public disclosure authorized report no: aus1511...

TRANSCRIPT

Report No: AUS1511

Republic of the Philippines

Strategy Update and Implementation Plan

Developing the Institutional Framework for the Water Supply and Sanitation Sector and Identifying Investment Plans & Programs

May 2013

EASPS

EAST ASIA AND PACIFIC

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Standard Disclaimer:

This volume is a product of the staff of the International Bank for Reconstruction and Development/ The World Bank. The findings, interpretations, and conclusions expressed in this paper do not necessarily reflect the views of the Executive Directors of The World Bank or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

Copyright Statement:

The material in this publication is copyrighted. Copying and/or transmitting portions or all of this work

without permission may be a violation of applicable law. The International Bank for Reconstruction and

Development/ The World Bank encourages dissemination of its work and will normally grant permission to

reproduce portions of the work promptly.

For permission to photocopy or reprint any part of this work, please send a request with complete

information to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, USA,

telephone 978-750-8400, fax 978-750-4470, http://www.copyright.com/.

All other queries on rights and licenses, including subsidiary rights, should be addressed to the Office of the

Publisher, The World Bank, 1818 H Street NW, Washington, DC 20433, USA, fax 202-522-2422, e-mail

Developing the Institutional Framework for the

Water Supply and Sanitation Sector and

Identifying Investment Plans & Programs

FINAL REPORT

MAY 2013

LIST OF ACRONYMS

ADB Asian Development Bank APIS Annual Poverty Indicator Surveys BWSA Barangay Water and Sanitation Association CAPEX Capital Expenditures CBO Community Based Organization CDA Cooperative Development Authority CIPH City-wide Investment Plan for Health CPC Certificate of Public Convenience CWA Clean Water Act DAR Department of Agrarian Reform DBM Department of Budget and Management DENR Department of Environment and Natural Resources DILG Department of the Interior and Local Government DOE Department of Energy DOF Department of Finance DOH Department of Health DPWH Department of Public Works and Highways EMB Environmental Management Bureau EO Executive Order FHSIS Field Health Services Information System FOREX Foreign Exchange GFI Government Financial Institutions GOP Government of the Philippines HHs Households HUC Highly Urbanized City IBRD International Bank for Rehabilitation and Development (World Bank) JMP Joint Monitoring Program KPI Key Performance Indicators LGU Local Government Units lps liters per second LWUA Local Water Utilities Administration MDG Millennium Development Goal MDGF Millennium Development Goal Fund MDFO Municipal Development Fund Office MDS Monthly Data Sheet MIPH Municipal-wide Investment Plan for Health mm millimeter MTPDP Medium Term Philippine Development Plan MWCI Manila Water Company, Inc. MWSI Maynilad Water Services, Inc. MWSS Metropolitan Waterworks and Sewerage System NAPC-WASCO National Anti-Poverty Commission-Water Supply Coordination Office NEDA National Economic and Development Authority NG National Government

NGO Non-Government Organizations NSSMP National Sewerage and Septage Management Programs NRW Non-Revenue Water NSO National Statistics Office

NWRB National Water Resources Board NWRMO National Water Resources Management Office OBA Output-Based Aid OP Office of the President OPEX Operational Expenditures PD Presidential Decree PIPH Province-wide Investment Plan for health PMO Project Management Office PNSDW Philippine National Standards for Drinking Water PPP Public-Private Partnership PSA Philippine Sanitation Alliance PSP Private Sector Participation PWSSR Philippine Water Supply and Sanitation Roadmap PSSR Philippine Sustainable Sanitation Roadmap R.A. Republic Act RO Regulatory Office RORB Return on Rate Base RWSA Rural water and Sanitation Association SBWRB Subic Bay Water Regulatory Board

SC Supreme Court

SEC Securities and Exchange Commission

TA Technical Assistance ToR Terms of Reference TWG Technical Working Group WB World Bank WD Water District WEDC Water, Engineering Development Center WHO/UNICEF World World Health organization/United Nation International Children

Emergency Fund WRC Water Water Regulatory Commission WSP Water Water Service Provider WSS Water Water Supply and Sanitation

TABLE OF CONTENTS

Page

EXECUTIVE SUMMARY 1 - 8

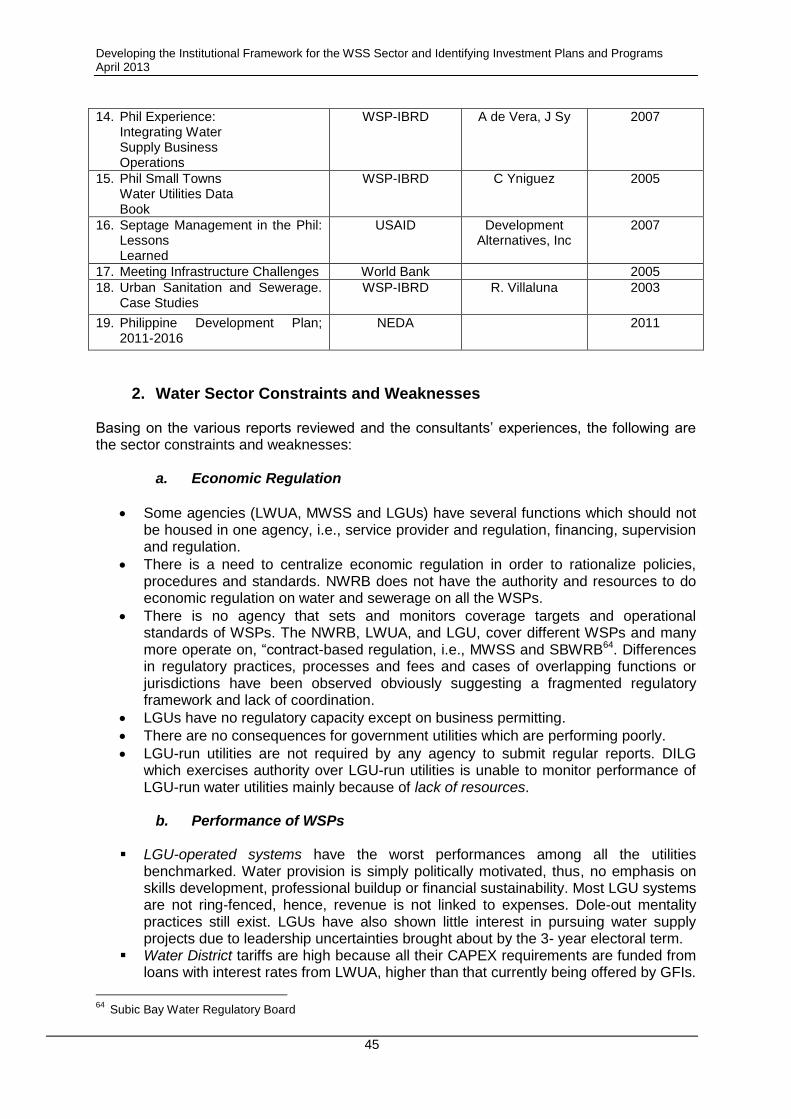

A INTRODUCTION 9 1. Background 9 2. Terms of Reference (TOR) 10 3. Methodology/Approach 10 4. Study Limitations 10 B. SECTOR ASSESSMENT 12 1. The Water and Sanitation Sector Overview 12 2. Water Supply Coverage 15

3. Millennium Development Goals: WS Targets 18 4. Public Health and Sanitation 19 5. WSS Sector Issues and Challenges 23 C. DEMAND GAP ANALYSIS 26 1. Population Projections 26 2. Served Population, 2011 28 3. Number of WSPs, 2011 32 4. LGUs with Septage and Sewerage facilities 32 5. Target Setting Basis 32 6. Target Summary 35 D. INVESTMENT REQUIREMENTS 37 1. Basic Formula 37 2. Basis for Infrastructure Cost Estimates 37 3. Unit Cost Estimates 38 4. Infrastructure Investment Requirements 40 5. Capacity Building Requirements 42 6. Fund Sourcing 43 E. INSTITUTIONAL RECOMMENDATIONS 44 1. Review of Sector Assessment Reports 44 2. Water Sector Constraints and Weaknesses 45 3. Sanitation Sector Constraints and Weaknesses 47 4. WSS Constraints Summary 48 5. Major Recommendations of Various WSS Studies 48 6. Institutional Recommendations 52 7. Structural Recommendations for DPWH 56 8. Infrastructure Programs 56

