prof vedolin presentation sqa 23july2014 - c.ymcdn.com · sqa 23july2014. introduction introduction...

TRANSCRIPT

M alkhozov,M ueller,Vedolin & Venter– 1

InternationalFunding Liquidity

Aytek M alkhozov

M cGill

Philippe M ueller

LSE

Andrea Vedolin

LSE

GyuriVenter

CBS

SQ A

23 July 2014

Introduction

Introduction

W hatwe do

W hatwe find

Illiquidity Proxies

M odel

Em piricalAnalysis

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 2

W hatwe do

M alkhozov,M ueller,Vedolin & Venter– 3

Providem easuresofcountry-leveland globalfunding illiquidity.

– 6 countries:Canada,Germ any,Japan,Switzerland,UK,US.

– M easuring noisein localyield curves,following Hu,Pan and W ang (2013).

Study thee ectthatthevariation in illiquidity overtim eand acrosscountrieshason internationalstock returns.

– Stylized internationalCAPM augm ented by m argin constraints,sim ilartoFrazziniand Pedersen (2013),to derivetestablepredictions.

– Study im pactofilliquidity on intercept/slopeofthesecurity m arketline.

– Exam ineperform anceofilliquidity/beta-sorted portfolios.

– M arket-neutraltrading strategies:Long levered high illiquidity-to-beta stocksand shortde-levered low illiquidity-to-beta stocks(BAIL).

W hatwe find

M alkhozov,M ueller,Vedolin & Venter– 4

Variation in liquidity m easurescan berelated to key m arketevents.

High correlation between localilliquidityindices,especiallyduring crisisperiods,butalso largeidiosyncraticfluctuations.

Globalilliquidity flattenstheSM L and increasesitsintercept.

Cross-country di erencein localilliquiditiesdrivesalphas.

Taking illiquidity into accountim provestheperform anceofthebetting-against-beta (BAB)strategy.

Illiquidity M easures

Introduction

Illiquidity Proxies

M otivation

Data

Term Structure

Sum m ary Stats

Correlations

Crisis

GlobalIlliquidity

M odel

Em piricalAnalysis

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 5

M otivation

M alkhozov,M ueller,Vedolin & Venter– 6

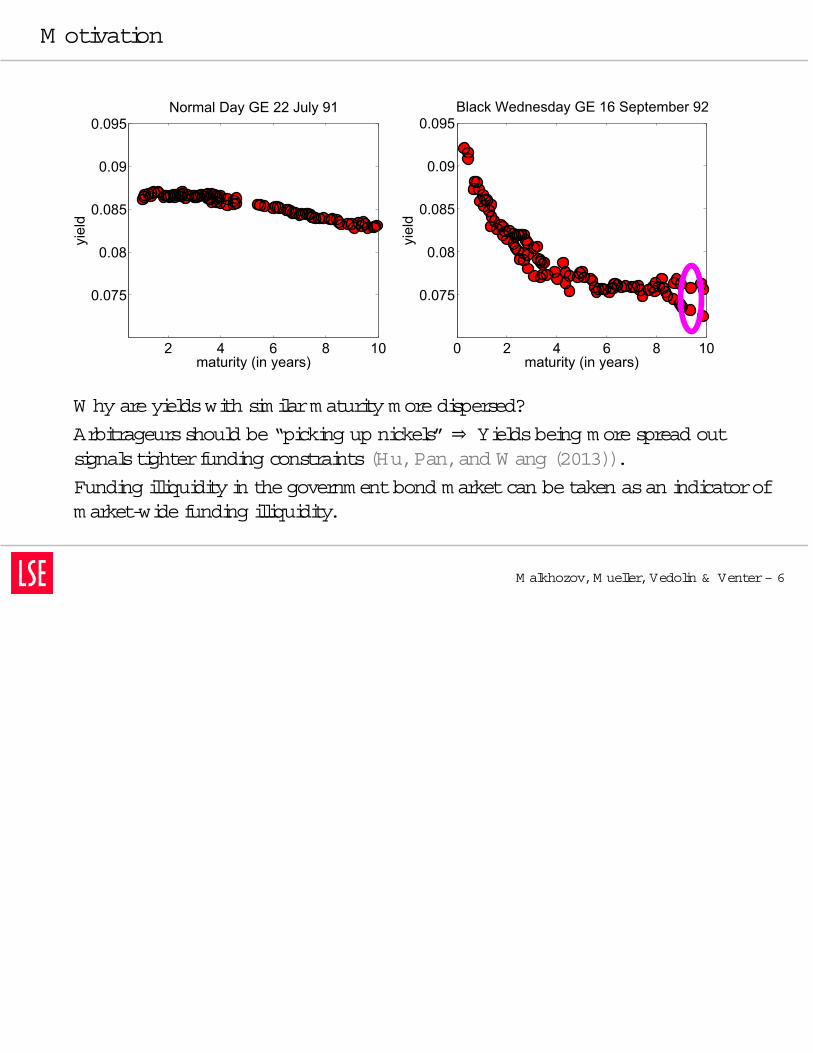

2 4 6 8 10

0.075

0.08

0.085

0.09

0.095Normal Day GE 22 July 91

maturity (in years)

yiel

d

0 2 4 6 8 10

0.075

0.08

0.085

0.09

0.095Black Wednesday GE 16 September 92

maturity (in years)

