protecting the parties to an m&a deal edwin godfrey dundas & wilson llp...

TRANSCRIPT

Protecting the Parties to an M&A Deal

Edwin Godfrey

Dundas & Wilson LLP

Industrijuristgruppen

Fefor Hotel, 8 March 2008

Presentation Agenda

• How can the Buyer be protected?• Warranties, representations and indemnities• The differences between them and their

consequences• How can the Seller be protected?• Vendor protection clauses, disclosure letters etc.• Tactics for each side• Based on English law and practice (also very widely

used in international deals)

How important is this subject?

• Most fascinating area of the law? - No!• Vital to the parties to a deal? – Definitely!• Letters of intent often refer to “usual reps and

warranties” – but working out a reasonable balance can be a major task

• Don’t leave it to the junior assistant – if anything goes wrong it will probably be here

• Not only the lawyers but the commercial team need to understand what is involved

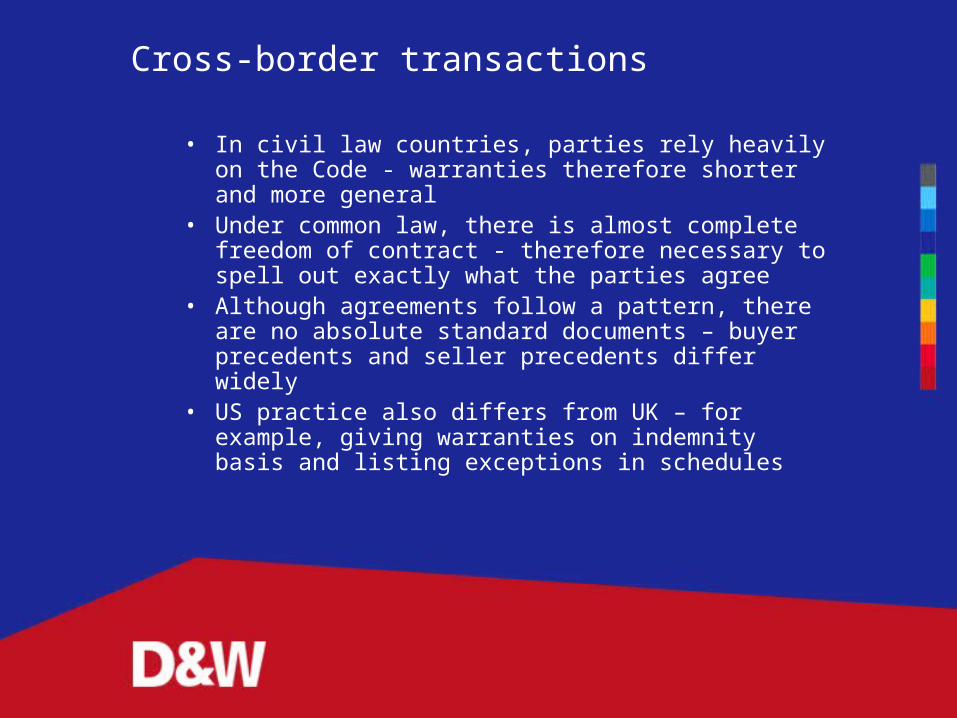

Cross-border transactions

• In civil law countries, parties rely heavily on the Code - warranties therefore shorter and more general

• Under common law, there is almost complete freedom of contract - therefore necessary to spell out exactly what the parties agree

• Although agreements follow a pattern, there are no absolute standard documents – buyer precedents and seller precedents differ widely

• US practice also differs from UK – for example, giving warranties on indemnity basis and listing exceptions in schedules

Shares or Assets?

• Does the Buyer acquire a company or a business, or a combination of both?

• Often driven by tax considerations – but leads to very different structures

• In an assets deal, Buyer needs protection for the agreed categories of assets and liabilities

• In a share deal, warranties etc. need to be much wider – Buyer needs protection against any surprises within the corporate envelope

The Meanings of English Legal Terms

• Need to distinguish between:• Conditions• Warranties• Representations• Indemnities

What is a Condition?

• Normally defined as a contractual term whose breach allows the innocent party to terminate the contract

• In the M&A context, most relevant in the form of conditions precedent

• A list of conditions (e.g. competition clearance, board approvals) must be fulfilled before the parties are obliged to complete the deal

• But a party may still be liable for failing to achieve a condition which is within its control

What is a Warranty?

