property council retail forum | may 2015

TRANSCRIPT

1

Economic drivers and emerging retail trends

PCA Retail Forum 15 May 2015

Tony DimasiManaging DirectorT 03 9600 0500M 0409 216 [email protected]

2

Key points

Economic drivers

1. Population growth

2. Key economic variables and their impacts on retail expenditure

3. Retail sector’s share of the household wallet

Emerging retail trends

1. Generational shifting; ageing population

2. Globalisation of retailing

3. The role of food vs fashion

4. Shopping centre scale and design

3

Economic drivers

4

Retail expenditure growth

*Other Food includes – Specialised food retailing, cafes, restaurants and other takeaway food

**All other retailing includes furniture/floor coverings, electrical/electronics, hardware/garden, newspaper/books, other recreational goods, pharmaceuticals and other retailing

FY2015- from April 2014 to March 2015

Source ABS Retail Trade Cat. 8501.0, May 2015

5

Retail food expenditure

*Other Food includes – Specialised food retailing, cafes, restaurants and other takeaway food

- FY2015- from April 2014 to March 2015

Source ABS Retail Trade Cat. 8501.0, May 2015

6

Retail expenditure growth

• Pre-GFC, retail exp. per capita was the driver of total retail growth

• Post GFC, in most years pop growth has been the key driver of retail sales growth

– exp. per cap. growth has not even kept up with inflation

Source: ABS Retail Trade Cat. 8501.0

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2020 2025

retail

population

Australian retail sales - growth per annum (ABS)

7

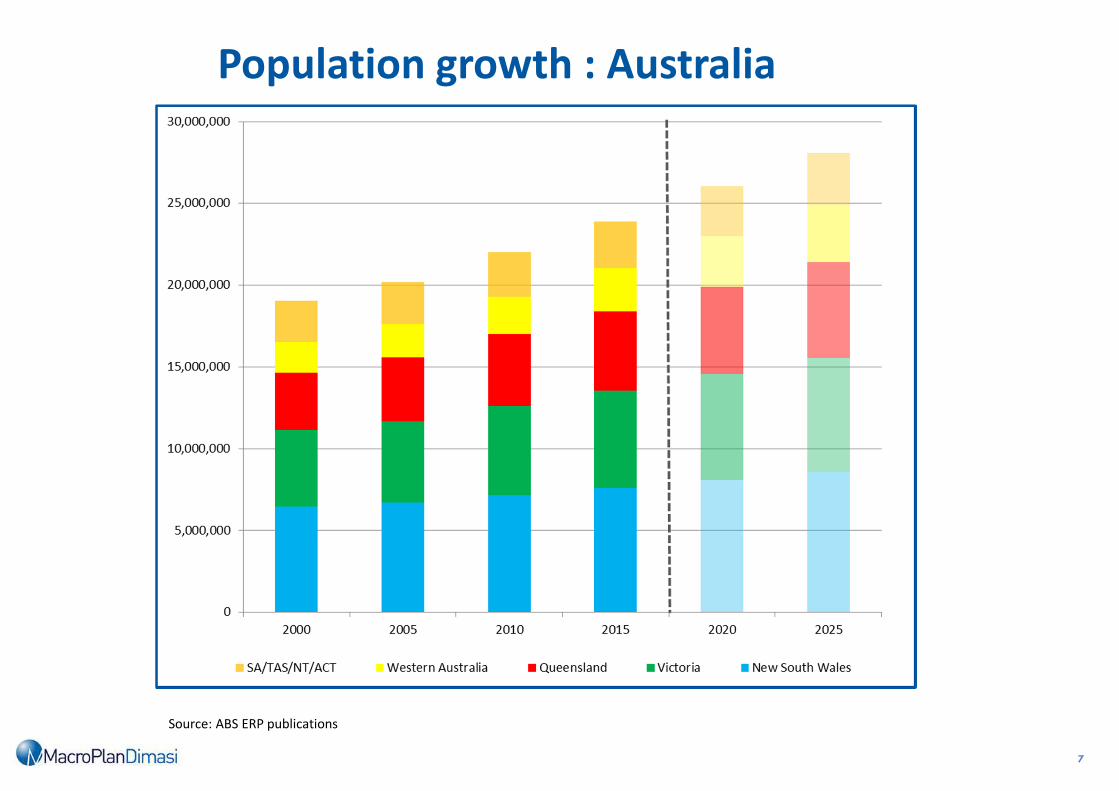

Population growth : Australia

Source: ABS ERP publications

8

Population growth – YOY change

Source: ABS Population Projections cat. 3332.0

9

Key economic variables, and implications for retail exp.

