product disclosure statement

TRANSCRIPT

Replacement Product Disclosure Statement

for the

Product Disclosure Statement dated 26 March 2015

for an offer of call and term deposits by

New Zealand Baptist Savings and Development Society Inc.

This document gives you important information about this investment to help you decide whether

you want to invest. There is useful information about this offer on www.business.govt.nz/disclose.

New Zealand Baptist Savings and Development Society Inc. has prepared this document in

accordance with the Financial Markets Conduct Act 2013.

You can also seek advice from a financial adviser to help you to make an investment decision.

Dated 30 April 2015

2

Section 1 - Key Information Summary

What is this?

This is an offer of call and term deposits. Call and term deposits are debt securities issued by New

Zealand Baptist Savings and Development Society Inc. (Baptist Savings, we, our or us). You give

Baptist Savings money, and in return Baptist Savings promises to pay you interest and repay the

money at the end of the term. If Baptist Savings runs into financial trouble, you might lose some or

all of the money you invested.

About Baptist Savings

Baptist Savings is an incorporated society and a registered charity (CC24623). Our purpose is to lend

money raised from depositors to New Zealand Christian churches and other organisations, although

our current lending policy is to lend only to Christian churches and registered charities. This is to

enable the borrowers to acquire and/or develop property and buildings, necessary for their worship,

community outreach, recreation and Christian witness (including church services). The property and

buildings are also used for camping facilities, medical centres, offices, day care centres, aged care

facilities and schools.

In January 2015, we were licensed by the Reserve Bank of New Zealand as a non-bank deposit taker.

Key terms of the offer

Call deposits

Description of call deposits

The call deposits are secured debt securities.

Term There is no fixed term as the call deposits are repayable on call.

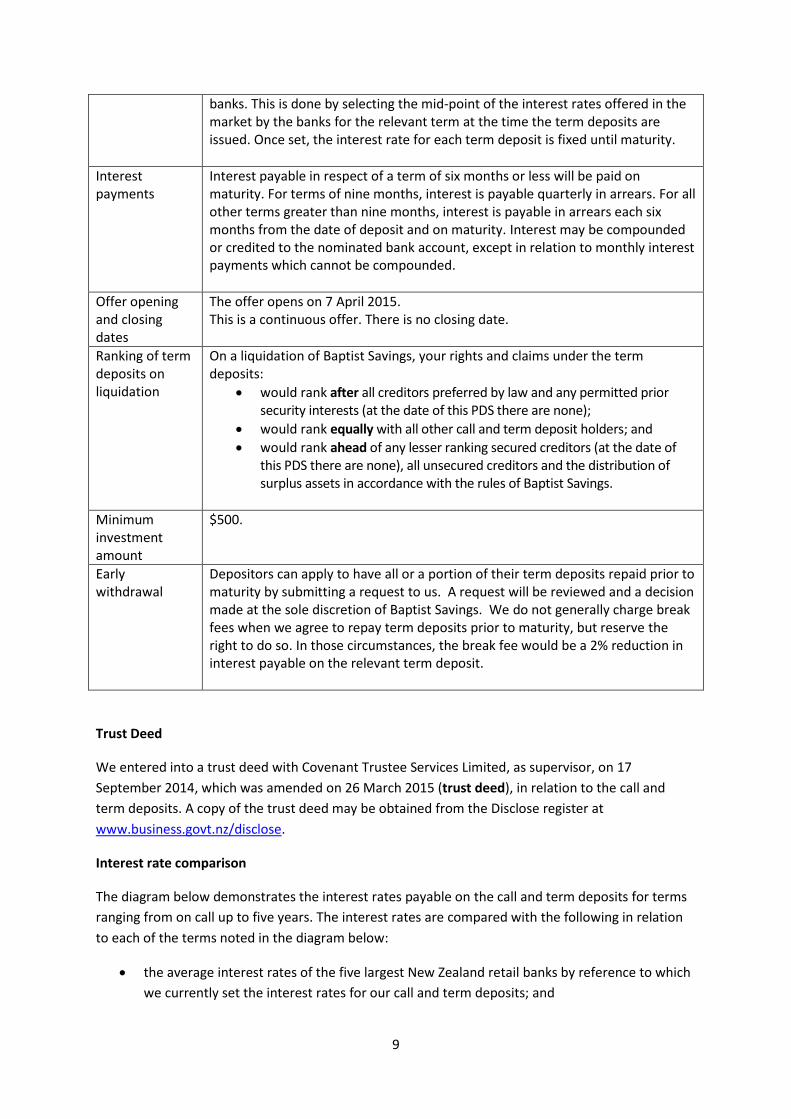

Interest rates The interest rate is available on our website and is subject to change without notice. The interest rate will be confirmed to you by letter following deposit. We set the interest rates on the call deposits on a regular basis after considering current market conditions. Our current policy is to set the interest rates by reference to the deposit interest rates of the five largest New Zealand banks. This is done by selecting the mid-point of the interest rates offered in the market by the banks at the time the call deposits are issued.

Interest payments

In arrears on 31 March and 30 September in each year (or where relevant, on the next business day following these dates) of the call deposit, or on closure of the call deposit.

Offer opening and closing dates

The offer opens on 7 April 2015. This is a continuous offer. There is no closing date.

3

Term deposits

Description of term deposits

The term deposits are secured debt securities.

Term Term deposits are issued for terms of 30 days, three months, six months, nine months, one year, 18 months, two years, three years and five years.

Interest rates The interest rates on the term deposits are set as described under “Interest rates” above. Once set, the interest rate for each term deposit is fixed until maturity.

Interest payments

Interest payable in respect of a term of six months or less will be paid on maturity. For terms of nine months, interest is payable quarterly in arrears. For all other terms greater than nine months, interest is payable in arrears each six months from the date of deposit and on maturity. Interest may be compounded or credited to the nominated bank account, except in relation to monthly interest payments which cannot be compounded.

Offer opening and closing dates

The offer opens on 7 April 2015. This is a continuous offer. There is no closing date.

Early withdrawal

Break fees may be charged at our discretion for early withdrawal. In those circumstances, the break fee would be a 2% reduction in interest payable on the relevant term deposit.

Who is responsible for repaying you?

Baptist Savings is responsible for repaying you, together with Baptist Savings Capital Limited and the

BSDS Strategic Trust, which are members of the Baptist Savings group, and guarantors in relation to

the call and term deposits. No other members of the Baptist Savings group are guarantors of the call

and term deposits.

How you can get your money out early

Depositors can apply to have all or a portion of their term deposits repaid prior to maturity by

submitting a request to us. However, the decision is made at our sole discretion. We do not

generally charge break fees when we agree to repay term deposits prior to maturity, but reserve the

right to do so as described above.

Baptist Savings does not intend to quote these call and term deposits on a market licensed in New

Zealand and there is no other established market for trading them. This means that you may not be

able to sell your call and term deposits before the end of their term.

4

How call and term deposits rank for repayment

On a liquidation of Baptist Savings, your rights and claims under the call and term deposits would

rank:

after all creditors preferred by law (e.g. the Inland Revenue for unpaid PAYE and employees

for holiday pay) and any permitted prior security interests (at the date of this PDS there are

none);

equally with all other call and term deposit holders; and

ahead of any lesser ranking secured creditors (at the date of this PDS there are none), all

unsecured creditors and the distribution of surplus assets in accordance with the rules of

Baptist Savings.

Further information regarding how the call and term deposits rank on the liquidation of Baptist Savings

can be found in section 4 of this PDS (key features of call and term deposits) on page 17.

What assets are these call and term deposits secured against?

