r&dflora.insead.edu/fichiersti_wp/inseadwp2000/2000-26.pdfr&d international perspectives on...

TRANSCRIPT

R&D

INTERNATIONAL PERSPECTIVES ON THE STATE

OF THE E-BUSINESS REVOLUTION

by

T. COLTMAN * T. M. DEVINNEY ** A. S. LATUKEFU †

and D. F. MIDGLEY ††

2000/26/MKT

* Ph.D. at the Centre for Corporate Change, Australian Graduate School of Management, University

of New South Wales, Sydney, Australia 2052. ** Director at the Centre for Corporate Change, Australian Graduate School of Management,

University of New South Wales, Sydney, Australia 2052. † Researcher at the Centre for Corporate Change, Australian Graduate School of Management,

University of New South Wales, Sydney, Australia 2052. †† Professor of Marketing, INSEAD, Boulevard de Constance, 77305 Fontainebleau Cedex, France. A working paper in the INSEAD Working Paper Series is intended as a means whereby a faculty researcher's thoughts and findings may be communicated to interested readers. The paper should be considered preliminary in nature and may require revision. Printed at INSEAD, Fontainebleau, France.

International Perspectives on the State of the e-Business Revolution

Tim Coltman Australian Graduate School of Management

University of New South Wales +61 2 9931 9368

+61 2 9313 7279 (fax) [email protected]

Timothy M. Devinney

Australian Graduate School of Management University of New South Wales

+61 2 9931 9382 +61 2 9313 7279 (fax)

’Alopi S. Latukefu Australian Graduate School of Management

University of New South Wales +61 2 9931 9510

+61 2 9313 7279 (fax) [email protected]

David F. Midgley

INSEAD Fontainebleau FRANCE

+33 1 6072 4229 +33 1 6074 5500 (fax)

Paper presented to the eCommerce and Global Business Forum, Santa Cruz, California, May 2000. This

research is supported by a grant from the Centre for Corporate Change at the AGSM and the R&D

Division of Insead.

Abstract

International Perspectives on the State of the E-Business Revolution

A common belief emanating from the US is that information and network-based systems herald a

‘new economy’ revolutionizing the way business is conducted. In this paper, we advance an

international perspective that questions whether e-business truly represents a revolution in the way firms’

operate or whether it is a more normal evolution driven by technology—i.e., whether it is simply a

variation on a theme. Although such a question appears mundane, it is fundamental that both academics

and business practitioners understand the answer to this question. For, in the end, the answer determines

the relevance of current academic theory and business practice to the supposed new reality.

Our paper builds on neo-institutional economic thinking and a recent theory of international

business structure to examine the three core determinants of the performance of multinational firms—the

supply-based pressures for global integration, the demand-based pressures for local responsiveness, and

the contracting pressures for transactional completeness—in an e-business setting. As will be shown, the

role that networking technology plays in determining the structure and strategy of multinational

enterprises in an e-business environment is likely to be more of a variation on a theme than a revolution—

once one accounts for the transactional changes that are occurring. Finally, we extend our perspective on

e-business to assist global managers dealing with the all-important issues of how to build and change

institutions to better exploit the potential of e-business.

State of the e-Business Revolution Page 1

INTRODUCTION

It is almost universally accepted that information and network-based systems will herald in a ‘new

economy’ completely changing the way business and commerce is conducted. According to the

‘e-vangelists’, the winners in the new economy will be those existing firms conducting more and more of

their business through the digital infrastructure (e.g., Ford and General Motors) or those new firms

seeking to exploit the potential of the ‘Net’ (e.g., Yahoo and Amazon). These predictions are fuelled by

increased attention in the popular press, and by a fascination with e-business stock by investors, both

large and small, and their growing disdain for ‘old economy’ operations.1

Booz-Allen & Hamilton (1999) finds that more than 90 per cent of top managers believe the

Internet will have a major impact on the global marketplace by 2001. Given this response, one could

assume that most managers no longer need convincing that they are in the throes of fundamental change

and are busy implementing electronic business plans that will convert their firms to the new economic

model. However, this could not be further from the truth. The reality is that many multinational

enterprises (MNEs) are hesitant to make the enormous investments and are concerned about committing

human and financial capital when they don’t clearly understand how the technology fits with their global

strategy. And their concern is appropriate, particularly in a world with uneven technology standards and

infrastructure across countries and market segments.

A substantial gap exists in our understanding of the e-business technology and its application to

global firms. To address this problem our paper provides a structured examination of the nature of the e-

business in light of the extant frameworks operating in international business (Bartlett & Ghoshal 1989)

and the economic nature of transactional phenomenon (Coase 1937; Williamson (1991; 1996)). Although

it may be considered heresy by e-vangelists, the promises of Internet driven growth for global MNEs may

be more hype than substance when taken from this perspective. There are serious questions regarding the

pace at which the ‘global’ networked economy is emerging and the ultimate suitability of electronically

based business for many MNEs in their roles as integrators across time and space.

State of the e-Business Revolution Page 2

Organization of the Paper

The subsequent sections pose and answer a series of related questions concerning the e-business

phenomenon in relation to the pressures facing, and strategic decisions available to, global firms. We

begin with a comparison of prediction versus reality and argue that much of the hype surrounding the

development of e-business has been wide of the mark. We then suggest a framework to demystify global

strategy and help us understand how it is affected by developments in e-business. In particular, we are

concerned with the growing relevance of institutional economics and contracting theory to assist us in

comprehending why e-business is occurring as it is and what the implications are for MNE strategy and

operations. Next, we extend this view of e-business to assist global managers dealing with the all-

important issues of how to build and change institutions to better exploit the potential of e-business.

ESPOUSED E-BUSINESS AND E-BUSINESS IN USE

Prior encounters with revolutionary technological change highlight the difference between what Argyris

and Schon (1978) have referred to as espoused theories (what we say about the technology) and theories-

in-use (how we actually use the technology). Nowhere is this difference more evident than in the current

discourse surrounding e-business.2 The actual impact e-business is having on the way people shop and

the way business is conducted on a day-to-day basis (theory in use) is still quite different from the way it

is talked about by the technological-elite and reported in the popular media (espoused theory).

Technology-in-use: Business-to-Consumer Perspective

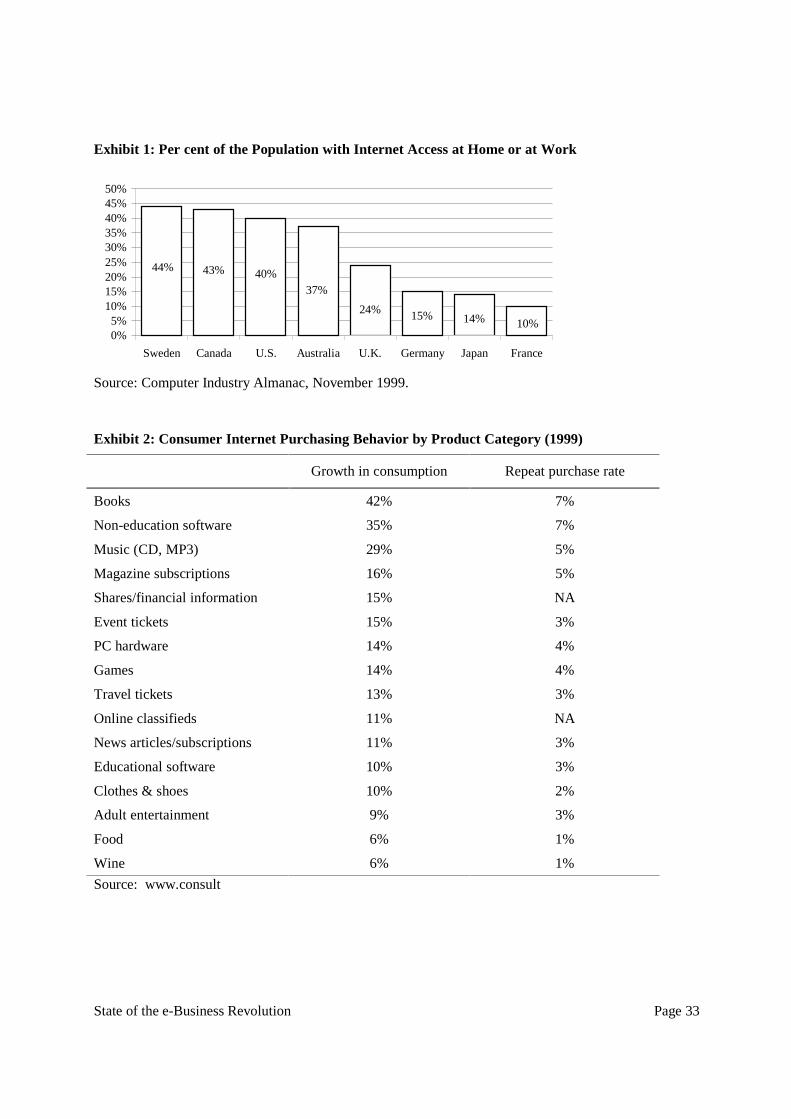

According to the usual statistical sources most people in OECD countries still lack or choose not to have

