property tax advanced seminar - · pdf fileproperty tax advanced seminar ... • 12:45 how...

TRANSCRIPT

1

Property

Tax

Advanced

Seminar

February 27, 2013

MELG Building

Webinar 1

o Click on link to check your system

http://www.elluminate.com/support/index.jsp

o If you are experiencing trouble, please call

technical support at: 1.866.388.8674, option

#2, #4, #1 or online at

http://www.elluminate.com/support/index.jsp

o Using telephone for audio – call

1.800.724.2485, passcode 917492#

Need Help?

2

2

Overview of Blackboard Collaborate

Whiteboard Tools Participant Window

Chat Room

Audio Controls (mic/speaker level)

Top Toolbar

Whiteboard Screens

3

Speakers

• Phil Boone

Michigan Department of Education

• Robert Dwan

Michigan School Business Officials

• Howard Heideman

Michigan Department of Treasury

• Andrew Lockwood

Michigan Department of Treasury

• Sharon Raschke

Dexter Community Schools

4

3

Agenda

• 8:45 am Blackboard Collaborate Overview – Debbie Kopkau, MSBO

• 8:50 Overview of School Property Tax – Robert Dwan, MSBO

• 9:15 Terminology, Personal Property Tax, Ad Valorem Property Tax Millage Levies, K12 and ISD – Howard Heideman and Andrew Lockwood, Michigan Department of Treasury

• 10:15 Break

• 10:30 Millage Rates, Millage Reduction Fractions, and Tax Rate Requests – Howard Heideman and Andrew Lockwood, Michigan Department of Treasury

• 11:30 Tax Rate Request – L-4029 – Sharon Raschke, Dexter Community Schools

• 12:00 pm Lunch

5

Agenda (Cont)

• 12:45 How Property Taxes Fit into State Aid – Phil Boone, Michigan Department of Education

• 1:25 Specific Tax Programs, Renaissance Zones, Tax Increment Financing and Board of Review – Howard Heideman and Andrew Lockwood, Michigan Department of Treasury

• 2:25 Break

• 2:40 County Settlement & Reconciliation of Property Tax Receivable – Sharon Raschke, Dexter Community Schools

• 3:40 Current Topics, Michigan State Tax Commission, Other Issues, Wrap-Up – Robert Dwan, MSBO and all speakers

• 4:00 Adjourn

6

4

7

Property Tax Advanced

School Property Tax Overview

Presenter: Robert Dwan, MSBO

Tax

Increment

Financing

Authorities

Property Tax Process

Township & City

Assessors

Taxable Value

Information (DS-4410)

County Equalization

Director

A

S

S

E

S

S

M

E

N

T

Updated in May

and at least

annually

thereafter

8

5

9

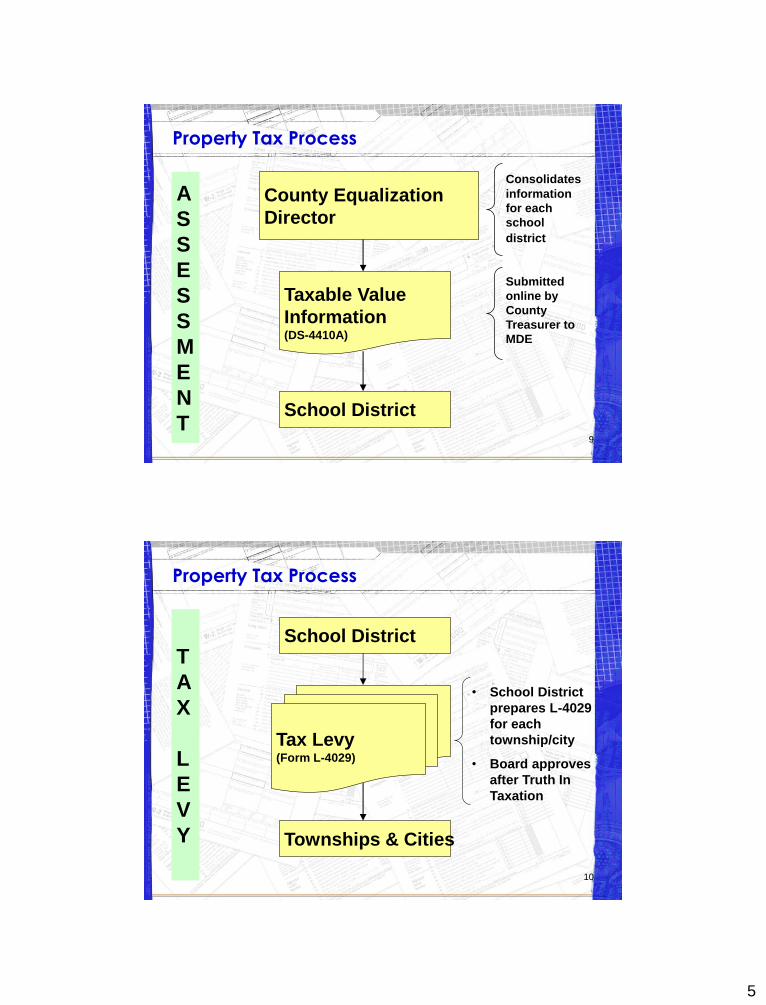

Property Tax Process

County Equalization

Director

Taxable Value

Information (DS-4410A)

School District

Consolidates

information

for each

school

district

A

S

S

E

S

S

M

E

N

T

Submitted

online by

County

Treasurer to

MDE

Property Tax Process

School District

Townships & Cities

• School District

prepares L-4029

for each

township/city

• Board approves

after Truth In

Taxation

Tax Levy (Form L-4029)

T

A

X

L

E

V

Y

10

6

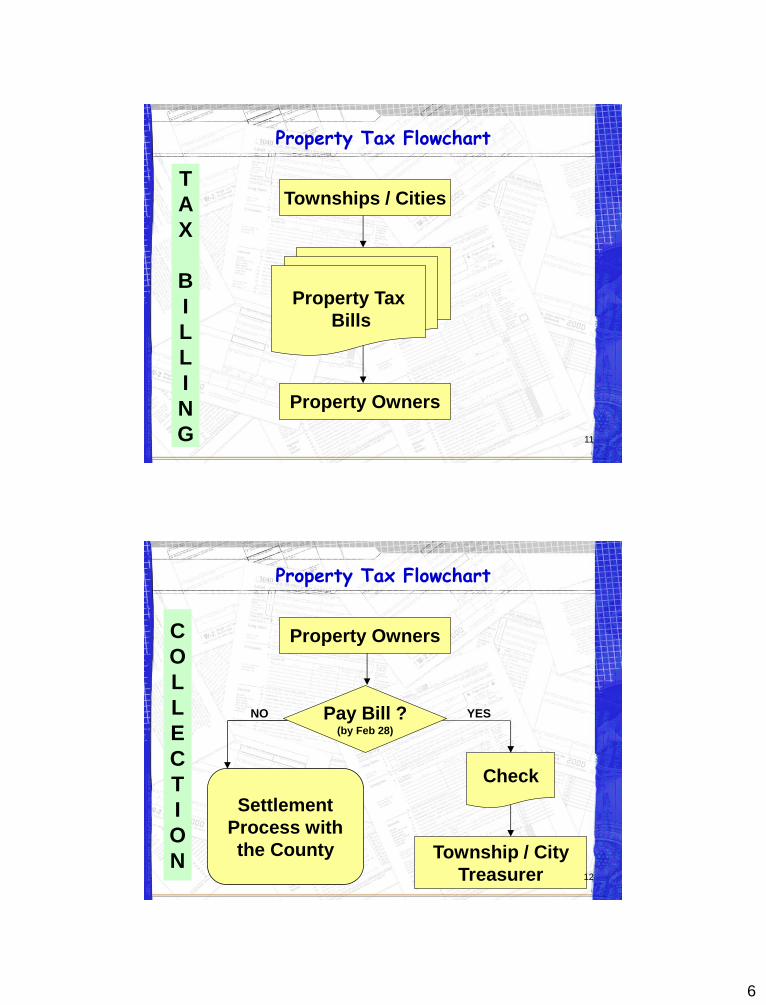

Property Tax Flowchart

Townships / Cities

Property Owners

Property Tax

Bills

T

A

X

B

I

L

L

I

N

G 11

Property Tax Flowchart

Property Owners

Township / City

Treasurer

Pay Bill ? (by Feb 28)

