professor john zietlow mba 621 spring 2006 present value chapter 3

TRANSCRIPT

Professor John ZietlowMBA 621

Professor John ZietlowMBA 621

Spring 2006Spring 2006

Present ValuePresent Value

Chapter 3Chapter 3

Chapter 3 OverviewChapter 3 Overview•3.1 The Theory of Present Value

– Borrowing, Lending and Consumption Opportunities– How Financial Markets Improve Welfare

•3.2 Future Value of a Lump Sum Amount– The Concept of Future Value– The Equation for Future Value– A Graphic View of Future Value

•3.3 Present Value of a Lump Sum Amount– The Concept of Present Value– The Equation for Present Value– A Graphic View of Present Value

•3.4 Future Value of Cash Flow Streams– Finding the Future Value of a Mixed Stream– Types of Annuities– Finding the Future Value of an Ordinary Annuity– Finding the Future Value of an Annuity Due– Comparison of an Ordinary Annuity with an Annuity Due

Chapter 3 OverviewChapter 3 Overview

•3.5 Present Value of Cash Flow Streams– Finding Present Value of a Mixed Stream– Finding the Present Value of an Ordinary Annuity– Finding the Present Value of an Annuity Due– Finding the Present Value of a Perpetuity– Finding the Present Value of a Growing Perpetuity

•3.6 Special Applications of Time Value– Compounding More Frequently than Annually– Nominal and Effective Annual Rates of Interest– Deposits Needed to Accumulate a Future Sum– Loan Amortization

•Appendix: Additional Special Applications of Time Value– Interest or Growth Rates– Determining the Number of Time Periods

The Focus on Present ValueThe Focus on Present Value

• Chapter describes how to account for time value of money in financial decision-making– Begins with finding future value of sum invested today– Finance uses compound rather than simple interest– Compound interest causes sum to grow very large with time

• Focus on present value: value of future CF measured today– Permits comparing values of CFs received at different times

• Present value concepts & calculations pervade finance– Managers use PV to evaluate capital investments– Investors use PV to value securities

• Begin with simplest cases--single cash flows– Then study complex, multiple CF streams

• A time line can be used to show CFs graphically

Using Timelines To Demonstrate Future Value And Present Value

Using Timelines To Demonstrate Future Value And Present Value

• Time period 0 is today; others represent future period-ends– Unless stated otherwise, period means year (end-of-year)– So t=1 is end of year 1; t=5 is end of year five

• Negative values represent cash outflows– Positive values represent cash inflows

• FV uses compounding to find terminal value of CFs – What is value in 5 years of $1 invested at 6% annual interest?

• PV uses discounting to find today’s value of future CFs– What is today’s value of $1 to be received in 5 years at a 6%

discount rate?• FV and PV can be computed in several ways

– Using financial calculators or computer spreadsheets– Using tables with present & future value factors (PVIF, FVIF)

Timeline Illustration of Future Value and Present Value

Timeline Illustration of Future Value and Present Value

Present Value

Present Value

0 1 2 3 4 5

-$10,000 $3,000 $5,000 $4,000 $3,000 $2,000

Discounting

End of Year

FutureValue

FutureValue

Compounding

Future Value Concepts & TermsFuture Value Concepts & Terms

• Basic Terminology of Future Value– Interest rate (r) is the annual rate of interest paid on the

principal amount. Also called compound annual interest– Present Value (PV) in this setting is the initial investment

amount (principal) on which interest is paid. In other cases, PV is the discounted present value of a future sum or sums

– Future Value (FV) is computed by applying annual interest to a principal amount over a specified period of time

– Number of compounding periods (n) is the number of years the principal will earn interest

• Basic formula for the end-of-period n future value of a sum invested today at interest rate r is:

• FVn = PV x (1 + r)n

Time Line for $78.35 Invested for Five Years at 5% Interest

Time Line for $78.35 Invested for Five Years at 5% Interest

0 1 2 3 4 5

PV = $78.35

FV5 = $100

End of Year

Demonstrating Simple (One CF) Future Value Computations

Demonstrating Simple (One CF) Future Value Computations

• Compute the FV of a $50 sum deposited at 4% interest at the end of years 1, 2, 3, and 4:

– FV end of year 1 = $50 x (1+ 0.04) = $52

– FV end of year 2 = $52 x (1.04) = $50 x (1.04)2 = $54.08

– FV end of year 3 = $54.08 x (1.04) = $50 x (1.04)3 = $56.24

– FV end of year 4 = $56.24 x (1.04) = $50 x (1.04)4 = $58.49• With compound interest, you earn interest on interest, so

FV can reach large amounts relatively quickly:– FV end of year 9 = $50 x (1.04)9 = $71.16– FV end of year 15 = $50 x (1.04)15 = $90.05– FV end of year 30 = $50 x (1.04)30 = $162.17

Simple Future Value Computations (Continued)

Simple Future Value Computations (Continued)

• Find the FV of $3,000 invested at 3.25% interest for 3 years:

• FV3 = PV x (1 + r)n = $3,000 (1.0325)3 = $3,302.11

• Find the FV of $735.5 invested at 6.35% for 5 years:

• FV5 = $735.5 x (1.0635)5 = $1000.62

• Find the FV of $100 invested at 6% for 15 months [Hint: 15 months can be specified as 1.25 years]:

• FV1.25 = $100 x (1.06)1.25 = $107.55

• Find the FV of $5,000 invested at 6.74% for 8 years, 3 months [Hint: express 3 months as 3/12=0.25 year]:

• FV8.25 = $5,000 (1.0674)8.25 = $8,536.86

• At high interest rates, FV builds up very fast !

The Power Of Compound Interest: Future Value Of $1 Invested At Different Interest Rates

The Power Of Compound Interest: Future Value Of $1 Invested At Different Interest Rates

Periods

0%Fu

ture

Va

lue

of

On

e D

ol la

r ($

)

1.000 2 4 6 8 10 12 14 16 18 20 22 24

10.00

15.00

20.00

25.00

30.00

5.00

10%

5%

15%

20%

Computing Future Values Algebraically And Using FVIF Tables

Computing Future Values Algebraically And Using FVIF Tables

• You deposit $1,000 today at 3% interest.

• How much will you have in 5 years?

• Could solve this using basic FV formula:

– FVn = PV x (1+r)n = $1,000 x (1.03)5 = $1159.27

• Or could use future value interest factor formula and table

– FV5 = PV x FVIFr%,n = $1,000 x FVIF3%,5

• Look up FVIF6%,5 in Future Value Interest Factor table

FVIF3%,5 = 1.159

FV5 = $1,000 x 1.159 = $1,159

Format Of A Future Value Interest Factor (FVIF) Table

Format Of A Future Value Interest Factor (FVIF) Table

Period 1% 2% 3% 4% 5% 6% 1 1.010 1.020 1.030 1.040 1.050 1.060 2 1.020 1.040 1.061 1.082 1.102 1.124 3 1.030 1.061 1.093 1.125 1.158 1.191 4 1.041 1.082 1.126 1.170 1.216 1.262 5 1.051 1.104 1.159 1.217 1.276 1.338 6 1.062 1.126 1.194 1.265 1.340 1.419 7 1.072 1.149 1.230 1.316 1.407 1.504

Computing Future Values Using ExcelComputing Future Values Using Excel

PV 1,000$ r 3.00%n 5FV? $1,159.3

Excel Function

=FV (interest, periods, pmt, PV)

=FV (.03, 5, 1000)

You deposit $1,000 today at 3% interest.

How much will you have in 5 years?

Present ValuePresent Value

• Present value is the current dollar value of a future amount

of money.

• It is based on the idea that a dollar today is worth more

than a dollar tomorrow.

• It is the amount today that must be invested at a given rate

to reach a future amount.

• It is also known as discounting, the reverse of

compounding.