Internet access (Exhibit 1). Even in the United States, the most networked country in the world,

approximately half the population still do not have Internet access.3 The reason for this differential

uptake is not just because of infrastructure. Germany, for example, has one of the best

telecommunications infrastructures in the world yet is considered a laggard due to delayed deregulation,

reluctance to use credit cards, high prices and conservative business practices (Veeramani & Talbert

1999). Ultimately the pervasiveness of Internet access internationally, is a complex brew of political,

State of the e-Business Revolution Page 3

industrial, societal and infrastructure related factors.

Exhibit 1 about here

For those who have access, either at home or in the office, the Internet has proven to be more of an

addition to their lives—sometimes helpful, at times entertaining, often slow and frustrating—than a

critical and indispensable part of their existence. For example, companies such as Peapod Inc., Netgrocer

Inc., and Streamline have invested millions of dollars into solving a nagging problem most people face

every week, shopping for groceries. Yet despite the best efforts of these companies, less than 1 per cent

of U.S. households order groceries online (Schwartz 1999; pg. 30) and these companies are facing

enormous financial and strategic pressure (CNN 2000a). The empirical evidence suggests that, in reality,

this often-mundane task is seen by many consumers as one of life’s small social pleasures and

furthermore that these consumers have no intention of giving up the physical shopping experience.4

Additionally, many products and services we purchase are ‘experience’ goods and have to be seen, felt or

touched by consumers before they can be appreciated. Exhibit 2 presents the experience of Internet e-

commerce in Australia (which Exhibit 1 shows to be close to the US in Internet penetration) and reveals

two facts: (1) most B2C5 e-commerce is concentrated in products that are validated externally (e.g.,

authors, musicians, brands, etc.) and (2) there is little consumer loyalty, even to a product category.

Notes John Davidson (2000), “consumers use the internet to find the lowest prices on earth, and then walk

into bricks and mortar stores and expect the retailers to match the price.”

Exhibit 2 about here

The bottom line is that despite the media attention, consumer electronic business is still in the

formative stage. Consumers continue to experiment online and there are many business related barriers—

security, privacy, uncertainty, low bandwidth, consumer protection as well as network access—to be

overcome before we can even begin to speak of revolutionary change in consumer outlook and behavior.

Technology in Use: Business-to-Business

At present, most MNEs are less interested in selling online to consumers than in using the Internet to

interact with suppliers and large buyers. Therefore, the potential for near-term transformative change and

State of the e-Business Revolution Page 4

exploitation of e-business lies in upstream B2B activities in contrast to the higher profile but more risky

downstream B2C activities. There are all sorts of reasons why MNEs are more willing than consumers to

communicate, negotiate, buy and sell online:

��Companies, and in particular MNEs, with their experience in managing far-flung subsidiaries, are

better equipped to communicate electronically. Many business transactions are already conducted at

a distance—by facsimile, mail, or electronic data interchange (EDI). These competencies are easily

translated to the e-business realm.6

��Companies are more cost-conscious, since every dollar saved in procurement is equal to a dollar of

new profit. This is most relevant to MNEs who maintain some of the largest procurement systems in

the world and tend to standardize this aspect of their operations.7

��As corporations develop online strategies aimed at reducing costs and increasing efficiency, network

externalities will have a particularly strong impact. Because MNEs have invested substantial

amounts of money in developing global IT supply chain infrastructures, the natural reaction for these

companies is to encourage others to do the same and generate further efficiency gains for the

complete network.8

��Opportunities to create close alliances with business partners offer innovative opportunities to form

strategic relationships or address customer problems in new ways. This is particularly pertinent to

MNEs who, in most cases, possess alliance relationships involving customers, suppliers, distribution

channel members, partners with complementary skills and resources, and sometimes competitors.9

��Functionality has seen the web browser become a default application for many companies and the

dominance of standard open platforms has allowed quick uptake of browser technology as the front-

end of MNE network systems.

The Aberdeen Group “pegs business-to-business at 10 to 20 times the business-to-consumer

market” (Tedeschi, 1999) and the Boston Consulting Group predicts that one-fourth of all business-to-

business purchasing will be conducted online by 2003 some $2 trillion over the Internet and $0.8 trillion

State of the e-Business Revolution Page 5

over private networks using EDI (BCG 1999). For many companies, like Ford, General Electric, Dell and

Cisco, the movement of products from detailed designs to basic commodities through a supply chain is

where the real value in e-business is to be found.

BCG (1999) argues that the most lucrative opportunities for B2B e-commerce are not in

production-oriented savings (estimated at 15 per cent), but in the transaction savings associated with the

procurement, maintenance and governance of indirect materials. Here cost savings associated with

activities such as: selecting products and vendors, filling out requisition forms, securing approvals,

sending out purchase orders, receiving goods, checking content matches the invoices, and sending out the

payment could reach 65 per cent as buyers’ internal purchasing and record keeping processes are

simplified. Traditionally, this has been a manual paper-based process, although some firms have used

EDI to achieve cost savings. However, EDI’s costly support requirement has made it difficult to justify

for many smaller enterprises where it was easier to rely on the fax and telephone for communication. The

development of web based procurement and handling systems such as Chemdex assuage this barrier.

Espoused e-Theory versus R-e-ality

Recent publications and practitioner frameworks are replete with anecdotal evidence touting the supposed

revolutionary aspects of e-business (See Coltman et al. (2000) for a discussion of this). Exhibit 3 presents

a list of the general predictions and the current reality (although clearly not a complete list). A litany of

the predictions would imply that that we would be operating in an business environment of new rules

(Kelly 1998), demanding radically different planning methodologies (Downes & Mui 1998), where speed

is paramount (Downes & Mui 1998), scale is irrelevant (Dyson 1997), intermediaries are by-passed

(Gilder 1994) and a fundamental product and customer rethink (Aldrich 1999) is necessary because our

models of branding (Kalakota & Whinston 1996) and pricing are irrelevant. However, the rhetoric of e-

business is, at times, atheoretic and more reflective of speculators’ hopes than business reality.

Exhibit 3 about here

In trying to understand why such visionary predictions have yet to come to fruition one need

simply refer to a Porteresque value chain. The operational and strategic impact of the complex stream of

State of the e-Business Revolution Page 6

exchange interactions connecting the organizational entity to primary suppliers and customers—

certainly will change in some way shape or form when new technologies and systems appear. However,

the more relevant question is whether these changes are competence enhancing or competence destroying

(Henderson & Clark 1990). If the changes are competence enhancing we would expect both a

reinforcement of existing structures and that the benefits of change will accrue to incumbents. If the

changes are competence destroying then we would expect that the benefits would accrue to new entrants

and the incumbents who are best able to jettison their old structures. Similarly, it is possible that at one

point in the value chain we would see competences reinforced (e.g., brands may take on greater value and

hence benefit incumbent producers) while at another we find competences being destroyed (e.g., supplier

relationship management may become moot in a world of open supplier auction systems making

dedicated systems obsolete).

