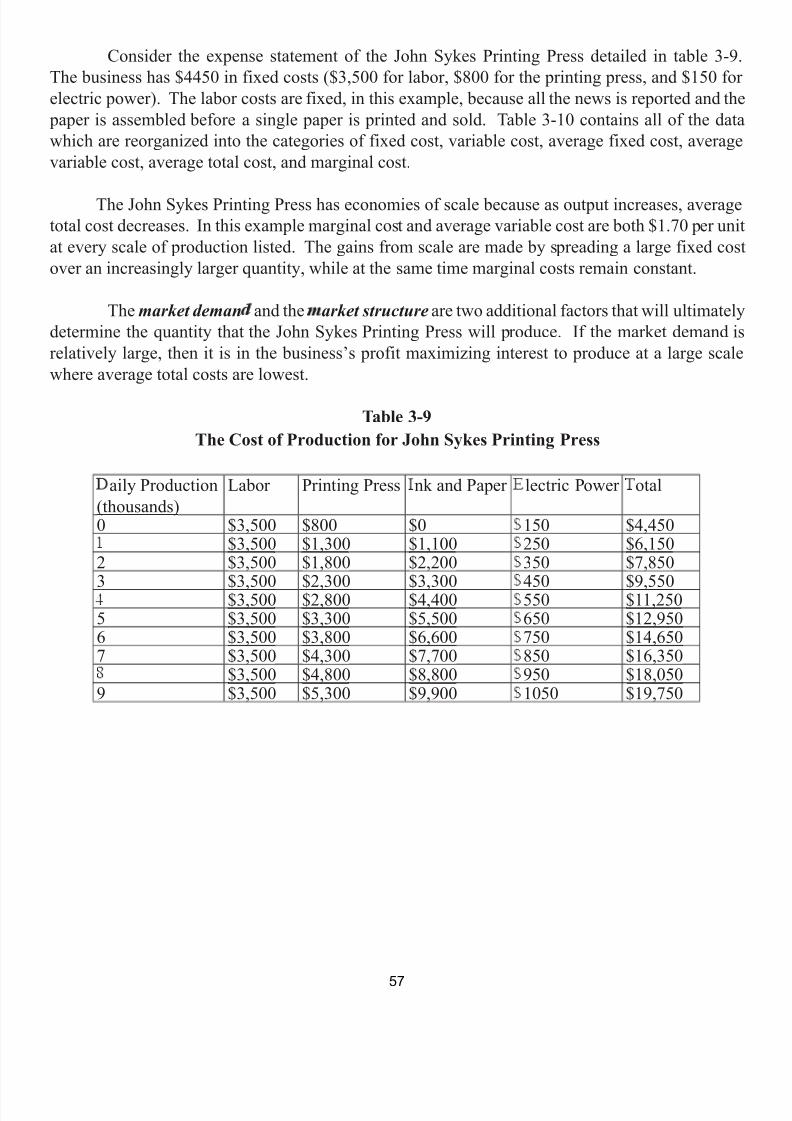

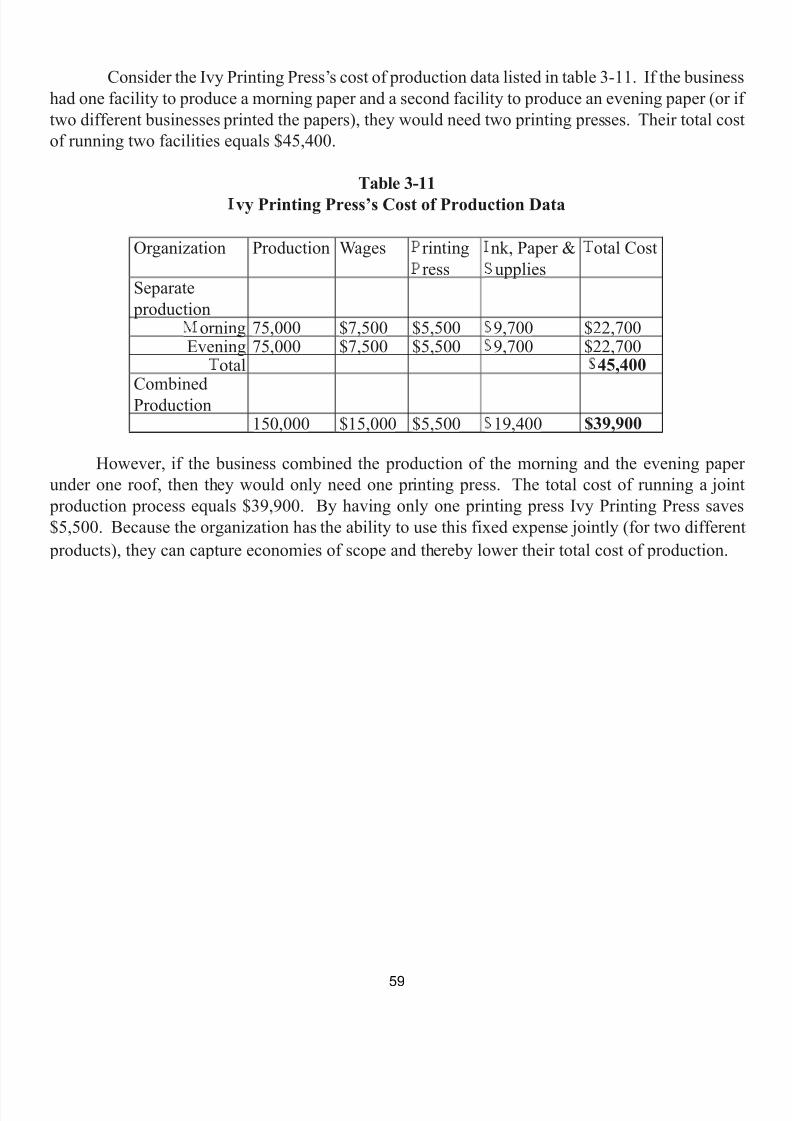

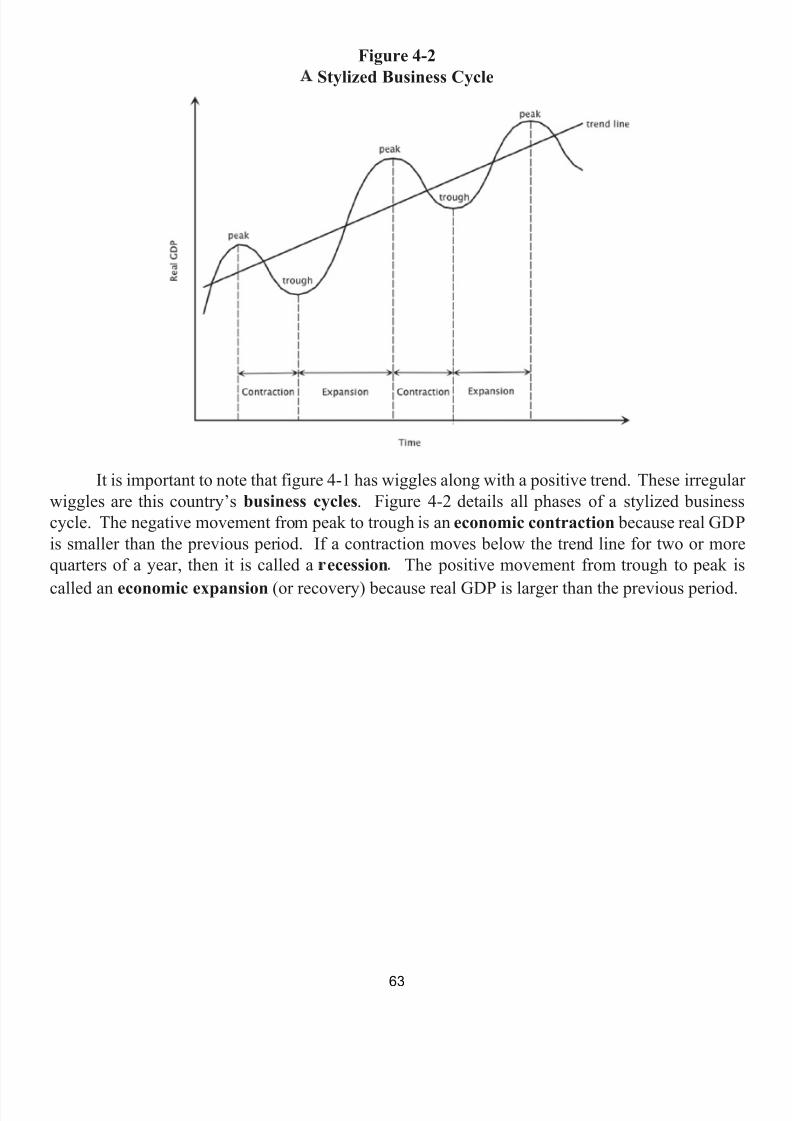

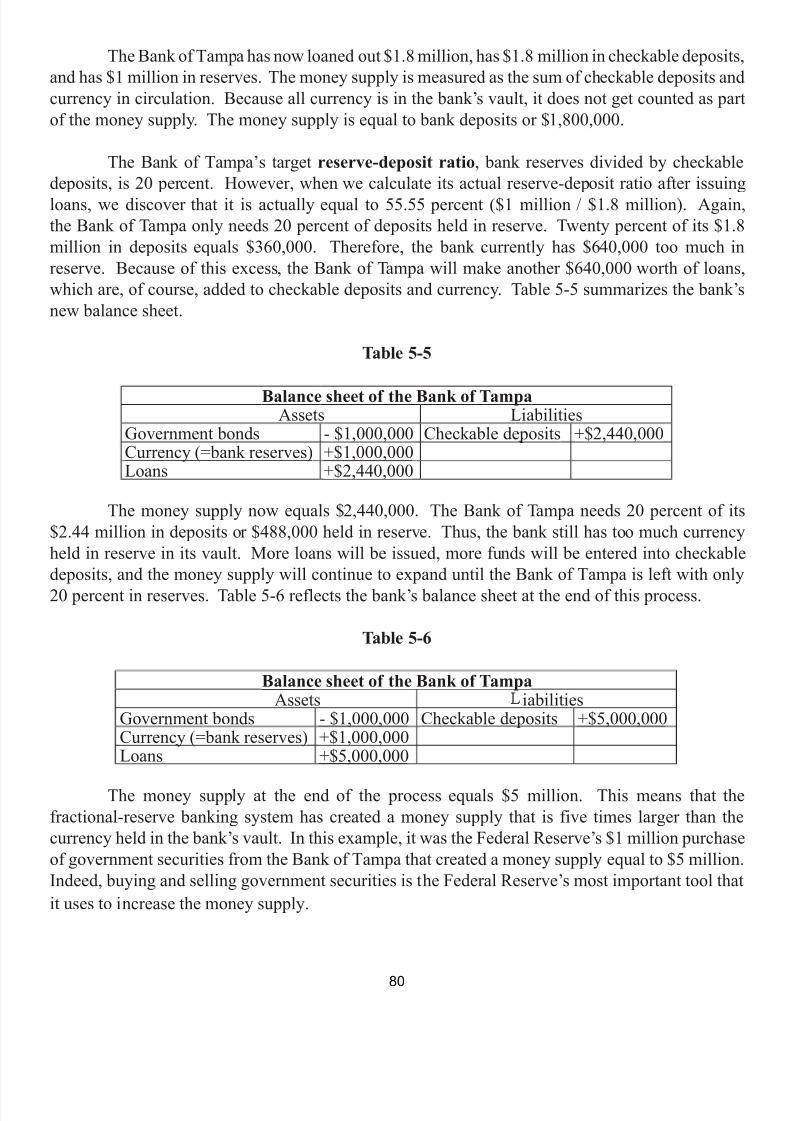

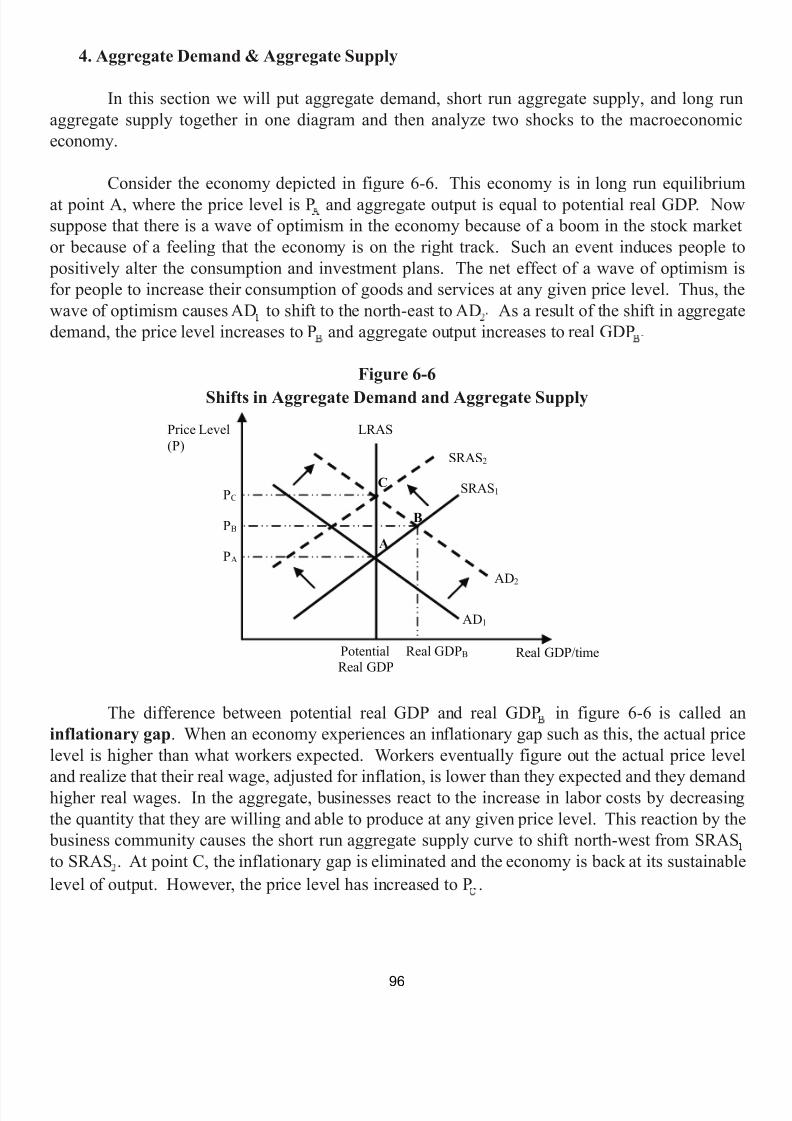

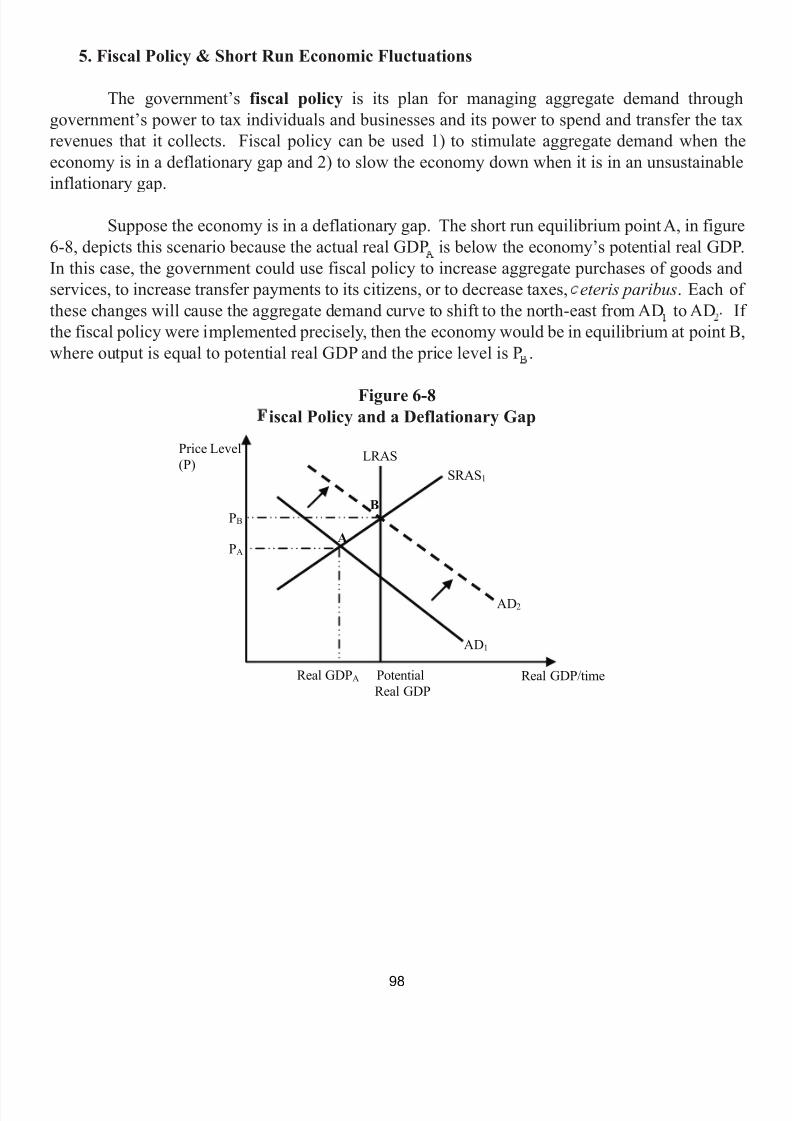

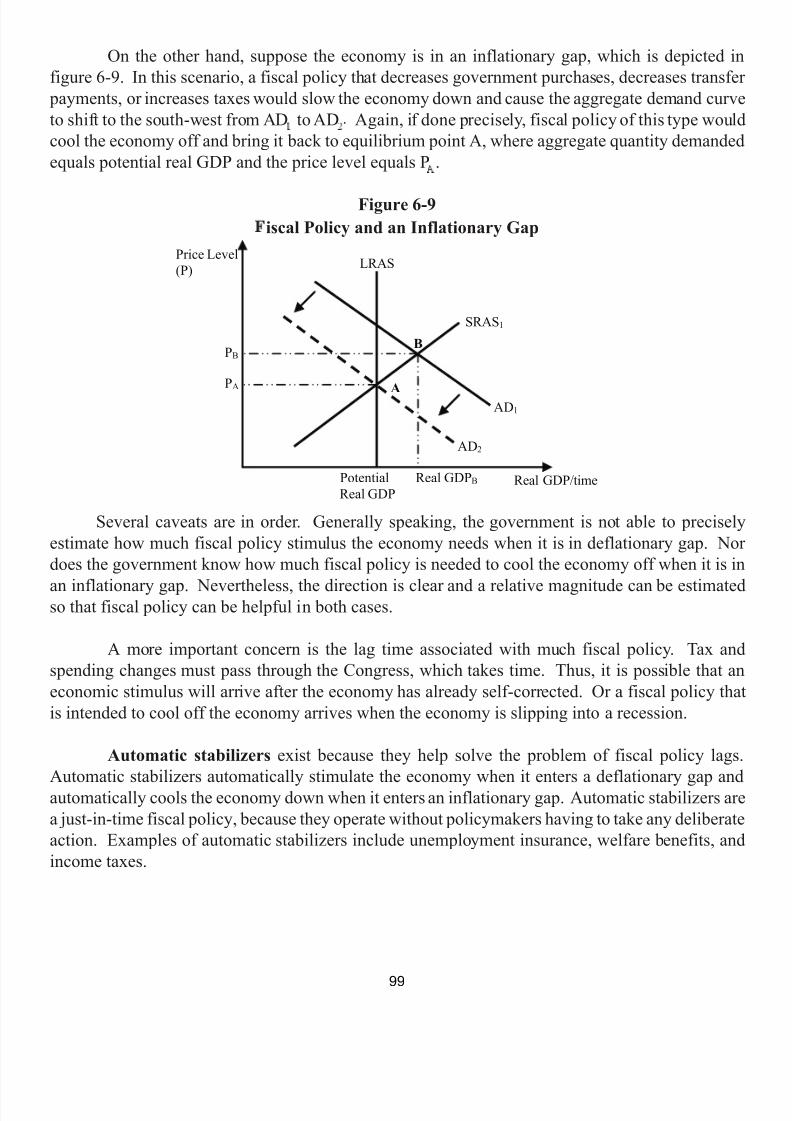

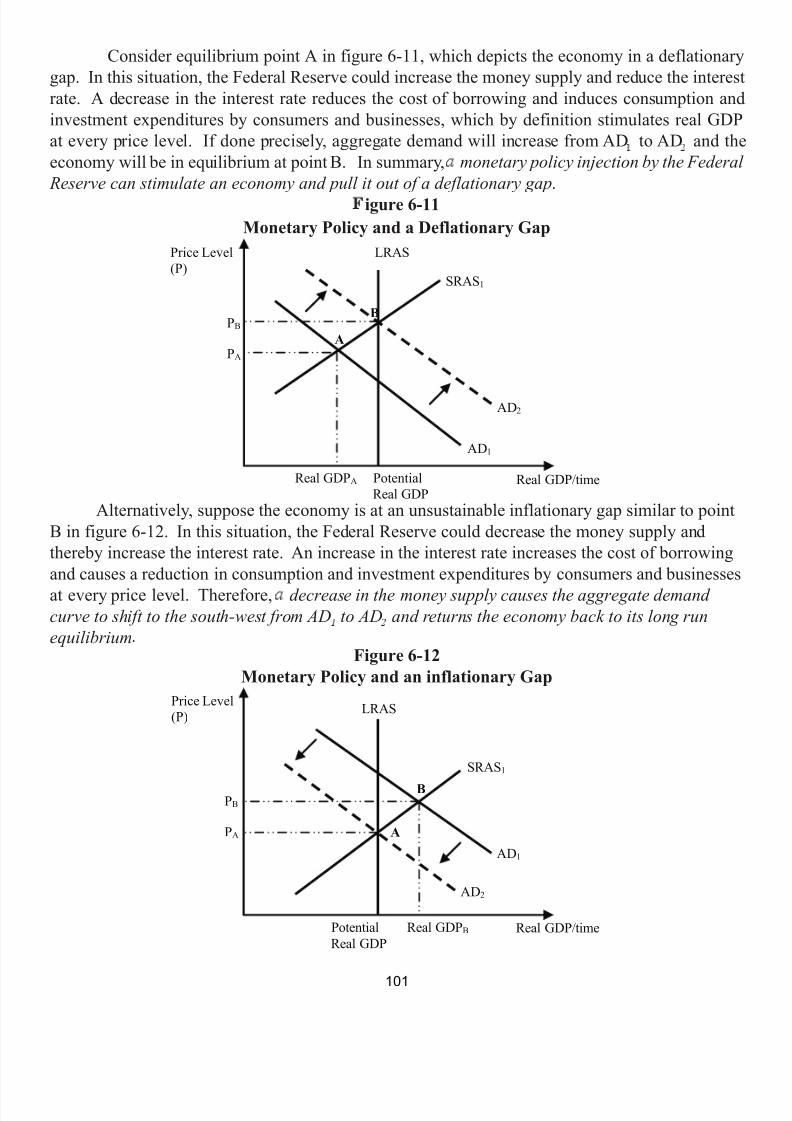

psu ivy fundamentals of economics

TRANSCRIPT

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 1/118

Fundamentals of Economics

Brian T. Kench,Ph.D.University of Tampa

Fifth Edition© Copyright 2011

Ivy Software

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 2/118

TABLE OF CONTENTS

ABLE OF CONTENTS PAGE

Chapter One - Comparative Advantage and the Benefits of Trade..............1

Chapter Two - Demand & Supply..............................................................15

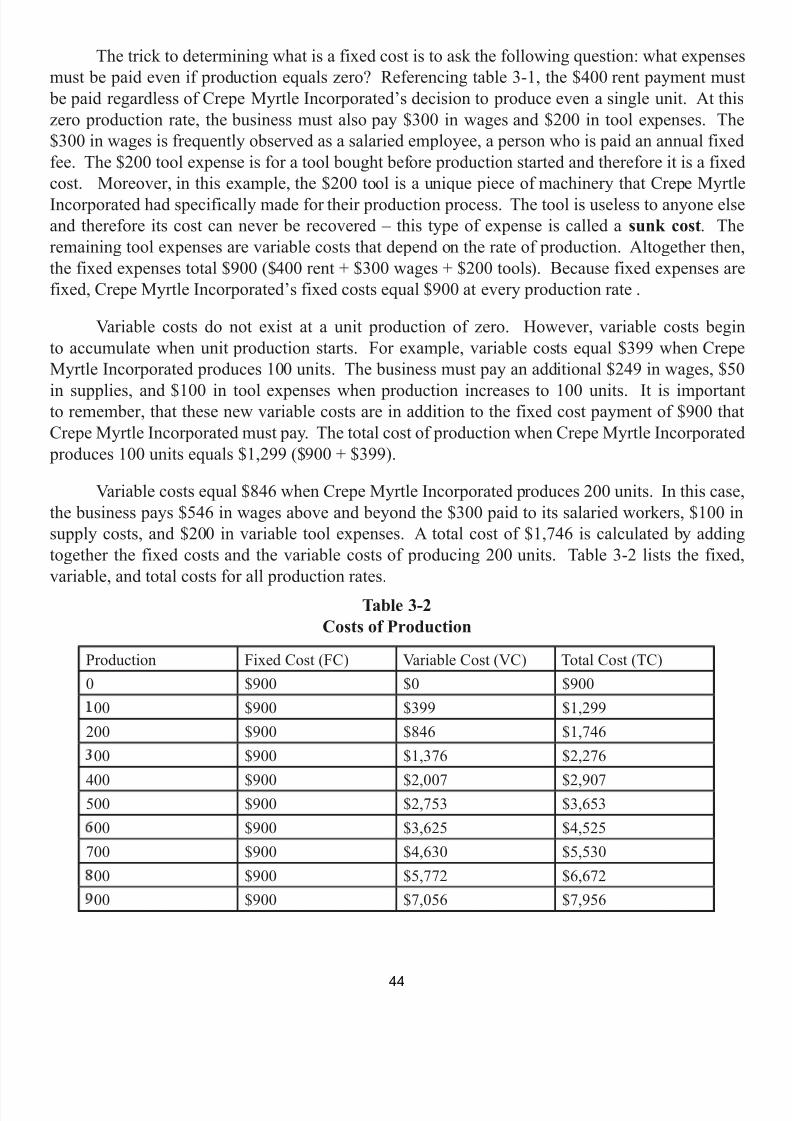

Chapter Three - he Costs of Production and Profit Maximization ..........43

Chapter Four - Economic Performance Metrics.........................................60

Chapter Five - Money & Banking...................................... .......................75

Chapter Six - Aggregate Demand & Aggregate Supply ............................87

Glossary........................................................................ ...........................102

Charts & Graphs.......................................................................................110

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 3/118

CHAPTER ONEComparative Advantage and the Benefits of Trade

“Central to the globalization debate is the issue of the extent to which the United Statesshould compel the application of U.S. laws and regulatory standards to activities inother countries…. Most foreign governments resist these demands both because they areintrusions on the sovereign policies the countries have adopted with regard to regulation,and because to adopt American standards dramatically reduces a country’s comparativeadvantage to the detriment of its workers hoping to improve their lives” (emphasis added).

George L. Pr est, Wa Street Journa , A10, 6 18 04

1. Introduction

The concepts of opportunity cost and comparative advantage are two of the most important

concepts in all of economics. The opportunity cost of any life activity is the cost of what you giveup to partake in that activity. For example, the opportunity cost of reading this book might be notwatching your child’s baseball game. Among a comparison of individuals, businesses or countries,the one who has the lowest opportunity cost of an activity has a comparative advantage in thatactivity. Economists have long used these concepts to prove the mutual advantage of individuals,

businesses or countries specializing in things with which they have a comparative advantage andtrading for the rest. As the quote above reveals, these concepts are mechanisms that assist informedand educated debates on current public policy.

The following key concepts will be covered in this chapter: the four factors of production,opportunity cost, production possibilities frontier, increasing opportunity cost, absolute advantageand comparative advantage.

1

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 4/118

2. Factors of Production

All the productive resources of the earth may be put in one of the following four categories:land, labor, capital, and entrepreneurial ability These four categories are collectively called thefactors of production The factors of production encompass all the possible productive resourcesused to produce goods and services. Moreover, the factors of production are all scarce economicresources because they are limited in supply.

The category of land includes all the gifts of nature – so called natural resources – that areused to produce goods and services. The category of abor includes work time and work effortthat people devote to producing goods and services. The category of capital includes all tools,instruments, machines, buildings, and other constructions that have been produced in the past that

businesses now use to produce goods and services. Finally, the category of entrepreneurial abilityincludes all human resources that organize the other factors of production. Entrepreneurs come upwith new ideas about what and how to produce, make business decisions, and bear the risks thatarise from these decisions .

Because the factors of production are limited in supply, they must be allocated amongmembers of human society. The price mechanism is one way, among several, that human societychooses to allocate scarce resources.

The market price of each factor of production has been assigned a unique name byeconomists. Rent is the unit price one pays for the use of land. Wage is the unit price one pays forthe services of labor. Interest is the unit price one pays for the use of capital. Profit is the incomeearned (or lost) by an entrepreneur for running a business.

3. Opportunity Cost and the Production Possibilities Frontier

The most fundamental principle in economics is opportunity cost The opportunity cost ofsomething is what you give up to get it. For example, you are currently using your time to earn agraduate degree; your opportunity cost of getting a graduate degree is missing time with friendsand family. In this section, the principle of opportunity cost is demonstrated by a productionpossibilities frontier. A production possibilities frontier is a model of an economy that shows howmuch the economy can produce using all of its factors of production efficiently.

2

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 5/118

Figure 1-1roduction Possibilities Frontier

The economy in figure 1-1 produces only two goods: eggs and wine. The data in figure 1.1are the industrial output from one week of work. Each of the following is illustrated in the figure:

• If all the factors of production are employed to produce eggs, the economy is able to produce 82 eggs in a week.

• One the other hand, if all the factors of production are employed to produce wine, theeconomy is able to produce 10 bottles of wine per week.

• If all factors of production are fully and efficiently used, then the economy would beoperating somewhere on the production possibilities frontier.

• Points A, B, C, D, E and F each represent bundles of goods that lie on the economy’s production possibilities frontier.

When an economy does not fully use its factors of production, then it ends up at a locationinside the production possibilities frontier. If the economy ends up at the output bundle locatedat point “G”, the economy has not fully and efficiently used its factors of production. Lastly, thiseconomy does o have enough factors of production to produce bundle “H” or any bundle beyond

