public relations & information department obere ... · dr shokri m. ghanem head, energy studies...

TRANSCRIPT

2

Organization of the Petroleum Exporting CountriesPublic Relations & Information DepartmentObere Donaustrasse 931020 ViennaAustria

Head, PR & Information DepartmentEditor-in-ChiefFarouk U. Muhammed, mni

EditorGraham Patterson

DesignerElfi Plakolm

TypesetterDiana Lavnick

CirculationLeo Rettenbacher

© Copyright 1999Organization of the Petroleum Exporting CountriesISSN 0474-6317

Cover photo courtesy of Saudi Aramco/S. M. Amin;photos on pages 12 and 18 courtesy Saudi Aramco;photos on 36 and 40 copyright OPEC

Printed in Austria by Ueberreuter Print and Digimedia

3

ontents

Foreword 4

Heads of Delegation 6

Members of the Board of Governors 8

National Representatives 10

Officials of the Secretariat 11

OPEC in the World Economy 12

Oil Market Developments 18

OPEC Press Releases 36

Activities of the Secretariat 40

4

I would like to start by welcoming the reader to the

1998 edition of the OPEC Annual Report. In my

foreword last year, I described as being like a “violent

storm” the oil price slump that began in the fourth

quarter of 1997, and lasted through the whole of

1998 and into the early months of this year. If I may

continue the metaphor from my current vantage

point of mid-1999, the storm now appears to have

passed, but there can be no doubt about the se-

riousness of the economic damage it has wreaked

not only on OPEC’s Member Countries, but also on

the rest of the oil industry.

The average price of the OPEC Reference Basket of

seven crudes last year was $12.28, the lowest annual

average since its introduction in 1987. It should be

pointed out that OPEC Member Countries’ revenues

from hydrocarbon exports took a severe hit, and

six of the Organization’s eleven Members registered

negative gross domestic product (GDP) growth rates

during 1998.

This decline in oil and gas revenues, nevertheless,

did compel OPEC Members to take a number of

economic and fiscal measures that should serve to

bolster their economies in the coming years. These

measures included boosting non-oil exports in order

to diversify sources of income and lessen reliance

on oil revenues, reducing government expenditure

where possible and privatizing some public utilities.

oreword

5

However, in the final analysis, it may well be that the most positive long-term change wrought

by the oil price slide of last year was the attention it focused on OPEC’s consistent theme —

the need for co-operation between the Organization and non-OPEC oil producers. OPEC has

long maintained that it cannot continue to shoulder the burden of stabilizing the oil market

alone, and in 1998 and 1999 we saw this point acknowledged by a number of important non-

OPEC nations, which voluntarily agreed to restrain their own oil output to help restore prices

to fair and equitable levels.

Two rounds of joint OPEC/non-OPEC production restrictions were agreed upon last year. When

the third round of such cuts was formalized by the 107th OPEC Conference last March, the

oil market began to regain its equilibrium, leading to the price levels we see today. There could

be no clearer demonstration of the need for OPEC/non-OPEC co-operation than the oil price

recovery that we have witnessed this year.

Finally, as I prepare to take my leave of OPEC, as soon as a new Secretary General is appointed

(following my own appointment as Presidential Adviser on Petroleum & Energy to the Nigerian

Government), may I say that I am proud and honoured to have been able to play a role in

the history of our esteemed Organization.

I wish OPEC and all its Member Countries continuing success not only in their endeavours to

bring stability and harmony to the world oil market, but also in giving their citizens, and indeed

the citizens of all the developing countries, a much better standard of living.

Dr Rilwanu LukmanSecretary General

6

Algeria

HE Dr Youcef YousfiMinister of Energy & Mines

Indonesia

HE Dr Kuntoro MangkusubrotoMinister of Mines & Energy(from March 1998)

Socialist People’sLibyan ArabJamahiriya

HE Abdalla Salem El-BadriSecretary of the GeneralPeople’s Committee of Energy

Islamic Republic of Iran

HE Bijan Namdar ZangenehMinister of Petroleum

Iraq

HE Dr Amer MohammedRasheedMinister of Oil

Kuwait

HE Sheikh Saud NasserAl-SabahMinister of Oil(from March 1998)

Heads of Delegation

7

Nigeria

HE Chief Rasheed GbadamosiMinister of National Planning

Qatar

HE Abdullah bin HamadAl AttiyahMinister of Energy & Industry

Saudi Arabia

HE Ali I. NaimiMinister of Petroleum& Mineral Resources

United Arab Emirates

HE Obaid bin SaifAl-NasseriMinister of Petroleum &Mineral Resources

Venezuela

HE Dr Erwin José ArrietaMinister of Energy & Mines

8

AlgeriaMr Rachid Boularas

(ad hoc from October 1998)

IndonesiaMr Soepraptono Soeleiman

(from March 1998)

Islamic Republic of IranHE Hossein Kazempour

Ardebili

IraqMr Saddam Zabin Hassan

KuwaitMs. Siham Abdulrazzak RazzouqiChairman of the OPEC Board of

Governors

Socialist People’sLibyan Arab Jamahiriya

Mr Ali A. Fituri

Members of the Board

9

VenezuelaMr Heliodoro Quintero

NigeriaDr Aboki Zhawa

(from March 1998)

QatarHE Abdulla H. Salatt

Saudi ArabiaHE Suleiman Jasir

Al-Herbish

United Arab EmiratesHE Mohamed D.

Al Hamli

of Governors

10

National Representatives

AlgeriaMr Rachid Boularas

IndonesiaMr Iin Arifin Takhyan (from September 1998)

Islamic Republic of IranDr Ali Akbar Gharani (from February 1998)

IraqMr Mubdir A. S. Al-Khudhair

KuwaitMr Wael Mohammad Al-Mudhaf

Socialist People’s Libyan Arab JamahiriyaMr Sultan K. Abushawashi

NigeriaMr Mohammed S. Barkindo

QatarMr Jassim Nama

Saudi ArabiaDr Majid A. Al-Moneef

United Arab EmiratesMr Ali Saeed Al-Badi

VenezuelaDr Gloria Mirt

to the Economic Commission Board

11

Secretary GeneralHE Dr Rilwanu Lukman

Director, Research DivisionDr Shokri M. Ghanem

Head, Energy Studies DepartmentDr Rezki Lounnas

Officers

Mr Simon Adewole (left May 1998)

Mr Hamid Dahmani

Mr Fathor Rahman

Dr Davoud Ghasemzadeh

Dr Abdul Muin

Mr Mohammad Alipour-Jeddi

Head, Petroleum Market Analysis DepartmentMr Javad Yarjani

OfficersMr Sunmonu Adeyeye (left November 1998)

Mr Aliakbar Vahidi Ale-Agha

Mr Khaled Baruni

Mr Uwaifo Egbe

Mr Faris A.R. Hasan

Mr Mohamed Behzad

Dr Seyed Mohammadreza Tayyebi Jazayeri

Mr Jamal Moh. D. Bahelil

Mr Oswaldo J. Salas Casanova

Head, Data Services DepartmentDr Deyaa L. Alkhateeb

OfficersMr Mohsen Khoshzamir

Mr Houshang Parvizi (left November 1998)

Dr Jorge Goncalves

Mr Vincent Job

Head, Administration & HumanResources DepartmentMr Abbas N. Afshar (left August 1998)

Acting Head of Department andHead, Human Resources Section

Dr Talal A. Dehrab

Officer

Mr Awni O. Al-Nuaimi (left September 1998)

Acting Head, Public Relations & InformationDepartmentMr Farouk U. Muhammed

OfficersMr Touss Sepehr (left April 1998)

Mr Fernando J. Garay

Head, Legal OfficeMr Ahmed Abdulaziz (left July 1998)

Head, Office of the Secretary GeneralDr Nafrizal Sikumbang (left October 1998)

Note

As of end-1998.

Officials of the Secretariat

12

The global economy in 1998 was affected, to various degrees, by the phenomenon of negative interaction

between the Asian financial turmoil, the oversupply of oil that resulted in the collapse of oil prices which

started in the last quarter of 1997, the devaluation of the Russian rouble, the depreciation of the yen

and the delay of financial reforms in Japan. All of these factors combined to create an unsettled international

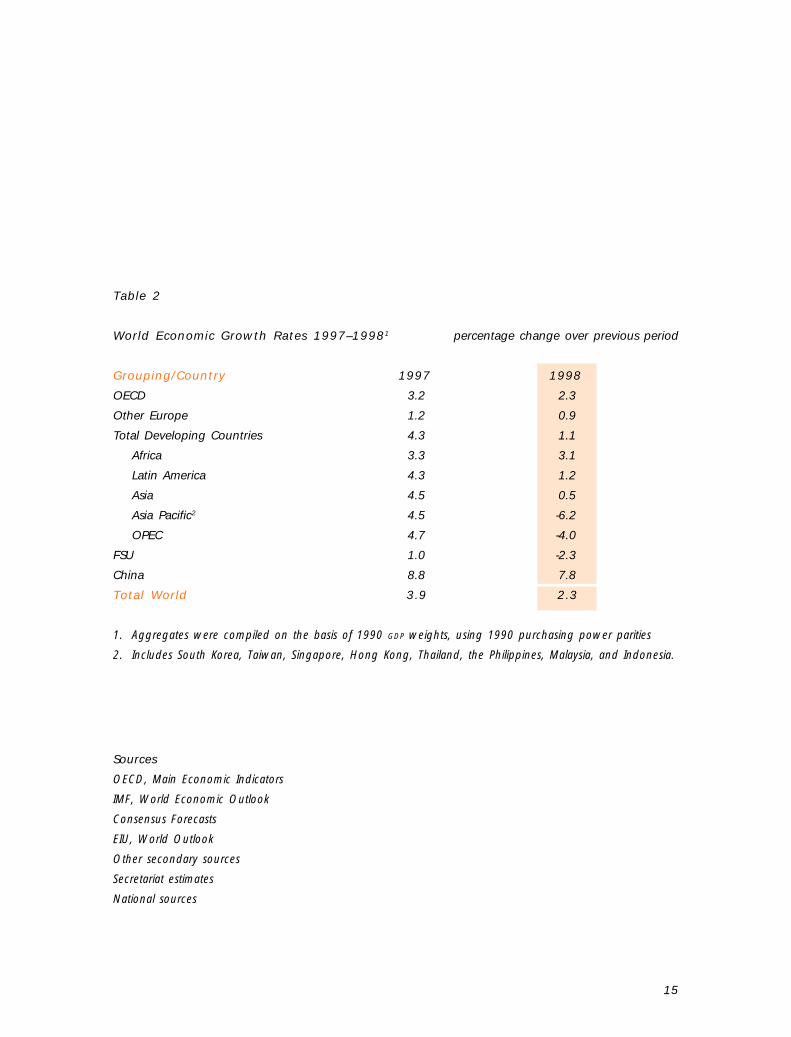

economic and financial environment. The overall world economic growth rate slowed to 2.3 per cent

in 1998, down from 3.9 per cent in the previous year. The gross domestic product (GDP) growth rate

of non-OPEC Developing Countries (DCs) in general fell to 2.3 per cent in 1998 compared to the 4.2

per cent growth rate in 1997, while the Asia Pacific countries (including South Korea, Taiwan, Singapore,

Hong Kong, Thailand, the Philippines, Malaysia and Indonesia) saw negative growth of –6.2 per cent

in 1998, after positive growth of 4.5 per cent in 1997. Similarly, growth in OPEC Member Countries (MCs)

as a whole fell significantly to –4.0 per cent in 1998, down from 4.7 per cent in the previous year (see

Table 1). Growth rates in the OECD countries slowed to 2.3 per cent in 1998 against 3.2 per cent in

1997 and Other Europe slowed to 0.9 per cent from 1.2 per cent (see Table 2).

