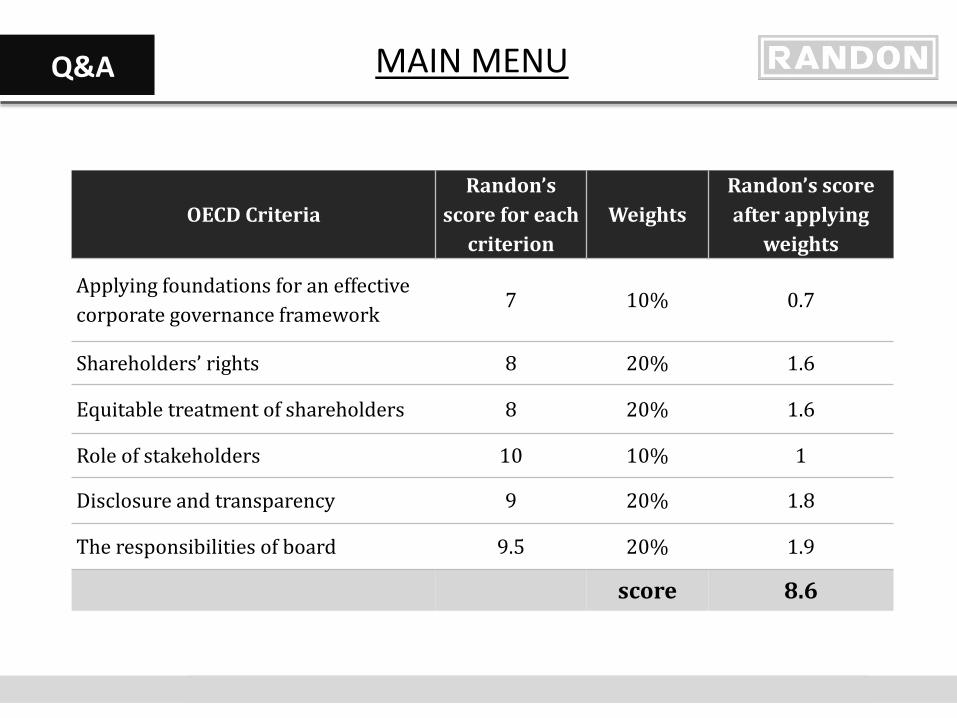

OECD Criteria Randon’s

score for each criterion

Weights Randon’s score after applying

weights

Applying foundations for an effective corporate governance framework

7 10% 0.7

Shareholders’ rights 8 20% 1.6

Equitable treatment of shareholders 8 20% 1.6

Role of stakeholders 10 10% 1

Disclosure and transparency 9 20% 1.8

The responsibilities of board 9.5 20% 1.9

score 8.6

MAIN MENU

Q&A

MAIN MENU

Q&A

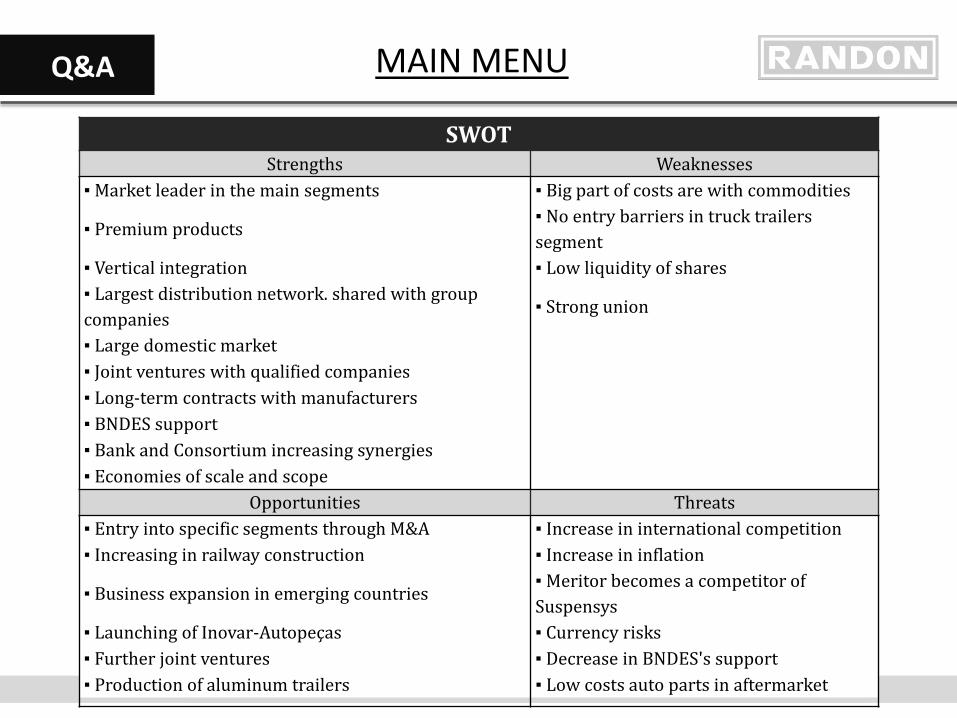

SWOT Strengths Weaknesses

▪ Market leader in the main segments ▪ Big part of costs are with commodities

▪ Premium products ▪ No entry barriers in truck trailers segment

▪ Vertical integration ▪ Low liquidity of shares ▪ Largest distribution network. shared with group companies

▪ Strong union

▪ Large domestic market ▪ Joint ventures with qualified companies ▪ Long-term contracts with manufacturers ▪ BNDES support ▪ Bank and Consortium increasing synergies ▪ Economies of scale and scope

Opportunities Threats ▪ Entry into specific segments through M&A ▪ Increase in international competition ▪ Increasing in railway construction ▪ Increase in inflation

▪ Business expansion in emerging countries ▪ Meritor becomes a competitor of Suspensys

▪ Launching of Inovar-Autopeças ▪ Currency risks ▪ Further joint ventures ▪ Decrease in BNDES's support ▪ Production of aluminum trailers ▪ Low costs auto parts in aftermarket