yiel

d

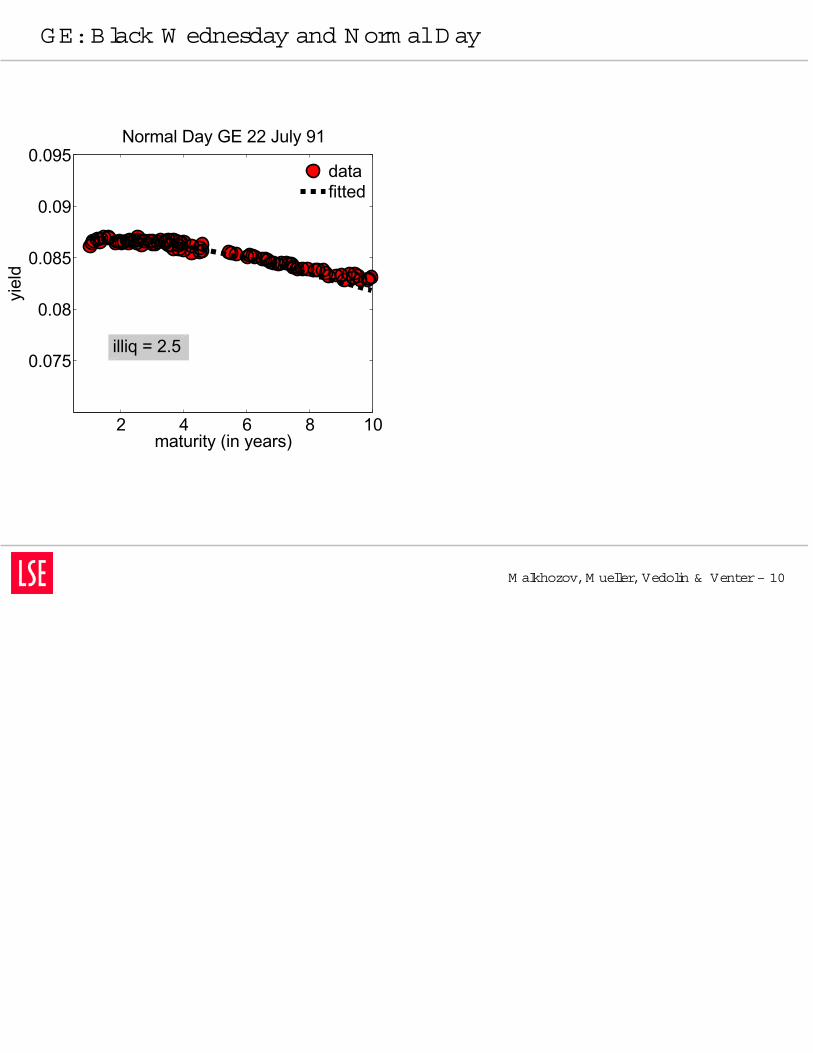

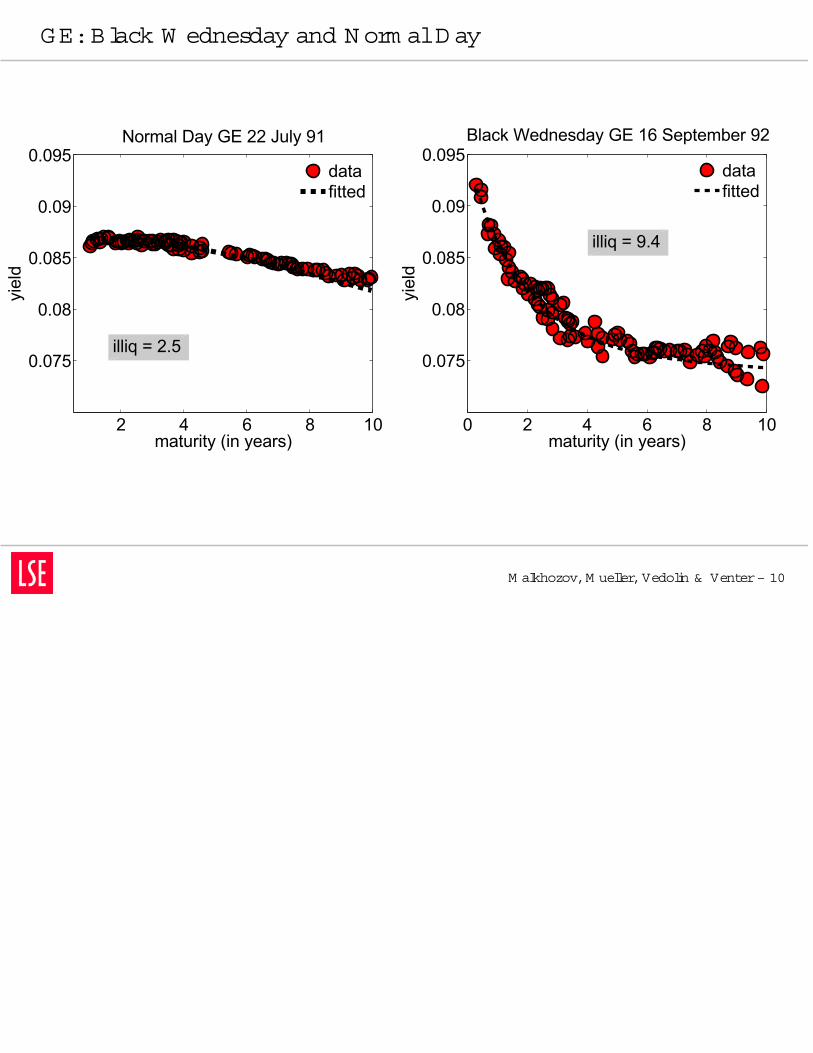

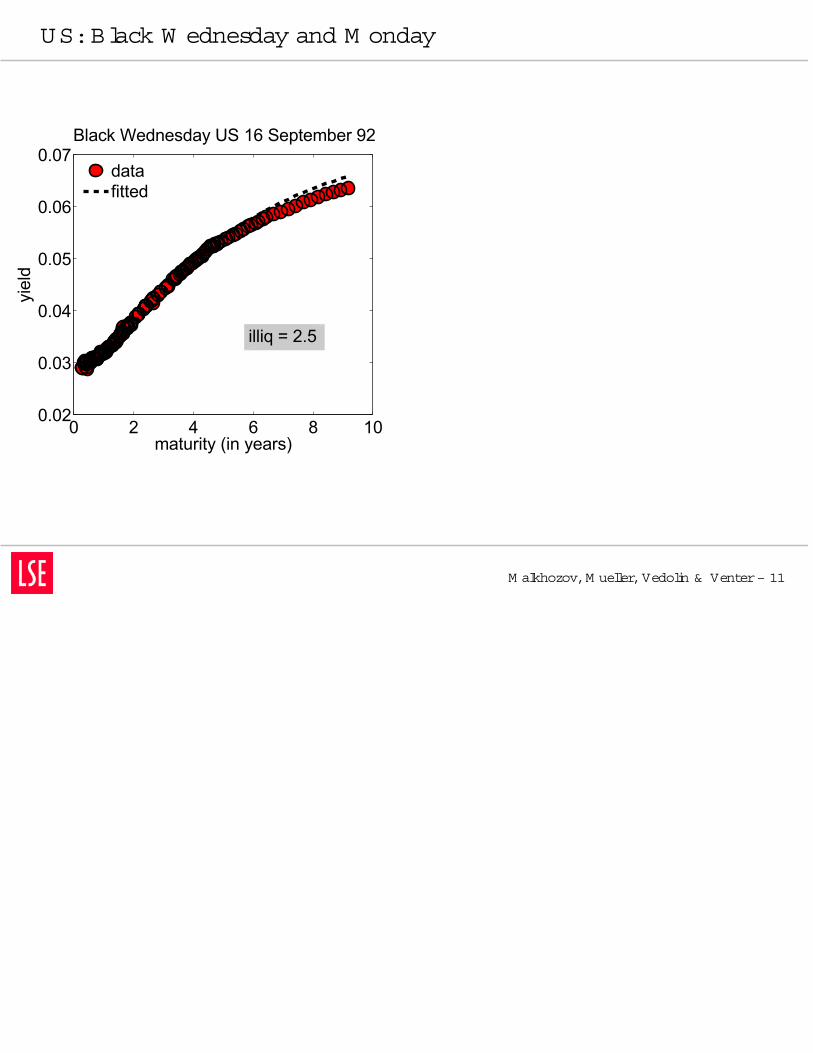

W hy areyieldswith sim ilarm aturity m oredispersed?

Arbitrageursshould be“picking up nickels”⇒ Yieldsbeing m orespread outsignalstighterfunding constraints(Hu,Pan,and W ang (2013)).

Funding illiquidityin thegovernm entbond m arketcan betaken asan indicatorofm arket-wide funding illiquidity.

D ata

Introduction

Illiquidity Proxies

M otivation

Data

Term Structure

Sum m ary Stats

Correlations

Crisis

GlobalIlliquidity

M odel

Em piricalAnalysis

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 7

W e study 6 countries:Canada,Germ any,Japan,Switzerland,UK,US.

W e usedaily bond data from Datastream .W eapply severaldatafiltersin orderto obtain securitieswith sim ilarliquidityandavoiding specialfeatures.

– W e excludebondswith option likefeatures.– W e consideronly securitieswith a m aturity ofm orethan one

yearatissue.– W e also excludebondswith a rem aining m aturity of15 yearsor

m oreasin an internationalcontextthey areoften notveryactively traded.

– FortheU.S.we excludetheon-the-run and first-o -the-runissuesforevery m aturity.

– Additionally,we excludebondsifthereported pricesareobviously wrong.

InternationalTerm Structures

Introduction

Illiquidity Proxies

M otivation

Data

Term Structure

Sum m ary Stats

Correlations

Crisis

GlobalIlliquidity

M odel

Em piricalAnalysis

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 8

W e em ploy theSvensson (1994)m ethod to fittheterm structureofinterestrates.Itassum esthattheinstantaneousforward ratefisgiven by

fm = 0 + 1exp

− m

1

+ 2m

1exp

− m

1

+ 3m

2exp

− m

2

,

wherem denotesthetim eto m aturity and t i,i= 0,1,2,3 areparam etersto beestim ated.

By integrating theforward curve,we derivethespotcurve:

sm = 0 + 1

1− exp

−m

1

−m

1

− 1

+ 2

1− exp

−m

1

m

1

− 1

− exp

−m

1

!

+ 3

1− exp

−m

2

m

2

− 1

− exp

−m

2

!

.

Illiquidity Proxies

Introduction

Illiquidity Proxies

M otivation

Data

Term Structure

Sum m ary Stats

Correlations

Crisis

GlobalIlliquidity

M odel

Em piricalAnalysis

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 9

W eestim ateparam etersbt = ( 0, 1, 2, 3, 1, 2) foreach day,bym inim izing theweighted sum ofthesquared deviationsbetween theactualand m odel-im plied prices:

bt = argm inN tX

i = 1

P i (b) − P i

t

×

1D i

2

whereN t isthenum berofbonds,P i (b) isthem odel-im plied priceforbond i,and D i isthecorresponding M acaulay duration forbond i.

Theilliquidity m easure isthen defined astherootm ean squareerrorbetween them arketyieldsand them odel-im plied yields,i.e.

Illiqt =

vuut 1

Nt

N tX

i = 1

(yit − yi (bt ))

2

whereyit ism arketyield and y

i (bt ) ism odel-im plied yield.

GE:Black W ednesday and N orm alD ay

M alkhozov,M ueller,Vedolin & Venter– 10

2 4 6 8 10

0.075

0.08

0.085

0.09

0.095Normal Day GE 22 July 91

maturity (in years)

yiel

d

datafitted

illiq = 2.5

GE:Black W ednesday and N orm alD ay

M alkhozov,M ueller,Vedolin & Venter– 10

2 4 6 8 10

0.075

0.08

0.085

0.09

0.095Normal Day GE 22 July 91

maturity (in years)

yiel

d

datafitted

0 2 4 6 8 10

0.075

0.08

0.085

0.09

0.095Black Wednesday GE 16 September 92

maturity (in years)

yiel

d

datafitted

illiq = 2.5

illiq = 9.4

US:Black W ednesday and M onday

M alkhozov,M ueller,Vedolin & Venter– 11

0 2 4 6 8 100.02

0.03

0.04

0.05

0.06

0.07

maturity (in years)

yiel

d

Black Wednesday US 16 September 92

datafitted

illiq = 2.5

US:Black W ednesday and M onday

M alkhozov,M ueller,Vedolin & Venter– 11

0 2 4 6 8 100.02

0.03

0.04

0.05

0.06

0.07

maturity (in years)

yiel

d

Black Wednesday US 16 September 92

datafitted

0 2 4 6 8 10 120.04

0.05

0.06

0.07

0.08

maturity (in years)

yiel

d

Black Monday US 19 October 1987

datafitted

illiq = 2.5 illiq = 14.7

Sum m ary StatisticsIlliquidity Proxies

M alkhozov,M ueller,Vedolin & Venter– 12

us ge uk ca jp sw

Panel A: Summary Statistics (in bp)

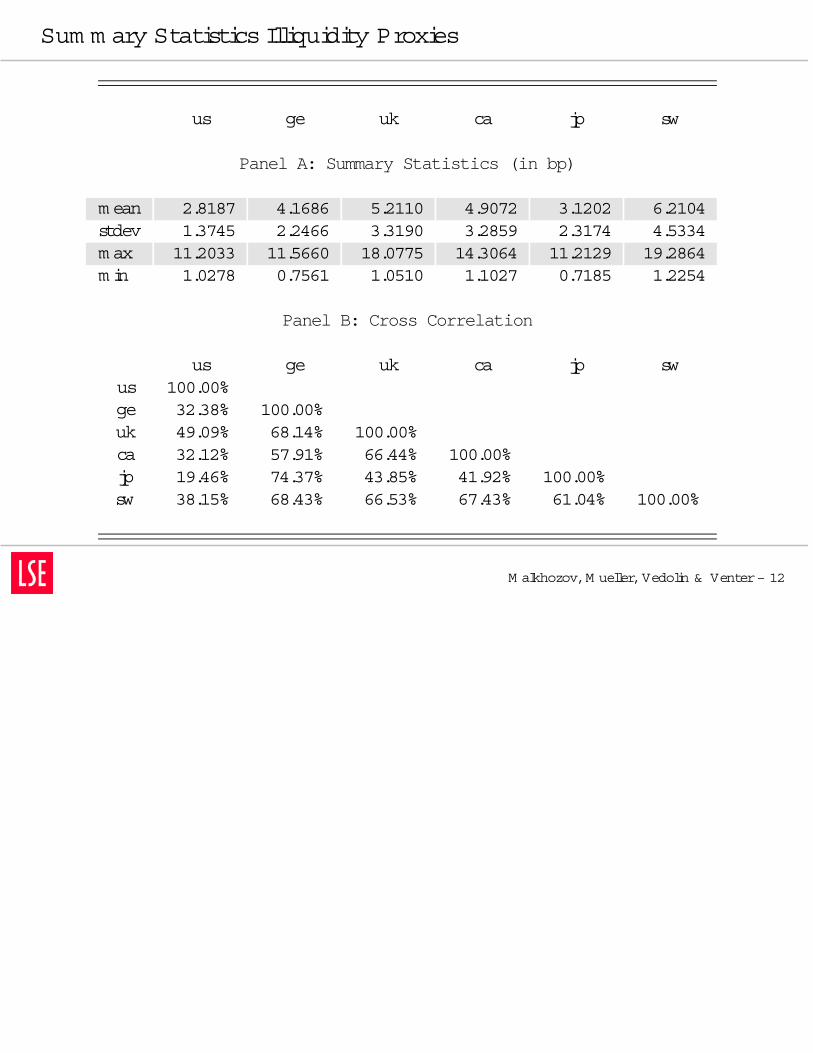

m ean 2.8187 4.1686 5.2110 4.9072 3.1202 6.2104stdev 1.3745 2.2466 3.3190 3.2859 2.3174 4.5334m ax 11.2033 11.5660 18.0775 14.3064 11.2129 19.2864m in 1.0278 0.7561 1.0510 1.1027 0.7185 1.2254

Panel B: Cross Correlation

us ge uk ca jp swus 100.00%ge 32.38% 100.00%uk 49.09% 68.14% 100.00%ca 32.12% 57.91% 66.44% 100.00%jp 19.46% 74.37% 43.85% 41.92% 100.00%sw 38.15% 68.43% 66.53% 67.43% 61.04% 100.00%