The e-vangelists live in a world where the Internet represents a system wide competence

destroying change. However, the evidence indicates that this may be true for some components of a

business but it is rare for it to be true for all areas of a firm’s operations. Indeed, one could argue that the

current dominance of B2B Internet activity is due to its competence enhancing nature. It is occurring now

because it is a marginal change from existing supply chain systems. Auction systems are only a

theoretical stone’s throw from traditional open and closed bidding and personal negotiation approaches to

procurement. Hence, the question we seek to address is where are the changes taking place and how are

they most likely to affect the operations and success of MNEs.

UNDERSTANDING E-BUSINESS EVOLUTION IN MNES

Whether induced by technical change or competitive interaction, market turbulence creates organizational

confusion. In providing focus for thinking about the impact of the Internet on the activity of MNEs we

utilize a recently articulated theory developed by Devinney, Midgley & Venaik (2000) (hereinafter

DMV). DMV provide a structured way of examining contestable markets by separating environmental

State of the e-Business Revolution Page 7

pressures from managerial decisions thereby elucidating a clearer understanding of the nature and

evolution of MNE strategy and performance.

According to DMV, the degree to which alternative MNE structures survive and thrive is

determined by the interaction between a series of pressures—that shape the firm—and the ways in which

managers react to these pressures strategically and operationally over time. DMV build on three

traditions. First, they expand the popular integration-responsiveness framework of Prahalad & Doz

(1987) and Bartlett & Ghoshal (1989) by subsuming within their theory the traditional cost driven

pressures of global integration (GI) and demand driven pressures of local responsiveness.10 Second, they

build on the neo-Austrian tradition of the resource-based theory of the firm (Wernerfelt 1984; Barney

1986) by articulating how path dependence and causal ambiguity create very different competing

structures that are sustainable in the same international market. In addition, this helps explain and

account for the organizational stickiness that limits the ability of the MNE to move from one structure to

another quickly. Third, DMV integrate into their theory the role of the completeness of contractual and

institutional structure operating in the market environment so as to account for issues of organizational

structure, ownership and governance, and the control of residual rents from the activities of the firm

(Carson et al. 1999).

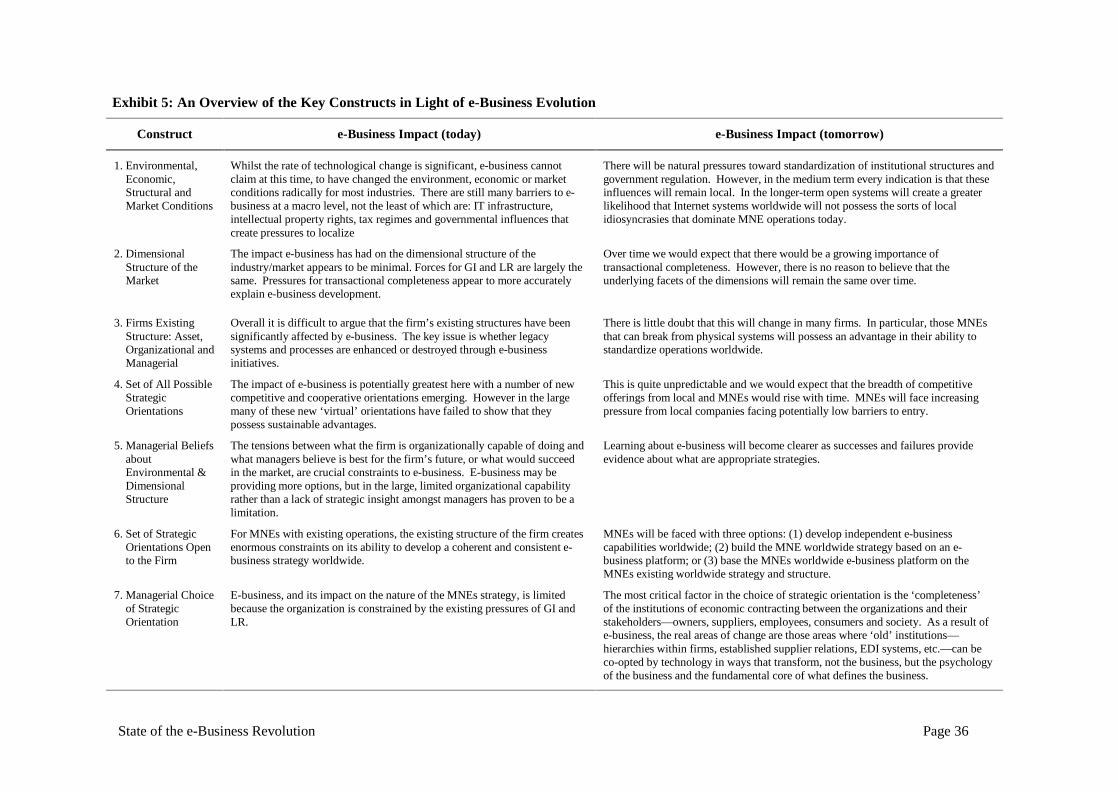

A schematic representation of DMV’s theory is given in Exhibit 4. The model provides a

rigorous way to develop a clearer understanding of the e-business phenomenon by separating the complex

interaction between environmental pressures and constraints from firm constraints and managerial beliefs

and reactions. Four macro constructs, operating over three dimensions (discussed shortly), are identified

in DMV that influence the choice of MNE strategic orientation:

1) The overarching higher level pressures associated with environmental, technological, and economic

and market conditions. These include the social, legal, business and governmental milieu within

which commerce occurs.

2) The way these pressures serve to determine the dimensional structure of the market (see Venaik,

Midgley & Devinney (2000) for an empirical discussion of this).

State of the e-Business Revolution Page 8

3) The set of strategic orientations possible in any given market. Based on the structure of the pressures

in a market there will be a limit to what is possible, both physically and competitively.

4) The influence of the firm’s existing structure. The path dependent nature of the evolution of the firm

will determine where, in any given time frame, it can operate effectively. This will have two related

effects.

a. Managerial beliefs regarding what is best for the firm. Manager’s will need to make choices

about what is ‘best’ from what is ‘possible’ and this will be influenced by their perceptions of

the nature of the pressures and what is possible for the firm to do.

b. The technological feasibility. Along with the pressures faced by the firm from the outside are

the constraints the firm places on itself from its historic operational and strategic choices.

Exhibit 4 about here

Hence we can think of examining the nature of the market and strategic structure of MNEs by

asking a series of related questions. What does the environment allow? How might we represent the

pressures from the environment in a parsimonious way? Given our parsimonious representation of the

pressures being faced, what is possible (ignoring any one firm)? Examining the firm itself, there are two

related questions. First, what is operationally and strategically feasible at any point in time? Second,

what do the managers of the firm believe is the correct strategic orientation at any point in time? It is the

interaction of all these questions, being answered by a host of related firms, that will ultimately determine

the strategic orientation of the MNE and whether that orientation is survivable.

The purpose of this paper is not to repeat DMV’s approach but use it to analyse MNE e-business

evolution. Exhibit 5 lists the macro and micro constructs discussed above and summarizes the relevant

impact e-business has had on the way these activities are organized and configured. The sections that

follow discuss these in greater depth and highlight the discussion with a series of short case studies.

Exhibit 5 about here

State of the e-Business Revolution Page 9

Developing a Parsimonious Model of the Environmental Pressures Facing MNEs

DMV put emphasis on a three dimensional structure of the MNE’s world. If we translate this to

the e-business realm, the question is whether there is any need to change the approach or points

emphasized. As noted in Exhibit 2 many of the beliefs about how e-business would change the world

failed to grasp that the underlying pressures acting upon a business—environmental, technological,

economic and transactional—play a key role in the way firms configure their value adding activities. If

these pressures do not change the firm has little incentive to alter its activities significantly. Taking a less

sanguine view of e-business there is no evidence that its development has changed the regulatory,

economic and transactional conditions dramatically for most industries. This is so for a few simple

reasons. The way the majority of people shop or the way most business is conducted on a day-to-day

basis remains largely the same (albeit sped up to a degree). Access to suitable IT infrastructure is a

problem in many developing countries and cultural idiosyncrasies provide significant hurdles for the sort

of global e-business that would be advantageous to MNEs. In India and China cash is strongly

preferred credit is unavailable and people don’t trust debit accounts to deliver money when they need it.