MAIN MENU

Q&A

MAIN MENU

Q&A

MAIN MENU

Q&A

MAIN MENU

Q&A

0

50

100

150

200

250

0

500

1000

1500

2000

2500

3000

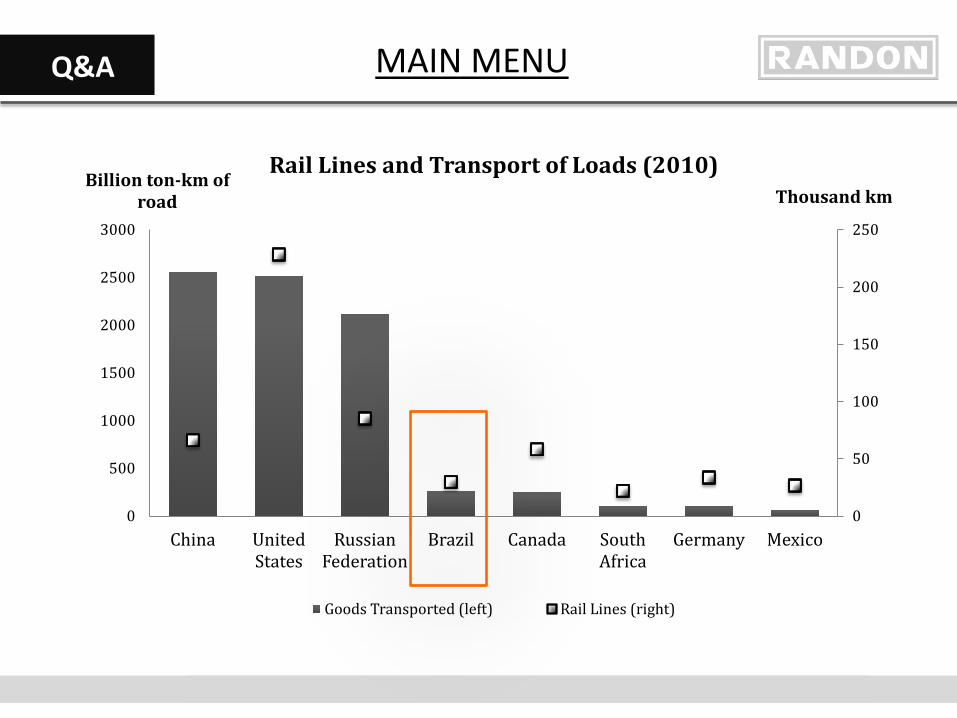

China United States

Russian Federation

Brazil Canada South Africa

Germany Mexico

Thousand km Billion ton-km of

road

Rail Lines and Transport of Loads (2010)

Goods Transported (left) Rail Lines (right)

MAIN MENU

Q&A

0

1

2

3

4

5

6

7

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

China United States

Brazil Germany Mexico Russian Federation

Turkey Canada

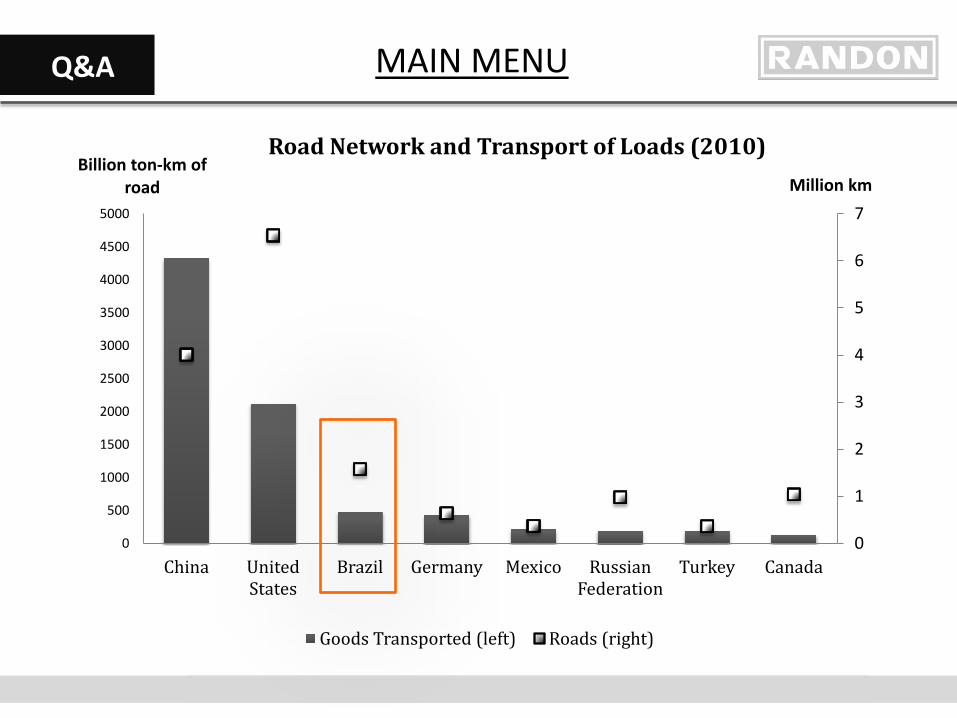

Million km Billion ton-km of

road

Road Network and Transport of Loads (2010)

Goods Transported (left) Roads (right)

MAIN MENU

Q&A

MAIN MENU

Q&A

Ranking of Global Trailers Producers in 2011

Position Producer Nationality Trailers

1 CIMC Group China 137.000

2 Wabash National Corp USA 46.526

3 Schmitz Cargobull AG Germany 45.000

4 Great Dane Limited Partnership USA 38.000

5 Utility Trailer Manufacturing USA 33.289

6 Randon S/A Implementos e Participações Brazil 25.477

7 Hyundai Translead Korea 24.522

8 Bernard-Krone Holding GmbH & Co Germany 20.000

9 Kogel Fahrzeugwerke GmbH Germany 14.500

10 Stoughton Trailers USA 11.800

MAIN MENU

Q&A

MAIN MENU

Q&A

MAIN MENU

Q&A

12%

14%

16%

18%

20%

22%

24%

26%

2 3 4 5 6 7 8 9

10 Net revenue

Net Revenue (BRL billion) Net revenue (USD)

