product disclosure statement · product disclosure statement for the offer of fully paid ordinary...

TRANSCRIPT

PRODUCT DISCLOSURE STATEMENT

For the offer of fully paid ordinary units in the Evans & Partners Australian Flagship Fund

ARSN 625 303 068 to raise up to $100,000,000 with the ability to raise an additional

$100,000,000 through oversubscriptions. This offer is not underwritten.

RESPONSIBLE E NT I T Y:

(AC N 152 367 649) (A F S L 410 433)

IN V ES TM E NT MANAG E R:

E VA N S A N D PA RT N ER S IN V E S T M EN T M A N AG EM EN T P T Y L IM I T ED

(AC N 619 080 045) (C A R 1255 264)

CONTENTS

IMPORTANT INFORMATION .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

LETTER OF INTRODUCTION .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

INVESTMENT OVERVIEW AND KEY DATES .... . . . . . . . . . . . . . . . . . . . . . . . . . . 8

KEY DATES.... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

ABOUT THE OFFER .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

ABOUT THE FUND .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

1. KEY BENEFITS AND RISKS .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2. FUND OVERVIEW .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

3. FUND OFFER .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

4. PORTFOLIO INVESTMENT PROCESS .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

5. SECTOR OVERVIEW .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

6. RISKS .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

7. FEES AND COSTS .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

8. FINANCIAL INFORMATION .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

9. INVESTIGATING ACOUNTANTS REPORT .... . . . . . . . . . . . . . . . . . . . . . . . . 45

10. TAX INFORMATION .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

11. KEY PEOPLE .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

12. ADDITIONAL INFORMATION .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

13. GLOSSARY .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

14. DIRECTORY .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

15. HOW TO INVEST .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

SUPPLEMENTARY PRODUCT DISCLOSURE STATEMENT .... . . . . . . .

APPLICATION FORM..... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

IMPORTANT INFORMATION

This Product Disclosure Statement (PDS) dated 13 April 2018 is an invitation to acquire ordinary units (Units) in the Evans & Partners Australian Flagship Fund (Fund) (ARSN 625 303 068).

This PDS was prepared and issued by Walsh & Company Investments Limited (ACN 152 367 649) (referred to in this PDS as “Walsh & Company”, “we”, “our” and “us”) in its capacity as the responsible entity (Responsible Entity) of the Fund.This document is important and requires your immediate attention. This PDS contains general financial and other information. It has not been prepared having regard to your investment objectives, financial situation or specific needs. It is important that you carefully read this PDS in its entirety before deciding to invest in the Fund and, in particular, in considering the PDS, that you consider the risk factors that could affect the financial performance of the Fund and your investment in the Fund. You should carefully consider these factors in light of your personal circumstances (including financial and taxation issues) and seek professional advice from your accountant, stockbroker, lawyer or other professional advisor before deciding whether to invest.

No person is authorised to give any information or make any representation in connection with the Offer which is not contained in this PDS. Any information or representation not so contained or taken to be contained may not be relied on as having been authorised by us in connection with the Offer.

Information relating to the Fund may change from time to time. Where changes are not materially adverse, information may be updated and made available to you on our website at www.australianf lagshipfund.com.au. A paper copy of any updated information is available free on request.

A SX LISTINGApplication will be made to ASX within seven days after the date of this PDS for the Fund to be listed on the ASX and for quotation of the Units issued pursuant to this PDS.

The fact that ASX may list the Fund is not to be taken as an indication of the merits of the Fund or the Units. ASX quotation, if granted, will commence as soon as practicable after holding statements are despatched.

The Responsible Entity does not intend to allot any Units unless and until ASX grants permission for the Units to be listed for quotation unconditionally or on terms acceptable to the Responsible Entity. If permission is not granted for the Units to be listed for quotation before the end of three months after the date of this PDS or such longer period permitted by the Corporations Act with the consent of ASIC, all Application Monies received pursuant to the PDS will be refunded without interest to Applicants in full within the time prescribed by the Corporations Act.

Neither ASIC nor ASX takes any responsibility for the contents of this PDS or the merits of the investment to which this PDS relates.

4

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

EXPOSURE PERIODThe Corporations Act prohibits the processing of applications to subscribe for Units in the Fund under this PDS (Applications) in the seven-day period after the lodgement of this PDS (Exposure Period). The Exposure Period may be extended by ASIC for up to a further seven days. The Exposure Period allows this PDS to be examined by potential investors prior to the raising of funds. The examination may result in the identification of deficiencies in this PDS, in which case any Application may need to be dealt with in accordance with the Corporations Act. Applications received during the Exposure Period will not be processed until after the expiry of the Exposure Period. No preference will be given to Applications received during the Exposure Period.

DATE OF INFORMATIONUnless otherwise stated, information in this PDS is current as at the date of this PDS.

CURRENC Y AND ROUNDING Unless otherwise indicated, references to $ are references to the lawful currency of Australia.

Any discrepancies between totals and the sum of all the individual components in the tables contained in this PDS are due to rounding.

NO GUAR ANTEENeither we nor our respective subsidiaries nor any other party makes any representation or gives any guarantee or assurance as to the performance or success of the Fund, the rate of income or capital return from the Fund, the repayment of the investment in the Fund or that there will be no capital loss or particular taxation consequence of investing in the Fund. An investment in the Fund is subject to investment risks. These risks are discussed in Section 6.

RESTRICTIONS ON THE DISTRIBUTION OF THIS PDSThis PDS does not constitute an offer of Units in any place in which, or to any person to whom, it would not be lawful to do so. The distribution of this PDS in jurisdictions outside Australia may be restricted by law and any person into whose possession this PDS comes (including nominees, or custodians) should seek advice on and observe those restrictions.

The Offer to which this PDS relates is available to persons receiving this PDS (electronically or otherwise) in Australia. It is not available to persons receiving it in any other jurisdiction.

This document is not an offer or an invitation to acquire securities in any country other than Australia. In particular, this document does not constitute an offer to sell, or the solicitation of an offer to buy, any securities in the United States of America (US) or to, or for the account or benefit of, any “US person”, as defined in Regulation S under the US Securities Act of 1933 (Securities Act) (US Person).

This document may not be released or distributed in the US or to any US Person. Any securities described in this PDS have not been, and will not be, registered under the Securities Act or the securities laws of any state or other jurisdiction of the US, and may not be offered or sold in the US, or to, or for the account or benefit of, any US Person, except in a transaction exempt from, or not subject to, the registration requirements under the Securities Act.

ELECTRONIC PDSAn electronic version of this PDS (including the Application Form once the Offer is open) is available from the Fund’s website at www.australianf lagshipfund.com.au.

5

COPY OF THIS PDSThe Responsible Entity will provide you with a copy of the PDS free of charge if you request one during the Offer period, within five days after receiving such a request.

FORWARD LOOKING STATEMENTSThis PDS may contain forward looking statements which are subject to known and unknown risks, uncertainties and other important factors that could cause the actual results, events, performance or achievements of the Fund to be materially different from those expressed or implied in such statements. Past performance is not a reliable indicator of future performance.

ENQUIRIESApplicants with enquiries concerning the Application Form or relating to this PDS and the Offer should contact us on 1300 454 801, or via email at [email protected].

Other than as permitted by law, applications for Units in the Fund will only be accepted following receipt of a properly completed Application Form.

GLOSSARY OF TERMSDefined terms and abbreviations included in the text of this PDS are set out in the Glossary in Section 13.

PHOTOGR APHS AND DI AGR AMSPhotographs, diagrams and artists’ renderings contained in this PDS that do not have accompanying descriptions are intended for illustrative purposes only. They should not be interpreted as an endorsement of this PDS or its contents by any person shown in these images nor an indication of the investments that may be made by the Fund.

6

LET TER OF INTRODUCTION

Dear Investor,It is my pleasure to invite you to become an investor in the Evans & Partners Australian Flagship Fund (Fund).The Fund will offer investors exposure to a concentrated portfolio of Australian equities. The portfolio will comprise investments in 20 to 40 of Australia’s most attractive publicly-listed companies as assessed by us, that have been carefully selected to deliver sustainable earnings growth and returns on capital.We will target annual cash distributions of 5% (Target Distribution) and will operate a distribution reinvestment plan that will allow investors to reinvest up to the Target Distribution in additional Units in the Fund at a 5% discount to the NAV. At its discretion, the full cost of the discount will be paid for by the Responsible Entity in its personal capacity.Guiding the investment decisions of the Fund will be a well-credentialed and experienced Investment Committee. I will chair this committee, and joining me are members of Evans Dixon, as well as highly experienced industry professionals and board directors, Margaret Jackson, former Chairman of Qantas, Flexigroup, and Spotless Group, David Crawford, Chairman of Lend Lease and South32, and Kevin McCann, former Chairman of Macquarie Group.We are also fortunate to have secured Ben Chan and Adam Alexander as the Portfolio Consultants to the Investment Committee. Ben has been rated in the top three analysts in Australia including multiple number one rankings in the building materials and steel sector over a number of years. Adam has been recognised as a leading stock picker in retailing and consumer goods and the hotels, restaurants, and leisure industries and consistently rated as a top three analyst with institutional fund managers.The selection of stocks for the Fund’s portfolio will ref lect the key characteristics of Evans and Partners’ approach to equity markets and the key investment themes identified by the Investment Committee and Portfolio Consultants. The Fund will target businesses we believe are undervalued and that have quality management and strong corporate governance standards, sound business models with a sustainable competitive advantage, solid financial positions, and sufficient growth to generate attractive returns. We are high conviction asset managers, and the portfolio will be overweight sectors and companies that the Investment Manager believes offer greater potential for higher risk-adjusted returns. At the same time, we understand that minimising the risk of capital loss is essential. Our approach is conservative and measured, and we will actively manage the risk profile of the Fund and invest in a portfolio of stocks that we believe will provide Unitholders with an appropriate level of down side protection while positioning for upside gain.We are launching the Fund in what we believe is a strong period of opportunity for the Australian market. As the pace of change in the global economy accelerates, exciting opportunities for Australian businesses continue to emerge. At the same time, change will also bring challenges for many Australian companies. We believe that the skills and experience of the Fund’s Investment Committee and Portfolio Consultants position the Fund to successfully navigate these opportunities and challenges.Please read this PDS carefully and consider the benefits and risks of the opportunity that is offered by the Evans & Partners Australian Flagship Fund. I look forward to welcoming you as an investor in the Fund.Yours sincerely,

