prol-anlassbÖrsengang/ praxisbeispiel the ipo … · 1 the ipo of vat michel gerber, head of...

TRANSCRIPT

1

The IPO of VATMichel Gerber, Head of Corporate Communications & Investor Relations

PROL-ANLASS BÖRSENGANG / PRAXISBEISPIEL

St Gallen, October 26, 2017

2

Without vacuum we wouldn’t have any of these…COMPANY HIGHLIGHTS

Solar panels

Flatscreens and displays

Health care Microchips

Electric carsSmartphones

3

VAT at a glanceCOMPANY HIGHLIGHTS

1 All numbers for FY 2016. 2 Segment net sales of business segments include intercompany sales. 3 Adjustment on Group level only.

Segment(% of total net sales)1

Segmentnet sales2 CHF 82m / +17%

Global Service

CHF 31m / -1%

IndustryValves

CHF 395m / +28%CHF 508m / +24%

Adj. EBITDA3

% margin CHF 40m / 49.4% CHF 10m / 22.1%CHF 129m / 30.3%CHF 158m / 31.1%

VAT Group AG

4

VAT’s success story over 50 years.PASSION. PRECISION. PURITY.

1965

1983

1988

2008

2009

2014

2015

VAT founded in Flawil (CH)

Acquisition of VAT by Partners Group and Capvis.

Ramp-up of manufacturing center in Malaysia

2012

Acquisition ofvacuum valvesproduct linefrom Inficon AG

Manufacturing center establ.-in Malaysia

Gate manufacturing est. in Taiwan

Acquisition ofSysmec (ROM)

Entry into thesemiconductorindustry

Establishmentof COMVAT AG

2016

IPO at SIXSwiss Exchange

5

1. READY FOR IPO1. READY FOR IPO

6

Rationale for going publicA flotation has several major advantages …

Profileü An IPO is a significant publicity event in itself, boosting

a company’s profile and credibilityü Transparency for all stakeholders such as customers

1. READY FOR IPO

Acquisition currency

ü Pay acquisitions with company sharesü Liquid paper with clear market value more attractive to

target shareholders

Funding

ü Capital increase at IPO for financing a company’s internal and external growth plans

ü Access to global equity markets and fundingü Reduced cost of capital

Monetisation / liquidity

ü Route to value realisationü Market valuation for the company and greater liquidity

for its shares, which allows shareholders to more easily sell or increase their interests

Employee incentivisation

ü Options / ESOP schemes based on publicly traded equity

ü Useful in attracting / retaining staff

… but also a number of obligations

Intense scrutiny of performance

û Reporting and disclosure requirements, certain information available to competitors

û Short termism inherent in continuing need to meet three / six monthly forecasts

û Restrictions on freedom of action

Takeover threat

û Risks of bid if sustained period of share price underperformance (although threat significantly reduced if significant (pre-IPO shareholders’) stake is retained post-IPO)

Management time / distractions

û Investor relations can absorb substantial senior management time

Expenseû Higher ongoing cost such as board, fees, investor

relations (IR), public relations (PR) etc.

7

Strong competitive position

n Innovative key market player in a (niche) sector n (Simple) business model with sustainable market position

What are the prerequisites for a successful IPO

A number of key factors should be taken into consideration when evaluating the viability of an IPO Attractive sector dynamics

1. READY FOR IPO

VATn Compelling industry dynamics and structure

– Combination of growth and healthy competitive environment– High entry barriers

Solid financial performance

n Strong long-term operating and financial track record n Easy to understand financials

Good growth and visibility

n Credible, low-risk growth prospectsn Predictability of earnings, limited volatility

Strong management

n Experienced and committed management teamn Best practices corporate governance

Timing considerations

n Market conditions n Institutional risk appetite / sentiment towards sectorn Competing new issue supply to be consideredn Availability of audited accounts

Minimum free float & capitalisation

n Minimum free float to appeal to broad range of investors and avoid liquidity discountn Dependent on listing location - typically > USD100mn Maintain financial flexibility for management to expand business