For example, the high costs associated with reliable delivery and payment makes it much more difficult

for Dagdang.com, an online Chinese bookstore, to expand. Amazon.com and Barnes&Noble.com had

few such problems. Many developing countries have weak legal protection of intellectual property rights

and local government attitudes toward enforcement particularly in more authoritarian regimes can

restrict e-business development opportunities.

However, that said, the nature of these pressures can be expected to change as new industries

arise. For example, it is unlikely that the drivers of the music industry will remain the same if technology

changes the relationship between the musician and the customer (see the Chaosmusic and Sanity case

later in the discussion). Disintermediation and reintermediation may imply that the specific pressures

towards global economies of scale either increase or decrease. Hence, although the notion of GI

pressures11 remains relevant, what defines the GI construct will change as open systems redefine

traditional value chain activities. For example, AutoXchange did not necessarily change the pressures

State of the e-Business Revolution Page 10

facing the global automobile corporations. However, web technology’s ability to provide small and

medium enterprises similar sorts of ‘scale advantages’ in supply chain management have allowed

operations like Chemdex and AT Kearney’s eBreviate system to reduce the importance of locational

proximity for many sorts of procurement requirements. Similarly, LR pressures12 can be expected to

evolve as consumer access widens and if the promises that the technology will change the nature of the

relationship between customer and producer prove true. We noted earlier that on-line grocery operations

have been unsuccessful in places like the US and Australia because of their inability to account for the

way people shop. However, similar services are booming in Europe mainly because restricted shopping

hours create an opportunity to substitute an e-service for the traditional Saturday shopping rush imposed

on European consumers. But even in this case the ability to ‘globalize’ such services is seriously

hampered by the simple fact that delivery must occur.13

Transactional Completeness. DMV have shown that one of the main problems with the IR

framework is that it fails to account for the transactional pressures that impact the firm’s value chain.

They propose a third dimension, transactional completeness, to address this gap. Transactional

completeness (TC) is derived from Grossman and Hart (1983) and Williamson (1991; 1996) and

addresses the issues of organizational form and the economics of information exchange between parties in

a value exchange. A firm is transactionally more complete the more the components of its value chain (or

value network) can be transacted openly in the market (or as if it is in a market). For example, a firm that

can outsource distribution, payment and maintenance in a reliable manner would be more transactionally

complete than one that must do this work in-house as a way of protecting its rights to the assets utilized.

Natural informational asymmetries, legal rights, path dependent activities and historical governance

structures are all pressures driving the ability to engage in more transactionally complete value

exchanges.

It is these sorts of pressures that are most likely to be affected by the evolution of the Internet and

can more accurately explain e-business development in MNEs. The successful use of e-business by firms

such as Amazon, Dell and Cisco has been based on an ability to leverage protection and trust either

State of the e-Business Revolution Page 11

through strong contractual bonds (i.e., patents or standards) or because of the policing power of the

marketplace (particularly in commodity or commodity-like markets). It is apparent that many of the e-

business beneficiaries in the international marketplace of late have largely been firms in those

environments where commodity products can be sourced in a reliable manner from the open market

such as books, toys, CD’s and computer equipment—and validation is ensured either by an existing

brand—e.g., the artist or author—or the ability to free ride on services provided by bricks and mortar

operations—e.g., auto dealers.

A company specializing in one-to-one service with individual pricing is generally going to be less

contractually complete. For example, professional services firms typically own and control much more

of the value chain and ‘webifying’ these activities across the value system in an efficient and effective

manner is much more difficult. For example, Orlikowski (1993) was able to illustrate the difficulty a

management consulting firm experienced implementing Lotus Notes groupware technology. Despite

strong executive support, potential cost savings and technical sophistication in the product, the system

was not widely used. The consulting firm’s structural properties competitive desire to protect individual

competencies and knowledge assets proved to be counter cultural to the premises underlying the e-

business groupware technology (i.e., shared information, co-operation and collaboration). Similar

phenomena are experienced with respect to the institution of ‘knowledge management’ systems where

formal IT structures fail without adaptive informal structures to support them (see, Soo, Midgley &

Devinney 1999).

Hennart (1991) and Dunning (1981; 1995) note how external markets have advantages over

internal coordination by replacing administrative fiat with price based incentives and transactional

alternatives. In examining the nature of the changes that e-business has wrought on the evolution of the

pressures facing MNEs it is the expansion of the usage of the price mechanism and the widening of

contractual choice (in our parlance TC) that has the potential for the greatest change. Although

opportunities for GI (by reducing diseconomies of scale) and LR (by having data mining tailor offerings

State of the e-Business Revolution Page 12

to consumers) will no doubt expand (it is unlikely we will see them contract) much of this must be looked

on as a second order effect driven by the ability to engage in a range of transactions with a range of

parties that was heretofore difficult and costly. For example, although e-Bay may allow a bidder in

Lebanon PA to buy a carpet from someone in Tajikistan this does not change the nature of the

relationship—i.e., auctions have existed for millennia—it just makes the range of transactional

possibilities greater by removing the need for the bidder to be on site. The fact that e-Bay needed to

purchase Butterfield & Butterfield is more telling since for truly valuable items independent verification

is much more important to completing a market than simply being able to decrease the thinness of the

market (i.e., increasing the number of bidders).

Developing a Parsimonious Model of MNE Organizational & Managerial Asset Structure and

Strategic Beliefs

Referring back to Exhibit 4, it is important to understand the structure of the MNE’s strategic positioning

on the three dimensions. The firm’s existing organizational structure its complex combination of assets,

legacy systems, resources and managerial processes and the beliefs of its managers can be both an asset

and a liability depending on how these factors are positioned relative to the pressures operating in the

marketplace. In this sense, DMV is a contingency model, whereby the fit between environmental

pressures and existing structures and preferences play an enormous part in the strategic and tactical

success of the firm. We can think of this in three inter-related ways. First, what is possible given the

existing structure of the firm? Second, what does management think is possible (both today and in the

future)? Third, what is it that is feasible—technically and organizationally—for the firm to achieve?14

This structure is useful in understanding the pressures in an e-business world. The existing

organizational structure is valuable when it complements e-business initiatives in ways that enable the

firm to create and deliver new customer value propositions. Dell Computer’s ability to leverage existing

catalogue sales competences and go direct to customers with a customized, price-competitive product

provides an excellent example. Dell was able to use these capabilities even in markets (e.g., Europe and

Asia) where catalogue sales were limited. Part of this success was due to the complementary nature of

State of the e-Business Revolution Page 13

the firm’s existing structure, what its management thought were the strategic possibilities, and their ability

to technically move the firm in that direction. On the other hand, existing competence can also be

destroyed or work against the ability of the firm to accommodate the new pressures it is facing. Novell’s

adherence to the proprietary IPX-based networking standards, a strategy it only recently abandoned in

favor of the open Internet protocol, represented a set of circumstances where managerial beliefs

constrained the company’s ability to move to a scientifically feasible and more market amenable strategy

(Economist 1998).

The Importance of Technical Feasibility. The resource-based theory of the firm puts emphasis on

the role that path dependence and causal ambiguity play in creating organizational stickiness. Technical

feasibility represents the space of strategic and tactical options available to the MNE at any point in time.

For MNEs with existing operations, this structure defines its ability to develop a coherent and consistent

e-business strategy worldwide. For instance, integrating processes to ensure accuracy and currency of

information and standardizing data fields to transfer information between newly constructed interfaces

and legacy systems represent significant changes. However, this is the easiest part of the e-business

transition. When we consider that e-business is as much about organizational, political and relationship

change as it is about technology, then the scope of change management task takes on a whole new

dimension. It is little wonder that the scale of the change daunts most MNEs because their sheer size and

spread implies that implementation of any e-business strategy must necessarily be more difficult than for

local firms or startups.