Under the trust deed, we, Baptist Savings Capital Limited and the BSDS Strategic Trust, have each

granted a security interest to Covenant Trustee Services Limited as supervisor, which secures our

payment obligations under the call and term deposits. The security interests are over all present

and after-acquired personal property, and over real property and property other than personal

property.

Further information regarding the security interests can be found in section 4 of this PDS (key

features of call and term deposits) on page 17.

Where you can find Baptist Savings’ financial information

The financial position and performance of Baptist Savings are essential to an assessment of Baptist

Savings’ ability to meet its obligations under the call and term deposits. You should also read section

5 of this PDS (Baptist Savings’ financial information) on page 19.

Key risks affecting this investment

Investments in debt securities have risks. A key risk is that Baptist Savings does not meet its

commitments to repay you or pay you interest (credit risk). Section 6 of the PDS (risks of investing)

discusses the main factors that give rise to the risk. You should consider if the credit risk of these

debt securities is suitable for you. The interest rates for these call and term deposits should also

reflect the degree of credit risk. In general, higher returns are demanded by investors from

businesses with higher risk of defaulting on their commitments. You need to decide whether the

offer is fair.

5

Baptist Savings considers that the most significant risks factors are:

Loan default risk

If a number of borrowers defaulted on their loan obligations around the same time, there may be

insufficient funds to fully repay our depositors. As at the date of this PDS, our five biggest loans

represent approximately 23% of our loan portfolio. If all or a majority of the borrowers under these

loans defaulted around the same time, this could significantly increase the risk of default on our

payment obligations to depositors.

Interest rate margin risk

We make our income from the difference in the interest we pay to depositors and what we earn

from borrowers and our investments. We set the interest rates we pay by reference to the deposit

rates set by banks. In the event of a drop in interest rates, the interest rate we receive on surplus

funds we have invested with banks may be less than the amount we pay under the call and term

deposits and this could have a significant impact on the income we receive.

This summary does not cover all of the risks of investing in the call and term deposits. You should

also read section 6 of this PDS (risks of investing) on page 23.

What is Baptist Savings’ credit rating?

Baptist Savings’ credit rating is B+, Stable Outlook.

A credit rating is an independent opinion of the capability and willingness of an entity to repay its

debts (in other words, its creditworthiness). It is not a guarantee that the financial product being

offered is a safe investment. A credit rating should be considered alongside all other relevant

information when making an investment decision.

Baptist Savings has been rated by Fitch Ratings Inc. (Fitch). Fitch gives ratings from AAA through

to C.

Credit rating1 Description of the rating

AAA Highest credit quality

AA Very high credit quality

A High credit quality

BBB Good credit quality

BB Speculative

B Highly speculative

CCC Substantial credit risk

CC Very high levels of credit risk

C Exceptionally high levels of credit risk

RD Restricted default

D Default

1 The modifiers “+” or “-” may be added to the above ratings to indicate relative status within the major rating

categories.

6

Table of contents

Section 1 Key Information Summary 2

Section 2 Terms of the offer 8

Section 3 Baptist Savings and what it does 11

Section 4 Key features of call and term deposits 17

Section 5 Baptist Savings’ financial information 19

Section 6 Risks of investing 23

Section 7 Tax 26

Section 8 Who is involved? 27

Section 9 How to complain 27

Section 10 Where you can find more information 28

Section 11 How to apply 28

Section 12 Contact information 28

7

Letter from the Chairman of the Baptist Savings Board

Baptist Savings was established in 1962 with the objective of helping Baptist Churches and their members assist other Baptist Churches fund their building programmes. This objective remained unchanged for the next five decades, while we continued to grow our deposits and lend to churches in a lightly regulated environment as an exempted charity. That situation has changed significantly in recent years, with a raft of new regulations in the wake of the global financial crisis of 2007. Our recent growth along with lending opportunities led the board to start lending to churches and Christian charities outside of the "Baptist family". This change gained further momentum in 2014 when we were asked to assimilate the loan portfolio of Presbyterian Savings and Development Society of New Zealand Incorporated, a similar church financing organisation. The removal of the exemptions enjoyed until now have been replaced by a more robust regulatory regime, which means that we are now subject to:

• Reserve Bank of New Zealand oversight as a licensed non-bank deposit taker • An independent supervisor monitoring us • The Financial Markets Conduct Act which requires us to issue this PDS and maintain the

associated Disclose register entry • Anti-Money Laundering and Countering Financing of Terrorism Act • Having to obtain an independent credit rating

Our board aspires for Baptist Savings to provide the best level of service to our depositors as a non-bank deposit taker in New Zealand by embracing these changes. This PDS is just one of the steps being taken to help ensure we comply with our obligations under the new regulatory regime in the interests of our investors, while enabling our borrowing entities to achieve their missional goals in a financially viable way.

Graham Shaw Chairman

8

Section 2 Terms of the offer

Terms of the offer

Call deposits

Description of call deposits

The call deposits are secured debt securities.

Term There is no fixed term as the call deposits are repayable on call.

Interest rates The interest rate is available on our website and is subject to change without notice. The interest rate will be confirmed to you by letter following deposit. We set the interest rates on the call deposits on a regular basis after considering current market conditions. Our current policy is to set the interest rates by reference to the deposit interest rates of the five largest New Zealand banks. This is done by selecting the mid-point of the interest rates offered in the market by the banks at the time the call deposits are issued.

Interest payments

In arrears on 31 March and 30 September in each year (or where relevant, on the next business day following these dates) of the call deposit, or on closure of the call deposit.

Offer opening and closing dates

The offer opens on 7 April 2015. This is a continuous offer. There is no closing date.

Ranking of call deposits on liquidation

On a liquidation of Baptist Savings, your rights and claims under the call deposits:

would rank after all creditors preferred by law and any permitted prior security interests (at the date of this PDS there are none);

would rank equally with all other call and term deposit holders; and

would rank ahead of any lesser ranking secured creditors (at the date of this PDS there are none), all unsecured creditors and the distribution of surplus assets in accordance with the rules of Baptist Savings.

Minimum investment amount

$100, with minimum withdrawal amounts of $100.

Term deposits

Description of term deposits

The term deposits are secured debt securities.

Term Term deposits are issued for terms of 30 days, three months, six months, nine months, one year, 18 months, two years, three years and five years.

Interest rates The interest rates are available on our website and are subject to change without notice. The interest rate will be confirmed to you by letter following deposit. We set the interest rates on the term deposits on a regular basis after considering current market conditions. Our current policy is to set the interest rates by reference to the deposit interest rates of the five largest New Zealand

9

banks. This is done by selecting the mid-point of the interest rates offered in the market by the banks for the relevant term at the time the term deposits are issued. Once set, the interest rate for each term deposit is fixed until maturity.

Interest payments

Interest payable in respect of a term of six months or less will be paid on maturity. For terms of nine months, interest is payable quarterly in arrears. For all other terms greater than nine months, interest is payable in arrears each six months from the date of deposit and on maturity. Interest may be compounded or credited to the nominated bank account, except in relation to monthly interest payments which cannot be compounded.

Offer opening and closing dates

The offer opens on 7 April 2015. This is a continuous offer. There is no closing date.

Ranking of term deposits on liquidation

On a liquidation of Baptist Savings, your rights and claims under the term deposits:

would rank after all creditors preferred by law and any permitted prior security interests (at the date of this PDS there are none);

would rank equally with all other call and term deposit holders; and

would rank ahead of any lesser ranking secured creditors (at the date of this PDS there are none), all unsecured creditors and the distribution of surplus assets in accordance with the rules of Baptist Savings.

