prof. jacob a. frenkel chairman, merrill lynch international former governor of the bank of israel...

TRANSCRIPT

Prof. Jacob A. Frenkel

Chairman, Merrill Lynch International Former Governor of the Bank of Israel

The Global EconomyChallenges to Recovery

The Global EconomyChallenges to Recovery

9th Dubrovnik Economic Conference DubrovnikJune 26 – 28, 2003

June 18, 2003

Table of ContentsTable of Contents

The US economy: Background and Challenges

A more sustainable growth outlook

Private sector reacts to challenges

A timely policy response

The path to economic recovery

Downside risks

Asset market vulnerability

Unwinding the current account deficit

Geo-political instability and oil shocks

Euroland economic outlook

Japan economic outlook

Emerging Asia and Latin America

Global Recessionary Deflation?

June 18, 2003

1.5

2.0

2.9

1.1

4.8

2.42.6

2.52.5

0

1

2

3

4

5

6

72-95 1996 1997 1998 1999 2000 2001 2002 Q1 03

US Economy Enjoys High ProductivityUS Economy Enjoys High Productivity

Source: Bureau of Labour Statistics

% year-on-year

Non-farm Productivity, last data point: Q1 03

1998-2002 average = 2.7%

June 18, 2003

Background and ChallengesBackground and Challenges

Non-sustainable rapid growth in the 1990s led to a series of real and financial imbalances

Bubbles burst in tech sectors and telecoms with fallouts in financial and real markets

Profit crunch required cost reduction

Manufacturing sector declined, employment weakened

Terrorism (9/11) damaged economic confidence

Corporate governance crisis damaged financial integrity

Confidence crisis and recession required policy response

Iraq crisis: before and after

June 18, 2003

Actual Numbers

Source: Bureau of Economic Analysis, last data point: Q1 03

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

96 97 98 99 00 01 02 03 04

ML Forecast

Quarterly Real GDP (4 Quarter percentage change)Quarterly Real GDP (4 Quarter percentage change)

Boom, Gloom and Modest US RecoveryBoom, Gloom and Modest US Recovery

Actual Numbers Average 1996-2000: 4.0%Average 2001-2002: 1.4%Average 2003-2004: 2.8%

June 18, 2003

A More Sustainable US Growth OutlookA More Sustainable US Growth Outlook

A flexible, competitive and deregulated economy enables:

A smooth response by corporates and households

A timely policy response

Real GDP growth forecast: 2.2% in 2003, 3.4% in 2004

Capital spending starts to recover; limited overhang

Consumer spending less buoyant but still robust

High and rising productivity yields a jobless recovery

Housing market remains a solid pillar

June 18, 2003

Quick Reaction of Economic Agentsand PoliciesQuick Reaction of Economic Agentsand Policies

A flexible and adaptable economy, with low inflation and moderate public debt has facilitated:

An effective private sector response:

A significant reduction in labor costs

A rapid adjustment of inventories

Mitigating the profit crunch

An effective policy response:

A decisive and timely monetary policy response

A series of fiscal stimulus packages

June 18, 2003

6

7

8

9

10

11

12

13

1996 1997 1998 1999 2000 2001 2002 2003

Profit Crunch Requires AdjustmentProfit Crunch Requires Adjustment

Source: Bureau of Economic Analysis, last data point: Q1 03

1992-2002 average = 10.1%

Profits as Share of Non-Financial Corporate GDPProfits as Share of Non-Financial Corporate GDP US Recession

%%

June 18, 2003

Companies Lay Off Workers to Cut CostsCompanies Lay Off Workers to Cut Costs

6.1%

3.5

4.0

4.5

5.0

5.5

6.0

6.5

J an-01 J un-01 Nov-01 Apr-02 Sep-02 Feb-03

Source: Bureau of Labour Statistics, last data point: May 03

SA Unemployment Rate, as % of Total Civilian Labour ForceSA Unemployment Rate, as % of Total Civilian Labour Force

