public sector financial management: part 9: … · • this is not about managing bank accounts to...

TRANSCRIPT

PUBLIC SECTOR FINANCIAL MANAGEMENT: PART 9: IN-YEAR BUDGET CONTROL AND MANAGEMENT

Andrew Graham Queens University School of Policy Studies www.andrewbgraham.ca

Structure • Today: Overview of In-Year Budget Control • Tomorrow: Class Exercise and Distribute Final

Assignment • Friday: Discussion of Final Assignment and Class Time

to Review

2

Reprise

• Focus on management of budgets in-year – Management Accounting

• Basis for adapting approved budget to changing circumstances for control purposes

• A key management skill

• In Year Budget Management Exercise: A scenario of a financial situation will be presented and you will be asked to brief your boss, the Deputy Minister as well as your colleagues on the Senior Management Committee

3

Definitions

• Cash, budget, treasury and liquidity can get confused at this point • No one term exists for the management of in-year budgets • This is not about managing bank accounts to ensure adequate cash is on hand: that

is a liquidity management function – commonly called cash management • This is not about the effective use of cash at hand in terms of short-term

investments: that is a treasury function

• Goal: managing the budget at hand effectively.

4

Cash Management = In-Year Budget Management

Why Budget and Forecast?

Budgets and Forecasts A budget is a formally approved plan for the operation for

a specific period. An approved budget becomes the benchmark to test your

actual results A forecast is a projection of activity based upon the latest

information.

Why Budget and Forecast?

Budgets and Forecasts Measure actuals and forecasts against the budget

throughout the planning process.

Analyze anticipated versus actual results – variance.

Predict future performance and anticipate changes. Assist in monitoring control of current performance. Provide early warning of deviations from plans. Take

actions needed.

Definition

In-year budget management is the system which compares actual expenditures against unit spending plans for a given financial year, identifies risks and variances and enables the adjustment of resource allocations to reflect

changed circumstances in the that year.

7

Budget Cash Management is not a way to re-open the budget decisions but to adapt to changing circumstances.

Effective in-year budget management creates opportunity for managers to: • Ensure that they remain within budget

• Alert senior management to shifts in demand for services or other cost drivers

• Maximize the use of their funds so that they are fully expended for their stated purpose and opportunities to meet emerging needs are met

• Reallocate within a current year so meet unanticipated needs • A means of assessing departmental, unit and individual performance

8

Key Part of the Job

• Responsibility of all responsibility centre managers • Key way to achieve results you plan to achieve

• Knowing how to do it is important • Uses tools of control, risk management, forecasting,

good financial reporting and analysis

9

Managing the Budget Reflects on Performance

• Out of control budgets suggest bad management or failure to adapt to changing circumstances.

• Money unspent in a persistent or perverse way suggests failure to deliver full program or program shifitng.

• An organization’s ability to collectively manage its current resources most effectively reflects its overall capacity to work as a team or unit toward a set of coherent goals

10

Managing the Budget Reflects on Performance

• The degree of flexibility and decentralization in an organization will have an impact on how cash is managed in terms of • how it can and cannot be redistributed,

• the degree of reporting and

• the scope and role of central corporate offices within the organization

11

What do flexibility and decentralization mean in this context?

Actual Cash Remains a Concern

ì In the public sector, even with accrual accounting, there remains a high measure of accountability for explaining what is happening to voted funds within one year.

ì Financial reporting requires this annualized approach. ì How the available budget is used remains a preoccupation of

many players in the scene: managers, clients, oversight groups and legislators

12

Importance of in-Year Budget Management

ì Organizations are always looking for spare capacity and this is one way of finding it in the short term.

ì It does not replace permanent reallocations, program evaluation or policy making that shifts resources in a formal way, i.e. legislatively or through other policy instruments.

ì Budgets can be complex landscapes.

13

A Matter of Balance

14

Delivery on Plans and Law

Adaptability to Changing Conditions

What could possibly go wrong? • Errors in repor*ng – accoun*ng systems can be wrong • Incomplete informa*on • Budget plan proved to be inaccurate

15

What could possibly go wrong? • Actual events did not conform to plan • Unan*cipated surges in demand or loss of revenue • Catastrophic events • Poor management decisions

16

The Objectives of Effective In-Year Budget Management

ì To have funds to pay the bills, i.e., sufficient liquidity ì To use budgeted resources for their program purposes and

not leave needed funds unspent ì To keep within the appropriated or authorized budget ì To have the organizational and resource capacity to react to

changes in plan ì To reallocate available funds to meet emerging, short-term

priorities.

17

The Big Three Questions

q What has happened so far?

q What do we think will happen to our plan for the rest of the year?

q What (if any) actions do we need to take to achieve our agreed plan?

