q2 2015 financial results - rns submit to the current status of the company and its business, ......

TRANSCRIPT

Q2 2015 Financial Results

DISCLAIMER

This presentation includes statements data, forecasts, goals and Company plans that are "forward-looking statements“, as defined in the Securities Law - 1968, whose occurrence is not certain and which are not solely in the Company's control. These forward-looking statements are included, inter alia, in discussions of strategy, objectives, goals, plans, events, future intentions or other information relating to future events or issues whose occurrence is not certain.

By their nature, forward-looking statements involve risk and uncertainty. Whether the forward looking information occurs or not is affected, inter alia, by risk factors characteristic to the Company's operations and developments in the general environment and external factors which impact the Frutarom Group and its area of activities.

This forward looking information could include facts and data based on the Company's subjective assessment, including with regards to the current status of the Company and its business, the current situation in the industry in which the Frutarom Group operates, macro-financial facts and information, all as are known to the Company on the date on which this presentation was prepared, some of which were given to the Company by external sources, the content of which was not independently examined by the Company, and therefore the Company is not responsible for their verity.

This presentation must be read together with the Company's periodic and immediate reports, and was not meant to replace the need for study of reports the Company has published, including, inter alia, the Company's periodic report for 2013, published on March 2014, and the Company's periodic reports subsequently published. These reports could include, inter alia, updates to the information regarding the Company's activities or of the forward looking statements appearing in this presentation.

Subject to the requirements of applicable law, the Company does not intend to update any industry information or forward-looking statements appearing in this presentation, and is not required to publish any additional presentations for its shareholders in future.

It is to be emphasized that the financial estimations and the pro-forma figures included in this presentation are based on figures which were not audited or reviewed by an auditor and therefore the actual results may differ from these financial estimations.

2

Frutarom - A Leading Fast Growing Global Flavor and Fine Ingredient House

Global company Broad product

portfolio Public company

Financial success since 2000

•Sales in over 150 countries •19,000 customers • A Top 10 flavor

house

•43,000 products •Over 4,000 raw

materials • Innovative

pipeline

•Listed on London & TLV Stock Exchanges •From $13M to

approx. $2.2 market cap

•10.1x growth in sales (CAGR 18%) •16.8x growth in

EBITDA •21.9x growth in net

profit

3

Frutarom - A Profitable Growth Story

4

Frutarom - A Global Company • 2000-2014 Sales CAGR of 18%

Sales office Acquisition

2006 2007 2009 2012 1990-2000 2003-2004 2011 2001-2002 2013 2005

1996 Tel Aviv stock exchange

IFF FS

Adumim

Raychan

Rieber

EAFI

Savoury Flavours

Oxford

Belmay

Jupiter

FSI Corona

Nesse

CH Hansen DE

CH Hansen IT

Etol

Mylner

Aromco

FSI OH

Acatris

Flachsmann Tohar

Meer

Rayner HK F&F

CPL Aroma

Flavour Key

Baltimore

Botanicare Kunshan

AM Todd

Russia

Canada

Turkey

France

Mexico

Ukraine

Poland

Kazakhstan

Hong Kong

Costa Rica

Czech Rep.

S. Africa

India

Brazil

Gewurzmuller

Abaco

Rad

London stock

exchange

JannDeRee

PTI

Aroma

Hagelin

2014

Citrasource

Montana

2015

Ingrenat

Food Blenders

5

Sonarome

BSA

Taiga

Vitiva

Foote&Jenks

Taura

Scandia

Sales & Marketing – 74 Offices

Production – 44 Sites

R&D – 44 Labs

Frutarom - A Global Company We provide our customers with global and local support

