public hearing to consider advanced clean cars program · public hearing to consider advanced clean...

TRANSCRIPT

Los Angeles, CaliforniaJanuary 26th, 2012

Public Hearing to Consider Advanced Clean Cars

Program

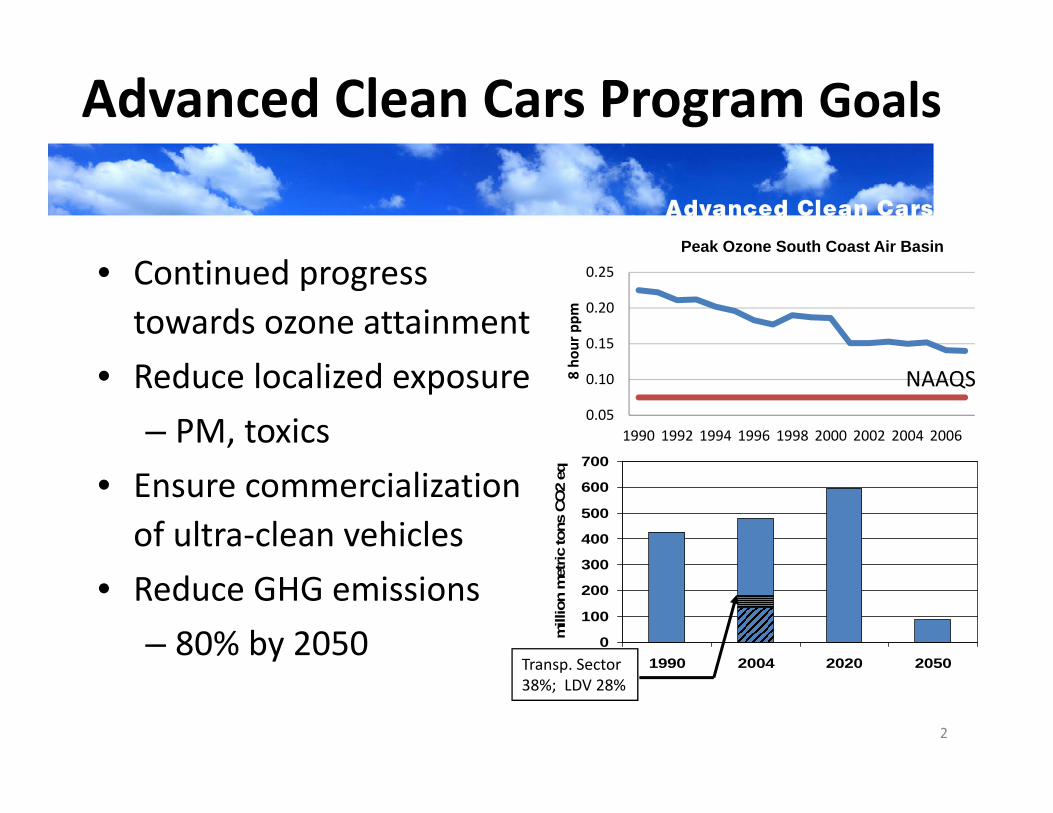

Advanced Clean Cars Program Goals

• Continued progress towards ozone attainment

• Reduce localized exposure– PM, toxics

• Ensure commercialization of ultra‐clean vehicles

• Reduce GHG emissions– 80% by 2050

2

0

100

200

300

400

500

600

700

1990 2004 2020 2050

mill

ion

met

ric to

ns C

O2

eq

Transp. Sector 38%; LDV 28%

0.05

0.10

0.15

0.20

0.25

1990 1992 1994 1996 1998 2000 2002 2004 2006

8 ho

ur ppm

Peak Ozone South Coast Air Basin

NAAQS

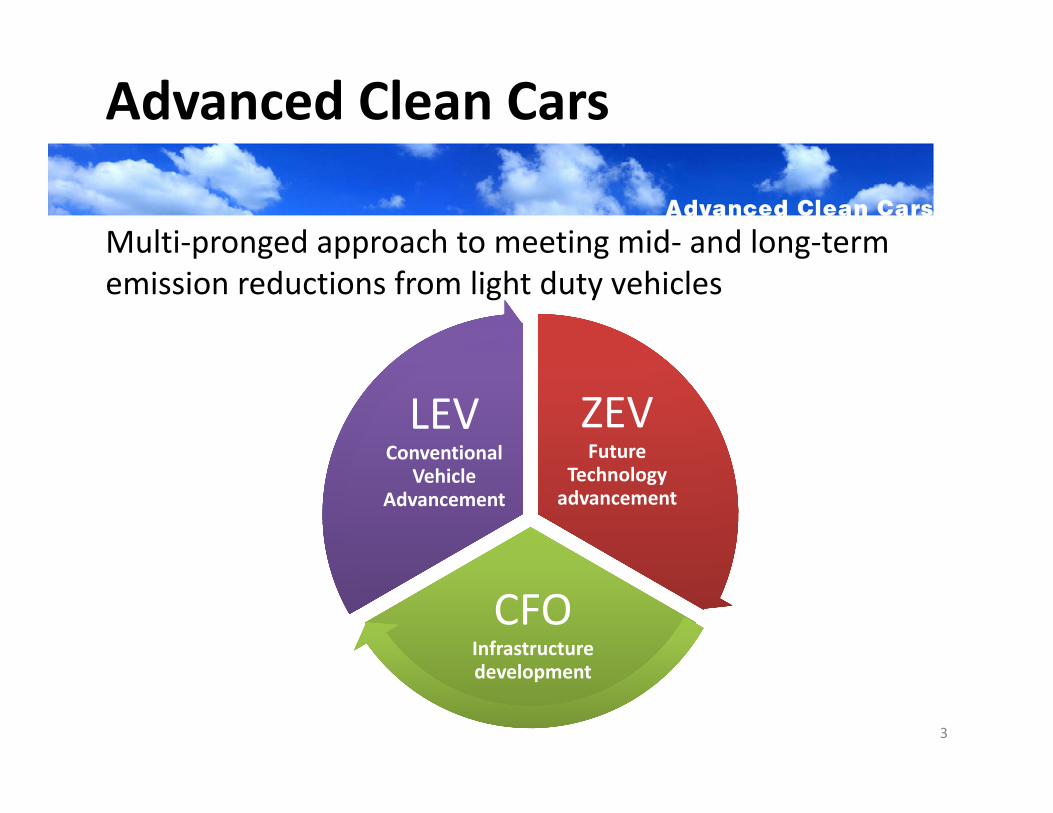

Advanced Clean Cars

Multi‐pronged approach to meeting mid‐ and long‐term emission reductions from light duty vehicles

3

ZEVFuture

Technology advancement

ZEVFuture

Technology advancement

CFOInfrastructure development

CFOInfrastructure development

LEVConventional

VehicleAdvancement

LEVConventional

VehicleAdvancement

Advanced Clean Cars Program – CEQA

• Staff prepared a programmatic integrated environmental analysis in accordance with ARB’s certified regulatory program under the California Environmental Quality Act

• Environmental analysis included in ISORs as Appendix B • Analyzed proposed regulations’ effects on the

environment– Based on regulated community compliance responses – Beneficial air quality impacts – Potential adverse impacts to aesthetics, biology, cultural, hazards,

hydrology, noise, transportation/traffic related to construction activities

• Feasible mitigation identified • Alternatives analyzed

4

Outreach

• 10 public workshops beginning in early 2010

• Multiple meetings with stakeholders

• 3 Community Meetings in July 2011– A panel of experts provided a local perspective and expert information on air pollution, climate change, and transportation

5

LEV III

ZEVZEV

CFOCFO

LEVLEV

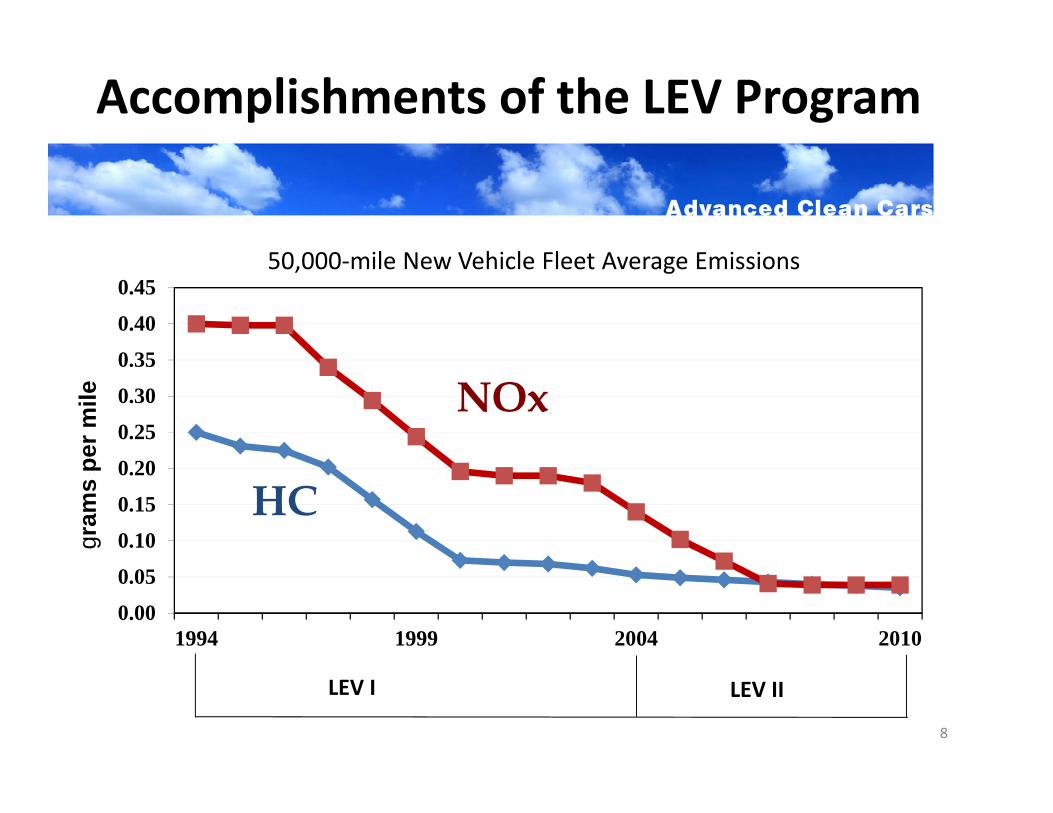

LEV III: Meeting Air Quality Standards

• LEV III regulations continue emission reductions for all new vehicles– More stringent standards – by 70% – for smog and soot

pollutants

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

1994 1999 2004 2010

50,000‐mile New Vehicle Fleet Average Emissions

Accomplishments of the LEV Program

HC

NOx

gram

s pe

r mile

LEV I LEV II

8

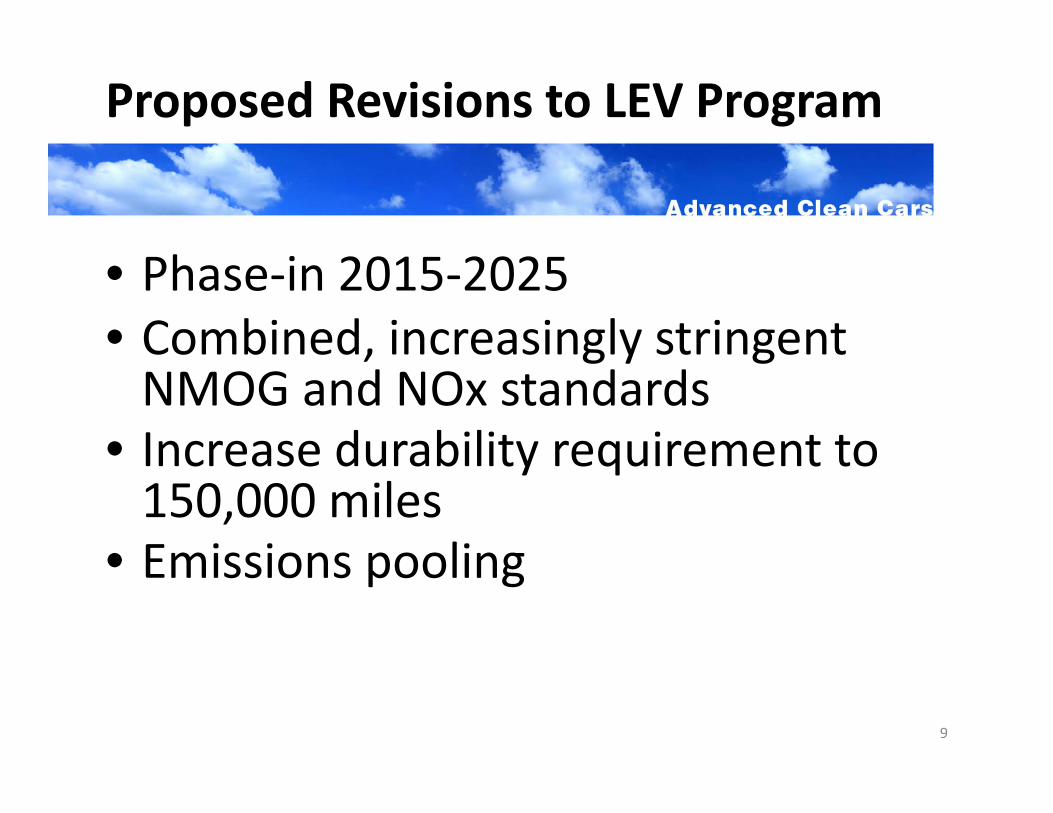

Proposed Revisions to LEV Program

• Phase‐in 2015‐2025• Combined, increasingly stringent NMOG and NOx standards

• Increase durability requirement to 150,000 miles

• Emissions pooling

9

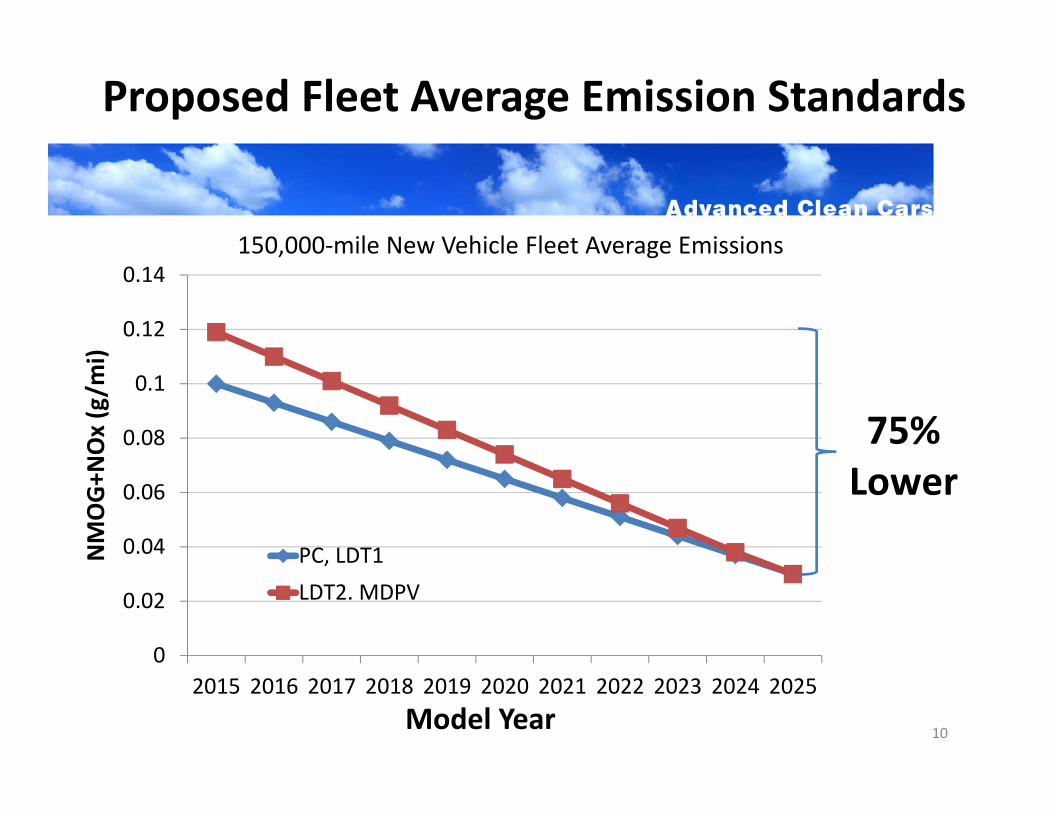

Proposed Fleet Average Emission Standards

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

PC, LDT1LDT2. MDPV

75%Lower

10Model Year

NMOG+N

Ox(g/m

i)

150,000‐mile New Vehicle Fleet Average Emissions

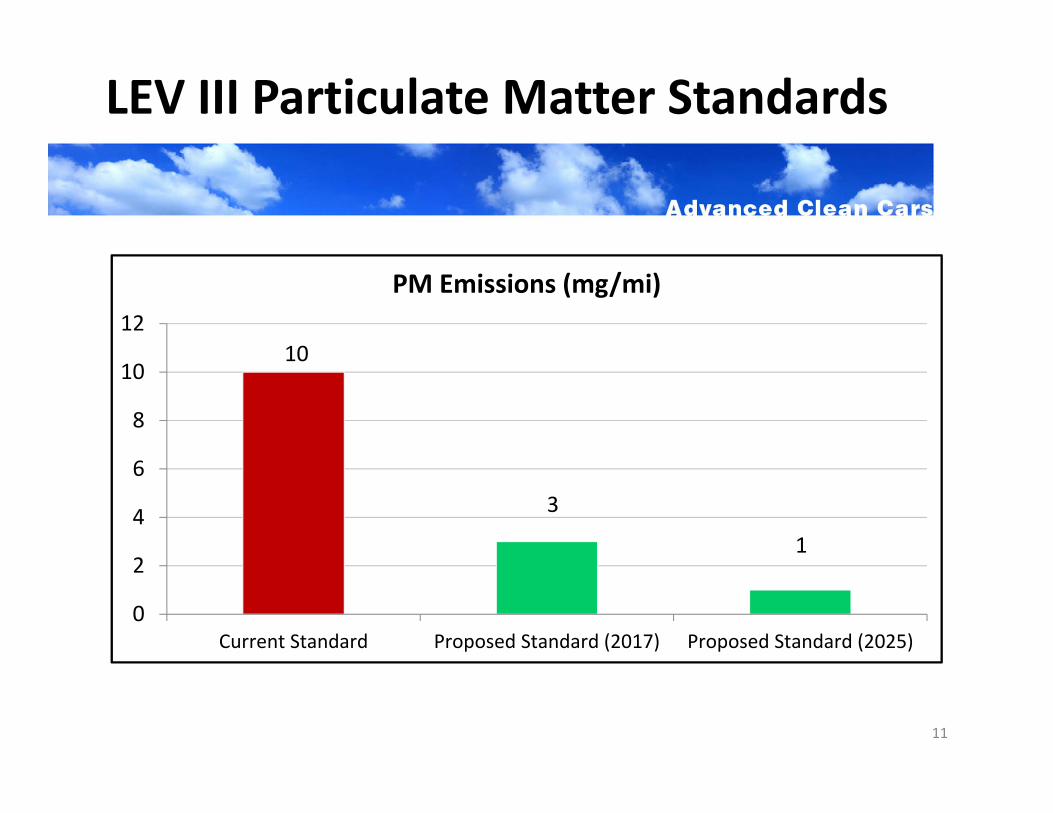

LEV III Particulate Matter Standards

11

10

3

1

0

2

4

6

8

10

12

Current Standard Proposed Standard (2017) Proposed Standard (2025)