• House prices – nexus appearing to break down.

• Wages growth has fallen away over the past 2 years

• Deflation in key (non-food) retail categories

• Non-retail essentials gobbling up the household budget (education, health,

housing)

10

House prices and confidence to spend

Source: ABS Consumer Price Index cat. 6401.0; REIA Median House Price Index

11

Wages growth falling away

Source: ABS Wage Price Index cat. 6345.0

12

“Essentials” vs. Retail goods inflation

Source: ABS Consumer Price Index Cat. 6401.0

0

20

40

60

80

100

120

140

160

180

200

220

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Food and non-alcoholic beverages Alcohol and tobacco

Clothing and footwear Furnishings, household equipment and services

Housing Health

Education Transport

Consumer price index (by group - FY2000-FY2014)

Retail/ tradeables

= low inflation

Non-retail/non-tradeables

= high inflation

FY

13

Retail sector’s share of the household wallet

Source: ABS House and Expenditure Survey and Survey of Income and Housing cat.6503

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1984 1988–89 1993–94 1998–99 2003–04 2009–10 2020?

Household furnishings and

equipment

Clothing and footwear

Personal care

Alcoholic beverages

Food and non-alcoholic beverages

Tobacco products

Miscellaneous goods and services

Household services and operation

Medical care and health expenses

Recreation

Transport

Domestic fuel and power

Current housing costs (selected

dwelling)

Re

tail

No

n-r

eta

il

Retail

Re

tail

No

n-r

eta

il

Non-

Retail

14

What will happen to retail expenditure growth?

• Food spending will continue to grow strongly.

• Non-food spending growth should improve, but remain below long-term trend.

• Overall, retail spend will have to fight hard to maintain share of household

budget.

15

Emerging retail trends

16

Ageing population

Source: ABS Cat 3222.0 (2013)

Australian Population forecasts – up to 2051

17

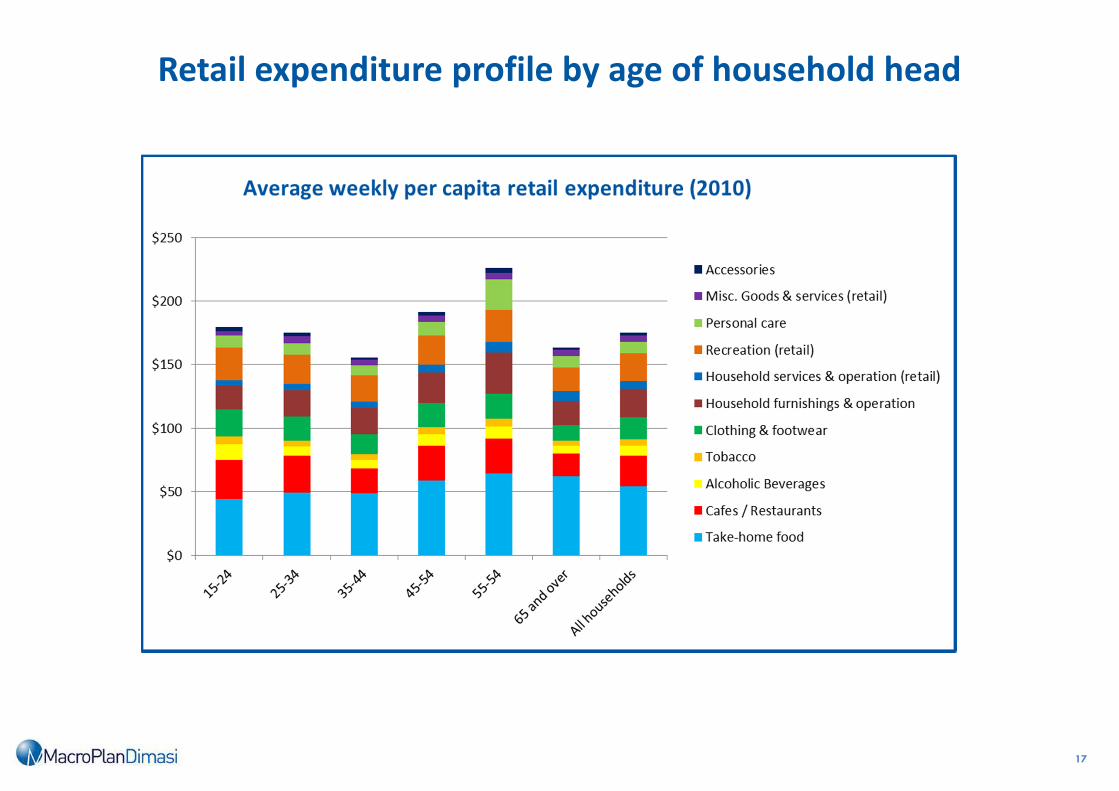

Retail expenditure profile by age of household head

18

Generational shifting – well underway

• Baby boomers : born 1946 – 64: Defined by their careers.

