prospects for lng imports 07. 23

TRANSCRIPT

chris rumley, marina kim, allison ball, and robert curtotti

december 2007

abare research report 07. 23

abare abar

ein

nova

tion

in e

cono

mic

s

natural gas in india prospects for LNG imports

abareconomics.com

ii

© Commonwealth of Australia 2007

This work is copyright. The Copyright Act 1968 permits fair dealing for study, research, news reporting, criticism or review. Selected passages, tables or diagrams may be reproduced for such purposes provided acknowledgment of the source is included. Major extracts or the entire document may not be reproduced by any process without the written permission of the Executive Director, ABARE.

ISSN 1037-8286ISBN 978-1-921448-07-2

Rumley, C., Kim, M., Ball, A. and Curtotti, R. 2007, Natural Gas in India — Prospects for LNG Imports, ABARE Research Report 07.23 Prepared for the Australian Government Department of Resources, Energy and Tourism, Canberra, December.

Australian Bureau of Agricultural and Resource EconomicsGPO Box 1563 Canberra 2601

Telephone +61 2 6272 2000 Facsimile +61 2 6272 2001Internet abareconomics.com

ABARE is a professionally independent government economic research agency.

ABARE project 3126

iii

natural gas in india » abare research report 07.23

foreword

Consumption of natural gas in India has the potential to rise signifi cantly, on the basis of robust economic growth, an expanding population and recent large domestic gas discoveries. However, realising this potential will depend on addressing several issues, including further deregulation of the gas sector, reforms in gas pricing and in key consumer markets, and the development of further gas infrastructure. These issues are creating signifi cant uncertainties about the prospects for future LNG imports, which play a small but growing role in the domestic gas market.

The objective in this study is to assess the potential growth in natural gas demand in India over the period to 2025 and to consider how such demand might be met. A number of gas supply options are considered, including the delivery of gas from existing and recently discovered domestic gas sources, the commence-ment of pipeline gas imports from Iran, and increased imports of LNG. The study concludes that LNG imports are likely to rise, particularly from the middle of the next decade, but that the share of LNG will be affected by the rate at which other gas supply options are developed.

The study also considers whether India will be able to secure the additional LNG it requires. Existing and planned LNG terminal capacity is expected to be suffi cient to meet India’s gas requirements over the medium to longer term. However, compe-tition from major LNG consuming countries that are willing to pay high prices may be a constraint to India’s ability to secure long term LNG supplies.

Phillip GlydeExecutive Director

December 2007

iv

natural gas in india » abare research report 07.23

acknowledgments

This study was funded by the Australian Government Department of Resources, Energy and Tourism, with assistance from BHP Billiton Petroleum Pty Ltd and Santos Ltd.

The authors wish to thank several colleagues for their valuable contributions throughout the course of the study: in ABARE, Karen Schneider, Terry Sheales, Jane Melanie, Paul Ross, Leanna Tedesco and Andrew Schultz; in the Department of Resources, Energy and Tourism, Geoff Stone and Willie Senanayake; in the Australian High Commission, New Delhi, Victoria Walker.

In addition, the authors gratefully acknowledge the information, insights and comments on a draft report that were provided by BHP Billiton Petroleum Pty Ltd, Chevron Australia Pty Ltd, ExxonMobil Australia Pty Ltd, ConocoPhillips Australia Pty Ltd, North West Shelf Australia LNG Pty Ltd, Santos Ltd, Shell Development (Australia) Pty Ltd and Woodside Energy Ltd.

Many organisations in India also provided valuable information and insights. The authors are grateful for contributions from: The Energy and Resources Institute (TERI), ExxonMobil Gas (India) Private Limited, GAIL (India) Limited, Indian Council of World Affairs, India Energy Forum, Ministry of Petroleum and Natural Gas, National Thermal Power Corporation (NTPC) Limited, Observer Research Foundation, Petro-leum and Natural Gas Regulatory Board, Petronet LNG Limited, Planning Commis-sion of India, PricewaterhouseCoopers Pvt Ltd and Reliance Industries Limited (RIL) .

conversions for natural gas and LNG

billion billion million million trillion cubic metres cubic feet tonnes oil tonnes British NG NG equivalent LNG thermal units

1 billion cubic metres NG 1.00 35.30 0.90 0.73 36.00

1 billion cubic feet NG 0.028 1.00 0.026 0.021 1.03

1 million tonnes oil equivalent 1.111 39.20 1.00 0.805 40.40

1 million tonnes LNG 1.38 48.70 1.23 1.00 52.00

1 trillion British thermal units 0.028 0.98 0.025 0.02 1.00Source: BP (2007).

v

natural gas in india » abare research report 07.23

contentssummary 1

1 introduction 8

2 energy and natural gas in India 11

primary energy consumption 11natural gas consumption 18natural gas supply 23gas pricing 33

3 factors affecting India’s future natural gas demand 38

gas market reform 38end use market reforms 40security of energy supply 45environmental issues 46

4 projecting natural gas demand in India 48

analytical framework 48key assumptions 49outlook for energy consumption, by fuel 52outlook for natural gas demand, by sector 58

5 natural gas supply considerations 61

domestic natural gas production 61cross border pipelines 63existing LNG import contracts 67natural gas supply and demand balance 67LNG import infrastructure 70international LNG outlook 71prospects for Australian LNG 75

6 conclusions 79

references 81

vi

natural gas in india » abare research report 07.23

boxes 1 recent economic performance in India 122 household consumption of noncommercial fuels in India 213 structure of the natural gas sector in India 274 evolution of gas pricing in India 345 alternative projections for India’s energy outlook to 2025 536 coal seam methane potential in India 637 international pipelines and LNG 65

fi guresA natural gas consumption, by sector, 2005 – India 2B natural gas consumption, by sector, reference case – India 4C potential gas demand and supply – India 6

1 total primary energy consumption – India 112 international comparison of primary energy

consumption, 2005 113 GDP and per person income – India 124 distribution of India’s population, 2005 125 foreign direct investment in India 136 structure of the Indian economy 137 international comparison of energy intensity, 2005 148 international comparison of energy consumption per

person, 2005 159 fuel mix in primary energy consumption – India 1610 electricity output, by fuel – India 1711 annual growth in electricity generation, by fuel,

1990–2005 – India 1812 natural gas consumption, by end use – India 1913 energy consumption in key sectors, by fuel – India 2014 energy consumption in the residential sector, by fuel – India 2115 natural gas supply – India 2516 LNG imports, by source – India 2617 natural gas sector structure – India 2718 gas pricing reform direction – India 35

vii

natural gas in india » abare research report 07.23

19 trends in population growth – India 5020 assumed fuel mix in electricity generation, reference case

– India 5121 fuel mix in electricity generation, 2025 – India 5322 comparison of energy consumption growth projections,

2005–25 – India 5423 comparison of natural gas demand projections,

2025 – India 5424 total primary energy consumption, by fuel – India 5625 projected average annual growth in energy consumption,

2005–25 – India 5626 fuel mix in total primary energy consumption – India 5727 projected electricity generation, by fuel – India 5828 natural gas consumption, by sector – India 5929 distribution of population between urban and rural areas

– India 6030 natural gas production scenarios – India 6231 potential gas demand and supply – India 6832 potential LNG imports – India 6933 world LNG trade 7134 Australian gas production and LNG exports 7735 Australian LNG exports, by destination 7736 outlook for LNG capacity in Australia 77

maps1 natural gas reserves – India 242 natural gas infrastructure – India 333 proposed international pipeline routes serving India 654 Australia’s natural gas reserves and infrastructure 76

viii

natural gas in india » abare research report 07.23

tablesA India’s total primary energy consumption, 2005 2B India’s LNG imports, by source, 2006 4C potential gas demand and supply balance – India 7

1 major energy and economic indicators – India 152 total primary energy consumption – India 163 installed electricity generation capacity, 2004-05 – India 174 natural gas consumption, by end use – India 185 city gas consumer base – India 226 distribution and consumption of compressed natural gas

in India, 2005-06 237 natural gas production – India 258 existing LNG terminals – India 299 changes in natural gas prices, by sector – India 3610 regions and sectors in GTEM in this study 4911 GDP and population assumptions – India 5012 growth in India’s GDP and primary energy consumption 5513 potential international gas pipeline projects – India 6714 potential gas demand and supply balance – India 6815 LNG terminals in India 7016 existing LNG plants – Asia Pacifi c market 7217 LNG plants under construction and planned

– Asia Pacifi c market 74

1

natural gas in india » abare research report 07.23

summary

» Since the discovery of large gas reserves off the west coast of India in the 1970s, natural gas has played an increasingly important role in meeting India’s growing energy demand. This trend is expected to continue, with forecast strong growth in natural gas demand over the period to 2025. Until recently, India relied on state controlled domestic production to meet its natural gas requirements. However, with mature domestic gas fi elds facing a decline in production, India is embracing the need for increased private sector partici-pation in the gas supply chain.

» Following the commissioning of India’s fi rst LNG (liquefi ed natural gas) import terminal in 2004, LNG imports rose to 6.2 million tonnes in 2006, just under a quarter of India’s natural gas consumption. LNG imports will continue to play an important role in supplying India’s demand for natural gas.

» The outlook is for increasing natural gas demand in India, given an expected combination of high economic growth, an expanding population and recent large domestic gas fi nds. However, realising this potential depends on addressing several major issues, including further deregulation of the gas sector, reforms in gas pricing and key consumer markets, such as electricity generation and fertiliser production, and the development of a national gas grid linking gas sources with geographically dispersed demand centres. These issues, particularly uncertainties about the prospects for domestic gas produc-tion and pricing, are creating some uncertainty over the outlook for LNG imports and future LNG procurement.

