qrp plan administrator's guide - ascensus · plan administrators may impose minimum age...

TRANSCRIPT

Qualified Retirement Plan

Plan Administrator’s Guide

Qualified Retirement Plan Plan Administrator’s GuideThe material in this desktop guide has been drawn from sources believed to be reliable. Every effort has been made to ensure the accuracy of the material. But IRS forms, government regulatory positions, and laws are subject to change, so the accuracy of this information is not guaranteed. This Guide is sold with the understanding that the publisher and the editor are not engaged in rendering legal or accounting services. The material in this Guide reflects the law and regulatory interpretations as of the publication date of April 2020.

The information is designed to answer common questions on qualified retirement plans; however, it may be necessary to refer to a more comprehensive text or other source to answer some questions. If you are unsure of an answer, consult a competent professional.

Ascensus® and the Ascensus logo are registered trademarks of Ascensus, LLC.

Copyright ©2020 Ascensus, LLC. All Rights Reserved.

This material may not be reproduced in whole or in part in any form or by any means without written permission from the publisher.

Printed in the United States of America.

This Guide is updated annually to incorporate new guidance issued throughout the year.

For information on industry and regulatory news, visit ascensus.com.

Contents

1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2 Plan Adoption . . . . . . . . . . . . . . . . . . . . . . . . 3

3 Plan Operations and Administration . . . . . . 6

4 Contributions . . . . . . . . . . . . . . . . . . . . . . . . . 9

5 Plan Testing . . . . . . . . . . . . . . . . . . . . . . . . . 11

6 Distributions . . . . . . . . . . . . . . . . . . . . . . . . 14

7 Portability . . . . . . . . . . . . . . . . . . . . . . . . . . 21

8 Reports and Notices . . . . . . . . . . . . . . . . . . 24

1

This Guide is a quick reference tool in a Q&A format for defined contribution plan administrators. Generally, when this Guide discusses qualified retirement plans (QRPs), unless indicated otherwise, it is referring to profit sharing and money purchase pension plans. Under all QRPs, the plan administrator is the individual or entity directly responsible for managing the plan’s daily operations.

For most plans, the employer sponsoring the plan serves as the plan administrator. But, depending upon the business, the employer may appoint another individual or entity to be the plan administrator and act as the employer’s representative. All references to the plan administrator in this Guide typically include individuals or entities working on behalf of or assisting the plan administrator with plan responsibilities. The plan administrator may wish to consult an attorney or tax advisor about questions that arise during the course of plan operations.

This Guide is intended to alert the plan administrator to various concepts and issues that are common to QRP operations. This Guide serves its purpose by bringing to the plan administrator’s attention important issues and requirements applicable to QRPs. It is not intended as a comprehensive source for ensuring compliance with all QRP rules under the Employee Retirement Income Security Act (ERISA) and the Internal Revenue Code (IRC). It is intended to assist the plan administrator in identifying plan administration issues—some of which may require tax or legal advice. This Guide is not a substitute for the competent tax and legal advice that a plan administrator may require from time-to-time while performing administrative duties.

1 Introduction

2 – Introduction

The QRP basic plan document and adoption agreement specify some of the plan operations for which the plan administrator is responsible. Depending upon the plan administrator’s relationship with the plan sponsor (e.g., the document provider for pre-approved plans), the plan administrator may directly or indirectly be involved in

• formulating plan policy consistent with plan documentation;

• determining participation, contribution, and distribution eligibility;

• maintaining plan records;

• preparing and filing government reports; and

• communicating regularly with employees (and beneficiaries) participating in the plan.

A plan administrator should clarify and document areas of responsibility for plan administration with the plan sponsor to ensure the timely performance of all required plan operations.

If a plan is not operated by the terms of its document or is otherwise noncompliant with Department of Labor (DOL) or Internal Revenue Service (IRS) requirements, plan disqualification could result. The DOL and the IRS provide correction programs to help plan administrators identify and correct plan defects.

3

Q What documents are required to establish a QRP?

A During the second restatement cycle, employers may use plan documents that generally consist of two components: the basic plan document (BPD) and the adoption agreement. The BPD contains all of the nonelective provisions and rules governing the plan. These rules are applicable to all adopting employers. The adoption agreement contains the elective plan provisions. Together with the default provisions in the BPD, the provisions that the employer selects in the adoption agreement govern how the plan will operate in terms of eligibility, vesting, contributions, allocations, etc. Once the employer signs the adoption agreement, the plan sponsor should keep a copy and give a copy of the plan document and the signed adoption agreement to the employer.

During the third restatement cycle (known as “Cycle Three”), which runs from February 1, 2017, through January 31, 2023, plan documents may consist of two formats—either a single plan document or a BPD with an adoption agreement. These documents are expected to be available sometime during 2020.