18

What Does a Manager Actually Do to Manage the Budget? • Receives regular reports on budget spent and the likely ouBurn • Understanding in-‐year pressures and ac*ons proposed • Finding internal realloca*ons or seeking realloca*ons from another source.

• Adjus*ng workflow and expenditures to adapt.

19

What Does a Manager Actually Do to Manage the Budget? • Ensuring appropriate informa*on is provided to the relevant scru*ny commiBees to support their work.

• Paying par*cular aBen*on to bids for capital funding and monitoring progress – these frequently slip from the ini*al *metable and you should know why

• Reviewing how services can be made more efficient.

20

Qualities of the Financial Performance Review Process

• Focus on a few critical aspects of performance • Look forward as well as back

• Explain and react to key risk considerations • Explain and react to key capacity considerations

21

Source: Reporting Principles, Canadian Comprehensive Audit Foundation, 2003

Qualities of the Financial Performance Review Process

• Explain other factors critical to performance • Integrate financial and non-financial information

• Provide comparative information • Present credible information, fairly interpreted

• Disclose the basis of reporting

22

23

In some countries, this is the law

The accounting officer in New Zealand must submit to the relevant treasury and executive authority within 15 days of the end of each month, information on:

· the actual revenue and expenditure for that month, in the format determined by the national Treasury · projections of anticipated expenditure and revenue for the remainder of the current financial year in the format determined by the national Treasury · information on conditional grants received and actual spending against them · information on all transfers · any material variances and a summary of actions to ensure that the projected expenditure and revenue remain within the budget.

Movement towards government-level Interim Financial Reports

24

25

Operational Cash Forecasting Goes Beyond Financial Statements

• Knowing about cash movements to date based on financial reports is not enough

• Encumbrances and anticipated risk or costs changes are not reflected

• Cash forecasting and financial reporting moves into the realm of bringing content, knowledge and numbers together

26

From Cash Flow to Cash Forecasting: Financial Statements

• Financial analysis uses the financial statements and other sources of information to: • help managers and outsiders understand an organization's financial

condition,

• make decisions about the organization, and

• compare an organization's financial performance to its peers, its past and its plans.

27

From Cash Flow to Cash Forecasting: Financial Statements

• There must be confidence in the retrospective information to then add in the value of management forecasting, commitments and risks

• Analysis of just financial statements rarely gives a final answer

• Rather, it indicates where further analysis is needed

28

From Cash Flow to Cash Forecasting: Financial Statements

• Good organization management, regardless of the size of the organization, demands that the organization regularly review its financial situation

• Financial Statements/Cash Forecasts/ Financial Report/Review of Performance Reports are different names for such a process

29

The In-Year Budget Management Mix

30

Reliable Cash

Management

Financial Data

Risk

Commitments

Forecasts

Projections

Comparisons

From Cash Flow to Cash Forecasting: Financial Statements

ì The cash management process is not a purely financial function. In fact it will fail if it is.

ì Managers’input at the beginning, middle and end is essential

ì Most financial information is submitted to the manager for decision

ì Means moving some decisions up the ladder, overseeing other financial managers, aggregating data to the level of the entity

31

Some other basic questions that good financial analysis can help answer

ì Is the organization on budget?

ì Will there be over-runs, will there be surpluses?

ì Have the budget assumptions changed? ì Is resource use matched to objectives?

ì How is the organization or its units performing relative to previous years, to each other and to plan?

ì Are significant shifts being detected in this data?

32

Some other basic questions that good financial analysis can help answer • What is the significance of these shifts? • Is there a need for extra-ordinary action? Supplementary

funding? Internal reallocation? Emergency funding? • How are managers performing? • What opportunities exist to solve problems internally or to

meet unplanned demands that are nonetheless important for the organization?

33

Elements of an In-Year Budget Management System

• An appropriated budget • Build in changes and modifications to the approved budget

to create an adjusted budget

• Cash flow projections over the budget period: the in-year cash flow or expenditure plan

• A system of measuring actual financial performance in relation to the projected plan

34

Elements of a Cash Management System

ì A system of monitoring performance, identification of variances and reporting results at the appropriate level

ì The capacity for management discussion and analysis of the results and variances

ì A governance mechanisms that would ì review the results, ì assess variances and their analysis, ì determine adjustments needed and ì make decisions needed to affect those adjustments.

35

Roles and Responsibilities • Senior management must set budgets and program direction • Line managers must manage the resources they are given to carry out

programs • Financial advisors must provide information for decision making to budget

setters as well as advice line managers about their budgets • Financial advisors must also provide information and analysis to identify

variances, offer comparisons and further analysis of budget perform and make recommendations to line managers and senior managers

36

Roles and Responsibilities • Financial advisors must prepare reports for senior mangers

to make decisions

• Line managers must respond to variances against plans with explanations, solutions and alternatives

• Senior managers must determine what actions to take based on these two sets of inputs.