These figures illustrate that a deterioration in the economic situation occurred all over the world, but most

severely affected were the Asia Pacific region and the OPEC MCs. These results were a consequence of

interaction between the Asian financial turmoil which resulted in a fall in oil demand, and excessive oil

supplies. Both groups of economies are extremely vulnerable to fluctuations in the world economy, for

while OPEC MCs' GDPs depend heavily on oil exports, Asia Pacific financial services rely very much on foreign

capital due to the limited level of local savings.

OPEC was second only to the Asia Pacific region as the leader of negative world economic growth in

1998. Petroleum export revenues fell by 33.5 per cent, that is from $166.0 billion in 1997 to $110.1bn

in 1998. This created a current account deficit of –$15.4bn compared to –$62.6bn for non-OPEC DCs,

and a surplus of $17.5bn in OPEC MCs in 1997 (see Table 3). Consequently OPEC MCs reserves (excluding

gold) retreated by 3.1 per cent from $76.7bn in 1997 to $74.3bn at the end of 1998.

PEC in theWorld Economy

13

There were also a number of related economic developments in 1998 in OPEC MCs. For instance, the

value of oil exports as a percentage of total OPEC exports dropped from 65.6 per cent in 1997 to 56.3

per cent in 1998. Conversely, the value of OPEC MCs' imports also decreased from $171.2bn in 1997

to $153.8bn in 1998.

In fact, OPEC MCs found themselves facing a gloomy year due to the oil price fall which led to a slump

in oil revenues in 1998. However, OPEC MCs considered as paramount, the need to continue the process

of implementing national economic reforms and achieve further fiscal consolidation. Some of these measures

included reducing government expenditure, boosting non-oil exports, diversifying income sources, and

expanding the role of the private sector through privatization of certain public utilities. Most MCs assumed

modest oil prices for their 1999 budgets.

The average OPEC Reference Basket price fell sharply by about $6.40/b, or 34.24 per cent, from the average

price in 1997 of $18.68/b, down to $12.28/b. However, the US dollar showed strength in the first three

quarters of 1998, then lost some ground in the fourth quarter, but it appreciated by about two per

cent over the whole year. In real terms, after accounting for inflation (of about 1.4 per cent) and

currency fluctuations, the real price of oil dropped by 33.83 per cent. The fall in nominal oil prices was

slightly cushioned by the rise of the dollar against the currencies in the Geneva I + US dollar currency

basket.

According to available international sources, the GDP of six of OPEC's 11 MCs registered negative growth

rates last year: –13.7 per cent in Indonesia, –2.3 per cent in IR Iran, –2.3 per cent in Kuwait, –2.0 per

cent in the SP Libyan AJ and the UAE, and –0.7 per cent in Venezuela. The rest of the MCs did not exceed

a GDP growth rate of 2.6 per cent.

Algeria's GDP growth rate was projected at six per cent prior to the oil price downturn, but was later revised

downward to 2.5 per cent, because the fall in oil export revenue put pressure on the country’s finances.

However, Algeria is a major natural gas exporter, and continued expansion in natural gas exports mitigated

the adverse effects of declining oil revenues to some extent.

Indonesia, which is geographically and economically part of South-East Asia, was badly affected. In order

to cope with its deteriorating economic condition, the country took a number of measures, including lowering

the oil price projection for its 1998–99 budget to $13/b, besides taking measures promoting its oil sector.

Due to the lack of available cash for much-needed investment in its oil sector, Iran looked increasingly

toward foreign investment capital. This included measures such as the reform of foreign investment laws,

the taxation system, national employment regulations, expansion of the electronic commerce system and

an easing of banking and customs procedures.

Despite the constraints in Iraq, its GDP achieved 16 per cent growth in 1998, following the preceding

year's growth rate of 25 per cent. The rates may appear exceptionally high, but this growth took place

from such a low base that it does not signify any substantial recovery.

In Libya the ‘Great Man-Made River’ project was affected by the cash crunch. Inflation was expected to

14

Table 1

OPEC Member Countries:

Real GDP Growth Rates 1997–1998 percentage change over previous period

Member Country 1997 1998

Algeria 1.3 2.5

Indonesia 4.6 -13.7

IR Iran 2.6 -2.3

Iraq 25.0 16.0

Kuwait 2.5 -2.3

SP Libyan AJ 0.5 -2.0

Nigeria 3.9 2.4

Qatar 15.5 2.0

Saudi Arabia 1.9 0.4

United Arab Emirates 0.3 -2.0

Venezuela 5.9 -0.7

Average OPEC* 4.7 -4.0

* Average OPEC was calculated on the basis of 1990 GDP weights using 1990 purchasing power parities.

Sources

International Monetary Fund, International Financial Statistics

IMF, World Economic Outlook

Economist Intelligence Unit, Country Reports, second and third quarters 1999

Asia Pacific Consensus Forecasts

Latin America Consensus Forecasts

Other secondary sources

Official OPEC Member Countries’ statistics

Secretariat estimates

OPEC in the World Economy

15

Table 2

World Economic Growth Rates 1997–19981 percentage change over previous period

Grouping/Country 1997 1998

OECD 3.2 2.3

Other Europe 1.2 0.9

Total Developing Countries 4.3 1.1

Africa 3.3 3.1

Latin America 4.3 1.2

Asia 4.5 0.5

Asia Pacific2 4.5 -6.2

OPEC 4.7 -4.0

FSU 1.0 -2.3

China 8.8 7.8

Total World 3.9 2.3

1. Aggregates were compiled on the basis of 1990 GDP weights, using 1990 purchasing power parities

2. Includes South Korea, Taiwan, Singapore, Hong Kong, Thailand, the Philippines, Malaysia, and Indonesia.

Sources

OECD, Main Economic Indicators

IMF, World Economic Outlook

Consensus Forecasts

EIU, World Outlook

Other secondary sources

Secretariat estimates

National sources

16

Table 3

Comparison: OPEC and Non-OPEC Developing Countries

1996 1997 1998*

OPEC non-OPEC OPEC non-OPEC OPEC non-OPEC

Real GDP growth rate 4.9 5.2 4.7 4.2 -4.0 2.3

Petroleum export value ($bn) 165.4 58.4* 166.0 55.0 110.1

Value of non-petroleum exports ($bn) 76.4 878.1* 86.9* 918.0 85.4

Oil exports as % of total exports 68.4 6.2* 65.6* 5.6 56.3

Value of imports ($bn) 153.3 1,083.3* 171.2* 1,126.0 153.8

Current account balance ($bn) 25.4 -74.5 17.5* -87.9 -15.4 -62.6

Average Reference Basket price ($/b) 20.29 18.68 12.28

Crude oil production (m b/d) 24.8 9.2 25.4 9.4 27.8 9.7

Reserves (excluding gold) ($bn) 71.7 521.3* 76.7* 541.5 74.3 652.8

* Estimated.

Sources

IMF, International Financial Statistics

IMF, World Economic Outlook

IMF, Direction of Trade Statistics

EIU, World Outlook 1999

EIU, Country Reports

OPEC Database

Secretariat's estimates

OPEC in the World Economy

17

stabilize at 24 per cent in 1998, compared to 25 per cent in 1997 and 39 per cent in 1996. Negative

growth of –2.0 per cent was witnessed in 1998.

In Nigeria, GDP growth slowed to 2.4 per cent during the year against 3.9 per cent growth in 1997. The

authorities cut back on funding for joint ventures in the oil sector, delayed the release of capital budget

funds, and capped foreign debt repayments.

Saudi Arabia's real GDP growth rate slowed to 0.4 per cent in 1998, compared to the previous year's rate

of 1.9 per cent. Oil export revenues were expected to fall to $29.4bn during 1998, 35 per cent lower

than the previous year's level. Investment in general was set to slow in 1998, as part of efforts to reduce

government expenditure. Meanwhile the authorities moved forward cautiously with the privatization of

state assets.

For other MCs, namely Kuwait, Qatar, and the UAE, the GDP growth rates were –2.3 per cent, 2.0 per

cent, and –2.0 per cent, respectively. The steep deceleration in GDP growth rates was due to the fall in

Asian oil demand and the financial crisis in the region, which is considered the main market for Gulf crudes.

Qatar’s GDP growth was not negative because of the mitigating effects of LNG sales.

Venezuela’s GDP growth rate was –0.7 per cent in 1998 compared to the previous year's reasonable growth

rate of 5.9 per cent.

In summary, the poor economic performance in 1998 resulted from the interaction between the Asian

financial crisis and excess oil supplies, which led to the international oil price collapse. This undoubtedly

affected OPEC MCs by hitting their oil revenues, and causing their GDP growth rates to decelerate. All

MCs still rely heavily on oil income as a source of foreign exchange and the mainstay of their budget

revenues. Therefore, the 1998 oil price fall seriously affected both the MCs’ budget structures, and the

financing of development projects in general.

18

OPEC Production

OPEC crude oil production in 1998, as reported by a number of selected secondary sources, averaged

27.73m b/d, which was 500,000 b/d higher than the 1996 average of 27.23m b/d. The increase was

attributed to a sharp rise of 923,000 b/d in Iraqi production, partly offset by various levels of decrease

in the production of eight other Member Countries, the largest being 144,000 b/d from Nigeria. However,

Qatar and the UAE registered minor increases.

The quarterly distribution of OPEC production was 28.36m b/d, 28.07m b/d, 27.25m b/d and 27.24m

b/d. Average production in the first two quarters of 1998 was higher than in 1997 by 1.44m b/d and

1.19m b/d respectively, but in the third and fourth quarters, production was lower than in 1997 by 100,000

b/d and 510,000 b/d, respectively (Table 4).

Direct communication by Member Countries, however, indicated a 1998 average of 28.10m b/d, being

2.72m b/d higher than the 1997 average of 25.38m b/d. The rise in output was the result of increases

of 998,000 b/d in Venezuela, 797,000 b/d in Iraq, 269,000 b/d in Saudi Arabia, 208,000 b/d in Qatar

and smaller increases in other countries, with Indonesia showing a minor decrease of 13,000 b/d

(Table 5). OPEC NGL production in 1998 averaged 2.91m b/d, which was 100,000 b/d higher than in

1997.