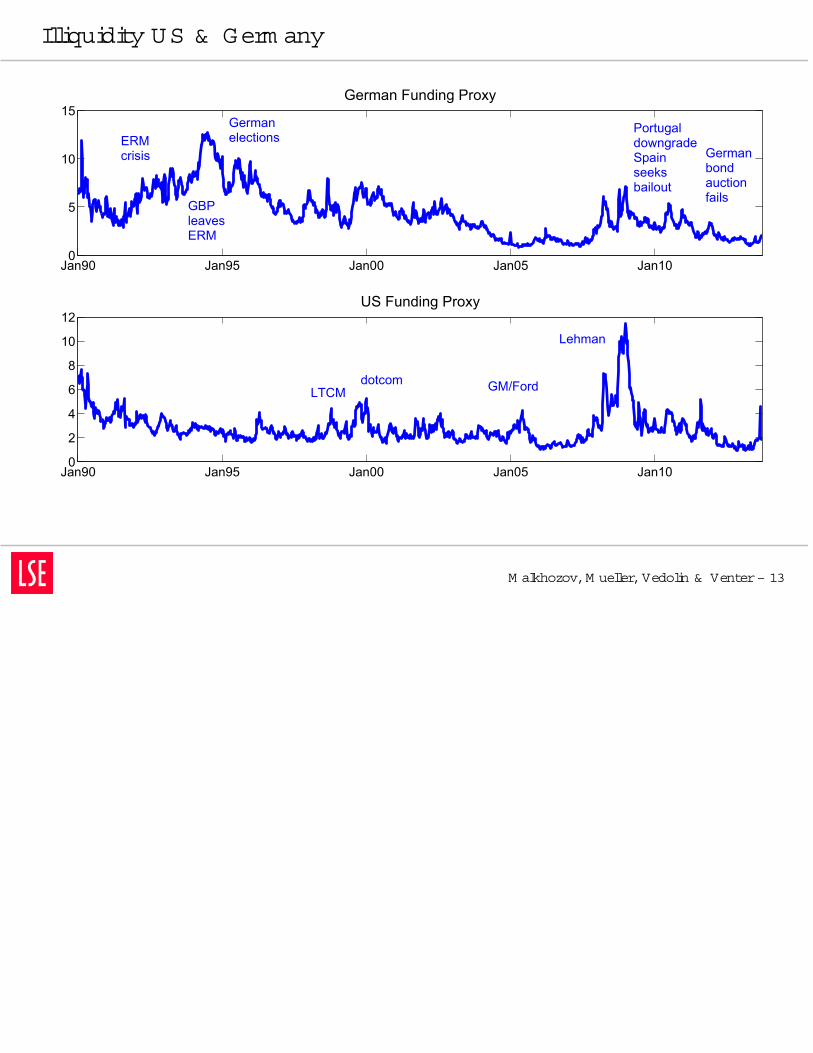

Illiquidity US & Germ any

M alkhozov,M ueller,Vedolin & Venter– 13

Jan90 Jan95 Jan00 Jan05 Jan100

5

10

15German Funding Proxy

Jan90 Jan95 Jan00 Jan05 Jan100

2

4

6

8

10

12US Funding Proxy

ERMcrisis

Germanelections

GBPleavesERM

Lehman

Germanbondauctionfails

PortugaldowngradeSpainseeksbailout

GM/ForddotcomLTCM

ConditionalCorrelation Illiquidity M easures

M alkhozov,M ueller,Vedolin & Venter– 14

1990 1995 2000 2005 2010−0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

ERMcrisis

Asiancrisis dot com

bubble

Lehman

Eurocrisis

W hilethereisa largeidiosyncraticcom ponentin each country-levelilliquidityrisk,thereisalso hugecom m onality,especiallyduring crisisperiods.

Slightupward trend hintstowardsm orem arketintegration overtim e.

Thisisnotassetspecific:Karolyi,Lee,and van Dijk (2012,equity),Karnaukh,Ranaldo,and Soderlind (2014,FX).

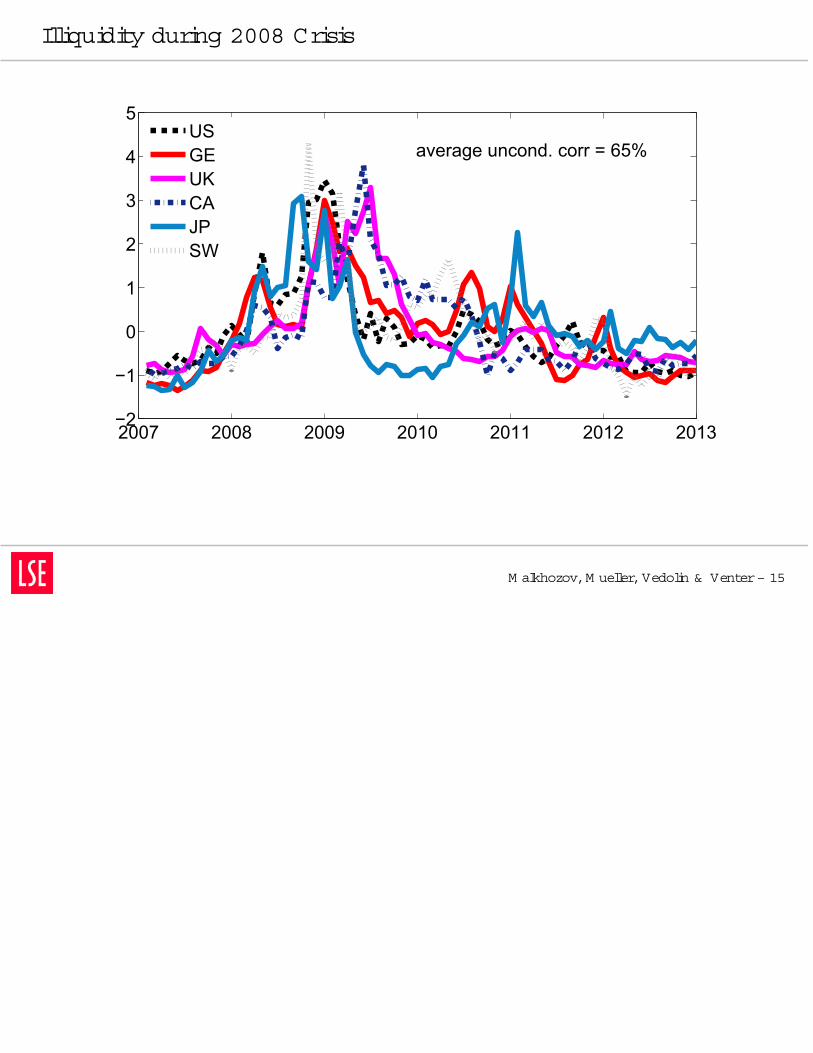

Illiquidity during 2008 Crisis

M alkhozov,M ueller,Vedolin & Venter– 15

2007 2008 2009 2010 2011 2012 2013−2

−1

0

1

2

3

4

5

USGEUKCAJPSW

average uncond. corr = 65%

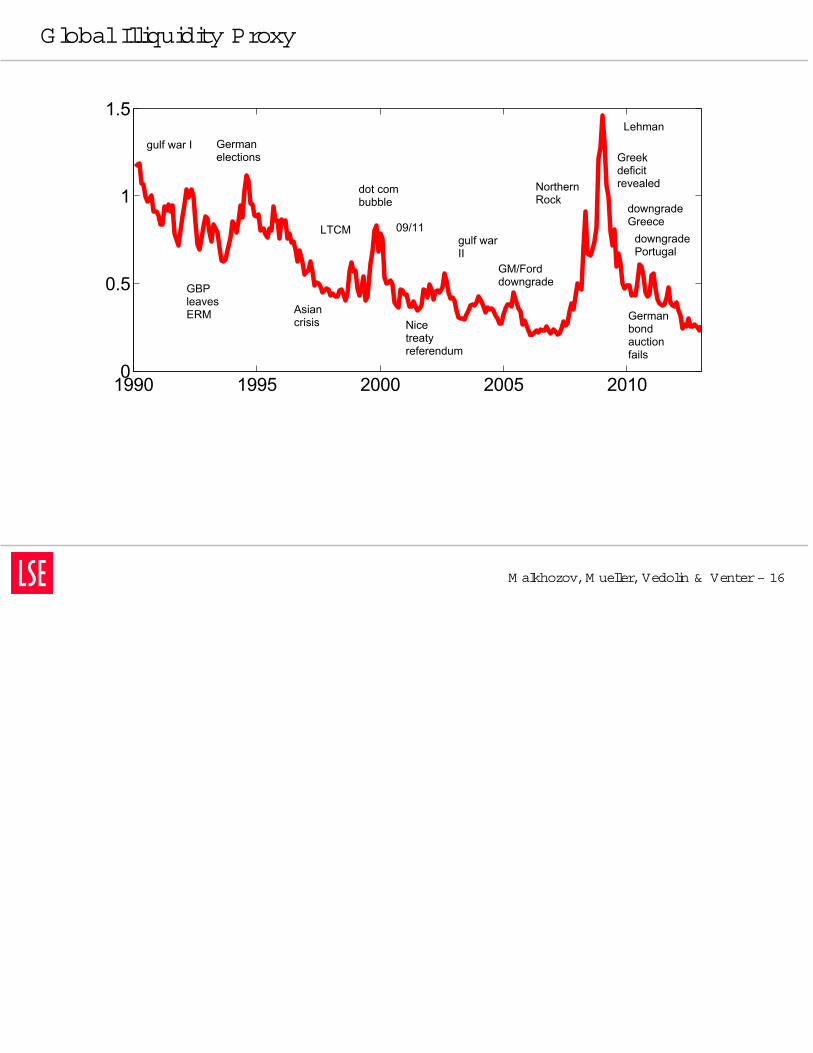

GlobalIlliquidity Proxy

M alkhozov,M ueller,Vedolin & Venter– 16

1990 1995 2000 2005 20100

0.5

1

1.5

Asian crisis

LTCM

dot combubble

09/11

Nicetreatyreferendum

gulf warII

GM/Forddowngrade

Lehman

Greekdeficit revealed

downgradeGreece

downgradePortugal

Germanbondauctionfails

GBPleavesERM

Germanelections

NorthernRock

gulf war I

M odel

Introduction

Illiquidity Proxies

M odel

M odel

CAPM

SM L

Sorted Portfolios

BAIL and BAB

Em piricalAnalysis

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 17

M odel

M alkhozov,M ueller,Vedolin & Venter– 18

Discrete-tim eOLG m odelwith 1 risklessand J risky assetsin supply jt .

Representativeagenthasm ean-variancepreferencesovernextperiod wealth

maxx t

xTt

Et [D t + 1 + Pt + 1] −

1 + rf

Pt

−

2xT

t Ωtxt

...and hasto postproportionalm argin ofm jt when investing x

jt P

jt in assetj:

s.t.X

j

m jt

xj

t

P j

t ≤ W t (1)

– m jt dependson agentand assetj,i.e.com binesboth investor-specificand

asset-specificcom ponents.

– Setting m arginsto zero m eansconstraint(1)neverbindsand thestandardCAPM holds.

W e assum ePPP holds,henceFX risk doesnotm atter.

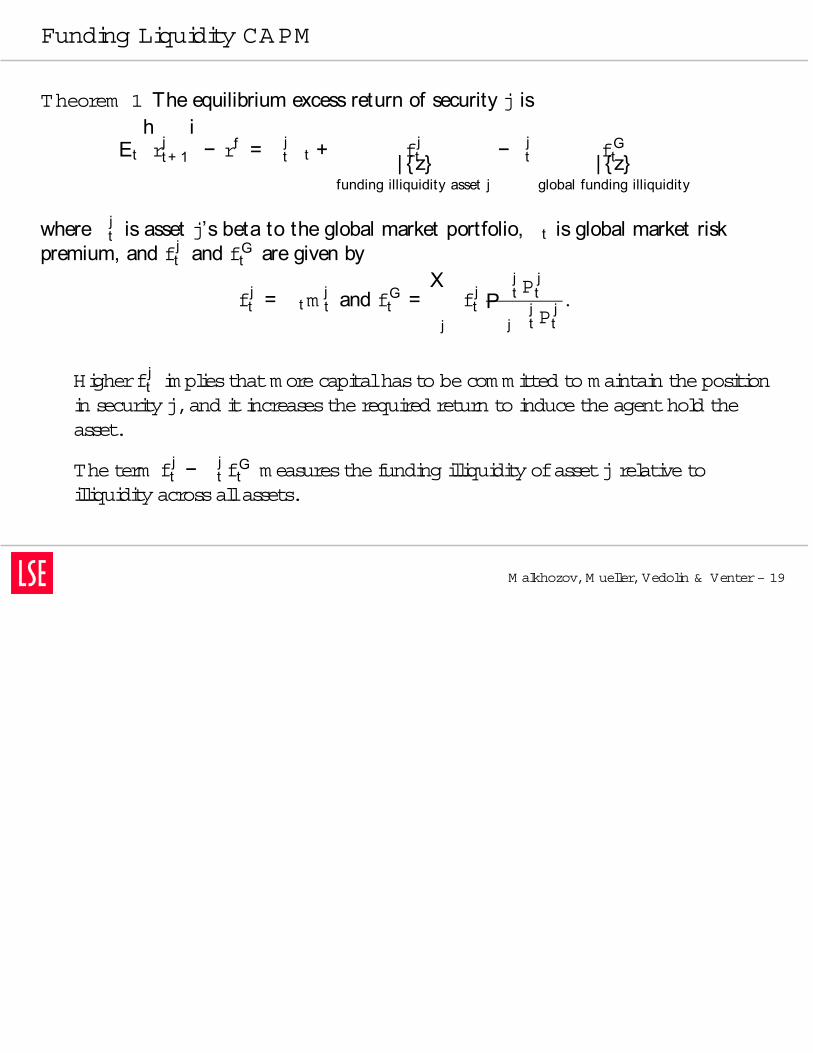

Funding Liquidity CAPM

M alkhozov,M ueller,Vedolin & Venter– 19

Theorem 1 The equilibrium excess return of security j is

Et

hrj

t + 1

i− rf = j

t t + fjt| z

funding illiquidity asset j

− jt fG

t| zglobal funding illiquidity

where jt is asset j’s beta to the global market portfolio, t is global market risk

premium, and fjt and fG

t are given by

fjt = tm

jt and fG

t =X

j

fjt

jt P

jtP

jjt P

jt

.