its production possibilities frontier.

�

�

�

�

�

�

�

�

�

�� �

�

3

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 6/118

3.1 Example 1

Suppose the economy in figure 1-1 produces at point “B” – 80 eggs and one bottle of wine.If the economy chooses to move from point “B” to point “C” and produce another three bottles ofwine, it can now only produce 70 eggs. Therefore the opportunity cost of another three bottles ofwine equals 10 eggs (80 eggs – 70 eggs). In other words, the economy is giving up the productionof 10 eggs in order to produce another three bottles of wine.

3.2 Example 2

If the economy in figure 1-1 chooses to move from point “C” to point “D” and produceanother three bottles of wine, it may now only produce 50 eggs. The opportunity cost of producinganother three bottles of wine is 20 eggs (70 eggs – 50 eggs). Again, the economy is giving up the

production of 20 eggs in order to produce another three bottles of wine.

3.3 Example 3

Lastly, if the economy in figure 1-1 chooses to move from point “D” to point “F” and produce another three bottles of wine, it has zero factors of production left for the production ofeggs and can produce zero eggs. The opportunity cost of producing another three bottles of wineis 50 eggs (50 eggs – 0 eggs).

3.4 Increasing Opportunity Cost

As we increase the production of wine at a constant increment ( .e., by three bottles), the

opportunity cost of wine production increases. This is known as the law of ncreasing opportunitycost; it is reflected in the bowed-out shape of the production possibilities frontier in figure 1-1. Asmore and more of an economy’s factors of production are employed in the production of wine, theeconomy must sacrifice the production of eggs at an increasing rate.

Economic agents always start by using their best factors of production. Therefore, aneconomy experiences increasing opportunity cost as they increase one good’s production. In thecase of wine production, wine producers use their best fertilizer and their best machines to producethe first bottles of wine. The factors of production that are well-suited for wine production happen

to be the worst factors of production for the production of eggs. Thus, the opportunity cost of thefirst bottle of wine, in terms of eggs, is small. But as we increase our demand for bottles of wine,the economy must substitute out factors of production that are better suited for egg production anduse them to produce wine. The sacrifice in terms of eggs increases as additional bottles of wine are

produced.

4

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 7/118

4. Absolute Advantage versus Comparative Advantage

To have an absolute advantage in something means that one has the lowest absolute production cost relative to those with whom they are compared. To have a comparative advantagein something means that one has the lowest opportunity cost relative to those with whom they arecompared.

David Ricardo first did the simple mathematics to demonstrate the concept of comparativeadvantage and the mutual advantage of trade in his 1817 book, The Principles of Political Economyand Taxation . Ricardo’s demonstration is one of the most important in all of economics and it isused as the root explanation for why

• one dines at a restaurant rather than cooking a meal at home;• one hires a landscaper to mow their lawn rather than mowing it for oneself;• Audi contracts with Bose Corporation to manufacture the sound system for its

automobiles rather than making the sound systems internally;• grocery stores in Boston, Massachusetts purchase oranges from Citrus Hills, Florida

rather than growing them in Boston; and• Sykes Corporation hires call centers in Bangalore, India, paying Indian employees

$2,100/year to answer consumer phone calls, rather than hiring employees in Tampa,Florida for a much higher wage year.

To help you get a better grasp of Ricardo’s analysis consider the following two examples.

5. Example 1: Elizabeth and Kyle

5.1 Self-Sufficiency

A self-sufficient individual makes everything that he needs in life from the factors of production with which he is endowed. Consider the following example in which Elizabeth andKyle each make wine and clothing: suppose that both Elizabeth and Kyle work a forty hour weekand both of them fully and efficiently use their endowed factors of production. Also assume that thethere is a constant opportunity cost between the production of a unit of wine and the productionof a unit of clothing. Because opportunity costs are constant and not increasing in this example,the production possibilities frontiers are linear and not bowed outward. This is done to simplify

our discussion.

5

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 8/118

5.2 Elizabeth’s Production Possibilities Frontier

First consider Elizabeth. In forty hours, Elizabeth may produce 20 pieces of clothing r160 bottles of wine r any other combination that lies between these extremes on her production

possibilities frontier (PPF) in figure 1-2. If Elizabeth chooses to spend twenty hours making clothingand twenty hours making wine, then she would produce 10 pieces of clothing and 80 bottles ofwine. This bundle is located a point “A” in Elizabeth’s clothing and wine production possibilitiesfrontier for a forty-hour-work week.

igure 1-2Elizabeth’s Production Possibilities Frontier

Assume that Elizabeth fully and efficiently uses her factors of production. Therefore, shewill produce a bundle of wine and clothing that is on the production possibility frontier and will not

produce a bundle that is below the production possibilities frontier. Further, because she always produces somewhere on the production possibilities frontier, we can use figure 1-2 to determineElizabeth’s opportunity cost of producing a bottle of wine and her opportunity cost of producing aunit of clothing.

Suppose that Elizabeth produces 80 bottles of wine and 10 units of clothing, which is depictedwith point “A”. If Elizabeth changed her mind and decided that she wanted to produce 20 unitsof clothing, how many bottles of wine could she produce? The answer is zero. Elizabeth needsforty hours (all that she has) to produce 20 units of clothing, which leaves her no time to devote tothe production of bottles of wine in that week. The opportunity cost of making another 10 units ofclothing (from 10 units to 20 units) is 80 bottles of wine.

