q1 fy10 20.06.09 2.30pm final.ppt - jsw.in coke consumption increased from 54.9% to 87.1% fluxes...

TRANSCRIPT

Q1 FY10

Global Development

Steel Scenario

Agenda

Financial Performance

Project Progress

2

Global DevelopmentGlobal DevelopmentGlobal DevelopmentGlobal Development

3

Global Development

Global growth rates revised upwards

IMF Revised GDP growth projection for 2010

2010 20102010

2009 2009

2009

-1.3

-3.8

1.6

-1.4

-3.8

1.51.9

0

4

2.5

0.6

4.7

World Adv. Economies Emerging Economies

%

Apr09 Est. July09 Est.

0

10

20

30

40

50

60

70

80

90

Jan

-07

Ma

r-0

7

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Ma

r-0

8

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Ma

r-0

9

Ma

y-0

9

Jul-

09

Receding volatility in the stock market

CBOE Volatility Index

80

100

120

140

160

180

Jan

-09

Jan

-09

Jan

-09

Fe

b-0

9

Fe

b-0

9

Ma

r-0

9

Ma

r-0

9

Ap

r-0

9

Ap

r-0

9

Ma

y-0

9

Ma

y-0

9

Jun

-09

Jun

-09

Metals Food Agricultural raw materials Crude oil

0%

2%

6% 6%

8%

12%

14%

RMB JPY INR EURO RUB GBP BRL

Commodity prices moving up USD depreciates against major currencies

Period: April 1,2009 to June 30,2009

Source: IMF/ Bloomberg/CBOE.com

CBOE: Chicago Board Options Exchange

World Adv. Economies Emerging Economies Jan

Ma

r

Ma

y

Jul

Se

p

No

v

Jan

Ma

r

Ma

y

Jul

Se

p

No

v

Jan

Ma

r

Ma

y

Jul

4

0

100

200

300

400

500

Jun-07 Oct-07 Feb-08 Jun-08 Oct-08 Feb-09 Jun-09

4.25 4.25

5.5

0.5

7.47

9

0.25

21.5

0.1

5.31 5.5

0.251 0.5

0.1

5.31 4.75

Federal Reserve

European Central

Bank

Bank of England

Bank of Japan

People's Bank of China

Reserve bank of

India

2008-Peak Jan-09 Jul-09

Interest rates continue to remain subdued

Global Development

TED Spread (bps)(%)

Easing Liquidity

-4.9 -2.6

2.4 4.5

40.8 42.2

53.4

68.9

Euro Area US Japan Britain Russia India Brazil China

2008-Peak Jan-09 Jul-09

BRIC: Stock indices firming up

% change from Dec31st 2008 to July 8, 2009 ($ terms)

Source: Economist/Bloomberg/Fxstreet.com 5

30.00

35.00

40.00

45.00

50.00

55.00

60.00

Jan

-07

Ma

r-0

7

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Ma

r-0

8

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Ma

r-0

9

-40.00

-30.00

-20.00

-10.00

0.00

10.00

20.00

Jan

-07

Ma

r-0

7

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Ma

r-0

8

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Ma

r-0

9

Economy showing signs of Recovery

Industrial Production Manufacturing Purchasing Managers Index

(Y-o-Y % Change)

Ap

r-0

9

Ap

r-0

9

-15

-10

-5

0

5

10

15

20

25

Jan

-07

Ma

r-0

7

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Ma

r-0

8

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Ma

r-0

9

World Advanced economies Emerging economies

Ma

y

Ma

y

Advanced economies Emerging economiesWorld Advanced economies Emerging economies

Retail Sales

(Y-o-Y % Change)