NOTE: QRPs are subject to a six-year restatement cycle (i.e., every six years employers must adopt new pre-approved plan documents).

Q Does the plan administrator have to do any more than sign required documentation to adopt a QRP?

A Before signing the plan documents, the employer should take formal steps, if necessary, to adopt the plan. These steps vary depending upon the employer’s legal structure. For example, if the business is organized as a corporation, the board of directors must adopt a resolution authorizing the adoption of the plan. If

2 Plan Adoption

4 – Plan Adoption

the business is a partnership, the plan administrator should consult the partnership agreement to determine the steps necessary, if any, to formally adopt the plan.

Q Does the plan administrator have to submit the plan documents to the IRS for approval?

A If the business has adopted a prototype plan, it generally can rely on the favorable opinion letter issued to the prototype plan sponsor concerning the tax qualification of the plan. If the plan is a volume submitter plan, the volume submitter practitioner receives an IRS advisory letter indicating approval of the specimen plan that the business can rely on.

NOTE: In June 2017, the IRS released Revenue Procedure (Rev. Proc.) 2017-41. This guidance describes the IRS’ new pre-approved qualified retirement plan program, which will replace the current master, prototype, and volume submitter programs with a single opinion letter program for standardized and nonstandardized documents. This change will affect plans being restated during Cycle Three. Rev. Proc. 2017-42 was later modified by Rev. Proc. 2018-42.

Q Once the plan is established, how are the plan assets protected?

A Employers generally must purchase a bond to protect the plan assets against acts of fraud or dishonesty. As a general rule, certain individuals (e.g., plan fiduciaries, officers, or employees) who “handle” plan assets must be bonded for at least 10 percent of the amount of the plan assets that they handle. Plan administrators, however, must be bonded for 10 percent of the full dollar value of the plan. The minimum bond amount, irrespective of plan asset value, is $1,000. The maximum amount required is $500,000. The maximum bond for plans that hold employer securities, however, is $1,000,000.

Plan Adoption – 5

Q How are employees notified about the new plan and its provisions?

A All eligible employees must receive a summary plan description (SPD), which is a comprehensive, easily understood explanation of the plan’s provisions. The plan sponsor typically will prepare the SPD for the employer. The employer must distribute the SPD to all eligible, common-law employees within 120 days of the plan’s adoption.

6

Q How does the plan administrator determine when an employee is eligible to participate in the plan?

A Before being allowed to participate in the plan, the employee must meet certain eligibility requirements, such as the plan’s minimum age and service requirements (discussed later). Once an employee has met the minimum age and service requirements (in addition to any other eligibility criteria), he may enter the plan. But in most QRPs, the employer designates specific dates (often referred to as plan entry dates) that a participant must reach before entering the plan.

Once an otherwise eligible employee has completed the initial age and service requirements, she must be allowed to enter the plan within six months of the time she completes such requirements or, if earlier, the first day of the following plan year.

Consequently, while plan entry dates may vary between plans, many QRPs designate the first day of the plan year and the first day of the seventh month of the plan year as the plan entry dates. For example, many plans that operate on a calendar-year basis choose plan entry dates of January 1 and July 1.

Q Can plan administrators exclude employees based on age?

A Plan administrators may impose minimum age requirements for purposes of determining an employee’s eligibility to participate in a QRP, but they may not require employees to reach an age greater than 21 before becoming eligible to participate in a QRP. Certain educational institutions may establish age requirements as high as age 26 if they require no more than one year of service to become 100 percent vested.

3 Plan Operations and Administration

Plan Operations and Administration – 7

Plan administrators may not exclude employees solely because the employee has reached a given age (e.g., age 65). Assuming an employee has met the plan eligibility requirements, he will continue to receive contributions beyond age 72 if he continues employment.

Q Is there a maximum service requirement that employees must meet before becoming eligible to participate in a QRP?

A A plan administrator may not require an employee to complete more than two years of service to be eligible for participation in a QRP (one year for 401(k) plans). In addition, if a plan requires more than one year of service for initial eligibility, the plan cannot require that an employee complete more than two years of service before she is 100 percent vested.

To be credited with a year of service for plan eligibility purposes, an employee generally must work a minimum number of hours (up to 1,000) during a 12-month computation period. For eligibility purposes, the first 12-month period starts on the employee’s date of hire.

NOTE: Effective for 2021 and later plan years, employees who have three consecutive 12-month periods of 500 hours of service and who satisfy the plan’s minimum age requirement must be allowed to make elective deferrals in an employer’s 401(k) plan. Plan years before 2021 need not be counted in determining the three consecutive 12-month periods. The current, more restrictive, eligibility rules could continue to be applied to other contribution sources (e.g., matching contributions) and to ADP/ACP safe harbor plans. Employers may also exclude such part-time employees from coverage, nondiscrimination, and top-heavy test rules.