DAV ID E VANS Chairman, Investment Committee

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

7

INVESTMENT OVERVIEW AND KEY DATES

KEY DATES

Date of PDS 13 April 2018

Offer Opening Date 27 April 2018

Offer Closing Date* 25 May 2018

Issue Date* 1 June 2018

Trading expected to commence on the ASX* 6 June 2018

* The above dates are indicative only and may vary, subject to the requirements of the Corporations Act and the ASX Listing Rules. The Responsible Entity may vary the dates and times of the Offer (including closing the Offer early) without notice.

ABOUT THE OFFERKEY OFFER DETAILS SUMMARY

MORE INFORMATION

Issuer The PDS and the Units are issued by Walsh & Company, the Responsible Entity.

Sections 11.6, 11.7 and 11.8

Offer The Offer comprises an offer of up to 62.5 million Units at a price per Unit of $1.60 to raise $100 million, with the ability to raise an additional $100 million through oversubscriptions.

Section 3

Purpose of the Offer

The Fund will use the net proceeds of the Offer to invest in a portfolio of ASX listed securities as determined by Evans and Partners Investment Management Pty Limited (Investment Manager). The Investment Committee will make recommendations to the Investment Manager in accordance with the investment strategy of the Fund.

Section 2.1

Application Price $1.60 per Unit. Section 3

Minimum Subscription

A minimum subscription of $50 million (31.25 million Units) must be raised by the Offer Closing Date.

If the Offer is unsuccessful, all Application Monies will be refunded, without interest.

Section 3.1

Minimum Application per Investor

The minimum Application amount per Investor is $2,000 (1,250 Units).

Section 15.1

Pro forma Net Asset Value (NAV) per Unit

$1.55 Section 8.2

Applicants The Offer is open to Applicants with a permanent address in Australia.

Section 3

Superannuation funds

Superannuation funds may invest subject to the investment mandate of the particular fund and the trustee’s general powers and duties.

Underwriting The Offer is not underwritten.

Costs of the Offer The Responsible Entity charges Structuring and Handling Fees for the Offer. There are also ongoing fees.

Section 7

8

ABOUT THE FUNDKEY FUND FEATURES SUMMARY

MORE INFORMATION

Fund Type The Fund is a unit trust which has been registered as a managed investment scheme under the Corporations Act and will apply to be listed on the ASX as an investment entity.

Section 2.2

Responsible Entity Walsh & Company is the Responsible Entity of the Fund. Section 11.6

Term of the Fund The Fund does not have a fixed investment term and is designed for the long-term investor.

Section 2.1

Investment Manager

Evans and Partners Investment Management Pty Limited is the investment manager for the Fund. The Investment Manager has been appointed for a term of 10 years (subject to a waiver from the ASX) and is responsible for investment decisions for the Fund. The Investment Manager and the Responsible Entity are both subsidiaries of the Evans Dixon Group.

Sections 2.2, 11.4 and 12.1

Investment Committee

The Investment Committee is comprised of a highly experienced group of industry professionals, including: David Evans, Executive Chairman of Evans Dixon; Margaret Jackson, former Chairman of Qantas, Flexigroup, and Spotless Group; Alan Dixon, Managing Director and CEO of Evans Dixon; David Crawford, AO, former Australian National Chairman of KPMG and current Chairman of Lendlease; Kevin McCann, former Chairman of Macquarie Group Limited and Macquarie Bank Limited and Origin Energy Limited and Chairman of Citadel Group Limited; and Ted Alexander, Head of Investments at Walsh & Company.

The Investment Committee has deep expertise and experience in a wide range of Australian businesses and will draw on this when evaluating investments.

The Investment Committee will recommend suitable investments to the Investment Manager, which is responsible for approval, trade execution, and portfolio management.

The Responsible Entity believes that a key investment benefit is that the Investment Manager will be able to draw upon the knowledge, experience and insights of the members of the Investment Committee.

Sections 2.2 and

11.1

Portfolio Consultants

Ben Chan and Adam Alexander have been assigned the role of Portfolio Consultants to the Investment Committee.

Ben has been rated in the top three analysts in Australia including multiple number one rankings in the building materials and steel sector over a number of years.

Adam has been recognised as a leading stock picker in retailing and consumer goods and the hotels, restaurants and leisure industries and consistently rated as a top three analyst with institutional fund managers.

The Portfolio Consultants will complete due diligence on potential investment opportunities and analysis against key criteria.

Sections 2.2 and 11.3

Investment objective

To provide investors with capital growth, attractive risk-adjusted returns and stable distributions over the medium to long-term through exposure to quality ASX listed securities.

Section 2.1

9

KEY FUND FEATURES SUMMARY

MORE INFORMATION

Investment strategy

The Investment Manager will target a concentrated portfolio of ASX listed securities, utilising the Investment Committee and Portfolio Consultants expertise and bottom-up, fundamental analysis with a strong quality overlay. Securities will be evaluated using the following criteria:

» strong industry thematic;

» a sustainable competitive advantage;

» attractive risk-adjusted returns;

» growing dividends;

» quality board and management; and

» attractive valuation.

Sections 2.1 and 2.2

Investment Process

The investment process is conducted by the Investment Manager who consults with the Investment Committee and Portfolio Consultants to assist with investment decisions. The Investment Committee and Portfolio Consultants, through their deep industry expertise and experience and the broad resources of Evans Dixon, will seek to identify key investment themes and source high conviction ideas for investments.

Section 4

Distribution policy The Responsible Entity intends to target a cash distribution of 5% per annum (based on the NAV at or around the beginning of the relevant distribution period) paid semi-annually (Target Distribution).

The Responsible Entity expects that the Target Distribution will provide Unitholders with greater certainty on the amount of upcoming distributions, however there is no guarantee this target will be achieved. To the extent the Target Distribution cannot be met from income of the Fund, distributions may include a capital component.

Section 2.5

10

KEY FUND FEATURES SUMMARY

MORE INFORMATION

Distribution reinvestment plan (DRP)

The Responsible Entity has established a DRP in respect of distributions.

Under the DRP, where Unitholders elect to reinvest up to the Target Distribution in additional Units in the Fund, the Responsible Entity intends to offer Unitholders an issue price which is set at a 5% discount to the NAV. At its discretion, the full cost of the discount will be paid for by the Responsible Entity, in its personal capacity, which may be effected through a partial waiver of fees. Where the Responsible Entity exercises this discretion, there will be no dilutive effect of value as a result of the DRP discount for Unitholders who elect not to participate in the DRP.

For any amount of distribution greater than the Target Distribution, the Responsible Entity may require that this amount be reinvested, for which there will be no discount on the Unit price. Unitholders will need to include all income distribution in their tax return, even if reinvested.

Section 2.6

Fund borrowings (gearing)

The Responsible Entity does not currently intend to gear the Fund.

Section 2.4

Derivative policy The Responsible Entity does not presently intend to invest in or use Derivatives.

Section 2.7

Ongoing Fees and Costs

The Responsible Entity and Investment Manager charge ongoing fees to manage the Fund.

The Investment Manager may also be entitled to a performance fee, payable by the Fund. Performance fees are calculated with reference to the higher of the S&P/ASX200 Accumulation Index (Index Return Hurdle) and the RBA Cash Rate (Absolute Return Hurdle) and are subject to a High Water Mark requirement (which can be reset in certain circumstances) and an overall cap.

The Responsible Entity has agreed to bear the cost of all out-of-pocket expenses (excluding transactional and operational costs) it incurs in connection with the investment and management of the Fund.