US Job Loss Jan 01-Dec 02 > 1.9m

June 18, 2003

-4

-3

-2

-1

0

1

2

3

4

5

6

1996 1997 1998 1999 2000 2001 2002 2003

Unit Labour Cost Pressures Have DeclinedUnit Labour Cost Pressures Have Declined

Source: Bureau of Labour Statistics; Unit Labour Costs, Non-farm Business Sector, last data point: Q1 03

% change% change

US Recession

June 18, 2003

-10

-8

-6

-4

-2

0

2

4

6

8

1996 1997 1998 1999 2000 2001 2002 2003

US Inventory Reflects FlexibilityUS Inventory Reflects Flexibility

Source: Census Bureau, last data point: Apr 03

% change% change

Inventories cut by $250bn in one year

Manufacturing & Wholesale Inventories, 3 Month % Change, AnnualisedManufacturing & Wholesale Inventories, 3 Month % Change, Annualised

June 18, 2003

Decisive US Fed Rate CutsDecisive US Fed Rate Cuts

1.25%

6.5%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

J an-99 J ul-99 Feb-00 Sep-00 Apr-01 Nov-01 J un-02 J an-03

%

Source: Federal Reserve Bank of New York

Federal Funds Target

June 18, 2003

8.4

4.1

2.93.4

2.8

1.6 1.61.9

2.3 2.2

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

71-81 82-92 1996 1997 1998 1999 2000 2001 2002 2003F

In a Low Inflation EnvironmentIn a Low Inflation Environment

Source: Bureau of Labour Statistics, Merrill Lynch forecast

% year-on-year

10 year average = 2.5%

June 18, 2003

-3.8-3.3

-2.4

-1.3

-0.1

0.5

1.2

-0.7

-3.6

-4.6

-3.8

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003F

2004F

Reinforced by Ample Fiscal StimulusReinforced by Ample Fiscal Stimulus

US Budget Balance as% of GDP

US Gross Public Debtas % of GDP

Source: IMF World Economic Outlook, April 2003

75 7367

58 5962

0

10

20

30

40

50

60

70

80

1994

1996

1998

2000

2002

2003F

June 18, 2003

-30

-25

-20

-15

-10

-5

0

5

10

15

20

J an-99 J an-00 J an-01 J an-02 J an-03

Capital Spending Leads the RecoveryCapital Spending Leads the Recovery

Source: Census Bureau, last data point: Apr 03

New Orders of Non-Defense Capital Goods, % change year-on-yearNew Orders of Non-Defense Capital Goods, % change year-on-year

% change

June 18, 2003

-15

-10

-5

0

5

10

15

20

25

30

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

US Tech Spending RecoversUS Tech Spending Recovers

Source: Bureau of Economic Analysis, last data point: Q1 03

Real Capital Spending on Tech Equipment & Software, % change quarterly YoYReal Capital Spending on Tech Equipment & Software, % change quarterly YoY

% change

June 18, 2003

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Mortgage Refinancing Supports ConsumptionMortgage Refinancing Supports Consumption

Source: Mortgage Bankers Association, last data point: 3rd June 03

US Recession

Mortgage Application Index for Refinancing

4 Week Moving Average4 Week Moving Average

Households “cash out” $150-200bn in 2002

June 18, 2003

US Retail Sales Rebound and StabiliseUS Retail Sales Rebound and Stabilise

0.0

1.0

2.0

3.0

4.0

5.0

6.0

J an-01 J ul-01 J an-02 J ul-02 J an-03

Source: Census Bureau, Retail Sales ex-autos, last data point: May 03

% year-on-year% year-on-year

June 18, 2003

400

600

800

1,000

1,200

1,400

1,600

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Robust US Housing StartsRobust US Housing Starts

Source: Census Bureau; Single-Family Housing Starts, 000s, SAAR, last data point: May 03

