r e n e w a b l e e n e r g y i n s p a i n kingston, 23 rd june 2008 world wind energy conference...

TRANSCRIPT

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Framework of reference Framework of reference and Perspectivesand Perspectives

for Wind Energy in Spain for Wind Energy in Spain

Hugo Lucas

IDAE – International Department

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Table of Contents

1. Current Situation of Wind Energy in Spain.

2. Technological Aspects.

3. Main Wind Energy Legislation in Spain.

4. Spanish Renewable Energy Plan (PER)

2005 – 2010. Wind Energy Area.

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Current Situation of Wind Energy in Spain

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

22,245

15,09

5

3,125

2,725

2,455

2,390

2,150

1,745

4,565

TOTAL EU-27

(ENDING 2007)

56,495 MW

Source: EWEA and IDAEProvisional Data

0 2000 4000 6000 8000 10000 12000 14000 16000 18000 20000 22000

REST

NETHERLANDS

PORTUGAL

UK

FRANCE

ITALY

DENMARK

SPAIN

GERMANY

Wind energy capacity (MW) in the European Union (EU-27) - 31/12/2007

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Development of Wind Energy in Spain (MW)

TOTAL SPAIN(ENDING 2007)

15,095 MW

Source: IDAE

Provisional Data

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

12000

13000

14000

15000

16000

ACUMULATEDCAPACITY

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

3200

3400

YEARLY INSTALLEDCAPACITY

IN OPEARATION

ACUMULATED

IN OPERATION 0,4 1,2 0,8 1,5 2,7 0,7 38 6 24 40 96 229 393 642 815 985 1.615 1.344 2.082 1.593 1.811 3.374

ACUMULATED 0,4 1,6 2,4 3,9 6,6 7,3 46 52 75 115 211 440 834 1.476 2.292 3.276 4.891 6.235 8.317 9.910 11.72115.095

86 87 88 89 90 91 92 93 94 95 96 97 98 99 2000 2001 2002 2003 2004 2005 2006 2007

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

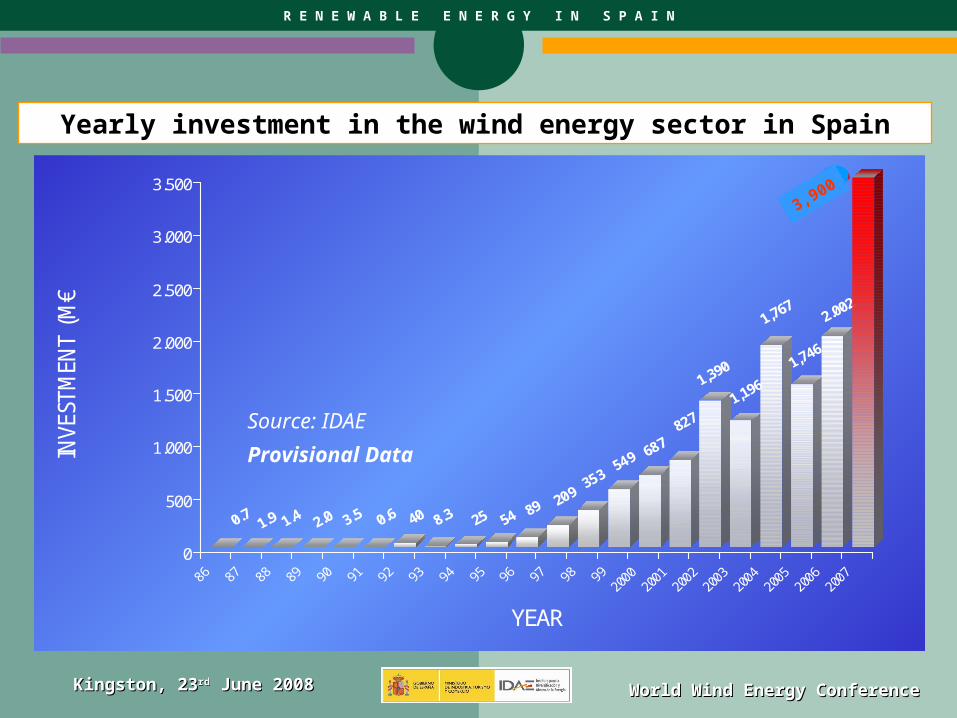

0

500

1.000

1.500

2.000

2.500

3.000

3.500

INVE

STM

ENT

(M€)

YEAR

Yearly investment in the wind energy sector in Spain

Source: IDAE

Provisional Data

3,900

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Average Cost890 EURO/kW inst.

