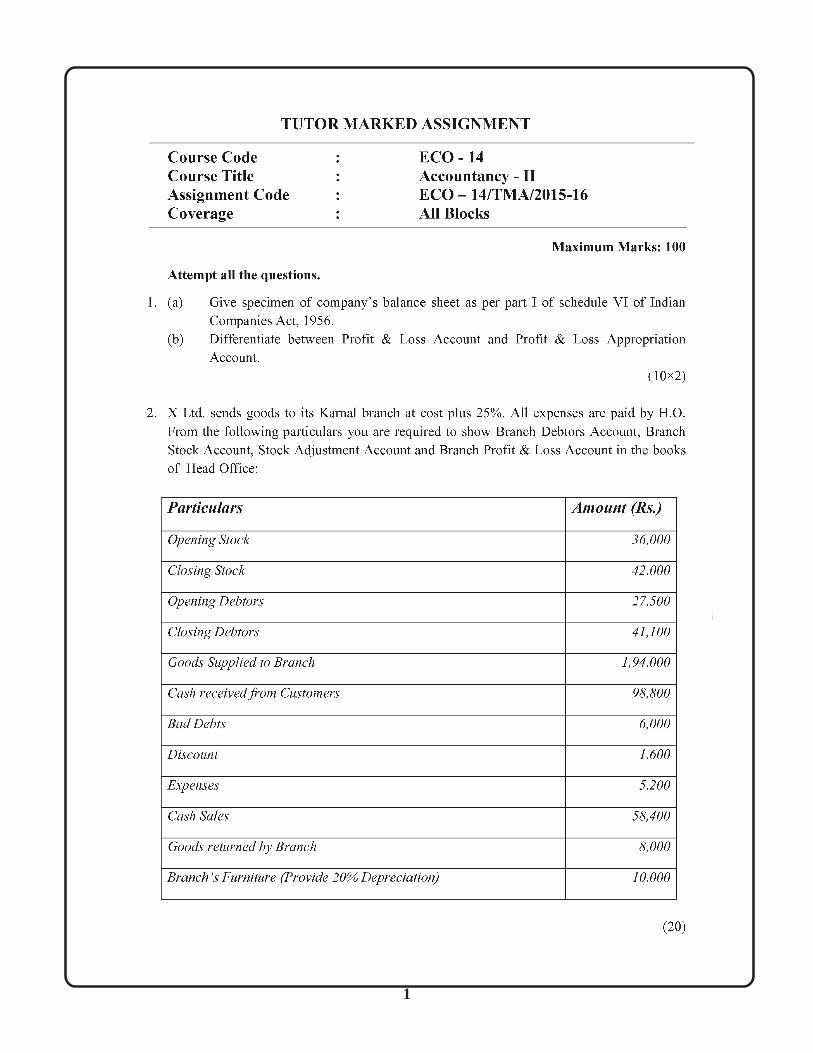

q. 1. (a) give specimen of company’ s balance sheet as per ... reserves specifying the nature of...

TRANSCRIPT

1

N

2

N

3

NAttempt all the questions.Q. 1. (a) Give specimen of company’s balance sheet as per part I of schedule VI of Indian Companies Act,

1956.Ans. Legal Requirements As To Company’s Balance Sheet (Schedule VI Part I)Part 1 to Schedule VI of the Companies Act, 1956 gives the format in which the balance sheet is to be prepared.

The schedule gives 2 types of formats, the horizontal format and the vertical format. A company can prepare itsbalance sheet in either of the 2 formats.

In the horizontal format, the liabilities including the share capital are placed on the left side and assets of alltypes on the right. The main heads in this form are arranged as under:

Horizontal Form:Balance Sheet of…….…..Co. Limited as at…………

ASSIGNMENT SOLUTIONS GUIDE (2015-2016)

E.C.O.-14Accountancy-II

Disclaimer/Special Note: These are just the sample of the Answers/Solutions to some of the Questions given in theAssignments. These Sample Answers/Solutions are prepared by Private Teacher/Tutors/Authors for the help and guidanceof the student to get an idea of how he/she can answer the Questions given the Assignments. We do not claim 100%accuracy of these sample answers as these are based on the knowledge and capability of Private Teacher/Tutor. Sampleanswers may be seen as the Guide/Help for the reference to prepare the answers of the Questions given in the assignment.As these solutions and answers are prepared by the private teacher/tutor so the chances of error or mistake cannot bedenied. Any Omission or Error is highly regretted though every care has been taken while preparing these Sample Answers/Solutions. Please consult your own Teacher/Tutor before you prepare a Particular Answer and for up-to-date and exactinformation, data and solution. Student should must read and refer the official study material provided by the university.