» While there are ambitious LNG import plans in India, this is not likely to translate into a signifi cant increase in LNG imports in the short to medium term. Pipeline natural gas imports could also provide an additional source of gas supply over the longer term, although these projects face signifi cant obstacles.

energy and natural gas consumption in India» Energy consumption in India has increased by almost 5 per cent a year since

1990, driven by rapid growth in economic output and population, and rising personal incomes. Total primary energy consumption (excluding noncommer-cial fuels, referred to as combustible renewables and waste) reached 379

2

natural gas in india » abare research report 07.23

million tonnes of oil equivalent (Mtoe) in 2005, compared with 186 million tonnes of oil equivalent in 1990. Coal is the main source of energy in India, accounting for 55 per cent of primary energy consumption in 2005, followed by oil, natural gas, renewable energy and nuclear power (table A).

» Natural gas use in India has grown at an average rate of more than 7 per cent a year since 1990, albeit from a small base. It accounted for 8 per cent of primary energy consumption in 2005. This rapid growth has been driven by government poli-cies to encourage natural gas use, including gas allocations to priority sectors such as electricity and fertilisers at subsidised prices, and expansions in gas infrastructure. In 2005, natural gas consumption in India was 32 billion cubic metres (equivalent to 23.4 million tonnes of LNG). Consumption, however, has been constrained by natural gas availability and, as such, does not refl ect the true potential for natural gas demand in the country.

» The electricity and fertiliser sectors are the main consumers of natural gas in India, partly subsidised by the government. These sectors, including captive electricity generation, accounted for 70 per cent of India’s natural gas consumption in 2005 (fi gure A; IEA 2007a).

» The use of LNG has been growing rapidly since its introduction to the Indian gas market in 2004. India currently has two operational LNG terminals on the west coast — Dahej and Hazira — with a combined capacity of 8.9 million tonnes. The Dahej terminal is supplied from Ras Gas in Qatar under a long term contract, supplemented by spot cargoes from other

table A India’s total primary energy consumption, 2005

consumption share Mtoe %

coal 208.0 54.9oil 128.6 33.9natural gas 28.8 7.6nuclear 4.5 1.2renewables a 9.1 2.4

total 379.0 100.0a Includes hydro/solar/wind/other; excludes combus-tible renewables and waste.Source: IEA (2007a).

other 3%residential 2%

other industries 25%

fertiliser 26%

electricity 44%

2005

natural gas consumption, by sectorfig AIndia

3

natural gas in india » abare research report 07.23

sources, while the Hazira terminal imports spot LNG cargoes as required (table B). India’s third LNG terminal, Dabhol in the south west, with an annual capacity of 5 million tonnes, is expected to be commissioned toward 2009.

factors affecting India’s future natural gas demand» A range of factors will affect the extent and profi le of India’s future natural gas

demand, including the development of a national gas pipeline network and the implementation of energy market and broader economic reforms. One of the most important factors will be the continuing deregulation of the domestic gas market. The government has made signifi cant progress in developing a regulatory framework to facilitate open access to the pipeline network and to promote public and private investment in gas pipeline infrastructure. The establishment of an independent regulator to monitor pipeline access and gas transport tariffs is expected to facilitate the development of a market based regime in India’s natural gas sector.

» The continuing transition from state administered, subsidised gas pricing toward market pricing is also a key factor in improving the overall availability of natural gas in India and will affect gas demand over the outlook period. The complex mix of administered and market gas prices that vary across consumer segments reduces incentive to invest in the expansion of domestic gas production and LNG imports.

» The reform processes in key end use markets, such as electricity and fertilisers, are also likely to have a direct impact on future gas demand in India. Recent policy initiatives in the fertiliser industry seek to convert the majority of nitrog-enous fertiliser production in India to natural gas. Electricity market reform, including government plans for substantial generation capacity augmentation, is likely to provide incentives for new investment in gas fi red power plants. The extent of natural gas use in electricity generation, as well as in fertiliser produc-tion, will depend to a large extent on gas availability and pricing.

projecting natural gas demand in India» The analysis of the potential demand for natural gas in India over the period

to 2025 presented in this report is based on results from ABARE’s global trade and environment model (GTEM). The projections of energy demand are based on an assumption that India’s GDP will grow at an average annual rate of 6.5 per cent over the period 2005–25 in the ‘reference case’. In an

4

natural gas in india » abare research report 07.23

alternative ‘high growth’ scenario, GDP growth is assumed to average 9.0 per cent a year over the same period, supported by higher levels of economic reform and productivity growth than in the reference case. This higher rate of GDP growth is consistent with the upper range of Indian Government projections.

» The projections are also based on assumptions relating to the fuel mix in electricity generation. In India there is considerable uncertainty about the expected fuel mix over the period to 2025. This is refl ected in the wide range of alterna-tive projections from Indian and international sources. In this study, the share of natural gas in electricity generation is assumed to be 7 per cent in 2025, around 2 percentage points lower than in 2005. This refl ects an assumed continued expansion in nuclear and coal fi red electricity generation over the projection period (IEA 2006a).

» On the basis of these assumptions, total primary energy consumption in India is projected to expand by 4 per cent a year to reach 837 million tonnes of oil equivalent in 2025. Natural gas consumption is projected to grow by 5 per cent a year between 2005 and 2025 to reach 74 million tonnes of oil equiva-lent in the reference case in 2025 (equivalent to 82 billion cubic metres and 60 million tonnes of LNG) (fi gure B). In the high growth scenario, gas consumption is projected to reach 89 million tonnes of oil equivalent in 2025 (equivalent to 99 billion cubic metres and 72 million tonnes of LNG). Driving this growth will be increases in demand in the fertilisers and other industrial sectors. This growth, however, will be dependent on the development of natural gas infrastructure, including transmission networks, and new sources of supply.

table B India’s LNG imports, by source, 2006

imports share Mt %

Qatar 5.19 84.3Egypt 0.42 6.8Oman 0.19 3.1Australia 0.12 1.9Abu Dhabi 0.06 1.0Malaysia 0.06 1.0Algeria 0.06 1.0Trinidad 0.06 1.0

total 6.16 100.0Source: FGE (2007a).

20

10

30

bm3

India

200520152025

residentialother industry

fertiliserelectricity

natural gas consumption, by sector, reference casefig B

5

natural gas in india » abare research report 07.23

natural gas supply considerations» India has three options to meet the anticipated growth in natural gas demand

over the period to 2025 — increase domestic gas production; increase LNG imports; and import natural gas via pipeline.

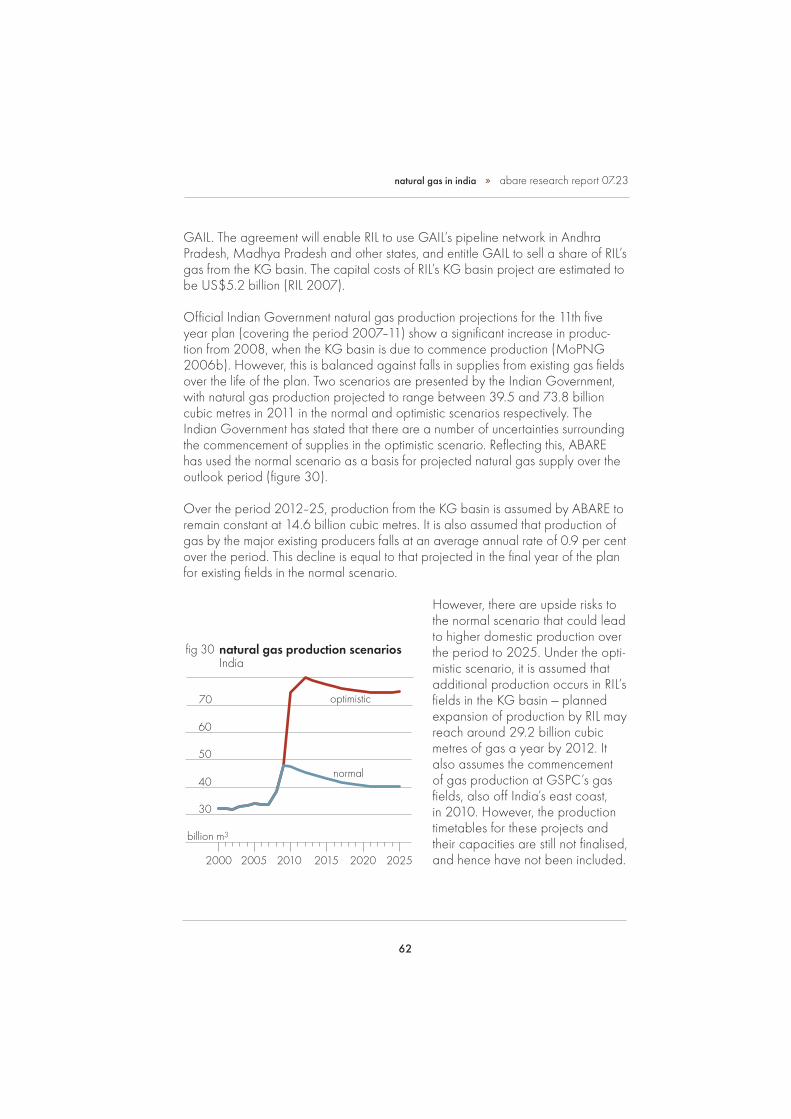

» It is assumed that there is a continued decline in production from existing mature domestic gas fi elds. However, the rate of this decline is expected to be slowed by the production of gas from recently discovered fi elds in the offshore Krishna Godavari (KG) basin from late 2008. While this and other new natural gas discoveries have the potential to expand domestic output signifi -cantly, the production timetables of these fi elds remain highly uncertain.