8 – Plan Operations and Administration

Q Does the plan administrator have to continue to monitor employee eligibility to participate in the plan?

A After initial participant enrollment in the plan has been completed, the plan administrator should periodically review the conditions for plan eligibility and participation as new employees become eligible to participate in the plan. The plan administrator should refer to the plan documents for minimum age and service requirements and plan entry dates and procedures.

As new employees become eligible, the plan administrator must provide them with a written summary that details information unique to the employer’s plan, such as entry dates, contribution formulas, vesting schedules, and other features. New employees also must receive an SPD within 90 days of becoming eligible to participate.

9

4 Contributions

Q What kind of contributions can be made to a profit sharing plan?

A If the employer has adopted a profit sharing plan, each plan year the employer must decide whether to make a contribution on behalf of the participants, as well as the amount of the profit sharing contribution. Profit sharing contributions may be made from accumulated or current year profits, and may range from zero to 25 percent of the aggregate compensation earned by plan participants during the employer’s tax year. Most employers elect a discretionary profit sharing formula, so each year the employer will determine whether to fund the plan.

Once made to the plan, the profit sharing contribution will be allocated to the individual accounts of plan participants (as of the last day of the plan year). The plan administrator should check the plan documents to determine if any special allocation rules apply to the plan.

Q What kind of contributions can be made to a money purchase pension plan?

A With money purchase pension plans, the plan administrator must make an annual employer contribution based on a formula specified in the plan documents. Employer contributions may range as high as 25 percent of the participant’s compensation.

10 – Contributions

Q How are contributions allocated to participants?

A Under most QRPs, contributions are allocated based on an individual’s compensation. Although the definition of compensation can vary between plans, the definition selected in the plan documents must fall within certain guidelines. Also, if the business maintaining a QRP is a sole proprietorship or partnership, contributions on the owner’s behalf must be determined in a different manner from contributions made on behalf of common-law employees.

Q When must plan administrators deposit employer contributions?

A To ensure the deductibility of the contribution for a given tax year, the plan administrator must deposit the contribution into the plan by the business’ federal income tax return due date (including extensions).

11

Q Are there any annual tests that a QRP might have to pass?

A To maintain its favorable tax status, a QRP must pass several tax qualification and nondiscrimination tests each plan year. These nondiscrimination rules exist to ensure that highly compensated employees (HCEs) and key employees do not receive, or have available to them, disproportionately more valuable benefits than those received by, or made available to, lower paid employees.

Q How does the plan administrator determine if an employee is an HCE?

A An HCE is someone who

• was a five percent owner at any time during the current plan year or preceding year, or

• during the preceding year earned more than $130,000 for 2020 ($125,000 for 2019) in compensation. For example, for the 2021 plan year, look back to the compensation figure in effect for 2020 ($130,000). (The plan administrator may elect to use the additional condition of membership in the top-paid group when determining HCE status. This election may be revoked.)

NOTE: To be considered a five percent owner, an individual must actually own (or be considered to own) more than five percent of the employing entity.

5 Plan Testing

12 – Plan Testing

Q Which employees are considered key employees?

A An employee is considered a key employee if, at any time during the plan year, the employee is

• an officer of the employer and has annual compensation greater than $180,000 for 2019 and $185,000 for 2020 (indexed),

• a five percent owner of the company, or

• a one percent owner of the company with annual compensation exceeding $150,000 (not indexed).

NOTE: To be considered a five percent or a one percent owner, an individual must actually own (or be considered to own) more than five percent or one percent of the employing entity.

Q How do the nondiscrimination rules apply to QRPs?

A IRC Section (Sec.) 401(a)(4) prohibits QRPs from discriminating in favor of HCEs. Under these rules, a plan must be nondiscriminatory in each of three general categories.

1. Amount of contributions or benefits

2. Availability of benefits, rights, and features

3. Effect of plan amendments and terminations

Q What is the minimum coverage rule?

A IRC Sec. 410(b) requires that a minimum percentage of non-HCEs be covered by the plan in relation to the percentage of HCEs covered by the plan. A plan will pass this test if at least 70 percent of the non-HCEs are covered by the plan.

Plan Testing – 13

Q What is the top-heavy rule?

A IRC Sec. 416 provides that a plan is top heavy if more than 60 percent of all plan assets are held in the accounts of key employees. If a plan is top-heavy, the plan administrator must follow special rules that may include making a minimum contribution for non-key employees.

Q What is the annual additions rule?