Non-OPEC Supply

Non-OPEC supply in 1998 averaged 44.34m b/d, which was 140,000 b/d lower than the 1997 average

of 44.48m b/d (Table 6). The fall of 140,000 b/d was largely the net effect of a 370,000 b/d decrease

in OECD production, mainly attributable to the USA and Norway, and an increase of 280,000 b/d in

the production of Developing Countries, mainly from Brazil.

il MarketDevelopments

19

Table 4

OPEC Crude Oil Production According to Secondary Sources 1,000 b/d

Average Average Change

1Q97 2Q97 3Q97 4Q97 1997 1Q98 2Q98 3Q98 4Q98 1998 98/97Algeria 847 847 851 858 851 868 830 796 796 822 -29

Indonesia 1,403 1,401 1,387 1,369 1,390 1,357 1,333 1,340 1,340 1,342 -48

IR Iran 3,662 3,637 3,617 3,679 3,649 3,615 3,690 3,504 3,538 3,586 -62

Iraq 1,142 1,080 1,266 1,270 1,190 1,583 2,046 2,409 2,402 2,113 923

Kuwait 2,088 2,065 2,082 2,119 2,088 2,204 2,097 2,018 1,987 2,076 -13

SP Libyan AJ 1,417 1,435 1,439 1,434 1,431 1,454 1,395 1,353 1,358 1,390 -42

Nigeria 2,179 2,218 2,255 2,272 2,231 2,238 2,159 2,015 1,941 2,087 -144

Qatar 553 590 646 671 616 698 674 638 637 661 46

Saudi Arabia 8,232 8,201 8,303 8,478 8,304 8,582 8,370 8,015 8,041 8,250 -54

UAE 2,261 2,223 2,257 2,258 2,250 2,395 2,283 2,195 2,176 2,261 12

Venezuela 3,132 3,183 3,254 3,339 3,228 3,367 3,190 2,971 3,026 3,137 -91

Total OPEC26,916 26,879 27,358 27,748 27,228 28,360 28,066 27,254 27,241 27,726 498

NoteTotals may not add up due to independent rounding.

SourceSecretariat’s assessment of selected secondary sources.

Following a turnaround in 1997, ie an average annual increase after average decreases for several years,

production in the former Soviet Union (FSU) stabilized in 1998, registering no change in comparison to

1997. FSU net oil exports continued their upward trend to reach 3.04m b/d in 1998, about 170,000

b/d higher than in 1997 (Table 7). Processing gains and production in China were also stable.

World Oil Demand

Total world oil demand during 1998 registered a weak growth of 290,000 b/d, or 0.4 per cent over

1997, a sharp drop in the rate of growth from the previous years and a level not seen since the beginning

20

of the 90s. In OECD countries, oil demand rose by 230,000 b/d, or 0.5 per cent, led by the growth

in North America and Western Europe of 450,000 b/d and 310,000 b/d, respectively. However, the growth

in consumption in North America and Western Europe was capped by the dramatic contraction of 540,000

b/d in demand from OECD Pacific countries, mainly Japan and South Korea. Developing Countries’ (DCs)

oil demand increased by only 340,000 b/d, or 1.9 per cent, as a result of the economic difficulties in

the leading oil consuming countries in Asia and Latin America. In the former centrally-planned economies

(CPEs), demand shrank by 270,000 b/d, or 3.1 per cent, due to the considerable contraction in apparent

demand from the FSU and China.

Table 5

OPEC Crude Oil Production as Communicated by Member Countries 1,000 b/d

Average Average Change

1Q97 2Q97 3Q97 4Q97 1997 1Q98 2Q98 3Q98 4Q98 1998 98/97

Algeria 795 800 799 799 798 907 822 791 791 827 29

Indonesia 1,327 1,327 1,327 1,341 1,330 1,388 1,316 1,282 1,277 1,315 -15

IR Iran 3,595 3,593 3,594 3,631 3,603 3,835 3,778 3,620 3,623 3,713 110

Iraq 1,380 1,298 1,393 1,464 1,384 1,445 2,218 2,528 2,518 2,181 797

Kuwait 2,008 2,005 2,009 2,006 2,007 2,191 2,064 1,978 1,975 2,051 44

SP Libyan AJ 1,393 1,395 1,394 1,401 1,396 1,506 .. .. .. 1,506 110

Nigeria 1,865 1,867 1,862 1,913 1,877 1,980 2,234 1,862 1,946 1,959 83

Qatar 404 402 396 418 405 530 671 619 631 613 208

Saudi Arabia 8,007 8,006 8,015 8,018 8,012 8,675 8,415 8,025 8,016 8,280 269

UAE 2,208 2,147 2,136 2,152 2,161 2,377 2,271 2,171 2,161 2,244 83

Venezuela 2,404 2,409 2,412 2,421 2,411 3,409 na na na 3,409 998

Total OPEC 25,385 25,250 25,337 25,564 25,384 28,243 na na na 28,100 2,716

na not available

Note

Totals may not add up due to independent rounding.

Oil Market Developments

21

Table 6

Estimated Non-OPEC Supply and NGL m b/d

Change Change Change

1995 1996 96/95 1997 97/96 1Q98 2Q98 3Q98 4Q98 1998 98/97USA 8.62 8.61 -0.02 8.61 0.00 8.64 8.53 8.15 8.14 8.36 -0.25Canada 2.39 2.46 0.07 2.58 0.12 2.68 2.56 2.57 2.61 2.61 0.03Mexico 3.07 3.28 0.22 3.42 0.13 3.54 3.55 3.48 3.45 3.51 0.09North America 14.08 14.35 0.27 14.61 0.26 14.87 14.63 14.21 14.21 14.48 -0.13Norway 2.88 3.24 0.36 3.33 0.09 3.35 3.16 2.88 3.11 3.12 -0.21UK 2.79 2.76 -0.03 2.74 -0.02 2.86 2.70 2.62 2.93 2.77 0.03Denmark 0.19 0.21 0.02 0.23 0.02 0.24 0.23 0.23 0.25 0.24 0.01Other Western Europe 0.50 0.50 -0.01 0.49 0.00 0.48 0.47 0.46 0.49 0.48 -0.02Western Europe 6.37 6.71 0.35 6.80 0.09 6.93 6.56 6.18 6.78 6.61 -0.19Australia 0.57 0.60 0.03 0.64 0.04 0.63 0.67 0.68 0.45 0.61 -0.03Other Pacific 0.10 0.09 -0.01 0.09 0.00 0.07 0.08 0.08 0.08 0.08 -0.02OECD Pacific 0.67 0.69 0.02 0.73 0.04 0.70 0.75 0.76 0.53 0.68 -0.05Total OECD* 21.12 21.75 0.63 22.14 0.39 22.50 21.94 21.14 21.51 21.77 -0.37Brunei 0.17 0.16 -0.01 0.16 0.00 0.16 0.14 0.15 0.17 0.15 -0.01India 0.73 0.70 -0.03 0.73 0.03 0.74 0.73 0.72 0.74 0.73 0.00Malaysia 0.74 0.73 -0.01 0.74 0.01 0.74 0.75 0.75 0.75 0.75 0.00Papua New Guinea 0.10 0.11 0.01 0.08 -0.03 0.06 0.09 0.09 0.09 0.08 0.00Vietnam 0.17 0.18 0.00 0.19 0.02 0.19 0.19 0.19 0.19 0.19 0.00Asia others 0.13 0.14 0.00 0.15 0.02 0.15 0.14 0.15 0.15 0.15 -0.01Other Asia 2.04 2.01 -0.03 2.05 0.04 2.04 2.03 2.04 2.07 2.05 0.00Argentina 0.75 0.82 0.06 0.87 0.05 0.87 0.89 0.89 0.88 0.88 0.01Brazil 0.94 1.05 0.12 1.09 0.03 1.20 1.23 1.24 1.39 1.26 0.18Colombia 0.59 0.63 0.04 0.66 0.03 0.73 0.72 0.76 0.84 0.76 0.10Ecuador 0.39 0.39 0.00 0.39 0.00 0.39 0.39 0.37 0.39 0.38 -0.01Peru 0.13 0.12 0.00 0.12 0.00 0.12 0.12 0.12 0.12 0.12 0.00Trinidad & Tobago 0.14 0.14 0.00 0.14 -0.01 0.13 0.13 0.13 0.14 0.14 0.00Latin America others 0.11 0.11 0.00 0.11 0.00 0.12 0.12 0.12 0.12 0.12 0.01Latin America 3.04 3.27 0.22 3.37 0.11 3.56 3.60 3.64 3.87 3.67 0.29Bahrain 0.16 0.19 0.03 0.19 0.01 0.19 0.20 0.20 0.20 0.20 0.00Oman 0.86 0.89 0.03 0.91 0.02 0.92 0.91 0.88 0.89 0.90 0.00Syria 0.63 0.62 -0.02 0.58 -0.04 0.56 0.57 0.57 0.56 0.56 -0.02Yemen 0.35 0.36 0.02 0.39 0.02 0.39 0.39 0.39 0.40 0.39 0.00Middle East 2.00 2.06 0.06 2.07 0.01 2.07 2.06 2.04 2.05 2.06 -0.02Angola 0.61 0.69 0.08 0.71 0.03 0.73 0.71 0.73 0.77 0.74 0.02Cameroon 0.10 0.09 -0.01 0.10 0.01 0.10 0.10 0.10 0.10 0.10 0.00Congo 0.18 0.21 0.03 0.27 0.05 0.27 0.27 0.27 0.27 0.27 0.00Egypt 0.95 0.93 -0.03 0.92 -0.01 0.90 0.89 0.88 0.88 0.89 -0.03Gabon 0.36 0.38 0.02 0.38 0.00 0.38 0.38 0.37 0.37 0.38 -0.01South Africa 0.15 0.18 0.03 0.19 0.01 0.20 0.20 0.20 0.20 0.20 0.01Africa other 0.15 0.16 0.01 0.18 0.01 0.18 0.19 0.18 0.19 0.19 0.01Africa 2.49 2.64 0.14 2.74 0.11 2.76 2.73 2.73 2.77 2.75 0.00Total DCs 9.58 9.98 0.40 10.24 0.26 10.43 10.43 10.45 10.76 10.52 0.28FSU 6.96 6.92 -0.04 7.10 0.18 7.18 7.09 6.99 7.12 7.09 0.00Other Europe 0.22 0.21 -0.01 0.20 -0.01 0.20 0.19 0.19 0.19 0.19 -0.01China 3.00 3.17 0.18 3.25 0.08 3.23 3.22 3.21 3.18 3.21 -0.04Non-OPEC production 40.87 42.03 1.16 42.93 0.90 43.55 42.87 41.99 42.76 42.79 -0.14Processing gains 1.43 1.49 0.05 1.55 0.07 1.55 1.55 1.55 1.55 1.55 0.00Non-OPEC supply 42.31 43.51 1.21 44.48 0.97 45.10 44.42 43.54 44.31 44.34 -0.14OPEC NGLs 2.53 2.66 0.13 2.81 0.15 2.91 2.91 2.91 2.91 2.91 0.10

* Former East Germany is included in the OECD.

