q2 2007 telus investor conference call august 3, 2007

TRANSCRIPT

Q2 2007 TELUS investor conference call

August 3, 2007

This session and answers to questions contain forward-looking statements that require assumptions about expected future events including 2007 guidance, competition, financing, financial and operating results, and regulation that are subject to inherent risks and uncertainties. There is significant risk that predictions and other forward looking statements will not prove to be accurate so do not place undue reliance on them.

Factors that could cause actual results to differ materially include but are not limited to: competition; capital expenditure levels (including possible spectrum purchases); financing and debt requirements (including share repurchases, debt redemptions and refinancing plans); tax matters (including acceleration or deferral of payment of significant cash taxes); regulatory developments (including local forbearance, local number portability, the timing, rules, process and cost of future spectrum auctions, and possible changes to foreign ownership restrictions); process risks (including conversion of legacy systems and billing system integrations); and other risk factors discussed herein and listed from time to time in TELUS’ reports.

There are many factors that could cause actual results to differ materially. For a full listing and description of the potential risk factors and assumptions, please refer to the TELUS 2006 annual report and updates in the 2007 quarterly reports (see Section 10 Risks and Risk Management in Management’s discussion and analysis), and other filings with securities commissions in Canada (sedar.com) and the United States (sec.gov).

All dollars referenced are in C$ unless otherwise specified.

TELUS forward looking statements

2

Darren Entwistlemember of the TELUS team

August 3, 2007

Q2 2007 TELUSinvestor conference call

TELUS pursued discussions on benefits of acquisition to June 26

Potential for TELUS to pursue offer on investment grade model

Completed assessment of this opportunity considering

Disadvantageous auction process

Substantive price offered by private equity consortium

Deteriorating debt market conditions

Positive benefits of not bidding

Timeline and uncertain outcome of competition approval

Risk to TELUS shareholders

TELUS does not intend to submit a competing offer

Decision on BCE acquisition

4

Stand-alone TELUS can continue to create future value

Wireline highlights – Q2 2007

5

Committed to consolidated care platform and its benefits

Resilient wireline revenue as per operating strategy

Data growth continues to be strong at 8%

Moderate NAL loss at 3%

Converted Alberta consumers to new customer care platform

Critical billing function performed well

Initial difficulties reduced capability for new orders

Additional resources impacted EBITDA by $29 million

Backlogs and call centre operations returning to normal

Major $200 million contract with Department of National Defence

Local forbearance in key markets beginning

Fort McMurray residential service deregulated July 25th

Large urban markets waiting for deregulation decisions

Vancouver, Victoria, Calgary, Edmonton, and Rimouski

Wireline highlights – Q2 2007

6

Continued resiliency in wirelineNew regulatory framework based on market forces

Wireless highlights – Q2 2007

7

Wireless Number Portability impacts

Churn increased 15 basis points

Higher gross and net additions contributed to higher COA

Investment in customer retention increased 32%

Wireless revenue growth of 11%

18th consecutive quarter of increased year over year ARPU

Data revenue growth up 64%

Operating profit (EBITDA) increased by 3%

Continued resiliency in wirelineReiterating full year wireless segment guidance

Wireless highlights – Q2 2007

8

AMP’D Mobile entered bankruptcy proceedings in U.S.

TELUS discontinuing sales in Canada

Continued rollout of high-speed EVDO and EVDO Rev A network

Introduction of new CDMA/GSM Blackberry World Edition

Advanced Wireless Services spectrum auction

Rules expected in fall for auction early 2008

TELUS advocates an open and fair auction process

Continued resiliency in wirelineCanadian wireless industry remains competitive and successful