Higherfjt im pliesthatm orecapitalhasto becom m itted to m aintain theposition

in security j,and itincreasestherequired return to inducetheagenthold theasset.

Theterm fjt −

jt f

Gt m easuresthefunding illiquidity ofassetj relativeto

illiquidityacrossallassets.

Security M arketLine

Introduction

Illiquidity Proxies

M odel

M odel

CAPM

SM L

Sorted Portfolios

BAIL and BAB

Em piricalAnalysis

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 20

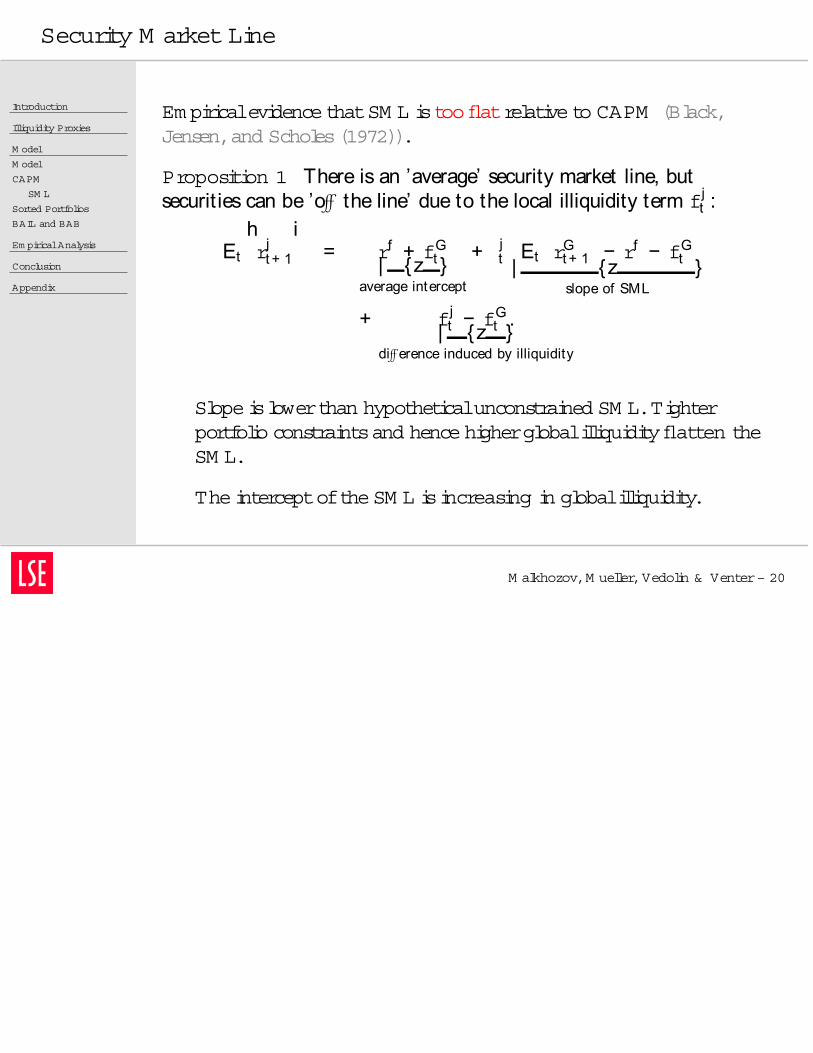

Em piricalevidencethatSM L istoo flatrelativeto CAPM (Black,Jensen,and Scholes(1972)).

Proposition 1 There is an ’average’ security market line, butsecurit ies can be ’off the line’ due to the local illiquidity term fj

t :

Et

hrj

t + 1

i= rf + fG

t| z average intercept

+ jt

Et

rG

t + 1

− rf − fG

t

| z slope of SML

+ fjt − fG

t .| z

diff erence induced by illiquidity

Slopeislowerthan hypotheticalunconstrained SM L.Tighterportfolio constraintsand hencehigherglobalilliquidity flatten theSM L.

TheinterceptoftheSM L isincreasing in globalilliquidity.

Sorted Portfoliosand Illiquidity

Introduction

Illiquidity Proxies

M odel

M odel

CAPM

SM L

Sorted Portfolios

BAIL and BAB

Em piricalAnalysis

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 21

Proposition 2 A security’s alpha with respect to the global market is

Et

hrj

t + 1

i− rf − j

t t = fjt −

jt f

Gt .

Holding illiquidity constant, a higher beta means loweralpha. Holdingbeta constant, the alpha increases in local and decreases in globalilliquidity.

Self-Financing Portfolios

Introduction

Illiquidity Proxies

M odel

M odel

CAPM

SM L

Sorted Portfolios

BAIL and BAB

Em piricalAnalysis

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 22

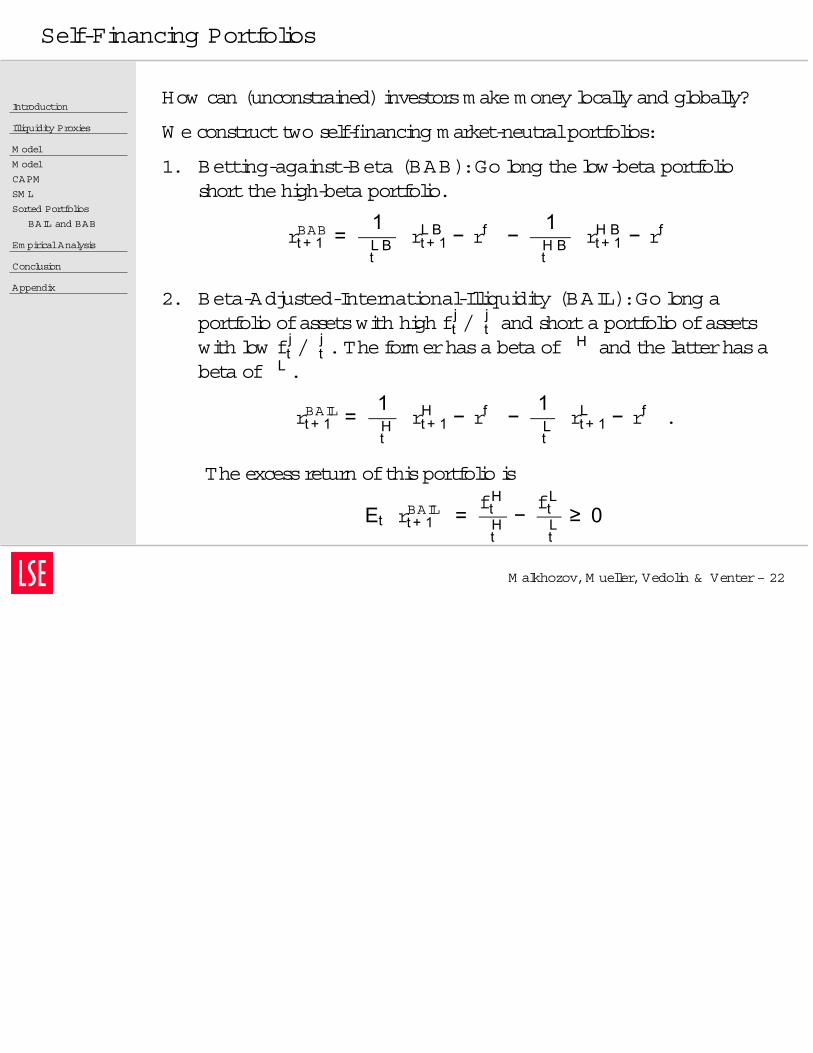

How can (unconstrained)investorsm akem oney locally and globally?

Self-Financing Portfolios

Introduction

Illiquidity Proxies

M odel

M odel

CAPM

SM L

Sorted Portfolios

BAIL and BAB

Em piricalAnalysis

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 22

How can (unconstrained)investorsm akem oney locally and globally?

W econstructtwo self-financing m arket-neutralportfolios:

1. Betting-against-Beta (BAB):Go long thelow-beta portfolioshortthehigh-beta portfolio.

rBABt + 1 =1L Bt

rL B

t + 1 − rf−

1H Bt

rH B

t + 1 − rf

2. Beta-Adjusted-International-Illiquidity (BAIL):Go long aportfolio ofassetswith high fj

t /jt and shorta portfolio ofassets

with low fjt /

jt .Theform erhasa beta of

H and thelatterhasabeta of L .

rBAILt + 1 =1Ht

rH

t + 1 − rf−

1Lt

rL

t + 1 − rf.

Theexcessreturn ofthisportfolio is

EtrBAILt + 1

=fH

tHt−fL

tLt≥ 0

Beta Arbitrage and Illiquidity

Introduction

Illiquidity Proxies

M odel

M odel

CAPM

SM L

Sorted Portfolios

BAIL and BAB

Em piricalAnalysis

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 23

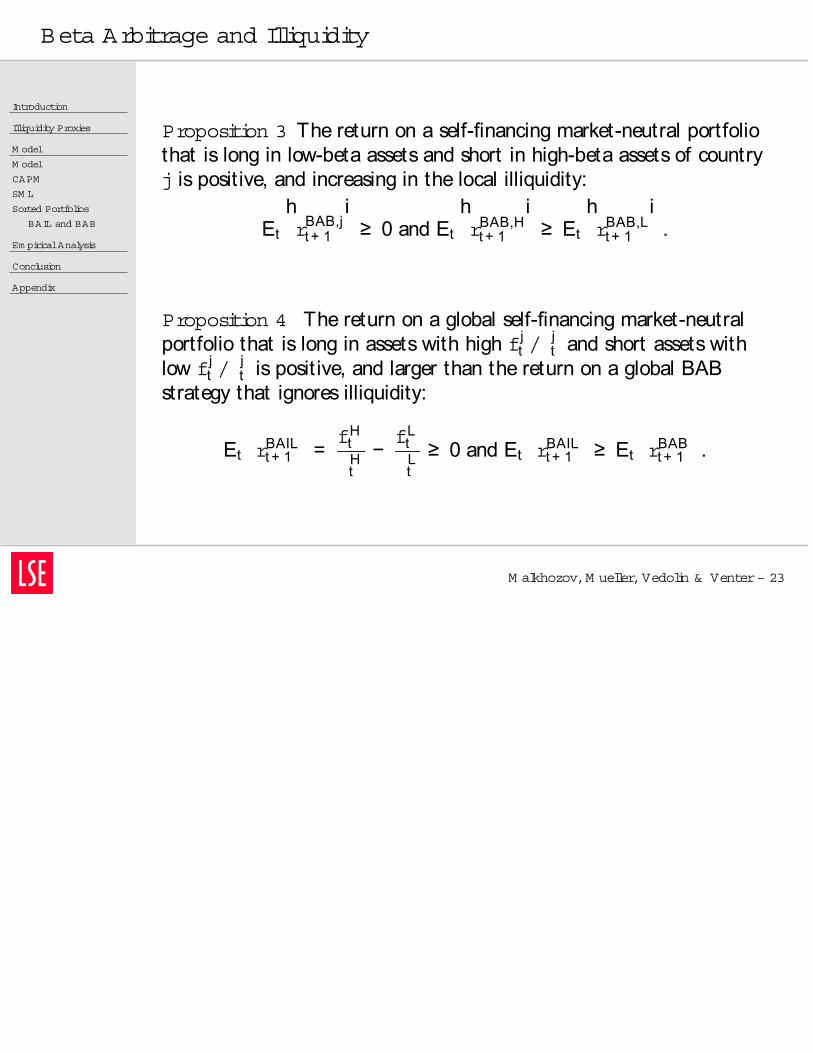

Proposition 3 The return on a self-financing market-neutral portfoliothat is long in low-beta assets and short in high-beta assets of countryj is posit ive, and increasing in the local illiquidity:

Et

hrBAB,j

t + 1

i≥ 0 and Et

hrBAB,H

t + 1

i≥ Et

hrBAB,L

t + 1

i.