Section 7

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

11

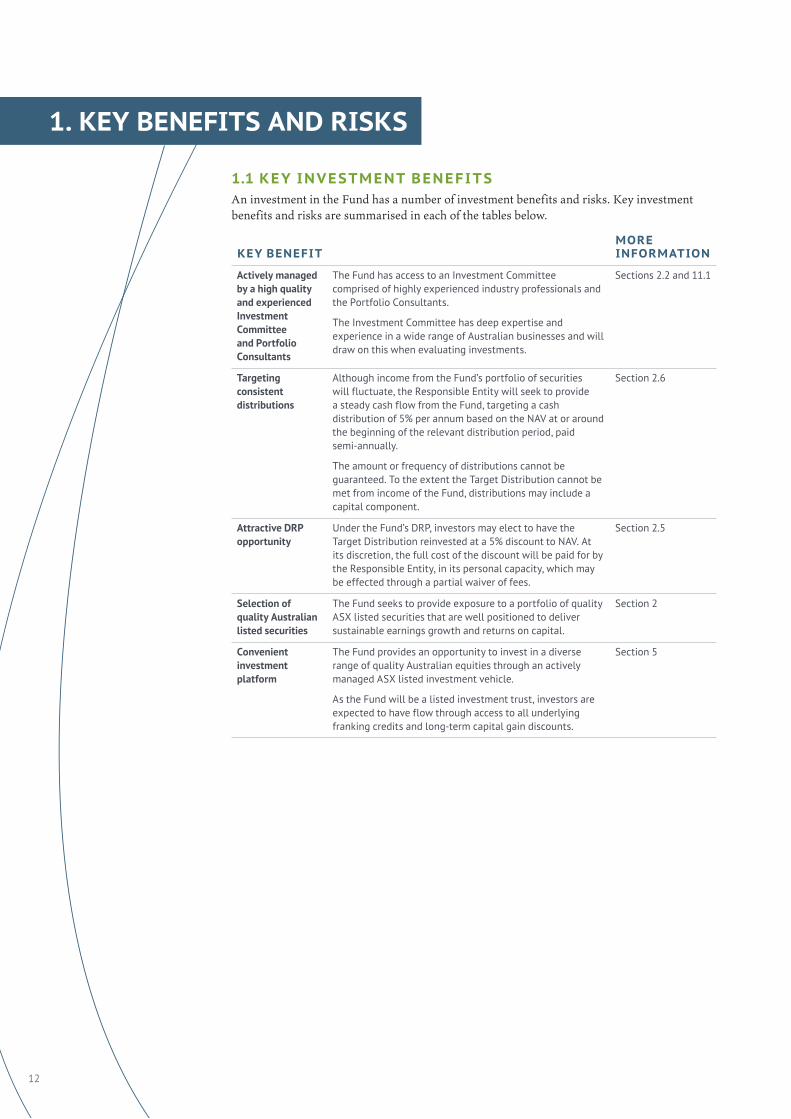

1.1 KEY INVESTMENT BENEFITSAn investment in the Fund has a number of investment benefits and risks. Key investment benefits and risks are summarised in each of the tables below.

KEY BENEFITMORE INFORMATION

Actively managed by a high quality and experienced Investment Committee and Portfolio Consultants

The Fund has access to an Investment Committee comprised of highly experienced industry professionals and the Portfolio Consultants.

The Investment Committee has deep expertise and experience in a wide range of Australian businesses and will draw on this when evaluating investments.

Sections 2.2 and 11.1

Targeting consistent distributions

Although income from the Fund’s portfolio of securities will fluctuate, the Responsible Entity will seek to provide a steady cash flow from the Fund, targeting a cash distribution of 5% per annum based on the NAV at or around the beginning of the relevant distribution period, paid semi-annually.

The amount or frequency of distributions cannot be guaranteed. To the extent the Target Distribution cannot be met from income of the Fund, distributions may include a capital component.

Section 2.6

Attractive DRP opportunity

Under the Fund’s DRP, investors may elect to have the Target Distribution reinvested at a 5% discount to NAV. At its discretion, the full cost of the discount will be paid for by the Responsible Entity, in its personal capacity, which may be effected through a partial waiver of fees.

Section 2.5

Selection of quality Australian listed securities

The Fund seeks to provide exposure to a portfolio of quality ASX listed securities that are well positioned to deliver sustainable earnings growth and returns on capital.

Section 2

Convenient investment platform

The Fund provides an opportunity to invest in a diverse range of quality Australian equities through an actively managed ASX listed investment vehicle.

As the Fund will be a listed investment trust, investors are expected to have flow through access to all underlying franking credits and long-term capital gain discounts.

Section 5

1. KEY BENEFITS AND RISKS

12

1.2 KEY INVESTMENT RISKSAs with most investments, the future performance of the Fund can be inf luenced by a number of factors that are outside the control of the Responsible Entity. The key risks are discussed in Section 6 and include:

KEY RISKMORE INFORMATION

Investment selection and strategy risk

The Fund’s performance depends on the investment decisions made. The Investment Manager may make investment decisions that result in low returns or loss of capital invested.

Section 6.1(a)

Equity risk There is a risk that the market price of securities will fall over short or extended periods of time. Unitholders in the Fund are exposed to this risk both through the underlying investments in which the Fund will invest and through general market fluctuations in the price of their Units.

Section 6.1(b)

Company specific risk

Investments by the Fund in a company’s securities will be subject to many of the risks to which that particular company is itself exposed. These risks may impact the value of the securities of that company, and may include factors such as changes in management, actions of competitors and regulators, changes in technology and market trends.

Section 6.1(c)

Concentration risk Funds that invest in a relatively small number of securities issuers are more susceptible to risks associated with any one issued security, from a single economic, political, or regulatory occurrence than more diversified funds might be.

Section 6.1(d)

Experience of the Investment Manager Risk

The Investment Manager was recently incorporated and has limited performance history.

The Investment Manager will draw upon input from the Investment Committee and the Portfolio Consultants who have extensive experience in the identification, acquisition, management, and disposal of a diverse range of asset classes.

Section 6.1(e)

Key personnel risk

There is a risk of departure of key staff or consultants with particular expertise in the sector, whether they are the staff or Directors of the Responsible Entity, the Investment Manager, members of the Investment Committee, the Portfolio Consultants or independent advisors or consultants. These departures may have an adverse impact on the earnings and value of the Fund.

Section 6.1(f)

13

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

13

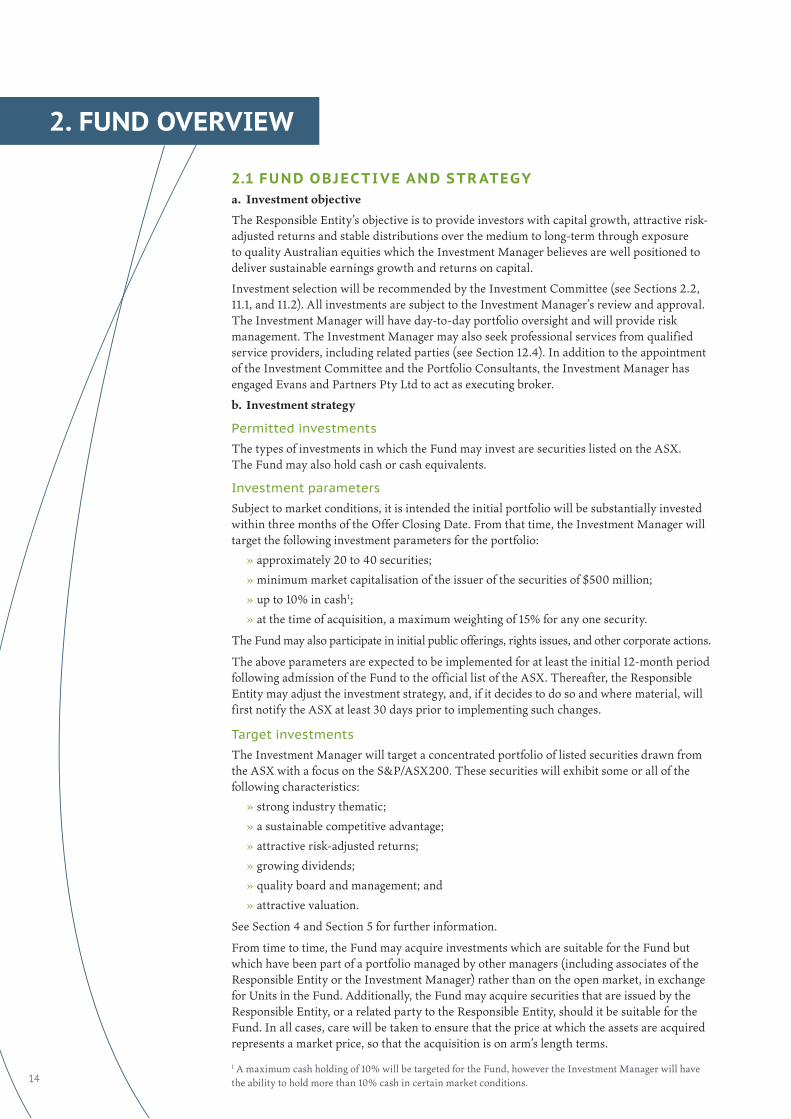

2.1 FUND OBJECTI VE AND STR ATEGYa. Investment objective

The Responsible Entity’s objective is to provide investors with capital growth, attractive risk-adjusted returns and stable distributions over the medium to long-term through exposure to quality Australian equities which the Investment Manager believes are well positioned to deliver sustainable earnings growth and returns on capital.