A IRC Sec. 415 limits the contribution amount that can be allocated to a participant for any plan year. The maximum amount that may be allocated to any participant during any plan year is limited to the lesser of 100 percent of the participant’s compensation or $56,000 for 2019 and $57,000 for 2020 (indexed for cost-of-living adjustments).

Q What type of compensation is used to perform the various qualification and nondiscrimination tests?

A To perform the various tests described previously, the plan administrator often must calculate each participant’s compensation first. The type of compensation used for each test, however, can vary. Some tests allow the plan to define the compensation type, while others have statutorily defined compensation types. The plan administrator should refer to the plan documents for more information.

14

Q How does the plan administrator determine which distribution options are available under the QRP?

A The plan documents specify the forms of distribution available under the plan. Plans subject to the Retirement Equity Act of 1984 (REA) must distribute assets in the form of an annuity unless the plan participant and his spouse properly waive this option. The plan documents will determine whether distributions may be taken in forms other than an annuity, or whether a waiver is required to do so.

Q When is a participant allowed to take distributions from the plan?

A A participant (or her designated beneficiary) generally may begin taking distributions upon one of the following events (known as “triggering events”).

• Attainment of normal retirement age (as defined in the plan)

• Death

• Disability

• Severance of employment

• Plan termination

• Qualified birth or adoption expenses (effective for distributions in 2020 and later years)

6 Distributions

Distributions – 15

The Coronavirus Aid, Relief, and Economic Security (CARES) Act permits a special distribution type: “Coronavirus-Related Distributions (CRDs).” Qualified individuals may request up to $100,000 in aggregate from their employer-sponsored retirement plans (plan permitting) on or after January 1, 2020, and before December 31, 2020. A qualified individual is defined as an individual who

• is diagnosed with the COVID-19 or SARS-CoV-2 virus (or whose spouse or dependent is diagnosed with the virus) in an approved test, or

• experiences certain related adverse financial consequences.

Plans may rely on a participant’s self-certification to determine if the participant is a qualified individual. Qualifying individuals may avoid mandatory 20 percent withholding on distributions, pay taxes on the distribution ratably over three years, avoid the 10 percent early withdrawal penalty tax, and, to the extent that the CRD is eligible for tax-free rollover treatment, roll over the distribution into any eligible retirement plan or IRA within a three-year window, starting on the day after the distribution is received. Plans are not required to provide a notice that explains tax and rollover options (i.e., the 402(f) notice) with a CRD.

The plan administrator should refer to the plan documents to determine the specific circumstances under which participants may receive distributions.

The plan administrator also should refer to the plan documents to determine the vesting schedule, if any, that applies to the plan. The vesting schedule determines the amount of benefits that a participant may receive once he incurs a triggering event.

Q Can a participant take a distribution before a standard triggering event occurs?

A In addition to the previously described standard triggering events, profit sharing plans may allow plan participants to take in-service distributions of employer contributions. An “in-service distribution” provision permits participants to take distributions from the plan before incurring a standard triggering event.

16 – Distributions

Similar to other distributions, the maximum amount that a participant may withdraw as an in-service distribution is the vested portion of her account balance. The amount, however, may be further limited depending on the length of time the employee has been a participant in the plan and depending on whether the in-service distribution is taken because of financial hardship. The plan administrator should refer to the plan documents to determine if the plan allows these types of distributions.

Q May the plan administrator make a distribution to a participant who has a hardship?

A Hardship distributions are available only from profit sharing plans with a 401(k) component. Before January 1, 2019, employers could allow participants to receive distributions of their elective deferrals before reaching a triggering event if they met the requirements of a financial hardship. (Hardship distributions could also include earnings on deferrals and QNECs and QMACs, but only such amounts accrued as of December 31, 1988, or if later, the end of the last plan year ending before July 1, 1989.)

Effective for plan years after December 31, 2018, the Bipartisan Budget Act of 2018 and subsequent final Treasury regulations allow participants to also receive hardship distributions of qualified nonelective contributions, qualified matching contributions, employer ADP safe harbor and QACA safe harbor contributions, and earnings on all of these amounts. Earnings on elective deferrals are also eligible for hardship distribution. The plan administrator should refer to the plan documents to determine if the plan allows this distribution reason for in-service distributions.

Q Is the plan administrator responsible for providing any notices at the time of distribution?

A The plan administrator must give a notice that describes tax treatment options to participants who request a payment from the plan. This notice generally must be provided to the participant at least 30 days, but no more than 180 days, before the distribution.

Distributions – 17

To satisfy requirements under IRC Sec. 411(a)(11) and REA, the plan administrator also may have to provide a notice to properly get a participant’s consent before distributions occur.

Q Does the plan administrator have to make distributions to participants who reach age 72?