Proposition 4 The return on a global self-financing market-neutralportfolio that is long in assets with high fj

t /jt and short assets with

low fjt /

jt is posit ive, and larger than the return on a global BAB

strategy that ignores illiquidity:

EtrBAIL

t + 1

=fH

tHt−fL

tLt≥ 0 and Et

rBAIL

t + 1

≥ Et

rBAB

t + 1

.

Em piricalAnalysis

Introduction

Illiquidity Proxies

M odel

Em piricalAnalysis

SM L

Sorted Pf

CAPM Alpha

BAIL vsBAB

Literature

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 24

Stock D ata and Equity Beta

Introduction

Illiquidity Proxies

M odel

Em piricalAnalysis

SM L

Sorted Pf

CAPM Alpha

BAIL vsBAB

Literature

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 25

Daily stock returns,volum e,and m arketcapitalization forthesixcountries.Theinitialsam plecoversm orethan 10k stocks.

Estim ateex-antebetasforany stock i:

ˆ TSi = ˆ

ˆ i

m,

wherethevolatilitiesarecalculated using a 1-yearwindow andcorrelationsareestim ated overa fiveyearwindow.

Finally,to accountforextrem ebeta estim atesdueto noiseandbiaseswhen wesorton beta,wefollow Vasicek (1973)by shrinkingbetastoward theircross-sectionalm ean,which issetto 1:

ˆi = 0.6 × ˆ TS

i + 0.4 × 1.

Prediction 1: Security M arketLine

Introduction

Illiquidity Proxies

M odel

Em piricalAnalysis

SM L

Sorted Pf

CAPM Alpha

BAIL vsBAB

Literature

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 26

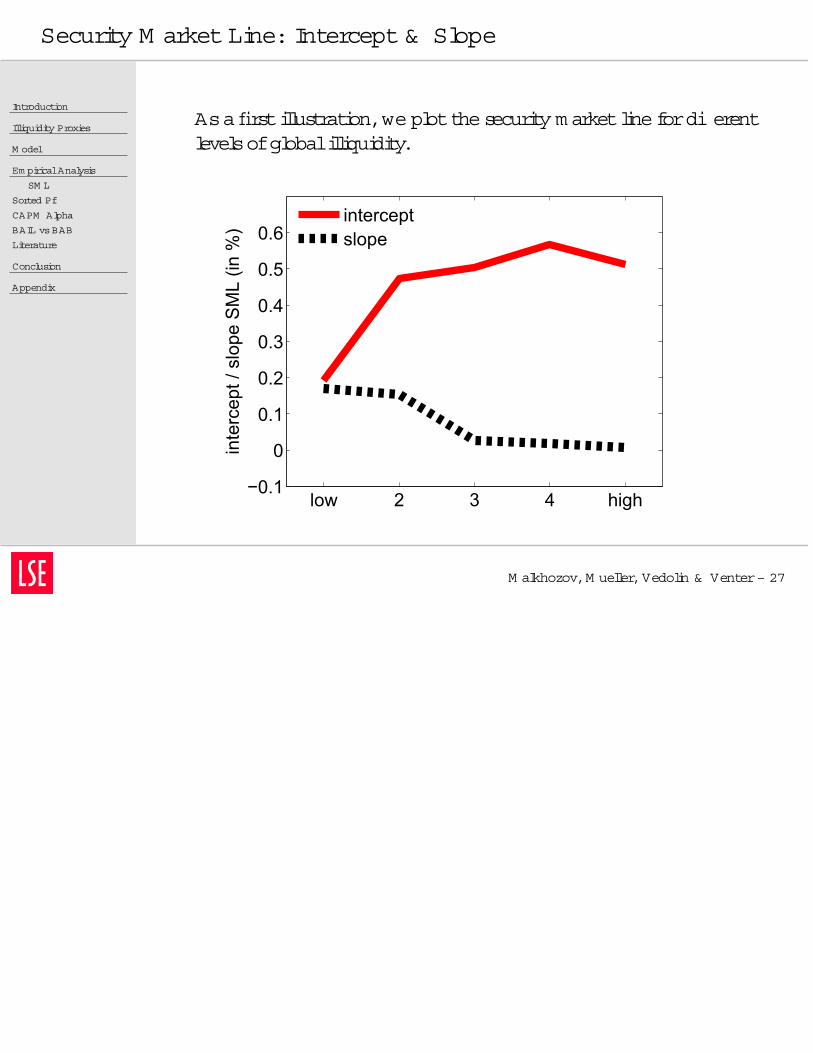

Prediction 1 In months of low global illiquidity, the intercept of theaverage security market line is lower than in months of high illiquidity.At the same time, low illiquidity months imply a higher slope than highilliquidity months.

Asa firstillustration,we plotthesecurity m arketlinefordi erentlevelsofglobalilliquidity.

First,considerthefollowing Fam aand M acBeth (1973)regressions:

rjt = t + t × jt + j

t

whererjt istheexcessreturn ofthej-th -sorted portfolio and jt

isthepost-ranking beta ofportfolio j.Thisgivesusthetim e-seriesoftheintercept t and theslope t oftheSM L foreach quintileofglobalilliquidity.

Security M arketLine: Intercept& Slope

Introduction

Illiquidity Proxies

M odel

Em piricalAnalysis

SM L

Sorted Pf

CAPM Alpha

BAIL vsBAB

Literature

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 27

Asa firstillustration,we plotthesecurity m arketlinefordi erentlevelsofglobalilliquidity.

low 2 3 4 high−0.1

0

0.1

0.2

0.3

0.4

0.5

0.6in

terc

ept /

slo

pe S

ML

(in %

)

interceptslope

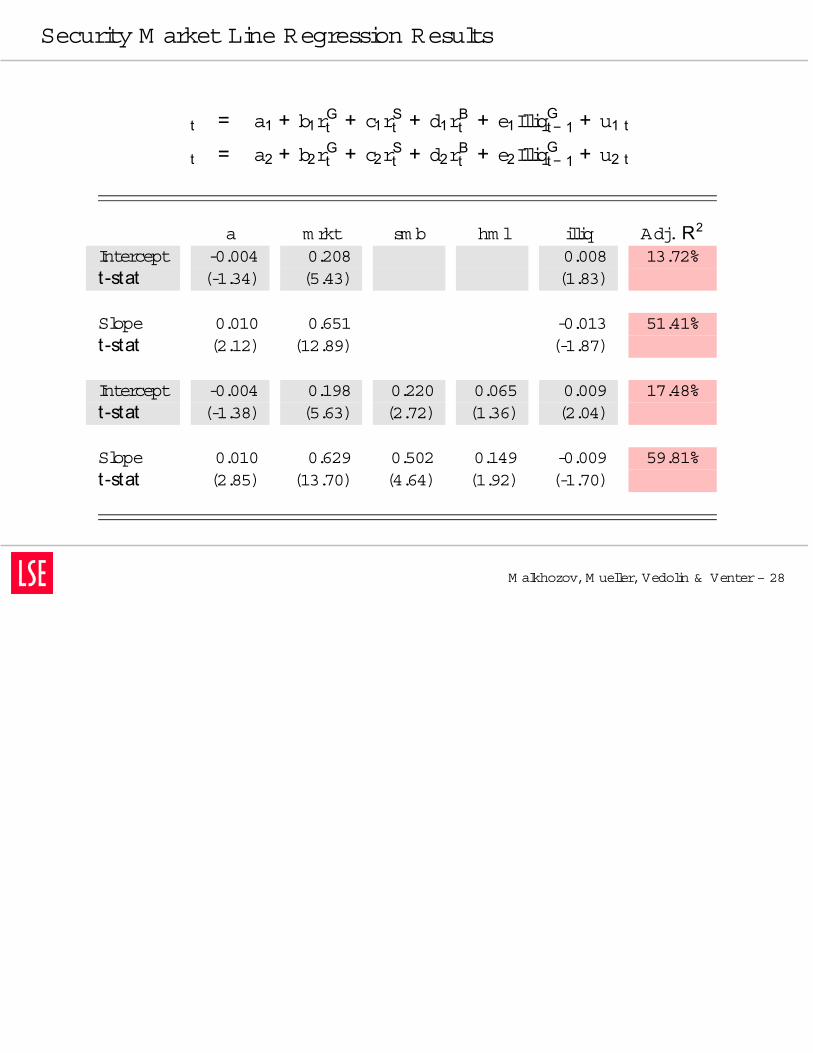

Security M arketLine Regression Results

M alkhozov,M ueller,Vedolin & Venter– 28

t = a1 + b1rGt + c1r

St + d1r

Bt + e1Illiq

Gt− 1 + u1t

t = a2 + b2rGt + c2r

St + d2r

Bt + e2Illiq

Gt− 1 + u2t

a m rkt sm b hm l illiq Adj.R2

Intercept -0.004 0.208 0.008 13.72%t-stat (-1.34) (5.43) (1.83)

Slope 0.010 0.651 -0.013 51.41%t-stat (2.12) (12.89) (-1.87)

Intercept -0.004 0.198 0.220 0.065 0.009 17.48%t-stat (-1.38) (5.63) (2.72) (1.36) (2.04)