Investment selection will be recommended by the Investment Committee (see Sections 2.2, 11.1, and 11.2). All investments are subject to the Investment Manager’s review and approval. The Investment Manager will have day-to-day portfolio oversight and will provide risk management. The Investment Manager may also seek professional services from qualified service providers, including related parties (see Section 12.4). In addition to the appointment of the Investment Committee and the Portfolio Consultants, the Investment Manager has engaged Evans and Partners Pty Ltd to act as executing broker.

b. Investment strategy

Permitted investments

The types of investments in which the Fund may invest are securities listed on the ASX. The Fund may also hold cash or cash equivalents.

Investment parameters

Subject to market conditions, it is intended the initial portfolio will be substantially invested within three months of the Offer Closing Date. From that time, the Investment Manager will target the following investment parameters for the portfolio:

» approximately 20 to 40 securities; » minimum market capitalisation of the issuer of the securities of $500 million; » up to 10% in cash1; » at the time of acquisition, a maximum weighting of 15% for any one security.

The Fund may also participate in initial public offerings, rights issues, and other corporate actions.

The above parameters are expected to be implemented for at least the initial 12-month period following admission of the Fund to the official list of the ASX. Thereafter, the Responsible Entity may adjust the investment strategy, and, if it decides to do so and where material, will first notify the ASX at least 30 days prior to implementing such changes.

Target investments

The Investment Manager will target a concentrated portfolio of listed securities drawn from the ASX with a focus on the S&P/ASX200. These securities will exhibit some or all of the following characteristics:

» strong industry thematic; » a sustainable competitive advantage; » attractive risk-adjusted returns; » growing dividends; » quality board and management; and » attractive valuation.

See Section 4 and Section 5 for further information.

From time to time, the Fund may acquire investments which are suitable for the Fund but which have been part of a portfolio managed by other managers (including associates of the Responsible Entity or the Investment Manager) rather than on the open market, in exchange for Units in the Fund. Additionally, the Fund may acquire securities that are issued by the Responsible Entity, or a related party to the Responsible Entity, should it be suitable for the Fund. In all cases, care will be taken to ensure that the price at which the assets are acquired represents a market price, so that the acquisition is on arm’s length terms.

2. FUND OVERVIEW

1 A maximum cash holding of 10% will be targeted for the Fund, however the Investment Manager will have the ability to hold more than 10% cash in certain market conditions.14

2.2 FUND STRUCTURE AND MANAGEMENT ARR ANGEMENTS The Fund is registered with ASIC as a managed investment scheme, and an application will be made for it to be listed on the ASX (expected code “EFF”) as an investment entity. Unitholders will hold Units in the Fund and receive the benefit of income and capital gains generated by the Fund’s underlying investments.

Figure 1 below sets out the ownership structure and management arrangements for the Fund.

FIGURE 1: EVANS & PARTNERS AUSTRALIAN FLAGSHIP FUND STRUCTURE

INVESTORS

Responsible Entity

Investment Manager

Units

INVESTMENTS

WALSH & COMPANYINVESTMENTS LIMITED

EVANS & PARTNERS Australian Flagship Fund

INVESTMENT COMMITTEE& PORTFOLIO CONSULTANTS

EVANS & PARTNERS INVESTMENT MANAGEMENT

PTY LIMITED

Investment Manager

As Investment Manager for the Fund, Evans and Partners Investment Management Pty Limited has appointed an Investment Committee who, in conjunction with the Portfolio Consultants, will generate investment ideas, undertake due diligence, monitor industry developments, and make portfolio management recommendations to the Investment Manager.

All investments are subject to the Investment Manager’s review and approval. The Investment Manager will have day-to-day portfolio oversight and will provide risk management. The Investment Manager may also seek professional services from qualified service providers, including related parties (see Section 12.4). In addition to the appointment of the Investment Committee and the Portfolio Consultants, the Investment Manager has engaged Evans and Partners Pty Ltd to act as executing broker.

Investment Committee and Portfolio Consultants

The Investment Committee is an advisory body of highly experienced corporate executives appointed by the Investment Manager. The Investment Manager’s decisions to act or not act on the recommendations of the Investment Committee are solely the responsibility of the Investment Manager.

The Investment Committee will provide recommendations to the Investment Manager, in respect of investment decisions and portfolio construction. The primary role of the Investment Committee is to:

» identify investment themes and opportunities;

» review information and carry out research and analysis with respect to potential and existing investments; and

» provide recommendations to the Investment Manager regarding the allocation of the Fund’s capital.

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

15

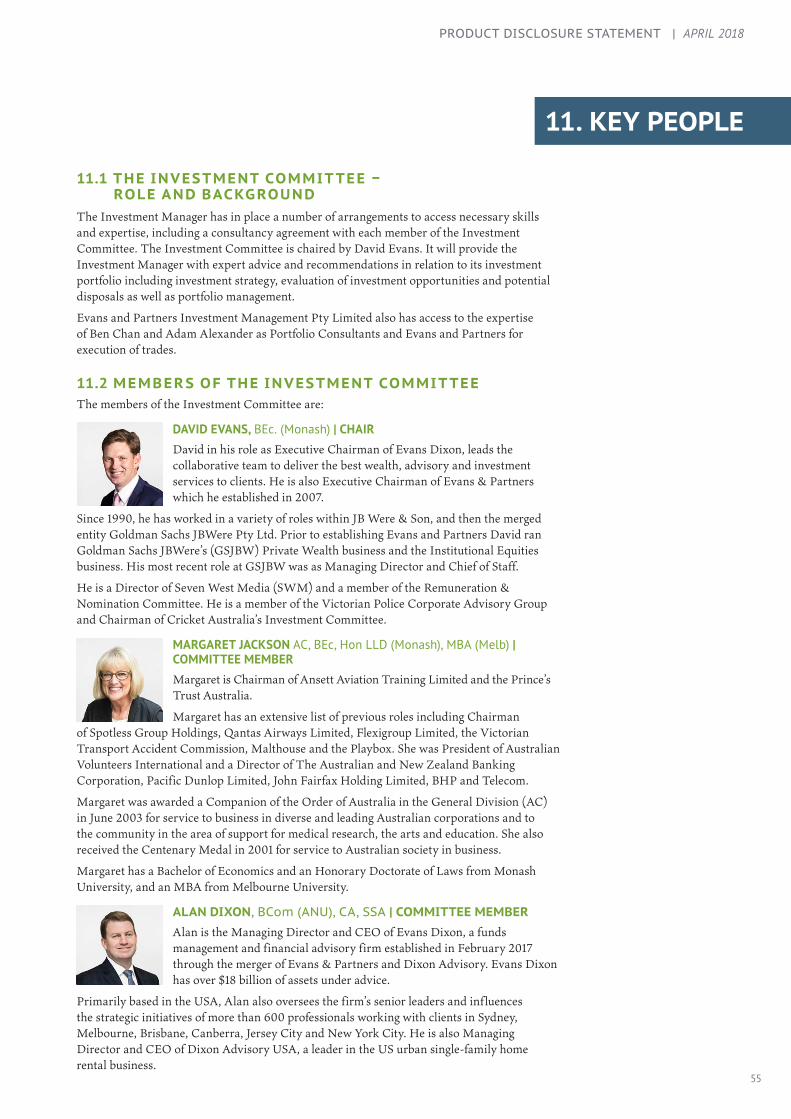

DAVID EVANS, BEc. (Monash)

CHAIR

» Executive Chairman of Evans Dixon Limited

» Director of Seven West Media and Chairman of Cricket Australia’s Investment Committee

» Previously Managing Director and Chief of Staff at Goldman Sachs JB Were

ALAN DIXON, BCom (ANU), CA, SSA

COMMITTEE MEMBER

» Managing Director and CEO of Evans Dixon Limited, inclusive of Dixon Advisory USA

» Director of New Energy Solar, an ASX listed infrastructure company focussed on solar power generating assets

» Previously Chartered Accountancy and Investment Banking roles in Australia

DAVID CRAWFORD AO, BCom, BLaw (Melb)

COMMITTEE MEMBER

» Chairman of Lendlease Corporation

» Chairman of South32

» Chairman of Australia Pacific Airports Corporation Limited

» Former Australian National Chairman of KPMG

TED ALEXANDER, BEc. (1st Hons) (UTAS), M.Phil Economics (Oxford)

COMMITTEE MEMBER

» Head of Investments, Walsh & Company Asset Management

» Former Head of Healthcare and Portfolio Manager at Magellan Financial Group and Former Head of Alternative Investments at Neptune Investment Management Limited

MARGARET JACKSON AC, BEc, Hon LLD (Monash), MBA (Melb)

COMMITTEE MEMBER

» Chairman of Ansett Aviation Training Limited and the Prince’s Trust Australia.

» Former Chairman of QANTAS Airways Limited, Flexigroup, Spotless Group and former director of the Australia and New Zealand Banking Group and BHP.

