prospects and challenges for economic growth in the south caucasus and other transition economies c....

TRANSCRIPT

Prospects and Challenges for Economic Growth in the South Caucasus and other Transition

Economies

C. Felipe Jaramillo The World Bank

Tbilisi, Georgia, February 1, 2007

1. Growth record since 1990

2. Recent trends in Transition Economies: 2005-06

3. The South Caucasus Economies

ECA – Real GDP Growth (%)

ECA – Index of Real GDP (1990=100)

South CaucasusIndex of Real GDP (1990=100)

20

40

60

80

100

120

140

160

180

19901991

19921993

19941995

19961997

19981999

20002001

20022003

20042005

2006p

2007f

A rmen ia A zerbaijan Georg ia CIS

GEORGIA

ARM

AZE

CIS

Transition, reforms and growth

Substantial progress was achieved by CEB -- markets have responded favourably to previous reforms.

Reform in CIS countries has been slower and less ambitious – but growth has picked up in recent years in reforming countries (and oil exporters)

With a positive external environment, most countries have enjoyed strong growth in 2004-06, leading in some cases to “reform complacency”

Average Reform Indicator 1990, 2000, 2006

0.00

1.00

2.00

3.00

4.00

CIS Other transitiooncountries

1990

2000

2006

Source: EBRD

2. Recent Economic Trends in Transition Economies – EU 8+2

EU 8: Poland, Czech, Hungary, Eslovenia, Slovakia, Latvia, Estonia, Lithuania+2: Romania, Bulgaria www.worldbank.org/eca

Short-term performance in EU8+2 remains very positive

External environment – remained broadly favorable (some slowdown, but falling oil prices)Financial markets in the region recovered firmly from the May-June 2006 turmoil supported by overall strong fundamentals Capital inflows translated into strong appreciation trendsBullish stock markets -- record highsOutlook: remains positive, with some EU8+2 countries vulnerable to sudden corrections

Growth gained further steam

0

2

4

6

8

10

12

14

16

CZ EE HU LV LT PL SK SI BG RO

1Q 06 2Q 06

3Q 06 2005

Rea

l GD

P G

row

th (

% y

oy)

Strong growth momentum maintained in 3QIncreasingly driven by vibrant domestic demand

Stimulated by strong credit expansion and wage growth (the Baltics and Romania/Bulgaria)

Growth likely to slow down in 2007 in line with euro-zone and closing output gaps

External imbalances mount…

-30-25-20-15-10-505

1015202530

3Q

05

4Q

05

1Q

06

2Q

06

3Q

06

3Q

05

4Q

05

1Q

06

2Q

06

3Q

06

3Q

05

4Q

05

1Q

06

2Q

06

3Q

06

3Q

05

4Q

05

1Q

06

2Q

06

3Q

06

3Q

05

4Q

05

1Q

06

2Q

06

3Q

06

Trade in goods, net Trade in services, net Income, netCurrent transfers, net Current account balance

EE LV LT BG RO

Current account balances have worsened in most economies (except HUN and POL) --- on the back of widening trade deficits exacerbated by real exchange rate appreciationThe largest external imbalances (the Baltics, Slovakia and Bulgaria/Romania) are generated in the private sector translating into booming private sector credit

Cu

rren

t ac

cou

nt

def

icit

(%

of

GD

P)

Increasing inflationary pressures

Inflationary pressures intensified in most countries Related to rapid output growth and closing of output gaps, labor market tightening, rapid credit expansion and pro-cyclical fiscal policiesIn response to increasing pressures, somewhat balanced by appreciation trends, most EU8+2 followed the ECB tightening cycle

0

2

4

6

8

10

2002

2004

2005

2006*

2002

2004

2005

2006*

2002

2004

2005

2006*

2002

2004

2005

2006*

2002

2004

2005

2006*

2002

2004

2005

2006*

2002

2004

2005

2006*

2002

2004

2005

2006*

2003

2004

2005

2006*

Contribution of regulated prices measures Contribution of market prices increase

CZ HU SK SI PL LV LT EE BG

Contribution to CPI inflation (perc. points)

Fiscal consolidation rather slowSizeable increase in fiscal deficit in 2006 projected in Hungary (to about 10% of GDP) and Slovakia