YES

Check

Settlement

Process with

the County

NO

C

O

L

L

E

C

T

I

O

N 12

7

Property Tax Flowchart

Township / City

Treasurer

Tax

Breakdown

School District

Check

C

O

L

L

E

C

T

I

O

N 13

Property Tax Flowchart

School District

Property Tax

Receivables

Worksheet

Deposits

Check in

Bank

C

O

L

L

E

C

T

I

O

N 14

8

Property Tax Process

Township & City

Treasurer

Settlement

County

• Townships &

Cities verify to

the County

parcel by parcel

• tax collections

• Taxes receivable

• As of March 1

S

E

T

T

L

E

M

E

N

T 15

16

Property Tax Process

County

Treasurer

Tax

Breakdown

School District

Check

D

E

L

I

N

Q

U

E

N

T

C

O

L

L

E

C

T

I

O

N

9

Property Tax Flowchart

County

Delinquent

Personal

Property

Taxes

Delinquent

Real

Property

Taxes

No Action

Check (Issues debt until

collected)

School District

Township/City collects delinquent

personal property taxes

County collects delinquent real

property taxes (bills back if uncollectible)

DELINQUENT

PAYOFF

17

Property Tax Process

School District

Property Tax

Receivables

Worksheet

Deposits

Check in

Bank

Used to calculate

taxes receivable

D

E

L

I

N

Q

U

E

N

T

P

A

Y

O

F

F

18

10

Glossary of Terms

19

20

Property Tax Advanced

Terminology

Presenters: Howard Heideman & Andrew Lockwood

Michigan Department of Treasury

11

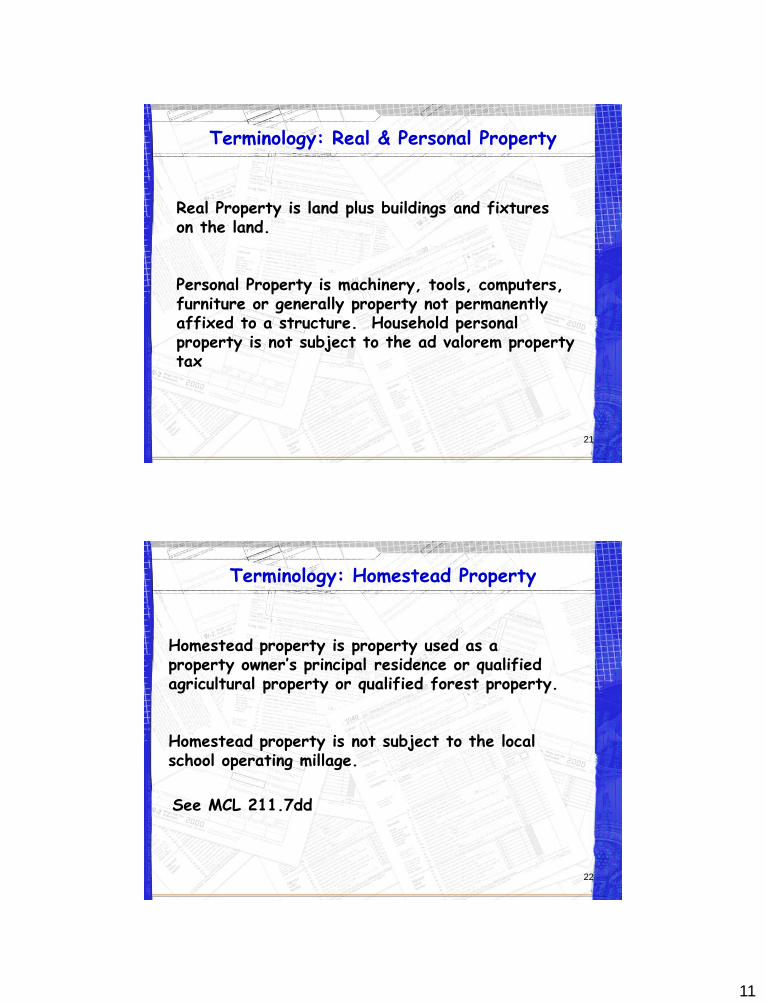

Terminology: Real & Personal Property

21

Real Property is land plus buildings and fixtures on the land.

Personal Property is machinery, tools, computers, furniture or generally property not permanently affixed to a structure. Household personal property is not subject to the ad valorem property tax

Terminology: Homestead Property

22

Homestead property is property used as a property owner’s principal residence or qualified agricultural property or qualified forest property.

Homestead property is not subject to the local school operating millage.

See MCL 211.7dd

12

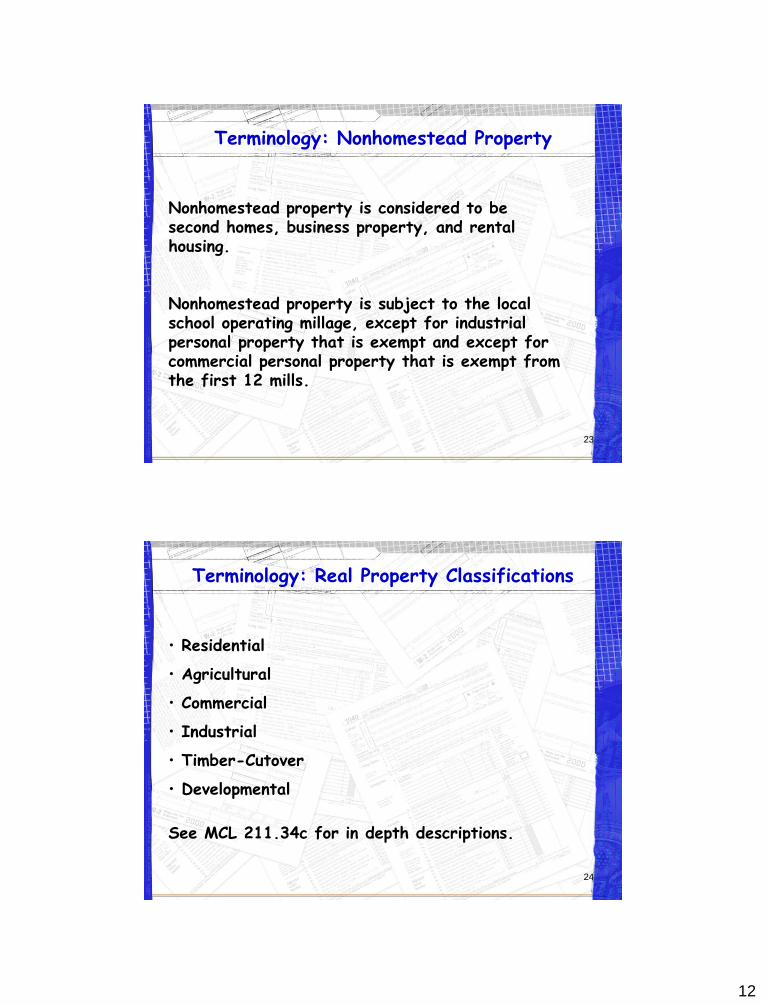

Terminology: Nonhomestead Property

23

Nonhomestead property is considered to be second homes, business property, and rental housing.

Nonhomestead property is subject to the local school operating millage, except for industrial personal property that is exempt and except for commercial personal property that is exempt from the first 12 mills.

Terminology: Real Property Classifications

24

• Residential

• Agricultural

• Commercial

• Industrial

• Timber-Cutover

• Developmental

See MCL 211.34c for in depth descriptions.