0100200300400500600700800900

100011001200130014001500160017001800

86 87 88 89 90 91 92 93 94 95 96 97 98 99 '00 '01 '02 '03 '04 '05 '06 '07

Year

€ / k

W

Source: IDAE

Average Cost 20071,170 €/kW inst.

Estimated value for 2007

Evolution of cost per kW of installed capacity (in nominal terms)

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Technological Aspects

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

96 % of installed capacity in 2007 were supplied by manufacturers established in Spain:

• Spanish technology (67 %): GAMESA, ECOTECNIA(*), ACCIONA WP

• Foreign technology (29 %): VESTAS, G. ELECTRIC, NORDEX, ENERCON

• Transfer technology (4 %): NAVANTIA-SIEMENS

Average WT power rating 1.560 kW

Average size of wind farm 27 MW

TOTAL: 3,374 MW

(*) ECOTÈCNIA was acquired last year 2007 by the French company ALSTOM.

Technological aspects. Market share by manufacturers in Spain (2007)

VESTAS

18,7%

ACCIONA WP

14,4%

ECOTÈCNIA

6,6%

G. ELECTRIC

6,1%

ENERCON

2,9%NAVANTIA-

SIEMENS

3,5%

GAMESA

45,8%

SIEMENS

0,9%

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

TOTAL: 15,095 MW

Accumulated installed capacity (MW) per technology (31-Dec-2007)

Source: IDAEProvisional Data

GAMESA EÓLICA56,3%

NAVANTIA-SIEMENS3,9%

G. ELECTRIC6,6%

ECOTÈCNIA7,8%

ACCIONA WP8,2%

VESTAS13,9%

ENERCON1,1%

OTROS2,2%

338

163

588

992

1.178

1.239

2.103

8.494

OTROS

ENERCON

NAVANTIA-SIEMENS

G. ELECTRIC

ECOTÈCNIA

ACCIONA WP

VESTAS

GAMESA EÓLICA

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

22.8 %

16.6 %15.4 %

14.0 %

10.5 %

7.1 %

4.4 %4.2 % 3.4 % 3.4 %

10.5 %

0

5

10

15

20

25

Source: BTM Consult – March 2008

Worldwide market share in 2007

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Wind turbines manufacturers (Spain)

ManufacturerManufacturer

Accumulated Accumulated capacity in capacity in

Spain, ending Spain, ending 20062006

Commercial Wind Commercial Wind

TurbinesTurbines

Plants in SpainPlants in Spain

(wind turbines assembly)(wind turbines assembly)

GAMESA EÓLICA6,947 MW (59.2%)

G 80-83-87-90 /2000G 52-58 /850

G 128 /4.5 (2008)

6 (Navarra -2-, Soria, La Coruña, Zaragoza,

Valladolid)

ECOTÉCNIA 957 MW (8.2%)Ecot. 74-80 /1670

Ecot. 100 /3000 (2008) 2 (La Coruña, Navarra)

ACCIONA WP 730 MW (6.2%)AW 70-77-82 /1500

AW 1xx /3000 (2009)2 (Navarra, Castellón)

M TORRES 25 MW (0.2%)TWT 72-77-82 /1650TWT 92 /2.5 (2009)

1 (Soria)

NAVANTIA - SIEMENS

469 MW (4.0%) Navantia-Siemens 1.3 1 (La Coruña)

EOZEN - VENSYS 0Eozen-Vensys 70-77

/15001 (Granada)

VESTAS1,470 MW (12.5%)

V 90 /3000V 80-90 /2000

V 120 /4.52 (Lugo, León)

G. ELECTRIC 785 MW (6.7%)GEWE 1.5 sl

GEWE 2.5 (2009)1 (Toledo)

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Existence of significant wind resources.

Stable regulatory framework for electricity generated

(Feed-in tariffs system; reasonable return on investment).

Regional support: planning, simple administrative procedures.

Technological maturity. Creation of a strong industrial sector.

Large scale production brings costs reduction (construction, operation and maintenance).