Belgium

Brazil

China

Denmark

France

Germany

India

Indonesia

Israel

Italy

Kazakhstan

Mexico

Netherlands

Norway

Poland

Serbia

Singapore

Slovakia

Slovenia

South Africa

Turkey

Ukraine

UK South

UK North

Corona, CA New Jersey

Cincinnati, OH Switzerland

Moscow Saint Petersburg

Perm Saratov

Hong Kong

Costa Rica

Georgia

Guatemala

Novosibirsk Belarus

Moldova

Florida

Peru

Chile

6

Australia

New Zealand

Canada

Growth Rate

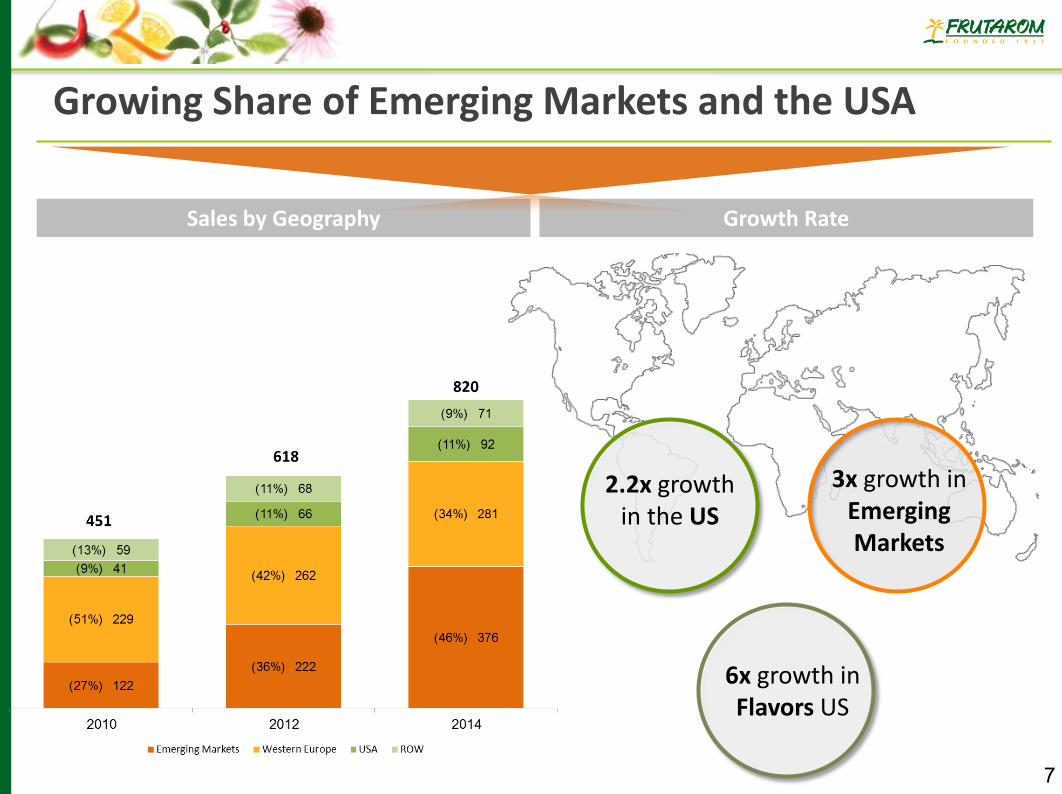

Growing Share of Emerging Markets and the USA

Sales by Geography

3x growth in Emerging Markets

2.2x growth in the US

6x growth in Flavors US

7

Hagelin • Strengthening position in the US and EM. • Expertise in Beverage

CitraSource • Strengthening Citrus capabilities & leadership • Presence in Florida – World

Center for Citrus

Recent Acquisitions – Realization Our Strategy

Continue to improve product mix & Strengthen position

in Health & Wellness

Geographic Focus Natural & Healthy

Emerging Markets

PTI Russia & CIS

• Strengthening Leadership in East Europe • Savory Solutions leadership

Aroma Guatemala

Strengthening market position in Central America

Vitiva Slovenia

• Food protection • Natural Colors • Health Ingredients

Montana Food Peru & Chile

Montana Food Peru & Chile

Strengthening market position in South America

• Natural Colors

Ingrenat Spain

• Food protection • Natural Colors

Opportunities for additional improvement in margins 8

North America

BSA Canada , India • Strengthening savory position

in North America and India

Sonarome India Strengthening market position in India and Africa

Leveraging Synergies

Strong management, R&D and sales

Taura Belgium, New Zealand • Leading position in New Zealand

and Australia • Strengthening market position in Natural

Fruit Based Ingredients and specialty solutions

Scandia Citrus • Strengthening position in the US. • Expertise in specialty solutions in Citrus