• Normally, a contractual term whose breach does not normally give a right of termination, but only damages

• Warranties may include statements of past and present facts about the business – but may also include undertakings for the future

• May be qualified by their own terms or other terms of the agreement

• Usual remedy is damages for breach of contract – but the agreement may also allow termination in some cases

What is a Representation?

• Some overlap with the concept of warranty (e.g in the phrase “representations and warranties”)

• Includes any statement (written, oral or even by conduct) which induces the recipient to rely on it

• It may appear in the contract, but may also be an informal assurance (e.g. in a conversation in the pub)

• Remedies depend on common law and the Misrepresentation Act 1967 – but these are commonly excluded by contract

Consequences of Misrepresentation

• Fraudulent misrepresentation may give right of action for the tort of deceit (and may also be criminal)

• Negligent misrepresentation may give a right to damages for negligence

• Any misrepresentation (even innocent) which induces a contract may give a right to rescind or claim damages

• But many consequences are typically excluded by the agreement (except in case of fraud)

Approach to Representations

• The Buyer normally gains much information outside the contract

• Examples: Seller’s information memorandum, data room, due diligence, meetings with employees

• Agreement must protect the Seller by excluding any representations not stated in the agreement

• Instead, the Buyer should ask for relevant warranties which are clearly stated in the agreement

• Also normal to exclude any right to cancel the contract for misrepresentation (unless fraudulent)

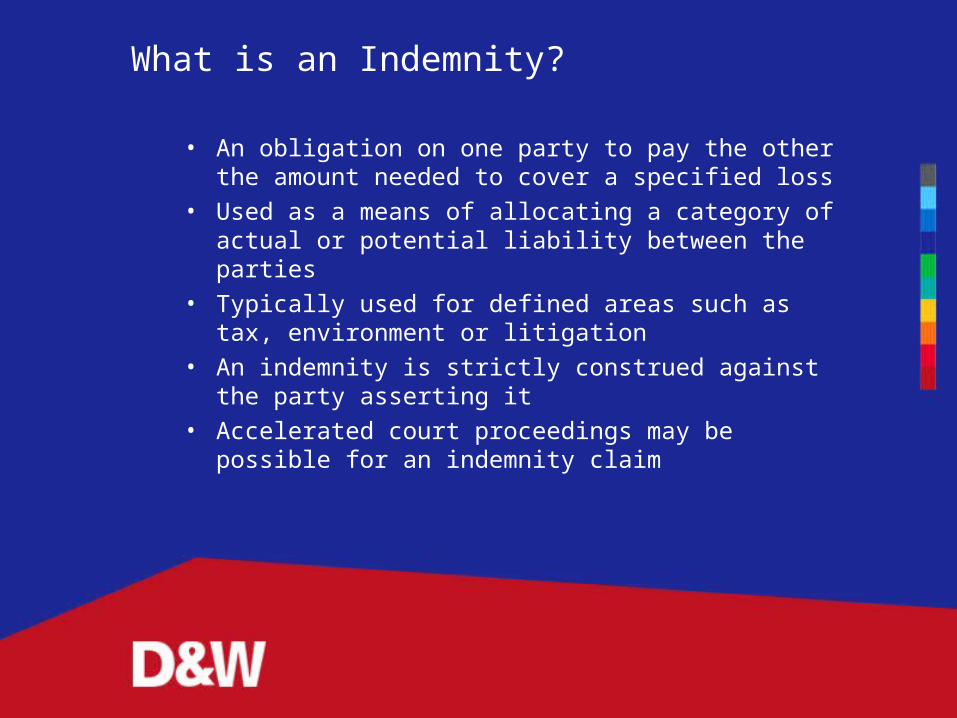

What is an Indemnity?

• An obligation on one party to pay the other the amount needed to cover a specified loss

• Used as a means of allocating a category of actual or potential liability between the parties

• Typically used for defined areas such as tax, environment or litigation

• An indemnity is strictly construed against the party asserting it

• Accelerated court proceedings may be possible for an indemnity claim

Approach to Indemnities

• Tax indemnities are normal in a share acquisition• In assets deals, mutual indemnities may be needed

for liabilities assumed by Buyer or retained by Seller• Liabilities to employees will pass with the business,

but may be indemnified• Indemnity may be needed for potential

environmental problems on industrial sites• Indemnities are not qualified by disclosures, only by

express carve-outs

Differences between Warranties and Indemnities

• Warranty claims are triggered by breach of contract - damages designed to put the innocent party in a position as if there had been no breach

• Indemnity claims do not need proof of a breach of contract – they are triggered by a specified event, with compensation as specified

• Warranty claims are subject to an obligation to mitigate loss, indemnities usually not

• Indemnities not usually qualified by disclosure – usually also treated differently in vendor protection provisions

The Purpose of Warranties

• Risk allocation – who bears the risk that the business may not be as the Buyer expects it?