(1) Share Capital:Authorised Capital:

XXX … Shares of Rs. … eachIssued Capital:

XXX … Equity Shares of Rs. … eachXXX … Preference Share of Rs. … each

Subscribed Capital: … Equity Shares of Rs. … each Rs. …Called up … Preference Share of Rs. … each Rs.… Called up Less Calls Unpaid

(i) By directors (ii) By Others

XXX Add: Forfeited shares (2) Reserves and Surplus:

XXX 1. Capital Reserve, not available forDividend

Horizontal Form:Figures for Figures for Figures for the Figures forthe previous Liabilities the current Assets the currentyear Rs. Rs. year Rs. Rs. year Rs.

(1) Fixed Assets:1. Goodwill

XXX 2. Land3. Building

XXX 4. LeaseholdsXXX 5. Railway Sidings

6. Plant and MachineryXXX 7. Furniture and FittingsXXX 8. Development of PropertyXXX 9. Patents, Trade Marks and DesignsXXX 10. Live StocksXXX 11. Vehicles etc.XXX (2) Investments:

(3) Current Assets, Loansand Advances:

XXX (A) Current Assets:

4

N

XXX 2. Capital Redemption ReserveXXX 3. Share Premium Account XXX 4. Other Reserves specifying the nature

of reserve and the amount in respect thereof.Less: Debit balance in Profit and Lossaccount (if any)

XXX 5. Surplus, that is balance in Profit andLoss account after providing for proposedallocation namely:Dividend, Bonus or Reserves

XXX 6. Proposed addition to reservesXXX 7. Sinking Funds

(3) Secured Loans:

XXX 1. DebenturesXXX 2. Loans and Advances from BanksXXX 3. Loans and Advances from subsidiariesXXX 4. Other Loans and Advances XXX 5. Interest accrued and due on secured

loans

(4) Unsecured Loans:

XXX 1. Fixed Deposits XXX 2. Loans and Advances from subsidiariesXXX 3. Short Term Loans and Advances

From BanksFrom Others

XXX 4. Other Loans and AdvancesFrom BanksFrom Others

(5) Current Liabilitiesand Provisions:

(A) Current Liabilities:XXX 1. Acceptances XXX 2. Sundry CreditorsXXX 3. Subsidiary CompaniesXXX 4. Unclaimed DividendsXXX 5. Interest accrued but not due on loansXXX 6. Advance payments and unexpired

discounts for the portion for which valuehas still to be given, e.g. in the case of thefollowing classes of companies:Newspaper, Fire Insurance, Theatres,Clubs, Banking, Steamship Companiesetc.

XXX 1. Interest accrued on investmentsXXX 2. Stores and Spare partsXXX 3. Loose Tools

XXX 4. Stock in trade

XXX 5. Work-in-progressXXX 6. Sundry Debtors: Debts outstanding

for a period exceeding 6 monthsOther DebtsLess: Provision7. (a) Cash balance in hand(b) Bank balance:With scheduled BanksWith others

XXX (B) Loans and Advances:XXX 8. (a) Advances and loans to

subsidiaries(b) advances and loans to partnershipfirms in which the Company or anyof its subsidiaries is a partner

XXX 9. Bills of ExchangeXXX 10. Advances recoverable in cash or

in kind (e.g. Rates, Taxes, Insurance,etc. prepaid)

XXX 11. Balances with customs, PortTrusts, and excise authorities etc.(4) Miscellaneous Expenditure:

XXX 1. Preliminary ExpensesXXX 2. Expenses, including Commission

or Brokerage on underwriting ofShares or Debentures

XXX 3. Discount allowed on the issue ofShares or Debentures

XXX 4. Interest paid out of capital duringconstruction period5. Development expenditure notadjusted6. Other sums (specifying nature)

XXX 5. Profit and Loss Account: (Thisis shown only when its debit balancecount not be written off out of othersreserves)

Figures for Figures for Figures for the Figures forthe previous Liabilities the current Assets the current

year Rs. Rs. year Rs. Rs. year Rs.

5

N(b) Differentiate between Profit & Loss Account and Profit & Loss Appr opriation Account.Ans. The difference between profit and loss account and profit and loss appropriation account is given below:

1. Profit & Loss A/c is the Income Statement showing Income and Expenses for a particular Accounting period toarrive at the Profit earned or Loss incurred. Where as Profit & Loss Appropriation Account is a statement showingthe utilisation of Profit shown in the P&L A/c above.2. Sales and/or Service Revenue,Other income, Operating, Administration, Marketing/Selling & other expenses forthe period are shown in the P&L A/c, Whereas Transfer of Profit to Reserves, Proposed Dividend, Taxes, etc., areshown in P& L Appropriation A/c3. In the vertical format P&L A/c items are referred to as ‘Above the Line’ items & P&L Appropriation items arereferred to as ‘Below the Line’ items. 4. Profit and loss account records all the operating and non operating incomes and expenses and incomes to arriveat net profit. This is Net Profit before tax. Further, we record provision for tax on the debit side of the Profit and lossaccount and get net profit after tax.Profit and Loss Appropriation account showcases the appropriation of profit. In case of Companies, only transfer tothe various reserves and proposed dividend are recorded on the debit side. Whereas, on the credit side appears Netprofit after tax broughtdown from the profit and loss account and the balance broughtdown from the last year’sprofit and loss appropriation account.