PM Emissions (mg/mi)

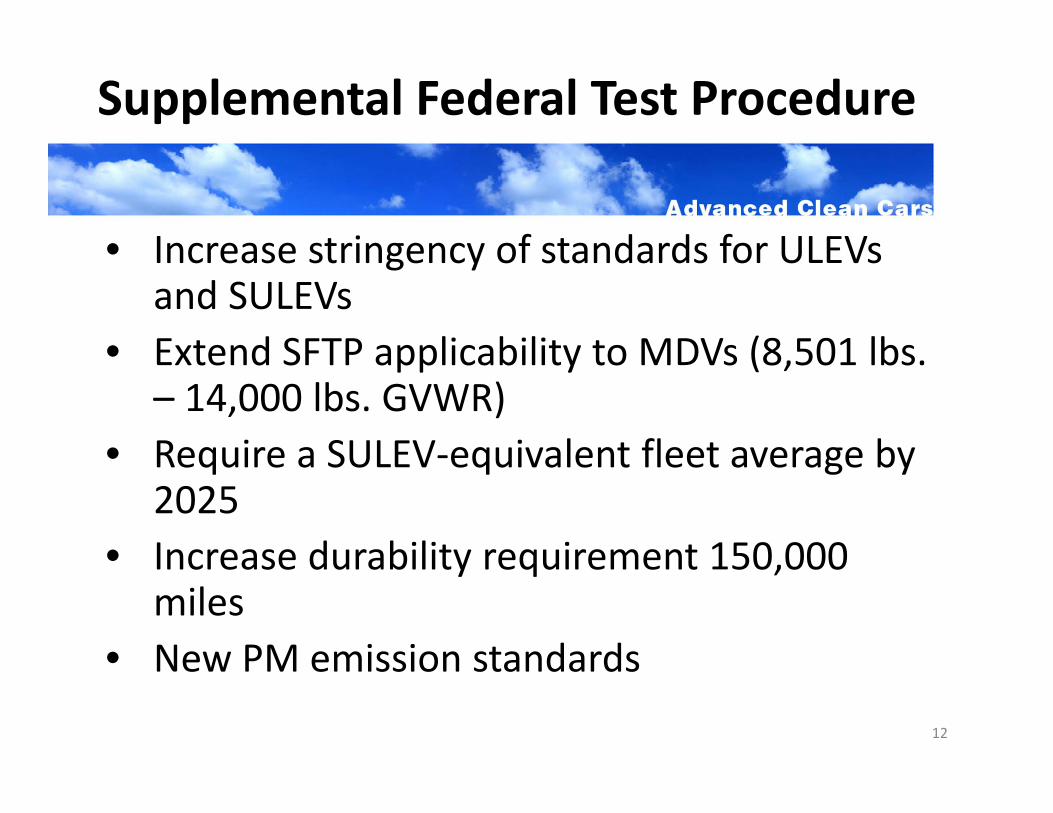

Supplemental Federal Test Procedure

• Increase stringency of standards for ULEVs and SULEVs

• Extend SFTP applicability to MDVs (8,501 lbs. – 14,000 lbs. GVWR)

• Require a SULEV‐equivalent fleet average by 2025

• Increase durability requirement 150,000 miles

• New PM emission standards

12

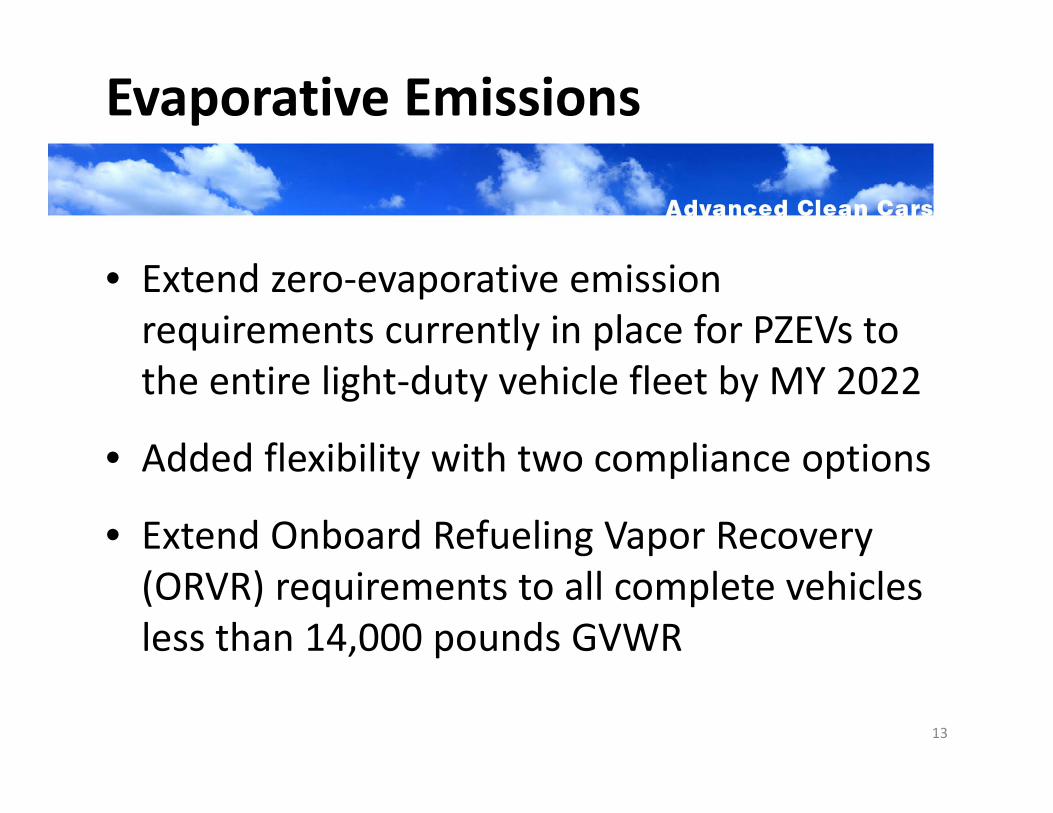

Evaporative Emissions

• Extend zero‐evaporative emission requirements currently in place for PZEVs to the entire light‐duty vehicle fleet by MY 2022

• Added flexibility with two compliance options

• Extend Onboard Refueling Vapor Recovery (ORVR) requirements to all complete vehicles less than 14,000 pounds GVWR

13

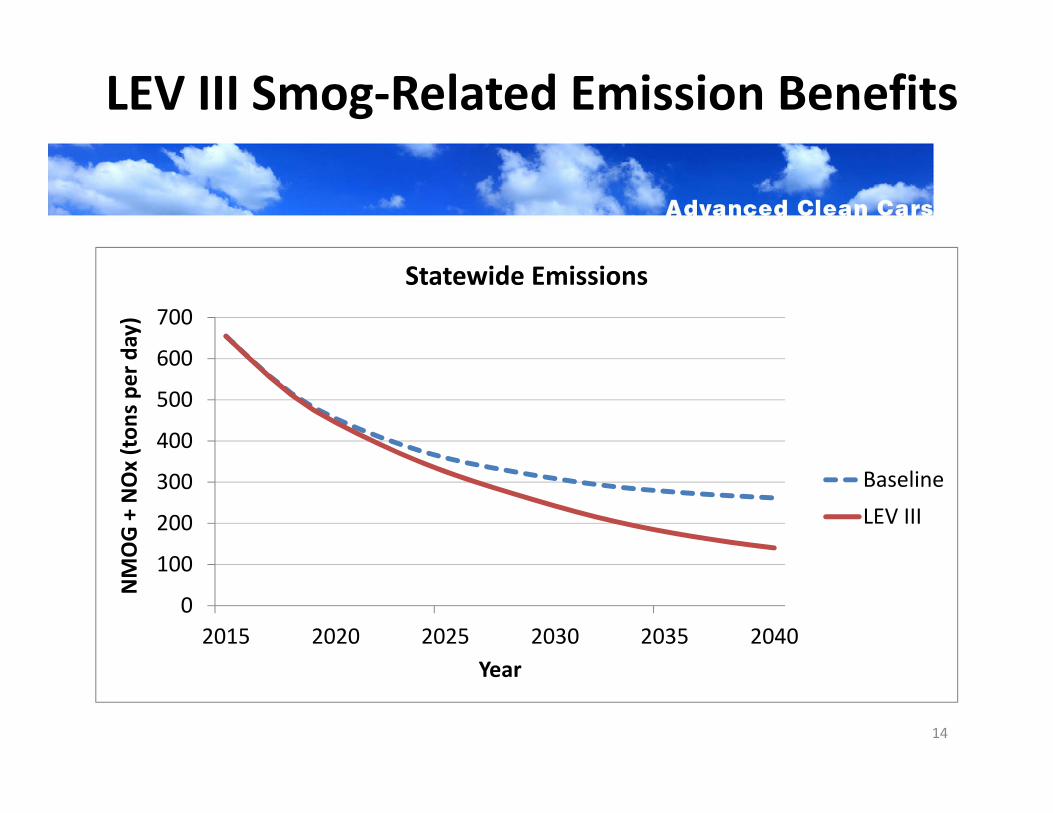

LEV III Smog‐Related Emission Benefits

0

100

200

300

400

500

600

700

2015 2020 2025 2030 2035 2040

NMOG + NOx(ton

s pe

r day)

Year

Statewide Emissions

BaselineLEV III

14

Other LEV III Amendments

• Minor amendments to the On‐Board Diagnostics regulations for the 2013 Model Year

• Changes to the specifications for certification gasoline to reflect current commercial gasoline.

15

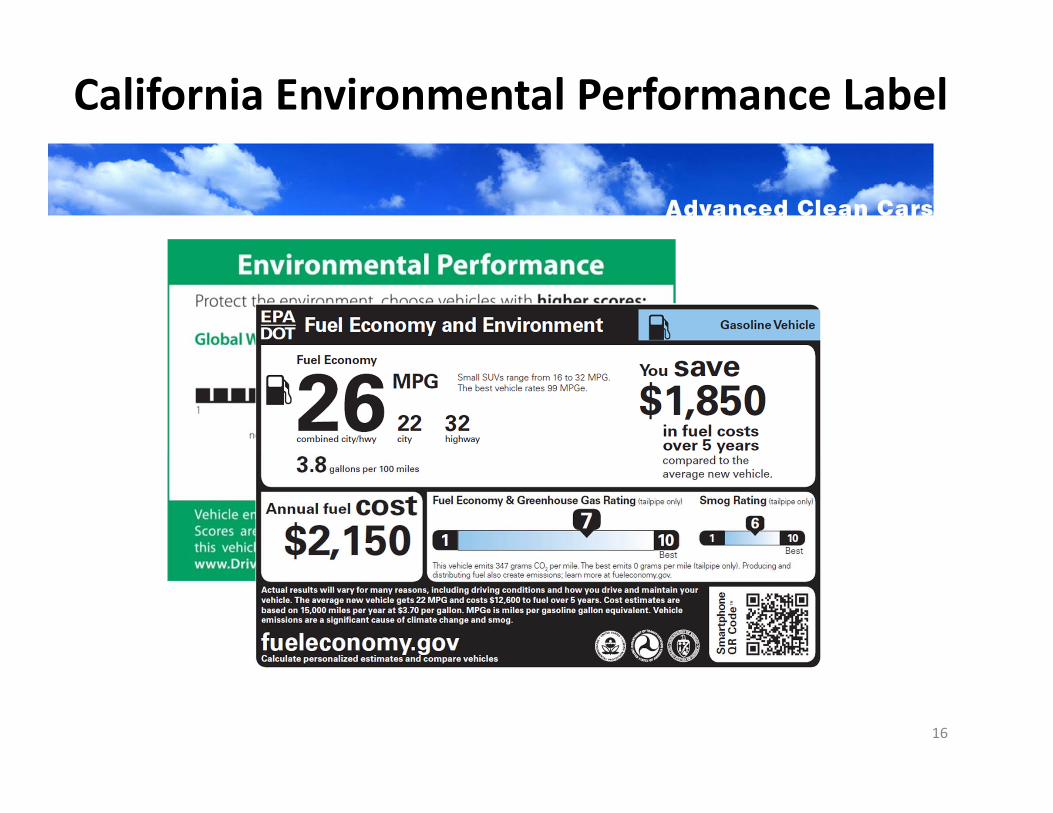

California Environmental Performance Label

16

LEV III: Reducing Greenhouse Gas Emissions

• LEV III regulations continue emission reductions for all new vehicles ‐ Greenhouse gas (GHG) standards reduce climate

emissions by 34%

18

GHG Standards: Background

• 2002: Legislature passes Pavley AB 1493• 2004: ARB approval of 2009‐2016 GHG standards• 2010: USEPA adoption of California 2012‐2016 GHG standards• 2010‐2011: Federal/California technical coordination• Nov. 2011: USEPA proposal for 2017‐2025 standards

19

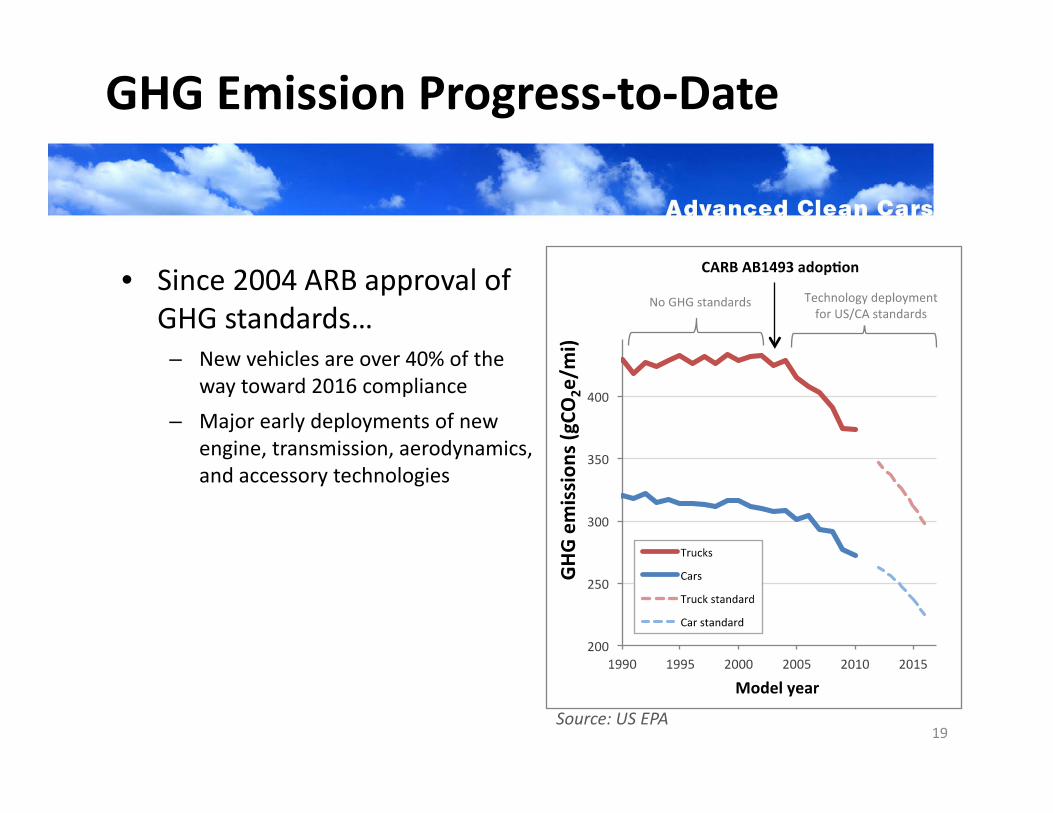

GHG Emission Progress‐to‐Date

• Since 2004 ARB approval of GHG standards…– New vehicles are over 40% of the

way toward 2016 compliance– Major early deployments of new

engine, transmission, aerodynamics, and accessory technologies

Source: US EPA

100

150

200

250

300

350

2010 2015 2020 2025

GHG emission

s (gCO

2e/m

i)

Model year

Truck Combined light duty Car

Previous rule Proposed rulemaking

20

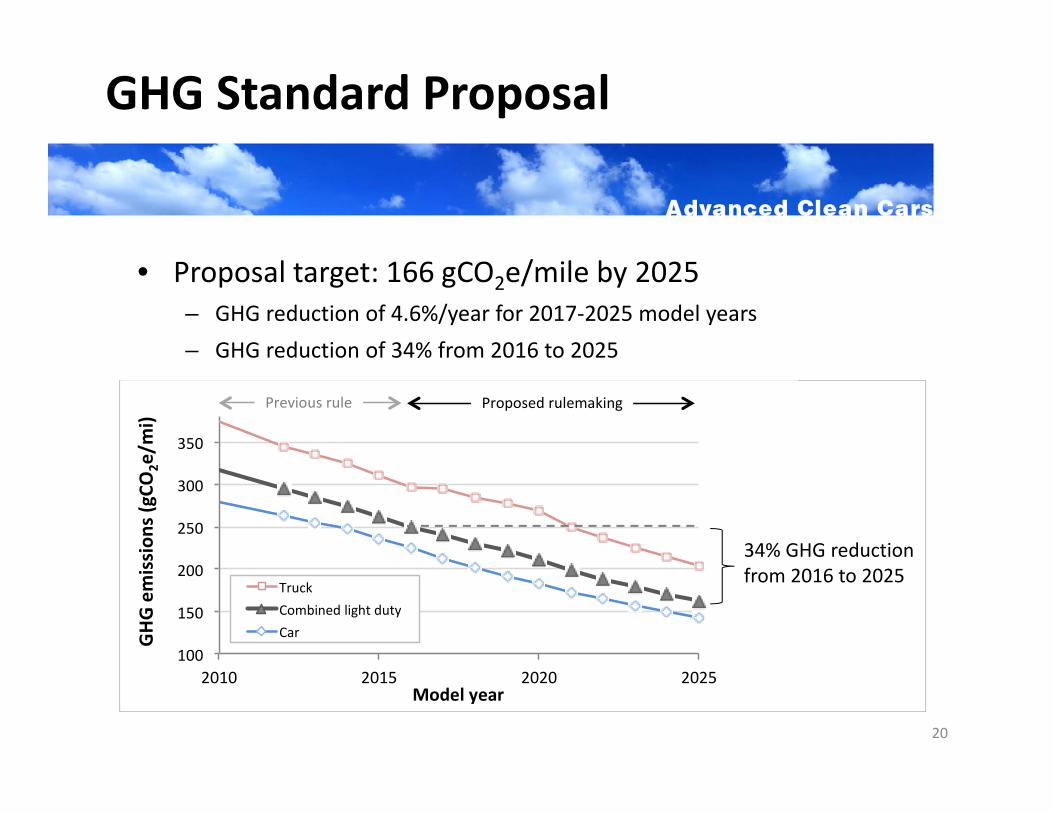

GHG Standard Proposal

• Proposal target: 166 gCO2e/mile by 2025– GHG reduction of 4.6%/year for 2017‐2025 model years– GHG reduction of 34% from 2016 to 2025