Note: Totals may not add up due to independent rounding.

22

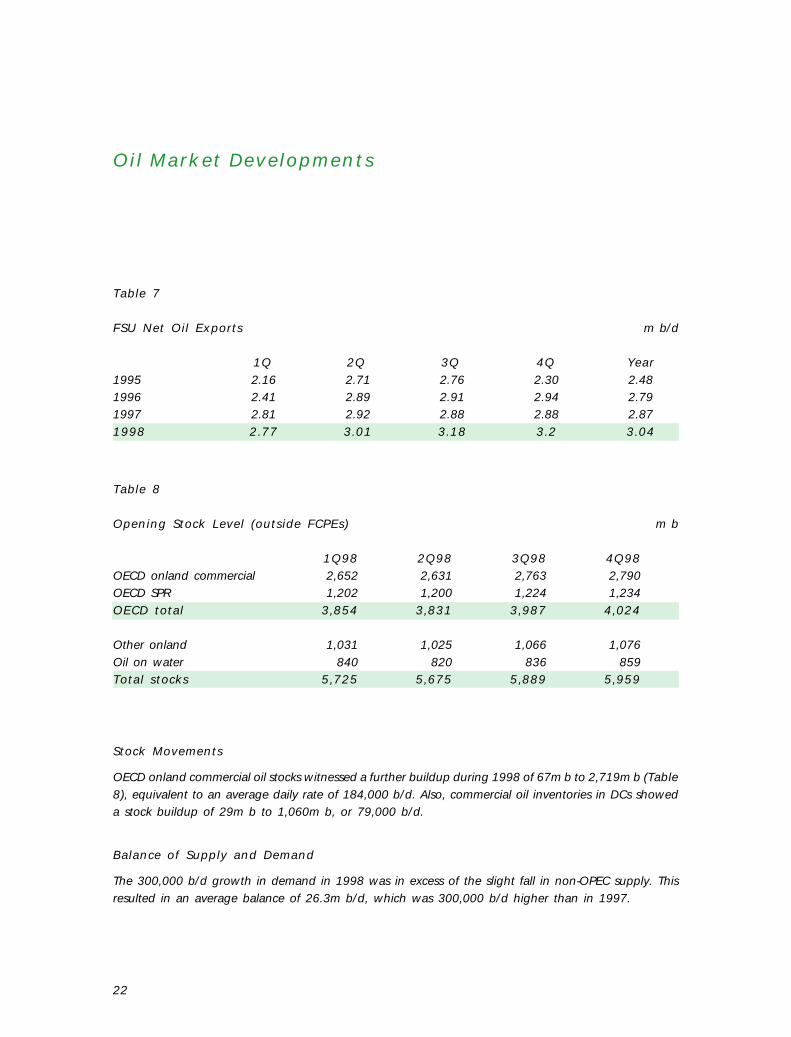

Table 7

FSU Net Oil Exports m b/d

1Q 2Q 3Q 4Q Year1995 2.16 2.71 2.76 2.30 2.48

1996 2.41 2.89 2.91 2.94 2.79

1997 2.81 2.92 2.88 2.88 2.87

1998 2.77 3.01 3.18 3.2 3.04

Table 8

Opening Stock Level (outside FCPEs) m b

1Q98 2Q98 3Q98 4Q98OECD onland commercial 2,652 2,631 2,763 2,790

OECD SPR 1,202 1,200 1,224 1,234

OECD total 3,854 3,831 3,987 4,024

Other onland 1,031 1,025 1,066 1,076

Oil on water 840 820 836 859

Total stocks 5,725 5,675 5,889 5,959

Stock Movements

OECD onland commercial oil stocks witnessed a further buildup during 1998 of 67m b to 2,719m b (Table

8), equivalent to an average daily rate of 184,000 b/d. Also, commercial oil inventories in DCs showed

a stock buildup of 29m b to 1,060m b, or 79,000 b/d.

Balance of Supply and Demand

The 300,000 b/d growth in demand in 1998 was in excess of the slight fall in non-OPEC supply. This

resulted in an average balance of 26.3m b/d, which was 300,000 b/d higher than in 1997.

Oil Market Developments

23

Table 9

World Supply/Demand Balance m b/d

1995 1996 1997 1Q98 2Q98 3Q98 4Q98 1998World demandOECD 44.9 46.0 46.7 47.3 45.5 46.7 48.1 46.9North America 21.6 22.3 22.7 22.7 23.0 23.5 23.5 23.2Western Europe 14.6 14.9 15.0 15.4 14.8 15.2 15.9 15.3Pacific 8.7 8.8 9.0 9.2 7.8 7.9 8.8 8.4DCs 16.3 17.0 17.6 17.8 17.9 17.9 18.3 18.0FSU 4.5 4.1 4.2 4.4 4.1 3.8 3.9 4.1Other Europe 0.7 0.7 0.7 0.8 0.8 0.8 0.8 0.8China 3.2 3.5 4.0 4.0 3.9 3.8 3.7 3.8(a) Total world demand 69.6 71.3 73.2 74.2 72.1 72.9 74.8 73.5Non-OPEC supplyOECD 21.1 21.8 22.1 22.5 21.9 21.1 21.5 21.8North America 14.1 14.4 14.6 14.9 14.6 14.2 14.2 14.5Western Europe 6.4 6.7 6.8 6.9 6.6 6.2 6.8 6.6Pacific 0.7 0.7 0.7 0.7 0.7 0.8 0.5 0.7DCs 9.6 10.0 10.2 10.4 10.4 10.4 10.8 10.5FSU 7.0 6.9 7.1 7.2 7.1 7.0 7.1 7.1Other Europe 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2China 3.0 3.2 3.3 3.2 3.2 3.2 3.2 3.2Processing gains 1.4 1.5 1.6 1.6 1.6 1.6 1.6 1.6Total non-OPEC supply 42.3 43.5 44.5 45.1 44.4 43.5 44.3 44.3OPEC NGLs 2.5 2.7 2.8 2.9 2.9 2.9 2.9 2.9(b) Total non-OPEC supplyand OPEC NGLs 44.8 46.2 47.3 48.0 47.3 46.4 47.2 47.2OPEC crude oil production(secondary sources) 25.0 25.7 27.2 28.4 28.1 27.3 27.2 27.7Total supply 69.8 71.9 74.5 76.4 75.4 73.7 74.5 75.0Balance (stock changeand miscellaneous) 0.2 0.6 1.3 2.1 3.3 0.8 -0.3 1.4Opening stock level (outside FCPEs) m bOECD onland commercial 2,663 2,554 2,548 2,652 2,631 2,763 2,790OECD SPR 1,168 1,176 1,194 1,202 1,200 1,224 1,234OECD total 3,831 3,730 3,742 3,854 3,831 3,987 4,024Other onland 1,025 998 1,001 1,031 1,025 1,066 1,076Oil on water 749 792 811 840 820 836 859Total stock 5,605 5,520 5,554 5,725 5,675 5,889 5,959Days of forward consumption in OECDCommercial onland stocks 58 54 54 56 58 59 58SPR 25 25 25 25 26 26 26Total 83 79 80 82 84 85 84Memo itemsFSU net exports 2.5 2.8 2.9 2.8 3.0 3.2 3.2 3.0[(a) – (b)] 24.7 25.1 25.9 26.2 24.8 26.5 27.6 26.3

NoteTotals may not add up due to independent rounding.

24

Table 10

Summarized Supply/Demand Balance m b/d

Growth1996 1997 1Q98 2Q98 3Q98 4Q98 1998 1998/97

World oil demand 71.3 73.2 74.2 72.1 72.9 74.8 73.5 0.3

Non-OPEC supply1 46.2 47.3 48.0 47.3 46.4 47.2 47.2 0.0

Balance 25.1 25.9 26.2 24.8 26.5 27.6 26.3 0.3

OPEC crude oil production2 25.7 27.2 28.4 28.1 27.3 27.2 27.7 0.5

Stock change & misc 0.6 1.3 2.1 3.3 0.8 -0.3 1.4 0.2

1. Including OPEC NGLs.

2. Selected secondary sources.

OPEC crude oil production, according to secondary sources, averaged 27.7m b/d in 1998, being 500,000

b/d higher than the previous year. Thus, as illustrated in Tables 9 and 10, the item 'stock change and

miscellaneous' reached a level of 1.4m b/d, which was 100,000 b/d higher than that of 1997, representing

a slight increase in stock build-up.

Oil Price Movements

The average annual price of the OPEC Reference Basket registered $12.28/b in 1998, its lowest value

since its introduction in 1987. The average monthly price of the Basket went through a continuous decline

in the first quarter to reach $12.41/b in March, its lowest value since 1988 (Table 11 and Figure 1).

The factors that led to this decline were oversupply of physical barrels and lower demand due to the

economic situation in South-East Asia and the mild weather in the northern hemisphere. Fears of the

introduction of increased Iraqi export volumes at a time when there was no sign of production cuts from

OPEC Member Countries put extra pressure on prices. During this quarter there was heavy stock building

in the Atlantic Basin. Refiners utilized the contango in the market to build crude oil stocks, and US refiners

in particular took advantage of the low crude prices and good refiners’ margins to increase their runs

and build product stocks.