Structural fiscal balances deteriorated in most countries (except Poland and Bulgaria)

Fiscal position likely to worsen in 2007 in the Czech Republic, Estonia, Bulgaria and Romania. Major adjustment only in Hungary

Concern: Fiscal policy may be exacerbating the imbalances of the current expansion cycle

Structural reforms largely stalled

Some further progress on privatization, but strategic sectors remain state-controlledLittle progress on further enhancing labor market flexibility (labor taxes, mobility) Limited progress in other areas of business environment, incl. the functioning of the judiciary in the newest member states Public finance reforms stalled (but ambitious plans in Hungary)Governance remains a problem in most countries

3. What is happening in the South Caucasus?

Georgia

Strong growth performance in recent years explained by pickup in reforms, solid fiscal management and growing positive market sentiment

Annual GDP Growth Rate 2003-2006

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2003 2004 2005 2006

Strong fiscal mgmt – fast revenue growth

Georgia: tax revenues, 2000-2006

-

1.0

2.0

3.0

4.0

2000 2001 2002 2003 2004 2005 2006p

12%

14%

16%

18%

20%

22%

Tax revenues, current bln GEL (left scale)

Tax revenues as % of GDP (right scale)

Strong pickup in FDI – beyond pipelineGeorgia: FDI inflows, 2000-2006

0

200

400

600

800

1,000

2000 2001 2002 2003 2004 2005 2006

mill

ion

$

Non-oil FDI Oil FDI

And more diversified FDI sourcesGeorgia: Cumulative FDI inflows by source, 2000-2006 (% )

15%

14%

9%

9%

7%

6%

6%

5%

5%

4%20%

0% 5% 10% 15% 20%

UK

USA

Azerbaijan

Turkey

Kazakhstan

Russia

Norway

Cyprus

Italy

France

Others

Has weathered well export restrictionsGeorgia: Export Trends, 2004-2006

0

5

10

15

20

25

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2004 2005 2006

%

0

50

100

150

200

250

300

Mill

ion

$

Export Total Russia's share in Exports

Georgia – emerging challenges

Some signs of overheating (inflation pick up, growing external imbalances, rapid credit growth)

Challenge of continuing to boost trade and diversify products and partners

Georgia: Inflation and CAB 2003-2006

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

Inflation (annual p.a.) CAB (% of GDP)

2003 2004 2005 2006

Armenia

Impressive fifth year of double digit growth – fueled by continued reforms and strong macro-fiscal management Fueled by private sector – consumption and investment (FDI and remittances)