• The discount rate is often also referred to as the

opportunity cost, the discount rate, the required return, and

the cost of capital.

The Logic Of Present ValueThe Logic Of Present Value

• Assume you can buy an investment that will pay $1,000 one

year from now

• Also assume you can earn 3.15% on equally risky

investments

• What should you pay for this opportunity?

• Answer: Find how much must be invested today at 3.15% to

have $1,000 in one year

PV x (1 + 0.0315) = $1,000

• Solving for PV gives:

46.969)0315.1(

000,1$

PV

Calculating The PV Of A Single AmountCalculating The PV Of A Single Amount

• The present value of a future amount can be found

mathematically by using this formula:

• Find the present value of $500 to be received in 7 years,

assuming a discount rate of 6%.

• Substitute FV7 = $500, n = 7, and r = .06 into PV formula

nnn

n

rFV

r

FVPV

)1(

1

)1(

53.332$503.1

500$

)06.1(

500$PV

7

Present Value of $500 to be Received in 7 Years at a 6% Discount Rate

Present Value of $500 to be Received in 7 Years at a 6% Discount Rate

0 1 2 3 4 5 6 7

PV = $332.53

FV7 = $500End of Year

Format Of A Present Value Factor (PVF) Table

Format Of A Present Value Factor (PVF) Table

Period 1% 2% 3% 4% 5% 6% 1 0.990 0.980 0.971 0.962 0.952 0.943 2 0.980 0.961 0.943 0.925 0.907 0.890 3 0.971 .942 0.915 0.889 0.864 0.840 4 0.961 0.924 0.888 0.855 0.823 .792 5 0.951 0.906 0.863 0.822 0.784 0.747 6 0.942 0.888 0.837 0.790 0.746 0.705 7 0.933 0.871 0.813 0.760 0.711 0.665

Calculating Present Value Of A Single Amount Using A Spreadsheet

Calculating Present Value Of A Single Amount Using A Spreadsheet

Example: How much must you deposit today in order to

have $500 in 7 years if you can earn 6% interest on your

deposit?

FV 500$ r 6.00%n 7PV? $332.5

Excel Function

=PV (interest, periods, pmt, FV)

=PV (.06, 7, 500)

The Power Of High Discount Rates: Present Value Of $1 Invested At Different Interest Rates

The Power Of High Discount Rates: Present Value Of $1 Invested At Different Interest Rates

Periods

Pre

sen

t V

a lu

e o

f O

ne

Do

llar

($)

0 2 4 6 8 10 12 14 16 18 20 22 24

0.5

0.75

1.00

0.25 10%

5%

15%20%

0%

Finding The Future Value Of Cash Flow Streams (Multiple Cash Flows)

Finding The Future Value Of Cash Flow Streams (Multiple Cash Flows)

• Two basic types of cash flows streams are observed:– A mixed stream has uneven cash flows (no pattern)– An annuity has equal annual cash flows

• Either type can represent cash inflows (receipts) or cash outflows (payments)

• FV of a stream equals sum of FVs of individual cash flows

• Basic formula for the FV of a stream (FVMn), where CFt equals a cash flow at end of year t:

FVMn = CF1 (1 +r)n-1 + CF2 (1 + r)n-2 + … + CFn (1 + r)n-n

n

t

nt rCF

1

1)1(

Finding The FV Of A Mixed StreamFinding The FV Of A Mixed Stream

• Find the end of year 5 future value of the following cash flows, which are invested at 5.5% annual interest (r=5.5%, n=5)– End of year 1: $3,500 (invested for four years)– End of year 2: $3,800 (invested for three years)– End of year 3: $2,000 (invested for two years)– End of year 4: $3,000(invested for one year)– End of year 5: $2,500 (invested for 0 year)

• Use FVMn formula to calculate terminal (future) value:

FVMn = CF1 (1 + r)n-1 + CF2 (1 + r)n-2 + … + CFn (1 + r)n-n

= $3,500 (1.055)4 + $3,800 (1.055)3 + $2,000(1.055)2 +

$3,000(1.055)+ $2,500 (1.00)

= $4,335.89 + $4,462.12 + $2,226.05 + $3,165+ $2,500

= $16,689.06

Future Value, at the end of 5 Years of a Mixed Cash Flow Stream Invested at 5.5%

Future Value, at the end of 5 Years of a Mixed Cash Flow Stream Invested at 5.5%

FV5 = $16,689.06

0 1 2 3 4 5

$3,500 $3,800 $2,000 $3,000 $2,500

$4,335.89

$4,462.12

$2,226.06

$3,165.00

$2,500.00

End of Year

The Future Value of An AnnuityThe Future Value of An Annuity

• Annuities are extremely important in finance– Virtually all bond interest payments structured as annuities– Many capital investment projects have annuity-like cash flows

• Two types of annuities: ordinary annuity & annuity due – Ordinary annuity: payments occur at end of period– Annuity due: payments occur at beginning of period

• FV of annuity due always higher than FV of ordinary annuity– Since CF invested at beginning--rather than end--of period, all

CFs earn one more period’s interest• Unless otherwise stated, will assume an ordinary annuity

– Much more commonly observed in actual finance practice

Finding the Future Value Of An Ordinary Annuity

Finding the Future Value Of An Ordinary Annuity

• FV of annuity (FVA) can be found as with FVM– Find FV of individual amounts, then sum FVs– Demonstrated with timeline (next slide)

• Since an annuity has equal payments,

CF1 = CF2 = CFn = PMT, can simplify FVM formula

• Express FV of annuity as the product of the payment amount (PMT) times the sum of the FV factors

• Summation term to the right of PMT is the future value interest factor of an annuity (FVIFAr,n)

1

1

)1(

tn

tn rPMTFVA

Calculating The Future Value of An Ordinary Annuity

Calculating The Future Value of An Ordinary Annuity

• How much will your deposits grow to if you deposit $1,000 at the end of each year at 4.3% interest for 5 years.

• Can show computation of FVA as sum of individual FVs:

FVA = $1,000 (1.043)4 + $1,000 (1.043)3 + $1,000 (1.043)2 +

$1,000 (1.043) + $1,000 (1.0)

= $1,000 (1.1834) + $1,000 (1.1346) + $1,000

(1.0878) +

$1.000 (1.043) + $1,000 (1.0) = $5,448.8

• Or can multiply payment times sum of FV factors:

FVA = $1,000 (1.1834 + 1.1346 + 1.0878 + 1.043 + 1.0)

= $1,000 (5.4488) = $5,448.8

Future Value, at the end of 5 Years of an Annuity Investing $1,000 per year at 4.3%Future Value, at the end of 5 Years of an

Annuity Investing $1,000 per year at 4.3%

FV5 = $5,448.8

0 1 2 3 4 5

$1,000 $1,000 $1,000 $1,000 $1,000

$1,183.4

$1,134.6

$1,087.8

$1,043.0

$1,000.0

End of Year

Finding The Future Value Of An Ordinary Annuity Using A Spreadsheet

Finding The Future Value Of An Ordinary Annuity Using A Spreadsheet

PMT 1,000$ r 4.3%n 5FV? $5,448.8

Excel Function

=FV (interest, periods, pmt, PV)

=FV (.043, 5,1000 )

How much will your deposits grow to at the end of five years if

you deposit $1,000 at the end of each year at 4.3% interest for 5

years?