Oil Market Developments

25

Table 11

Average Monthly Spot Prices for Selected Crudes, 1998 $/b

Crude (API) Sul wt% Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec Av98

OPEC Reference Basket 14.42 13.45 12.41 12.76 13.14 11.67 12.06 11.89 12.91 12.41 11.19 9.69 12.28

Arab Light (34.2) 1.70 13.61 12.80 11.67 12.18 12.73 11.88 11.87 12.48 13.17 12.72 11.92 9.90 12.20

Dubai (32.5) 1.43 13.41 12.41 11.53 12.23 12.75 11.80 12.11 12.25 13.08 12.69 11.96 10.11 12.15

Bonny Light (36.7) 0.10 15.25 14.11 13.14 13.51 14.46 11.89 12.01 12.14 13.59 12.66 11.15 9.96 12.77

Saharan Blend (44.1) 0.10 15.56 14.48 13.49 13.82 14.55 12.06 12.47 12.41 13.73 12.83 11.25 10.23 13.02

Minas (33.9) 0.10 14.64 13.60 12.40 13.13 12.54 11.87 12.74 12.00 11.69 12.59 11.54 9.89 12.31

Tia Juana Light (32.4) 1.20 13.95 13.05 11.95 11.93 12.08 10.81 11.32 10.56 12.07 11.33 10.03 8.74 11.44

Isthmus (32.8) 1.50 14.53 13.68 12.66 12.51 12.84 11.37 11.89 11.42 13.03 12.06 10.49 9.01 12.08

Other crudes

Arab Heavy (28.0) 3.00 12.11 11.10 9.77 10.53 11.33 10.48 10.47 11.36 12.17 11.82 11.07 9.15 10.90

Murban (39.4) 0.80 14.12 12.90 11.96 12.70 13.54 12.48 12.73 12.85 13.58 13.04 12.26 10.41 12.67

Iran Light (33.9) 1.40 13.40 12.34 11.31 11.98 12.53 11.68 11.67 12.28 12.97 12.52 11.72 9.80 11.97

Iran Heavy (31.0) 1.60 12.90 11.79 10.71 11.23 11.78 10.97 11.17 11.66 12.63 12.22 11.37 9.51 11.45

Kuwait Export (31.4) 2.60 12.80 11.69 10.61 10.99 11.55 10.73 10.97 11.33 12.39 12.01 11.24 9.31 11.26

Mandji (28.8) 1.30 12.83 11.38 10.56 10.95 11.86 9.62 10.01 10.07 11.72 11.02 9.73 8.60 10.65

Zueitina (42.3) 0.20 15.26 14.11 13.10 13.42 14.35 11.90 12.06 12.02 13.38 12.52 11.05 9.93 12.70

Es Sider (37.0) 0.50 15.45 14.29 13.34 13.64 14.59 12.20 12.25 12.05 13.54 12.71 11.26 10.13 12.90

Forcados (29.5) 0.21 15.15 14.04 12.95 13.29 14.24 11.58 11.75 11.99 13.41 12.65 11.14 9.91 12.62

Dukhan (41.4) 1.10 14.02 13.09 12.14 12.85 13.22 12.49 12.49 12.54 13.04 12.77 12.13 10.38 12.55

Oman (32.9) 0.79 13.59 12.66 11.78 12.43 12.71 11.96 12.01 12.11 12.65 12.15 11.46 9.78 12.06

Tapis (44.3) 0.20 15.81 15.12 13.43 15.09 14.52 13.69 13.82 13.16 13.62 14.37 12.97 10.97 13.81

Urals (36.1) 2.50 14.31 13.11 12.17 12.40 13.00 10.17 11.26 11.56 12.78 11.41 10.46 9.42 11.78

Suez Mix (33.0) 1.40 13.03 11.65 10.62 10.88 11.75 9.33 9.69 9.78 11.20 10.46 9.03 8.21 10.42

Brent (38.0) 0.26 15.10 14.04 13.11 13.43 14.41 12.16 12.05 11.98 13.33 12.58 11.08 9.90 12.71

Oriente (29.2) 0.90 13.16 12.49 10.94 11.24 11.11 10.65 11.35 10.84 12.33 11.87 10.33 8.30 11.17

WTI (40.0) 0.40 16.63 16.15 15.17 15.29 14.91 13.74 14.05 13.44 14.85 14.36 13.10 11.26 14.36

North Slope (27.0) 1.06 14.78 13.49 12.33 12.39 12.30 11.70 12.89 12.53 14.00 13.31 11.61 9.36 12.50

Differentials

Min.RBP* – Basket 6.58 7.55 8.59 8.24 7.86 9.33 8.94 9.11 8.09 8.59 9.81 11.31 8.72

Bonny Light – Arab Heavy 3.14 3.01 3.37 2.99 3.13 1.41 1.55 0.78 1.42 0.84 0.09 0.81 1.87

Bonny Light – Saharan Blend -0.31 -0.36 -0.35 -0.31 -0.09 -0.17 -0.46 -0.27 -0.14 -0.16 -0.10 -0.27 -0.25

Brent – WTI -1.53 -2.11 -2.06 -1.86 -0.50 -1.58 -2.00 -1.46 -1.52 -1.79 -2.03 -1.36 -1.65

Brent – Dubai 1.69 1.63 1.58 1.20 1.66 0.36 -0.06 -0.28 0.25 -0.11 -0.89 -0.21 0.56

* The Minimum Reference Basket price is $21/b starting from August 1990 as set during the 87th Meeting of the OPEC Conference, held on

26–27 July 1990. Tia Juana Light spot price = (TJL netback/Isthmus netback) x Isthmus spot price, whereas the netback values for the calculations

are taken from RVM.

Source: OPEC Data Bank.

26

In April, the price of the OPEC Basket recovered on the back of OPEC’s Extraordinary Meeting of the

Conference in late March which announced a production cut of 1.245m b/d by Member Countries. The

recovery continued into May when the monthly Basket price registered $13.14/b as there was news of

further production cuts by OPEC at a time when US refiners were increasing their demand for crude

in order to cover their gasoline requirements. However, WTI prices moved lower at the month’s end

as storage in Cushing, Oklahoma (the delivery point of NYMEX WTI futures) was full, forcing many partici-

pants to sell their positions. The price of the Basket reversed its direction and reached a ten-year low of

$11.67/b in June as the market considered the actual production cuts by OPEC and non-OPEC during

April and May as insufficient to clear the stock overhang. The oversupply situation at a time when storage

facilities were full took prices during the month to 12-year lows. The OPEC Conference decision at the

end of June, to cut an additional 1.355m b/d, changed the price direction and it moved upwards. Total

production cuts agreed upon reached 2.6m b/d for OPEC Members and 500,000 b/d for non-OPEC

producers.

Prices improved in July as OPEC Member Countries showed their commitment to the agreement

through a series of announcements of deep cuts to their August exports. There was extra support

from higher utility demand in Asia, concerns about unrest in Nigeria, good refiners’ margins in the

Mediterranean and an expected decrease in North Sea supply due to field maintenance. The

improvement in prices was reversed in the first half of August due to several factors: a high build

in OECD stocks, especially products, led to fears of refinery run cuts at a time when North Sea

maintenance was approaching its end, and the market understood then that certain OPEC Countries

were not ready to cut production at a time when the production levels agreed upon in June were

perceived by the market as not enough to clear the stock overhang. A rally started in the second

half of August and continued throughout September on the back of higher cuts in export volumes

from certain OPEC Members and as surveys showed that compliance with the June agreement reached

90 per cent. This coincided with continuous draws on US crude stocks and bad weather conditions

in the USA, which led to production disruptions in the Gulf of Mexico and the closure of refinery

and import unloading facilities in the USA.

In October, despite a reported 98 per cent compliance with the OPEC agreement and expectations of

further cuts, heavy pressure on prices was exerted by fears of a possible recession in the economies of

many countries, which coincided with the increase in North Sea production and the return of production

from the Gulf of Mexico. The pressure increased in November, and the monthly Basket price dropped

by $1.22/b, as there was a build up in crude stocks in the USA and heavy flows of imported crude.

Mild weather and high stocks coincided with ample availability of North Sea supplies, thereby de-

pressing European markets. In December, the monthly Basket price fell to $9.69/b as high product stocks

Oil Market Developments

27

Figure 1

Weekly Movement of Crude Prices 1998

28

undermined product prices and refiners‘ margins in the USA, thereby curtailing demand and lowering

crude prices. The only help for prices came from a cold snap that led to freezing temperatures in the

US North-East.

The WTI/Brent differentials were normal for most of the year, except in May when this differential was

negative. This was caused by the purchase of most of the cargoes by one trading house, which led to

an inflated Brent price at a time when WTI prices were depressed in the futures market due to full storage

at Cushing, Oklahoma, the delivery point of the NYMEX WTI futures contract.

Brent/Dubai differentials started narrowing and reached a negative 25¢/b by mid-June and stayed in negative

territory for most of July and August, as European prices were under heavy pressure from high stocks,

while Asian prices were supported by OPEC cuts which affected those markets more. In September, the

differentials regained their positive values due to a strong Brent market, as cargoes were amassed to meet

US refiners’ demand. However, in October the differential was negative again as disruptions in Asian supplies

and demand from India and China, in addition to strong fuel oil prices, supported Dubai while Brent

prices fell continuously under the influence of the supply glut.

The Refining Industry

The domestic refining configuration and capacity of OPEC Member Countries has not undergone any major

changes since 1997. Crude distillation capacity for the year 1998 was 8.36m b/d, an increase of 290,000

b/d, or 3.6 per cent compared to the 8.07m b/d of the previous year. All the increase in capacity took

place in the Middle East (Table 12).

Distillation capacity grew by 240,000 b/d in IR Iran and Saudi Arabia’s capacity rose by 90,000 b/d. However,

Kuwait registered a decline of 40,000 b/d during the year. The vacuum distillation capacity in OPEC Member

Countries registered a growth of 60,000 b/d, from 2.39m b/d in the previous year, to 2.46m b/d in 1998,

mainly due to the increases of 20,000 b/d, 30,000 b/d and 20,000 b/d in IR Iran, Kuwait and the United

Arab Emirates, respectively.

Total conversion capacity decreased slightly by 20,000 b/d from 1.62m b/d in 1997 to 1.60m

b/d in 1998. The decline was due to the falls in catalytic hydro-cracking capacity in Kuwait and

the United Arab Emirates, partially offset by a rise in catalytic cracking and hydro-cracking capacity

in IR Iran.

The conversion/distillation ratio in OPEC Member Countries of 19.1 per cent for the year 1998

Oil Market Developments

29

Table 12

OPEC Domestic Refinery Configuration, 1998 1,000 b/d

Crude Vaccum Thermal Catalytic Catalytic Catalytic Catalytic Total Conv/CrudeDistillation Operation Cracking Reforming Hydro- Hydro- Con- Distillation

Region treating cracking version per cent

Latin America

Venezuela 1,183.2 548.3 82.0 233.9 53.9 233.9 – 315.9 26.7

Total 1,183.2 548.3 82.0 233.9 53.9 233.9 – 315.9 26.7

Africa

Algeria 462.2 11.0 – – 88.0 82.0 – – –

SP Libyan AJ 342.0 7.5 – – 14.4 37.7 – – –

Nigeria 424.0 124.5 – 82.7 70.1 109.2 – 82.7 19.5

Total 1,228.2 143.0 – 82.7 172.5 228.9 – 82.7 6.7

Middle East

IR Iran 1,447.8 541.5 141.1 32.6 138.8 164.4 138.8 312.5 21.6

Iraq 603.0 82.7 – – 43.5 113.0 38.0 38.0 6.3

Kuwait 829.6 357.0 60.0 38.0 48.0 491.2 161.0 259.0 31.2

Qatar 63.0 – – – 11.5 39.4 – – –

Saudi Arabia 1,780.0 447.5 78.1 103.6 193.4 553.1 87.8 269.5 15.1

UAE 291.0 61.9 – – 29.9 115.4 26.7 26.7 9.2

Total 5,014.4 1,490.6 279.2 174.2 465.1 1,476.4 452.4 905.8 18.1

Far East

Indonesia 929.7 266.0 91.4 101.5 93.0 23.4 99.7 292.6 31.5

Total 929.7 266.0 91.4 101.5 93.0 23.4 99.7 292.6 31.5

Total OPEC 8,355.5 2,447.9 452.7 592.2 784.5 1,962.7 552.1 1,597.0 19.1

30

shows a decline compared to the 20.1 per cent ratio in 1997. This decline is the result of a drop

in total conversion capacity on the one hand and the increase in crude distillation capacity on the

other.

