quebec’s sales recording module (srm): fighting the zapper ... · pdf filecanadian tax...

TRANSCRIPT

canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4, 715 - 61

715

Quebec’s Sales Recording Module (SRM): Fighting the Zapper, Phantomware, and Tax Fraud with Technology

Richard Thompson Ainsworth and Urs Hengartner*

P r é c i s

Le 28 janvier 2008, Jean-Marc Fournier, le ministre du revenu du Québec, a annoncé que d’ici la fin de 2009, Revenu Québec allait tester un nouvel appareil anti-fraude — le « module d’enregistrement des ventes » (Mev) — dans le secteur de la restauration. Le Mev est conçu pour détecter les enregistrements numériques des ventes qui ont été effacés ou supprimés dans les caisses enregistreuses électroniques et les systèmes au point de vente — un type de fraude qui contribue à plus de 425 millions $ par année de recettes fiscales non perçues uniquement dans le secteur de la restauration. Les études menées par le Québec indiquent que les restaurateurs recourent de plus en plus à la technologie pour modifier les enregistrements numériques dans le but de soustraire des revenus du fisc et d’éviter de déclarer et de verser les taxes qu’ils ont perçues. Le Mev aidera les vérificateurs de la province à mettre au jour ces activités frauduleuses.

Les autorités fiscales du monde entier ont adopté deux approches pour s’assurer de l’intégrité des enregistrements des ventes dans les secteurs à forte utilisation de l’argent en espèces : une approche axée sur les caisses enregistreuses, et une autre approche qui mise plutôt sur les principes de conformité et de coercition dans la promotion de bonnes pratiques commerciales. Avec la mise en place du Mev, le Québec prend les moyens pour devenir une administration fiscale axée sur les caisses enregistreuses.

L’article présente le Mev dans le cadre d’une analyse comparative. Les approches technologiques de l’Allemagne et de la Grèce (deux administrations axées sur les caisses enregistreuses) sont comparées avec celle des Pays-Bas (une administration fiscale qui mise sur les principes) qui prend appui sur d’intenses vérifications axées sur les technologies pour vérifier l’exactitude des enregistrements numériques.

Dans sa conclusion, l’auteur suggère qu’il y aurait lieu de s’inspirer du projet de rationalisation de la taxe de vente des États-Unis qui recourt à la certification par l’administration des technologies fiscales en vue d’assurer l’exactitude des déterminations des taxes sur les opérations.

* RichardThompsonAinsworthisoftheSchoolofLaw,GraduateTaxProgram,BostonUniversity(e-mail:[email protected]).UrsHengartnerisoftheDavidR.CheritonSchoolofComputerScience,UniversityofWaterloo(e-mail:[email protected]).

716 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

A b s t r A c t

On January 28, 2008, Quebec’s minister of revenue, Jean-Marc Fournier, announced that by late 2009 Revenu Québec would begin testing an anti-fraud device—the “sales recording module” (SRM)—in the restaurant sector. The SRM is designed to detect the erasure of digital sales records in electronic cash registers and point-of-sale systems—a type of fraud that contributes to more than $425 million annually in lost tax revenues in the restaurant sector alone. Quebec studies indicate that restaurateurs are increasingly employing technology to alter digital records in order to conceal income from the business and avoid reporting and remitting taxes due. The SRM will assist provincial auditors in detecting such fraudulent activities.

Revenue authorities around the globe have taken two approaches to assuring the integrity of business records in cash-intensive industries: one approach secures the till; the other relies on principles of compliance and enforcement to encourage good business practices. With the introduction of the SRM, Quebec is taking steps to become a “fiscal till” jurisdiction.

This article considers the SRM in a comparative context. The technological approaches of Germany and Greece (both of which are fiscal till jurisdictions) are contrasted with the approach adopted in the Netherlands (a principles-based jurisdiction), which relies on intensive technology-based audits to assure digital record accuracy.

The article concludes with a suggestion that there may be something to learn from the US streamlined sales tax initiative, which employs government certification of tax technology to ensure the accuracy of transaction tax determinations.

Keywords: Fraud n tax evasion n restaurants n anti-avoidance n technology n srM

c o n t e n t s

Introduction 717Structure of Our Argument 723Schematic of Skimming with Zappers 724Fiscal Tills: Greece, Quebec, and Germany 728

Greece: Fiscal electronic Devices (FeCRs, AFeD Printers, and FeSDs) 728FeCRs and AFeD Printers 729FeSDs 732How FeCRs with AFeD Printers and FeSDs Defeat Zappers and Phantomware 733

Quebec: SRMs 735Germany: Smart Cards embedded in eCRs 741The Role of Audits in Fiscal Till Jurisdictions 746

Comprehensive Audit: The Netherlands 748Blending Rules and Principles: Certification of Third-Party Service Providers 751

1. How Does a CSP Get eCR and POS System Data? 7522. How Can a CSP Be Sure That the Data It Has Are Accurate

(Free from Manipulation)? 7543. What Standards Should the Government Use To Certify a CSP’s

Automated System? 7544. What Is the Most efficient and Cost-effective Way for a CSP

To Satisfy the Government’s Standards? 755Conclusion: Assessing Quebec’s SRM 757Appendix Comparison of Solutions in the Five Jurisdictions—A Graphic Summary 759

quebec’s sales recording module (srm) n 717

intro duc tio n

OnJanuary28,2008, theQuebecministerof revenue, Jean-MarcFournier, an-nounced1thatbylate2009RevenuQuébecwouldbegintestingadevice,the“salesrecordingmodule”(SRM),whichisprojectedtosubstantiallyreducetaxfraudintherestaurantsector.2OnNovember30,2009,thepilotprogramwasunderwaywith46restaurantsinsevencitiesinvolved.By2010or2011,SRMswillbemandatoryinallQuebecrestaurants,wheretheywillassureaccuracyandretentionofbusinessrecordswithinelectroniccashregisters(eCRs).TheQuebecgovernmenthasprom-isedtoprovidethenecessarynumberofSRMstorestaurantsatnocost.ThecosttotheQuebectreasuryforthewholeprogramisestimatedtobe$55million.3

TheproblemthattheSRMaddressesistheerasureofsalesrecordsfromtheeCRthroughaback-officeoreCR-embeddedprogram.TheeCR’srecordsarethecentral(insomecases,theonly)repositoryofbusinessdata.Asaresult,theeCR’sdataarerelieduponbytaxauthoritiestoverifysalesandincome.Thetargetisalwayscash.Credit,debit,cheque,orbanktransfertransactionsleaveotheraudittrails,butcashtransactionsarefoundonlyintheeCR.

InQuebec,asintherestoftheworld,restaurantsarethemostvulnerabletothisfraud.TheSRMtargetsthissector,althoughsimilarfraudscouldoccuringrocerystoresoranyotherbusinessmakingcashsalesdirectlytoconsumers.Business-to-businesstransactionsarenotcoveredbytheSRM.

ItiscleartoQuebec’srevenueministerthatnotonlyarelargevolumesofcashbeingskimmed(removedfromthesalesandprofitsrecordsofrestaurantsbytheirowners),butthisfraudagainstthepublicfiscisincreasing.Itisfacilitatedandaccel-eratedbytechnology.ThedigitalmanipulationofbusinessrecordskeptbymoderneCRsisalltooprevalent.Add-onsoftware(zappers),factory-ordistributor-installedsoftware,andold-fashionedmanualreprogrammingofeCRs (phantomware)arethemechanismsthroughwhichthemanipulationsarise.Twoexamplesofzappersareshowninfigures1and2.RevenuQuébechaspursuedthesedevices (knowngenerallyas“camoufleurdeventes,”orsaleszappers)overthepastdecade,andisconvincedthatsomethingmorethanatraditionalauditisneededtocounteractthemanipulations.

1 RevenuQuébec,“Pourplusd’équitédanslarestauration:ilfautqueçasepasseau-dessusdelatable”[“ForMoreequityintheRestaurantSectorItIsRequiredThat[BusinessIsConducted]AbovetheTable”],Communiqué de presse,January28,2008(online:http://www.revenu.gouv.qc.ca/eng/ministere/centre_information/communiques/autres/2008/28jan.asp)(translationonfilewithRichardT.Ainsworth,referredtoinsubsequentnotesasR.T.A.).

2 RevenuQuébec,“L’évasionfiscaleauQuébec:Facturationobligatoiredanslesecteurdelarestauration—Sous-déclarationdesrevenusdanslesecteurdelarestauration”[“TaxevasioninQuebec:ObligatoryBillingintheRestaurantSector—Under-DeclarationofRevenuesintheRestaurantSector”],January28,2008(PowerPointpresentationandtranslationonfilewithR.T.A.).TheFrenchtermforthedeviceis“moduled’enregistrementdesventes”(MeV).

3 CarolineRodgers,“Québecvadel’avantpourstopperlafraudefiscale,”January28,2008,atHôtels, Restaurants & Institutions(online:http://www.hrimag.com/spip.php?article2771)(translationonfilewithR.T.A.).

718 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

Relyingonmorethan230casessince1997,andsurveysofskimmingactivityintherestaurantsector,theministerofrevenuesummarizedthesituationasfollows:

Althoughthemajorityofrestaurateurscomplywiththeirtaxobligations,therestau-rantsectorremainsanareaoftheQuebececonomywheretaxevasionisrampant,bothintermsofincometaxandsalestaxes.Taxlossesinthissectorareimportant.QuebecRevenueestimatesthattheyare$425millionforthe2007-2008fiscalyear.4

Thezappers(andphantomwareapplications)thatarethemajorfacilitatorsofthis fraud are not confined to Quebec. Zappers and phantomware have spreadthroughoutCanada5andaroundtheworld. It isnotsurprising, therefore, thatanumberofjurisdictionshavelookedatautomatedsalessuppressionandhaveadopt-edtechnologicalcountermeasures,someofwhicharestrikinglysimilartotheSRM.Otherjurisdictionslooktotechnologyforanswers,butdifferwithrespecttothesophisticationofthetechnologythattheywoulddeploy.Inyetotherjurisdictions,traditionalauditratherthantechnologyispreferred;however,themostsuccessfulof these “audit-only” jurisdictions are adopting comprehensive (multitax) auditstrategies,withteamsofauditorssupportedbycomputerspecialists—ineffect,a“supersized”traditionalaudit.

Areviewofapproachesindicatesthattwopolicyorientationsguideenforcementactions in this area: one approach is rules-based; the other is principles-based.6Theyarenotmutuallyexclusive—degreesofblendingarecommon.Rules-based

4 Supranote2.Thebasisfortheminister’sestimatesisarigorousempiricalstudyperformedbyQuebec’sMinistèredesFinances,“TaxevasioninQuebec:ItsSourcesandextent”(2005)vol.1,no.1Economic Fiscal and Budget Studies1-6(online:http://www.finances.gouv.qc.ca/documents/eeFB/en/eef b_vol1_no1a.pdf ).Inapersonale-mailcommunication,June23,2009(onfilewithR.T.A.),GillesBernard,directeurgénéraladjointdelarecherchefiscale,RevenuQuébec,respondedtoaquestiononthe$425millionfigureusedbytheminister.Indicatingancillarylossesof$8millioninother(unspecified)taxes,Bernardstated,“Thetaxlossesare417M$(QST+IncomeTax).TheQST[Quebecsalestax]represents133M$andtheIncometaxlossesare284M$.Thislastamountcanbedoubledtotakeintoaccountthefederalincometax.”

5 CanadaRevenueAgency,“BusinessesWarnedAgainstUsingTaxCheatingSoftware,”Tax Alert,December9,2008:“TheCanadaRevenueAgency(CRA)isawarethatelectronicsalessuppressionsoftwareiscurrentlybeingmarketedandsoldtoCanadianbusinesses.Businessownersareremindedthathidingincometoevadetaxesisagainstthelaw.Usingthissoftwareisnotworththerisk....Businessesthathaveusedelectronicsalessuppressionsoftwarearesuspectedofhavinghiddenthousandsoftransactionsandmillionsofdollarsinsales”(online:http://www.cra-arc.gc.ca/nwsrm/lrts/2008/l081210-eng.html).SeealsoDarahHansen,“CookingtheBooks,”Vancouver Sun,December11,2008:followingallegationsbytheCRAthatfourChineserestaurantsinBritishColumbiahadparticipatedinahigh-techschemethatusedzapperstoevadetaxonmillionsofdollarsofreceipts,fivepeoplewerefacing25chargesaspartofanationwideinvestigation(online:http://www.canada.com/vancouversun/story.html?id=6c945ca6-f84a-43f6-86ad-221814731593&p=2).Alsoseeinfranote8.