Q. 2. X Ltd. sends goods to its Karnal branch at cost plus 25%. All expenses are paid by H.O. From thefollowing particulars you are required to show Branch Debtors Account, Branch Stock Account, Stock Ad-justment Account and Branch Profit & Loss Account in the books of Head Office.

Particulars Amount (Rs.)Opening Stock 36,000Closing Stock 42,000Opening Debtors 27,500Closing Debtors 41,100Good Supplied to branch 1,94,000Cash received from Customers 98,800Bad Debts 6,000

XXX 7. Other Liabilities (if any)(B) Provisions:

XXX 8. Proposed DividendsXXX 9. Provision for TaxationXXX 10. Provision for ContingenciesXXX 11. Provision for Provident Fund schemesXXX 12. Provision for insurance, pension and

similar staff benefit schemes. XXX 13. Other Provisions

(6) CONTINGENT LIABILITIES (byway of footnote only):

1. Uncalled liabilities on partly paidshares

2. Liabilities under Guarantee3. Arrears of dividends on cumulativepreference shares

4. Claim against the company nowacknowledged as debts 5. Liabilities on Bills Receivablediscounted but not matured.

XXXXXXXXXXXXXXX

XXX

Figures for Figures for Figures for the Figures forthe previous Liabilities the current Assets the current

year Rs. Rs. year Rs. Rs. year Rs.

XXX XXX XXX XXX

6

N

Discount 1,600Expenses 5,200Cash Sales 58,400Goods returned by Branch 8,000Branch’s Furnitur e (Provide 20% Depreciation) 10,000Ans.

Branch AccountDate Particulars Amount Date Particulars Amount

Opening Stock 36,000 Closing Stock 42,000Opening Debtors 27,500 Closing Debtors 41,100Goods sent to branch 194,000 Goods Sent to branch (goods returned)8,000Branch P&L A/c 12,000 branch debtor a/c 120,000

cash a/c (cash sales) 58,400Total 269,500 Total 269,500

Branch Stock AccountDate Particulars Amount Date Particulars Amount

Opening Stock 36,000 Good sent to branch (Goods retruned)8,000Goods Sent to branch 194,000 Branch Cash 58,400

Branch Debtors 120,000 Closing Stock 42,000

Total 230,000 228,400Branch Debtors Account

Date Particulars Amount Date Particulars AmountOpening balance 27,500 Branch A/c (Cash) 98,800branch P&L a/c( Sales) 120,000 Branch P&L Account (bad debt) 6,000

Branch P&L A/c (Discount) 1,600Closing balance 41,100

147,500 147,500Branch Stock Adjustment Account

Date Particulars Amount Date Particulars AmountTo goods sent to branch by Stock reserve( goods returned) 1,600 (loading opening stock) 7,200to stock reserve (closing stock) 8,400 by goods sent to branch

(loading on goods sent) 178,480to branch P&L 175,680

Total 185,680 185,680Branch Profit and loss account

Date Particulars Amount Date Particulars AmountTo Branch Debtor accout (bad debt) 6,000 by Branch account (excess of stock)12,000To Branch Debtor accout (discount) 1,600 by Branch Stock adjustment accout 175,680To Cash (expenses) 5,200To Depreciation 2,000To P& L Account 172,880