Foreign Refining Capacity

The foreign refining capacity of OPEC Member Countries, based on equity ownership, increased by 150,000

b/d, from 2.14m b/d in 1997 to 2.29m b/d in 1998. All of the increase came from the Asia/Far East

region, with the acquisition by Saudi Arabia of 85 per cent of the 170,000 b/d Bataan refinery in the

Philippines (Table 13).

OPEC Member Countries’ share of foreign refining capacity climbed to 5.2 per cent in 1998; a rise of

0.3 per cent compared with 1997. The increase, of course, came from the Asia/Far East region, where

OPEC’s share rose to 3.1 per cent in 1998, 1.1 per cent higher than in the previous year. OPEC’s equity

ownership in Western Europe and the USA remained almost unchanged at 5.4 per cent and 6.7 per cent,

respectively. OPEC Member Countries’ supply agreements remained unchanged from the previous year

at 2.94m b/d during 1998.

At the regional level, supply agreements to the USA top the list, with 1.41m b/d committed by Saudi

Arabia and Venezuela, followed by Western Europe with a total commitment of 870,000 b/d and the

Asia/Far East region with 650,000 b/d. Even though OPEC Member Countries’ supply agreements remained

unchanged volume-wise, they fell by 0.2 per cent during 1998 to 7.2 per cent. The drop in share is the

result of the increase in refining capacity in the three regions.

Tanker Market

The volume of international trade in oil increased by 4.6 per cent from 1,979 million tonnes in 1997

to 2,075m t in 1998, due primarily to low oil prices and the growth of 2.3 per cent in the world economy.

In spite of this, the continuing financial crisis in South-East Asian economies, impacted negatively on long-

haul freight rates along the Middle East/Far East route. The freight rate on this route declined by six points

to an average of Worldscale 63 for the year. The average rate on the long-haul routes to the West remained

at the preceding year’s level of W59. Freight rates for products declined generally on all the major routes.

Higher crude oil production for the year resulted in increases in the average monthly volume of tankers

chartered in the spot market and tankers used for storage by 5.8m t and 700,000 t to 133.9m t and

12.5m t, respectively.

Oil Market Developments

31

Table 13

OPEC Foreign Downstream Crude Refining Capacity, 1998 1,000 b/d

Based on Equity Ownership Based on Crude Supply Agreements

Asia/Far East W Europe USA Total Asia/Far East W Europe USA Total

IR Iran 17.0 – – 17.0 15.0 – – 15.0

Kuwait – 250.0 – 250.0 – 225.0 – 225.0

SP Libyan AJ – 98.6 – 98.6 – 150.0 – 150.0

Saudi Arabia 390.3 135.3 312.5 838.1 640.0 180.0 600.0 1,420.0

UAE – 109.3 – 109.3 – 109.0 – 109.0

Venezuela – 224.1 751.5 975.6 – 205.0 813.0 1,018.0

Total 407.3 817.31,064.0 2,288.6 655.0 869.0 1,413.0 2,937.0

Regional refiningcapacity/intake 13,329.9 15,065.015,993.0 44,387.9 11,503.7 13,874.9 15,193.4 40,572.0

OPEC share offoreign refiningcapacity/intake (%) 3.1 5.4 6.7 5.2 5.7 6.3 9.3 7.2

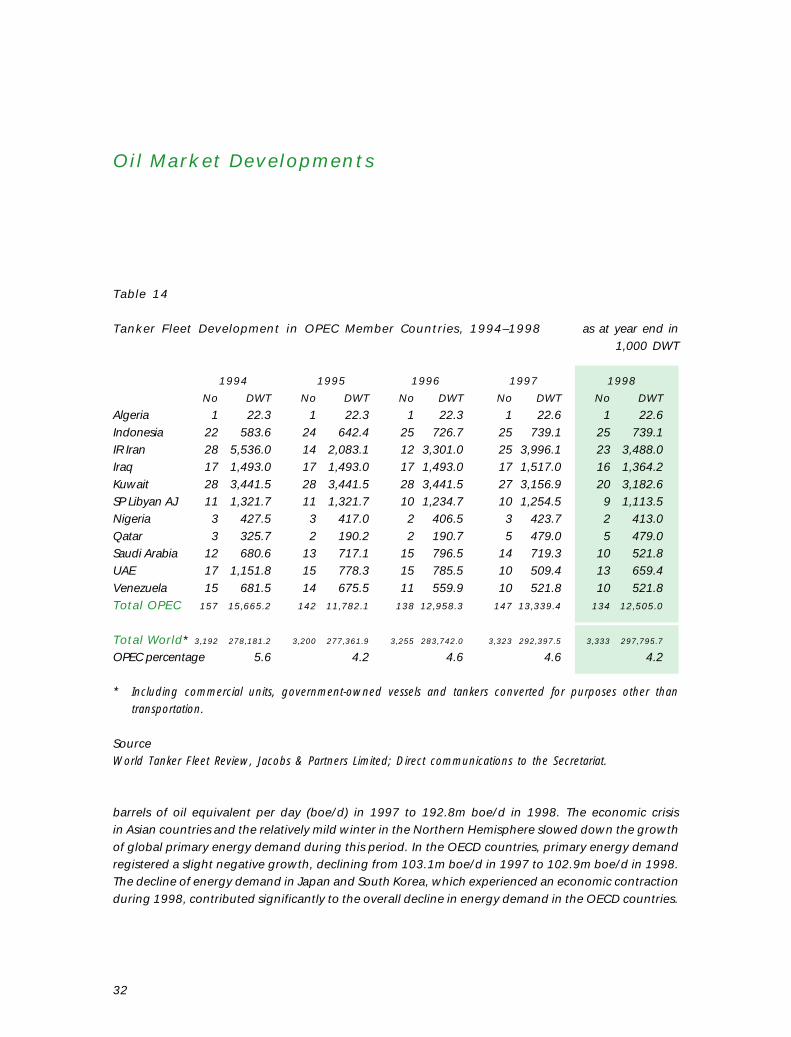

Tanker Fleet Size

The world tanker fleet increased by 5.4m dead-weight tonnes (DWT) to 297.80m DWT in 1998. On the

other hand, OPEC’s tanker fleet decreased by 834,400 DWT to 12.51m DWT as at the end of 1998

(Table 14). OPEC’s share of the total world tanker fleet thus declined to 4.2 per cent in 1998 from 4.6

per cent in 1997. IR Iran, Saudi Arabia and Iraq remained the three largest fleet owners within OPEC.

The OPEC liquid gas carrier fleet, which totalled 2.1m cubic metres as at December 31, 1998, represents

8.5 per cent of the world’s liquid gas carrier fleet. LNG carriers account for 77.2 per cent of the OPEC

liquid gas carrier fleet, while the balance of 22.8 per cent are LPG carriers.

Primary Energy Developments

In 1998, world primary energy demand registered a marginal growth of 0.3 per cent, from 192.2m

32

Table 14

Tanker Fleet Development in OPEC Member Countries, 1994–1998 as at year end in

1,000 DWT

1994 1995 1996 1997 1998

No DWT No DWT No DWT No DWT No DWT

Algeria 1 22.3 1 22.3 1 22.3 1 22.6 1 22.6

Indonesia 22 583.6 24 642.4 25 726.7 25 739.1 25 739.1

IR Iran 28 5,536.0 14 2,083.1 12 3,301.0 25 3,996.1 23 3,488.0

Iraq 17 1,493.0 17 1,493.0 17 1,493.0 17 1,517.0 16 1,364.2

Kuwait 28 3,441.5 28 3,441.5 28 3,441.5 27 3,156.9 20 3,182.6

SP Libyan AJ 11 1,321.7 11 1,321.7 10 1,234.7 10 1,254.5 9 1,113.5

Nigeria 3 427.5 3 417.0 2 406.5 3 423.7 2 413.0

Qatar 3 325.7 2 190.2 2 190.7 5 479.0 5 479.0

Saudi Arabia 12 680.6 13 717.1 15 796.5 14 719.3 10 521.8

UAE 17 1,151.8 15 778.3 15 785.5 10 509.4 13 659.4

Venezuela 15 681.5 14 675.5 11 559.9 10 521.8 10 521.8

Total OPEC 157 15,665.2 142 11,782.1 138 12,958.3 147 13,339.4 134 12,505.0

Total World* 3,192 278,181.2 3,200 277,361.9 3,255 283,742.0 3,323 292,397.5 3,333 297,795.7

OPEC percentage 5.6 4.2 4.6 4.6 4.2

* Including commercial units, government-owned vessels and tankers converted for purposes other than

transportation.

SourceWorld Tanker Fleet Review, Jacobs & Partners Limited; Direct communications to the Secretariat.

Oil Market Developments

barrels of oil equivalent per day (boe/d) in 1997 to 192.8m boe/d in 1998. The economic crisis

in Asian countries and the relatively mild winter in the Northern Hemisphere slowed down the growth

of global primary energy demand during this period. In the OECD countries, primary energy demand

registered a slight negative growth, declining from 103.1m boe/d in 1997 to 102.9m boe/d in 1998.

The decline of energy demand in Japan and South Korea, which experienced an economic contraction

during 1998, contributed significantly to the overall decline in energy demand in the OECD countries.

33

In OECD North America, despite the strong economic growth in the USA, primary energy demand

only registered a marginal growth due to the relatively mild winter of 1998 compared to that of

1997 (Table 15).

In developing countries, the economic crisis in South-East Asia counterbalanced the overall increase in

energy demand in the DCs, expanding their energy requirements moderately by 1.7 per cent, from 46.8m

boe/d in 1997 to 47.6m boe/d in 1998. In other regions, the FSU, China and Eastern European countries,

energy demand registered a marginal decline to 42.3m boe/d in 1998.

As regards primary energy demand broken down by fuel, despite the decline in gas consumption in the

USA during the relatively warm winter of 1998, the strong increase in gas demand in the European countries,

the FSU and DCs expanded global natural gas demand by a moderate 1.1 per cent, from 37.7m boe/d

in 1997 to 38.2m boe/d in 1998. World oil demand increased by a marginal 0.4 per cent, from 70.7m

boe/d in 1997 to 70.9m boe/d in 1998. World coal demand, however, declined from 44.9m boe/d in

1997 to 44.4m boe/d in 1998, due to the strong decline in coal consumption in European countries

and the FSU as a result of fuel substitution from coal to gas for power generation. The return to normal

precipitation in the USA, after experiencing high rainfall levels in 1997, cut hydro power output there

sharply. However, the strong increase in hydro power output in other countries, such as Japan, the DCs,

and European countries, drove hydro power demand up by a moderate 1.3 per cent, from 5.2m boe/d

in 1997 to 5.3m boe/d in 1998.