MAIN MENU

Q&A

Distributions centers of trailers segment

MAIN MENU

Q&A

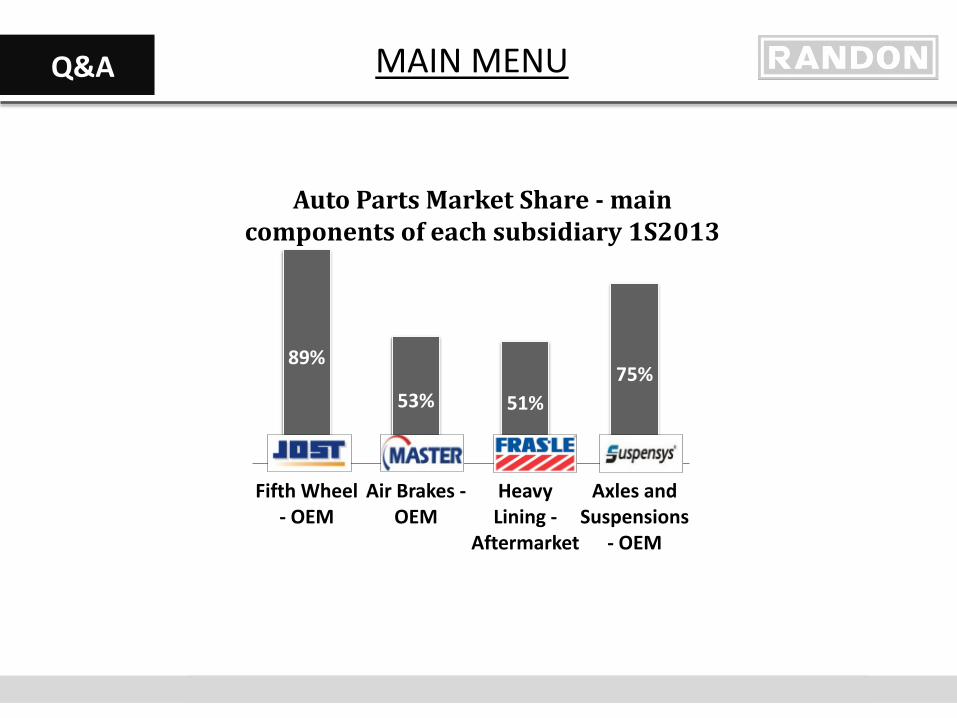

89%

53% 51% 75%

Fifth Wheel - OEM

Air Brakes - OEM

Heavy Lining -

Aftermarket

Axles and Suspensions

- OEM

Auto Parts Market Share - main components of each subsidiary 1S2013

MAIN MENU

Q&A

MAIN MENU

Q&A

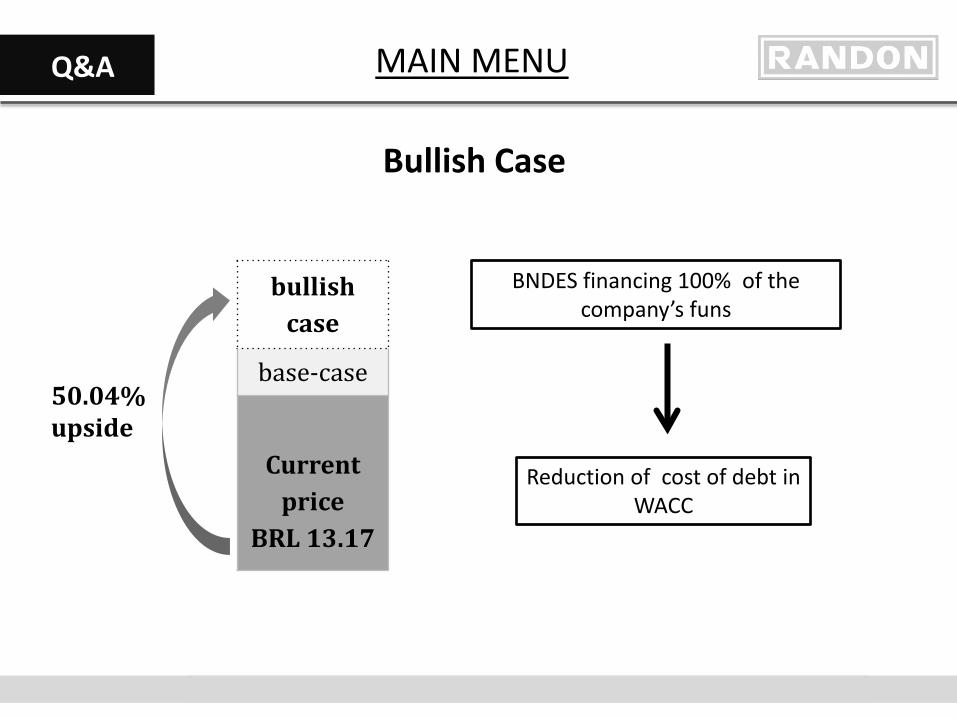

bullish case

base-case

Current

price BRL 13.17

50.04% upside

Bullish Case

MAIN MENU

BNDES financing 100% of the company’s funs

Reduction of cost of debt in WACC

Q&A

MAIN MENU

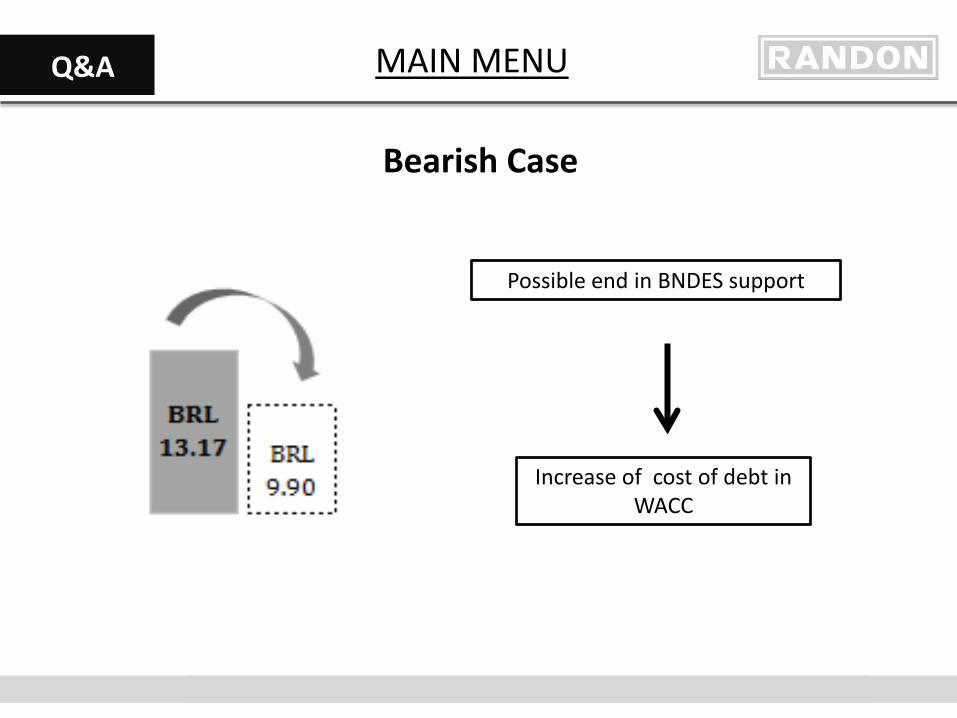

Possible end in BNDES support

Increase of cost of debt in WACC

Bearish Case

Q&A

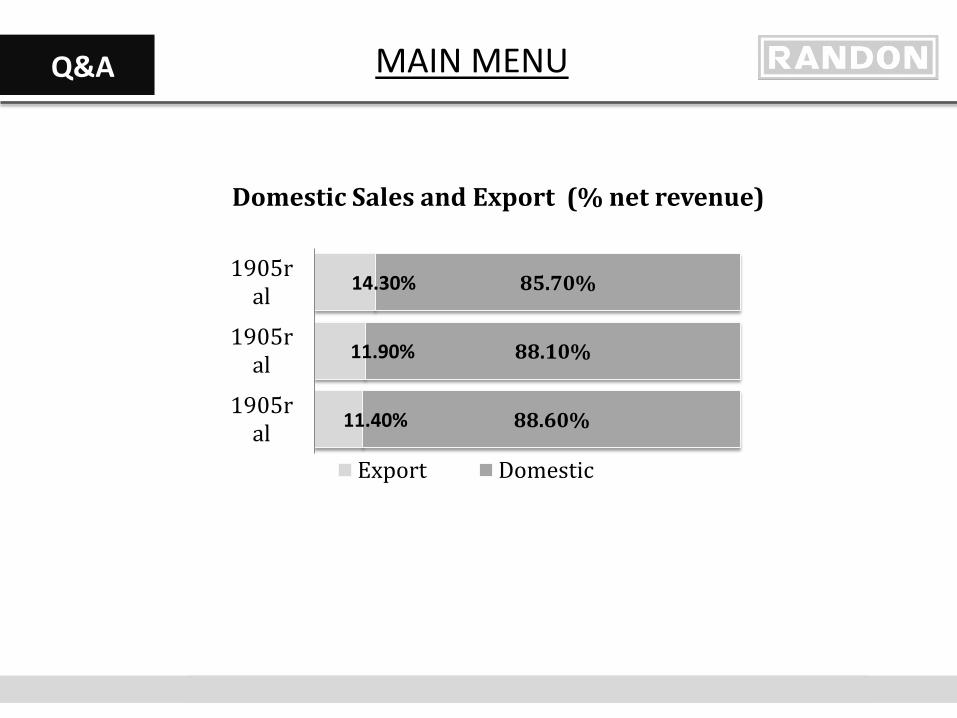

Domestic Sales and Export (% net revenue)

11.40%

11.90%

14.30%

88.60%

88.10%

85.70%

1905ral

1905ral