37

38

Budget Appropriated

Adjusted Budget

Budget Plan for Year

Cash Requirements

Hold Backs/Reserves/

Adjustments

Reporting Results: Actual vs

Plan: Financial and Operations

Variance Reports and

Analysis Management

Discussion and Analysis

Senior Management

Reporting and Review

Senior Management

Direction: Reallocation

Adjusted Budget Plan for Year

Assess Budget Implications for Next Year

The In-Year Budget Management Cycle

Expenditure Plans of Organization: Budget, Program

• All financial reporting and in-year decisions begin with a budget allocation to a responsibility centre

• Difficult to hold a manager accountable if she/he does not know his/her budget

39

Impediments to establishing a base budget

• Uncertainty in the financial position • Failure of legislative authority to approve appropriations

• Failure of the department/ministry to distribute the budget to responsibility centres

• Program change announcements made without budget adjustments

40

Impediments to establishing a base budget

ì Senior managers withhold authorities pending further changes

ì Dependency on external funding sources, e.g. intergovernmental transfers

ì Multiple sources of program funding within the organization but not within the responsibility centre, e.g. centrally held funds

ì Creation of reserves, hold-backs and only provisional budgeting

41

42

[1] Grants and Contributions are a Special Fund and cannot be reallocated to other budgets. [2] Capital Expenditures are a Special Fund and cannot be reallocated with permission from Management Board using a formal submission process. However, some non-recurring salary costs for project management and implementation can be built into the capital budget.

Allotment Original Budget - April 1

Salaries 217,600,000

Benefits [1] 43,520,000

Overtime Salary Dollars 4,085,000

Operating and Maintenance 64,766,850

Grants and Contributions[2] 5,600,000

Capital Expenditures [3] 7,500,000

Total 343,071,850

Average FTE Costing 68,000

Total Number of Approved FTEs [4] 3200

Expenditure Plans of Organization: Budget, Program

• Budgets for responsibility centers are the result of the budgetary process that is then modified within the organization as funds are distributed

43

Reviewing what is a responsibility centre in an organization: chief

defining characteristics.

44

[1] Allowances are automatically distributed in the same way.

Allotment DMO Policy Operations Inspection CIO CFO Total

FTE 150 150 1200 1100 300 300 3200

Salaries 10,200,000 10,200,000 81,600,000 74,800,000 20,400,000 20,400,000 217,600,000

Allowances 2,040,000 2,040,000 16,320,000 14,960,000 4,080,000 4,080,000 43,520,000

Overtime 0 250,000 1,000,000 2,335,000 500,000 0 4085000

O & M 3,000,000 2,000,000 20,000,000 24,000,000 11,000,000 4,766,850 64,766,850

Gs & Cs 2,000,000 3,600,000 0 0 0 0 5600000

Capital 500,000 300,000 2,000,000 2,000,000 2,500,000 200,000 7,500,000

Total 17,740,000 18,390,000 120,920,000 118,095,000 38,480,000 29,446,850 343,071,850

Expenditure Plans of Organization: Budget, Program

ì Subject to adjustments and clarifications: ì In-year program adjustments ì External charges, e.g. central services ì Reserves and partial distributions by senior management

ì Objective is to arrive at the Adjusted Budget of the responsibility centre – this gives the actual base of funds available

45

To Get to an Adjusted Budget

ì Take original budget ì Apply changes: increases, decreases, etc ì Allocate to units and total. ì An adjusted budget is not a projection: it reflects decisions and changes

subsequent to the original budget ì Important to clarify exactly what the budget manager has to work with at

the start ì Budgets can also be adjusted throughout the year as part of the cash

management process, as new funds become available (or are removed) or to reflect policy changes.

46

47

LINE ITEM BUDGET This fiscal year

CHANGES ADJUSTED BUDGET

This fiscal year SALARIES 3,500,000 750,000* 4,250,000 OVERTIME 500,000 (100,000)** 400,000 TRAINING 250,000 75,000¹ 325,000 TOTAL STAFF COST

4,250,000 725,000 4,975,000

*Salary adjustments from collective bargaining = 400,000 plus 350,000 from DM’s special youth employment funds

** Departmental target to reduce overtime – your share is 100K

¹Special central agency funding – one year only – for technology training.

Developing a Cash Flow Plan for the Responsibility Centre

• In-year cash management requires a sense of how funds will flow or be expended

• Eliminate non-cash accruals

48

Do Not Just Divide by 12!

Developing a Cash Flow Plan for the Responsibility Centre ì Generally managers are expected to prepare cash flow plans based

on: ì Historical data ì Their program plans – the implementation side ì Know commitments ì Addressing risks

ì Not all funds flow at once – some costs are distributed over the fiscal year, some are spent at one time, some are held in reserve

ì Often capital is on a different cash flow cycle and not included.