Source: IMFA

pr-

09

6

Steel ScenarioSteel ScenarioSteel ScenarioSteel Scenario

7

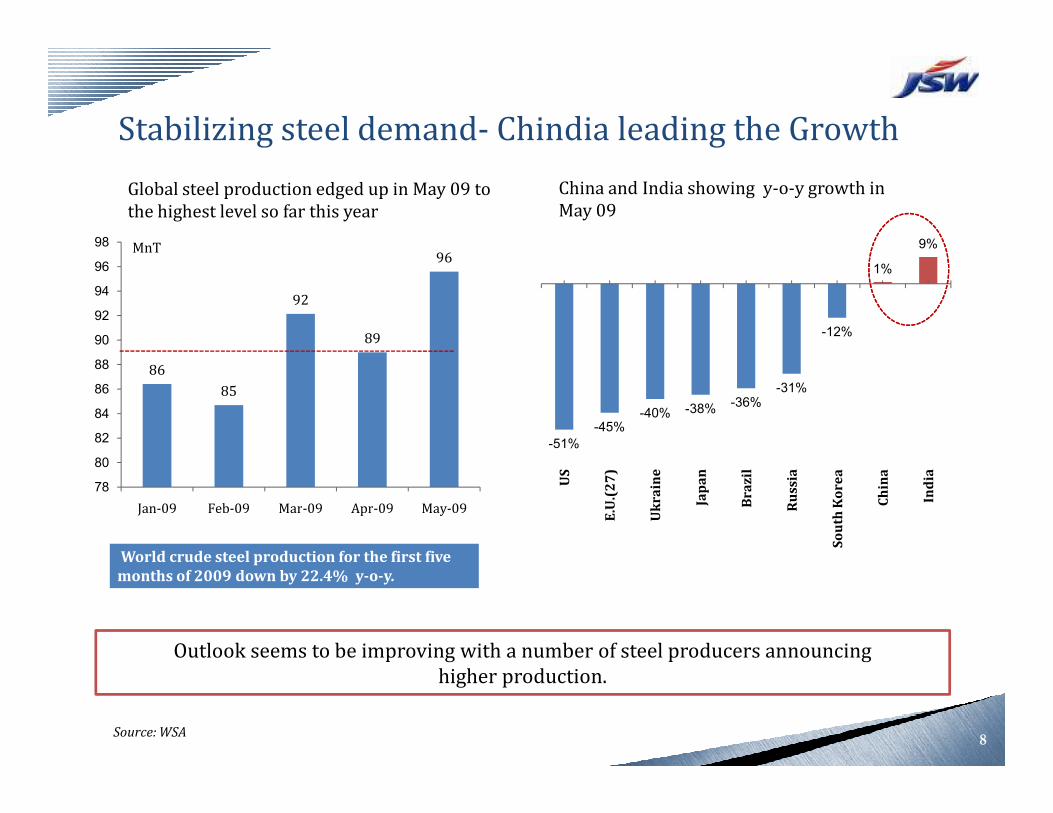

Global steel production edged up in May 09 to the highest level so far this year

86

85

92

89

96

84

86

88

90

92

94

96

98

-40% -38%-36%

-31%

-12%

1%

9%

China and India showing y-o-y growth in May 09

MnT

Stabilizing steel demand- Chindia leading the Growth

78

80

82

84

Jan-09 Feb-09 Mar-09 Apr-09 May-09

-51%

-45%-40% -38%

-36%

US

E.U

.(2

7)

Uk

ra

ine

Jap

an

Br

az

il

Ru

ssia

So

uth

Ko

re

a

Ch

ina

Ind

ia

Outlook seems to be improving with a number of steel producers announcing higher production.

Source: WSA8

World crude steel production for the first five

months of 2009 down by 22.4% y-o-y.