Minimum investment amount

$500.

Early withdrawal

Depositors can apply to have all or a portion of their term deposits repaid prior to maturity by submitting a request to us. A request will be reviewed and a decision made at the sole discretion of Baptist Savings. We do not generally charge break fees when we agree to repay term deposits prior to maturity, but reserve the right to do so. In those circumstances, the break fee would be a 2% reduction in interest payable on the relevant term deposit.

Trust Deed

We entered into a trust deed with Covenant Trustee Services Limited, as supervisor, on 17

September 2014, which was amended on 26 March 2015 (trust deed), in relation to the call and

term deposits. A copy of the trust deed may be obtained from the Disclose register at

www.business.govt.nz/disclose.

Interest rate comparison

The diagram below demonstrates the interest rates payable on the call and term deposits for terms

ranging from on call up to five years. The interest rates are compared with the following in relation

to each of the terms noted in the diagram below:

the average interest rates of the five largest New Zealand retail banks by reference to which

we currently set the interest rates for our call and term deposits; and

10

other than as noted below, the average interest rates of the three finance companies in New

Zealand having a credit rating between B and BB+.

Rates are as published at 12:00 noon on 24 March 2015 on www.interest.co.nz.

We are the only licensed non-bank deposit taker in New Zealand that is also a registered charity.

Because of this, our business is different to most other issuers of call and term deposits, in

particular, in the way we set the interest rates on our call and term deposits. Currently, we are the

only issuer of call and term deposits in the market which sets their interest rates in the way we do,

however, we have included the comparative data in the diagram below on the basis following.

The interest rates for the call and term deposits are determined by reference to the average deposit

rates of selected banks in New Zealand (as illustrated by the green bar in the diagram below), which

generally have a lower credit risk than us, in order to allow us to on-lend to our borrowers at

preferential rates. The five banks whose interest rates we currently use to set the interest rates on

the call and term deposits currently have credit ratings of between A- and AA-. Our credit rating is

currently B+.

The credit risk of the finance companies included in the diagram below is closer to our credit risk.

The three finance companies used to compile the data represented by the red bar in the diagram

below currently have credit ratings of between B and BB+. Our current credit rating of B+ sits within

this band. The difference between the interest rates on the call and term deposits (illustrated by the

blue bar) and the average interest rates of the finance companies used (illustrated by the red bar),

allows us to lend to our borrowers at lower interest rates.

The interest rates for the call and term deposits should reflect the degree of credit risk. However,

the interest rate you receive (as illustrated by the blue bar in the diagram below) may not reflect the

degree of credit risk in relation to our payment obligations under the call and term deposits. You

need to decide whether the offer is acceptable to you.

0

1

2

3

4

5

6

7

8

Interest Rate (%)

Term

Baptist Savings

Banks

Finance Companies

11

* The interest rates indicated by the red bars above for each of on call and the 90 day, six month and nine

month terms represent the interest rate offered by a single finance company, as the other two finance

companies do not offer terms of less than one year.

Section 3 Baptist Savings and what it does

Overview of Baptist Savings

The Baptist Savings group

The Baptist Savings group (Group) comprises three entities. The key operational arm is Baptist

Savings, which is an incorporated society and a registered charity that has been lending to Christian

churches and charities since its creation by the Baptist Union in 1962. It is the trading arm of the

Group, receiving call and term deposits and making loans to Christian churches and charities

throughout New Zealand. Anyone can invest with us.

Baptist Savings was originally set up by the Baptist Union of New Zealand, to allow the Baptist

community to deposit money to be lent to other Baptist churches and associated trusts. The

Baptist Union is governed by the Assembly Council, who together with the existing directors of

Baptist Savings, appoint any new directors of Baptist Savings. In 2013, our rules were amended to

allow us to lend to other Christian churches and organisations, although our current lending policy

requires the borrower organisations to be registered charities.

In January 2015, we were licensed by the Reserve Bank of New Zealand as a non-bank deposit taker.

Baptist Savings is supported by the BSDS Strategic Trust, which is the investment arm of the Baptist

Savings Group. The BSDS Strategic Trust holds surplus funds of the Group and invests these funds

with banks and in the bond market in order to enable us to meet our obligations to depositors and

borrowers under the loans. The BSDS Strategic Trust is a registered charity. Seven directors of

Baptist Savings are also trustees of the BSDS Strategic Trust.

The third component is Baptist Savings Capital Limited, which is a registered charity. Baptist Savings

Capital Limited has issued shares to the Presbyterian Savings and Development Society of New

Zealand Incorporated, and also to some of our borrowers representing 5% of their loans (as

described in Note 3 on page 23 of this PDS).

Three directors of Baptist Savings Capital Limited are also directors or senior managers of Baptist

Savings.

The BSDS Strategic Trust and Baptist Savings Capital Limited are guarantors in relation to the call and

term deposits.

Our operations and activities

(a) Loan application and loan assessment policies

Typically Christian churches or charities approach us to discuss projects for which they need finance.

If that initial contact is positive they fill out an application form which gathers data from them and

12

authorises us to gather data from others. You can find a copy of this on our website, see

www.baptistsavings.co.nz.

The key questions that we need to answer when assessing a loan application are:

Does the project appear to be well conceived, given, who they are and what they are trying

to achieve in their particular context, and is it consistent with our purpose (see section 1

‘About Baptist Savings’)?

Do they have the income and means to make the payments to service the loan they are

seeking? We require copies of their financial statements as evidence of this.

Is there adequate security if something goes wrong?

Have they invested with us in the past?

If we don’t know them well, are there credible people who can speak for the applicant’s

integrity and whether they are a ‘good risk’ to lend to?

Are they a registered charity?

Our General Manager then writes a report for the relevant decision maker(s) (as noted below) to

consider, with a recommendation to grant or not grant the loan. The delegated authority levels for

granting loans as at the date of this PDS are as follows, if the loan is:

Less than $250,000, the General Manager decides.

$250,000 - $500,000, the Finance Committee of the board decides.

Over $500,000 or for any loan of any amount outside of normal policy settings, the full

board decides.

Our loan application and loan assessment policies may be changed by the board of Baptist Savings

without notice.

All loans granted are reported to the full board at the following board meeting. The board is also

advised of applications that are declined and the reasons for those decisions.

(b) Security

Before any funds are advanced to a borrower, we require the return of:

A completed loan agreement; and

A certificate confirming insurance is in place.

We also require confirmation that the mortgage has been registered on settlement.

(c) Engaging with borrowers who are struggling to meet their obligations to us

Since 2010, only three of our borrowers have got into the position where they have not been able to

make payments.

In these situations, we immediately make contact with the borrower, progressing to a face to face

meeting if problems continue. The board is notified as soon as a loan is technically in default, and

is involved in any decision on how to respond. We also engage with the relevant denominational

or other applicable leadership groups, and on two occasions in the past 10 years, have funded

advisors to assist struggling borrowers.

13

(d) Our loan portfolio

The table below shows the pattern of who we lend to by borrower type as at 28 February 2015.

Type of borrower Number of loans Percentage of total value of loan portfolio

Baptist & Presbyterian churches 104 62%

Other churches 27 20%

Christian charities 30 18%

Total 161 100%

Historically, due to the nature of our business and the Christian context in which we operate,

economic downtowns have not had a material effect on the level of deposits we receive or the

volume of loans made to our borrowers. We have a reinvestment rate of over 90% with our

depositors as at the date of this PDS.