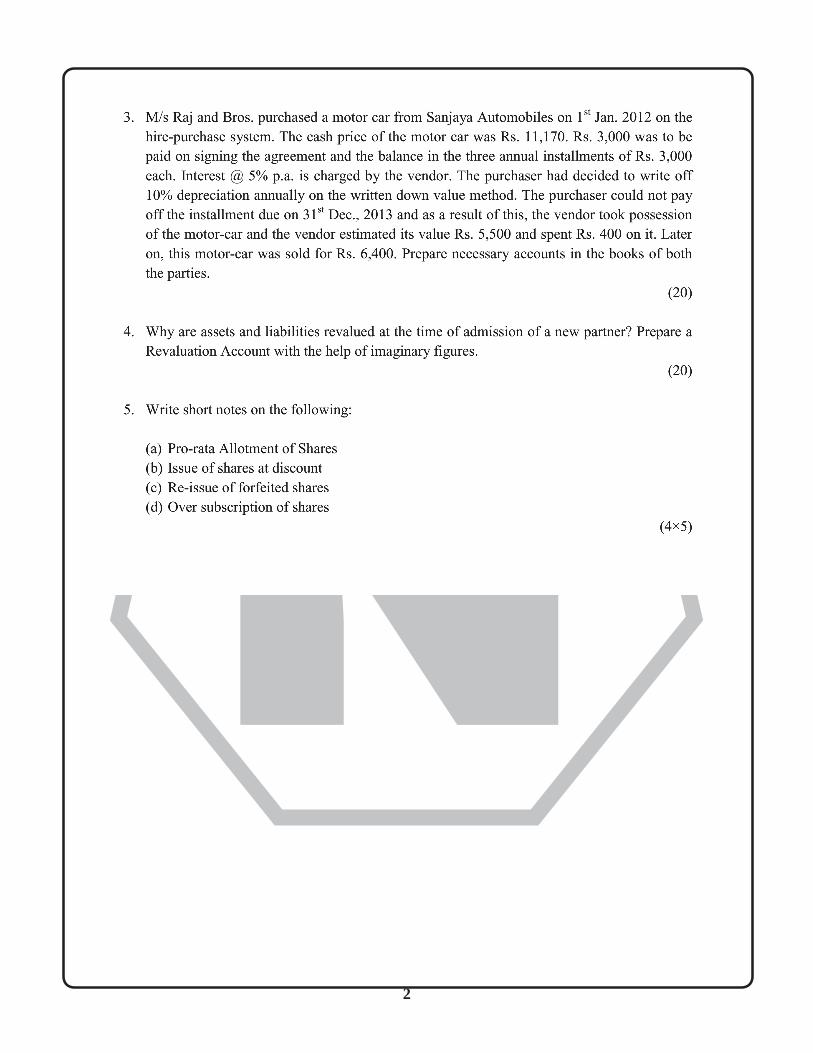

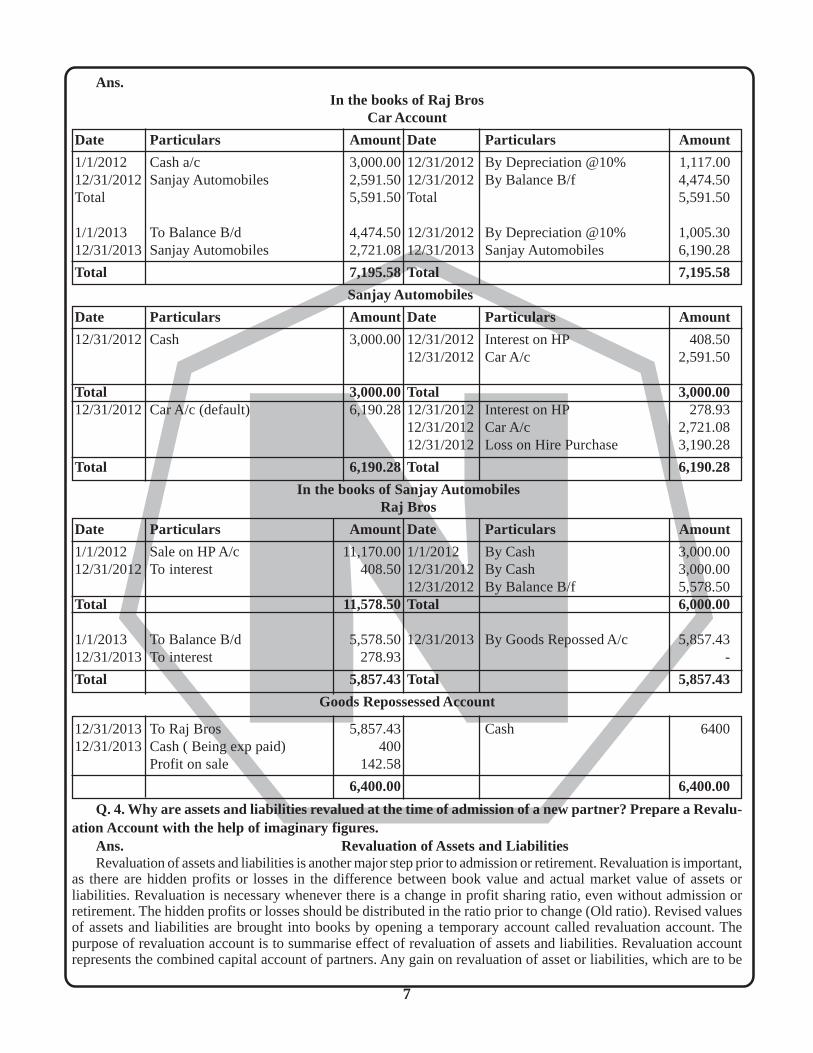

Total 187,680 187,680Q. 3. M/s Raj and Bros. purchased a motor car from Sanjay Automobiles on 1st Jan. 2012 on the hire

