quiz 3 preparation slides

TRANSCRIPT

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 1/23

Valuing Accounts Receivables (AR)

AR Are reported as a Current Asset on thebalance sheet.

Sales on account raise the possibility of accountsnot being collected.

AR Are reported at the amount the company

thinks they will be able to collect or NetRealizable Cash Value (NRV).

AR Valuation can be difficult because an unknownamount of receivables will become uncollectible.

Accounts ReceivableAccounts Receivable Valuation on BSValuation on BS

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 2/23

Valuing Accounts Receivables (AR)Net Realizable Cash Value (NRV) =

Accounts Receivable (AR)- Uncollectible Accounts Receivable

Net Realizable Cash Value of AR (NRV)

In ACCRUAL accounting,Uncollectible AR are debited to

Bad Debt Expense(or Uncollectible Accounts Expense)

In CASH accounting, credit sales aren·t recorded,so Bad Debt (or Uncollectible Accounts) Expense IsNOT Allowed

Accounts Receivable (AR)Accounts Receivable (AR)

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 3/23

Management estimates uncollectible accountsas a percentage of Net Credit Sales*, based on past

experience and anticipated credit policy* Credit Sales ² Returns & Allowances ² Discounts

Current-period Net Credit Salesx the pre-determined percentageBad Debts Expense (for the period)

SO 3 Distinguish between the methods and bases companiesSO 3 Distinguish between the methods and bases companiesuse to value accounts receivable.use to value accounts receivable.

Accounts ReceivableAccounts Receivable ADA (% of Sales)ADA (% of Sales)