6 europeanCommission,Directorate-GeneralTaxationandCustomsUnion,FiscalisCommitteeProjectGroup12,CashRegisterProjectGroup,“CashRegisterGoodPracticeGuide,”December2006,5-6(unpublishedreportonfilewithR.T.A.).

quebec’s sales recording module (srm) n 719

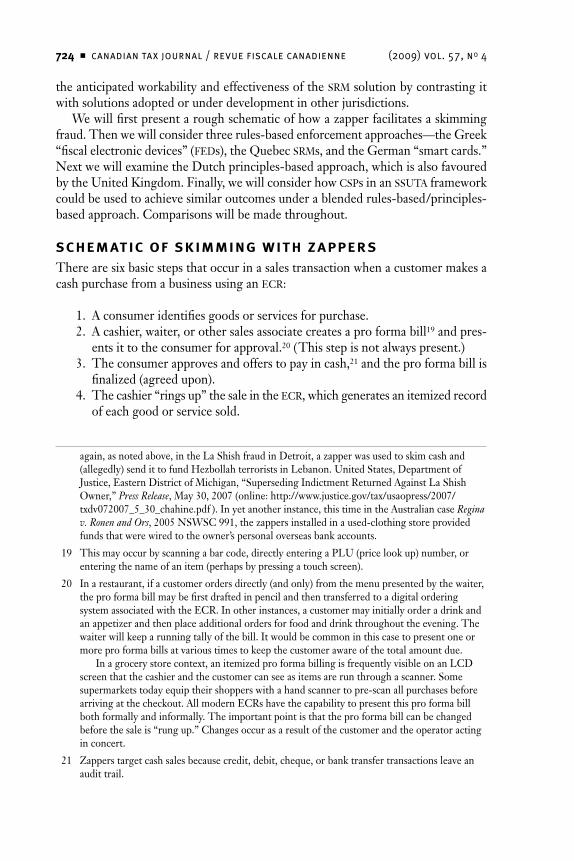

Fig

ur

e 1

Old

-Sty

le Z

appe

r, H

ard-

Wir

ed in

to E

lect

roni

c Ca

sh R

egis

ter

Thi

sis

an

old-

styl

eza

pper

,whi

chh

asb

een

hard

-wir

edin

toth

eel

ectr

onic

cas

hre

gist

er(e

CR

)and

isth

eref

ore

easy

tod

etec

t.T

hep

ictu

res

how

sth

eto

pof

the

eC

Rr

emov

ed;t

hela

rge

whi

tea

rrow

poi

nts

toth

ede

vice

.(R

epro

duce

dby

per

mis

sion

oft

heg

over

nmen

tofQ

uebe

c.)

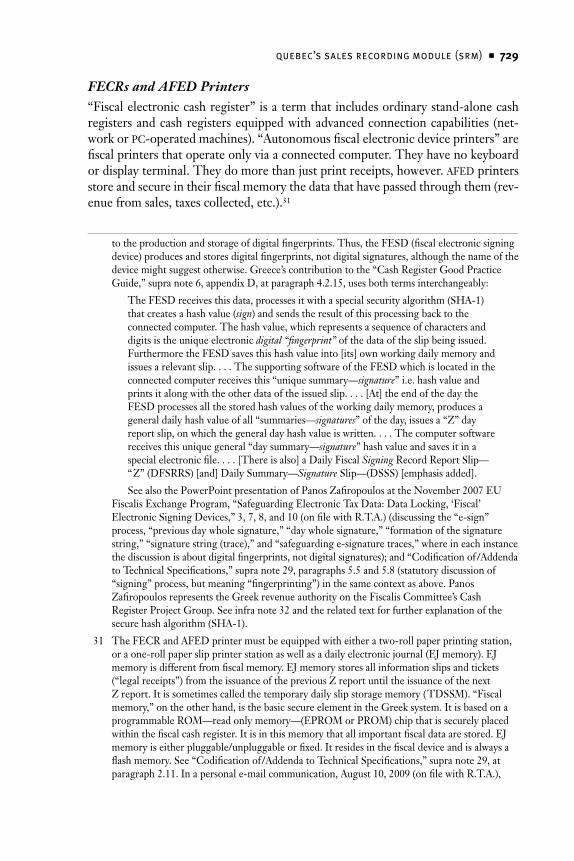

720 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4Fi

gu

re

2 M

oder

n Za

pper

Usi

ng M

emor

y S

tick

Thi

sis

am

ore

mod

ern

zapp

er,w

hich

isa

mem

ory

stic

k(“

dong

le”)

that

isin

sert

edin

toth

eba

ck-o

ffice

com

pute

rsy

stem

that

co

llect

sda

tafr

omth

ebu

sine

ss’s

elec

tron

icc

ash

regi

ster

s.(R

epro

duce

dby

per

mis

sion

oft

heg

over

nmen

tofS

wed

en.)

quebec’s sales recording module (srm) n 721

jurisdictions adopt comprehensive and mandatory legislation regulating and/orcertifying cash registers. Jurisdictions taking this approach include Greece andGermany.WiththeadoptionoftheSRM,Quebecwillalsofallwithinthisgroup.Thesejurisdictionsareclassifiedgenerallyas“fiscaltill”(alsocalled“fiscalmemory”)jurisdictions.

Principles-based jurisdictionsrelyoncompliant taxpayers followingtherules.Complianceisenforcedwithanenhancedauditregime.Comprehensivemultitaxaudits (the simultaneous examinationof income, consumption, andemploymentreturns)areperformedbyteamsthatincludecomputerauditspecialists.Auditsarefrequently unannounced and preceded by undercover investigations that collectdatatobeverified.7JurisdictionstakingthisapproachincludetheUnitedKingdom,Canada, and theNetherlands.Francehas implementedaprogramofpreventiveauditsthattargettechnologyproviders.8AsimilareffortcanbefoundinQuebec,wherethecustomerlistsofauditedtechnologyprovidershavebeenusedtomaplaterauditsofbusinessessuspectedoftechnology-assistedskimming.9PriortotheadoptionoftheSRM,Quebecfellsquarelywithinaprinciples-basedclassification.Movingforward,Quebecwillmergebothapproaches,eventhoughitappearsthattheCanadaRevenueAgency(CRA)willcontinuetopursueonlyprinciples-basedenforcementtechniques.10

7 Forexample,therecentCanadianinvestigationinBritishColumbiaintotheallegeddistributionofsalessuppressionsoftwarebyInfoSpecSystemsInc.involvedaneight-monthundercoverinvestigationbytheRoyalCanadianMountedPolice(RCMP).Duringthisphaseoftheoperation,undercoverRCMPofficersposedaspotentialbuyersofsalessuppressionsoftware.ThisevidencesupportedallegationsthatInfoSpecSystemsInc.knowinglyprovidedrestaurantswithzappers.CanadaRevenueAgency,“ChargesLaidinLarge-ScaleTaxFraudInvestigation,”News Release,December10,2008(online:http://www.cra-arc.gc.ca/nwsrm/rlss/2008/m12/nr081210-eng.html).

8 “CashRegisterGoodPracticeGuide,”supranote6,at6.ThisistheapproachthattheCRAtookintheInfoSpecSystemsinvestigation.Targetingthesoftwareprogram(Profitek)“documents,CDs,computerfiles,salesnotebooks,anelectroniccalendar,e-mailandotherclientlists,”theCRAwasabletoconductanationwideinvestigation,which(accordingtotheVancouver Sun)is“continuingand[CRAofficials]expectmorechargestobelaid.”Hansen,supranote5.

9 Forexample,seetheinvestigationofAudioLabLP:RevenuQuébec,“RevenuQuébecenquêtesurunconcepteurdelogicieldepointdeventesoupçonnéd’avoirconçuetdistribuéuncamoufleurdeventes”[“RevenuQuébecInvestigationofaSoftwareDesignerOutletSuspectedofHavingDevelopedandDistributedZappers”],Communiqué de presse,October14,2005(online:http://www.revenu.gouv.qc.ca/en/ministere/centre_information/communiques/ev-fisc/2005/14oct.aspx)(translationonfilewithR.T.A.);andtheinvestigationofMichaelRoyreportedinRevenuQuébec,“FinesofMorethanOneMillionDollars—AFatherandHisTwoSonsConvictedforTaxevasioninConnectionwiththeZapper,”News Release,May2,2003(online:http://www.revenu.gouv.qc.ca/eng/ministere/centre_information/communiques/ev-fisc/2003/02mai.asp)(onfilewithR.T.A.).

10 InitsrecentTax Alertdealingwithsalessuppressionsoftware,theCRAemphasizedthatithas“over5,000employeesdedicatedtofindingunreportedbusinessincomeandensuringthattheproperamountoftaxesispaid,evenwhensalesrecordsaremissing.”Tax Alert,supranote5.

722 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

Itwouldbeveryhelpfulifacomparativecross-methodologyanalysisofthevari-ousapproachescouldbepresented(rules-basedwithandwithouttechnologyversusprinciples-basedwithandwithoutacomprehensiveaudit).Weneedtoquantifythecomplianceimprovementagainstthecostofgettingthatcompliance.Unfortunately,mostofthetechnologysolutionsareinprototype.PerhapsQuebec(asitmeasurestheeffectivenessofmovingfromtraditionalauditalonetotechnologyandaudit)willhavegoodmeasuresinafewyears.

Amidalltheinternationalconcern,itisnotablethattheUnitedStatesdoesnothaveacoordinatedzapperenforcementeffort.Infact,theUnitedStateshasuncov-ered only two zappers, one at Stew Leonard’s Dairy in Norwalk, Connecticut,where$17millionincashwasskimmed,11andtheotherattheLaShishrestaurantchaininDetroit,Michigan,wherecashsalestotalling$20millionwerezappedandallegedlysenttoHezbollahinLebanon.12ThereasonforthislowenforcementrateisthattheUSauthoritiesarehamperedintheirapproachtozappers.Federalincometaxauditsarenotcoordinatedwithstateandlocalretailsalestaxaudits,sotheauditsarenotcomprehensiveintheDutchsense.Inaddition,federalcomputerauditspe-cialistsarenotnormallyassignedtoauditsofsmallandmedium-sizedenterprises(SMes),andthisiswherethezappersare.

Nevertheless,iftheUnitedStatesbecameseriousaboutthisproblem,itmighthaveauniqueblendofrules-andprinciples-basedsolutionsinanextensionoftheStreamlinedSalesandUseTaxAgreement13(SSUTA).UndertheSSUTA,certifiedthird-partysoftwareproviders(CSPs)14couldbetaskedwithassuringeCRaccuracy.NotonlyistheSSUTAlegalframeworkoperational,butatpresentlevelsoftech-nology,aCSPcouldreadilyassurestatesthatthecorrectretailsalestaxwasbeingcollectedandremitted.At thesametime, itcouldassure federalauthorities thatzappers were not being used to underreport income. CSPs indemnify both sides

11 TheLeonardcasecameaboutwhenaUScustomsofficerinspectedasuitcasecarriedbyMr.LeonardononeofhistripstoSt.Martin:United States v. Leonard,37F.3d32,at35(2dCir.1994);aff ’d.67F.3d460(2dCir.1995).Detailsofthetaxfraudarepreservedintheappealsofthesentence.