purchase system. The cash price of the motor car was Rs. 11,170. Rs. 3,000 was to be paid on signing theagreement and the balance in the three annual installments of Rs. 3,000 each. Interest @ 5% p.a. is chargedby the vendor. The purchaser had decided to write off 10% depreciation annually on the written down valuemethod. The purchaser could not pay off the installment due on 31st Dce., 2013 and as a result of this, thevendor took possession of the motor-car and the vendor estimated its value Rs. 5,500 and spent Rs. 400 on it.Later on this motor-car was sold for Rs. 6,400. Prepare necessary accounts in the books of both the parties.

7

N

Ans.In the books of Raj Bros

Car Account

Date Particulars Amount Date Particulars Amount

1/1/2012 Cash a/c 3,000.0012/31/2012 By Depreciation @10% 1,117.0012/31/2012Sanjay Automobiles 2,591.5012/31/2012 By Balance B/f 4,474.50Total 5,591.50Total 5,591.50

1/1/2013 To Balance B/d 4,474.5012/31/2012 By Depreciation @10% 1,005.3012/31/2013Sanjay Automobiles 2,721.0812/31/2013 Sanjay Automobiles 6,190.28

Total 7,195.58Total 7,195.58

Sanjay Automobiles

Date Particulars Amount Date Particulars Amount

12/31/2012Cash 3,000.0012/31/2012 Interest on HP 408.5012/31/2012 Car A/c 2,591.50

Total 3,000.00Total 3,000.0012/31/2012Car A/c (default) 6,190.2812/31/2012 Interest on HP 278.93

12/31/2012 Car A/c 2,721.0812/31/2012 Loss on Hire Purchase 3,190.28

Total 6,190.28Total 6,190.28

In the books of Sanjay AutomobilesRaj Bros

Date Particulars Amount Date Particulars Amount

1/1/2012 Sale on HP A/c 11,170.001/1/2012 By Cash 3,000.0012/31/2012To interest 408.5012/31/2012 By Cash 3,000.00

12/31/2012 By Balance B/f 5,578.50Total 11,578.50Total 6,000.00

1/1/2013 To Balance B/d 5,578.5012/31/2013 By Goods Repossed A/c 5,857.4312/31/2013To interest 278.93 -

Total 5,857.43Total 5,857.43

Goods Repossessed Account

12/31/2013To Raj Bros 5,857.43 Cash 640012/31/2013Cash ( Being exp paid) 400

Profit on sale 142.58

6,400.00 6,400.00

Q. 4. Why are assets and liabilities revalued at the time of admission of a new partner? Prepare a Revalu-ation Account with the help of imaginary figures.

Ans. Revaluation of Assets and LiabilitiesRevaluation of assets and liabilities is another major step prior to admission or retirement. Revaluation is important,

as there are hidden profits or losses in the difference between book value and actual market value of assets orliabilities. Revaluation is necessary whenever there is a change in profit sharing ratio, even without admission orretirement. The hidden profits or losses should be distributed in the ratio prior to change (Old ratio). Revised valuesof assets and liabilities are brought into books by opening a temporary account called revaluation account. Thepurpose of revaluation account is to summarise effect of revaluation of assets and liabilities. Revaluation accountrepresents the combined capital account of partners. Any gain on revaluation of asset or liabilities, which are to be