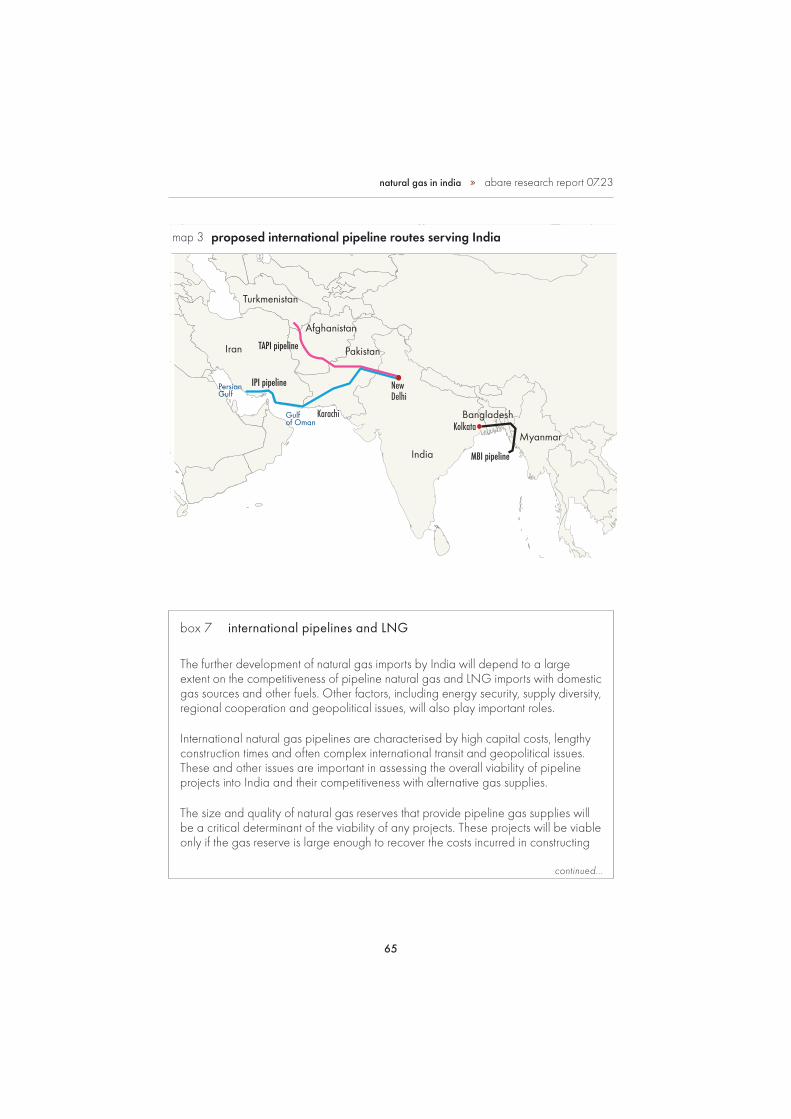

» Over the longer term, there is potential to develop pipeline natural gas imports. Several international pipelines have been under discussion in India for many years, including from Iran, Turkmenistan and Myanmar. Only the Iran–Pakistan–India pipeline project is considered to have potential as a source of supply to India over the period to 2025. Given the uncertainties that surround the supply of pipeline gas from Iran, a possible startup date is assumed to be after 2020.

» India’s decision to import pipeline gas will depend signifi cantly on geopolitical and energy security issues but the competitiveness of pipeline gas with other sources of gas will also play an important role. Distance and volume are key variables that affect the unit cost of transporting LNG and pipeline gas. While transporting natural gas via pipeline can be more cost effective than transporting LNG in some cases, the political risks associated with transiting through other countries can increase the costs of pipeline projects. In contrast, the fl exibility of LNG supply can largely avoid geopolitical sensitivities and may address some of the energy security concerns of gas importing countries.

indicative gas supply and demand balance» A potential natural gas supply and demand balance for India is provided in

fi gure C and table C, based on demand projections and current and expected gas supply. This balance assumes that production from gas fi elds in the KG basin would add supply of around 14.6 billion cubic metres a year to existing domestic production, starting from late 2008. Production from fi elds operational as at June 2007 is assumed to gradually decline over the outlook period. It is also assumed that the supply of LNG under long term contract with Qatar reaches 7.5 million tonnes a year (10.4 billion cubic metres) from 2009 and that an international pipeline from Iran could add 37 billion cubic metres a year after 2020.

6

natural gas in india » abare research report 07.23

» Based on these assumptions, it is expected that around 4.0 billion cubic metres (2.9 million tonnes) of additional gas will need to be procured by 2015. Additional gas requirements are projected to expand to 18.6 billion cubic metres (13.6 million tonnes) in 2020, and 31.6 billion cubic metres (23.1 million tonnes) in 2025. Assuming that this additional gas will be sourced from LNG, India’s total LNG imports are projected to reach 10.5 million tonnes in 2015 and 21.1 million tonnes in 2020. The introduction of imported pipeline gas from Iran by 2025 could meet the requirement in that year. However, if the pipeline does not proceed, India’s total LNG imports would be 30.6 million tonnes in 2025.

» In the high growth scenario, additional gas requirements are projected to be 6.9 billion cubic metres (5.1 million tonnes) in 2015 and 27.1 billion cubic metres (19.8 million tonnes) in 2020. Signifi cant additional gas is still required in 2025 even if the pipeline from Iran eventuates. This implies that India’s total LNG imports in the high growth scenario would be 12.6 million tonnes in 2015 and 27.3 million tonnes in 2020. If the pipeline from Iran does not proceed by 2025, total LNG imports would be 42.7 million tonnes in 2025.

» While existing and planned LNG terminal capacity should be adequate to meet India’s LNG requirements over the medium to longer term, sourcing the additional gas and uncertainty about domestic and imported gas timetables

60

40

20

80

60

40

20

80

bm3 bm3

India

reference case high growth case

2025Iran

pipeline

2025no Iran pipeline

202020152005 2025Iran

pipeline

2025no Iran pipeline

202020152005

pipeline gas from Irangas supply shortfall/additional LNG

actual gas consumptiondomestic gas supply contracted LNG supply

potential gas demand and supplyfig C

7

natural gas in india » abare research report 07.23

are likely to provide a challenge for India in the coming years. It also suggests that new long term LNG supply contracts will be required to meet demand.

» There are currently a number of LNG supply projects in the Asia Pacifi c region, both existing and planned, that have the capacity to meet India’s long term gas requirements. However, the current world LNG market is characterised by a tight supply–demand situation. Hence, competition from major LNG importing countries that are willing to pay high prices may be a constraint to India securing long term LNG supplies.

» Over the period to 2025 there is the potential for Australia to become a more signifi cant supplier of LNG, including to India. A number of LNG projects currently under construction or in the planning stage could add substantial capacity to Australia’s LNG export infrastructure. Other areas of potential future cooperation between Australia and India include research and develop-ment and the transfer of technology (for example, in the development of coal seam methane resources) and investment in upstream and downstream gas sectors in each country.

table C potential gas demand and supply balance – India

2015 2020 2025 2015 2020 2025 billion m3 billion m3 billion m3 Mt Mt Mt

assumed natural gas supplycontracted LNG supply 10.4 10.4 10.4 7.5 7.5 7.5domestic gas supply 43.1 40.6 40.5 31.5 29.6 29.6pipeline gas from Iran 0 0 37.0 0 0 27.0total 53.4 51.0 87.8 39.0 37.2 64.1

projected natural gas consumption – reference case 57.4 69.5 82.4 41.9 50.8 60.2– high growth scenario 60.4 78.1 99.0 44.1 57.0 72.3

gas supply shortfall/possible additional LNG – including pipeline gas from Iran– reference case 4.0 18.6 – 2.9 13.6 –– high growth scenario 6.9 27.1 11.2 5.1 19.8 8.2

gas supply shortfall/possible additional LNG – excluding pipeline gas from Iran– reference case 4.0 18.6 31.6 2.9 13.6 23.1– high growth scenario 6.9 27.1 48.2 5.1 19.8 35.2

total LNG imports – excluding pipeline gas from Iran– reference case 14.4 28.9 41.9 10.5 21.1 30.6 – high growth scenario 17.3 37.4 58.5 12.6 27.3 42.7

8

introduction

India’s economy has undergone signifi cant transformation since a range of struc-tural reforms were undertaken in the 1990s. These reforms included opening the economy to more international trade and investment, abolishing industrial licensing, fl oating the exchange rate, and increasing domestic and foreign private partici-pation in fi nancial markets. The reform process has stimulated strong economic growth in India, with gross domestic product (GDP) expanding at an average rate of 6.1 per cent a year between 1990 and 2006. As a result, India now has the world’s third largest economy (on a purchasing power parity basis).

The expansion in economic output, supported by a large and growing population, has led to a strong rise in energy consumption in India. Primary energy consump-tion (excluding combustible renewables and waste) has increased at an average annual rate of nearly 5.0 per cent since 1990, and India now ranks fi fth in the world in terms of energy consumption. However, unlike many other countries in Asia that have had sustained periods of high economic growth, including China, much of India’s growth has been led by the services sector. This sector is less energy intensive than the industry sector and has moderated the rate of growth in India’s energy requirements. Even so, because of India’s sheer size, the actual expansion in energy consumption has been signifi cant.