34% GHG reduction from 2016 to 2025

100

150

200

250

300

350

35 40 45 50 55 60

GHG emission

(gCO

2e/m

i)

Vehicle footprint ( 2)

21

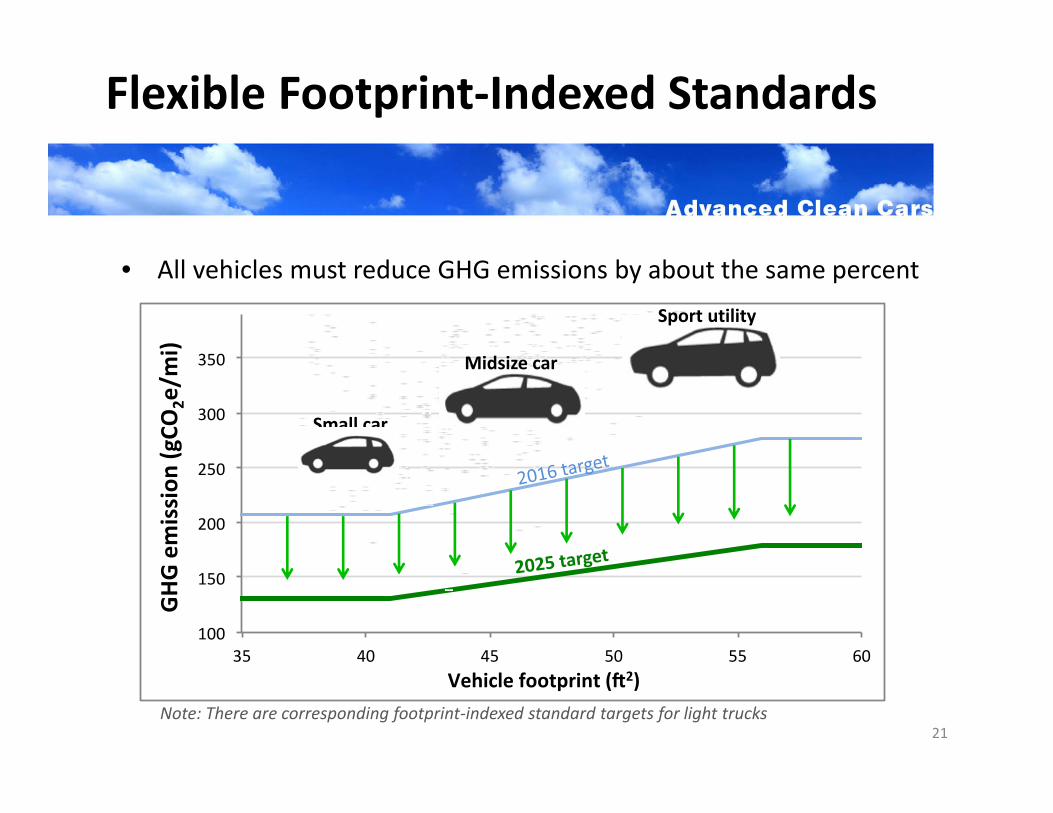

Flexible Footprint‐Indexed Standards

• All vehicles must reduce GHG emissions by about the same percent

Note: There are corresponding footprint‐indexed standard targets for light trucks

Small car

Midsize car

Sport utility

22

Flexibility Preserves Vehicle Choice

• Company sales‐weighted averaging• Footprint‐indexed targets• Separate car and truck standards• Credit banking (5‐year carryforward, 3‐year carryback)• Technology‐specific credit opportunities

0%

20%

40%

60%

80%

100%

2010 2015 2020 2025

New

veh

icles of each techno

logy ty

pe

Model year

Conven onal

Advanced Low‐GHG

Conven onal Vehicles

ZEV

23

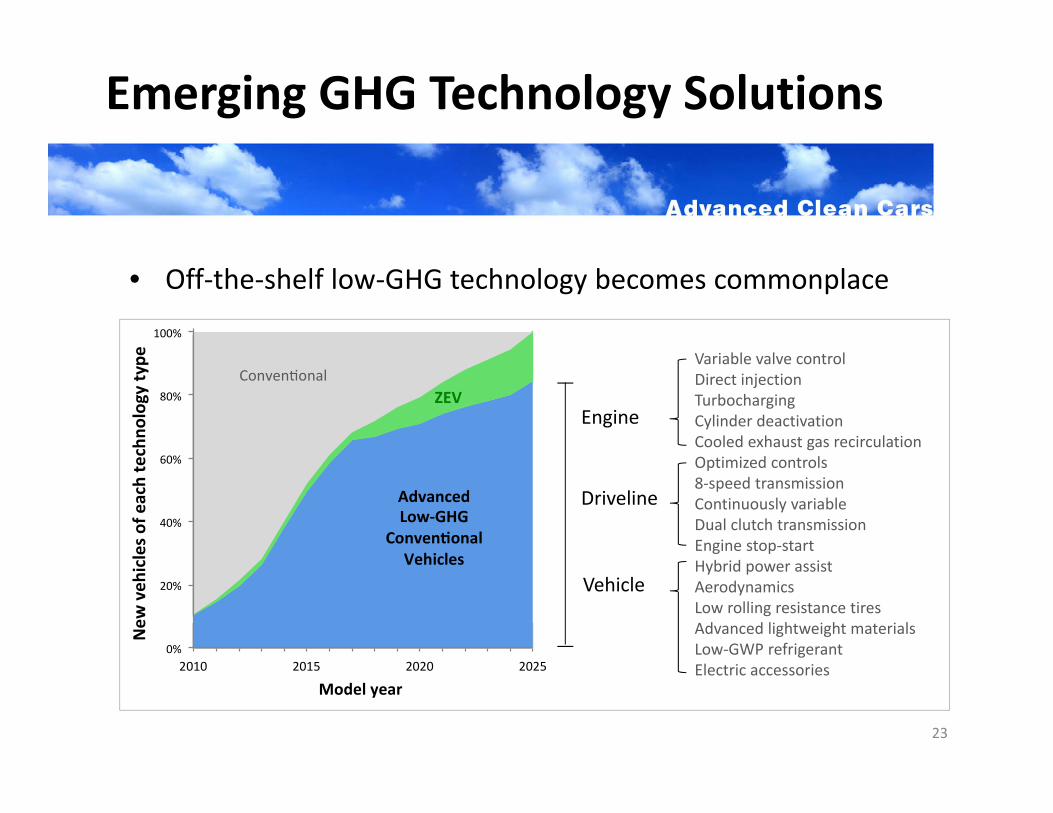

Emerging GHG Technology Solutions

• Off‐the‐shelf low‐GHG technology becomes commonplace

Variable valve controlDirect injectionTurbochargingCylinder deactivationCooled exhaust gas recirculationOptimized controls8‐speed transmissionContinuously variableDual clutch transmissionEngine stop‐startHybrid power assistAerodynamicsLow rolling resistance tiresAdvanced lightweight materialsLow‐GWP refrigerantElectric accessories

Engine

Driveline

Vehicle

24

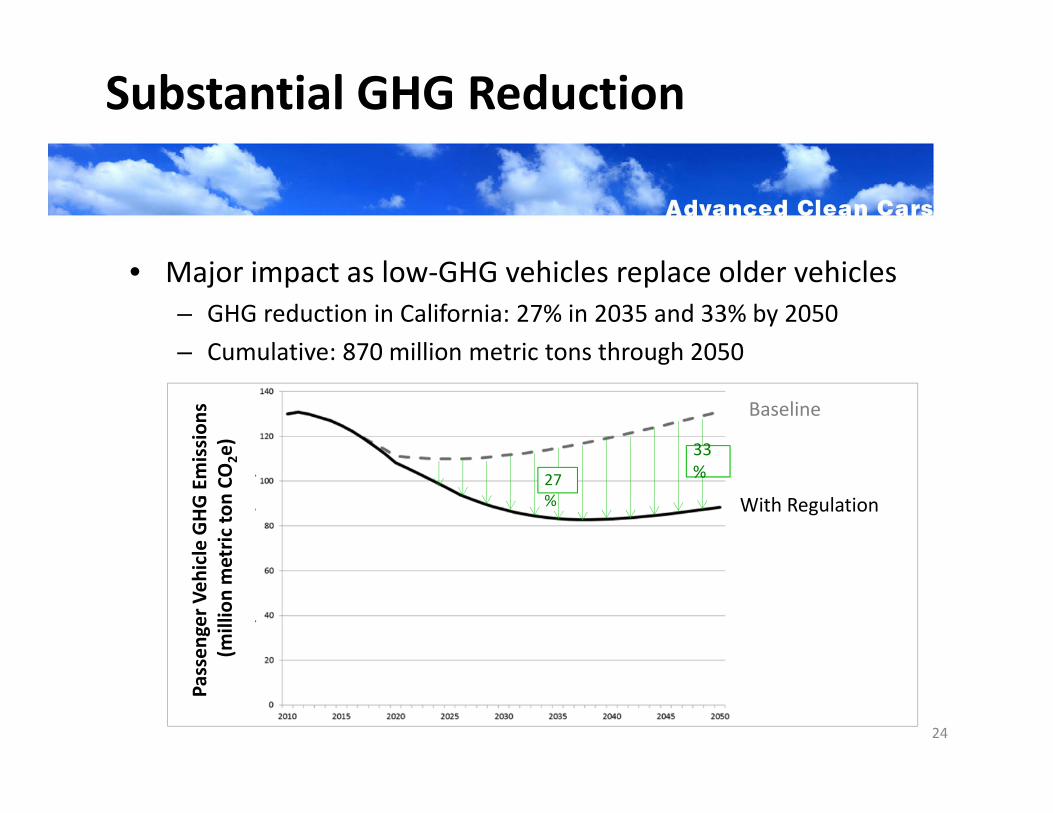

Substantial GHG Reduction

• Major impact as low‐GHG vehicles replace older vehicles– GHG reduction in California: 27% in 2035 and 33% by 2050– Cumulative: 870 million metric tons through 2050

Baseline

With Regulation

Passen

ger V

ehicle GHG Emission

s (m

illion metric

ton CO

2e)

27%

33%

25

Federal Coordination

• ARB rulemaking has paralleled federal regulation timing• “Deemed to comply” provision

– ARB intends to deem compliance with US EPA GHG regulation as sufficient for ARB GHG regulation compliance, provided the final federal standards are substantially similar

• Mid‐Term Review– ARB intends to participate in the federal agencies’ “Mid‐

Term Review” to review standards for model years 2022‐2025 (that is to be completed by April 2018).

26

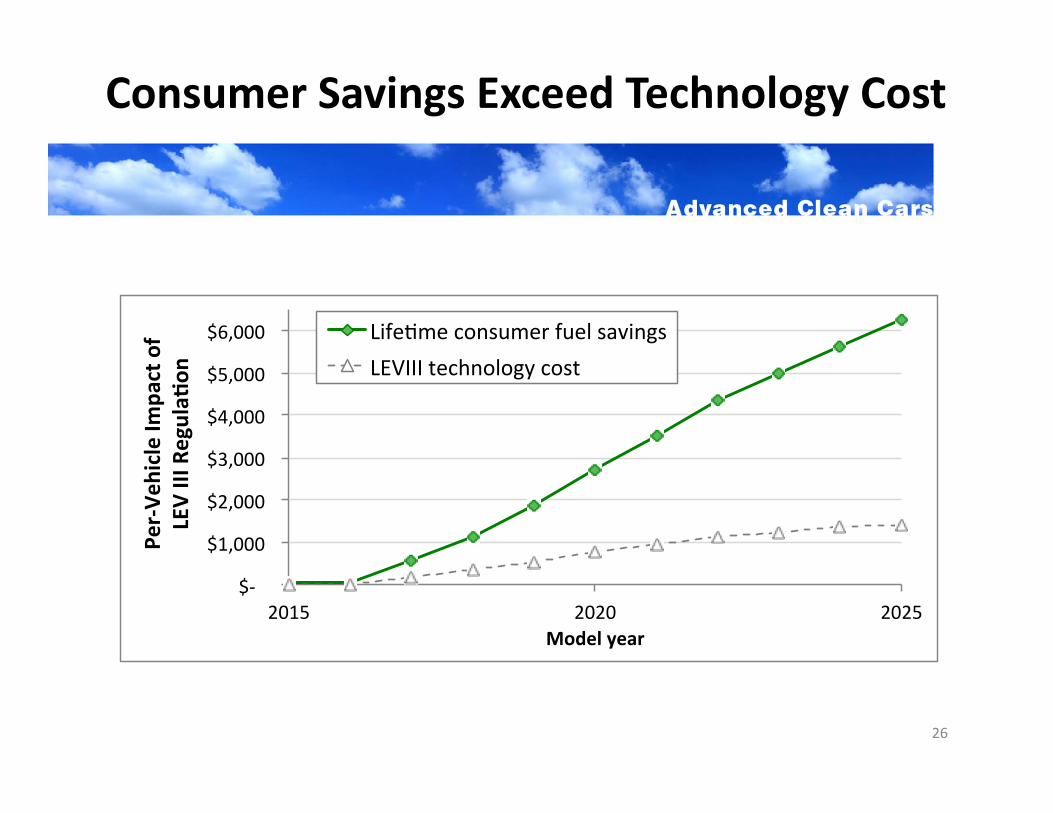

Consumer Savings Exceed Technology Cost

$‐

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

2015 2020 2025

Per‐Ve

hicle Im

pact of

LEV III Regula

on

Model year

Life me consumer fuel savings LEVIII technology cost

LEV III Regulation Summary

• Achieves maximum feasible and cost‐effective emission reductions

• Accelerates transition to a cleaner fleet of California vehicles• Provides manufacturers with lead time and flexibility• Staff recommends Board adopt LEV III regulation as proposed

27

ZEV

28

ZEVZEV

CFOCFO

LEVLEV

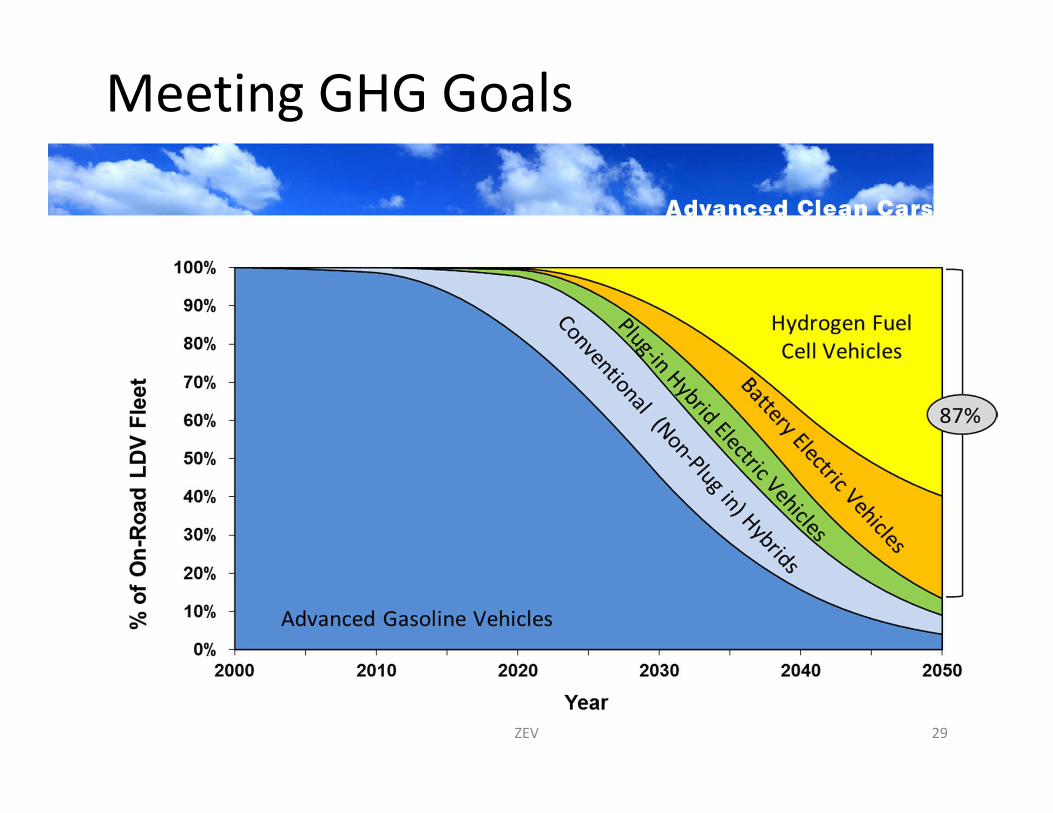

Meeting GHG Goals

ZEV 29

0

100

200

300

400

500

600

GHG emission

s (g/mi)

Fuel‐cycle

Other vehicle (HFC, N2O, CH4)

Vehicle use (exhaust)