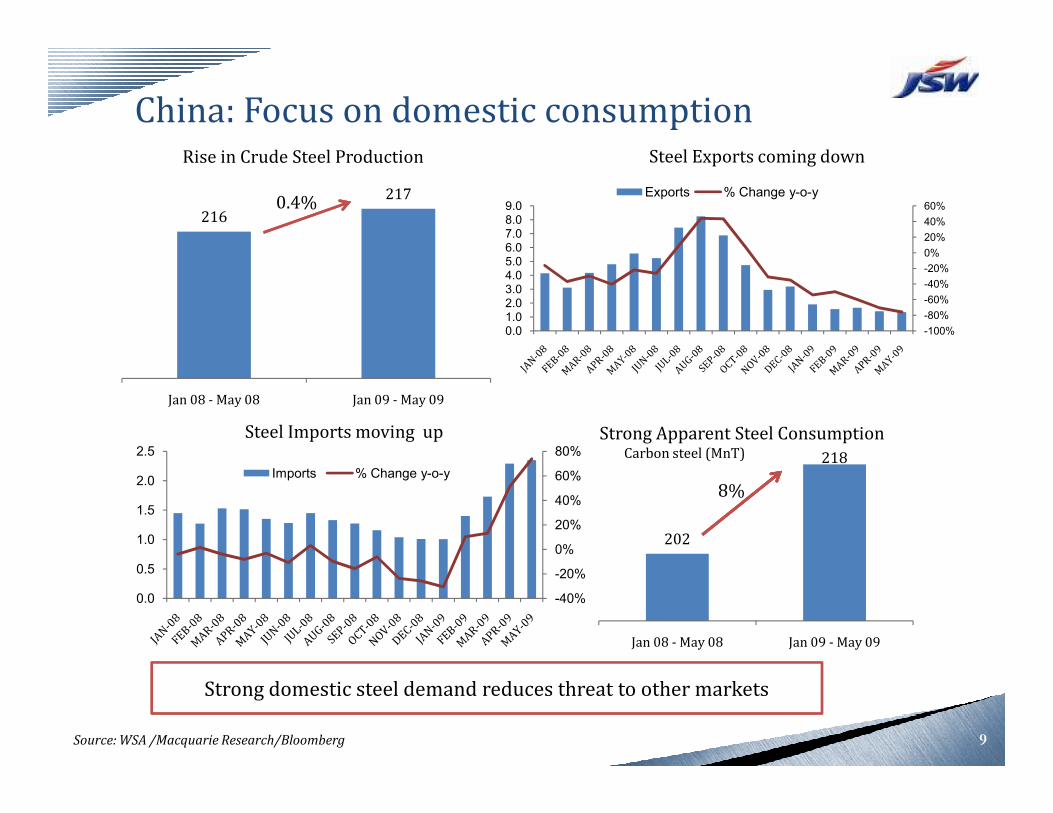

216

217

Jan 08 - May 08 Jan 09 - May 09

Steel Exports coming down

China: Focus on domestic consumptionRise in Crude Steel Production

0.4%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

0.01.02.03.04.05.06.07.08.09.0

Exports % Change y-o-y

-40%

-20%

0%

20%

40%

60%

80%

0.0

0.5

1.0

1.5

2.0

2.5

Imports % Change y-o-y

Jan 08 - May 08 Jan 09 - May 09

202

218

Jan 08 - May 08 Jan 09 - May 09

Strong domestic steel demand reduces threat to other markets

8%

Strong Apparent Steel ConsumptionCarbon steel (MnT)

Source: WSA /Macquarie Research/Bloomberg

Steel Imports moving up

9

India: Growth intactGDP growth rate(Y-o-Y % Change)

* RBI estimates

Sectoral Trends for Apr-May 09(Y-o-Y % Change)

10.5

6.5

11.7

3.9

1.9

0

2

4

6

8

10

12

14

Two Wheelers

Sales

PV Sales Cement Production

Infrastructure Index

IIP

9.5 9.79

6.75.7

FY06 FY07 FY08 FY09 FY10E *

Source: SIAM/JPC/EAC

* RBI estimates

Apparent Steel Consumption(MnT)

12.2

12.85.2%

13.5

14.0

Steel Production(MnT)

3.4%

Apr-Jun 09 Apr-Jun 09 Apr-Jun 08 Apr-Jun 08

10

Sales

Budget Boosters for the Industry

Allocation for programs that will support Infrastructure spending

� Allocation to Housing, NHAI, Railways, JNNRUM, APDPR ~Rs. 458 bn (USD 9.6 bn).

� Plan expenditure Rs. 3,251.5 bn ( USD 67.9 bn) increase of 34% over previous year.

� IIFCL will refinance 60% of commercial bank loans for PPP projects in critical sectors amounting Rs. 1,000 bn (USD 20.89bn).

Indian Steel industry to benefit from the proposed measures.

USD/Rs. = 47.87

Source : RBI reference rate as on 30.06.09

NHAI = National Highway Authority of India

JNNURM = Jawaharlal Nehru National Urban Renewal Mission

APDPR= Accelerated Power development and Reform Programme

IIFCL : India Infrastructure Finance Company Ltd.11

amounting Rs. 1,000 bn (USD 20.89bn).

� Excise duty for petrol driven trucks/lorries reduced from 20% to 8%.