13

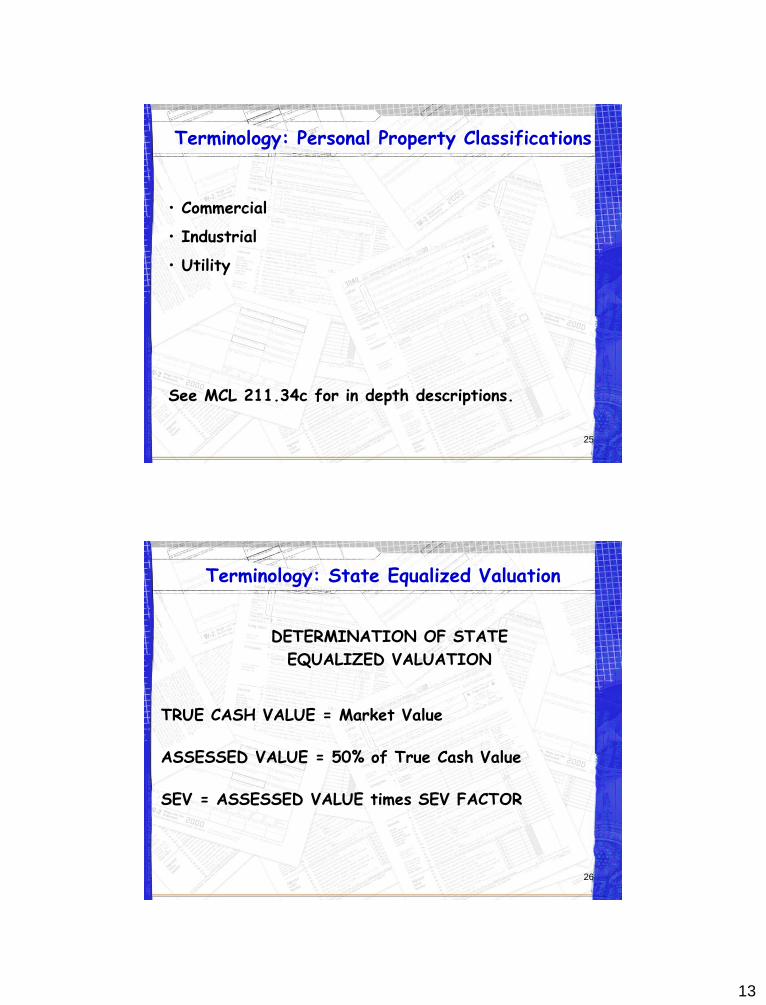

Terminology: Personal Property Classifications

25

• Commercial

• Industrial

• Utility

See MCL 211.34c for in depth descriptions.

Terminology: State Equalized Valuation

DETERMINATION OF STATE

EQUALIZED VALUATION

TRUE CASH VALUE = Market Value ASSESSED VALUE = 50% of True Cash Value SEV = ASSESSED VALUE times SEV FACTOR

26

14

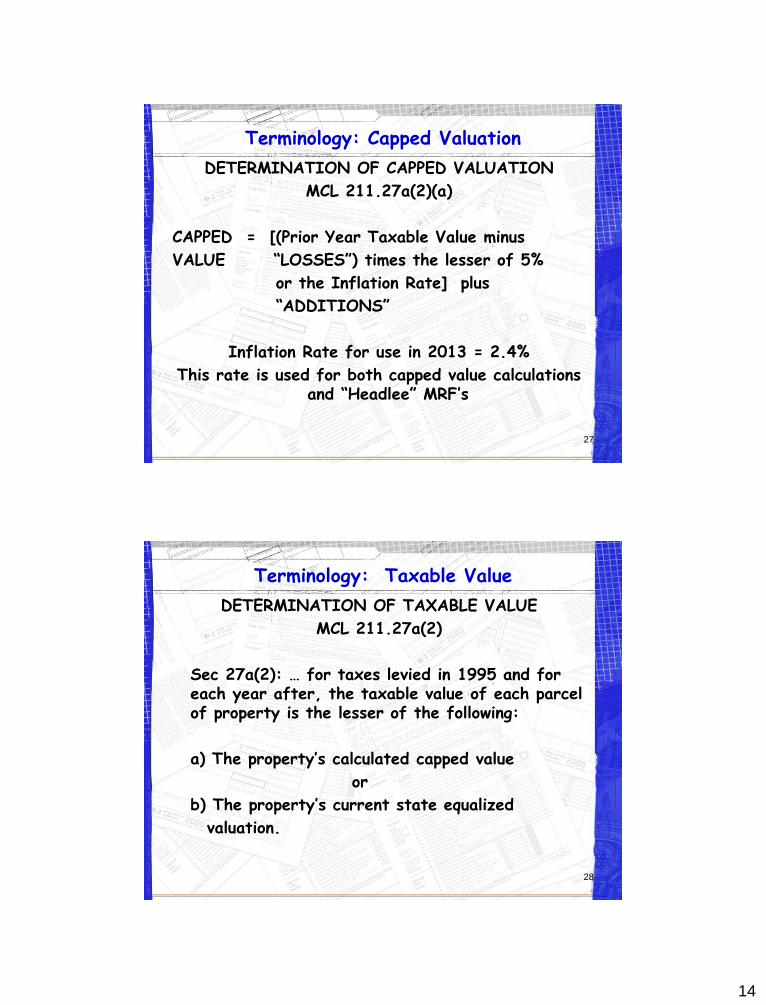

Terminology: Capped Valuation

DETERMINATION OF CAPPED VALUATION

MCL 211.27a(2)(a)

CAPPED = [(Prior Year Taxable Value minus

VALUE “LOSSES”) times the lesser of 5%

or the Inflation Rate] plus

“ADDITIONS”

Inflation Rate for use in 2013 = 2.4%

This rate is used for both capped value calculations and “Headlee” MRF’s

27

Terminology: Taxable Value

DETERMINATION OF TAXABLE VALUE

MCL 211.27a(2)

Sec 27a(2): … for taxes levied in 1995 and for each year after, the taxable value of each parcel of property is the lesser of the following:

a) The property’s calculated capped value

or

b) The property’s current state equalized

valuation.

28

15

29

Property Tax Advanced

Personal Property Tax Reform

Presenter: Howard Heideman Michigan Department of Treasury

• Small Taxpayer Exemption – Beginning in 2014, all of a taxpayer’s industrial and commercial personal property within a local tax collecting unit will be exempt, so long as the combined taxable value of such property within the unit is less than $40,000.

• Exemption for New Personal Property – Beginning in 2016, Eligible Manufacturing Personal Property (EMPP) first placed in service after 2012 will be 100% exempt.

• Existing Personal Property Exemptions – Starting in 2016, EMPP first placed in service in 2005 or earlier will be 100% exempt. In each subsequent year, one additional year would be added until all existing EMPP would be exempt in 2023.

30

PERSONAL PROPERTY TAX REFORM

16

• Eligible Manufacturing Personal Property (EMPP) – All industrial and commercial personal property (PP) located on a parcel of real property if the PP is used more than 50% of the time in industrial processing or direct integrated support.

• Existing Property Tax Abatements – Beginning in 2014, existing PA 198, tech park and enterprise zone PPT abatements would be extended until, or terminate on, the date the property qualifies for the new exemptions

• PA 328 exemptions will continue until the later of that date or the original exemption expiration date.

• Exemptions tied to approval of Local Use Tax Legislation at August 2014 Statewide Election 31

PERSONAL PROPERTY TAX REFORM

• In FY 2014 & FY 2015, requirement to reimburse for loss of debt taxes

• Beginning in FY 2016, Use Tax and SAF reimbursement would begin. SET and basic school operating mills would be made from payment from state use tax to the SAF through appropriation.

• ISD Operating and Debt Loss would be 100% reimbursed by the Use Tax through the Metropolitan Authority.

• Sinking fund and recreational mills would be reimbursed at an estimated 80% by the Use Tax through the Metropolitan Authority.