Consolidated highlights – Q2 2007

9

Strongly positioned to advance growth strategy

Committed to improving performance in coming quarters

Second quarter impacted by special events

Committed to original consolidated guidance for 2007

Balancing interests of debt and equity holders

Refinanced $1.5 billion 7.5% notes at lower interest cost

Repurchased $170 million of shares in quarter

Repurchased 45.6 million shares for $2.1 billion since 2004

Quarterly per share dividend 37.5 cents, up 36%

Robert McFarlaneEVP & Chief Financial Officer

August 3, 2007

Q2 2007 TELUSinvestor conference call

Wireless segment – Q2 2007 financial results

11

($M) Q2-06 Q2-07 Change

Revenue 945 1,048 11%

EBITDA1 441 451 2.2%

Capital expenditures 147 173 17%

1 EBITDA includes non-cash charge of $1.8M in Q2-07 for net cash settlement feature of options granted prior to 2005. Excluding this charge EBITDA (as adjusted) increased by 2.7%

Higher COA & retention costs related to WNP impacted EBITDA while EVDO Rev A investments contribute to capex increase

WNP update

12

Results reflect first full quarter of WNP

Industry1 TELUS

Gross additions 8.0 % 16%

Net additions 1.6% 3.5%

Churn 6 bps 15 bps

COA 3.0% 7.9%

1 Based on Q2-07 wireless results from Rogers, Bell, and TELUS

Wireless EBITDA normalization

13

($M) Q2-06 Q2-07 Change

EBITDA (as adjusted)1 441 453 2.7%

Incremental COA (due to higher loading) - 20

Incremental cost of retention (COR) - 27

EBITDA (excl. incremental COA & COR) 441 500 13%

With advent of WNP, higher COA and COR significantly affected EBITDA growth

1 Excludes non-cash charge of $1.8M in Q2-07 for net cash settlement feature of options granted prior to 2005.

Amp’d Mobile Canada Update

14

Parent Amp’d Mobile, Inc. entered bankruptcy in U.S. in June

Disruptions of Amp’d Live content expected - Amp’d Mobile sales discontinued in Canada

Voice and basic messaging services continue for Amp’d clients

Migration of Amp’d Canada subscribers now underway

No notable impact expected on reported revenue or subscribers

Impact of writedowns on Q2-07 results: $11.8M write-off in ‘other expenses’ for Amp’d US venture capital

investment Approx. $2M opex impact on EBITDA $5M for accelerated depreciation of assets used to support Amp’d Negative EPS impact of approximately 4 cents

Amp’d Mobile subscribers being migrated to TELUS

total wireless subscribers

Postpaid 80%

Prepaid 20%

net additions

Q2-06 Q2-075.3 million

4.2M

1.0M

Wireless subscriber results

Continued strong net additions

15

prepaid

postpaid128K124K

77%83%

Wireless ARPU growth

Data ARPU

Q2-07

$63.65

6.58

57.07

16

48% increase in data more than offsetting voice decline

Voice$63.18

4.45

58.73

Q2-06

1.61.8

1.451.3

Source: Company reports, analyst reports. Sprint Nextel and T-Mobile USA Q1-07.

* TELUS estimates for Rogers blended churn – not including 90K TDMA subscriber write down in Q2-07

2.6

1.6*

Q2 2007 wireless churn (%)

Churn remains at best in class levels

17

2.7

Wireline segment – Q2 2007 financial results

18

($M) Q2-06 Q2-07 Change

Revenue 1,190 1,180 (0.8)%

EBITDA (reported) 456 434 (4.9)%

Capital expenditures 311 309 (0.9)%

Results impacted by implementation of new wireline billing and client care system in Alberta

Wireline revenue profile

19

($M) Q2-06 Q2-07 Change

Voice – Local 523 516 (1.5)%

Voice – Long Distance 206 168 (19)%

Data 403 435 7.8%

Other 58 62 7.6%

Total External Revenue 1,190 1,180 (0.8)%

Continued solid data growth offsets local and LD erosion

Long distance revenue normalized

($M) Q2-06 Q2-07 Change

Long distance revenue (reported) 206 168 (19)%

One-time system implementation adjustment

(13)

Long distance revenue (normalized) 206 181 (12)%

20

Flat to positive wireline revenue growth adjusted for system implementation impact

Total external revenue (excl. system impacts)