Using some simple math and the assumption of constant opportunity costs we can reduce andfigure out the opportunity cost of one unit of clothing. If 10 units of clothing have an opportunitycost of 80 bottles of wine, then one unit of clothing has an opportunity cost of eight bottles ofwine for Elizabeth By using algebra and solving for one bottle of wine, we can also prove that heopportunity cost of one bottle of wine is one-eighth of a unit of clothing for Elizabeth

�

�

� �

6

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 9/118

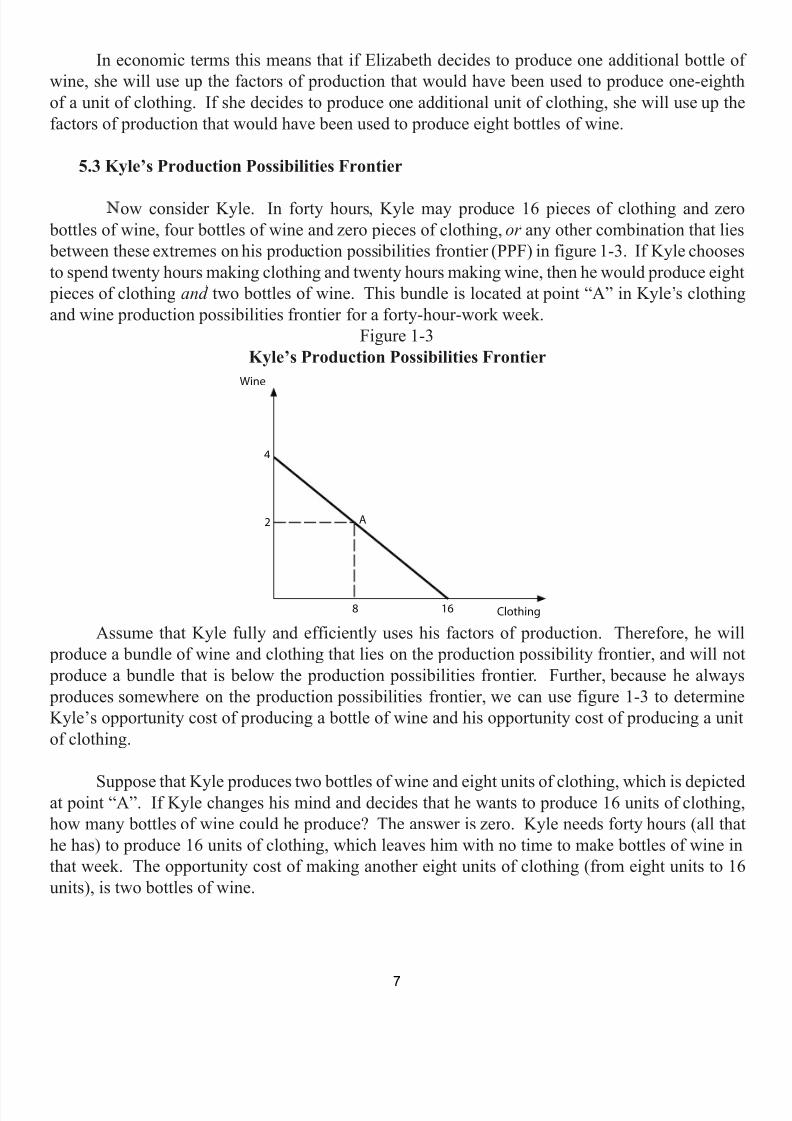

In economic terms this means that if Elizabeth decides to produce one additional bottle ofwine, she will use up the factors of production that would have been used to produce one-eighthof a unit of clothing. If she decides to produce one additional unit of clothing, she will use up thefactors of production that would have been used to produce eight bottles of wine.

5.3 Kyle’s Production Possibilities Frontier

ow consider Kyle. In forty hours, Kyle may produce 16 pieces of clothing and zero bottles of wine, four bottles of wine and zero pieces of clothing, or any other combination that lies between these extremes on his production possibilities frontier (PPF) in figure 1-3. If Kyle choosesto spend twenty hours making clothing and twenty hours making wine, then he would produce eight

pieces of clothing and two bottles of wine. This bundle is located at point “A” in Kyle’s clothingand wine production possibilities frontier for a forty-hour-work week.

Figure 1-3Kyle’s Production Possibilities Frontier

Assume that Kyle fully and efficiently uses his factors of production. Therefore, he will produce a bundle of wine and clothing that lies on the production possibility frontier, and will not produce a bundle that is below the production possibilities frontier. Further, because he always produces somewhere on the production possibilities frontier, we can use figure 1-3 to determineKyle’s opportunity cost of producing a bottle of wine and his opportunity cost of producing a unitof clothing.

Suppose that Kyle produces two bottles of wine and eight units of clothing, which is depictedat point “A”. If Kyle changes his mind and decides that he wants to produce 16 units of clothing,how many bottles of wine could he produce? The answer is zero. Kyle needs forty hours (all thathe has) to produce 16 units of clothing, which leaves him with no time to make bottles of wine inthat week. The opportunity cost of making another eight units of clothing (from eight units to 16units), is two bottles of wine.

�

7

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 10/118

Using some simple math and the assumption of constant opportunity costs, we can reduce andfigure out the opportunity cost of one unit of clothing. If eight units of clothing have an opportunitycost of two bottles of wine, then one unit of clothing has an opportunity cost of one-fourth of abottle of wine for Kyle . By using algebra and solving for one bottle of wine, we can show that theopportunity cost of one bottle of wine is four units of clothing for Kyle

In economic terms this means that if he wants to produce one unit of clothing, he mustsacrifice the resources needed to produce one-fourth of a bottle of wine. And if Kyle wants to

produce one bottle of wine, then he must sacrifice the resources needed to produce four units ofclothing.

5.4 Absolute Advantage and Comparative Advantage

Does Elizabeth or Kyle have an absolute advantage in the production of wine? Elizabethcan produce more wine over the course of forty hours relative to Kyle (160 bottles for Elizabethversus four bottles for Kyle). Therefore, Elizabeth has an absolute advantage in the production ofwine .

Does Elizabeth or Kyle have an absolute advantage in the production of clothing? Elizabethcan produce more clothing over the course of forty hours relative to Kyle (20 units of clothing forElizabeth versus 16 units of clothing for Kyle). Therefore, Elizabeth has an absolute advantage inthe production of clothing, too .

Although it is clear that Elizabeth is better at producing wine and clothing relative to Kyle,the concept of absolute advantage tells us nothing about whether or not Elizabeth or Kyle might

benefit from specializing in the production of one of the two goods and trading for the other. Andlet us not be shy here, trading in this context is fully analogous to outsourcing in contemporary

business language. The concept that can help inform Elizabeth and Kyle about the benefits of tradeis the concept of comparative advantage.

The concept of comparative advantage states that when comparing producers, the one withthe lowest opportunity cost in the production of some good or service has a comparative advantagein the production of that good or service. In our problem, who has a comparative advantage in the

production of a bottle of wine? Who has a comparative advantage in the production of clothing?

First, let’s look at the production of wine. Elizabeth’s opportunity cost of producing one bottle of wine is one-eighth of a unit of clothing and Kyle’s opportunity cost of producing one bottle of wine was four units of clothing. Therefore, Elizabeth has a comparative advantage in the production of wine because she has to give up less clothing (one-eighth of a unit versus four unitsof clothing) to make one bottle of wine .

8

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 11/118

What about clothing? Elizabeth’s opportunity cost of producing one unit of clothing is eight bottles of wine and Kyle’s opportunity cost of producing one unit of clothing is one-fourth of a bottle of wine. Therefore, Kyle has a comparative advantage in the production of clothing becausehe has to give up less wine (one-fourth of a bottle versus eight bottles of wine) to make one unit ofclothing .

5.5 Trade

An individual or a business should specialize in the production of a good or service in whichthey have a comparative advantage. Below we will prove why this is always the correct thing todo. In our current problem, we have discovered that Elizabeth has a comparative advantage in the

production of wine and Kyle has a comparative advantage in the production of clothing. With thisinformation, we may conclude that Elizabeth should specialize in the production of wine and tradefor clothing and Kyle should specialize in the production of clothing and trade for wine.

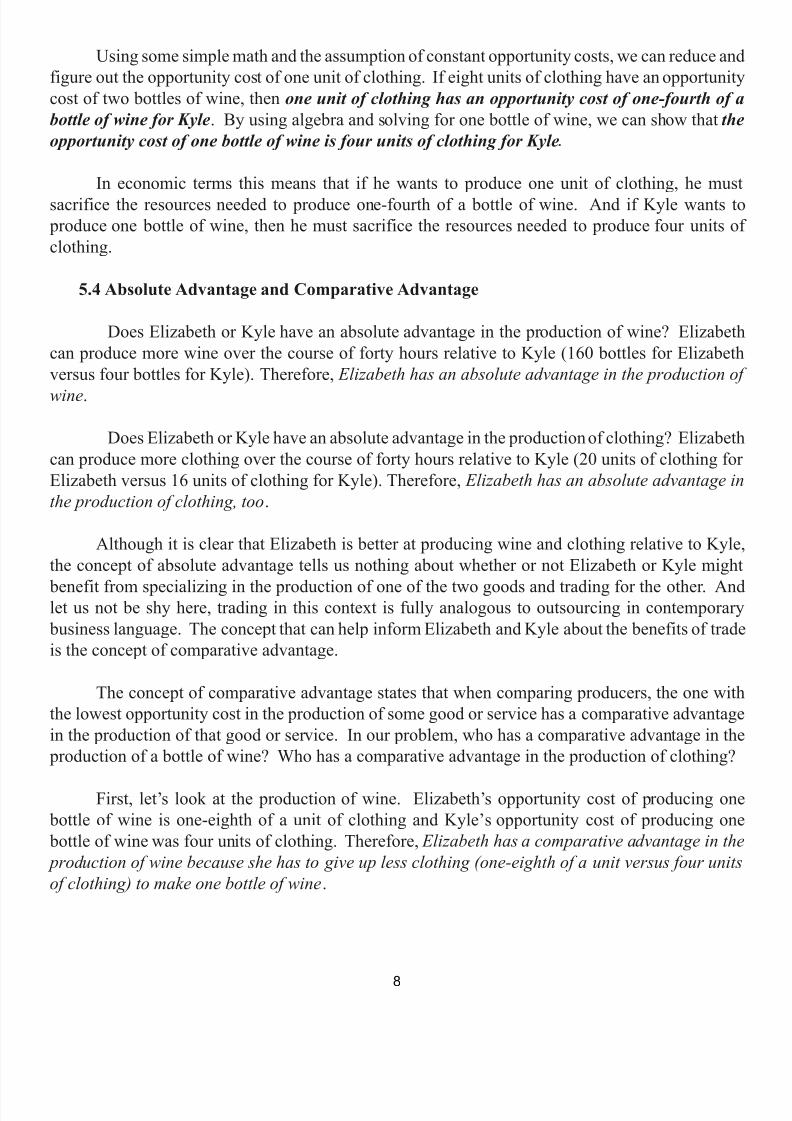

Suppose Elizabeth and Kyle sit down and negotiate the following trade. Elizabeth proposesthat she will produce all 160 bottles of wine and zero units of clothing and sell 32 bottles of wineto Kyle in exchange for 8 units of clothing. Kyle, who decides to produce 16 units of clothing andzero bottles of wine, agrees to accept the proposed trade.

Do both Elizabeth and Kyle benefit from this proposed trade? The answer is unambiguously:es. In figure 1-4 bundle “B” illustrates the bundle that Elizabeth ends up with after the trade with

Kyle. This demonstrates that Elizabeth is better off as a result of trading with Kyle because she is beyond her self-sufficient production possibilities frontier. That is to say, without trading, Elizabethcould not have bundle “B”, and this is the proof that we have been searching for. Elizabeth clearly

benefits from specializing in wine and trading with Kyle for units of clothing.Figure 1-4

lizabeth’s After Trade PPF

�

�

9

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 12/118

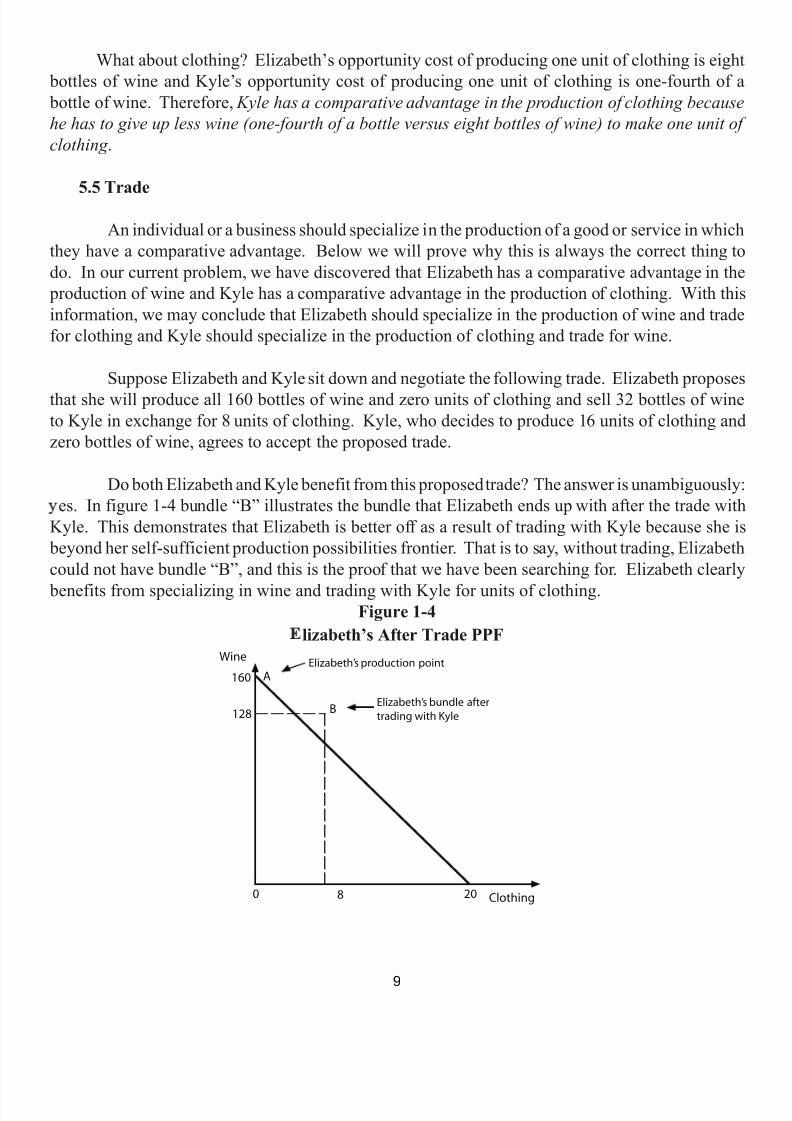

In figure 1-5 bundle “B” illustrates the bundle that Kyle ends up with after the trade withElizabeth. This demonstrates that Kyle is better off as a result of trading with Elizabeth because heis beyond his self-sufficient production possibilities frontier. That is to say, without trading, Kylecould not have bundle “B”. That, again, is proof that Kyle benefits from specializing in clothingand trading with Elizabeth for bottles of wine.

Figure 1-5Kyle’s After Trade PPF

5.6 The Range of Possible Trading Terms

Both Elizabeth and Kyle become better off when Elizabeth sells Kyle 32 bottles of wine inexchange for eight units of clothing. Can we figure out all the transactions between Elizabeth andKyle that would make them better off? Again, the answer is yes.

The terms of the trade discussed above are 32 bottles of wine for eight units of clothing,which reduces to four bottles of wine for each unit of clothing. Elizabeth found this to be a good

deal because her opportunity cost of making one unit of clothing is eight bottles of wine. Becauseshe is able to buy a unit of clothing from Kyle for four bottles of wine, Elizabeth uses more ofher factors of production to produce wine and thus moves beyond her self-sufficient production

possibilities frontier. Therefore, any trade in which a unit of clothing costs less than eight bottlesof wine (Elizabeth’s opportunity cost of producing a unit of clothing) will benefit Elizabeth. Thus,the maximum price Elizabeth would be willing to pay for a unit of clothing from Kyle is a smidgenless than eight bottles of wine.

�

�

10

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 13/118

What is the smallest number of bottles of wine that Kyle will accept in exchange for oneunit of clothing? Kyle would be willing to accept a smidgen more than his opportunity cost of

producing a unit of clothing, which is one-fourth of a bottle of wine. Surely, Kyle would prefer 7.9 bottles of wine for one unit of clothing, but he would be willing to accept a smidgen more than hisopportunity cost of producing one unit of clothing.

Therefore, the range of possible terms of trade for one unit of clothing is a smidgen morethan one-fourth of a bottle of wine up to eight bottles of wine. Any trade that occurs within this pricing range will unambiguously make both Elizabeth and Kyle better off. The actual price that isnegotiated, however, depends on the bargaining power of the parties involved.

What about the range of prices for a bottle of wine? Elizabeth specializes in the productionof wine and she will accept from Kyle anything that is greater than one-eighth of a unit of clothing(her opportunity cost of producing a bottle of wine). Furthermore, Kyle is willing to pay an amountthat is less than his opportunity cost of producing a bottle of wine, which equals four units ofclothing. The range of possible prices for one bottle of wine is a smidgen more than one-eighth ofa unit of clothing up to four units of clothing. Any trade that occurs within this pricing range willunambiguously make both Elizabeth and Kyle better off.

11

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 14/118

6. Example 2: Cape Cod and Nantucket

Table 1-1 contains the labor hours required to produce one lobster dinner or one crab dinneron Cape Cod and Nantucket. Again, for simplicity, assume that opportunity costs are constant andthat each location has the same set of scarce resources.

Table 1-1Labor Hours to Produce Dinners

Number of labor hours neededto make one lobster dinner

per worker

umber of labor hourseeded to make one crab

dinner per worker Cape Cod 3 9

antucket 2 4

6.1 Absolute Advantage in the Production of a Lobster Dinner and a Crab Dinner

In this example, the location that can produce one unit of a good in the fewest hours oflabor has an absolute advantage in that good. Cape Cod can produce one lobster dinner in threehours while it takes Nantucket two hours to produce a lobster dinner. Therefore, Nantucket hasan absolute advantage over Cape Cod in the production of a lobster dinner because it can make alobster dinner in the fewest hours.

antucket also has an absolute advantage over Cape Cod in the production of a crab dinner because it can produce 1 crab dinner in fewer hours relative to Cape Cod. It takes Nantucket fourhours to produce a crab dinner, while Cape Cod produces a crab dinner in nine hours.

6.2 The opportunity Cost of Producing one Lobster Dinner on Cape Cod and Nantucket

Cape Cod has the capability to produce one lobster dinner in three hours or one crab dinnerin nine hours. This implies that in the time that it takes to make one lobster dinner on Cape Cod,one-third of a crab dinner can be produced. If Cape Cod chooses to use its time and resourcesto produce one lobster dinner, then it is also choosing to ot produce one-third of a crab dinner.Therefore, the opportunity cost of one lobster dinner is one-third of a crab dinner on Cape Cod

Nantucket has the capability to produce one lobster dinner in two hours or one crab dinner infour hours. This implies that in the time it takes to make one lobster dinner on Nantucket, one-half of a crab dinner can be produced. If Nantucket chooses to use its time and resources to produceone lobster dinner, then it is also choosing to not produce one-half of a crab dinner. Therefore, theopportunity cost of one lobster dinner is one-half of a crab dinner on Nantucket .