The recessions experienced over the last 25 years as noted in the table below have not had a

material impact on our financial position. We have used the term recession not only in the narrow

sense of two quarters of negative economic growth, but also in the wider sense of a sustained

period of poor economic performance2. See the table below which lists years affected by recession

over the last 25 years and our performance during those periods:

Recession Year

Deposits ($m)

Capital3 ($000’s)

Surplus4 ($000’s)

1989 3.4 231 2

1990 3.8 284 42

1991 5.3 305 42

1992 7.3 408 100

1993 9.6 549 126

1998 15.1 1113 99

2008 33 4,726 354

2009 49.7 5,377 571

Please note that the information above represents an historic trend and there is no guarantee that

this trend will continue in future. A recession or economic downturn may impact the ability of our

borrowers to make repayments under the loans, or the level of deposits we receive, either or both

of which may impact our profitability in future. Please note that past performance is not a guide to

future performance.

Most of the land and buildings that our loans are secured over are used as churches, so are either

purpose built for this or have been adapted to suit that purpose. Some of the land and buildings are

2 See the statistics at rbnz.govt.nz/statistics/key-graphs/graphdata.xls, and the discussion on page 4 of

http://www.rbnz.govt.nz/research_and_publications/discussion_papers/2014/dp14_02.pdf 3 Capital comprises retained earnings.

4 Surplus is the equivalent of net profit.

14

set up as camping facilities, medical clinics, early childhood centres, aged care facilities, schools and

offices. The residential properties are zoned for that use and if not currently being used as such,

could be converted back to being purely private residences and sold.

The first table below breaks our loans down into commercial property loans, or mixed commercial

and residential property loans (where the property is predominantly commercial). The second table

below breaks our loans down into residential property loans, or mixed residential and commercial

property loans (where the property is predominantly residential). Our practice has been to take an

Auckland District Law Society form registered ‘all obligations’ first ranking mortgage security over all

advances, with two exceptions. The first is for loans less than $20,000 and the second is for loans

made from the Jubilee Fund, which is an historic fund that is for starting churches which was gifted

to us by the Baptist Union in 2014. As at the date of this PDS, there are two unsecured loans made

from the Jubilee Fund which are outstanding that are for sums greater than $20,000.

What is the loan to value ratio referred to in the tables below? This is the amount borrowed divided

by the value of the property the borrower is providing as security, e.g. $100,000 (loan) / $500,000

(value of security) = 20% loan to value ratio. This provides us with a degree of comfort that the

security provided by the borrower should be sufficient to cover the amount of the loan in the event

of a borrower default. Lower loan to value ratios provide greater comfort than higher ones. We

require a registered or government valuation as evidence of the loan to value ratio.

Loans over commercial and predominantly commercial property as at 28 February 2015

Loan to Value Ratio

Number of loans

Total value of loans

Percentage of loan portfolio

80%+ 1* $1.2m 2%

60-79% 4 $2.4m 4%

40-59% 21 $20.4m 34.4%

20-39% 31 $24.6m 41.4%

0-19% 64 $10.5m 18%

Unsecured 2 $0.089m 0.2%

Total 123 $59.3m 100%

* This loan was repaid on 24 March 2015.

Loans secured over residential and predominantly residential property as at 28 February

2015

Loan to Value Ratio

Number of loans

Total value of loans

Percentage of loan portfolio

80%+ 0 0 0%

60-79% 6 $4.9m 39%

40-59% 6 $2.4m 19%

20-39% 11 $4.3m 34%

0-19% 15 $0.9m 8%

Total 38 $12.5m 100%

Notes:

1. If the residential property market price level dropped by 20% then none of our borrowers (as at

28 February 2015) would be in a negative equity position (i.e. their loan would not be larger than the

15

value of their property), as none have a loan to value ratio over 80% based on the current valuations

that we hold. The market would have to fall by 25% before the value of any property that we have a

loan over, would be less than the loan secured by it.

2. If the commercial property market price level dropped by 25% then only 1 out of 123 of our

borrowers (as at 28 February 2015) would be in a negative equity position. As noted above, this loan

was repaid on 24 March 2015.

3. If we enforced a mortgage and sold a building but there were insufficient proceeds to completely

repay the loan, we still have the right to sue the church or charity to recover any money owed. While

we reserve the right to do so in a particular case, depositors are best to assume that we would not

use aggressive recovery strategies such as these against a church community and its members. Thus,

if the proceeds of a mortgagee sale were insufficient to discharge a church’s debt, then we will likely

take a loss from our capital.

Purchase of Presbyterian Savings and Development Society of New Zealand Incorporated’s loan

portfolio and depositors’ funds

In 2013, our rules were amended so that we could lend to other Christian churches and

organisations, not just Baptist churches and organisations.

As a result of this, we were able to purchase the Presbyterian Savings and Development Society of

New Zealand Incorporated’s $14 million loan portfolio on 31 October 2014, including the transfer to

us of $32 million of their depositors’ funds for a payment of $60,000.

The effect of these two changes is that we now have over $19 million in non-Baptist lending, which is

over 25% of our total lending at the date of this PDS and we expect this to increase further.

One of the conditions of our contract with Presbyterian Savings and Development Society of New

Zealand Incorporated, is that we will pay them a retention bonus on 30 November 2015 of 0.5% of

the total value of their former deposits that are still lodged with us on 30 October 2015.

The industry in which we operate

For over 50 years, we have been offering call and term deposits to the public, and anyone can

invest with us. We are classified as a non-bank deposit taker and are licensed under the Non-

bank Deposit Takers Act 2013. We are part of the financial services industry and operate

alongside banks and other non-bank deposit takers which issue call and term deposits.

However, we are the only licensed non-bank deposit taker in New Zealand that is also a registered

charity. We are also unique in that our current lending policy only allows us to lend to Christian

churches and other registered charities that have a Christian purpose.

Churches and charities typically rely heavily on donations from members and others, which by

their voluntary nature cannot be guaranteed. However, increasingly churches have other sources

of income and our loans are also serviced by the profits of early childhood centres, office rents

and aged care fees.

16

Keys to generating income

The basic keys for us to generate income are:

Interest Rate Margin: the preservation of the rate margin between what we pay our

depositors, and what we can lend those funds out for (the margin for which is typically 2%)

or alternatively, what we can invest any surplus funds with the banks for (the margin for

which is typically between 0.25% and 0.5%);

Investment Portfolio: growing our loan portfolio and having less invested with the banks as

a proportion is critical to our profitability, together with the effective management of our

investments;

Growing non-Baptist Lending: between 2013 and the date of this PDS, we have added 57

non-Baptist loans to our portfolio for a total of $22 million, and are working on raising our

profile in other Christian denominations and churches through advertising, seminars and

networking.

Board of directors and senior management

Directors

The chair of our board is Graham Shaw BCom who has been on the board since 2008, and is a member of Wellington Central Baptist Church. He is a:

Chartered Accountant of the New Zealand Institute of Chartered Accountants

Member of the Institute of Directors of New Zealand

Fellow of the New Zealand Institute of Management

Companion of the Institute of Professional Engineers New Zealand

Non-executive director of Xero Limited

Non-executive director of Gentrack Group Limited

Non-executive director of Pushpay Holdings Limited

He is also involved in the governance of three other companies.

He was previously the:

Chief Executive of the national law firm Kensington Swan from 2002 to 2004

Chief Executive of Works Infrastructure from 1997 to 2002

Chief Financial Officer of Works Civil Construction from 1989 to 1997

James Palmer BA LLB has been on the board since 2014. He has been a solicitor with Palmer &

Associates Law since 2011, practicing in general commercial law.