12 UnitedStates,DepartmentofJustice,easternDistrictofMichigan,“LaShishFinancialManagerSentencedto18MonthsinPrisonforTaxevasion,”Press Release,May15,2007(online:http://nefafoundation.org/miscellaneous/FeaturedDocs/U.S._v_Aouar_DOJPR_Sent.pdf ).TheLaShishfraudapparentlycametolightasaresultoftheowner’sfailuretofileataxreturn.“Authoritiesdeclinedtocommentonhowthereportedcrimewasdiscovered,butaccordingtocourtrecords,Mr.Chahinefailedtofileataxreturnin2003”:RoyFurchgott,“WithSoftware,TillTamperingIsHardToFind,”New York Times,August20,2008(online:http://www.nytimes.com/2008/08/30/technology/30zapper.html).

13 StreamlinedSalesTaxGoverningBoard,StreamlinedSalesandUseTaxAgreement,adoptedNovember12,2002,amendedNovember19,2003,andfurtheramendedNovember16,2004(hereinreferredtoas“theSSUTA”).

14 SeeSSUTAsection230,definingacertifiedsoftwareprovideras“[a]nagentcertifiedundertheAgreementtoperformalltheseller’ssalesandusetaxfunctions,otherthantheseller’sobligationtoremittaxonitsownpurchases”(online:http://www.streamlinedsalestax.org/uploads/downloads/Archive/SSUTA/SSUTA%20As%20Amended%2009-30-09.pdf ).

quebec’s sales recording module (srm) n 723

(governmentandtaxpayer)againstloss.15CertificationoftheCSPwouldneedtobeundertakenjointly(bystateandfederalagencies),aswouldoversightoftheiroper-ation.QuebechasnotconsideredanSSUTA/CSPsolution,butitmightneedtolookatthisoptionifitplanstoextendtheSRMoutsidetherestaurantsector.

s truc t ure o F o ur A rgument

Thisarticlemovesbeyondadiscussionofthevarietyofsalessuppressionprogramsinuse—zappersandphantomware.16Itgoesbeyondadiscussionoftheeconomicimpactthatthiskindoffraudhasonlocalbusinesses,17andsidestepsaspeculativeinquiryintowherethemoneyfromthisfraudultimatelygoes—intothebusinessorinto the owner’s pockets.18 Those matters have been considered elsewhere. Ourconcernhereisonenforcementefforts,particularlytheSRM.Theintentistoassess

15 UndertheSSUTA,aCSPneedstoprovideasuretybondtoreceiveacontractfromthegoverningboard.Someenterpriseswillalsotakeoutaninsurancepolicy.

16 Fordiscussionoftheseprogramsandpossiblecountermeasures,seeRichardT.Ainsworth,“ZappersandPhantomware:TheNeedforFraudPreventionTechnology”(2008)vol.50,no.12Tax Notes International1017-29;RichardThompsonAinsworth,“ZappersandPhantomware:AreStateTaxAdministratorsListeningNow?”( July14,2008)vol.49State Tax Notes103-15;RichardThompsonAinsworth,“Zappers:Technology-AssistedTaxFraud,SSUTA,andtheencryptionSolutions”(2008)vol.61,no.4The Tax Lawyer1075-1110;andRichardT.AinsworthandHirokiAkioka,“electronicTaxFraud—AreThere‘SalesZappers’inJapan?”(2009)vol.11Kansai University Review of Economics1-34.

17 Thereisevidencethatthepresenceofazapperinthelocaleconomyhasadirectcompetitiveimpactonotherbusinessesinthearea,aswellasanimpactonenterprisesthatselleCRstoretailingbusinesses.Inapersonale-mailcommunication,February11,2008(onfilewithR.T.A.),MichaelO’Sullivan(ahearingofficerintheStateofConnecticutDepartmentofRevenue)indicated,“Myonlyrecentinstancethatinvolveda‘zapper’likeproductwasananonymouscallmyofficereceivedfromsomeoneinthecashregisterbusinesslookingforinformationonfilingacomplaintagainstacompetitor.Apparentlythecallerwasattemptingtomakeasaleatarestaurantandwasinformedthatanothercompanyattemptingtosecurethesamesalehadofferedtoinstallsuchaprogramintheregisterifhe/shewasgiventhesale.Thecallerdidnotelaborateastowhotheothersalespersonwasemployedbyoranyspecificsabouttheworkingsoftheprogram.Wedirectedtheindividualtoourspecialinvestigationsection.”ThesameobservationhasbeenmadebyGermaninvestigators:“Tillmanufacturersconfirmthatcustomersenquireaboutsuch[salessuppression]functions[ineCRs],andthattheyinfluencecustomerpurchasingdecisions.”SeetheGermanWorkingGrouponCashRegisters,Interim Report,March16,2005,citingBRHcomments2003,no.54,FederalParliamentcircular15/2020,November24,2003(original,inGerman,andtranslationonfilewithR.T.A.).

18 Theeconomicsofwherethemoneyfromskimminggoesisdifficulttoassess.Itmostlikelydependsonthepersonalmotivationsofthefraudster.Forexample,intheskimmingfraudatAleefGaragenewsstand/conveniencestoresintheUnitedKingdom,theskimmedfundswenttounder-the-tablepaymentstomorethan250workers.Becauseregularwageswereverylow,allowingemployeestoqualifyforwelfare,cashfromskimmingbecameanecessarysupplementforworkerretention.HMRevenue&Customs,“CompanyDirectorsJailedfor£5millionFraud,”News Release,November13,2007(online:http://nds.coi.gov.uk/clientmicrosite/Content/Detail.aspx?ClientId=257&NewsAreaId=2&ReleaseID=330199&SubjectId=36).Then

724 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

theanticipatedworkabilityandeffectivenessoftheSRMsolutionbycontrastingitwithsolutionsadoptedorunderdevelopmentinotherjurisdictions.

Wewillfirstpresentaroughschematicofhowazapperfacilitatesaskimmingfraud.Thenwewillconsiderthreerules-basedenforcementapproaches—theGreek“fiscalelectronicdevices”(FeDs),theQuebecSRMs,andtheGerman“smartcards.”NextwewillexaminetheDutchprinciples-basedapproach,whichisalsofavouredbytheUnitedKingdom.Finally,wewillconsiderhowCSPsinanSSUTAframeworkcouldbeusedtoachievesimilaroutcomesunderablendedrules-based/principles-basedapproach.Comparisonswillbemadethroughout.

schem Atic o F sK imming with Z A PPer s

TherearesixbasicstepsthatoccurinasalestransactionwhenacustomermakesacashpurchasefromabusinessusinganeCR:

1. Aconsumeridentifiesgoodsorservicesforpurchase. 2. Acashier,waiter,orothersalesassociatecreatesaproformabill19andpres-

entsittotheconsumerforapproval.20(Thisstepisnotalwayspresent.) 3. Theconsumerapprovesandofferstopayincash,21andtheproformabillis

finalized(agreedupon). 4. Thecashier“ringsup”thesaleintheeCR,whichgeneratesanitemizedrecord

ofeachgoodorservicesold.

again,asnotedabove,intheLaShishfraudinDetroit,azapperwasusedtoskimcashand(allegedly)sendittofundHezbollahterroristsinLebanon.UnitedStates,DepartmentofJustice,easternDistrictofMichigan,“SupersedingIndictmentReturnedAgainstLaShishOwner,”Press Release,May30,2007(online:http://www.justice.gov/tax/usaopress/2007/txdv072007_5_30_chahine.pdf ).Inyetanotherinstance,thistimeintheAustraliancaseRegina v. Ronen and Ors,2005NSWSC991,thezappersinstalledinaused-clothingstoreprovidedfundsthatwerewiredtotheowner’spersonaloverseasbankaccounts.

19 Thismayoccurbyscanningabarcode,directlyenteringaPLU(pricelookup)number,orenteringthenameofanitem(perhapsbypressingatouchscreen).

20 Inarestaurant,ifacustomerordersdirectly(andonly)fromthemenupresentedbythewaiter,theproformabillmaybefirstdraftedinpencilandthentransferredtoadigitalorderingsystemassociatedwiththeeCR.Inotherinstances,acustomermayinitiallyorderadrinkandanappetizerandthenplaceadditionalordersforfoodanddrinkthroughouttheevening.Thewaiterwillkeeparunningtallyofthebill.Itwouldbecommoninthiscasetopresentoneormoreproformabillsatvarioustimestokeepthecustomerawareofthetotalamountdue.

Inagrocerystorecontext,anitemizedproformabillingisfrequentlyvisibleonanLCDscreenthatthecashierandthecustomercanseeasitemsarerunthroughascanner.Somesupermarketstodayequiptheirshopperswithahandscannertopre-scanallpurchasesbeforearrivingatthecheckout.AllmoderneCRshavethecapabilitytopresentthisproformabillbothformallyandinformally.Theimportantpointisthattheproformabillcanbechangedbeforethesaleis“rungup.”Changesoccurasaresultofthecustomerandtheoperatoractinginconcert.

21 Zapperstargetcashsalesbecausecredit,debit,cheque,orbanktransfertransactionsleaveanaudittrail.

quebec’s sales recording module (srm) n 725

5. TheeCRthendirectstheprintertoissueapaperreceipt(invoice)forthecustomer.UndertheSRM(andotherfiscaltillsystems),thisistobeaverydetailedreceipt,whichwillincludea. alistoftheitemspurchased;b. apriceforeachitem;c. ataxabilitydeterminationforeachitem;d. asegregatedtaxamountforeachofthetaxeditems(ininstanceswhereall

itemsatanestablishmentaretaxed,andtaxedatthesamerate—astheywouldbeatarestaurant,forexample—thisfunctionwillbeperformedinaggregate);

e. theamountofcashtendered;f. thenetamountreturnedtothecustomerinchange;g. thedateandtimeofpurchase;h. thename,address,andidentificationnumberofthevendor;andi. thereceipt(invoice)numberofthetransaction.

6. Attheendoftheday,aseriesofelectronicreportsisgenerated,basedontransactionssentthroughtheeCR.22Thesereportsarereliedonbycompli-anceauditors.Thereportsarea. thedailyZreport(withresetfunctionality);23

b. thexreport;24andc. theelectronicjournal.25

22 Itisimportanttonotethatthefraudweareaddressingisa“backroom”issue.Wearenotsomuchconcernedwiththefalsificationofimmediatereal-timerecordsaswiththealterationofrecordsattheendoftheday.Seeinfranote26andtherelatedtextforfurtherdetailsofthispractice.

23 Oneofthemostimportantfunctionsofacashregisteristorecordthedetailsofdailytransactions—sales,taxescollected,mediatotals,discounts,voids,andmore.Thereportprintedattheendofthedayorshiftthatcontainsthisinformation,andresetstherecordforthenextdayorshift,isknownasthe“Z”report.TheZreportfunctionprintsthesalesonthecashregistertapewhileerasingthedatafromthememory.AZreportisaonce-onlyreportforasetperiodoftime.ManycashregistershaveaZ2featurethatallowsZreportstobeaddedtogether.Whenanoperator“Z2’sthemout,”thesereportsareerasedforalongerperiodoftime.Anexampleofa“Z2”reportisamonthlyreportthatwillbeusedtodateandrecordmonthlycashregistersales.everytimetheregisteris“Z’dout”(Reporttaken),thattotaliserasedfromthedailysalesfilesandaddedtothe“Z2”file.

24 xreportsareidenticalininformationandtimespantoZreports.xreportsonlyprovidereports;theydonotresetorclearthememory.xreportscanbetakenasoftenasneededwithnoeffectonsalesdatarecorded.

25 See“CashRegisterGoodPracticeGuide,”supranote6,appendixG,atparagraph1.2:“TheelectronicJournalusuallycontainsALLtransactionskeyedintothemorecomplextypesoftillsystemsandisthereforethedefinitiverecordtoobtainforauditpurposes.(Thereareexceptions,whereelectronicJournalscanbeprogrammed‘not-to-store’certainkeyingtransactionse.g.‘TrainingMode.’)”TheelectronicjournalshouldnotbeconfusedwiththeZreport—itisnotarecapoftheday’ssales.Theelectronicjournaltapeissupposedtobeacontinuous,step-by-steprecordofeverytransactionmade.Itismostusefulforgoingbackduringadaytolookformistakesthatweremade.Thisjournalhasbeenastapleintheelectroniccashregisterindustrysincethebeginning.ItcanbeusedtochecktheZreport.