ü

ü

ü

ü

ü

ü

ü

8

Preparation for the IPO – Roadmap1. READY FOR IPO

Corporate governance and structure Strategy and

business plan

Equity Story / Positioning

Financial policy & capital structure

Financial statements

Financial reporting and controls

Indicative valuation Public Relations

and Marketing

n The IPO process will be facilitated if in the run-up to it general corporate strategy, actions and events are reviewed with the IPO in mind

n There are a number of preparatory issues that can usefully be addressed prior to the commencement of the IPO execution process

9

IPO readiness managed in 9 work streams over 7 months

1. Controlling capabilities and global finance organization

2. Governance review

3. Enterprise risk management and internal control system – The 3 lines of defence

4. Management cycle – From strategy to business plan to budget to rolling forecast, incl. Value driver tree

5. Annual report

6. Website

7. Enterprise risk management and stress test – No surprises

8. Accounting and reporting – From cost accounting to external published financial statements; consolidation and cash flow statement; external audit issues; variance analysis (price, volume, sales mix, foreign exchange,

costs)

9. Foreign exchange management and risks – Cash flow at risk, value at risk, simulations, hedging

1. READY FOR IPO

10

Financial statements

Financial policy & capital structure IPO framework Legal issues Other issues

Financial reporting and controls

Governance and Board

Forms basis of the equity story, feeds through to execution documentsn Reflect near / medium term

strategy, operational and financial goals / constraints

n Clearly identify drivers of each revenue and cost line

n Build an equity investment case, to:− Pre-empt investor concerns − Support premium valuation vs.

comparables

n Preparation of financials is a key IPO timetable critical path item

n Prospectus requires 3 years of historical audited financials− Audit of interims required

depending on timing of IPOn Detailed operating & financial review

providing narrative on divisional performance

n Set up robust financial reporting procedures, systems and controls− Systems must be proven, timely

and accuraten Financial controls cover:

− High level controls (governance, internal audit, risk management)

− IT environment / procedures− Forecasting and budgeting− Treasury− Management / statutory

reporting

n Refine capital structure, appropriate for listed company

n Establish key performance indicators expected to drive future profitability − Form basis for ongoing

presentation of financialsn Set clear financial objectives

n Determine target IPO timing and listing location

n Construct appropriate IPO syndicaten Appoint legal and accounting

advisors n Review gating items with working

group

n Share capital structure / shareholder arrangements

n Review outstanding litigation and contingent liabilities

n Construct appropriate articles of association

n Management / employee incentive schemes

n Related party transactionsn Pensions (funding position)n Property (documentation of title,

environmental issues)n Insurance policiesn Appointment of other advisers

Progress towards compliance or near-compliance with the Swiss code of best practice for Corporate Governance and Corporate Governance Directive of SIX Swiss Exchange

Business plan1 3

7 8

4

5 6

2

10

IPO preparation checklist1. READY FOR IPO

11

2. GOING PUBLIC2. GOING PUBLIC

12

Develop a compelling equity story – Investment highlights2. GOING PUBLIC

Pure play business model focused on mission-critical high-end vacuum valves1

Technology leadership resulting in long-standing, trust-based partnerships with blue-chip customers2

Undisputed no. 1 market position and high barriers to entry3

Multi-dimensional growth driven by accelerating importance of vacuum as key enabler of proliferating technologies4

Proven management team with a clear strategy and highly skilled workforce5

Best-in-class financial profile based on high profitability and strong cash flow generation through the cycle6

13

Set appropriate offer structure2. GOING PUBLIC

To ensure a smooth IPO process, key transaction parameters should be defined early in the process. However, flexibility to react to general market backdrop should be maintained

n Capitalisation– Optimize ROE for shareholders – Ensure debt financing without excessive costs or limitations – Maintain financial flexibility for management to expand business

(internal and external growth) taking into account the company’s growth trajectory and its cash generating potential going forward