A Plan participants must begin taking required minimum distributions (RMDs) once they reach a certain age. The age when RMDs must generally begin is increased from age 70½ to age 72. This applies to distributions required in 2020 and later years, for those who reach age 70½ in 2020 or a later year. Employers may allow participants who are still working to delay RMDs until April 1 following the year of retirement. This delayed starting date does not apply to five percent owners. Once triggered, an RMD must be taken annually by December 31. In general, the RMD amount will be determined by dividing the balance in the participant’s individual account by the applicable life expectancy factor. Beneficiaries of deceased retirement plan participants also may be required to take certain distributions from the plan.

NOTE: To be considered a five percent owner, an individual must actually own (or be considered to own) more than five percent of the employing entity.

Q Are all 2020 RMDs waived?

A The CARES Act waives the 2020 RMD requirement. The waiver also applies to individuals who turned 70½ in 2019 but did not take their first RMD before January 1, 2020. In absence of additional relief, the next RMD for those individuals must be taken by December 31, 2021. 2020 is also disregarded for purposes of counting the five-year period for beneficiary distributions, effectively adding one year to the remaining period.

A distribution that is taken in 2020, but that is not an RMD because of the waiver, may be rolled over to another eligible retirement plan or IRA within 60 days of the distribution. But if

18 – Distributions

the 60th day falls on or after April 1, 2020, and before July 15, 2020, the individual will have until July 15, 2020, to complete the rollover. While these distributions may be rolled over, they are not subject to mandatory 20 percent withholding, the 402(f) notice (the notice that explains tax and rollover options), or the direct rollover requirements.

Q Can a distribution of plan assets be made to an ex-spouse in the case of a divorce?

A Under limited circumstances, a distribution of a plan participant’s benefits may be made pursuant to a divorce or legal separation. The plan administrator must ensure that any distribution relating to child support, alimony, or marital property is considered a qualified distribution according to the terms of the plan. To accomplish this, the plan administrator (or the plan’s legal counsel) should review the plan documents and any domestic relations order that concerns plan assets to determine whether the order is a qualified domestic relations order (QDRO) under the plan. Once this determination has been made, the plan administrator must notify all persons affected by the determination within a reasonable time. Any distribution of benefits made pursuant to a QDRO is nontaxable to the participant if the alternate payee is the spouse or former spouse of the participant.

Q Can the IRS place a levy on plan assets?

A Creditors generally may not levy plan assets. A limited exception to this rule exists for the benefit of the IRS, which is recognized as the tax collector for the United States Government. The IRS may attempt to satisfy a tax lien through levy upon plan assets. Under these circumstances, the financial organization in custody of the plan assets will receive an IRS form called a “Notice of Levy.” It will then be incumbent upon the financial organization to follow the appropriate steps required by law.

Distributions – 19

Q Can a participant take a loan from a QRP?

A Under certain circumstances, plan participants may be eligible to receive loans from their plan assets. The plan administrator should refer to the plan documents to determine if the plan offers a plan loan program.

Q Are there any requirements that loans have to meet to be exempt from the prohibited transaction rules?

A All QRP loan programs generally must have the following characteristics.

• Loans must be made available to all participants and beneficiaries on a reasonably equivalent basis.

• Loans must not be made available to HCEs, officers, or shareholders in an amount or ratio greater than the amount available to other employees.

• Loans must be made in accordance with specific loan provisions as described in the loan disclosures part of the SPD.

• Loans must bear a reasonable interest rate.

• Loans must be adequately secured.

• Loans must have level amortization, with payments at least quarterly.

• Loans generally must be repaid within five years.

• Loans must not exceed statutory limits.

20 – Distributions

NOTE: The CARES Act permits an increase in the maximum plan loan amount. The retirement plan loan maximum for a qualified individual is increased from the lesser of $50,000 or 50 percent of the participant’s vested balance to the lesser of $100,000 or 100 percent of the participant’s vested balance. A qualified individual is defined as an individual who

• is diagnosed with the COVID-19 or SARS-CoV-2 virus (or whose spouse or dependent is diagnosed with the virus) in an approved test, or

• experiences certain related adverse financial consequences.

Plans may rely on a participant’s self-certification or documentation to determine if the participant is a qualified individual. The increase applies to loans made during the 180-day period beginning on March 27, 2020. Also, for qualified individuals with outstanding plan loans, loan repayment dates that occur between March 27, 2020, and December 31, 2020, may be delayed for one year, with the amortization period—including the five-year repayment deadline—adjusted accordingly.

21

Q Can a participant roll over distributions to other retirement plans?

A Many different types of plan assets may be rolled over to an IRA or to another employer’s QRP. Distributions that may be rolled over are called eligible rollover distributions.

Q Which distributions are eligible rollover distributions?

