proton,case study upm

TRANSCRIPT

Staff Paper 8/2006

Business Response to the Regional Demands and Opportunity: A Study of Malaysian Automobile

Industry

Rashid Abdullah Faculty of Economics and Management

Universiti Putra Malaysia 43300 UPM Sedang, Selangor, Malaysia

Business Response to the Regional Demands and Opportunity: A Study of Malaysian Automobile Industry

Rashid Abdullah

.

Abstract This paper examines the business response taken by both automakers (Proton) and supplier (Ingress) in preparing them to face the regional market liberalization of AFTA. As the key automaker in Malaysia, Proton sale is mainly in domestic market and able to capture 68 percent of the total market because of the highly tariffs and custom tax is imposed on all foreign cars. However, things won’t be the same when AFTA is implemented. Both Proton and suppliers should be wise to take measures in to be more competitive among in this auto sector by the year 2005. The key competitiveness lies mainly on technology and market. In order to achieve it, they have to consider their limitations accordingly by put more investment particularly in four main core items namely; technology, own design, cost and quality control, and penetrating into new niche market. New export market and new collaboration with foreign giants and counterpart may workable in both domestic-Malaysian, and regional-ASEAN market.

Introduction

Over the past four decades, the automobile industry has been the subject of long government intervention. The industry has driven industrial development and experienced upgraded domestic technological capabilities (Humphrey, 1999; Abdulsomad, 1999). The automobile industry has also been politicized, and thus was incorporated into national development strategy (MIDA, 1986)1. Promoting the automobile industry in developing economies requires protective instruments (tariffs, quantitative restrictions, investment controls, refund schemes, etc.) by national governments to protect local industry. External pressures (Rasiah, 1999) due to the World Trade Organization (WTO), Association of South East Asian Nation (ASEAN) Free Trade Area (AFTA) and Asia-Pacific Economic Cooperation (APEC)–to reduce tariff and other protection have had direct implications for automakers and national governments. With these commitments, the push towards freer markets is putting tremendous pressure on governments and industry players alike to re-position and re-engineer them in the light of a liberal regime.

AFTA was established in fourth ASEAN summit in January 1992 in Singapore. Its objective is to create an integrated domestic market within ASEAN and increase the region’s competitive edge as a production base in the world market. A crucial in this direction is the liberalization of trade through the elimination of tariffs and non-tariffs

1 Malaysia, for example, ‘initiated’ a national car project in the early 1980s.

1

barriers (NTBs)2 among ASEAN members. This activity has provided the push for

greater efficiency in production and long-term competitiveness in the automobile industry. Moreover, the expansion of intra-regional trade will give ASEAN consumer wider choice and better quality products. In principal, AFTA covers all manufactured and agricultural products, although the time table for reducing tariffs and removing qualitative restrictions and other NTBs differ for the two groups of members – the original six (Thailand, Malaysia, Singapore, Indonesia, Philippines) and the newer four countries (Cambodia, Laos, Myanmar and Vietnam). The CEPT3 scheme, which is instrument to achieve AFTA, requires tariff notes levied on a wide range of products traded within the region to be reduced to 0-5% by 20024. Quantitative restrictions and other NTBs are also to be eliminated accordingly. With AFTA, the national automotive markets in ASEAN – which have been protected by high tariffs – will eventually be opened to foreign competition. (Table 2 Tariff Rates in Malaysia). Although the automotive sector of member countries was until recently in the Temporary Exclusion List (TEL)5

of the CEPT, it should have been phased into the Inclusion List (IL)6 by the year 2000. Tariff reductions on items in the IL are targeted at stimulating economic growth and enhancing trade in the region.

Theoretically, the transition to a free trade will allow economies of scale in the production of vehicles and auto component parts in the ASEAN region. It will also enable firms to undertake greater specialized production runs and reduce the unit cost of production, thereby making suppliers more efficient in pricing and quality. Competitive producers can in turn export their productions throughout the region at almost duty-free prices. For the automotive industry, the bottom line attraction is lower production costs, lower prices and a bigger market. AFTA could well translate into price cuts of about 20-50% on vehicles in several ASEAN countries, where high tariffs and inefficient domestic industries been resulted in consumer welfare losses. However, in practice, differing objectives and political considerations of member countries suggest that a consensus may be difficult, though not impossible to achieve.

Getting automotive industries off the ground was no easy task for countries in

2 Article 5 of the CEPT agreement makes it mandatory for countries to remove any qualitative restrictions and other NTBs for products already included in the CEPT scheme for AFTA. Among the NTBs faced by the private sectors are: discretionary import licenses; custom uplifts; delay in clearance of goods at custom check points; the need to comply with differing national products standards and rules and regulations. All Quantitative Restrictions (QRs) such as quotas, licenses also will be eliminated. 3 CEPT (http://www.asean.or.id/economic/afta/afta_ag2.html) scheme for AFTA list. Retrieved on 1

stAugust, 2002.

4 As per status of the tariff reduction as of January 1, 2002, 98.4 per cent of the total tariff lines (products) for the original six member countries are already in the Inclusion List of the CEPT Scheme for tariff concessions. Of this 96.2 per cent have duties between 0-5 percent. Individually, the percentage of products at 0-5 per cent is as follows: Brunei-99.8 per cent, indonesia-99.1 per cent, Malaysia- 90.8 per cent, Philippines- 96.3 per cent, Singapore- 100 per cent, and Thailand- 94.8 per cent. 5

Products in the TEL can be shielded from trade liberalization for a temporary period only. These

products will have to be transferred into the IL and be subjected to tariff reductions until tariff reach 0.5%. 6 Products in the IL are those that have to undergo immediate liberalization through reduction in CEPT tariff rates, removal of quantitative restrictions and other NTBs. Tariffs on these products should have been down to a maximum of 20% by 1998 and to 0-5% by 2000.

2

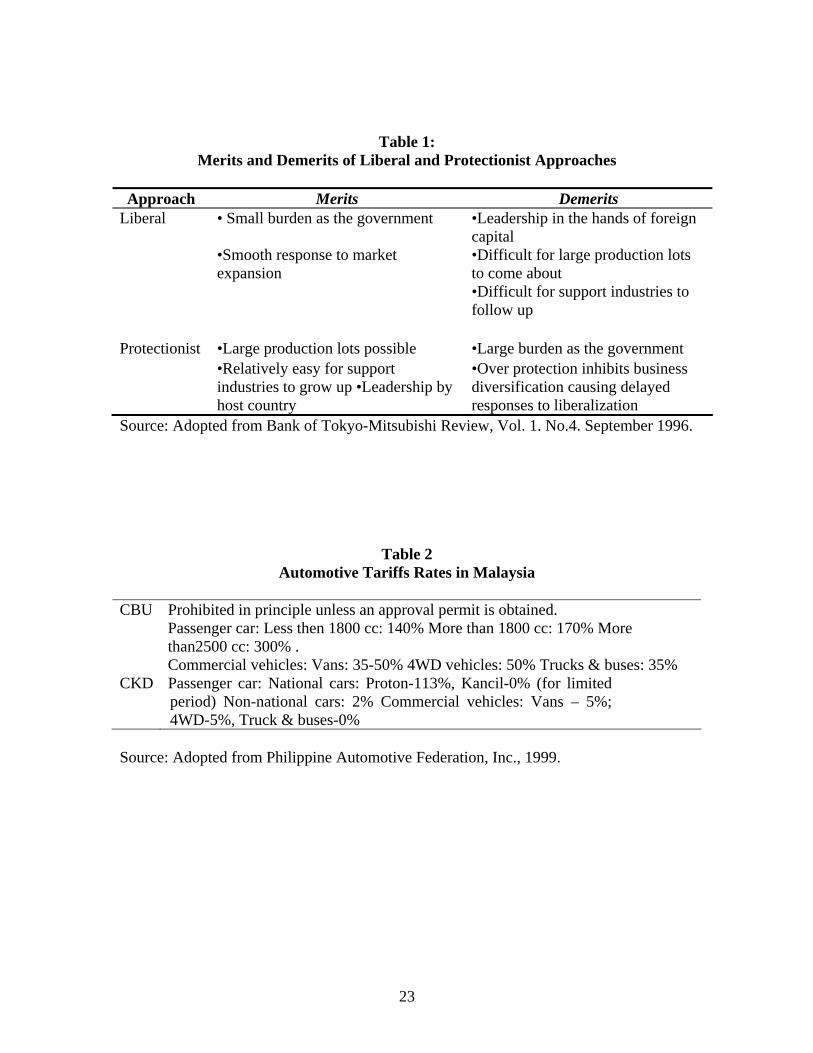

ASEAN region because at the time they had weak, primary-industries-led economic bases. But for all that they had in common, each ASEAN country had its own approach to the automotive industry depending on how it viewed the effects of competition and how nationalistic it felt-whether it thought “we can increase our competitiveness as a country by letting the foreign manufacturers we have attracted compete freely in our markets” (liberals), or “we will become more competitive by giving monopolistic protection to specific automakers, preferably our own” (protectionists). Malaysia was originally the only protectionist; the other three adapted liberal policies (Thailand, Philippines and Indonesia. Still both approaches have their strengths and weaknesses (Table 1), though the weaknesses tended to be more visible, first because demand, while growing, was still small in absolute terms and second because industrial base in the region were rather too frail to push ahead with domestic production. “National car” program resulted so far indicate that by doing so will enable the country to (1) have more control in what happens, and (2) enable support industries to grow (to achieve higher local content). Some of the merits and demerits of liberal and protectionist approaches adopted by the ASEAN-4 are highlighted in Table 1.

Automotive development and the local content policy became prominent following the launch of Proton, Malaysia’s first national car project (NCP) in 1983. There were several reasons for the government’s shift in policy in the automotive industry. Among them were the limited success of the initiatives in the 1960s and 1970s, and the desire to promote local Bumiputera participation in the industry (Abdulsomad, 1998). A joint venture between Mitsubishi Motor Corporation (MMC), Mitsubishi Corporation (MC)7, and the Heavy Industries Corporation of Malaysia (HICOM), Proton rolled out its first cars in 1985. The national car project was aimed at rationalizing the automotive industry, promoting related industries (parts, components and supporting industries), enhancing greater utilization of locally made components, encouraging the upgrading of technology, engineering and technical skills, and increasing the participation of local suppliers in the industry which was then dominated by foreign and local-Chinese capitalists. The rapid growth of Proton can be attributed to the strong government support, protection and preferential treatment measures (Table 2).