• Prompting disclosure – warranties incentivise the Seller to disclose as much as possible to minimise his risk

• Disclosures (before signing) or breaches (afterwards) may give grounds for adjusting the price

• Triggers for termination (in case of a gap between contract and completion)

• A claim for damages after the event is only a last resort, not the main object of the warranties

Split Exchange and Completion

• Completion (called closing in US practice) can take place immediately after signing the contract

• But if conditions remain to be fulfilled, completion will be postponed

• What happens if liabilities arise in the gap period?• Buyer may ask for warranties to be repeated at

completion (“bringdown” in the US), placing risk firmly on Seller

• Alternatively, Seller may only undertake not to do or permit anything in its control which would cause warranties to be untrue at completion

Who Gives the Warranties?

• Simple answer where there is a single Seller• Where there are multiple Sellers, smaller

shareholders may be unwilling to give warranties, or to give them without strict limitations

• Some Sellers may also warrant only areas within their knowledge

• Institutional shareholders or trustee Sellers may also refuse to warrant anything beyond their title to the shares or assets

• Sales by auction may have no or few warranties

Liabilities in case of Multiple Sellers

• Buyer will want the liabilities of Sellers to be “joint and several” – this means the Buyer can sue any Seller for the full amount of the claim, leaving that Seller to claim contribution from the others

• Sellers may seek to limit liability to their proportion of any claim

• Special provisions needed to make up the shortfall if some Sellers give no warranties at all

• If there is joint and several liability in the contract, Sellers may still regulate the liability between themselves by separate agreement

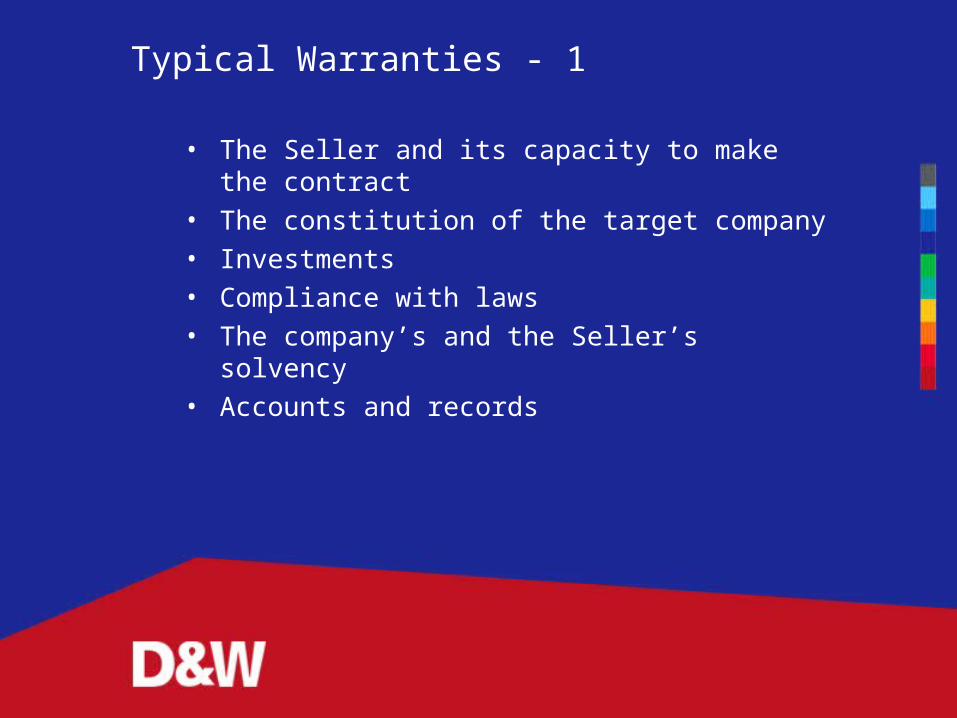

Typical Warranties - 1

• The Seller and its capacity to make the contract• The constitution of the target company• Investments• Compliance with laws• The company’s and the Seller’s solvency• Accounts and records