When we examined the difference between European e-business and US e-business, it is apparent

that one reason European firms are having such difficulty is their inability to deal with feasibility issues.

European firms face high organizational switchover costs that undermine and constrain their e-business

initiatives. Some of this is environmental—e.g., the European Union’s data privacy directive—but much

of it is due to the natural structures that have evolved to create more consensus-driven management

structures in Europe. In other words, European firms are constrained by the fact that they cannot expand

their ‘feasible set’ of strategic options as quickly as their American rivals.

State of the e-Business Revolution Page 14

For any specific e-business strategy to fall into the MNE’s feasible set it must fit with the

constraints of the broader environment, the firm’s existing structure and the transactional characteristics

of exchange that are possible. In other words, the business orientation must be achievable and the MNE

must be able to ‘get’ to its new strategic position from its existing point of operation. For most firms, the

‘best’ option is rarely available to them simply because they cannot organizationally move from where

they are to where they want to be. Hence, as Carson et al. (1999) note, firms end up accepting remedially

efficient15 second or third best options simply because the organizational slate cannot be completely

wiped clean. In other words, the switchover costs are simply too great.

Remedial efficiency limits MNEs to three e-business strategy options: (1) develop a new MNE

company with independent e-business capabilities worldwide; (2) alter the MNE’s existing worldwide

strategy and base it on an e-business platform; or (3) base the worldwide e-business platform on the

MNE’s existing worldwide strategy and structure. All three options are simple (but enormous) trade-offs

between: (a) the value of existing assets and structures relative to the new e-business assets and structures

and (b) the costs of switching over to a new structure. The latter is clearly the more complex and critical

issue because it entails trading off the cost of building a new structure versus the capitalization or

destruction of existing assets. Option (1) may have high asset value but enormous costs associated with

building brand awareness. Option (2) may have high asset value because of existing brands and

relationships but massive switchover costs as existing structures are abandoned. Option (3) has lower

switchover costs but potentially lower long run asset value should the pressure for change in the market

be great.

Managerial Beliefs. Every firm has a belief system that is shared by senior managers. Within the

context of the DMV model, the managerial belief system comprises an understanding about what the firm

is capable of doing organizationally, what is ‘best’ for the firm’s future, and what would succeed in the

market (i.e., what are the relevant pressures). More technically put, managerial beliefs are the preferences

that managers have, over the three dimensions (GI, LR, and TC), about the appropriate direction to go and

the relative trade-off between the three dimensions; e.g., what does it cost me, in terms of local

State of the e-Business Revolution Page 15

responsiveness to be more globally integrated? It is a reflection of the relative cost of various strategic

choices about the degree of GI, LR or TC. Murtha, Lenway and Bagozzi (1998) show that a range of

managerial beliefs about the appropriateness of different MNE strategic orientations exist, even within the

same firm. DMV emphasize the matching between what is technically feasible for a firm and what

manager’s believe is appropriate.

On the traditional dimensions of GI and LR there is no specific managerial orientation that can be

said to dominate any other but it is unlikely that e-business initiatives will generate large benefits for

firms shunning additional economies of scale or local responsiveness. However, if web based business

systems create a world more amenable to constant returns to scale it is conceivable that an orientation

toward TC and LR will dominate. But the most obvious, and for us the most important, belief relates to

transactional completeness and whether managers think the quality and reliability of the exchange is

enhanced through e-business. It might seem as if TC could go in only one direction but this, too, is not

clear. For example, universities have been reluctant to embrace online delivery of course material even

though they deal largely with information exchange. Academics believe that electronic delivery of course

material removes a key facet of the value chain, the interactive face-to-face exchange with students. A

move to complete distance delivery is believed to have such strong adverse selection characteristics—i.e.,

only the ‘lower’ quality price sensitive producers would do it that way. Similarly, in places with strong

privacy concerns, such as Europe or Australia, the benefits of more complete contracting arrangements

may be stifled and political pressures could lead to markets that are even less transactionally complete

than before the advent of web technology.

What is quite clear today is that the plethora of inconsistent managerial beliefs regarding what

works and doesn’t work is fragmenting the strategies being seen in the market creating conflicts between

what is feasible for a MNE to achieve and what managers think they can achieve. But what this

discussion should highlight is that there is a natural conflict between the pressures for change and the

forces of the status quo. An interesting area of study would be to ask where the pressures for change are

State of the e-Business Revolution Page 16

originating. To what degree are they coming from managerial beliefs pulling firm to a new technically

feasible set or are they coming from the base environmental and technological pressures?

The Expansion of Market Opportunities and MNEs’ Choice of New Strategic Orientations

Two of the important insights from DMV are that: (1) the potential ‘space’ available in the market is

limited to the maximal set of technically feasible options open to the firms (called the feasible frontier),

and (2) that there is no a priori dominant position open to firms along this frontier. Taking this to the e-

business realm it implies: (1) that the space available to MNEs can only be expanded if the feasible

options available to actual or potential firms allow it, and (2) there is no a priori dominant outcome to be

expected. Hence, the way Barnes & Noble reacted to the swift entrance of Amazon.com into the online

bookselling business, or the way E*trade, Ameritrade and My Discount Broker are competing against the

major conventional stock brokerage firms can be explained by the obvious lack of dominance of any one

strategy in a world where the frontier of options has expanded.

At a more structural or value chain level there is also evidence that the differential impact that

open systems technology is having on MNE’s value networks is leading to simultaneous

disintermediation and reintermediation, sometimes in very interesting ways. Hence, firms operating as

cooperators rather than competitors are able to capitalize on market expanding opportunities that benefit

all firms (perhaps not necessarily proportionately). AutoXchange, involving Ford, General Motors and

Daimler-Chrysler and the online retail consortium NetXchange, involving America’s Sears Roebuck and

France’s Carrefour are two illustrations of such systems.

Three overlapping questions are relevant to this discussion (and for which there are yet to be clear

answers). First, have strategic holes that were unavailable to existing and potential players in the market

been opened up? For example, are options for GI previously unavailable now open to exploitation?

Second, has there been a differential expansion of the feasible frontier of strategic options in any one

direction; i.e., towards GI, LR or TC? In other words, if the feasible set of options has been expanded has

this disproportionately occurred on one dimension, such as greater TC? Third, has this expansion

State of the e-Business Revolution Page 17

occurred in areas where existing MNEs are operating or where potential competitors can now operate in

parallel with established players?

In a very real sense, these questions are the most interesting since they are the most visible and

relate most directly to MNE performance. Hence, firms like E-Bay have arisen as nascent MNEs by

filling in a previously unoccupied space newly created by the expansion of the feasible frontier into

higher levels of TC and GI. Auctions have always been relatively ‘complete’ in the sense that buyers and

sellers only bought and sold items through auctions when quality verification and payment were clear

(e.g., in the case of commodities). What web based systems did is expand their scope to a wider market

clientele. Chemdex has done a similar thing but also added on-line consulting that has simultaneously

allowed it to tailor the delivery of its services to specific customers, thereby reacting to expansions of the

frontier in both the realm of TC and LR. What should be clear is that the most critical factor in this

discussion is the ‘completeness’ of the institutions permitting contracting between the organizations and

their stakeholders—owners, suppliers, employees, consumers and society. The real areas of change are

those areas where ‘old’ institutions—hierarchies within firms, established supplier relations, EDI systems,

etc.—can be co-opted by technology in ways that transform, not the business, but the psychology of the

business and the fundamental core of what defines the business.

CASE STUDIES

The previous discussion has shown how we can integrate e-business developments into existing models of

MNEs. This does not simply validate the theory but also provides a normative mode of understanding that

helps to demystify what is at times a confusing and daunting phenomenon. In the examples that follow we

illustrate how we can use the DMV approach to understand a number of very specific cases. The first two

case sets use the banking and technology industries both sectors that are particularly amenable to e-

business as illustrations of how environmental pressures and constraints restrict the adoption rate of e-

business. The third case group investigates music retailing as an instance of how LR pressures influence

the heterogeneity of firm structures and perpetuates fragmentation. The fourth case series examines the

State of the e-Business Revolution Page 18

business-to-business sector to show the differential impact e-business has on the industry value chains.