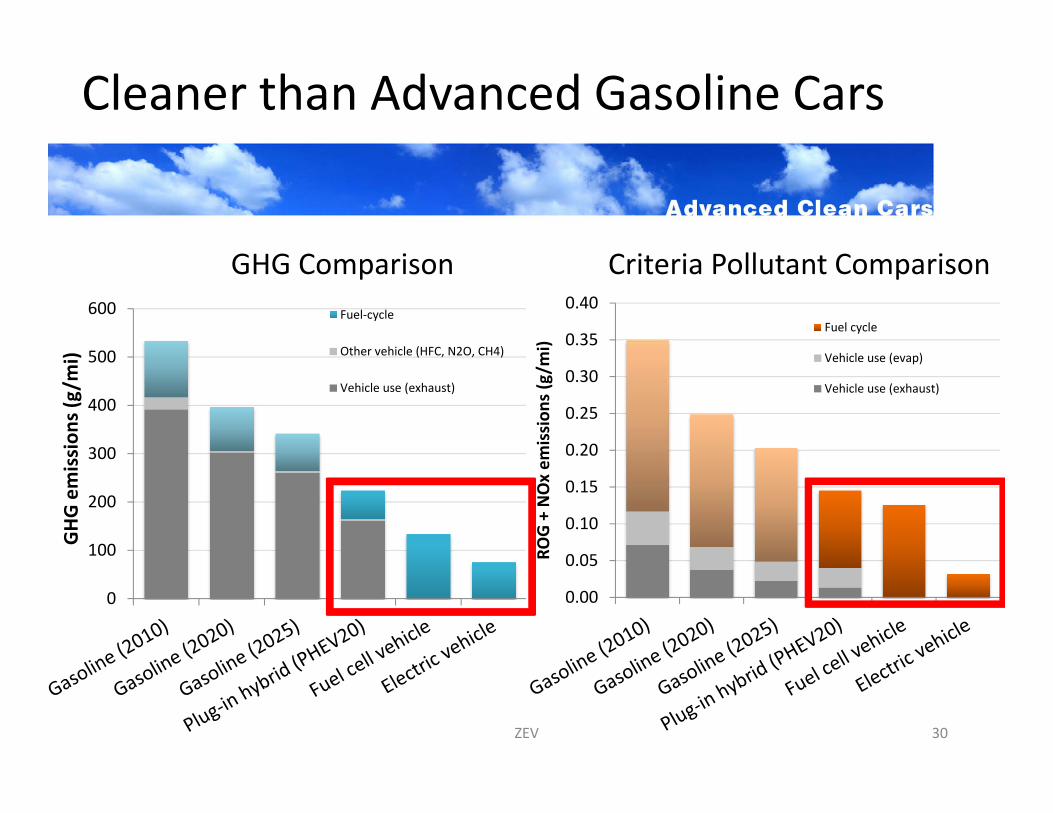

Cleaner than Advanced Gasoline Cars

GHG Comparison Criteria Pollutant Comparison

ZEV

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

ROG + NOx em

ission

s (g/m

i)

Fuel cycle

Vehicle use (evap)

Vehicle use (exhaust)

30

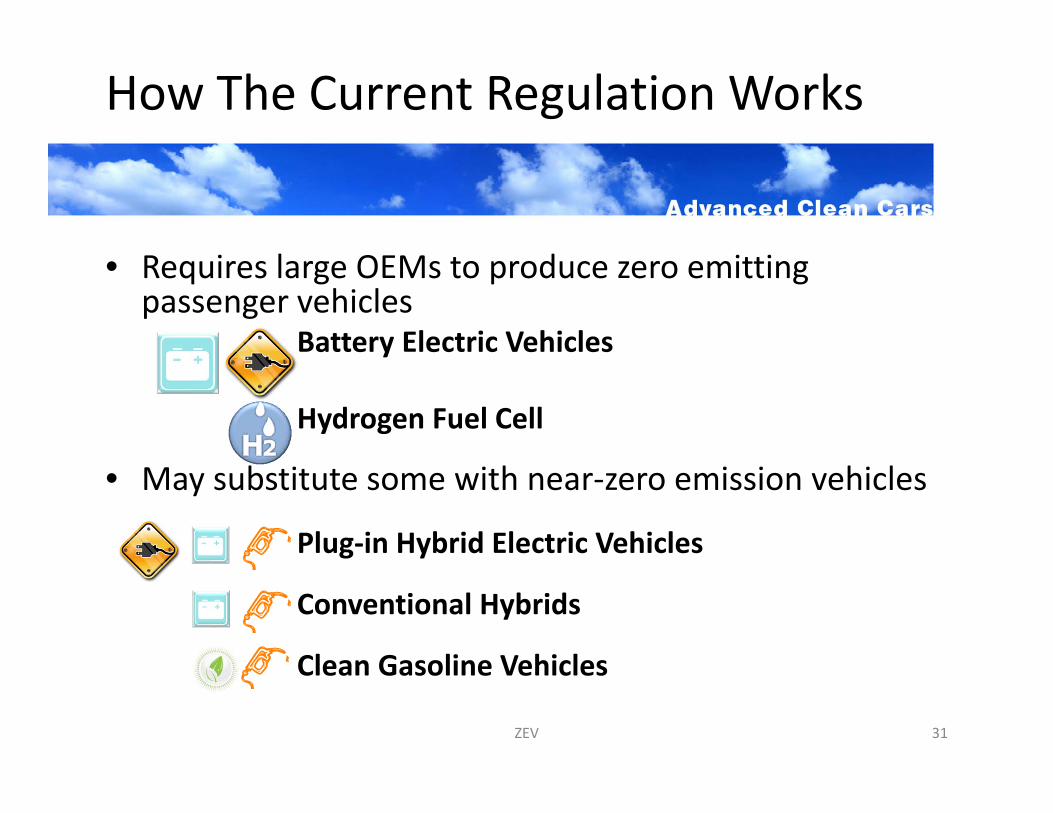

How The Current Regulation Works

• Requires large OEMs to produce zero emitting passenger vehicles

Battery Electric Vehicles

Hydrogen Fuel Cell

• May substitute some with near‐zero emission vehicles

Plug‐in Hybrid Electric Vehicles

Conventional Hybrids

Clean Gasoline Vehicles

ZEV 31

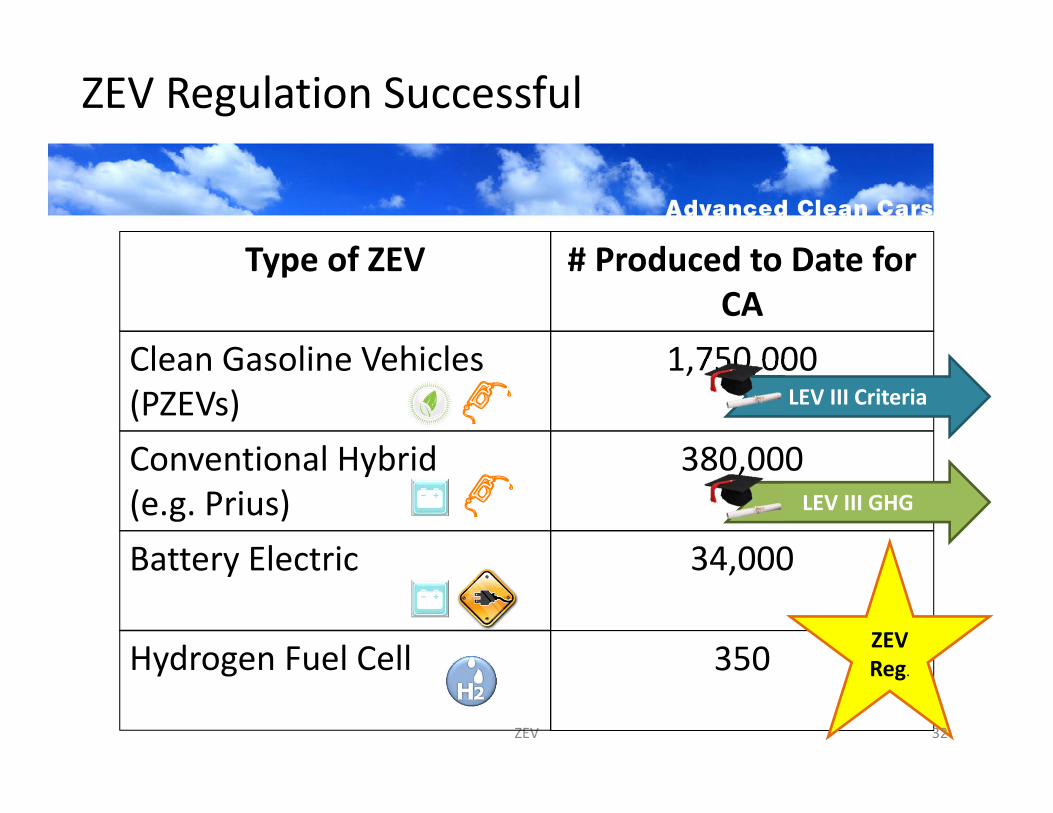

ZEV Regulation Successful

ZEV

Battery Electric

Hydrogen Fuel Cell

Conventional Hybrid (e.g. Prius)

Clean Gasoline Vehicles (PZEVs)

Type of ZEV # Produced to Date for CA

1,750,000

380,000

34,000

350

LEV III Criteria

ZEV Reg.

LEV III GHG

32

Fuel Cell Vehicles

Battery Electric VehiclesPlug‐In Hybrids

Lots of ZEVs!

Summary of Staff’s Proposal

• Increase ZEV requirement• Include more manufacturers• Amend ZEV Credits• Amend PHEV Credits• Added Flexibility

34

‐

50,000

100,000

150,000

200,000

250,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Annu

al ZEV

s

Current Regulation ‐ZEVs

Current Regulation ‐PHEVs

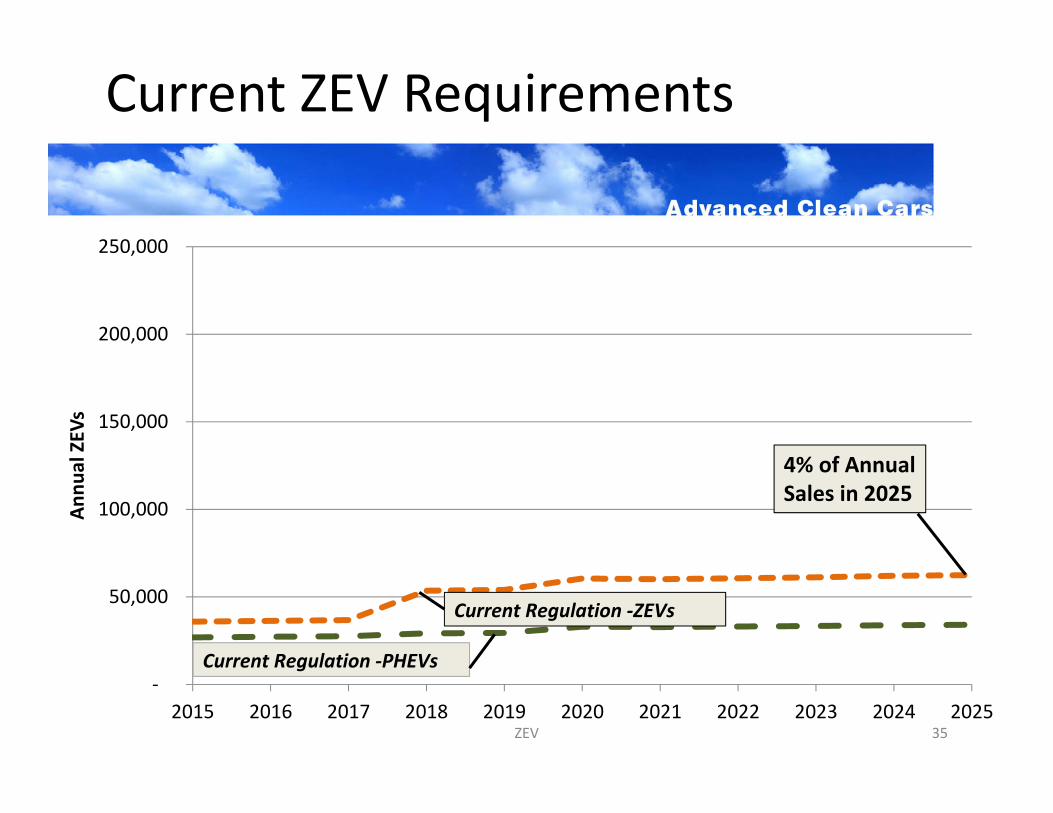

Current ZEV Requirements

ZEV

4% of Annual Sales in 2025

35

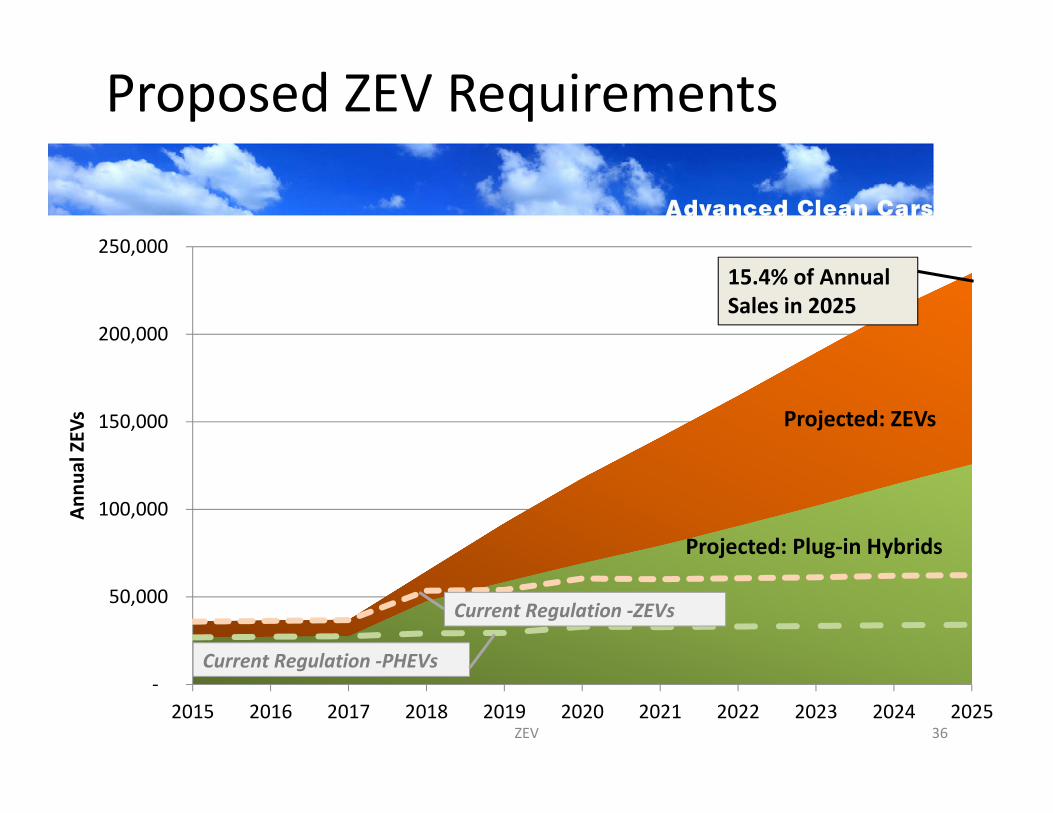

Proposed ZEV Requirements

ZEV

‐

50,000

100,000

150,000

200,000

250,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Annu

al ZEV

s

Current Regulation ‐ZEVs

Current Regulation ‐PHEVs

Projected: Plug‐in Hybrids

Projected: ZEVs

15.4% of Annual Sales in 2025

36

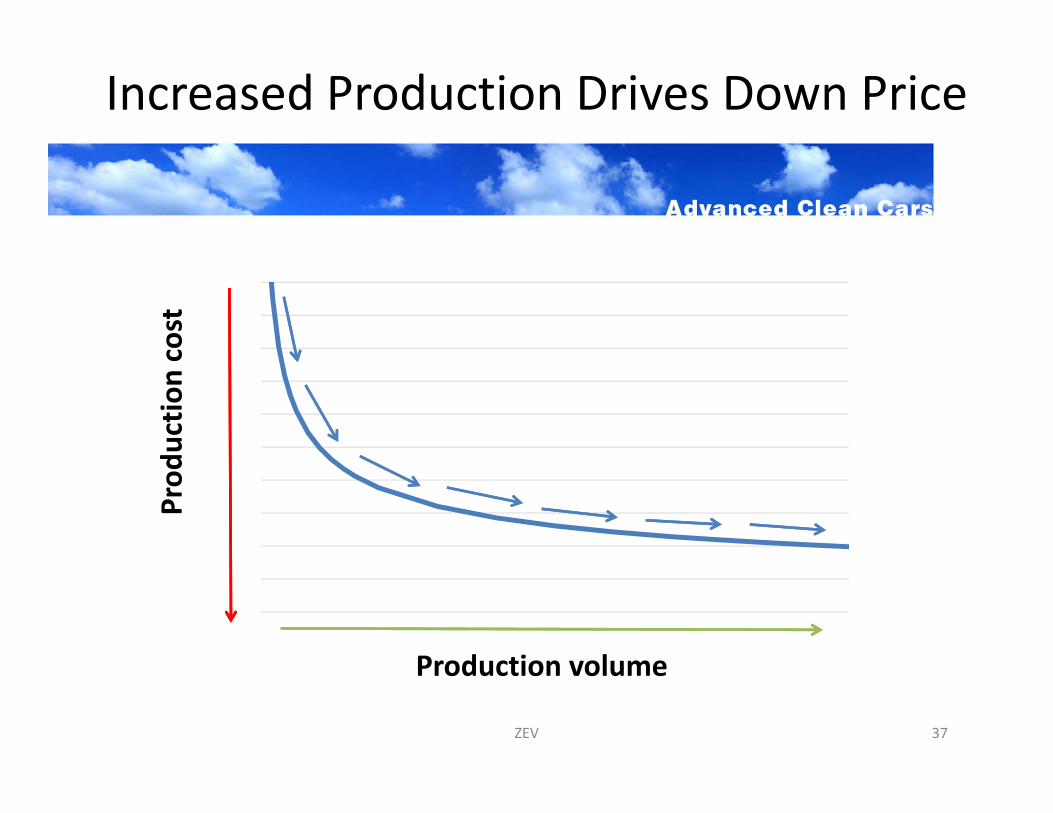

Increased Production Drives Down Price

ZEV 37

Prod

uctio

n cost

Production volume

38

CEO of Nissan at Detroit Auto Show

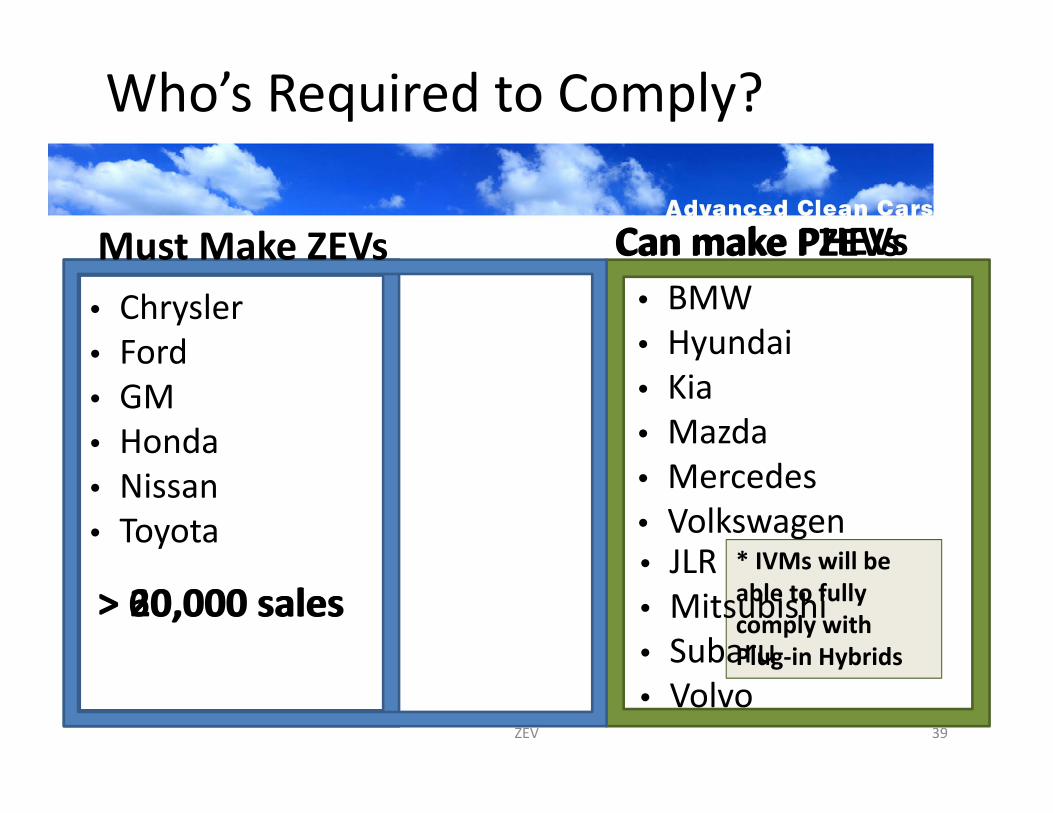

Who’s Required to Comply?