726 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

If,afterstep6,azapperisinsertedintheeCR,orinthepoint-of-sale(POS)system,aseventhstepisaddedtothesequence.ThezapperallowstheusertoeliminatefromtheeCRandtheenterprise’sbusinessrecordsalltracesof(someorall)cashsaleswithoutfearofleavingadigitalrecordofthemanipulation(assumingtheab-senceofananti-frauddevice).Phantomwareapplicationswoulddothesamething,exceptthattheirprogrammingisembeddedintheeCR’soperatingsystem,nottem-porarilyaddedandthenremovedfromtheeCR.

Atthispoint,thecustomerhasinhishandsanaccuratereceipt(fromstep5),but(attheendoftheday)thezapperwillrewritetheinternalmemoryofthisreceiptinthe eCR—including the records in the Zreport, the xreport, and theelectronicjournal.This rewritingcreatesanewsalesprofilewithin theeCR.Selectedcashsalesareomitted.Forexample,inticketfiles(thedigitalrecordofspecificinvoicesissuedinsequence),thefilewouldberenumberedifanentireticketwereelimina-ted.Ifonlysomeitemsareremovedfromsometickets,orifthepriceofanitemischangedonaspecificticket,theamountsduewillberecalculated(andanewtaxduedetermined).ThealteredticketfileswillnowconfirmthealteredZreport,xreport,andelectronicjournal.TheeCR’srecordswillnotmatchcustomerreceipts,buttherecordsoftheeCRwillbeinternallyconsistent.26

Thus,oneofthecommon(traditionalaudit)approachestodetectingazapperisforanauditteamtovisitanestablishmentsuspectedofusingasalessuppressionde-vice(inadvanceoftheaudit),makecashpurchases,savethereceipts,andthentrytomatchthereceiptswiththedigitalfilesintheeCR.ThisisinfacthowRevenuQuébecuncovereditsfirstzapperin1996.27

Thenextthingtonoticeisthatitiseasytoskimsaleswithoutzapping.Thiscanbedoneatstep2,butitrequirescollusionbetweenthevendorandthecustomer.Aconsumertenderingcashcouldbeorallyofferedalowerprice(perhapsatax-free

26 Anti-fraudtechnologysuchasQuebec’sSRMandGermany’ssmartcards(discussedbelow)isnotdesignedtoeliminateallskimmingbutonlytopreservetherecordsofthetransactionsthatmakeittostep5.Theproblemofthezapperhasnotbeenthereal-timeskimmingfraudthatoccursatthecashregisterasthecustomerpays,butthefraudthatoccursinthebackroomaftertherestauranthasclosedfortheevening.Atthispoint,thezappergoesinandmanipulatestherecordstoallowthefraudstertomakethemlook“good.”Thereiscommonlysomestrategythatthefraudsterusestomakereceiptsnormal.Thus,azapperwouldbeusedonanightwhenanexceptionallylargeamountofcashhadbeentakenin.Iftheaveragedailycashtakewas,say,1,000eurosordollars,andinoneday10,000wasreceived,thenitwouldbeagoodtargetdayforazapper.However,adaywhencashreceivedwaslow(500,forexample)wouldnotbeagoodtargetday.Informationprovidedinpersonale-mailcommunicationswithMarcSimard,September15,2009andNorbertZisky,November18,2008(bothonfilewithR.T.A.).MarcSimardisthedirecteurdelarechercheentechnologiesliéesaucontrôlefiscal,RevenuQuébec;NorbertZiskyiswithGermany’sNationalMetrologyInstitute,orPTB(Physikalisch-TechnischeBundesanstalt).

27 Ainsworth,“ZappersandPhantomware:AreStateTaxAdministratorsListeningNow?,”supranote16,at104,note5.

quebec’s sales recording module (srm) n 727

price)whentheproformainvoiceisdrafted.Ifthecustomeragrees,thesaleissimplynot“rungup.”Asaresult,norecordoftheactual(finalized)transactionwillappearinthedailyZreportorthexreport.

Itispossiblethattheelectronicjournalmightpreservea“trace”oftheoriginaltransaction(iftheproformawasdraftedwiththeassistanceoftheeCR).Thetrans-actionwouldappearasanabortedsale.Itwouldlooktotheauditorasifthecustomerhaddeclinedthepurchasewhenshesawtheproformainvoice.Inarestaurantcon-text,multipleabortedsalesmightraisesuspicions,becausenormallythemealwouldalreadyhavebeenconsumed.However,inagroceryorconveniencestore,ahair-dresser’s,orabutcher’sshop,wherethecustommightbetodiscussatransactionbasedonaproformainvoice,abortedsalesmightnotsuggestthatanythingisamiss.

Somefiscaltilljurisdictionstrytoblockfraudsatstep2bypreservingeachkey-strokeintheelectronicjournal.ThesejurisdictionscertifyeacheCR.Tamper-proofelectronicjournalsaremadearequirementofcertification.

Anotherthingtonoticeisthatthereisaperiodoftime(afterthesaleiscomplet-edatstep3andbeforethezapperisinserted)whentherecordswithintheeCRarecompleteandaccurate.Thisperiodlastsatleastuptostep5—thepointwheretheeCRdirectstheprintertoissueaninvoiceforthecustomer.Theserecordsneedtobeaccuratebecausethecustomerwilldemandanaccurateinvoice.

Asaresult,manyfiscaltilljurisdictionsfocusonpreservingtamper-proofinvoices,andthesequencingofthoseinvoicesatstep5.ThisiswhattheSRMdoes.TheSRMmakeseveryreceiptusefulforcheckingtheeCR.Forexample,evenacreditcardtransaction(whichwasnottamperedwith)canprovideevidenceofmanipulation,ifan auditor can tell that the receiptwas renumbered.The SRMwill indicate thatsomeotherreceiptfurtherupthechainismissing,andanauditorwouldthenbeginthesearchforthemissingcashtransactions.

Principles-basedjurisdictionsfocusonthissamepoint,step5,buttheyneedtodirectlyfindanalteredreceipt.WithoutanSRM(orsimilardevicethatusesselectdataonthereceipttoderiveasignaturethatisprintedonthereceipt),itisdifficulttotellifasequenceofreceiptshasbeenmanipulated.Thismakespre-auditcashpurchasesand savedreceiptsacritical componentofaprinciples-basedauditor’sworkplan.TracesofazappercanalsobefoundbycomputerspecialistsexaminingtheelectronicjournalaswellasthexandZreportsproducedatstep6.

Afinalthingtonoticeisthatallcriticalelementsofthetaxreturn(atleastallele-mentsthatwouldbederivedfromaspecificeCR)areavailableatstep5.Theitemspurchased (step5a), the price charged (step5b), the taxability determination(step5c),andthetaxcollectedperitemorperinvoice(step5d)areallavailable.Inaddition,thecustomerhaspaidthetax.

Thus,itisentirelypossiblethatfiscaltill jurisdictionscouldrequirereal-timeproformareturnsbasedonthesefigures.Theycouldalsorequirereal-timeremissionofthetax.Inaretailsalestaxjurisdiction,thevendormightberequiredtoremittheentirereturnandpayment.Inavalue-addedtax(VAT)jurisdiction,theremittancewouldrepresentonlytheoutputportionofthereturn.TheinputVATcredits(de-ductions)wouldneedtobegatheredfromotherfiles.

728 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

Fisc A l till s: greece , Quebec , A nd ger m A n y

InadditiontoGreece,Quebec,andGermany,fiscaltilljurisdictionsincludeArgentina,Brazil,Bulgaria,Italy,Latvia,Lithuania,Poland,Russia,Turkey,andVenezuela.28ThediscussionthatfollowssetstheGreekandGermanregimesalongsideQuebec’sSRMinordertoilluminatetheattributesofthisnewanti-fraudtechnology.

Greece: Fiscal Electronic Devices (FECRs, AFED Printers, and FESDs)

Greecehashadcomprehensive,rules-basedfiscaltilllegislationinplaceforover20years.Technicalspecificationsforfiscalelectronicdevices,orFeDs,werepublishedwidelyin2004.29Whenconsideredasawhole,theserulesattempttoprovidedatasecurityatbothstep2andstep5ofthetransactionsequence.Inotherwords,theGreekapproachistosecuredatawhentheproformareceiptisbeinggenerated,andwhentheprinterisbeingdirectedtoissuethefinalreceipt.

UnderGreekrules,FeDsaredividedintotwocategories:(1)fiscalelectroniccashregisters (FeCRs),whichareaccompaniedbyautonomousfiscalelectronicdeviceprinters(AFeDprinters);and(2)fiscalelectronicsigningdevices(FeSDs).ThefirstareusedonlyinB2Ctransactions;thesecondmaybeusedineitherB2CorB2Btrans-actions.Bothpreservedigital“fingerprints”30ofdatafromtax-relateddocuments.

28 See“CashRegisterGoodPracticeGuide,”supranote6,appendixD,atparagraph1.

29 Aeuropeandirective(98/34/eCofJune22,2998)requiresthatwheneveramemberstateadoptsnewtechnicalrules,specifications,orlegalrequirements,thatstateisobligedtoannouncethistotheeuropeanUnionbeforetherulestakeeffect.Accordingtothisdirective,thereisaminimumstandstillperiodofthreemonths.Duringthisperiod,anymemberstate(ortheeuropeanCommission)hastherighttoexpressa“detailedopinion.”Theissuanceofadetailedopinionextendsthestandstillperiodforanotherthreemonths,allowingforfurtherconsiderationoftherulesbyallparties.GreecemadethetechnicalspecificationsforFeDspublicin2004.Asaresult,theGreekrulesarewellknownnotonlywithintheeuropeanUnionbutalsoamongthelargercommunityofeCRmanufacturersanddistributors.TherulesareavailableinGreekandinofficialtranslationsinenglish,French,andGerman,andcanbeaccessedontheInternet:“Codificationof/AddendatoTechnicalSpecificationsforInland-RevenueApprovedRegistersandSystems(OperatingProcedures)”(online:http://ec.europa.eu/enterprise/tris/pisa/app/search/index.cfm?fuseaction=pisa_notif_overview&iYear=2004&inum=135&lang=eN&sNLang=eN).

30 Atthispoint,itisnecessarytodefinetwokeytermsinthelanguageofcryptography:“digitalfingerprint”and“digitalsignature.”Adigitalfingerprintisastringofcharacterscomputedwithacryptographic(oropenmathematicalone-way)functionappliedtoaparticularsetofdata.Itisofconstantsize(20bytesiscommon)andcollusion-resistant(thatis,itisveryunlikelythattwodatasetswiththeidenticalfingerprintcanbefound).Adigitalsignatureisdifferent.Itiscomputedbyacryptographicfunctionthatisappliedtothedigitalfingerprint;thus,itisastepremovedfromtheoriginaldata.Inaddition,adigitalsignaturemakesuseofaprivatekey(knownonlytotheentitycomputingthesignature)andapublickey(availabletoanyone).Anyonecantakethepublickeyanduseittodeterminewhethertheentityusedthecorrespondingprivatekeytocreatethedigitalsignature.