• Hold Harmless and Out of Formula School Districts would be 100% reimbursed by the Use Tax through the Metropolitan Authority

32

PPT Plan Reimbursement

17

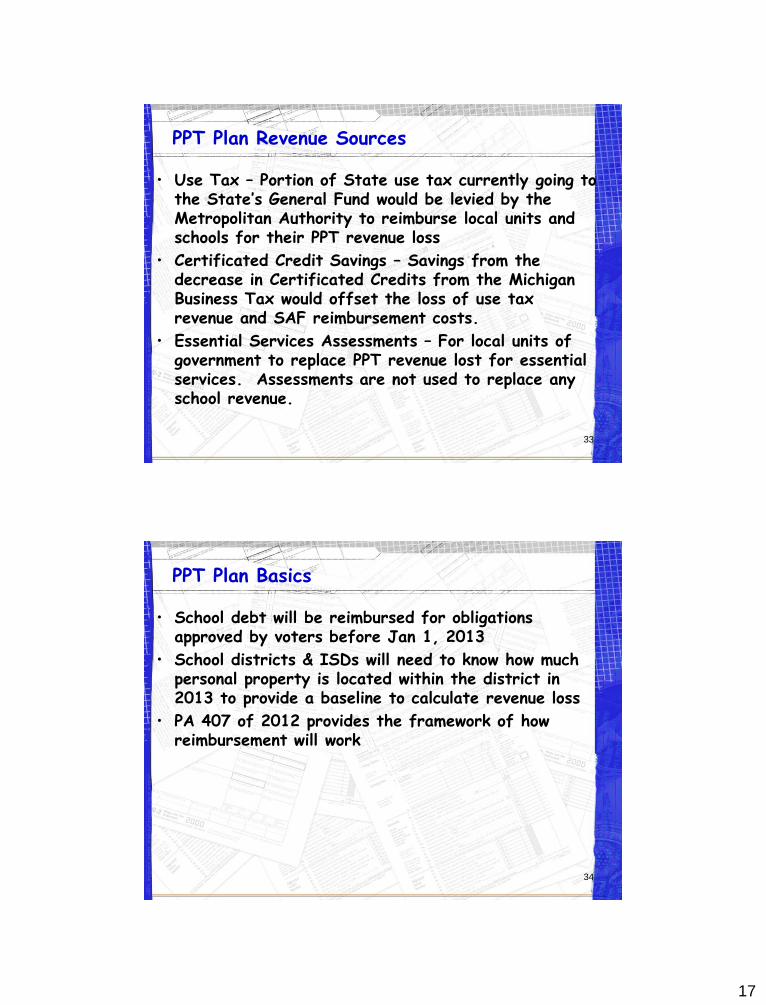

• Use Tax – Portion of State use tax currently going to the State’s General Fund would be levied by the Metropolitan Authority to reimburse local units and schools for their PPT revenue loss

• Certificated Credit Savings – Savings from the decrease in Certificated Credits from the Michigan Business Tax would offset the loss of use tax revenue and SAF reimbursement costs.

• Essential Services Assessments – For local units of government to replace PPT revenue lost for essential services. Assessments are not used to replace any school revenue.

33

PPT Plan Revenue Sources

• School debt will be reimbursed for obligations approved by voters before Jan 1, 2013

• School districts & ISDs will need to know how much personal property is located within the district in 2013 to provide a baseline to calculate revenue loss

• PA 407 of 2012 provides the framework of how reimbursement will work

34

PPT Plan Basics

18

35

PPT Plan Basics – Reimbursement Table

Local Government Reimbursements

Funding Source Type of Service/Cost Rate of Reimbursement

Special Assessment for Essential Services Up to 100% of lost PPT revenue

essential services (local option) (police,fire,ambulance, and jail

Portion of state use tax is K-12 operating costs 100% of lost PPT revenue

dedicated to school aid fund

ISD operating costs and existing 100% of lost PPT revenue

K-12 and ISD school bond debt

Portion of 6% use tax is levied by Sinking fund and recreational mills Estimated 80% of lost PPT revenue

Statewide Metropolitan Authority Non-essential services Estimated 80% of lost PPT revenue to all

(all services except police, fire, jail, community colleges and other municipalities

and ambulance) losing over 2.3% of taxable value to PPT exemptions

36

Property Tax Advanced

Ad Valorem Property Tax Millage Levies, K12

Presenters: Howard Heideman & Andrew Lockwood

Michigan Department of Treasury

19

Ad Valorem Property Tax Millage Levies

K-12

1. General Operating Levy

2. Hold Harmless Levy

3. Building & Site Sinking Fund Levy

4. Debt Levy

5. Recreational Levy

37

Ad Valorem Property Tax Millage Levies, K-12

Millage Taxable Value Base

General Non-Homestead &

Operating Non-Qualified Agricultural/Forest Property

Truth

“Headlee” in Tax

YES YES

General Operating Levy cannot exceed 18 mills or 1993 levy, whichever is less.

38

20

Ad Valorem Property Tax Millage Levies, K-12

Industrial Personal Property Beginning in 2008, industrial personal property is exempt from the State Education Tax and 18 mill local school operating tax. Prior to FY12, School Aid Fund revenues were reimbursed through the Michigan Business Tax.

39

Ad Valorem Property Tax Millage Levies, K-12

Commercial Personal Property Also beginning in 2008, commercial personal property is exempt from 12 mills of the local school operating tax. Prior to FY12, School Aid Fund revenues were reimbursed through the Michigan Business Tax.

40

21

Ad Valorem Property Tax Millage Levies, K-12

Millage Taxable Value Base

Supplemental PRE and Qual. Ag./Forest in

“Hold the local school district

Harmless”

Truth

“Headlee” in Tax

YES YES

Lesser of Annual School Code Limit Millage and the 1994 Certified Millage, as permanently reduced, times the current year millage reduction fraction for all property. (Letter 3-29-99)

41

Exemption & Specific Taxation Programs

Hold Harmless School Districts Because industrial and commercial personal property are treated like PRE and Ag property, hold harmless millage rates are levied on industrial and commercial personal property. Commercial personal property is only exempt from 12 school operating mills. It is only subjected to the first 12 hold harmless mills.

42

22

Hold-Harmless Mills

Section 1211 of school code, MCL 380.1211 (3):

• Hold-Harmless Districts must reduce mills to limit increase in combined state and local revenue per pupil to lesser of: – $ increase in foundation allowance

– % increase in general price level

43

Hold-Harmless Mills

When foundation allowance increases by more than inflation, hold-harmless districts must reduce their millage rate to limit state/local increase to inflation.

To allow hold-harmless districts to receive full dollar increase in foundation allowance, their foundation increases were limited to inflation, with rest of increase paid under Sec.20j.

44

23

Ad Valorem Property Tax Millage Levies, K-12

Millage Taxable Value Base

Sinking Fund All properties within

the local school district

Truth

“Headlee” in Tax

Yes No

See Attorney General Opinion 7131

45

Ad Valorem Property Tax Millage Levies, K-12

Millage Taxable Value Base

Debt All properties within

the local school district

Truth

“Headlee” in Tax

No No

46

24

Ad Valorem Property Tax Millage Levies, K-12

Millage Taxable Value Base

Recreational All properties within

the local school district

Truth

“Headlee” in Tax

Yes Yes

47

48

Property Tax Advanced

Ad Valorem Property Tax Millage Levies, ISD

Presenters: Howard Heideman & Andrew Lockwood

Michigan Department of Treasury

25

Ad Valorem Property Tax Millage Levies, ISD

1. Allocated Operating Levy

2. Special Education

3. Vocational Education

4. Enhancement

49

Ad Valorem Property Tax Millage Levies, ISD

ISD Millage Taxable Value Base

Allocated All properties within

Operating the intermediate school

district

Truth

Maximum “Headlee” in Tax

150% of what Yes Yes

was authorized in 1993

Allocated through voter-approved fixed allocation or by county allocation board.