12

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 15/118

6.3 The Opportunity Cost of Producing one Crab Dinner on Cape Cod and Nantucket

Cape Cod has the capability to produce one crab dinner in nine hours or one lobster dinnerin three hours. This implies that in the time it takes to make one crab dinner on Cape Cod, threelobster dinners can be produced. If Cape Cod chooses to use its time and resources to produce onecrab dinner, then it is also choosing to o produce three lobster dinners. Therefore, the opportunity

cost of one crab dinner is three lobster dinners on Cape Cod antucket has the capability to produce one crab dinner in four hours or one lobster dinner

in two hours. This implies that in the time it takes to make one crab dinner on Nantucket, twolobster dinners can be produced. If Nantucket chooses to use its time and resources to produce onecrab dinner, then it is also choosing to o produce two lobster dinners. Therefore, the opportunitycost of one crab dinner is two lobster dinners on Nantucket .

6.4 Comparative Advantage in the Production of a Lobster Dinner and a Crab Dinner

A location has a comparative advantage in the production of a good or service if itsopportunity cost is lower relative to the location with which it is compared. In this example, CapeCod has a comparative advantage in the production of lobster dinners because the opportunitycost of producing a lobster dinner on Cape Cod is lower than that of Nantucket. Precisely, theopportunity cost of producing one lobster dinner is one-third of a crab dinner on Cape Cod andone-half of a crab dinner on Nantucket.

On the other hand, Nantucket has a comparative advantage in the production of a crabdinner because its opportunity cost of producing a crab dinner is lower than that of Cape Cod. The

opportunity cost of producing one crab dinner is two lobster dinners on Nantucket, while on CapeCod the opportunity cost of producing one crab dinner is three lobster dinners.

6.5 Who Should Specialize in What?

Because Cape Cod has a comparative advantage in the production of a lobster dinner, itshould specialize in that task. Likewise, because Nantucket has a comparative advantage in the

production of a crab dinner, it should specialize in producing crab dinners.

13

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 16/118

6.6 The Range of Possible Prices for a Lobster Dinner and a Crab Dinner

Because Cape Cod has a comparative advantage in the production of a lobster dinner, itwill specialize in the production of that good. Cape Cod will benefit from trading with Nantucketwhenever they receive more than one-third of a crab dinner for a lobster dinner. Again, this is true

because one-third of a crab dinner is the opportunity cost of producing one lobster dinner on CapeCod.

antucket, too, will benefit by purchasing lobster dinners from Cape Cod, so long as the price they pay is lower then its opportunity cost of producing a lobster dinner. Recall, that theopportunity cost of producing a lobster dinner on Nantucket is one-half of a crab dinner.

Therefore, the range of possible prices for one lobster dinner is a smidgen larger than one-third of a crab dinner (Cape Cod’s opportunity cost of making a lobster dinner) up to a smidgenless than one-half of a crab dinner (Nantucket’s opportunity cost of making a lobster dinner). Anytrade that occurs within this pricing range will unambiguously make both Cape Cod and Nantucket

better off because they will move to a location beyond their self-sufficient production possibilitiesfrontier.

antucket has a comparative advantage in the production of a crab dinner, and it willspecialize in the production of that good. Nantucket will benefit from trade with Cape Cod wheneverit receives more than two lobster dinners for each crab dinner. Again, this is true because twolobster dinners is the opportunity cost of producing a crab dinner on Nantucket.

Here, too, Cape Cod, benefits by purchasing crab dinners from Nantucket, so long as the

price paid is lower then its opportunity cost of producing a crab dinner. Again, the opportunity costof producing one crab dinner on Cape Cod is three lobster dinners.

Therefore, the range of possible prices for one crab dinner is a smidgen more than twolobster dinners (Nantucket’s opportunity cost of making a crab dinner) up a bit less than three lobsterdinners (Cape Cod’s opportunity cost of making a crab dinner). Any trade that occurs within this

pricing range will unambiguously make both Nantucket and Cape Cod better off because they willmove to a location beyond their self-sufficient production possibilities frontier.

14

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 17/118

CH PTER T ODeman & Supp y

1. Introduction

This chapter introduces the odel of demand and supply . Economists use the model ofdemand and supply to analyze how buyers and sellers interact in the marketplace. It shows howmarket prices are determined and it demonstrates how many units of a good or service will be

bought and sold. Examples of markets include EBay.com, the New York Stock Exchange, therestaurant market, the gasoline market, and furniture market. Markets are everywhere.

The following key concepts will be covered in this chapter: a demand schedule, a demandcurve, a demand function, the law of demand, the market demand curve, the market demand schedule,the price elasticity of demand, the cross price elasticity of demand, the income elasticity of demand,

a supply schedule, a supply curve, a supply function, the law of supply, the market supply curve, themarket supply schedule, the elasticity of supply, and comparative-static analysis.

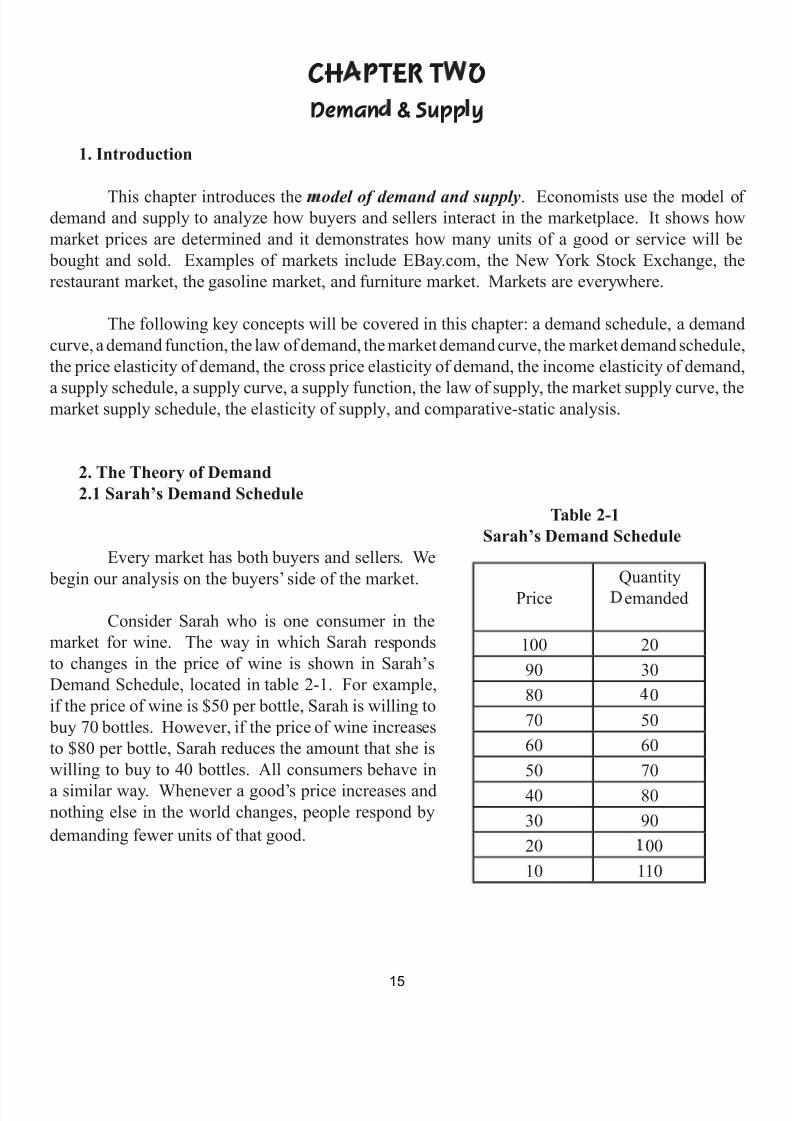

2. The Theory of Demand2.1 Sarah’s Demand Schedule

Table 2-1 Sarah’s Demand Schedule

Every market has both buyers and sellers. We begin our analysis on the buyers’ side of the market.

Consider Sarah who is one consumer in themarket for wine. The way in which Sarah respondsto changes in the price of wine is shown in Sarah’sDemand Schedule, located in table 2-1. For example,if the price of wine is $50 per bottle, Sarah is willing to

buy 70 bottles. However, if the price of wine increasesto $80 per bottle, Sarah reduces the amount that she iswilling to buy to 40 bottles. All consumers behave ina similar way. Whenever a good’s price increases andnothing else in the world changes, people respond bydemanding fewer units of that good.

PriceQuantityemanded

100 2090 3080 070 5060 6050 7040 8030 9020 0010 110

15

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 18/118

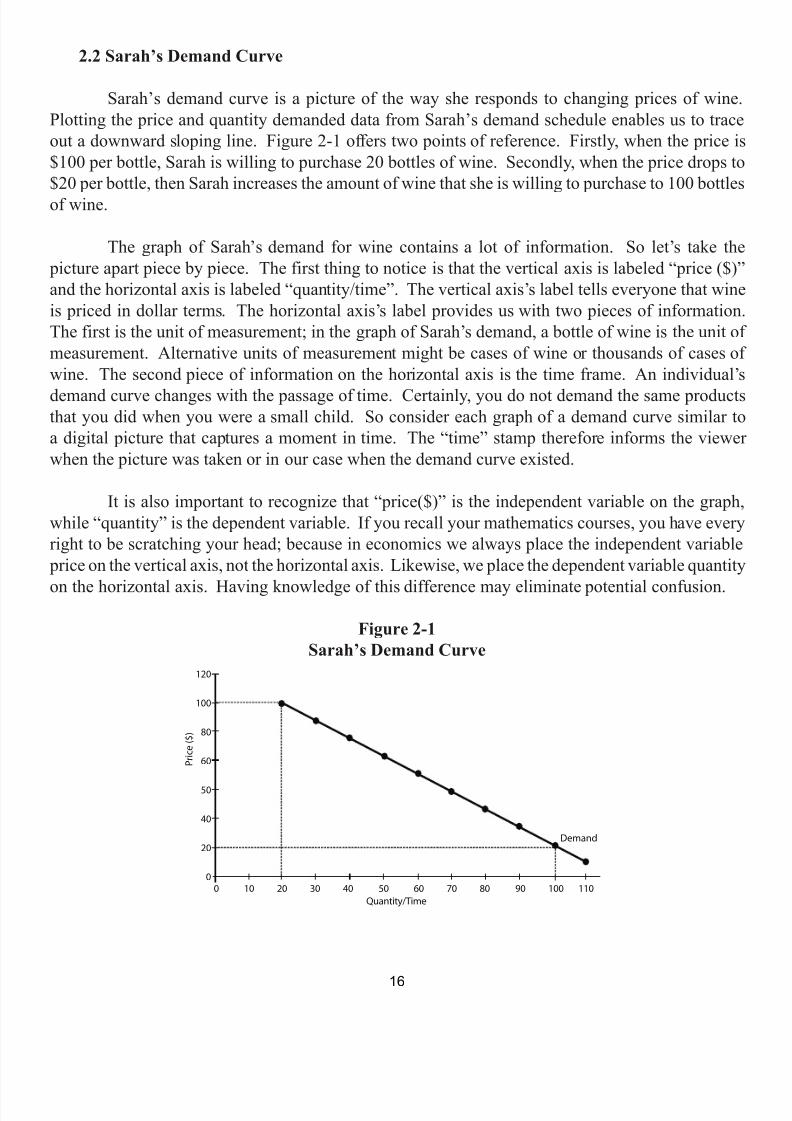

2.2 Sarah’s Demand Curve

Sarah’s demand curve is a picture of the way she responds to changing prices of wine.Plotting the price and quantity demanded data from Sarah’s demand schedule enables us to traceout a downward sloping line. Figure 2-1 offers two points of reference. Firstly, when the price is$100 per bottle, Sarah is willing to purchase 20 bottles of wine. Secondly, when the price drops to$20 per bottle, then Sarah increases the amount of wine that she is willing to purchase to 100 bottlesof wine.

The graph of Sarah’s demand for wine contains a lot of information. So let’s take the picture apart piece by piece. The first thing to notice is that the vertical axis is labeled “price ($)”and the horizontal axis is labeled “quantity/time”. The vertical axis’s label tells everyone that wineis priced in dollar terms. The horizontal axis’s label provides us with two pieces of information.The first is the unit of measurement; in the graph of Sarah’s demand, a bottle of wine is the unit ofmeasurement. Alternative units of measurement might be cases of wine or thousands of cases ofwine. The second piece of information on the horizontal axis is the time frame. An individual’sdemand curve changes with the passage of time. Certainly, you do not demand the same productsthat you did when you were a small child. So consider each graph of a demand curve similar toa digital picture that captures a moment in time. The “time” stamp therefore informs the viewerwhen the picture was taken or in our case when the demand curve existed.

It is also important to recognize that “price($)” is the independent variable on the graph,while “quantity” is the dependent variable. If you recall your mathematics courses, you have everyright to be scratching your head; because in economics we always place the independent variable

price on the vertical axis, not the horizontal axis. Likewise, we place the dependent variable quantity

on the horizontal axis. Having knowledge of this difference may eliminate potential confusion.

Figure 2-1Sarah’s Demand Curve

�

��

�

�

�

�

�

�

�

�

16

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 19/118

2.3 Sarah’s Demand Function

Sarah’s quantity demanded of wine depends on independent variables other than the priceof wine. Some of the more influential variables are the rices of complementary goods and theprices of substitute goods

• Complementary goods. Because Sarah likes to eat Gouda cheese and wheat crackersas she drinks wine, she considers them complementary goods to wine. Thus, Sarahconsiders the price of Gouda cheese and the price of wheat crackers when she decideshow many bottles of wine she is willing to buy at any given price.

• Substitute goods. Sarah enjoys drinking wine, Tanqueray gin, and other fine liquors andshe considers these beverages substitutes for one another. Thus, Sarah considers the priceof Tanqueray gin and the price of other fine liquors when she decides how many bottlesof wine she is willing to buy at any given price.

Another factor affecting Sarah’s demand for wine is her income.

• If wine is a normal good , then positive changes in income will induce Sarah to purchasemore bottles of wine at any given price.

• If wine is an inferior good for Sarah, then positive changes in income will induce Sarahto purchase fewer bottles of wine at any given price.

Does Sarah enjoy drinking wine? Obviously this matters, too. Economists lump measures

of satisfaction, enjoyment, pleasure, tc. into the category “ astes and preferences .

• For example, after Sarah discovers that she enjoys a particular vineyard and vintage ofwine, she reveals through her market behavior that she is now willing to purchase more

bottles of this wine at any given price.

• If she drinks a different brand of wine and finds it horribly bad, then she will reveal thatshe is willing to buy fewer bottles of that wine at any given price.

One other important category is Sarah’s expectations of the future Suppose that Sarahunexpectedly discovers that her favorite wine and vintage is soon to run-out. Because of this newinformation, Sarah reveals that she is now willing to buy more bottles at any given price. Anexample of this behavior occured when hurricanes Katrina and Rita blew ashore in the U.S. in2005. Buyers hoarded gasoline - that is, they bought more gasoline at every given price relative to

before the storms developed - because they expected gasoline shortages after the storms.

17

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 20/118

All of these variables may be succinctly expressed in the following general equation, wheresignifies a general function:

Q = f (P ;P ,P ,I,T & P, E)Sarah’s quantity demanded of wine is a number, say 15 bottles, and it is the dependent

variable which depends on many independent variables. The quantity demanded depends, foremost,on the market price of a bottle of wine (P ne). The price of wine is an independent variable becauseit is determined by the wine market. The other independent variables that affect Sarah’s quantitydemanded of wine are the price of complements (P comp ement ), the price of substitutes (P u st tute ), income(I), tastes and preferences (T & P), and expectations of the future (E).

2.4 The Law of Demand

Unlike Sarah’s quantity demanded of wine, which is a number, her demand or wine is a

set of numbers. It is a relationship that reveals how many bottles of wine she demands at each andevery price of wine.

Consider this question: What is Sarah’s quantity demanded of wine when the price is $90 per bottle? In order to get a simple answer to this question we have to make an assumption: theceteris paribus assumption. eteris paribus is a Latin phrase that means other things equal. Forour purposes, when the eteris paribus assumption is imposed, every independant variable exceptthe price of wine is held constant.

The eteris paribus assumption is analogous to taking a digital picture of the marketplace,whereby you stop the market in both time and space. Once all motion stops, we may more easilyanalyze the marketplace. In particular, we can discover how many bottles of wine Sarah willdemand when the price is $9.

If the price of wine decreases, then ceteris paribus the quantity demanded of wine willincrease. The reverse is also true. If the price of wine increases, then ceteris paribus the quantitydemanded of wine will decrease. This negative relationship between the price of wine and thequantity demanded always holds true – it is called the law of demand

demanded wine

18

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 21/118

2.5 Shifts of the Demand Curve

The demand curve shifts only when there is a change in one of the independent variablesheld fixed under the eteris paribus assumption. Therefore, the demand curve shifts only when asecond proverbial digital photo of the marketplace is taken. Something other than the price of winehas to be different in some way for the demand curve for wine to shift. There are no exceptions to

this ruleMoreover, a demand curve shift only to the south-west or to the orth-east For example,

if the price of Gouda cheese, a omplement to wine, increases, then Sarah is willing to buy fewer bottles of wine at any given price. Because of the increase in the price of Gouda cheese, Sarah’sdemand curve for wine shifts to the south-west. This is so because Sarah likes wine and cheesetogether and the more expensive cheese is, the fewer blocks of cheese and bottles of wine she will

buy.