49

Developing a Cash Flow Plan for the Responsibility Centre ì Such flows are predictable within limitations. e.g. salary dollars ì Some are less predictable in terms of planning, e.g. overtime, but

such unpredictability can be mitigated using historical data ì Cash flows can be limited by managerial discretion:

ì Spending authority limits, ì Internal budget restrictions, ì External restrictions, e.g., salary dollars for salary only ì Tolerance boundaries.

50

Developing a Cash Flow Plan for the Responsibility Centre

• Some items are spent all at once, e.g. transfers or major capital purchases.

• Are there any other rules of the game set in place by the organization: • Informal reserves and hold-backs • Reporting frequency • Degree of detail • Contingency funds – formal and informal • Budget conditions • Limitations on managerial flexibility

End result: Managers Expenditure Plan

51

Factors to take into account in building a cash flow plan

• Previous patterns of inflow in past year, e.g. for an NGO: donations tend to peak during major fund-raising events with regularity, major government funding tends to flow two times a year provided the grants is approved in advance

• Anticipation of any changes that might cause such a flow to alter, e.g. the organization decides that it will change its fund-raising campaign to a different type and a different time, a major donor adjusts some criteria and is reviewing its procedures which may create delays.

52

Factors to take into account in building a cash flow plan

• Timing of the maturity of investments or endowments in various funds;.

• Awareness of the timing of cash requirements to match them up with inflows, e.g. major capital expenses are anticipated for the summer, thereby necessitating a cash outflow demand surge in late summer; this will not help anticipate inflows, but will inform and condition the risks and urgencies around the first two elements.

53

54

Expenditure Plans of Organization: budget, program

Financial Performance Reports

Manager’s Expenditure

Plan

The Financial Analysis Process

ì Whenever possible gets comparative data: ì - for the organization over time, ì - for the organization's peers, and ì - for benchmarking organizations (if they exist).

ì Organize the information and complete the analysis. ì Will compare financial performance to the Manager’s

Expenditures Plan – often input into organizational financial system

55

Analyzing Expenditures

• Estimating the timing of expenditures is critical for cash flow purposes

• Dividing the budgeted amount by 12 months is not a good strategy

• As the fiscal year progresses, analyze projected spending amounts.

56

Analyzing Expenditures

• Use the projected budget as a basis for the cash flow • Make sure all reductions or increases are accounted for

in the cash projection

• For example, if spending freezes have been enacted, have the anticipated savings been accounted for in the cash flow projection?

57

Analyzing Expenditures ì Analyze expenditure patterns ì Salaries and benefits are usually the largest expenditures ì Getting the timing right is key to managing cash flow ì Are there months that have additional payments, costs or

less demand? ì Review the timing of other payments.

58

Analyzing Expenditures ì How are materials and supplies purchased? Just-in-time

purchasing throughout the year? Ordered in bulk at various points during the fiscal year?

ì Don’t forget about the impact of restricted funds. These can require significant cash outlays at the start of the fiscal year

ì Having an annual purchasing cutoff date helps when closing the books But it also can create a big stack of bills that have to be paid at the same time.

59

Analyzing Expenditures ì As cash flexibility decreases, priorities will need to be set in order

to determine what gets paid first. ì Salaries and benefits have specific statutory timelines for payment ì That leaves vendor payments for providing flexibility. Maximizing

the use of the billing cycle will become important. In extreme cases, vendors may need to be asked to accept a delay in payments – depends on contractual obligations.

ì Prepare a contingency plan for cash shortages

60

Looking for Problem Areas and Identifying Variances: The uses of historical data

• Why it is important? • Developing comparisons year to year

• Understanding what has changed and what remains the same

• Developing useful variance reporting based on historical data

61

62

Focus on Trend Information and Explaining It

“Overall, the value of new construction in the City for the first three months of the year is 28% more than the same time period last year. The overall increase is due to the new RCMP E-Division Headquarters building.” – City of Surry Quarterly Financial Report, May, 2011

63

All Overtime Hours Used by Month by Fiscal Year

-

15,000

30,000

45,000

60,000

APR MAY JUN JUL AUG SEP OCT NOV DEC JAN FEB MAR

Month

All

Ove

rtim

e H

ou

rs U

sed

2001/02

2000/01

1999/00

1998/99

1997/98

1996/97

1995/96

An Example of the Use of Historical Data

64

York Catholic District School Board

2010-11 YEAR END FINANCIAL REPORT

Note: Excludes General School Budget balance carry-forwards to isolate true Board Working Fund Surplus

Working Fund Accumulated Surplus ("Uncommitted") History as Percentage of Operating Revenues

1998-2011

1.73% 1.64% 1.79%

2.89%

2.39%

1.79% 1.76%1.44% 1.30% 1.17%

0.59%

1.61%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

Year

Perc

enta

ge

Trend Analysis 65

Variance to be Recouped?