10 year average

US Recession

June 18, 2003

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

5.5

J an-99 J an-00 J an-01 J an-02 J an-03

GDP growth

YoY Employment Growth

`

The Recovery Remains JoblessThe Recovery Remains Jobless

Source: BEA, BLS, last data point: Employment May 03, GDP Mar 03

% YoY growth

June 18, 2003

Global Growth OutlookGlobal Growth Outlook

Merrill Lynch Forecasts, June 2003Merrill Lynch Forecasts, June 2003

2000 2001 2002E 2003F

World* 4.0 1.2 1.9 2.2

US 3.8 0.3 2.4 2.2

Euroland 3.5 1.4 0.8 0.6

J apan 2.4 -0.2 0.2 0.2

Asia Pacific

(ex. J apan)

6.7 4.0 5.7 5.1

Latin America 4.1 0.1 -1.2 1.4

(*) IMF forecasts

June 18, 2003

Downside RisksDownside Risks

Vulnerable Asset Markets Could further Affect Confidence

The investment rebound could be short-lived

Household spending could retrench

Disorderly Unwinding of US Current Account Deficit if:

Foreign investors reduce holdings of US assets

US Dollar weakens and forex markets remain volatile

US savings recover too rapidly

US investment recovers too slowly

Geo-political Instability and Oil Shocks

Global recessionary deflation?

June 18, 2003

Risk Aversion in US MarketsRisk Aversion in US Markets

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

J ul-98 Jan-99 Jul-99 Jan-00 Jul-00 Jan-01 Jul-01 Jan-02 Jul-02 Jan-03

Source: Merrill Lynch, last data point: 17 June 03

Risk Aversion Index, 30 days moving average

Index composed of Equity Implied Volatility, Swap Spreads & Spread Ratio between BBB & BB CorpsIndex composed of Equity Implied Volatility, Swap Spreads & Spread Ratio between BBB & BB Corps

Russia/LTCMcollapse

September 11

Accounting scandals

Fall of Baghdad

June 18, 2003

High US Corporate Debt RatioHigh US Corporate Debt Ratio

60%

65%

70%

75%

80%

85%

90%

95%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Source: Census Bureau, last data point: Q4 02

10 year average = 75%

Long-Term Debt/Income, all Manufacturing IndustriesLong-Term Debt/Income, all Manufacturing Industries

June 18, 2003

9

11

13

15

17

19

21

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

US Corporate Debt Servicing ManageableUS Corporate Debt Servicing Manageable

Source: Bureau of Economic Analysis, last data point: Q1 03

%%

10 year average = 12.8%

Current = 14.3%

US RecessionInterest Expense/EBITDAInterest Expense/EBITDA

June 18, 2003

0

50

100

150

200

250

1996 1997 1998 1999 2000 2001 2002

0

20

40

60

80

100

120

140

160

180

200

Insert Footnote Text

Corporate Bond Defaults Rise Globally Corporate Bond Defaults Rise Globally

No. of issuers US$ bn

Source: Standard & Poor’s

Amount defaulted

No. of issuers

June 18, 2003

27 46 21 37

226

415 417

733

0

100

200

300

400

500

600

700

800

Q1 2002 Q2 2002 Q3 2002 Q4 2002

UpgradesDowngrades

US Corporate Credit Ratings WorsenUS Corporate Credit Ratings Worsen

Source: Standard & Poor’s

US$ bn

US rating actions by value

June 18, 2003

60

80

100

120

140

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Are Residential Prices Sustainable?Are Residential Prices Sustainable?