50

26

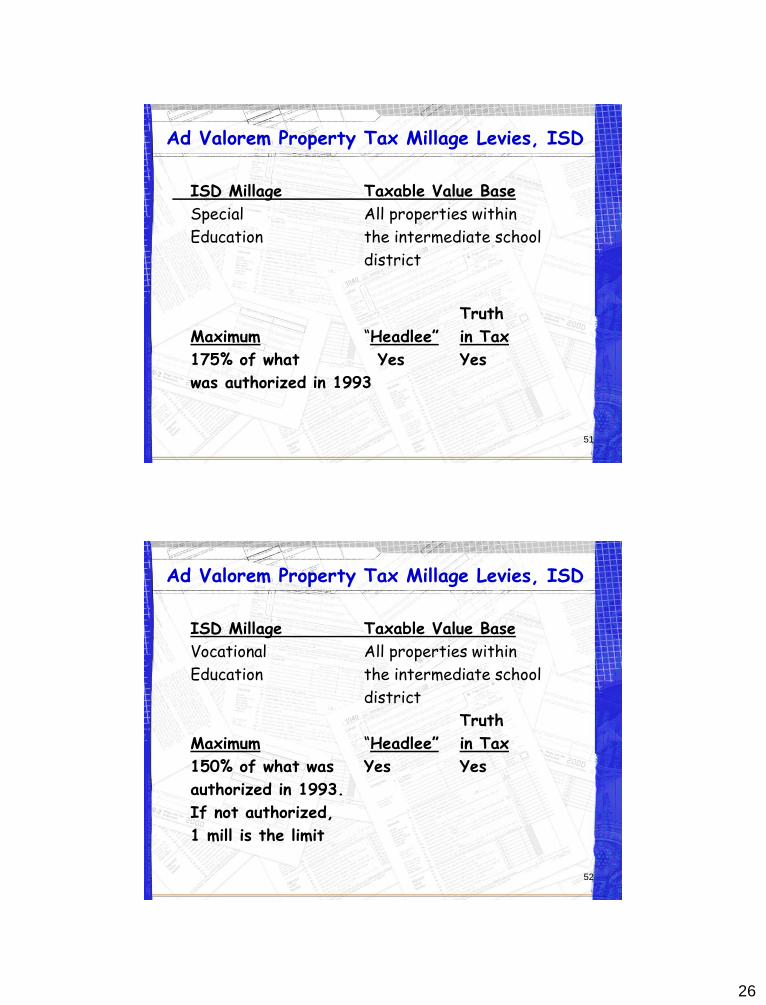

Ad Valorem Property Tax Millage Levies, ISD

ISD Millage Taxable Value Base

Special All properties within

Education the intermediate school

district

Truth

Maximum “Headlee” in Tax

175% of what Yes Yes

was authorized in 1993

51

Ad Valorem Property Tax Millage Levies, ISD

ISD Millage Taxable Value Base

Vocational All properties within

Education the intermediate school

district

Truth

Maximum “Headlee” in Tax

150% of what was Yes Yes

authorized in 1993.

If not authorized,

1 mill is the limit

52

27

Ad Valorem Property Tax Millage Levies, ISD

ISD Millage Taxable Value Base

Enhancement All properties within

the intermediate school

district

Truth

Maximum “Headlee” in Tax

Not to exceed Yes Yes

3 mills

53

Ad Valorem Property Tax Millage Levies

STATE EDUCATIONSTATE EDUCATIONTAXTAX

NOT SUBJECTTO “HEADLEE”

NOT SUBJECTTO TRUTH INTAXATION

NOT TO BE REPORTED BY THE LOCAL SCHOOLDISTRICT or ISD ON THE L-4029 - TAX RATE

REQUEST

54

28

Break

55

56

Property Tax Advanced

Millage Rates/Millage Reduction Fractions

Presenters: Howard Heideman & Andrew Lockwood

Michigan Department of Treasury

29

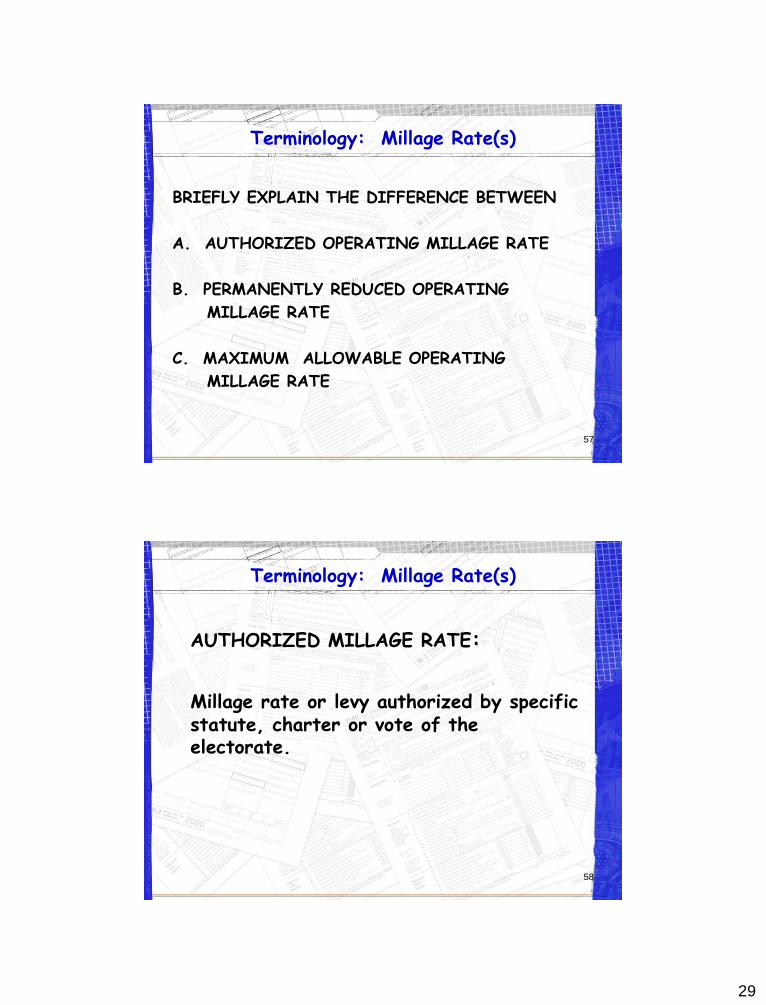

Terminology: Millage Rate(s)

BRIEFLY EXPLAIN THE DIFFERENCE BETWEEN

A. AUTHORIZED OPERATING MILLAGE RATE

B. PERMANENTLY REDUCED OPERATING

MILLAGE RATE

C. MAXIMUM ALLOWABLE OPERATING

MILLAGE RATE

57

Terminology: Millage Rate(s)

AUTHORIZED MILLAGE RATE:

Millage rate or levy authorized by specific statute, charter or vote of the electorate.

58

30

Terminology: Millage Rate(s)