Following these examples, we re-review the framework to address the all important and practical problem

of designing appropriate institutional structures to effectively support e-business.

ANZ–Grindlay’s and Wingspan—Native e-Business versus Existing Structures

Traditional bricks and mortar banks like ANZ—Grindlay’s16 develop, package and sell financial products

through proprietary distribution channels (i.e., local branch offices). Regulatory pressures and customer

relationship demands create strong incentives for local responsiveness over most components of the value

chain. A central concern in the industry has always been the high costs of distribution and technology-

oriented strategies have been used extensively used in the industry to reduce costs.17 The main mode of

competition was scale, market coverage and breadth of product and service offerings. Hence, banks ran

their operations very much in a multidomestic fashion with strong internalization of functions (low levels

of TC). The arrival of virtual banks like Wingspan.com and Security First represented the first foray into

banking by completely contractual players where e-tail delivery was backed up with contracted services

(rather than ownership).

ANZ response has been to avoid commodity status and the bank has come down firmly on the side

of complementing its traditional operations with an integrated e-business capability, particularly in trading

with its alliance with E*trade. E-business provides both an opportunity to reduce costs and add value,

enabling customers to review transaction details, transfer funds and pay bills in a secure manner over the

Internet. Such approaches are still incremental rather than revolutionary and repleat with problems of

remedial efficiency—i.e., ANZ simply cannot change its systems and reduce its infrastructure costs

quickly enough. The level of transactional completeness remains relatively low, local responsiveness is

still important and control through vertical value chain integration is still the dominant paradigm.

Wingspan on the other hand reflects a trend to a more globally integrated, commodity-based

approach. The site offers a dizzying array of financial products and services and has adopted a strategy

that seeks to expose more of the value chain to market competition. Financial products are sourced via

contractual arrangements with Bank One (Wingspan’s parent company) and vendor partners.

State of the e-Business Revolution Page 19

There are several observations we can make about these examples. First, despite developments in

the US, total virtual banking has not had an impact in the global banking industry. This is partly a result

of government regulation, customer insecurity with globally operated banks and the fact that local banks

have been quick to offer an adequate online capability. Second, the example illustrates the difficulty in

attempting to revolutionize the banking sector; an industry built on strong history and entrenched

managerial beliefs. Bank One recently fired Wingspan’s chief advocate, CEO Dick Vague, and according

to industry analysts, the firm will be either integrated back into Bank One as a ‘clicks and mortar’ strategy

(Computerworld 1999) or sold off to a third party.18 Lastly, it is apparent that significant changes in the

way banking is conducted will be dependent upon steady erosion rather than a revolutionary event. It is

likely that partial substitutes like Intuit’s Quicken or Microsoft Money will continue to pressure

incumbents, who will move into alliances with partners offering disintermediated components of the

financial services value constellation.

Bank One’s inability to embrace and exploit the Wingspan.com business model can be explained

by the realization that: (a) Wingspan represented a competence destroying change that did not allow it to

broadly exploit the skills, competences and knowledge embedded in its traditional routines and

procedures; and, (b) as an incumbent it managers may have been less than enthusiastic to embrace

technological changes that threatened to render their existing products non-competitive—and thereby

cannibalize their existing market position (Afuah 2000). Hence after an initial foray into the strategy of

building a separate e-business firm with its own strategy, Bank One has reverted to an incremental model

more in line with that taken by ANZ.

Since there is little reason to believe that customers enjoy banking, the organisational stickiness

Bank One attempted to break and ANZ has accommodated does not necessarily bode well for financial

services over the long term if the technological issues can be resolved. As banks and other financial

service providers continue to place more services online and new competitor types enter the market space,

we will see growing pressures for banks to become more transactionally complete as more of their

services become pure commodities. Relationship management will become more difficult and the branch

State of the e-Business Revolution Page 20

as the traditional image of the bank will continue to be replaced by new value propositions such as virtual

alliances.

Cisco and Compaq—Managing the Channel of Distribution

With firm growth rates among the fastest in the world the information technology (IT) sector provides a

number of interesting examples of e-business in action. Rapid technological change and short product life

cycles combine to create strong forces for global integration in this industry. Yet Cisco and Compaq

provide contrasting examples of the difficulties associated with channel switchover costs in e-business.

For Cisco, e-business was a natural evolution. Its core product the router does not have a

floppy disk drive, so downloading software updates over the Internet to an IT literate customer base

provided an obvious benefit. According to Arago-Stemel, a Cisco IT manager, the company ‘lucked out’

when it first embarked on e-business in 1994 since they didn’t have any real plan (Clark 1997). However

a closer analysis reveals a number of important characteristics that were easily enhanced through e-

business. Firstly, as an industry leader Cisco’s routing operating protocols (RIP) emerged as the industry

standard providing strong contractual bonds and hence high levels of TC but with a potential threat of

high switching cost to the customer (who may become captive to Cisco’s standard). Secondly, the

company’s philosophy is that it will partner with virtually any company and is quite prepared to contract

out non-value added competencies (Time 2000). The relationship Cisco has with FedEx illustrates the

point. Cisco chose to outsource the distribution component of the value chain, depending on FedEx for

delivery of all ordered products to customers. The opportunity for joint gain in this arrangement is

enhanced through a FedEx developed embedded extranet architecture. When a customer queries the

delivery status of a router on Cisco’s web page, the query is sent to a FedEx database, the FedEx server

then transparently returns a status report for the customer. Thus the ability to outsource and hence focus

on high value added competences were central to Cisco’s success.

Compaq on the other hand illustrates the difficulty of entering into a direct-sales strategy that

involves value chain disintermediation. In an attempt to imitate the success of Dell, the company is

State of the e-Business Revolution Page 21

struggling with switchover feasibility and remedial efficiency issues (Carson et al. 1999). The strategic

logic was straightforward enough, eliminate reseller margins and utilize the savings to go direct to

customers with a customizable, price competitive product. Unfortunately, the reality was not as simple. In

Compaq’s case, its success has been determined largely by its long-standing, close channel relationship

with resellers. Not surprisingly when these resellers learned of Compaq’s decision to sell direct to the

customer, they let their displeasure be known. Compaq Australia has been on the receiving end of this

displeasure, when all Compaq products were tossed out of the country’s leading retail outlets. The cost to

Compaq Australia of the debacle is estimated at $60 million in lost revenue (The Australian 1999). The

Compaq story is one that other firms are loath to repeat.

The reason Compaq is struggling with disintermediation, has nothing to do with whether or not

profits are possible. Rather it has everything to do with deciding how to move into a new distribution

channel without jeopardizing existing channel relationships. As noted by Carson et al. (1999), just

because something is feasible and preferable is a necessary, not sufficient, condition for its adoption.

Institutional structures, such as intermediaries, satisfy the complex requirements of customers and

suppliers that cannot be unraveled overnight. Sanchez and Mahoney (1996) note that there is a complex

and not necessarily clear relationship between technical capability and organizational design. Cisco has

been able to use a modular design approach to coordinate processes without the need to exercise

coordination continually (hence, it has high TC). Compaq tried to mimic this logic but found that its

existing value chain structure was not willing or capable of accommodating the change simply because it

was not in its interests to do so.