• Chrysler• Ford• GM• Honda• Nissan• Toyota

* IVMs will be able to fully comply with Plug‐in Hybrids

ZEV

• BMW• Hyundai• Kia• Mazda• Mercedes• Volkswagen• JLR• Mitsubishi• Subaru• Volvo

Must Make ZEVs Can make PZEVs

> 60,000 sales> 20,000 sales

39

Can make PHEVs

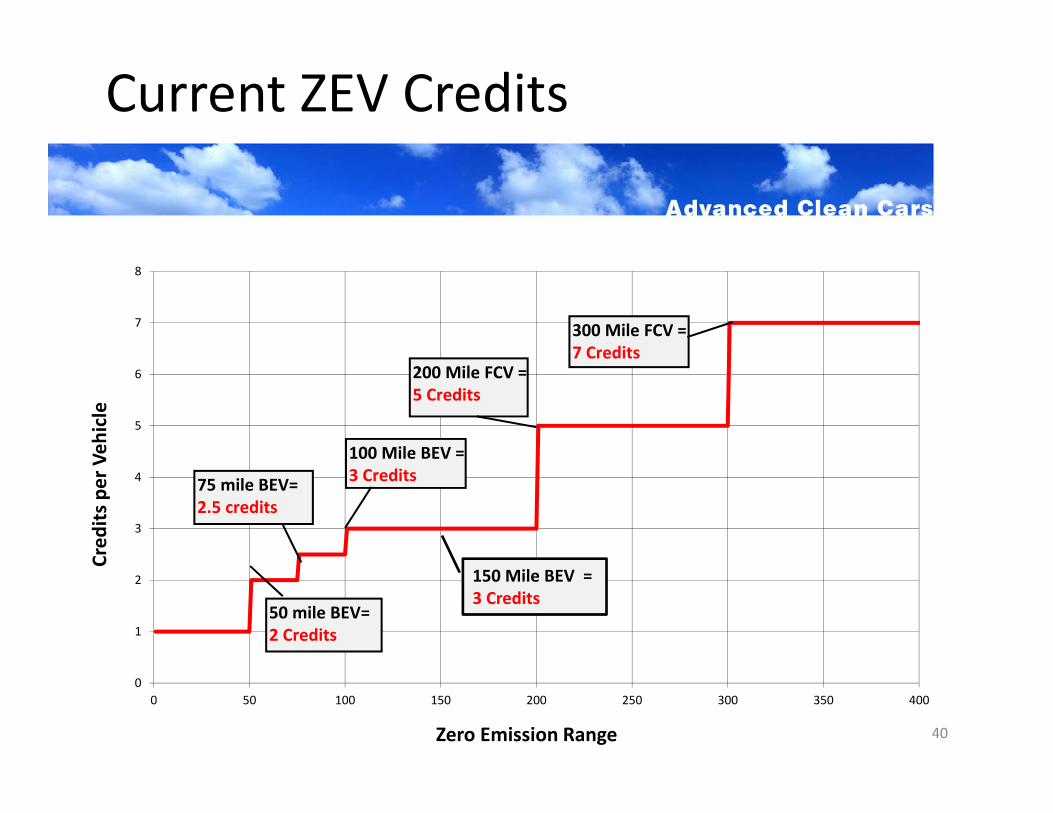

Current ZEV Credits

40

0

1

2

3

4

5

6

7

8

0 50 100 150 200 250 300 350 400

Cred

its per Veh

icle

Zero Emission Range

50 mile BEV= 2 Credits

100 Mile BEV = 3 Credits

200 Mile FCV = 5 Credits

75 mile BEV= 2.5 credits

300 Mile FCV = 7 Credits

150 Mile BEV = 3 Credits

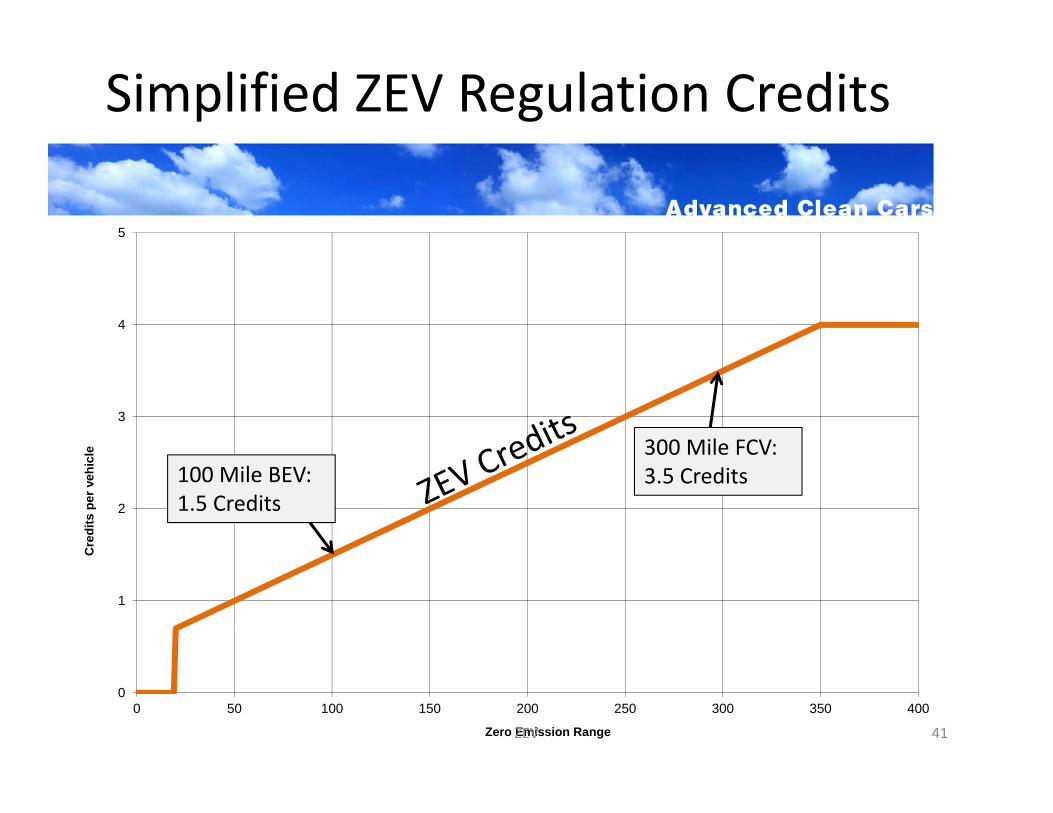

0

1

2

3

4

5

0 50 100 150 200 250 300 350 400

Cre

dits

per

veh

icle

Zero Emission Range

Simplified ZEV Regulation Credits

100 Mile BEV: 1.5 Credits

300 Mile FCV: 3.5 Credits

ZEV 41

0

1

2

3

4

5

0 50 100 150 200 250 300 350 400

Cre

dits

per

veh

icle

Zero Emission Range

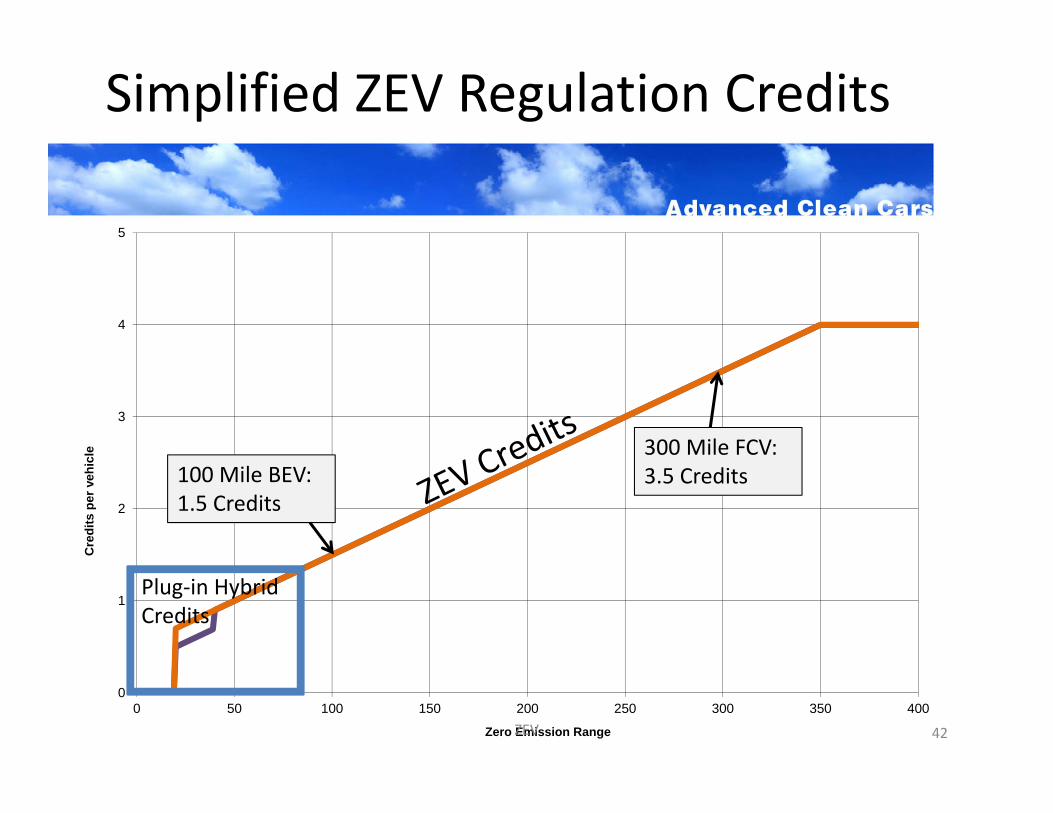

Simplified ZEV Regulation Credits

Plug‐in Hybrid Credits

100 Mile BEV: 1.5 Credits

300 Mile FCV: 3.5 Credits

ZEV 42

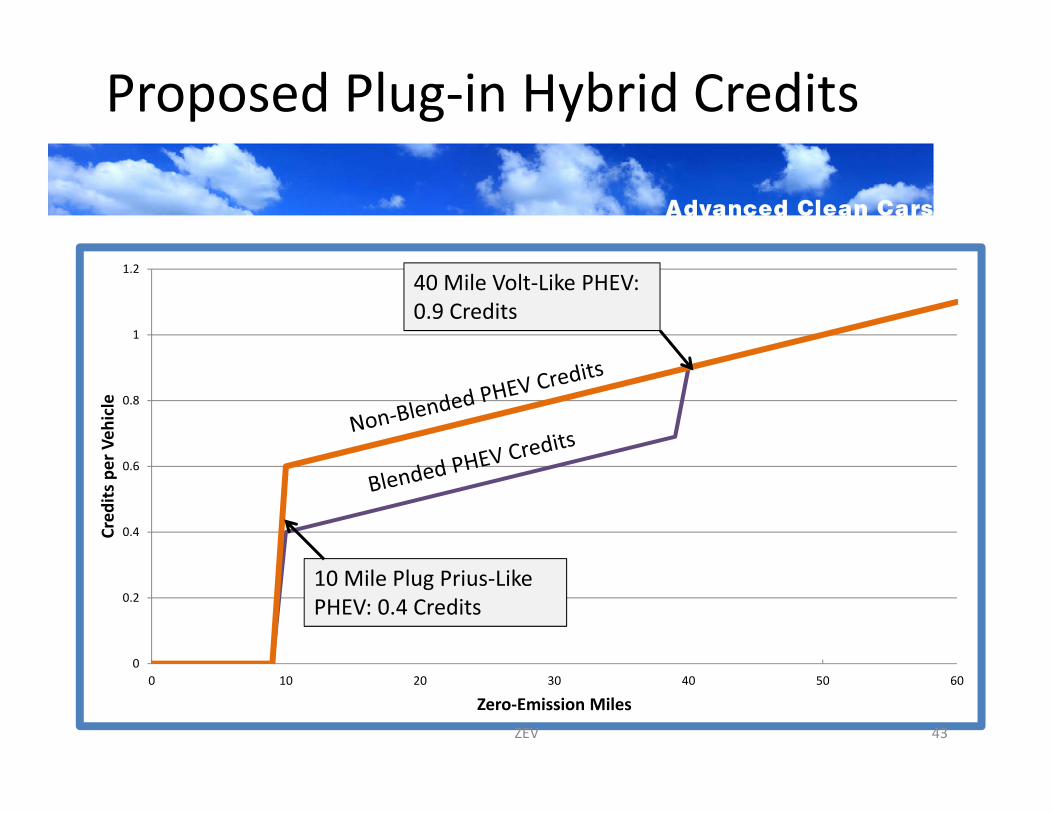

Proposed Plug‐in Hybrid Credits

0

0.2

0.4

0.6

0.8

1

1.2

0 10 20 30 40 50 60

Cred

its per Veh

icle

Zero‐Emission Miles

10 Mile Plug Prius‐Like PHEV: 0.4 Credits

40 Mile Volt‐Like PHEV: 0.9 Credits

ZEV 43

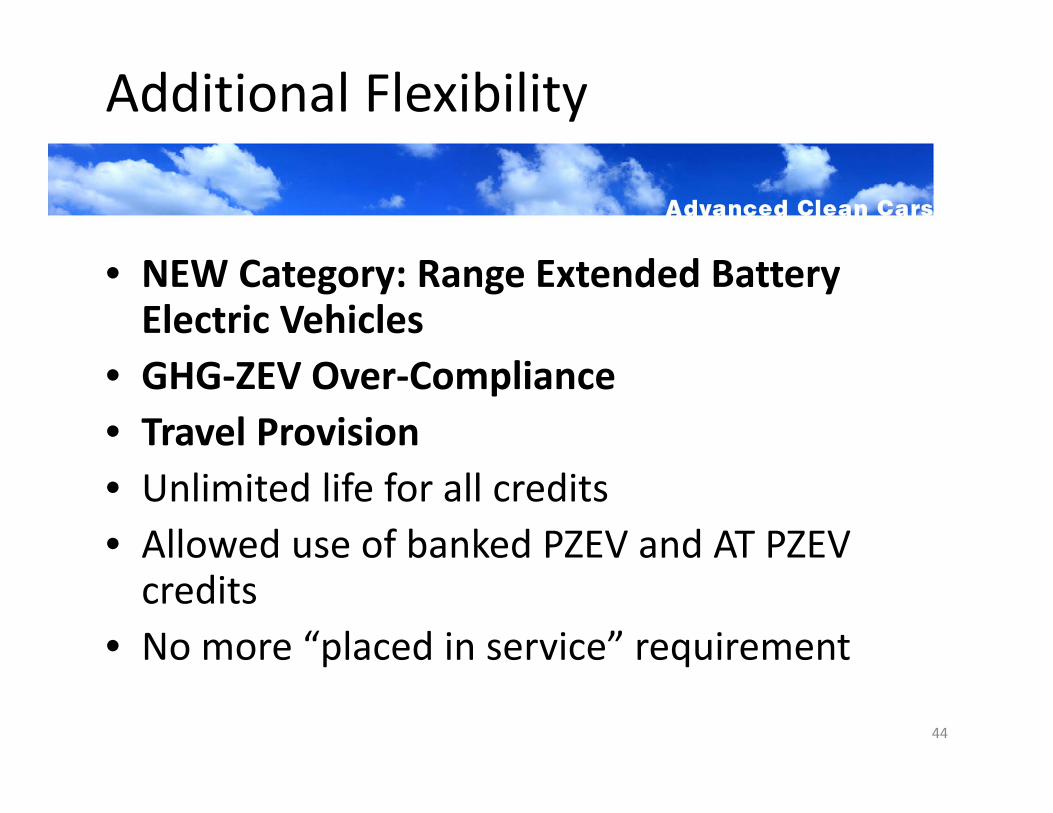

Additional Flexibility

• NEW Category: Range Extended Battery Electric Vehicles

• GHG‐ZEV Over‐Compliance• Travel Provision• Unlimited life for all credits• Allowed use of banked PZEV and AT PZEV credits