1905ral

Export Domestic

MAIN MENU

Q&A

MAIN MENU

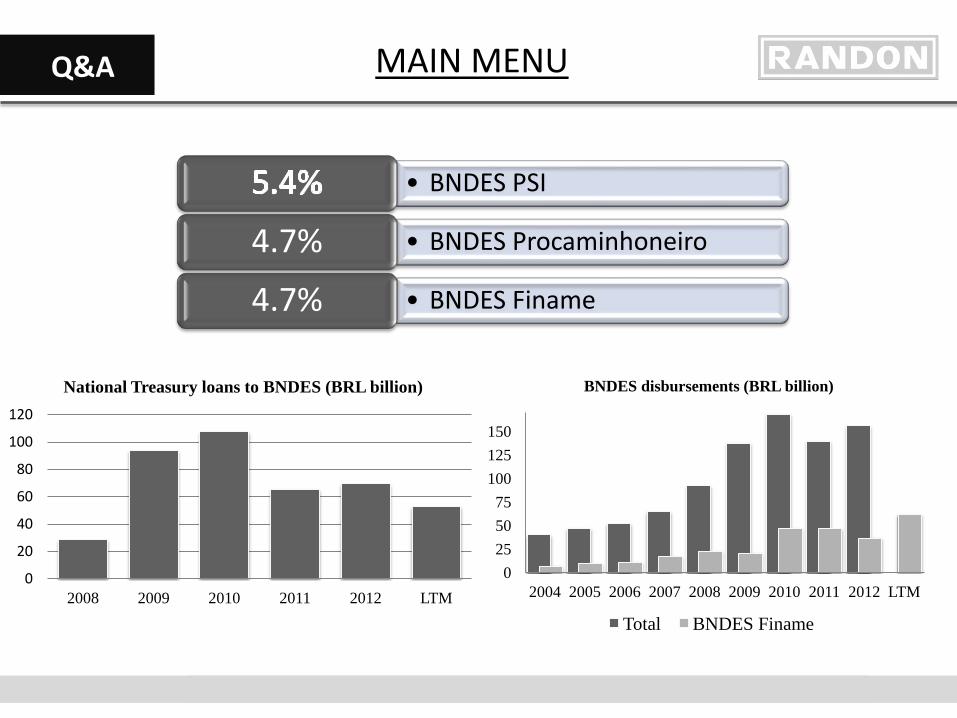

• BNDES PSI

• BNDES Procaminhoneiro 4.7% • BNDES Finame 4.7%

0 25 50 75

100 125 150

2004 2005 2006 2007 2008 2009 2010 2011 2012 LTM

BNDES disbursements (BRL billion)

Total BNDES Finame

0

20

40

60

80

100

120

2008 2009 2010 2011 2012 LTM

National Treasury loans to BNDES (BRL billion)

Q&A

MAIN MENU

Company’s Strategy

• Strategic partnerships; • Maintain the leadership in domestic market; • Advance in international markets; • Decentralization of the productive structure; • Diversification of the product portfolio and

promotion of vertical integration.

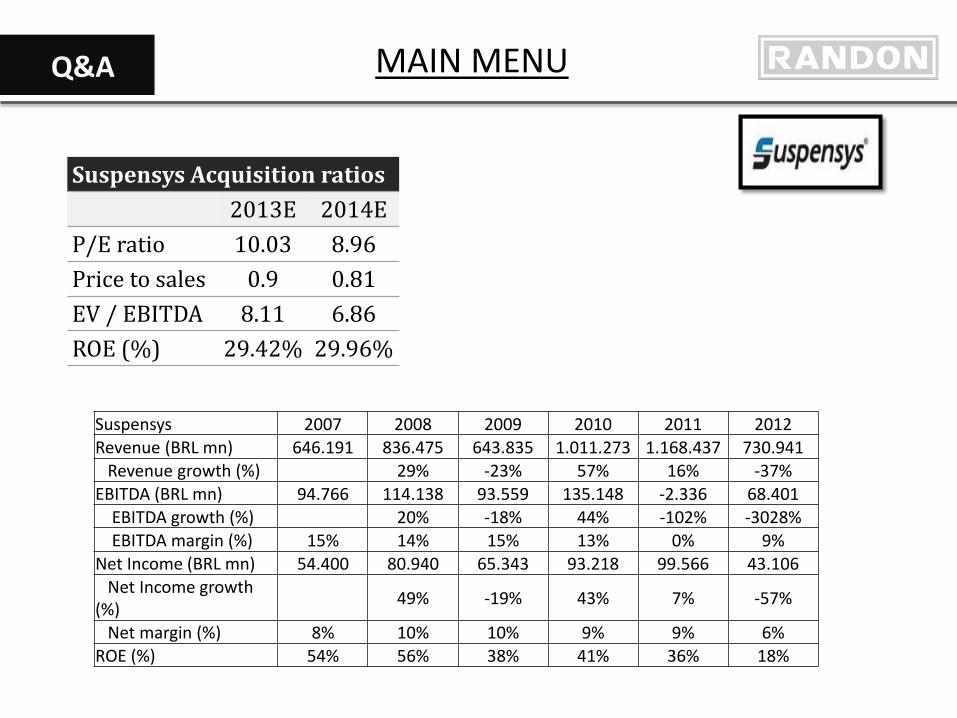

Suspensys Acquisition ratios 2013E 2014E P/E ratio 10.03 8.96 Price to sales 0.9 0.81 EV / EBITDA 8.11 6.86 ROE (%) 29.42% 29.96%