Percen tage-of-Sales

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 4/23

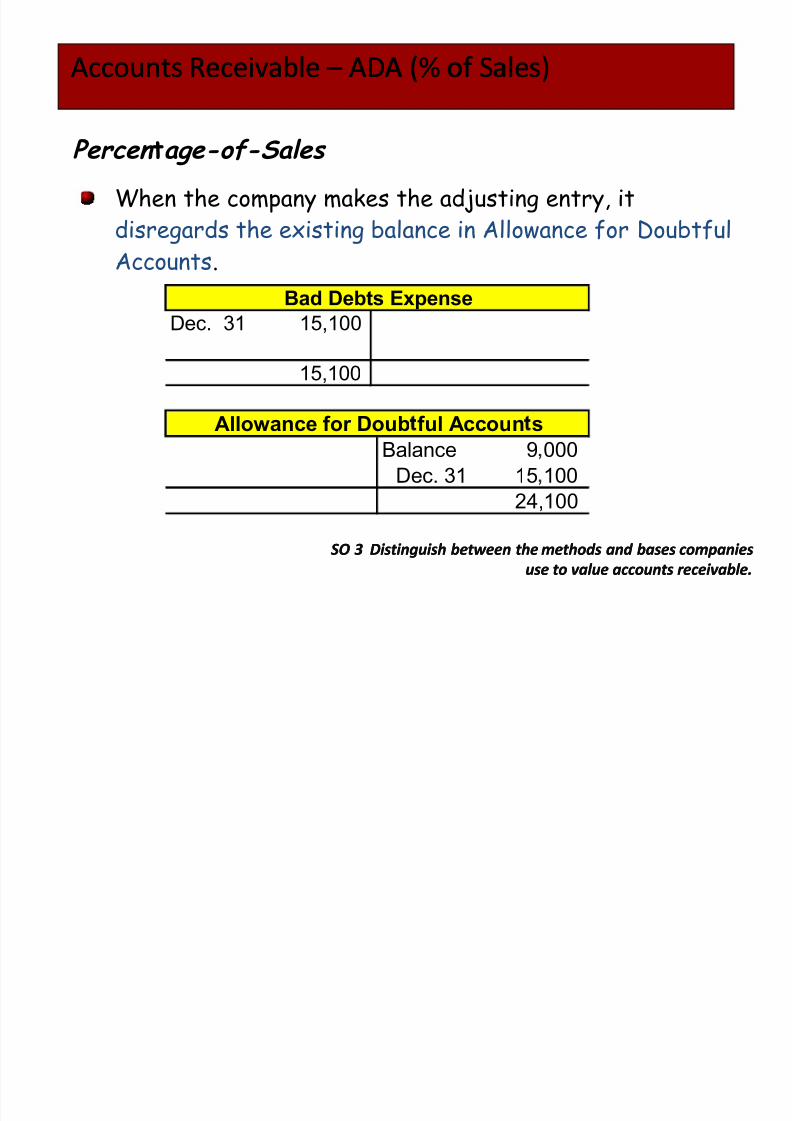

When the company makes the adjusting entry, itdisregards the existing balance in Allowance for DoubtfulAccounts.

SO 3 Distinguish between the methods and bases companiesSO 3 Distinguish between the methods and bases companiesuse to value accounts receivable.use to value accounts receivable.

Accounts ReceivableAccounts Receivable ADA (% of Sales)ADA (% of Sales)

Dec. 31 15,100

15,100

Bad Debts Expense

Percen tage-of-Sales

Balance 9 000

Dec. 31 15 100

24,100

Allowance f or Doub f ul Accoun s

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 5/23

Illustration: If the trial balance shows Allowance forDoubtful Accounts with a credit balance of $528, the companywill make the following adjusting entry.

SO 3 Distinguish between the methods and bases companiesSO 3 Distinguish between the methods and bases companiesuse to value accounts receivable.use to value accounts receivable.

Accounts ReceivableAccounts Receivable ADA (% Receivables)ADA (% Receivables)

Bad Debts Expense 1,700Dec. 31

Allowance for Doubtful Accounts 1,700

P er cen tag e-of-R eceiv abl es

* $2,228 (Desired ADA, based on AR aging schedule)² 528 (Existing credit balance)1,700