Chaosmusic.com versus Sanity.com and MP3—Local Responsiveness with Electronic Delivery

The music industry and its associated distribution channels are changing at a rapid pace. Perhaps some of

the most interesting in terms of what is happening with the onset of direct digital distribution of music

(through the internet) and traditional distribution in physical media (i.e., CDs, DVD). Amazon created its

business through the distribution of physical goods (i.e., books and CDs), using the technology as a

logistics tool. However with the establishment of a network by which the product is sold ‘informationally’,

State of the e-Business Revolution Page 22

a new set of players has emerged that deal not only in the informational selling space, but also transmit the

product ‘online’ to the customer. These businesses are built purely on network principles and represent a

new category of firm. The advent of Napster and Gnutella technologies implies that, in some ways, we

cannot class these operations as a physical industry since they are widely dispersed. For example, the

ability to share music and video from point to point rather than through a single server completely muddies

the distinction between seller and buyer. For firms in this industry, particularly at the retail interface, face

real questions as to whether a ‘clicks and mortar’ model is viable or whether a more technologically open

and flexible pure Internet play is the better option. This was made quite salient in AOL’s decision to pull

the plug on its own “unauthorised freelance project”—i.e., the Gnutella development group—because of

its potential for undermining the operations of Time Warner (CNN 2000b).

The music business is an example of a disintermediated value chain with variable strategic

orientations depending on the firm’s position on the value chain. Artists are both local and global, as are

record companies. Retailing operations have major chains, such as Virgin and HMV, and local

operations, such as Borders (in the USA), Sanity (in Australia) and WOM (in Germany). The tension is

increased by the development of native Internet players all along the music (or media) value chain. Two

recently listed Australian players at the retail end of the game, Sanity.com and Chaosmusic, can

demonstrate this.

Sanity.com is a hybrid clicks and mortar operation in the mode of companies like

Barnes&Noble.com. Its beginning is in pure retail operations and it has grown to over 200 stores

countrywide. Sanity.com sources its music and content through third party suppliers such as Global New

Media and Global Fulfilment and maintains a strategic portal relationship with EMI (EMI holds a 10 per

cent share in the company). The portal arrangement allows Sanity.com to source content (both textual

and audio visual) for use on its own web site as well as gaining access to EMI catalogues for the sale of

EMI produced music through the site. Chaosmusic.com is a pure Internet play with no pre-established

operations. Chaos obtains its content through its relationship with a network of online partners including

genre specialist sites as well as portal and media websites. It acquires its physical product through both

State of the e-Business Revolution Page 23

local and overseas suppliers, including Valley Media Inc. (US). A key component to Chaosmusic’s

strategy is to supply the infrastructure to allow artists to upload and sell their music through the web using

the company’s audio-delivery and e-business systems. This infrastructure includes Liquid Audio and

MP3 capabilities as well as website development that allows local musicians to maintain sites, get their

music reviewed, broadcasted and sold, and have their gigs listed on Chaosmusic’s event calender.

Both Sanity.com and Chaosmusic focus on high levels of local responsiveness, although at

different ends of the value chain. Sanity’s local responsiveness is based on its ability to provide customer

service through its bricks and mortar stores and to use that as a primary source of its customer

intelligence. Chaosmusic’s local responsiveness is concentrated down at the content end, with more

weight put on pushing local content and building its brand as an ‘alternative’ music environment.

South Fresh & Sydney Fish Market—Alternative B2B Models in Traditional Business

Very few people would associate the long-established craft of fishmongering with electronic business, but

seafood wholesalers in New Zealand (South Fresh Limited) and Australia (Sydney Fish Market) offer a

different perspective and represent the sort of radical change in traditional markets also represented by

Chemdex. These traditional firms provide important insights into how e-business is being used to add

value and support transactions between businesses.

As an intermediary located between the fish processor (or fisherman) and the buyer (supermarket

chains), South Fresh’s value proposition is based on a proven ability to move high quality perishable

goods (i.e., fish) cheaper and faster than the competition. Distribution logistics are critical and demand

that the firm be flexible and locally responsive. Transaction costs are high to ensure operational standards

and procedures are followed and quality is maintained. In this sense e-business provides a natural adjunct

to the business operations by reducing invoice exchanges, supporting online settlement and providing a

level of rigorous management throughout the transaction. Since the company already has an EDI network

in place this change is reflective of continual improvement rather than radical change.

The most significant insight we gain from this case however relates to the level of TC. Put

simply, fish quality is a function of time and temperature the higher the temperature the less time one

State of the e-Business Revolution Page 24

has before it deteriorates (and smells). It is often difficult to know whether you are getting a quality

product or not, and the truth is often stretched when discussing the product’s full history. Since most

people can’t determine the reliability of the product, low levels of TC characterize the fish industry. In

such an industry a highly respected and trusted fishmonger plays an important role. According to Toby

Warren, CEO of South Fresh, in this industry “relationships are the key and business will always be done

on the basis of relationships, through people they know and trust.”

Although it is unlikely that e-business will change this aspect of the fish industry, South Fresh

operates using a model that uses technology as a complement to local responsiveness. South Fresh’s

system allow fishermen to know which purchasers are demanding which fish at what time. Hence, they

can send their boats out on any given day with specific targets to meet. For example, if John Dory is being

demanded then they can focus their efforts on the John Dory stock. Using a system that allows fishermen

to ‘reserve’ demand, they can be assured that either all or some portion their catch is sold to specific

buyers and the buyers can be assured that their demand will be met in a timely fashion. While both

systems are still embryonic, the more exciting aspect of this case relates to the new ways in which

information can be used further upstream in the value chain. E-business developments do more than

improve the order and procurement process, they also provide suppliers with an ability to match

production with demand. The South Fresh web site provides dynamic information updated every thirty

seconds on current inventory levels and reserve order quantities. Any catch over that reserved ahead of

time can either be sold for a fixed price using the order book system or put up for auction. South Fresh’s

operations increase TC by reducing wastage and stabilizing price and quantity. It increases LR by

guaranteeing that demand is met when it needs to be met.

In the case of the Sydney Fish market (SFM; the largest fish market in the Southern Hemisphere),

recent government deregulation initiatives have created strong pressure to find new ways to add value to

the fishmongering proposition. The threat of market erosion is real and increasing numbers of suppliers

(particularly in the growing aquaculture sector) are selling direct to buyers. Unlike South Fresh, the SFM

State of the e-Business Revolution Page 25

chose to address this problem using a more traditional means of creating a market clearing mechanism.

They embarked on a two-pronged approach. For existing fishing fleets, an on-line Dutch (or declining

price) auction operates. However, to capture the aquaculture market (which is more likely to go direct to

customers) an e-catalogue business model is used (with posted prices). For all suppliers often located

in remote geographical areas the ability of the SFM to provide a reliable market and price is an

attractive proposition. For the buyer, a centralized trading hub offers advantages by bringing together a

large range of fishing fleets and specialty aquaculture supply. The e-catalogue allows aquaculture

producers to decide when they harvest their stock, leaving them with no price risk. The Dutch auction

reduces the quantity risk of fishermen but leaves them with price risk. The aim of the SFM system is to

increase TC by reducing the thinness of the market for large breeds of fish.

Although both firms would like to source and distribute on an international scale, the main

challenge to the fishmonger is the fact that they are currently restricted to local markets because of

distribution economics and relationship problems. Fish produce does not move easily over fiber optic

cable and what increases in transactional completeness that can be achieved are unlikely to create more

than limited opportunities for further global expansion.

Summary—Mapping the Impact of E-Business

A simple way of pulling these case studies together is to examine what the implications are for the

direction of the expansion of the operating space open to firms and how this differs across the value

chain. Exhibit 6 shows our hypotheses as to where the feasible frontier is expanding and how radical

those changes may be. Exhibit 7 presents a summary discussion on the where along the value chain there

are pressures for change.

Exhibits 6 & 7 about here

Exhibit 6 shows that the dominant expansion is in the area of transactional completeness. In all

four cases, web based systems create more complete contracting possibilities either by reducing the role

of intermediaries (music), expanding ordering and placement systems (fishmongering and IT equipment),

State of the e-Business Revolution Page 26

and/or expanding the possibilities of one-to-one product placement (music and banking). In the case of

IT equipment opportunities for greater GI have opened up but this is based heavily on the fact that IT

companies were sourcing components globally before the dominance of web based procurement systems.

But the second strongest effect is in expansion of the ability of MNEs and local firms to increase their

responsiveness to local customer demands.