India’s energy mix is currently dominated by coal and oil, although the role of natural gas has been increasing. Natural gas consumption grew by 7.4 per cent a year between 1990 and 2005 and accounted for nearly 8 per cent of primary energy consumption in 2005. The main natural gas consumers in India are the electricity generation and fertiliser industries, which account for more than two-thirds of natural gas use. The consumption of natural gas in other industries and in households is relatively small, although growing rapidly.

While demand for natural gas in India is strong, actual consumption has been constrained by the availability of natural gas supplies. India has relatively large natural gas reserves and prospects for further discoveries are good. However, the natural gas market has been dominated by government owned companies selling gas at heavily subsidised prices, reducing incentives for private investment in production facilities. Production of gas from mature domestic fi elds is dwindling, and has resulted in the Indian Government restricting gas supplies to mainly the

1

9

natural gas in india » abare research report 07.23

priority sectors. However, private sector participation in India’s gas market is increasing, which should lead to an increase in domestic gas production. Gas sold privately is based on market prices, creating a complex domestic gas pricing system.

Imports of liquefi ed natural gas (LNG) to India commenced in 2004, after more than a decade of planning. In 2005, LNG imports accounted for around a fi fth of natural gas consumption in India. Two LNG import terminals are operational on the west coast of India, and a third is near completion, although imports are still well under capacity. To date, LNG imports have mainly been sourced from Qatar under a long term contract. But with high natural gas demand, India has also imported a number of spot cargoes of LNG, including from Australia. In 2006, India accounted for 6 per cent of Asia’s total LNG imports.

Natural gas demand is expected to continue to grow strongly in India, fuelled mainly by continued economic and population growth and hence growing demand for electricity. Continued switching to natural gas by fertiliser plants will also be a key driver of demand, particularly given the high price of alternative oil based feedstock. Realising this potential growth will depend on the availability and competitiveness of natural gas supplies, both domestic and imports, and the rate of development of gas infrastructure. Other factors likely to affect the outlook for natural gas demand include the pace of market oriented reforms in gas, elec-tricity and fertiliser markets, including in gas pricing, and an increasing emphasis on energy security and environmental concerns.

There are plans to expand LNG import infrastructure signifi cantly in India, although there is considerable uncertainty about the likely size of India’s future LNG market. The availability and competitiveness of other gas supplies and other fuels and the development of infrastructure will govern the penetration of LNG in India, as will developments in international LNG markets. In the next few years, the outlook for the supply–demand balance in the international LNG market is expected to become increasingly tight, in which case India would need to be willing to pay higher prices to secure additional LNG cargoes. Over the longer term, there is suffi cient potential in the Middle East and the Asia Pacifi c, including in Australia, to supply LNG to India, although many potential projects will require a commitment to long term contracts from buyers to underpin their development.

Natural gas imports via pipeline could also provide an additional source of supply to the Indian market over the longer term. Several options have been under consid-eration for some time, including from Iran. In addition to cost effectiveness, these

10

natural gas in india » abare research report 07.23

projects will have to overcome signifi cant geopolitical issues and the associated development risks that have stalled their development to date.

The key objective in this study is to assess the potential growth in natural gas demand in India and, in particular, the role that LNG could play in that market. A range of projections of energy and natural gas demand in India are presented, refl ecting the uncertainty surrounding prospects for India’s gas market. As well as economic and population growth, other factors that could infl uence the outlook for natural gas in India are examined, including further reforms in gas and end user markets and environmental and energy security policies.

Potential sources of natural gas supply are also assessed, including the capacity to expand domestic gas production, options for natural gas imports by pipeline, and the scope for increasing LNG imports. An update of recent developments in international LNG markets, including the potential for Australia to supply LNG to India, is also provided.

11

energy and natural gas in India

primary energy consumption Primary energy consumption in India has grown rapidly since 1990, at an average rate of 4.8 per cent a year. (The focus in this study is commercial fuels. Unless otherwise noted, references to energy consumption exclude noncommercial fuels, principally combustible renewables and waste.) In 2005, primary energy consumption was 379 million tonnes of oil equivalent, compared with 186 million tonnes of oil equivalent in 1990 (fi gure 1; IEA 2007a). India was the world’s fi fth largest energy user in 2005, behind the United States, China, the Russian Federation and Japan (fi gure 2; IEA 2007a,b).

Driving the growth in energy consumption has been India’s increasing population and strong economic performance. Together these factors have underpinned rising personal incomes and increasing urbanisation. GDP in India grew at an average annual rate of 6.1 per cent between 1990 and 2006, following the implementation of reforms in the early 1990s (box 1).

2

300

100

200

Mtoe

1990 1995 20052000

renewablesnucleargas

oil

coal

total primary energy consumption Indiafig 1

2000

1000

500

1500

MtoeAustraliaIndiaJapanRussian

FederationChinaUnited

States

international comparison of primary energy consumption, 2005fig 2

12

natural gas in india » abare research report 07.23

box 1 recent economic performance in India

The Indian economy has grown strongly since the early 1990s. The strengthening of economic activity has been underpinned by broad based structural reforms imple-mented in 1991. These included liberalisation of tax and tariff policies, the opening of fi fteen industries that had previously been restricted to the public sector, liber-alisation of parts of the fi nancial sector, and an easing of foreign direct investment

restrictions.

Average annual growth in the Indian economy between 1990 and 2004 was around 5.7 per cent. In the three years since then, GDP growth has increased even further, to average 8.9 per cent a year (fi gure 3; IMF 2007a). Higher growth rates have led to strong increases in per person incomes and signifi cant falls in the proportion of the population living in poverty. In addition, there has been steady growth in the share of the population living in urban areas (fi gure 4; World Bank 2007). India’s infl ation performance has also improved, despite sustained capital infl ows and continued increases in fuel prices.

Although India has had several governments since the program of reforms began, each government has made growth and reform a focus of its economic agenda. This continued commitment to reform has encour-aged both Indian and foreign busi-nesses to substantially increase their investment in the economy. From

4000

2000

1000

3000

US$PPP

1992 200720021997

%

2

4

6

8

annual GDP growthGDPper

person

GDP and per person incomeIndia

fig 3

1000

600

400

200

800

million

rural populationurban population

1990 1995 20052000

distribution of India’s population, 2005fig 4

continued...

13

natural gas in india » abare research report 07.23

box 1 recent economic performance in India continued

1992-93 to 2006-07 investment spending grew from 1.8 trillion Indian rupees (US$42.8 billion) to 12.2 trillion Indian rupees (US$182.8 billion) (IMF 2007b). Although the share of foreign direct investment is still low relative to the size of India’s economy, in real terms it has increased by around 27 per cent a year to reach more than US$15.7 billion in 2006-07 (fi gure 5; Ministry of Commerce and Industry 2007).

The services sector has been the main driver of economic growth in India, accounting for more than half of economic output in 2005 and contrib-uting almost three-quarters to overall growth over the period 1990–2005 (fi gure 6; ADB 2006). The growth in the services sector is mainly due to its lower reliance on India’s weak infra-structure (for example, electricity and transport) and its ability to benefi t from technological changes, particularly IT.

After an initial decline in the post-reform period, the industry sector has begun a gradual recovery, supported by growth in both domestic and export demand. The manufacturing sector, in particular, has benefi ted from licensing and trade reforms. Although the share of agriculture in the economy fell from 31 per cent in 1990 to 19 per cent in 2005, the sector provides employment for more than 60 per cent of the workforce. Lifting the growth rate in the agriculture sector is one of the major challenges faced by the Indian Government in ensuring an ongoing reduction in poverty.

2006-07US$b

1994-95

1998-99

2006-07

2002-03

8

4

12

foreign direct investment in India fig 5

services 41%

industry 28%

agriculture 31%

services 54%

industry 27%

agriculture 19%

1990

2005

structure of the Indian economyfig 6

14

natural gas in india » abare research report 07.23

India’s energy intensity, or energy consumption per unit of economic output, declined by 15 per cent between 1990 and 2005, as the services sector, which is less energy intensive than the industry sector, continued to expand its share of the economy (table 1). The current level of energy intensity in India, at 0.1 tonnes of oil equivalent per US$1000, is low relative to other major energy consuming econo-

mies (fi gure 7; IEA 2007a,b).

Energy consumption per person has risen by more than 58 per cent since 1990 to 0.35 tonnes of oil equivalent in 2005. India’s popula-tion expanded by almost a third over the same period, to reach 1.1 billion in 2005 as a result of a historically high fertility rate and a declining mortality rate. Energy consumption per person in India is one of the lowest in the world and is signifi cantly lower than in other major energy consuming countries (fi gure 8; IEA 2007a,b).

0.4

0.2

0.1

0.3

Australia IndiaJapanRussian Federation

ChinaUnited States

toe/2000US$'000

international comparison of energy intensity, 2005fig 7

box 1 recent economic performance in India continued

To sustain high rates of economic growth, India needs to undertake further structural reforms, particularly those leading to improvement in the state of its physical infra-structure, notably roads, ports and electricity. Recognising that infrastructure defi cit is a major barrier to India’s long term growth potential, the government is working to address regulatory and investment issues in order to attract foreign investment into the sector. Another key challenge is to improve education and labour policies to take advantage of India’s imminent demographic dividend — the expansion in the working age population that has the potential to create growth in both the supply of labour and domestic saving. Ongoing effort to continue fi scal consolidation, agricul-tural and trade liberalisation, and reforms in the areas of energy, environment, health and welfare is also required.

Sources: Reserve Bank of India (2007); McKinsey and Co (2007).