*

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 6/23

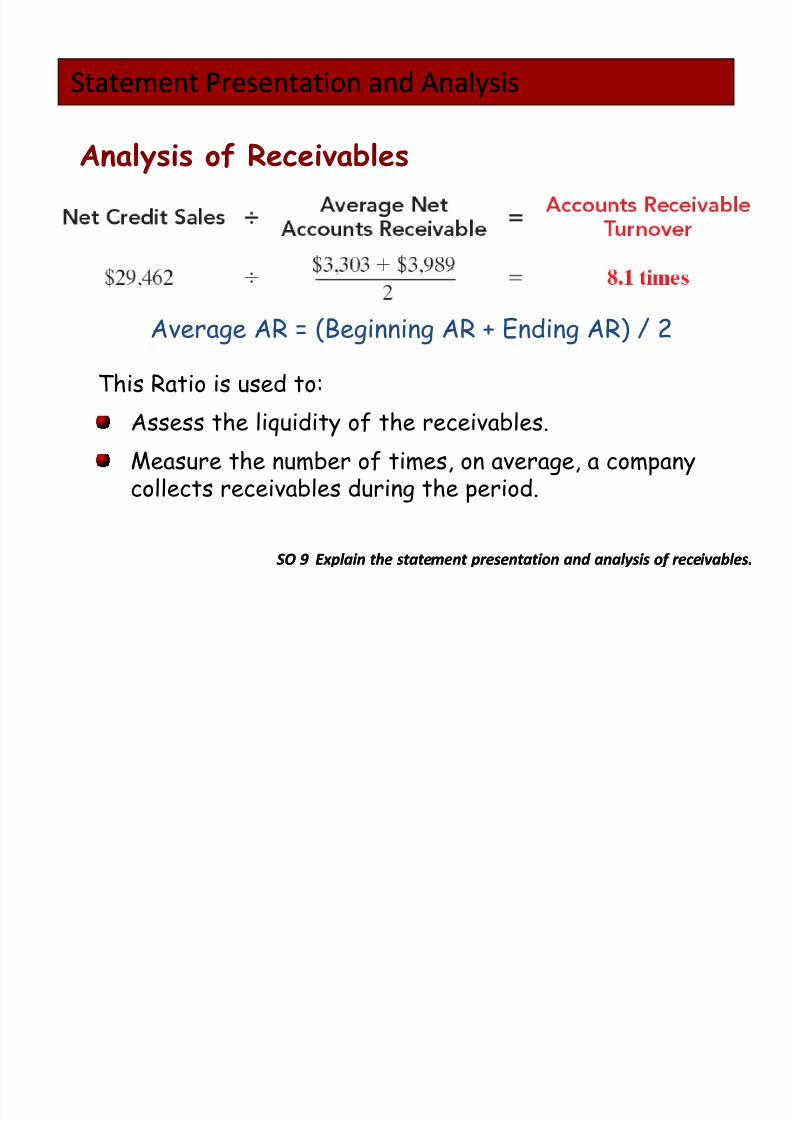

Analysis of Receivables

This Ratio is used to:

Assess the liquidity of the receivables.

Measure the number of times, on average, a companycollects receivables during the period.

SO 9 Explain the statement presentation and analysis of receivables.SO 9 Explain the statement presentation and analysis of receivables.

Statement Presentation and AnalysisStatement Presentation and Analysis

Average AR = (Beginning AR + Ending AR) / 2

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 7/23

Variant of the accounts receivable turnover ratio is averagecollection period in terms of days.

Used to assess effectiveness of credit and collectionpolicies.

Collection period should not exceed credit term period.

SO 9 Explain the statement presentation and analysis of receivables.SO 9 Explain the statement presentation and analysis of receivables.

Statement Presentation and AnalysisStatement Presentation and Analysis

Analysis of Receivables

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 8/23

SO 5 Compute the maturity date of and interest on notes receivable.SO 5 Compute the maturity date of and interest on notes receivable.

Notes ReceivableNotes Receivable

Computing Interest

Time in Terms of One Year (Fraction) =

(Total # months / 12) or (Total # days / 360)NOTE: Lenders typically use 360 days (instead of 365),because it yields more Interest Revenue

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 9/23

Depreciable Annual Accum. Year Cost Years Depr. Exp. Deprec.

2010 108,000$ / 5 = 21,600$ 21,600$

2011 108,000 / 5 = 21,600 43,200

2012 108,000 / 5 = 21,600 64,800

2013 108,000 / 5 = 21,600 86,400

2014 108,000 / 5 = 21,600 108,000

108,000$

E 10E 10--6 (a altered)6 (a altered) -- SL DepreciationSL Depreciation

Depreciation Expense - Machine 21,600

Accumulated Depreciation - Machine 21,600

2010 Journal Entry

Depreciable Cost = 120,000 Cost ² 12,000 Salvage = 108,000 Depreciation Expense (Annual) = 108,000 / 5 Years = 21,600 Depreciation Rate = 1 / 5 Year Useful Life = 20%

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 10/23

Declinin

Beginning B lance Ann al Accum.

Year B k value Rate Expen e Deprec.

2010 120,000$ x 40% = 48,000$ 48,000$

2011 72,000 x 40% = 28,800 76,800

2012 43,200 x 40% = 17,280 94,080

2013 25,920 x 40% = 10,368 104,448

2014 15,552 x 40% = 3,552 108,000

108,000$

E 10E 10--6 (c altered)6 (c altered) -- DDB DepreciationDDB Depreciation

Plugged

Depreciation Expense - Machine 48,000

Accumulated Depreciation - Machine 48,000

2010 Journal Entry

Depreciable Cost = 120,000 Cost (Ignore Salvage Value)

Depreciation Rate = 2 / 5 Year Useful Life = 40% Depreciation Expense = Book Value x 40%

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 11/23

Brief Exercise 10Brief Exercise 10--7 Revising Depreciation7 Revising Depreciation

Depreciation Expense - Equipment 4,500

Accumulated Depreciation - Equipment 4,500

Journal entry for 2010

SO 4 Describe the procedure for revising periodic depreciation.SO 4 Describe the procedure for revising periodic depreciation.