• No more “placed in service” requirement

44

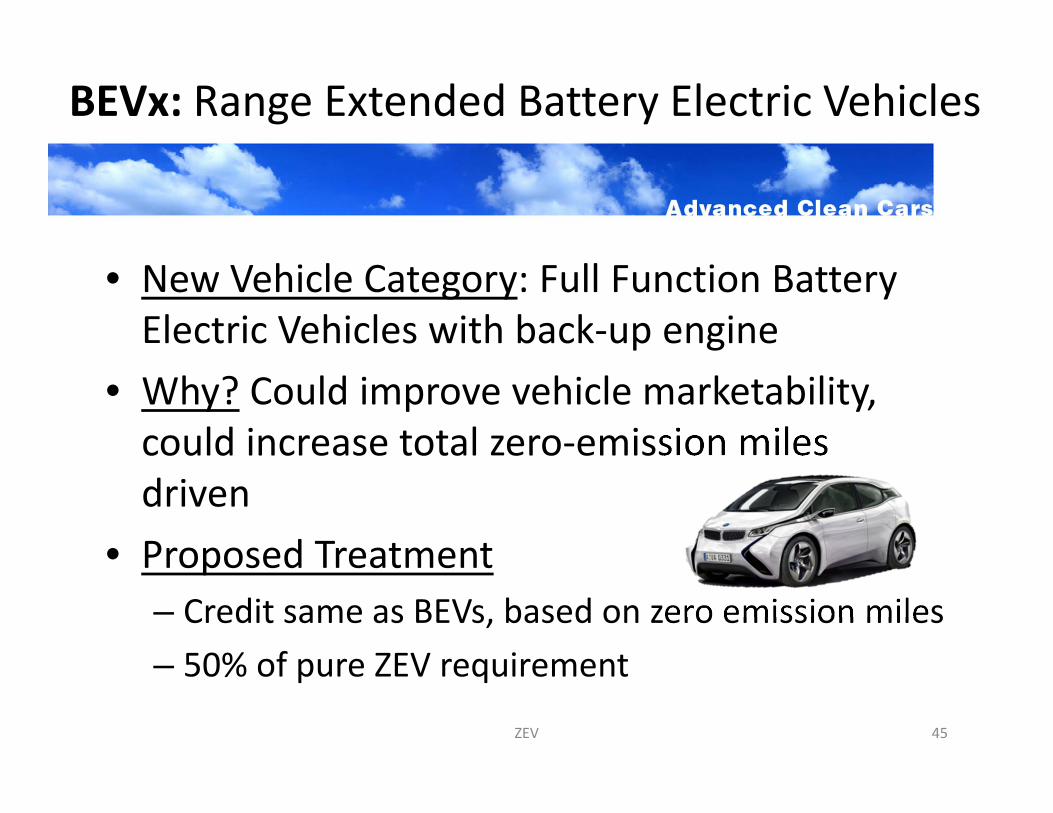

BEVx: Range Extended Battery Electric Vehicles

• New Vehicle Category: Full Function Battery Electric Vehicles with back‐up engine

• Why? Could improve vehicle marketability, could increase total zero‐emission miles driven

• Proposed Treatment– Credit same as BEVs, based on zero emission miles– 50% of pure ZEV requirement

ZEV 45

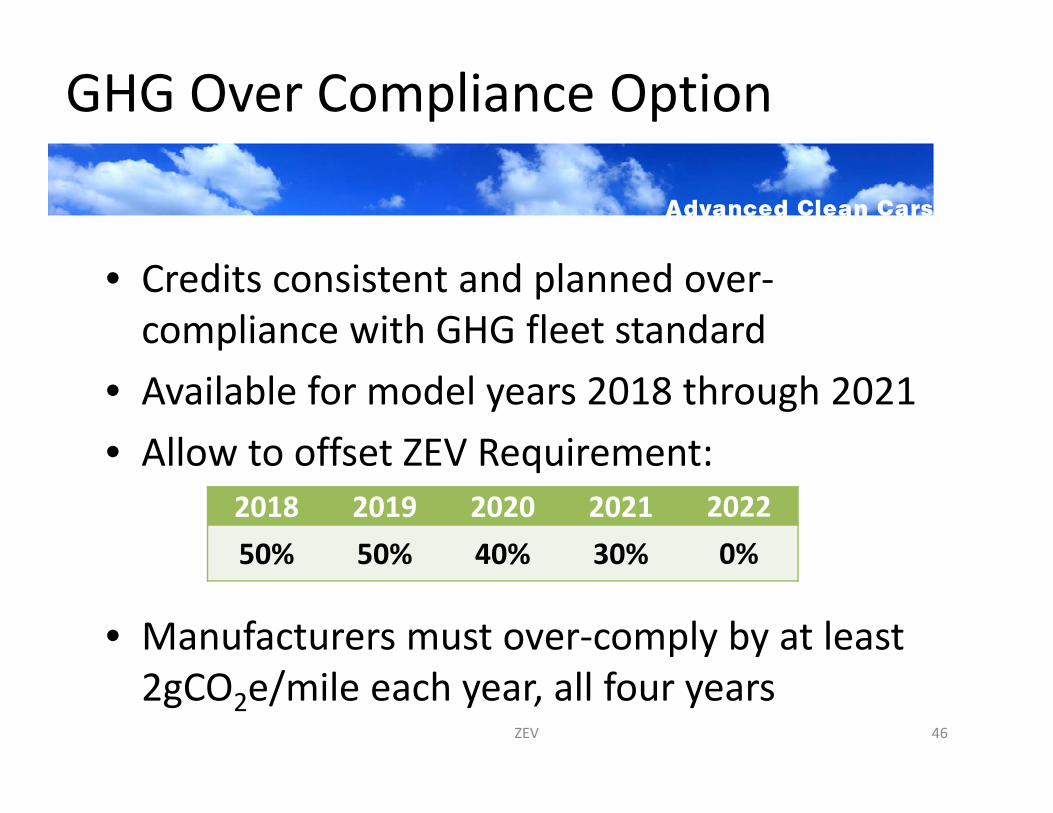

GHG Over Compliance Option

• Credits consistent and planned over‐compliance with GHG fleet standard

• Available for model years 2018 through 2021• Allow to offset ZEV Requirement:

• Manufacturers must over‐comply by at least 2gCO2e/mile each year, all four years

2018 2019 2020 2021 202250% 50% 40% 30% 0%

ZEV 46

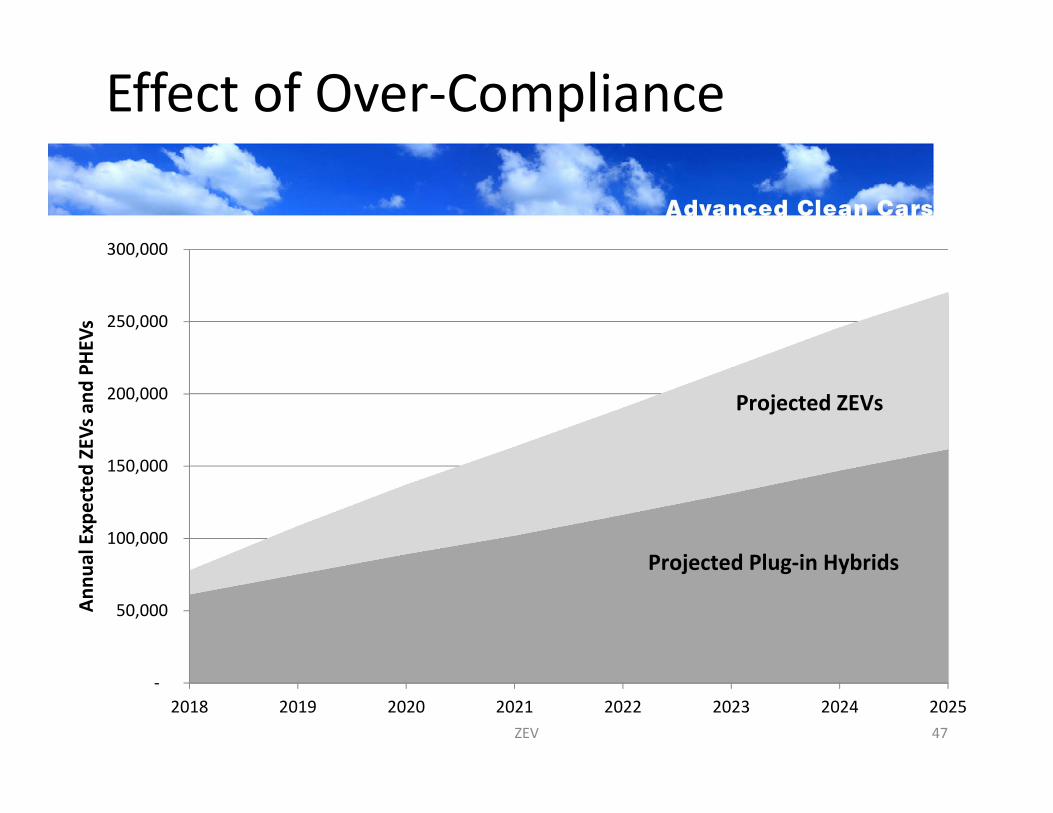

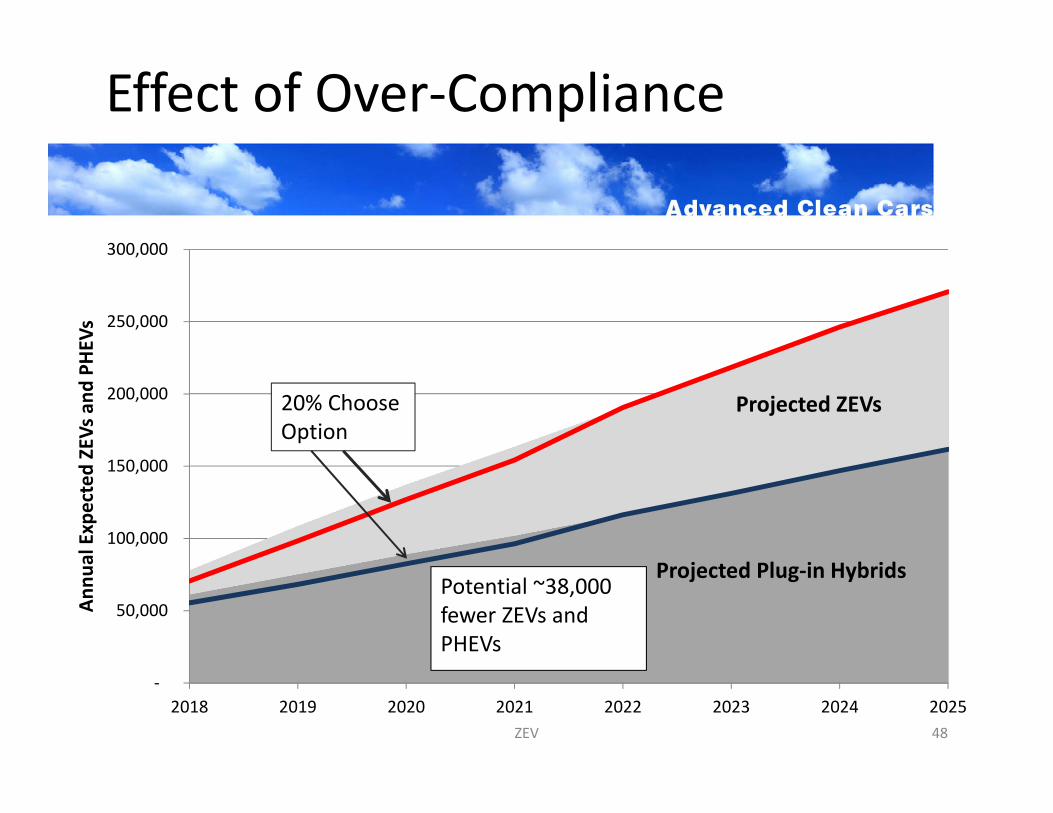

Effect of Over‐Compliance

ZEV

‐

50,000

100,000

150,000

200,000

250,000

300,000

2018 2019 2020 2021 2022 2023 2024 2025

Annu

al Expected ZEVs and

PHEV

s

Projected ZEVs

Projected Plug‐in Hybrids

47

‐

50,000

100,000

150,000

200,000

250,000

300,000

2018 2019 2020 2021 2022 2023 2024 2025

Annu

al Expected ZEVs and

PHEV

sEffect of Over‐Compliance

ZEV

Potential ~38,000 fewer ZEVs and PHEVs

20% Choose Option

Projected ZEVs

Projected Plug‐in Hybrids

48

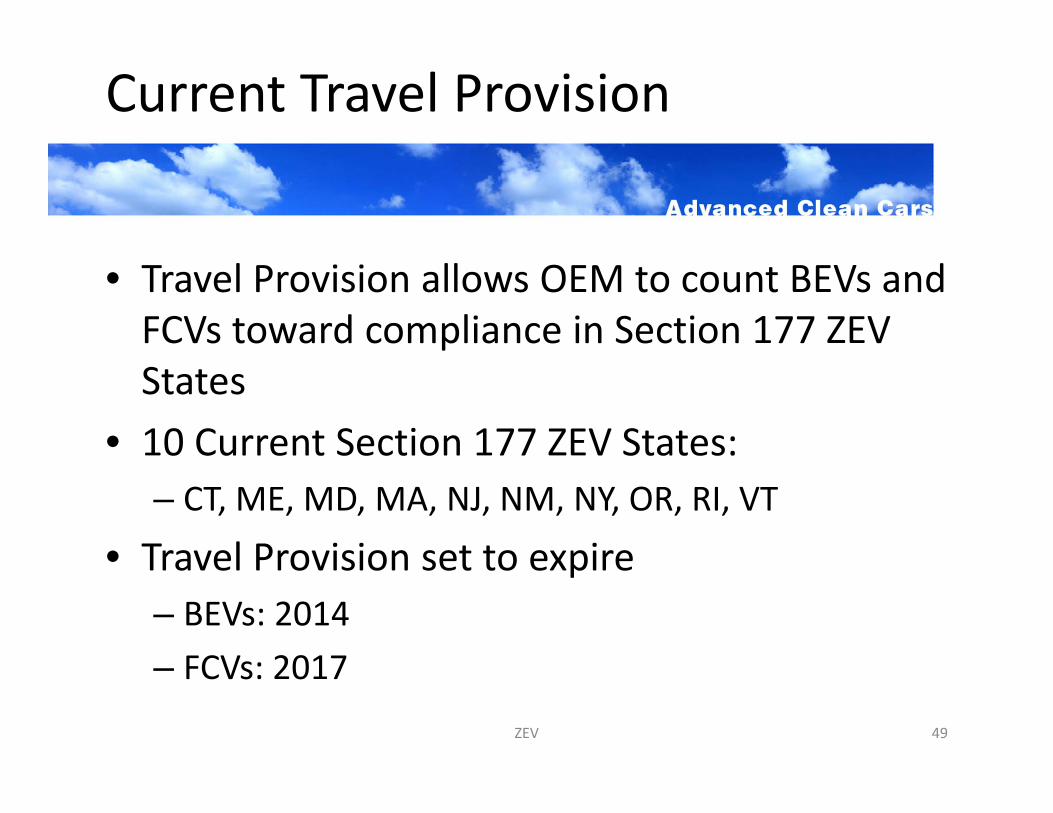

Current Travel Provision

• Travel Provision allows OEM to count BEVs and FCVs toward compliance in Section 177 ZEV States

• 10 Current Section 177 ZEV States:– CT, ME, MD, MA, NJ, NM, NY, OR, RI, VT

• Travel Provision set to expire– BEVs: 2014– FCVs: 2017

ZEV 49

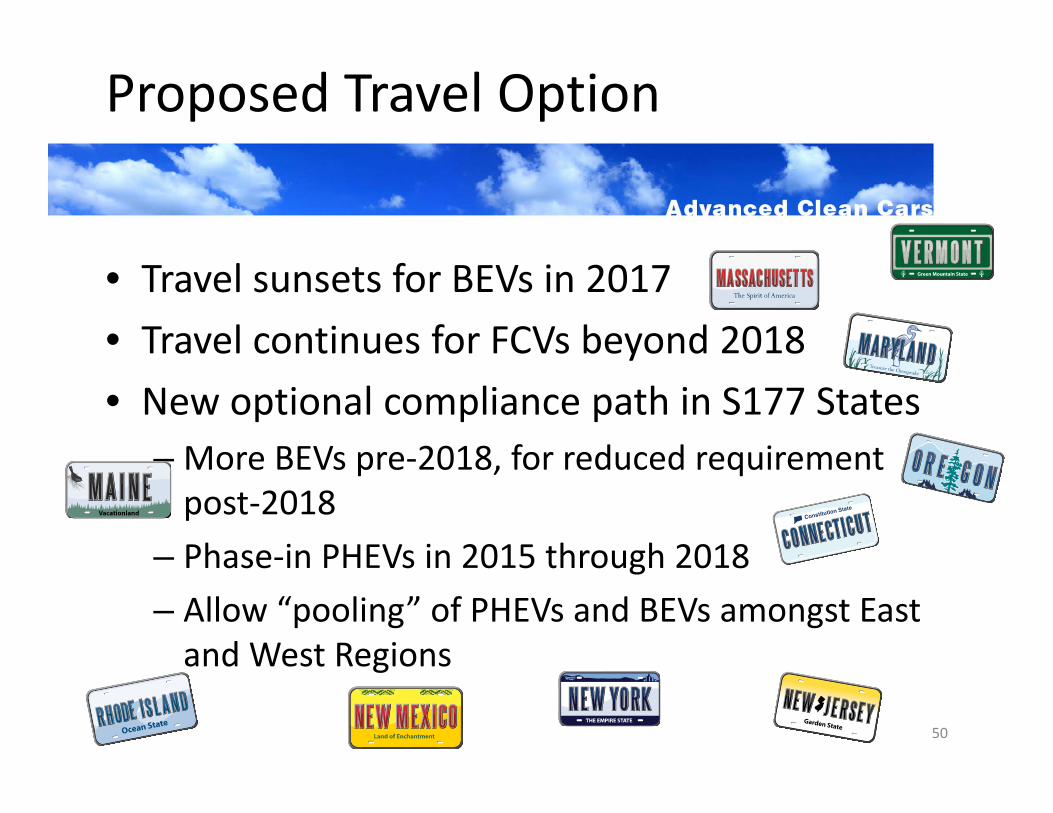

Proposed Travel Option

• Travel sunsets for BEVs in 2017• Travel continues for FCVs beyond 2018• New optional compliance path in S177 States

– More BEVs pre‐2018, for reduced requirement post‐2018

– Phase‐in PHEVs in 2015 through 2018– Allow “pooling” of PHEVs and BEVs amongst East and West Regions