Suspensys 2007 2008 2009 2010 2011 2012 Revenue (BRL mn) 646.191 836.475 643.835 1.011.273 1.168.437 730.941 Revenue growth (%) 29% -23% 57% 16% -37% EBITDA (BRL mn) 94.766 114.138 93.559 135.148 -2.336 68.401 EBITDA growth (%) 20% -18% 44% -102% -3028% EBITDA margin (%) 15% 14% 15% 13% 0% 9% Net Income (BRL mn) 54.400 80.940 65.343 93.218 99.566 43.106 Net Income growth (%) 49% -19% 43% 7% -57%

Net margin (%) 8% 10% 10% 9% 9% 6% ROE (%) 54% 56% 38% 41% 36% 18%

Q&A

MAIN MENU

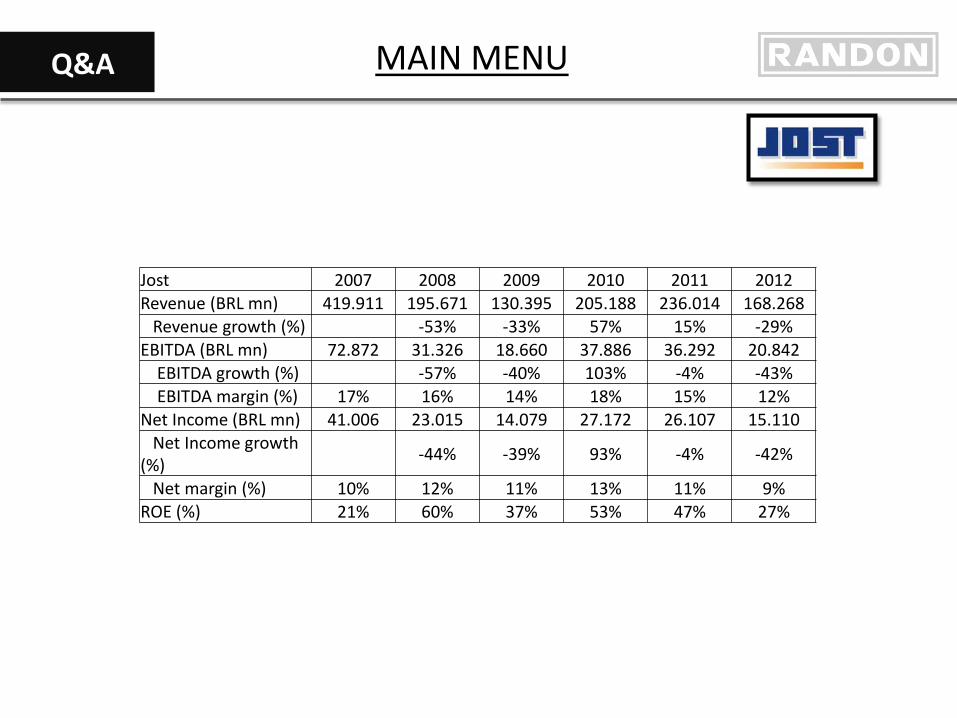

Jost 2007 2008 2009 2010 2011 2012 Revenue (BRL mn) 419.911 195.671 130.395 205.188 236.014 168.268 Revenue growth (%) -53% -33% 57% 15% -29% EBITDA (BRL mn) 72.872 31.326 18.660 37.886 36.292 20.842 EBITDA growth (%) -57% -40% 103% -4% -43% EBITDA margin (%) 17% 16% 14% 18% 15% 12% Net Income (BRL mn) 41.006 23.015 14.079 27.172 26.107 15.110 Net Income growth (%) -44% -39% 93% -4% -42%

Net margin (%) 10% 12% 11% 13% 11% 9% ROE (%) 21% 60% 37% 53% 47% 27%

Q&A

MAIN MENU

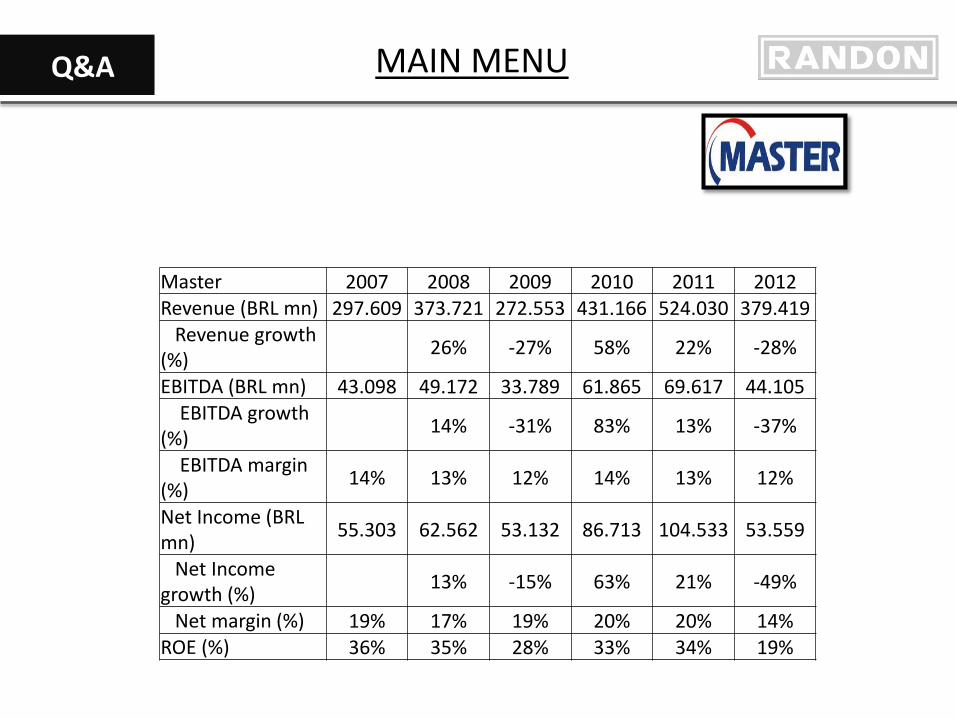

Master 2007 2008 2009 2010 2011 2012 Revenue (BRL mn) 297.609 373.721 272.553 431.166 524.030 379.419 Revenue growth (%) 26% -27% 58% 22% -28%

EBITDA (BRL mn) 43.098 49.172 33.789 61.865 69.617 44.105 EBITDA growth (%) 14% -31% 83% 13% -37%