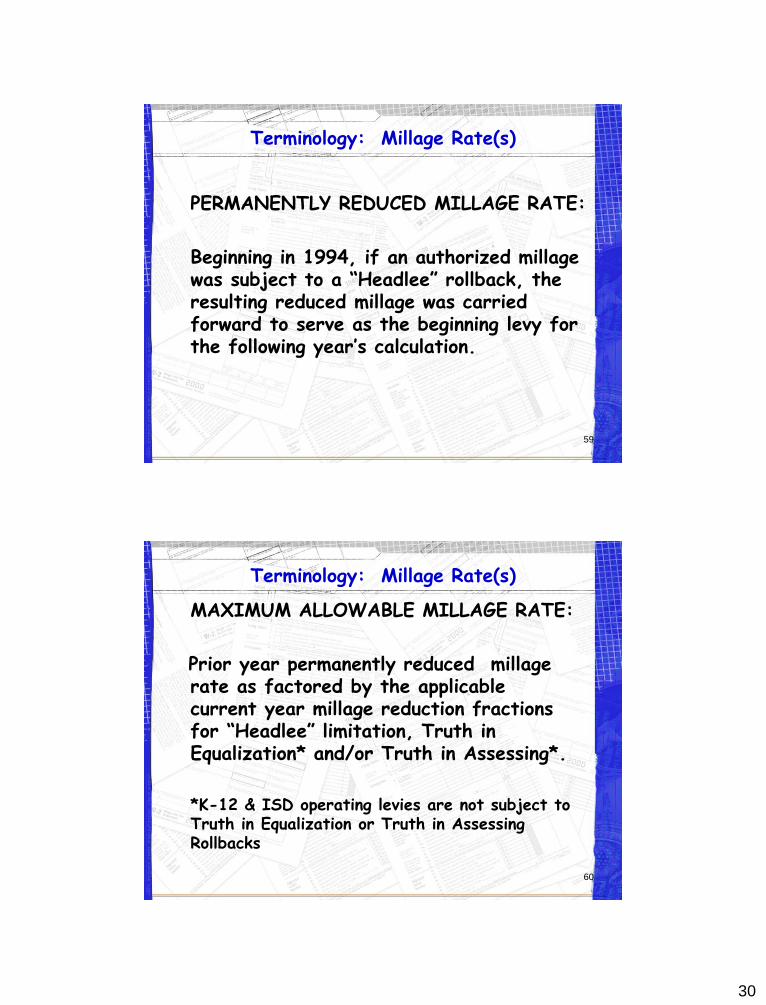

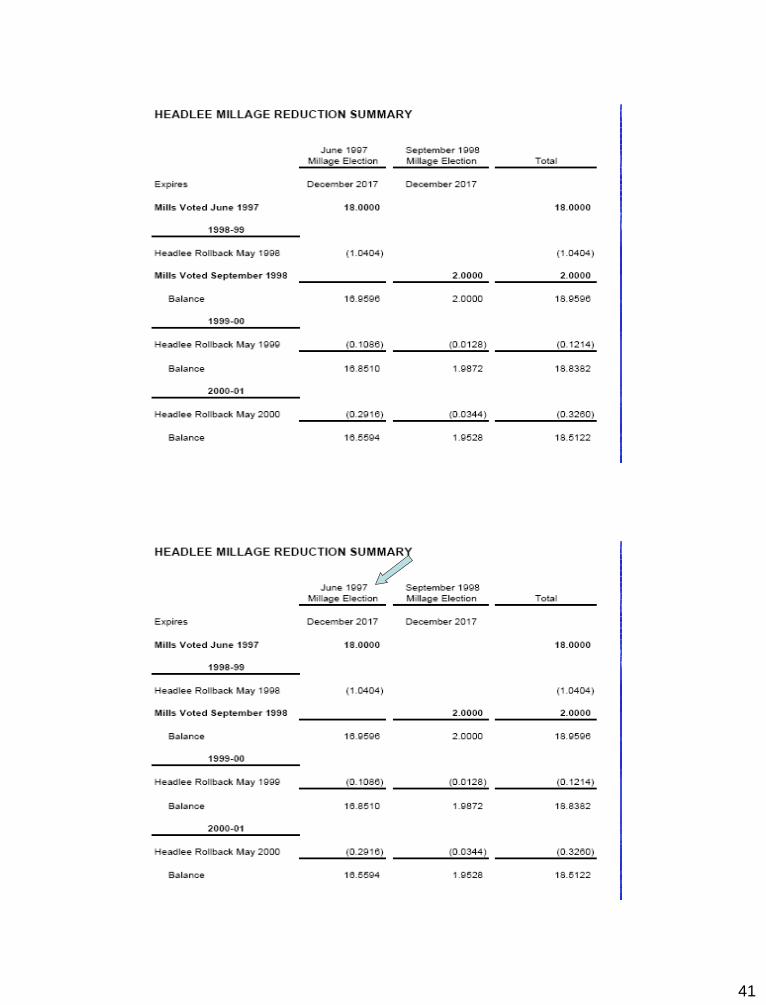

PERMANENTLY REDUCED MILLAGE RATE:

Beginning in 1994, if an authorized millage was subject to a “Headlee” rollback, the resulting reduced millage was carried forward to serve as the beginning levy for the following year’s calculation.

59

Terminology: Millage Rate(s)

MAXIMUM ALLOWABLE MILLAGE RATE:

Prior year permanently reduced millage rate as factored by the applicable current year millage reduction fractions for “Headlee” limitation, Truth in Equalization* and/or Truth in Assessing*.