15

natural gas in india » abare research report 07.23

fuel mix in primary energy consumption

Coal accounts for the largest share of primary energy consumption in India, at 55 per cent in 2005 (fi gure 9; IEA 2007a). Strong economic growth has led to an increase in coal use in the past few years. Demand for coal grew at an average rate of 4.6 per cent a year from 1990 to 2005 reaching 208 million tonnes of oil equivalent in that year (table 2). India has large reserves of coal, which is its most abundant domestic energy source. The country is the world’s third largest coal producer and consumer after China and the United States (MoC 2006).

Oil is also an important energy source in India, accounting for 34 per cent of primary energy consumption in 2005. Oil consumption grew at an average rate of 4.9 per cent a year between 1990 and 2005 and its share of primary energy consumption remained largely unchanged. The combination of rising oil consump-tion and fairly stable production has left India increasingly dependent on imports.

table 1 major energy and economic indicators – India

annual growth

1990 2000 1990 2000 2005 –2000 –2005 % %

energy consumption a Mtoe 186.3 310.7 379.0 5.2 4.1GDP b US$b 1 406.3 2 402.1 3 362.1 5.5 7.0GDP per person b US$ 1 655.4 2 364.4 3071.5 3.6 5.4population million 849.5 1 015.9 1 094.6 1.8 1.5energy intensity a b toe/US$’000 0.13 0.13 0.11 –0.2 –2.7energy consumption per person a toe 0.22 0.31 0.35 3.4 2.5a Excludes combustible renewables and waste. b In 2000 US dollars on a purchasing power parity basis.Source: IEA (2007a).

6

4

2

Australia IndiaJapanRussian Federation

ChinaUnited States

toe

international comparison of energy consumption per person, 2005fig 8

16

natural gas in india » abare research report 07.23

India’s oil import dependency (imports as a share of consump-tion) increased from 48 per cent in 1990 to 88 per cent in 2005 (IEA 2007a), giving rise to concerns over energy security.

India’s consumption of natural gas rose at an average rate of 7.4 per cent a year from 1990 to 2005, reaching 29 million tonnes of oil equivalent (equivalent to 32 billion cubic metres of gas or 23 million tonnes of LNG) in 2005. This rapid growth, albeit from a small

base, is a result of the increasing importance of natural gas as a fuel in electricity generation, and the production of fertiliser and steel. Until 2004 when LNG imports commenced, natural gas consumption was met entirely from domestic production.

Renewable energy, including hydropower, contributes only a small part of India’s primary energy consumption, at 2 per cent in 2005. Supportive government programs providing subsidies and tax and fi nancial incentives seek to increase the use of renewable energy as a means of achieving a cleaner fuel mix and meeting energy security objectives. Although use of nuclear power has grown steadily, it accounted for only 1 per cent of total primary energy consumption in 2005. The pace of nuclear power development has been constrained by modest domestic uranium resources.

renewablesnucleargasoilcoal

%

1990 1995 20052000

40

20

80

60

fuel mix in primary energy consumption Indiafig 9

table 2 total primary energy consumption – India

1990 2000 2005

Mtoe % Mtoe % Mtoe %coal 106.1 56.9 164.3 52.9 208.0 54.9oil 62.6 33.6 114.4 36.9 128.6 33.9natural gas 9.8 5.3 21.0 6.8 28.8 7.6nuclear 1.6 0.9 4.4 1.4 4.5 1.2renewables a 6.2 3.3 6.5 2.1 9.1 2.4

total 186.3 100.0 310.7 100.0 379.0 100.0a Includes hydro/solar/wind/other. Excludes combustible renewables and waste.Source: IEA (2007a).

17

natural gas in india » abare research report 07.23

electricity generation

Electricity consumption in India grew more rapidly than overall energy use in the period 1990–2005, at 6.1 per cent a year, to reach 699 terawatt hours in 2005. The largest electricity consumers in India are the industry sector, accounting for nearly half of electricity use in 2005, and the residential and services sectors at 22 per cent and 20 per cent respectively (IEA 2007a). Electricity generation is dominated by state owned utilities, which account for almost 90 per cent of India’s total installed capacity. However, the share of private sector generators is growing, particularly in captive or own use electricity genera-tion.

Electricity generated from coal is the largest source of electricity genera-tion in India, at 69 per cent in 2005 (fi gure 10; IEA 2007a). Current coal fi red power plant capacity repre-sents more than half of total electricity generation capacity in the country. The share of hydroelectricity, the next largest source of electricity generation in India, has declined from 25 per cent in 1990 to 14 per cent in 2005, as the growth in thermal generating capacity has outstripped that of hydro (table 3).

Natural gas represented nearly 9 per cent of electricity generation in 2005, compared with 3 per cent in 1990 and was the fastest growing thermal fuel (fi gure 11; IEA 2007a). It is being used in gas turbine and combined cycle gas power plants, which currently account for more than 10 per cent of India’s elec-tricity generation capacity. Oil fi red elec-tricity generation accounted for 4.5 per cent, while nuclear power accounted for 2.5 per cent in 2005. Electricity genera-tion from renewables other than hydro accounted for around 1 per cent of total generation in 2005.

table 3 installed electricity generation capacity, 2004-05 – India

capacity share GW %

coal 67.8 57.2oil 1.2 1.0natural gas 11.9 10.1nuclear 2.8 2.3hydro 30.9 26.1other renewables 3.8 3.2

total 118.4 100.0Source: CEA (2006a).

%

1990 20052000

40

20

80

60

hydro + otherrenewablesnucleargasoilcoal

electricity output, by fuelIndia

fig 10

18

natural gas in india » abare research report 07.23

natural gas consumptionAs discussed above, natural gas consumption in India has grown steadily over recent years, at an average rate of more than 7 per cent a year since 1990. In 2005, consumption of natural gas by end use sectors was 32.0 billion cubic metres (equivalent to 23.4 million tonnes of LNG), compared with 10.9 billion cubic metres (7.9 million tonnes) in 1990 (table 4). These consumption levels do not, however, refl ect the underlying demand for natural gas in India over this period as consumption has been limited by natural gas supplies.

Until recently, all natural gas produced in India was subject to allocation by the Ministry of Petroleum and Natural Gas, on the recommendation of the intermin-

isterial Gas Linkage Committee. Natural gas allocations were based on sectoral priorities, gas availability and potential gas markets in particular regions. At present, a large proportion of natural gas continues to be allo-cated to priority consumers such as the electricity generation and ferti-liser sectors, while the remaining quantity is traded directly between buyers and sellers.

30 40% 10 20

other renewables

natural gas

oil

nuclear

coal

hydro

annual growth in electricity generation, by fuel, 1990–2005 Indiafig 11

table 4 natural gas consumption by end use – India

1990 2000 2005 billion m3 billion m3 billion m3

electricity 3.8 10.3 14.2fertiliser 5.9 9.8 8.3other industries 1.1 2.7 8.0residential 0.0 0.3 0.7other 0.1 0.2 0.9

total 10.9 23.3 32.0– LNG equivalent (million tonnes) 8.0 17.0 23.4Source: IEA (2007a).

19

natural gas in india » abare research report 07.23

gas consumption, by sector

Electricity generation currently accounts for almost half of India’s natural gas consumption. Natural gas use by electricity utilities grew at an average rate of over 9 per cent a year, from 3.8 billion cubic metres in 1990 to 14.2 billion cubic metres in 2005 (table 4 and fi gure 12; IEA 2007a).

Existing gas fi red power plants in India require more than 19 billion cubic metres of natural gas a year to operate at full capacity. However, as a result of diffi culties in securing natural gas supply, gas fi red power plants have been running at less than full capacity, switching to higher cost liquid fuels such as naphtha where feasible.

The fertiliser sector is the second largest consumer of natural gas in India, accounting for around a quarter of natural gas consumption in 2005. Demand for natural gas from the fertiliser industry grew at an average annual rate of 2 per cent from 1990, to reach 8.3 billion cubic metres in 2005 (IEA 2007a). The expansion in the use of natural gas by the fertiliser industry refl ects the high priority placed by the government on boosting agricultural production through greater fertiliser use.

India currently produces nitrogenous (mainly urea) and phosphatic fertilisers, with natural gas used as a feedstock in urea production. During 2004-05, natural gas based fertiliser production accounted for 66 per cent of total fertiliser production. Production based on naphtha, fuel oil and low sulfur heavy stock (a residual fuel processed from crude oil that can be used in the place of fuel oil) constituted the remaining 34 per cent (MoPNG 2006a). Gas prices for both electricity generation and fertiliser production are partly subsidised by the government.

Other industrial users, including iron and steel, glass, ceramic and elec-tronics manufacturers are rapidly increasing their share of natural gas consumption. Gas consumption in the industry sector has grown at an average rate of 14 per cent a year, from 1.1 billion cubic metres in 1990 to 8.0 billion cubic metres in 2005. There has been substitution away

30

10

20

25

5

15

billionm3

1990 1995 20052000

other

other industry

fertiliser

electricity

residential

natural gas consumption, by end use Indiafig 12

20

natural gas in india » abare research report 07.23

from coal in this sector toward electricity and, to a lesser extent, natural gas (fi gure 13; IEA 2007a).

While small in absolute terms, natural gas use in the residential sector has grown strongly, at an average rate of 20 per cent a year since 1990. Household natural gas consumption was virtually nonexistent in 1990, but rose to more than 0.7 billion cubic metres in 2005. Rapid economic growth and rising incomes have led to a shift in consumer preferences from coal and noncommercial fuels to more convenient and clean fuels such as petroleum products and electricity (see box 2). Natural gas constitutes a marginal share in the residential fuel mix, although use of natural gas has been growing rapidly in recent years following an expansion in gas supply infrastructure.

city gas

Natural gas is supplied to residential, commercial and industrial consumers via underground pipeline distribution networks within metropolitan areas. Residential consumers use city gas for cooking, water and space heating, and air condi-tioning, while commercial and industrial consumers also use gas for steam raising and power generation, dryers, furnaces and boilers.