1,190 1,193 0.3%

Wireline EBITDA normalization

21

($M) Q2-06 Q2-07 Change

EBITDA 456 434 (4.9)%

System implementation impacts:

LD revenue adjustment

Increased labour costs

-

-

(13)

(16)

EBITDA (excl. system impacts) 456 463 1.5%

System implementation significantly impacted wireline EBITDA

1.13 million total

Internet subscribers

High-speed85%

Dial-up15%

High-speed Internet net additions

Q2-06 Q2-07

963K

172K

High-speed Internet subscribers

Results reflect system implementation in AlbertaLowering annual guidance from > 135K to > 125K

22

29K

14K

% of network access lines lost (yr. over yr.)

Q1-06

-2.7%

Q2-06

-2.6%

Q3-06

-2.8%

Q4-06

-3.0%

Network access line results

-2.9%

Q1-07

Stable overall line losses due to business line growth

23

-3.1%

Q2-07

Wireless

High-speed Internet

Dial-up Internet

Res NALs

Bus NALs

(millions)10.910.4

Q2-07Q2-06

9.9

Q2-05

TELUS total subscriber connections

24

Connections increasing with wireless and Internet growth

Consolidated – Q2 2007 financial results

25

($M excluding EPS) Q2-06 Q2-07 Change

Revenue 2,135 2,228 4.4%

EBITDA1 897 885 (1.4)%

EPS (reported) 1.03 0.76 (26)%

EPS (excl. tax adjustments) 0.69 0.73 5.8%

Capital Expenditures 459 482 5.0%

Increased expenses related to WNP, new system implementation & Amp’d affected results

1 EBITDA includes non-cash charge of $1.8M in 2007 for net cash settlement feature of options granted prior to 2005. Excluding this charge EBITDA (as adjusted) decreased by 1.2%

$1.03

Q2-06

Other(incl.

lower avg o/s shares)

Net tax related

adjustments

EPS continuity

26

Billing & client care

system

Q2-07Amp’d write-down

$0.31

$0.14

$0.04

COA & COR

$0.76

Normalized EBITDA1

1 Normalized to exclude billing system, restructuring, acquisition & retention, and AMP’d impacts

$0.13

$0.06

$0.08

$0.05

Restructuring costs

Share buy backs – 3rd Normal Course Issuer Bid

27

Q2-07 In 2007Since NCIB

inception

Total investment (M) $170 $370 $2,140

Total shares (M) 2.7 6.2 45.6

Shares outstanding (M) - 331.7 26.8

% change in o/s shares(end of period)

1.8%

Year to date

7.5%

since Dec-04

Outstanding shares already 2% lower than at 2006 year end

Strong record of returning capital

1

2

3

4

2003 2004 2005 2006 2007E1,2

Dividends

Share repurchases

$ per share

0.60

3.30 3.43

0.82

3.73

0.801.10

1.50

0.60

2.33

0.22

2.50

2 See forward looking statement caution.

1 Annualized dividend, plus YTD NCIB share repurchases as at June 30/07, annualized

2.23

28

1.11

Launched unsecured commercial paper program in Q2

Backstopped by credit facility

Can issue up to $800 million

$664 million issued, as at June 30

Successfully raised $1 billion in March at 4.8% blended

Redeemed $1.5 billion 7.5% Notes on June 2007 maturity

Financing update

29

Strong balance sheet with extended maturities and lower interest

TELUS debt maturity schedule ($M)

No significant debt maturities until 2011

Debt Deferred FX Hedge Liability

30

0500

1,0001,500

2,000

2,5003,000

$ 3,500

2007 2008 2009 2010 2011 2012 2013 2014+

2007 guidance* - consolidated

2007 guidance1 YoY growth

Revenue $9.175 to $9.275B 6 to 7%

EBITDA (as adjusted)2 $3.725 to $3.825B 4 to 7%

EPS (as adjusted)3 $3.25 to $3.45 17 to 24%

Capital expenditures approx. $1.75B 8%

Original consolidated guidance reconfirmed

* See forward looking statement caution

2 Excludes expense of approx. $180 million in 2007 for net cash settlement feature for options.3 Excludes an after-tax charge per share of approx $0.33 for cash settlement feature for options. Year over year growth rate normalized for $0.48 of positive tax-related adjustments in 2006.