F. ACTION PLANNING FOR THE DPWH 61 1. The DPWH 61 2. DPWH WSS Sector Role 61

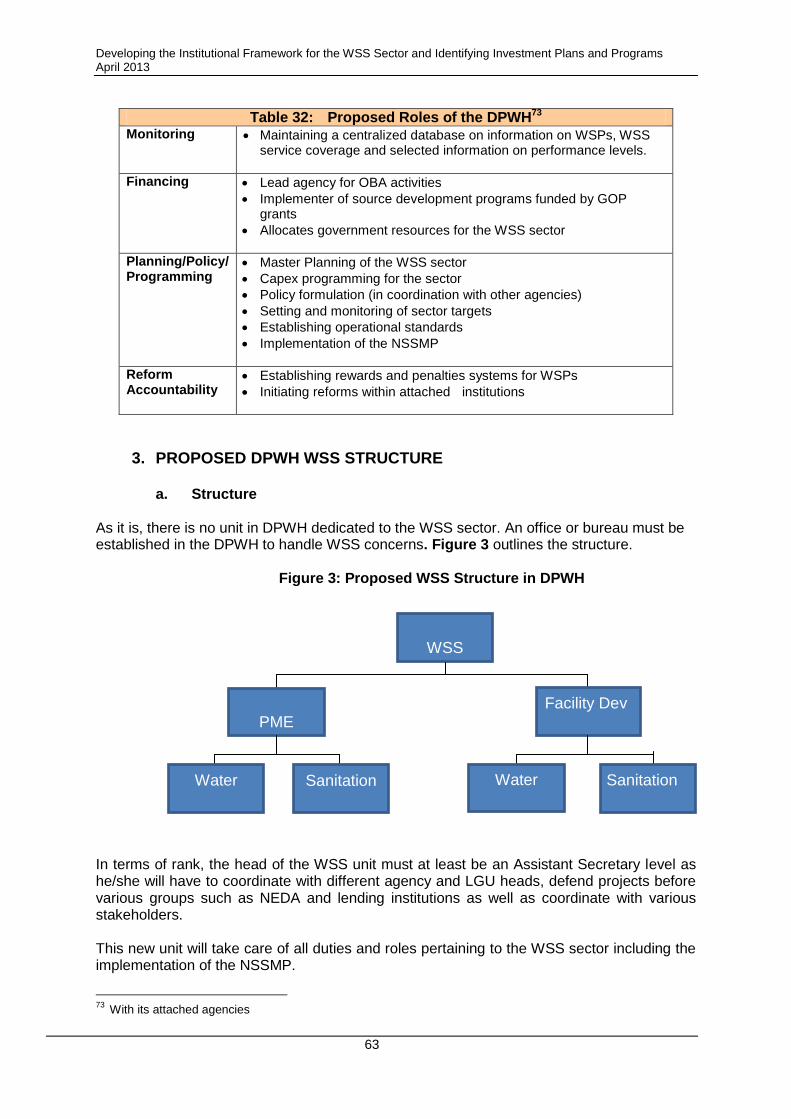

3. Proposed DPWH WSS Structure 63 4. Action Plans 64

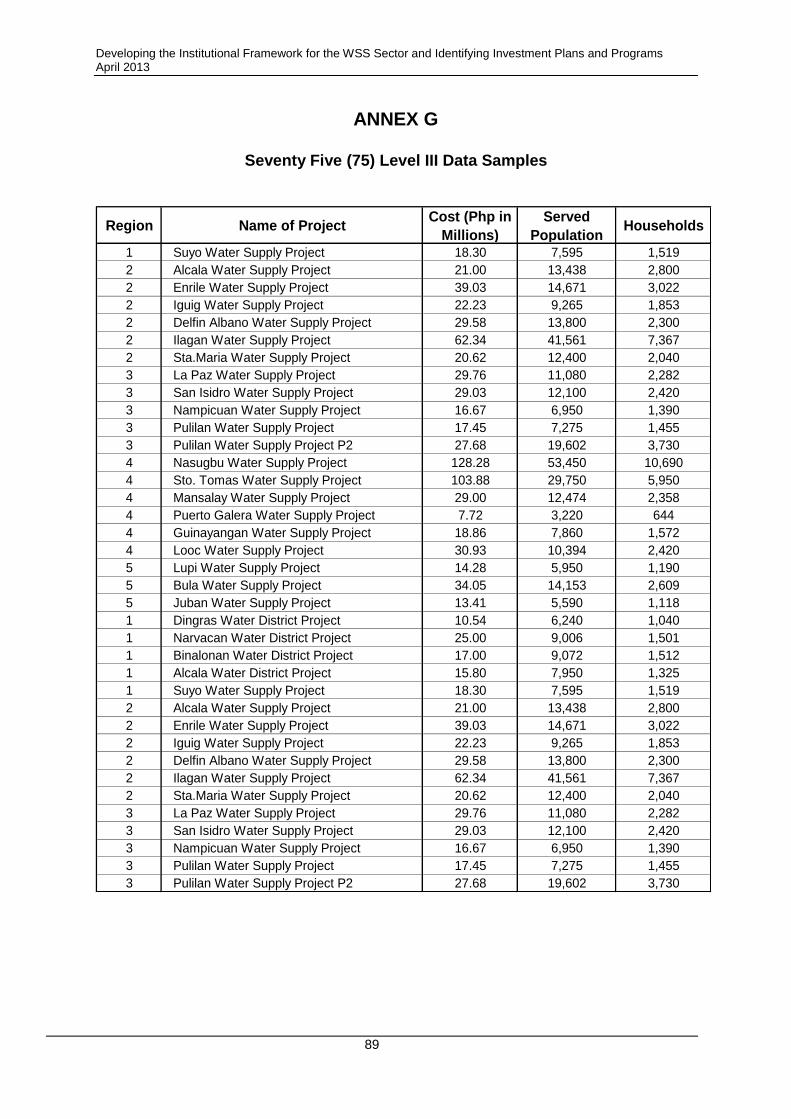

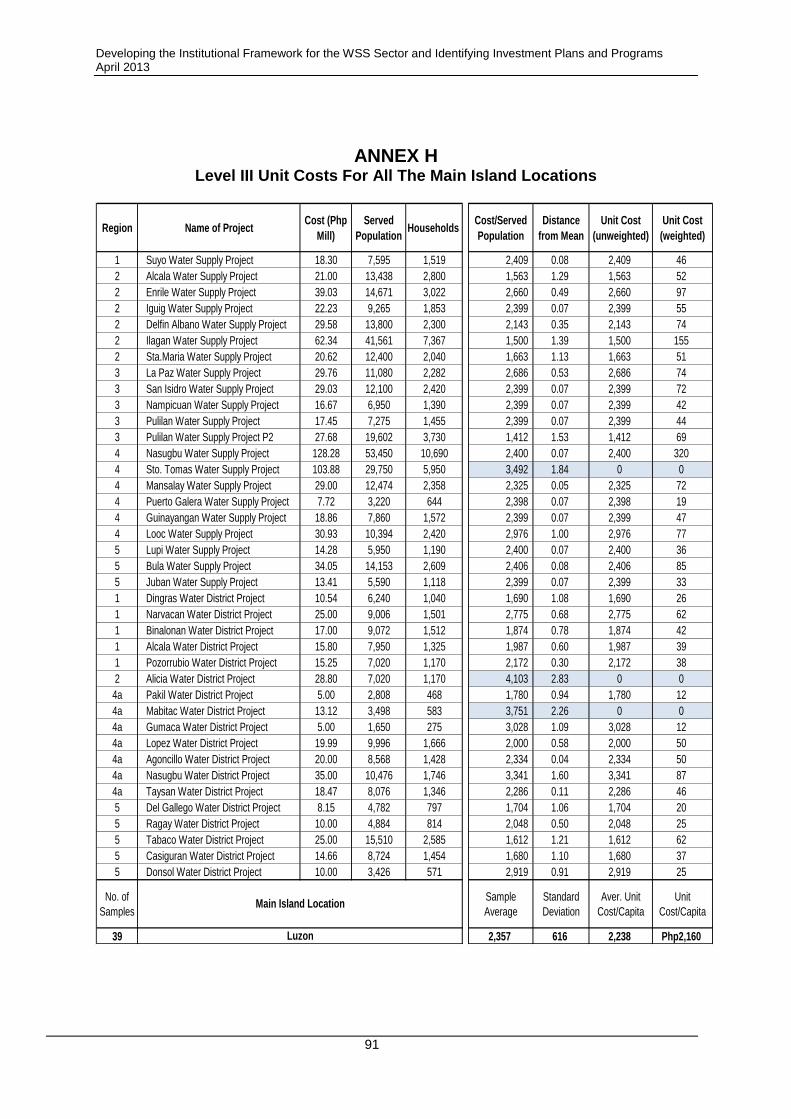

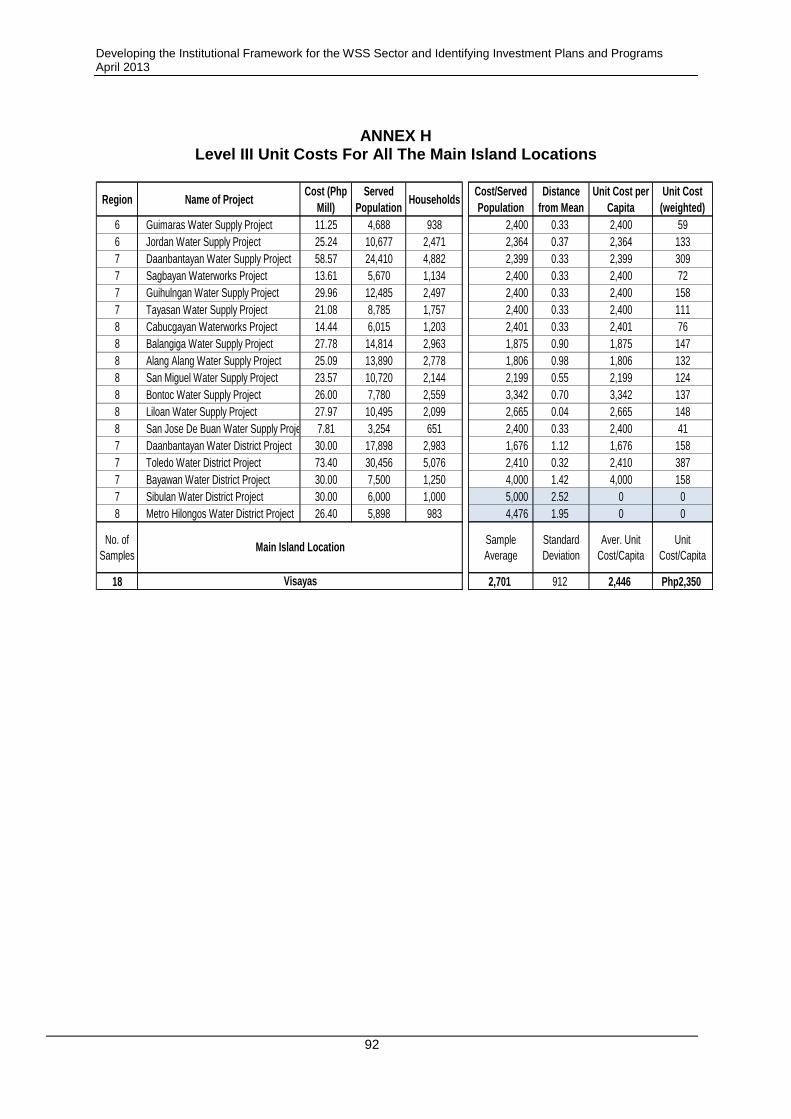

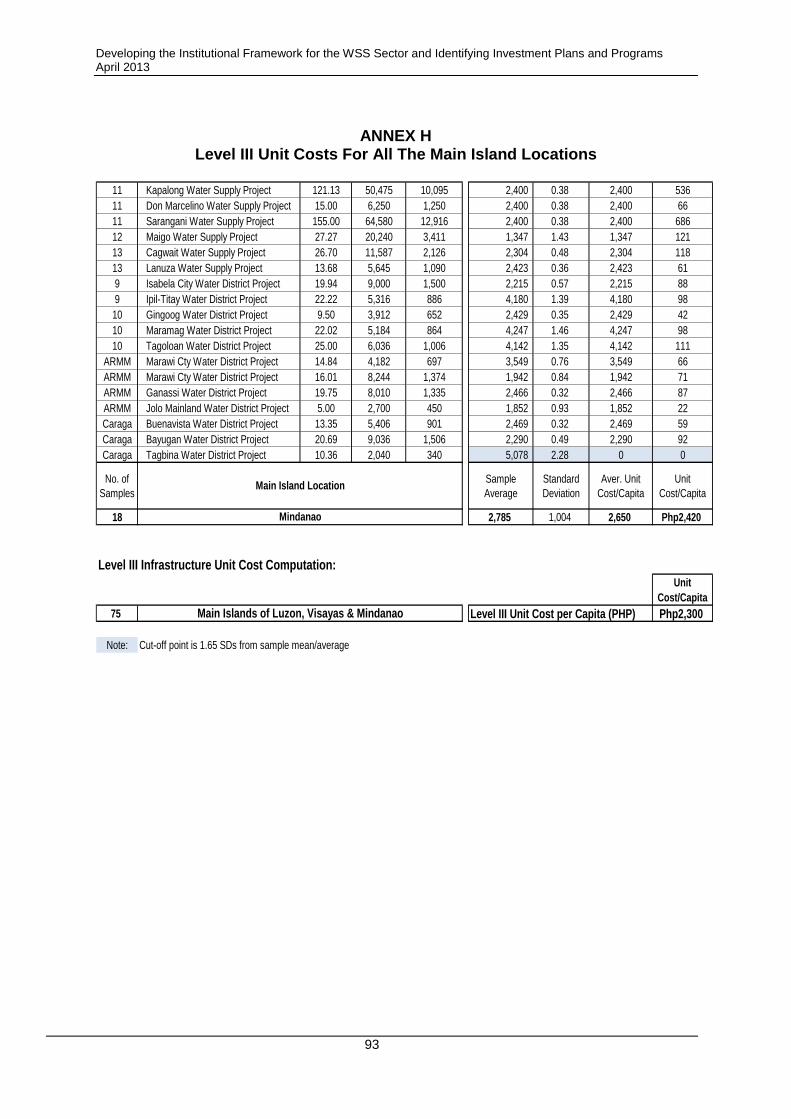

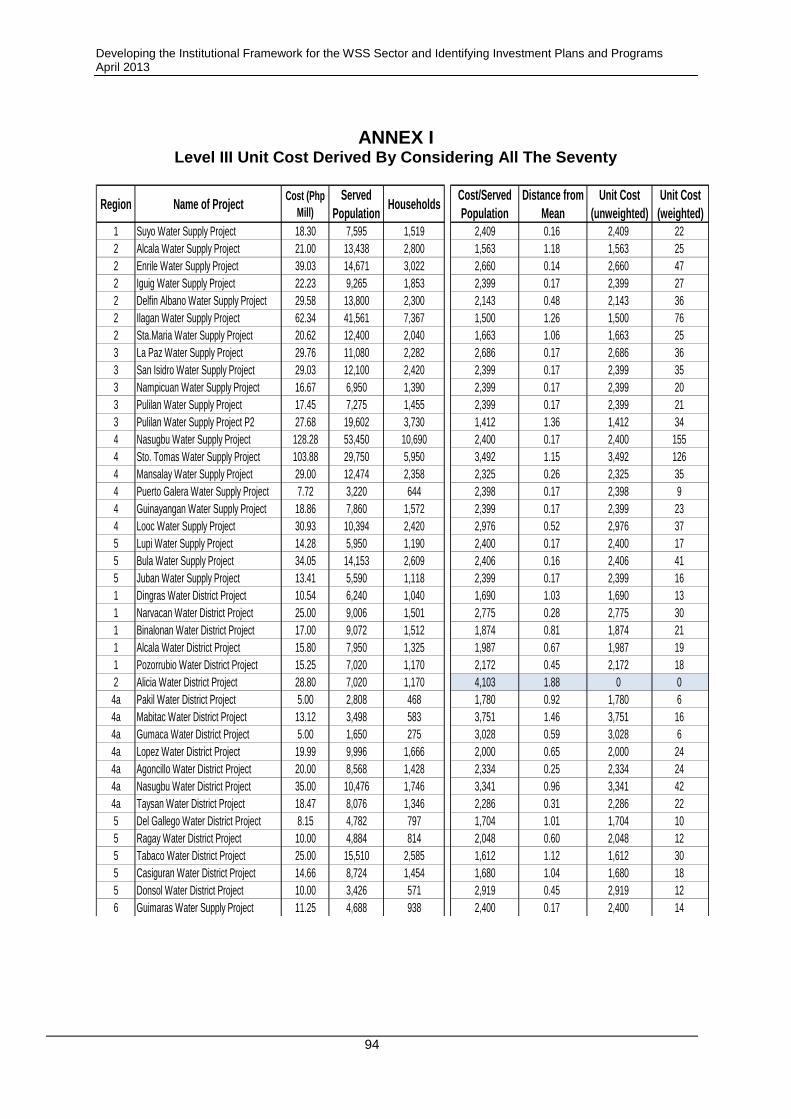

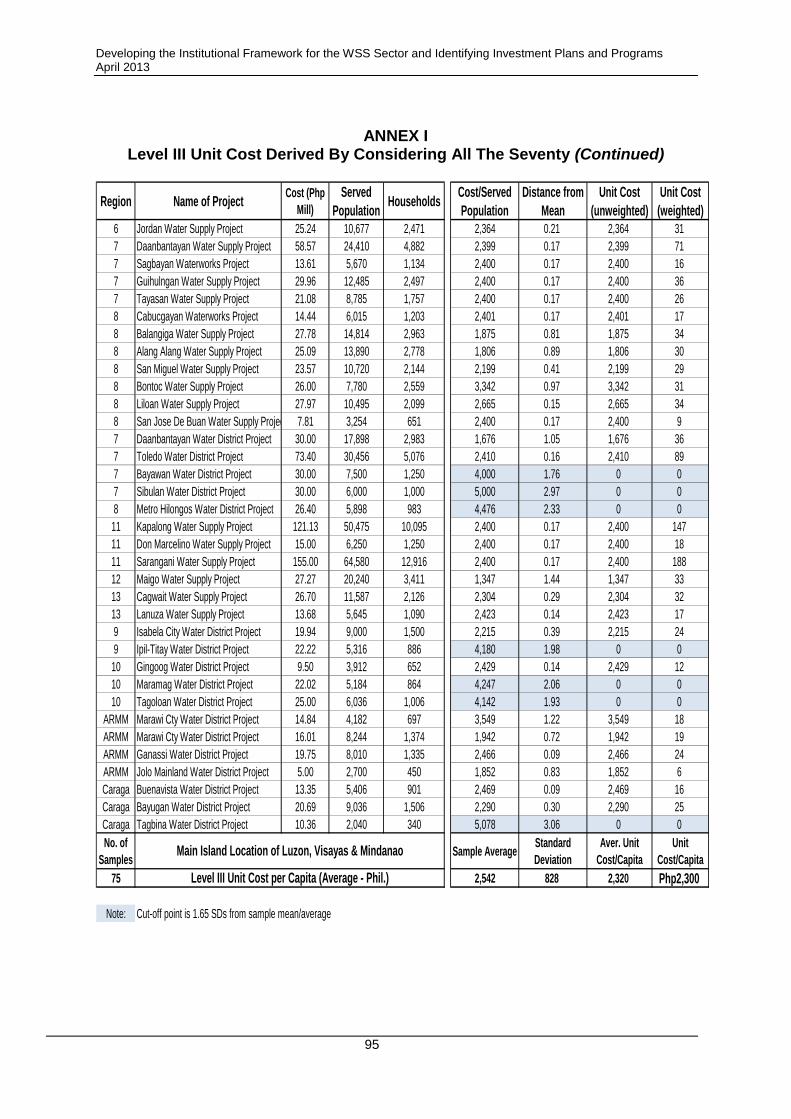

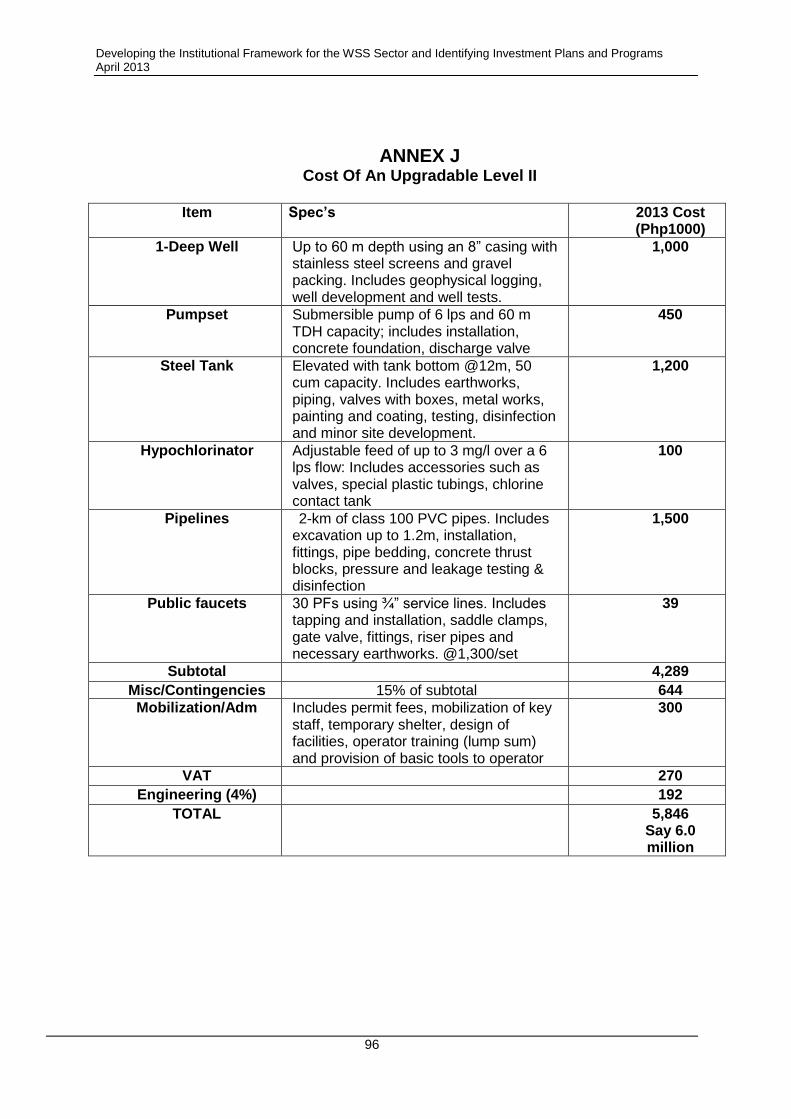

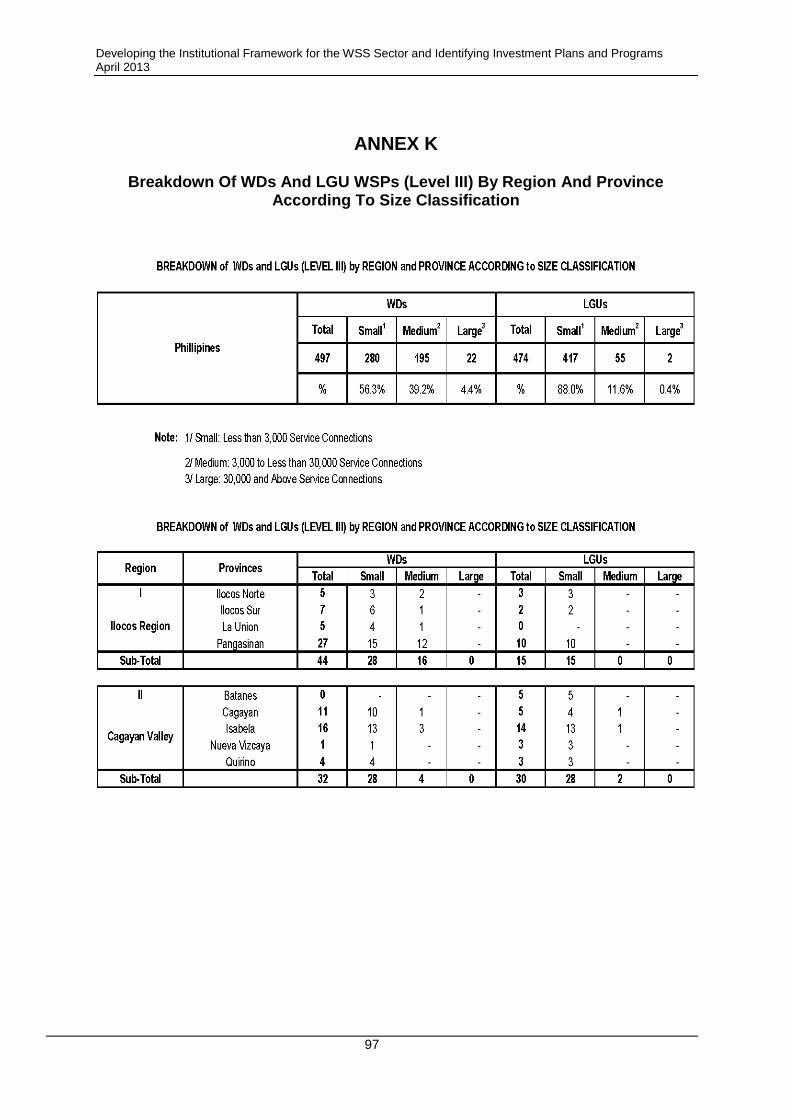

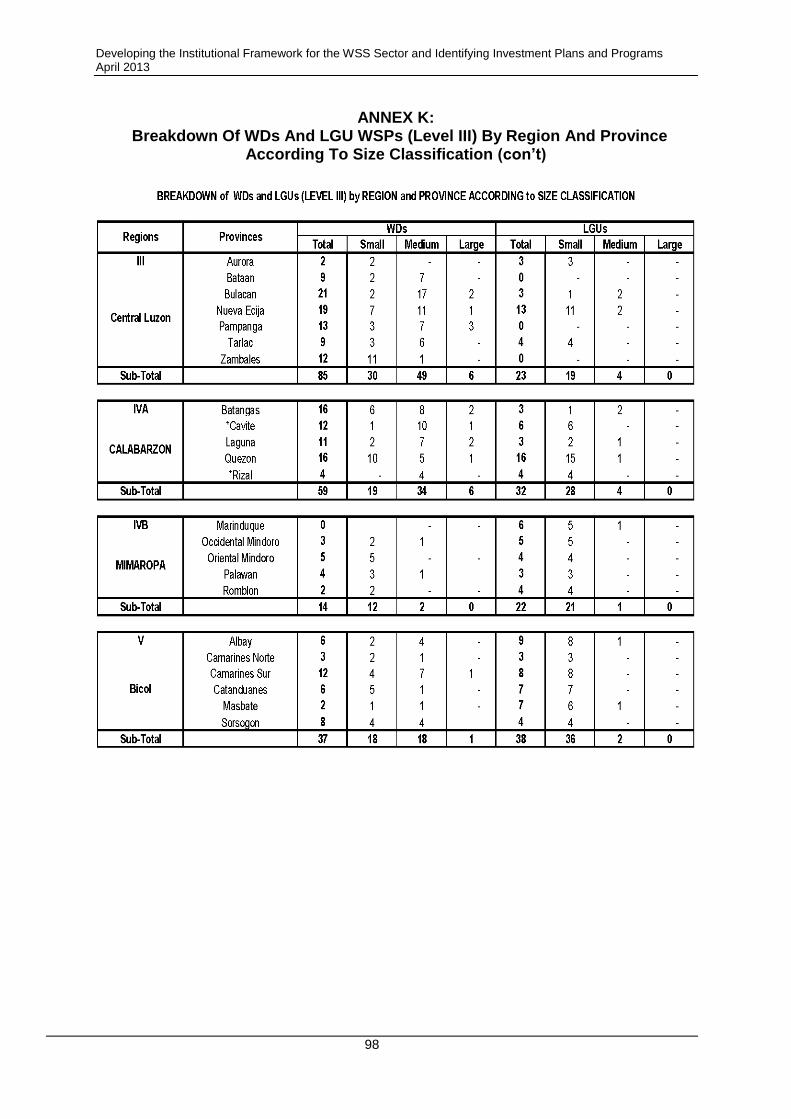

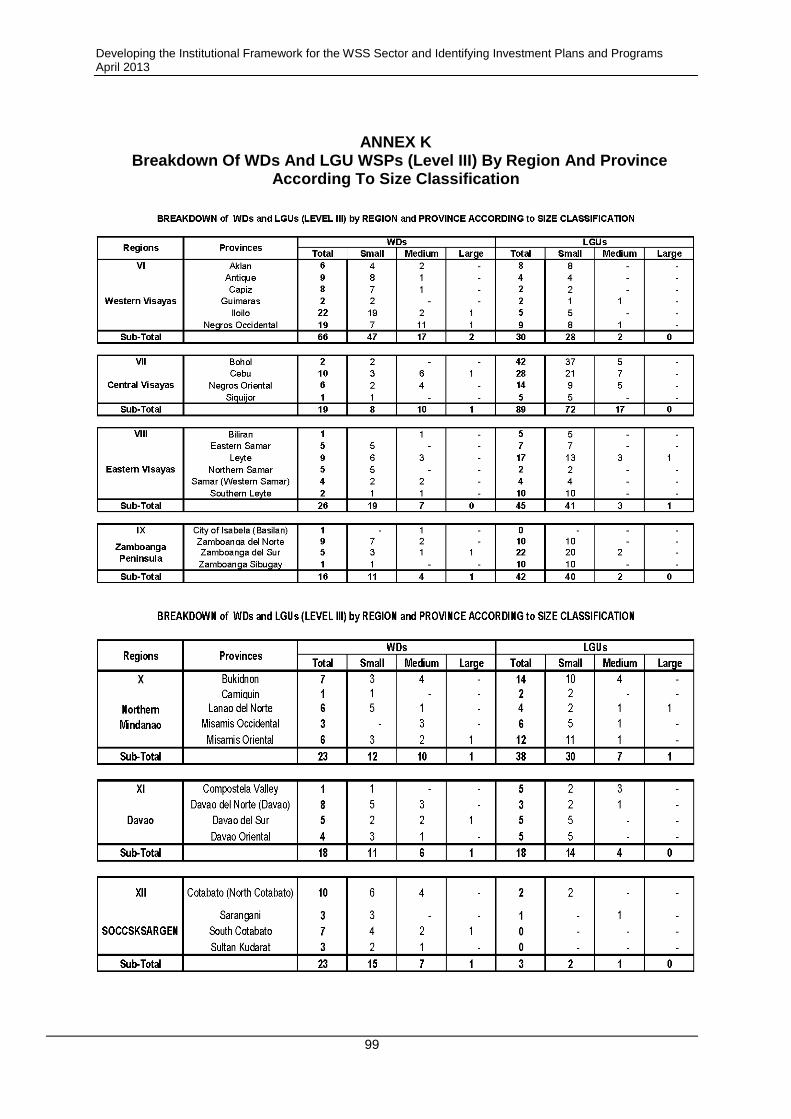

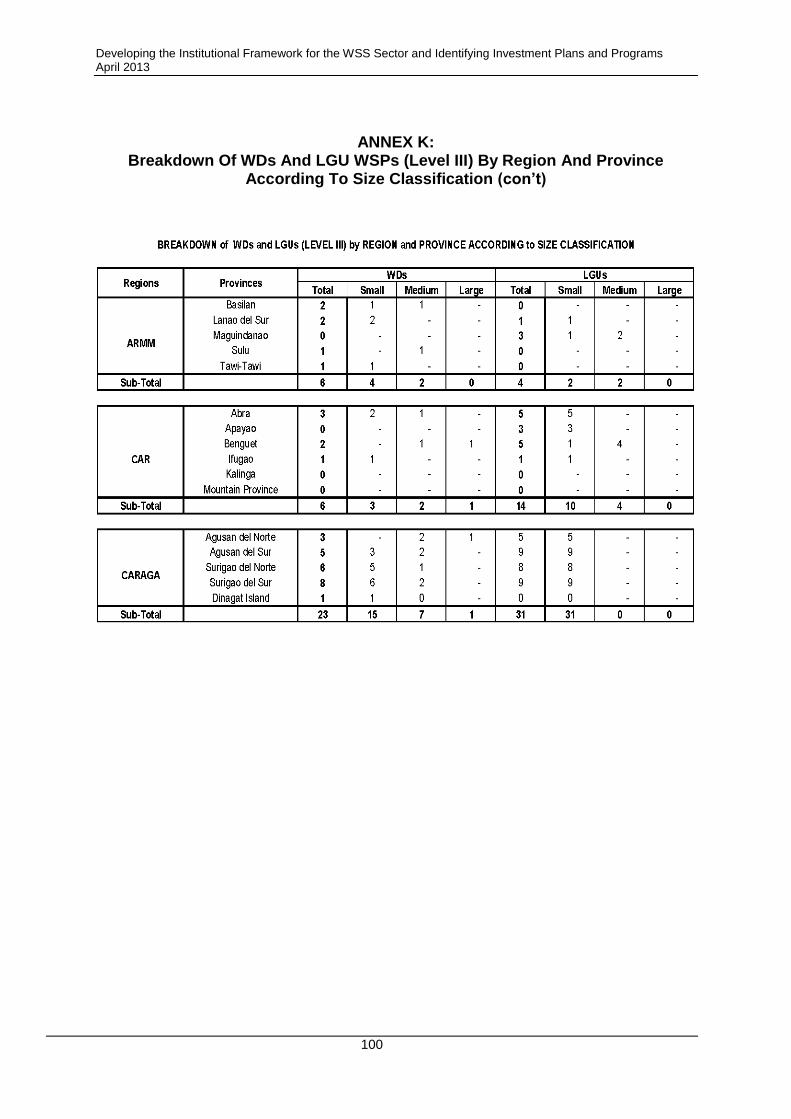

Annexes A Terms of Reference 67 B Summary of Population Projections 69 C Sample Letter of DPWH Secretary Sent to Various Agencies 75 D Data Template

77 E Population Served in 2011 by Regions 78 F Number of Water Supply Providers 84 G Seventy Five Level III Data Samples 89 H Level III Unit Cost for all Main Island Locations 91 I Level III Unit Cost Considering All Samples 94 J Cost of an Upgradable Level III 96 K Breakdown of WDs and LGU WSPs According to Size Classification 97 Tables 1: Primary WSS Agencies and their Roles 13 2: Water Supply Providers 14 3: 2003 Market Share by Type of Provider 15 4: Population Served by Water Supply Providers, as of 2000 16 5: Regional Coverage 16 6: JMP: Use of Improved Drinking Water Sources 18 7: MDG Target for Water Supply 19 8: Projected Population Projections 29 9: Agencies Furnishing Data 30 10: 2011 Served Population 30 11: Comparison between 2003 and 2011 Coverage Data 30 12: Regional Comparison of Population Coverage, 2007 vs 2011 31 13: Comparison of Water Supply Providers 32 14: Water Supply Target Population To Be Served 35 15: Target Population To Be Served 35 16: Target LGUs 36 17: Unit Cost for Level III Water Supply System Infrastructure 39 18: Water Supply Investment Requirements, Php B 40 19: Sanitation Targets 41 20: Sanitation Investment Requirements 41 21: Summary of WSS Infrastructure Investment Requirements 42 22: WSP Training Duration 42 23: Major Sector Reports/Papers 44 24: Major Institutional Recommendations 48 25: Recommendations for Sector Framework 52 26: Major Roles of Agencies 53 27: Government WSPs by Connection Size 56 28: Water Supply Funding Source Requirements 57 29: WS Government Funding Requirements 57 30: Sanitation Fund Sources 58 31: Summary of WSS Funding Requirements from the National Government 58 32: Proposed Roles of the DPWH 63

33: Initial Manpower Complement of the WSS Unit 64 Figures: 1: Water Supply Coverage: NEDA and JMP 19 2: Types of Trends-Population Projections 27 3: Proposed WSS Structure in DPWH

63 References 101

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

1

EXECUTIVE SUMMARY Developing the Institutional Framework for the Water Supply and Sanitation Sector and Identifying Investment Plans and Programs 1. The Secretary of the DPWH was appointed as the “Water Czar” to promote the

development of the sector. With the water supply MDG targets due by 2015 and with the water supply roadmap envisioning universal coverage by 2025, there is a need to establish the extent of investment required to improve water supply coverage and to sustain water supply operation through improved governance of water service providers and local governments. This project, through a Technical Assistance of the World Bank, was conceived to (1) determine the appropriate WSS structure within DPWH and develop its implementation and operation plan, and (2) identify targets, investment plans and programs.

2. The following methodology and approach were adopted for this study:

i. Stock taking on the type of utilities, their location and number of service connections (levels II and III);

ii. The following activities were done in parallel with the stock taking activities.

Population projections for all the towns/cities with the 2010 census data as baseline;

Gathering of data for cost estimating purposes,

Review of past sector reports to have an overview of reforms recommended;

iii. Tabulation of the data gathered to determine population served with Level III/II facilities;

iv. Determination of the demand gap by towns/cities;

v. Determination of the targeted % served by level III/II systems for the different design years, 2015, 2020 and 2025;

vi. Determination of the unit system cost in building a level III and II system,

including the upgrading of level IIs to level IIIs; vii. Identification of the total Investment requirements and the programs needed;

viii. Determination of the roles of the DPWH within the water sector and preparation

of its institutional framework;

ix. Recommendation of sector roles for the different agencies. 3. Out of 1,617 towns and cities outside the National Capital Region, 1,286 (80%) have

level II and/or level III services as reported by end of 2011.