EBITDA margin (%) 14% 13% 12% 14% 13% 12%

Net Income (BRL mn) 55.303 62.562 53.132 86.713 104.533 53.559

Net Income growth (%) 13% -15% 63% 21% -49%

Net margin (%) 19% 17% 19% 20% 20% 14% ROE (%) 36% 35% 28% 33% 34% 19%

Q&A

MAIN MENU

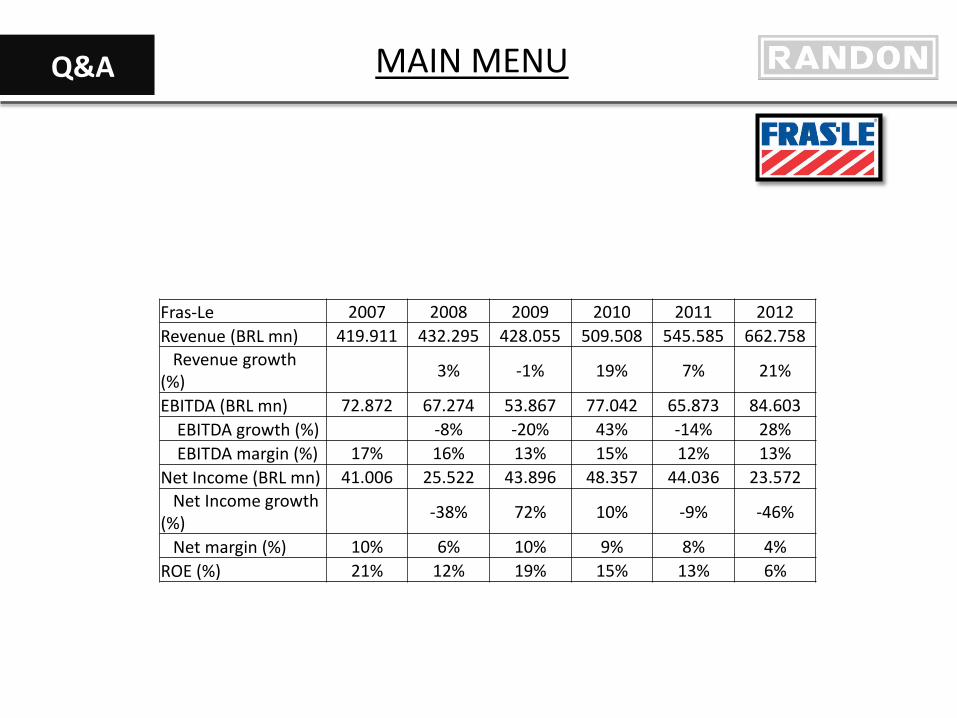

Fras-Le 2007 2008 2009 2010 2011 2012 Revenue (BRL mn) 419.911 432.295 428.055 509.508 545.585 662.758 Revenue growth (%) 3% -1% 19% 7% 21%

EBITDA (BRL mn) 72.872 67.274 53.867 77.042 65.873 84.603 EBITDA growth (%) -8% -20% 43% -14% 28% EBITDA margin (%) 17% 16% 13% 15% 12% 13% Net Income (BRL mn) 41.006 25.522 43.896 48.357 44.036 23.572 Net Income growth (%) -38% 72% 10% -9% -46%

Net margin (%) 10% 6% 10% 9% 8% 4% ROE (%) 21% 12% 19% 15% 13% 6%

Q&A

MAIN MENU

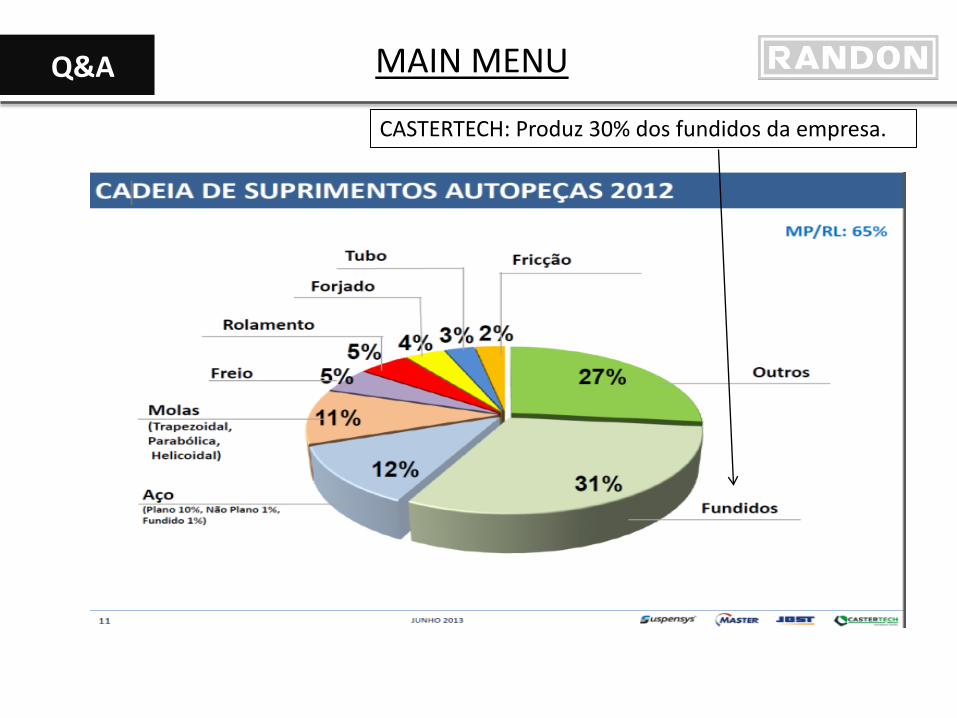

CASTERTECH: Produz 30% dos fundidos da empresa.