Book value, 1/1/10Book value, 1/1/10 $20,000$20,000

Salvage valueSalvage value

Depreciable costDepreciable cost

Useful life (revised) /Useful life (revised) /

Annual depreciationAnnual depreciation

Book Value at theBook Value at the

date of change in thedate of change in the

estimate =estimate =

29,00029,000 9,000 =9,000 =

$20,000.

-- 2,0002,000

18,00018,000

4 years4 years

$ 4,500$ 4,500

Illustration 10-17

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 12/23

Chan Company sells office equipment on September 30, 2010,for $35,000 cash. The office equipment originally cost$72,000 and as of January 1, 2010, had accumulated

depreciation of $42,000. Depreciation for the first 9 monthsof 2010 is $5,250.

1. Record depreciation to date, updating BV (5,250 for Jan - Sept)

2. Eliminate current BV (Asset & Accumulated Depreciation)

3. Recognize any value received (35,000 in Cash; No assets)

4. Recognize Gain/Loss ($35,0000 received ² 24,750 BV = $10,250 Gain)

BE10BE10--10 (altered)10 (altered) -- Sale of Sale of Plant AssetsPlant Assets

Gain on Sale: Proceeds ($ + FMV of assets) > Book Value of asset

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 13/23

Journal Entryb) Record sale of asset

BE10BE10--10 (altered)10 (altered) -- Sale of Sale of Plant AssetsPlant Assets

Gain on Sale: Proceeds ($ + FMV of assets) > Book Value of asset

Current V of Asset = 72,000 ² 47,250 = $24,750

Gain/Loss on Sale = $35,000 received ² 24,750 BV = $10,250 Gain

Cash (No assets received) 35,000Accumulated Depreciation ² Equipment 47,250

Equipment 72,000Gain on Sale ² Equipment 10,250

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 14/23

Journal Entryb) Record sale of asset

BE10BE10--10 (altered)10 (altered) -- Sale of Sale of Plant AssetsPlant Assets

Loss on Sale: Proceeds ($ + FMV assets) < Book Value of asset

Current V of Asset = 72,000 ² 47,250 = $24,750

Gain/Loss on Sale = $20,000 received ² 24,750 BV = $4,750 Loss

Cash (No assets received) 20,000Accumulated Depreciation ² Equipment 47,250Loss on Sale ² Equipment 4,750