8

N

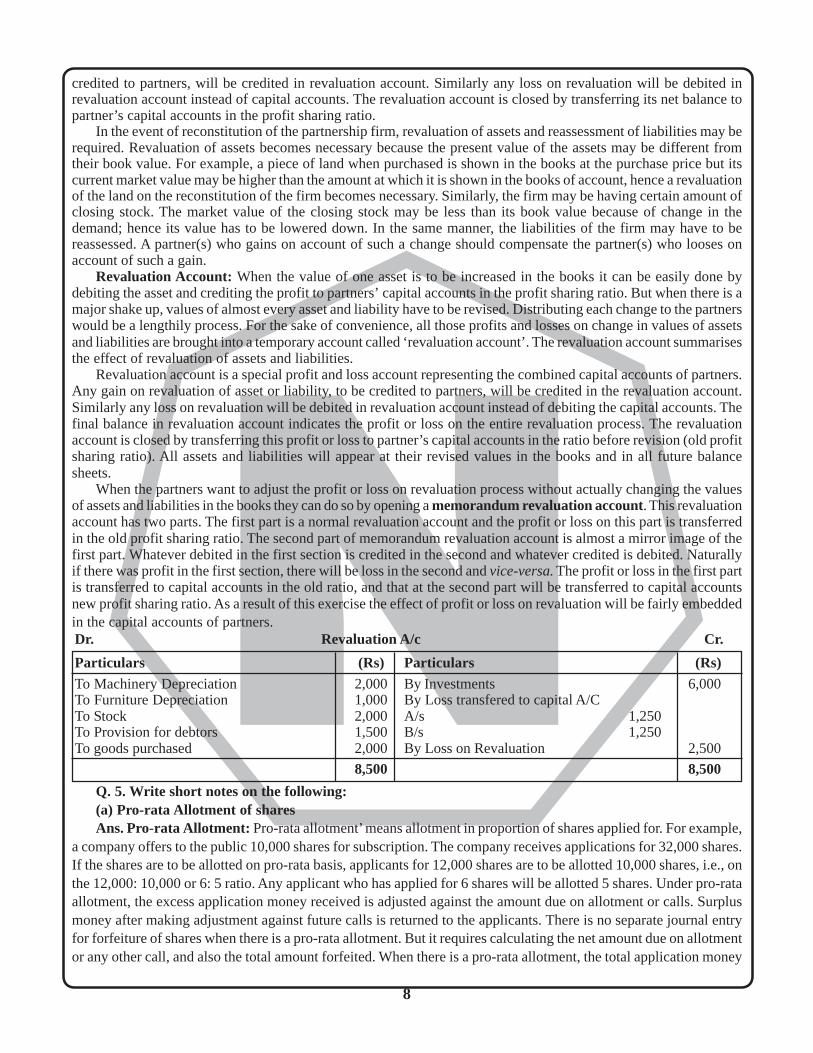

credited to partners, will be credited in revaluation account. Similarly any loss on revaluation will be debited inrevaluation account instead of capital accounts. The revaluation account is closed by transferring its net balance topartner’s capital accounts in the profit sharing ratio.

In the event of reconstitution of the partnership firm, revaluation of assets and reassessment of liabilities may berequired. Revaluation of assets becomes necessary because the present value of the assets may be different fromtheir book value. For example, a piece of land when purchased is shown in the books at the purchase price but itscurrent market value may be higher than the amount at which it is shown in the books of account, hence a revaluationof the land on the reconstitution of the firm becomes necessary. Similarly, the firm may be having certain amount ofclosing stock. The market value of the closing stock may be less than its book value because of change in thedemand; hence its value has to be lowered down. In the same manner, the liabilities of the firm may have to bereassessed. A partner(s) who gains on account of such a change should compensate the partner(s) who looses onaccount of such a gain.

Revaluation Account: When the value of one asset is to be increased in the books it can be easily done bydebiting the asset and crediting the profit to partners’ capital accounts in the profit sharing ratio. But when there is amajor shake up, values of almost every asset and liability have to be revised. Distributing each change to the partnerswould be a lengthily process. For the sake of convenience, all those profits and losses on change in values of assetsand liabilities are brought into a temporary account called ‘revaluation account’. The revaluation account summarisesthe effect of revaluation of assets and liabilities.

Revaluation account is a special profit and loss account representing the combined capital accounts of partners.Any gain on revaluation of asset or liability, to be credited to partners, will be credited in the revaluation account.Similarly any loss on revaluation will be debited in revaluation account instead of debiting the capital accounts. Thefinal balance in revaluation account indicates the profit or loss on the entire revaluation process. The revaluationaccount is closed by transferring this profit or loss to partner’s capital accounts in the ratio before revision (old profitsharing ratio). All assets and liabilities will appear at their revised values in the books and in all future balancesheets.

When the partners want to adjust the profit or loss on revaluation process without actually changing the valuesof assets and liabilities in the books they can do so by opening a memorandum revaluation account. This revaluationaccount has two parts. The first part is a normal revaluation account and the profit or loss on this part is transferredin the old profit sharing ratio. The second part of memorandum revaluation account is almost a mirror image of thefirst part. Whatever debited in the first section is credited in the second and whatever credited is debited. Naturallyif there was profit in the first section, there will be loss in the second and vice-versa. The profit or loss in the first partis transferred to capital accounts in the old ratio, and that at the second part will be transferred to capital accountsnew profit sharing ratio. As a result of this exercise the effect of profit or loss on revaluation will be fairly embeddedin the capital accounts of partners.Dr. Revaluation A/c Cr.