City gas distribution systems in India are not well developed, primarily as a result of limited supplies of natural gas and the allocation of gas to priority sectors such as electricity generation and fertilisers. However, city gas distribution has been

%

1990 1990 20052005 20002000industrial residential

40

20

80

60

electricitynatural gaspetroleum productscoal

energy consumption in key sectors, by fuel Indiafig 13

21

natural gas in india » abare research report 07.23

box 2 household consumption of noncommercial fuels in India

Indian households have traditionally relied on noncommercial or biomass fuels, including fi rewood, crop residue and animal waste, as a source of energy, primarily for cooking. In 2004, 69 per cent of the Indian population, or 740 million people, are estimated to have relied on biomass resources as their primary fuel for cooking, predominantly in rural households (IEA 2006a, 2007a).

If noncommercial fuels are included in the residential fuel mix, they constitute the largest share of residential energy consumption in India, at 124 million tonnes of oil equiva-lent in 2005, or 79 per cent of energy consumption in the sector. While demand for noncommercial fuels has traditionally been strong, their share has declined from 84 per cent in 1990 (fi gure 14, which includes combustible renewables and waste; IEA 2007a). However, there are some uncertainties over the reliability of these data, given the informal nature of the sector.

In the past, the Indian Government has initiated various measures to promote the use of cleaner fuels in the residen-tial sector, primarily by subsidising petroleum products such as kerosene and liquefi ed petroleum gas. This approach had limited success, particu-larly in lower income households, which still rely predominantly on noncommercial fuels. Abundant supplies of biomass fuels at zero cost, together with low afford-ability and poor delivery infrastructure for commercial fuels have inhibited and will continue to inhibit wider penetration of modern fuels in the residential sector.

Some reluctance to discontinue cooking with fi rewood may also refl ect taste prefer-ences and the familiarity of cooking with traditional technologies. For instance, many wealthy households in India retain a wood stove for baking traditional breads. As incomes increase and fuel options widen, the fuel mix may change, but wood is unlikely to be entirely excluded (IEA 2006a).

%

1990 20052000

40

20

80

60

electricitynatural gaspetroleum productscoalcombustible renewables and waste

energy consumption in the residential sector, by fuel Indiafig 14

22

natural gas in india » abare research report 07.23

growing rapidly over the past few years, from two cities — Delhi and Mumbai — in 2002-03 to ten cities in 2005-06 across the western, northern and southern regions of the country (MoPNG 2006a).

The largest city gas distribution networks currently operate in the cities of Mumbai and Delhi, and the state of Gujarat (cities of Surat, Bharuch and Ankleshwar), with more than 500 000 consumers in various sectors. City gas sales grew to almost 2 billion cubic metres in 2005-06, compared with 1.6 billion cubic metres the previous year, an increase of 22 per cent (table 5).

compressed natural gas

Compressed natural gas (CNG) is used as an automotive fuel in a limited number of cities in India. The initially sluggish growth in CNG demand from the automotive sector has picked up as a result of recent directives by the Supreme Court of India to control air pollution caused by vehicular traffi c through the promotion of CNG use. The directives included expansion of CNG infrastructure, conversion of buses, taxis and auto-rickshaws from liquid fuel to CNG, and allocation of natural gas to the transport sector in Delhi and Mumbai.

In 2003, the Supreme Court ordered the government to draw up plans for the introduction of clean fuels such as CNG in eleven cities apart from Delhi and Mumbai — Kolkata, Chennai, Bangalore, Hyderabad, Ahmedabad, Sholapur, Surat, Lucknow, Kanpur, Agra and Pune (De 2004).

table 5 city gas consumer base in India

sales volume

industrial commercial residential total 2005-06 a 2004-05 a no. no. no. no. million m3 million m3

MGL (Mumbai) 40 819 258 433 259 292 455 413IGL (Delhi) 47 215 46 727 46 989 445 405GGCL (Gujarat) 750 2 500 200 000 203 250 1 088 813

total 837 3 534 505 160 509 531 1 988 1 631a Includes CNG. MGL = Mahanagar Gas Ltd; IGL = Indraprastha Gas Ltd; GGCL = Gujarat Gas Company Ltd.Sources: MGL (2007); IGL (2007); GGCL (2007).

23

natural gas in india » abare research report 07.23

CNG sales have grown recently at an average rate of 61 per cent a year, from around 69 million cubic metres in 2000-01 to around 690 million cubic metres in 2005-06 (MoPNG 2006a). In 2005-06, the CNG distribution network included 281 stations in Delhi, Mumbai and Gujarat, with CNG powering more than 300 000 vehicles in these cities (table 6; MoPNG 2006a).

natural gas supply

domestic gas reserves

India’s proved natural gas reserves have increased from 0.7 trillion cubic metres in 1990 to more than 1 trillion cubic metres in 2006. This represents less than 1 per cent of total proved gas reserves in the world. These reserves can sustain the current level of production for around 34 years (BP 2007). Around 70 per cent of India’s proved gas reserves are located in offshore basins (map 1; IEA 2007c).

The recent discovery of natural gas in the Krishna–Godavari basin and neigh-bouring areas, off the east coast of India, was the biggest gas fi nd since the Bombay High (now Mumbai High) discovery on India’s western offshore territory in the 1970s. Reliance Industries Ltd (RIL) was the fi rst to announce a gas discovery in the Krishna–Godavari basin in 2002, followed by a number of discoveries by Gujarat State Petroleum Corporation Ltd (GSPC) and Oil and Natural Gas Corporation Ltd (ONGC). Estimated gas reserves of these combined discoveries, yet to be certifi ed, exceed 1.5 trillion cubic metres (IEA 2006a).

Substantial parts of India’s territory remain unexplored, suggesting potential for further growth in domestic gas reserves from future gas discoveries and more accu-rate estimation of existing reserves.

table 6 distribution and consumption of compressed natural gas in India, 2005-06

Delhi Mumbai Gujarat total

CNG stations units 146 120 15 281CNG vehicles units 106 483 170 003 33 403 309 889price Indian rupees/kg 18.00 20.19–21.30 22.55–23.41 consumption billion m3 a year 0.47 0.29 na na Not available.Source: MoPNG (2006a).

24

natural gas in india » abare research report 07.23

natural gas reserves Indiamap 1

gas and oil field

gas and oil basin

gas field

BANGLADESH

BHUTANNEPAL

Mumbaioffshore

Krishna–Godavari Basin

25

natural gas in india » abare research report 07.23

domestic gas production

Natural gas production in India increased at an average rate of 4 per cent a year, from 11.9 billion cubic metres in 1990 to 28.8 billion cubic metres in 2005 (fi gure 15; IEA 2007d), although estimates of India’s gas production vary between sources. Around 70 per cent of domestic produc-tion comes from offshore fi elds, operated by ONGC and private sector companies/joint ventures. The Mumbai High fi elds account for almost three-quarters of India’s offshore gas production (table 7).

20

10

30

1990 200520001995

billion m3

imports

domestic gas production

natural gas supply India fig 15

table 7 natural gas production – India

1990-91 2000-01 2004-05 2005-06 s billion m3 billion m3 billion m3 billion m3

onshore Gujarat 1.70 3.15 3.71 3.83Assam/Nagaland 2.01 2.20 2.25 2.41Arunachal Pradesh 0.03 0.03 0.04 0.05Tripura 0.07 0.38 0.50 0.48Tamil Nadu 0.06 0.20 0.68 0.91Andhra Pradesh 0.05 1.60 1.71 1.66Rajasthan nil 0.16 0.21 0.24

total onshore 3.92 7.73 9.09 9.58

of which OIL 1.52 1.86 2.01 2.27ONGC 2.40 5.56 5.66 5.75joint ventures/private nil 0.31 1.43 1.56

offshore ONGC (Mumbai High) 14.08 18.47 17.31 16.82joint ventures/private nil 3.29 5.36 5.80

total offshore 14.08 21.75 22.67 22.62

grand total 18.00 29.48 31.76 32.20s Estimated. Note: These data for total gas production differ from IEA (2007a,d). For consistency, IEA data have been used throughout this report, however, these data have been included to provide state based data that are not available from the IEA.Source: MoPNG (2006a).

26

natural gas in india » abare research report 07.23

Until the opening up of the oil and gas sector to private participation in the late 1990s, natural gas production in India was dominated by two national oil compa-nies, ONGC and OIL (box 3). These companies still account for the largest share of domestic gas production, at 77 per cent in 2005-06. Private companies/joint ventures, which make up the rest of India’s gas production, have increased their share rapidly from nil in 1990-91 to nearly 23 per cent in 2005-06.

Existing onshore and offshore gas fi elds operated by national oil companies are facing declining production over the medium term, which places an increased emphasis on identifying new sources of gas supply, either domestic or imported.

LNG imports

India has placed increasing focus on LNG imports as a potential means of meeting domestic natural gas demand. LNG imports have risen steadily since the commis-sioning of India’s fi rst LNG terminal at Dahej in the State of Gujarat in early 2004. From just under 2 million tonnes that year, LNG imports reached more than 6 million tonnes in 2006. In the fi rst half of 2007, LNG imports by India were 4.1 million tonnes, a rise of more than 66 per cent compared with the fi rst half of 2006.

While Qatar was the sole supplier of LNG to India in 2004 and remains the largest LNG supplier at present, the range of suppliers is becoming increasingly diverse. In 2005, India imported LNG from Australia and Oman. Additional

supplies were sourced from Egypt, Trinidad and Tobago, Abu Dhabi, Malaysia and Algeria in 2006 (fi gure 16; FGE 2007a).