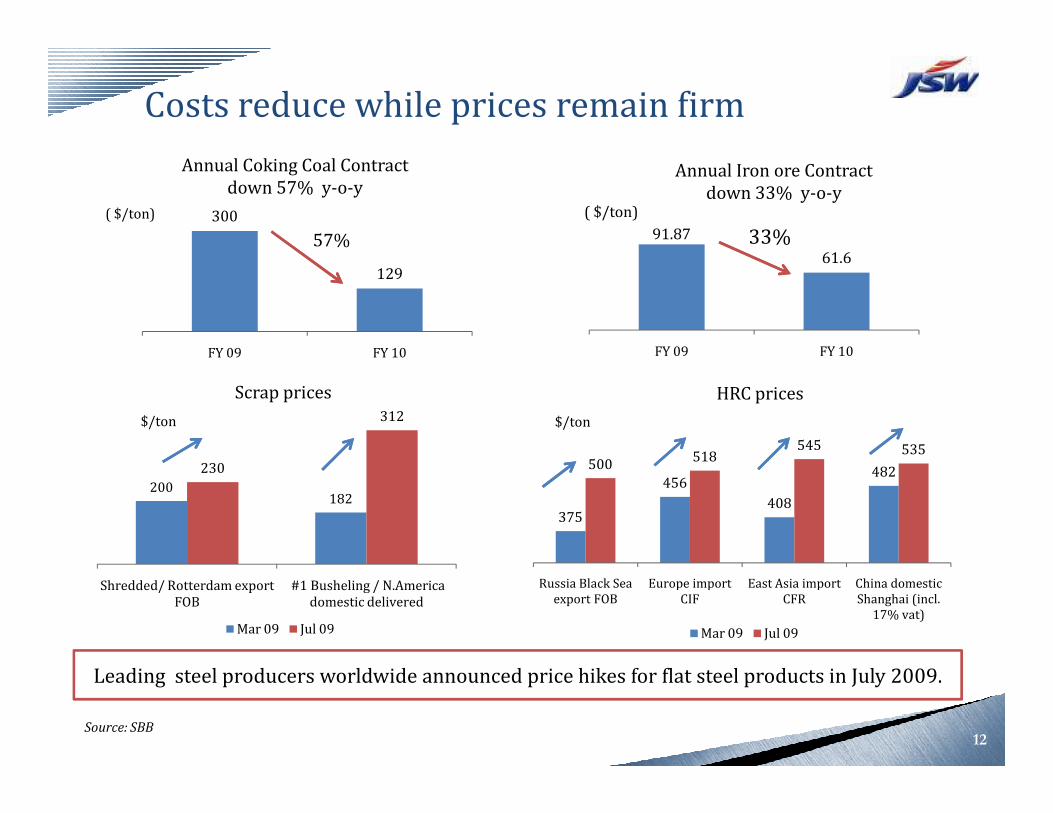

Costs reduce while prices remain firm

Scrap prices HRC prices

300

129

FY 09 FY 10

91.87

61.6

FY 09 FY 10

Annual Coking Coal Contract down 57% y-o-y

Annual Iron ore Contract down 33% y-o-y

( $/ton) ( $/ton)

57% 33%

375

456

408

482500

518545 535

Russia Black Sea export FOB

Europe import CIF

East Asia import CFR

China domestic Shanghai (incl.

17% vat)

Mar 09 Jul 09

200182

230

312

Shredded/ Rotterdam export FOB

#1 Busheling / N.America domestic delivered

Mar 09 Jul 09

$/ton$/ton

Source: SBB

Leading steel producers worldwide announced price hikes for flat steel products in July 2009.