– Take dividend policy into consideration

n Lock-ups– Lock-ups from company, selling shareholders and management

customary for Swiss IPOs

– Extended lock-ups can mitigate overhang-concerns to a certain extent

n Free float– The amount of capital (and votes) that should be offered to

the public at the time of the IPO should both demonstrate the commitment to manage the Issuer as a real public company and should be of significant size to ensure sufficient market liquidity and create event-status for Issuer

– Balance between liquidity / free float and pre-IPO shareholder(s) commitment, particularly in private equity exit

– Important to align investors’ and management interests: highly recommendable that company’s management retain meaningful stake post IPO

– Secondary share offering generally accepted as long as company profitable

n Listing locations / distribution– In principle, preferable to align incorporation and listing

location

– Avoid “orphan” stock syndrome

– Principle choice of distribution to be taken early in the process as it influences documentation and marketing

– Offering into the US?

– Friends and family programme?

14

Set realistic valuation expectations2. GOING PUBLIC

Key is to understand how investors will look at the investment case

n When valuing a company it is most important to understand how the market will look at the company – what valuation methodology they will use, what comparable companies, what multiple and what time period they are looking at

n This understanding is key to set realistic valuation expectations but also to refine the equity story, choose the right timing window and select the right target investors

Methodology n Which is the principle valuation methodologyn Sector specific

n Situation specific

n Comparability

n Positioning

n Sector specific

n Visibility / predictability

n Timing of the offering

Comparable

Multiple

Time period

n Who is/are the best comparables

n What is the key valuation multiple

n How will investors value unique company vs. comparable companies?

n Will investors look at current or forward year?

n How far forward will they look?

15

3. BEING PUBLIC«GOING PUBLIC» IS LIKE CLIMBING THE MATTERHORN, BUT WHAT ABOUT THE PLAN WHEN “BEING PUBLIC”?

3. BEING PUBLIC«GOING PUBLIC» IS LIKE CLIMBING THE MATTERHORN, BUT WHAT ABOUT THE PLAN WHEN “BEING PUBLIC”?

16

Thorough preparation and seamless execution strategy3. BEING PUBLIC

• Met with 29 high quality institutions in Zurich, Geneva, London and New York ahead of the intention to float announcement (ITF)− Created significant early momentum from investors (including Private Banking)

• Lead an anchor process to build a core group of institutional investors− Received significant demand indications ahead of launch, further de-risking the process

• Extensive pre-deal investor education provided detailed valuation feedback with numerous early order indications enabling syndicate banks to build a solid shadow book ahead of launch

IPO execution

• Overall, VAT’s management met with c. 240 investors in Switzerland, UK, US, Germany and France in an extensive 10-day roadshow, with 54 one-on-one sessions and 11 group meetings/calls

• Bank internal Private Banking distribution power was instrumental to the IPO, submitting the by far largest order in the book on the first day of bookbuilding, thus de-risking the execution and generating early momentum

• In the final phase of the bookbuilding, banks effectively communicated price guidance and early books close message in order to drive demand and price momentum

Extensive early investor engagement pre-launch

Successful post-launch marketing

Effective price guidance

Successful outcome for VAT

• Successfully positioned VAT away from selected vacuum component and semiconductor capital equipment peers towards Swiss best-in-class industrial peers

• Priced at the top end of the initial price range despite more volatile market conditions during bookbuilding and some comparable companies trading down

− 11.9x in terms of EV/EBITDA 2016E(1) and 4.8% dividend yield 2016E(2)

Largest EMEA IPO in 2016 up to that day with seamless execution

• Equity story / positioning• Early alignment of all key parties

Pre-IPO preparation

1 Based on syndicate research analyst estimates.2 Assuming dividend of CHF 65m out of reserves from capital contributions for FY16.

17 17

Life as a public company - understanding and managing your audience

Effective identification and targeting of key

investors

Effective communication with investors

Release of trading / results statements

Managing guidance

Dealing with sell-side analysts

Understanding institutional investors

“Underpromise and overdeliver!”