At present, India has two opera-tional LNG import terminals — Dahej and Hazira — in Gujarat state, while a third terminal at Dabhol in the state of Maharashtra is under construction (table 8). There are several other proposed LNG terminals in various stages of plan-ning. These are discussed further in chapter 5.

Mt

200620052004

6

4

2

Australia

otherEgypt

OmanQatar

LNG import capacity

LNG imports, by source countryIndia

fig 16

27

natural gas in india » abare research report 07.23

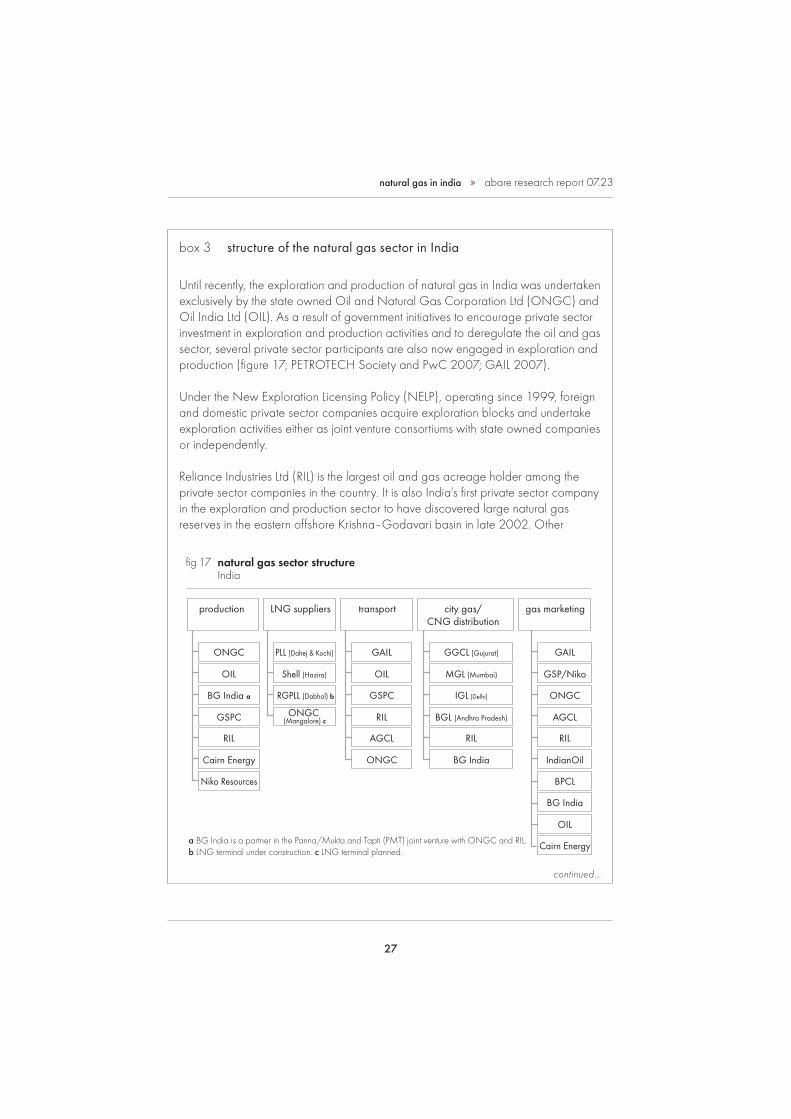

box 3 structure of the natural gas sector in India

Until recently, the exploration and production of natural gas in India was undertaken exclusively by the state owned Oil and Natural Gas Corporation Ltd (ONGC) and Oil India Ltd (OIL). As a result of government initiatives to encourage private sector investment in exploration and production activities and to deregulate the oil and gas sector, several private sector participants are also now engaged in exploration and production (fi gure 17; PETROTECH Society and PwC 2007; GAIL 2007).

Under the New Exploration Licensing Policy (NELP), operating since 1999, foreign and domestic private sector companies acquire exploration blocks and undertake exploration activities either as joint venture consortiums with state owned companies or independently.

Reliance Industries Ltd (RIL) is the largest oil and gas acreage holder among the private sector companies in the country. It is also India’s fi rst private sector company in the exploration and production sector to have discovered large natural gas reserves in the eastern offshore Krishna–Godavari basin in late 2002. Other

continued...

natural gas sector structure Indiafig 17

production LNG suppliers transport city gas/CNG distribution

gas marketing

GAIL GAILONGC PLL (Dahej & Kochi) GGCL (Gujurat)

OIL GSP/NikoOIL Shell (Hazira) MGL (Mumbai)

GSPC ONGCBG India a RGPLL (Dabhol) b IGL (Delhi)

RIL AGCLGSPC ONGC(Mangalore) c BGL (Andhra Pradesh)

AGCL RILRIL RIL

ONGC IndianOilCairn Energy BG India

BPCLNiko Resources

BG India

OIL

Cairn Energya BG India is a partner in the Panna/Mukta and Tapti (PMT) joint venture with ONGC and RIL. b LNG terminal under construction. c LNG terminal planned.

28

natural gas in india » abare research report 07.23

box 3 structure of the natural gas sector in India continued

private sector participants in exploration and production activities include BG India, Niko Resources and Cairn Energy.

Pipeline gas transport is primarily undertaken by state owned GAIL (India) Ltd, formerly the Gas Authority of India Ltd. GAIL is India’s largest gas transmission and marketing company, with a high pressure pipeline network of around 5600 kilome-tres. The largest pipeline network, Hazira–Vijaipur–Jagdishpur, with a total length of more than 2800 kilometres, covers the states of Gujarat, Rajasthan, Madhya Pradesh, Uttar Pradesh, Haryana and Delhi in the north west of the country. The 610 kilometre long Dahej–Vijaipur pipeline owned by GAIL transports regasifi ed LNG received at the Dahej terminal operated by Petronet LNG Ltd (PLL).

GAIL also has regional gas distribution grids, totalling around 1 800 kilometres of varying length and diameter in Ahmedabad, Assam, Baroda, Cauvery basin, Hazira, Krishna-Godavari basin, Mumbai, Rajasthan and Tripura. Other regional natural gas pipeline operators include Gujarat Gas Company Ltd (GGCL) and Gujarat State Petronet Ltd (GSPL) in Gujarat, Assam Gas Company Ltd (AGCL) and Tripura Natural Gas Company Ltd (TNGCL) in Assam and Tripura respectively. Indraprastha Gas Ltd (IGL) in Delhi, Mahanagar Gas Ltd (MGL) in Mumbai and GGCL in Gujarat are also developing city gas distribution networks for the supply of compressed natural gas (CNG) and city gas in their respective areas.

The gas produced by ONGC and part of the gas from joint venture consortiums, such as the Panna/Mukta and Tapti joint venture formed by BG India, ONGC and RIL, is marketed by GAIL. The gas produced by OIL is marketed by OIL itself, except in Rajasthan where GAIL markets its gas. Gas produced by Cairn Energy and Gujarat State Petroleum Corporation Ltd (GSPC) is being sold directly by the respective companies.

Companies operating India’s LNG import facilities include Petronet LNG Ltd (PLL) and Shell Hazira. PLL, the operator of India’s fi rst LNG receiving and regasifi cation terminal at Dahej, Gujarat, is comprised of four state owned oil and gas companies — GAIL, ONGC, Indian Oil Corporation Ltd (IndianOil) and Bharat Petroleum Corporation Ltd (BPCL). The Hazira LNG Terminal and Port is partnered by Shell Gas BV and Total Gaz Electricité Holdings France, representing two of the largest private LNG suppliers in the world.

continued...

29

natural gas in india » abare research report 07.23

Dahej terminal, Gujarat

Petronet LNG Ltd (PLL) was formed by the Indian Government as a joint venture to set up LNG terminals and import LNG. GAIL, ONGC, Indian Oil Corporation Ltd (IndianOil) and Bharat Petroleum Corporation Ltd (BPCL) are the key partners and promoters of PLL. The terminal at Dahej has an annual design capacity of 6.5 million tonnes of LNG. The company plans to expand the capacity to 10 million tonnes of LNG a year by the end of the decade.

table 8 existing LNG terminals – India

project commis- potential location developer capacity supplier sioned expansion Mt pa

Dahej, Petronet LNG Ltd (PLL) 6.5 a RasGas, Qatar; 2004 10 million tonnes a Gujarat spot cargoes year by 2010

Hazira, Shell Hazira LNG 2.4 spot cargoes 2005 planned expansion Gujarat Terminal and Port to 5–10 million tonnes a yearDabhol, Ratnagiri Gas and 5.0 yet to be delayed by Maharashtra Power Private Ltd fi nalised various issues, (RGPPL) expected 2009 a Debottlenecking increased capacity from 5 million tonnes a year to 6.5 million tonnes a year in early 2007.Sources: PLL (2007a); Shell (2007).

box 3 structure of the natural gas sector in India continued

Ratnagiri Gas and Power Private Ltd (RGPPL) is a special purpose organisation that has been incorporated to take over assets and revive the former Dabhol Power Company project in the state of Maharashtra. The Dabhol project is an integrated facility consisting of a gas fi red power plant and an associated LNG receiving and regasifi cation terminal. The RGPPL shareholders include GAIL, state owned National Thermal Power Corporation Ltd (NTPC), Maharashtra State Electricity Board Holding Co Ltd (MSEB) and Indian fi nancial institutions.