Gray Hughson BCA has been on the board since 2014, and is a member of Karori Baptist Church. He is a consultant for Moore Stephens, Markham Wellington Limited, having previously been a principal in various accounting firms since 1973. He holds a variety of directorships and is a member of the Institute of Directors. Elizabeth Johnstone DipPharm has been on the board since 2014, and is a member of Karori Baptist Church. She is a New Zealand registered pharmacist, and since 2004 has been the National Manager of the Professional Development programme for New Zealand pharmacists. Previously she was the National Moderator, Pharmacy Industry Training Organisation from 2002 to 2007, and the

17

Assessor/Moderator of New Zealand national pharmacist registration exams since 1998. Alastair McLay BCom BD has been on the board since 1989, and is a member of Northcote Baptist

Church. He is currently the manager of Christians Against Poverty in Northcote, and was previously

the Director of Finance and Business Services for NZI from 1989 to 2003.

Rod Robson LLB BAppTheol (Carey) who has been on the board since 2011, is a member of Linwood

Baptist Church. He has been a pastor, a youth pastor, the chief legal advisor for Work and Income,

and is currently working as a consultant for us on compliance and regulatory issues.

Roger Nicholson has been a director since 2004, and is a member of Nelson Baptist Church. He is a

trustee of the City of Nelson Civic Trust and the Managing Trustee of the Nelson Christian Trust. He

was previously employed by Duncan Cotterill Asset Management from 1999-2011, and has a

background in small and medium sized business management.

Daniel Palmer DipBus has been an ex officio director since 2012, when he was appointed as the

National Administrator of the Baptist Union. He is a member of Manukau City Baptist Church. He

has a background in the financial management of companies and was the financial controller for DHL

NZ Limited and the financial manager of Air New Zealand.

Senior managers

Our General Manager is John Smeaton, who has held that position since 2009, and is a member of

Laingholm Baptist Church. Prior to that he was an accountant with BDO Spicers and worked for the

Bank of New Zealand as a Branch Manager and Agribusiness Manager.

Our Business Development Manager is Andrew L’Almont, who has held that position since 2011 (he

was previously a director). He is a registered financial advisor. He was the CEO/Director for

Mortgage Express Limited from 2000 to 2011 and the CEO/Director of Harcourts Financial Services

from 1998 to 2000.

Section 4 Key features of call and term deposits

Ranking and security

The call and term deposits are secured by a security interest which we have granted under the terms of

the trust deed over all of our assets to Covenant Trustee Services Limited, as supervisor. The security

interest secures all amounts payable by us on the call and term deposits and all other moneys payable

by us under the terms of the trust deed. As at 28 February 2015, the amount of the liability secured by

the security interest was $126,571,714 and the total value of the assets subject to the security interest

was $135,741, 862. 5 In the event of our liquidation, the call and term deposits would rank equally

with all other call and term deposits and behind all preferred claimants and any permitted prior security

interests (at the date of this PDS there are none).

We may incur further liabilities which rank equally with, or in priority to, the call and term deposits on

our liquidation, including by issuing further call and term deposits. This could also include fees payable

5 These amounts are estimated based on unaudited financial information as at 28 February 2015.

18

to our supervisor, Covenant Trustee Services Limited, under the trust deed, any fees payable to a

receiver appointed in respect of our assets, statutory based claims such as employee entitlements,

outstanding interest payments and amounts owing to trade creditors.

We are also permitted under the trust deed to create security interests over our assets which rank in

priority to the security interests granted in favour of Covenant Trustee Services Limited under the trust

deed to secure any borrowing or money owed in purchasing or acquiring assets, provided that the

amount secured by all prior ranking security interests does not exceed 1% of our total tangible assets.

Except as set out above, the trust deed prevents us from creating any security interest over our

property which ranks in priority to, or equally with, the security interest granted to Covenant Trustee

Services Limited under the trust deed in relation to the call and term deposits.

As at the date of this PDS, we have not granted any security interests which rank in priority to, or

equally with, Covenant Trustee Services Limited’s security interest.

The diagram below illustrates the ranking of the call and term deposits on our liquidation6 and is based

on $91,523,721 of call and term deposits being in issue, being the number of call and term deposits

issued by Baptist Savings as at 31 August 2014.

Ranking on liquidation of Baptist Savings

Examples Indicative amount as at 31.08.14

Higher ranking/earlier priority Lower ranking/later priority

Liabilities that rank in priority to the call and term deposits

Creditors preferred by law (including IRD for unpaid tax) and any permitted prior ranking security interests

$50,318

Liabilities that rank equally with the call and term deposits

Call and term deposits, including the accrued interest

$92,459,521

Liabilities that rank below the call and term deposits

Lesser ranking secured creditors and unsecured creditors

$22,674

Equity

Distribution of surplus assets

$8,675,485

Guarantees

Both the BSDS Strategic Trust and Baptist Savings Capital Limited are part of the Group, and have

given unlimited and unconditional guarantees in relation to our obligations under the call and term

6 The financial information in this table is stated as at 31 August 2014, however, we granted the security

interest to Covenant Trustee Services Limited under the trust deed on 17 September 2014. The information in this table has therefore been adjusted to reflect the position had the security interest been in place on 31 August 2014.

19

deposits by executing guarantor accession deeds in favour of Covenant Trustee Services Limited, as

supervisor, and for the benefit of our depositors. These guarantees are secured by a security interest

over all present and after-acquired personal property, and over real property and property other

than personal property.

The security interest is insufficient to repay the liability of the guarantee.

Covenant Trustee Services Limited does not guarantee our obligations under the call and term

deposits.

Transfer

Baptist Savings does not intend to quote these call and term deposits on a market licensed in

New Zealand and there is no other established market for trading them. This means that you may

not be able to sell the call and term deposits before the end of their term.

The trust deed permits Baptist Savings to delay a transfer of the call and term deposits to undertake

customer due diligence on the transferee to its satisfaction in accordance with the requirements of

the Anti-Money Laundering and Countering Financing of Terrorism Act 2009 and may charge a fee to

you for conducting the customer due diligence.

Section 5 Baptist Savings’ financial information

Baptist Savings is required by law and its trust deed to meet certain financial requirements. This

table shows how Baptist Savings is currently meeting those requirements. These are minimum

requirements. Meeting them does not mean that Baptist Savings is safe. The section on specific

risks relating to Baptist Savings’ creditworthiness sets out risk factors that could cause its financial

position to deteriorate. The offer register provides a breakdown of how the figures in this table are

calculated, as well as full financial statements.

20

Key Ratios

Capital Ratio7 8

31.8.14

31.8.13

31.8.12

Capital ratio 10.5% 10.7% 10.0%

Minimum capital ratio as per the trust deed

8% with a credit rating, 10% without a credit rating

Not applicable. The trust deed was entered into on 17 September 2014

Not applicable. The trust deed was entered into on 17 September 2014

Minimum capital ratio that must be set out in the trust deed under the Deposit Takers (Credit Ratings, Capital Ratios, and Related Party Exposures) Regulations 2010

8% with a credit rating, 10% without a credit rating

8% with a credit rating, 10% without a credit rating

8% with a credit rating, 10% without a credit rating

The capital ratio is a measure of the extent to which Baptist Savings is able to absorb losses without becoming insolvent. The lower the capital ratio, the fewer financial assets Baptist Savings has to absorb unexpected losses arising out of its business activities.