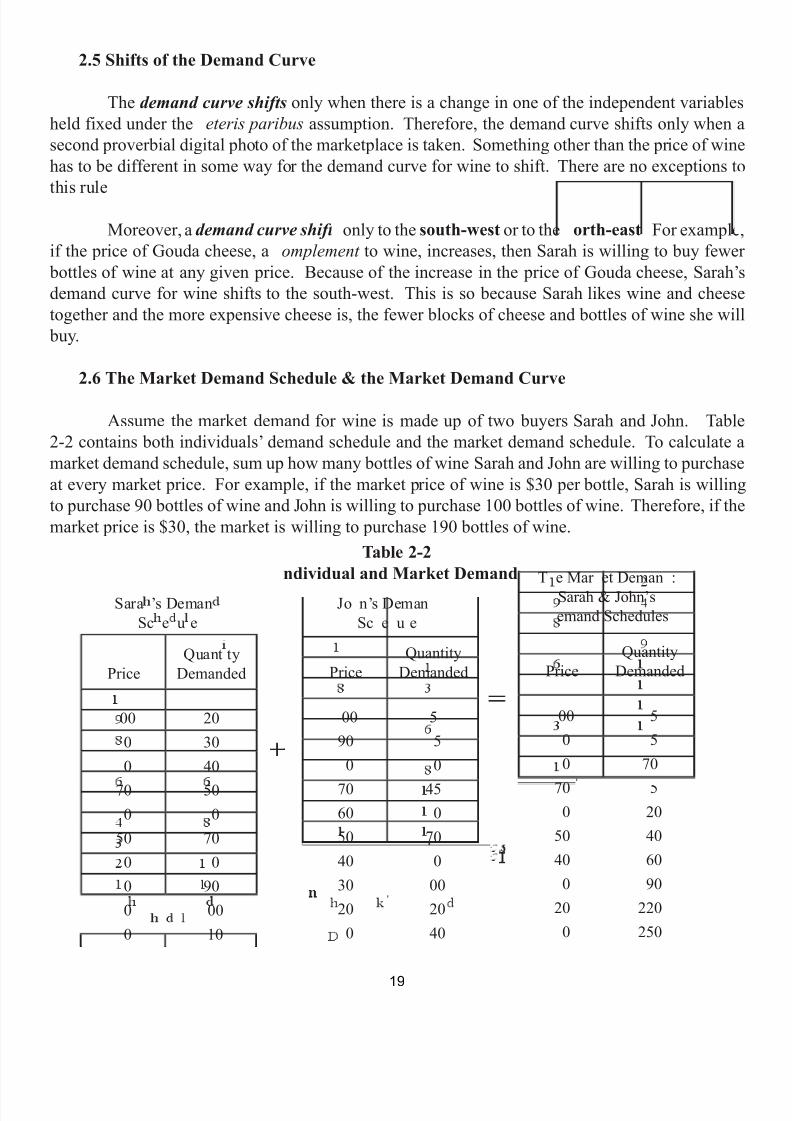

2.6 The Market Demand Schedule & the Market Demand Curve

Assume the market demand for wine is made up of two buyers Sarah and John. Table2-2 contains both individuals’ demand schedule and the market demand schedule. To calculate amarket demand schedule, sum up how many bottles of wine Sarah and John are willing to purchaseat every market price. For example, if the market price of wine is $30 per bottle, Sarah is willingto purchase 90 bottles of wine and John is willing to purchase 100 bottles of wine. Therefore, if themarket price is $30, the market is willing to purchase 190 bottles of wine.

Table 2-2ndividual and Market Demand

PriceQuant ty

Demanded

00 200 300 40

70 500 0

50 700 00 900 000 10

PriceQuantity

Demanded

00 590 5

0 0

70 4560 050 7040 030 0020 20

0 40

PriceQuantity

Demanded

00 50 50 70

70 50 20

50 4040 60

0 9020 220

0 250

Sara ’s DemanSc e u e

Jo n’s DemanSc e u e

T e Mar et Deman :Sarah & John’semand Schedules

19

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 22/118

The market demand function (below) contains one additional independent variable: thenumber of buyers in the market . As the number of buyers in the market increases, ceteris

paribus the market demand curve shifts to the north-east. And if the umber of buyers in themarket decreases, ceteris paribus , the market demand curve shifts to the south-west.

= f (P ;P ,P ,I,T & P, E,# of Buyers)

The horizontal summation of Sarah and John’s demand curves yields the market demandcurve and it is depicted in figure 2-2.

igure 2-2arket Demand Curve

ne

��

�

�

�

�

�

�

�

�

�

�

�

�

Market Demand Curve

20

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 23/118

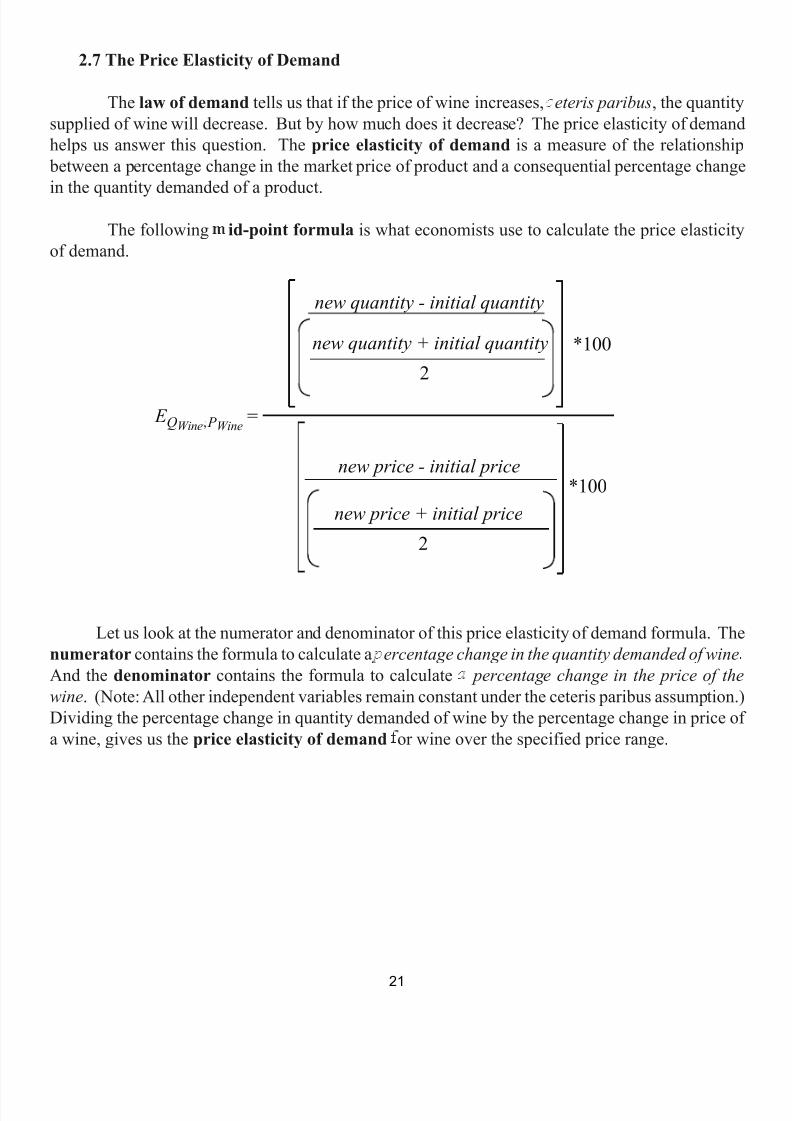

2.7 The Price Elasticity of Demand

The law of demand tells us that if the price of wine increases, eteris paribus , the quantitysupplied of wine will decrease. But by how much does it decrease? The price elasticity of demandhelps us answer this question. The price elasticity of demand is a measure of the relationship

between a percentage change in the market price of product and a consequential percentage change

in the quantity demanded of a product.The following id-point formula is what economists use to calculate the price elasticity

of demand.

Let us look at the numerator and denominator of this price elasticity of demand formula. Thenumerator contains the formula to calculate a ercentage change in the quantity demanded of wineAnd the denominator contains the formula to calculate percentage change in the price of thewine . (Note: All other independent variables remain constant under the ceteris paribus assumption.)Dividing the percentage change in quantity demanded of wine by the percentage change in price ofa wine, gives us the price elasticity of demand or wine over the specified price range.

new quantity - initial quantity

new quantity + initial quantity

new price - initial price

new price + initial price2

2

*100

*100

E QWine , P Wine

=,

21

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 24/118

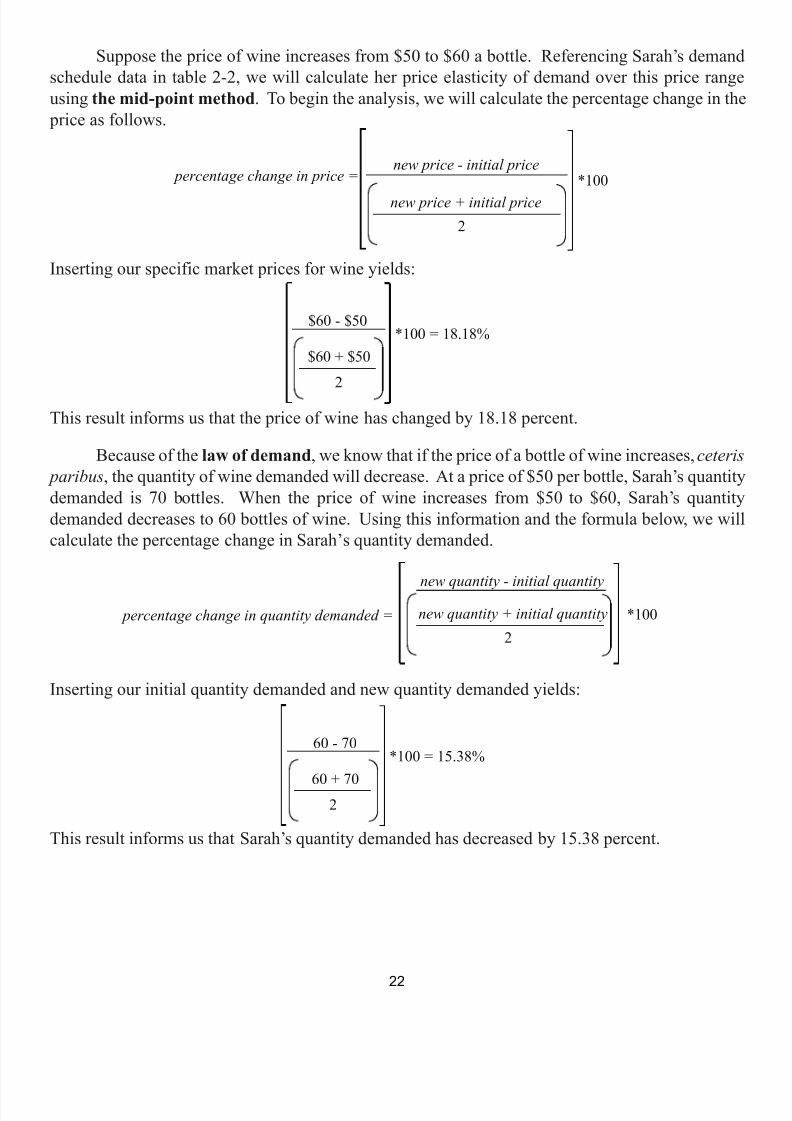

Suppose the price of wine increases from $50 to $60 a bottle. Referencing Sarah’s demandschedule data in table 2-2, we will calculate her price elasticity of demand over this price rangeusing the mid-point method . To begin the analysis, we will calculate the percentage change in the

price as follows.

Inserting our specific market prices for wine yields:

This result informs us that the price of wine has changed by 18.18 percent.

Because of the law of demand , we know that if the price of a bottle of wine increases, ceteris paribus , the quantity of wine demanded will decrease. At a price of $50 per bottle, Sarah’s quantitydemanded is 70 bottles. When the price of wine increases from $50 to $60, Sarah’s quantitydemanded decreases to 60 bottles of wine. Using this information and the formula below, we willcalculate the percentage change in Sarah’s quantity demanded.

Inserting our initial quantity demanded and new quantity demanded yields:

This result informs us that Sarah’s quantity demanded has decreased by 15.38 percent.

new price - initial price

new price + initial price2

*100 percentage change in price =

$60 - $50

$60 + $50

2

*100 = 18.18%

new quantity - initial quantity

new quantity + initial quantity2

*100 percentage change in quantity demanded =

60 - 70

60 + 70

2

*100 = 15.38%

22

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 25/118

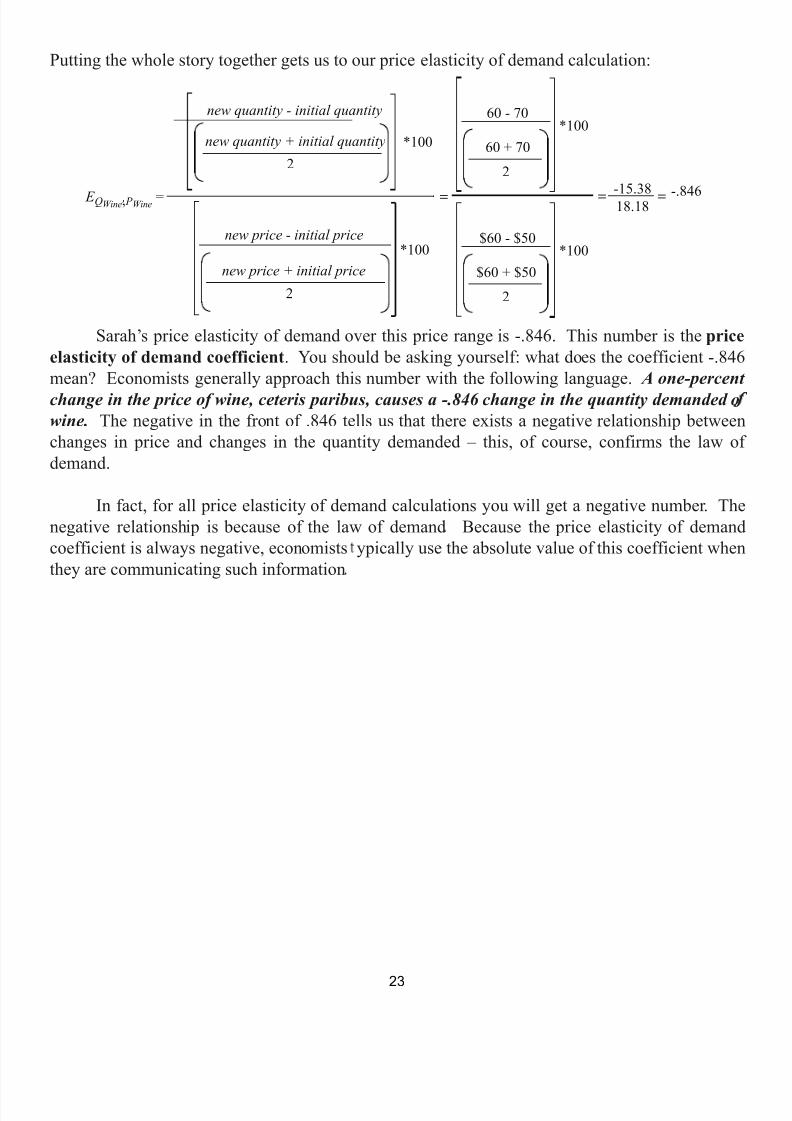

Putting the whole story together gets us to our price elasticity of demand calculation:

Sarah’s price elasticity of demand over this price range is -.846. This number is the priceelasticity of demand coefficient . You should be asking yourself: what does the coefficient -.846mean? Economists generally approach this number with the following language. A one-percentchange in the price of wine, ceteris paribus, causes a -.846 change in the quantity demanded owine. The negative in the front of .846 tells us that there exists a negative relationship betweenchanges in price and changes in the quantity demanded – this, of course, confirms the law ofdemand.

In fact, for all price elasticity of demand calculations you will get a negative number. Thenegative relationship is because of the law of demand Because the price elasticity of demandcoefficient is always negative, economists ypically use the absolute value of this coefficient whenthey are communicating such information

new quantity - initial quantity

new quantity + initial quantity

new price - initial price

new price + initial price2

2

*100

*100

E QWine , P Wine =

60 - 70

60 + 70

2

*100

$60 - $50

$60 + $50

2

*100

� �

-15.3818.18

� -.846,

23

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 26/118

Here is a second question you should be asking yourself: does the size of the number matter?In this case, size does matter. Consider the following three categories that economists use to analyzea price elasticity of demand calculation.

The first price elasticity of demand category is a coefficient with an absolute value of lessthan one . If the price elasticity of demand has an absolute value of less than one, then the demandcurve is inelastic around the prices analyzed. In this category, a one-percent price change generatesa less than one-percent change in the quantity demanded. When the demand curve is inelastic,consumers do not radically change their quantity demanded when the market price changes. Forexample, consumers of insulin (a product that diabetics need to live) do no change their consumptionof insulin when the price of insulin changes. Insulin consumers are not responsive to price changes

because there are few substitute goods available.

The second price elasticity of demand category is a coefficient with an absolute value of greater than one . If the price elasticity of demand has an absolute value of greater than one,then the demand curve is elastic around the prices analyzed. In this category, a one-percent price

change generates a greater than one-percent change in the quantity demanded. When the demandcurve is elastic, consumers significantly change their quantity demanded when the market pricechanges. For example, a study has proven that when the price of a Honda Civic increases by one-

percent, consumers decrease their quantity demanded by four-percent. Honda Civic consumers areresponsive to price changes because there are a lot of other cars available.

The last price elasticity of demand category is a coefficient with an absolute value of one . Ifthe price elasticity of demand has an absolute value of precisely one, then the demand curve is unitelastic or of unitary elasticity around the prices analyzed. Here, a one-percent change in pricegenerates an equal one-percent change in the quantity demanded.

2.8 The Cross Price Elasticity of Demand

Economists use the cross price elasticity coefficient to observe whether two goods arerelated; and if they are related, whether the goods are complements or substitutes . For example,if the price of Gouda cheese increases, Sarah’s demand for wine shifts to the south-west, ceteris

paribus , because Sarah considers wine and cheese complements . However, until now we have not been able to express by how much her demand for wine changes. Economists use a cross priceelasticity of demand calculation to assist in this task.

Consider the following two cross price elasticity examples. First, suppose the demandschedule in table 2-1 assumes that the price of Gouda cheese is $6.50 per pound. When the market

price of wine is $50 per bottle, Sarah demands 70 bottles of wine. If the price of Gouda cheeseincreases to $8.50 per pound, then ceteris paribus at a price $50 per bottle of wine Sarah’s quantitydemanded of wine decreases to 60 bottles.