Equipment 72,000

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 15/23

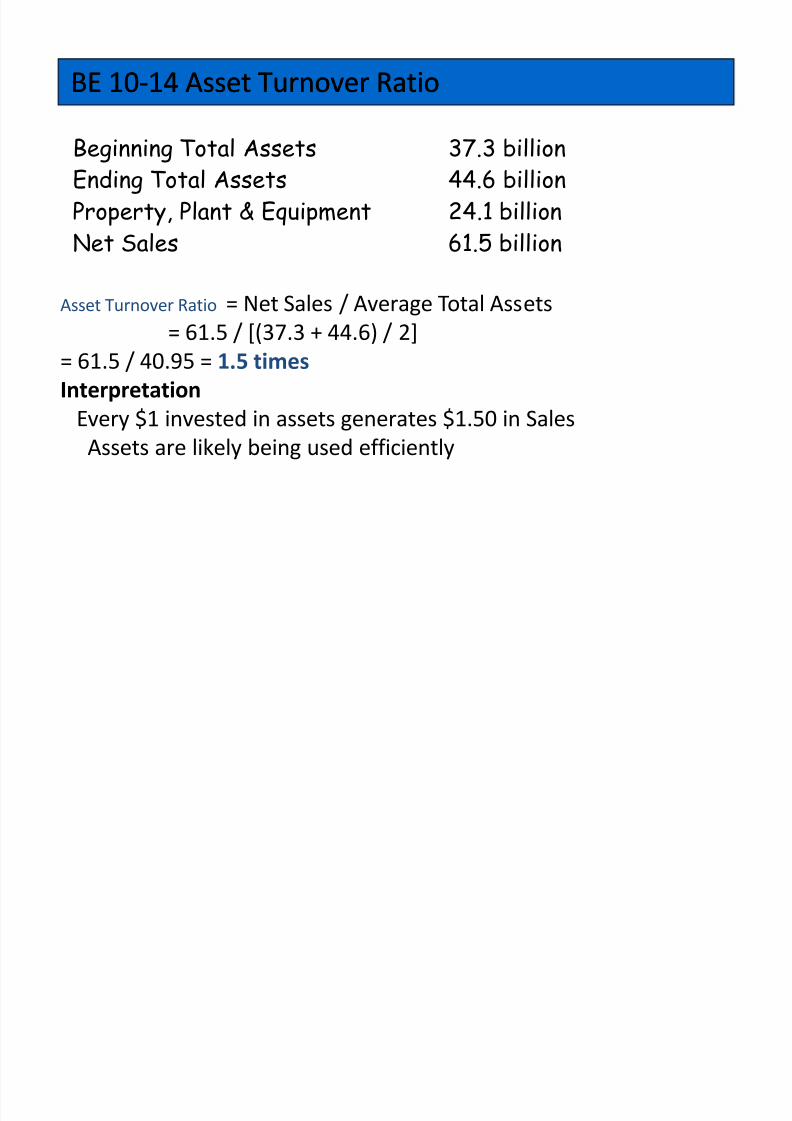

Beginning Total Assets 37.3 billionEnding Total Assets 44.6 billionProperty, Plant & Equipment 24.1 billionNet Sales 61.5 billion

BE 10BE 10--14 Asset Turnover Ratio14 Asset Turnover Ratio

Asset Turnover Ratio = Net Sales / Average Total Assets

= 61.5 / [(37.3 + 44.6) / 2]

= 61.5 / 40.95 = 1.5 times

Interpretation

Every $1 invested in assets generates $1.50 in SalesAssets are likely being used efficiently

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 16/23

Accounting for Current LiabilitiesAccounting for Current Liabilities

SO 3 Expla in th e acco un ting for o th er c urren t l iab il ities .SO 3 Expla in th e acco un ting for o th er c urren t l iab il ities .

Sales Ta x Pa yable Retailer collects tax from customers as sales occur

Periodically remits collections to state (NYS Sales Tax)

Determining Sales T ax Payable1. Sales tax stated as % of the sales price2. Sales Tax is totaled separately or part of total receipts3. If Sales Tax is part of total receipts (NOT separated):

Sales = Cash Receipts / (1 + Sales Tax %)Sales T ax = Total receipts - Sales (as determined above)

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 17/23

Mandatory:

FICA tax

Federal income tax

State income tax

Payroll Deductions

SO 6 Compute and record the payroll f or a pay period.

Determining the PayrollDetermining the Payroll

Voluntary:

Charity

Retirement

Union dues

Health and life insurance

Pension plans

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 18/23

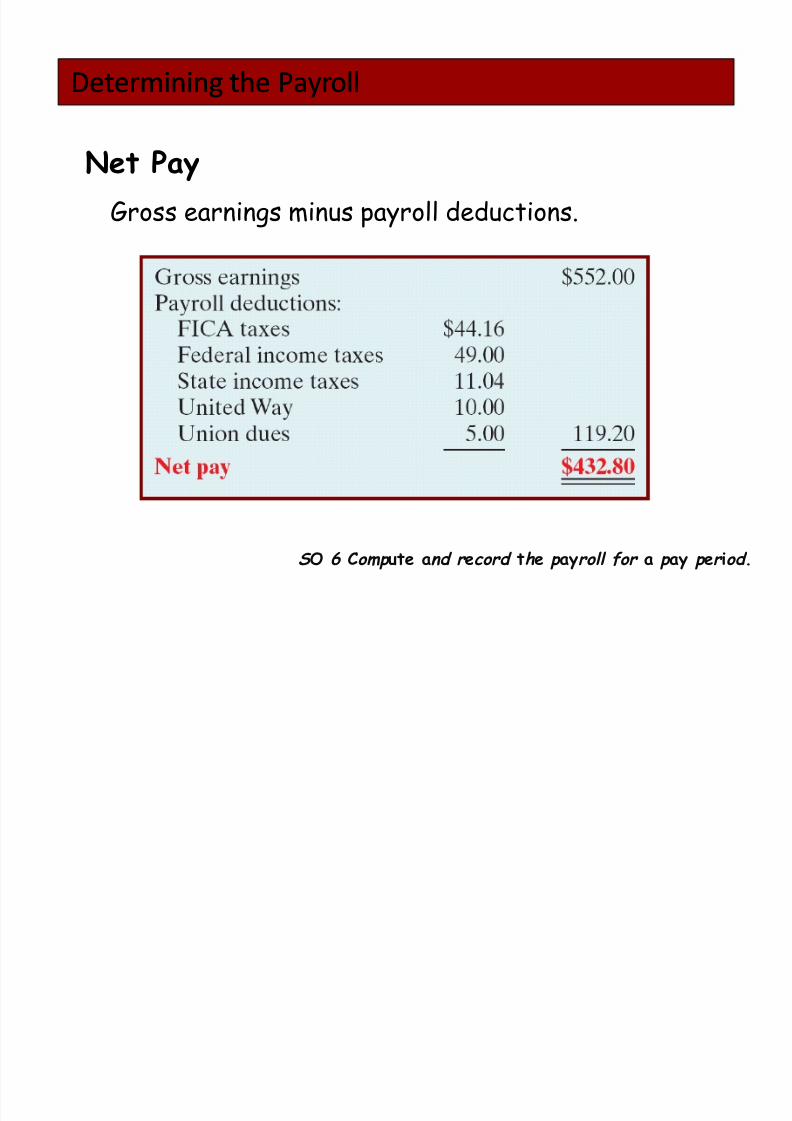

Gross earnings minus payroll deductions.

Net Pay

SO 6 Comp ute and r ecord the p ayroll for a p ay p er iod .