7 We are exempt from the requirements under sections 34 and 35 of the Non-bank Deposit Takers Act 2013 to

include a capital ratio within the trust deed and to maintain our capital ratio in accordance with the amount included in the trust deed until 30 November 2016 by virtue of the Deposit Takers (Charities) Exemption Notice 2014. The trust deed requires us to maintain the capital ratio as referred to in the third row in the table above. We are also exempt from the requirements under sections 23 and 25 of the Non-bank Deposit Takers Act 2013 to have a current credit rating and in relation to governance until 1 May 2015 by virtue of the Deposit Takers (Charities) Exemption Notice 2014. However, as noted above, we have obtained a credit rating. 8 The capital used to calculate the capital ratio noted above includes fully paid up perpetual non-cumulative

preference shares issued by Baptist Savings Capital Limited to certain churches and charities who have borrowed from us. The shares that have been issued to the churches and charities represent 5% of the loans made to them by Baptist Savings and were funded by those loans. The purpose of the shares is to raise capital for Baptist Savings to meet our capital requirements under the non-bank deposit taker regime supervised by the Reserve Bank of New Zealand. These shares may count for up to 25% of our total capital. The Reserve Bank of New Zealand is currently considering whether in future, shares which have been funded in this manner may be counted as capital. The board of Baptist Savings is currently reviewing its capital policy to ensure that whatever decision the Reserve Bank of New Zealand reaches, Baptist Savings continues to meet the capital requirements.

21

Related Party Exposures9

31.8.14 31.8.13 31.8.12

Aggregate exposure to related parties as calculated under the Deposit Takers (Credit Ratings, Capital Ratios, and Related Party Exposures) Regulations 201010

105% 111% 121%

Maximum limit on aggregate exposures to related parties under trust deed

15% of capital with effect from 1 November 2016.

Not applicable. The trust deed was entered into on 17 September 2014

Not applicable. The trust deed was entered into on 17 September 2014

Maximum limit on aggregate exposures to related parties under trust deed that must be included under the Deposit Takers (Credit Ratings, Capital Ratios, and Related Party Exposures) Regulations 2010

15% 15% 15%

Related party exposures are financial exposures that Baptist Savings has to related parties. A related party is an entity that is related to Baptist Savings through common control or some other connection that may give the party influence over Baptist Savings (or Baptist Savings over the

9 We are exempt from the requirements under sections 37 and 38 of the Non-bank Deposit Takers Act 2013 to

include a maximum limit on related party exposures within the trust deed and to not exceed the maximum limit on related party exposures until 30 November 2016 by virtue of the Deposit Takers (Charities) Exemption Notice 2014. 10

We have applied for a specific exemption from the Reserve Bank of New Zealand to the effect that the Baptist Union will not be considered a related party for the purposes of our related party exposure calculations which we will be required to comply with from 30 November 2016. That application is still being considered as at the date of this PDS. For the purposes of the calculations set out above, we have assumed that the Baptist Union is not a related party.

22

related party). These related parties include, for example, the BSDS Strategic Trust and Baptist Savings Capital Limited as well as churches we lend to that our directors or their children attend or trusts of which our senior managers or their spouses are trustees.

Liquidity Ratio11 31.8.14 31.8.13 31.8.12

Liquidity calculated in accordance with the trust deed

20% 16% 22%

Minimum liquidity requirements under the trust deed

15% Not applicable. The trust deed was entered into on 17 September 2014

Not applicable. The trust deed was entered into on 17 September 2014

Liquidity requirements help to ensure that Baptist Savings has sufficient realisable assets on hand to pay its debts as they become due in the ordinary course of business. Failure to comply with liquidity requirements may mean that Baptist Savings is unable to repay investors on time, and may indicate other financial problems in its business.

Selected financial information

Year to 31.8.2014

Year to 31.8.2013

Year to 31.8.2012

Total assets $101.2m $93.5m $81.3m

Total liabilities $92.5m $85.6m $74m

Net profit after tax $0.3m $0.4m $0.6m

Net cash flows from operating activities

$0.7m $0.7m $0.5m

Cash and cash equivalents $2.5m $3.9m $4.1m

Capital $8.7m $7.9m $7.3m

Notes:

1. Total assets have increased strongly since 2012 because of a sustained marketing programme to

increase our deposit base, and more recently the transfer to us of $32 million in deposits previously

invested with the Presbyterian Savings and Development Society of New Zealand Incorporated.

11

We are exempt from the requirements under sections 40 and 41 of the Non-bank Deposit Takers Act 2013 to ensure the trust deed contains liquidity requirements and to comply with the liquidity requirements set out in the trust deed until 30 November 2016 by virtue of the Deposit Takers (Charities) Exemption Notice 2014. We are required to manage our liquidity in accordance with requirements set out in the trust deed.

23

2. Net profits have reduced since 31 August 2014 because of the write down of a loss made on an

investment, and the recent high costs of regulatory compliance e.g. obtaining a credit rating,

supervisor costs, increased legal advice, etc.

3. Capital is made up of retained earnings and fully paid up perpetual non-cumulative preference

shares issued by Baptist Savings Capital Limited to churches and charities who have borrowed from

us. The shares that have been issued to the churches and charities represent 5% of the loans made

to them by Baptist Savings and were funded by those loans. The purpose of the shares is to raise

capital for Baptist Savings to meet our capital requirements under the non-bank deposit taker

regime supervised by the Reserve Bank of New Zealand. These shares may count for up to 25% of

our total capital. The Reserve Bank of New Zealand is currently considering whether in future,

shares which have been funded in this manner may be counted as capital. The board of Baptist

Savings is currently reviewing its capital policy to ensure that whatever decision the Reserve Bank of

New Zealand reaches, Baptist Savings continues to meet the capital requirements.

4. Baptist Savings is exempt from income tax due to its charitable status. Revenues, expenses and

other assets are recognised inclusive of the amount of GST as Baptist Savings is a provider of

financial services.

Financial covenants

The trust deed with Covenant Trustee Services Limited requires that:

The maximum amount owing by any one borrower or a related group of borrowers (such as

organisations or charities which are related through common membership or control)

cannot exceed the greater of 35% of our capital, or $5 million. However, the supervisor has

the power to waive this requirement in an appropriate case, as it has done once previously

in order to allow one of our borrowers to purchase the loan of another which was in default.

We may only borrow on the security of a security interest that ranks in priority to that

granted to Covenant Trustee Services Limited under the trust deed up to the value of 1% of

our total tangible assets.

Section 6 Risks of investing

General risks

Your investment is subject to the general risk that we become insolvent and are not able to meet

our obligations to you to pay interest and to repay the principal when due under the call and term

deposits.

In the event we experience significant losses through banks or companies whose bonds that we have

invested in becoming insolvent, and/or we experience significant losses through our lending, we may

not have the funds to meet our obligations to our investors under the terms of any call or term

deposit.

24

Specific risks relating to Baptist Savings’ creditworthiness

Loan default risk

Baptist Savings provides loans. If a number of borrowers defaulted on their loan obligations at or

around the same time, there may be insufficient funds to fully repay our depositors.

As at the date of this PDS, our five biggest loans represent approximately 23% of our loan portfolio.

If all or a majority of the borrowers under these loans defaulted at or around the same time, this

could significantly increase the risk of default on our payment obligations to depositors.

In these situations, we immediately make contact with the borrower, progressing to a face-to-face

meeting if problems continue. The board is notified as soon as a loan is technically in default, and is

involved in any decision on how to respond. We also engage with the relevant denominational or

other applicable leadership groups, and on two occasions in the past 10 years, have funded advisors

to assist struggling borrowers.

While a registered first mortgage provides additional security for us in the event of a default by a

borrower, it does not provide immediate recovery of any funds still outstanding. As it could be a

significant period of time before a property could be sold, there would be a delay between a

borrower defaulting and when we could recover some or all of the loan from the sale of a property.