Electricity demand from nuclear power in 1998 also registered a moderate growth of 1.6 per cent, from

12.6m boe/d in 1997 to 12.8m boe/d in 1998. The significant additional new capacity of nuclear power

in South Korea, combined with the return to normal operation of nuclear power in the USA, after experiencing

a major maintenance schedule in 1997, contributed significantly to the increase of global nuclear power

output in 1998 (Table 16).

Environmental Matters

The Third Conference of the Parties (COP3) to the United Nations Framework Convention on Climate Change

(UNFCCC) adopted the Kyoto Protocol in December 1997. This Protocol officially opened for signature

in March 1998. By December 1998, 67 countries had signed the Protocol, while Fiji and Tuvalu were

the only countries to have actually ratified it. The Fourth Conference of the Parties (COP4) was the most

important environmental meeting in 1998 and adopted the so-called Buenos Aires Plan of Action,

whereunder the Parties declared their determination to strengthen the implementation of the Convention

and prepare for the future entry into force of the Kyoto Protocol.

34

Table 15

World Primary Energy Demand by Country Group, 1997–1998

1997 1998

m boe/d m boe/d % growth rate

OECD 103.1 102.9 –0.2

Developing countries 46.8 47.6 1.7

Other regions 42.3 42.3 –0.1

World 192.2 192.8 0.3

Oil Market Developments

COP4 was held on November 2–14, 1998, in Buenos Aires, Argentina. Delegates made their way

to South America to work out an agenda for the years 1999 and 2000, and to fill in the details

of the Kyoto Protocol left unresolved from the COP3 meeting in Kyoto. The resulting “Buenos Aires

Plan of Action” sets out a work programme aiming for completion at COP6 in late 2000. The Plan

of Action has 142 elements covering Articles 6, 12 and 17, the “Mechanisms” of the Kyoto Protocol

(formerly known as “Flexible Mechanisms”); the Clean Development Mechanism (CDM), joint imple-

mentation (JI) and emissions trading.

In addition, the Buenos Aires Plan of Action includes a work programme dealing with other major issues,

such as the financial mechanisms and the development and transfer of technologies. Voluntary commitments

for developing countries provided the main area of contention. However, this issue was removed from

the COP4 agenda, in the face of strong criticism by developing countries, and does not appear on the

work programme for COP5 and COP6.

The Buenos Aires Plan of Action includes a work plan for the implementation of Articles 4.8 and 4.9.

Negotiations failed to reach any conclusion on the second review of the adequacy of existing commitments

to deal with climate change. The OPEC delegations, while insisting on the implementation of Articles 4.8

and 4.9 of the Convention and 2.3 and 3.14 of the Protocol, stated on different occasions that there

should be progress on all issues and not just the issues of specific interest to developed countries. The

OPEC Secretariat, as in the past, organised co-ordination meetings to assist the Member Countries' delegations

in exchanging views and harmonising contributions.

35

In late October, immediately prior to COP4, the OPEC Secretariat held a preparatory meeting for

OPEC and non-OPEC producers at its Secretariat in Vienna. Guest speakers included Prof Graciela

Chichilnisky of Columbia University, Mr Frank Joshua of UNCTAD, Dr Knut Rosendahl from Norway,

Dr Leena Srivastava from the TERI Institute in New Delhi and Dr Robert Williams, a senior UNIDO

representative. Dr Martin Bartenstein, Austria's Minister of Environment, Youth and Family, whose

country held the Presidency of the European Union (EU) at the time, gave a speech on the EU’s

views on the subject. The presentations were followed by a panel discussion involving all the experts.

On the following day, the OPEC Secretariat held a one-day, closed pre-COP4 co-ordination meeting

for Member Countries.

Table 16

World Primary Energy Demand by Fuel, 1997–1998

1997 1998

m boe/d m boe/d % growth rate % share

Coal 44.9 44.4 -1.0 23.0

Oil 70.7 70.9 0.4 36.8

Gas 37.7 38.2 1.1 19.8

Hydro 5.2 5.3 1.3 2.7

Nuclear 12.6 12.8 1.6 6.6

Traditional fuels 21.1 21.3 0.8 11.0

Total 192.2 192.8 0.3 100.0

36

Press Release No 2/98, Vienna, Austria, March 30, 1998

104th (Extraordinary) Meeting of the OPEC Conference

The 104th (Extraordinary) Meeting of the Conference of the Organization of the Petroleum Exporting

Countries (OPEC) convened in Vienna, Austria, on March 30, 1998. The Meeting was presided over

by HE Obaid Bin Saif Al-Nasseri, Minister of Petroleum and Mineral Resources of the United Arab

Emirates and Alternate President of the 103rd Meeting of the Conference. The Conference welcomed

HE Dr Kuntoro Mangkusubroto, Minister of Mines & Energy of Indonesia, and HE Sheikh Saud Nasser

Al-Saud Al-Sabah, Minister of Oil of Kuwait, and paid tribute to their predecessors in office, HE Ida

Bagus Sudjana of Indonesia and HE Issa Mohammed Al-Mazidi of Kuwait. The Conference also

expressed its pleasure at the re-appointment of HE Chief (Dr) Dan Etete as Minister of Petroleum

Resources of Nigeria.

The Conference expressed its pleasure in welcoming to the Meeting representatives of important fellow

oil-producer Mexico, a presence which was viewed as a sign of the new spirit of co-operation which is

emerging amongst oil producers.

OPEC Member Countries have observed, with concern, the severe weakening of crude oil prices

throughout the winter, a deterioration brought about, in part, by lower-than-expected demand

as a result of the unseasonably mild winter in the Northern Hemisphere and the on-going economic

downturn in South-East Asia but, more particularly, by excess supplies of crude to the world oil

market.

Reflecting their serious desire to stabilize the market in the interests of all oil producers, OPEC Member

Countries have agreed to voluntarily cut the following amounts from their current production, with effect

from April 1, 1998 until the end of the year (in barrels per day).

PEC Press Releases

37

Algeria 50,000 Qatar 30,000

Indonesia 70,000 Saudi Arabia 300,000

Islamic Republic of Iran 140,000 United Arab Emirates 125,000

Kuwait 125,000 Venezuela 200,000

SP Libyan AJ 80,000

Nigeria 125,000 Total 1.245m b/d

These cuts will be based on production as given by selected secondary sources for the month of February

1998, namely (in 1,000 b/d):

Algeria 868 Nigeria 2,258

Indonesia 1,380 Qatar 700

Islamic Republic of Iran 3,623 Saudi Arabia 8,748

Kuwait 2,205 United Arab Emirates 2,382

SP Libyan AJ 1,453 Venezuela 3,370

These figures do not constitute new quotas and the cuts are intended to be only temporary until the

end of 1998.

In light of its exceptional circumstances, Iraq is not called upon to participate in this agreement.

The Conference recognizes and appreciates the production cuts pledged by some non-OPEC oil-

producing countries, in particular the Sultanate of Oman, Mexico and others, and agreed to continue

consultations with the non-OPEC oil producers so as to establish and maintain stability in the oil market

in the future. This is entirely consistent with the mandate of the Organization, one of whose principal

aims is to ensure the “stabilization” of international oil markets with a view to “eliminating harmful and

unnecessary fluctuations”.

The Conference appealed to other non-OPEC oil exporters to support these measures to stabilize the

market by moderating their output, in the interests of all concerned.

The Conference also expressed its gratitude to the Government of the Federal Republic of Austria and

to the authorities of the City of Vienna for their warm hospitality and the excellent arrangements made

for the Meeting.

As decided in Indonesia in November 1997, the next Ordinary Meeting of the Conference will be

convened in Vienna, Austria, on June 24, 1998.

Press Release No 4/98, Vienna, Austria, June 24, 1998

105th Meeting of the OPEC Conference

The 105th Meeting of the Conference of the Organization of the Petroleum Exporting Countries (OPEC)

convened in Vienna, Austria, on June 24, 1998.

The Conference unanimously elected HE Obaid Bin Saif Al-Nasseri, Minister of Petroleum and Mineral

Resources of the United Arab Emirates and Head of its Delegation, as its President. HE Chief (Dr) Dan

38

Etete, Minister of Petroleum Resources of Nigeria and Head of its Delegation, was unanimously elected

Alternate President.

The Conference expressed its pleasure at the presence of high-level representatives of Mexico, the Russian

Federation, and the Sultanate of Oman, whose support in measures being taken to stabilize the market

is welcomed by the Organization.

The Conference reviewed the Secretary General’s report, the report of the Economic Commission Board,

the report of the Ministerial Monitoring Sub-Committee (MMSC), chaired by HE Bijan Namdar Zangeneh,

Minister of Petroleum of the Islamic Republic of Iran, and various administrative matters.

Having reviewed the current market situation, the Conference agreed to make further reductions in

the production of Member Countries (excluding Iraq), bringing total reductions to 2.6 million b/d, so that

the base (using February 1998 production levels as given by OPEC selected secondary sources), total

reductions and Member Countries’ production will be as follows (in b/d):

Base Reductions ProductionAlgeria 868,000 80,000 788,000

Indonesia 1,380,000 100,000 1,280,000

Islamic Republic of Iran 3,623,000 305,000 3,318,000

Kuwait 2,205,000 225,000 1,980,000

SP Libyan AJ 1,453,000 130,000 1,323,000

Nigeria 2,258,000 225,000 2,033,000

Qatar 700,000 60,000 640,000

Saudi Arabia 8,748,000 725,000 8,023,000

United Arab Emirates 2,382,000 225,000 2,157,000

Venezuela 3,370,000 525,000 2,845,000

Total 2.6m b/d

The above agreement is effective from July 1, 1998 and valid for one year. Member Countries emphasized

their firm commitment to this agreement.

The Conference expressed its appreciation for the reductions which were pledged by non-OPEC

producing countries since March 1998, totalling in excess of 500,000 b/d, including 200,000 b/d from

Mexico, 100,000 b/d from the Russian Federation, and 50,000 b/d from Oman, among others. This will

bring the total supply withdrawn from the market to more than 3.1m b/d.

The Conference expressed its appreciation to the Government of the Federal Republic of Austria and

the authorities of the City of Vienna for their warm hospitality and the excellent arrangements made for

the Meeting.

OPEC Press Releases

39

The Conference passed Resolutions which will be published on July 24, 1998, after ratification by Member

Countries.

Press Release No 7/98, Vienna, Austria, November 26, 1998

106th Meeting of the OPEC Conference

The 106th Meeting of the Conference of the Organization of the Petroleum Exporting Countries (OPEC)

convened in Vienna, Austria, on November 25 and 26, 1998.