Cross Selling opportunities

Optimization & Savings

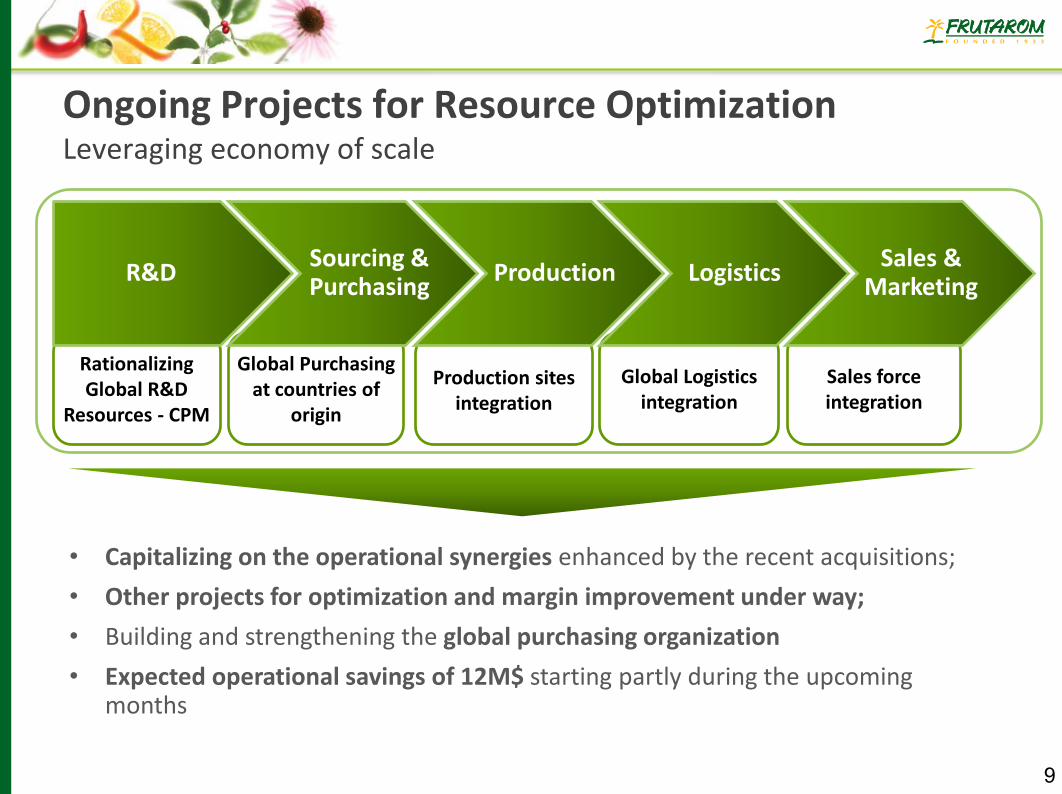

Ongoing Projects for Resource Optimization Leveraging economy of scale

Rationalizing Global R&D

Resources - CPM

Global Purchasing at countries of

origin

Production sites integration

Global Logistics integration

Sales force integration

Production Sourcing & Purchasing

Logistics Sales &

Marketing R&D

• Capitalizing on the operational synergies enhanced by the recent acquisitions;

• Other projects for optimization and margin improvement under way;

• Building and strengthening the global purchasing organization

• Expected operational savings of 12M$ starting partly during the upcoming months

9

10

H1 Business Update -

1 Pro-forma growth - Assuming acquisitions performed in 2015 had been consolidated in the appropriate parallel period of 2014 and that Montana Food,

acquired during the fourth quarter of 2014, had been consolidated as of January 1, 2014.