Determining the PayrollDetermining the Payroll

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 19/23

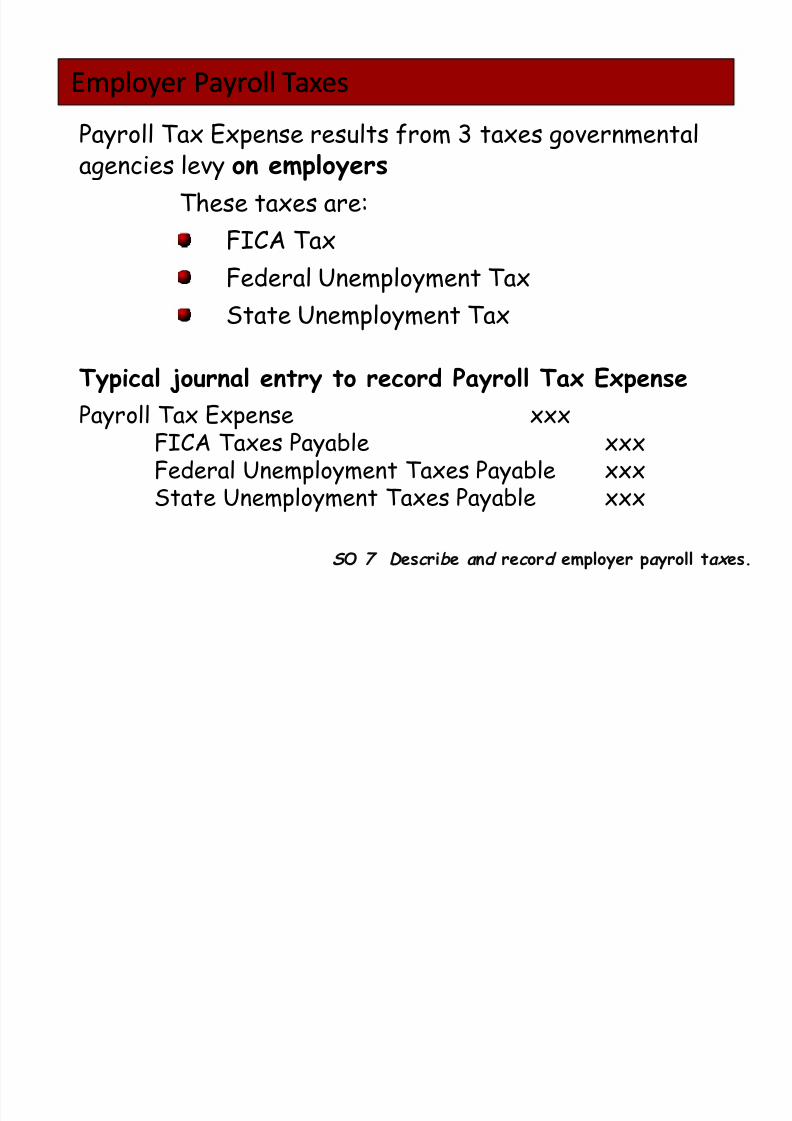

Payroll Tax Expense results from 3 taxes governmentalagencies levy on employers

SO 7 Desc rib e a nd rec ord employer pa yroll ta xes.

Employer Payroll TaxesEmployer Payroll Taxes

These taxes are:

FICA Tax

Federal Unemployment TaxState Unemployment Tax

T ypical journal entry to record Payroll T ax Expense

Payroll Tax Expense xxxFICA Taxes Payable xxxFederal Unemployment Taxes Payable xxxState Unemployment Taxes Payable xxx

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 20/23

Paid-in Capital - total amount of cash and other assets paidin to the corporation by stockholders in exchange for capitalstock

PaidPaid--in Capitalin Capital

PaidPaid--in Capital inin Capital in

Excess of ParExcess of ParAccountAccount

Sources of Owner·s Equity (Corporate Capital)

Common StockCommon StockAccountAccount

Preferred StockPreferred StockAccountAccount

Corporate CapitalCorporate Capital Owners EquityOwners Equity

SO 2 Differen tia te be tw een pa id SO 2 Differen tia te be tw een pa id--in cap ital and re ta ined earn ings .in cap ital and re ta ined earn ings .

1. Money Invested by Owners (Stockholders)2. Money made by corporation

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 21/23

PaidPaid--in Capitalin Capital

Retained EarningsRetained EarningsAccountAccount

Additional PaidAdditional Paid--in Capitalin CapitalAccountAccount

Two PrimarySources ofEquity

Common StockCommon StockAccountAccount

Preferred StockPreferred StockAccountAccount

Corporate CapitalCorporate Capital

SO 2 Differen tia te be tw een pa id SO 2 Differen tia te be tw een pa id--in cap ital and re ta ined earn ings .in cap ital and re ta ined earn ings .

Re ta ined Earn ings - Net Income a corporation retains forfuture use (Earned but NOT property of/distributable to owners)

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 22/23

PaidPaid--in Capitalin Capital

Retained EarningsRetained EarningsAccountAccount

PaidPaid--in Capital inin Capital inExcess of ParExcess of ParAccountAccount

Less:Less:Treasury StockTreasury StockAccount

Two PrimarySources ofEquity

Common StockCommon StockAccountAccount

Preferred StockPreferred StockAccountAccount

Accounting for Treasury StockAccounting for Treasury Stock

SO 4 Ex pla in th e acco un ting for treas ury s tock .SO 4 Ex pla in th e acco un ting for treas ury s tock .

8/6/2019 Quiz 3 Preparation Slides

http://slidepdf.com/reader/full/quiz-3-preparation-slides 23/23

Cash (10,000 x $17) 170,000

Treasury Stock (10,000 x $15) 150,000

Paid-in Capital - Treasury Stock 20,000

ReRe--Issuance of Treasury StockIssuance of Treasury StockAboveCost

E 13-7a Nunez originally issued 200,000 shares of $5 par,common stock for $12.50 per share. On March 1st thecompany re-acquired 50,000 shares for $15 per share.

On July 1st 10,000 shares were re-issued at $17 per share.

NOTE: Re-Issuance of Treasury Stock Increases total Assets &total Stockholders· Equity by $170,000

A corporation does not realize a gain or suffer a loss from stocktransactions with its own stockholders.