Source: Bank for International Settlements

Residential Price Indices , 1992 =100, logarithmic scaleResidential Price Indices , 1992 =100, logarithmic scale

FranceFrance

USA

ItalyItaly

GermanyGermany

JapanJapan

UK

June 18, 2003

A Rising Current Account DeficitA Rising Current Account Deficit

-6

-5

-4

-3

-2

-1

0

1996 1997 1998 1999 2000 2001 2002 2003F

Source: Bureau of Economic Analysis, Merrill Lynch

Current Account balance as % of GDPCurrent Account balance as % of GDP

June 18, 2003

Risks to External Financing of DeficitsRisks to External Financing of Deficits

US current account deficit projected to remain above 4% of GDP, worsening net foreign liability position

A potentially disorderly unwinding of US current account deficit is possible if:

Loss of confidence or a shift in portfolio preferences reduces foreign investors appetite for US assets

US Savings recover too quickly

US Investments recover too slowly

Possible disruption of exchange rates and interest rates

June 18, 2003

0

50

100

150

200

250

300

1996 1997 1998 1999 2000 2001 2002 2003

Foreign Investors Withdraw from US MarketsForeign Investors Withdraw from US Markets

US$ bn, 12 months moving average

Foreign Foreign Purchases of Purchases of

US Stocks US Stocks

Foreign Purchases Foreign Purchases of US Corporate of US Corporate

Bonds Bonds

Source: Federal Reserve, last data point: Mar 03

June 18, 2003

US Dollar WeakensUS Dollar Weakens

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

Jan-02 Mar-02 Jun-02 Sep-02 Nov-02 Feb-03 Apr-03

`

Source: Bloomberg

US$/Euro

June 18, 2003

15

20

25

30

35

40

45

J an Apr J ul Sep Dec Mar J un Sep Dec

1990-19912002-2003Nymex Future Curve

Oil Price (WTI)Oil Price (WTI)

Source: Bloomberg

$/bbl$/bbl

08/01/90 - Iraq 08/01/90 - Iraq invades Kuwaitinvades Kuwait

01/17/91 - Operation 01/17/91 - Operation Desert Storm beginsDesert Storm begins 02/28/91 - Cessation of war02/28/91 - Cessation of war