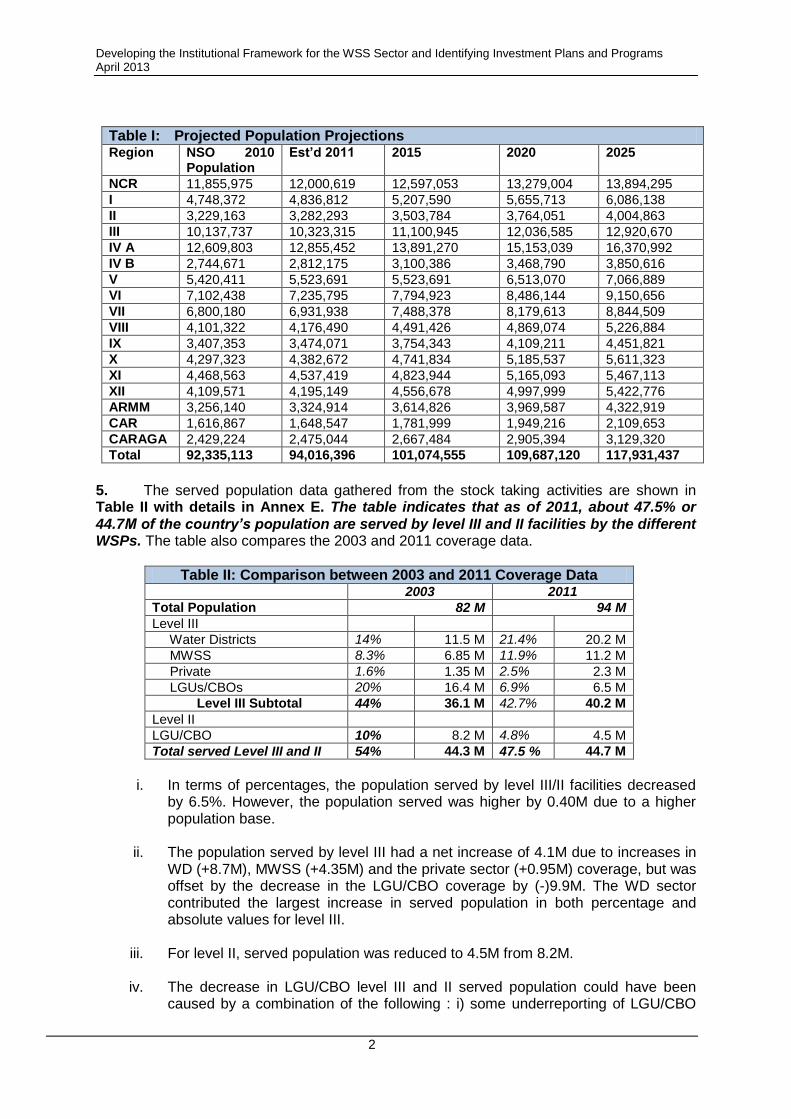

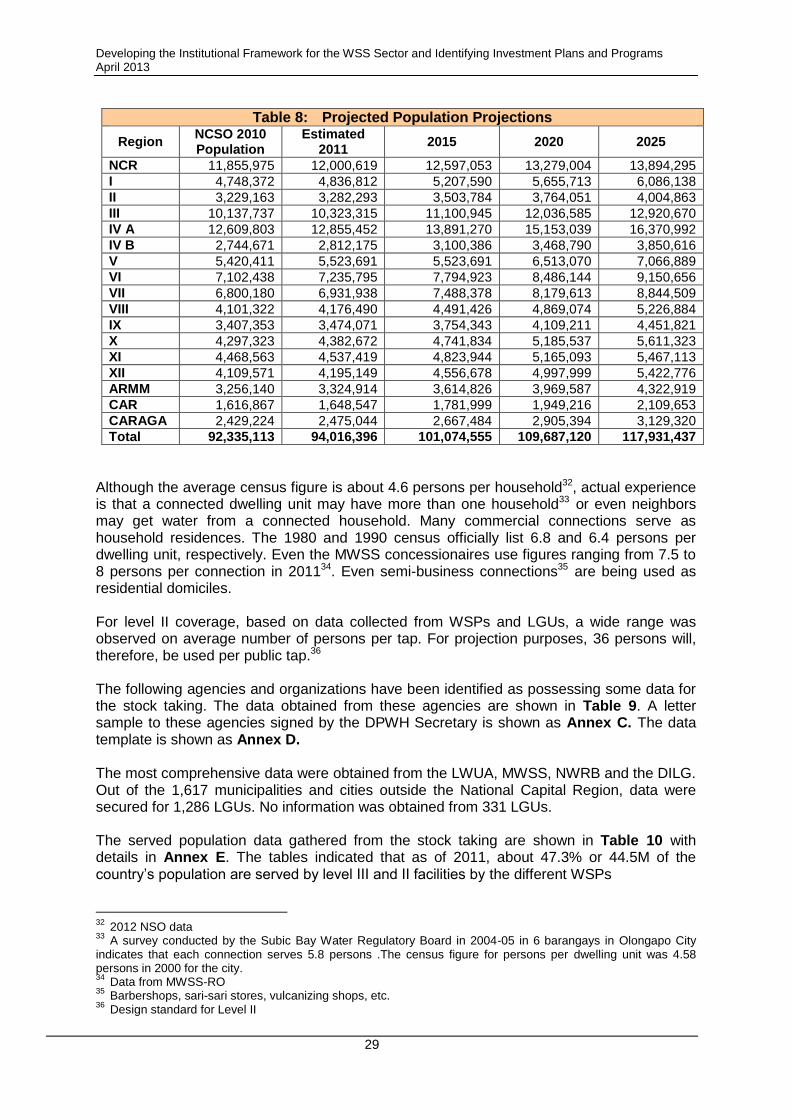

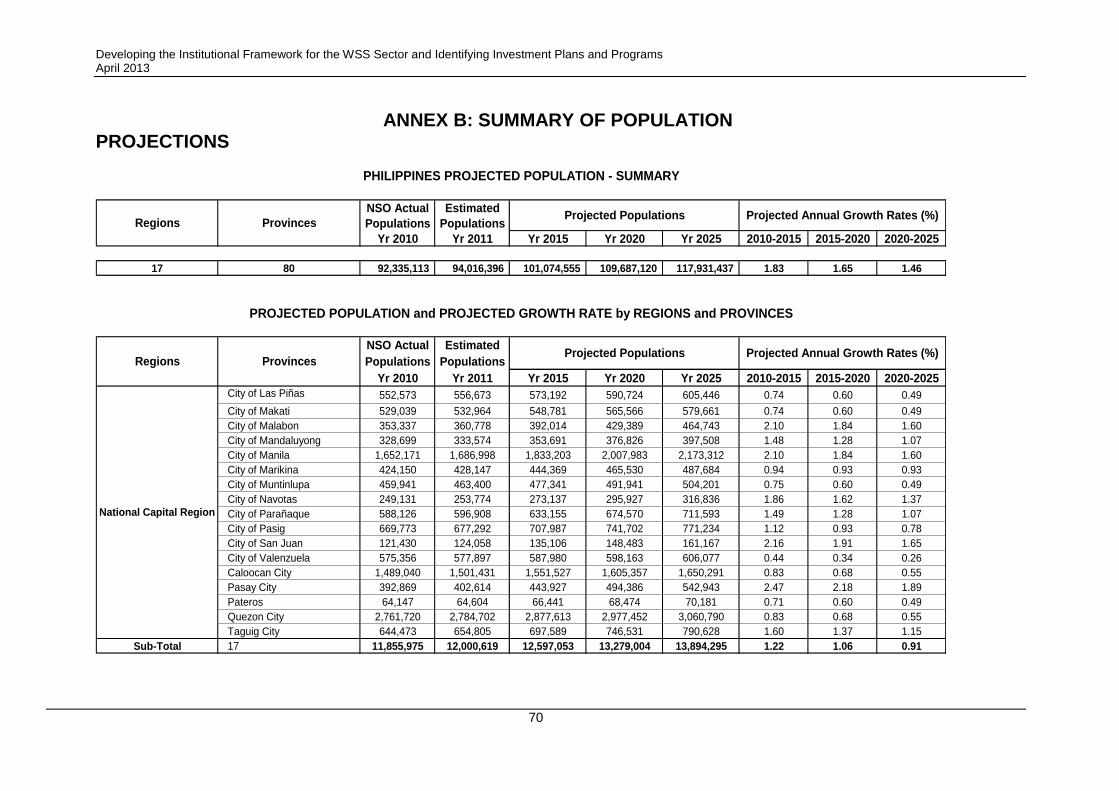

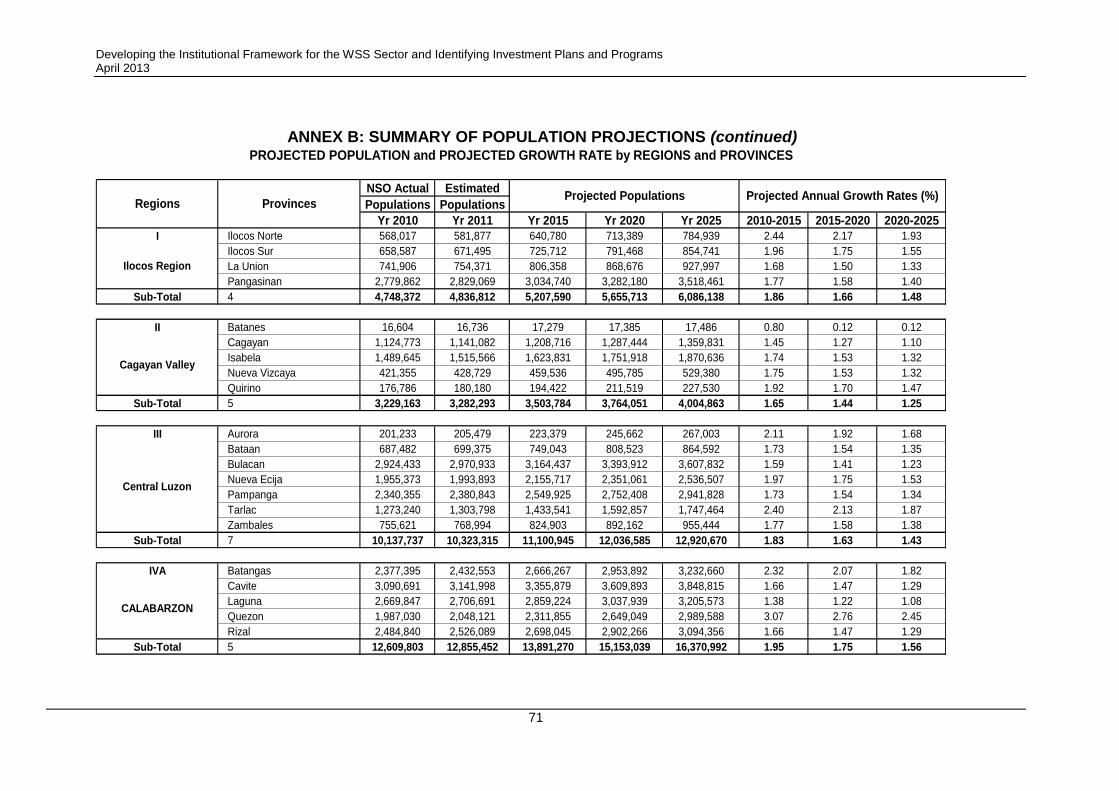

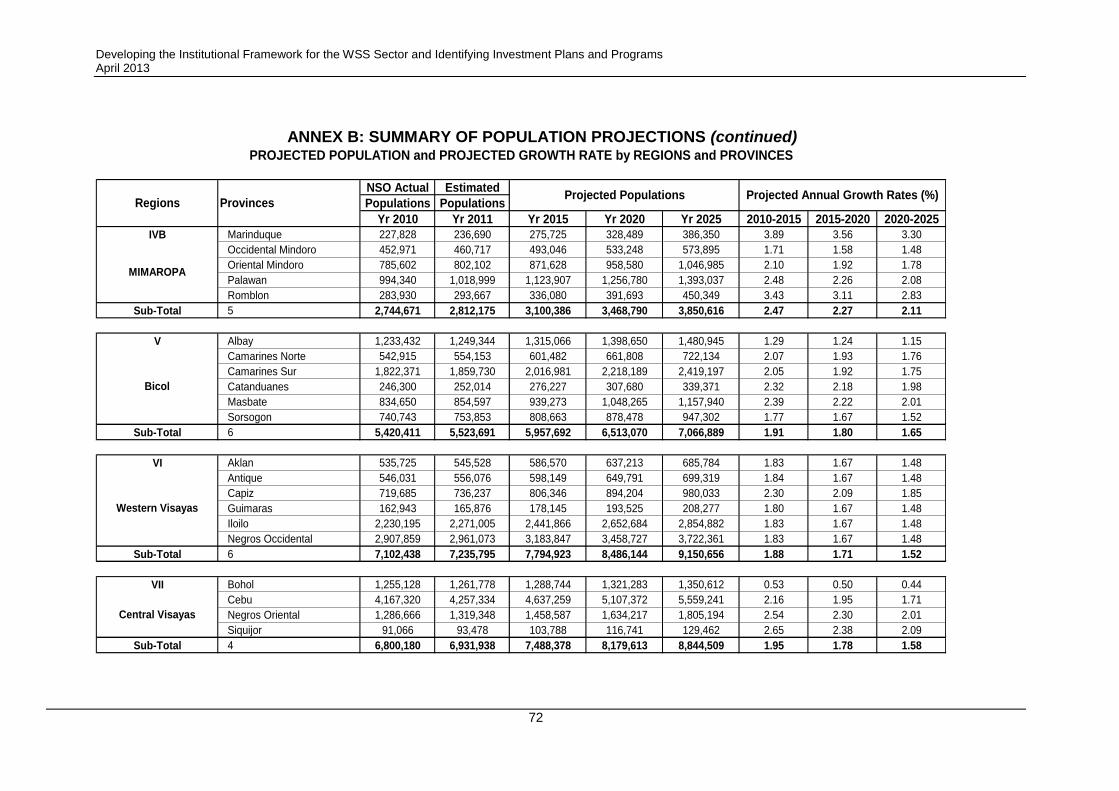

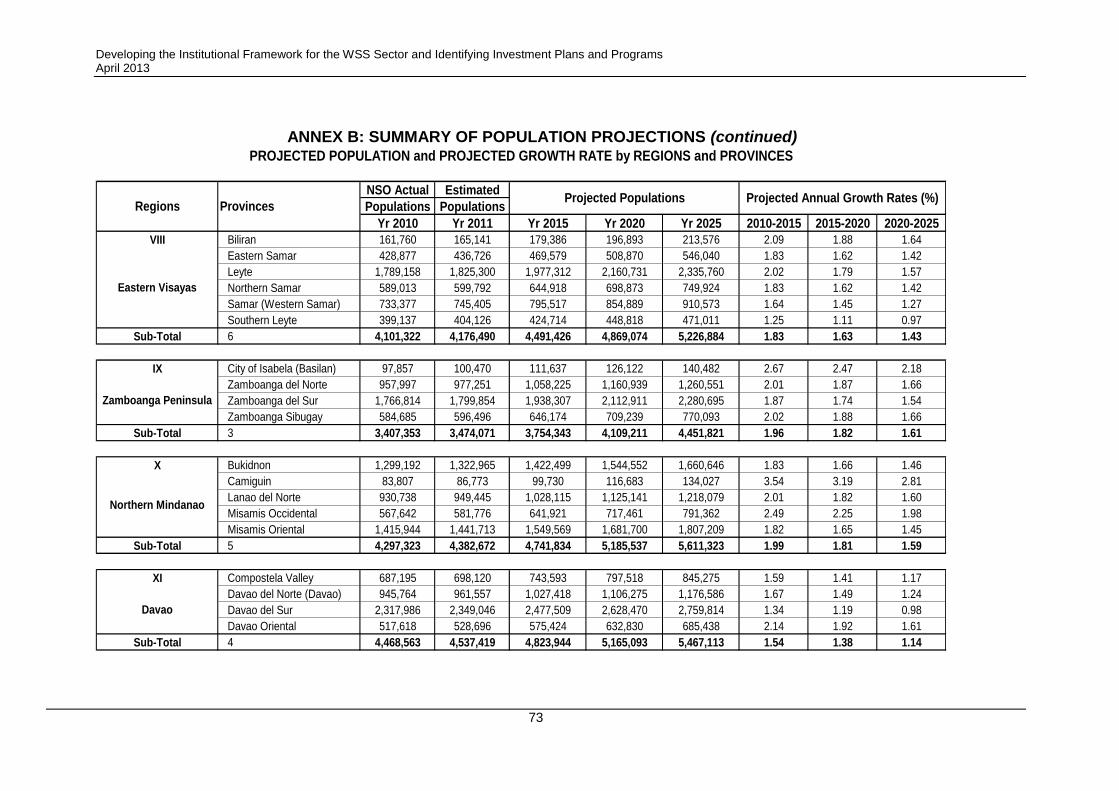

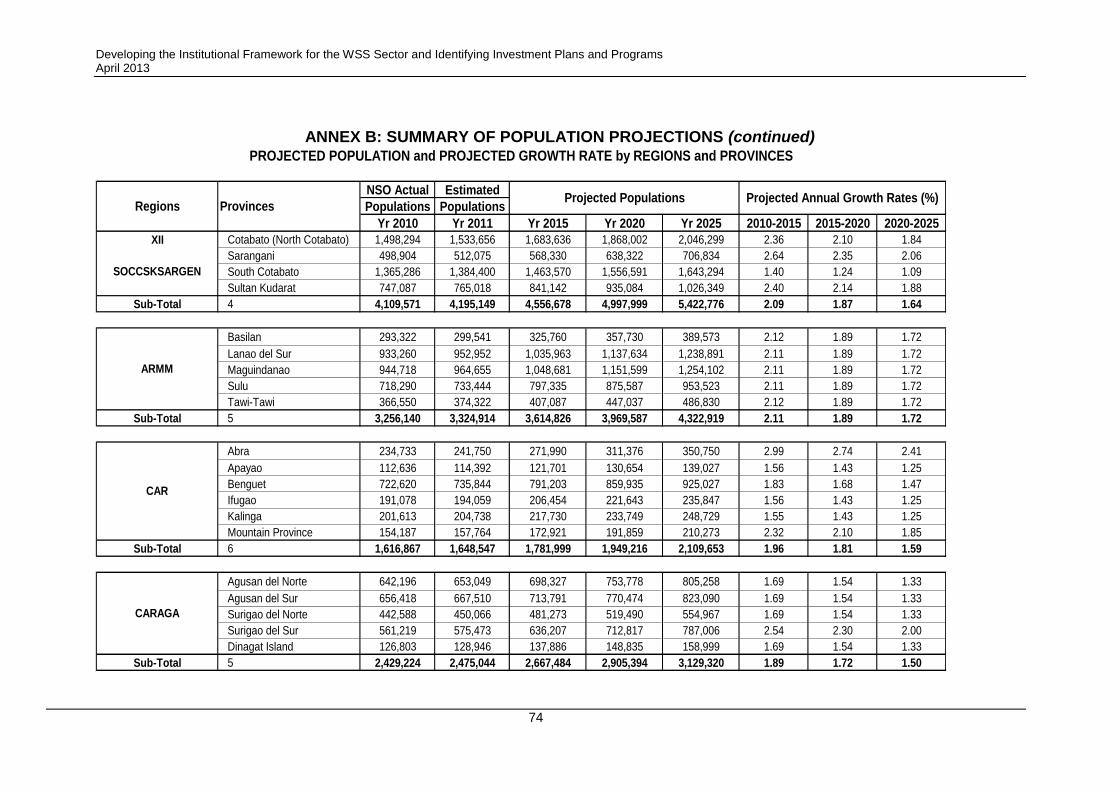

4. Table I shows the projected population projections.

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

2

Table I: Projected Population Projections Region NSO 2010

Population Est’d 2011 2015 2020 2025

NCR 11,855,975 12,000,619 12,597,053 13,279,004 13,894,295

I 4,748,372 4,836,812 5,207,590 5,655,713 6,086,138

II 3,229,163 3,282,293 3,503,784 3,764,051 4,004,863

III 10,137,737 10,323,315 11,100,945 12,036,585 12,920,670

IV A 12,609,803 12,855,452 13,891,270 15,153,039 16,370,992

IV B 2,744,671 2,812,175 3,100,386 3,468,790 3,850,616

V 5,420,411 5,523,691 5,523,691 6,513,070 7,066,889

VI 7,102,438 7,235,795 7,794,923 8,486,144 9,150,656

VII 6,800,180 6,931,938 7,488,378 8,179,613 8,844,509

VIII 4,101,322 4,176,490 4,491,426 4,869,074 5,226,884

IX 3,407,353 3,474,071 3,754,343 4,109,211 4,451,821

X 4,297,323 4,382,672 4,741,834 5,185,537 5,611,323

XI 4,468,563 4,537,419 4,823,944 5,165,093 5,467,113

XII 4,109,571 4,195,149 4,556,678 4,997,999 5,422,776

ARMM 3,256,140 3,324,914 3,614,826 3,969,587 4,322,919

CAR 1,616,867 1,648,547 1,781,999 1,949,216 2,109,653

CARAGA 2,429,224 2,475,044 2,667,484 2,905,394 3,129,320

Total 92,335,113 94,016,396 101,074,555 109,687,120 117,931,437

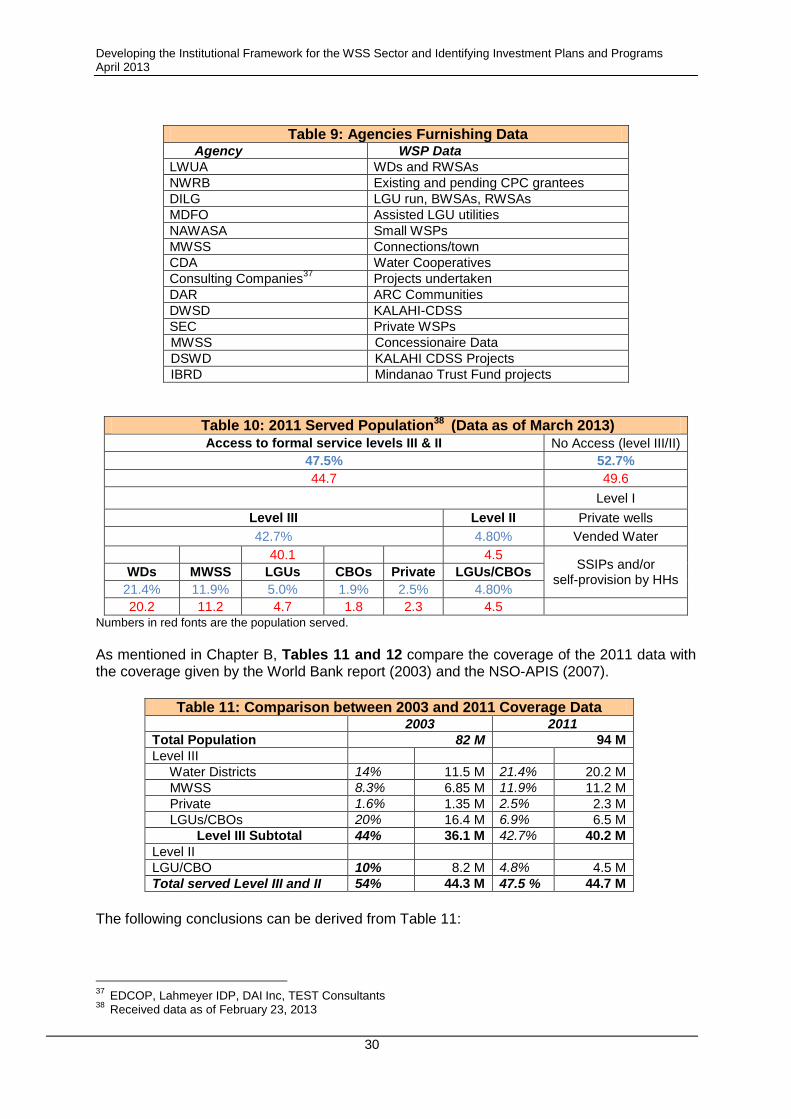

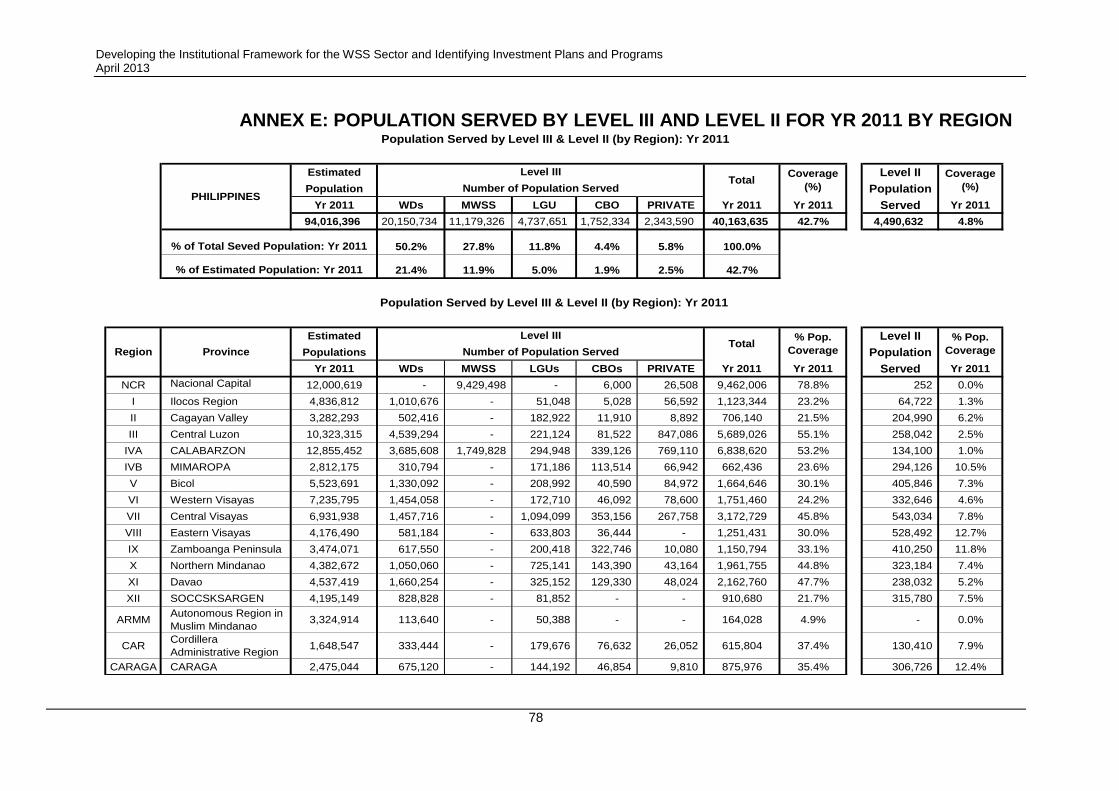

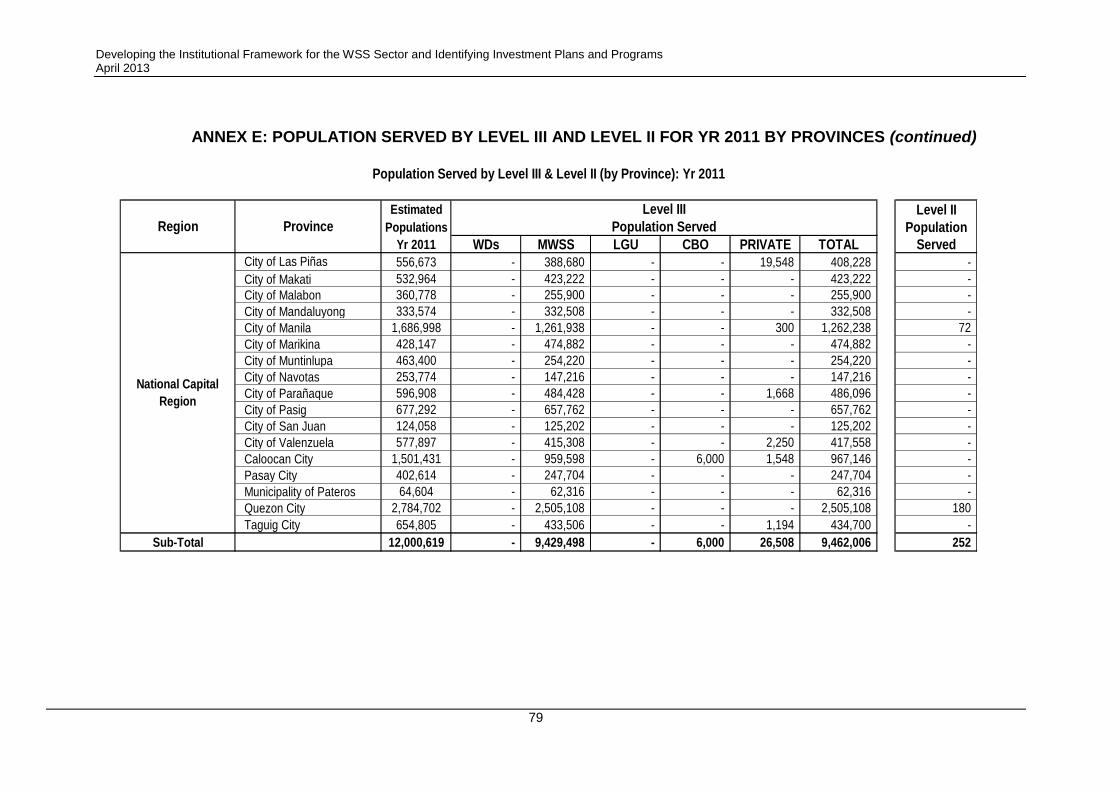

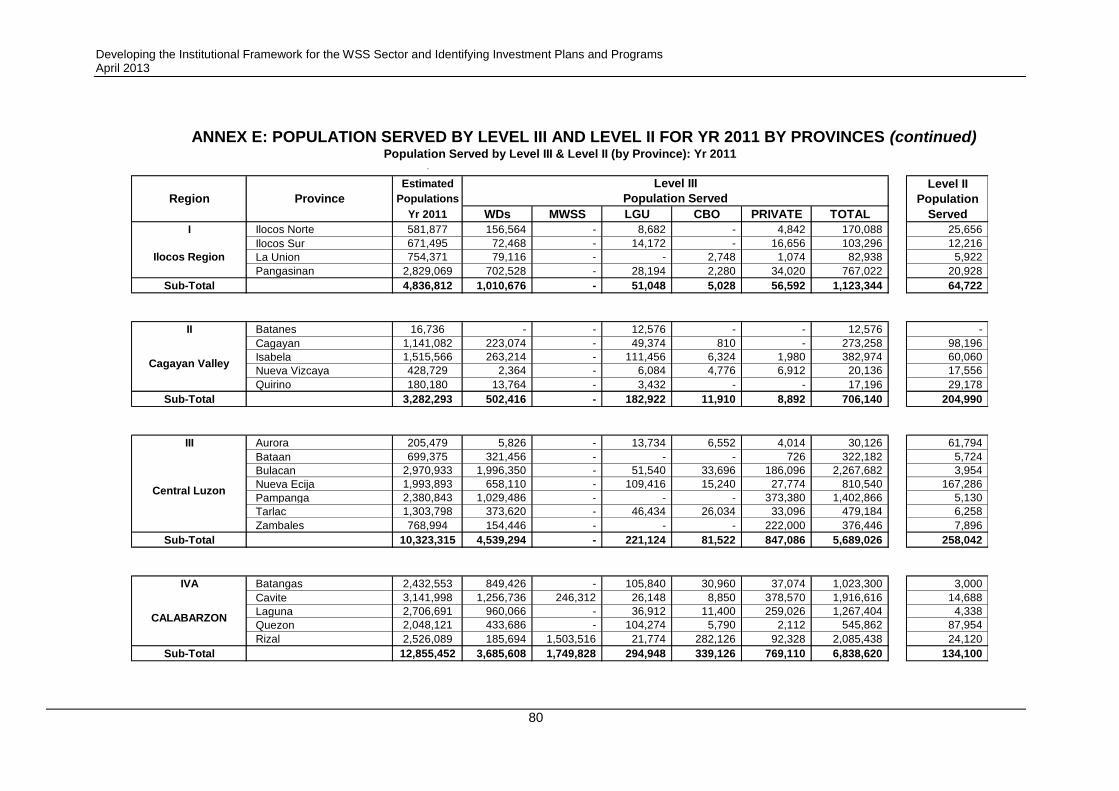

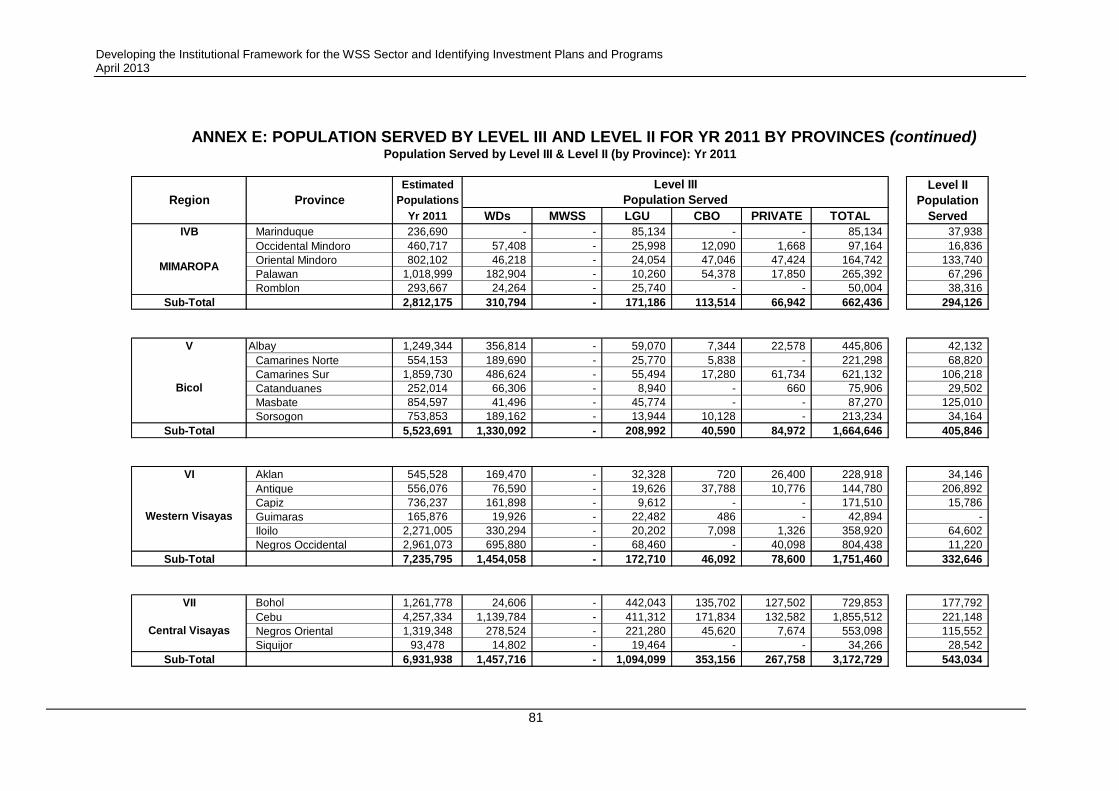

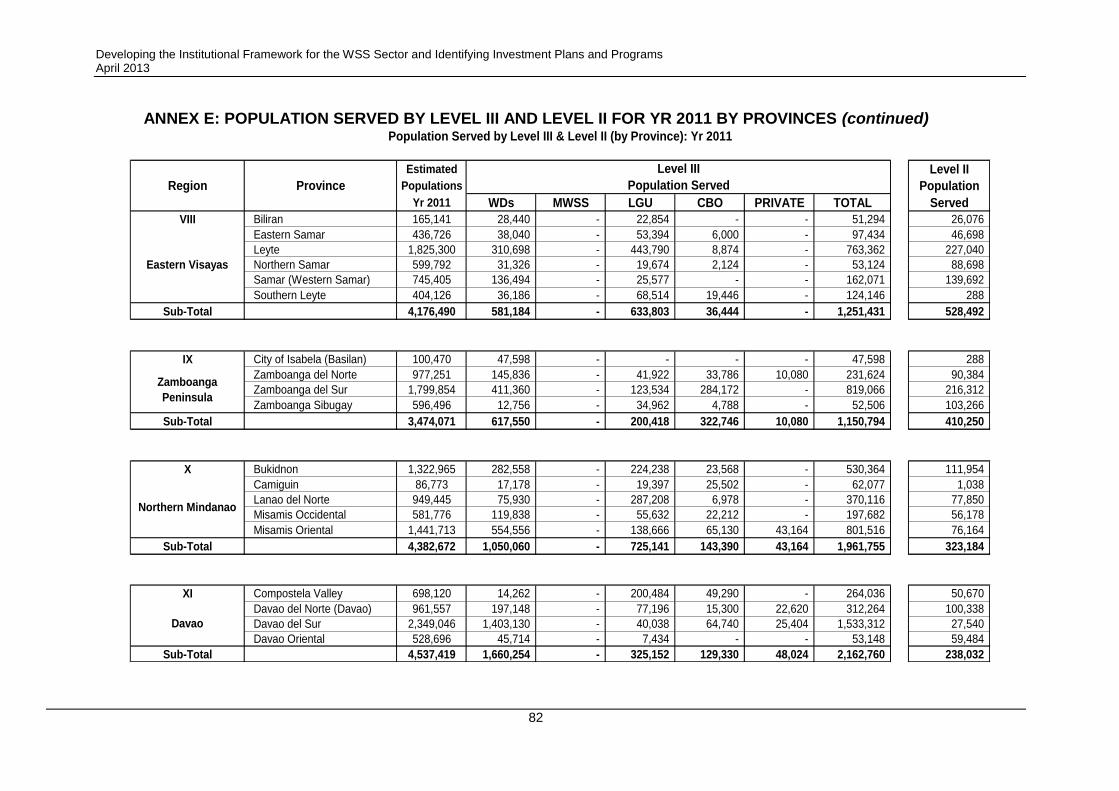

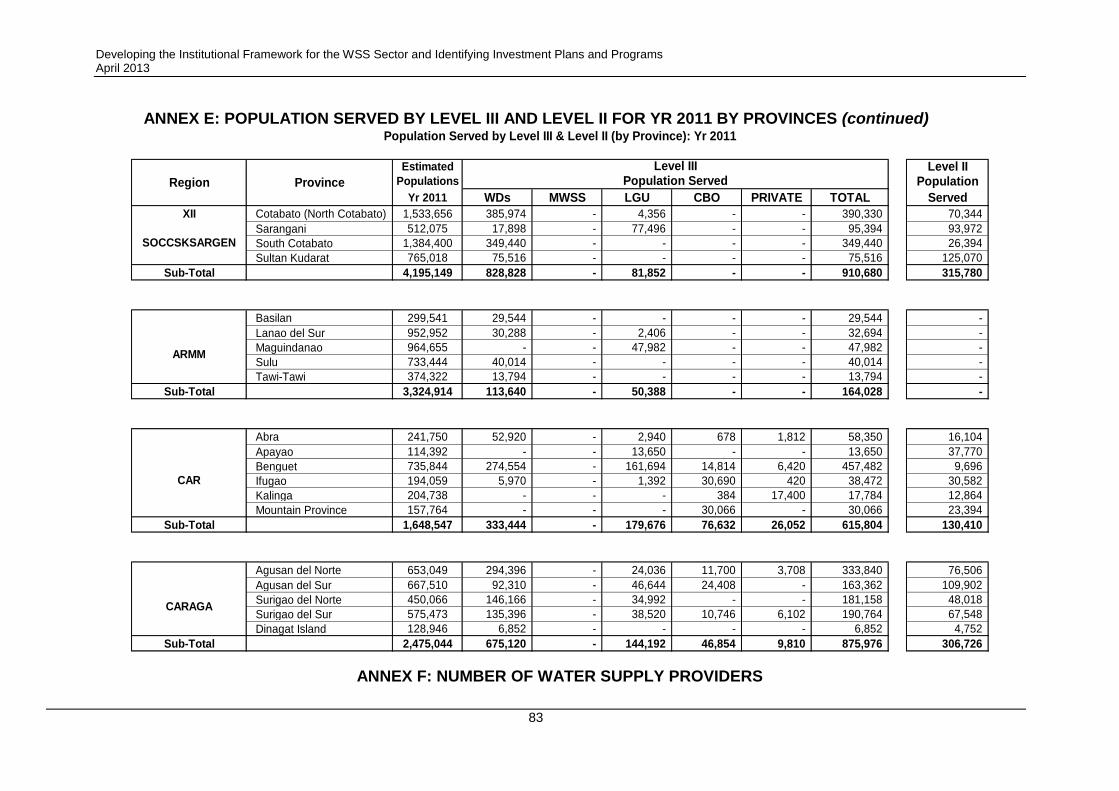

5. The served population data gathered from the stock taking activities are shown in Table II with details in Annex E. The table indicates that as of 2011, about 47.5% or 44.7M of the country’s population are served by level III and II facilities by the different WSPs. The table also compares the 2003 and 2011 coverage data.