Particulars (Rs) Particulars (Rs)To Machinery Depreciation 2,000 By Investments 6,000To Furniture Depreciation 1,000 By Loss transfered to capital A/CTo Stock 2,000 A/s 1,250To Provision for debtors 1,500 B/s 1,250To goods purchased 2,000 By Loss on Revaluation 2,500

8,500 8,500

Q. 5. Write short notes on the following:(a) Pro-rata Allotment of sharesAns. Pro-rata Allotment: Pro-rata allotment’ means allotment in proportion of shares applied for. For example,

a company offers to the public 10,000 shares for subscription. The company receives applications for 32,000 shares.If the shares are to be allotted on pro-rata basis, applicants for 12,000 shares are to be allotted 10,000 shares, i.e., onthe 12,000: 10,000 or 6: 5 ratio. Any applicant who has applied for 6 shares will be allotted 5 shares. Under pro-rataallotment, the excess application money received is adjusted against the amount due on allotment or calls. Surplusmoney after making adjustment against future calls is returned to the applicants. There is no separate journal entryfor forfeiture of shares when there is a pro-rata allotment. But it requires calculating the net amount due on allotmentor any other call, and also the total amount forfeited. When there is a pro-rata allotment, the total application money

9

N

paid by an applicant is more than the exact amount due on application. The excess amount is treated as an advanceagainst allotment or any other future calls. The net amount due on allotment or any other calls is the differencebetween the amount due on allotment or any other calls and the excess amount received in application.

(b) Issue of share at discountAns. Shares are said to be issued at a discount when they are issued at a price lower than the face value. For

example if a share of Rs. 10 is issued at Rs. 9, it is said that the share has been issued at discount. The excess of theface value over the issue price [i.e. Re.1 (Rs. 10 – Rs. 9)] is called as the amount of discount.Share discount account showing a debit balance denotes a loss to the company which is in the nature of capital loss.Therefore, it is desirable, but not compulsory, to write it off against any Capital Profit available or Profit and LossAccount as soon as possible, and the unwritten off part of it is shown in the asset side of the Balance Sheet under theheading of ‘Miscellaneous Expenditure’ in a separate account called ‘Discount on issue of Shares Account’.Conditions for issue of shares at discount: For issue of shares a discount the company has to satisfy the followingconditions given in section 79 of the Companies Act, 1956:

(1) At least one year must have elapsed since the company became entitled to commence business. It means thata new company cannot issue shares at a discount at the very beginning.

(2) If the company has already issued such types of shares.(3) An ordinary resolution to issue the shares at a discount has been passed by the company in the General

Meeting of shareholders and sanction of the Company Law Tribunal has been obtained.(4) The resolution must specify the maximum rate of discount at which the shares are to be issued but the rate of

discount must not exceed 10% of the face value of the shares. For more than this limit, sanction of theCompany Law Tribunal is necessary.

(5) The issue must be made within two months from the date of receiving the sanction of the Company LawTribunal or within such extended time as the Company Law Tribunal may allow.

(c) Re-issue of forfeited sharesAns. Forfeited of SharesWhen any company allots share to the applicants, it is done on the basis of a legal contract between the company

and the applicant, which makes it binding upon the shareholders to pay the amount of allotment and calls wheneverthey are due. Now if any shareholder fails to pay the allotment and or call money due to him, the shareholder violatesthe contract and the company is entitled to take its share back, which is known as forfeiture of shares. The companycan forfeit such shares if authorised by the Articles of Association. Forfeiture of share can be done according to therules laid shown in the Articles and if no rules are given in Articles, the provisions of Table A, regarding forfeiturewill apply. Forfeiture of shares means cancellation of allotment to defaulting shareholders and to treat the amountalready received on such shares is not returnable to him–it is forfeited.Procedure in Case of Share Forfeiture

The usual procedure is that the defaulting shareholder must be given a minimum 14 days notice requiring him topay the amount due on his shares along with interest on it stating that if he fails to pay the amount and the interest onit, the shares will be forfeited. In spite of this notice, the shareholder does not pay the unpaid amount. The directorsafter passing a resolution will forfeit the shares and information will be given to the defaulting shareholder about theforfeiture his shares.Re-issue of Forfeited shares

Shares forfeited becomes the property of the company and the directors of a company have an authority to re-issue the shares once forfeited by them in accordance with the provisions contained in Articles of Association. Table‘A’ provides that “A forfeited shares may be sold or otherwise disposed off on such terms and in such manner as theBoard thinks fit”. They can re-issue the forfeited shares at par, at premium or at discount. However, if the shares arere-issued at discount, the amount of the discount does not exceed the amount paid on such shares by the originalshareholder but in case of shares originally issued at a discount, the maximum permissible discount will be amountpaid on such shares by the original shareholder plus the amount of original discount.