30

natural gas in india » abare research report 07.23

PLL has a long term sale and purchase agreement with Ras Laffan LNG Company Ltd (RasGas) for the phased supply of 7.5 million tonnes of LNG a year from Qatar to India, starting in 2004 and expiring in 2029. The fi rst phase of 5 million tonnes of LNG a year is already in progress, while the second phase of an additional 2.5 million tonnes of LNG a year is due to begin in 2009. GAIL, the sole transporter of the regasifi ed LNG, has upgraded the Hazira–Vijaipur–Jagdishpur (HVJ) pipeline from Dahej to Vijaipur to synchronise with the LNG terminal.

GAIL, IndianOil and BPCL market the regasifi ed LNG to their respective customers. The gas is sold to existing industrial customers requiring increased volumes of gas or to those who currently use liquid fuels such as naphtha or fuel oil in their manu-facturing process. These customers are located in the states of Gujarat, Mahar-ashtra and along the HVJ pipeline.

Hazira terminal, Gujarat

The Hazira terminal in the state of Gujarat is partnered by Shell Gas BV and Total Gaz Electricité Holdings France. The fi rst LNG shipment, sourced from Australia, arrived at the terminal in April 2005. The Hazira terminal has an annual capacity of 2.4 million tonnes, which can be increased to 5–10 million tonnes a year, if required. To date the Hazira LNG terminal has been operating well below capacity. Terminal partners source LNG from various projects around the world as required, rather than on a long term contract basis.

The Hazira LNG terminal has access to existing pipeline infrastructure to transport and deliver gas to customers. A pipeline from Hazira to Mora has been laid to connect to the Gujarat grid operated by Gujarat State Petronet Ltd (GSPL). The terminal is also connected to GAIL’s pipeline network, and Shell and GAIL have initialled a broad framework of agreement to deliver gas from the Hazira terminal to GAIL’s customers.

Dabhol terminal, Maharashtra

Ratnagiri Gas and Power Private Ltd (RGPPL) was set up in 2005 under the Indian Government’s restructuring plan to take over the assets and revive the former Dabhol Power Company project. The project includes a 2184 megawatt gas fi red power plant and a linked LNG import and regasifi cation facility. The Dabhol power project was shut down in May 2001 following a power tariff dispute between its initial promoter, Enron Power Corporation, and the only customer, Maharashtra State Electricity Board Holding Co Ltd (MSEB).

31

natural gas in india » abare research report 07.23

RGPPL is now a wholly owned Indian project with GAIL, National Thermal Power Corporation Ltd (NTPC), MSEB and Indian fi nancial institutions as the main share-holders. GAIL was given the mandate to revive the LNG facility, while NTPC was to revive the associated power plant. The power plant resumed operation in April 2006 using naphtha as fuel in the absence of gas supply. In July 2006 the power plant was shut down again as a result of the high cost of naphtha supplies. The plant restarted in late August 2007, using imported LNG (Platts 2007a).

The Dabhol LNG import terminal is planned to have an annual capacity of 5 million tonnes of LNG, of which 2.1 million tonnes is required for the power plant, with the remaining quantity available for supply to various consumers. Commis-sioning of the terminal has been delayed, primarily as a result of signifi cant cost overruns, and is now expected to occur toward 2009 after the completion of associated facilities.

In the absence of long term supply contracts, RGPPL has entered into a medium term arrangement with PLL for the supply of spot LNG to be delivered at PLL’s Dahej terminal and transported to Dabhol via the recently completed Dahej–Dabhol pipeline. PLL signed a short term LNG import agreement in mid-2007 with Qatari supplier Rasgas to meet RGPPL requirements and is also sourcing cargoes from the spot market (Platts 2007b).

gas supply infrastructure

India’s natural gas pipeline network is made up of high pressure interstate transmis-sion pipelines, located mostly in the north western part of India, and regional gas distribution grids in western, southern and eastern regions of the country. India currently does not have any major storage facilities for natural gas.

The total length of the gas transmission system is 6300 kilometres, of which more than 5600 kilometres are operated by GAIL. Other gas pipeline operators include Gujarat Gas Company Ltd and Gujarat State Petronet Ltd in Gujarat, Assam Gas Company Ltd and Tripura Natural Gas Company Ltd in Assam and Tripura respec-tively. At the core of India’s transmission system is the Hazira–Vijaipur–Jagdishpur (HVJ) pipeline, which carries natural gas from the western offshore fi elds to end users in Gujarat, Madhya Pradesh, Rajasthan, Uttar Pradesh, Haryana and Delhi. The HVJ pipeline is more than 2800 kilometres long, and has a design capacity of 12.2 billion cubic metres a year (equivalent to 8.9 million tonnes of LNG) (MoPNG 2006a; GAIL 2007).

32

natural gas in india » abare research report 07.23

GAIL also operates more than 1800 kilometres of regional gas pipelines in Ahmedabad, Assam, Baroda, Cauvery basin, Hazira, Krishna–Godavari basin, Mumbai, Rajasthan and Tripura. These pipelines are smaller and vary in length from less than 1 kilometre up to 55 kilometres. In addition, there are a number of city gas distribution grids, which supply gas to households, commercial and indus-trial users, and the transport sector.

While GAIL is the largest gas transmission and distribution company in India, it also provides access to third parties for the transmission of natural gas. Currently, transmission tariffs on the interstate gas pipelines — HVJ and Dahej–Vijaipur — are regulated, while transmission tariffs on the regional gas pipelines and LPG pipe-lines are not regulated.

The total capacity of the transmission network is 51.1 billion cubic metres a year (equivalent to 37.3 million tonnes of LNG). The amount of gas transmitted via GAIL’s pipeline network has increased by almost 30 per cent in recent years, from 22.5 billion cubic metres in 2001-02 to 28.8 billion cubic metres in 2005-06 (GAIL 2006).

GAIL has drawn up major plans for the expansion of the interstate gas transmission grid, which would allow expansion of India’s gas supply infrastructure and provide connections between various gas sources and geographically dispersed markets (map 2; GAIL 2006). The proposed grid would add a further 8400 kilometres of natural gas transmission pipelines in line with the emergence of gas sources on the west and east coasts of the country, and require investment of approximately US$5 billion. Several private companies also have plans to construct interstate pipelines, including in Andhra Pradesh, Maharashtra, Gujarat, Goa, Madhya Pradesh, Orissa, West Bengal and Tamil Nadu (MoPNG 2006a).

The integrated gas pipeline network would also enable the development of city gas distribution projects in the country by catering to a large number of cities and towns falling in the catchment area of the existing and future pipeline networks. Recent developments in downstream petroleum and natural gas regulation, such as the enactment of the Petroleum and Natural Gas Regulatory Board Act in 2006 and the formulation of the Gas Pipeline Policy, are expected to provide further impetus for the expansion of gas supply infrastructure in the country. The regulatory framework in the natural gas sector is discussed further in the following chapter.

33

natural gas in india » abare research report 07.23

gas pricingUntil recently, all natural gas produced in India was subject to an administered pricing mechanism, based on subsidised consumer prices. After an attempt to bring gas prices to parity with import prices of alternative fuels in the late 1990s proved unsuccessful, the Indian Government has set gas prices on an ad hoc basis (see box 4 on the evolution of gas pricing in India). At present, India has a mix of administered and market gas prices that vary across consumer segments and depend on their eligibility for administered gas pricing.

Jaipur

Amritsar

New Delhi

Chandigarh

natural gas infrastructure Indiamap 2

Dahej

Hazira

Kochi

Kolkata

Chennai

existing pipelines

proposed pipelines

existing LNG import terminals

under construction/planned LNG import terminals

BangaloreMangalore

Dabhol

Pune

Hyderabad Kakinada

BANGLADESH

BHUTANNEPAL

Kota

Ahmadabad

Jamnagar

Vijaipur

Mumbai

Jagdishpur

Bhatinda

Srinagar

Bhopal

Patna

34

natural gas in india » abare research report 07.23

box 4 evolution of gas pricing in India

Historically, natural gas prices in India have been regulated using a variety of mecha-nisms. Until the 1970s, gas prices were based on recommendations made by expert committees. During the 1970s and most of the 1980s, prices were determined by the monopoly gas producers — ONGC and OIL — on a negotiated basis. Since 1987, the government has set uniform gas prices across the country, with an exception of the north east region, which receives gas at concessional prices.

In 1997, natural gas prices were pegged to the import parity price of a basket of internationally traded fuel oils. Prices were set to increase progressively as a proportion of the fuel oil basket price, from 55 per cent in 1997-98 to 85 per cent in 2000-01. To curb any major fl uctuations in gas prices, the government set a price band, with a fl oor price of 2150 Indian rupees per thousand cubic metres and a ceiling price of 2850 Indian rupees per thousand cubic metres. However, in 1999-2000 gas prices reached the ceiling price, as international fuel oil prices continued to increase. The process of raising gas prices to achieve full import parity was stalled and gas prices remained at this ceiling until 2005-06.

In July 2005, the gas price for priority sectors — electricity generation and fertiliser sectors and other users specifi ed on occasion by the government or court — was revised upwards to 3200 Indian rupees per thousand cubic metres. The price of gas in the north east region was pegged at 60 per cent of the revised price. However, the price of gas for consumers in all other sectors more than doubled to 6893 Indian rupees per thousand cubic metres (table 9).

Administered gas prices were revised further in 2006, with prices for nonpriority sectors such as steel raised by around 23 per cent, and by 20 per cent for city gas distribution companies and customers consuming less than 18.25 million cubic metres a year. The priority sectors continue to pay 3200 Indian rupees per thousand cubic metres. Further rises in gas prices are anticipated once the Tariff Commission under the Ministry of Commerce and Industry makes recommendations on prices for gas sold under the administered pricing mechanism.