The Conference unanimously elected HE Dr Youcef Yousfi, Minister of Energy & Mines of Algeria and

Head of its Delegation, as its President. HE Abdullah bin Hamad Al-Attiyah, Minister of Energy & Industry

of Qatar and Head of its Delegation, was unanimously elected Alternate President.

The Conference warmly received high-level representatives from Mexico, the Russian Federation, and

the Sultanate of Oman, non-OPEC oil-exporting countries whose continued support of measures being

taken to support oil prices is welcomed by the Organization.

The Conference reviewed the Secretary General’s report, the report of the Economic Commission Board,

the report of the Ministerial Monitoring Sub-Committee (MMSC), chaired by HE Bijan Namdar Zangeneh,

Minister of Petroleum of the Islamic Republic of Iran, and various administrative matters.

The Conference appointed Mr Ali A. Fituri, Governor for the Socialist Peoples Libyan Arab Jamahiriya,

as Chairman of the Board of Governors for the year 1999, and Dr Aboki Zhawa, Governor for Nigeria,

as Alternate Chairman for the same period.

The Conference decided to realign the scheduling of its bi-annual Ordinary Meetings, which, henceforth,

will take place in the months of March and September rather than June and November.

The Conference, having reviewed the market situation, decided that, at its next Ordinary Meeting,

it will assess the market situation and take whatever actions or measures that might be deemed appropriate

should prices remain at unacceptable levels.

The Conference approved the Budget of the Organization for the year 1999.

The Conference expressed its appreciation to the Government of the Federal Republic of Austria and

the authorities of the City of Vienna for their warm hospitality and the excellent arrangements made for

the Meeting.

The Conference passed Resolutions which will be published on December 27, 1998, after ratification

by Member Countries.

The next Ordinary Meeting of the Conference will be convened in Vienna, Austria, on March 23, 1999.

40

Office of the Secretary General

Traditionally, the activities of the Office of the Secretary General (SGO) centre around meeting the

requirements of the Chief Executive in the execution of his duties, and 1998 was no exception. During

the year, considerable time and energy was concentrated on preparing documentation for and servicing

Meetings of the Conference, the Ministerial Monitoring Sub-Committee (MMSC) and the Board of Governors

(BoG). In addition to co-ordinating the preparation of reports and documentation for submission to the

various ministerial and gubernatorial gatherings, the staff of the SGO were also occupied with taking minutes

of the Meetings, preparing precis of the discussions held and summaries of the decisions taken, as well

as preparing formal, edited minutes of the deliberations for distribution to Ministers and Governors, as

apppropriate.

The SGO was also concerned with co-ordinating the Secretariat’s protocol, as well as organizing the many

missions conducted by the Secretary General and other members of the Secretariat staff during the year,

and in preparing monthly accounts of the Secretariat’s activities for distribution to Member Countries.

Research Division

With the restructuring process in the Secretariat having been finalised during the course of the year, and

the Departments gradually approaching their full staff complement, the Research Division pursued its

activities, sharing the work among its Petroleum Market Analysis Department (PMAD), EnergyStudies Department (ESD) and Data Services Department (DSD). The new structure maintains

the basic mission and responsibilities of the Division, namely to conduct a continuous programme of research

on energy and related matters; to analyse and forecast developments in the energy and petrochemical

industries; to monitor closely the oil and products markets; to follow world economic and financial issues,

with emphasis on the international hydrocarbons industry; and to maintain and expand data services in

support of those activities in the Secretariat. All these research endeavours are performed under the guidance,

ctivitiesof the Secretariat

41

supervision and co-ordination of the Director of Research, to fulfil the needs of the Member Countries

in particular, and to contribute to the international community in these fields in general.

The restructuring process has provided an opportunity to reinforce a more structured and integrated

research programme in the Division and to harmonise and optimise the workflow among the

Departments, where many of the activities are of a complementary nature. In the new structure,

the Division’s work has been allocated in such a way that the emphasis of PMAD’s assignments is

aimed at keeping Member Countries abreast of oil market developments in the short-term, while

ESD concentrates on research studies and projects of a more long-term nature, with the support

and participation of DSD in all areas as appropriate.

The philosophy of teamwork, which has always been encouraged as a policy, will continue to be a natural

reflection of the working environment. Similar to the successful Environmental Task Force and taxation

teams established in the Division, an inter-disciplinary modelling group was created, again comprising

staff from all three Departments, whose key activities will centre on modelling projects.

Last year, during this interim restructuring period, an abrupt crude oil price decline was witnessed, which

had serious implications for oil market stability and a negative impact on oil-producing countries. The pace

and duration of these developments required rigorous efforts to prevent further deterioration in oil market

conditions and reverse the trend. All three Departments were closely involved in preparing and providing

reports, studies and up-to-date data for the various Meetings of the Conference, the MMSC, the BoG and

the Economic Commission Board (ECB).

The Division devoted extensive efforts to timely assessments of international oil market trends and

developments in the world economy. Briefings on daily oil price movements, weekly and monthly oil market

reports, monthly production monitoring reports, and other regular studies were prepared for submission

to meetings of the above bodies, or distribution to Member Countries’ representatives. In addition to covering

key aspects of the market, such as the refining industry, oil companies, transportation, storage, stock

movements, oil trade, price differentials and formulae, economic and financial developments, the US dollar

and various economic indicators, detailed analysis of current issues was also provided in annual and

complementary reports. These focused on the reasons behind recent price movements, the world refinery

industry and medium term expectations for product trade, and the role of storage in the marketing of

crude oil and petroleum products.

Besides close monitoring of current oil market conditions and trends, the Division focused its research

activities on in-depth studies related to environmental policies, long-term energy projections for the oil

42

and energy markets, and demand prospects for gas and solids, in order to provide a broader range of

policy options and responses for the Member Countries. The annual study Oil and Energy Outlook to

2020, provided the world energy demand growth in the long run, using the OPEC World Energy Model

(OWEM). In its projections, the world energy-mix pattern based on its reference case assumptions is described,

and regional oil demand and production outlook discussed. In addition to required OPEC oil production

and trade volumes up to 2020 in the reference case, alternative market share development options and

their implications for OPEC revenues are also analysed.

Due to the increasing importance and dynamic character of the environmental debate taking place among

international bodies, and its important implications for OPEC, the Division’s work in this area has been

intensified in terms of research, monitoring and co-ordination activities. The Quarterly Environmental Report

provides an update on scientific facts, highlights policy issues and options in areas such as taxation, the

oil and gas industry, alternative energy sources, energy and trade, and includes analysis of the negotiating

process in relevant conferences and subsidiary bodies. Within the quantitative framework of OWEM,

the possible impacts of implementation of the Kyoto Protocol upon OPEC export revenues were analysed

and, in this context, optimum market share development for OPEC was assessed. Two special reports were

also prepared on Key Developments in the Climate Change Debate, and The United Nations Framework

Convention on Climate Change – Joint Implementation, Activities Implemented Jointly and Emissions Trading.

The Secretariat also organised a meeting on The Run-up to COP4: Major Issues for Developing Countries

while a co-ordination meeting in preparation for the Fourth Conference of the Parties to the UNFCCC

was held in October 1998.

In addition, a number of studies and reports were prepared or drafted by the various Departments, including

The impact of electrical vehicles and the use of compressed natural gas on the gasoline market; Coal

developments and future prospects; Key aspects of non-OPEC oil production; The use of energy models

in energy policy analysis and forecasting; and Oil taxation in the OECD: an energy policy perspective.

DSD continued with its major task of providing up-to-date, consistent and reliable data, matching the

needs of the Research Division and the Member Countries. Therefore, as in the past, utmost importance

was given to maintaining a satisfactory and expanding database through the systematic collection of

information and data from numerous sources, specialised publications and direct communications. The

high quality of the data is assured through careful analysis, comparison and validation utilising new software.

Besides direct input data modules for the in-house models, delivery of key and up-to-date information

to end-users is assured through regular dissemination of electronic reports, including publications such

as the Annual Statistical Bulletin, Quarterly Energy and Oil Statistics, and the Annual Report. Activities to

expand direct exchange of data through electronic means and sources, such as the Internet and electronic

media, increased. The Department also continued its activities in systems development, technical support

Activities of the Secretariat

43

to other Departments, data base administration and maintenance, user support, network support, PC and

software installations.

The various Departments of Research Division and the Public Relations & Information Department (PRID),

also worked closely together on preparing a number of speeches for the Secretary General and other

senior Secretariat officials to deliver at various international fora, as well as co-operating on other publications

such as the Monthly Oil Market Report and the Quarterly Environmental Report. Additionally, a number

of articles were assessed for possible publication in the quarterly OPEC Review by Research Division, which

also commented on and reviewed various articles on energy and environmental issues that were published

in other energy journals.

Besides providing a regular flow of information and data to Member Countries, requests for information

on various topics were handled on an ad hoc basis, and the Departments of the Research Division also

accommodated trainees from Member Countries. The Division also organised a number of lectures and

presentations from institutions in the energy field, to facilitate discussions and exchange views on pertinent

issues of common interest. Staff attended and addressed international conferences and seminars, and

participated in various roundtable discussions, expert groups and co-ordination meetings.

Public Relations & Information Department

The restructured Public Relations & Information Department (PRID) came into existence on January 1, 1998.

It incorporated the OPEC Library, which had been established by an earlier Public Relations Department

in the 1960s, before becoming part of DSD nearly two decades ago. In its new guise, PRID maintained

the Secretariat’s long tradition of providing an effective internal and external information service, taking

full advantage of recent technological advances. The Department produced publications and news stories,

drafted speeches, provided an internal daily news service, edited reports and other written matter, handled

on a daily basis, enquiries from the local and international media and the general public, produced audio-

visual material and undertook other important information and public relations assignments. This was in

addition to the Library’s activities, dealt with separately below.

PRID’s use of advanced technology enabled it to devise effective new ways of presenting the

viewpoints and activities of OPEC and its Member Countries to interested parties, notably the media, energy

analysts, researchers, students and the public. This was through the ongoing development of the OPEC

Web site on the Internet (http://www.opec.org), which was heavily used as people grew aware of

its availability and the quality of its content. Similarly, the electronic mail facility ([email protected]) became

established as a day-to-day feature of the Department’s activities, with a growing number of enquiries

44

as the year progressed. Traditional means of information exchange, by telephone, fax and regular

correspondence, were also much in evidence.

On the publications front, the monthly OPEC Bulletin, with 12 issues for the second successive year, continued

to provide high-quality coverage of the Organization’s activities for its worldwide readership. It published

speeches delivered by the OPEC Secretary General and other senior officials, as well as addresses, Resolutions

and Press Releases from Meetings of the OPEC Conference. Also published were articles by notable players

in the energy industry. In addition, there was an exclusive interview with the Chairman of the Group

of 77 plus China. The Bulletin’s regular columns included commentaries on topical issues, oil market analyses,

news stories from Member Countries and major financial centres around the world, and an Environmental

Notebook.

As part of OPEC’s contribution to intellectual discourse, the OPEC Review continued to enlighten readers