Annual GDP Growth rate 2003-2006

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2003 2004 2005 2006

Armenia – emerging challenges

Rapid credit growth from a small base

Appreciation pressures and external competitiveness challenge

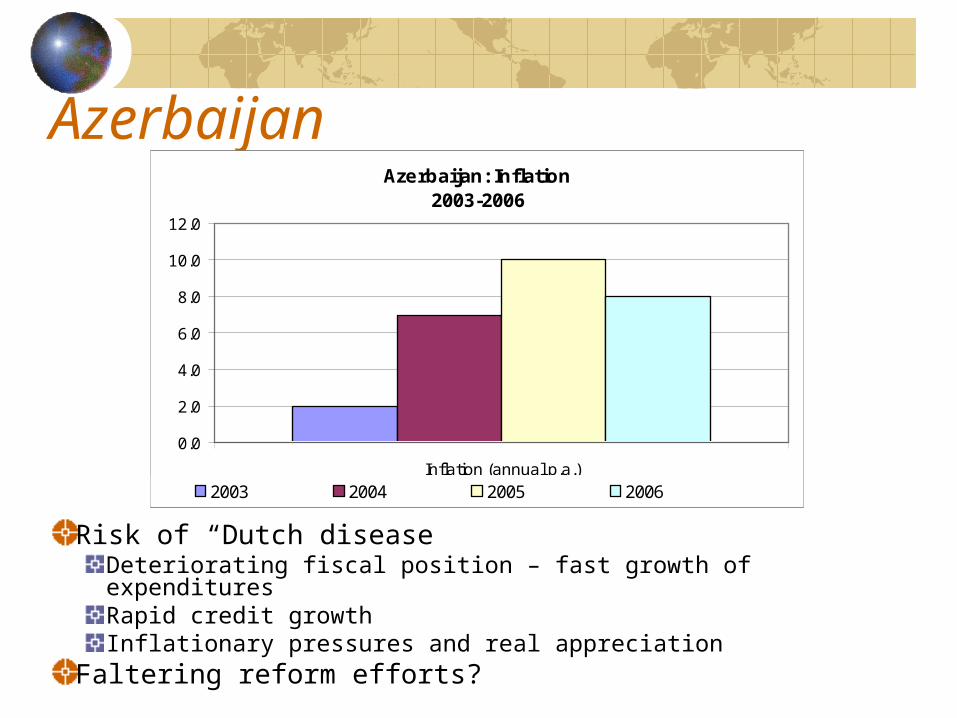

Azerbaijan

Very high growth since 2003 derived from large oil exports

Annual GDP Growth rate 2003-2006

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2003 2004 2005 2006

Azerbaijan

Risk of “Dutch disease” Deteriorating fiscal position – fast growth of expenditures Rapid credit growthInflationary pressures and real appreciation

Faltering reform efforts?

Azerbaijan: Inflation 2003-2006

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Inflation (annual p.a.)

2003 2004 2005 2006

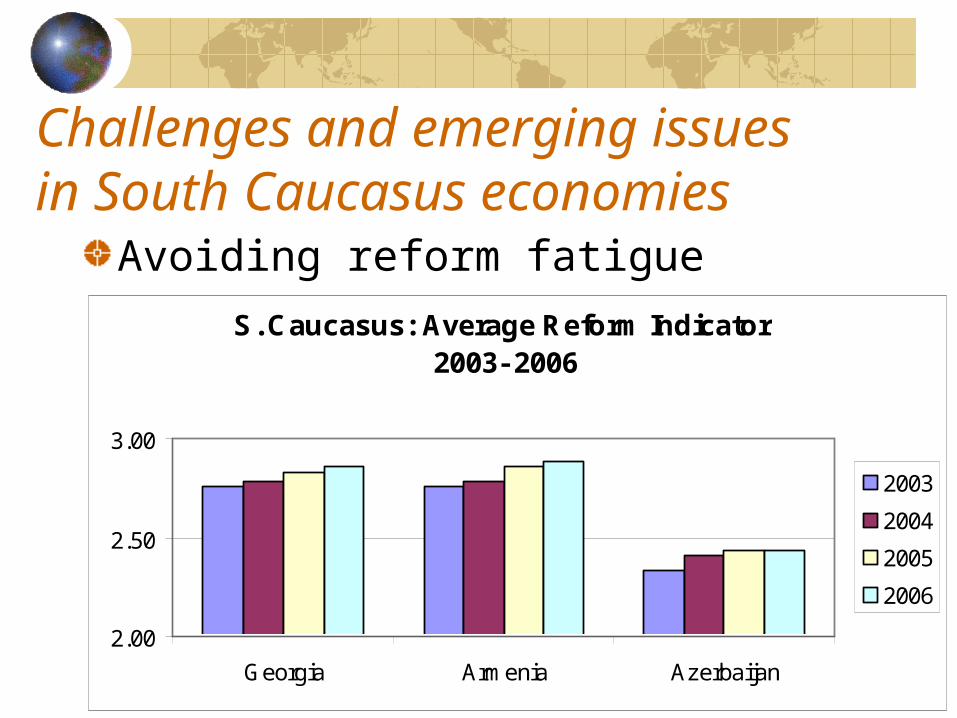

Challenges and emerging issues in South Caucasus economies

Avoiding reform fatigue

S. Caucasus: Average Reform Indicator 2003- 2006

2.00

2.50

3.00

Georgia Armenia Azerbaijan

2003

2004

2005

2006

Challenges and emerging issues in South Caucasus economies

Dealing with appreciation pressures – micro and regulatory reforms to boost competitiveness

Need to address trade bottlenecks -- continue to expand and diversify export supply and markets

Challenges of financial development

The End

Prospects and Challenges for Economic Growth in the South Caucasus and other Transition

EconomiesC. Felipe Jaramillo The World Bank

Tbilisi, Georgia, February 1, 2007