50

Summary

• Focus the regulation on low‐carbon technologies

• Increase requirements to drive down costs and achieve commercialization

• Simplify and streamline regulatory requirements

51

CFO

52

ZEVZEV

CFOCFO

LEVLEV

CFO Background

• Adopted in 1990, revised in 2000

• Vehicle projections drive requirement to build outlets

• Updates needed to support ZEVs

Clean Fuels Outlet 53

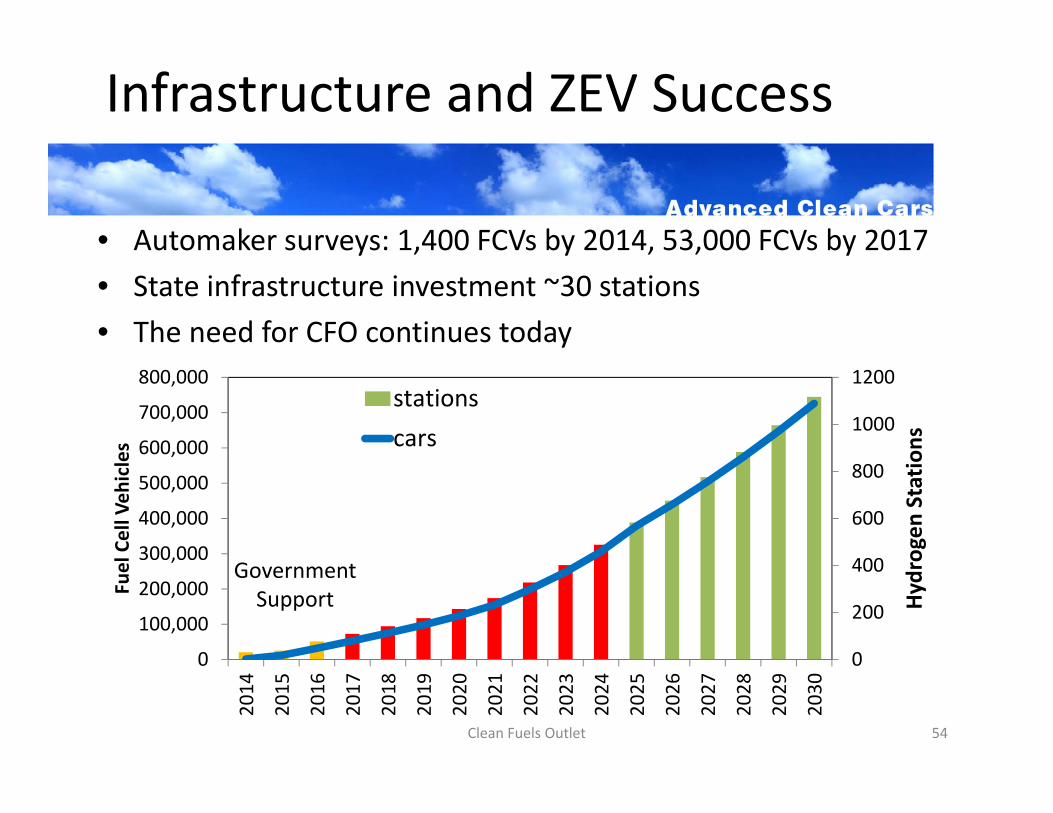

Infrastructure and ZEV Success

• Automaker surveys: 1,400 FCVs by 2014, 53,000 FCVs by 2017• State infrastructure investment ~30 stations• The need for CFO continues today

Clean Fuels Outlet 54

GovernmentSupport

0

200

400

600

800

1000

1200

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Hydrogen Stations

Fuel Cell Veh

icles

stationscars

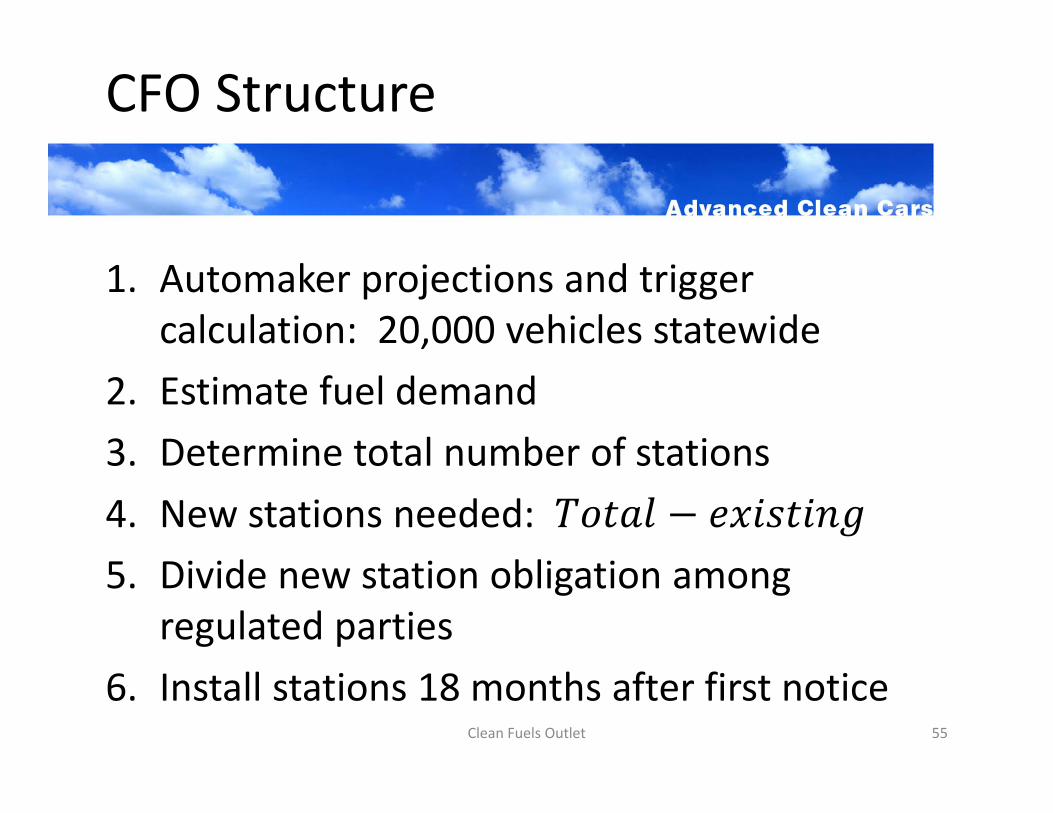

CFO Structure

1. Automaker projections and trigger calculation: 20,000 vehicles statewide

2. Estimate fuel demand3. Determine total number of stations4. New stations needed: 5. Divide new station obligation among

regulated parties6. Install stations 18 months after first notice

Clean Fuels Outlet 55

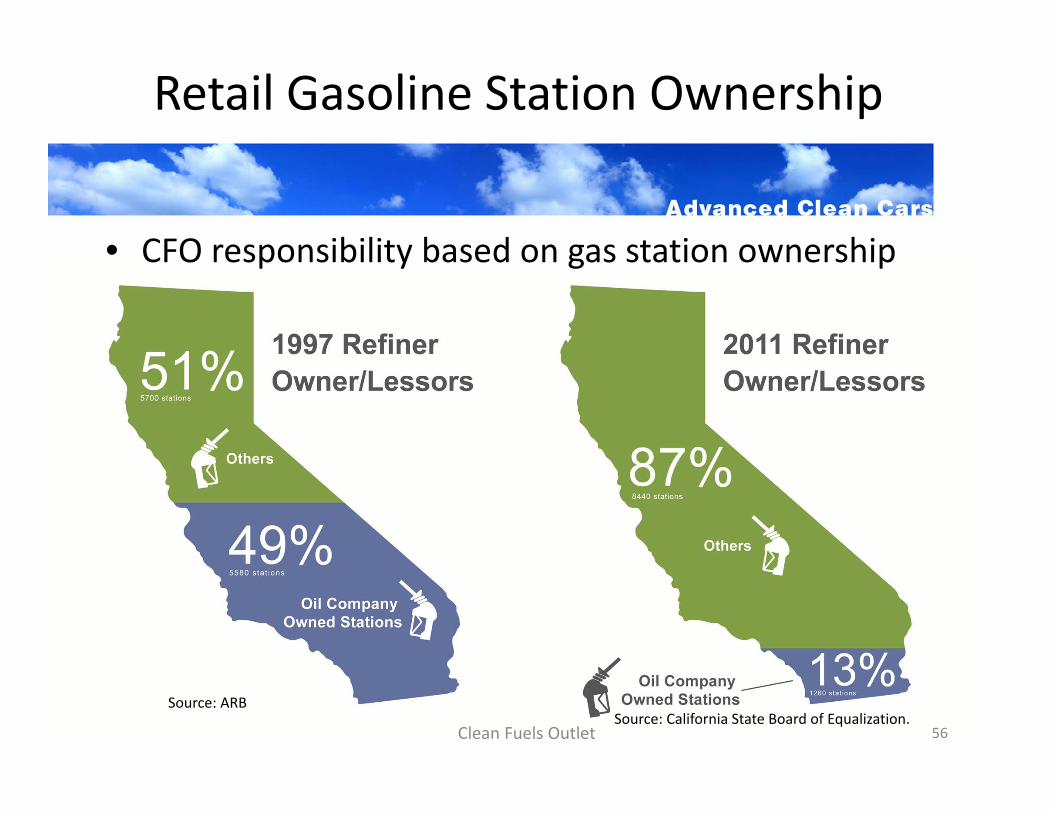

Retail Gasoline Station Ownership

• CFO responsibility based on gas station ownership

Clean Fuels Outlet 56

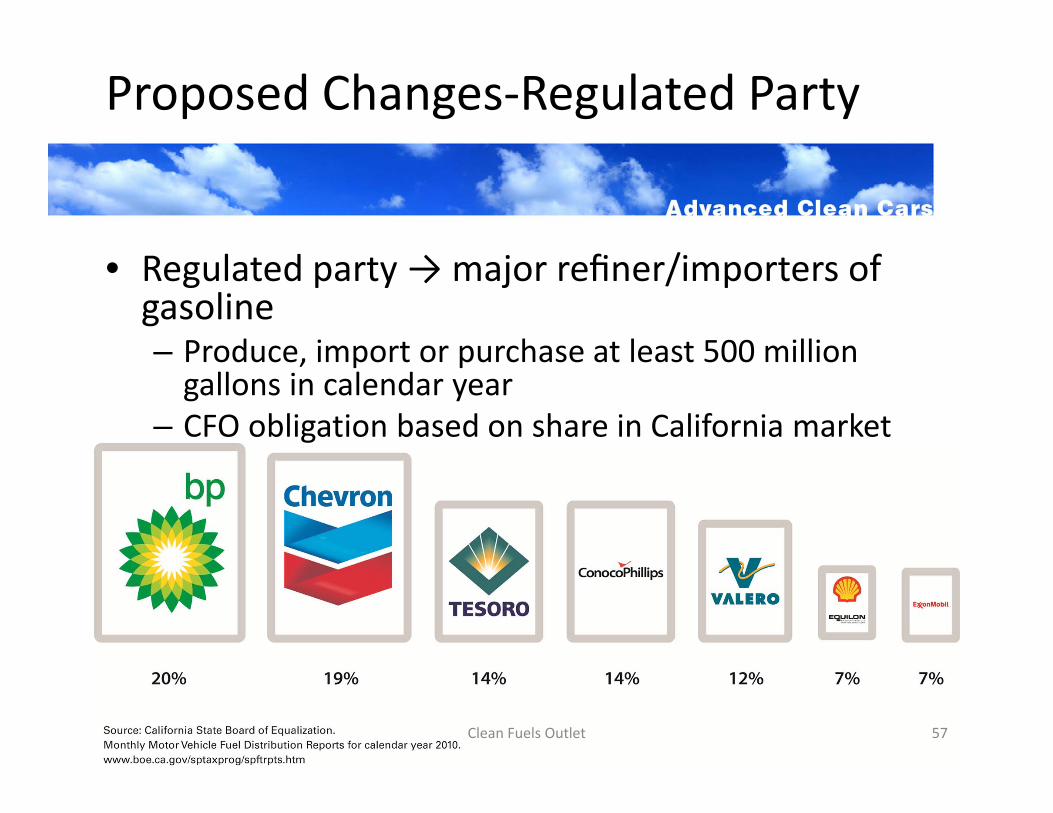

Source: ARBSource: California State Board of Equalization.

Proposed Changes‐Regulated Party

• Regulated party → major refiner/importers of gasoline– Produce, import or purchase at least 500 million gallons in calendar year

– CFO obligation based on share in California market

Clean Fuels Outlet 57

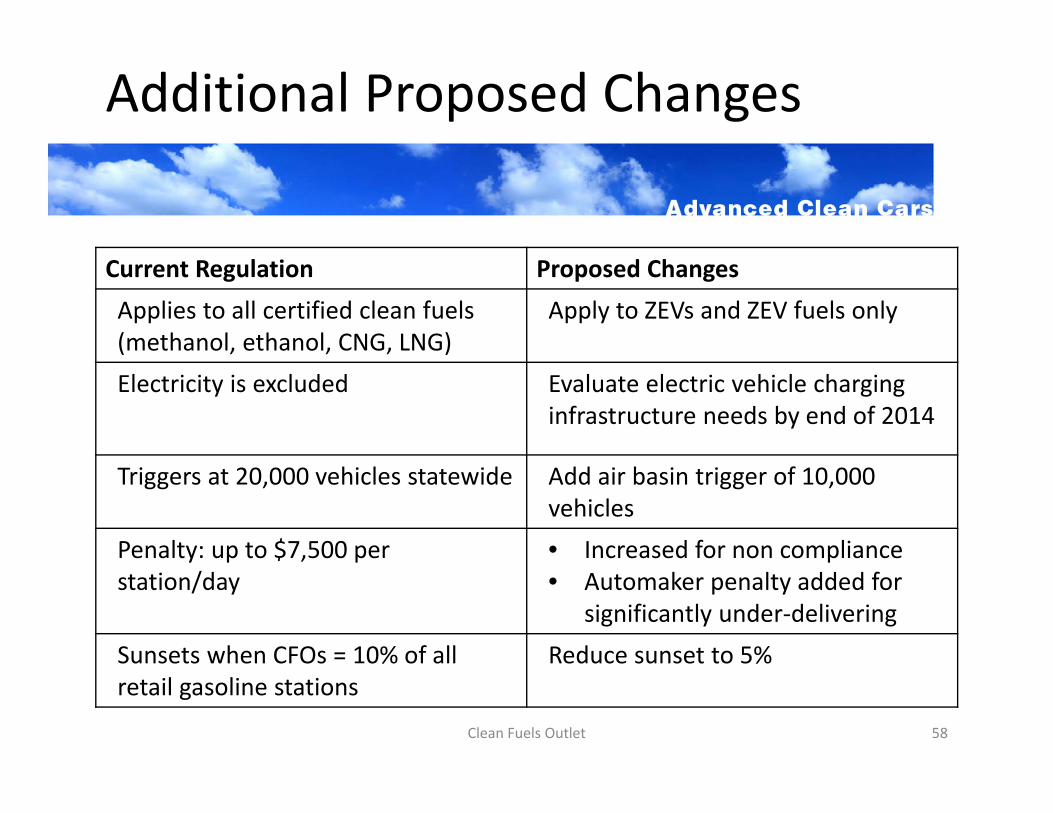

Additional Proposed Changes

Current Regulation Proposed ChangesApplies to all certified clean fuels (methanol, ethanol, CNG, LNG)

Apply to ZEVs and ZEV fuels only

Electricity is excluded Evaluate electric vehicle charging infrastructure needs by end of 2014

Triggers at 20,000 vehicles statewide Add air basin trigger of 10,000 vehicles

Penalty: up to $7,500 per station/day

• Increased for non compliance• Automaker penalty added for

significantly under‐deliveringSunsets when CFOs = 10% of all retail gasoline stations

Reduce sunset to 5%

Clean Fuels Outlet 58

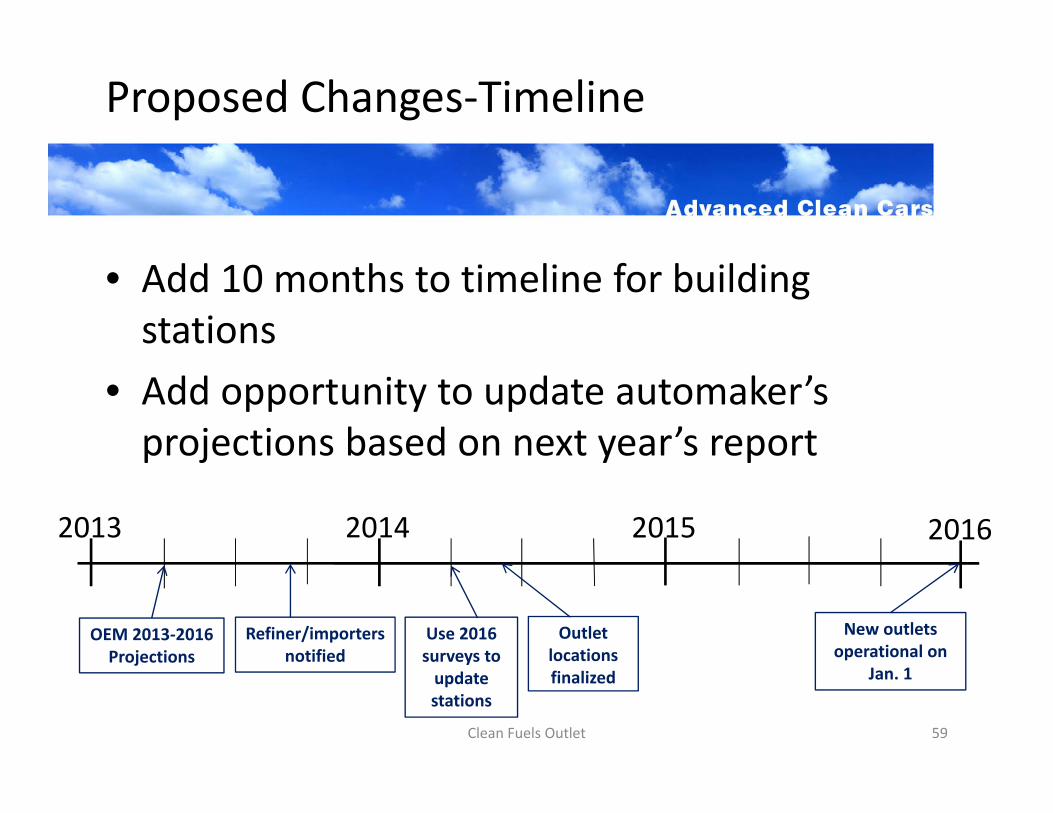

Proposed Changes‐Timeline

Clean Fuels Outlet 59

• Add 10 months to timeline for building stations

• Add opportunity to update automaker’s projections based on next year’s report

2013 2014 2015 2016

OEM 2013‐2016 Projections

Refiner/importers notified

Use 2016 surveys to update stations

Outlet locations finalized

New outlets operational on

Jan. 1

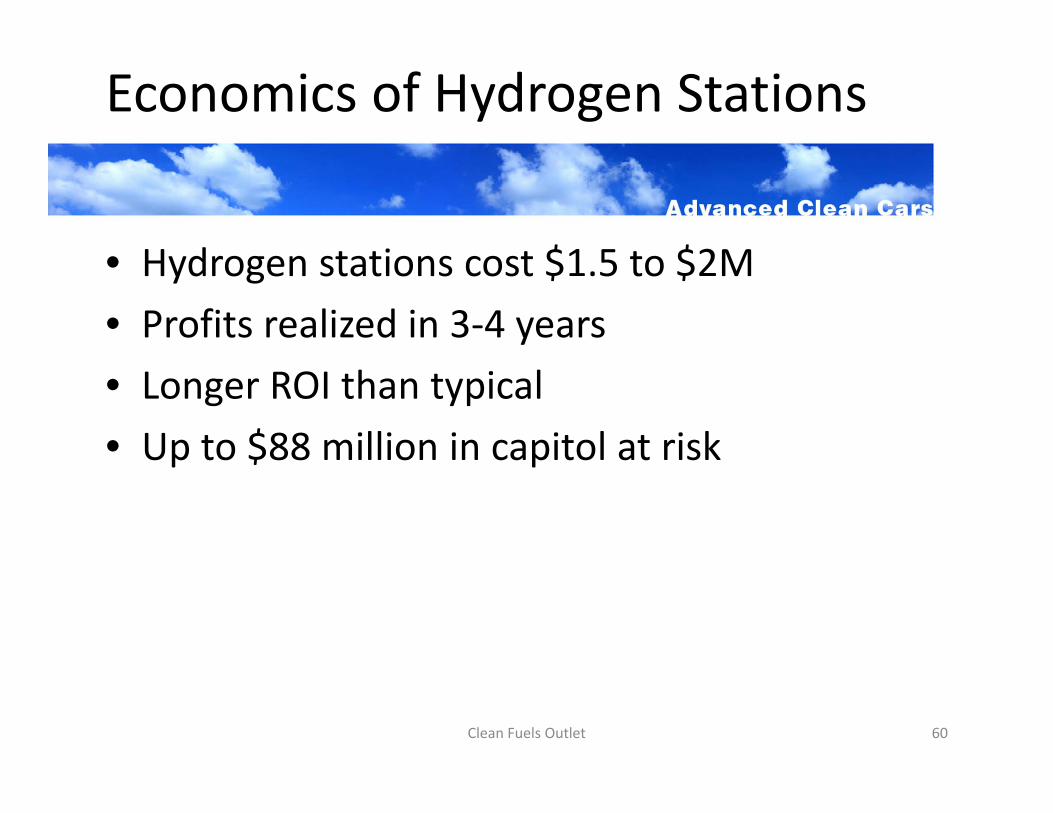

Economics of Hydrogen Stations

• Hydrogen stations cost $1.5 to $2M• Profits realized in 3‐4 years• Longer ROI than typical• Up to $88 million in capitol at risk