KEVIN MCCANN AM, BA, LLB (Hons)(Syd).

COMMITTEE MEMBER

» Chairman of Citadel Group Limited, Telix Pharmaceuticals Limited, The Sydney Harbour Federation Trust and the Menzies Research Centre

» Former Chairman of Macquarie Group Limited and Macquarie Bank Limited, Origin Energy Limited, Healthscope Limited and ING Management Limited

BEN CHAN, BCE, Bcom (Melb), CFA

PORTFOLIO CONSULTANT

» Portfolio Manager, Evans and Partners

» Former primary analyst at Merrill Lynch

» Consistently rated in the top three analysts in Australia including multiple number one rankings in the building materials and steel sector

ADAM ALEXANDER, BCom (Melb)

PORTFOLIO CONSULTANT

» Portfolio Manager, Evans and Partners

» Former Head of Consumer, Retail and Entertainment Research at Goldman Sachs

» Consistently rated as a top three analyst with Institutional Fund Managers

INVESTMENT COMMITTEE AND PORTFOLIO CONSULTANTS

See Section 11 for further information.

16

Responsible Entity

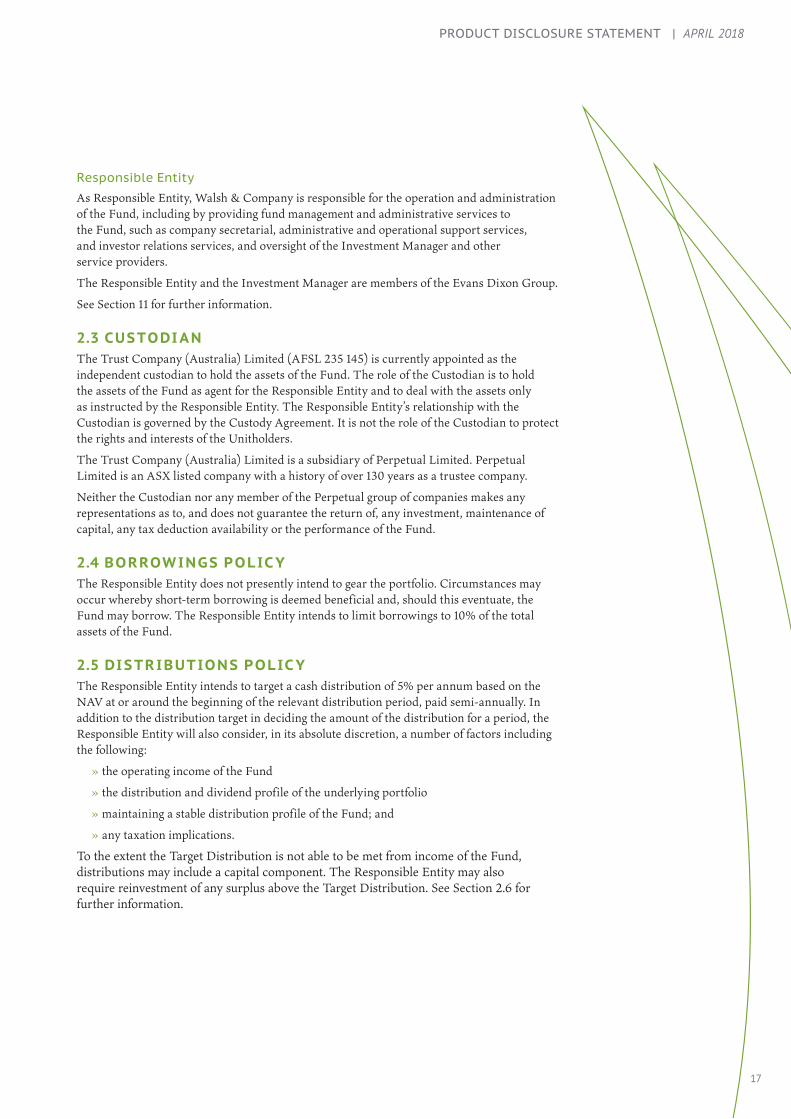

As Responsible Entity, Walsh & Company is responsible for the operation and administration of the Fund, including by providing fund management and administrative services to the Fund, such as company secretarial, administrative and operational support services, and investor relations services, and oversight of the Investment Manager and other service providers.

The Responsible Entity and the Investment Manager are members of the Evans Dixon Group.

See Section 11 for further information.

2.3 CUSTODI ANThe Trust Company (Australia) Limited (AFSL 235 145) is currently appointed as the independent custodian to hold the assets of the Fund. The role of the Custodian is to hold the assets of the Fund as agent for the Responsible Entity and to deal with the assets only as instructed by the Responsible Entity. The Responsible Entity’s relationship with the Custodian is governed by the Custody Agreement. It is not the role of the Custodian to protect the rights and interests of the Unitholders.

The Trust Company (Australia) Limited is a subsidiary of Perpetual Limited. Perpetual Limited is an ASX listed company with a history of over 130 years as a trustee company.

Neither the Custodian nor any member of the Perpetual group of companies makes any representations as to, and does not guarantee the return of, any investment, maintenance of capital, any tax deduction availability or the performance of the Fund.

2.4 BORROW INGS POLIC YThe Responsible Entity does not presently intend to gear the portfolio. Circumstances may occur whereby short-term borrowing is deemed beneficial and, should this eventuate, the Fund may borrow. The Responsible Entity intends to limit borrowings to 10% of the total assets of the Fund.

2.5 DISTRIBUTIONS POLIC YThe Responsible Entity intends to target a cash distribution of 5% per annum based on the NAV at or around the beginning of the relevant distribution period, paid semi-annually. In addition to the distribution target in deciding the amount of the distribution for a period, the Responsible Entity will also consider, in its absolute discretion, a number of factors including the following:

» the operating income of the Fund

» the distribution and dividend profile of the underlying portfolio

» maintaining a stable distribution profile of the Fund; and

» any taxation implications.

To the extent the Target Distribution is not able to be met from income of the Fund, distributions may include a capital component. The Responsible Entity may also require reinvestment of any surplus above the Target Distribution. See Section 2.6 for further information.

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

17

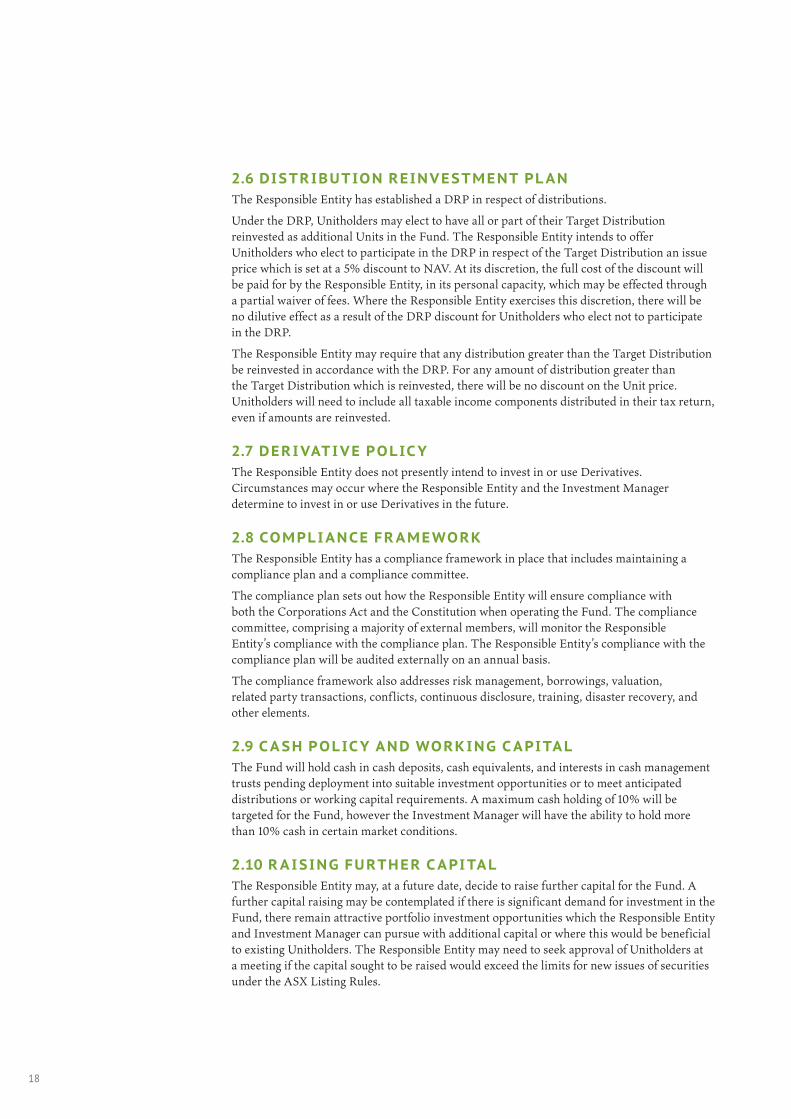

2.6 DISTRIBUTION REINVESTMENT PL ANThe Responsible Entity has established a DRP in respect of distributions.

Under the DRP, Unitholders may elect to have all or part of their Target Distribution reinvested as additional Units in the Fund. The Responsible Entity intends to offer Unitholders who elect to participate in the DRP in respect of the Target Distribution an issue price which is set at a 5% discount to NAV. At its discretion, the full cost of the discount will be paid for by the Responsible Entity, in its personal capacity, which may be effected through a partial waiver of fees. Where the Responsible Entity exercises this discretion, there will be no dilutive effect as a result of the DRP discount for Unitholders who elect not to participate in the DRP.