Table II: Comparison between 2003 and 2011 Coverage Data 2003 2011

Total Population 82 M 94 M

Level III

Water Districts 14% 11.5 M 21.4% 20.2 M

MWSS 8.3% 6.85 M 11.9% 11.2 M

Private 1.6% 1.35 M 2.5% 2.3 M

LGUs/CBOs 20% 16.4 M 6.9% 6.5 M

Level III Subtotal 44% 36.1 M 42.7% 40.2 M

Level II

LGU/CBO 10% 8.2 M 4.8% 4.5 M

Total served Level III and II 54% 44.3 M 47.5 % 44.7 M

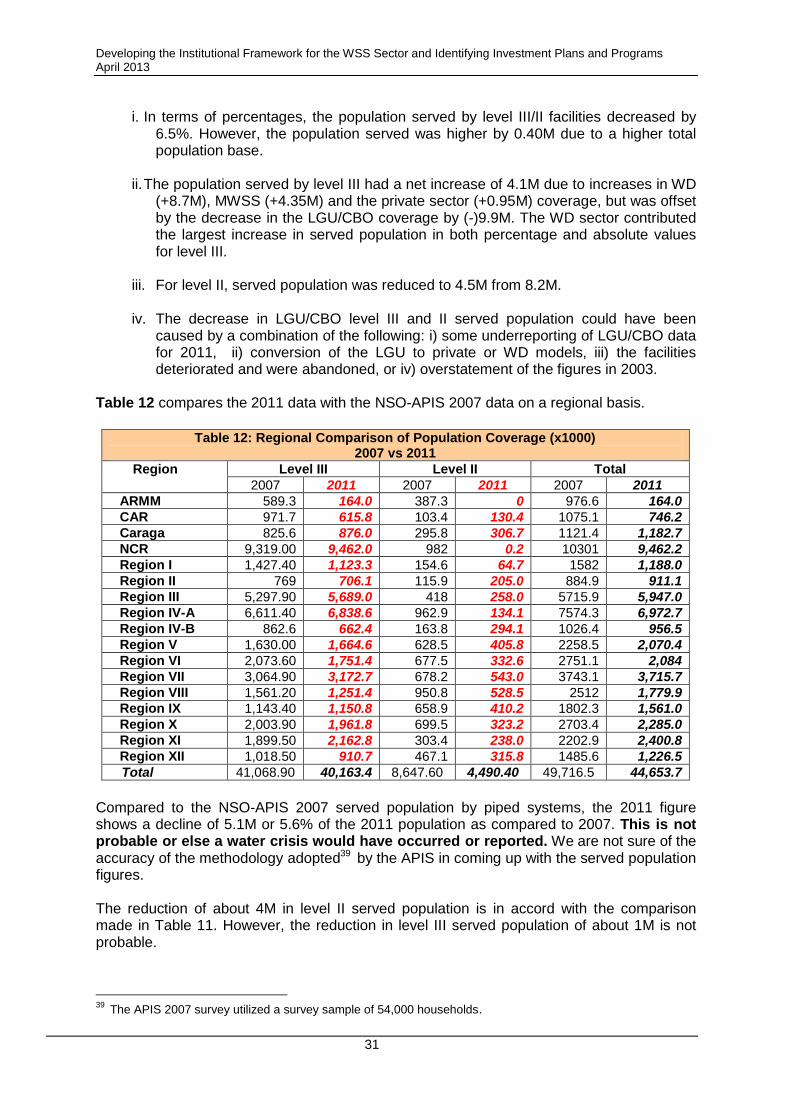

i. In terms of percentages, the population served by level III/II facilities decreased

by 6.5%. However, the population served was higher by 0.40M due to a higher population base.

ii. The population served by level III had a net increase of 4.1M due to increases in WD (+8.7M), MWSS (+4.35M) and the private sector (+0.95M) coverage, but was offset by the decrease in the LGU/CBO coverage by (-)9.9M. The WD sector contributed the largest increase in served population in both percentage and absolute values for level III.

iii. For level II, served population was reduced to 4.5M from 8.2M.

iv. The decrease in LGU/CBO level III and II served population could have been

caused by a combination of the following : i) some underreporting of LGU/CBO

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

3

data for 2011, ii) conversion of the LGU to private or WD models, iii) the facilities deteriorated and were abandoned or iv) the figures in 2003 may have been overstated.

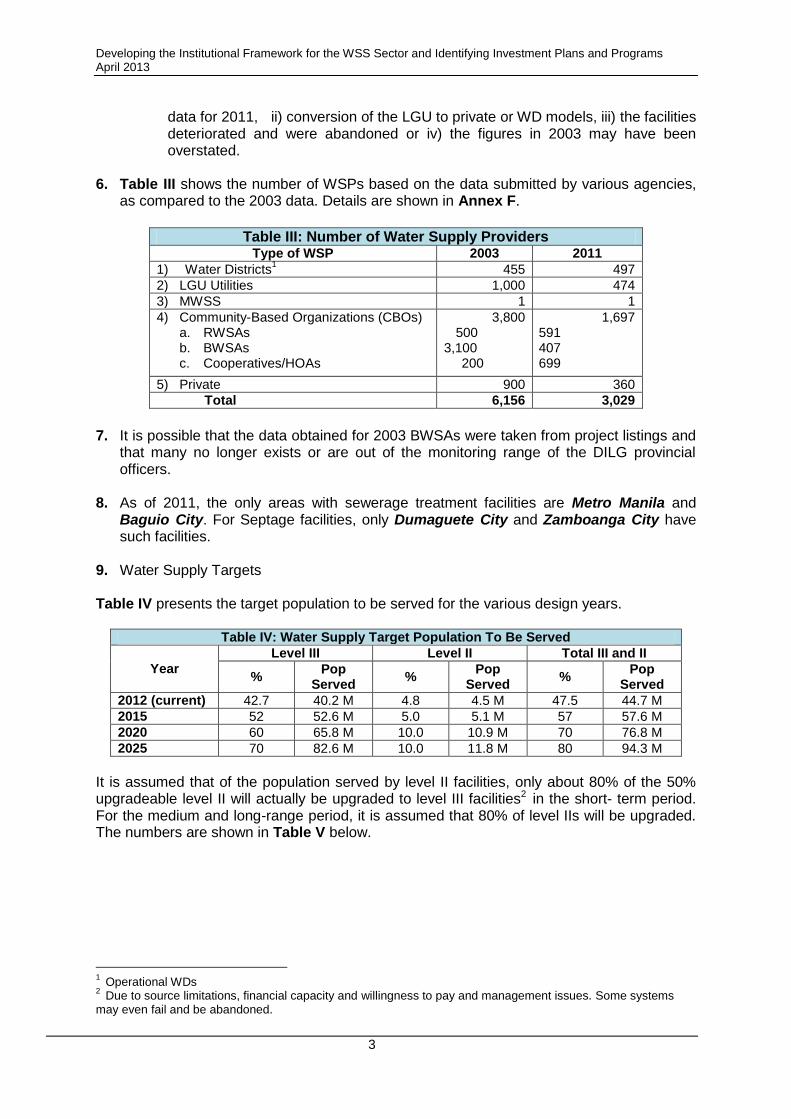

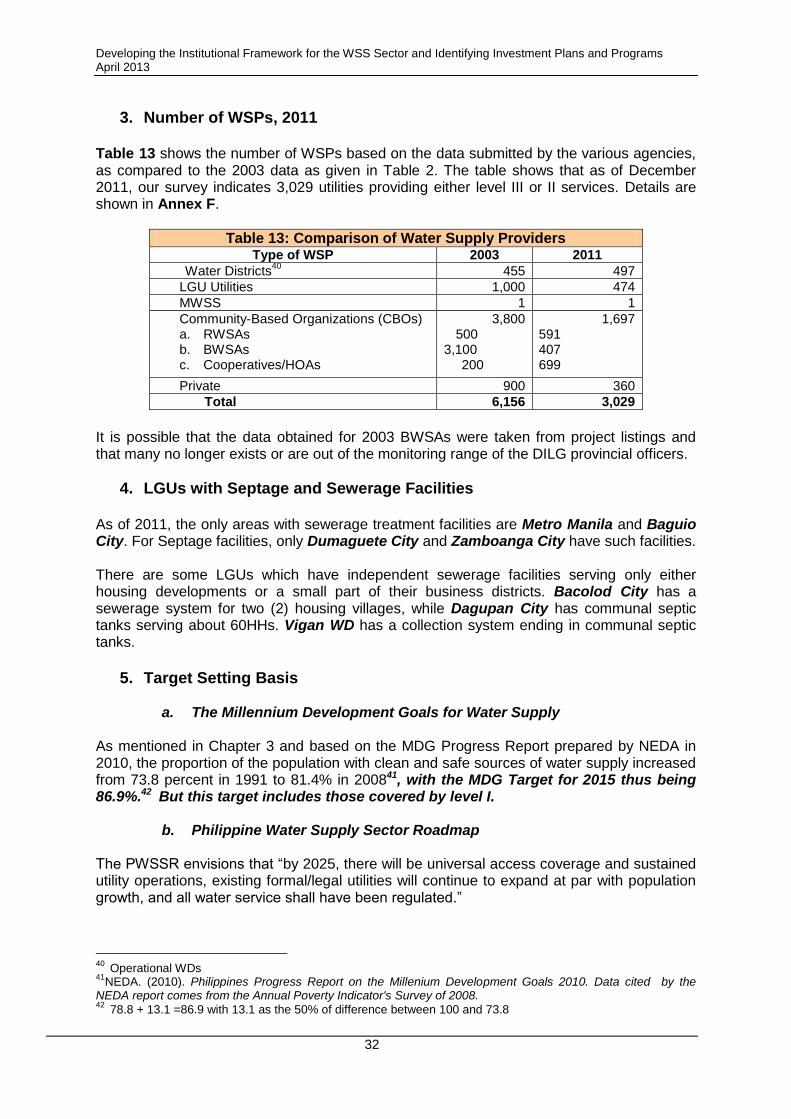

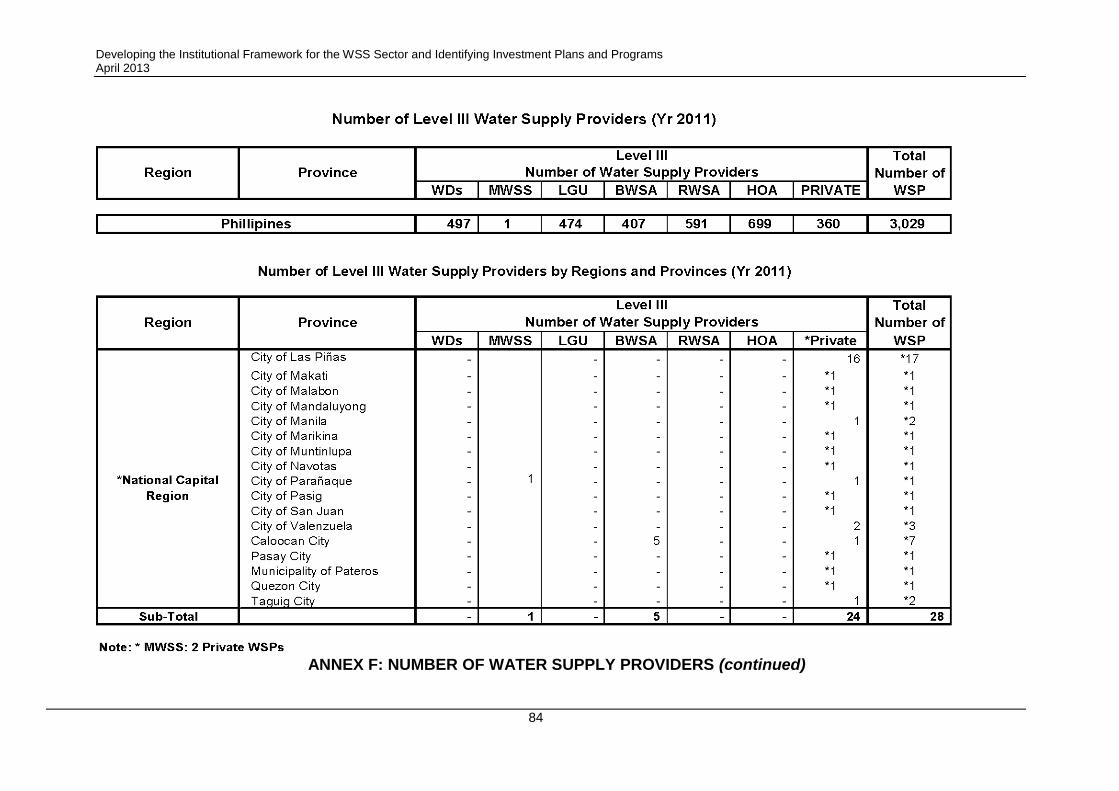

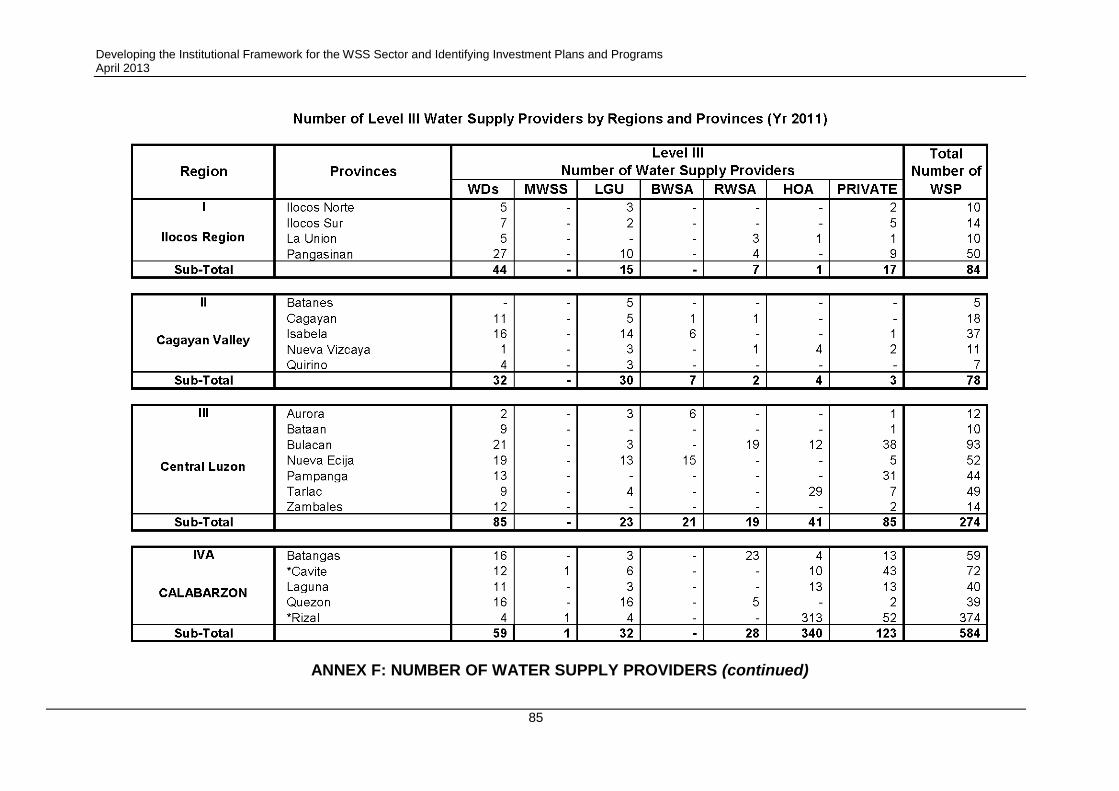

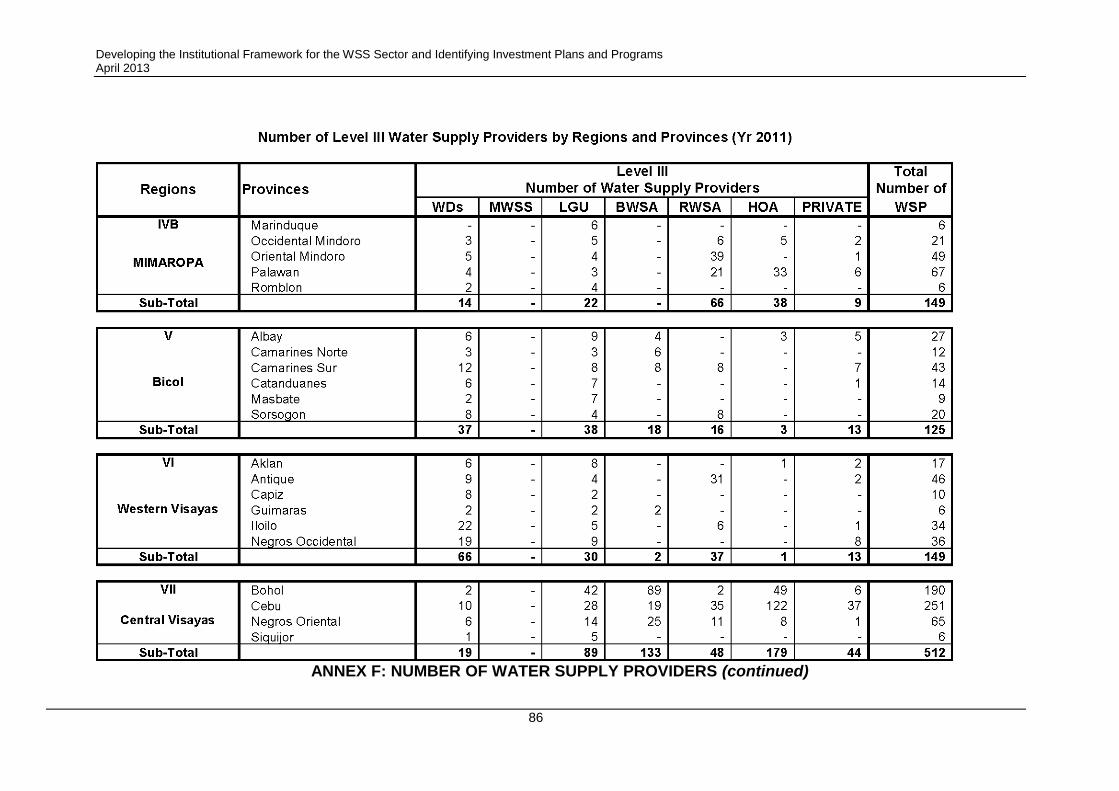

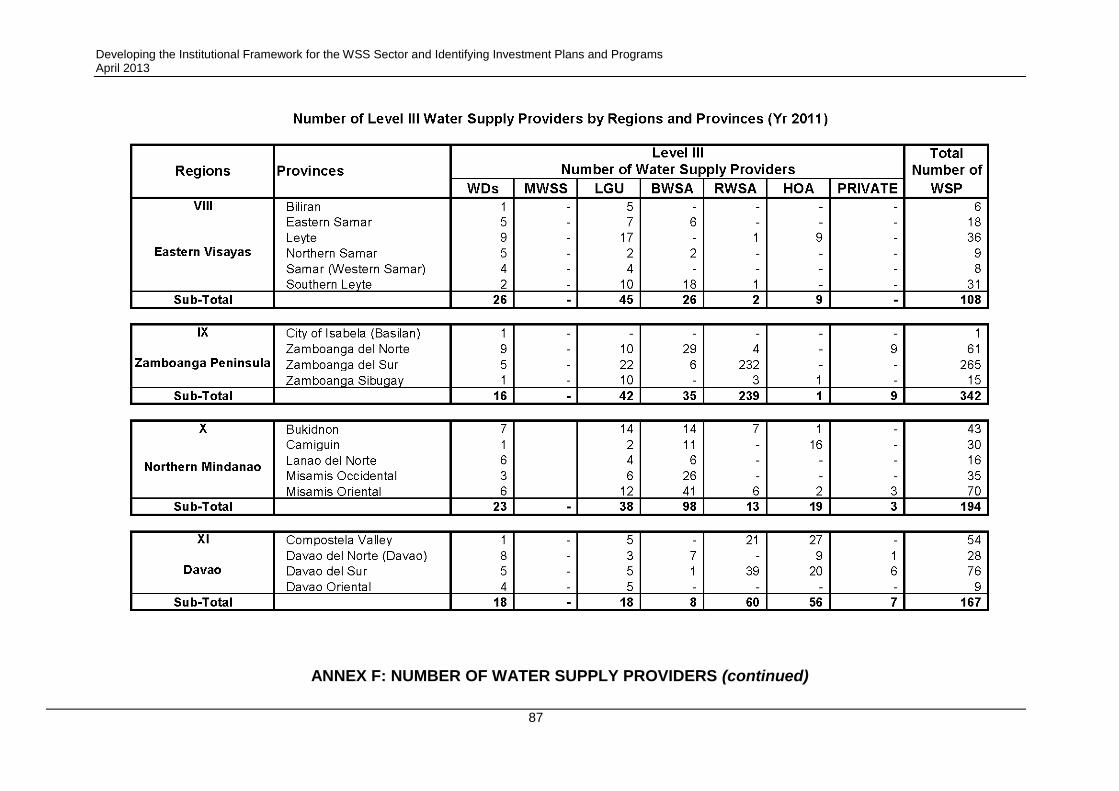

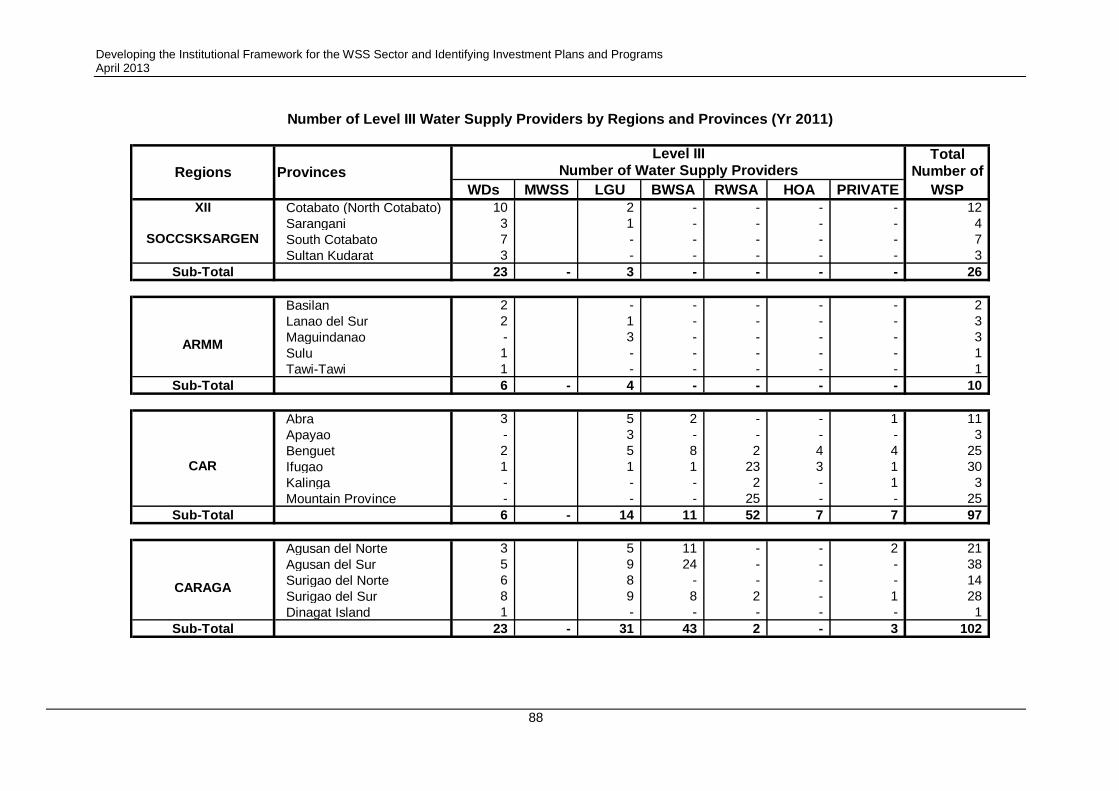

6. Table III shows the number of WSPs based on the data submitted by various agencies,

as compared to the 2003 data. Details are shown in Annex F.

Table III: Number of Water Supply Providers

Type of WSP 2003 2011

1) Water Districts1 455 497

2) LGU Utilities 1,000 474

3) MWSS 1 1

4) Community-Based Organizations (CBOs) a. RWSAs b. BWSAs c. Cooperatives/HOAs

3,800 500 3,100 200

1,697 591 407 699

5) Private 900 360

Total 6,156 3,029

7. It is possible that the data obtained for 2003 BWSAs were taken from project listings and

that many no longer exists or are out of the monitoring range of the DILG provincial officers.

8. As of 2011, the only areas with sewerage treatment facilities are Metro Manila and

Baguio City. For Septage facilities, only Dumaguete City and Zamboanga City have such facilities.