Apart from the preferential import duties and sales taxes accorded to Proton, the government provided technical, financial and other assistance through a special vendor development program to develop the entrepreneurship of the local suppliers. Local sales were also boosted by government procurement orders for the national car. In addition, civil servants were given low interest rate loans to purchase Proton cars.

This study focuses on the Malaysian automobile industry and the possible

disadvantages and advantages that may be caused by the introduction of the AFTA. The disadvantages can include loses incurred by the alleviation of protectionist measures, reduction in the overall import, and can have a negative affect on marketing position. On the other hand, it may open greater opportunities for the automotive industry through the regional cooperation and allow the industry to penetrate both regional and global markets. In order to do this, the goals of automobile industry are as how to become cost 7 Mitsubishi Motor Corporation (MMC) 15%, Mitsubishi Corporation 15%, HICOM 70%.

3

competitive, improve quality, maintain dominance on the domestic market and became competitive in the international market.

The purpose of this paper is to examine business strategies taken by both

automaker and supplier in Malaysia facing the implementation of AFTA after 2005. It argues that regional market liberalization, in the form of AFTA affected their strategies shaped towards preparing themselves to be more competitive. This paper is divided into three parts. The first part gives background overview of the automobile industry in ASEAN and Malaysia’s current position. Part two examines the strategies implemented by both automaker-Proton and a supplier (Ingress) company in facing the AFTA challenges and finally, a conclusion is offered in the final part.

Literature Review

One of the classical strategy recommend for industries is the Porter’s (1980) generic business strategy. According to him, these are three generic strategies that can be adopted by firms in an industry: cost leadership, differentiation, and focus. The cost leadership strategy can be obtained by having access to cheaper inputs or by being more efficient. This strategy emphasizes on lowering costs as opposed to lowest price as to obtain the greatest profit. The cost strategy includes control of the operating costs, lowest cost of sources of supply, keeps costs under control, and maximizes utilization of resources or capacity. On the other hand, differentiation can be achieved through better quality, unique products or services, product image, lower price, customer sensitive, customer service and reputation. Focus strategy is a “niche” marketing strategy that can be obtained through lower costs or differentiation, addressing at specific target markets.

Dess and Davis (1982) examined the generic strategies of Porter, and found that

the lowest cost and differentiation strategy were supported in their findings. The third strategy, focus, was found to be less conclusive; this was due to the differences in opinion of the panel of experts on the interpretation of the “focus” strategy. Bowman (1992) explored the manager’s perceptions of the generic business strategies in the United Kingdom. By using factor analysis, he found that the generic strategies were grouped into four factors: competing on price, offering unique products/services, cost control, and product/service development. The result implies that the two factors were associated with competitive behavior; while the second two factors were associated with internal competencies which may or may not lead through to changes in the offerings of the firm (Bowman, 1992). As such Bowman believed that the results shared that the business strategies were related to the internal activities and the external competitive market positioning.

Md. Zabid (2000) found that the competitive strategies pursued in the electronics

industry were cost, differentiation, cost price, and marketing niche strategies. There also a positive relationship between the competitive advantage positions and the generic strategies pursued. Competitive advantage can be defined as a unique position a firm develops vis-à-vis its competitors (Bamberger, 1989). A firm can create and sustain its

4

competitive positions by developing distinctive competencies with its available skills and resources. Bamberger also identified general factors contributing to competitive advantage positions like product quality, quality of management, good image and personal contact, reliability of delivery, reputation, low costs positions, market share, financial capability, pricing policy and modern production techniques. Bamberger also found that the critical factors important for competitive advantage might not be similar in different industrial situations like the electronics, clothes and food. In the electronics industry Md. Zabid (2000) found that the seven competitive advantage factors were marketing capabilities, organizational capabilities, product/service quality, image and financial integrity, technological competence, sales management and network, and socio-financial capabilities.

Methodology

This study relies mainly on primary information. The author conducted two field surveys, from April to May 2001 and from March to April 2002. After objectives were set to tracing the trends of automaker and suppliers’ relationship particularly between Proton and its vendors8, the first step of this research entailed visiting Proton and selected 12 vendors and interviews have been conducted with their staffs. The author was able to interview Proton’s manager of Supplier Sourcing and Technology (SST) department and its executives and selected 12 suppliers. Additional to this, structured questionnaires were sent through mail to 78 Proton’s suppliers categorized under Small and Medium Industries (SMIs)9

with 30 or 40.5 per cent response rate. This study also applies case study approach particularly on Proton (only one automaker is selected. Malaysia has two automakers namely Proton and Perodua) and Ingress represented the suppliers. The case study is the preferred strategy for this study for two main reasons. The first is closely related to the objective of the study, that is, to discover to what extent both automaker and suppliers have arranged their response to the current challenge of regional changes particularly AFTA. Secondly, it involves the question of what type of business response that has been arranged, and how far the responses have been taken place. Ingress is being selected because it involved in strategic alliance to acquire technologies from foreign Multi-National Corporations (MNCs)-Katayama through a "hands-on” learning process (Ali, 1992; Hensley and White, 1993). The same also applied for Proton as it acquires technology learning from MMC.

Result and Discussion

8 Vendor is Malaysian term of supplier. 9 The new definition for the small companies are companies who have 50 workers and less; and annual sales of not more than 10 million. While the medium companies are companies that have less than 150 workers and annual sales of not more than RM25 million (Berita Harian, 1998).

5

AFTA and Its Implications for Malaysian Automobile Industry For automobile industry, all the components and parts that are needed to the car industry will be affected. From tires till the engines are included in the CEPT. Malaysia has used high import duty and local content policies to protect national cars, domestic assemblers and component part makers. (Refer to Table 2). With the introduction of AFTA, all trade barriers will be removed and this is turn can have the negative implications for Malaysian automobile industry. Domestically, Proton has the advantage in terms of dominant market share and a well-established distribution and service network. Mentioned situation will remain for the next three years at least, following Malaysia’s deferment to 2005 of market opening measures for the auto sector under the AFTA agreement and Malaysia’s commitment to WTO. But the situation concerning the Proton’s dominance in the local market after the 2005 can be threatened. Removal of all the trade barriers can result the following: (1) Foreign competition, which can pose serious threat to the future development of the local automobile industry, (2) Outside pressure on the local market from other manufacturers in both component and finished products, and (3) Collapse of the inefficient and weak firms at the expense of stronger ones. The issue is what can be the way? Do Proton and its suppliers ready for this? This paper attempts to discuss alternative measures taken by them to face the challenges.

However, AFTA, for auto, in a positive perspective would drive the regional

manufacturing integration and cost competitiveness among ASEAN countries rather being a threat to them. It is expected will be more technology transfer to this region and more opportunity to the labor. ASEAN is a key strategic automotive market for many reasons: ASEAN population is 510 million. Currently the car sales have been increasing. In 1998, it was 500,000, in 2000, 1 million and projected to be 1.5 million in the year 2003. The leading supplier for the whole ASEAN region is Proton with 22 per cent of the market due to its monopoly in the Malaysia market. Toyota is the second in the list with 20 per cent share10.

Another reason is the growing economic growth of the ASEAN countries. Despite

of the effected GDP in 1998 due to economic turmoil, its growth average in selected ASEAN countries (Indonesia, Malaysia, Philippines, Thailand, and Vietnam) is averaged at 8 percent and projected growth rate for the year 2000-2004 will be the same average at 8-10 per cent. Since the market is very attractive, many foreign giants from Japan and the US have already invested in this region. From 1995-1999, US giants like Ford, General Motors (GM)11, Daimler, Chrysler, have invested in Thailand.

Malaysia has delayed the inclusion of 218 tariff lines (products) on Completely

Built-in (CBU) and Completely Knocked-down (CKD) automotive products until 2005. The delay was due to providing domestic automotive industry more times to recover from

10 The integrated sales of this region would be the fifth in the world by the year 2005-ARA. 11 GM has invested 750 million in Thailand to open up a base. Volvo has already negotiating with local Thailand companies to open a base. Comparatively, their investment in other ASEAN countries rather low due to the flexibility and trade regulation that is not so tight in Thailand compared to others in ASEAN.

6

the impact of the regional financial crisis of 1997. The delay also to allow domestic industry to undertake necessary restructuring exercise and prepare for market opening under AFTA, without disrupting long-term development of the industry. Proton business response to AFTA

Proton has to response accordingly and has to take into account its vision, position, challenges ahead and to prepare the strategy12. Currently, Proton cars13 are conquered 64 per cent of domestic sales since 1987. From that year their market share was always above 60 per cent and has been improving the sales every year until 1997 before dropping because of the economic downturn. Proton also gains its mileage as one of the top three players in the domestic market share: (1988-73%; 1991-64 %; 1994-71 %; 1997-64%; and 1998-63%) (Proton, 2000).