• Gen X : b. 1965 – 79: Seeking more “balance” in their lives.

• Gen Y : b. 1980 – 94: Millenials; KIPPERS.

• Gen Z : b. 1995 – 2009: Digital natives; Social media junkies; marketing savvy.

• Gen Alpha : b. 2010 - : Will live to 90+

19

Generational shifting

20

Generational shifting

21

Transition of (spending) power

• Baby boomers have largely driven the Australian retail market to this point

• They have given retailers loyalty and consistency, once won over

• But their influence will wane measurably over the next twenty years

• Gen Y’s and Gen Z’s combined influence will increase enormously

• Both these cohorts are much less conformist, more demanding, less loyal to “brand”

• Both are generally harder to keep as regular customers

• They are very comfortable with online shopping, but at the same time looking for more

“experiential”, more social interaction – i.e. equally open to the right bricks and mortar

offer

22

23

Globalisation of retailing

• Potentially, the recent arrivals could open in the order of 100 – 120 stores.

• These stores could attract sales of $1.5 - $2 billion, generally out of the Apparel category,

which is worth about $30 billion.

• The category has been hit hard post-GFC, compounded by a combination of consumer

disinterest and long term deflation; the new globals have added a much needed element

of excitement.

• The discount department stores in particular have suffered as a consequence of these

factors, but stand to be further hit by the new entrants.

• Not all new internationals will succeed – we have seen international failures before in

Australia.

24

Foreign invasion – how much more?

Key questions

• Which of the recent arrivals will make a big impact – and last the distance ?

• History has shown patchy results for many previous entrants.

• What happens if some of the recent (key) entrants fall over ?

Possible upside

• What about more Asian retailers, given proximity, growth of Asian economies, and

increasing proportions of Asian origin population in Australia.

• Can the recent entrants exceed expectations, and will they roll out more stores ?

• Can the recent entrants expand the category e.g. fashion, winning back household

budget share ?

Generally, though, I expect to see more and more global retailers in this country.

25

26

The role of food – retail sales Australia

Source: ABS Retail Trade Cat. 8501.0

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Mar-85 Mar-95 Mar-05 Mar-15

Food (take-home) Catered food (cafés, restaurants, take-away food)

Household goods Clothing, footwear, personal accessories

Department stores Other

$ (millions)

Food (take-

home): 41%

of total retail

turnover

Food (take-

home): 36%

of total retail

turnover

27

The role of food – regional shopping centres

28

29

Centres keep increasing in size

67,000

99,000

134,000

0

40,000

80,000

120,000

160,000

1995 2005 2015

DS DDS Smkt Mini-major Retail spec Total

Australia's Leading Regionals: Avge Size (sq.m)

• History of major

regional centres in

Australia shows they

have doubled in size

over past twenty

years.

• That increase has

occurred fairly

evenly over each of

the past two

decades

30

Shopping centre design

• Continual increases in size enable continual improvement – which is essential.

• Design has moved/is moving from functionality to creating “sense of place” (plus

functionality).

• Incorporating F&B as a main purpose – and using F&B to help create that sense of place.

• Making centres more attractive/beautiful spaces for people.

• But we remain somewhat confused, even conflicted, about main street/open air.

• A real commitment to open air design requires more creativity – and involves more

cost/greater risk (at least in the short term).

• However, the agenda can’t be dictated solely by the planning fraternity/approval

authorities – the industry needs a well thought out position.

31

www.macroplan.com.au

Melbourne

Level 4, 356 Collins Street

Melbourne VIC 3000

PH: (03) 9600 0500

Sydney

Level 4, 39 Martin Place

Sydney NSW 2000

PH: (02) 9221 5211

Brisbane

Level 15, 111 Eagle Street

Brisbane QLD 4000

PH: (07) 3221 8166

Gold Coast

Level 2 The Wave

89-91 Surf Parade

Broadbeach QLD 4218

PH: (07) 3221 8166

Perth

Ground Floor

12 St Georges Terrace

Perth WA 6000

PH: (08) 9225 7200

Adelaide

Ground Floor

89 King William Street

Adelaide SA 5000

PH: (08) 8221 6332