9. Water Supply Targets

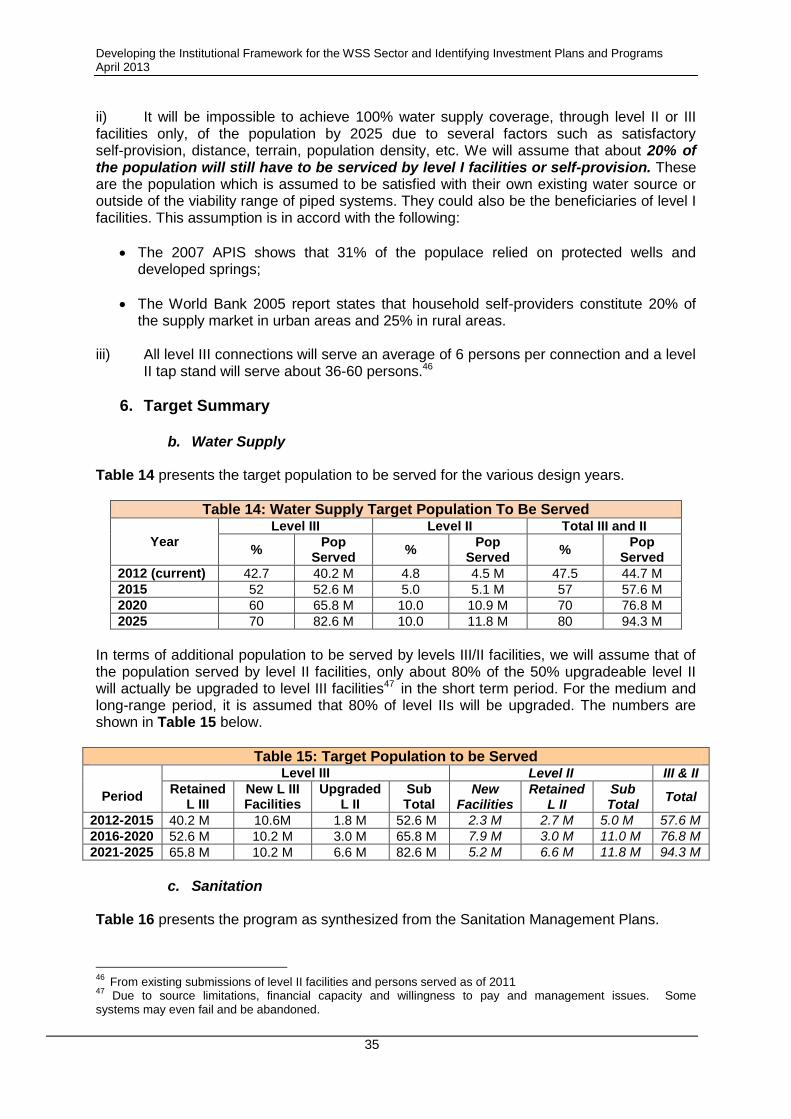

Table IV presents the target population to be served for the various design years.

Table IV: Water Supply Target Population To Be Served

Year

Level III Level II Total III and II

% Pop

Served %

Pop Served

% Pop

Served

2012 (current) 42.7 40.2 M 4.8 4.5 M 47.5 44.7 M

2015 52 52.6 M 5.0 5.1 M 57 57.6 M

2020 60 65.8 M 10.0 10.9 M 70 76.8 M

2025 70 82.6 M 10.0 11.8 M 80 94.3 M

It is assumed that of the population served by level II facilities, only about 80% of the 50% upgradeable level II will actually be upgraded to level III facilities2 in the short- term period. For the medium and long-range period, it is assumed that 80% of level IIs will be upgraded. The numbers are shown in Table V below.

1 Operational WDs

2 Due to source limitations, financial capacity and willingness to pay and management issues. Some systems

may even fail and be abandoned.

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

4

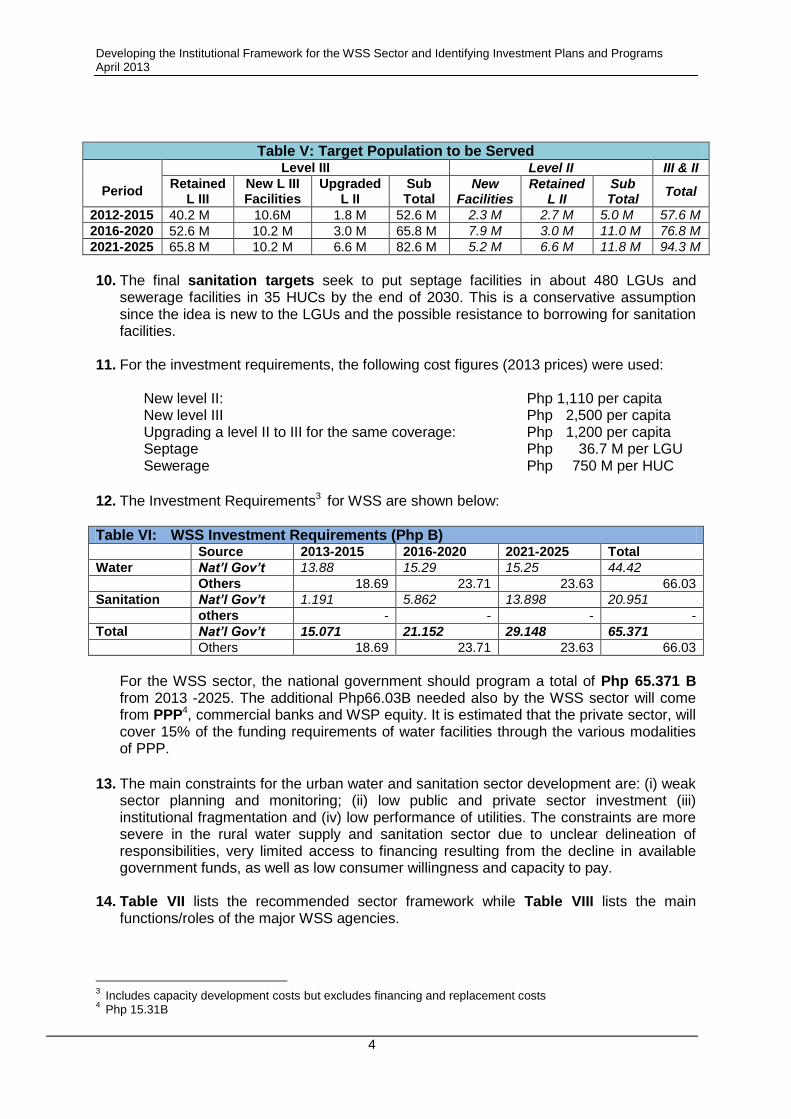

Table V: Target Population to be Served

Period

Level III Level II III & II

Retained L III

New L III Facilities

Upgraded L II

Sub Total

New Facilities

Retained L II

Sub Total

Total

2012-2015 40.2 M 10.6M 1.8 M 52.6 M 2.3 M 2.7 M 5.0 M 57.6 M

2016-2020 52.6 M 10.2 M 3.0 M 65.8 M 7.9 M 3.0 M 11.0 M 76.8 M

2021-2025 65.8 M 10.2 M 6.6 M 82.6 M 5.2 M 6.6 M 11.8 M 94.3 M

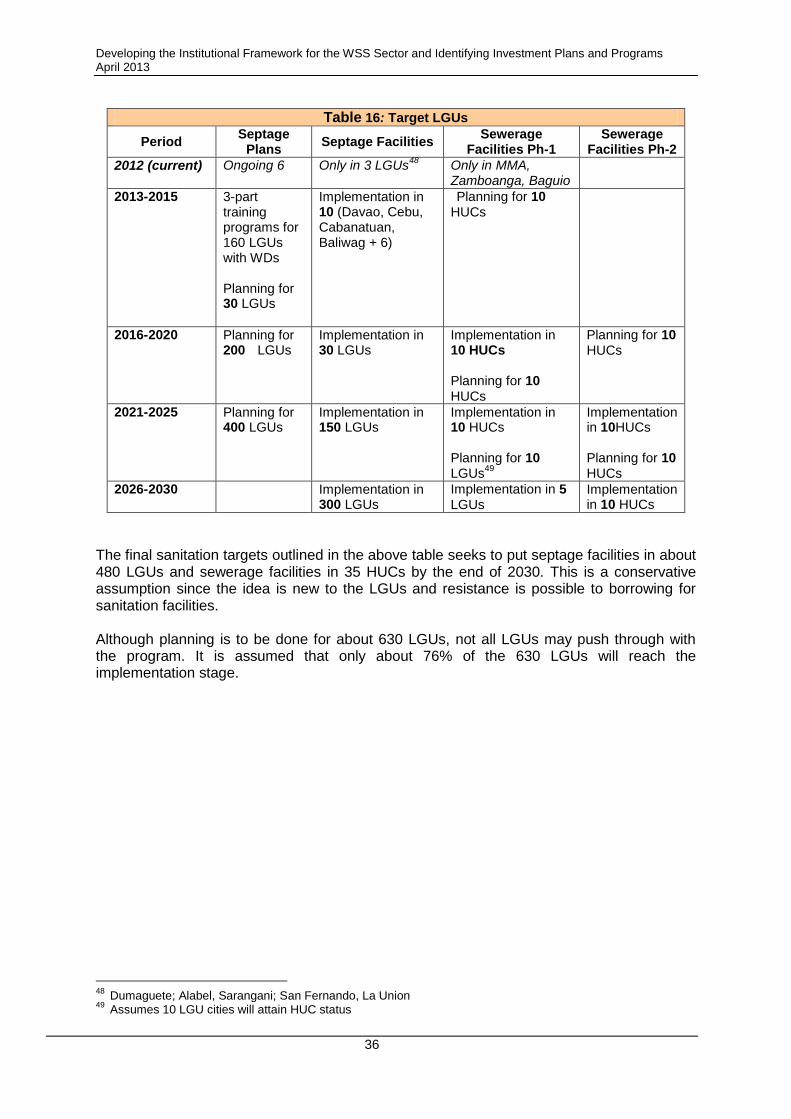

10. The final sanitation targets seek to put septage facilities in about 480 LGUs and

sewerage facilities in 35 HUCs by the end of 2030. This is a conservative assumption since the idea is new to the LGUs and the possible resistance to borrowing for sanitation facilities.

11. For the investment requirements, the following cost figures (2013 prices) were used:

New level II: Php 1,110 per capita New level III Php 2,500 per capita Upgrading a level II to III for the same coverage: Php 1,200 per capita Septage Php 36.7 M per LGU Sewerage Php 750 M per HUC

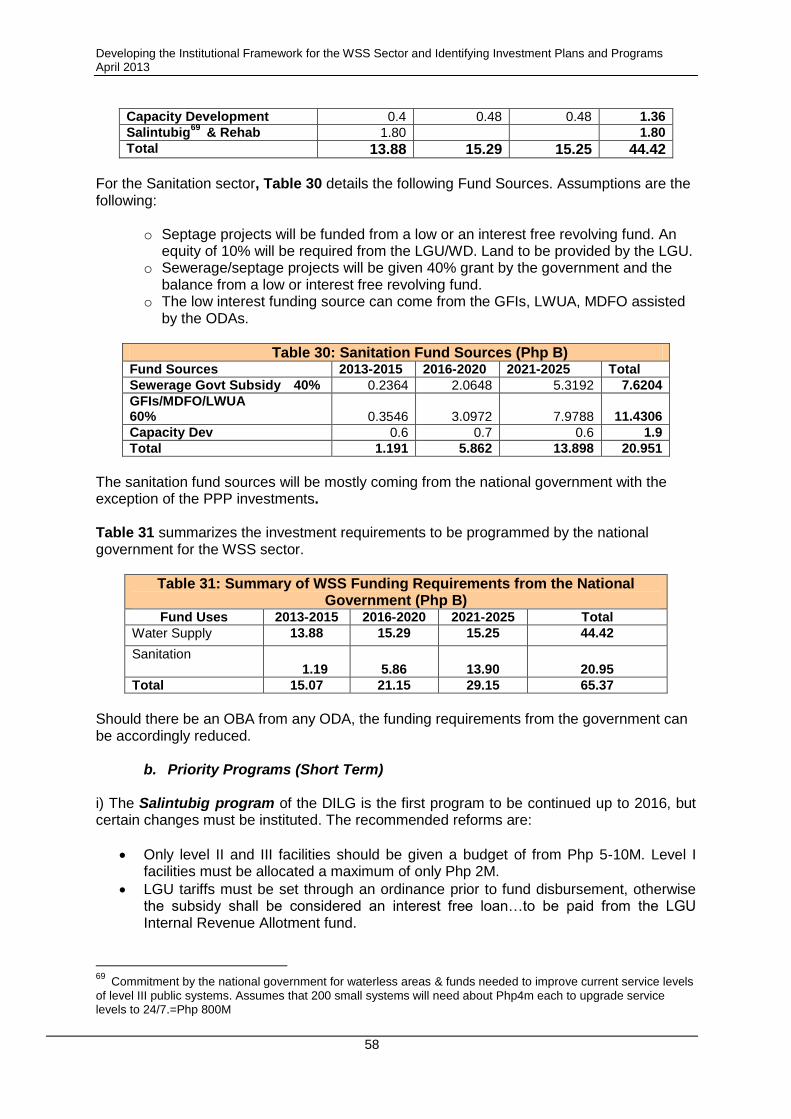

12. The Investment Requirements3 for WSS are shown below:

Table VI: WSS Investment Requirements (Php B) Source 2013-2015 2016-2020 2021-2025 Total

Water Nat’l Gov’t 13.88 15.29 15.25 44.42

Others 18.69 23.71 23.63 66.03

Sanitation Nat’l Gov’t 1.191 5.862 13.898 20.951

others - - - -

Total Nat’l Gov’t 15.071 21.152 29.148 65.371

Others 18.69 23.71 23.63 66.03

For the WSS sector, the national government should program a total of Php 65.371 B from 2013 -2025. The additional Php66.03B needed also by the WSS sector will come from PPP4, commercial banks and WSP equity. It is estimated that the private sector, will cover 15% of the funding requirements of water facilities through the various modalities of PPP.

13. The main constraints for the urban water and sanitation sector development are: (i) weak

sector planning and monitoring; (ii) low public and private sector investment (iii) institutional fragmentation and (iv) low performance of utilities. The constraints are more severe in the rural water supply and sanitation sector due to unclear delineation of responsibilities, very limited access to financing resulting from the decline in available government funds, as well as low consumer willingness and capacity to pay.

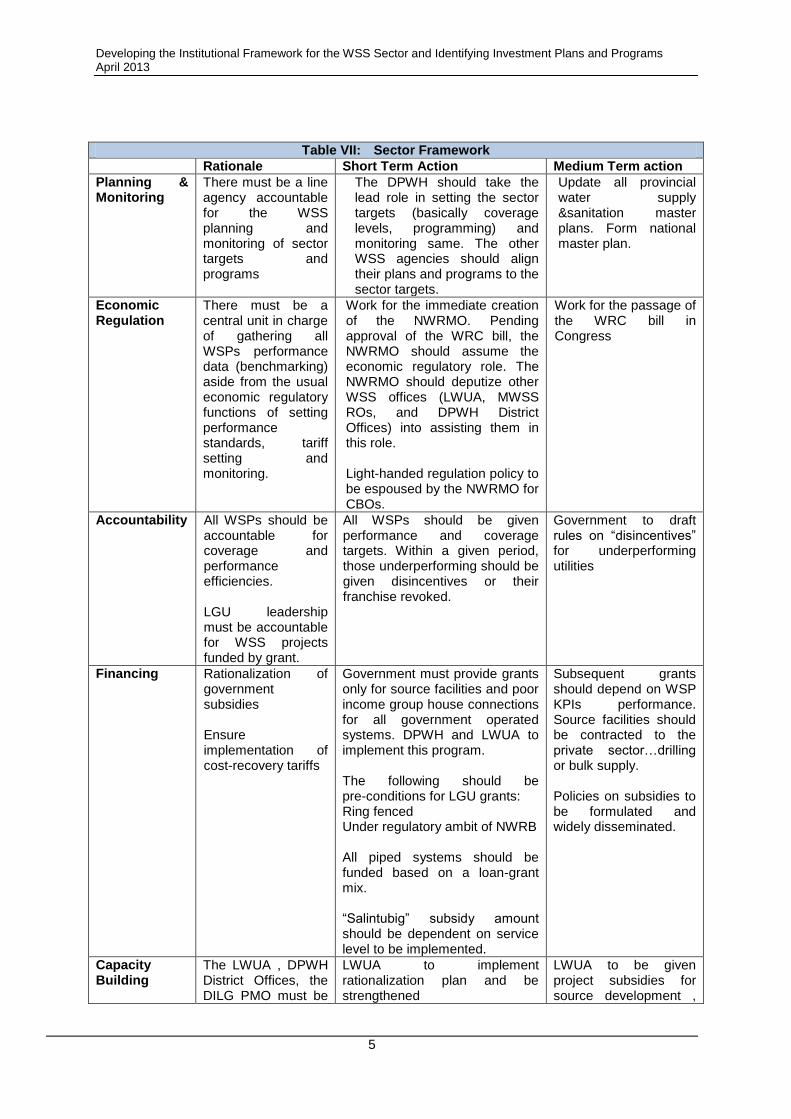

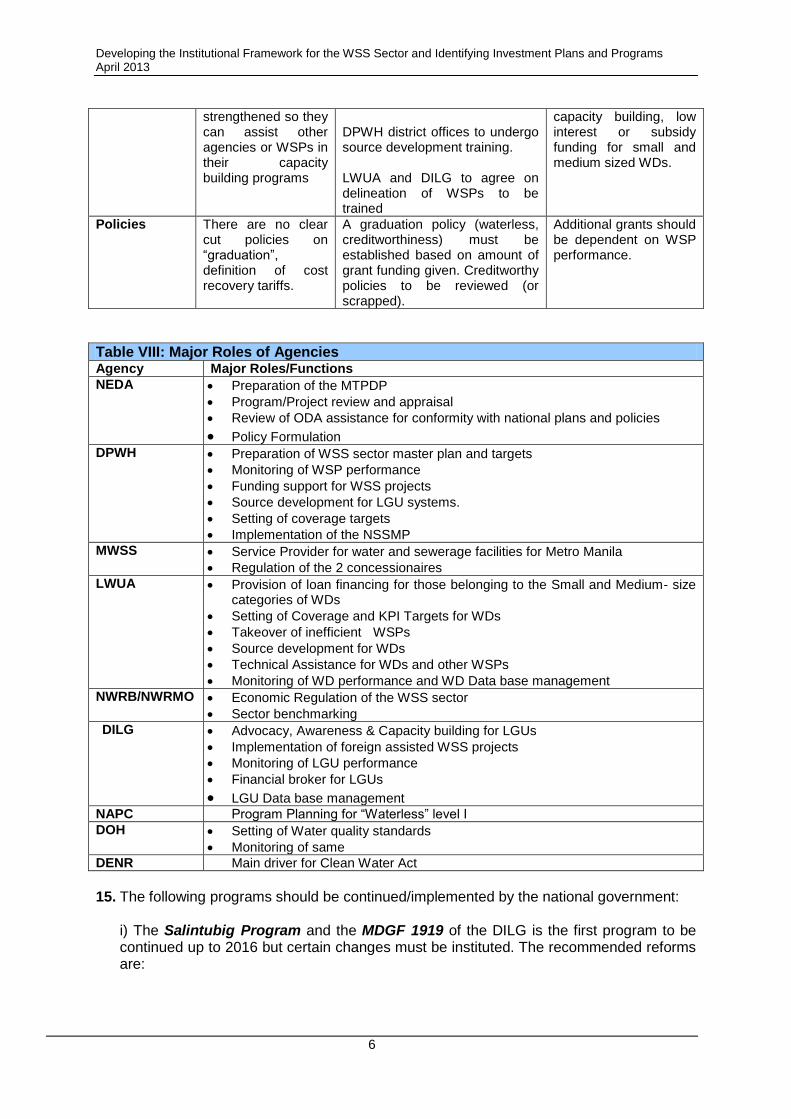

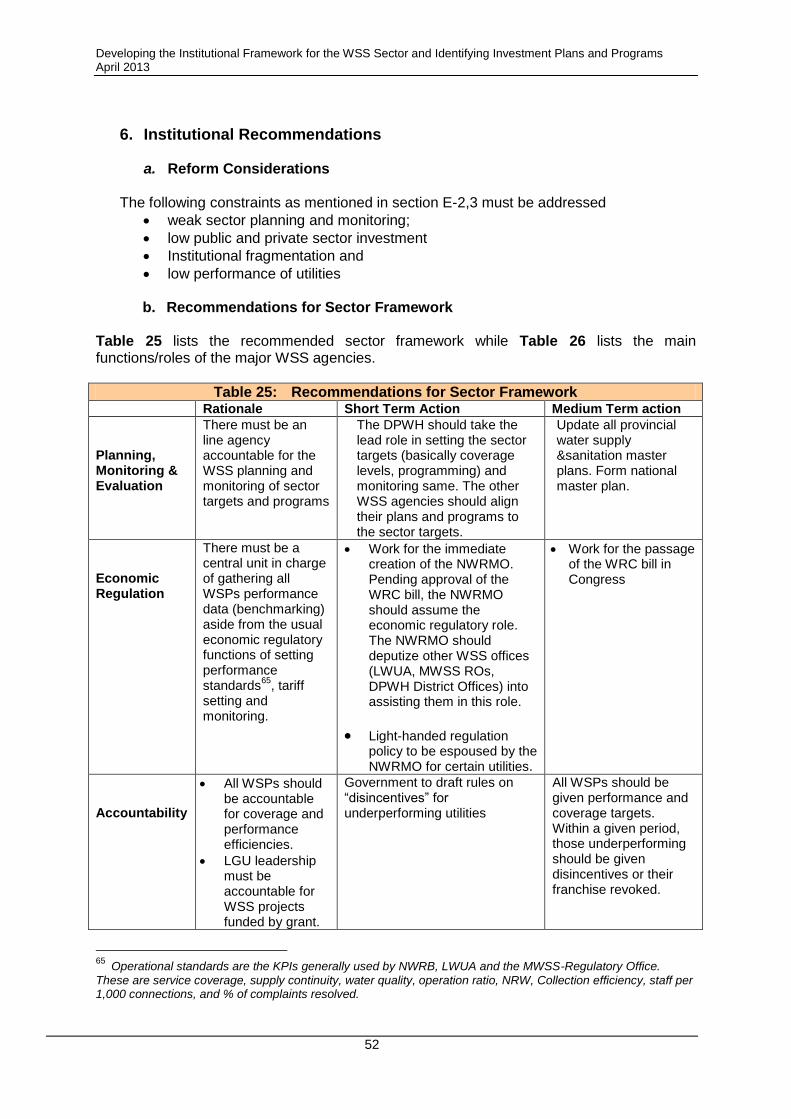

14. Table VII lists the recommended sector framework while Table VIII lists the main

functions/roles of the major WSS agencies.

3 Includes capacity development costs but excludes financing and replacement costs

4 Php 15.31B

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

5

Table VII: Sector Framework

Rationale Short Term Action Medium Term action

Planning & Monitoring

There must be a line agency accountable for the WSS planning and monitoring of sector targets and programs

The DPWH should take the lead role in setting the sector targets (basically coverage levels, programming) and monitoring same. The other WSS agencies should align their plans and programs to the sector targets.

Update all provincial water supply &sanitation master plans. Form national master plan.

Economic Regulation

There must be a central unit in charge of gathering all WSPs performance data (benchmarking) aside from the usual economic regulatory functions of setting performance standards, tariff setting and monitoring.

Work for the immediate creation of the NWRMO. Pending approval of the WRC bill, the NWRMO should assume the economic regulatory role. The NWRMO should deputize other WSS offices (LWUA, MWSS ROs, and DPWH District Offices) into assisting them in this role. Light-handed regulation policy to be espoused by the NWRMO for CBOs.

Work for the passage of the WRC bill in Congress

Accountability All WSPs should be accountable for coverage and performance efficiencies. LGU leadership must be accountable for WSS projects funded by grant.

All WSPs should be given performance and coverage targets. Within a given period, those underperforming should be given disincentives or their franchise revoked.

Government to draft rules on “disincentives” for underperforming utilities

Financing Rationalization of government subsidies Ensure implementation of cost-recovery tariffs

Government must provide grants only for source facilities and poor income group house connections for all government operated systems. DPWH and LWUA to implement this program.

The following should be pre-conditions for LGU grants:

o Ring fenced o Under regulatory ambit of NWRB

All piped systems should be funded based on a loan-grant mix. “Salintubig” subsidy amount should be dependent on service level to be implemented.

Subsequent grants should depend on WSP KPIs performance. Source facilities should be contracted to the private sector…drilling or bulk supply. Policies on subsidies to be formulated and widely disseminated.

Capacity Building

The LWUA , DPWH District Offices, the DILG PMO must be

LWUA to implement rationalization plan and be strengthened

LWUA to be given project subsidies for source development ,

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

6

strengthened so they can assist other agencies or WSPs in their capacity building programs

DPWH district offices to undergo source development training. LWUA and DILG to agree on delineation of WSPs to be trained

capacity building, low interest or subsidy funding for small and medium sized WDs.

Policies There are no clear cut policies on “graduation”, definition of cost recovery tariffs.

A graduation policy (waterless, creditworthiness) must be established based on amount of grant funding given. Creditworthy policies to be reviewed (or scrapped).

Additional grants should be dependent on WSP performance.

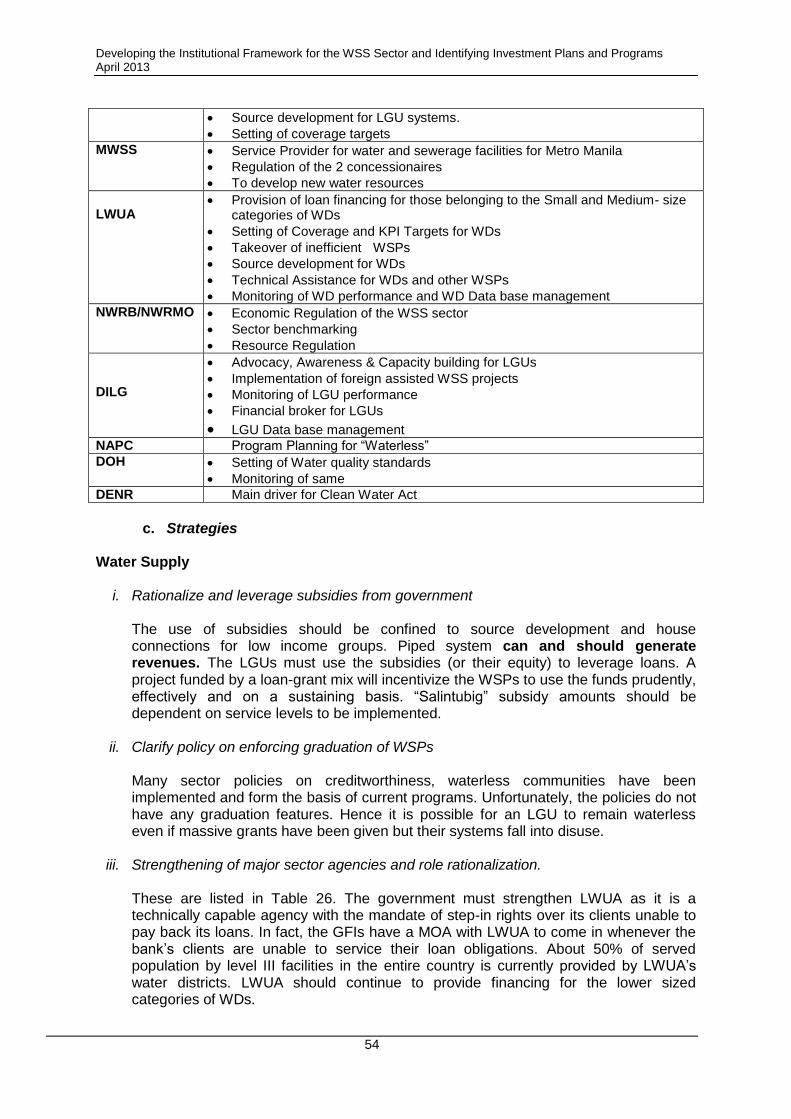

Table VIII: Major Roles of Agencies Agency Major Roles/Functions

NEDA Preparation of the MTPDP

Program/Project review and appraisal

Review of ODA assistance for conformity with national plans and policies

Policy Formulation DPWH Preparation of WSS sector master plan and targets

Monitoring of WSP performance

Funding support for WSS projects

Source development for LGU systems.