We are here

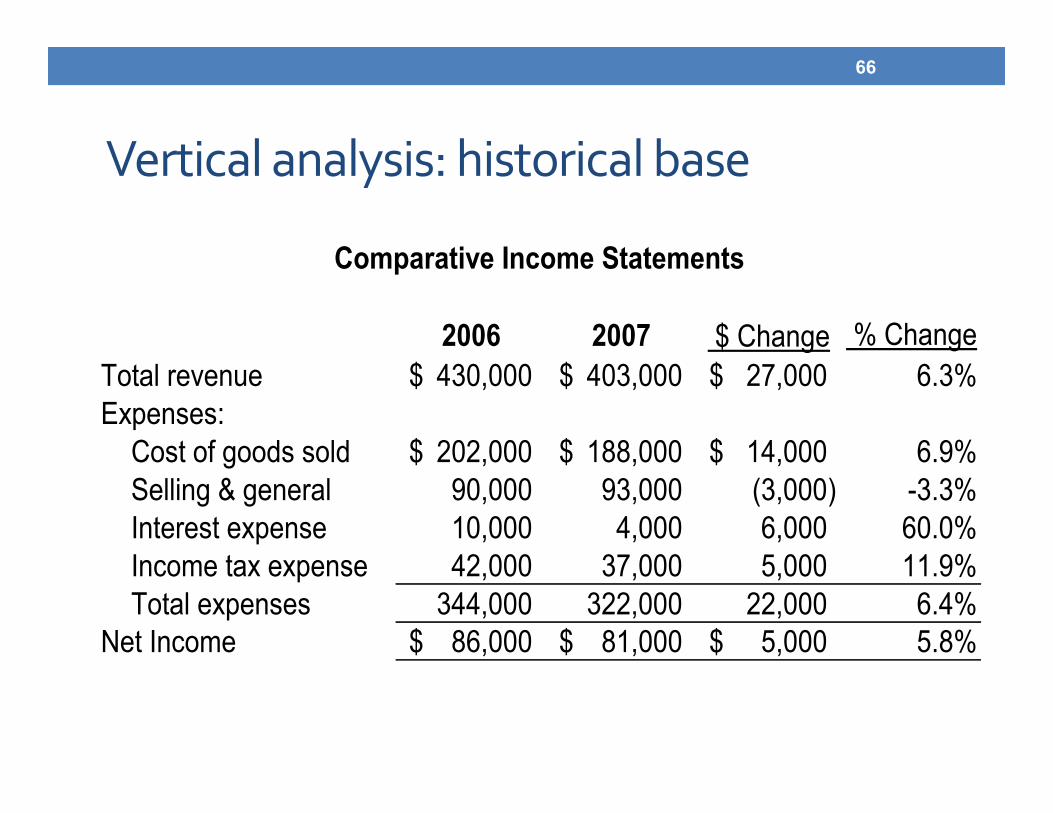

Vertical analysis: historical base

66

2006 2007 $ Change % ChangeTotal revenue 430,000$ 403,000$ 27,000$ 6.3%Expenses:

Cost of goods sold 202,000$ 188,000$ 14,000$ 6.9%Selling & general 90,000 93,000 (3,000) -3.3%Interest expense 10,000 4,000 6,000 60.0%Income tax expense 42,000 37,000 5,000 11.9%Total expenses 344,000 322,000 22,000 6.4%

Net Income 86,000$ 81,000$ 5,000$ 5.8%

Comparative Income Statements

Sometime historical data is non-monetary

67

Table 3: Shelter Admissions

0510152025303540

J F M A M J J A S O N D

Month

Adm

issi

ons

200220032004

Analyzing Encumbrances and Commitments

68

• Key tool in governments to ensure that budgets do not go over approved limits

• “Financial commitments are obligations to outside organizations or individuals that become liabilities if and when terms of exiting contracts, agreement or legislation are met.” – CICA

• Will generally not be in your financial reports, but rather in your forward spending plans

• For cash forecasting, commitments may not be formal entries but rather managerial statements of intention that certain funds will be fully spent for their intended purpose even though they do not appear as either formal commitments in a cash balance sheet or liabilities in an accrual based balance sheet

Analyzing Encumbrances and Commitments

• Positive uses: inform management of actual flexibility and spending plans

• Negative use: protect funds

• Danger of unspent funds at the end of the year • Committed amounts reduce the balance available for

expenditure in the remaining portion of the year and must be brought into the calculation of any projection.