12

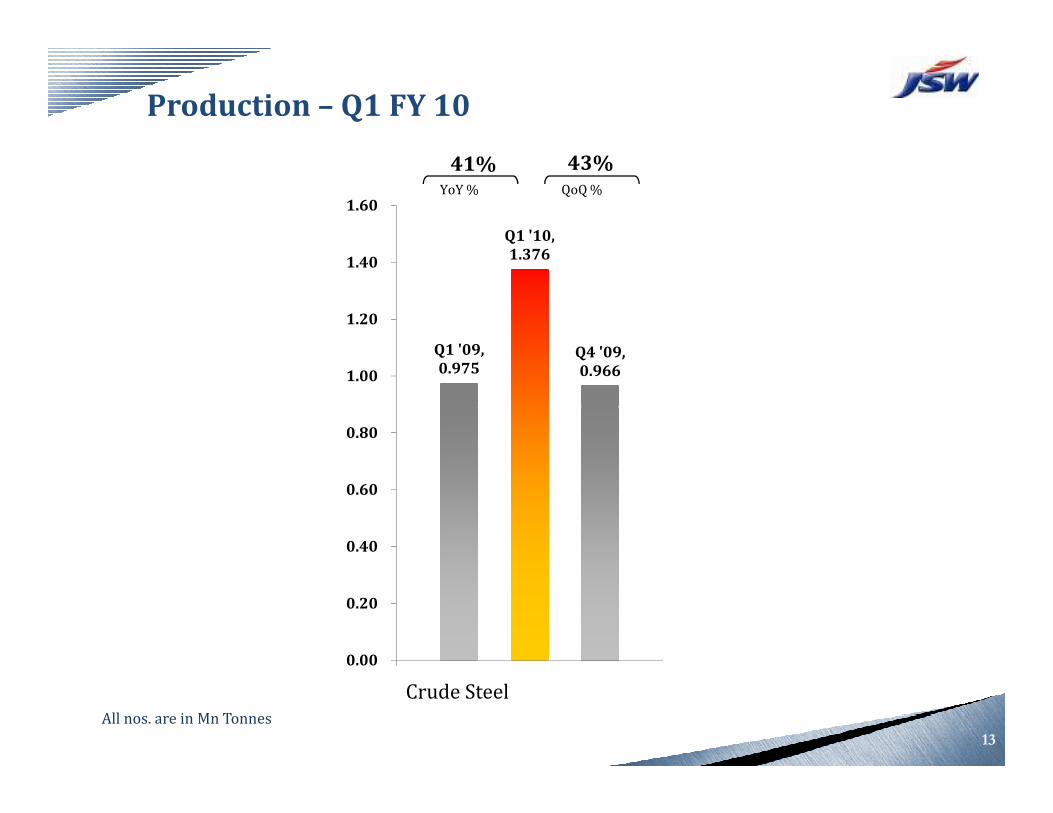

Production – Q1 FY 10

Q1 '09,

0.975

Q1 '10,

1.376

Q4 '09,

0.9661.00

1.20

1.40

1.60 YoY % QoQ %

41% 43%

13

0.00

0.20

0.40

0.60

0.80

Crude SteelAll nos. are in Mn Tonnes

Production – Q1 FY 10

Q1 '10,

0.181

YoY % QoQ %

98% 108%Q1 '09,

0.593

Q1 '10,

0.871Q4 '09,

0.826

Rolled : Flat

YoY % QoQ %

47% 5%

14

Q1 '09,

0.092Q4 '09,

0.087

Rolled : Long

Q1 '09,

0.161

Q1 '10,

0.227

Q4 '09,

0.23

Q1 '09,

0.23

Q1 '10,

0.355 Q4 '09,

0.322

CR / CRCA

YoY % QoQ %

54% 10%

GI / GL

YoY % QoQ %

41% -1%

All nos. are in Mn Tonnes

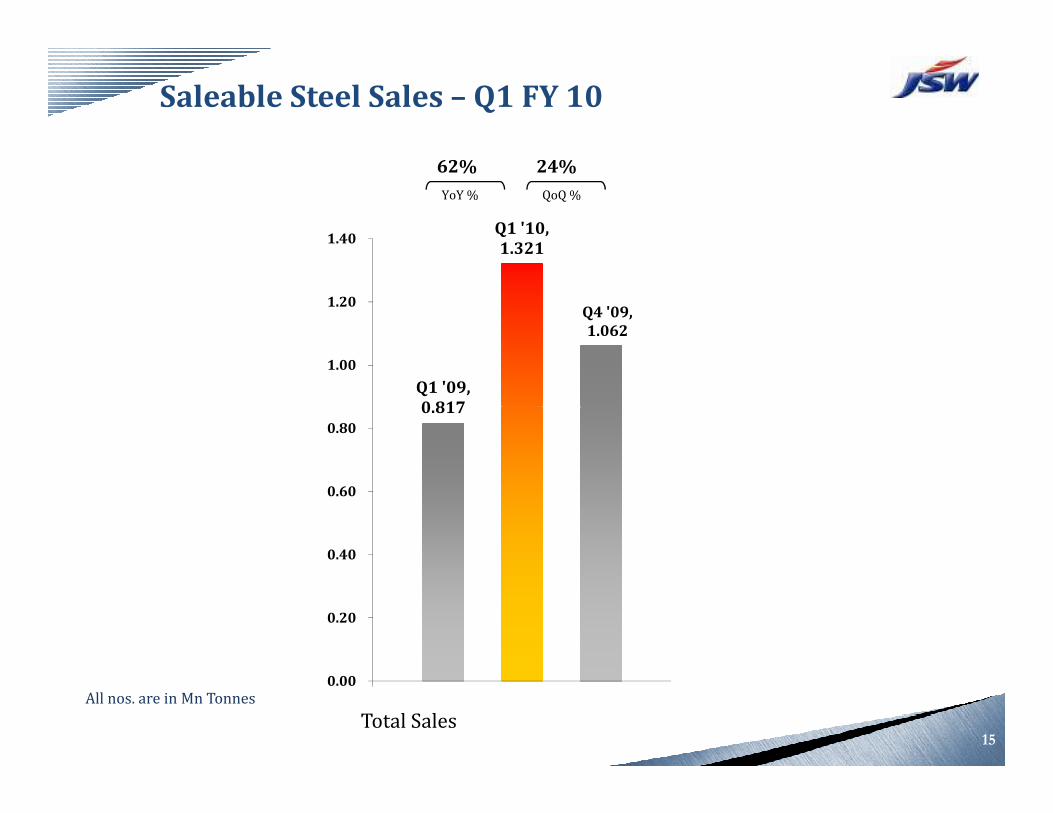

Saleable Steel Sales – Q1 FY 10

Q1 '09,

0.817

Q1 '10,

1.321

Q4 '09,

1.062

1.00

1.20

1.40

YoY % QoQ %

62% 24%

15

0.817

0.00

0.20

0.40

0.60

0.80

Total SalesAll nos. are in Mn Tonnes

Saleable Steel Sales – Q1 FY 10

Q1 '09,

0.582

Q1 '10,

0.855

Q4 '09,

0.855

YoY % QoQ %

47% 0%

Q1 '09,

0.207

Q1 '10,

0.366 Q4 '09,

0.330

YoY % QoQ %

77% 11%

16

Q1 '09,

0.065

Q1 '10,

0.154

Q4 '09,

0.096

Rolled : Flat

Q1 '09,

0.169

Q1 '10,

0.311

Q4 '09,

0.110

Semis

YoY % QoQ %

84% 183%

Value Added (CR/GI/PPGI)

Rolled : Long

YoY % QoQ %

136% 60%

All nos. are in Mn Tonnes

Product Mix

0.817

1.321

1.136, 86%

Export and Domestic SalesSaleable Steel Sales

(MnT, % Share)

0.065, 8%0.154, 12%

0.207, 25% 0.366, 28%

1.3210.817

Rolled: Long

Value added: Flat

(MnT, % Share)

Q1 FY 09 Q1 FY10

Exports Domestic

0.310, 38% 0.185, 14%

0.507, 62%

17

Q1 FY09 Q1 FY10

0.311, 24%0.169, 21%

0.376, 46% 0.489, 37%

Semis

Rolled : HR Products

8 10

18

50

67

Q1 FY09 Q2 FY09 Q3 FY09 Q4 FY09 Q1 FY10

JSW Shoppe % Share through JSW Shoppe in Q1 FY10

Focus on Retail Sales (Domestic)