Setting of coverage targets

Implementation of the NSSMP

MWSS Service Provider for water and sewerage facilities for Metro Manila

Regulation of the 2 concessionaires

LWUA Provision of loan financing for those belonging to the Small and Medium- size categories of WDs

Setting of Coverage and KPI Targets for WDs

Takeover of inefficient WSPs

Source development for WDs

Technical Assistance for WDs and other WSPs

Monitoring of WD performance and WD Data base management

NWRB/NWRMO Economic Regulation of the WSS sector

Sector benchmarking

DILG Advocacy, Awareness & Capacity building for LGUs

Implementation of foreign assisted WSS projects

Monitoring of LGU performance

Financial broker for LGUs

LGU Data base management NAPC Program Planning for “Waterless” level I

DOH Setting of Water quality standards

Monitoring of same

DENR Main driver for Clean Water Act

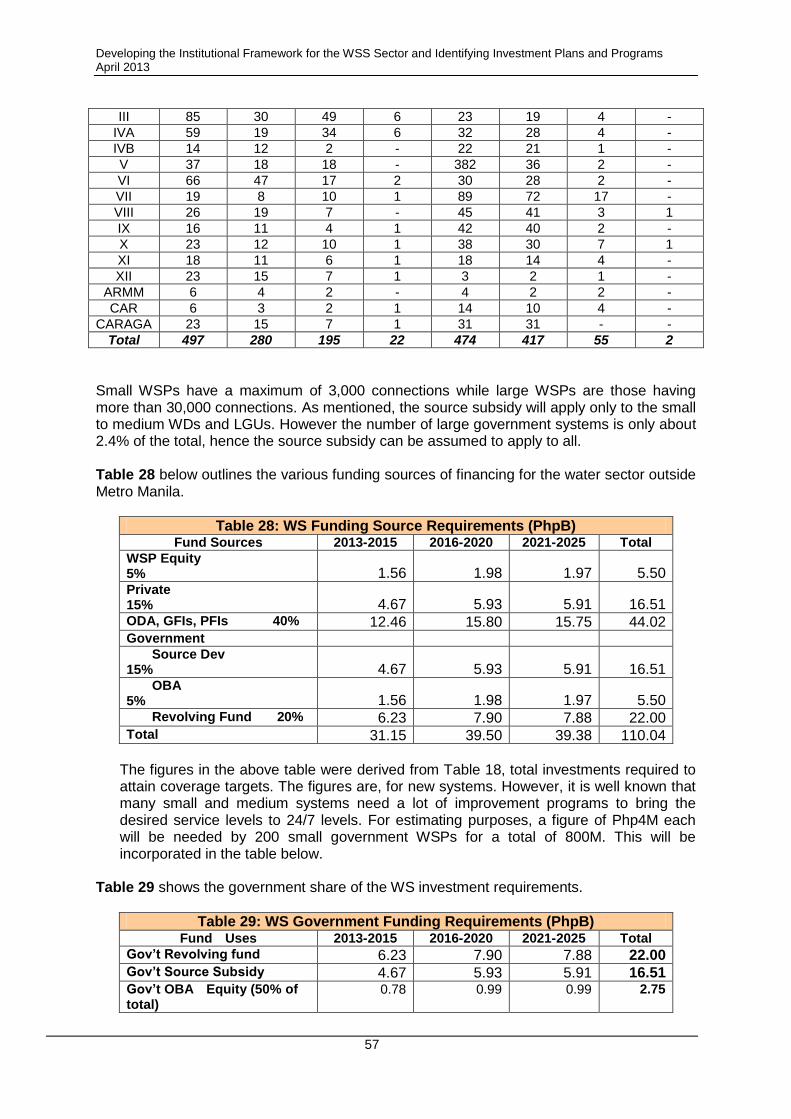

15. The following programs should be continued/implemented by the national government:

i) The Salintubig Program and the MDGF 1919 of the DILG is the first program to be continued up to 2016 but certain changes must be instituted. The recommended reforms are:

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

7

Only level II and III facilities should be given a budget of from Php 5-10M. Level I facilities must be allocated a maximum of only Php 2M.

LGU tariffs must be set through an ordinance prior to fund disbursement, otherwise, the subsidy shall be considered an interest free loan…to be paid from the LGU Internal Revenue Allotment Fund.

Groundwater source development activities shall be assisted by the LWUA and DPWH technical staff.

A graduation policy for waterless communities be formulated and implemented strictly.

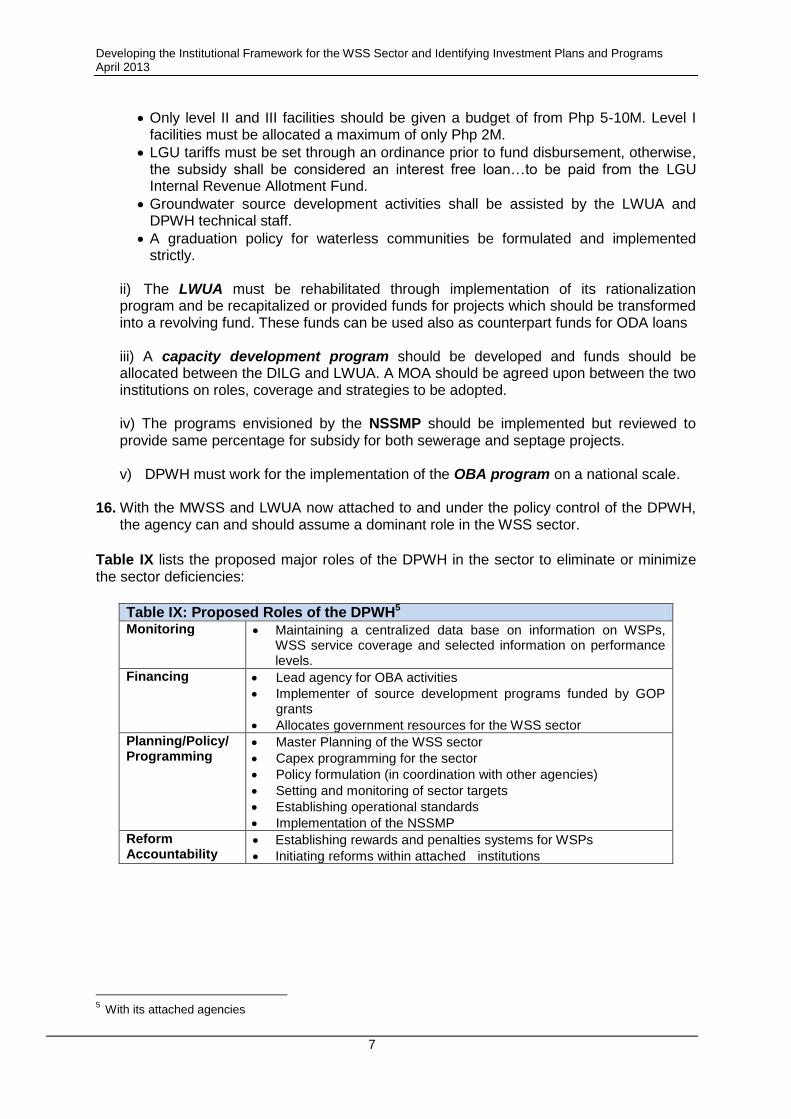

ii) The LWUA must be rehabilitated through implementation of its rationalization program and be recapitalized or provided funds for projects which should be transformed into a revolving fund. These funds can be used also as counterpart funds for ODA loans

iii) A capacity development program should be developed and funds should be allocated between the DILG and LWUA. A MOA should be agreed upon between the two institutions on roles, coverage and strategies to be adopted. iv) The programs envisioned by the NSSMP should be implemented but reviewed to provide same percentage for subsidy for both sewerage and septage projects. v) DPWH must work for the implementation of the OBA program on a national scale.

16. With the MWSS and LWUA now attached to and under the policy control of the DPWH,

the agency can and should assume a dominant role in the WSS sector.

Table IX lists the proposed major roles of the DPWH in the sector to eliminate or minimize the sector deficiencies:

Table IX: Proposed Roles of the DPWH5 Monitoring Maintaining a centralized data base on information on WSPs,

WSS service coverage and selected information on performance levels.

Financing Lead agency for OBA activities

Implementer of source development programs funded by GOP grants

Allocates government resources for the WSS sector

Planning/Policy/ Programming

Master Planning of the WSS sector

Capex programming for the sector

Policy formulation (in coordination with other agencies)

Setting and monitoring of sector targets

Establishing operational standards

Implementation of the NSSMP

Reform Accountability

Establishing rewards and penalties systems for WSPs

Initiating reforms within attached institutions

5 With its attached agencies

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

8

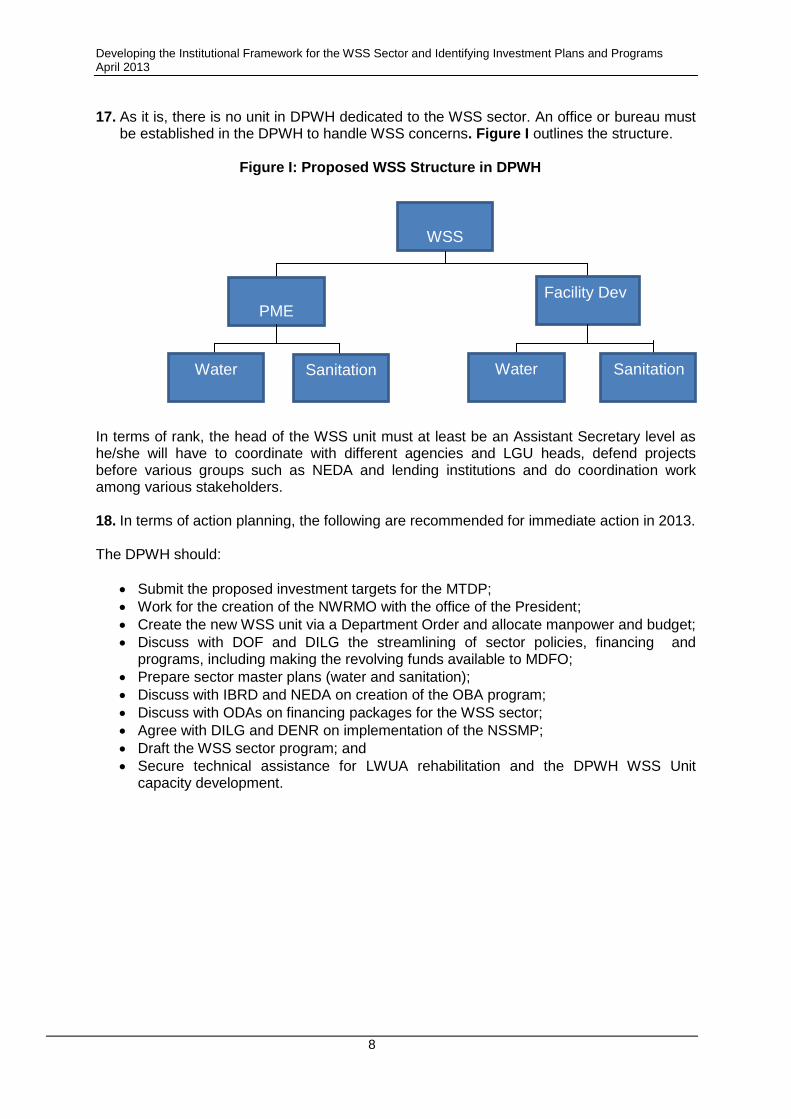

17. As it is, there is no unit in DPWH dedicated to the WSS sector. An office or bureau must be established in the DPWH to handle WSS concerns. Figure I outlines the structure.

Figure I: Proposed WSS Structure in DPWH

In terms of rank, the head of the WSS unit must at least be an Assistant Secretary level as he/she will have to coordinate with different agencies and LGU heads, defend projects before various groups such as NEDA and lending institutions and do coordination work among various stakeholders.

18. In terms of action planning, the following are recommended for immediate action in 2013. The DPWH should:

Submit the proposed investment targets for the MTDP;

Work for the creation of the NWRMO with the office of the President;

Create the new WSS unit via a Department Order and allocate manpower and budget;

Discuss with DOF and DILG the streamlining of sector policies, financing and programs, including making the revolving funds available to MDFO;

Prepare sector master plans (water and sanitation);

Discuss with IBRD and NEDA on creation of the OBA program;

Discuss with ODAs on financing packages for the WSS sector;

Agree with DILG and DENR on implementation of the NSSMP;

Draft the WSS sector program; and

Secure technical assistance for LWUA rehabilitation and the DPWH WSS Unit capacity development.

WSS

Facility Dev PME

Sanitation Water Sanitation Water

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

9

A. INTRODUCTION

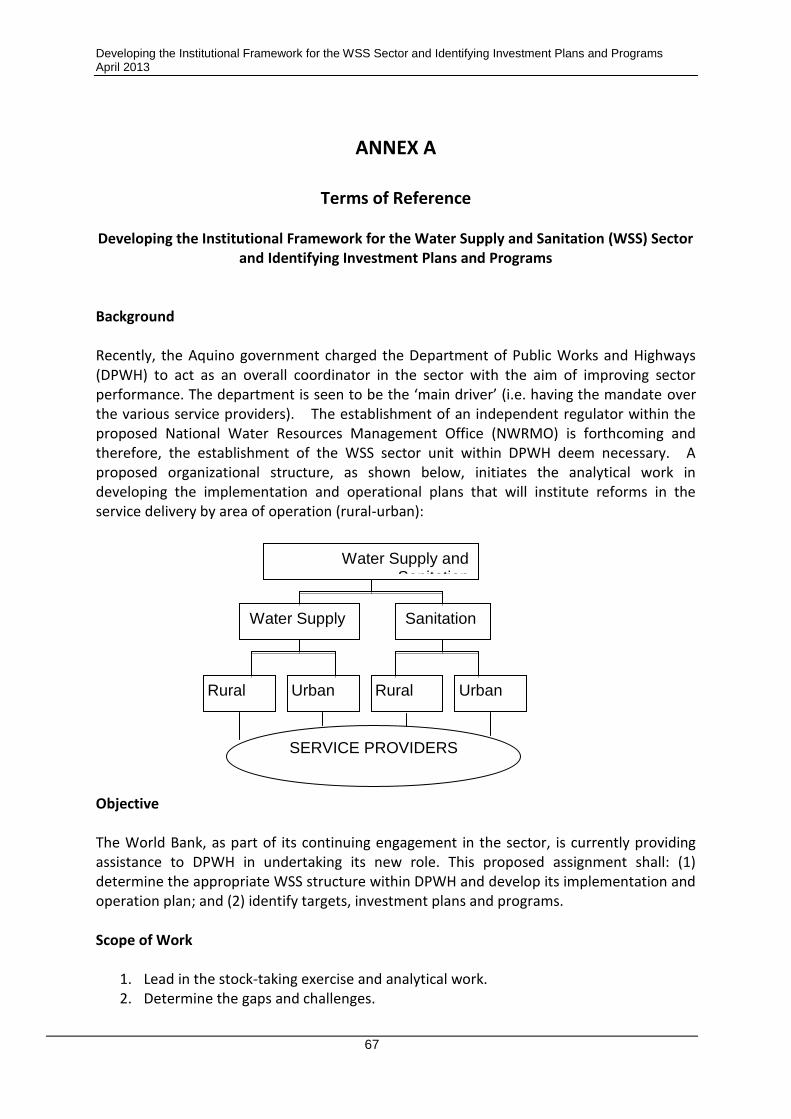

1. Background In 2011, the Aquino government charged the Department of Public Works and Highways (DPWH) to act as an overall coordinator in the water supply and sanitation (WSS) sector with the aim of improving sector performance. The department is seen to be the ‘main driver’ (i.e., having the mandate over the various service providers) and is the lead agency under the Inter-Agency Committee on Water that formulated the development and implementation plan of the proposed National Water Resources Management Office (NWRMO). The Secretary of the DPWH was appointed as the “Water Czar” to promote the development of the sector. With the water supply millennium development goal (MDG) targets due by 2015 and with the water supply roadmap envisioning universal coverage by 2025, there is a need to establish the extent of investment required to improve water supply coverage and to sustain water supply operation through improved governance of water service providers and local governments. A team, through a Technical Assistance (TA) of the World Bank, was engaged to (1) determine the appropriate WSS structure within DPWH and develop its implementation and operation plan, and (2) identify targets, investment plans, and programs.

2. Terms of Reference (shown as Annex A)

a. Objective This assignment shall: (1) determine the appropriate WSS structure within DPWH and develop its implementation and operation plan; and (2) identify targets, investment plans, and programs.

b. Scope of Work

i. Determine the gaps and challenges within the short-term (2015), medium-term (2020) and long-term period (2025);

ii. Develop an institutional framework of the WSS sector within DPWH and develop

implementation and operational plan; iii. Identify (politically) feasible actions or policy recommendations to improve the service

provision:

Determine interim or ‘quick-wins’ actions that can be undertaken.

Identify key elements that can be changed gradually in the short-to-medium-term (evolving role of Local Water Utilities Administration (LWUA), water districts (WDs), local government units (LGUs), etc.) and provide recommendation on how to bring about these changes;

iv. For each of the recommendations, identify:

Rationale for any recommended changes, i.e., problems or challenges that the recommended changes will be addressing

Policy instruments (Executive Orders [EOs.], Administrative Orders[AOs], etc.) needed to implement the changes

Action plan for implementing the recommendations

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

10

Key players involved

Expected outcomes; and

v. Develop a Policy Note and presentation materials for government decision makers based on the above work.

3. Methodology/Approach

The following methodology and approach was agreed upon with World Bank and the team members:

i. Determination of the major agencies and other organizations which would have data on the type of utilities, their location, and number of service connections (levels II and III). Design of the form for the stock taking data;

ii. Assignment of the study team members to each of these agencies for stock taking

activities and interaction with various officials of the agencies/organizations identified;

iii. While the stock taking activities are on-going, the following activities are parallel activities: - Population projections for all the towns/cities with the 2010 census data as baseline; Gathering of data for cost estimating purposes - Review of past sector reports to have an overview of reforms recommended;

iv. Tabulation of the data gathered, i.e., type of WSPs, connections, and other data to

determine population served with Level III/II facilities;

v. Determination of the demand gap by towns/cities;

vi. Determination of the targeted % served by level III/II systems for the different design years, 2015, 2020 and 2025;

vii. Determination of the unit-system cost in building a level III and II system, including the

upgrading of level IIs to level IIIs;

viii. Identification of the total Investment requirements and the programs needed;

ix. Determination of the roles of the DPWH within the water sector and preparation of its institutional framework; and

x. Recommend sector roles for the different agencies.

4. Study Limitations

i. It is impossible to determine the population served by potable water as potability has its own parameters (meeting Philippine National Standards for Drinking Water [PNSDW] standards, monthly microbiological tests, chlorine residual data, etc.). Hence, the study will get the population served only by level III and II facilities as the served population with no value judgement on potability.

ii. Many of the stock taking data from the LGUs/CBOs have been supplied by the

Department of Interior and Local Government (DILG) regional offices. However, some LGUs have not been able to submit WSS data as of March 2013. When no current

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

11

data from an LGU is obtained, data from past sector studies will be used whenever available and applicable.

iii. The team had planned on securing data on financial ratios (operating ratio) to

determine sustainability of the existing facilities. However, initial discussions with the agencies reveal that such data is either not available or is inaccurate. Only the WDs have such data.

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

12

B. SECTOR ASSESSMENT

1. Water and Sanitation Sector Overview

a. Sector Institutions and their Roles

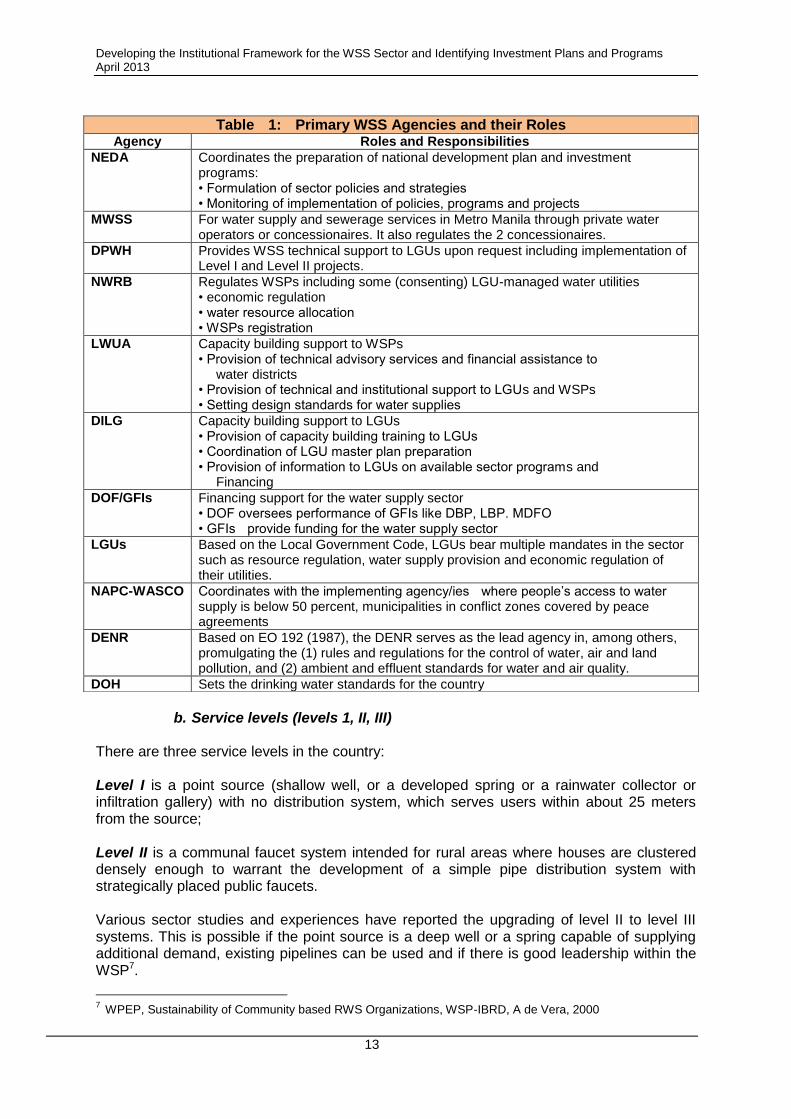

The major agencies involved in the sector are the National Economic Development Authority (NEDA), Department of Public Works and Highways (DPWH), Department of Finance (DOF), Department of Interior and Local Government (DILG), Department of Environment and Natural Resources (DENR), the Metropolitan Waterworks and Sewerage System (MWSS), Local Water Utilities Administration (LWUA), the National Water Resources Board (NWRB). Except for the MWSS, LWUA and the NWRB which are dedicated sector agencies, sector involvement among the rest merely form part of their overall mandates.

Local government units (LGUs) also play a critical role in the sector especially due to their area management role in local territories. Under the 2004-2010 Medium-Term Philippine Development Plan (MTPDP), the National Anti-Poverty Commission Water Supply Coordination Office (NAPC-WASCO) was created as the central coordinating unit for the implementation of the President’s Priority Program on Water (P3W). This program gives special attention to “waterless” LGUs. Several agencies appropriate oversight responsibilities for the sector resulting to overlaps in resource and economic regulation. The DENR and LGUs both have resource regulatory functions. On the other hand, while economic regulation is the core function of the NWRB, the same role is also played by LGUs (for LGU-run utilities), LWUA (for water districts), MWSS (for private water supply providers in Metro Manila) and other local Regulatory Boards created by LGUs to regulate private WSPs. Table 1 shows the delineated roles and responsibilities of the major agencies in the sector as of 2012. General policies concerning the water and sanitation sector are formulated by the NEDA in its Medium-Term Philippines Development Plan (MTPDP). Examples of general policies are decentralization of water supply provision, use of public-private partnership (PPP) and coverage targets. The MTPDP 2004–2010 aims at extending coverage of potable water to 92%–96% by 2010 through public and private investment, with priority given to 400 barangays with poor water supply coverage.[6 The responsibilities are defined by the 1976 Water Code of the Philippines and the 2004 Clean Water Act, which consolidated laws on water supply and sanitation and water resources management. The DOF takes the lead in financing water policies at the national level. The NWRB, under the DENR, is responsible for water resources management. However, the NWRB has limited capacity to execute these functions because of inadequate financial and technical capacities. The DPWH provides technical assistance in rural water supply systems. National standards for drinking water quality, as well as standards concerning sanitation and sewerage collection, are set by the Department of Health (DOH).

6

National Economic and Development Authority (NEDA) (2004). Medium-Term Philippine Development Plan 2004–2010

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

13

b. Service levels (levels 1, II, III)

There are three service levels in the country:

Level I is a point source (shallow well, or a developed spring or a rainwater collector or infiltration gallery) with no distribution system, which serves users within about 25 meters from the source; Level II is a communal faucet system intended for rural areas where houses are clustered densely enough to warrant the development of a simple pipe distribution system with strategically placed public faucets.

Various sector studies and experiences have reported the upgrading of level II to level III systems. This is possible if the point source is a deep well or a spring capable of supplying additional demand, existing pipelines can be used and if there is good leadership within the WSP7.

7 WPEP, Sustainability of Community based RWS Organizations, WSP-IBRD, A de Vera, 2000

Table 1: Primary WSS Agencies and their Roles Agency Roles and Responsibilities

NEDA Coordinates the preparation of national development plan and investment programs: • Formulation of sector policies and strategies • Monitoring of implementation of policies, programs and projects

MWSS For water supply and sewerage services in Metro Manila through private water operators or concessionaires. It also regulates the 2 concessionaires.

DPWH Provides WSS technical support to LGUs upon request including implementation of Level I and Level II projects.

NWRB Regulates WSPs including some (consenting) LGU-managed water utilities • economic regulation • water resource allocation • WSPs registration

LWUA Capacity building support to WSPs • Provision of technical advisory services and financial assistance to water districts • Provision of technical and institutional support to LGUs and WSPs • Setting design standards for water supplies

DILG Capacity building support to LGUs • Provision of capacity building training to LGUs • Coordination of LGU master plan preparation • Provision of information to LGUs on available sector programs and Financing

DOF/GFIs Financing support for the water supply sector • DOF oversees performance of GFIs like DBP, LBP. MDFO • GFIs provide funding for the water supply sector

LGUs Based on the Local Government Code, LGUs bear multiple mandates in the sector such as resource regulation, water supply provision and economic regulation of their utilities.

NAPC-WASCO Coordinates with the implementing agency/ies where people’s access to water supply is below 50 percent, municipalities in conflict zones covered by peace agreements

DENR Based on EO 192 (1987), the DENR serves as the lead agency in, among others, promulgating the (1) rules and regulations for the control of water, air and land pollution, and (2) ambient and effluent standards for water and air quality.