10

N

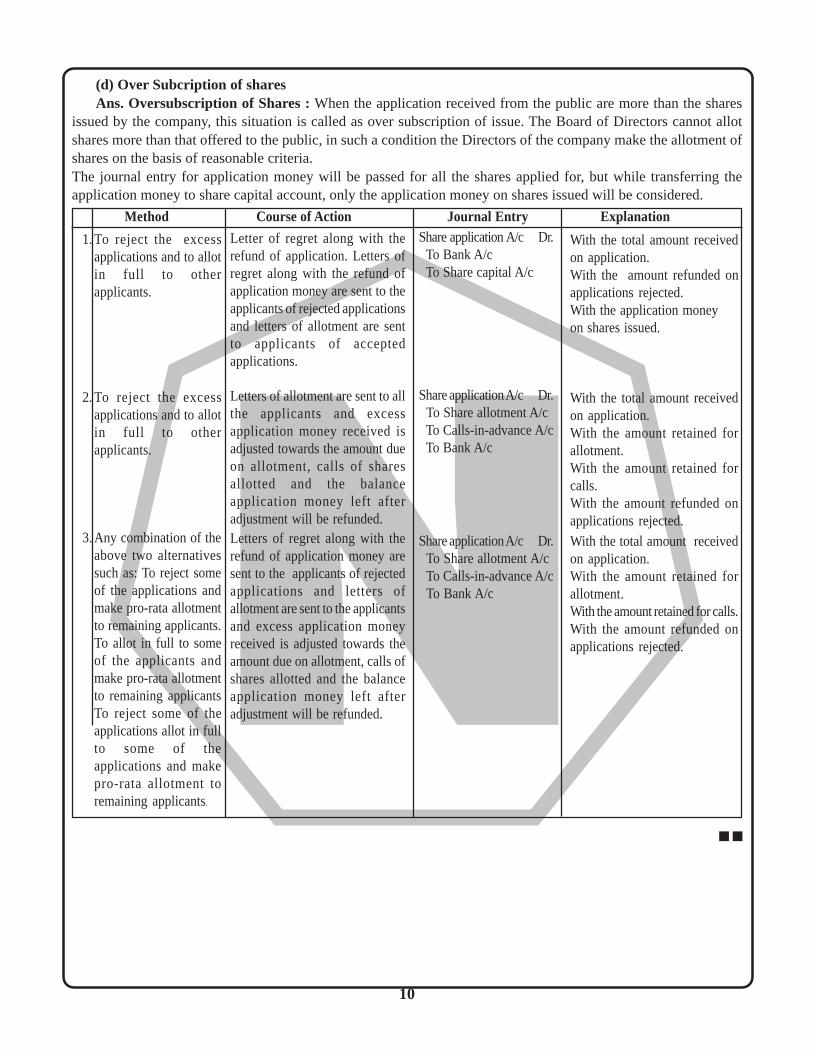

(d) Over Subcription of sharesAns. Oversubscription of Shares : When the application received from the public are more than the shares

issued by the company, this situation is called as over subscription of issue. The Board of Directors cannot allotshares more than that offered to the public, in such a condition the Directors of the company make the allotment ofshares on the basis of reasonable criteria.The journal entry for application money will be passed for all the shares applied for, but while transferring theapplication money to share capital account, only the application money on shares issued will be considered.

Method Course of Action Journal Entry ExplanationShare application A/c Dr. To Bank A/c To Share capital A/c

Share application A/c Dr. To Share allotment A/c To Calls-in-advance A/c To Bank A/c

Share application A/c Dr.To Share allotment A/cTo Calls-in-advance A/cTo Bank A/c

With the total amount receivedon application.With the amount refunded onapplications rejected.With the application moneyon shares issued.

With the total amount receivedon application.With the amount retained forallotment.With the amount retained forcalls.With the amount refunded onapplications rejected.

With the total amount receivedon application.With the amount retained forallotment.With the amount retained for calls.With the amount refunded onapplications rejected.

1.To reject the excessapplications and to allotin full to otherapplicants.

2.To reject the excessapplications and to allotin full to otherapplicants.

3.Any combination of theabove two alternativessuch as: To reject someof the applications andmake pro-rata allotmentto remaining applicants.To allot in full to someof the applicants andmake pro-rata allotmentto remaining applicantsTo reject some of theapplications allot in fullto some of theapplications and makepro-rata allotment toremaining applicants.

Letter of regret along with therefund of application. Letters ofregret along with the refund ofapplication money are sent to theapplicants of rejected applicationsand letters of allotment are sentto applicants of acceptedapplications.

Letters of allotment are sent to allthe applicants and excessapplication money received isadjusted towards the amount dueon allotment, calls of sharesallotted and the balanceapplication money left afteradjustment will be refunded.Letters of regret along with therefund of application money aresent to the applicants of rejectedapplications and letters ofallotment are sent to the applicantsand excess application moneyreceived is adjusted towards theamount due on allotment, calls ofshares allotted and the balanceapplication money left afteradjustment will be refunded.

■ ■