0.770,88%

0.103,12%

No

. of

sho

pp

e

(Excl. semis)

(MnT, % Share)

38%

7%

55%Value added: Flat

Rolled : Long

JSW Shoppe Others

Q1 FY09 Q2 FY09 Q3 FY09 Q4 FY09 Q1 FY10

468

592

FY 09 June' 09

Avg. Sales through JSW Shoppe(Tonnes/month/shoppe)

27%

18

Rolled : HR Products

Financial PerformanceFinancial PerformanceFinancial PerformanceFinancial Performance

19

ParticularsQ1’10

Growth over

Q1’09 Q4’09

Volume (Mn t) : Crude Steel Production 1.376 41 % 43 %

: Saleable Steel Sales 1.321 62 % 24 %

Net Sales (Rs. crs) 3,894 6 % 19 %

Blended (Rs./t) : Sales Realisation 27,159 - 34 % - 3 %

: Cost of Production 20,113 - 34 % - 24 %

Key Highlights

20

: Cost of Production 20,113 - 34 % - 24 %

Operating EBITDA Margin

(Excluding Fx Gain/Loss)19.1 %

EBITDA (Rs. crs) 988 50 % 96 %

Profit before tax (Rs. crs) 496 54 % 556 %

Profit after tax (Rs. crs) 340 55 % 591 %

Excluding Production / Sales out of trial run from 1st April’09 to 9th April’09

Sales Realisation v/s Cost of Production

FX Loss,

1582

FX Loss,

1626

20000

25000

30000

35000

YoY % QoQ %

- 34% - 24%

30,607 20,113 26,608Q1 '09,

41168

Q1 '10,

27159

Q4 '09,

27881

25000

30000

35000

40000

45000

YoY % QoQ %

- 34% - 3%

21

Blended Realisation (Rs. / t)

Cost,

28981Cost,

21683

Cost,

25026

-5000

0

5000

10000

15000

20000

Q1 '09 Q1 '10 Q4 '09

FX gain

1570

Blended Cost (Rs. / t)

0

5000

10000

15000

20000

� Own coke consumption increased from 54.9% to 87.1%

� Fluxes consumption reduced from 349 kg/t to 314 kg/t

� Increase in Corex Gas Utilisation from 93% to 97.2%.

Efficiency Improvements at Vijayanagar (Q1 FY10 Vs Q1 FY09)

22

� Gas mixing station commissioned to improve utilisation of coke oven gas,

93% Gas utilisation achieved in Recovery type Coke Oven.

� Power generation increased from 149 MW to 180 MW.

� LD Gas recovery increased from 87 m3 to 104 m3 from SMS1.

� Yield at HSM improved from 96.8% to 97.14%

Standalone Financials – Q1 FY 10Rs. Cr.

Q1 FY 10 Q1 FY 09 Variance

Turnover 4,158.51 3,983.79 174.72 4%

EBITDA 988.09 660.09 328.00 50%

EBITDA Margin 25.2% 17.9%

Less : Non-operating income 5.51 4.96

Less : Forex gain / (loss) 235.92 (362.78)

Operating EBITDA (net of Forex gain / loss) 746.66 1,017.91 (271.25) - 27%

23

Operating EBITDA (net of Forex gain / loss) 746.66 1,017.91 (271.25) - 27%

Operating EBITDA margin (net of Forex gain / loss) 19.1% 27.6%

Interest 220.64 153.14 67.50 44%

Depreciation 271.80 185.21 86.59 47%

Profit Before Tax 495.65 321.74 173.91 54%

Profit after Tax 340.02 219.35 120.67 55%

EPS : Diluted 17.72 11.27 6.45 57%

Operational Performance - USA

PRODUCTION (NT) SALES (NT)

Q1 FY 10 Q1 FY 09 Q1 FY 10 Q1 FY 09

Plate Mill 27,727 143,077 14,376 79,796

Pipe Mill 5,432 66,431 4,308 68,156

Slab 15,450 -

USD Mio

24

Particulars Q1 FY 10 Q1 FY 09

Turnover 17.97 217.50

EBITDA + Other Income (13.74) 44.92

Profit Before Tax (32.12) 25.63

Profit After Tax (21.00) 17.68

USD Mio

Consolidated Financial – Q1 FY10

Q1 FY 10 Q1 FY 09

Total Income 4,013.78 4,479.42

EBITDA 928.11 843.48

Cash Profit 629.78 608.72

Rs. Cr.

25

Cash Profit 629.78 608.72

Profit Before Tax 313.16 388.85

Net Profit 234.08 250.23

Financial Covenants Relaxation / Waivers

Loan / Facility Loan O/S

(USD mio)

Syndicated External Commercial Borrowings 175

Advance Payment Against Steel Supply Agreement 150

Syndicated ECB USD 175 mio

– Consent of required majority of lenders actual (79.5%) for proposed amendments obtained till September 30, 2011.