External stakeholders such as shareholders, potential new investors, analysts, press, employees, clients will all take a much more active interest in any communication once the company is public. Hence, effective PR and IR will be of utmost importance

3. BEING PUBLIC

18

A different corporate life3. BEING PUBLIC

1. Professional management – on all levels

2. Clearly defined management processes

3. Policies, rules and regulations which enforce and enable these processes

4. Open and honest communication vis-à-vis all stakeholders

5. Delivery of strong short-term results and creation of mid- and long-term value

6. Capital structure and dividend payments in accordance with shareholders’ and company’s interests

19

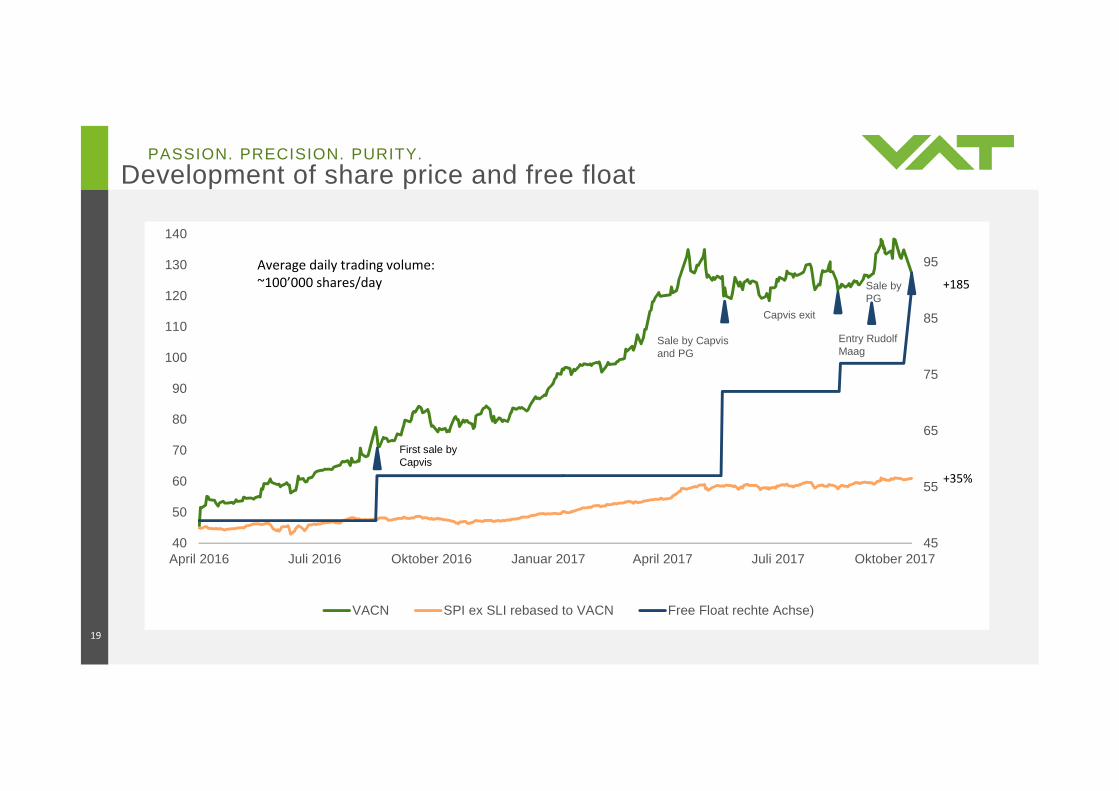

Development of share price and free floatPASSION. PRECISION. PURITY.

45

55

65

75

85

95

40

50

60

70

80

90

100

110

120

130

140

April 2016 Juli 2016 Oktober 2016 Januar 2017 April 2017 Juli 2017 Oktober 2017

VACN SPI ex SLI rebased to VACN Free Float rechte Achse)

+185

+35%

Average daily trading volume: ~100’000 shares/day

First sale by Capvis

Sale by Capvis and PG

Capvis exit

Entry Rudolf Maag

Sale byPG