Q&A

MAIN MENU

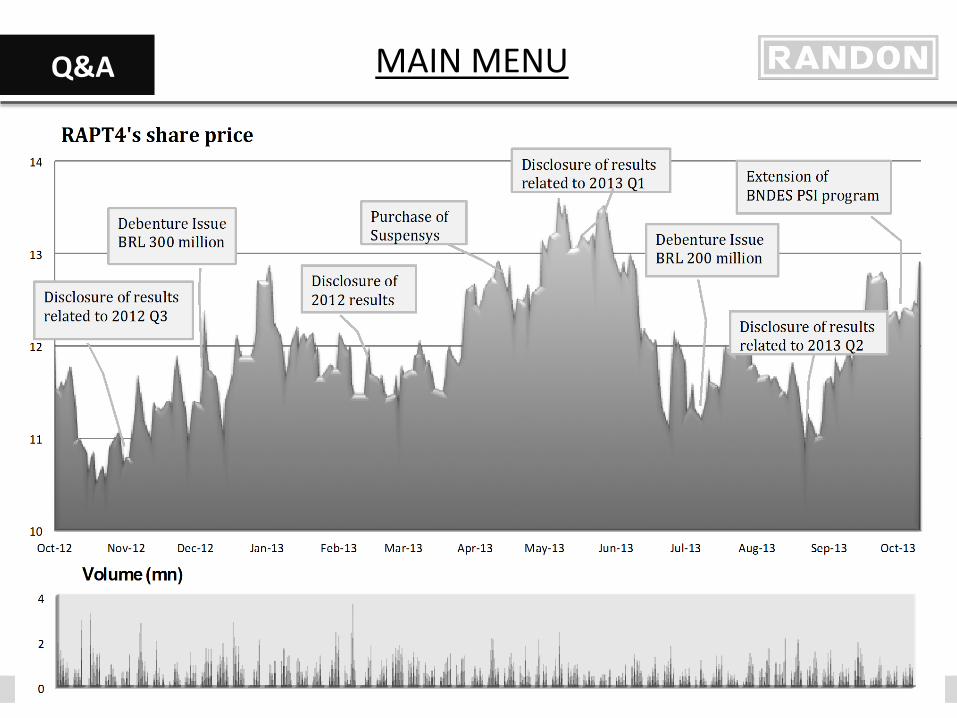

Principais eventos históricos

Q&A

MAIN MENU

Agribusiness

Q&A

MAIN MENU

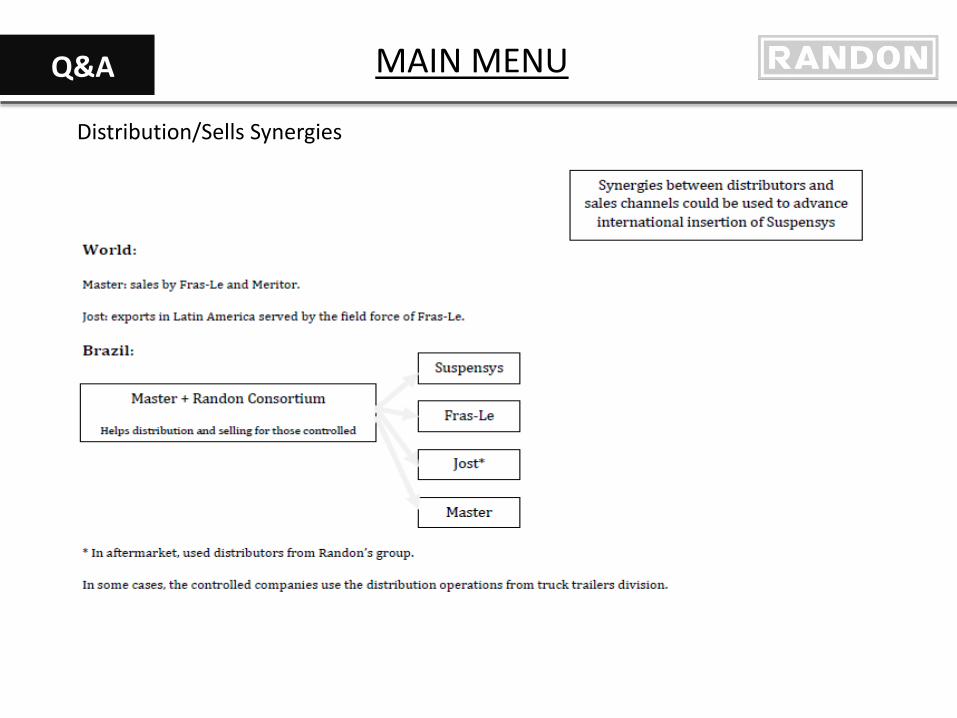

Distribution/Sells Synergies

Q&A

MAIN MENU

Sensibility Analysis

Q&A

MAIN MENU

Risk Matrix

Q&A

MAIN MENU

Introduction Investment Case Risks Conclusion

INTRODUTION

Main Shareholders

Free Float: 57.5%

Dramd (Controller group): 40.6%

Others: 1.9%

Stock Data Price at 10/20/2013: BRL 13.17 52 Week Price Range: BRL 10.56 - 13.6 Market Cap (bn): BRL 3.21 Shares Outstanding: 243.78 K Daily Volume (LTM Avarage): BRL 12.19 mn Beta (12m): 0.53

Main Shareholders

Free Float: 57.5%

Dramd (Controller group): 40.6%

Others: 1.9%

Stock Data Price at 10/20/2013: BRL 13.17 52 Week Price Range: BRL 10.56 - 13.6 Market Cap (bn): BRL 3.21 Shares Outstanding: 243.78 K Daily Volume (LTM Avarage): BRL 12.19 mn Beta (12m): 0.53

Stock Data Price at 10/20/2013: BRL 13.17 52 Week Price Range: BRL 10.56 - 13.6 Market Cap (bn): BRL 3.21 Shares Outstanding: 243.78 K Daily Volume (LTM Avarage): BRL 12.19 mn Beta (12m): 0.53

MAIN MENU

Introduction Investment Case Risks Conclusion

INTRODUTION

Market Price BRL 3 bn

Target Price BRL 16,15

BUY Recommendation

31% Upiside Potential

MAIN MENU

Net revenue per segment

Introduction Investment Case Risks Conclusion

BUSINESS DESCTIPTION

Vehicles and

trailers 51%

Auto parts 47%

Financial services

2%

Truck trailers

83%

Special vehicles

10%

Rail Wagons 7%

Suspension Systems

36%

Friction materials

34%

Air Brakes 21%

Castings 9% Data from 1S 2013

MAIN MENU

Introduction Investment Case Risks Conclusion

WHY BUY?

Good opportunities in the coming years for the sector

Confirmative Valuation

Randon is the most prepared company to leverage market opportunities

MAIN MENU

Introduction Investment Case Risks Conclusion

INDUSTRY OVERVIEW

Porter Analysis Key characteristics:

Low entry barriers – process

with low technology

B2C trade – demand on request

Low penetration of imports

Large customer base 0 1 2 3 4 5

Threat of New Entrants

Bargaining Power of Buyers

Bargaining Power of Suppliers

Competition in the Industry

Threat of Substitute Products

TRUCK TRAILERS

MAIN MENU

Introduction Investment Case Risks Conclusion

INDUSTRY OVERVIEW

Porter Analysis Key characteristics: High entry barriers – requires

high technology processes

B2B trade – concentrated customer base

Joint engineering strategy - integration between subsidiaries

Drivers: domestic and international automotive production and aftermarket needs.