24

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 27/118

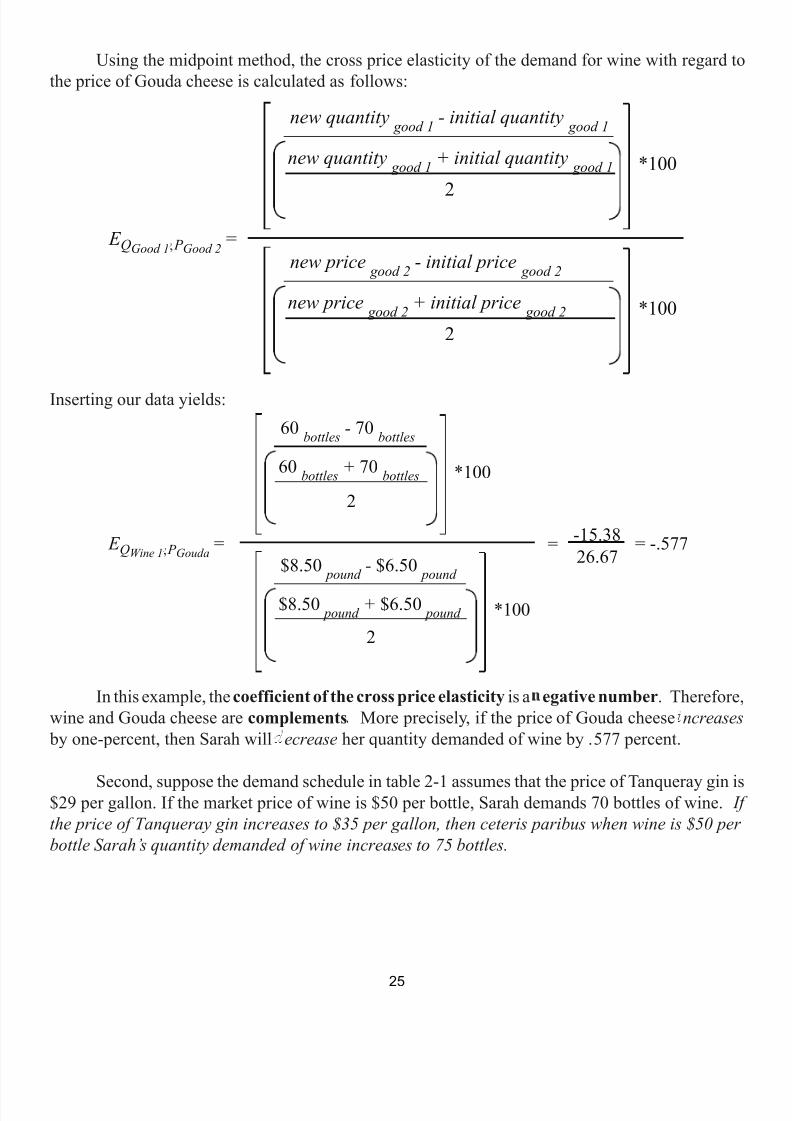

Using the midpoint method, the cross price elasticity of the demand for wine with regard tothe price of Gouda cheese is calculated as follows:

Inserting our data yields:

In this example, the coefficient of the cross price elasticity is a egative number . Therefore,wine and Gouda cheese are complements More precisely, if the price of Gouda cheese ncreases

by one-percent, then Sarah will ecrease her quantity demanded of wine by .577 percent.

Second, suppose the demand schedule in table 2-1 assumes that the price of Tanqueray gin is$29 per gallon. If the market price of wine is $50 per bottle, Sarah demands 70 bottles of wine. Ifthe price of Tanqueray gin increases to $35 per gallon, then ceteris paribus when wine is $50 perbottle Sarah’s quantity demanded of wine increases to 75 bottles.

new quantity good 1 - initial quantity good 1

new quantity good 1 + initial quantity good 12

*100

E QGood 1 , P Good 2

=new price good 2 - initial price good 2

new price good 2 + initial price good 22

*100

60 bottles - 70 bottles

60 bottles + 70 bottles

2

*100

E QWine 1 , P Gouda =$8.50 pound - $6.50 pound

$8.50 pound + $6.50 pound

2

*100

= -15.3826.67

= -.577

,

,

25

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 28/118

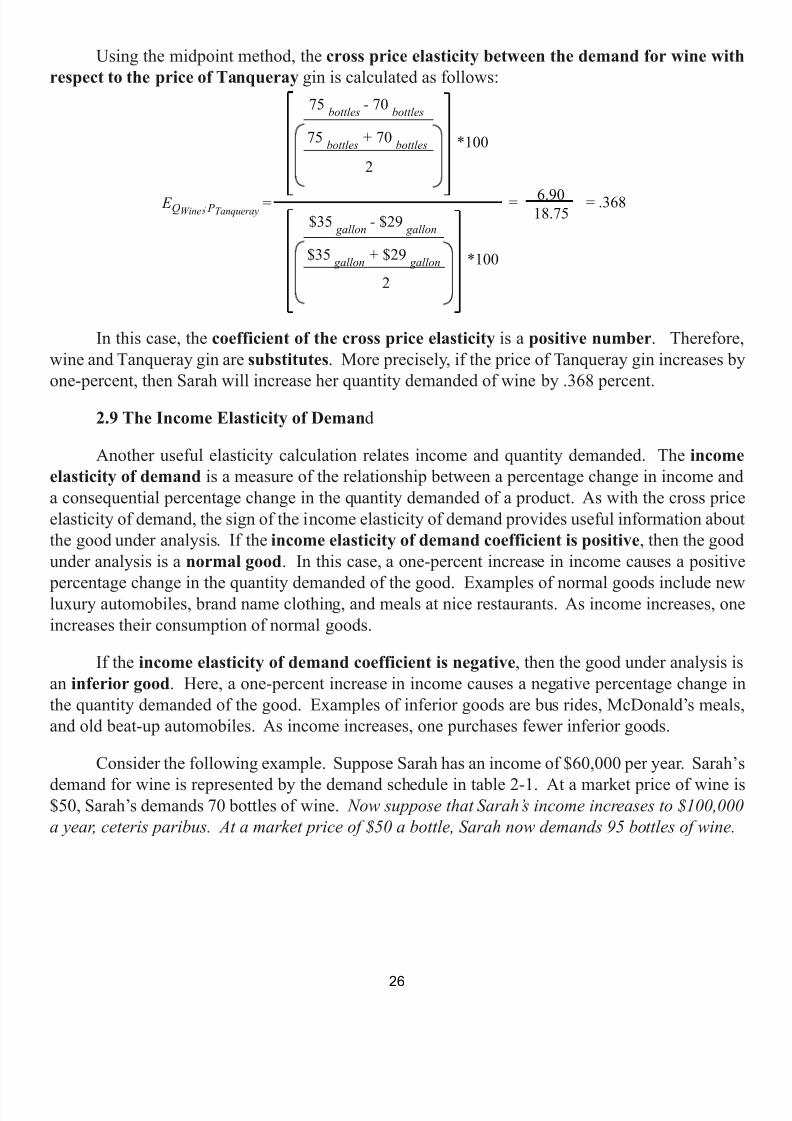

Using the midpoint method, the cross price elasticity between the demand for wine withrespect to the price of Tanqueray gin is calculated as follows:

In this case, the coefficient of the cross price elasticity is a positive number . Therefore,wine and Tanqueray gin are substitutes . More precisely, if the price of Tanqueray gin increases byone-percent, then Sarah will increase her quantity demanded of wine by .368 percent.

2.9 The Income Elasticity of Deman d

Another useful elasticity calculation relates income and quantity demanded. The incomeelasticity of demand is a measure of the relationship between a percentage change in income anda consequential percentage change in the quantity demanded of a product. As with the cross priceelasticity of demand, the sign of the income elasticity of demand provides useful information aboutthe good under analysis. If the income elasticity of demand coefficient is positive , then the goodunder analysis is a normal good . In this case, a one-percent increase in income causes a positive

percentage change in the quantity demanded of the good. Examples of normal goods include newluxury automobiles, brand name clothing, and meals at nice restaurants. As income increases, oneincreases their consumption of normal goods.

If the income elasticity of demand coefficient is negative , then the good under analysis isan inferior good . Here, a one-percent increase in income causes a negative percentage change inthe quantity demanded of the good. Examples of inferior goods are bus rides, McDonald’s meals,and old beat-up automobiles. As income increases, one purchases fewer inferior goods.

Consider the following example. Suppose Sarah has an income of $60,000 per year. Sarah’s

demand for wine is represented by the demand schedule in table 2-1. At a market price of wine is$50, Sarah’s demands 70 bottles of wine. Now suppose that Sarah’s income increases to $100,000a year, ceteris paribus. At a market price of $50 a bottle, Sarah now demands 95 bottles of wine.

75 bottles - 70 bottles

75 bottles + 70 bottles

2

*100

E QWine , P Tanqueray

=$35 gallon - $29 gallon

$35 gallon + $29 gallon

2

*100

= 6.9018.75

= .368

26

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 29/118

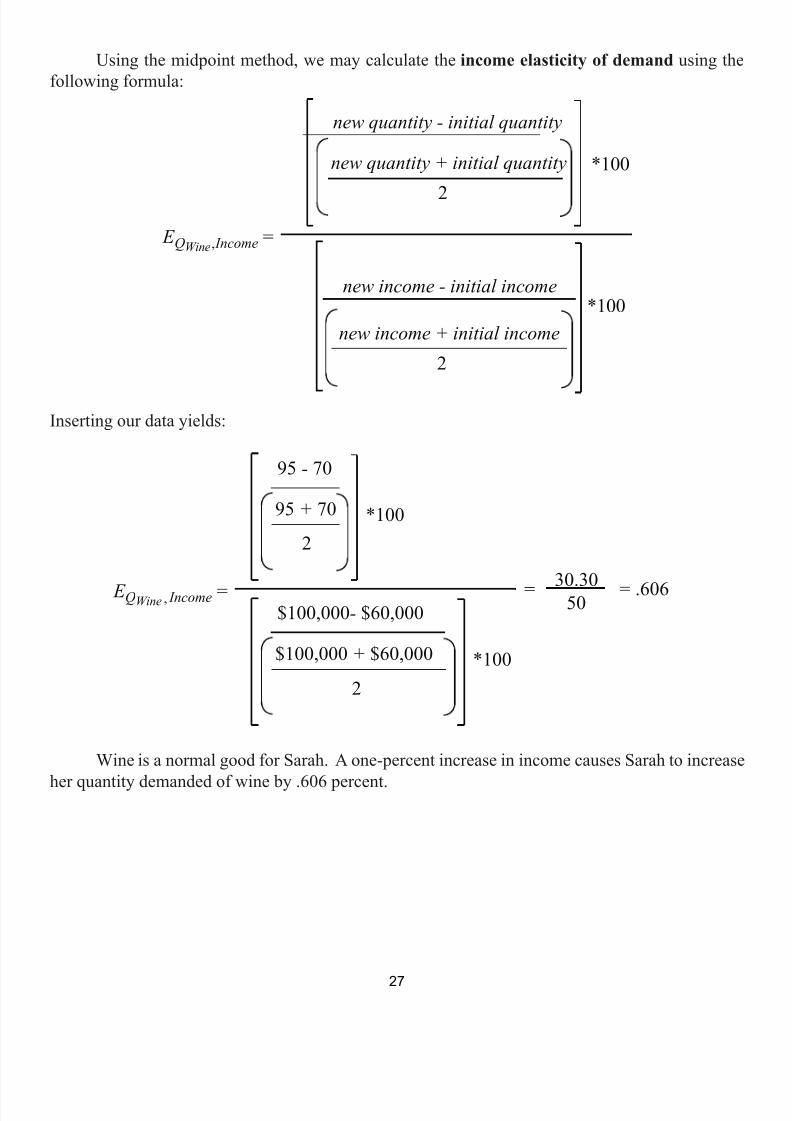

Using the midpoint method, we may calculate the income elasticity of demand using thefollowing formula:

Inserting our data yields:

Wine is a normal good for Sarah. A one-percent increase in income causes Sarah to increase

her quantity demanded of wine by .606 percent.

new quantity - initial quantity

new quantity + initial quantity

new income - initial income

new income + initial income2

2

*100

*100

E QWine , Income

=

95 - 70

95 + 70

2

*100

E QWine , Income =$100,000 - $60,000

$100,000 + $60,000

2

*100

= 30.30

50 = .606

,

,

27

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 30/118

3. Supply

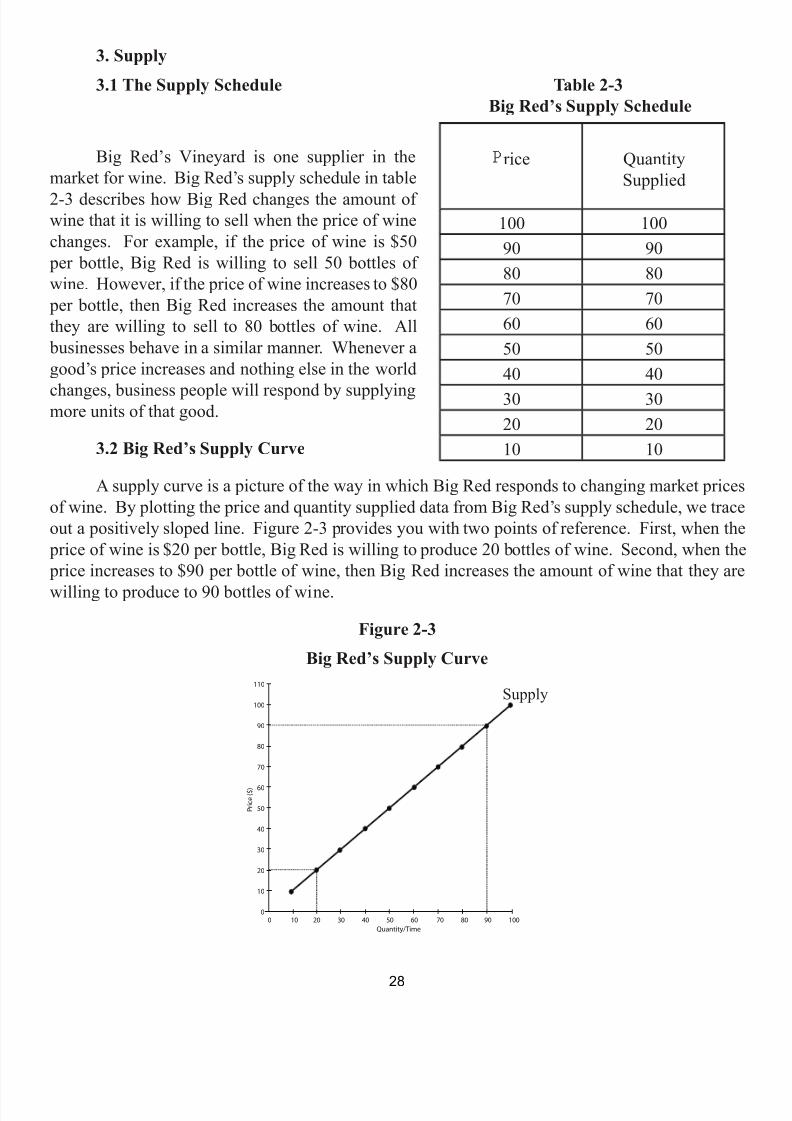

3.1 The Supply Schedule Table 2-3 Big Red’s Supply Schedule

Big Red’s Vineyard is one supplier in themarket for wine. Big Red’s supply schedule in table2-3 describes how Big Red changes the amount ofwine that it is willing to sell when the price of winechanges. For example, if the price of wine is $50

per bottle, Big Red is willing to sell 50 bottles ofwine. However, if the price of wine increases to $80

per bottle, then Big Red increases the amount thatthey are willing to sell to 80 bottles of wine. All

businesses behave in a similar manner. Whenever agood’s price increases and nothing else in the world

changes, business people will respond by supplyingmore units of that good.

3.2 Big Red’s Supply Curve

A supply curve is a picture of the way in which Big Red responds to changing market pricesof wine. By plotting the price and quantity supplied data from Big Red’s supply schedule, we traceout a positively sloped line. Figure 2-3 provides you with two points of reference. First, when the

price of wine is $20 per bottle, Big Red is willing to produce 20 bottles of wine. Second, when the price increases to $90 per bottle of wine, then Big Red increases the amount of wine that they arewilling to produce to 90 bottles of wine.

Figure 2-3

Big Red’s Supply Curve

rice QuantitySupplied

100 10090 9080 8070 7060 6050 5040 4030 3020 2010 10

�

��

�

�

�

�

�

�

�

�

�

�

�

�

Supply

28

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 31/118

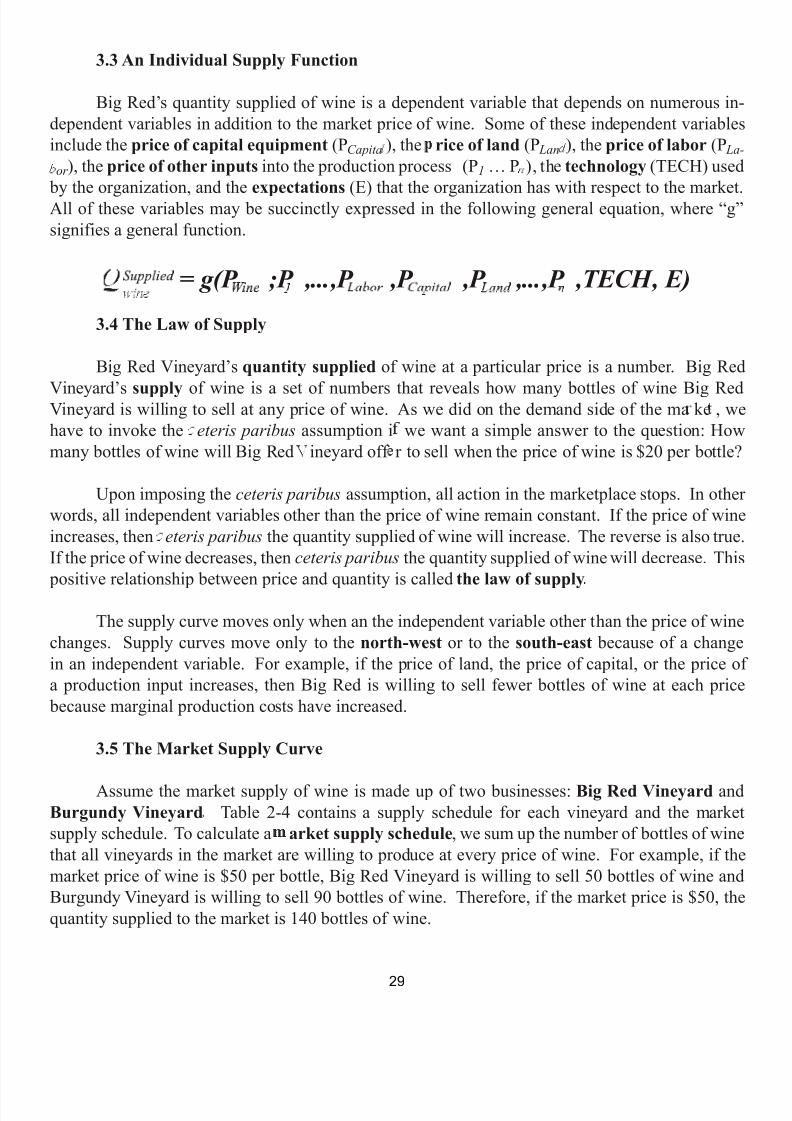

3.3 An Individual Supply Function

Big Red’s quantity supplied of wine is a dependent variable that depends on numerous in-dependent variables in addition to the market price of wine. Some of these independent variablesinclude the price of capital equipment (PCapita ), the rice of land (P Lan ), the price of labor (P La-

or ), the price of other inputs into the production process (P 1 … P ), the technology (TECH) used

by the organization, and the expectations (E) that the organization has with respect to the market.All of these variables may be succinctly expressed in the following general equation, where “g”signifies a general function.