ItisimportanttorecognizethisdistinctionbecausetheGreeksystem(informaldocuments,namesofequipment,andpublicpresentations)frequentlyusestheterm“signature”inreference

quebec’s sales recording module (srm) n 729

FECRs and AFED Printers“Fiscalelectroniccashregister”isatermthatincludesordinarystand-alonecashregistersandcashregistersequippedwithadvancedconnectioncapabilities (net-workorPC-operatedmachines).“Autonomousfiscalelectronicdeviceprinters”arefiscalprintersthatoperateonlyviaaconnectedcomputer.Theyhavenokeyboardordisplayterminal.Theydomorethanjustprintreceipts,however.AFeDprintersstoreandsecureintheirfiscalmemorythedatathathavepassedthroughthem(rev-enuefromsales,taxescollected,etc.).31

totheproductionandstorageofdigitalfingerprints.Thus,theFeSD(fiscalelectronicsigningdevice)producesandstoresdigitalfingerprints,notdigitalsignatures,althoughthenameofthedevicemightsuggestotherwise.Greece’scontributiontothe“CashRegisterGoodPracticeGuide,”supranote6,appendixD,atparagraph4.2.15,usesbothtermsinterchangeably:

TheFeSDreceivesthisdata,processesitwithaspecialsecurityalgorithm(SHA-1)thatcreatesahashvalue(sign)andsendstheresultofthisprocessingbacktotheconnectedcomputer.Thehashvalue,whichrepresentsasequenceofcharactersanddigitsistheuniqueelectronicdigital “fingerprint”ofthedataoftheslipbeingissued.FurthermoretheFeSDsavesthishashvalueinto[its]ownworkingdailymemoryandissuesarelevantslip....ThesupportingsoftwareoftheFeSDwhichislocatedintheconnectedcomputerreceivesthis“uniquesummary—signature”i.e.hashvalueandprintsitalongwiththeotherdataoftheissuedslip....[At]theendofthedaytheFeSDprocessesallthestoredhashvaluesoftheworkingdailymemory,producesageneraldailyhashvalueofall“summaries—signatures”oftheday,issuesa“Z”dayreportslip,onwhichthegeneraldayhashvalueiswritten....Thecomputersoftwarereceivesthisuniquegeneral“daysummary—signature”hashvalueandsavesitinaspecialelectronicfile....[Thereisalso]aDailyFiscalSigningRecordReportSlip—“Z”(DFSRRS)[and]DailySummary—SignatureSlip—(DSSS)[emphasisadded].

SeealsothePowerPointpresentationofPanosZafiropoulosattheNovember2007eUFiscalisexchangeProgram,“SafeguardingelectronicTaxData:DataLocking,‘Fiscal’electronicSigningDevices,”3,7,8,and10(onfilewithR.T.A.)(discussingthe“e-sign”process,“previousdaywholesignature,”“daywholesignature,”“formationofthesignaturestring,”“signaturestring(trace),”and“safeguardinge-signaturetraces,”whereineachinstancethediscussionisaboutdigitalfingerprints,notdigitalsignatures);and“Codificationof /AddendatoTechnicalSpecifications,”supranote29,paragraphs5.5and5.8(statutorydiscussionof“signing”process,butmeaning“fingerprinting”)inthesamecontextasabove.PanosZafiropoulosrepresentstheGreekrevenueauthorityontheFiscalisCommittee’sCashRegisterProjectGroup.Seeinfranote32andtherelatedtextforfurtherexplanationofthesecurehashalgorithm(SHA-1).

31 TheFeCRandAFeDprintermustbeequippedwitheitheratwo-rollpaperprintingstation,oraone-rollpaperslipprinterstationaswellasadailyelectronicjournal(eJmemory).eJmemoryisdifferentfromfiscalmemory.eJmemorystoresallinformationslipsandtickets(“legalreceipts”)fromtheissuanceofthepreviousZreportuntiltheissuanceofthenextZreport.Itissometimescalledthetemporarydailyslipstoragememory(TDSSM).“Fiscalmemory,”ontheotherhand,isthebasicsecureelementintheGreeksystem.ItisbasedonaprogrammableROM—readonlymemory—(ePROMorPROM)chipthatissecurelyplacedwithinthefiscalcashregister.Itisinthismemorythatallimportantfiscaldataarestored.eJmemoryiseitherpluggable/unpluggableorfixed.Itresidesinthefiscaldeviceandisalwaysaflashmemory.See“Codificationof/AddendatoTechnicalSpecifications,”supranote29,atparagraph2.11.Inapersonale-mailcommunication,August10,2009(onfilewithR.T.A.),

730 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

Adigitalfingerprintofthedatafromtheelectronicjournalmemory(eJmemory)iscomputedwithasecurehashalgorithm(SHA-1).32Thishashvalueispermanentlysafeguarded33 and stored in the fiscal memory. Daily sums (receipts and VATamounts)aresavedintothefiscalmemory,cumulativelyandonadailybasis.Thisfunction essentially preserves the x and the Z reports along with the electronicjournalwithdigitalfingerprints.34DisconnectinganyGreekdevice(inanefforttopreventatransactionfrombeingrecorded,ortoswitchdevices)willsealthedevice

PanosZafiropoulosconfirmed,“ThetypeoffiscalmemoryisROMbased,butwhatit[sic]isusedis[a]One-TimeProgrammable(OTP)ROMorUVerasableProgrammable(eP)ROMchip.Thisiswhythischipshallbeprotectedandcoveredbyspecialepoxyglue,insuchmannerthat[it]isimpossibletotakeitout(orreplaceit)withoutbreaking/destroyingthecasecover(theenclosure)oftheFiscalelectronicDevice.”

Securityforthefiscalmemoryisprovidedbyplacingthecircuitsinaspecialboxthatisplacedinaspeciallymodulatedreceptacle;theboxisanintegralpartofthemachine.AsdescribedbyZafiropoulos,thisfiscalmemoryboxisclampedandsealedwithanepoxyresininsuchawaythatremovalofthetaxmemoryboxisimpossiblewithoutdestroyingthecover.Thepreservationofdataisindependentofanypowersource.“CashRegisterGoodPracticeGuide,”supranote6,appendixD,atparagraphs4.1,4.2.14,and4.3.6;and“Codificationof /AddendatoTechnicalSpecifications,”supranote29,atparagraphs2.11.4(includingatechnicaldiagramofthesealedbox)and2.17(specifyingthecasing,casingelements,andcasingseals).

32 Thesecurehashalgorithm(SHA-1)wasdevelopedbytheUSNationalInstituteofStandardsandTechnology.SHA-1isawidelyacceptedcryptographichashfunction.Itproducesa40-characterstringbyhexadecimalsymbols(20bytes),andthestring(orthe“hashvalue”)uniquelydefinestheprocesseddata(inthecaseofaneCRissuingreceiptsinB2Ctransactions,thesedataarethevaluesontheprintedreceipt).SHA-1isdescribedindetailintheFederal Information Processing Standards Publication180-2,“AnnouncingtheSecureHASHStandard,”August1,2002(online:http://csrc.nist.gov/publications/fips/fips180-2/fips180-2.pdf ).

33 “CashRegisterGoodPracticeGuide,”supranote6,appendixD,atparagraphs4.3.1and4.3.2,specifiesthephysicalsecurityprecautionstaken:

4.3.1. Special security screwAccesstotheinsideoftheFCR[fiscalcashregister]isprotectedbyaspecialsecurityscrewconnectingtheupperpartoftheFCRwiththelowerpart.Thisscrewisfittedina...partofthemechanismcover[thatisvisibletotheclient].AccesstotheinsideoftheFCRisimpossiblewithouttheremovaloftheprotectivescrew.Forthesealingadesignatedmaterialisused(ex.Leadseal),whichdoesnottoleratescrapingsanditiscarriedoutinsuchawayastomake[it]impossibletoremoveitwithoutdestroyingit.

4.3.2. Authorized technicians - Access control codeOpeningandre-sealingcanbecarriedoutonlybyanauthorizedtechnicianofthesuitabilitylicenseholder,employedfortherepairingofmalfunctions.TheFeDfirmwarecontrols,throughaspecial algorithm—access code-password,theaccessofauthorizedtechnicianstoit[emphasisinoriginal].

34 Seeibid.,appendixD,atparagraph4.2.15,discussingthedailyfiscalsigningrecordreportslip—“Z”(DFSRRS)andthedailysummary—signatureslip(DSSS).Seealso,ibid.,adiscussionoftheperiodicalsummaryofmemoryreadingslip(PSMRS),whichisalsopreserved:“Note:Thekeepingofthestoredfiledofrequireddataofthesigningprocessisregulatedbythesameconditionsasthekeepingoftheelectronicjournal,mentionedearlier.”Notethatthereferenceto“thesigningprocess”shouldinsteadread“digitalfingerprintingprocess.”

quebec’s sales recording module (srm) n 731

inlessthan30seconds;anillegalreceiptmessagewillprintandwillberecordedonthetaxdataZregister;andafter10disconnect/reconnectefforts, thedevicewillautomaticallyshutdown.35Thisprocesstiesincloselywithapenaltyregime(ap-pliedagainstmanufacturers/distributorsofeCRsandretailers)thataimstodeterthesaleoruseofuncertifieddevices.36Anauthorizedtechnicianwithanaccesscontrolcodewillbeneededtorestorethedevice.37

ThecostofFeCRsvariesfrom�200-250to�800-1,000,dependingonthemanu-facturer.38everymanufacturer,developer,orimporterofaneCRintoGreecemustseekapprovalforeachspecificmodelthatitintendstosellintheGreekmarket.39AlicencetosellaspecificeCRisissuedbyaspecialtechnical(interparty)40body(com-mittee)andwillbeissuedonlywhentheeCRconformstoallstatutorytechnicalspecifications.41ApplicationsaremadetotheDepartmentofFiscalelectronicCashRegistersandSystemsoftheMinistryofFinanceandmustbeaccompaniedbyaworkingmodelofthesystemforwhichalicenceissought.Thecommitteehastheauthoritytoexamineanyadditionaldata(includingexperienceinthefield,businesssolvency,creditworthiness,andthetechnicalcapacityofpersonnel),andtheauthor-itytorecallandcancellicencesincaseswherematerialchangeshavebeenmadeinsystemsorintheconditionsunderwhichthelicencewasgranted.

Onceamodelhassuccessfullypassedalltests,thecommitteegivestotheinter-estedcompanyauniquelicencenumberforthespecificmodel.ThelicencenumberisrecordedbytheNation-WideInformationCenteroftheMinistryofFinanceandisprintedoneachreceipt(“legalreceipt”)issuedineachretailtransaction.Inaddition,thisnumberisrequiredtobeplacedonalabelthatisvisiblyfixedtoeachmachine.Asaresult,thecertificationofaspecificeCRcanbecheckedboththrough

35 “Codificationof/AddendatoTechnicalSpecifications,”supranote29,chapter3,atparagraph7.10,disconnection(discussingblockingofthedevice[7.10.2];recordsofthedisconnectionretained[7.10.3];theless-than-30-secondsrule[7.10.4];whathappenstoatransactionthatisinprocesswhenthedisconnectionoccurs[7.10.5];andrecordskeptintheZregister[7.10.6]).

36 “CashRegisterGoodPracticeGuide,”supranote6,appendixD,atparagraph4.2.1.

37 Seesupranote33,paragraph4.3.2.

38 PanosZafiropoulos,personale-mailcommunication,February24,2008(onfilewithR.T.A.).

39 Thereareroughly300,000to350,000FeCRsandPOSsystemswithsecurerecordingdevices(FeSDs)inGreece.Theturnoverofthesedevicesisbetween30,000and40,000machinesannually.Thereareover300differentmodelsofeCRscertifiedforuseintheGreekmarket,representingapproximately50differentmanufacturers,importers,anddistributors:“CashRegisterGoodPracticeGuide,”supranote6,appendixD,atparagraph4.1.

40 AninterpartybodyunderGreekrulesisacommittee,eachmemberofwhichisassignedbyoneofthepoliticalpartiesintheGreekParliament.Althoughthetermofofficeisfortwoyears,thecompositionofthecommitteewillchangeaspoliticalpowershiftsinGreekelections.

41 Technicalspecificationschangewithadvancingtechnology,andrevisionstothelawaremadeeverytwotofouryears.GuidanceonthesematterscomesprimarilyfromspecializedlaboratoriesoftheNationalTechnicalUniversityofAthens(NTUA).TheNTUAisalsoassignedbythecommitteetoperformallthenecessaryevaluationtestsoncarriedsamplesofFeCRs.

732 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

avisualinspectionofthemachineandbymatchingthelicencenumberonthema-chinewithagivenreceipt.