Exhibit 7 provides a value chain schematic that shows the components of the changes. For

simplicity we have broken the value chain into four generic stages. The most critical changes are

emphasized with thicker lines. In the case of retail banking the main drivers are coming from

downstream marketing pressures allowing for greater tailoring of offerings. Because customers self-

select this allows banks to reduce their overall costs. In the case of the music industry, the main pressure

is in the distribution technology. This is having both upstream effects (through production and the ability

of artists to go direct through their own sites) and downstream effects (through the threat it is creating

with an alternative retail environment). With the IT equipment industry we see logistics as the main

driver, with both material sourcing and outbound logistics driving production and selling. A similar

phenomenon is occurring with fishmongering. Procurement systems create an environment where

wastage is reduced through better ordering and just-in-time harvesting.

CONCLUSION

Our discussion and examples show how the existing models of strategy and structure can be used to

understand the impact of e-business on the structure of MNE and local firms. As noted earlier, it is

important to recognize that the opportunities and threats open systems and web technology pose vary

considerably from market to market and firm to firm. This is because the relevant level of analysis is the

component(s) of the value chain (or network) and the transactions (either internally or externally) that are

affected by the new technologies. Hence, simple prescriptions and predictions will tend to fail because,

even if the changes in the fundamental pressures are the same for all firms in an industry, what is

technically feasible for any one firm and the beliefs that managers hold about what is happening will vary

State of the e-Business Revolution Page 27

considerably. Without understanding this, understanding the impact of e-business development will be

impossible.

Because of the predominance of the net in opening up transactional possibilities we have stressed

the notion of transactional completeness and hopefully shown that the standard integration-responsiveness

framework is unable to accommodate e-business development mainly because it fails to account for this

critical component of strategy and structure. In addition, DMV and Carson et al. (1999), the basis of our

dialogue, place special significance on the fact that managerial beliefs and technical (or organizational)

feasibility seriously limit the nature and speed of any actual change a MNE can make in a limited period

of time. In developing e-business ‘compliant’ organizational structures MNEs must take into account the

fact that they must, to some degree or another, destroy, change and build institutional arrangements that

allow their strategies to be fulfilled. This requires not only that there is profit to be earned (in more

technical terms that the change is remedially efficient) but that it is also possible for the MNE to do it (in

more technical terms that the switchover from one structure to another is feasible). In the latter case, the

MNE needs to consider both the cost of switching into the new structure and the cost of switching out of

the old. Both Bank One/Wingspan and Compaq failed to understand this because their manager’s felt that

bold strategies were necessary. The opposite was true in the case of ANZ and Sanity.com who chose to

stay close to their existing structures. Companies such as Cisco, Chaosmusic and South Fresh had no

existing structures so were able to align their strategy and structure to the emerging pressures.

Perhaps this point is self-evident, but start-ups have the freedom to choose from a broader palette

of strategic options than existing firms. This does not mean that all start-ups will choose wisely or indeed

that those who choose wisely will necessarily succeed (given that choice of strategy and structure is only

part of the competitive advantage equation) but they are less constrained. Existing firms must pay more

attention to how they migrate from one form to another. In particular, we have suggested that for existing

MNEs most of the new forms will be evolutionary hybrids rather than revolutionized organizations. And

in working out how to migrate to these hybrid forms we have also suggested that managers pay particular

State of the e-Business Revolution Page 28

attention to their institutional arrangements. For it is along this dimension that there is greatest

opportunity for enhancing efficiency and minimizing the dangers of switchover from one form to another.

State of the e-Business Revolution Page 29

Endnotes

1Berkshire Hathaway and Procter and Gamble are two recent examples of this phenomenon. The poor performance of Berkshire Hathaway—its earnings down 40 per cent and its stock down 20 per cent in 1999—is attributed to its focus on ‘old economy’ stocks (Khalfani 2000). Procter and Gamble hit almost 50 per cent of its yearly high in mid-March 2000 based on poor profit performance driven by analyst’s beliefs about a defunct ‘old’ business model (Schlesinger 2000). 2 We define e-business as any business that is conducted, in whole or in part, through a digital infrastructure. 3 It is clear that this number is a moving target. 4 There is every indication that similar effects are driving the near term fortunes of other e-commerce retailers. See, Streitfeld (2000). 5 B2C = business-to-consumer; B2B business-to-business

6 For example, Dell’s online strategy worked because existing catalogue based competencies quick response, low-cost fulfillment system characterised by direct customer interactions and made-to-order manufacturing were naturally compatible with an e-business model. 7 For example, the opportunity to achieve significant savings in the procurement of parts, has been the driving force behind the announcement by Ford, General Motors and Daimler Chrysler to join forces to create the world’s largest virtual market known as ‘autoXchange’ (The Australian, February 25, 2000). 8 For example, in the case of Air Products, there has been a strong commitment to an Internet-based strategy, integrating the company’s suppliers, customers and other stakeholders into their informational framework. 9 For example, for Chemdex e-business goes much deeper than ordering books from Amazon or PCs from Dell. Corporate customers require relationships and Chemdex consultants provide on-site assistance to assist firms map their existing systems into Chemdex software—seeing the company grow from 3 suppliers in January 1998 to 335 suppliers and more than a million products (Economist 1999). 10 Political pressures operate over all the dimensions. Hence something like tariffs may be considered both a GI and an LR pressure. Venaik, Midgley & Devinney (2000) discuss why this is logical and how it might be accommodated empirically. 11 Cost reduction, multinational customers, multinational competitors, investment intensity, technological intensity and universal access to raw materials and energy 12 Differences in customer needs, distribution channels, availability of substitutes and adaptation to market structure and host governmental demands 13 It is also interesting to speculate what the reaction to this trend will be like. For example, if large established players like Tengelmann can build their own competence it is likely they will dominate this end of the business too. However, if the change is competence destroying the only possible reaction by establish retailers is to push for extended shop hours to reduce the desire to shop on-line. In this case the impact to a society like Germany could be quite large. 14 In this context we use ‘technically feasible’ broadly. It is meant to represent the firms tangible and intangible assets and includes property, products, information technology, reward systems, financial control systems and production processes. However, it does not include the beliefs and strategic orientation of the management. 15 Remedial efficiency refers to the fact that an option chosen may not be Pareto optimal but is efficient conditional on the path dependent and other internal or external constraints operating at the time of the choice. 16 ANZ—Grindlay’s operates as ANZ in some locations (Australia, UK, Hong Kong, China, etc.) and ANZ—Grindlay’s in others (mainly South Asia and the Middle East). 17 Report for the Australian Government titled E-Commerce Beyond 2000 (2000), identifies the use of IT as the major force shaping the financial services sector over the past two decades. 18 The reverse phenomenon was the fate of Advanz Bank, Germany’s first Internet bank that ultimately succumbed to Dresdner Bank’s approaches.

State of the e-Business Revolution Page 30

Bibliography

Afuah, A. (2000) “How Much Do Your Co-Opetitors’ Capabilities Matter In The Face Of Technological Change?” Strategic Management Journal, 21, 387–404.

Argyris, C., and D.A. Schon (1978) Organizational Learning. Boston: Addison-Wesley.

The Australian, (1999) “Compaq’s Big Test Begins,” August 24.

Bartlett, C., and S. Ghoshal (1989) Managing Across Borders: The Transnational Solution. Boston: Harvard Business School Press.

Barney, J.B. (1986) “Types of Competition and the Theory of Strategy: Towards an Integrative Framework,” Academy of Management Review, 11, 791–800.

Barwise, P. (1997) “Brands in a Digital World,” Journal of Brand Management, 4 (4), 220–223.

Bitner, M. J. (1995) “Building Service Relationships: It’s All About Promises,” Journal of the Academy of Marketing Science, 23 (4), 246–251.

Booz Allen and Hamilton (1999) Competing in the Digital Age: How the Internet will Transform Global Business. New York: EIU.

Carson, S., Devinney, T., Dowling, G., and G. John (1999) “Understanding Institutional Designs Within Marketing Value Systems,” Journal of Marketing, 63 (Special Issue), 115–130.