69

Developing a Spending Plan/Forecast

• Level of detail should reflect need for information, risk, materiality and timeliness, e.g. once a month, once quarterly

• Managers should be able to project cash flows over the year

70

Developing a Spending Plan/Forecast

• Dividing by 12 hardly useful or generally not realistic – forecast should reflect the ebbs and flows of expenditure patterns

• Block or grant expenditures tends to be all at once

71

Quality of Forecasting and Data • Key to provide financial information derived from current

information, known changes and trends and announcement

• Comparison of data from current year to prior years always useful

72

Translating and Interpreting Data

• Usefulness of different perspectives • Budget managers

• Financial advisor

• Organizational head

• Corporate financial advisor

73

Translating and Interpreting Data

• Role of the challenge function • Reporting that makes data relevant to managers and to

decision makers: management’s discussion and analysis (MD&As)

74

Compare and Contrast

75

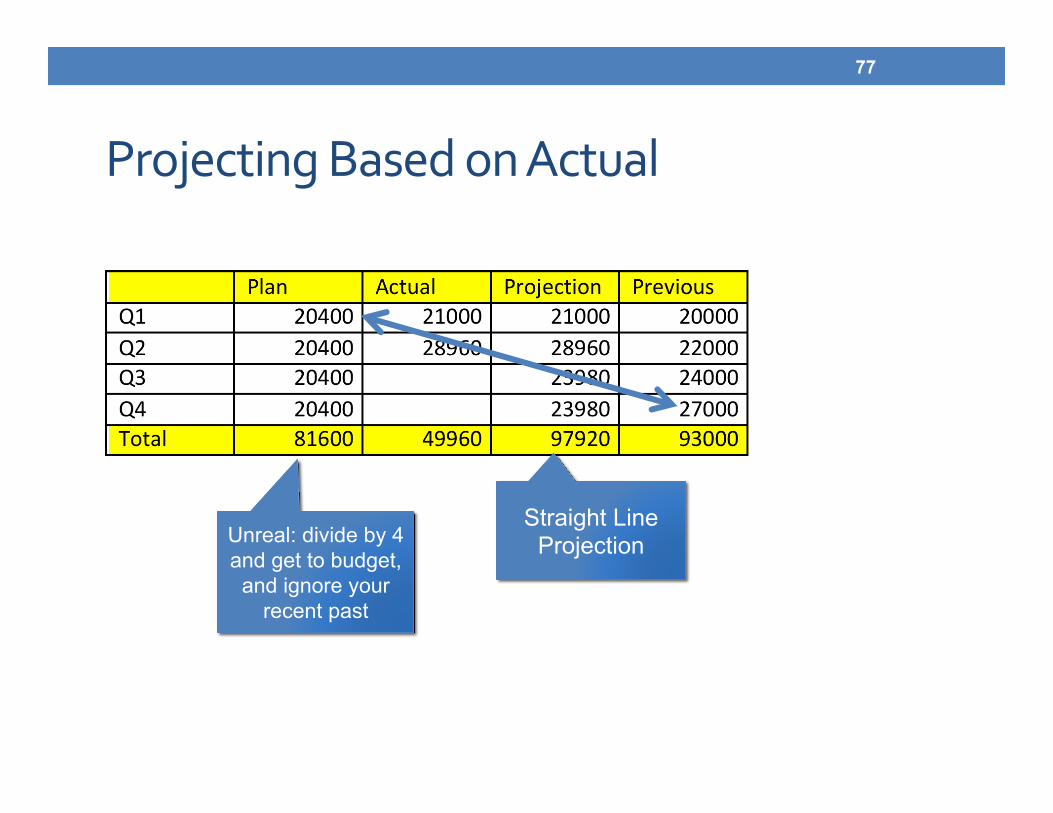

Projecting Based on Actual: Example • Here is what we know: The Opera*ons Branch with an approved salary budget of $81,600,000 at mid year in the fiscal year is repor*ng increasing salary pressures.

• Actuals indicate that it has spent 60% of its total budget when only half way through the year. This is a leap from previous year of 45%, which at mid year is a safe cushion

76

Projecting Based on Actual

77

Straight Line Projection Unreal: divide by 4

and get to budget, and ignore your

recent past

Projecting Based on Actual

78

0

20000

40000

60000

80000

100000

120000

Q1 Q2 Q3 Q4

Plan

Actual

Projec*on

Previous

The Gap

Management Discussion and Analysis

• Should provide basis for discussion and decision making • Language should be business-oriented and not excessively

detailed

79

Management Discussion and Analysis

• Objective and easily readable analysis of financial activities based on currently know facts, decisions or conditions

• Projections are an essential part of cash forecasting, but should be fact based whenever possible

• Otherwise projections should be subject to a variety of opinions to test the hypotheses they contain

80

Questions the Management Report must answer…..

ì Are we going to be within our budget allotments? ì Are we operating according to our budget plan? ì How does our performance compare with relevant historical

data? ì Does this performance mean that more funds may be

necessary or that some funds may become surplus in this area and available for reallocation?

ì What are the variances and why have they occurred?