1 Confirmed August 3, 2007

31

($8)

135

$191

19

(0.7)

(459)

$897

Q2-06

$286

350

$186

(7)

(3)

(482)

$885

Q2-07

Funds avail. for debt redemption

Accounts Receivable Securitization

Free cash flow (before cash settled option pmt)

Restructuring payments (net of expense)

Cash income taxes; and other

Capex

EBITDA

($M)

(271) (213)Interest expense paid

13 15Non-cash portion of share-based compensation

(95) (125)Dividends

13 0.2Share Issuance (non-public)

($18) ($532)Net change in cash

(10) (817)Net debt issuance / (repayment)

Working capital & other (2) 68

(249) (170)Purchase of shares for cancellation (NCIB)

Appendix – Free cash flow (2007 definition)

(8)

(9)Cash related to other expenses

Free cash flow $191 $162

Cash settled options paid -

(24)

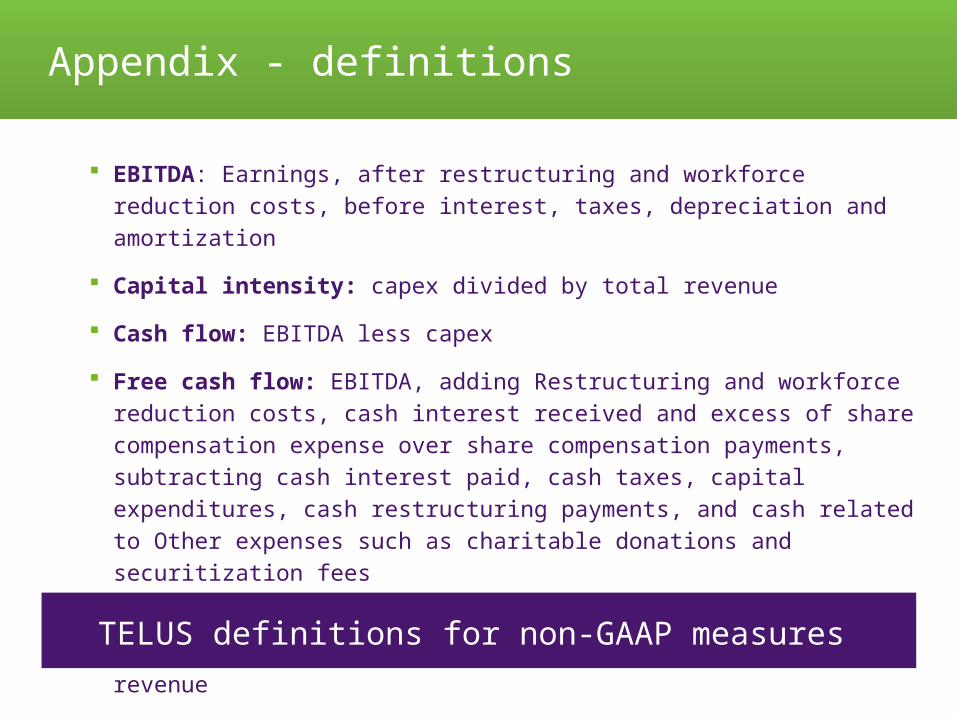

EBITDA: Earnings, after restructuring and workforce reduction costs, before

interest, taxes, depreciation and amortization

Capital intensity: capex divided by total revenue

Cash flow: EBITDA less capex

Free cash flow: EBITDA, adding Restructuring and workforce reduction costs,

cash interest received and excess of share compensation expense over share

compensation payments, subtracting cash interest paid, cash taxes, capital

expenditures, cash restructuring payments, and cash related to Other expenses

such as charitable donations and securitization fees

Cost of retention (COR): total costs to retain existing subscribers, often

presented as a percentage of network revenue

Appendix - definitions

TELUS definitions for non-GAAP measures