DOH Sets the drinking water standards for the country

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

14

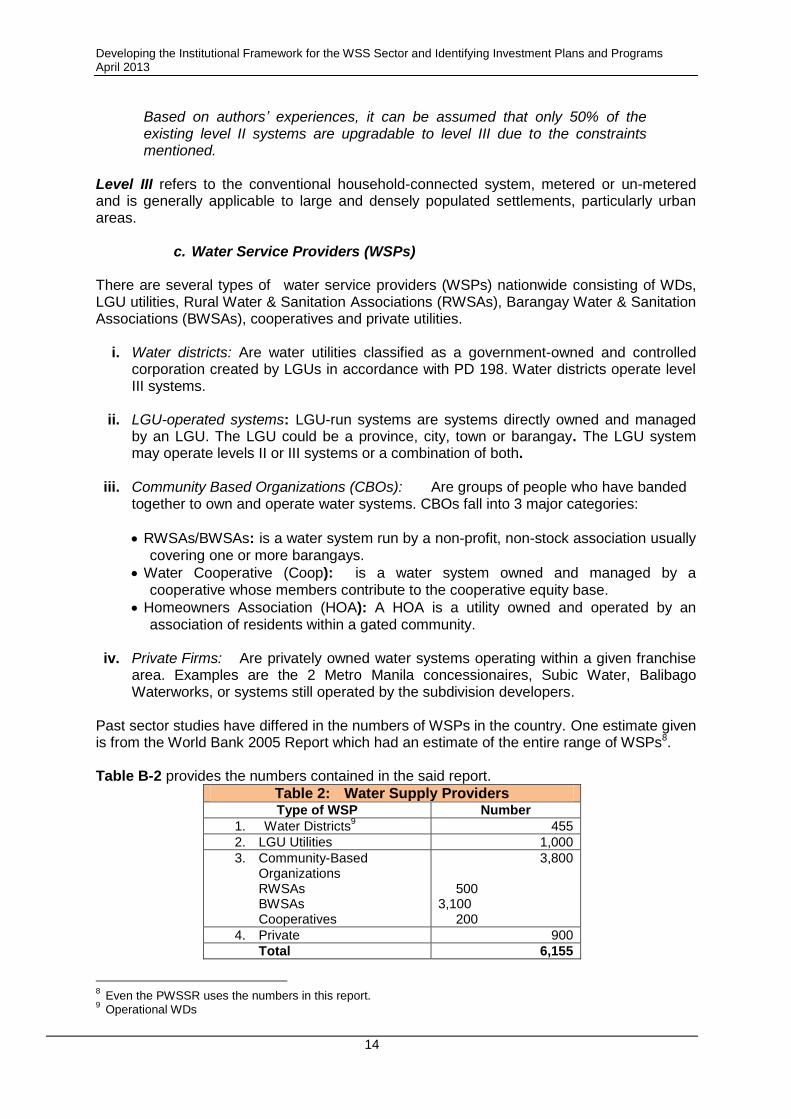

Based on authors’ experiences, it can be assumed that only 50% of the existing level II systems are upgradable to level III due to the constraints mentioned.

Level III refers to the conventional household-connected system, metered or un-metered and is generally applicable to large and densely populated settlements, particularly urban areas.

c. Water Service Providers (WSPs)

There are several types of water service providers (WSPs) nationwide consisting of WDs, LGU utilities, Rural Water & Sanitation Associations (RWSAs), Barangay Water & Sanitation Associations (BWSAs), cooperatives and private utilities.

i. Water districts: Are water utilities classified as a government-owned and controlled

corporation created by LGUs in accordance with PD 198. Water districts operate level III systems.

ii. LGU-operated systems: LGU-run systems are systems directly owned and managed

by an LGU. The LGU could be a province, city, town or barangay. The LGU system may operate levels II or III systems or a combination of both.

iii. Community Based Organizations (CBOs): Are groups of people who have banded

together to own and operate water systems. CBOs fall into 3 major categories:

RWSAs/BWSAs: is a water system run by a non-profit, non-stock association usually covering one or more barangays.

Water Cooperative (Coop): is a water system owned and managed by a cooperative whose members contribute to the cooperative equity base.

Homeowners Association (HOA): A HOA is a utility owned and operated by an association of residents within a gated community.

iv. Private Firms: Are privately owned water systems operating within a given franchise

area. Examples are the 2 Metro Manila concessionaires, Subic Water, Balibago Waterworks, or systems still operated by the subdivision developers.

Past sector studies have differed in the numbers of WSPs in the country. One estimate given is from the World Bank 2005 Report which had an estimate of the entire range of WSPs8. Table B-2 provides the numbers contained in the said report.

Table 2: Water Supply Providers Type of WSP Number

1. Water Districts9 455

2. LGU Utilities 1,000

3. Community-Based Organizations RWSAs BWSAs Cooperatives

3,800

500 3,100 200

4. Private 900

Total 6,155

8

Even the PWSSR uses the numbers in this report. 9 Operational WDs

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

15

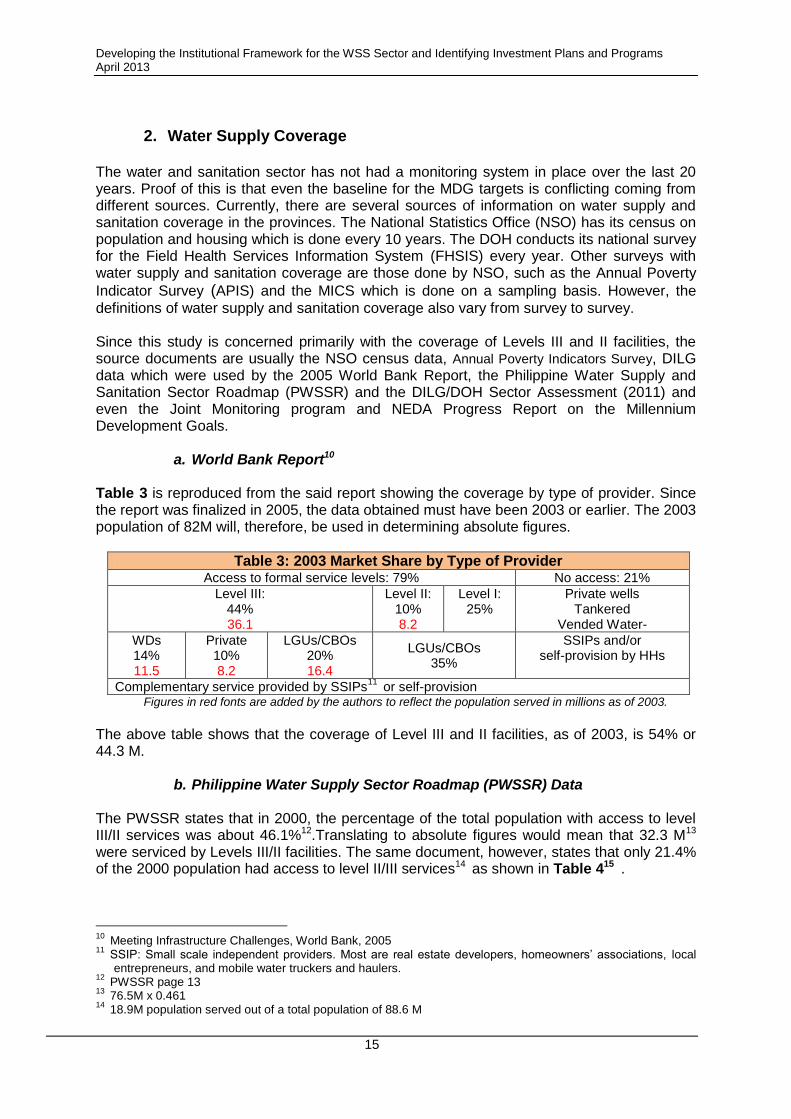

2. Water Supply Coverage

The water and sanitation sector has not had a monitoring system in place over the last 20 years. Proof of this is that even the baseline for the MDG targets is conflicting coming from different sources. Currently, there are several sources of information on water supply and sanitation coverage in the provinces. The National Statistics Office (NSO) has its census on population and housing which is done every 10 years. The DOH conducts its national survey for the Field Health Services Information System (FHSIS) every year. Other surveys with water supply and sanitation coverage are those done by NSO, such as the Annual Poverty

Indicator Survey (APIS) and the MICS which is done on a sampling basis. However, the

definitions of water supply and sanitation coverage also vary from survey to survey. Since this study is concerned primarily with the coverage of Levels III and II facilities, the source documents are usually the NSO census data, Annual Poverty Indicators Survey, DILG data which were used by the 2005 World Bank Report, the Philippine Water Supply and Sanitation Sector Roadmap (PWSSR) and the DILG/DOH Sector Assessment (2011) and even the Joint Monitoring program and NEDA Progress Report on the Millennium Development Goals.

a. World Bank Report10 Table 3 is reproduced from the said report showing the coverage by type of provider. Since the report was finalized in 2005, the data obtained must have been 2003 or earlier. The 2003 population of 82M will, therefore, be used in determining absolute figures.

Table 3: 2003 Market Share by Type of Provider Access to formal service levels: 79% No access: 21%

Level III: 44% 36.1

Level II: 10% 8.2

Level I: 25%

Private wells Tankered

Vended Water-

WDs 14% 11.5

Private 10% 8.2

LGUs/CBOs 20% 16.4

LGUs/CBOs 35%

SSIPs and/or self-provision by HHs

Complementary service provided by SSIPs11

or self-provision Figures in red fonts are added by the authors to reflect the population served in millions as of 2003.

The above table shows that the coverage of Level III and II facilities, as of 2003, is 54% or 44.3 M.

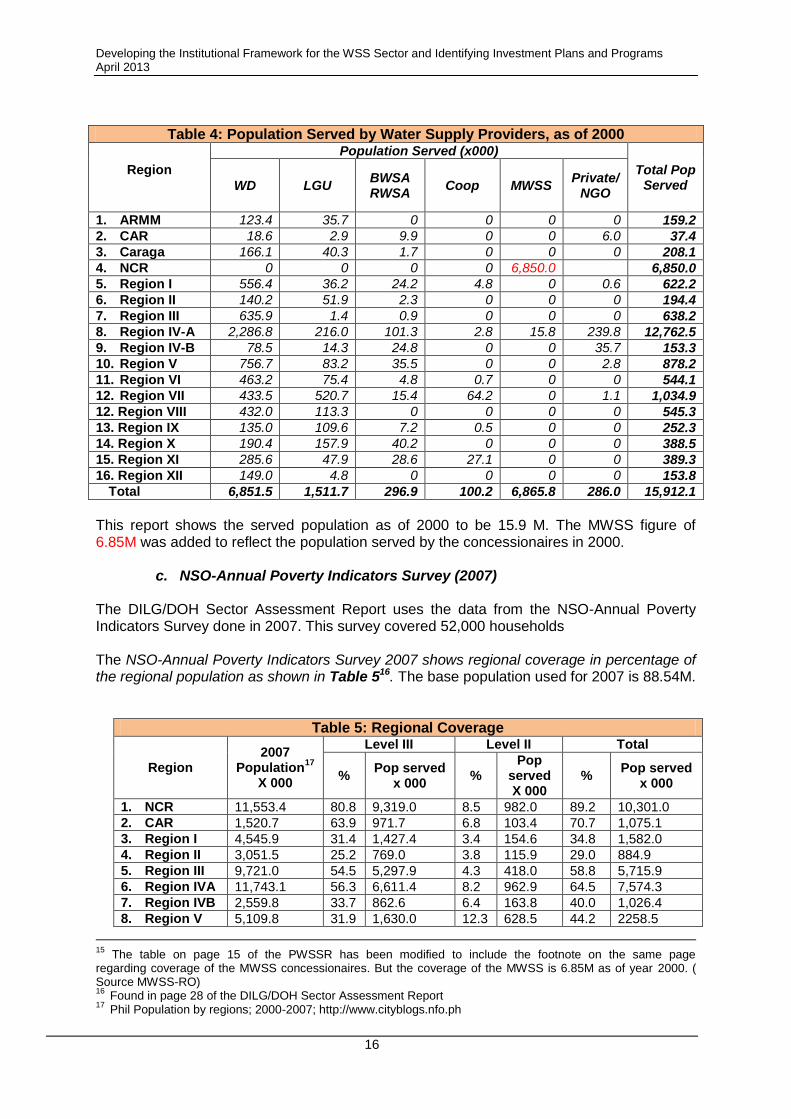

b. Philippine Water Supply Sector Roadmap (PWSSR) Data The PWSSR states that in 2000, the percentage of the total population with access to level III/II services was about 46.1%12.Translating to absolute figures would mean that 32.3 M13 were serviced by Levels III/II facilities. The same document, however, states that only 21.4% of the 2000 population had access to level II/III services14 as shown in Table 415 .

10

Meeting Infrastructure Challenges, World Bank, 2005 11

SSIP: Small scale independent providers. Most are real estate developers, homeowners’ associations, local entrepreneurs, and mobile water truckers and haulers.

12 PWSSR page 13

13 76.5M x 0.461

14 18.9M population served out of a total population of 88.6 M

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

16

Table 4: Population Served by Water Supply Providers, as of 2000

Region

Population Served (x000)

Total Pop Served WD LGU

BWSA RWSA

Coop MWSS Private/

NGO

1. ARMM 123.4 35.7 0 0 0 0 159.2

2. CAR 18.6 2.9 9.9 0 0 6.0 37.4

3. Caraga 166.1 40.3 1.7 0 0 0 208.1

4. NCR 0 0 0 0 6,850.0 6,850.0

5. Region I 556.4 36.2 24.2 4.8 0 0.6 622.2

6. Region II 140.2 51.9 2.3 0 0 0 194.4

7. Region III 635.9 1.4 0.9 0 0 0 638.2

8. Region IV-A 2,286.8 216.0 101.3 2.8 15.8 239.8 12,762.5

9. Region IV-B 78.5 14.3 24.8 0 0 35.7 153.3

10. Region V 756.7 83.2 35.5 0 0 2.8 878.2

11. Region VI 463.2 75.4 4.8 0.7 0 0 544.1

12. Region VII 433.5 520.7 15.4 64.2 0 1.1 1,034.9

12. Region VIII 432.0 113.3 0 0 0 0 545.3

13. Region IX 135.0 109.6 7.2 0.5 0 0 252.3

14. Region X 190.4 157.9 40.2 0 0 0 388.5

15. Region XI 285.6 47.9 28.6 27.1 0 0 389.3

16. Region XII 149.0 4.8 0 0 0 0 153.8

Total 6,851.5 1,511.7 296.9 100.2 6,865.8 286.0 15,912.1

This report shows the served population as of 2000 to be 15.9 M. The MWSS figure of 6.85M was added to reflect the population served by the concessionaires in 2000.

c. NSO-Annual Poverty Indicators Survey (2007)

The DILG/DOH Sector Assessment Report uses the data from the NSO-Annual Poverty Indicators Survey done in 2007. This survey covered 52,000 households The NSO-Annual Poverty Indicators Survey 2007 shows regional coverage in percentage of the regional population as shown in Table 516. The base population used for 2007 is 88.54M.

Table 5: Regional Coverage

Region 2007

Population17

X 000

Level III Level II Total

% Pop served

x 000 %

Pop served X 000

% Pop served

x 000

1. NCR 11,553.4 80.8 9,319.0 8.5 982.0 89.2 10,301.0

2. CAR 1,520.7 63.9 971.7 6.8 103.4 70.7 1,075.1

3. Region I 4,545.9 31.4 1,427.4 3.4 154.6 34.8 1,582.0

4. Region II 3,051.5 25.2 769.0 3.8 115.9 29.0 884.9

5. Region III 9,721.0 54.5 5,297.9 4.3 418.0 58.8 5,715.9

6. Region IVA 11,743.1 56.3 6,611.4 8.2 962.9 64.5 7,574.3

7. Region IVB 2,559.8 33.7 862.6 6.4 163.8 40.0 1,026.4

8. Region V 5,109.8 31.9 1,630.0 12.3 628.5 44.2 2258.5

15

The table on page 15 of the PWSSR has been modified to include the footnote on the same page regarding coverage of the MWSS concessionaires. But the coverage of the MWSS is 6.85M as of year 2000. ( Source MWSS-RO) 16

Found in page 28 of the DILG/DOH Sector Assessment Report 17

Phil Population by regions; 2000-2007; http://www.cityblogs.nfo.ph

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

17

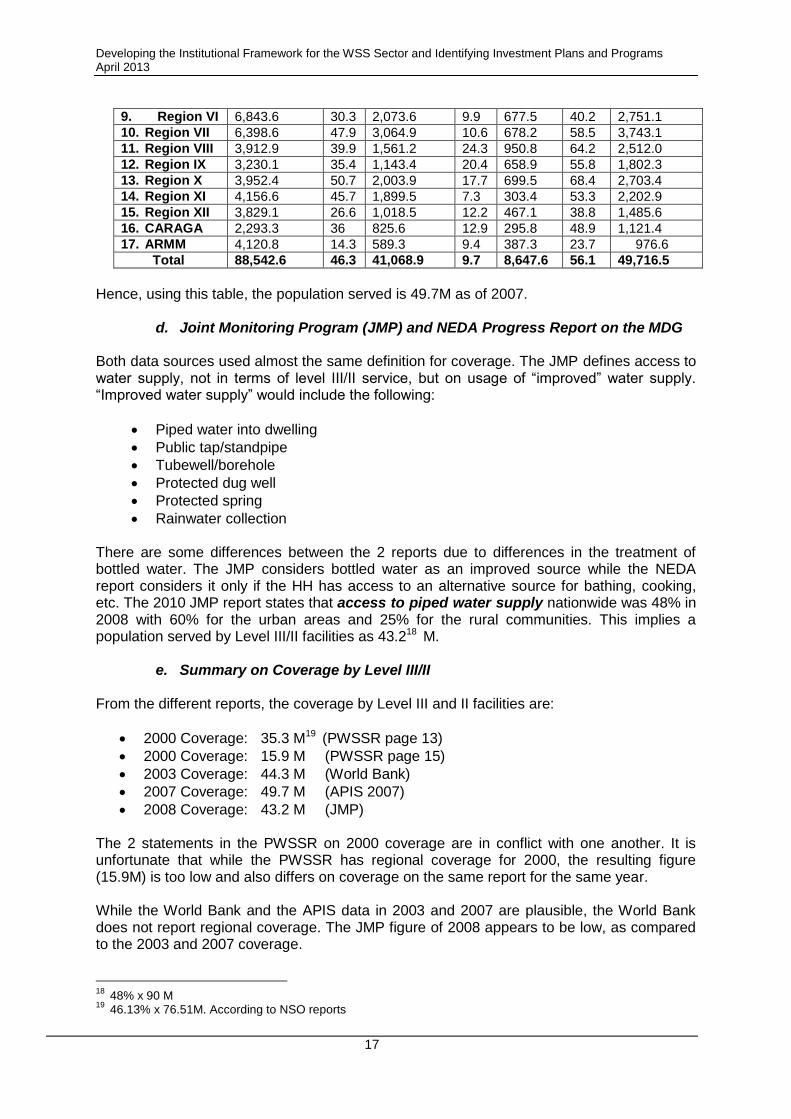

9. Region VI 6,843.6 30.3 2,073.6 9.9 677.5 40.2 2,751.1

10. Region VII 6,398.6 47.9 3,064.9 10.6 678.2 58.5 3,743.1

11. Region VIII 3,912.9 39.9 1,561.2 24.3 950.8 64.2 2,512.0

12. Region IX 3,230.1 35.4 1,143.4 20.4 658.9 55.8 1,802.3

13. Region X 3,952.4 50.7 2,003.9 17.7 699.5 68.4 2,703.4

14. Region XI 4,156.6 45.7 1,899.5 7.3 303.4 53.3 2,202.9

15. Region XII 3,829.1 26.6 1,018.5 12.2 467.1 38.8 1,485.6

16. CARAGA 2,293.3 36 825.6 12.9 295.8 48.9 1,121.4

17. ARMM 4,120.8 14.3 589.3 9.4 387.3 23.7 976.6

Total 88,542.6 46.3 41,068.9 9.7 8,647.6 56.1 49,716.5

Hence, using this table, the population served is 49.7M as of 2007.

d. Joint Monitoring Program (JMP) and NEDA Progress Report on the MDG Both data sources used almost the same definition for coverage. The JMP defines access to water supply, not in terms of level III/II service, but on usage of “improved” water supply. “Improved water supply” would include the following:

Piped water into dwelling

Public tap/standpipe

Tubewell/borehole

Protected dug well

Protected spring

Rainwater collection

There are some differences between the 2 reports due to differences in the treatment of bottled water. The JMP considers bottled water as an improved source while the NEDA report considers it only if the HH has access to an alternative source for bathing, cooking, etc. The 2010 JMP report states that access to piped water supply nationwide was 48% in 2008 with 60% for the urban areas and 25% for the rural communities. This implies a population served by Level III/II facilities as 43.218 M.

e. Summary on Coverage by Level III/II

From the different reports, the coverage by Level III and II facilities are:

2000 Coverage: 35.3 M19 (PWSSR page 13)

2000 Coverage: 15.9 M (PWSSR page 15)

2003 Coverage: 44.3 M (World Bank)

2007 Coverage: 49.7 M (APIS 2007)

2008 Coverage: 43.2 M (JMP) The 2 statements in the PWSSR on 2000 coverage are in conflict with one another. It is unfortunate that while the PWSSR has regional coverage for 2000, the resulting figure (15.9M) is too low and also differs on coverage on the same report for the same year. While the World Bank and the APIS data in 2003 and 2007 are plausible, the World Bank does not report regional coverage. The JMP figure of 2008 appears to be low, as compared to the 2003 and 2007 coverage.

18

48% x 90 M 19

46.13% x 76.51M. According to NSO reports

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

18

This report will use both the 2003 coverage figure of the World Bank Report and the NSO-APIS 2007 regional data for comparison of existing data.

3. MDGs: Water Supply Targets

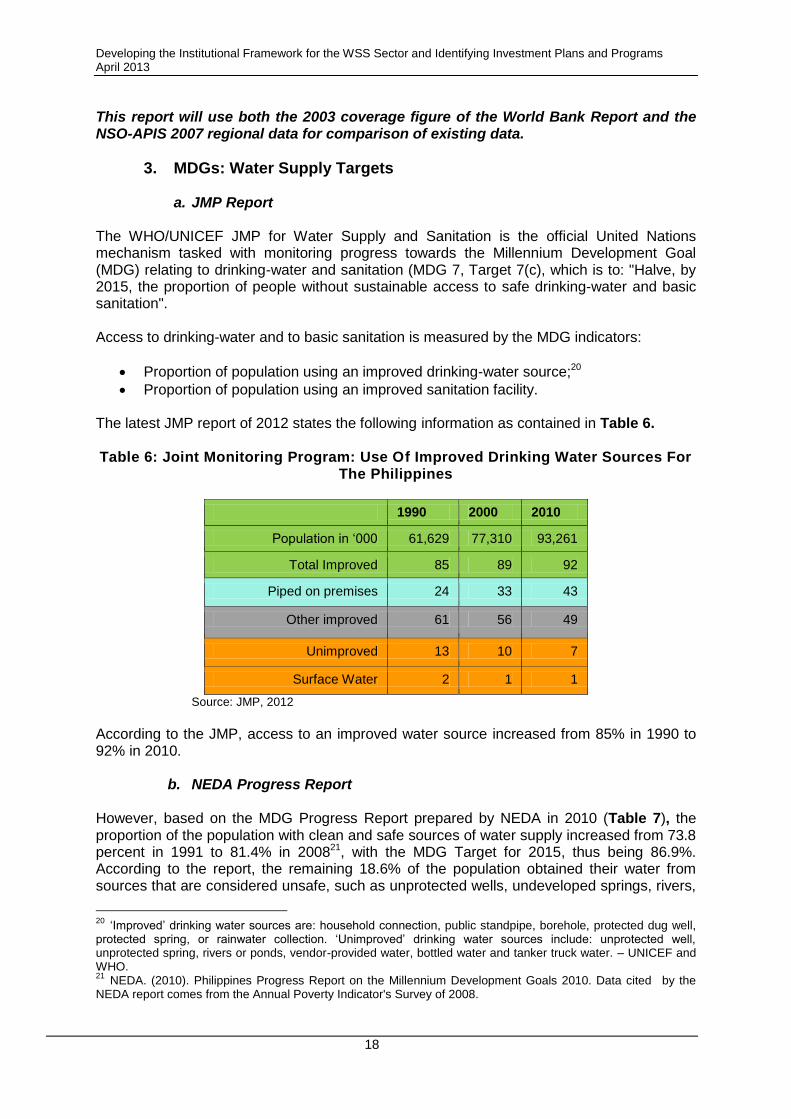

a. JMP Report

The WHO/UNICEF JMP for Water Supply and Sanitation is the official United Nations mechanism tasked with monitoring progress towards the Millennium Development Goal (MDG) relating to drinking-water and sanitation (MDG 7, Target 7(c), which is to: "Halve, by 2015, the proportion of people without sustainable access to safe drinking-water and basic sanitation".

Access to drinking-water and to basic sanitation is measured by the MDG indicators:

Proportion of population using an improved drinking-water source;20

Proportion of population using an improved sanitation facility.

The latest JMP report of 2012 states the following information as contained in Table 6.

Table 6: Joint Monitoring Program: Use Of Improved Drinking Water Sources For

The Philippines

1990 2000 2010

Population in ‘000 61,629 77,310 93,261

Total Improved 85 89 92

Piped on premises 24 33 43

Other improved 61 56 49

Unimproved 13 10 7

Surface Water 2 1 1

Source: JMP, 2012

According to the JMP, access to an improved water source increased from 85% in 1990 to 92% in 2010.

b. NEDA Progress Report

However, based on the MDG Progress Report prepared by NEDA in 2010 (Table 7), the proportion of the population with clean and safe sources of water supply increased from 73.8 percent in 1991 to 81.4% in 200821, with the MDG Target for 2015, thus being 86.9%. According to the report, the remaining 18.6% of the population obtained their water from sources that are considered unsafe, such as unprotected wells, undeveloped springs, rivers,

20

‘Improved’ drinking water sources are: household connection, public standpipe, borehole, protected dug well, protected spring, or rainwater collection. ‘Unimproved’ drinking water sources include: unprotected well, unprotected spring, rivers or ponds, vendor-provided water, bottled water and tanker truck water. – UNICEF and WHO. 21

NEDA. (2010). Philippines Progress Report on the Millennium Development Goals 2010. Data cited by the NEDA report comes from the Annual Poverty Indicator's Survey of 2008.

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

19

ponds, streams, rainwater, tanker trucks, and peddlers, among others.