The challenges for Proton facing AFTA including (1) Low exports volumes14, (2)

Proton doesn’t own its products. Proton models line up includes Saga, Iswara, Wira, and Satria (including Satria Gti). Tiara, Putra and Waja, which comes on various body sizes, were ranging from 1.1, 1.3, 1.5, 1.6, 1.8 and the 2.0 litter engines. Models Wira and Perdana, which are largely Mitsubishi designs15, while Tiara, which is Citroen design, and for Satria and Putra which are Malaysian redesigned variants of Wira. Except for Waja, other products are not owned by Proton per se including engine. In addition to that, all those key models (except Waja) are aging. (3) Although Proton already penetrated the export market since 1986 but it’s seemed that Proton acquired low brand power outside Malaysia16. As a result, Proton received weak customer loyalty and retention rate besides perceived quality of Proton is not encouraging. (4) Competition from MNCs in ASEAN. US giants like Ford, General Motors (GM), Daimler, Chrysler, already has invested in Thailand. Proton should successfully place itself to be domestic or regional player or prepare it response to these challenges. In order to achieve this, a

12 Proton’s vision is to become a successful Malaysian automotive engineering and manufacturing company globally by being customer oriented and producing competitively priced and innovative products. 13 Proton models line up includes Saga, Iswara, Wira, Satria (including Satria Gti), Perdana V6, Tiara, Putra, and Waja, which comes on various body sizes ranging from 1.1, 1.3, 1.5, 1.6, 1.8 and the 2.0 liter engines. Models Wira and Perdana which are largely Mitsubishi designs, Tiara which is Citroen design, and Satria and Putra which are Malaysian redesign variants of Wira, and the latest Waja is purely Malaysian engineering and design. Proton has also acquired Lotus Engineering of Britain, and has since manufactured the Elise model (sport classic model) in its Shah Alam plant). 14 Less than 10 per cent of its total sales: Proton Corporate Information, 2000. 15 As far as product development is concerned, Mitsubishi plays a very important role in engines and transmissions as well as body structure design. Meanwhile, Lotus, a subsidiary of Proton, is contributing its expertise to Proton’s existing model line, especially in area of ride, handling and noise vibration. 16 According to a survey conducted by JD Power and Associates of United Kingdom on Cars Customer Satisfaction Index Study in 2000, in term of vehicle quality and reliability, Proton should give priority to these items accordingly: power window and locking system; no.2. Seats; no.3. Rear parcel shelf; no.4. Rust/corrosion; no.5. Heater, air con. & Ventilation; no.6. Sunroof; no.7. Mirrors; no.8. Water leak; no.9. Carpet; no.10. Fuel gauge; and no. 11. Wipers for almost all of its models sold in the UK.

7

few strategies should be carefully selected and implemented accordingly. Given promising position in the auto market of ASEAN, Proton has potential to gain success.

Proton’s strategies lie on focusing on these few viable measures that it has

capability to do it: (1) Proton has to look on new product development to improve the capability of the existing models; (2) Venture to new market, (3) Flexibility in manufacturing; and (4) Building network of alliance. (5) Improve customer care and brand image, and (6) Building world-class vendor.

Attaining Cost Leadership and differentiation: Product development investment and product image Proton needs to take measures like developing domestic technology, and rapidly launch new product and attaining cost leadership. In order to come up with new products, that achieve the target of development in speed, cost effective, product appeal, and better ride and handling, Proton moves to produce its own-design car and has invested a lot in R&D capabilities to create its own product brand- the Waja (GX) model. This strategy is to produce models that will compete in the same space as imports that qualify for tariff reduction under AFTA. As a result, Proton eschewed the use of existing Mitsubishi or Citroen chassis to design its own platform. With the exception of engines and transmissions, it is local in term of design engineering, and manufacturing. Waja makes its debut in September 2000 after 1.7 million man-hours of R&D effort over three years and investment of close to RM1 billion. A hefty RM600 million alone was spent to develop the platform for the Waja. It was the First Proton Model to be largely designed and engineered in-house. The Waja’s high local content is perceived able to greatly reduce the company’s foreign exchange outflows and royalty payments. Approximately RM400 million (US$105 million) would be saved on foreign exchange outflows by minimizing the import content for the car and a further RM500 million on royalty payments over the lifespan of the product. In addition, Proton could earn as much as RM450 million in foreign exchange inflows through exports. The car meets Euro III emission levels and new EU impact regulations (40% offset deformable barrier crash and 50km/h-side impact). Consistent with the introduction of Waja version 1.6, Proton is planning the production of the next models begin with extended version of Waja, GXM scheduled to be produced in the mid 2003, the next models line up including SCM24 in the third quarter of 2003 and SCM 44 in the first quarter of 2004.

Although, it is not yet clearly decided, Proton should think to replace its Wira

range of passenger cars. Proton still may retaining the Wira brand name but only following a substantial increase in import of Malaysia engineering expertise involving the use of Proton’s own camshaft profile (campro engines). The move will be a departure from Proton’s practice of producing and branding variants of the Mitsubishi Lancer for Malaysian market. By using the Malaysian engine (Campro) can help bring down the costs by between 20 percent and 30 percent. The current Wira models consist of about 60 percent imported components, including gear and engine parts.

8

In order to enhance its brand image, coincides with the Waja’s arrival, Proton introduces new marquee identity of gold tiger stripes17 instead of crescent logo placed in the previous models. This is a part of a broader effort to strengthen the brand locally and abroad.

Complementary to this, Proton also moves a step further to produce its own new

engine and EMS18. The EMS 40019 has been produced in mid 2001, while both EMS70020 and CAMPRO21 scheduled to be produced on first quarter 2003. CAMPRO engines took just nine months from the drawing board to the first working prototype, against a typical industry period of 12 months, with collaboration between Proton and Lotus engineers. Proton also doing R&D collaborating22

with Petronas Sauber Formula1 teams to come up with its own engines and car. Proton also has a network of alliance with Renault to produce GX 1.8 model engine and transmission. Network strategies alliance is very important to acquire new technology, marketing and resources acquirement and improvement. Proton made a major step in upgrading its engineering capabilities with the acquisition of Lotus Group International Limited23, a British automotive engineering company and manufacture of luxury sports car in October 1996. With this acquisition, Proton gains a great engineering expertise, which will enhance them to improvise and come up with new models that are globally competitive and innovative. Improving Research and Development (R&D) Some US$23 million was invested in Computer Aided Design (CAD) and Computer Aided Engineering /Manufacturing (CAE/M) software before the US$255 million development program got underway for the company’s fifth major model line after the Saga, Wira, Tiara and Perdana. The GX (Waja) platform enables can house various power trains and will spawn several models. It was developed on a modular blueprint (the finished car has more than a dozen modules including fuel tank, suspension, steering and 17 Previously three different logos were used in the domestic, European and general exports markets. The new logo- the “Proton’s Mark of Pride” will singularly represent the Proton brand in all domestic and international markets. A shield shaped badge featuring the Proton brand name and a tiger head, to portray the power of a single idea: “The Spirit of Achievement.” The symbol can be interpreted through a number of levels, all pointing to the ideas of pride, leadership and performance. The diamond shape, derived from Proton’s very first top mark and the color scheme maintain a sense of continuity with the past and are symbolic of the Proton’s pride in its achievements. The tiger head is a reference to the two tigers displayed on Malaysia’s coat of arms and conveys national heritage. It is a reference to Malaysia’s origins and clearly communicates Proton as a national project. 18 EMS stands for Engine Management System i.e. the electronic control unit of the engine to determine engine tuning for fuel, air mixture, etc. 19 EMS 400- electronic control unit for current Wira engine coded as 4G1 developed with Siemen VDO. 20 EMS 700- electronic control unit for CAMPRO engine developed with Siemen VDO. 21 CAMPRO is Proton’s newly developed engine with LOTUS, ranging from 900cc to 2.2 liters V6. 22 Proton also working with SIRIM to develop high-tech, low-cost engine components, as well as with PORIM to developing alternative fuel using palm oil. The agreement for this has been signed on 24 August 1999. In addition, Proton also works for hybrid technology to effectively reduce engine emissions. 23 Proton purchased 80 per cent of lotus from URL http://www.britain.org.my/trade/sector-summary/automotive.htm

9

doors) in 30 months with design-in help from 20 First Tier local suppliers. This current Waja model contains a local content ratio of about 80-90% in the first cars to roll off the assembly line with 1.6-liter Mitsubishi mated to either an automatic or manual transmission powers the launch model. The next version of 1.8 liter powered by a Renault engine, will be available both for domestic and export markets, in mid 200324. In the second phase Proton will install its own engine into the car, making good on the Waja’s description as the first true Malaysian car. Handling and suspension was engineered by Lotus, Proton’s British subsidiary. Although facing the aging of the existing key products (LM, M-Car, and PF 41 models), the Wira model at present is seemed will be continued.

To enhance their design capability, Proton now have invested in a much faster

and cost-effective alternative with the advent of Rapid Prototyping (RP), a relatively new class of computerized technology used for building physical prototype parts and tools. RP enables Proton to build prototype parts and tools directly from 3D CAD25 data utilizing state-of-the-art Stereo lithography and Laminated Object Manufacturing machines. This is an important step in the process, simply because a rendering of a solid model communicates information 10 times more easily than engineering drawings. In a short period of time and with excellent detail, finish and accuracy, RP prototype is able to provide solution for new design concept. Proton invested more than US$100 million in a modern R&D facility, featuring the most advanced rapid prototype center in South East Asia, the only climatic chamber test lab in ASEAN and the only passenger safety sled in Asia outside Japan and Korea. Proton can also handle short-run productions of plastic and metal prototype parts with the modern technology such as the Homologation and Testing Department ensures domestically manufactured cars meet international standards before they are exported and sold26.

RP sees to it that the product that gets manufactured eventually fits all

engineering requirements. Here, the engineers will be able to measure cost savings and quality, and consequently make improvements to a product before it goes into mass production. This is obviously a highly specialized facility. In Proton, RP serves both internal and external customers. RP is also able to produce a prototype within an hour to two days, depending on the parts involved when it would take a traditional machinist or craftsman at least two weeks. Due to its ability to build prototypes in a very short timeframe, RP actually empowers the R&D Division to be more creative and be able to embark on varying degrees of experimentation in terms of product design and engineering. To improve its production capacity, Proton is planning to build its second

24 GXM model –an extended model of the currant GX. 25 CAD (IBM’s CATIA) and computer system also ensures effective data transfer and communication between Proton and its vendors and other related companies. 26 For instance, if a Proton car were to be sold in Europe, the model would have to be homologated to comply with European design and engineering specifications, as well as legislative requirements, before the car was allowed to go on the road. Development testing spans the full spectrum – static, running, turning, braking and all other aspects of drive ability – to ensure that in-house requirements are met. Other tests include emissions, noise, engine power, safety and strength, which forms part of the more comprehensive crash test. All aspects of testing are simultaneously taken into account during product development. In most cases, development testing is more stringent and severe than homologation testing.