The Responsible Entity may require that any distribution greater than the Target Distribution be reinvested in accordance with the DRP. For any amount of distribution greater than the Target Distribution which is reinvested, there will be no discount on the Unit price. Unitholders will need to include all taxable income components distributed in their tax return, even if amounts are reinvested.

2.7 DERI VATI VE POLIC YThe Responsible Entity does not presently intend to invest in or use Derivatives. Circumstances may occur where the Responsible Entity and the Investment Manager determine to invest in or use Derivatives in the future.

2.8 COMPLI ANCE FR AMEWORK The Responsible Entity has a compliance framework in place that includes maintaining a compliance plan and a compliance committee.

The compliance plan sets out how the Responsible Entity will ensure compliance with both the Corporations Act and the Constitution when operating the Fund. The compliance committee, comprising a majority of external members, will monitor the Responsible Entity’s compliance with the compliance plan. The Responsible Entity’s compliance with the compliance plan will be audited externally on an annual basis.

The compliance framework also addresses risk management, borrowings, valuation, related party transactions, conf licts, continuous disclosure, training, disaster recovery, and other elements.

2.9 C A SH POLIC Y AND WORKING C APITALThe Fund will hold cash in cash deposits, cash equivalents, and interests in cash management trusts pending deployment into suitable investment opportunities or to meet anticipated distributions or working capital requirements. A maximum cash holding of 10% will be targeted for the Fund, however the Investment Manager will have the ability to hold more than 10% cash in certain market conditions.

2.10 R A ISING FURTHER C APITALThe Responsible Entity may, at a future date, decide to raise further capital for the Fund. A further capital raising may be contemplated if there is significant demand for investment in the Fund, there remain attractive portfolio investment opportunities which the Responsible Entity and Investment Manager can pursue with additional capital or where this would be beneficial to existing Unitholders. The Responsible Entity may need to seek approval of Unitholders at a meeting if the capital sought to be raised would exceed the limits for new issues of securities under the ASX Listing Rules.

18

2.11 C APITAL MANAGEMENT POLIC YSubject to any restrictions imposed under the Corporations Act, ASX Listing Rules, and the Fund’s Constitution, the Responsible Entity aims to apply active capital management strategies.

The Fund may undertake a buyback of its Units in the event that they trade at a discount to NAV. The Responsible Entity will need to obtain Unitholder approval for the buyback and comply with any Corporations Act, ASX Listing Rules and Constitution restrictions if it intends to buyback more than 10% of the smallest number of Units on issue over the previous 12 months. To fund the buyback of Units, the Fund may liquidate some of its investments and, although not presently intended, may employ gearing up to the limit stated in Section 2.4.

2.12 VALUATION POLIC Y The Responsible Entity may determine valuation methods and policies for the Fund and amend them from time to time, provided that the valuation methods and policies are consistent with the Australian Standards and significant accounting policies (See Section 8.4), within the range of ordinary commercial practice, and the valuation produced is reasonably current at the time of issue or redemption of Units.

2.13 ALLOC ATION POLIC YWhere the Responsible Entity uses an executing broker for the Fund’s investments, the Responsible Entity will require the executing broker to maintain an allocation policy to ensure aggregated orders, where applicable, are allocated on the basis of fairness and priority.

2.14 REPORTS TO UNITHOLDERSThe Responsible Entity intends to provide Unitholders with:

» periodic reports setting out Unitholder account details;

» quarterly updates on key information about the Fund including performance updates;

» half-yearly auditor reviewed reports;

» annual audited reports;

» annual distribution advice statements (as applicable);

» regular income tax statements; and

» monthly Net Tangible Asset updates.

The Responsible Entity will also comply with all laws and the ASX Listing Rules as they relate to reports to be provided to Unitholders. For further information, please visit www.australianf lagshipfund.com.au.

19

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

19

Walsh & Company is the Responsible Entity of the Fund and the issuer of Units under this PDS. The Offer comprises an offer of:

» a minimum of 31.25 million Units; and

» a maximum of 62.5 million Units.

The Responsible Entity may at its discretion accept oversubscriptions for up to an additional 62.5 million Units.

The Offer comprises an offer of Units at a price per Unit of $1.60. This is the total amount payable on subscription for a Unit, and includes the structuring fee and handling fee. See Section 7.

None of the Units are restricted securities or otherwise subject to escrow. More than 20% of the Units are expected to be held by investors who are not affiliated with the Responsible Entity.

To participate in the Offer, your Application Form must be received by 5:00pm (AEST) on the Offer Closing Date. The Offer Closing Date may be brought forward by the Responsible Entity. If the Offer Closing Date is brought forward, only Application Forms lodged by that time will be considered by the Responsible Entity.

The Offer is only available to investors who have a permanent address in Australia at the time they accept the Offer.

3.1 MINIMUM SUBSCRIPTIONThe Minimum Subscription for the Offer is the receipt of valid Applications and Application Monies for not less than 31.25 million Units. If this Minimum Subscription is not achieved by the Offer Closing Date, the Responsible Entity will repay all money received from Applicants (without interest) within seven days after that date or such later date as may be permitted by the Corporations Act.

3.2 NO COOLING-OFF PERIODAs the Fund is to be listed no cooling-off period applies under the Corporations Act.

3. FUND OFFER

20

4.1 INVESTMENT PROCESS The investment process is conducted by the Investment Manager, who consults with the Investment Committee and Portfolio Consultants to assist with investment decisions.

INVESTMENT IDEA

In the first stage of the investment process the Investment Committee and Portfolio Consultants implement a top-down thematic approach by relying on their deep industry expertise and experience in addition to the broad resources of Evans Dixon.

The Investment Committee is comprised of professionals with strong track records in their respective fields of Australian business, including financials, infrastructure, property, healthcare, energy and resources.

By applying their knowledge and expertise, the Investment Committee and the Portfolio Consultants have identified, and will continue to monitor for, key investment themes and structural trends that are expected to underpin revenue growth over the medium to long term.

These key themes guide the Fund’s investment process by focusing research efforts on specific industries and companies in these areas, and are ultimately expressed through the portfolio’s individual security holdings.

Examples of these key themes include changing demographics, tourism, housing and infrastructure, and coal substitution. Further detail and examples of key investment themes are outlined in Section 5.

INVESTMENT RESEARCH

Following the identification of targeted key investment themes, initial screening is used to identify companies which may benefit. Screens are both quantitative and qualitative, depending on the investment theme and companies being assessed.

The Portfolio Consultants and Investment Manager then conduct in-depth, bottom-up research and analysis on the identified securities, as well as frequent monitoring of existing securities. This bottom-up research may involve: industry; business quality, operational, and financial analysis; evaluation of management; and valuation.

Securities are assessed against the following key criteria:

» Sustainable Competitive Advantage: Evaluation of the industry positioning of the security, its medium to long term opportunities and the sustainability of its competitive advantage. High barriers to entry, a strong track record and robust balance sheet are qualities which are favoured.

» Attractive Risk-Adjusted Returns; Growing Dividends: Assessment in detail of the security’s future earnings potential and the risks around it, both upside and down. A key focus is the returns the security is generating on its invested capital and the returns it provides to shareholders.

4. PORTFOLIO INVESTMENT PROCESS

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

21

» Quality Board and Management: A heavy emphasis is placed on the strength of the security’s management track record and the experience of the board of the directors.

» Attractive Valuation: A range of valuation methodologies will be employed to determine the relative attractiveness of a security. The aim is to identify where the market has mispriced an element of the security (i.e. earnings growth, future projects, market share gains) and then to take advantage of that opportunity with a view to the long term.

Following in-depth assessment of the short-listed securities, the Portfolio Consultants then make recommendations to the Investment Committee regarding the purchase or sale of securities in the portfolio, based on the relative attractiveness of securities. Recommendations may take place on an ad-hoc basis or at regularly scheduled Investment Committee meetings. Following consideration by the Investment Committee, any approved security purchase or sale will then be recommended to the Investment Manager for approval and trade execution.

PORTFOLIO MANAGEMENT

The portfolio is constructed in a concentrated manner. When determining security weightings, a range of factors will be considered. For each security, this may include: the assessed valuation to price, business quality and risk, size and liquidity, portfolio concentration (including by sector, product and geographic market), and each security’s correlation to existing portfolio holdings.

The Investment Manager will target the following portfolio construction, within the investment parameters in Section 2.1, once the Fund is substantially invested:

» approximately 20 to 40 securities;

» minimum market capitalisation of the issuer of the securities of $500 million;

» up to 10% in cash; and

» at the time of acquisition, a maximum weighting of 15% for any one security.