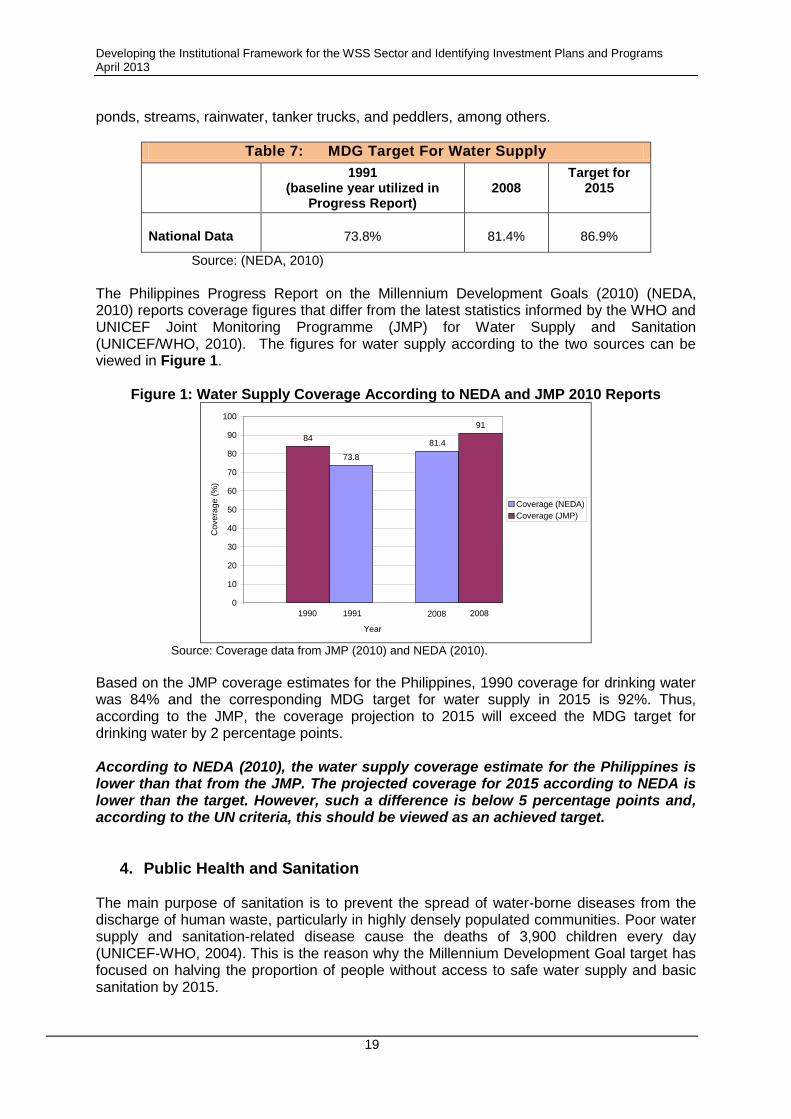

Table 7: MDG Target For Water Supply

1991 (baseline year utilized in

Progress Report) 2008

Target for 2015

National Data

73.8%

81.4%

86.9%

Source: (NEDA, 2010)

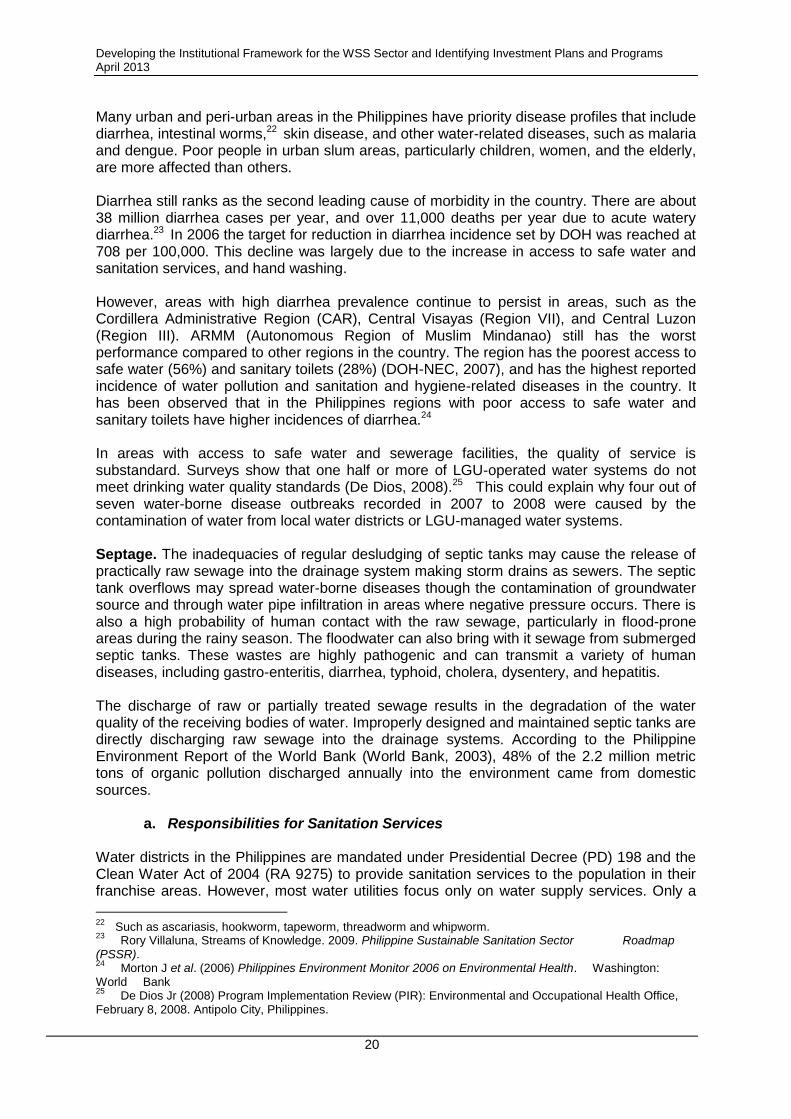

The Philippines Progress Report on the Millennium Development Goals (2010) (NEDA, 2010) reports coverage figures that differ from the latest statistics informed by the WHO and UNICEF Joint Monitoring Programme (JMP) for Water Supply and Sanitation (UNICEF/WHO, 2010). The figures for water supply according to the two sources can be viewed in Figure 1.

Figure 1: Water Supply Coverage According to NEDA and JMP 2010 Reports

73.8

81.484

91

0

10

20

30

40

50

60

70

80

90

100

1990 1991 2008

Year

Co

ve

rag

e (

%)

Coverage (NEDA)

Coverage (JMP)

1990 200820081991

Source: Coverage data from JMP (2010) and NEDA (2010).

Based on the JMP coverage estimates for the Philippines, 1990 coverage for drinking water was 84% and the corresponding MDG target for water supply in 2015 is 92%. Thus, according to the JMP, the coverage projection to 2015 will exceed the MDG target for drinking water by 2 percentage points. According to NEDA (2010), the water supply coverage estimate for the Philippines is lower than that from the JMP. The projected coverage for 2015 according to NEDA is lower than the target. However, such a difference is below 5 percentage points and, according to the UN criteria, this should be viewed as an achieved target.

4. Public Health and Sanitation The main purpose of sanitation is to prevent the spread of water-borne diseases from the discharge of human waste, particularly in highly densely populated communities. Poor water supply and sanitation-related disease cause the deaths of 3,900 children every day (UNICEF-WHO, 2004). This is the reason why the Millennium Development Goal target has focused on halving the proportion of people without access to safe water supply and basic sanitation by 2015.

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

20

Many urban and peri-urban areas in the Philippines have priority disease profiles that include diarrhea, intestinal worms,22 skin disease, and other water-related diseases, such as malaria and dengue. Poor people in urban slum areas, particularly children, women, and the elderly, are more affected than others. Diarrhea still ranks as the second leading cause of morbidity in the country. There are about 38 million diarrhea cases per year, and over 11,000 deaths per year due to acute watery diarrhea.23 In 2006 the target for reduction in diarrhea incidence set by DOH was reached at 708 per 100,000. This decline was largely due to the increase in access to safe water and sanitation services, and hand washing. However, areas with high diarrhea prevalence continue to persist in areas, such as the Cordillera Administrative Region (CAR), Central Visayas (Region VII), and Central Luzon (Region III). ARMM (Autonomous Region of Muslim Mindanao) still has the worst performance compared to other regions in the country. The region has the poorest access to safe water (56%) and sanitary toilets (28%) (DOH-NEC, 2007), and has the highest reported incidence of water pollution and sanitation and hygiene-related diseases in the country. It has been observed that in the Philippines regions with poor access to safe water and sanitary toilets have higher incidences of diarrhea.24 In areas with access to safe water and sewerage facilities, the quality of service is substandard. Surveys show that one half or more of LGU-operated water systems do not meet drinking water quality standards (De Dios, 2008).25 This could explain why four out of seven water-borne disease outbreaks recorded in 2007 to 2008 were caused by the contamination of water from local water districts or LGU-managed water systems. Septage. The inadequacies of regular desludging of septic tanks may cause the release of practically raw sewage into the drainage system making storm drains as sewers. The septic tank overflows may spread water-borne diseases though the contamination of groundwater source and through water pipe infiltration in areas where negative pressure occurs. There is also a high probability of human contact with the raw sewage, particularly in flood-prone areas during the rainy season. The floodwater can also bring with it sewage from submerged septic tanks. These wastes are highly pathogenic and can transmit a variety of human diseases, including gastro-enteritis, diarrhea, typhoid, cholera, dysentery, and hepatitis. The discharge of raw or partially treated sewage results in the degradation of the water quality of the receiving bodies of water. Improperly designed and maintained septic tanks are directly discharging raw sewage into the drainage systems. According to the Philippine Environment Report of the World Bank (World Bank, 2003), 48% of the 2.2 million metric tons of organic pollution discharged annually into the environment came from domestic sources.

a. Responsibilities for Sanitation Services Water districts in the Philippines are mandated under Presidential Decree (PD) 198 and the Clean Water Act of 2004 (RA 9275) to provide sanitation services to the population in their franchise areas. However, most water utilities focus only on water supply services. Only a

22

Such as ascariasis, hookworm, tapeworm, threadworm and whipworm. 23

Rory Villaluna, Streams of Knowledge. 2009. Philippine Sustainable Sanitation Sector Roadmap (PSSR). 24

Morton J et al. (2006) Philippines Environment Monitor 2006 on Environmental Health. Washington: World Bank 25

De Dios Jr (2008) Program Implementation Review (PIR): Environmental and Occupational Health Office, February 8, 2008. Antipolo City, Philippines.

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

21

few water districts have initiated activities for sanitation, mostly limited to providing septage collection services to septic tank users. Collected septage is commonly discharged in an uncontrolled manner in rivers and dumpsites. Due to the low priority given by WDs to sanitation, the main responsibility for sanitation lies largely with the LGUs. The existing legal and regulatory mechanisms are generally adequate, although some local governments are behind with implementation procedures. Most local government officials understand well the issues and approaches required. The major hindrances are the lack of budgets for monitoring, maintenance, and service expansion, and the lack of an urban management paradigm in which both government and the citizenry understand the problems, agree on the solutions, and are willing to take the steps necessary to improve prevailing conditions. While LGUs are mandated to provide essential services, including water and sanitation services, 97% of funds earmarked for water and sanitation go to water supply and only 3% for sanitation and wastewater treatment (Philippine Water Supply Roadmap, 2008).26 There have been pilot projects on sewerage and wastewater treatment implemented by national agencies and LGUs. However, some of them have become non-operational (e.g., stabilization pond in Cauayan, Isabela) due to poor operation and maintenance. Although some capacity building has been provided by development agencies without local government support, investment capital and long-term capacity building support, it will not result in effective sanitation and wastewater management programs. To ensure sustainability it is important that initiatives are broadly supported by all stakeholders, notably the communities, which need to be achieved through extensive and long-term awareness campaigns aimed at behavioral change and demand creation for sanitation services.

b. Sanitation Coverage

i) JMP 2010 Report Based on the 2010 WHO-UNICEF Joint Monitoring Program (JMP) Report, in 2008, total households with improved use of sanitation facilities reached 80% in the urban areas and 69% in the rural areas or a combined total of 76%. Based on this, the Philippine Sustainable Sanitation Roadmap (PSSR) states that projections for 2015, the year for which the MDG sanitation target is set, indicates that the 79% target coverage to meet the MDG, can be achieved27. In spite of this, 25% still have no access to sanitary facilities and 14% still practice open defecation in the rural areas. The Annual Poverty Indicator Survey (APIS) Report indicates that for households with sanitary toilet, the regions with the lowest coverage are ARMM (50.0%), Region VIII (77.7%), Region IX (78.6%), Regions VII and IVB (79.9%). Similar to water supply, data for sanitation is also conflicting. A DOH Field Health Information Survey report indicated that coverage is actually declining. In 2008, the Environmental Health Report says we have reached 76.8% coverage which is still way below the DOH’s National Objectives for Health (NOH) target of 91% in 2010. The MTPDP also targeted 86-91% coverage within the period 2004 to 2010. Moreover, while the MDG goals are about access to sanitary toilets, the issue on the quality of toilets, such as bottomless septic tanks and lack of adequate septage management, still needs to be addressed.

26

NEDA. 2008. Philippine Water Supply Sector Roadmap. 27

Government of the Philippines. 2007. Philippine Sustainable Sanitation Roadmap. Manila.

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

22

ii) Philippine Sustainable Sanitation Sector Roadmap Access to sanitation. Some 20 million Filipinos do not have access to improved sanitation, about 15 million share toilets, and 9% of the population still defecates in the open.28 On-site sanitation (latrines, many connected to septic tanks which, however, are generally poorly constructed) is the principle form of wastewater treatment in Philippine cities. Only an estimated 3% of the population is currently connected to a piped sewerage network. Outside of Metro Manila, only three cities (Baguio, Vigan and Zamboanga) have sewer systems, serving less than 3% of their service area populations (WPEP, 2003). The Vigan and Zamboanga systems were built by the Americans in the late 1920s or early 1930s. The systems cover limited areas in the downtown business districts and serve an insignificant portion of the urban population of the host cities (EMB, 2005 - National Water Quality Status Report: 2001 to 2005). Thus, domestic wastewater largely goes untreated (at least 90% according to the World Bank) and the majority of the population is exposed to raw sewage. The World Bank estimates that the Philippines lose $1.4 billion per year in the form of health, environmental, and economic costs.

iii) Phil Water Situation Report29

c. Sanitation Initiatives

i. National Sewerage and Septage Management Program (NSSMP). The NSSMP has been approved by NEDA in 2012. The NSSMP describes the needed institutional arrangements, financing options, and intervention and investment frameworks that will help LGUs and service providers develop sewerage, septage, and combined sewerage-septage projects. In the program, capital cost for septage management is estimated to range from PhP4 million to PhP71 million per project and per LGU, or a total of PhP12.3 billion for all the septage management undertakings. On the other hand, capital costs for sewerage systems are estimated at PhP820 million per highly urbanized city (HUC) at PhP410 million per phase or a total of PhP14 billion for 17 HUCs. Total capital costs for both septage management and sewerage systems are estimated at PhP26.3 billion. The LGU or local water districts shall shoulder cost for all septage management programs, while a 40-60 percent cost sharing for the sewerage systems shall be implemented (40% from the national government, 60% between HUCs and water districts). The 40% NG capital cost share, estimated to be about PhP5.6 billion, will be spread until 2020.

28

Rory Villaluna, Streams of Knowledge. 2009. Philippine Sustainable Sanitation Sector Roadmap (PSSSR). 29

WEDC Report, 2006

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

23

ii. Philippine Sanitation Alliance (PSA). This USAID technical assistance program began in 2007 and has facilitated six LGUs (including Dumaguete, municipalities in Mactan Island, and San Fernando in La Union) to implement septage management with reference to the relevant provisions in the Clean Water Act of 2004. The PSA program was due to finish in September 2011. The program at Dumaguete has been very successful. The septage treatment plant (SpTP) started operations in October 2010. There is 50:50 cost sharing between the WD and LGU. The SpTP for San Fernando is presently under construction. For sewerage development in highly urbanized areas outside Manila, the national government can provide 40% cost share. However, there is no cost sharing for septage management which is viewed to be affordable for beneficiaries (e.g., at Dumaguete P2/m3 of water used is added to the water bill).

5. WSS Sector Issues and Challenges.

The MTPDP (Medium Term Philippine Development Plan) identifies and prioritizes the issues and challenges besetting the sector. These include the disparities in water supply coverage across regions, depletion of groundwater (especially in Metro Manila and Metro Cebu), lack of cost recovery on investments, institutional weaknesses and low willingness of consumers to pay. Pollution of water sources poses an additional threat to the sustainability of water supply systems and exposes the population to environmentally-related diseases.

a. WSP Service Performance. Results of benchmarking conducted by DILG covering

45 utilities also reveal that performance levels of utilities based on key performance indicators still fall under ideal or industry standards. Among the WSPs covered, the LGUs have the most dismal performance in almost all of the indicators used in the study. Benchmarking of these WSPs and five more utilities will be updated under the

MDGF 1919 program30

being coordinated by NEDA and DILG.

The slow expansion of services, low quality of services and inefficient operations of

water utilities are attributed to the weak regulatory and financing framework in the sector, lack of technical and managerial capacity, lack of access to financing for WSS (water and sanitation) development and dependence on subsidies for the majority of service providers. Thus, regulatory, financing and utility reforms are imperative to drive WSPs to improve their service performance.

Utility reform measures such as ring-fencing, benchmarking, business planning and

performance contracting have been introduced as part of capacity building and performance improvement glide path for WSPs.

b. Regulation. NWRB, by virtue of RA 2677 (Public Service Law), regulates private

providers and LGU-run utilities. In 2002, EO 123 was issued to address the conflicting role of LWUA as both a financing institution and a regulator, by transferring the regulation of water districts to NWRB (2002). However the regulation of WDs was never really done by NWRB due to inadequate resources. In fact, NWRB wrote LWUA stating that the LWUA maintain the status quo until NWRB is able to do it. In 2010, EO 806 was issued transferring the administration of NWRB from the Office of the President to DENR. EO 860 also superseded EO 123 by transferring the regulation of

30

MDGF 1919 is a UNICEF-funded program called ”Enhancing Access to and Provision of water services with Active Participation of the Poor”. This involves the application and replication of water governance sound practices and other capacity development tools, to be piloted in 36 waterless municipalities in 5 regions.

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

24

water districts back to LWUA on the basis that the Water Code does not provide for the economic regulation of water service providers by NWRB. EO 860 glossed over the fact that the mandate given to NWRB to regulate water utilities was not contained in the Water Code but rather in the Public Service Act. The same EO also justified the removal of the DOF and DOH Secretaries from the board of NWRB.

In 2009 the Water Sub-Committee of INFRACOM endorsed the passage of a bill

proposing the creation of a Water Regulatory Commission (WRC) as the ideal solution to address the economic regulatory concerns of the sector. Patterned after the Energy Regulatory Commission, the purpose of the WRC is to consolidate all water regulatory powers, currently housed in several agencies, into one authority. It is envisioned that with the creation of the WRC, there will finally exist an oversight body for water supply and sanitation—setting targets, rationalizing tariffs across the country and attracting investments into the sector. The proposed bill has been filed in Congress in 2012.

In October 2011, President Benigno Aquino III issued Executive Order No. 62

mandating the creation of an Inter-Agency Committee on Water under the leadership of the Department of Public Works and Highways (DPWH), which was tasked to develop the Water Sector Master Plan that will effectively address the issues and concerns of the water sector. The Committee was likewise directed to recommend to the President the appropriate organizational structure of all concerned agencies for the effective implementation of the water sector master plan. The National Economic and Development Authority (NEDA), Department of Budget and Management (DBM), Department of Interior and Local Government (DILG), Office of the President (OP) and such other concerned agencies were made part of the Inter-agency Committee on Water.

NEDA and DPWH then jointly commissioned a study on the Preparation of the

Philippine Water Resources Sector Development Plan. The study was designed to develop a framework plan for the efficient and effective management of the country’s water resources. The result of the framework plan was the recommendation to reconstitute, elevate and strengthen the current NWRB into a National Water Resources Management Office (NWRMO) under the Office of the President through the issuance of an EO.

In 2012, a draft EO had been prepared creating the National Water Resources

Management Office. c. Financing. The financing policy for the sector calls for the rationalization of allocation

of public resources to focus on the identified 432 waterless barangays and municipalities, and to expand services of formal providers to unserved populations in respective franchise areas. The policy recognizes the scarcity of public resources, and thus espouses targeted subsidies and leveraging with private resources. However, it has been noted that national government subsidies were not directed to the Roadmap targets and, instead of improving the enabling environment for private financing institutions to lend to water supply and sanitation projects, government financing crowds out private bank financing. Specifically:

National government subsidy for waterless barangays and municipalities, amounting to P1.5 billion in 2009, was given to LWUA and was apparently used to support the revival and creation of new water districts. Although it may be argued that these investments contributed to service expansion, still the public

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

25

resources were not used for the top priority areas. Moreover, the sustainability of these revived or new water districts has to be assessed. If these new districts do not achieve technical and financial viability, then the investments would have been put to waste.

About 212 (40%) out of 524 municipalities identified as beneficiaries of this fund were not in the original list of 432; the identification of municipalities/ beneficiaries have become largely discretionary under the LWUA administration. The current Waterless Barangay Program is now (2013) being implemented by the DILG and NAPC (National Anti-Poverty Commission).

LWUA financing competed directly with private financing, instead of encouraging market-based lending for utilities that have the ability to access the capital market. LWUA offered deeply concessional terms and constricted the issuance of financing waivers for water districts to borrow from other sources. Without the waiver, water district loans outside of LWUA will be in junior positions.

Development partners have been seeking from the government unequivocal and operational rationalization guidelines on the allocation of grants and subsidies. In particular, devel-opment partners are asking for the criteria for providing these grants and subsidies for water supply and sanitation projects, how the grants can be leveraged so that more resources will be generated, and the most efficient, effective and sustainable financing model to implement leveraging of public with private resources.

d. Public-Private Partnerships (PPP). There is no concerted effort to encourage

PPPs. Private sector participation on bulk supply or distribution is largely private sector initiated and is thus episodic and sporadic. There is no clear policy on incentives and regulation, especially those dealing with LGUs. Fortunately, however, there is a strong entrepreneurial spirit, as evidenced by the entry of bulk suppliers to WDs and small water service providers in areas with no water supply facilities.

e. Key Challenges for Septic Management:31

Little awareness of septage management among local governments and utilities.

National institutions lack of septage management expertise

Little national funding to implement the Clean Water Act, including septage management projects.

Very little enforcement of environmental regulations for non-industrial sources.

f. Lack of Monitoring and Updated Data This is already evident from the conflicting numbers in population served by the different reports. There is no agency responsible for collating data on WSPs.

g. Emerging threat of climate change particularly to the sources of water and existing facilities. Climate change provisions should be factored in the design of facilities as well as other ancillary programs like watershed development programs.

31

AECOM International Development and Swiss Institute of Aquatic Sciences and Technology (for USAID). 2010. A Rapid Assessment of Septage Management in Asia: Policies and Practices in India, Indonesia, Malaysia, the Philippines, Sri Lanka, Thailand, and Vietnam.

Developing the Institutional Framework for the WSS Sector and Identifying Investment Plans and Programs April 2013

26

C. DEMAND-GAP ANALYSIS The demand-gap analysis will need two sets of data: how many are being served now and what is the future target. To determine how many are being served now, a stock taking of existing WSPs and their number of service connections were gathered from the different public agencies, as well as from private groups. To determine the future targets, It is necessary to do population projections to determine the population for year 2011 and the different design years.

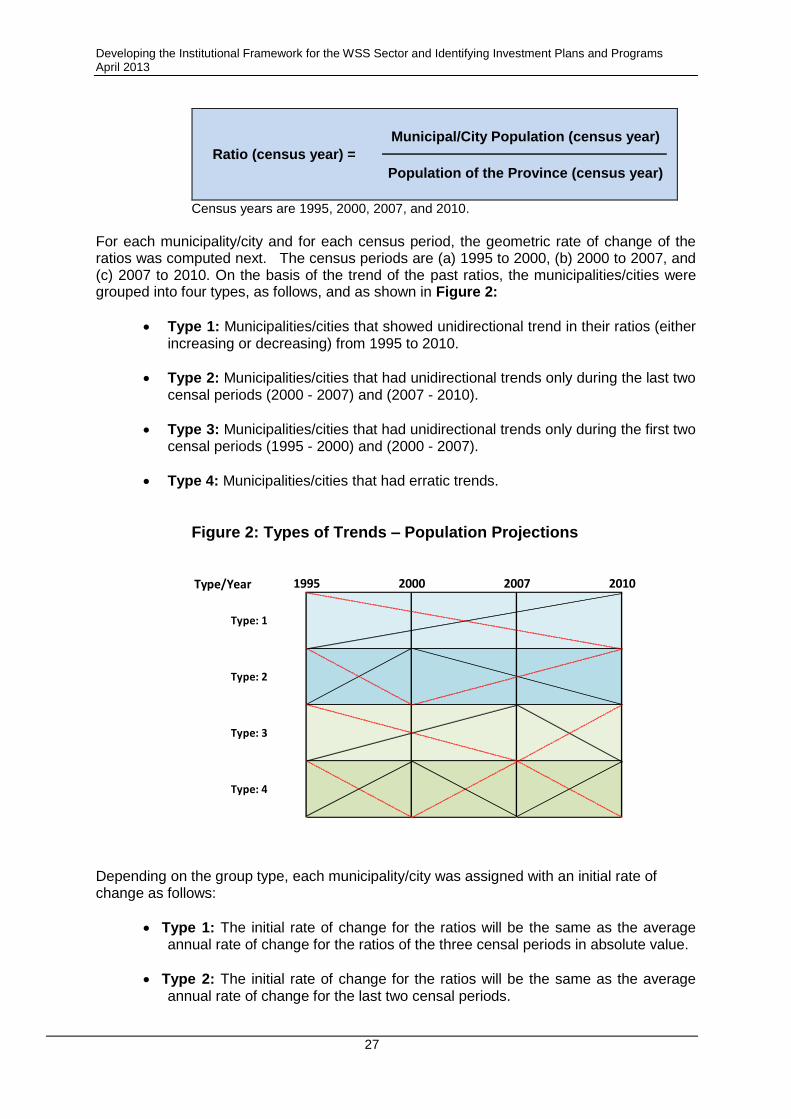

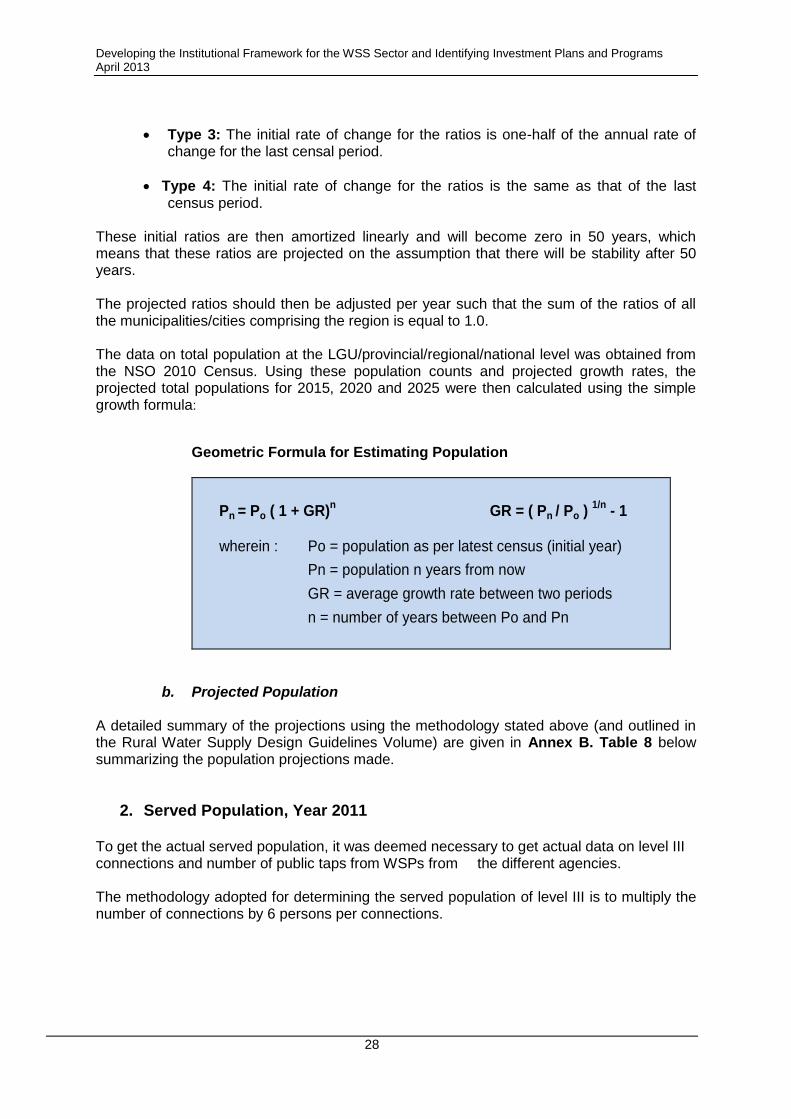

1. Population Projections Population projections are estimates of future populations based on statistical models that extrapolate past and present trends into the future. Population projections involve the ratio method and the geometric rate of increase method in extrapolating population for the different design years.For this study, the design/target years are 2015, 2020, and 2025.

Pertinent data listed below were acquired from National Statistics Office (NSO), Water Districts, City or Municipal Planning and Development Offices, and the Internet:

1995 Census of Population, National Statistics Office;

2000 Census of Population, National Statistics Office;

2007 Census of Population, National Statistics Office;

2010 Census of Population, National Statistics Office;

Projected Populations by Five-Year Age Group and Sex, by Region and Province and by Five Calendar Years: 2000 – 2040 (Medium Series).