10

plant in Tanjong Malim in the state of Perak and expected to be established in the first quarter of 2003. Focus: Markets and distribution Domestically, Proton already acquired about 65 per cent of the market share with the acquisition of USPD27 and transformed it into Proton Edar in order to position itself closer to customers as its marketing strategy. Thus, domestic distribution and sales is being channeled through both Edaran Otomobil National (EON) and USPD, effectively turning them into competitors. Previously, these two sales operations sold different models. Through this new acquisition of sales and distributor company, Proton is directly accessible to enhance customer care. As for export markets, UK and Australia remains major export market28. Consistent to the existing exports market, Proton is developing the markets in the Middle East and other Muslim countries as well as in the ASEAN countries. Currently, Proton has CKD assembly plants in Iran (from August 2002) and China, India (with Hindustan Motors), and a joint venture set up between Proton Edar and PT Ningz Multiusaha in to assemble and distribute Proton vehicle in Indonesia is the first effort to penetrate the regional market. Building World-Class Vendor-Procurement practices of Proton Local component parts vendors also have important role to play. If Proton were to graduate into a global player, so too must its vendors. The tiering of vendors under modular approach adopted for the Waja is a step in the right direction. For the first time, 20 tier-one vendors designed and made components in collaboration with Proton engineers. By working closely with Proton and taking on more R&D, design and engineering responsibility themselves, these vendors can hasten the manufacturing process and improve on product quality whilst allowing the national car to better utilize its resources. In order to be competitive particularly consistent to AFTA challenges, vendors have to ensure every part or component supplied to Proton is consistently good29 and reliable in use. Two main challenges to vendors are cost reduction and continuous improvement. Proton encourages and liaises with third party vendors, and in doing so, achieves two objectives. Firstly, encourages vendors to be more involved in the development stage of the process. Vendors are invited to work together with engineers on the design of new models. This saves time and ensures that market feedback is taken into account when new models are introduced. Secondly, this is a good opportunity for Proton to educate vendors. In this instance, design intricacies and development processes are explained, so vendors appreciation and learn about them. This leads to better cooperation among all parties concerned, and at the end of the day; engineering design objectives are

27 Proton owned 100 per cent equity; business activity is sales of motor vehicles and related spare parts and accessories. 28 As at September 2000, total export to UK was 124,380 cars and Australia are 14,814 cars. International Business Division, Proton Corporate Information, 2000. 29 “Good” according to Proton’s standard means not only meeting the specifications, but surpass them.

11

achieved in a shorter timeframe. However, in order for vendors to be a partner in product development (design-in), vendors should achieve a certain level of capability.

Generally Proton could acquire the necessary inputs through three different activities, which are import, to manufacture in-house, and outsourcing from local suppliers. However, there are two major choices of procurement activities in which Proton could select either to import or to procure domestically. The decision is not only based on commercial considerations but technically competence to be sufficiently competitive. The further discussion only will examine the practices of procurement activities through local channels. Commercially, Proton would procure inputs from the cheapest and most reliable source. In other words, the alternative that provides the lowest price plus transaction costs to Proton will be selected. In regards to procuring parts domestically, Proton also find itself faced with the decision of whether to undertake a particular activity in-house or to outsource from its local vendors. Procurement activity also could affect the benefits on local vendors. The decision to produce in-house or outsource will depend on comparative costs and benefits of the alternatives. Proton outsourced most of non-body and engine and transmission parts domestically from its vendors. Table 3, shows the 3 major items from each group outsourced by Proton domestically.

In order to be sufficiently competitive, Proton is very careful in its procurement practices. From the interview conducted with the Suppliers Sourcing and Technology (SST) department of Proton, this paper could concludes that Proton is very careful to place its investment if the local suppliers could supply the required quality and price accordingly.

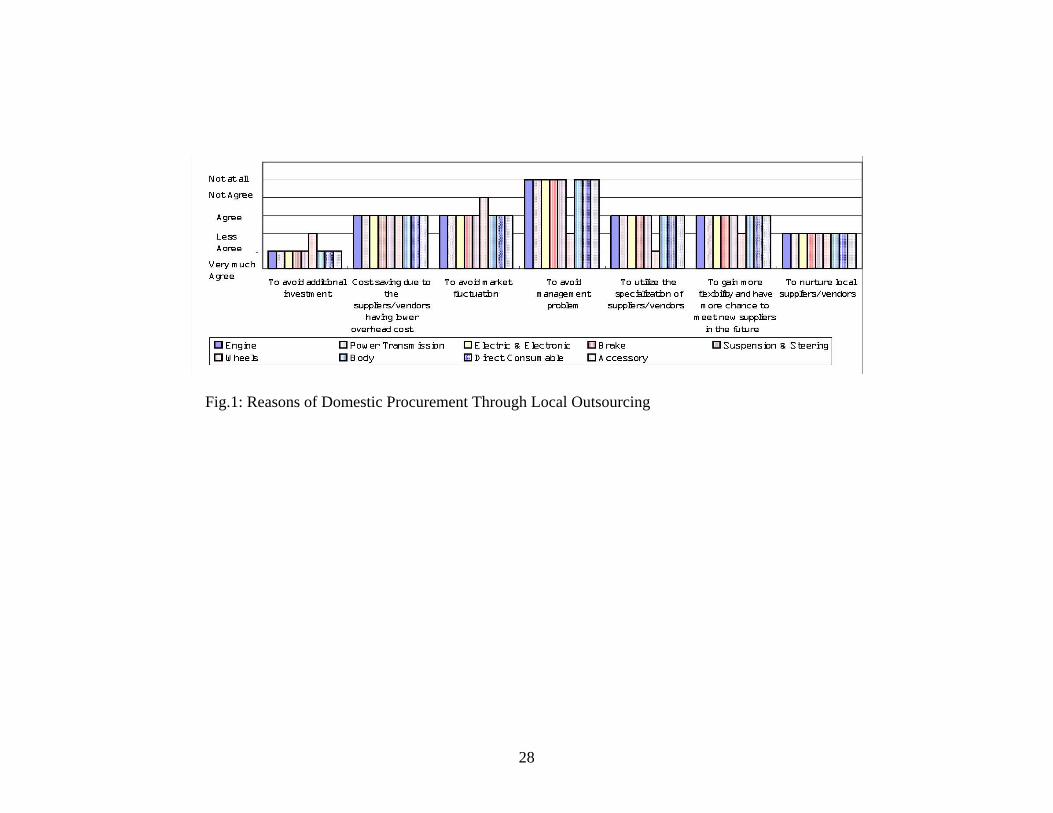

Fig. 1 provides the reasons of domestic procurement of Proton that gives very high ranking of additional investment in almost all categories of parts it outsourced except for wheels. This is very important as additional investment could lead to the increment of its parts and components overhead costs. Most of the automobile parts and components are very customizes items in its nature according to the models. Proton car’s production also very limited about 25,000 cars for all models (Proton’s Vendors Briefing, April 2002). Thus, this additional investment cost will bear by vendors, as they already possessed lower overhead costs and their own expertise. In other words Proton could help in nurturing the local vendors and helps them to increase their organization learning.

In case of domestic procurement, Proton is also very careful in vendor’s selection.

Generally, Proton must control the quality of their products in order to maintain high quality parts and components. This study uses an open-ended questionnaire to proton to enable it identify how they screen and select the vendors. Vendors undergo a very high-scrutinized process before them being appointed as suppliers. The result shows two of the major channels preferred and practiced by Proton in vendor’s selections: (1) Searching through its own procedure and (2) vendors approached Proton directly. Although the role of the Vendors Development department of the Ministry of Entrepreneurs Development and introduced by Proton Vendors Association (PVA), but it were less preferable. Thus, vendors have to aware and familiar with all the requirements

12

needed by Proton before they are appointed. Vendor’s selection and developments taking time are almost thirteen months before they could start the first trial production and followed by mass production. Typical lead-time for pre-selection of vendor to mass production stage is between 15 to 27 months.

Proton gets to know the suppliers by searching itself and from the introduction of

suppliers themselves. Therefore suppliers have to present themselves and their products, which might not necessarily match the parts, required by Proton. The suppliers usually have good performance records, sufficient machinery, and experience in that particular production, good financial status and technologically competence. In order to examine how Proton scrutinizes its potential suppliers and also its existing suppliers, this research find that Proton prefers to use standard criteria commonly used as devices in the selection of vendors. Proton listed the criteria according to degree of preference as below:

Criteria number 1, 2 and 3 were given top priority as usually practiced meant that

51-90 per cent of the time. While factors number 4 and 5 were occasionally practiced this meant that 21-50 percent of the time. Proton from the beginning gives much attention on QCD matters. The author asked Proton on what factor ii gives most attention among QCD, trust and technology, QCD has been opted as the most priority taken when it makes deal with suppliers. This priority was interpreted in its Supplier Chain Strategy Policy of Proton as: 1) Intense Competition – 4 Suppliers per Part Group; 2) Encourage New Capable Players; 3) Export 20-30% of Production; 4) 3 Years Contract with Minimum 3% per annum Cost Down (currently practiced by Proton) year on year; 5) R&D Center; 6) Innovation that gives Competitive Edge-Rewarded.

The result of the field survey also attest on the practice of long-term relationship

between Proton and its suppliers to the fact that on-going or long-term relationships could reduce transaction costs, which are the cost of registration about the price and the cost of controlling the suppliers’ quality and delivery. Moreover Proton still states that long-term relationships and regular orders make them more flexible than trying to specify a complicated contract. Proton is very sure that through this kind of relationship it could save cost and time to investigate and screen the new supplier candidate. It also could reduce the costs in controlling the suppliers in term of QCD. Through these relationships Proton is familiar with the supplier and dare to provide assistance in order to improve quality, reducing cost, efficient in delivery and assisting their development technically.