From 2010 to the date of this PDS, three of our borrowers have defaulted under their loans.

Interest rate margin risk

We are unique in relation to other non-bank deposit takers in that we set the interest rates on the

call and term deposits by reference to the deposit rates set by the five largest New Zealand banks.

For us, this means that a drop in interest rates would affect the interest rate we receive on surplus

funds we have invested with banks and we may receive less than the amount we pay under the call

and term deposits. This could have a significant impact on the income we receive. Should this

situation occur, we would have the option to raise the interest rates payable by borrowers under

some of the loans, however, there are naturally limits on our ability to do this as significant interest

rate increases may cause our borrowers to default or have to refinance or repay their loans.

This could significantly increase the risk of default on our payment obligations under the call and

term deposits.

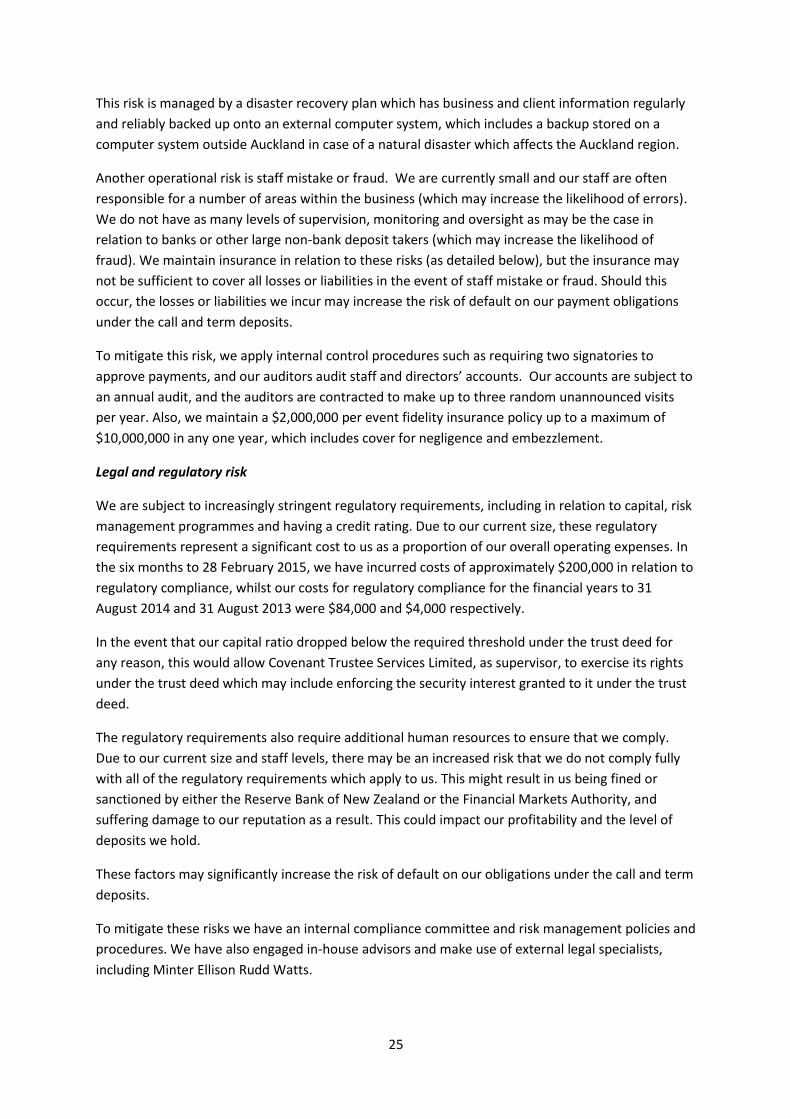

Operational risk

Unlike banks or other large non-bank deposit takers which may have internal IT specialists, due to

our size, we do not have internal IT personnel but rely on external third parties to effectively manage

our business including administering loans and making repayments to our depositors. We also rely

on a financial software programme from an external provider which is not designed specifically for

Baptist Savings. In the event of a system failure or degradation, the fact that we do not have internal

IT personnel may result in the loss of information or there may be significant delays in recovering

payments from our borrowers or meeting our payment obligations to depositors. This may increase

the risk of default on our payment obligations under the call and term deposits.

25

This risk is managed by a disaster recovery plan which has business and client information regularly

and reliably backed up onto an external computer system, which includes a backup stored on a

computer system outside Auckland in case of a natural disaster which affects the Auckland region.

Another operational risk is staff mistake or fraud. We are currently small and our staff are often

responsible for a number of areas within the business (which may increase the likelihood of errors).

We do not have as many levels of supervision, monitoring and oversight as may be the case in

relation to banks or other large non-bank deposit takers (which may increase the likelihood of

fraud). We maintain insurance in relation to these risks (as detailed below), but the insurance may

not be sufficient to cover all losses or liabilities in the event of staff mistake or fraud. Should this

occur, the losses or liabilities we incur may increase the risk of default on our payment obligations

under the call and term deposits.

To mitigate this risk, we apply internal control procedures such as requiring two signatories to

approve payments, and our auditors audit staff and directors’ accounts. Our accounts are subject to

an annual audit, and the auditors are contracted to make up to three random unannounced visits

per year. Also, we maintain a $2,000,000 per event fidelity insurance policy up to a maximum of

$10,000,000 in any one year, which includes cover for negligence and embezzlement.

Legal and regulatory risk

We are subject to increasingly stringent regulatory requirements, including in relation to capital, risk

management programmes and having a credit rating. Due to our current size, these regulatory

requirements represent a significant cost to us as a proportion of our overall operating expenses. In

the six months to 28 February 2015, we have incurred costs of approximately $200,000 in relation to

regulatory compliance, whilst our costs for regulatory compliance for the financial years to 31

August 2014 and 31 August 2013 were $84,000 and $4,000 respectively.

In the event that our capital ratio dropped below the required threshold under the trust deed for

any reason, this would allow Covenant Trustee Services Limited, as supervisor, to exercise its rights

under the trust deed which may include enforcing the security interest granted to it under the trust

deed.

The regulatory requirements also require additional human resources to ensure that we comply.

Due to our current size and staff levels, there may be an increased risk that we do not comply fully

with all of the regulatory requirements which apply to us. This might result in us being fined or

sanctioned by either the Reserve Bank of New Zealand or the Financial Markets Authority, and

suffering damage to our reputation as a result. This could impact our profitability and the level of

deposits we hold.

These factors may significantly increase the risk of default on our obligations under the call and term

deposits.

To mitigate these risks we have an internal compliance committee and risk management policies and

procedures. We have also engaged in-house advisors and make use of external legal specialists,

including Minter Ellison Rudd Watts.

26

Liquidity risk

Our ability to meet our payment obligations to depositors is linked to our lending activities and the

repayment by borrowers of amounts outstanding under the loans we provide to them. The amounts

received from depositors are held for a short term (from 30 days to five years), while the amounts

we lend to borrowers are lent for significantly longer terms. At the date of this PDS, our maximum

loan term is 20 years, although because we do not charge penalties for early repayment, loans are

often repaid prior to maturity. Depositors may also withdraw their deposits prior to the expiry of the

term in certain circumstances. Because of this, there is a risk that at any one time there might not be

enough cash to fully meet our obligations to our depositors.

We mitigate this risk by maintaining at least 15% of the funds we have invested with banks in liquid

short term cash investments to cover the possibility that a lot of deposits are not renewed on

maturity. At the date of this PDS, we have over 40% of the funds we have invested with banks in

such short term cash investments and we have a reinvestment rate of over 90% with our depositors.