= g(P ;P ,...,P ,P ,P ,...,P ,TECH, E)

3.4 The Law of Supply

Big Red Vineyard’s quantity supplied of wine at a particular price is a number. Big Red

Vineyard’s supply of wine is a set of numbers that reveals how many bottles of wine Big RedVineyard is willing to sell at any price of wine. As we did on the demand side of the ma ke , wehave to invoke the eteris paribus assumption i we want a simple answer to the question: Howmany bottles of wine will Big Red ineyard off r to sell when the price of wine is $20 per bottle?

Upon imposing the ceteris paribus assumption, all action in the marketplace stops. In otherwords, all independent variables other than the price of wine remain constant. If the price of wineincreases, then eteris paribus the quantity supplied of wine will increase. The reverse is also true.If the price of wine decreases, then ceteris paribus the quantity supplied of wine will decrease. This

positive relationship between price and quantity is called the law of supply

The supply curve moves only when an the independent variable other than the price of winechanges. Supply curves move only to the north-west or to the south-east because of a changein an independent variable. For example, if the price of land, the price of capital, or the price ofa production input increases, then Big Red is willing to sell fewer bottles of wine at each price

because marginal production costs have increased.

3.5 The Market Supply Curve

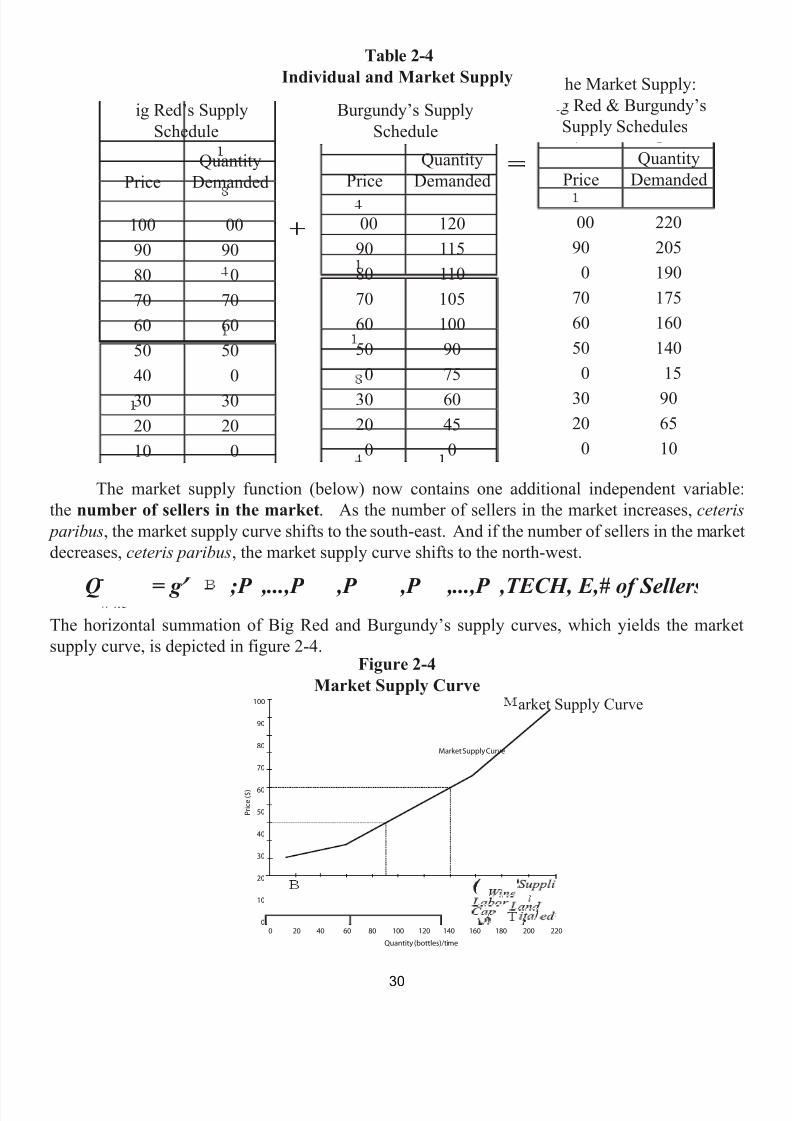

Assume the market supply of wine is made up of two businesses: Big Red Vineyard andBurgundy Vineyard Table 2-4 contains a supply schedule for each vineyard and the marketsupply schedule. To calculate a arket supply schedule , we sum up the number of bottles of winethat all vineyards in the market are willing to produce at every price of wine. For example, if themarket price of wine is $50 per bottle, Big Red Vineyard is willing to sell 50 bottles of wine andBurgundy Vineyard is willing to sell 90 bottles of wine. Therefore, if the market price is $50, thequantity supplied to the market is 140 bottles of wine.

29

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 32/118

Table 2-4Individual and Market Supply

The market supply function (below) now contains one additional independent variable:the number of sellers in the market . As the number of sellers in the market increases, ceteris

paribus , the market supply curve shifts to the south-east. And if the number of sellers in the marketdecreases, ceteris paribus , the market supply curve shifts to the north-west.

Q = g P ;P ,...,P ,P ,P ,...,P ,TECH, E,# of SellersThe horizontal summation of Big Red and Burgundy’s supply curves, which yields the marketsupply curve, is depicted in figure 2-4.

Figure 2-4Market Supply Curve

PriceQuantity

Demanded

100 0090 9080 070 7060 6050 5040 030 3020 2010 0

PriceQuantity

Demanded

00 12090 11580 11070 10560 10050 90

0 7530 6020 45

0 0

PriceQuantity

Demanded

00 22090 205

0 19070 17560 16050 140

0 15

30 9020 65

0 10

ig Red’s SupplySchedule

Burgundy’s SupplySchedule

he Market Supply:ig Red & Burgundy’sSupply Schedules

w ne

��

�

�

�

�

�

�

�

�

�

�

�

�

arket Supply Curve

30

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 33/118

3.6 The Supply Elasticity

The law of supply tells us that if the price of wine increases, eteris paribus, then the quantitydemanded of wine will increase. But by how much does it increase? The price elasticity of supplyhelps us answer this question. The price elasticity of supply is a measure of the relationship

between a percentage change in the market price of a product and a consequential percentage

change in the quantity supplied of a product.The following mid-point formula is what economists use to calculate the price elasticity of

supply.

The umerator contains the formula to calculate a percentage change in the quantity suppliedof wine The denominator contains the formula for calculating a ercentage change in the priceof the wine Dividing the percentage change in quantity supplied of wine by the percentage changein price of a wine, gives us the rice elasticity of supply or wine over the specified price range

Suppose the price of wine increases from $50 to $60 a bottle and as a result the quantitythat Burgundy is willing supply to the market increases from 90 bottles to 100 bottles. Using themid-point formula, we will now calculate Burgundy’s elasticity of supply over the $50 to $60 pricerange.

new quantity - initial quantity

new quantity + initial quantity

new price - initial price

new price + initial price2

2

*100

*100

eQWine , P Wine =

new quantity - initial quantity

new quantity + initial quantity

new price - initial price

new price + initial price2

2

eQWine , P Wine =

100 - 90

100 + 90

2

*100

$60 - $50

$60 + $50

2

*100

� �

10.53

18.18�

.579

,

,

31

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 34/118

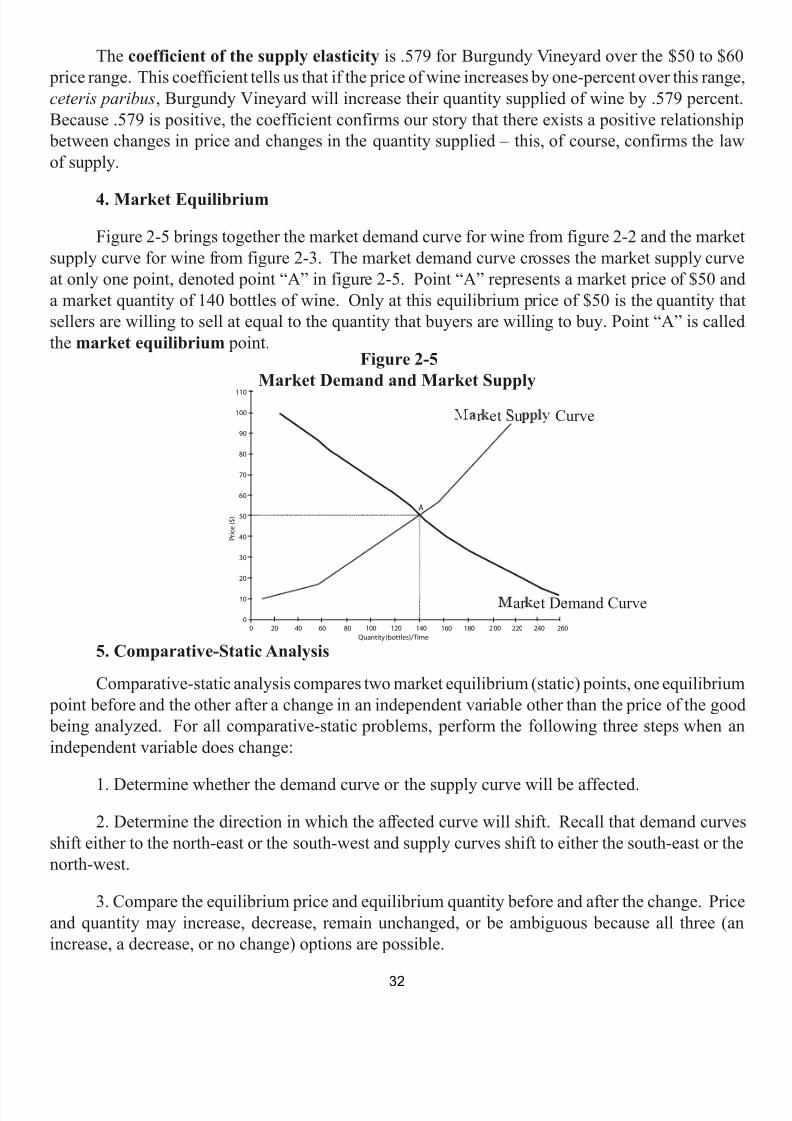

The coefficient of the supply elasticity is .579 for Burgundy Vineyard over the $50 to $60 price range. This coefficient tells us that if the price of wine increases by one-percent over this range,ceteris paribus , Burgundy Vineyard will increase their quantity supplied of wine by .579 percent.Because .579 is positive, the coefficient confirms our story that there exists a positive relationship

between changes in price and changes in the quantity supplied – this, of course, confirms the lawof supply.

4. Market Equilibrium

Figure 2-5 brings together the market demand curve for wine from figure 2-2 and the marketsupply curve for wine from figure 2-3. The market demand curve crosses the market supply curveat only one point, denoted point “A” in figure 2-5. Point “A” represents a market price of $50 anda market quantity of 140 bottles of wine. Only at this equilibrium price of $50 is the quantity thatsellers are willing to sell at equal to the quantity that buyers are willing to buy. Point “A” is calledthe market equilibrium point.

Figure 2-5Market Demand and Market Supply

5. Comparative-Static Analysis

Comparative-static analysis compares two market equilibrium (static) points, one equilibrium point before and the other after a change in an independent variable other than the price of the good being analyzed. For all comparative-static problems, perform the following three steps when anindependent variable does change:

1. Determine whether the demand curve or the supply curve will be affected.

2. Determine the direction in which the affected curve will shift. Recall that demand curvesshift either to the north-east or the south-west and supply curves shift to either the south-east or thenorth-west.

3. Compare the equilibrium price and equilibrium quantity before and after the change. Priceand quantity may increase, decrease, remain unchanged, or be ambiguous because all three (anincrease, a decrease, or no change) options are possible.

�

��

�

�

�

�

�

�

�

�

�

�

�

�

mand Curvear et De

Curver et Su

32

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 35/118

5.1 A Shift in Demand 5.1.1 An Increase in the Price of a Substitute

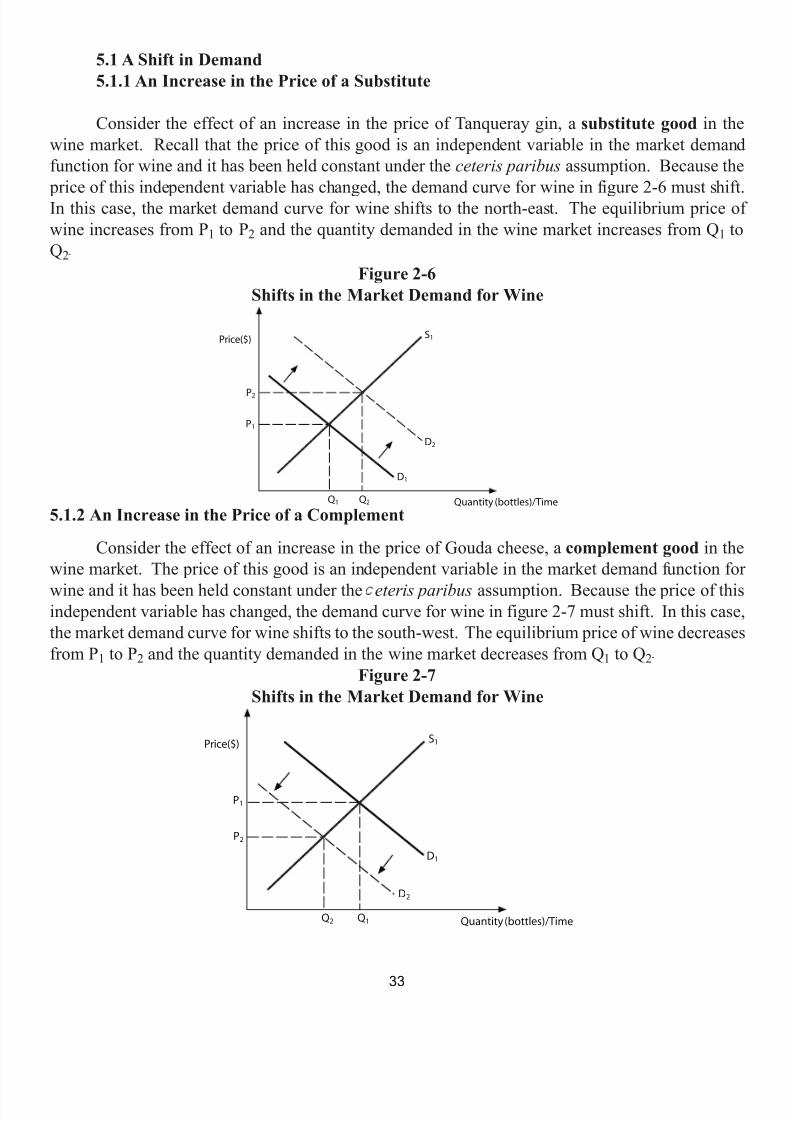

Consider the effect of an increase in the price of Tanqueray gin, a substitute good in thewine market. Recall that the price of this good is an independent variable in the market demandfunction for wine and it has been held constant under the ceteris paribus assumption. Because the

price of this independent variable has changed, the demand curve for wine in figure 2-6 must shift.In this case, the market demand curve for wine shifts to the north-east. The equilibrium price ofwine increases from P 1 to P 2 and the quantity demanded in the wine market increases from Q 1 toQ2

Figure 2-6Shifts in the Market Demand for Wine

5.1.2 An Increase in the Price of a Complement

Consider the effect of an increase in the price of Gouda cheese, a complement good in thewine market. The price of this good is an independent variable in the market demand function for

wine and it has been held constant under the eteris paribus assumption. Because the price of thisindependent variable has changed, the demand curve for wine in figure 2-7 must shift. In this case,the market demand curve for wine shifts to the south-west. The equilibrium price of wine decreasesfrom P 1 to P 2 and the quantity demanded in the wine market decreases from Q 1 to Q 2

Figure 2-7Shifts in the Market Demand for Wine

�

P1

Quantity (bottles)/Time

P2

Q1Q2

Price($)

D2

D1

S1

33

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 36/118

5.1.3 A Decrease in Income for a Normal Good

Consider the effect of a decrease in income in the economy, and assume that wine is a normalgood . Section 2.3 defines a normal good. Income is an independent variable in the market demandfunction for wine and it has been held constant under the ceteris paribus assumption. Becauseincome has changed, the demand curve for wine in figure 2-8 must shift. In this case, the marketdemand curve for wine shifts to the south-west. The equilibrium price of wine decreases from P 1

to P2 and the quantity demanded in the wine market decreases from Q 1 to Q 2.

Figure 2-8Shifts in the Market Demand for Wine

5.1.4 A Decrease in Income for an Inferior Good

Consider the effect of a decrease in the income in the economy, and assume now that wine

is an inferior good . Section 2.3 defines an inferior good. Income is an independent variablein the market demand function for wine and it has been held constant under the ceteris paribusassumption. Because income has changed, the demand curve for wine in figure 2-9 must shift. Inthis case, the market demand curve for wine shifts to the north-east. The equilibrium price of wineincreases from P 1 to P 2 and the quantity demanded in the wine market increases from Q 1 to Q 2.