• Continuous growth in above industry average rate

• H1 YoY LFL growth1 of 6.1%; Q2 YoY LFL growth1 of 4.8%

• Improving value proposition to costumers through expansion of products portfolio and leverage of Cross-Selling

• Nine acquisitions in 2015 with yearly sales of 125M$; Five acquisitions during Q2 2015 with yearly sales of 97M$

• Geographic focus on high growth spots - Continues strengthening position in North-America and India; First strategic acquisition in Asia-Pacific; Deepening position in Citrus field and Savory Solutions in North-America

• Strategic acquisitions with product & technology focus - Entering into growing and profitable fields such as natural colors and food protection by natural solutions

• Strong future acquisition pipeline

• After undergoing internal growth averaging 4.4% in 2014 and 5.3% in Q1 2015, Q2 2015 sales were affected by some stockpiling of inventory among a number of customers who temporarily reduced their purchases

• H1 YoY LFL growth of 0.2%; Q2 YoY LFL sales declined 4.9%

• Customers have recently resumed placing orders and their rate of purchases is expected to grow in the upcoming months

• Continue working towards optimizing resources to create operational savings and strengthening competitive position • Strengthening global purchasing system while utilizing the increased purchasing power with emphasis on turning to source

countries for the purchase of raw materials • Expected operational savings of 12M$ starting partly during the upcoming months • Non-recurring expenses of 2.2M$ related to operational efficiency and in connection with acquisitions

M&A

FLAVORS

FINE INGREDIENTS

OPTIMIZATION &

SAVINGS

11

H1 Business Update -

• Strengthening position in India through Sonarome and BSA acquisitions • Deepening penetration to the Asia Pacific region through Taura acquisition

• Entering Canadian Market with the acquisition of BSA • Construction has been completed on new state-of-the-art plant in China which features sophisticated laboratories for

R&D and applications

• H1/2015 - Equity/Assets ~ 46%; Net Financial Debt/Assets ~ 26% • Solid balance sheet supports future M&A activity in line with growth strategy • Acquired companies mainly during mid-end Q2/2015 already consolidated in balance sheet ; Will start to contribute

to sales and profitability starting Q3/2015

• USD considerably strengthening against most other global currencies continued during Q/2 2015 • The effect of currencies on reported USD sales was 14.4% in Q2 2015 and 14.0% in H1 2015 • Exposure to currency fluctuations is reduced by the fact that raw material purchases and operational expenditures in

various countries also paid for in most cases in the respective local currencies • Currency affect on reported USD-based results is expected to reduced at the beginning in Q4 2015 if exchange rates