The interesting point is that the long-term relationship makes Proton more willing

to provide some assistance to its suppliers in order to improve quality of parts and to reduce the costs of production. Due to the harsh competition in the final market particularly facing the market liberalization and tax deduction of AFTA, Proton has to reduce cost of production by improving their productivity as well as requesting their suppliers to reduce price in order to increase, or at least maintain their competitiveness. This research finds that Proton requested cost reduction, usually about 3 to 5 per cent, annually and the present practices recorded that Proton is cut the price 3 to 5 per cent per year automatically. Table 5 shows the request about Proton agreement in each aspect derived from long-term relationship.

13

Ingress30 Business Response to AFTA

With the liberalization of domestic markets arising from Malaysia’s commitments to AFTA and WTO, the local vendors too will face increased competition and hence will have to turn to foreign markets for their long-term survival. Liberalization of automotive trade may see Ingress’s orders from its Malaysia buyer’s decline slightly, but its orders from buyers in Thailand would increase their production. The region vehicle production would be consolidated, boosting production volumes and making more projects economically viable for Ingress.

Ingress is principally an investment holding company whilst its subsidiary and

associated companies are principally involved in automotive component manufacturing, engineering services, power and electrical services and railway electrification. The range of automotive manufacturing and services offered are as follows: (1) Co-extruded Moldings31

(Belt-line Molding, Quarter Moldings, Door Sash and Related Components, Rain Rails, Glass Guides, Bellows32, EGR Pipe33

) Weather-strips, Roof Drip Moldings, Windshield Moldings; and (2) Complete Door-in-White34, and Apron. As at 15 January 2001, the Ingress Group has a total of 827 employees35. To date Ingress has 5 associate companies namely IESB, IPSB, IRSB, IAV, ITSB36.

If ASEAN automobile trade is

liberalized, how will Ingress be affected? The answer is complex, as it will

30 Business vision of Ingress is “To be a leading ASEAN-based automotive components manufacturer by winning more customers with global reach utilizing and optimizing state-of-the-art technology. It was founded in May 1991 and incorporated in Malaysia under the Companies Act, 1965, on 9 August 1999 as Ingress Corporation Sdn. Bhd. 31 IESB-Co-extruded moldings are parts made from extruded polyvinyl chloride (“PVC”) over a roll-formed steel core. The moldings are generally used to seal around windows, doors and other gaps or joints in the vehicle’s exterior 32 IAV-Bellows-(also known as flex joint) is a component of the vehicle exhaust system which, being flexible, absorbs engine vibration. The bellows comprise a roll-formed steel tube surrounded by braided steel. Production of bellows shall commence in 2001 for supplying MSC pick-up trucks and GM/Isuzu models in the following year. Its technology source and partner, Katayama, presently manufactures bellows in Japan. Bellows are supplied either directly to the automaker or to the automaker’s exhaust system supplier, depending on the automaker’s preference. Bellows tend to be employed only when vibration suppression is of great importance, such as on medium/upper-level passenger cars, and commercial vehicles (including pick-ups) with diesel engines. 33 EGR Pipe-Exhaust Gas Recirculator Valve (EGR) pipe is another new product of Ingress. It is a metal pipe with a “bellows” feature at its center used for recirculating the exhaust gas from an engine to the intake side in order to achieve a reduction in emission level of nitrous oxide (a harmful component in the engine exhaust) to the environment. 34 IRSB-Complete Door Assemblies (Door-In-White)-At present Ingress uses its press line and hemming machinery to produce the door-in-white, a complete door assembly consisting of outer and inner door panels and door sash. It has the ability to produce a variety of other large steel parts that its customers may wish to outsource in the future. These are all high-value parts, and are used on every vehicle. 35 Management 75, Executive 100, Clerical jobs 63, General workers 589. 36 IESB-Ingress Engineering, IPSB-Ingress Precision, IRSB-Ingress Research, IAV-Ingress Automotive Venture (Thailand), ITSB-Ingress Technology. (Ingress Prospectus dated 22 January 2001).

14

simultaneously assist and disadvantage the company in different ways37.. In line with these risks, Ingress has given priority to put challenges in term of QCDE I38 -(Quality, Delivery, Cost, Environment, and Innovation) by looking inward, including maintaining its competitiveness technologically, in terms of cost efficiency, products and services quality and reliability of the company by utilizing all expertise possessed by Ingress. Looking forwards, including maintaining the relationship with its customers domestically, and diversifying its customer base especially through joint venture and searching for niche market domestically and regionally. Facing the Challenges

Ingress should response carefully and appropriately particularly related to the new trends brought by new approach of what so called world car projects. As parts and components supplier, Ingress should able to read and define these challenges and transform it into strategies. World car projects are a new trend that is related to parts and procurements concepts summarized as follows: (1) Common design for all cars to be manufactured, (2) “Design-in” supplier will jointly design the parts. QCD and VAVE issue will be taken-up in the design stage, (3) Consolidate effort in the development-able to reduce the development period from 3 years to less than 1 year, (4) Nominated supplier must have affiliate companies in the production location for parts production, and (5) Utilization of local inputs: materials and tooling.

QCD matters are very important issue to look upon and highly emphasized by

Proton and other Ingress’s buyers. QCD challenges faced by Ingress could be summarized as follows:

(1) Quality: Comply to the world standard e.g. for the rejection, it is 40 PPM (Toyota target is 10 PPM);compliance to the world quality system e.g. ISO 9000, QS 900 and ISO 14000; additional compliance to specific quality standard awarded by the buyers; and continuous improvement on quality level including. Value added/value engineering (VAVE) activities.

(2) Cost: Including incorporating local value added; comply with the basic costing requirement “standard costing”; and including future cost reduction in costing proposal.

(3) Delivery: 100 percent achievement to “on-tine” delivery; availability of a comprehensive material ordering; production planning; and delivery tracking and

37 The risks include constraints in labor supply, the possible increase in the operating and capital costs due to increase in labor supply, changes in economic and business conditions, foreign exchange rate fluctuations, increase in the prices of the imported and local components, unfavorable changes in government and international policies, the introduction of new and superior technology or products and services by competitors. 38 Quality including targeted reject part e.g. PPM-parts per million, warranty and market recall, reputation, etc; Delivery means has to be near to customer, to be global suppliers and put the company’s product presence everywhere in the industry; Cost including yearly reduction, penetration pricing, cost saving program, etc.; environment- recycle ability and deletion of PVC, towards pollution free products, etc.; and for Innovation including to follow the innovative trend in the industry for example all-aluminum construction, etc.

15

stock control system; and complying ability to the electronic ordering and invoicing system e.g. EDI and able to meet the sudden increase in volume.

This is supported by the research result provided. 28 suppliers or 36% out of 78

respondents (100%) agreed that price and quality are very important and highly emphasized by Proton. 17 of them or 22% agreed that prompt delivery is the third criteria that paid high attention by Proton. On the other hand, three most important aspects considered by Proton that being the primary and major priority are QCD, Uninterrupted Supply and Technology; while Proximity is given secondary (less important but not trivial) priority. Reputation and Capability Building In order to accelerate its reputation among the customers, Ingress is working hard to achieve certain standard in its products. Some of the main achievements are tabled in Table 6.

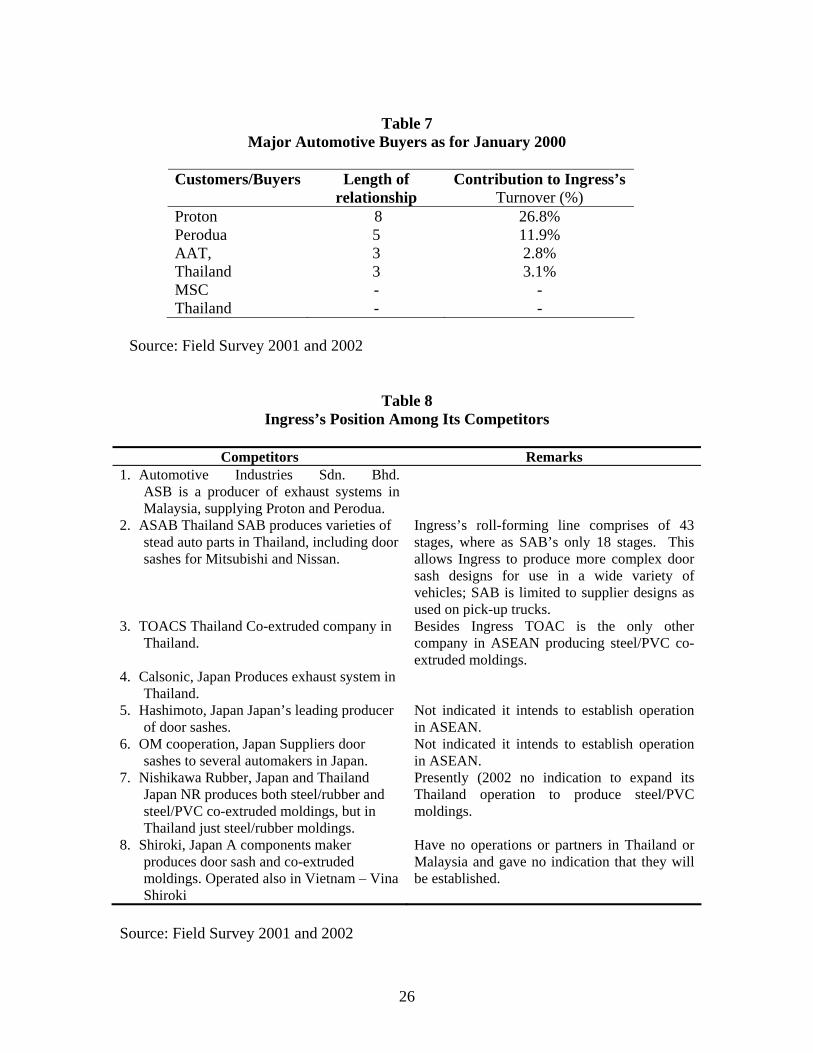

Maintaining Major Buyers/Searching Potential Future Buyers and Niche Market The major customers of Ingress together with the number of years of relationship and the contribution of each customer to the company’s turnover for the financial year ended 31 January 2000 are as shown in Table 7. Although it’s seemed that Ingress is dependent on four major buyers, Ingress has tendencies to maintain its favorable position in the domestic market, whilst diversifying its customers especially in the fast growing ASEAN market. Additionally through IRSB and TSSB two of the Ingress’s subsidiaries, Ingress are actively participated in providing engineering services to the sub-sector of industrial automation, computer aided design and manufacture (CAD/CAM) of jigs, tools and dies. Given this scenario, Ingress is successfully maintaining its favorable condition in domestic market and penetrating ASEAN markets through long-term relationship with the current customers. Maintaining Advantages vis-a-via the Competitors Ingress uses steel roll-forming and large steel pressing technologies to produce the parts: co-extruded moldings, door sash, bellows, and door-in-white assembly. At present level, Ingress is achieving some advantages particularly on market and technological levels in order to position itself as one of the regional in its product specialization (Table 8). Currently, Ingress is capable to maintain its position in its main products competitively. This position has been enhanced by a few strategies taken in the domestic and regional markets. Table 5 (p9) shows how Ingress has maintained its domestic and regional buyers through a long-term relationship. As a result of new collaboration with its technical provider cum its joint venture partner, (Katayama), Ingress has achieved some new development in penetrating the regional market. Ingress presently supplies door sash for the Ranger/Fighter pick-up truck produced by Auto Alliance Thailand (AAT) Thailand since its launch joint venture with Katayama that already a Mazda’s supplier for the parts in Japan. Regarding co-extruded moldings, Ingress is a potential supplier candidate for