INITIAL PORTFOLIO

Subject to market conditions, it is intended the initial portfolio will be substantially invested within three months of the Offer Closing Date.

4.2 ETHIC AL CONSIDER ATIONSThe Investment Manager’s investment decisions in respect of the Fund are primarily based

on economic factors, and they do not specifically take into account labour standards or environmental, social or ethical considerations in the selection, retention, or realisation

of investments.

2222

The Investment Manager is of the view that the key investment themes identified by the Investment Committee and Portfolio Consultants within the Australian economy may enable well positioned companies to generate strong sales growth and returns above their cost of capital. While the list is not exhaustive, and these themes will change over time, several of these themes are explored below along with some of the key beneficiaries of these themes.

Using these themes as a starting point, the Investment Manager will rely on the Investment Committee and Portfolio Consultants’ industry experience and fundamental analysis to identify companies operating within these themes that it believes will outperform the broader Australian market.

FIGURE 1: KEY INVESTMENT THEMES

DISRUPTION INDUSTRY LEADERS

COALSUBSTITUTION

HEALTH &WELLNESS

TOURISM

CHANGINGDEMOGRAPHICS

INCOMEGENERATION

HOUSING &INFRASTRUCTURE

EVANS & PARTNERS Australian Flagship Fund

1. TOURISM Monetising the increasingly mobile Chinese consumermer

Inbound tourism to Australia is benefitting from Asia’s increasingly mobile middle class. Asia’s rising GDP has driven income growth for China’s large middle class, and its growing group of millennials who are more experience driven than their older counterparts. Increased disposable income has given these demographics the ability to travel with increased frequency.

China currently provides the largest cohort of tourists to Australia with over 1.3 million Chinese tourists visiting in 2017 and this is expected to more than triple over the next decade. Chinese tourists also spent $10.4 billion over the year, the most of any tourist cohort and more than double the spend from visitors from the US of $3.8 billion.

By the end of 2017 there were approximately 190 f lights per week from China to Australia. Despite the large number of inbound Chinese tourists, Chinese passport ownership is low at 8.7% compared to 25% in Japan, 35% in the US and 60% in Australia. Should the level of passport ownership increase, the Investment Manager sees potential upside to the number of inbound trips made and expects this theme still has significant runway for growth.

Companies exposed to this theme include: Sydney Airport; Flight Centre; Crown Resorts Star Entertainment; and Ardent Leisure.

5. SECTOR OVERVIEW

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

23

FIGURE 2: CHINESE TOURISTS AND TOTAL SPEND IN AUSTRALIA

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

07 08 09 10 11 12 13 14 15 16 17

Chinese Tourists: Visitors and Total Spend in Australia

Spend in Australia (LHS) Visitors (RHS)

Source: Tourism Research Australia

A$m Visitors

Source: Tourism Research Australia, International Visitor Survey August 2017; Investment Manager

2. HEALTH AND WELLNESS Leveraging Australia’s clean food reputation to the world

Australia’s reputation for producing high quality food, manufactured under strict quality standards is generally well understood among Chinese and other Asian consumers. Australia is China’s 6th largest supplier of food with exports valued at $5.3 billion in 2016.

Exporting to Asia has enabled a number of Australian companies to expand off shore. This expansion has occurred in a number of categories such as dairy, proteins and fruits, grains, wheat, infant formula, vitamins and supplements, wine and numerous other verticals.

The Investment Manager believes that as China’s gross domestic product (GDP) per capita grows, demand for high quality foods should continue to expand, and Australia is well placed to supply the region.

In addition to food products, Australia is home to a number of companies which supply innovative health and wellness solutions to the global market. This has been in part driven by a high standard of local education, a strong local health system, and Australia traditionally incentivising innovation in healthcare leading to companies successfully making investments in research and development.

Companies exposed to this theme include: A2 Milk; Bellamy’s; Synlait Milk; Blackmores; CSL; Resmed; Cochlear; and Treasury Wine.

24

FIGURE 3: MERCHANDISE EXPORTS FROM AUSTRALIA TO CHINA (A$M)

0

2,000

4,000

6,000

8,000

10,000

12,000

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Merchandise Exports from Australia to China (A$m)

Source: ABS

Source: Australian Bureau of Statistics - International Trade in Goods and Services, Australia; Investment Manager

3. CHANGING DEMOGR APHICS Australian ageing population creates differing spend patterns

Like many of its global peers, the age profile of Australia’s population is experiencing a shift. Over the last two decades the proportion of Australians aged 61 and over increased from 15% to 20% of the population, while those aged under 20 years of age as a percentage of the population declined from 29% to 25% (see figure 4 below). The ageing of the population is in part due to greater life expectancy of both men and women, as well as historical birth rates and immigration profiles. Overall, Australians now enjoy one of the highest life expectancies in the world, and the Investment Manager is of the view that this demographic shift will continue to have implications for the Australian equity market.

As the proportion of older people in Australia continues to grow, a focus on services to promote health and wellbeing is increasingly important. There are a number of market sectors that this trend will impact ranging from healthcare services in hospitals, pathology, aged care to retirement planning and other financial planning services.

Companies exposed to this theme include: Ramsey; Healthscope; Sonic; Japara; Regis; Challenger; AMP; Cochlear; and CSL.

FIGURE 4: AUSTRALIA POPULATION – BREAKDOWN BY AGE

0%

5%

10%

15%

20%

25%

30%

<20 21-30 31-40 40-50 51-60 61-70 >71

Australian Population – Breakdown by age

1997 June 2017

Source: Australian Bureau of Statistics, Estimated Resident Population By Single Year of Age; Investment Manager.

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

25

4. HOUSING AND INFR A STRUCTURE Investing in long dated cash generating assets

As Australia’s major cities grow, the type of housing being constructed will continue to change. Australia’s five major cities are all on the coast which may lead to land constraints close to the city and therefore an incentive for increased urban infill, creating opportunities for strategic land acquisitions and development solutions. The availability of traditional freestanding dwellings shifting further inland may also increase building costs and require more innovative, lightweight and efficient construction solutions.

Given this growing trend of an expanding urban sprawl, state and federal governments have announced or are considering a large number of long dated, major infrastructure projects. The direct impact of these projects on contractors is well understood however there are also significant equity market investment opportunities in the secondary suppliers to these projects.

In addition to public funding, a number of these projects are also being developed in conjunction with ASX listed companies, enabling investors to easily gain exposure to long term structural developments. Some larger projects currently in the early stages include WestConnex, the 33 kilometre underground motorway scheme in Sydney, the Westgate tunnel project in Melbourne, as well as major upgrades to both the Sydney and Melbourne metro rail services.

Detailed spending forecasts provided by governmental departments and contracts being awarded for the project life allow for good visibility over these projects when being analysed by the Investment Manager. Once completed, the Investment Manager expects these projects to provide a stable stream of long dated, inf lation hedged cash f lows that support dividend payouts to investors.

Companies exposed to this theme include: Transurban; Lend Lease; Adelaide Brighton; Boral; CIMIC; James Hardie; Stockland.

FIGURE 5: AUSTRALIA – TRANSPORT INFRASTRUCTURE WORK

0

5

10

15

20

25

30

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Australia – Transport infrastructure work yet to be done

Roads

Source: ABS

$bn

Railways

Source: Australian Bureau of Statistics – Engineering Construction Activity Australia; Investment Manager

26

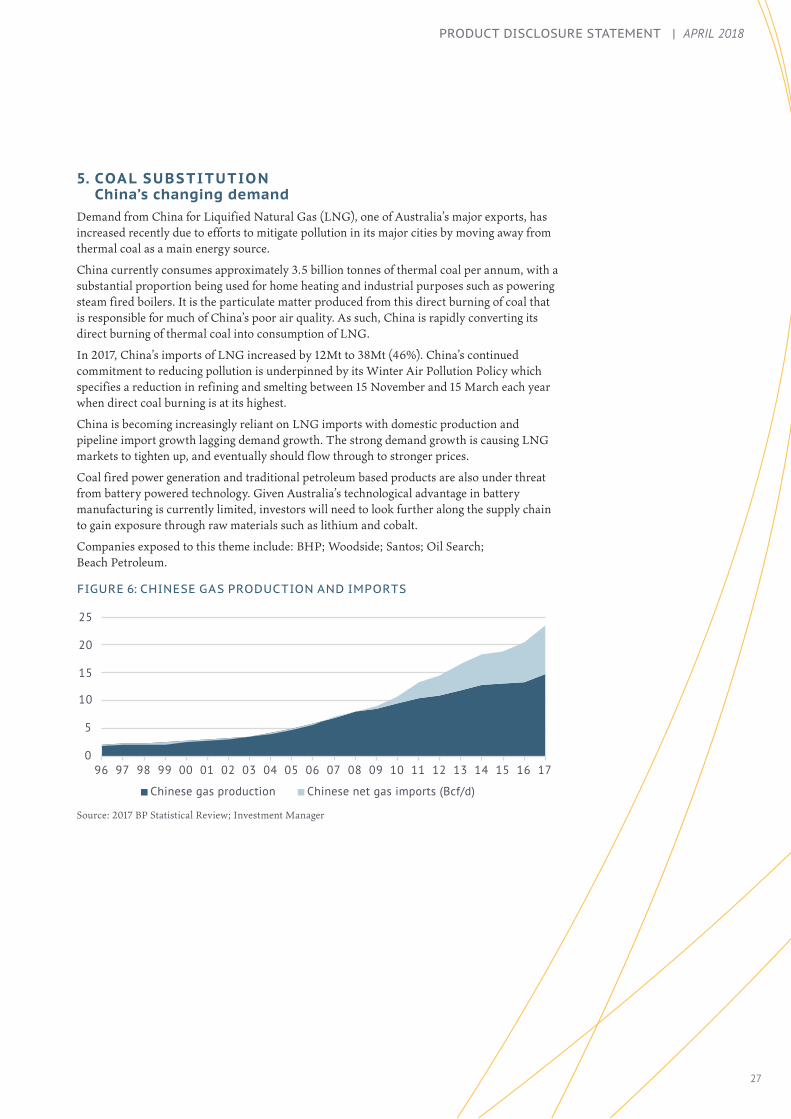

5. COAL SUBSTITUTION China’s changing demand

Demand from China for Liquified Natural Gas (LNG), one of Australia’s major exports, has increased recently due to efforts to mitigate pollution in its major cities by moving away from thermal coal as a main energy source.