Key elements for wind energy success in Spain

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Main Wind Energy Legislation

in Spain

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

FRAMEWORK OF REFERENCE IN THE EUROPEAN UNION (EU-27)

“Renewable Energy in Europe Road Map” -COM(2006) 848 final- RES: 20 % of primary energy consumption. [Proposal for a Directive “on the promotion of the use of energy from renewable sources”. Brussels, 23.01.2008 –COM(2008) 19 final-]

“WHITE PAPER” (December 1997): Contribution from Renewable Energy Sources of 12 % relative to primary energy consumption.

Directive 2001/77/EC: Contribution of 21 % relative to the annual electricity consumption. (Spain: 29.4 %)

RES – Overall target by 2010

New targets by 2020

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Main legislation at national level

- Spanish Electric Power Act 54/1997 (dated November 27th).

- Royal Decree 661/2007, on Special Regime.

(Order ITC/3860/2007, electricity tariffs year 2008)

Regional level- Administrative Procedures.

REGULATORY FRAMEWORK OF REFERENCE IN SPAIN

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

LEARNING BY DOING

RD 2366/1994 Feed-In Tariff

RD 2818/1998 Feed-In Tariff

RD 436/2004 Feed-In Tariff Premium

RD 661/2007 Feed-In Tariff Premium

Small capacity facilities.

Revision of the tariffs and technologies.

Increase maximum capacity.

Revision of the tariffs and technologies.

Windfall profits in the market option. Insufficient development of biomass and cogeneration.

Cap & Floor.

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

RD 661/2007. MOTIVATIONS

The modification of the economic and legal framework regulating the special scheme in force so far (RD 436/2004) became necessary for several reasons:

The growth undergone by the special scheme in the last years has pointed to the need to regulate some technical aspects to contribute to the increase of these technologies, safeguarding the system’s security and guaranteeing its supply quality, as well as the restrictions to the production.

The economic scheme established in the Royal Decree 436/2004 of 12thMarch, because of the behaviour undergone by the market priceswhere some variables not considered earlier have become moreremarkable, made necessary to modify the payment system.

New targets for installed capacity are established incompliance with the objectives in the Renewable Energies Plan 2005-2010 and the Energy Saving and Efficiency Strategy for Spain” (E4), towhich the retribution scheme set out in this Royal Decree shall apply.

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

RD 661/2007. SCOPE OF APPLICATION

Category a): Producers using cogeneration or other ways of electricity production from waste energy.

Category b):Installations using any of the non-consumable renewable energies, biomass or any kind of biofuel as primary energy, whenever their titleholder does not carry out production activities under the ordinary scheme.

Category c):Power plants that use waste with energy recovery not stated in category b) as primary energy.

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

RD 661/2007. MAIN CHARACTERISTICS

Objective: - Legal and economic scheme for the Special

Regime.- Consolidate the regulatory framework, giving

stability and predictability to the system.

Characteristics: - Feed-in tariff system.- Guaranteed along the life-time of RES

installations.- Adapted to the development of each renewable

area.

Methodology: - Two alternative options for the remuneration of

kWh:

1. Regulated price: Independent of capacity and year of

commissioning.

2. Open sale in the market:‘Pool’ price + Premium +

Complements. Upper and lower limits for the sum

(‘pool’+premium)

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

RD 661/2007. MARKET OPTION

When producers decide to participate in the market, the obtained premium will vary according to the market price (‘pool’) set up on an hourly basis.

Premium + ‘Pool’

Premium

‘Pool’

73,66

Top limit

Premium of reference

Bottom limit(€/MWh)

87,79

(€/MWh)43,39

30,27

57,52 87,79

2008

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

RD 661/2007. OTHER ASPECTS

Other relevant aspects:

Wind farms are obliged to remain connected to the network in case of sudden voltage drop, contributing in this way to its stability.

Installations have to present a financial guarantee to be allowed to connect to the grid (20 €/kW).

Costs of deviation: The real cost of deviation will be passed on also to the installations with regulated tariff.

In 2008, a new Renewable Energies Plan for the period 2011-2020 will be drawn up.

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

UPDATING AND REVISION OF TARIFFS, PREMIUMS

AND SUPPLEMENTS The amounts of tariffs, premiums, supplements and cap & floor limits will be annually updated having the consumer price index (CPI) as a reference minus 0.25 until the 31st of December 2012 and minus 0.5 since then.

During 2010, in view of the result of the follow-up reports on the extent of fulfilment of the Renewable Energies Plan (PER) 2005-2010, the review of tariffs, premiums, supplements and cap & floor limits will take place, bearing in mind the costs associated with each of these technologies, the extent of participation in the special scheme in the meeting of the demand and its effect on the technical and economical system, always guaranteeing reasonable profitability rates with reference to the price of money on the capital market.