Figure 2-9Shifts in the Market Demand for Wine

P1

Quantity (bottles)/Time

P2

Q1Q2

Price($)

D2

D1

S1

�

34

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 37/118

5.2 A Shift in Supply 5.2.1 An Increase in the Price of Labor

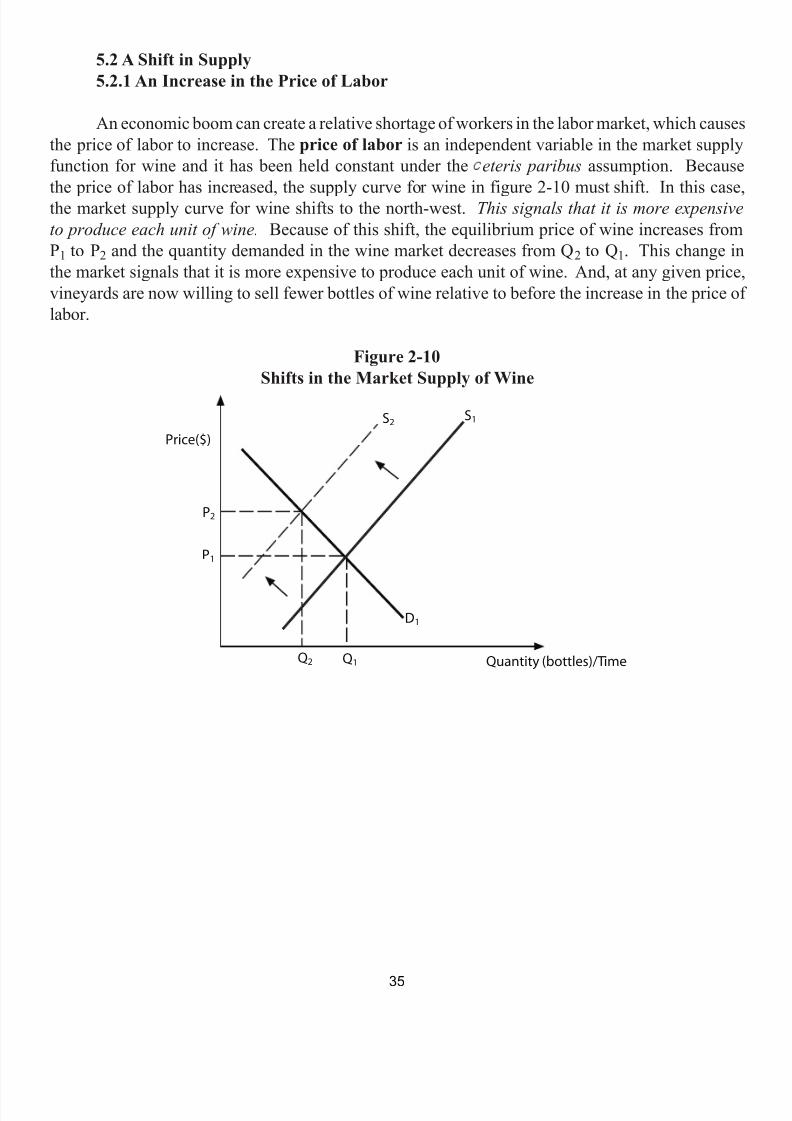

An economic boom can create a relative shortage of workers in the labor market, which causesthe price of labor to increase. The price of labor is an independent variable in the market supplyfunction for wine and it has been held constant under the eteris paribus assumption. Because

the price of labor has increased, the supply curve for wine in figure 2-10 must shift. In this case,the market supply curve for wine shifts to the north-west. This signals that it is more expensiveto produce each unit of wine. Because of this shift, the equilibrium price of wine increases fromP1 to P 2 and the quantity demanded in the wine market decreases from Q 2 to Q 1. This change inthe market signals that it is more expensive to produce each unit of wine. And, at any given price,vineyards are now willing to sell fewer bottles of wine relative to before the increase in the price oflabor.

Figure 2-10Shifts in the Market Supply of Wine

�

35

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 38/118

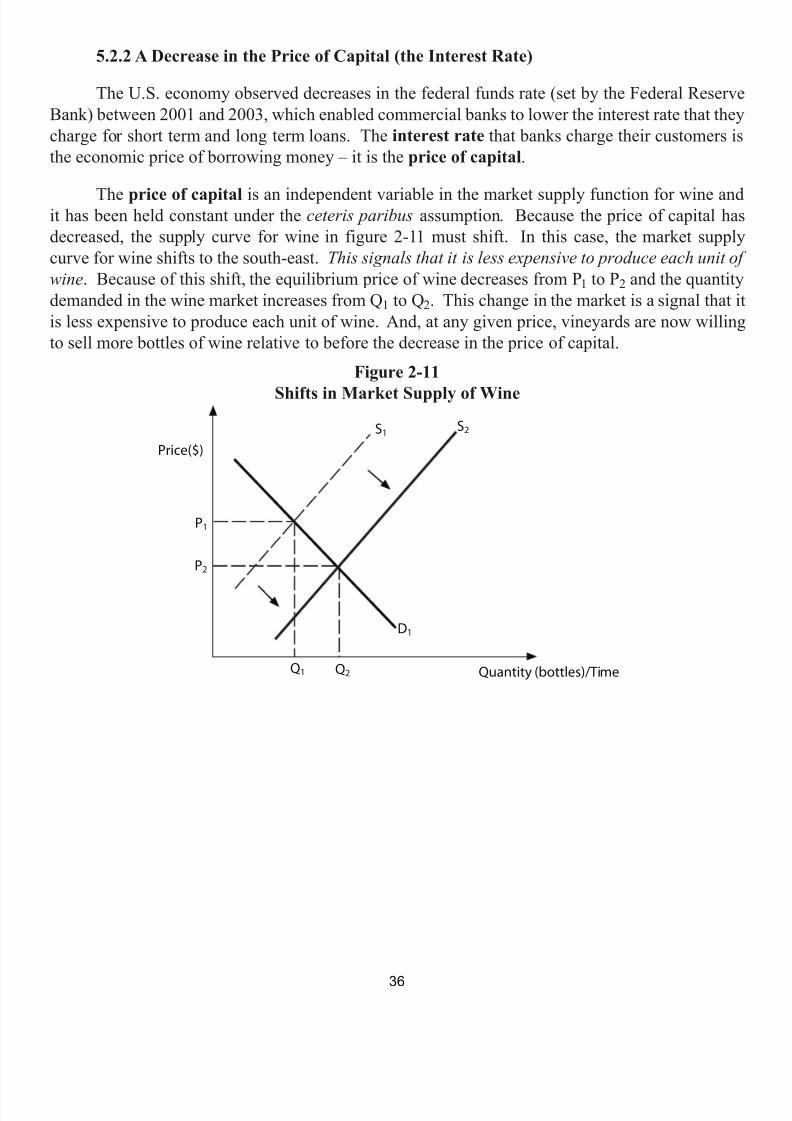

5.2.2 A Decrease in the Price of Capital (the Interest Rate)

The U.S. economy observed decreases in the federal funds rate (set by the Federal ReserveBank) between 2001 and 2003, which enabled commercial banks to lower the interest rate that theycharge for short term and long term loans. The interest rate that banks charge their customers isthe economic price of borrowing money – it is the price of capital .

The price of capital is an independent variable in the market supply function for wine andit has been held constant under the ceteris paribus assumption. Because the price of capital hasdecreased, the supply curve for wine in figure 2-11 must shift. In this case, the market supplycurve for wine shifts to the south-east. This signals that it is less expensive to produce each unit ofwine . Because of this shift, the equilibrium price of wine decreases from P 1 to P 2 and the quantitydemanded in the wine market increases from Q 1 to Q2. This change in the market is a signal that itis less expensive to produce each unit of wine. And, at any given price, vineyards are now willingto sell more bottles of wine relative to before the decrease in the price of capital.

Figure 2-11

Shifts in Market Supply of Wine

�

36

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 39/118

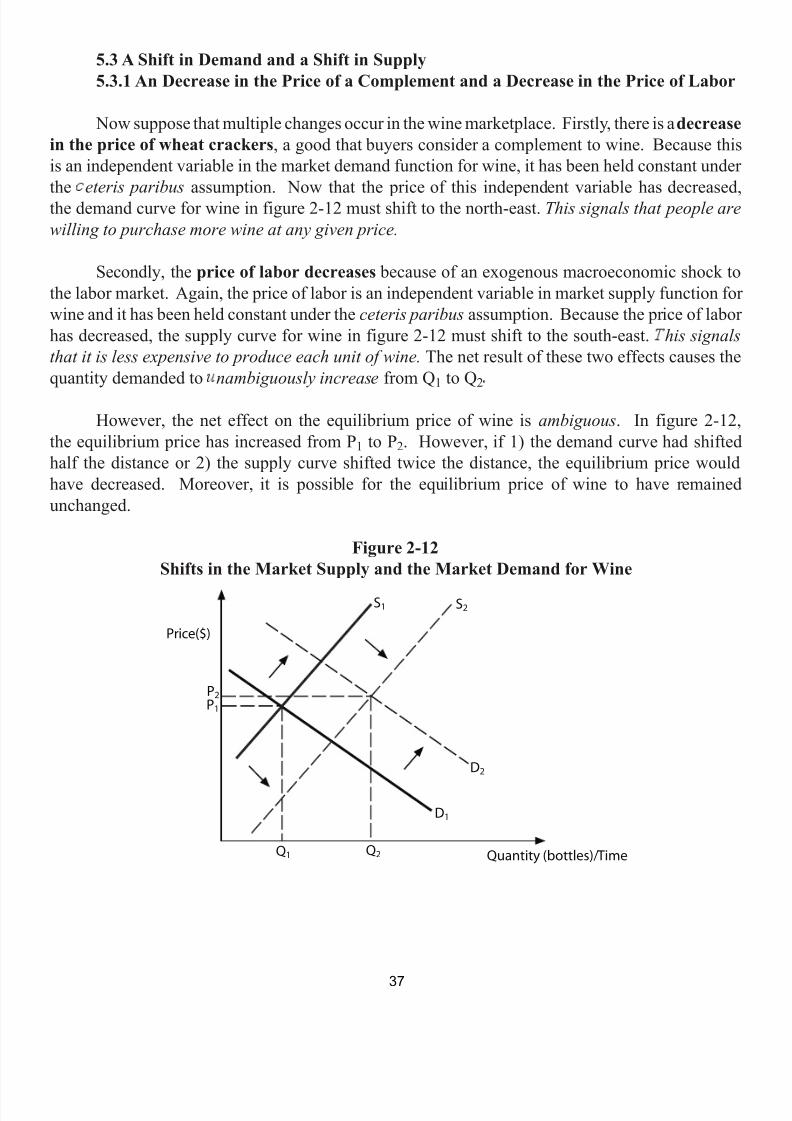

5.3 A Shift in Demand and a Shift in Supply 5.3.1 An Decrease in the Price of a Complement and a Decrease in the Price of Labor

Now suppose that multiple changes occur in the wine marketplace. Firstly, there is a decreasein the price of wheat crackers , a good that buyers consider a complement to wine. Because thisis an independent variable in the market demand function for wine, it has been held constant under

theeteris paribus

assumption. Now that the price of this independent variable has decreased,the demand curve for wine in figure 2-12 must shift to the north-east. This signals that people arewilling to purchase more wine at any given price.

Secondly, the price of labor decreases because of an exogenous macroeconomic shock tothe labor market. Again, the price of labor is an independent variable in market supply function forwine and it has been held constant under the ceteris paribus assumption. Because the price of laborhas decreased, the supply curve for wine in figure 2-12 must shift to the south-east. his signalsthat it is less expensive to produce each unit of wine. The net result of these two effects causes thequantity demanded to nambiguously increase from Q 1 to Q 2

However, the net effect on the equilibrium price of wine is ambiguous . In figure 2-12,the equilibrium price has increased from P 1 to P 2. However, if 1) the demand curve had shiftedhalf the distance or 2) the supply curve shifted twice the distance, the equilibrium price wouldhave decreased. Moreover, it is possible for the equilibrium price of wine to have remainedunchanged.

Figure 2-12Shifts in the Market Supply and the Market Demand for Wine

�

37

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 40/118

5.3.2 An Increase in the Number of Buyers and an Increase in the Price of Land

Successful expenditures on advertising can have the effect of creating new buyers of wine.The number of buyers is an independent variable in the market demand function for wine, whichhas been held constant under the ceteris paribus assumption. With an increase in the number of

buyers, the demand curve for wine in figure 2-13 will shift to the north-east. This signals that more people are willing to purchase wine at any given price.

Second, suppose that there is a simultaneous increase in the price of land because all vineyardowners try to marginally increase their production capacity. The price of land is an independentvariable in market supply function for wine and it has been held constant under the ceteris paribusassumption. Because the price of land has increased, the market supply curve for wine in figure2-13 will shift to the north-west. The net result of these two effects causes the price of wine toincrease from P 1 to P 2.

However, the net effect on the equilibrium price is ambiguous . In figure 2-13, the equilibriumquantity has not changed. However, for example, if 1) the demand curve had shifted twice thedistance or 2) the supply curve shifted half the distance, the equilibrium quantity would haveincreased. Moreover, it is possible for the equilibrium quantity to have decreased if the demandshifted half the distance or supply curve shifted twice the distance shown in Figure 2-13. Thus,in this case, we would need additional information about the magnitude of the shifts for us todetermine the actual affect on the equilibrium quantity of wine.

Figure 2-13Shifts in the Market Supply and Market Demand for Wine

�

38

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 41/118

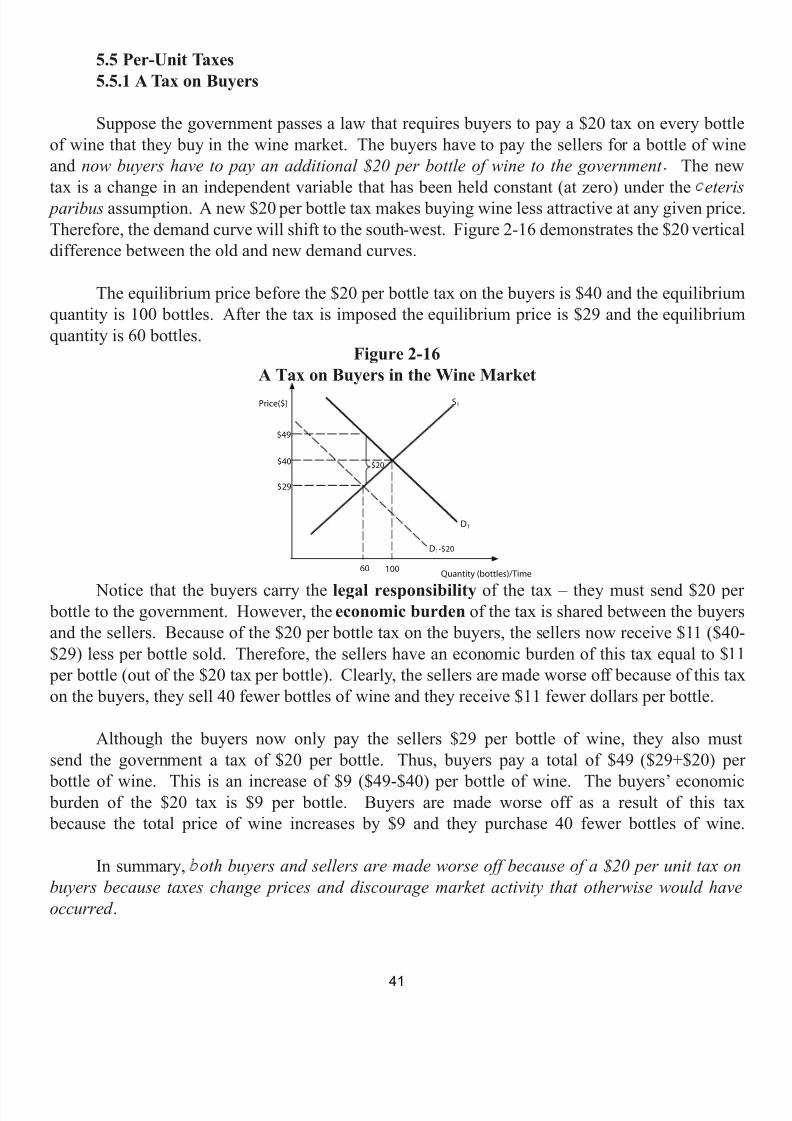

5.4 Price Controls 5.4.1 A Binding Price Ceiling

A price ceiling is a government imposed and legally enforced maximum market price.Governments implement such policies with noble intentions. For example, government enforcedrent controls impose a maximum price for apartments, with the intention of increasing the number

of affordable apartments for lower income tenants. Nevertheless, the collective group of rentersand the market as a whole are never better off because of government imposed price ceilings ina market. Moreover, history has demonstrated that low income families have fewer apartmentsavailable to them when rent controls are in place.

Consider the wine market in figure 2-14. Before the price ceiling is imposed, the equilibrium price is $50 and the equilibrium quantity is Q 2 Now suppose the government imposes a priceceiling of $30 in the wine market. This means that $30 is the maximum price that any seller maycharge for a bottle of wine.

Figure 2-14A Binding Price Ceiling in the Wine Market

The $30 price ceiling is “ binding because the market price changes as a result of thegovernment policy. At a price ceiling of $30, the quantity demanded is Q 3 and the quantitysupplied at the price ceiling is Q 1. Because of the price ceiling, the quantity demandedexceeds the quantity supplied. There is a shortage of bottles of wine at the price ceiling.

The actual quantity sold in the market, however, equals Q 1. Therefore, the price ceilinghas actually reduced the number of bottles of wine bought and sold in the market by Q 2-Q1 It is

because of this, that we say that in the aggregate buyers and sellers are worse as a result of the $30 price ceiling.

Suppose, instead, the government imposed a price ceiling of $60 per bottle of wine. Inthis case, the maximum price that any seller may charge for a bottle of wine is $60. Becausethe equilibrium price is $50, the price ceiling is “ non-binding . The fact that the governmenthas declared that the price of wine cannot increase beyond $60 has no effect on this winemarket. The actual market price of wine remains in equilibrium at $50 per bottle. At theequilibrium price of $50, the quantity demand and the quantity supplied is Q 2. Thus, a non-

binding price ceiling has absolutely no effect on the equilibrium price or equilibrium quantity.

�

�

�

39

7/21/2019 PSU IVY Fundamentals of Economics

http://slidepdf.com/reader/full/psu-ivy-fundamentals-of-economics 42/118

5.4.2 A Binding Price Floor

A price floor is a government imposed and legally enforced minimum market price.Governments have implemented price floors with noble intentions, too. For example, the intentionof creating a living-wage for low income workers is a reason why policy-makers enact minimumwage legislation. Nevertheless, low-income workers, as a group, are never better off with aminimum wage. Some workers that are willing to work at a price below the minimum wage are nolonger offered a job after the minimum wage is imposed.