16

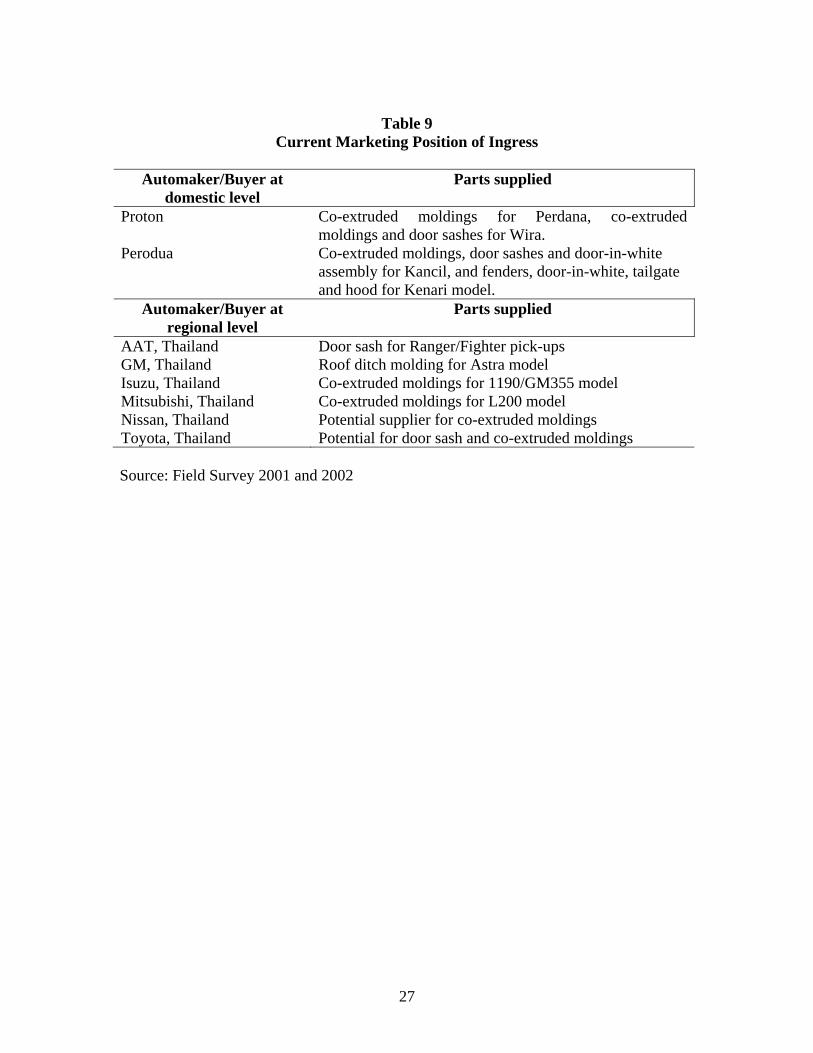

AAT in near future, as AAT currently does not apply bellows on either its petrol or diesel pick-ups. In the long term, its seem that Ingress remain a candidate to supply new programs which emerge from AAT based on the current development and good relationship with. General Motors (GM) also has awarded the roof ditch moldings contract to Ingress for the new-aborted Astra passenger car. Katayama supplies bellows to GM in the US. Isuzu currently is emerging as a key buyer for Ingress in Thailand. Ingress and Katayama have won a contract to supply co-extruded moldings for the 1190/GM355 worldwide model. Katayama is the worldwide development source for bellows for the model, and Ingress is supplying the Thailand volume. These two contracts will cause Ingress to double its investment in Thailand. Ingress also supplies co-extruded moldings for the L200 (TOACS also supplies Mitsubishi with co-extruded moldings). Mitsubishi sources the door sash for the L200 model from SAB, the two companies have also relations and SAB is likely to supply door sashes for the future models. Mitsubishi granted Ingress a mandate to supply bellows for its L200 model. Ingress from the beginning has had a relation with Nissan in Thailand. Nissan is started opening to new suppliers, including Ingress, for the future contracts for these parts. In addition to these automakers, Toyota Thailand is expected to remains its traditional suppliers in Thailand for the next few years at least, and the chance of Ingress supplying Toyota soon is small. At present Toyota Thailand sources co-extruded moldings from TOACS, door sash and bellows are imported from Japan.

Domestically, Ingress has supplied Perodua the second Malaysian automaker

since 1996. It presently supplies co-extruded moldings, door sash and door-in-white assembly for the Kancil model. The two companies have close relationship: Ingress Technologies was established for the purpose of producing door-in-white assemblies for Perodua, and it’s 30 percent owned by the automaker.

It secured contracts to supply fenders for Kancil model, and door-in-white

assembly, tailgate and hood for the second car model. As for Proton, Ingress currently supplies co-extruded moldings and door sash for the Waja model. Table 9 is providing the summary of the current position of Ingress in the domestic and regional market. This result shows that, the strategy to venture to a new niche regional market in Thailand with Ingress’s technical provider-Katayama was fruitful particularly to establish its production and market base in Thailand as a hub of ASEAN automotive industry. Technological Internalization Ingress places much emphasis on quality, both in its products and services. This is reflected in a number of accreditation and rewards achieved/obtained to-date such as the ISO 9002 and QS 9000 in 1977 and 1998 respectively (Table 6 p10). All standards procedures are guided by the principles of Total Quality Management (TQM) in accordance to the requirements of ISO 9002 and QS 9000. R&D is well emphasized by Proton in particular, on its suppliers and the same concern is applied in Ingress. These certificates cover the area of manufacturing of moldings and weather-strip as well as door sash. Undertaking the important of R&D, Ingress has established a wholly owned subsidiary namely IRSB in 1996, to undertake all the R&D jobs. Ingress has invested RM

17

4.3 million including in providing the CAD and CAE/M between the years 1997-2000. On-going technical assistance with Katayama Kogyo of Japan and presently Ingress has on-line data transfer and consultancy that would pave the way for joint development and work sharing. IRSB or presently known as ITC possesses mechanization including semi and fully automation besides fully robotic mechanization39. In addition to this, ITC is going to have its own fabrication not only in Malaysia but also within ASEAN region including fitting and assembly at customers’ site. In term of quality, Ingress should strengthen competitiveness by setting high quality standards and competitive cost. In particular, Ingress has successfully achieved parts quality level to comply with the world standards- e.g. 40-PPM40. Through various internal engineering, Ingress has achieved compliance the world quality system- various ISO standards as well as accredited with various Protons’ award41. Marketing and Building Network of Technical Alliance

Ingress possesses technologies that scarce in ASEAN. Steel roll forming is applied in both its co-extruded moldings and door sash operations. Co-extrusion, flocking and stretch bending technologies are employed in the manufacture of moldings; sash operation requires various welding technologies including seam and plasma welding, as well as a rotary-bending process. Strategically, the focus on specialization for rolls forming, extrusion/stamping, and to build own and internal expertise in product development and product extension for these related specialization seems reasonable. In order to acquire adequate forces to build its own internal stabilization, the collaboration with existing technology provider-Katayama Kogyo of Japan42, has been enhanced. As a result of this long-standing and stable relationship, Katayama advanced its commitment from being merely the technology provider for Ingress, by being the partner of the company by acquire 10 percent share in Ingress Precision. On a long-term basis, both companies endeavor an international operation for the Southeast Asian market with the establishment of Ingress Auto ventures (IAV)43

with Katayama provides 23 percent of share to tap into domestic and export markets in Thailand. As a parts and components supplier, Ingress’s localization in Thailand would reduce cost and limits exposure to currency fluctuation- one of the challenges that vulnerable to Ingress. Currently, Ingress is the suppliers for Mitsubishi Sittipol Corporation (MSC), Isuzu Manufacturing Corporation Thailand (IMCT), and Honda Automobile Thailand Company (HATC)44. Thailand market is very important to Ingress as the gate to penetrate ASEAN’s market.

39 ITC own products are robotic, plasma welding, MS cutting, dust collector, anti rust spray and turkey molding line. With all this, ITC is adequately provides the service to Ingress. 40 PPM denotes that rejected parts per million; Toyota target is 10 PPM. This data is acquired from the author’s recent case study at Ingress- April-May, 2002. 41 Accredited various automakers’ awards-Most Improved Vendor in 1996; most successful customer award 1997, Product Development awards 1996, etc. 42 Katayama is a shareholder of Ingress (IAV Thailand-23 percent and IPSB (Malaysia) -10 percent) and Ingress’s main source of technology and one of Japan’s largest producers of roll-formed automotive components, including co-extruded molding, door sash and bellows. 43 IAV operated since 1998, manufactures and supplies roll-formed plastic moldings and weather-strips as well as roll-formed metal automotive door sash and related components in Thailand. 44 Sash COMP, R/L FR DR UP; sash R/L FR DR, and CTR LWR.