81

Questions the Management Report must answer…..

• What is the responsibility centre manager going to do about the negative variances?

• Are positive variances within a retention range for the local manager or are they available for other needs outside the unit but within the organization?

• Do we have the needs and authorities to reallocate these funds? • What does this information tell us about the performance of the manager in

this unit? • What does this information tell us about the long-term funding?

82

Reporting and Discussing Risk in Cash Management

• Need to distinguish between short-term and long-term risk • Risk is a key element in determining to change budget

allocations either temporarily or permanently

83

Reporting and Discussing Risk in Cash Management

• Key risk in cash management is over-expenditure of budget or failure to fully use funds available and needed

• Other types of risk to consider: • Inappropriate use of funds • Surges or declines in demand leading to cost over-runs or under-usage • Emerging and unanticipated issues: mad cow, SARS, BP

• Financial reports should not originate the organization’s development of risk but should reflect its overall management process,

84

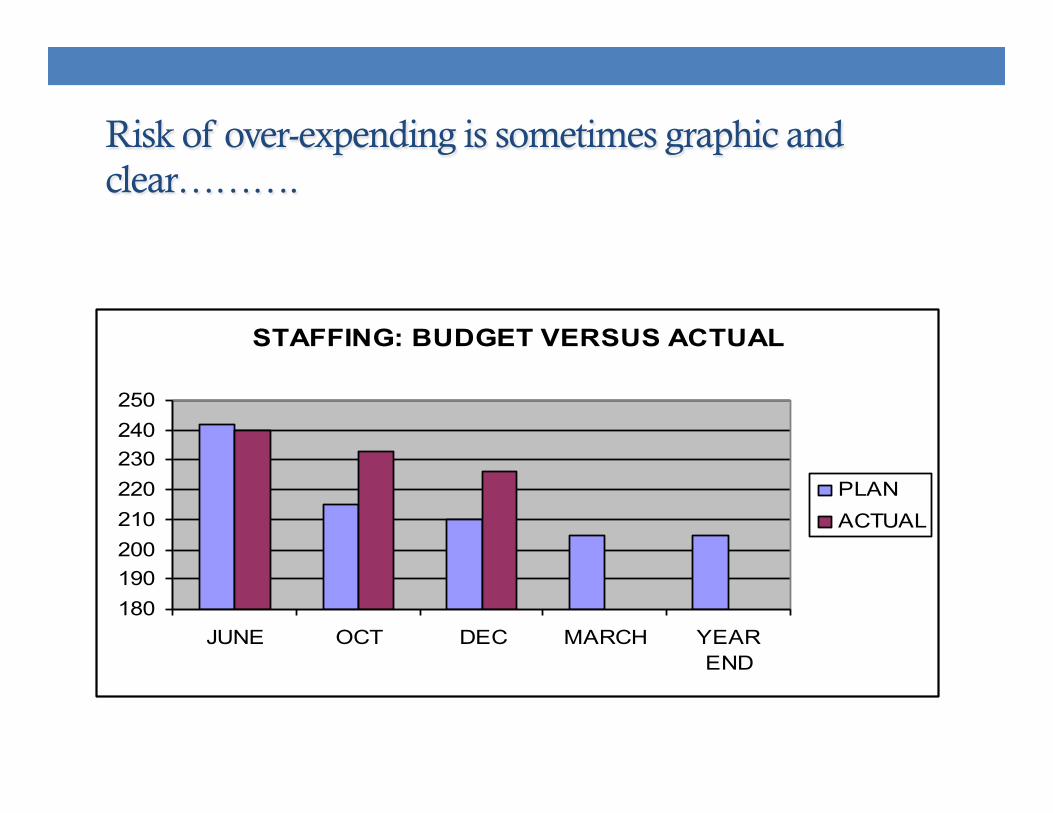

Risk of over-expending is sometimes graphic and clear……….

85

STAFFING: BUDGET VERSUS ACTUAL

180190200210220230240250

JUNE OCT DEC MARCH YEAREND

PLANACTUAL

Cash Forecast Report • Can take many forms: briefing notes, PowerPoint

presentation, charts, graphs

• Should have some predictability in format and language

86

Cash Forecast Report • Some analytical information that is important:

• Historical comparisons

• The cost of the variance to date, i.e. how much of the actual budget has been spent

• The projected variance should nothing change, i.e. the straight line projection

• The variance in comparison to similar units in the system

87

Cash Forecast Report ì Additional components of the report that set managerial

context: ì What caused the gap between expectations and results, e.g. fewer

retirements or transfers than required? ì Workload determinants that changed in actual performance, e.g.

inmate population increases and opening of an old unit for an emergency

ì Inefficiencies that remain, e.g. excessive posts. ì Limitations of the budget itself ì Actions that could be taken to correct the situation.