Cash Flows Of An Ordinary Annuity Versus An Annuity Due

Cash Flows Of An Ordinary Annuity Versus An Annuity Due

Comparison of ordinary Annuity and Annuity Due Cash Flows ($1,000, 5 Years)

Annual Cash Flows

0 $ 0 $1,000

1 1,000 1,000

2 1,000 1,000

3 1,000 1,000

4 1,000 1,000

5 1,000 0

Total $5,000 $5,000

End of yeara Annuity A (ordinary) Annuity B (annuity due)

aThe ends of years 0, 1,2, 3, 4 and 5 are equivalent to the beginnings of years 1, 2, 3, 4, 5, and 6 respectively

Calculating The Future Value Of An Annuity Due

Calculating The Future Value Of An Annuity Due

)1()1( due)annuity ( 1

1

rrPMTFVA tn

tn

tn

t

rPMT )1( 1

• Equation for the FV of an ordinary annuity can be converted into an expression for the future value of an annuity due,

FVAn (annuity due), by merely multiplying it by (1 + r)

Future Value, at the end of 5 Years of an Annuity Due Investing $1,000 per year at 4.3%

Future Value, at the end of 5 Years of an Annuity Due Investing $1,000 per year at 4.3%

FV5 = $5,683.1

0 1 2 3 4 5

$1,000 $1,000 $1,000 $1,000 $1,000

$1,234.30

$1,183.41

$1,134.60

$1,087.80

$1,043.00

End of Year

Finding The Future Value Of An Annuity Due Using A Spreadsheet

Finding The Future Value Of An Annuity Due Using A Spreadsheet

• How much will your deposits grow to at the end of five years

if you deposit $1,000 at the beginning of each year at 4.3%

interest for 5 years?

PMT $1,000r 4.30%n 5FV $5,448.89FVA? $5,683.19

Excel Function

=FV (interest, periods, pmt, PV)

=FV (.043, 5, 1,000 )

=$5,448.89*(1.043)

The Present Value Of A Mixed StreamThe Present Value Of A Mixed Stream

• Continuing to let CFt represent the cash flow at the end of year t, the present value of an n-year mixed stream of cash flows, PVMn, can be expressed as:

nn2211n )r1(

1CF

)r1(

1CF

)r1(

1CFPVM

t1

n

1t )r1(

1CF

n,r1

n

1t

PVIFCF

Calculating The PV Of A Mixed StreamCalculating The PV Of A Mixed Stream

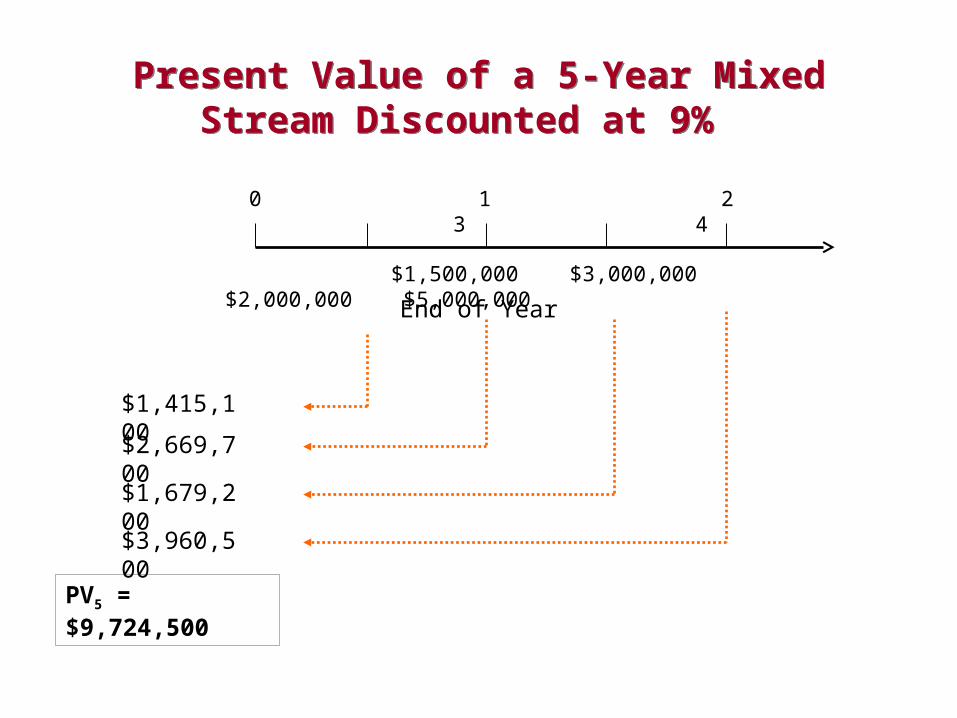

• Assume you must find the PV of the following year-end cash flows, if the discount rate is 6%:– End of year 1: $1,500,000 End of year 2: $3,000,000– End of year 3: $2,000,000 End of year 4: $5,000,000