18

Technologically, through partnership, Katayama developed the manufacturing

processes used by Ingress. The automated facility installed in its manufacturing plants ensures consistency in product quality whilst minimizing rejects. With the assistance of Katayama, Ingress has modeled its productivity and quality standards after those of Katayama. Regular technical audit were held jointly in Malaysia to establish Ingress’s capabilities and measures were taken under the supervision of Katayama so that improvement targets are met. This systematic approach in transfer-of-technology has been instrumental in the rapid progress of Ingress. In summary, the key benefits of Ingress relationship with Katayama are: (1) Up-to date technology; (2) Access to global contracts; and (3) Acquire broad customer base.

Conclusion

Business collaboration in the auto sector is also extending beyond partners to include competitors. However, Proton may not yet reach this point at the moment. The same also applied to vendors. They may collaborate with their technical provider into strategic alliance and explore the new niche market and new product development. Even if both Malaysian automaker and vendors are not willing to trade its equity for technological or market gains, they should expedite the search for compatible global partners that have strategic and synergistic fits with its aspirations. Domestically, Proton has the advantage in terms of dominant market share and well-established distribution and service network. This status quo will remain for the next three years at least, following Malaysia’s deferment to 2005 of market opening measures for the auto sector under AFTA. But there is no guarantee that Proton car’s dominance in local scene will not be threatened beyond that date. It is becoming increasingly clear that trade and market liberalization will have significant implications on how business is done in a globalize market and the automotive sector is no exception. Liberalization will cause some firms- especially the inefficient and weaker ones-to collapse at the expense of stronger ones. To meet the challenges of liberalization, it is imperative that Proton and vendors link up with the best players in the automotive business. A strengthened Proton and vendors both financially and technologically-will definitely be better positioned to reap the benefits of trade and market liberalization.

The additional timeframe, which Malaysia’s has gained from a delayed entry into AFTA, should also put to good use. Getting into and nurturing any sort of alliance and technological internalization takes times as it involves building trust into relationship and internal capabilities building. Both Proton and vendors should move fast to identifying the right partners for collaboration and the right technical expertise to acquire, in order for both strategies to capitalize effectively on the breathing space they have been given to prepare for open competition in the future. Thriving under a protected regime in the long term is not the answer and unless efforts through alliance and upgrading the technology while venturing to new niche market are created, it is unlikely Proton and its vendors will continue to enjoy the dominance it presently hold in the domestic market. As for both Proton and suppliers, the ultimate test will come when protectionist measures are

19

removed. The latest spate of achievements has undoubtedly placed the national automobile industry in a much better position to compete with its established contenders. Yet, the risks associated with doing it alone can be significantly lowered if the players were to enter into strategic and technologically tie-up for win-win situation. To be cost-competitive and efficient in facing the challenges of liberalization, both Proton and vendors may have to collaborate at various fronts. Some examples as already discussed including joint R&D, product development, venturing into the use of more common parts and components, combined purchasing strategies and complementation through specialization in production and supply as well as accurately venturing into the new niche markets beyond domestic level.

This study found that among Proton’s strategies are (1) Attaining cost leadership

and differentiation strategies by improving the R&D sector and accelerating investment in product development, (2) Exploring new niche market and alliance in order to expand the distribution channels, (3) providing new brand images to accelerate public confidence and brand loyalty in the domestic and international market, and (4) Diversifying parts and component sources and selecting reputable suppliers would help in achieving cost reduction effort of the company, and creating strategic alliance to improve technical capability as well as to penetrating new market and acquiring faster transfer of technology and technical-know-how. Local vendors also have to follow the steps taken and advised by Proton as they also depend the market on Proton cars at least until they also could graduate to be regional players. Tiering of vendors for components parts supply is already the norm among global auto markets. And unless Proton has a core group of reliable vendors that can supply it with high quality components parts at competitive costs on a timely basis, Proton may be forced to look elsewhere to fulfill its dream of becoming a truly world-class player. As for Ingress, these main strategies perceived workable: (1) To establish itself as an ASEAN based regional player by winning more customers with regional reach, (2) To rationalizing its operations particularly technological internalization efforts and embark on continuous improvement programs in Malaysia and Thailand to increase its competitiveness, (3) To look at the possibility penetrating of direct exports to other assemblers outside and within ASEAN, such as Japan (possibly through strategic alliance with Katayama), and the growing markets such as in India and Turkey; and (4) To participate actively in global bidding of projects in partnership with Katayama. In general, local suppliers are suggest to have two major choices to enhancing its technological capability: (1) To work with their technical counterpart (through new collaboration in order to tap both technical expertise and market opportunities at regional level, and, (2) To speed up technology learning and release their dependence on technical provider by enhancing their in-house R&D capability. By this way, they could gradually implant the technology learning and decreasing royalty payment as well. The problem is, establishing in-house R&D is not an easy job and needs high capital and time consuming. However, they could position themselves to be second tier suppliers for the time being and gradually increase their organizational learning to speed up their capability to be the first tier supplier. They should learn carefully from the buyer’s development planning on supplier development and outsourcing trend to accurately position them in this industry.

20

The results of this study is supporting Porter’s generic strategies which found that cost leadership through enhancing R&D, outsourcing practices to access cheaper inputs, and product development, would be the choices for business strategies to be practiced by both automaker and suppliers. The third strategy, focus, was found supporting the former strategies through exploring niche market; increase public confidence and venturing with new partner in marketing. For the same purpose, differentiation strategy supported by organizational learning on technological improvement and R&D would help them to come up with new brand image and new product development. This study suggests that both cost leadership and focus in niche market be highly supported by differentiation practices in order to make the main strategies more workable. The results also suggest that, the sources of competitive advantages are many, and firms need to find that fits with its business strategy. Base on the firm’s own resources and capabilities, it could provide a basis for their business strategies.

References Abdullah, Rashid. (2002). Automaker-supplier relationship: Intra-firm and inter-firm

technological linkage in the Malaysian automobile industry. In Abu Bakar, Engku Muhammad Nazri. (Ed.), Proceeding of National Seminar in Decision Science. School of Quantitative Science, Sintok: Universiti Utara Malaysia. pp. 64-73.

Abdulsomad, Kamaruding. (1999). Promoting industrial and technology development

under contrasting industrial policies. In Jomo, K.S. , Felker, Greg. , & Rasiah, Rajah. (Eds.), Industrial Technology Development in Malaysia. London: Routledge.

Ali, A. (1992). Malaysia’s Industrialization: The Quest for Technology. Singapore:

Oxford University Press. Bamberger, L. (1989). Developing competitive advantage in small and medium-size

firms. Long Range Planning. Vol 22 (5), pp. 80-88. Bowman, C. (1992). Interpretive competitive strategy. In Faulkner, D. , & .Johnson, G.

The Challenge of Strategic Management. (Eds.), London: Routledge. Dess, G.G. , & Davis, P.S. (1982). An empirical examination of Porter’s (1980) generic

strategies. Academy of Management Proceedings, pp. 7-11. Hensley, M.L. , & White, E.P. (1993). The privatization experience in Malaysia:

Integrating build-operate-own and build-operate-transfer techniques within the national privatization strategy. The Columbia Journal of World Business. pp. 69-82.

Humphrey, John. (1999). Globalization and supply chain networks: the auto industry in

Brazil and India. In Gereffi, G. (Ed.), Global Production and Local Jobs. Geneva: International Institute for Labour Studies.

21

Malaysia Industrial Development (MIDA). (1986). Various Publications. Kuala Lumpur. Md.Zabid, M.A. Rashid. (2000). Business strategies and competitive advantage factors in

the electronics industry. Journal Pengurusan. Vol.19. pp. 27-39. Porter, M. (1980). Competitive Strategy. New York/London: Macmillan Press. Proton Corporate Information. (2000). Shah Alam: Proton. Rasiah, R. (1998). Regulation and market structure of South East Asia’s car industry.

Kuala Lumpur: Institute of Malaysia and International Studies. (IKMAS), University Kebangsaan Malaysia.

Rasiah, Rajah. (1999). Liberalization and the car industry in South East Asia. Occasional

Paper #99, Department of Intercultural Communication and Management, Copenhagen: Copenhagen Business School.

Acknowledgement

My gratitude is extends to all those who assisted me in my research in Malaysia and Japan though I am not able to list their names. Credit also goes to my academic supervisors, as well as top management executives and managers of both Proton and vendors in Malaysia, which provided me guidance and advises at different stages of my research in 2001 and 2002. I am also grateful to the Setsutaro Kobayashi Memorial Fund, Fuji Xerox Company of Japan for awarding me research grants in order to conduct my work successfully.

22

Table 1: Merits and Demerits of Liberal and Protectionist Approaches

Approach Merits Demerits

Liberal • Small burden as the government •Leadership in the hands of foreign capital

•Smooth response to market expansion

•Difficult for large production lots to come about

•Difficult for support industries to follow up

Protectionist •Large production lots possible •Large burden as the government •Relatively easy for support

industries to grow up •Leadership by host country

•Over protection inhibits business diversification causing delayed responses to liberalization

Source: Adopted from Bank of Tokyo-Mitsubishi Review, Vol. 1. No.4. September 1996.

Table 2 Automotive Tariffs Rates in Malaysia

CBU Prohibited in principle unless an approval permit is obtained.

Passenger car: Less then 1800 cc: 140% More than 1800 cc: 170% More than2500 cc: 300% . Commercial vehicles: Vans: 35-50% 4WD vehicles: 50% Trucks & buses: 35%

CKD Passenger car: National cars: Proton-113%, Kancil-0% (for limited period) Non-national cars: 2% Commercial vehicles: Vans – 5%; 4WD-5%, Truck & buses-0%

Source: Adopted from Philippine Automotive Federation, Inc., 1999.