APSSA USD 150 mio

- Waiver from required majority of lenders for March 2009 covenants obtained till March 31, 2009.

- For future period, lenders consent to bring the covenants in line with the other loan is being pursued.

26

3,828 3,815

678 445

6000

7000

8000

9000

10000

3.3 3.26

2.5

3

3.5

3,815

445

5,000

7,000

9,000

11,000

Adj. Long Term Debt Gearing - Standalone

Long Term Debt & Networth

FX Loss

FCL

Rs

. Cr.

X

10,047

Rs

. Cr.

9,8849,884

8,309

5,542 5,625

0

1000

2000

3000

4000

5000

As on 31/03/09 As on 30/06/09

FX LOSS FCL RTL

1.241.17

0.5

1

1.5

2

D:E Adj L.T. Debt/EBITDA

5,625

(1,000)

1,000

3,000

L.T. Debt Networth

27

Adj. L.T. Debt Gearing of 1.17

RTL

Q4 FY09 Q1 FY10

Wt Avg Cost of Debt (%) 8.22 8.23

FD & MF (Rs. Cr.) 190 136

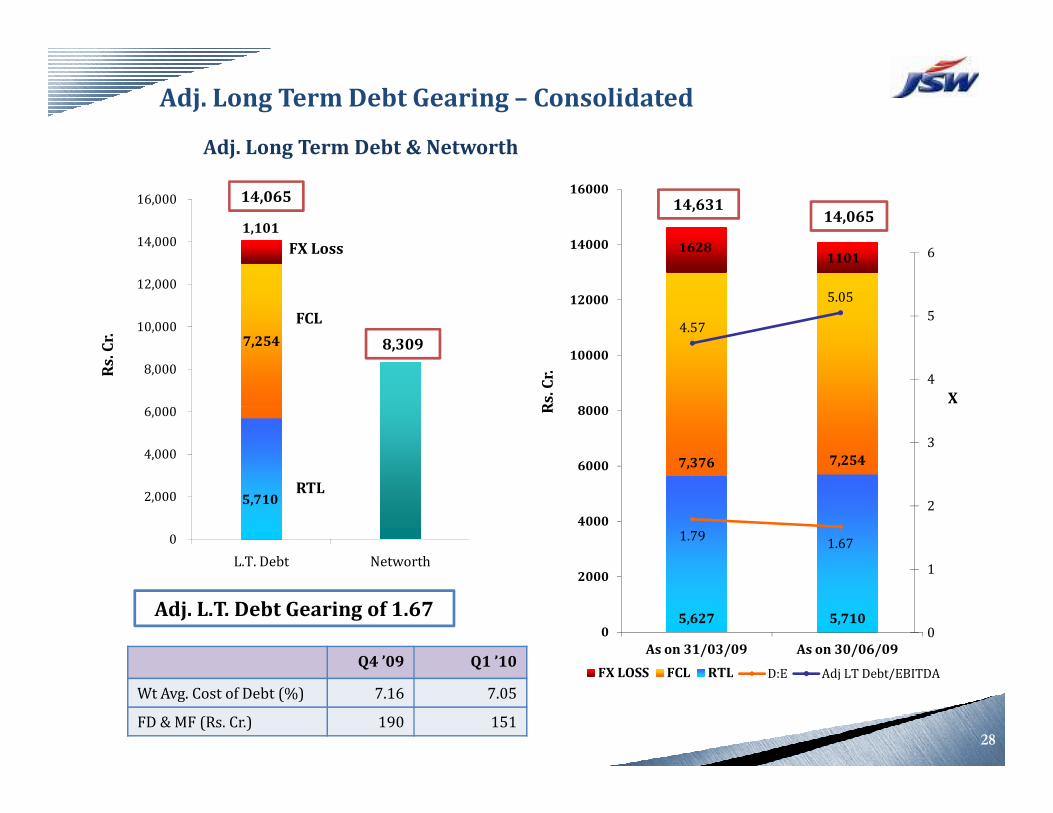

Adj. Long Term Debt Gearing – Consolidated

Adj. Long Term Debt & Networth

7,254

1,101

6,000

8,000

10,000

12,000

14,000

16,000

FX Loss

FCL

X

14,631

Rs

. Cr.

14,065

Rs

. Cr.

14,065

8,309

16281101

8000

10000

12000

14000

16000

4.57

5.05

4

5

6

28

Adj. L.T. Debt Gearing of 1.67

5,710

0

2,000

4,000

6,000

L.T. Debt Networth

RTL

Q4 ’09 Q1 ’10

Wt Avg. Cost of Debt (%) 7.16 7.05

FD & MF (Rs. Cr.) 190 151

Rs

. Cr.