All loans made to borrowers are subject to being called up at any time.

Concentration risk

We only lend to Christian churches and other Christian charities in New Zealand. Churches and

charities typically rely heavily on donations from members and others, which by their voluntary

nature cannot be guaranteed. Therefore, the income received by our borrowers may not be

consistent and this may impact their ability to make payments to us under the loans. However,

increasingly churches have other sources of income and our loans are also serviced by the profits of

early childhood centres, office rents and aged care fees.

Due to the nature of Christian churches (many being unincorporated societies), enforcing any

security provided in relation to a loan may be more difficult and costly than would be the case for

individual or corporate borrowers. This may affect the amount we recover under a loan. Similarly,

because our purpose is to provide financing to Christian churches and charities, in the event of a

default under a loan, we are unlikely to use aggressive recovery strategies which would involve us

suing a church, charity or its members. Thus, if the proceeds of a mortgagee sale were insufficient

to discharge a borrower’s debt, then we will likely take a loss in relation to the loan.

These factors may significantly increase the risk of default on our payment obligations to depositors.

We mitigate this risk through our conservative lending policies, of generally only lending up to a 60%

loan to value ratio for commercial property (including church buildings) and 80% for residential

property.

Section 7 Tax

New Zealand residents will have resident withholding tax deducted from their interest payments,

and there may be other tax consequences from acquiring or disposing of the call and term deposits.

The resident withholding tax rates at the date of this PDS are 28% for companies (other than

corporate trustees) and 10.5%, 17.5%, 30% and 33% for all other investors. If you do not provide us

27

with your IRD number, you will automatically have resident withholding tax deducted at the

maximum rate (33% at the date of this PDS). If you do not provide us with your resident withholding

tax rate, you will automatically have resident withholding tax deducted at the maximum rate (33% at

the date of this PDS), unless you are a company, in which case it will be deducted at 28%.

If you have queries relating to the tax consequences of your investment then you should seek

independent financial and tax advice which is specific to your circumstances before deciding to

invest.

Section 8 Who is involved?

Who is involved?

Name Role

Issuer New Zealand Baptist Savings and Development Society Inc.

Issuer of the call and term deposits.

Supervisor Covenant Trustee Services Limited

Provides independent oversight of us in relation to the call and term deposits.

Guarantors BSDS Strategic Trust and Baptist Savings Capital Limited

Guarantee Baptist Savings’ obligations under the call and term deposits.

Solicitor to the issuer Minter Ellison Rudd Watts Lawyers

Legal adviser to the issuer.

Section 9 How to complain

We endeavour to maintain a very good relationship with all of our investors. If you are unhappy with the service you receive from us, please contact our General Manager, John Smeaton: General Manager 477 Great South Road Penrose Auckland 1642 Telephone: 0800 SAVINGS (0800 728 4647) Email: [email protected]. If after talking to the General Manager you are not satisfied, you have the right to ask him to refer the matter to the Chairman, Graham Shaw, who can be contacted at the address and phone number set out above. Complaints may also be made to Covenant Trustee Services Limited at: Covenant Trustee Services Limited Level 18, 48 Emily Place Auckland 1010

28

Telephone: (09) 302 0638 Baptist Savings is a member of a dispute resolution scheme, Financial Services Complaints Limited (FSCL). If Baptist Savings cannot agree on how to resolve your issue, you can refer the matter to FSCL: Financial Services Complaints Limited Level 12, 45 Johnston Street Wellington Telephone: 0800 347 257 Email: [email protected] Financial Services Complaints Limited will not charge you a fee for investigating or resolving a complaint. Complaints can also be made to the Financial Markets Authority through its website www.fma.govt.nz.

Section 10 Where you can find more information

Further information regarding Baptist Savings and the call and term deposits is available on the offer

register at www.business.govt.nz/disclose and can be obtained by request from the Registrar of

Financial Service Providers.

Section 11 How to apply

To apply for the call or term deposits, you need to complete an application form and submit it to us.

An application form is attached to this PDS and an online version can be found at

www.baptistsavings.co.nz.

Section 12 Contact information

Baptist Savings

477 Great South Road

Penrose

Auckland 1642

P O Box 12738

Toll free phone 0508 7245 464 (SAVINGS)

www.baptistsavings.co.nz

Deposit Application Form

Surname/Church/Organisation/Trust

Mr Mrs Miss Ms First Names/Trustees/Authorised Officers

Postal address and post code

/ /

Date of birth (Optional)

Telephone (home) (business) (mobile)

Email (tick if happy to receive communication by email) Church (optional)

DEPOSIT DETAILS (please tick) SAVINGS ACCOUNTS – DIRECT CREDIT DETAIL

Amount to be invested $ …………………………………. Regular amount to be saved $ …………. Regular Savings Call Account Other Term (term / maturity date)

Fixed Investment

30 days 3 months 6 months

9 months 1 year 18 months

2 years 3 years 5 years

Direct Credit must be made to NZ Baptist Savings & Development Society Inc. at BNZ, Dominion Road. Account number 02 0264 0225481 000 with payee particulars

MATURITY INSTRUCTIONS INTEREST INSTRUCTIONS

(Baptist Savings will contact investors prior to maturity of all term investments)

Add interest to principal

Pay by cheque

Direct credit bank account

I wish to forgo interest

Reinvest principal Repay principal I wish to accept a lower rate of interest …….. % pa (state)

Investor’s bank account details: (new investors please provide copy of bank deposit slip)

Investor’s IRD number: For joint account (second IRD number required):

Please state which Resident Withholding Tax rate applies:

10.5% 17.5% 30% 33% 28% (Company default rate) Exempt (IRD certificate required)

NEW INVESTOR IDENTIFICATION

Under the Anti-Money Laundering and Countering Financing of Terrorism Act 2009, Baptist Savings is required to verify your identity and

address.

Personal Investors

We require certified copies of the following documents:

1. To verify your identity:

A. a certified copy of your Passport; or alternatively

B. certified copies of both your Driver’s License and Birth Certificate.

2. To verify your address:

A. a copy of your bank statement; or alternatively

B. a copy of an invoice from a utility company, addressed to you at your current residential address.

All photocopies to be certified as a “certified correct copy of original” by a Justice of the Peace, Solicitor, Chartered Accountant or your

pastor. Any person certifying a document must not be related to you, your spouse or partner, a person who lives at your address, or a

fellow trustee.

Churches, trusts, and other unincorporated bodies

All trustees and/or senior officers must provide identity and address verification as specified for personal investors above

Corporate entities

All directors and/or senior officers* must provide identity and address verification as specified for personal investors above

YOUR PRIVACY

Personal information gathered on this form will be held securely by Baptist Savings. The information will be used to administer your

investments with us and to offer other investment opportunities with us. Certain information will be released to Inland Revenue to comply

with tax requirements. You have the right to access your personal information that we hold at any time and to correct it.

DECLARATION

I/We have read and understood the PDS dated 30 April 2015 and agree to be bound by the terms of the trust deed (including any

amendments to it). I/We agree to the terms outlined above in relation to document certification and the Privacy Act 1993 and the use of

personal information. I/We hereby declare that all information I/We have submitted in this application form is true and correct.

SIGNED …………………………………………………………………………………………………………………………

P O Box 12738, Penrose, Auckland 1642 Phone (09) 582 0037 Ι Fax (09) 525 1170 Freephone (0508) 728 464 (SAVINGS) Email [email protected] Website www.baptistsavings.co.nz

NZ BAPTIST SAVINGS & DEVELOPMENT SOCIETY INC.