remain at their current levels

FINANCIAL POSITION

GLOBAL PRESENCE

CURRENCY HEADWIND

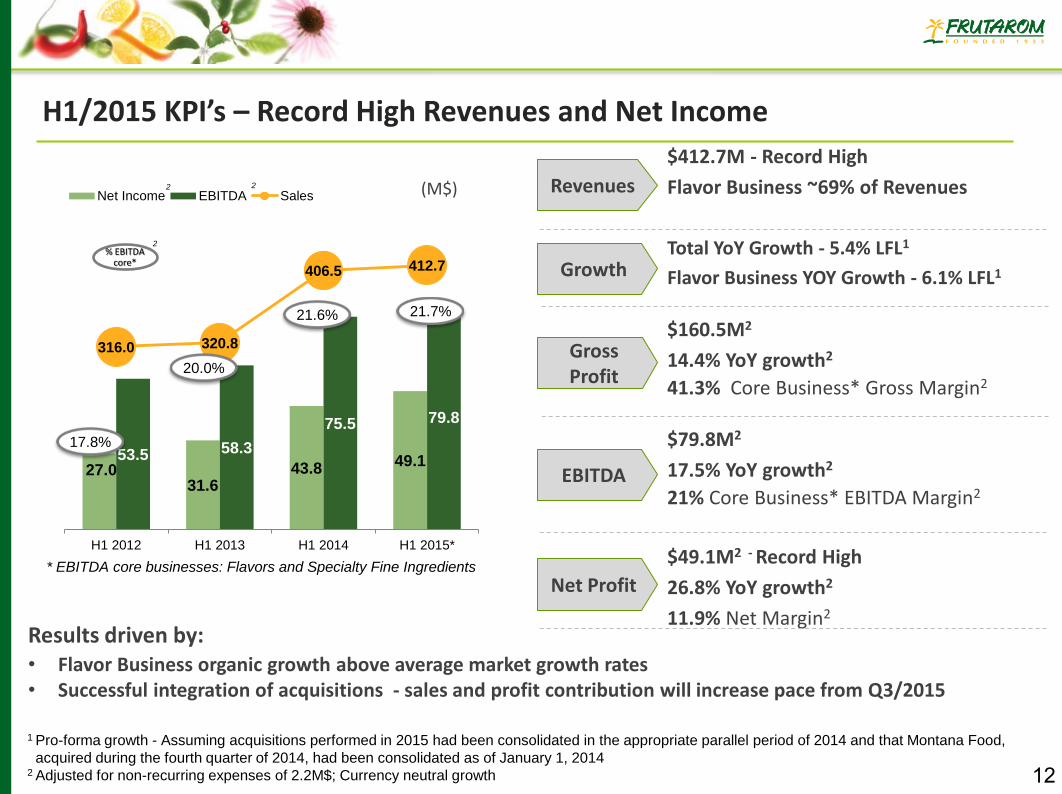

H1/2015 KPI’s – Record High Revenues and Net Income

* EBITDA core businesses: Flavors and Specialty Fine Ingredients

$412.7M - Record High

Flavor Business ~69% of Revenues

Total YoY Growth - 5.4% LFL1

Flavor Business YOY Growth - 6.1% LFL1

$160.5M2

14.4% YoY growth2

41.3% Core Business* Gross Margin2

$79.8M2

17.5% YoY growth2

21% Core Business* EBITDA Margin2

$49.1M2 - Record High

26.8% YoY growth2

11.9% Net Margin2

Gross Profit

EBITDA

Growth

Revenues

Net Profit

1 Pro-forma growth - Assuming acquisitions performed in 2015 had been consolidated in the appropriate parallel period of 2014 and that Montana Food,

acquired during the fourth quarter of 2014, had been consolidated as of January 1, 2014 2 Adjusted for non-recurring expenses of 2.2M$; Currency neutral growth

12

(M$) 2 2

Results driven by: • Flavor Business organic growth above average market growth rates • Successful integration of acquisitions - sales and profit contribution will increase pace from Q3/2015