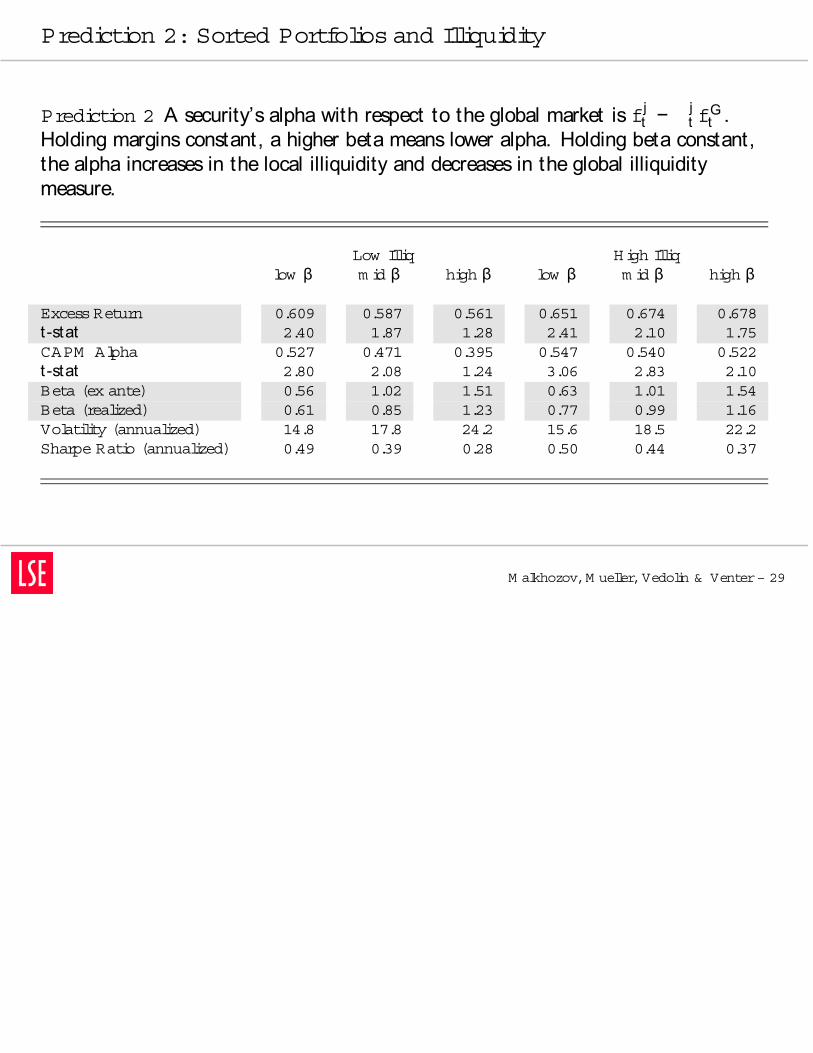

Slope 0.010 0.629 0.502 0.149 -0.009 59.81%t-stat (2.85) (13.70) (4.64) (1.92) (-1.70)

Prediction 2: Sorted Portfoliosand Illiquidity

M alkhozov,M ueller,Vedolin & Venter– 29

Prediction 2 A security’s alpha with respect to the global market is fjt −

jt f

Gt .

Holding margins constant, a higher beta means lower alpha. Holding beta constant,the alpha increases in the local illiquidity and decreases in the global illiquiditymeasure.

Low Illiq High Illiqlow β m id β high β low β m id β high β

ExcessReturn 0.609 0.587 0.561 0.651 0.674 0.678t -stat 2.40 1.87 1.28 2.41 2.10 1.75CAPM Alpha 0.527 0.471 0.395 0.547 0.540 0.522t -stat 2.80 2.08 1.24 3.06 2.83 2.10Beta (ex ante) 0.56 1.02 1.51 0.63 1.01 1.54Beta (realized) 0.61 0.85 1.23 0.77 0.99 1.16Volatility (annualized) 14.8 17.8 24.2 15.6 18.5 22.2Sharpe Ratio (annualized) 0.49 0.39 0.28 0.50 0.44 0.37

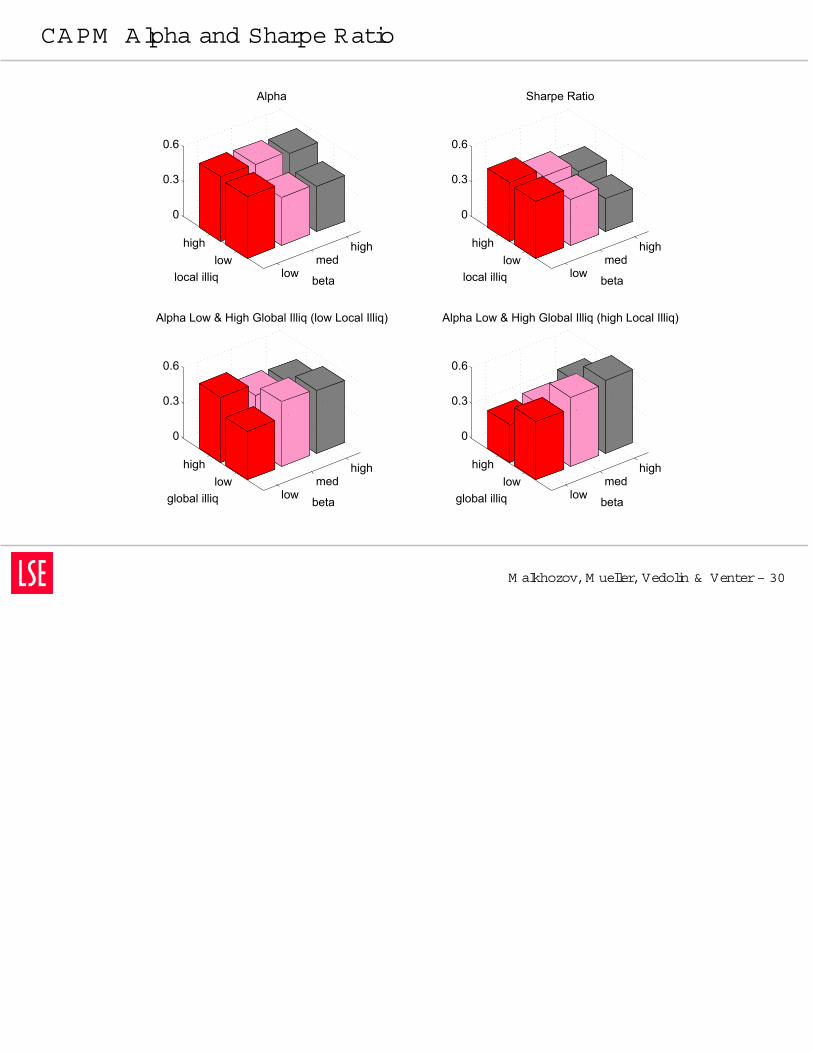

CAPM Alpha and Sharpe Ratio

M alkhozov,M ueller,Vedolin & Venter– 30

lowmed

highhigh

low

0

0.3

0.6

beta

Alpha

local illiq lowmed

highhigh

low

0

0.3

0.6

beta

Sharpe Ratio

local illiq

lowmed

highhigh

low

0

0.3

0.6

beta

Alpha Low & High Global Illiq (high Local Illiq)

global illiqlowmed

highhigh

low

0

0.3

0.6

beta

Alpha Low & High Global Illiq (low Local Illiq)

global illiq

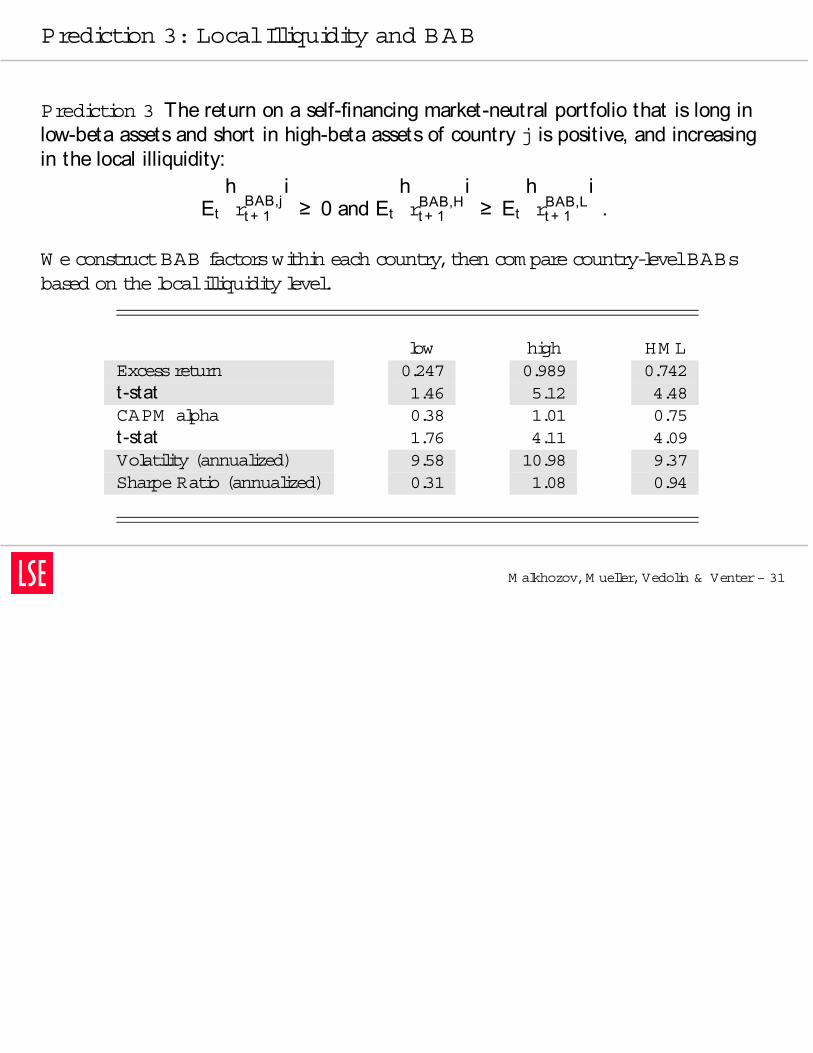

Prediction 3: LocalIlliquidity and BAB

M alkhozov,M ueller,Vedolin & Venter– 31

Prediction 3 The return on a self-financing market-neutral portfolio that is long inlow-beta assets and short in high-beta assets of country j is posit ive, and increasingin the local illiquidity:

Et

hrBAB,j

t + 1

i≥ 0 and Et

hrBAB,H

t + 1

i≥ Et

hrBAB,L

t + 1

i.

W econstructBAB factorswithin each country,then com parecountry-levelBABsbased on thelocalilliquidity level.

low high HM LExcessreturn 0.247 0.989 0.742t-stat 1.46 5.12 4.48CAPM alpha 0.38 1.01 0.75t-stat 1.76 4.11 4.09Volatility (annualized) 9.58 10.98 9.37Sharpe Ratio (annualized) 0.31 1.08 0.94