FESDsUnderGreekrules,abusinessownercanchoosetouseeitheranFeCR(anordinary,inexpensivecertifiedcashregister)oranFeSD.IfanFeSDisselected,itprobablymeansthattheownerhasthecapabilities,thetechnologyskills,orabudgetalloca-tionthatwouldallowtheuseofasophisticatedcomputersystem.

FeSDsaredesignedforB2Bapplications.Theyareusedprimarilytocomputeadigitalfingerprint42ofcriticaltaxdatathatisthenprintedontheinvoice.FeSDscanbeusedforanytaxdocument,includingafinalretailreceipt.TheFeSDisconnectedto thebusiness’s computer systemvia adedicatedport (RS-232;ethernet RJ-45;USB).AdrivermustbeinstalledtoallowthecomputersystemtointerfacewiththeFeSD.essentially,theFeSDfunctionsasavirtualprinter,allowingtheback-officesoftware(eRPsystemoraccountingsoftwarepackage)tofunctionnormally.How-ever,everytaxdocumentrequiredtoberecordedisdivertedthroughtheinterfacetotheFeSD,whereadigitalfingerprintiscreated(theSHA-1algorithmisapplied)andafingerprintistransmittedto(andprintedon)eachdocument.Thewhole-dayfingerprintispermanentlysavedintheFeSD’sfiscalmemory.43Thispreservesalldataonthedocumentindetail.44

Currently,thecostofanFeSDisbetween�450and�650;thus,anFeSDalonecancostmorethananFeCR.Forthisreason,smallerbusinessesdonotnormallyuseFeSDstoissuelegalreceipts.45economiesofscalealsocomeintothepicture,be-causeasingleFeSDcansupportmanycashregisterslinkedonanetwork.Itcanbeinstalledremotely(eveninanothercity),andneednotbedirectlyconnectedtothePOSterminal.

AnFeSDownerisobligatedtopreservefingerprinteddocumentsandtostorethemonasafedigitalmedium(opticalormagnetic).Thus,auditorscanchecktheintegrityofthesefilesbyrunningthesamealgorithm(SHA-1)andcomparinganewfingerprintagainsttheexistingonessecuredwithintheFeSD’sfiscalmemory.

42 “CashRegisterGoodPracticeGuide,”supranote6,appendixD,atparagraph4.2.15,discussingthisprocessas“signing”thereceipt,bywhichitmeansthatthefingerprintisbeingattachedtotheinvoice.ThePowerPointpresentationbyZafiropoulos,“SafeguardingelectronicTaxData,”supranote30,at2,3,7,and10,describesthisasane-signingprocess.

43 Fromahardwareandasecurityperspective,thereisverylittledifferencebetweenanAFeDprinter(withanelectronicjournal)andanFeSD.

44 PanosZafiropoulos,personale-mailcommunication,February24,2008,itemD(onfilewithR.T.A.).

45 InanefforttomitigatethecostofFeSDs,thetaxlawallowsownerstodepreciatethesedevicesasfixedassetsoverthreeyears.ThereisalsoagovernmentloanprogramtoassistinthepurchaseofallFeDs(FeCRs,AFeDprinters,andFeSDs).Theinterestontheseloansissubsidizedat3percent.

quebec’s sales recording module (srm) n 733

How FECRs with AFED Printers and FESDs Defeat Zappers and PhantomwareBecauseFeCRsarecertifiedforcompliancewithalltechnicalspecificationssetoutinGreeklaw—alawthatissupportedandupdatedregularlybytheresearchlabora-toriesoftheNationalTechnicalUniversityofAthens—itisaverysimplemattertodeterminewhetheraspecificeCRhasbeentamperedwith.

Factory-installedphantomwaremustberemovedbeforecertification.Ifaself-helpversionofphantomware46isontheeCR,eitheritwillbeblocked,ortherewillbearecordofthemanipulationsothatitsimpactonrevenueswillbeneutralized.OnlytruedatafromrealtransactionswillbepreservedandfingerprintedwithSHA-1inthefiscalmemory.Useofanadd-onzapperwillbeaviolationofthelicensingregulations.Itwillbedetectedinthesamemannerasself-helpphantomware.Se-verepenaltiesapply,butdetectiondoesrequireanaudit.

Throughthecertificationprocess,47theMinistryofFinancepreservesacopyofallapprovedfirmware.Accordingtotheministry,48itisasimplemattertocalculateachecksumvalue(CRC-3249orSHA-1)fortheobjectcodeofthefirmware.AnyauditorcanthenreadthecontentsoftheprogrammemoryofacertifiedeCRand

46 Foradiscussionofself-helpphantomware,seeAinsworth,“ZappersandPhantomware:TheNeedforFraudPreventionTechnology,”supranote16.

47 Over400differenttypesofeCRsandPOSsystemshavebeencertifiedtodate:PanosZafiropoulos,personale-mailcommunication,May28,2008(onfilewithR.T.A.).Thecertificationprocessmeansthat

afiscalcashregisteranditsfunctionalityiscompliantwiththegivensetoftechnicalrequirements,[andthatithasbeen]testedandfinallyapproved.Acopyofitsfirmware(theobjectcode)islaiddownduringtheapprovalprocess.Achecksumvalue(CRC-32orSHA-1)isalsocalculatedfortheobjectfileofthatfirmware.

Anyonewheneverhewants(let’ssayanauditorforauditpurposes)canreadthecontentoftheprogrammemoryofatestedmachineandeasilyunderstandifthereareanychangescomparingitwiththeobjectfilewhichisoriginallykeptinthecompetentdepartment.Thisisaprocessthatofcoursecanbedone,butrequiresalittlebitmore[effort]andmorequalifiedstaff.

PanosZafiropoulos,personale-mailcommunication,July22,2008(onfilewithR.T.A.).Therequirementsforthetestingaresetoutinthe“Codificationof/AddendatoTechnicalSpecifications,”supranote29.

48 PanosZafiropoulos,personale-mailcommunication,July22,2008(onfilewithR.T.A.).

49 CRC-32,orcycleredundancycheck,takesasinputadatastreamofanylength,andproducesasoutputavalueofacertainspace,commonlya32-bitinteger.Theterm“CRC”isoftenusedtodenoteeitherthefunctionorthefunction’soutput.ACRCcanbeusedasachecksumtodetectalterationofdataduringtransmissionorstorage.CRCsarepopularbecausetheyaresimpletoimplementinbinaryhardware,areeasytoanalyzemathematically,andareparticularlygoodatdetectingcommonerrorscausedbynoiseintransmissionchannels.TheCRCwasinventedbyW.WesleyPeterson:W.WesleyPetersonandD.T.Brown,“CyclicCodesforerrorDetection,”(1961)vol.49,no.1Proceedings of the Institute of Radio Engineers228-35.AlthoughCRC-32maynotbefullysecure,becausethesamehashvaluecouldbegeneratedwithdifferentdata,circumventingtheCRCisprobably(1)beyondthetechnicalskillofmost

734 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

determinewhetherchangeshavebeenmadeinthefirmware(throughphantomwareorzappers)bycomparinghisreadingwiththatofthefilekeptintheMinistryofFinance.

FeSDsaccomplishthesameresultasFeCRs.NeitherphantomwareapplicationsnorzapperinstallationsareeffectivewhenanFeSDisinstalled.TheFeSDwillfinger-printeachdocumentandpreserveatraceinthefiscalmemoryofthedevice.Deletionormanipulationoftherecordsassociatedwithcashreceiptsisnolongerpossiblewithoutdetection.

Thus,ifaGreekvendorproducesaproformareceiptthroughaneCR,thedetailsofthereceiptwillberecordedintheelectronicjournal.IftheeCRisanFeCR,thesedataentertheelectronicjournal,andwhentheAFeDprinterissetuptocapturethedata,theywillbefingerprintedwithasecurehashalgorithm(SHA-1).Thisfea-turemakesitpossibletoidentifyenterprisesthathaveroutinelyofferedcustomerslowerpricesinexchangeforvoidingtheproformainvoiceatstep2.ThiswouldnotbepossiblewithFeSDs.FeSDsarevirtualprinters,andifdataarenotbeingsenttoaprinter,anFeSDwillhavenoneedtoe-signit.

BothoftheGreeksolutionsareveryeffectiveatstep5enforcement.Ifareceiptisprinted,boththeFeCRwithanAFeDprintersolutionandtheFeSDsolutionwillassuretaxauthoritiesthatthetaxcollectedoncashtransactionshasbeenrecorded.Itisimportanttonote,however,thatalloftheseeffortsaredirectedonlyataccuraterecordretention.Returnsmuststillbepreparedandfiled,andpaymentsremittedforthetaxesdueorcollected,andtherevenueauthoritystillneedstoaudittoen-surecompliance.Admittedly,thisauditshouldbeeasier,butitisstillneeded.50

SMes,and(2)veryhighriskforthemanufacturer,whowouldfindthatallmachinesalreadysoldandinstalledinGreecewouldlosetheircertification.

exclusiverelianceontheCRC-32maynotbewellplacedtoday.TheCRC-32wasdesignedtodealwithnoiseintransmissionchannels.Itwasnotdesignedtodealwithmaliciouspeople(see,forexample,AxelleApvrille,“TrashCRC32,”June9,2009,Fortiguard Blog(online:http://blog.fortinet.com/tag/crc32/ ).GiventheCRC-32valueofaparticularfirmware,itiseasytoproducesomeother(maybemalicious)firmwarewiththesameCRC-32value.Forexample,theWebsiteforCRC32 Compensation Tools/Library(online:http://www.cr0.org/progs/crctools/ )offersatoolthattakesafile(forexample,maliciousfirmware),anoffsetinthefile,andatargetCRC-32value(forexample,CRC-32valueofcertifiedfirmware).Ifwetakethevaluereturnedbythetoolandinsertitintothefileatthegivenoffset,theCRC-32ofthefilewillnowequalthetargetCRC-32value.

Consideringtheavailabilityofthesetools,theMinistryofFinanceshouldnotbelievethatanattackisbeyondtheskillofmostSMeowners.evenifthiswerethecase,theownerwouldnothavetoperformthisattackhimself;therecouldbeathird-partysupplierwiththetechnicalexpertisetomakeandinstallthemaliciousfirmware.Thus,usingonlytheCRC-32forensuringtheintegrityofthefirmwareisnotsecure.However,theMinistryofFinancealsohasacopyoftheactualfirmware,notjustitsCRC-32value,onfile.Theministryshouldalwayscomparethefirmwareitself.ForSHA-1,comparingthefingerprintsissufficient.Inaddition,physicalanti-tamperingmechanismsusedbytheGreekministrymakeitdifficultforathirdpartytoreplacethefirmware.

50 SeeZafiropoulos,“SafeguardingelectronicTaxData,”supranote30,at12.

quebec’s sales recording module (srm) n 735

Quebec: SRMs

QuebecisrespondingtosalessuppressionfraudmuchasGreecehasresponded,butonbothamorelimitedandatechnologicallymoresophisticatedscale.51WheretheGreeksolutionisbasedondigitalfingerprints,Quebecgoesfurtherandprovidesdatasecuritythroughdigitalsignatures.Quebechasdeterminedthattechnologicalassistanceisnecessarybecausetherearenotsufficientauditresourcestohandletheestimated500newcaseseachyear,involvingcloseto10,000delinquentvendors.52

ComparedwiththeGreekapproach,theQuebecsolution(settobefullyrolledoutbetween2010and2011)islimitedintworespects:(1)itsscopeislimitedtotherestaurantsector,and(2)itsrangeislimitedtoanFeSD-likesolution.Quebechasspecificallyrejectedthe“FeCRwithanAFeDprinter”typeofsolution.53LikeGreece,Quebecapproaches the sales suppressionproblemfromanadequacyofbusinessrecordsperspective.Butalsoliketheprinciples-basedjurisdictions(theUnitedKing-domand theNetherlands),Quebec supplements technology solutionswith veryaggressivetraditionalaudits.