• Plug year-end cash flows into PVM formula, with k=9%:

3214 )06.1(

1000,000,2$

)06.1(

1000,000,3$

)06.1(

1000,500,1$ PVM

4)06.1(

1000,000,5$

PVM4 = $1,500,000 (0.9434) + $3,000,000 (0.8899)

+ $2,000,000 (0.8396) + $5,000,000 (0.7921) = $9,724,500

Present Value of a 5-Year Mixed Stream Discounted at 9%

Present Value of a 5-Year Mixed Stream Discounted at 9%

$1,500,000 $3,000,000 $2,000,000 $5,000,000

End of Year

PV5 = $9,724,500

$1,415,100

$2,669,700

$1,679,200

$3,960,500

0 1 2 3 4

Finding The PV Of An Ordinary AnnuityFinding The PV Of An Ordinary Annuity

• Since, for an annuity, PMT = CF1 = CF2 = …… = CFn, the PVMn formula can be modified to compute the present value of an n-year annuity, PVAn.

• The rightmost term is the formula for the present value interest factor for an annuity, PVIFAr,n

• If PMT = $1,250, n = 6 years, and r = 5%, find PVA6:

PVA6 = PMT x PVIFA5%,6 = $1,250 x 5.0757 = $6,344.625

nrt

n

tn PVIFAPMT

rPMTPVA ,

1 )1(

1

Present Value of a 6-Year Mixed Stream Discounted at 5%

Present Value of a 6-Year Mixed Stream Discounted at 5%

$1,250 $1,250 $1,250 $1,250 $1,250 $1,250

End of Year

PV5 = $6,344.6

$1,190.476

$1,133.787

$1,079.797

$1,028.378

0 1 2 3 4 5 6

$979.407

$932.769

Calculating The PV Of A PerpetuityCalculating The PV Of A Perpetuity

• Frequently need to calculate the PV of a perpetuity--a stream of equal annual cash flows that lasts “forever”

– Most common finance example: valuing preferred stock

• Can modify the basic PVAn formula for n = (infinity):

• The summation term reduces to 1/r, so PVA simplifies to:

PVA = PMT x 1/r =

• Assume a preferred stock pays $1.5/share, and the appropriate discount rate is r = 0.07. Find stock’s PV:

PVA = PMT x 1/r = = $1.5 x (14.286) = $21.43

tt r

PMTPVA)1(

1

1

r

PMT

07.0

50.1$

Compounding More Frequently Than Annually

Compounding More Frequently Than Annually

• Can compute interest with semi-annual, quarterly, monthly (or more frequent) compounding periods– Semi-annual interest computed twice per year– Quarterly interest computed four times per year

• To change basic FV formula to m compounding periods:– Divide interest rate r by m and– Multiply number of years n by m

• Basic FV formula becomes:

nm

n m

rPVFV

1

Demonstrating Compounding More Frequently Than Annually

Demonstrating Compounding More Frequently Than Annually

• Find FV at end of 2 years of $125,000 deposited at 5.13 percent interest

• For semiannual compounding, m equals 2:

• For quarterly compounding, m equals 4:

93.326,138$02565.01000,125$2

0513.01000,125$ 4

22

2

FV

687.415,138$0128.01000,125$4

0513.01000,125$ 8

24

2

FV

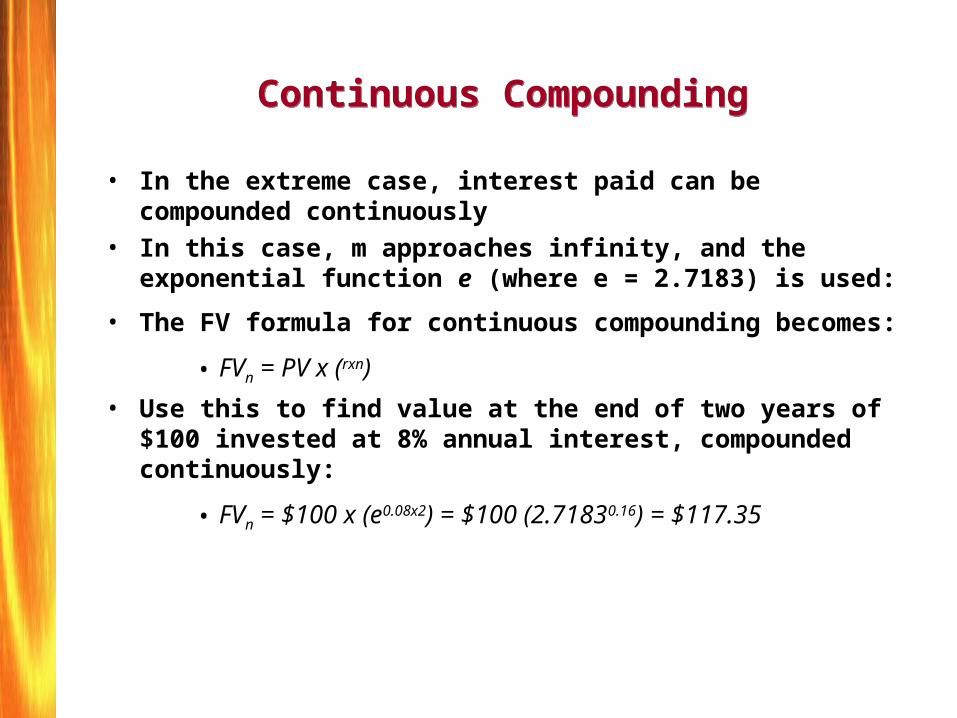

Continuous CompoundingContinuous Compounding

• In the extreme case, interest paid can be compounded continuously

• In this case, m approaches infinity, and the exponential function e (where e = 2.7183) is used:

• The FV formula for continuous compounding becomes:

• FVn = PV x (rxn)

• Use this to find value at the end of two years of $100 invested at 8% annual interest, compounded continuously:

• FVn = $100 x (e0.08x2) = $100 (2.71830.16) = $117.35

A Basic Result: The More Frequent The Compounding Period, The Larger The FVA Basic Result: The More Frequent The

Compounding Period, The Larger The FV

• FV of $100 at end of 2 years, invested at 8% annual interest,

compounded at the following intervals:

– Annually: FV = $100 (1.08)2 = $116.64

– Semi-annually: FV = $100 (1.04)4 = $116.99

– Quarterly: FV = $100 (1.02)8 = $117.17

– Monthly: FV = $100 (1.0067)24 = $117.30

– Continuously: FV = $100 (e 0.16) = $117.35

The Nominal (Stated) Annual Rate Versus The Effective (True) Annual Interest RateThe Nominal (Stated) Annual Rate Versus The Effective (True) Annual Interest Rate

• Nominal, or stated, rate is the contractual annual rate charged by a lender or promised by a borrower– Does not reflect compounding frequency

• Effective rate – the annual rate actually paid or earned– Does reflect compounding frequency

• Can make substantial difference at high interest rates. Credit cards often charge 1.5% per month:– Looks like 12 months/year x 1.5%/month = 18% per year– Actual rate (1.015)12 = 1.1956-1 = 0.1956 = 19.56% per year