A Most distributions are eligible rollover distributions except for amounts that are

• required minimum distributions (RMDs),

• distributions that are part of a series of substantially equal periodic payments that will last for the participant’s lifetime (or joint lives of the participant and beneficiary) or for a specified period of 10 years or more,

• distributions paid to nonspouse beneficiaries of deceased participants,

• certain distributions to correct plan excess contributions, and

• distributions of assets from the plan because of hardship.

Q What types of plans are eligible to receive rollovers?

A An employee may roll over any eligible rollover distribution from one eligible employer-sponsored retirement plan into another eligible retirement plan. Eligible retirement plans include

• Traditional, Roth, and SIMPLE IRAs,

• 401(a) qualified plans,

7 Portability

22 – Portability

• 403(a) qualified annuity plans,

• 403(b) plans, and

• governmental 457(b) plans.

NOTE: Individuals may roll over assets from Traditional IRAs, QRPs, 403(b) plans, and governmental 457(b) plans to SIMPLE IRAs. But they first must satisfy a two-year waiting period beginning on the date that the first contribution under the employer’s SIMPLE IRA plan was made to the SIMPLE IRA.

Q How does the plan administrator roll over assets directly to an IRA or to another plan?

A IRS regulations allow the plan administrator to establish reasonable procedures that participants must follow to elect a direct rollover. The plan administrator also may ask participants and the provider of the receiving IRA (or a representative of the new employer’s plan) to provide reasonable information about the IRA or plan as a condition of the direct rollover.

When issuing a check for a direct rollover, the regulations specify that the check must be made payable to the trustee, custodian, or issuer of the IRA or new plan. For example, if John Q. Smith elects a direct rollover to his IRA at ABC Financial Organization, the payee line of the check should read “ABC Financial Organization as trustee of John Q. Smith’s IRA.”

Q What if a participant chooses to take a distribution of the assets rather than directly rolling over the assets?

A Eligible rollover distributions that are not directly rolled over to an IRA or to another eligible plan are subject to mandatory 20 percent federal income tax withholding. In other words, a plan participant who requests a check payable to herself will receive only 80 percent of the payment. The plan administrator must withhold 20 percent of the payment and send it to the IRS as income tax withholding to be credited against the participant’s income tax liability. The participant cannot waive withholding on any eligible rollover distribution that is paid directly to her.

Portability – 23

Q Can plan participants directly roll over their pretax and after-tax assets to different retirement plans?

A The IRS allows individuals to split pretax and after-tax employer plan assets that are directly rolled over to multiple destinations (i.e., other employer plans or IRAs). For individuals attempting to roll over pretax assets to a Traditional IRA and after-tax assets to a Roth IRA, this eliminates the need to complete two separate indirect rollovers.

Q What is the difference between a direct rollover and a transfer?

A While the transactions do have some similarities (e.g., in both types of transactions, checks generally are made payable to a new trustee or custodian), the differences between the two transactions are quite distinct. A direct rollover occurs when a participant who is eligible to receive a distribution elects to move his retirement assets directly to another QRP or directly to an IRA. In other words, a participant’s account balance is being moved to an entirely different plan. Because a direct rollover technically represents a distribution followed by an immediate rollover, the distributing plan must comply with all of the standard distribution procedures (e.g., providing REA notices).

With a transfer, an employer generally is moving an entire plan from one trustee/custodian to another. Because an entire plan generally is being moved in a transfer, no distribution reporting is required and the plan administrator need not follow the standard distribution procedures.

24

8 Reports and Notices

Q What types of reports and notices must the plan administrator provide?

A The following is a summary of possible disclosure and reporting requirements.

REQUIRED DOCUMENTS DESCRIPTION TIMING

Notice to Interested Parties

A plan must inform interested parties if it applies for an IRS determination letter as to the plan’s qualified status.

The plan administrator must provide the notice no less than 10 and no more than 24 days before the time the application is filed.

Beneficiary Designation Form

Allows participants to name beneficiaries for their plan assets.

The employee should complete this form when she begins participation in the plan.

Summary Plan Description (SPD)

Provides vital plan information in an easily understood manner.

Distribute the SPD to employees within 120 days after plan adoption. Distribute the SPD to each new participant within 90 days after plan entry and to each beneficiary receiving benefits within 90 days after commencement of benefits.

Summary of Material Modifications (SMM)

Summary of changes to the document that also affect the SPD; or may provide updated SPD.

Distribute the SMM to employees within 210 days after the end of the plan year during which the change was adopted. The plan administrator must distribute the SMM to each plan participant and beneficiary receiving benefits.

Participant Disclosure/Reporting

Reports and Notices – 25

REQUIRED DOCUMENTS DESCRIPTION TIMING

Summary Annual Report (SAR)

Summary of Form 5500, including plan expenses and value of plan assets, and right to receive full 5500.