June 18, 2003

-12

-10

-8

-6

-4

-2

0

2

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002f 2003f

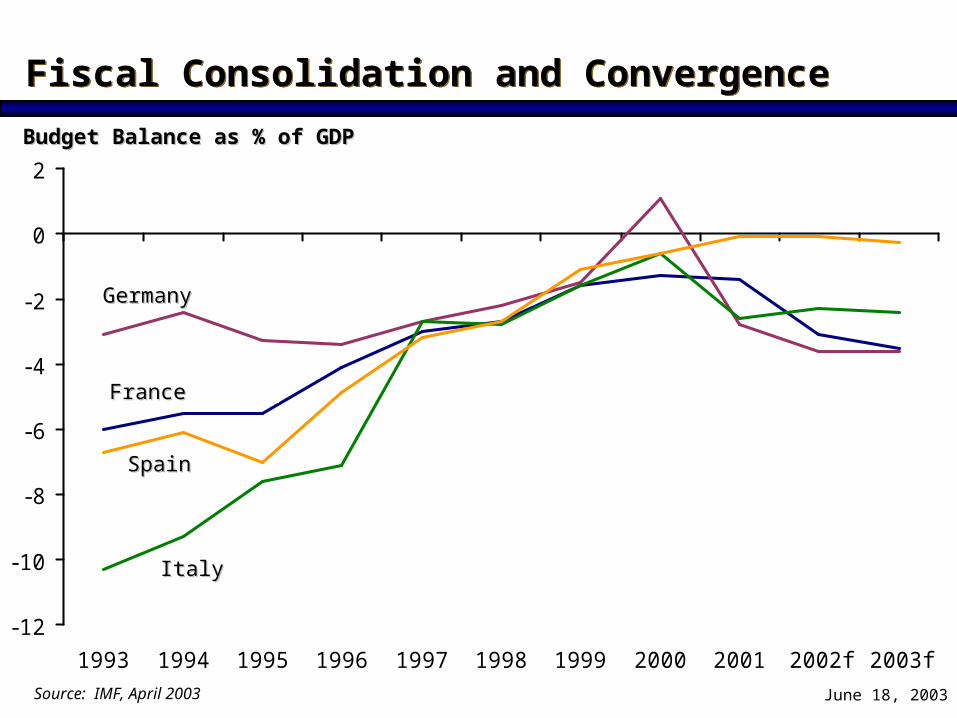

Fiscal Consolidation and ConvergenceFiscal Consolidation and Convergence

Source: IMF, April 2003

Budget Balance as % of GDPBudget Balance as % of GDP

FranceFrance

GermanyGermany

ItalyItaly

SpainSpain

June 18, 2003

Euroland Economic OutlookEuroland Economic Outlook

Euro strength & US weakness dampen growth prospects

Unemployment is rising again

Business & consumer confidence are falling

Controversies concerning the “stability and growth” pact

The German engine is lagging

Structural measures are essential for future growth

European Recovery Lags Behind USEuropean Recovery Lags Behind US

June 18, 2003

Euroland Recovery Lags Behind USEuroland Recovery Lags Behind US

2.4

0.81

0.20.4

21.8

2.2

0.6

1

0.2

0.6

22.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

US Euroland France Germany I taly Spain UK

2002E 2003F

% Real GDP Growth

Source: Merrill Lynch forecasts

June 18, 2003

Long Term Recession in JapanLong Term Recession in Japan

4.1

0.30.7

1.4

3.9

0.9

-2.9

-1.4

2.4

-0.2

0.2 0.21.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

1982-9

1

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003E

Real GDP %, YoY

OECD 10-year Avg = 2.4%OECD 10-year Avg = 2.4%Japan 10-year Avg = 0.5%Japan 10-year Avg = 0.5%

Source: ESRI, Merrill Lynch forecasts

June 18, 2003

-4.9

-3.8

-5.5

-7.1-7.4 -7.2

-7.7-7.4

-9.0

-8.0

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

F

Fiscal Laxity has Created Public Debt ProblemFiscal Laxity has Created Public Debt Problem

Japan Budget Balanceas % of GDP

Japan Gross Public Debtas % of GDP

Source: IMF World Economic Outlook, April 2003

92

108

134

154162

0

20

40

60

80

100

120

140

160

180

19

96

19

98

20

00

20

02

20

03

F

June 18, 2003

Slow Progress on Japanese Bank RestructuringSlow Progress on Japanese Bank Restructuring

A few major banks start to deal with bad loans and strengthen their capital base

But…

Under-provisioning for bad loans persists

Weak capital base and low profitability of banks limit speed of bad loan disposal

Market confidence in financial sector is low

June 18, 2003

Asian Economic OutlookAsian Economic Outlook

Growth remains strong across Asian region: China and India insulated by strong local markets Tech-dependent Asia pulled by policy easing

Countries with strong policy frameworks experience stronger growth

High level of foreign reserves and current account surpluses have reduced vulnerability

Incomplete corporate and bank restructuring

Solid Recovery Continues In 2003Solid Recovery Continues In 2003

June 18, 2003

Latin America Economic OutlookLatin America Economic Outlook

Smaller fiscal deficits and lower inflation are key

Corporate governance and political stability remain critical factors

Region dependent on capital inflows

Argentina: needs to be reborn Brazil: on the road to recovery Mexico and Chile: bright spotsVenezuela, Ecuador and Peru: in trouble

Outlook Reflects Domestic Policies and US GrowthOutlook Reflects Domestic Policies and US Growth

June 18, 2003

If US and Europe Stay the Course, Global If US and Europe Stay the Course, Global Recessionary Deflation Will Be AvoidedRecessionary Deflation Will Be Avoided

Global Recessionary Deflation?Global Recessionary Deflation?

US: Very unlikely Flexible and competitive economy High productivity growth Decisive policy response

Euroland: Unlikely but watch for Germany Benefits from single currency and convergence Structural rigidities Political and institutional challenges

Japan: In the midst of deflation Rigid policy framework Needs financial restructuring

END