88

Cash Forecast Report • Should be a regular submission to the senior management

committee of the organization

• Should move financial information, various background information, etc into the realm of text, ideas and integration

89

Cash Forecast Report • Generally the role of finance to prepare but not the role of

finance to address: operational managers, responsibility centre heads, their bosses are key to this

90

Cash Forecast Report • It cannot cover all data – only relevant information:

• Exceptional performance issues

• Issues that the senior management wants to keep a close eye on

• Highly political or contentious issues

• Separate funds

• Areas of operational vulnerability or poor performance

91

Cash Forecast Report

• Questions to ask about variance: • What does the trend look like: is it in the right direction? If so, can we

tolerate the slower pace?

• Is this isolated to this unit or a general phenomenon?

• Did we set realistic targets?

• Can we fund the shortfall that we see emerging?

• Is this manger delivering and, if not, is this enough to force us to take some action like removing him and finding some else.

92

Cash Forecast Report • Should be a consensual document or at least focused on key

decisions that CFO wants to receive or see made

• Should be devoid of surprise for all players

• Role of the top manager: Deputy or organizational head: steering towards decisions, reconciling differences

93

94

Salaries Operating Grants

Original Budget

2,000,000 3,500,000 1,000,000

Adjusted Budget

2,225,000 3,000,000 1,000,000

Planned Expenditures to date

1,250,000 1,500,000 750,000

Actual Expenditures

1,110,000 1,800,000 600,000

Variance from Plan

140,000 (300,000) 150,000

But this is not enough……. • Need to project to year-end • Need to identify end-of-year overages and

underages • Or, have to project to balance the budget

95

96

Salaries Operating Grants

Original Budget 2,000,000 3,500,000 1,000,000

Adjusted Budget 2,225,000 3,000,000 1,000,000

Planned Expenditures to date

1,250,000 1,500,000 750,000

Actual Expenditures

1,110,000 1,800,000 600,000

Variance from Plan

140,000 (300,000) 150,000

Commitments 200,000 150,000

Projected Expenditures Year End

2,150,000 3,200,000 900,000

Projected Variance at Year End

75,000 (200,000) 100,000

Sure Signs that there will be trouble

• Governance flaws – poor oversight of spending. No managerial review unless there is a problem.

• Absence of communication with operational front-end of the organization in budgeting and monitoring..

• Lack of cooperation.

97

Sure Signs that there will be trouble

• Failure to maintain reserves or contingencies where warranted..

• Insufficient consideration of long-term collective bargaining agreement and human resource policy effects.

• Flawed multiyear projections.

• Inaccurate revenue and expenditure estimations.

98

Sure Signs that there will be trouble ì No integration of position control with payroll costing. ì Limited access to timely personnel, payroll, and budget control

data and reports. ì Escalating reliance general fund or reserve encroachment to fund

regular programming. ì Lack of regular monitoring. . Poor cash flow analysis and

reconciliation. ì Failure to recognize year-to-year trends.

99

Some Solutions for Serious Cash Management Problems

100

Panic!

Some Serious Solutions for Serious Cash Management Problems • Prepare your story and a plan: read The Cash Management Games People Play • Find ways to slow down spending where there is discretion • Review commitments (both formal and informal) to determine flexibility to shut

down or slow down • Reduce staff where this will work quickly and without further costs, e.g.

severance • Not filling positions • Slowing down staffing • Delay orders, put them off until the next period or year

101

Some Serious Solutions for Serious Cash Management Problems ì Slow down programs/ eliminate services ì Beg or borrow from others within the department: avoid

mortgaging your future if you can ì Seek temporary relief from your boss, the organization as a whole ì Seek out contingency funds, if they exist ì Examine possible use of non-restricted funds ì Seek a change in budget if it can be justified

102

Setting the Rules for Distribution and Redistribution of Surpluses, Carry-Forwards etc

• Huge tension between protecting your own resources and making a corporate contribution: affects information flow for senior management

• Important to understand how financial and performance information may be used

103

Setting the Rules for Distribution and Redistribution of Surpluses, Carry-Forwards etc

• Danger of surprise in rules change – unless subject to extraordinary situations

104

Danger in awarding bad management: coming to the rescue is one

thing but doing it several years running simply creates new rules

That rewards bad behaviour.

Setting the Rules for Distribution and Redistribution of Surpluses, Carry-Forwards etc

• Example of reporting surpluses that financial analysis does not disclose: is it kept in the responsibility centre or does the organization have a ‘wish list’ or ‘critical needs list’ that distributes available funds to the list with no hold back in the responsibility centre – impacts human behaviour significantly

• Issue of the use of the carry-forward provisions: is that rolled up corporately and used for other purposes or is it retained within the responsibility centre: has an impact on high level flexibilities

105

106

Ende Fin

Lopussa

Koniec

Final

Sionunda