The plan administrator must distribute the SAR annually, the later of nine months after the close of the plan year or two months after the SAR is due (in the case of an IRS granted extension) to each plan participant and beneficiary receiving benefits.

Qualified Domestic Relations Order (QDRO)

The plan administrator must determine whether a DRO meets the IRC Sec. 414(p) specifications to be a QDRO.

The plan administrator, upon receipt of a DRO, must promptly notify each affected plan participant and beneficiary of the plan’s procedures for determining the DRO’s qualified status. The plan administrator must send a second notice once a QDRO determination has been made.

Form 1099-R The plan administrator must provide a Form 1099-R to each participant or beneficiary who receives a distribution from the plan.

Forms 1099-R are due to participants by January 31 of the year after distribution.

Form 1098-Q The QLAC issuer must generate Form 1098-Q for each plan participant who purchases a QLAC.

Forms 1098-Q are due to participants by January 31.

IRS Form W-4P or Substitute Form

Explains IRS withholding requirements and allows distribution recipients to make withholding elections.

In general, the plan administrator must provide the notice annually to individuals receiving periodic payments from the plan and each time an individual receives a nonperiodic payment.

Participant Benefit Statement

Statement of nonforfeitable balance, includes certain required disclosures.

A plan administrator must provide a statement of benefits to plan participants at least quarterly for plans that allow participants to direct their investments. Plans that are not participant-directed must provide benefit statements annually.

26 – Reports and Notices

REQUIRED DOCUMENTS DESCRIPTION TIMING

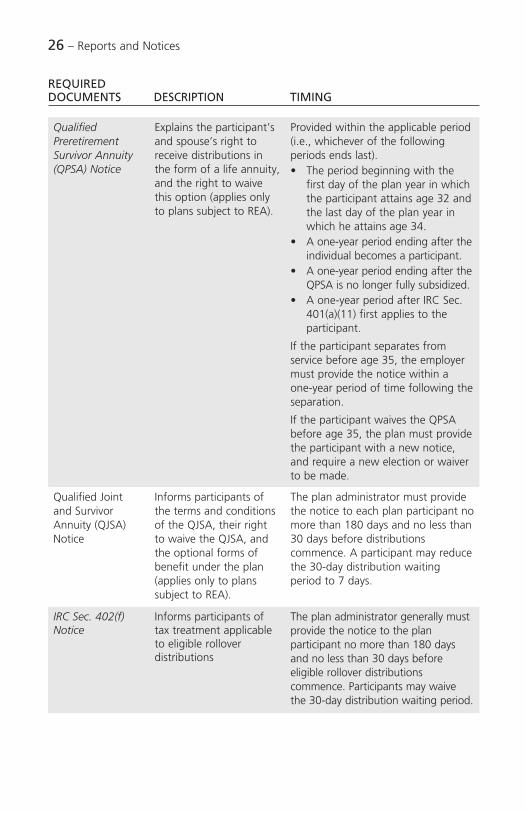

Qualified Preretirement Survivor Annuity (QPSA) Notice

Explains the participant’s and spouse’s right to receive distributions in the form of a life annuity, and the right to waive this option (applies only to plans subject to REA).

Provided within the applicable period (i.e., whichever of the following periods ends last).• The period beginning with the

first day of the plan year in which the participant attains age 32 and the last day of the plan year in which he attains age 34.

• A one-year period ending after the individual becomes a participant.

• A one-year period ending after the QPSA is no longer fully subsidized.

• A one-year period after IRC Sec. 401(a)(11) first applies to the participant.

If the participant separates from service before age 35, the employer must provide the notice within a one-year period of time following the separation.

If the participant waives the QPSA before age 35, the plan must provide the participant with a new notice, and require a new election or waiver to be made.

Qualified Joint and Survivor Annuity (QJSA) Notice

Informs participants of the terms and conditions of the QJSA, their right to waive the QJSA, and the optional forms of benefit under the plan (applies only to plans subject to REA).

The plan administrator must provide the notice to each plan participant no more than 180 days and no less than 30 days before distributions commence. A participant may reduce the 30-day distribution waiting period to 7 days.

IRC Sec. 402(f) Notice

Informs participants of tax treatment applicable to eligible rollover distributions

The plan administrator generally must provide the notice to the plan participant no more than 180 days and no less than 30 days before eligible rollover distributions commence. Participants may waive the 30-day distribution waiting period.

Reports and Notices – 27

REQUIRED DOCUMENTS DESCRIPTION TIMING

IRC Sec. 411(a)(11) Notice

Explains a participant’s distribution options and automatic rollover requirement.

The plan administrator generally must provide the notice to the plan participant no more than 180 days and no less than 30 days before distributions commence. Participants may reduce the 30-day waiting period to 7 days.