Thefirstmajor legislativeresponsetozappers inQuebeccameinJune2000,whenbookkeepingandrecord-keepingrequirementswereenactedspecifyingthatelectronicallystoreddata,togetherwiththemeanstoreadsuchdata,formedpartofaQuebecbusiness’sregularbookkeepingobligations.54Becausezappersmakedigitalrecordsunreliable,itwastheneasytospecificallyprohibitthedesign,manufacture,installation,sale,orleaseofzappersintheprovince.55Thelatterisapresumption-of-userule:itprovidesthatwheneverRevenuQuébecfindsazapper,itisallowedtopresumethatthezapperwasusedtosuppresssales.56

ThebusinessrecordsthatQuebecwasprimarilyconcernedaboutweretheZandxreportsandtheelectronicjournal,aswellasallofthedigitalsupportingfilesthat

51 Quebecperformedtwoempiricalstudiesofthezapperproblem.ThefirstwasconductedsoonaftertheJune2000legislativereformscameintoeffect.Itwasa“bookkeepingandrecords”auditconductedon70enterprises.Ituncovered41zappers.Soonthereafter,thesecond,morescientificstudy(“TaxevasioninQuebec,”supranote4)wasconducted.Theuseofstatisticalsamplingtechniquesmadethissecondstudymoreaccurateandauthoritative.DaveBergeron,personale-mailcommunication,June6,2008(onfilewithR.T.A.).DaveBergeronisanITspecialistwho,since2000,hasbeenworkingonzappersaspartofaspecializedauditunitatRevenuQuébec.

52 GillesBernard,“SolutionfortheUnder-ReportingofIncomeintheRestaurantSector,2,”PowerPointpresentationattheFederationofTaxAdministratorsAnnualConferenceheldinDenver,ColoradoonJune2,2009(onfilewithR.T.A.).

53 ThealternativeofcertifyingeCRsandmandatingtheuseofadevicesimilartoanAFeDprinterwasconsideredandexpresslyrejectedforcost(aswellasothertechnologicalandenforcement-based)reasons.Personale-mailcommunicationsfromDaveBergeron,November18,2008andMarcSimard,September15,2009(bothonfilewithR.T.A.).

54 ActRespectingtheMinistryofRevenue,RSQ,c.M-31,sections34and35.

55 Ibid.,section34.2.

56 Ibid.,section34.1.

736 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

werekeptinaneCRorPOSsystem.ThesearetherecordsthatresidewithinaneCRatstep5.Theyarepresumedaccuratebecausetheserecordsarethebasisofthedatasenttotheprintertoproducethecustomer’sreceipt.

ThisbringsQuebectotheplacewhereallfiscaltill jurisdictionsendup—thelegislativelydefined“legal receipt.”The legal receipt is thecentral enforcementdocumentinallfiscaltilljurisdictions.Quebecisnoexception;itrequiresthatallrestaurantsalesmustbeaccompaniedbyareceipt,andthenfurtherspecifiesthatthisreceiptmustpassthroughtheSRM,whereitise-signed.57

Penaltiesfornotissuingalegalreceiptareserious.Quebec’s2006-7budgetsum-marizedthepenaltiesasfollows:

Restaurantoperatorswhofailtoremitaninvoicetoacustomerwillincurapenaltyof$100asaresultofthisomissionandwillcommitanoffenceforwhichtheywillbeliabletoafineofnolessthan$300andnomorethan$5000.Forasecondoffencecommit-tedwithinfiveyears,thefinewillbenolessthan$1000andnomorethan$10000,andforanysubsequentoffencewithinthatperiod,nolessthan$5000andnomorethan$50000.58

Thelegalreceiptcanbeaveryeffectivetoolagainstskimmingbycollusionwiththecustomer(step2skimming).Ifanestablishmentconspireswithitscustomerstochargealesseramountinexchangeforengagingincashtransactionsunaccompan-iedbyaformalreceipt,therestaurantoperatorisinviolationofthelegalreceiptrule.Ifsurveillancedetectsthefraud,penaltieswillapply.Thereisavariantofthisfraudthatistroubling,becauseitdoesnotinvolvedirectcollusionwiththecustomer;instead,theoperatororownerproducesxeroxed,scanned,orotherwiseduplicatedvalidreceipts.59Theseremainamongthefraudsthatcanonlybedetected(atpres-ent)bytraditionalaudits,andtheyarethereasonforthehighmonetarypenaltiesattachedtothefailuretoprovidealegalreceipt.

Forexample,ifapizzashop’smostcommonorderisasinglelargepepperonipizza,itwouldbepossibletoissueonereceiptforthispizzaearlyintheday(theeCRwouldprinttheorder,price, tax,date, time,andnameoftheestablishmentcorrectly).Ifthisreceiptwasreproducedandgiventoeverycustomerwhoorderedthesamepizzathatday(withoutringingeachsubsequentsalethroughtheeCR),thecashreceivedcouldbeskimmedandthecustomerwouldhaveanapparentlyvalid

57 RSQ,c.T-0.1,section425.Therequirementforlegalreceiptsisfoundinseveralotherfiscaltilljurisdictions,includingHungary,Greece,Finland,Portugal,Denmark,andLatvia.See“CashRegisterGoodPracticeGuide,”supranote6,appendixA,atparagraphs1.3.1.1to1.3.1.5,andappendixD,atparagraphs3.2.1and4.2.6.

58 Québec,MinistèredesFinances,2006-2007Budget,AdditionalInformationontheBudgetaryMeasures,March23,2006,145.

59 Bernard,supranote52,indicatedthat“[i]fthesignedinvoiceisreturnedtothePOS,itispossibletodevelopaprogramthatre-usessignedinvoicesinspecificcircumstances.TheneteffectisequivalenttousingaZapper.”

quebec’s sales recording module (srm) n 737

receipt.Thetelltalesignofthisfraudisthetimecodeonthereceipt.Anauditorsuspectingthisfraudwouldneedtoorderapepperonipizzaat,say,5:00p.m.andnoticethatthereceiptindicatedasaleat8:00a.m.IfthereceiptpassedthroughtheSRM,itwouldalsohaveapparentlyaccuratebarcodes—althoughRevenuQuébecindicatesthatahand-heldscanner(discussedbelow)willbeabletocheckforthisfraudbycomparingtimestamps.

RevenuQuébecunveileditsplansfortheSRMpilotprojectinJanuary2008.AprototypewasdemonstratedattheannualconferenceoftheFederationofTaxAd-ministrators(FTA)inDenver,ColoradoonJune2,2009.60ThepilotprogrambeganinNovember2009.ParticipatingrestaurantsmustinstalltheSRMmicrocomputerbetweentheireCRorPOSsystemandreceiptprinter.61TheSRMwillreceivedata62fromspecifiedtransactions(thedraftingofguestchecks,registerreceipts,orcreditnotes).FromtheextracteddatatheSRMwillproduceadigitalfingerprintandadig-ital signatureof thefingerprint,whichwill thenbe transmitted to theprinter.63Hand-heldreaders(usedbyauditors)donotusepublickeyinfrastructure(PKI)64to

60 Physically,theprototypeSRMwasarelativelysmall(2×1×6-inch)metalbox,connectedtotheprinterandtheeCRbystandardcables.

61 Participationinthepilotprojectisvoluntary.Afterthepilotprojecthasended,mandatoryinstallationofthedeviceinrestaurantsthroughoutQuebecwilltakeplacegraduallyduring2010and2011.

62 RevenuQuébecwillnotdisclosethedataelementsthatareselectedforsigning.Thisinformationis“confidentialforsecurityreasons.”MarcSimard,personale-mailcommunication,August10,2009(onfilewithR.T.A.).

63 Inapersonale-mailcommunication,August7,2009(onfilewithR.T.A.),MarcSimardexplained:

Inadditiontoensuretheintegrityoftheinformationpresentedonthereceipt,thesolutiondesignedbyRevenuQuébecensuresthatthebar-codescannedbythe[hand-held]readerisproducedbythecertificatedeliveredby[RevenuQuébec]tothespecificMeV[SRM]whichgeneratesthissignature.ThesignatureisproducedbyacombinationofSHA-256andeCC-224.

ThismethodusesacertificatewhichincludesapublicandaprivatekeyissuedforeachMeV[SRM]withinformationthatidentifiestheMeV[SRM]andtherestaurant.

Wechoosetheellipticcurvealgorithm(eCC)toreducethelengthoftheresult(tobeconvertedtoabarcode)andtomaintainagoodstrength.TheefficiencyofeCCiswell-known,sinceitprovidessimilarcryptographicstrengthasRSAbutusesshorterkeys.Forourcase,eCCwitha224-bitkeysizeprovidessimilarstrengthtoRSAwitha2048-bitsize(seeNIST-800-57http://csrc.nist.gov/publications/nistpubs/800-57/SP800-57-Part1.pdf ).

64 Publickeyinfrastructure(PKI)isasetofhardwareandsoftwareproceduresusedtocreate,manage,store,distribute,andrevokedigitalcertificates.Incryptography,aPKIisanarrangementthatbindspublickeyswithrespectiveuseridentitiesbymeansofacertificateauthority.Theuseridentitymustbeuniqueforeachcertificateauthority.Thebindingisestablishedthroughtheregistrationandissuanceprocess,which,dependingonthelevelofassurancethatthebindinghas,maybecarriedoutbysoftwareatthecentralauthority,orunderhumansupervision.

738 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

verifythatanyreceiptunderquestionwasactuallyproducedbyaspecificSRM(asdoestheGermansolution).65WiththeSRM,itisthe“SRMcertificate”thatperformsthisfunction.66

Thedigitalsignaturewillthenbeprintedonthereceiptfromwhichitwasde-rived.Thedigitalsignature,thedigitalfingerprint,andtherecordeddatawillallbepreservedwithinthefiscalmemoryoftheSRMforsevenyears.67Restaurantswillberequiredtosubmitsalessummaries,generatedbytheSRM,whentheysubmittheirtaxdeclarations.

TheQuebecgovernmentbelievesthattheSRMwill

n permitrestaurant[patrons]toverifythatthetaxestheypayareproperlyrecordedandassurethemthatthesefundswillberemittedtotheState;

n facilitatetheinterventionofRevenueQuebecincaseswhereareceiptisnotissuedorrecorded[step2skimming]orwhereattemptsaremadewithzappersorphantom-waretomanipulatethedataonthereceipt[step7skimming];

n allowRevenueQuebectoeasilyverifywhetherornotaspecificreceipthasbeenrecorded;

n preservesalesdataforthestatutorilyrequiredperiod;n makethedata-contentofeCRsmoreuniformandeasiertoaudit;n allowRevenueQuebectoquicklyidentifycaseswheresaleshavenotbeendeclared.68

AcriticaldifferencebetweentheGreekandtheQuebecapproachesisthatundertheGreeksystem,itisnotnecessarytohavemultipleFeSDsinanestablishmentthatnetworksmultipleeCRs—agrocerystoreoralargerestaurant,forexample.AlthoughasingleSRMmighthavebeenusedinasimilarmanner,toe-signreceiptsformultipleeCRs,thiswasdeemedtobeasecurityriskbyQuebecauthorities.Thus,anSRMhasaone-to-onerelationshipwith thereceiptprinter (butnotnecessarilywitheach

65 Thevalueofthehand-heldreadertoauditorscannotbeoverestimated.WhenQuebec’suseofabar-codescannerwasdemonstratedinJune2009attheFTA’sannualconference,theresponseoftheGermanrepresentatives,forexample,wasverypositive.SubsequentcorrespondencesuggestedthatGermanymayemulatethistechnique:

Inour[Germany’s]solutionweprintthedigitalsignature[on]thereceipt.Ifyouwanttoverifythereceiptyouhavetotypealldataofreceiptincludingthesignature[intoaPC].Ittakesalongtimebecauseyouwillmakeinputerrors.[If ]...youtestit,youwillfindoutthatthisisnotagoodpractice....I[haveused]apencilscanner....Itworks[well]andyouaremuchfaster.YoucanalsouseanormalscannerwithOCR.Wearetestingdifferentsolutions....Ifweusebarcodeswehavetohaveabarcodescanner.

NorbertZisky,personale-mailcommunication,August10,2009(onfilewithR.T.A.).