5,627 5,710

7,376 7,254

0

2000

4000

6000

8000

As on 31/03/09 As on 30/06/09

FX LOSS FCL RTL

1.791.67

0

1

2

3

D:E Adj LT Debt/EBITDA

Project ProgressProject ProgressProject ProgressProject Progress

29

Blast Furnace commenced commercial

production in April’09

Rated Capacity : 7800 TPDCapacity utilisation for Q1 FY10: 74%

30

Hot Strip Mill- Phase I (3.5 MTPA)

Project Progress till 30th June, 2009 % Progress

Civil 77

Structural Fabrication 93

Structural Erection 84

Equipments Erection 25

31

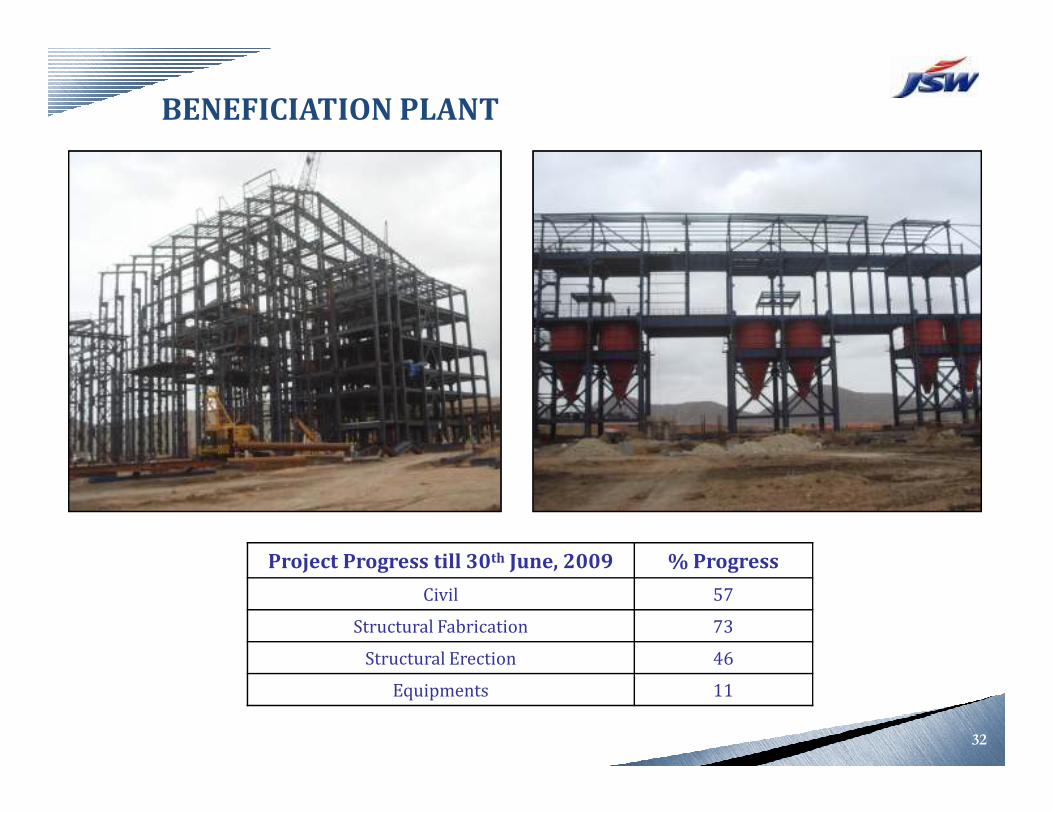

BENEFICIATION PLANT

Project Progress till 30th June, 2009 % Progress

Civil 57

Structural Fabrication 73

Structural Erection 46

Equipments 11

32

3.2 MTPA Expansion3.2 MTPA Expansion3.2 MTPA Expansion3.2 MTPA Expansion

33

BLAST FURNACE

34

Steel Melting Shop

35

COKE OVEN

36

SINTER PLANT

37

30 MW Power Plant Commissioned: Downstream

38

Q & A

39

Forward Looking and Cautionary Statement

Certain statements in this report concerning our future growth prospects are forward

looking statements, which involve a number of risks, and uncertainties that could

cause actual results to differ materially from those in such forward looking statements.

The risk and uncertainties relating to these statements include, but are not limited to

risks and uncertainties regarding fluctuations in earnings, our ability to manage

growth, intense competition within Steel industry including those factors which may

affect our cost advantage, wage increases in India, our ability to attract and retain

highly skilled professionals, time and cost overruns on fixed-price, fixed-time framehighly skilled professionals, time and cost overruns on fixed-price, fixed-time frame

contracts, our ability to commission mines within contemplated time and costs, our

ability to raise the finance within time and cost client concentration, restrictions on

immigration, our ability to manage our internal operations, reduced demand for

steel, our ability to successfully complete and integrate potential acquisitions, liability

for damages on our service contracts, the success of the companies in which the

Company has made strategic investments, withdrawal of fiscal/governmental

incentives, impact of regulatory measures, political instability, legal restrictions on

raising capital or acquiring companies outside India, unauthorized use of our

intellectual property and general economic conditions affecting our industry. The

company does not undertake to update any forward looking statements that may be

made from time to time by or on behalf of the company.

40