23

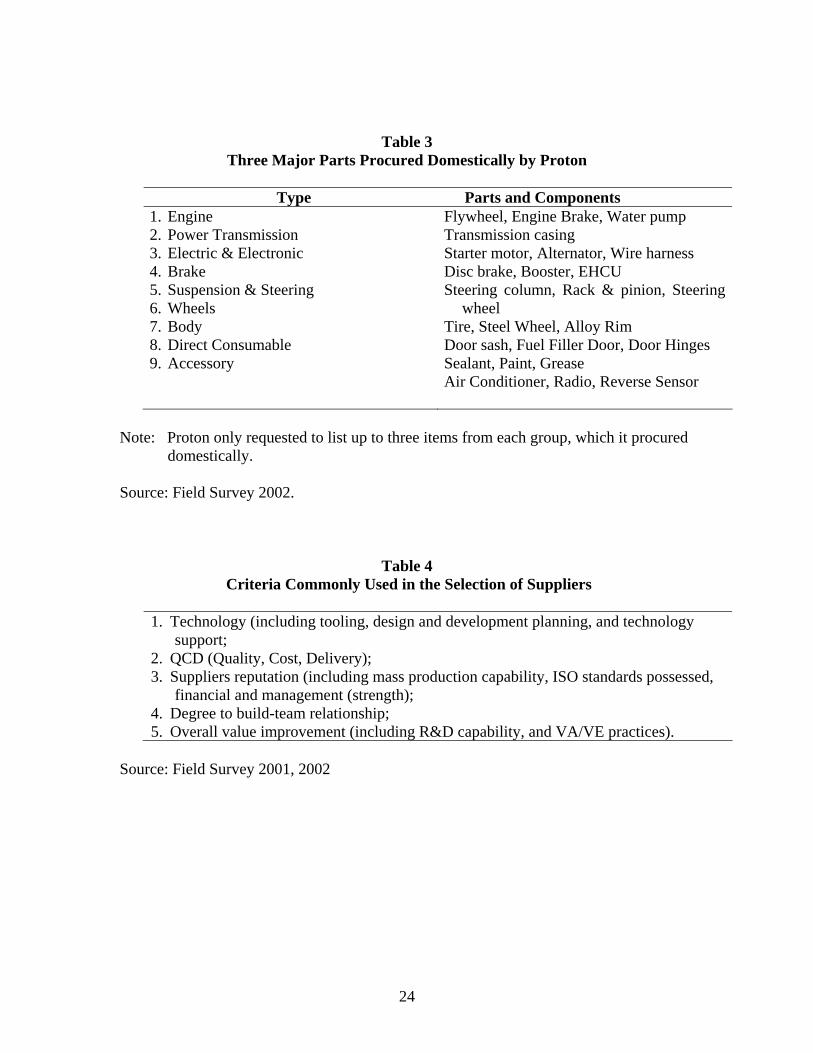

Table 3 Three Major Parts Procured Domestically by Proton

Type Parts and Components

1. Engine 2. Power Transmission 3. Electric & Electronic 4. Brake 5. Suspension & Steering 6. Wheels 7. Body 8. Direct Consumable 9. Accessory

Flywheel, Engine Brake, Water pump Transmission casing Starter motor, Alternator, Wire harness Disc brake, Booster, EHCU Steering column, Rack & pinion, Steering

wheel Tire, Steel Wheel, Alloy Rim Door sash, Fuel Filler Door, Door Hinges Sealant, Paint, Grease Air Conditioner, Radio, Reverse Sensor

Note: Proton only requested to list up to three items from each group, which it procured

domestically. Source: Field Survey 2002.

Table 4 Criteria Commonly Used in the Selection of Suppliers

1. Technology (including tooling, design and development planning, and technology

support; 2. QCD (Quality, Cost, Delivery); 3. Suppliers reputation (including mass production capability, ISO standards possessed,

financial and management (strength); 4. Degree to build-team relationship; 5. Overall value improvement (including R&D capability, and VA/VE practices).

Source: Field Survey 2001, 2002

24

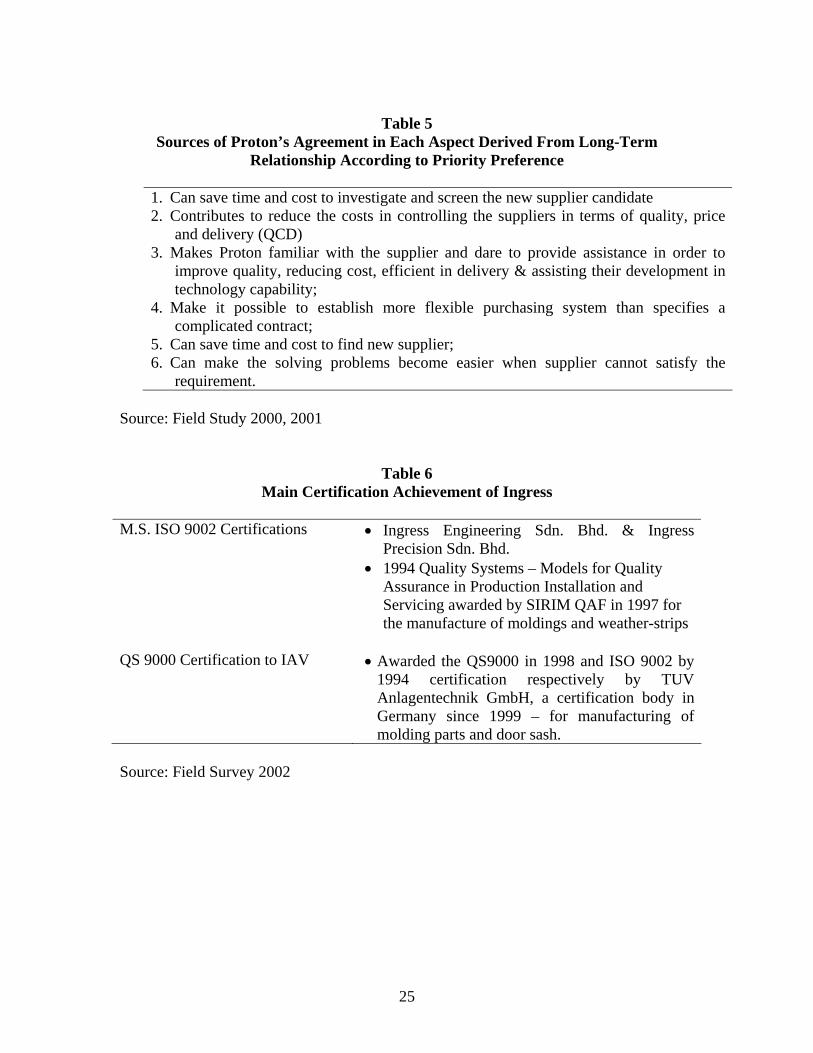

Table 5

Sources of Proton’s Agreement in Each Aspect Derived From Long-Term Relationship According to Priority Preference

1. Can save time and cost to investigate and screen the new supplier candidate 2. Contributes to reduce the costs in controlling the suppliers in terms of quality, price

and delivery (QCD) 3. Makes Proton familiar with the supplier and dare to provide assistance in order to

improve quality, reducing cost, efficient in delivery & assisting their development in technology capability;

4. Make it possible to establish more flexible purchasing system than specifies a complicated contract;

5. Can save time and cost to find new supplier; 6. Can make the solving problems become easier when supplier cannot satisfy the

requirement. Source: Field Study 2000, 2001

Table 6 Main Certification Achievement of Ingress

M.S. ISO 9002 Certifications • Ingress Engineering Sdn. Bhd. & Ingress

Precision Sdn. Bhd. • 1994 Quality Systems – Models for Quality

Assurance in Production Installation and Servicing awarded by SIRIM QAF in 1997 for the manufacture of moldings and weather-strips

QS 9000 Certification to IAV • Awarded the QS9000 in 1998 and ISO 9002 by

1994 certification respectively by TUV Anlagentechnik GmbH, a certification body in Germany since 1999 – for manufacturing of molding parts and door sash.

Source: Field Survey 2002

25

Table 7

Major Automotive Buyers as for January 2000

Contribution to Ingress’s Customers/Buyers Length of relationship Turnover (%)

Proton 8 26.8% Perodua 5 11.9% AAT, 3 2.8% Thailand 3 3.1% MSC - - Thailand - -

Source: Field Survey 2001 and 2002

Table 8 Ingress’s Position Among Its Competitors

Competitors Remarks

1. Automotive Industries Sdn. Bhd. ASB is a producer of exhaust systems in Malaysia, supplying Proton and Perodua.

2. ASAB Thailand SAB produces varieties of stead auto parts in Thailand, including door sashes for Mitsubishi and Nissan.

Ingress’s roll-forming line comprises of 43 stages, where as SAB’s only 18 stages. This allows Ingress to produce more complex door sash designs for use in a wide variety of vehicles; SAB is limited to supplier designs as used on pick-up trucks.

3. TOACS Thailand Co-extruded company in Thailand.

Besides Ingress TOAC is the only other company in ASEAN producing steel/PVC co-extruded moldings.

4. Calsonic, Japan Produces exhaust system in Thailand.

5. Hashimoto, Japan Japan’s leading producer of door sashes.

Not indicated it intends to establish operation in ASEAN.

6. OM cooperation, Japan Suppliers door sashes to several automakers in Japan.

Not indicated it intends to establish operation in ASEAN.

7. Nishikawa Rubber, Japan and Thailand Japan NR produces both steel/rubber and steel/PVC co-extruded moldings, but in Thailand just steel/rubber moldings.

Presently (2002 no indication to expand its Thailand operation to produce steel/PVC moldings.

8. Shiroki, Japan A components maker produces door sash and co-extruded moldings. Operated also in Vietnam – Vina Shiroki

Have no operations or partners in Thailand or Malaysia and gave no indication that they will be established.

Source: Field Survey 2001 and 2002

26

Table 9

Current Marketing Position of Ingress

Automaker/Buyer at domestic level

Parts supplied

Proton Co-extruded moldings for Perdana, co-extruded moldings and door sashes for Wira.