ERISA Sec. 404(c) Notice

Disclosure of intent to satisfy ERISA Sec. 404(c), including investment options

The plan administrator generally provides this information with the SPD.

Sarbanes-Oxley Blackout Notice

The plan administrator must notify affected plan participants if a blackout period (i.e., a period during which participants cannot make changes to their retirement plan assets) will last more than three consecutive business days.

The plan administrator generally should provide the notice no more than 30 days before the blackout period starts.

Qualified Default Investment Alternatives (QDIAs)

Default fund information to be followed if participant does not make investment elections. Includes participant’s rights to make own elections

The plan administrator generally must provide this notice at least 30 days before the first day of the plan year.

Participant Directed Fee Disclosures

Disclosure of fees assessed against participant accounts

Timing of initial/annual notice• Provided on or before the date

participant can first direct investments

• Annually thereafterStatement of fees is provided on a quarterly basis (included in participant statement)

28 – Reports and Notices

REQUIRED DOCUMENTS DESCRIPTION TIMING

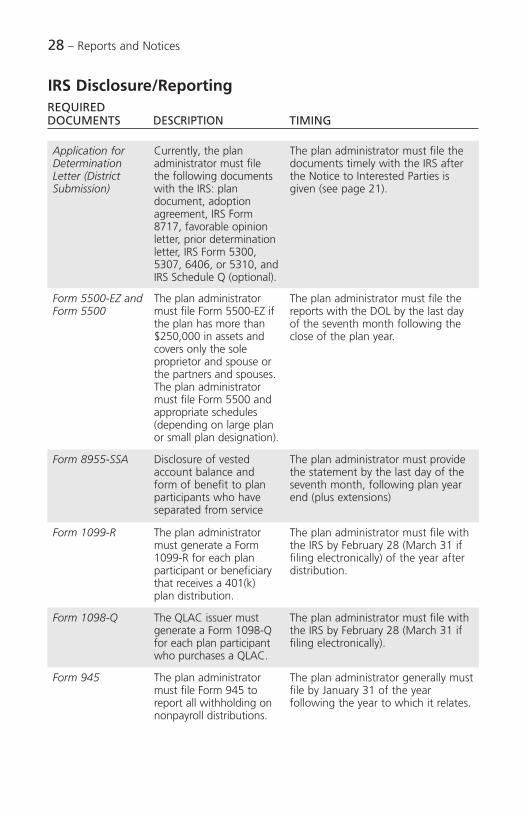

Application for Determination Letter (District Submission)

Currently, the plan administrator must file the following documents with the IRS: plan document, adoption agreement, IRS Form 8717, favorable opinion letter, prior determination letter, IRS Form 5300, 5307, 6406, or 5310, and IRS Schedule Q (optional).

The plan administrator must file the documents timely with the IRS after the Notice to Interested Parties is given (see page 21).

Form 5500-EZ and Form 5500

The plan administrator must file Form 5500-EZ if the plan has more than $250,000 in assets and covers only the sole proprietor and spouse or the partners and spouses. The plan administrator must file Form 5500 and appropriate schedules (depending on large plan or small plan designation).

The plan administrator must file the reports with the DOL by the last day of the seventh month following the close of the plan year.

Form 8955-SSA Disclosure of vested account balance and form of benefit to plan participants who have separated from service

The plan administrator must provide the statement by the last day of the seventh month, following plan year end (plus extensions)

Form 1099-R The plan administrator must generate a Form 1099-R for each plan participant or beneficiary that receives a 401(k) plan distribution.

The plan administrator must file with the IRS by February 28 (March 31 if filing electronically) of the year after distribution.

Form 1098-Q The QLAC issuer must generate a Form 1098-Q for each plan participant who purchases a QLAC.

The plan administrator must file with the IRS by February 28 (March 31 if filing electronically).

Form 945 The plan administrator must file Form 945 to report all withholding on nonpayroll distributions.

The plan administrator generally must file by January 31 of the year following the year to which it relates.

IRS Disclosure/Reporting

Reports and Notices – 29

REQUIRED DOCUMENTS DESCRIPTION TIMING

SPD Provides vital plan information in an easily understood manner.

File with DOL if requested.

SMM Summary of changes to the document that also affect the SPD; or may provide updated SPD.

File with DOL if requested.

Department of Labor Disclosure/Reporting

REQUIRED DOCUMENTS DESCRIPTION TIMING

Form 945-A Certain plan administrators deemed “semiweekly depositors” must file Form 945-A to report the withholding amount collected each day.

This form is attached to Form 945.

Ascensus provides administrative and recordkeeping services and is not a broker-dealer or an investment advisor .

237 (4/2020)