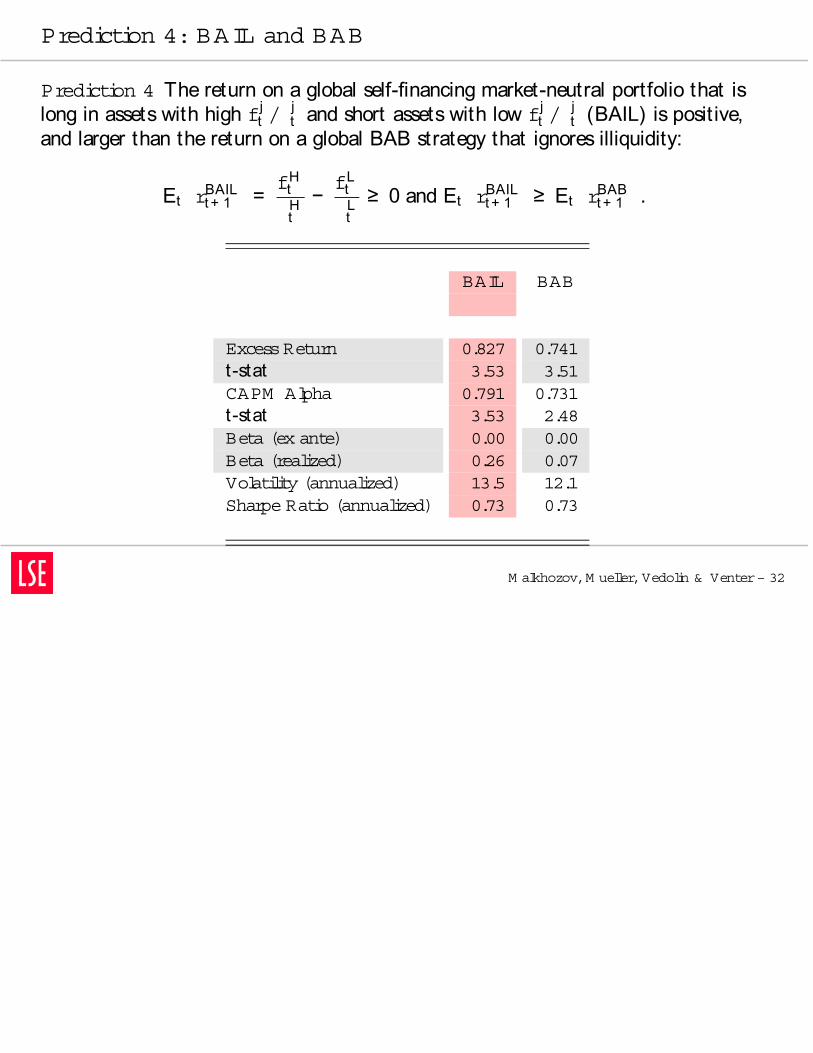

Prediction 4: BAIL and BAB

M alkhozov,M ueller,Vedolin & Venter– 32

Prediction 4 The return on a global self-financing market-neutral portfolio that islong in assets with high fj

t /jt and short assets with low fj

t /jt (BAIL) is positive,

and larger than the return on a global BAB strategy that ignores illiquidity:

EtrBAIL

t + 1

=fH

tHt−fL

tLt≥ 0 and Et

rBAIL

t + 1

≥ Et

rBAB

t + 1

.

BAIL BAB

ExcessReturn 0.827 0.741t-stat 3.53 3.51CAPM Alpha 0.791 0.731t-stat 3.53 2.48Beta (ex ante) 0.00 0.00Beta (realized) 0.26 0.07Volatility (annualized) 13.5 12.1Sharpe Ratio (annualized) 0.73 0.73

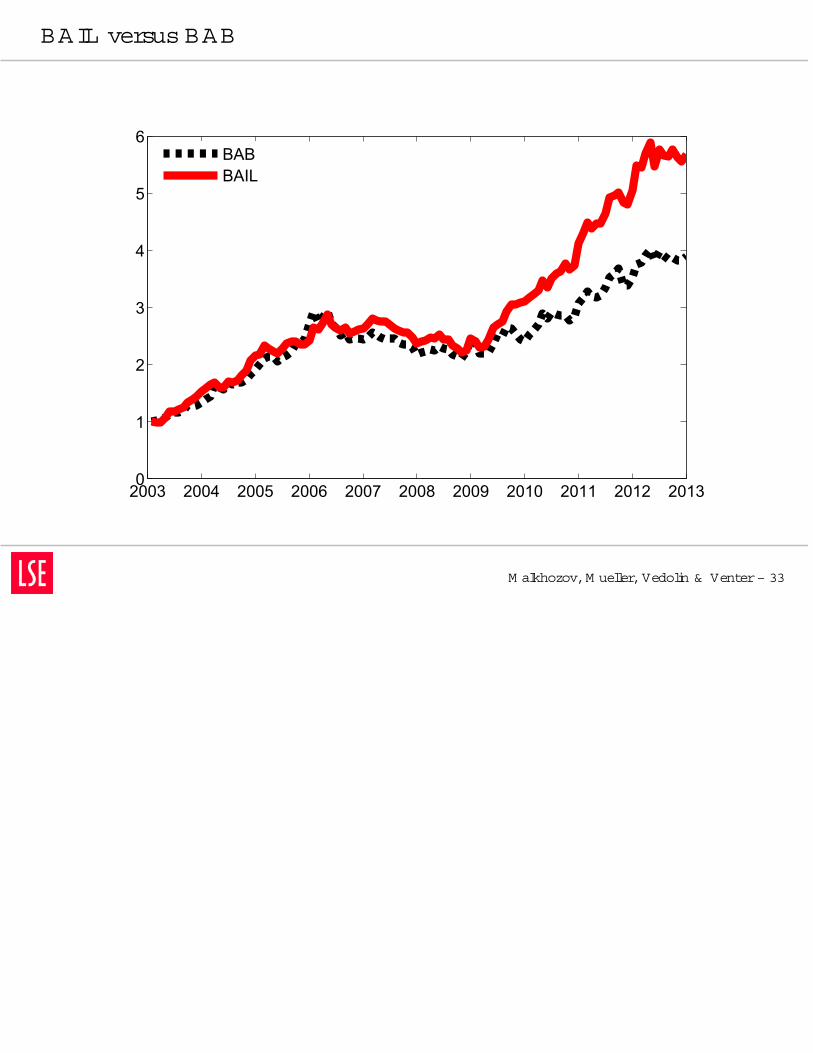

BAIL versus BAB

M alkhozov,M ueller,Vedolin & Venter– 33

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

1

2

3

4

5

6

BABBAIL

BAIL versus BAB (cont.)

Introduction

Illiquidity Proxies

M odel

Em piricalAnalysis

SM L

Sorted Pf

CAPM Alpha

BAIL vsBAB

Literature

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 34

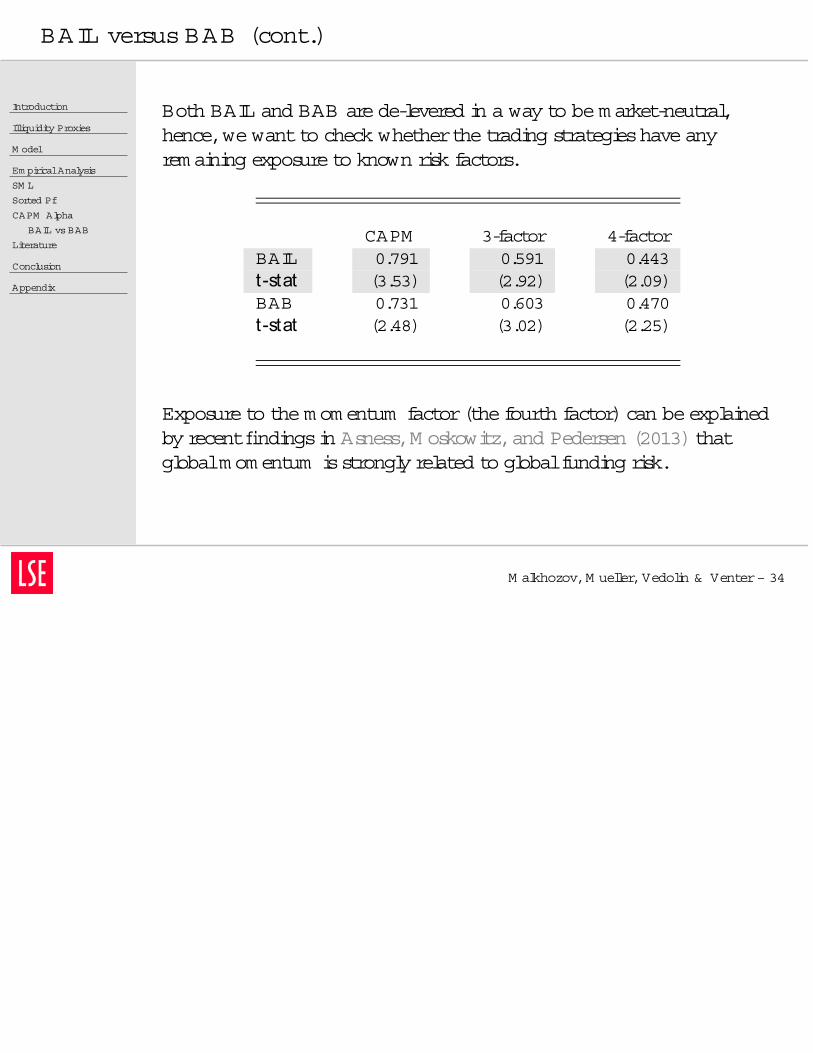

Both BAIL and BAB arede-levered in a way to bem arket-neutral,hence,we wantto check whetherthetrading strategieshaveanyrem aining exposureto known risk factors.

CAPM 3-factor 4-factorBAIL 0.791 0.591 0.443t-stat (3.53) (2.92) (2.09)BAB 0.731 0.603 0.470t-stat (2.48) (3.02) (2.25)

Exposureto them om entum factor(thefourth factor)can beexplainedby recentfindingsin Asness,M oskowitz,and Pedersen (2013)thatglobalm om entum isstrongly related to globalfunding risk.

Literature

Introduction

Illiquidity Proxies

M odel

Em piricalAnalysis

SM L

Sorted Pf

CAPM Alpha

BAIL vsBAB

Literature

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 35

Funding constraints & assetprices:

Xiong (2001),Kyleand Xiong (2001),Grom b and Vayanos(2002,2012),Krishnam urthy(2003),Brunnerm eierand Pedersen (2009),Garleanu and Pedersen (2011),Frazziniand Pedersen (2013).

Liquidity risk & internationalstock returns:

Bekaert,Harvey,and Lundblad (2007),Lee(2011),Karolyi,Lee,andvan Dijk (2012),Am ihud,Ham eed,Kang,and Zhang (2013).

InternationalFinance,portfolio constraints & segm entation:

Black (1974),Stulz(1981),Errunza and Losq (1985,1989),Eun andJarakiram anan (1986),Hietala (1989),Pavlova and Rigobon (2007)

Conclusion

Introduction

Illiquidity Proxies

M odel

Em piricalAnalysis

Conclusion

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 36

Conclusion

Introduction

Illiquidity Proxies

M odel

Em piricalAnalysis

Conclusion

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 37

Thispaperstudiesa world econom y whereagentsaresubjecttoagent-and country-specificm argin constraints,and deriveaninternationalfunding-liquidityadjusted CAPM whereexpectedreturnsnotonlydepend on theglobalm arketrisk ofassetsbutalsoon localand globalilliquidity m easures.

Higherilliquidity⇒ Higherinterceptand lowerslopeofSM L.

Higherilliquidity⇒ Higheralpha and Sharperatio.

M arket-neutralBAIL strategyproducessignificantabnorm alreturnswith a Sharperatio of0.73 and outperform sa standard BABstrategy.

Conclusion

Introduction

Illiquidity Proxies

M odel

Em piricalAnalysis

Conclusion

Conclusion

Appendix

M alkhozov,M ueller,Vedolin & Venter– 37

Thispaperstudiesa world econom y whereagentsaresubjecttoagent-and country-specificm argin constraints,and deriveaninternationalfunding-liquidityadjusted CAPM whereexpectedreturnsnotonlydepend on theglobalm arketrisk ofassetsbutalsoon localand globalilliquidity m easures.

Higherilliquidity⇒ Higherinterceptand lowerslopeofSM L.

Higherilliquidity⇒ Higheralpha and Sharperatio.

M arket-neutralBAIL strategyproducessignificantabnorm alreturnswith a Sharperatio of0.73 and outperform sa standard BABstrategy.

Thank you very m uch foryourattention!