*K-12 & ISD operating levies are not subject to

Truth in Equalization or Truth in Assessing Rollbacks

60

31

Millage Reduction Fractions

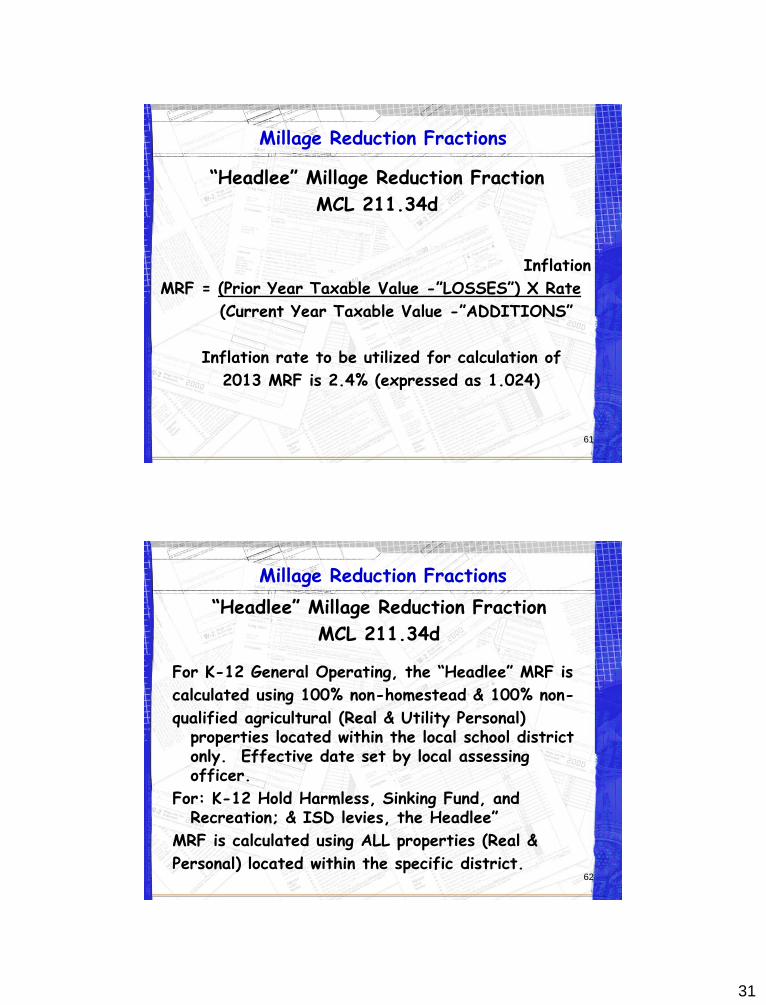

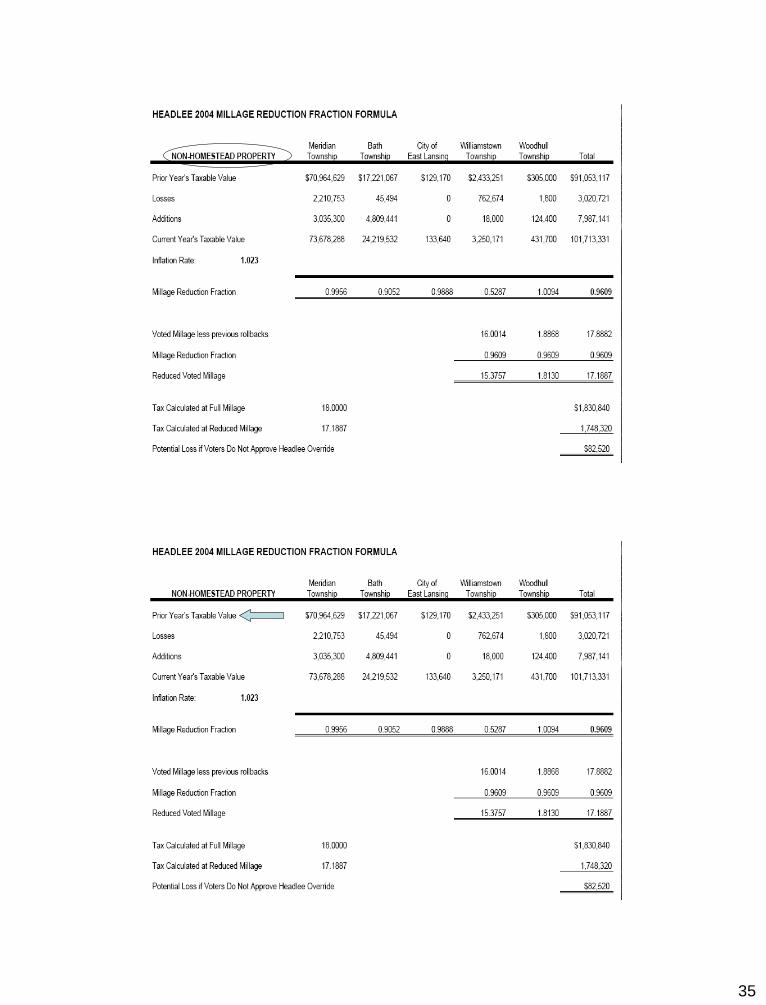

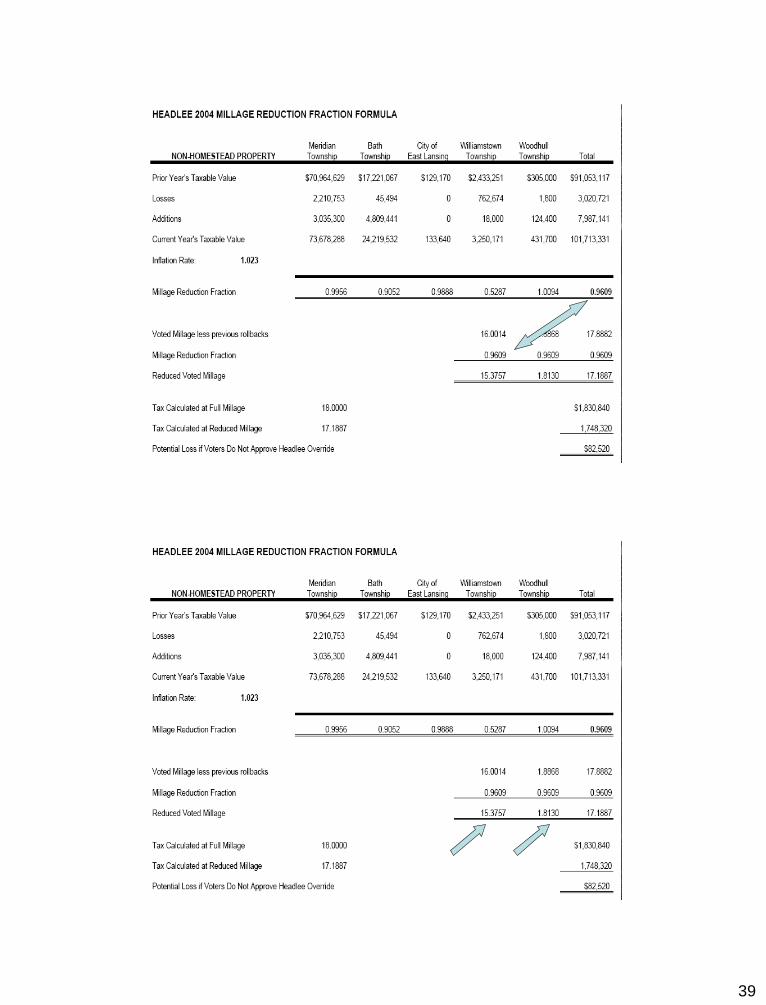

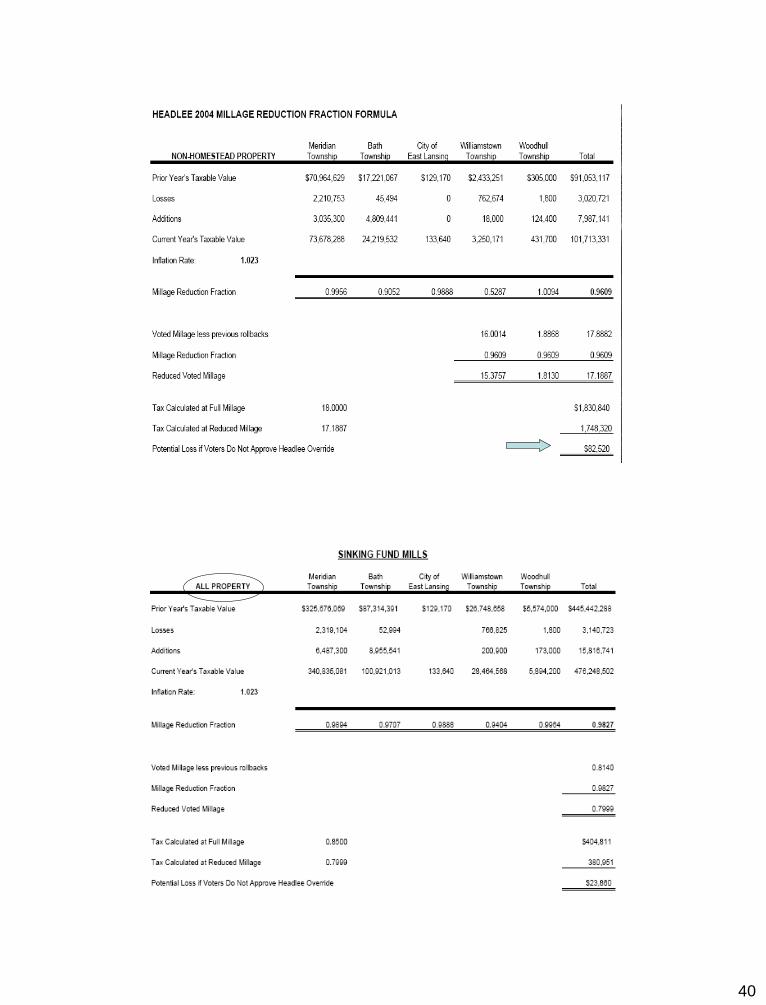

“Headlee” Millage Reduction Fraction

MCL 211.34d

Inflation

MRF = (Prior Year Taxable Value -”LOSSES”) X Rate

(Current Year Taxable Value -”ADDITIONS”

Inflation rate to be utilized for calculation of

2013 MRF is 2.4% (expressed as 1.024)

61

Millage Reduction Fractions

“Headlee” Millage Reduction Fraction

MCL 211.34d

For K-12 General Operating, the “Headlee” MRF is

calculated using 100% non-homestead & 100% non-

qualified agricultural (Real & Utility Personal) properties located within the local school district only. Effective date set by local assessing officer.

For: K-12 Hold Harmless, Sinking Fund, and Recreation; & ISD levies, the Headlee”

MRF is calculated using ALL properties (Real &

Personal) located within the specific district.

62

32

Millage Reduction Fractions

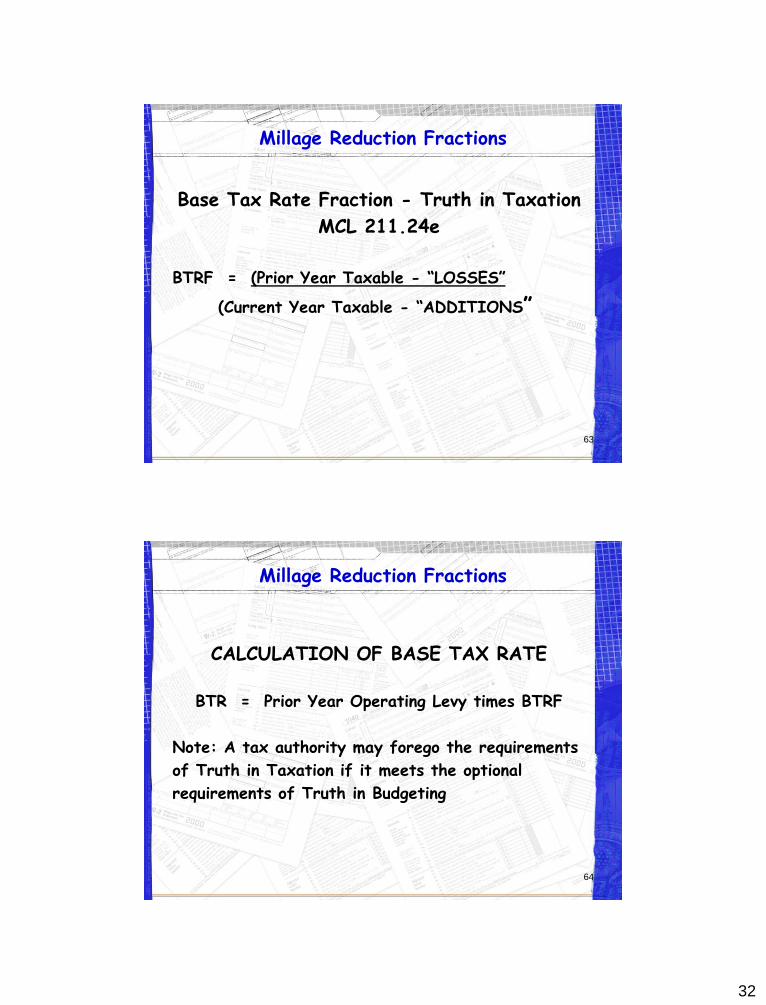

Base Tax Rate Fraction - Truth in Taxation

MCL 211.24e

BTRF = (Prior Year Taxable - “LOSSES”