Typical Warranties - 2

• The company’s recent business and the effect of the sale

• The company’s assets• Special warranties on land and buildings• The company’s contracts• Financing arrangements• Directors and employees• Taxation

Qualifications on Warranties

• Warranties are basically absolute statements of fact• But they may be qualified by:

• Their own terms (using express carve-outs, or concepts such as “materiality” or “awareness”)

• Vendor protection provisions (usually set out in a separate schedule)

• The contents of a disclosure letter

Contentious Issues on Warranties

• Scope of protection (e.g. “materiality”, “awareness”)• General warranty of disclosures or data room• Indemnity or “pound for pound” basis (cf. US

practice)• Extent of vendor protection provisions• Rights of rescission or termination• Assignability of warranties• Control of third party litigation

Measure of Damages for Breach

• Normal approach (common law) is to put the Buyer in a position as if there had been no breach

• This involves assessing what effect the breach has on the value of the acquired shares – difference between the price paid and the market price assuming no breach

• But some breaches of warranty may not affect share value at all (e.g. defect in an asset if the company is valued for its profit level, or if the Buyer has made a good bargain)

• Buyers may therefore argue for “pound for pound” compensation (instead, or as an alternative), but Sellers will resist this

Vendor Protection

• Usually a heavily negotiated part of the agreement• Typical headings:

• Cap on aggregate liability (e.g. total value of the consideration, or a stated fraction of it)

• Minimum amount per claim (“de minimis”)• Threshold or deductible for all claims (note the important

difference)• Time limits (general limit, longer for tax and environment)• No duplication of claims• Exclusion of claims caused by the Buyer• etc

Effect of Disclosure or Buyer’s Knowledge

• Disclosure letter will make Buyer formally aware of is contents

• No duty to disclose matters not covered by warranties

• But failure to disclose matters affecting warranties may cause a claim and may also be fraudulent

• What if Buyer independently knows that a warranty is untrue? Agreement should cover this situation

• Agreement usually provides that only formal disclosures qualify the warranties

The Disclosure Letter

• Addressed by the Seller to the Buyer and referred to in the agreement

• Disclosures set out in the agreed letter are exceptions to the warranties (but not normally to the indemnities)

• Usually refers to:• Entries in public registers• Listed documents with copies attached to the

letter• Narrative statements in the letter

Approach to the Disclosure Letter

• The agreement normally requires matters to be “fairly disclosed”

• Seller will want to make as much as possible count as disclosed

• But Seller will resist warranting the disclosure letter itself

• Buyer will want specific disclosure, not just a general reference to a category of documents

• Case law makes clear that merely making known the means by which knowledge may be obtained is not enough

Due Diligence

• May be limited to reviewing an actual or virtual data room, or much more extensive

• Likely to include legal, financial, commercial and technical due diligence

• Appropriate level depends on nature and value of the business

• Results should be distilled and used to prepare specific warranties and indemnities

• Employees and companies passing to the Buyer need to be protected from suit by the Seller, as they are usually the source of the information

Security for Breach of Warranties

• May for example consist of:• A retention of part of the price• A joint bank account (escrow) for part of the

price• Right of set-off against deferred consideration

(e.g. earn-out)• Parent company guarantee for the Seller

Assignment of Warranties

• Assignment of warranties to a member of the Buyer’s group is often allowed – but not usually to a third party buyer of the company

• Even if allowed, note that assignee can only recover its own loss, and no more than the assignor could have recovered

• May be possible to achieve a similar result by making the target company a party to the agreement or by giving rights to other parties – Contracts (Rights of Third Parties) Act 1999

Tactics for the Buyer

• Keep control of the drafting• Get the maximum reasonable warranty cover in all

relevant areas• Make sure vendor protection is not too wide for the

size of the transaction• Be careful about the level and timing of the Seller’s

disclosures• Get indemnity cover for tax and environment• Identify through due diligence the real problems

which need special indemnities

Tactics for the Seller

• In an assets deal or a sale by auction, control of the drafting may be possible

• Keep warranties within reasonable bounds relevant to the type of business being sold

• Get a reasonable set of limitations of liability, e.g. caps, cushions, time limits etc

• Disclose as much as reasonably possible to dilute the effect of the warranties

• Take particular care over carve-outs and limits to indemnities

The End!

Questions and Discussion

• Protecting the Parties to an M&A Deal