Clean Fuels Outlet 60

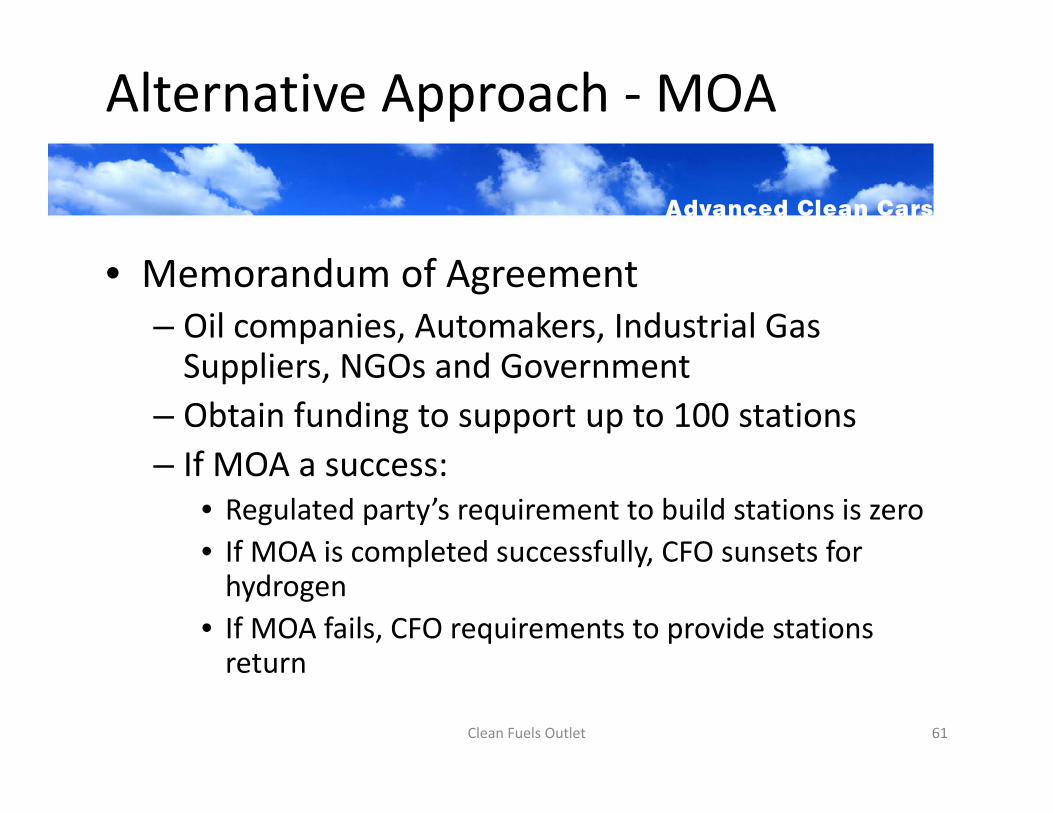

Alternative Approach ‐MOA

• Memorandum of Agreement – Oil companies, Automakers, Industrial Gas Suppliers, NGOs and Government

– Obtain funding to support up to 100 stations– If MOA a success:

• Regulated party’s requirement to build stations is zero• If MOA is completed successfully, CFO sunsets for hydrogen

• If MOA fails, CFO requirements to provide stations return

Clean Fuels Outlet 61

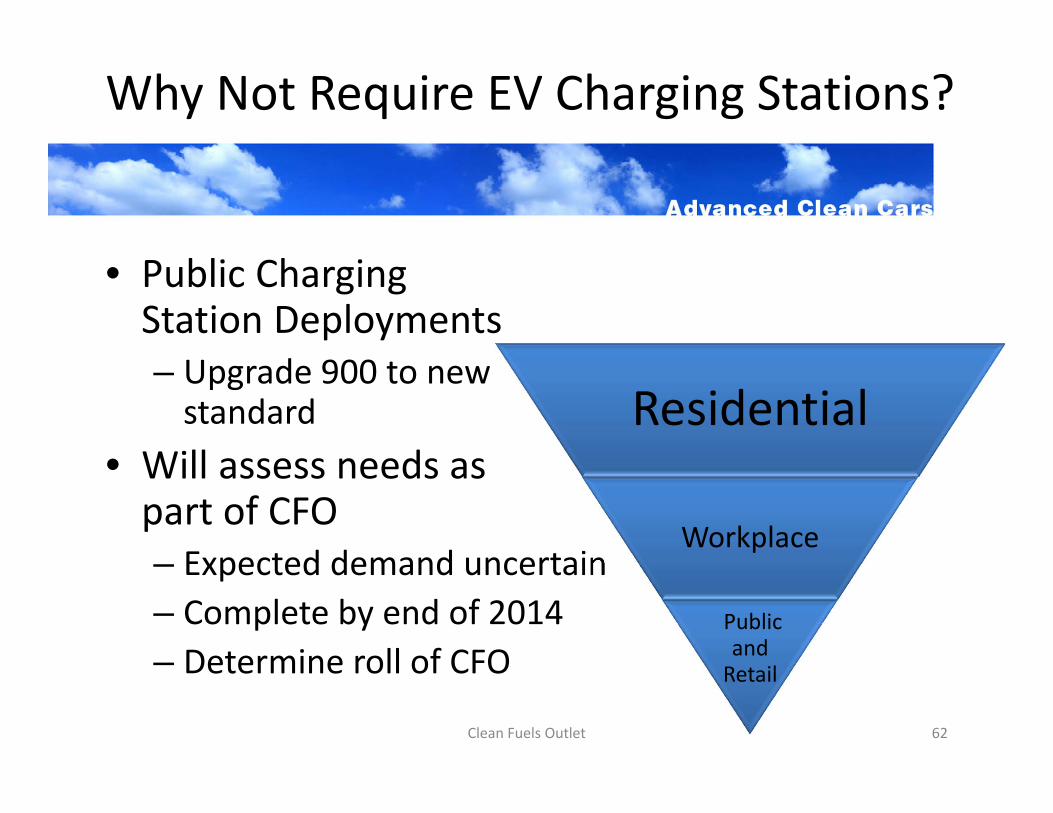

Why Not Require EV Charging Stations?

• Public Charging Station Deployments– Upgrade 900 to new standard

• Will assess needs as part of CFO– Expected demand uncertain– Complete by end of 2014– Determine roll of CFO

Clean Fuels Outlet 62

Residential

Workplace

PublicandRetail

Summary

• Hydrogen fueling stations are needed to commercialize ZEVs

• CFO amendments necessary to bridge gap between funded and self‐sustaining

• MOA may provide a collaborative approach to ensuring hydrogen stations

Clean Fuels Outlet 63

Overall Economic Impacts of ACC Program

Clean Fuels Outlet 64

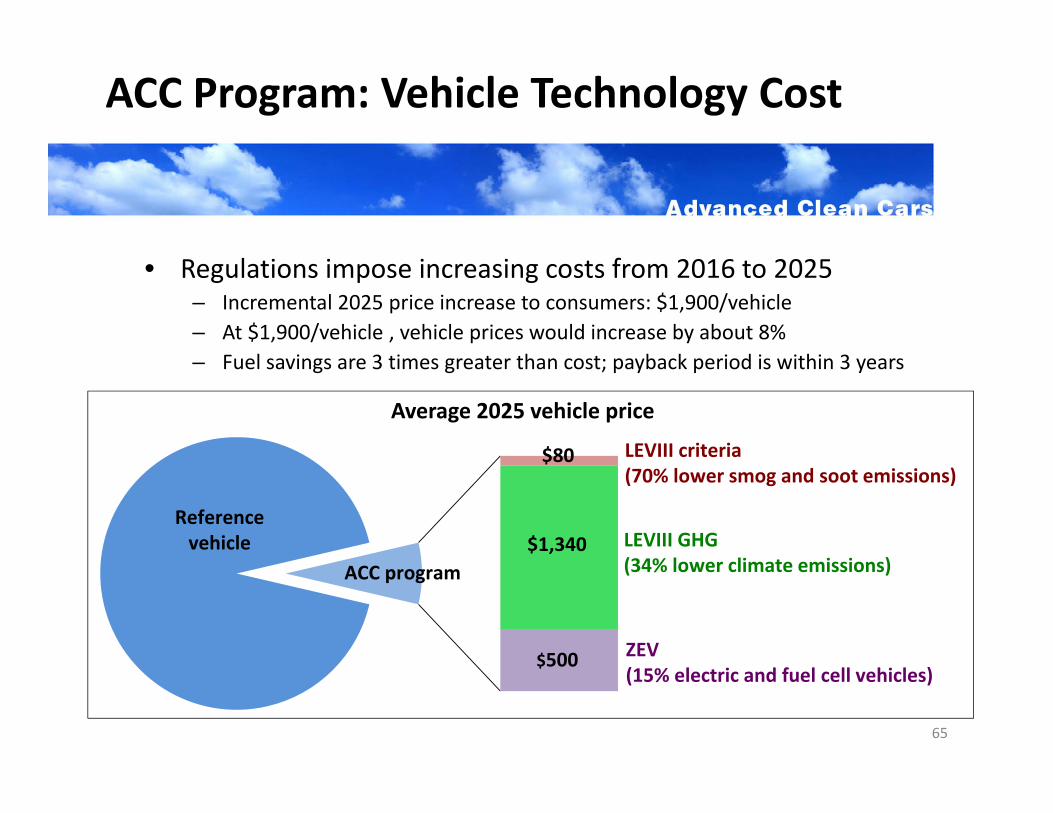

65

ACC Program: Vehicle Technology Cost

• Regulations impose increasing costs from 2016 to 2025– Incremental 2025 price increase to consumers: $1,900/vehicle– At $1,900/vehicle , vehicle prices would increase by about 8%– Fuel savings are 3 times greater than cost; payback period is within 3 years

ACC program

LEVIII criteria(70% lower smog and soot emissions)

$80

$1,340

$500

LEVIII GHG(34% lower climate emissions)

ZEV(15% electric and fuel cell vehicles)

Referencevehicle

Average 2025 vehicle price

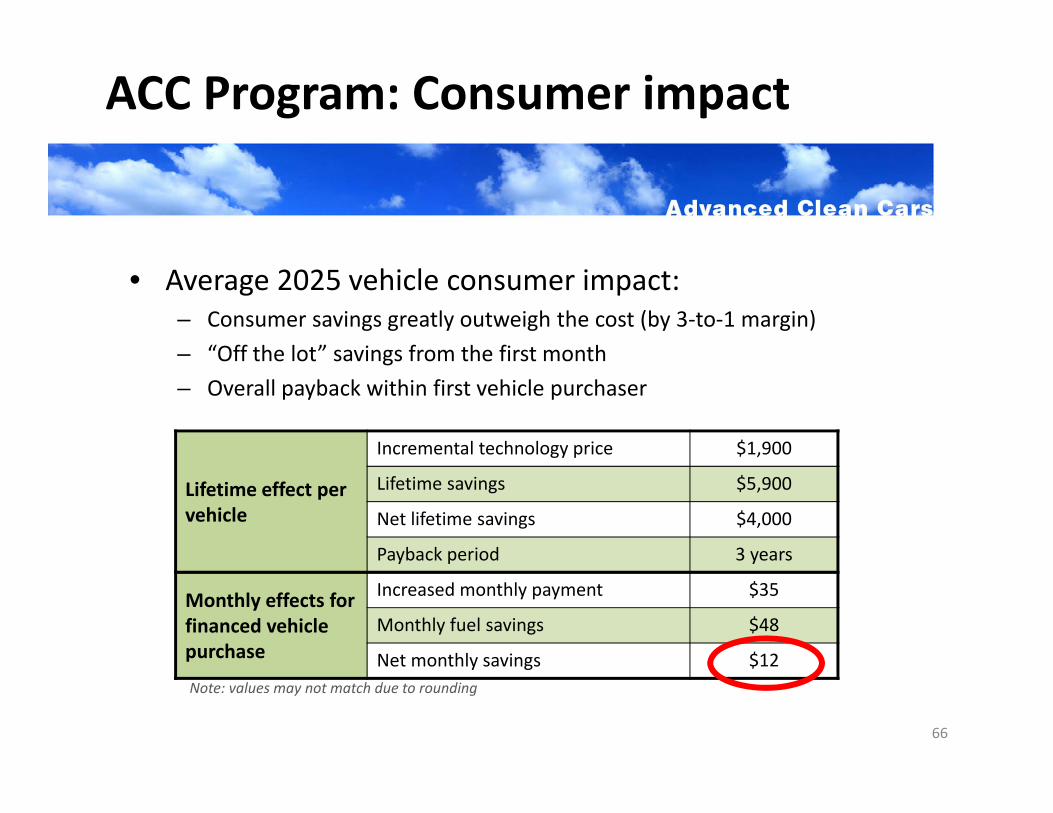

66

ACC Program: Consumer impact

• Average 2025 vehicle consumer impact:– Consumer savings greatly outweigh the cost (by 3‐to‐1 margin)– “Off the lot” savings from the first month– Overall payback within first vehicle purchaser

Lifetime effect per vehicle

Incremental technology price $1,900

Lifetime savings $5,900

Net lifetime savings $4,000

Payback period 3 years

Monthly effects for financed vehicle purchase

Increased monthly payment $35

Monthly fuel savings $48

Net monthly savings $12Note: values may not match due to rounding

67

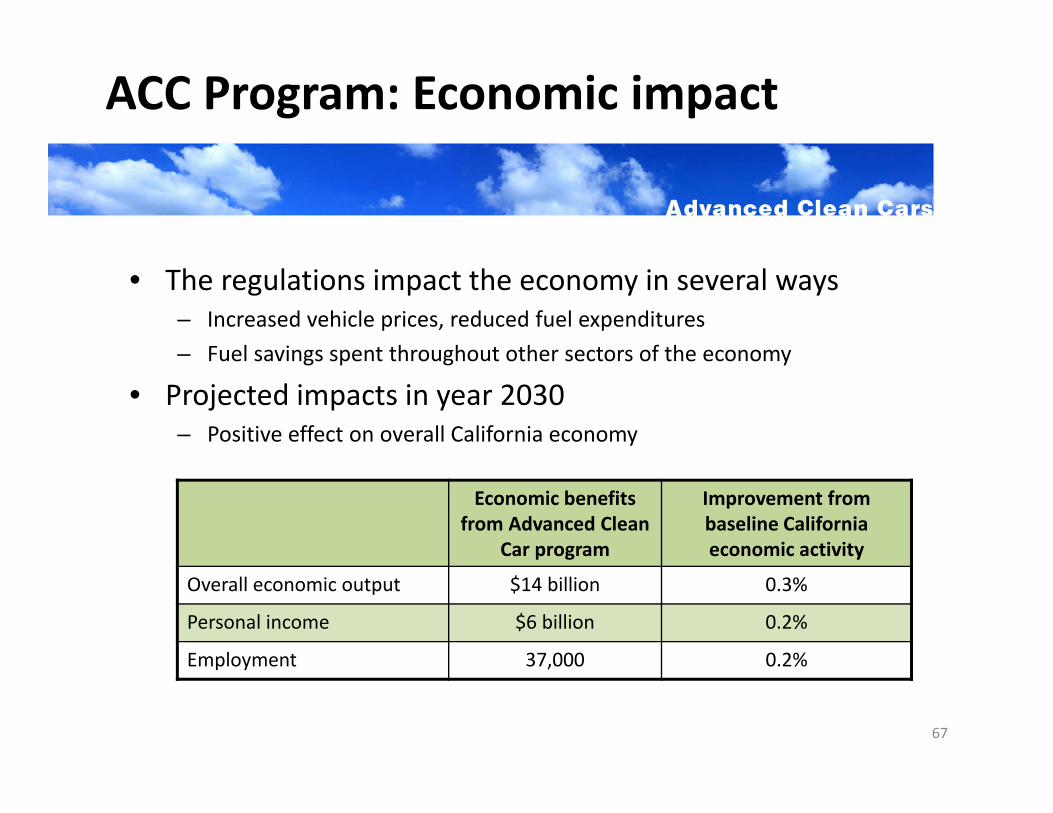

ACC Program: Economic impact

• The regulations impact the economy in several ways– Increased vehicle prices, reduced fuel expenditures– Fuel savings spent throughout other sectors of the economy

• Projected impacts in year 2030– Positive effect on overall California economy

Economic benefits from Advanced Clean

Car program

Improvement from baseline California economic activity

Overall economic output $14 billion 0.3%

Personal income $6 billion 0.2%

Employment 37,000 0.2%