11

m

m

rEAR

Effective Rates Are Always Greater Than Or Equal To Nominal Rates

Effective Rates Are Always Greater Than Or Equal To Nominal Rates

• For annual compounding, effective = nominal

• For semi-annual compounding

• For quarterly compounding

%0.808.0)08.01(11

08.01

1

EAR

%16.80816.010816.112

08.01

2

EAR

%24.80824.010824.114

08.01

4

EAR

Special Applications Of Time Value: Deposits Needed To Accumulate A Future Sum

Special Applications Of Time Value: Deposits Needed To Accumulate A Future Sum

• Frequently need to determine the annual deposit needed to accumulate a fixed sum of money so many years since

• This is closely related to the process of finding the future value of an ordinary annuity

• Can find the annual deposit required to accumulate FVAn dollars, given a specified interest rate, r, and a certain number of years, n by solving this equation for PMT:

nr,

n

n

1t

1t

n

FVIFA

FVA

r)(1

FVA

PMT

Calculating Deposits Needed To Accumulate A Future Sum

Calculating Deposits Needed To Accumulate A Future Sum

• Suppose a person wishes to buy a house 5 years from nowand estimates an initial down payment of $35,000 will berequired at that time.

• She wishes to make equal annual end-of-year deposits in an account paying annual interest of 4 percent, so she must determine what size annuity will result in a lump sum equal to $35,000 at the end of year 5.

• Find the annual deposit required to accumulate FVAn dollars, given an interest rate, r, and a certain number of years, n by solving equation PMT:

98.461,6$4163.5

000,35$

5%,4

5 FVIFA

FVAPMT

A Loan Amortization TableA Loan Amortization Table

Loan Amortization Schedule ($6,000 Principal, 10% Interest 4 Year Repayment Period

Payments

1 $1,892.74 $6,000 $600 $1,292.74 $4,707.26

2 1,892.74 4,707.26 470.73 1,422.01 3,285.25

3 1,892.74 3,285.25 328.53 1,564.21 1,721.04

4 1,892.74 1,721.04 172.10 1,720.64 -a

End of

year

aDue to rounding, a slight difference ($.40) exists between beginning-of-year 4 principal (in column 2) and the year-4 principal payment (in column 4)

Loan Payment

(1)

Beginning-of-year

principal(2)

Interest[.10 x (2)]

(3)

Principal[(1) – (3)]

(4)

End-of-year principal[(2) – (4)]

(5)

Determining Growth RatesDetermining Growth Rates

1997 1,000$ 1998 1,127 1999 1,158 2000 2,345 2001 3,985 2002 4,677 2003 5,525

It is first important to notethat although there are 7

years show, there are only 6time periods between the

initial deposit and the final value.

At times, it may be desirable to determine the compound interest

rate or growth rate implied by a series of cash flows. For example, assume you invested $1,000 in a mutual fund in

1997 which grew as shown in the table below. What compound growth rate did this investment achieve?

Determining Growth Rates (Continued)Determining Growth Rates (Continued)

This chart shows that $1,000 is the present value, the future

value is $5,525, and the number of periods is 6. Want to find the rate, r, that would cause $1,000 to grow to

$5,525 over a six-year compounding period. Use FV formula: FV= PV x (1+r)n $5,525=$1,000 x (1+r)6

Simplify & rearrange: (1+r)6 = $5,525 $1,000 = 5.525 Find sixth root of 5.525 (Take yx, where x=0.16667), subtract 1 Find r = 0.3296, so growth rate = 32.96%

Excel Function

=Rate(periods, pmt, PV, FV)

=Rate(6, ,1000, 5525)

1997 1,000$ 1998 1,127 1999 1,158 2000 2,345 2001 3,985 2002 4,677 2003 5,525

Much Of Finance Involves Finding Future And (Especially) Present Values

Much Of Finance Involves Finding Future And (Especially) Present Values

Central To All Financial Valuation Techniques

Techniques Used By Investors & Firms Alike

Chapter 4: Bond & Stock Valuation

Chapters 7-9: Capital Budgeting