2

27.0 31.6

43.8 49.1 53.5 58.3

75.5 79.8

316.0 320.8

406.5 412.7

H1 2012 H1 2013 H1 2014 H1 2015*

Net Income EBITDA Sales

% EBITDA core*

17.8%

20.0%

21.6% 21.7%

17.0%

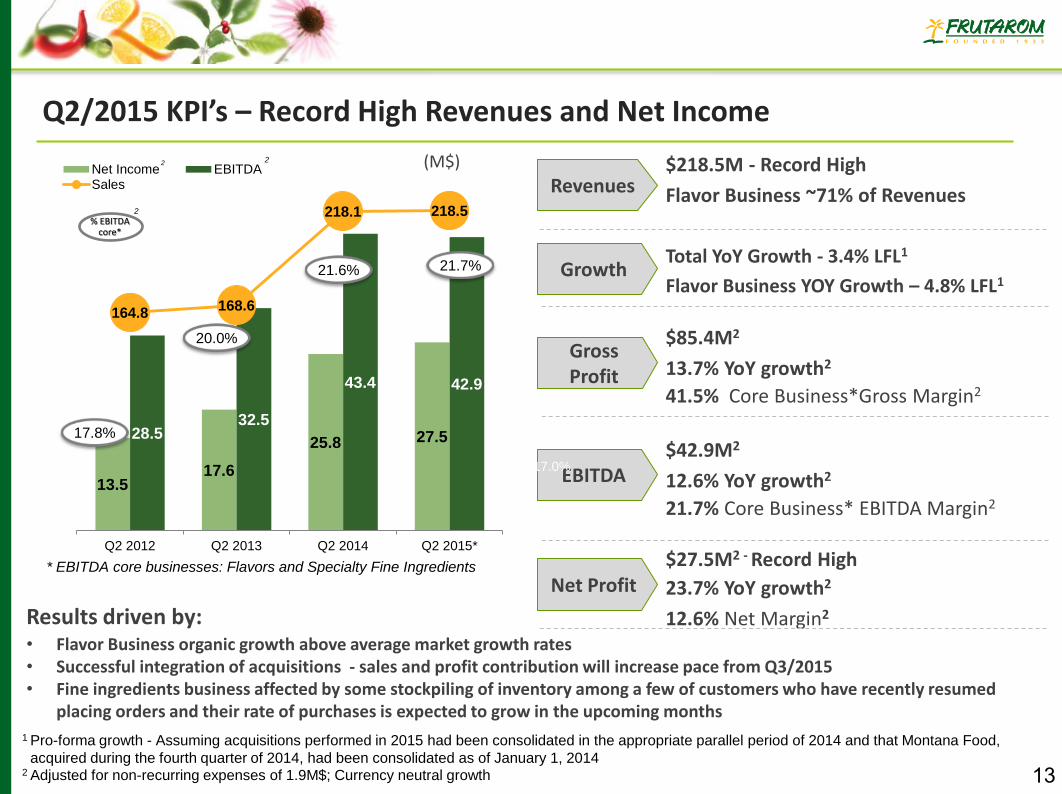

Q2/2015 KPI’s – Record High Revenues and Net Income

* EBITDA core businesses: Flavors and Specialty Fine Ingredients

$218.5M - Record High

Flavor Business ~71% of Revenues

Total YoY Growth - 3.4% LFL1

Flavor Business YOY Growth – 4.8% LFL1

$85.4M2

13.7% YoY growth2

41.5% Core Business*Gross Margin2

$42.9M2

12.6% YoY growth2

21.7% Core Business* EBITDA Margin2

$27.5M2 - Record High

23.7% YoY growth2

12.6% Net Margin2

Gross Profit

EBITDA

Growth

Revenues

Net Profit

1 Pro-forma growth - Assuming acquisitions performed in 2015 had been consolidated in the appropriate parallel period of 2014 and that Montana Food,

acquired during the fourth quarter of 2014, had been consolidated as of January 1, 2014 2 Adjusted for non-recurring expenses of 1.9M$; Currency neutral growth

Results driven by: • Flavor Business organic growth above average market growth rates • Successful integration of acquisitions - sales and profit contribution will increase pace from Q3/2015 • Fine ingredients business affected by some stockpiling of inventory among a few of customers who have recently resumed

placing orders and their rate of purchases is expected to grow in the upcoming months

13

2 2

2

13.5 17.6

25.8 27.5 28.5 32.5

43.4 42.9

164.8 168.6

218.1 218.5

Q2 2012 Q2 2013 Q2 2014 Q2 2015*

Net Income EBITDASales

% EBITDA core*

17.8%

20.0%

21.6% 21.7%

17.0%

(M$)

Above-Industry Organic Growth

Frutarom’s Strategic Goals

Over $1.5 billion in revenues by 2020

Proven Acquisition

Track Record

Margin Expansion

Continue successful strategy of combining rapid profitable organic growth with strategic acquisitions

Over 22% EBITDA in our core business by 2020

Over $1.5 billion in revenues by 2020

* Given current product mix

*

14

Maintain Positive Outlook for 2015-2016

Profitable internal growth in core business

Focus on innovative, health oriented, natural product mix

Successful integration of the recent acquisitions

Additional projects to improve efficiency and merge activities and operations

Strengthening & leveraging global purchasing

Strong acquisitions pipeline

15

Frutarom’s Vision

To Be The Preferred Partner For Tasty And Healthy Success