Every four years and from then on, a new revision will be done maintaining the above criteria.

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Spanish Renewable Energy Plan (PER 2005 – 2010).

Wind Energy Area

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

• Approved by the Council of Ministers on 26th of August

2005.

• Targets of PER 2005-2010. In 2010, RES will represent:

– 12.1% of total energy consumption,

– 30.3% of electricity production,

In addition, biofuels will represent 5.83% of diesel and petrol consumption in the transport sector.

• Estimated investment for this period: 23,598.64 M€.

• In general, individual targets for each technology have

been increased.

• Decisive role of wind energy.

THE RENEWABLE ENERGY PLAN (PER) 2005-2010

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Capacity (MW)

Production (GWh)

Producción (ktep)

Capacity (MW)

Production (GWh)

Production (ktep)

Hidro-electric (> 50 MW) 13.521 25.014 1.979 13.521 25.014 1.979 Hidro-electric (10 MWto 50 MW) 2.897 5.794 498 3.257 6.480 557 Hidro-electric (< 10 MW) 1.749 5.421 466 2.199 6.692 575 Biomass 344 2.193 680 2.039 14.015 5.138 biomass power plants 344 2.193 680 1.317 8.980 3.586

co-firing in coal plants 0 0 0 722 5.036 1.552

Municipal solid waste 189 1.223 395 189 1.223 395 Wind power 8.155 19.571 1.683 20.155 45.511 3.914 Solar photovoltaic 37 56 5 400 609 52 Biogas 141 825 267 235 1.417 455

Solar thermoelectric _ _ _ 500 1.298 509TOTAL ELECTRICITY GENERATION 27.033 60.097 5.973 42.495 102.259 13.574

Biomass 3.487 4.070

Low temperature solar thermal 51 376TOTAL THERMAL AREAS 3.538 4.446

TOTAL LIQUID BIOFUELS (transport) 228 2.200

9.739 20.220

141.567 167.100

6,9% 12,1%

TARGETS OF THE SPANISH RENEWABLE ENERGIES PLAN - 2005 - 2010

Electricity generation

Thermal uses

TOTAL RENEWABLE ENERGIES

(Energy scenario: Tendency/ REP)

Renewable energies / Primary energy (%)

Situation in 2004 Target situation in 2010

CONSUMPTION OF PRIMARY ENERGY (ktep)

THE RENEWABLE ENERGY PLAN (PER) 2005-2010

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

RENEWABLE ENERGY PLAN (2005 – 2010)

PARAMETERS ALL RENEWABLE AREAS

Public support 8,492.24 million €

Investment 23,598.64 million €

Total Energy Production 10,480,526 toe

Jobs Created 94,925 Jobs

Avoided Emissions as compared to NG Combined Cycle

2005 - 2010 Period : 76,983,254 tons CO2

THE RENEWABLE ENERGY PLAN (PER) 2005-2010

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

• Overall target (year 2010) 20,155 MW

• Generated electricity (2010) 45,511 GWh/year

•Related investment (2005-2010) 11,756 million €

• NO subsidies to investment.

• Emissions avoided (year 2010) 16,930,092 t CO2

• Estimation of job creation (2005-2010):

- Design and Construction 34,680 jobs

- Operation and Maintenance 3,113 jobs

RENEWABLE ENERGY PLAN (WIND ENERGY AREA). SUMMARY

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Proposed Measures:

Development of transport grid.

Updating and improvement of the regulatory procedures

regarding grid access and operating conditions.

Establishment of a single operation centre for the Special

Regime.

Improvement of wind generators behaviour, regarding

network.

PER 2005-2010:MAIN MEASURES IN WIND ENERGY AREA

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

SUMMARY

Target for wind energy in Spain: 20,155 MW (year 2010).Next year, starting new Renewable Energy Plan for 2011-2020.

Third position world-wide, with 14,600 MW commissioned (ending 2007).

Spanish technologists among the ten largest

manufacturers.

Stable legal framework: Feed-in Tariffs System, with premiumprice recognising environmental benefits.

R E N E W A B L E E N E R G Y I N S P A I N

Kingston, 23Kingston, 23rdrd June 2008 June 2008 World Wind Energy ConferenceWorld Wind Energy Conference

Thank youwww.idae.es