66 “The MEV [SRM] certificate[isused]toverifythatthereceiptwasproducedbyaspecificMeV[SRM]....[S]alessummariesaregeneratedandsignedbytheMeV[SRM].”MarcSimard,personale-mailcommunication,September15,2009(onfilewithR.T.A.).

67 Supranote2,slides6through8.

68 Ibid.,slide12.

quebec’s sales recording module (srm) n 739

eCR).69Thisdifferencehasasignificantfinancialimpactwhentheestimated$650costofeachSRMisfactoredintotheequation.

StepshavebeentakentopreventtamperingwiththeSRMonceitisinstalled.TheSRMisphysicallysecurewithinasealedmetalcasethatcannotbebrokenintowith-outleavingatrace.70TheSRMdoesnotcomewithabackuppowersource.UnlessrestaurateursalreadyhaveabackuppowersourcefortheireCRs,theSRMwillnotoperateincasesofpoweroutage,andtheoutagewillleavearecordofdisconnec-tionandreconnectionintheSRM.Thus,RevenuQuébecwillbealertedtoconductappropriate inspectionswheneverdisconnectionoftheSRMoccurs,regardlessofthecause.71

TheQuebecgovernmenthaspromisedtoshoulderthe$55millioncostofprovid-ingSRMstorestaurants,72butthereisnodiscussioninQuebecaboutextendingSRMapplicationsoutsidetherestaurantsector.Thisisthecaseeventhoughautomatedsalessuppressiontechnologyisnotconfinedtorestaurantfraud.73ItalsoappearsthatverysmallrestaurantsmaynotberequiredtouseSRMs.74

69 InformationpresentedwhentheSRMwasannounced(supranote2,slide7),showingoneSRMconnectedtoeitherasingleeCRoraPOSsystem,wasambiguousinthisregard,anddidnotreflecttheintendedone-to-onerelationship.ApersonalconversationwithDaveBergerononAugust11,2008clarifiedthispoint.

70 WewonderedhoweasyitwouldbeforanauditortodetectaphysicalinvasionoftheSRM.Therearenopubliclyavailable(detailed)responsesonthispointfromRevenuQuébec.Thisquestionmaybetooclosetothegovernment’ssecurityconcernstobeansweredingreatdetail,butcorrespondencewiththeministryonthispointstatesthat“safetyseals[willbeused]todetectattemptstophysicallybreakintotheMeV[SRM].”MarcSimard,personale-mailcommunication,September15,2009(onfilewithR.T.A.).Inaddition,fromappearances(aprototypewasmadeavailableforinspectionattheJune2009FTAconference),theSRMappearstobeverysecure.AttheFTAconferenceandothervenues,RevenuQuébechasbeenveryclearthatanyattempttophysicallybreakintotheSRMwillbedetected.SimilarsafeguardshavebeenbuiltintotechnologicalsolutionsadoptedinGreece,Germany,andotherfiscaltilljurisdictions.

71 Withregardtoelectricaldisconnections,whathappensifarestaurantsimplydecidestodisconnecttheSRMfromitspowersourceandmakesomesaleswiththeprinterdirectlyconnectedtotheeCR(bypassingtheSRM)?RevenuQuébechasindicatedthatthisissuefallsintotheauditarea.WiththeSRM’sabilitytodetectdisconnections,ministryofficialsfeelconfidentthateffortstodefeatthedeviceinthismannerwillbeidentifiable;thesubsequentreconnectionwouldalsoberecorded.MarcSimard,personale-mailcommunication,September15,2009(onfilewithR.T.A.).UnliketheGreeksystem,whichwillautomaticallyshutdowntheeCRafteritregistersaspecifiednumberofattempteddisconnectionsandreconnections,theSRMdoesnotappeartodothesame.

72 Supranote3.

73 Forexample,zappershavebeenfoundingrocerystoresintheUnitedStatesandtheNetherlands,inclothingestablishmentsinAustralia,andinhairdressingsalonsinFrance.

74 Supranote58,at144-45,indicatingthattheobligationofarestauranttouseSRMswillbedependentonwhethertherestaurantisrequiredtoremitareceipttocustomers.Thatrequirementisnotexpectedtobeuniversal,butinsteadwilllikelybedefinedandlimitedbyregulation.

740 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

SRMs,however,arenottheendofthestory.Quebec’sviewisthatSRMswillnoteliminatetheneedfortraditionalauditenforcement;rather,theSRMwillsupplementorextendthetraditionalaudit.75SRMswillintegrateintotraditionalauditstrategiesinthreeways:

1. theywillbethebasisforpre-auditinvestigation; 2. they will provide for rapid, digitally efficient confirmation of compliance

withbusinessrecordrequirements;and 3. theywillbringefficienciestoformalauditsbystandardizingrecordformats.

Withrespecttothefirstitem,althoughimmediatelyaftertheMarch23,2006budgetspeech,inspectionofbooksandaccountscontinuedasbefore,oncetheSRMisinplaceRevenuQuébecwillacceleratetheuseof(non-audit)inspectionteams.76Theseinspectorsarechargedwithmakingunannouncedvisitstorestaurants,toin-spectbooksandrecordsandtotakebackupcopiesofeCRandPOSprogramsintheirsearchforzappersandotherfrauds.Theseteamsaremadeupofanauditorandacomputerspecialist.WithSRMs,theseinspectorswillbeabletomorequicklyiden-tify the irregularities that would warrant transferring a case for formal audit orcriminalinvestigation.77

Withrespecttotheseconditem,thedigitalfingerprintandsignatureenvisionedfortheSRMisnotthesameasthealphanumerichashvalue(SHA-1)thatisprintedonthelegalreceiptinGreece.78TheSRMprintsabarcodethatcanbereadbyapocketcomputerthroughanintegratedopticalscanner.Thebarcodewillimmedi-atelyverifythatareceiptisa“legalreceipt,”certifiedbyagovernment-issuedSRM,andthatbothincomeandconsumptiontaxamountshavebeenproperlyrecordedinthefirm’sbusinessrecords.79Thehand-heldscanner isacritical (andgloballyunique)toolinRevenuQuébec’sefforttoincreasetheeffectivenessofitsaudits.80

75 Supranote2,slide12.

76 InQuébec (Sous-ministre du Revenu) c. Paré,2004CanLII39110(Que.CA),RevenuQuébecinspectionteamshadusedwarrantstosearchforzapperswithintheSquirrelcomputerizedcashregistersystemtowhichthedefendantheldexclusivedistributionrights,eventhoughtheinspectiondidnotrisetothelevelofaformalaudit.

77 RichardT.AinsworthandDaveBergeron,“Zappers:AutomatedSalesSuppression,”NewYorkProsecutor’sTrainingInstitute,Syracuse,NY,July31,2008(PowerPointpresentation,onfilewithR.T.A.).

78 Forexample,Zafiropoulos,“SafeguardingelectronicTaxData,”supranote30,at7,presentedthefollowingsignaturestringasarepresentativeexampleofthee-signingscriptthatwouldbefoundonareceiptissuedbyaGreekFeSD:D5A63F82962AB37886F975820883A76415DB614e0459000835920410030925eZI03013095.

79 Supranote2,slide12.

80 CouldacompleteauditofanestablishmentbeperformedwithanSRMandahand-heldscanner?RevenuQuébecindicatesthatthehand-heldscannerisnotintendedtobeusedforthispurpose.MarcSimard,personale-mailcommunication,September15,2009(onfilewith

quebec’s sales recording module (srm) n 741

Withrespecttothethirditem,theSRMwillmaketraditionalauditsmoreeffi-cientbystandardizingthedataflowsfromeCRsandPOSsystemsinusethroughouttheprovince.ItwillnolongerbenecessarytohavesubspecialistsinparticulareCRsavailabletoassistRevenuQuébecauditors,becausetheSRMwillstandardizethedatathatanauditorwillneedtodownloadontoalaptopcomputerinordertoper-formanaudit.81

Germany: Smart Cards Embedded in ECRs

The German Working Group on Cash Registers, representing the highest-tiercentralandregionaltaxauthorities,hasbeenexaminingautomatedsalessuppres-siontechnology(bothphantomwareandzapperapplications)inuseinthecountry.Aninterimreporthasbeenreleased.82Theproblemisdeemedtobeserious,andatechnologicalsolutionisenteringthefinalstagesoftesting.

TheGermansolution involvesstoringcriticaldata fromsales transactionsonsmartcardssecurelyembeddedineCRs.TheGermanNationalMetrologyInstitute(Physikalisch-TechnischeBundesanstalt [PTB]) is thehomeof the INSIKAproject(Integrierte Sicherheitslösung für Kassensysteme—Integrated Security SolutionsforCashRegisters).INSIKAbeganworkonprototypesofthesmartcardsolutionin2008.

PapersondigitalsignaturesbyNorbertZiskyofthePTB83convincedtheworkinggroupthatsigningtechniqueshadbeensufficientlytestedinsecurecommunication

R.T.A.).SimardexplainsthattheSRM(andthescanner)ispartofafour-partfraudpreventionstrategy(basedinlargepartonthedeterminationthatthefraudproblemismuchlargerthanzappersalone,andthatamuchbroadereffortisneeded).Thefour-partstrategycomprisesthefollowingsteps:

(1) Therestaurateurisobligedtoremitapaperreceiptorinvoicetotheclient.Thisisthekeytoconfirmingthataneconomictransactionhasoccurredbetweenabusinessanditscustomers.Inmostcaseswhereincomeisnotdeclared,hiddentransactionswerenotrecordedintheelectroniccashregister(eCR).

(2) RestaurateursmustproduceinvoicesusinganMeV[SRM]approvedbyRevenuQuébec,whichforcesthemtokeeprecords.

(3) RevenuQuébecwillstepupitsinspectionactivitiestoensurethatthetwoabovemeasuresareadheredto.NotethattheMeV[SRM]willallowustoredesignandspeeduptheinspectionprocessanddeterminemoreefficientlywhetherornotarestaurantiscomplyingwiththelaw.Withoutsuchinspections,businessesseekingtomaskincomewouldsimplynot[record]transactionsinthecashregister,regardlessofthecontrolmechanismsinplace(GreekorGermansolution,MeV[SRM],etc.).

(4) Thegeneralpublicismadeawareofrestaurateurs’obligationtoremitaninvoicetotheircustomers,inordertore-establishfiscalequityandfaircompetition.

81 Bernard,supranote52.

82 GermanWorkingGrouponCashRegisters,Interim Report,supranote17.

83 NorbertZisky,“ManipulationsschutzelektronischerRegistrierkassenundKassensysteme”[“ManipulationProtection—electronicCashRegistersandPOSSystems”],GermanFederalStandardsLaboratory,BrunswickandBerlin(May2005)(unpublisheddraftonfilewithR.T.A.);

742 n canadian tax journal / revue fiscale canadienne (2009) vol. 57, no 4

settingswithmeasuringinstruments84thattheycouldformthebasisofasolutiontozappers.

TheINSIKAprojectwaschargedwithcompletingthetechnicalspecificationsforasignaturesmartcardbythesummerof2008.85TheworkwascompletedinFebru-ary2009.Includedwiththetechnicalspecificationsforthesignaturesmartcardisadeterminationof thedata structuresand formats,communicationprotocols,andsecurityanalysisforthesystem.Thefinalresultsoftheprojectwerepublishedat

and(March15,2004)(unpublisheddraft,translationonfilewithR.T.A.).Sincetheseearlypapers,therehavebeenseveralmodificationstoZisky’sproposal.Thecriticalchangesincludethefollowing:

1 Thesignaturedevice(smartcards)distributedbythetaxauthoritieswillbepersonalizedtothetaxpayernottothecashregister(cashbox);

2 Thesignaturedevicewillhaveasetofdedicatedsumstorageswhichwillbecontrolledbythesignaturedeviceitself.It[will]generatetherelevantdatafromthesetofdatatobesigned.Inthe[casewheretheremaybe]alossofsigneddatathetaxauthorities[willbe]abletoreadthestoreddatafromthesmartcard.Thesumstorages[arerequired]to[be]readoutperiodicallyand[arerequired]tobestoredaftersigning.