0 1 2 3 4 5

Threat of New Entrants

Bargaining Power of Buyers

Bargaining Power of Suppliers

Competition in the Industry

Threat of Substitute Products

AUTO PARTS

MAIN MENU

Introduction Investment Case Risks Conclusion

INDUSTRY OVERVIEW

AUTO PARTS

OEM

(Original Equipment

Manufacturer)

Company

Long-term contracts

MAN

biggest player in the market

Suspensys

Partnership

MAIN MENU

Introduction Investment Case Risks Conclusion

INDUSTRY OVERVIEW

•9%

•16% Auto Parts

MAIN MENU

Introduction Investment Case Risks Conclusion

RENEWAL OF TRUCK FLEET

Brazil 16.6 years

USA 7 years

EURO V technology efficiency gains

Average age of truck fleet

Finame PSI program: Annual interest rates = 4.5 – 6%

Anticipation of the

Renewal of Truck Fleet

Potential Growth Driver

BNDES support

MAIN MENU

Introduction Investment Case Risks Conclusion

RECENT INDUSTRY GROWTH

2012 Q3

8.8%

2013 Q3

15.5%

Δ%

6.7 EBITDA Margin

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012 2013E

Truck production (BRL thousand)

Adverse Events

Recovery

MAIN MENU

Introduction Investment Case Risks Conclusion

INDUSTRY GROWTH ESTIMATED

50

100

150

200

250

300

2000 2004 2008 2012 2016E 2020E

National Truck Production (thousand units)

CAGR2000-2012

8.15%

CAGR2013-2020

6.82%

Agriculture Pulling Demand

MAIN MENU

Randon is the most prepared company to leverage market opportunities

ERP-SAP

GROWTH DRIVERS

Increase Productivity Gain Economies of Scale

Introduction Investment Case Risks Conclusion

MAIN MENU

Introduction Investment Case Risks Conclusion

GROWTH DRIVERS

SR Bulk Trailer - 3 axis without tires

Company Average price after 4

years of use (BRL) Randon X

Competitors

Randon 52.000

Guerra 49.000 -5.8%

Noma 48.000 -7.7%

Facchini 43.000 -17.3%

Librelato 43.000 -17.3%

Pastre 40.000 -23.1% BT Bulk Trailer - 7 axis without tires

Company Average price after 4

years of use (BRL) Randon X

Competitors

Randon 66.000 Guerra 63.000 -4.5%

Noma 61.000 -7.6%

Facchini 57.000 -13.6%

Librelato 57.000 -13.6%

Pastre 53.000 -19.7%

MAIN MENU

Introduction Investment Case Risks Conclusion

GROWTH DRIVERS

Investments in R&D

E-coat painting system

Proving ground

MAIN MENU

Introduction Investment Case Risks Conclusion

GROWTH DRIVERS

GROWTH POTENTIAL 30% ROE EV/EBITDA 6.9

More expensive dollar

International expansion

SYNERGIES FOR AUTO PARTS SEGMENT AND FOR TRUCK

TRAILERS SEGMENT

MAIN MENU

Introduction Investment Case Risks Conclusion

GROWTH DRIVERS

Distribution Network

High

Medium

Medium

Low

Medium

Finance Service

✔

✔

✗

✗

✗

Premium Products

✔

✗

✗

✗

✗

MAIN MENU

Introduction Investment Case Risks Conclusion

VALUATION

UPSIDE: 31%

Target Price: BRL 16.15

Current Price: BRL 12.31 11.15.2013

DCF COMPONENTS

DCF Model Multiples Analysis Margins

Cash per share Debt per share Terminal Value 10 years projected Cash Flows Target Price

BRL 4.55 BRL 8.16 BRL 14.70 BRL 5.06 BRL 16.15

Confirmative Valuation

MAIN MENU

Introduction Investment Case Risks Conclusion

VALUATION

DCF Model Multiples Analysis Margins

National market growth Gain in market-share International expansion Strong dollar

10 YEARS FORECAST

SALES CAGR: 9.5%

EPS growth (2013E – 2022E): 10.18%

MAIN MENU

Introduction Investment Case Risks Conclusion

VALUATION

DCF Model Multiples Analysis Margins

WACC

Increase in competitiviness: 0.5% Financial crisis: 0.3% Lose Government and BNDES support: 0.5%

EXTRA RISKS 1.3%

MAIN MENU

Introduction Investment Case Risks Conclusion

VALUATION

DCF Model Multiples Analysis Margins

0

20

40

60

80

100

120

140

0%

5%

10%

15%

20%

25%

2008Q1 2008Q3 2009Q1 2009Q3 2010Q1 2010Q3 2011Q1 2011Q3 2012Q1 2012Q3 2013Q1

Gross Margin (%) Commodities - Metal Commodities - Energy

Source: IPEA and Company Data

GROSS MARGINS

MAIN MENU

Introduction Investment Case Risks Conclusion

VALUATION

DCF Model Multiples Analysis Margins

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

0

200

400

600

800

1000

1200

2011 2012 2013-E 2014-E 2015-E 2016-E 2017-E 2018-E 2019-E 2020-E 2021-E 2022-E

EBITDA EBITDA Margin

EBITDA MARGINS

MAIN MENU

Introduction Investment Case Risks Conclusion

VALUATION

DCF Model Multiples Analysis Margins

Multiples Target Price: BRL 15.46

UPSIDE: 25.6%

EV/EBITDA P/E Randon Implementos e Participações SA 7.31x 14.83x

Fras Le SA 7.3x 13.9x Global and National Similar Competitors Meritor Inc. 5.7x 10.7x Autometal SA 5.9x 11x Iochpe-Maxion SA 6.7x 15.2x Mahle Metal Leve SA 7.6x 15.6x CIMC Group Ltd. 10x 17.4x Wabash National Corp. 5.8x 11.6x WABCO Holdings Inc. 9.7x 15.1x PACCAR Inc. 9x 15.6x Federal-Mogul Corp. 6.6x 14.7x Genuine Parts Co. 9.1x 17.1x LKQ Corp. 14.3x 25x Honeywell Int. Inc. 8.8x 15.6x Mean 8.26x 15.38x Median 8.2x 15.4x

MAIN MENU

Introduction Investment Case Risks Conclusion

RISKS ANALYSIS 9

,0

9,8

1

0,5

1

1,3

1

2,0

1

2,8

1

3,5

1

4,3

1

5,0

1

5,8

1

6,5

1

7,2

1

8,0

1

8,7

1

9,5

2

0,2

2

1,0

2

1,7

2

2,5

2

3,2

2

4,0

2

4,7

2

5,5

2

6,2

2

6,9

2

7,7

2

8,4

2

9,2

2

9,9

3

0,7

3

1,4

3

2,2

3

2,9

3

3,7

3

4,4

3

5,2

3

5,9

3

6,6

3

7,4

3

8,1

3

8,9

3

9,6

4

0,4

4

1,1

Freq

uenc

y (x

)

Target Price (BRL)

Buy: 71.21% Hold: 17.29%

Sell: 11.5%

Monte Carlo

MAIN MENU

Monte Carlo

Q&A

MAIN MENU