(Current Year Taxable - “ADDITIONS”

63

Millage Reduction Fractions

CALCULATION OF BASE TAX RATE

BTR = Prior Year Operating Levy times BTRF

Note: A tax authority may forego the requirements

of Truth in Taxation if it meets the optional

requirements of Truth in Budgeting

64

33

65

Millage Reduction Fractions

“LOSSES”

MCL 211.34d(1)(h)

Property Destroyed Property Removed

Exempt Property Decrease in Occupancy

Environmental Contamination

“LOSSES” NOT:

Platting, Splits, Combinations, Zoning Changes

66

Millage Reduction Fractions

“ADDITIONS” MCL 211.34d(1)(b)

Omitted Real Property Omitted Personal Property

New Construction Previously Exempt Property Replacement Construction

Remediation of Environmental Contamination Increase in Occupancy (Ruled unconstitutional, WpW) Public Services (Ruled unconstitutional, Toll Northville)

34

Millage Reduction Fractions

“ADDITIONS” NOT:

Platting, Splits, Combinations

Zoning Changes

Transfers of Ownership

67

68

35

36

37

38

39

40

41

42

43

44

45

90

Property Tax Advanced

L-4029

Presenter:

Sharon Raschke, Dexter Community Schools

46

91

L-4029 Tax Rate Request

92

•This form can be obtained from Michigan Treasury’s website at

www.michigan.gov/treasury

•Form must be completed and submitted to local municipal and

county Treasurers on or before September 30 of each year.

•If a summer levy is requested, the form must be submitted earlier.

•Tax Rate Requests must be approved in accordance with Truth in

Taxation Hearing requirements.

47

Completing the L-4029

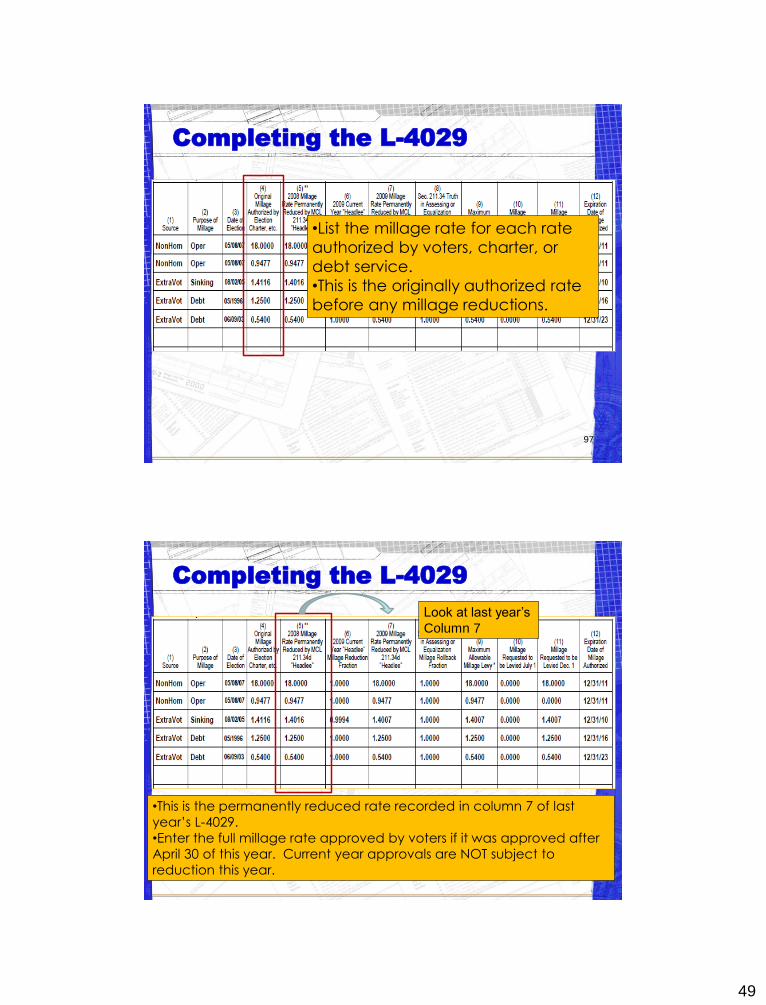

93

A separate L-4029 is

prepared for each

municipality

Report TV for all school district

properties and non-primary

residency exemption (Non-PRE)

properties within the municipality

(from DS-4410)

Completing the L-4029

94

Enter the source for each millage.

This includes charter, extra-voted, non-

PRE

48

Completing the L-4029

95

•Enter the purpose of the millage.

•Examples are operating, debt service,

special ed, voc ed, and sinking fund

millage.

Completing the L-4029

96

Record the election date and year

for each millage authorized by district

voter approval.

49

Completing the L-4029

97

•List the millage rate for each rate

authorized by voters, charter, or

debt service.

•This is the originally authorized rate

before any millage reductions.

Completing the L-4029

98

Look at last year’s

Column 7

•This is the permanently reduced rate recorded in column 7 of last

year’s L-4029.

•Enter the full millage rate approved by voters if it was approved after

April 30 of this year. Current year approvals are NOT subject to

reduction this year.

50

Completing the L-4029

99

•List the Millage

Reduction Fraction

(MRF) certified by the

county treasurer for

the current year.

•The MRF shall be

recorded with four

decimal places.

•Current year MRF in

Column 6 shall not

exceed 1.0000. This

prevents roll up of millage

rates.

•Enter 1.0000 for current

year approved millage

(after April 30).

•Enter 1.0000 for debt, as

debt millage is not

subject to MRF.

Completing the L-4029

100

Calculation Column

•Multiply rate in

Column 5 by the MRF

in Column 6.

•Round DOWN to

fourth decimal place.

1.4016 x 0.9994 = 1.400759

rounds to 1.4007

51

Completing the L-4029

101

•This column is always 1.0000 for

school districts, since schools are

not subject to Truth in Assessing or

Equalization millage rollback

fractions.

Completing the L-4029

102

Calculation Column

•Multiply rate in Column 7 by the rollback fraction in Column 8.

•Round DOWN to fourth decimal place.

•Since Column 8 is always 1.0000 for schools, Column 9 always

Column 7 for schools.

52

Completing the L-4029

103

•Enter the tax rate approved by the board

of education for summer and winter levies

•The sum of the rates cannot exceed the

maximum allowable levy in Column 9.

All school taxes are

on winter tax roll in

this example.

Completing the L-4029

104

•Record the millage expiration date.

•This is always a 12/31 date with the

year of millage expiration.

53

Completing the L-4029

• Don’t forget the certification section!

• Be sure to complete the prepared by section, so the county

officials know who to contact with any questions.

• Board president and secretary must sign the L-4029 as

approved by the board.

105

L-4029 for District Levying Hold Harmless Mills Assume a district is levying 18 mills on Non-homestead property and 5 Hold-Harmless mills. This is reported on the L-4029 as 5 mills levied on all property and 13 (Additional) mills levied on non-homestead property. See Annual STC Millage Rollback Bulletin (2010-2)

106

Completing the L-4029

54

Completing the L-4029

107

Report millage levy for:

•Principal Residence,

Qualified Ag, Qualified

Forest and Industrial

Personal

•Commercial Personal

•All Other.

108

L-4029 Random Thoughts

•Consider having your county equalization

department or treasurer’s office review L-4029

before finalizing.

•Don’t forget that a separate report must be

completed for each municipality within the

school district.

•Forward a copy of the executed L-4029 to your

bond counsel for their records.

55

L-4029 - Tax Rate Request

109

Lunch – 12:00 – 12:45 pm

110