Appendix

Introduction

Illiquidity Proxies

M odel

Em piricalAnalysis

Conclusion

Appendix

Com parison Global

Com parison Am ihud

Com parison VIX

Em bedded Leverage

M alkhozov,M ueller,Vedolin & Venter– 38

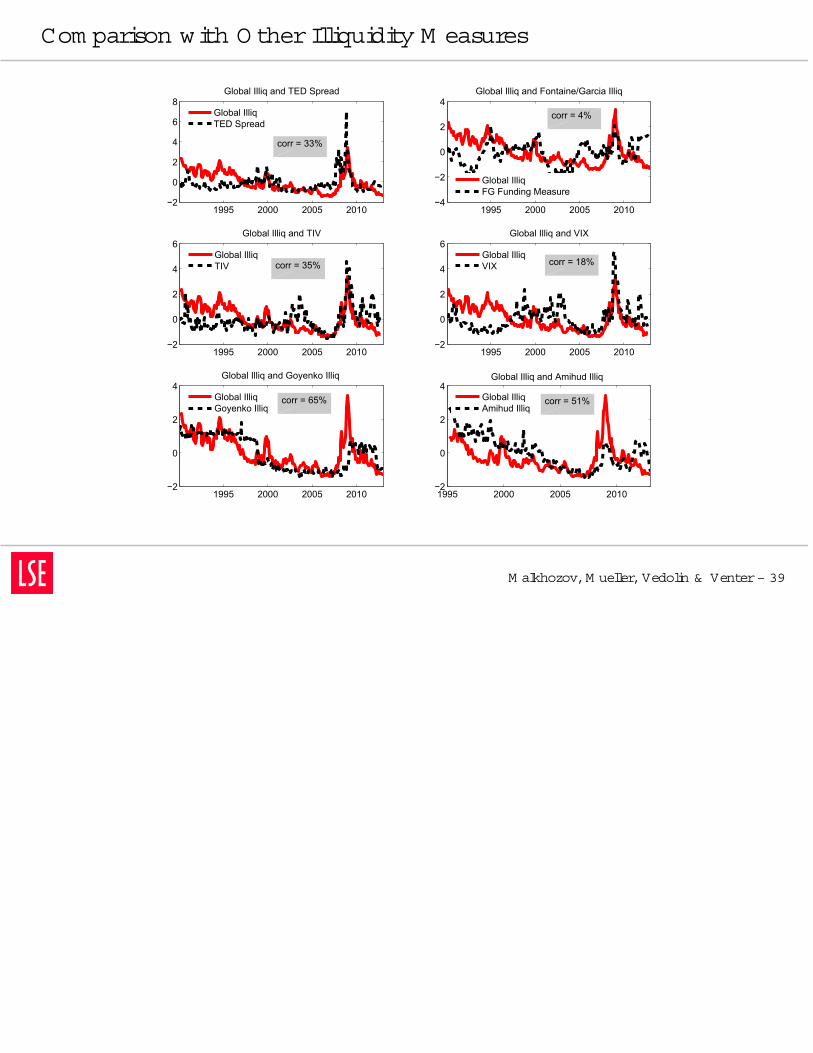

Com parison with O therIlliquidity M easures

M alkhozov,M ueller,Vedolin & Venter– 39

1995 2000 2005 2010−2

0

2

4

6

8Global Illiq and TED Spread

Global IlliqTED Spread

1995 2000 2005 2010−4

−2

0

2

4Global Illiq and Fontaine/Garcia Illiq

Global IlliqFG Funding Measure

1995 2000 2005 2010−2

0

2

4

6Global Illiq and TIV

Global IlliqTIV

1995 2000 2005 2010−2

0

2

4

6Global Illiq and VIX

Global IlliqVIX

1995 2000 2005 2010−2

0

2

4Global Illiq and Goyenko Illiq

Global IlliqGoyenko Illiq

1995 2000 2005 2010−2

0

2

4Global Illiq and Amihud Illiq

Global IlliqAmihud Illiq

corr = 33%

corr = 4%

corr = 35% corr = 18%

corr = 65% corr = 51%

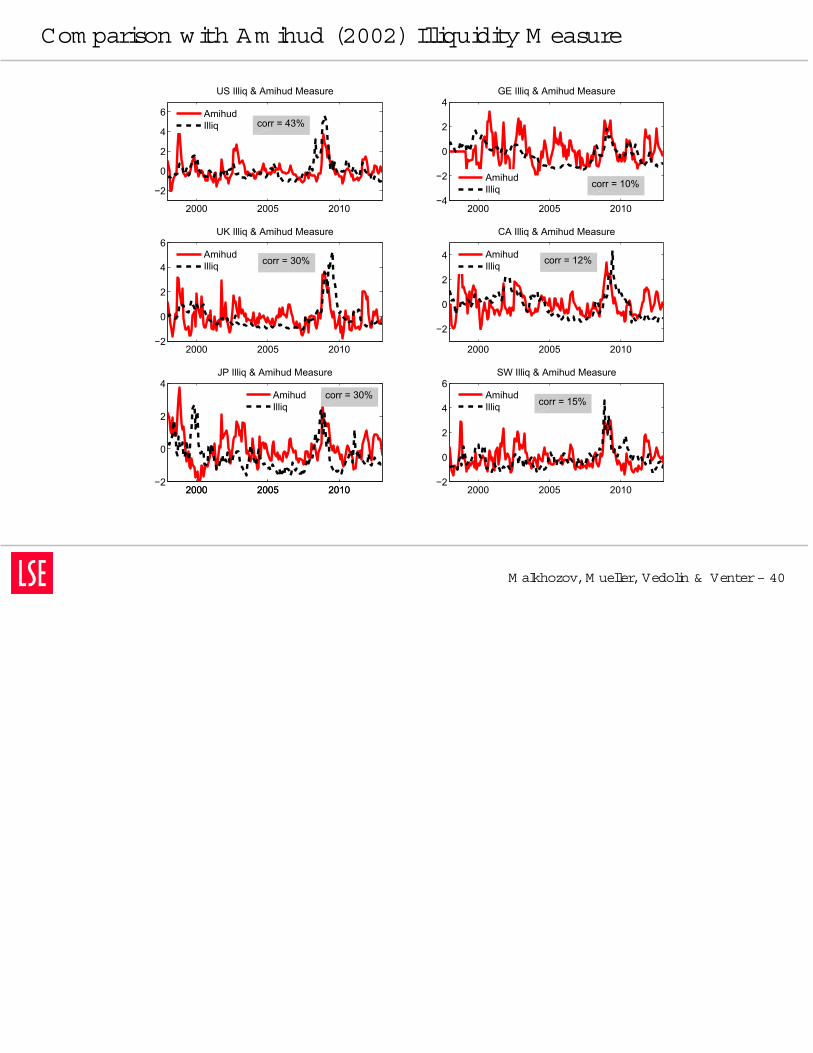

Com parison with Am ihud (2002) Illiquidity M easure

M alkhozov,M ueller,Vedolin & Venter– 40

2000 2005 2010

−2

0

2

4

6

US Illiq & Amihud Measure

AmihudIlliq

2000 2005 2010−4

−2

0

2

4GE Illiq & Amihud Measure

AmihudIlliq

2000 2005 2010−2

0

2

4

6UK Illiq & Amihud Measure

AmihudIlliq

2000 2005 2010

−2

0

2

4

CA Illiq & Amihud Measure

AmihudIlliq

2000 2005 2010−2

0

2

4

6SW Illiq & Amihud Measure

AmihudIlliq

2000 2005 2010−2

0

2

4JP Illiq & Amihud Measure

2000 2005 2010

AmihudIlliq

corr = 43%

corr = 10%

corr = 30% corr = 12%

corr = 15%corr = 30%

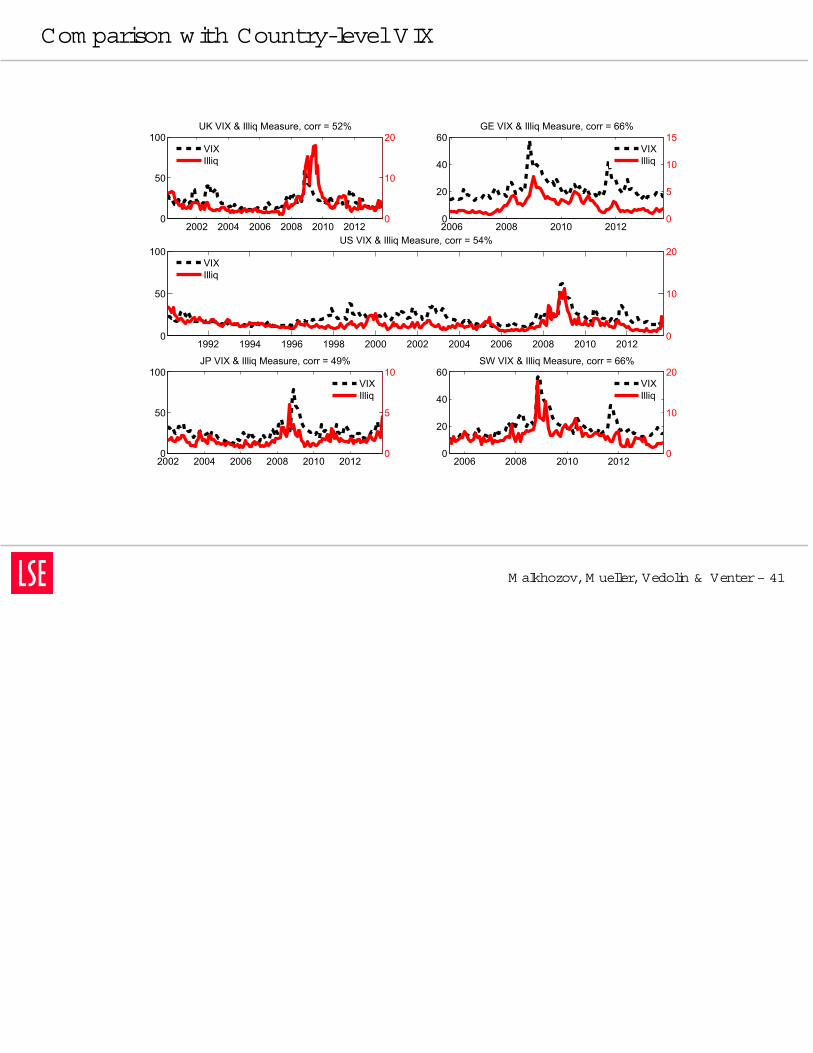

Com parison with Country-levelVIX

M alkhozov,M ueller,Vedolin & Venter– 41

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 20120

50

100US VIX & Illiq Measure, corr = 54%

0

10

20VIXIlliq

2006 2008 2010 20120

20

40

60GE VIX & Illiq Measure, corr = 66%

0

5

10

15VIXIlliq

2002 2004 2006 2008 2010 20120

50

100UK VIX & Illiq Measure, corr = 52%

0

10

20VIXIlliq

2002 2004 2006 2008 2010 20120

50

100JP VIX & Illiq Measure, corr = 49%

0

5

10VIXIlliq

2006 2008 2010 20120

20

40

60SW VIX & Illiq Measure, corr = 66%

0

10

20VIXIlliq

LetThem Buy ETFs orO ptions!

Introduction

Illiquidity Proxies

M odel

Em piricalAnalysis

Conclusion

Appendix

Com parison Global

Com parison Am ihud

Com parison VIX

Em bedded Leverage

M alkhozov,M ueller,Vedolin & Venter– 42

Argum entthatpeoplewho wantleveragecan sim ply buy optionsorETFs.Butthey deliverlow expected returns(FrazziniandPedersen (2012)):

Intuition:Em bedded leveragealleviatesinvestors’leverageconstraints,and thereforeassetswith em bedded leverageyieldlowerexpected returns.

A portfolio which islong low-em bedded-leveragesecuritiesandshorthigh-em bedded-leveragesecuritiesearnslargeabnorm alreturns,with t-statisticsof8.6 forequity options,6.3 forindexoptionsand 2.5 forETFs.