China currently consumes approximately 3.5 billion tonnes of thermal coal per annum, with a substantial proportion being used for home heating and industrial purposes such as powering steam fired boilers. It is the particulate matter produced from this direct burning of coal that is responsible for much of China’s poor air quality. As such, China is rapidly converting its direct burning of thermal coal into consumption of LNG.

In 2017, China’s imports of LNG increased by 12Mt to 38Mt (46%). China’s continued commitment to reducing pollution is underpinned by its Winter Air Pollution Policy which specifies a reduction in refining and smelting between 15 November and 15 March each year when direct coal burning is at its highest.

China is becoming increasingly reliant on LNG imports with domestic production and pipeline import growth lagging demand growth. The strong demand growth is causing LNG markets to tighten up, and eventually should f low through to stronger prices.

Coal fired power generation and traditional petroleum based products are also under threat from battery powered technology. Given Australia’s technological advantage in battery manufacturing is currently limited, investors will need to look further along the supply chain to gain exposure through raw materials such as lithium and cobalt.

Companies exposed to this theme include: BHP; Woodside; Santos; Oil Search; Beach Petroleum.

FIGURE 6: CHINESE GAS PRODUCTION AND IMPORTSChinese Gas Production and Imports

Source: 2017 BP Statistical Review, E&P analysis

0

5

10

15

20

25

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Chinese gas production Chinese net gas imports (Bcf/d)

Source: 2017 BP Statistical Review; Investment Manager

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

27

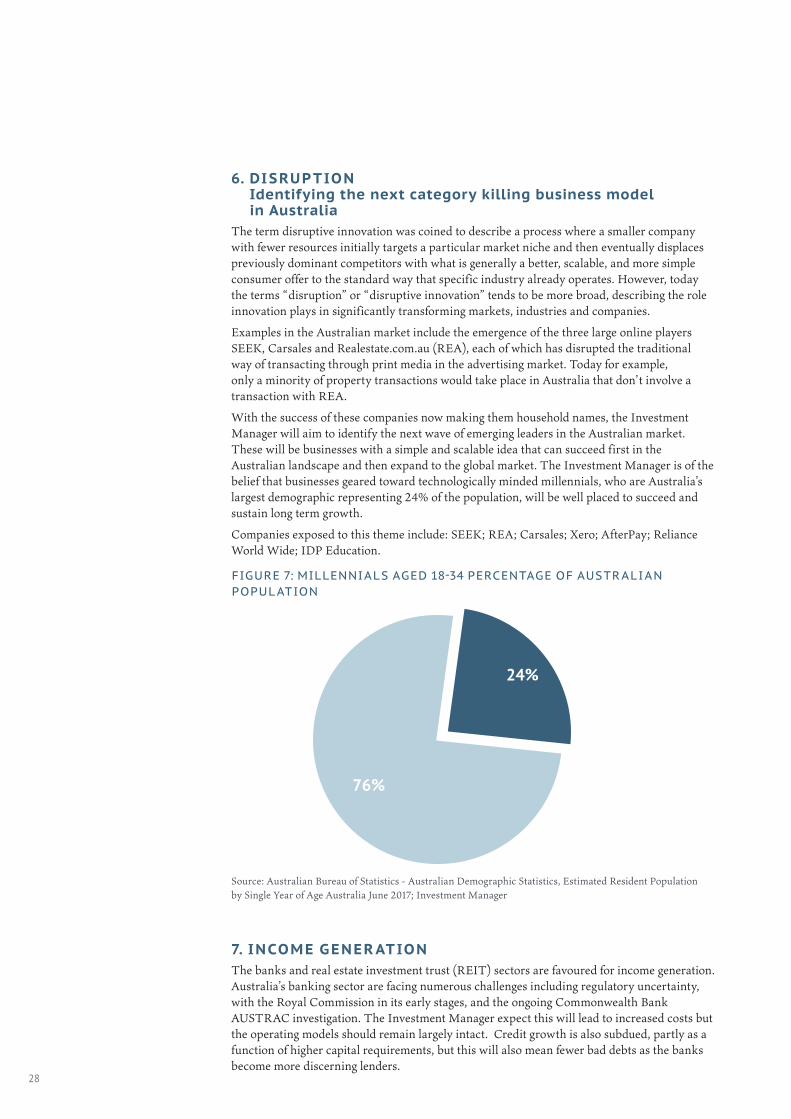

6. DISRUPTION Identifying the next category killing business model in Australia

The term disruptive innovation was coined to describe a process where a smaller company with fewer resources initially targets a particular market niche and then eventually displaces previously dominant competitors with what is generally a better, scalable, and more simple consumer offer to the standard way that specific industry already operates. However, today the terms “disruption” or “disruptive innovation” tends to be more broad, describing the role innovation plays in significantly transforming markets, industries and companies.

Examples in the Australian market include the emergence of the three large online players SEEK, Carsales and Realestate.com.au (REA), each of which has disrupted the traditional way of transacting through print media in the advertising market. Today for example, only a minority of property transactions would take place in Australia that don’t involve a transaction with REA.

With the success of these companies now making them household names, the Investment Manager will aim to identify the next wave of emerging leaders in the Australian market. These will be businesses with a simple and scalable idea that can succeed first in the Australian landscape and then expand to the global market. The Investment Manager is of the belief that businesses geared toward technologically minded millennials, who are Australia’s largest demographic representing 24% of the population, will be well placed to succeed and sustain long term growth.

Companies exposed to this theme include: SEEK; REA; Carsales; Xero; AfterPay; Reliance World Wide; IDP Education.

FIGURE 7: MILLENNIALS AGED 18-34 PERCENTAGE OF AUSTRALIAN POPULATION

24%

76%

Millenials Aged 18-34 of the Australian Population

Source: ABSSource: Australian Bureau of Statistics - Australian Demographic Statistics, Estimated Resident Population by Single Year of Age Australia June 2017; Investment Manager

7. INCOME GENER ATIONThe banks and real estate investment trust (REIT) sectors are favoured for income generation. Australia’s banking sector are facing numerous challenges including regulatory uncertainty, with the Royal Commission in its early stages, and the ongoing Commonwealth Bank AUSTRAC investigation. The Investment Manager expect this will lead to increased costs but the operating models should remain largely intact. Credit growth is also subdued, partly as a function of higher capital requirements, but this will also mean fewer bad debts as the banks become more discerning lenders.

28

A slowing housing market is also a challenge to this sector, however mortgage default rates remain still very low (approximately 1%) and it should be remembered that with mortgage insurance and high initial deposits required, the Australian market has more fail safes than other overseas markets (such as the US with non recourse lending in many states) which have experienced large declines in recent years. With all these concerns in mind, valuations are not stretched with the sector as a whole offering approximately 45% higher yield than the market as a whole.

Companies exposed to this theme include: NAB; CBA; WBC; ANZ.

FIGURE 8: BANK SECTOR YIELD RELATIVE TO ASX200 YIELD

0

2

4

6

8

10

12

08 09 10 11 12 13 14 15 16 17 18

Bank Sector Yield relative to ASX 200

ASX 200 Bank dividend yield ASX 200 yield

Source: Thomson Reuters Datastream; Investment Manager

8. INDUSTRY LEADERSThe Investment Manager believes industry leading Australian companies should form a part of a balanced portfolio. Industry leaders are companies with a large market share in a particular industry, having established high barriers to entry for new competitors, domestic or foreign. Industry leaders display characteristics such as a track record of strong returns, proven management, sustainable competitive advantage and a robust balance sheet.

Companies exposed to this theme include: Wesfarmers; Woolworths; Telstra; Macquarie Group; Amcor; Brambles; and JB Hi-Fi.

FIGURE 9: INDUSTRY LEADER CHARACTERISTICS

HIGH BARRIERSTO ENTRY

ROBUSTBALANCE

SHEET

PROVENMANAGEMENT

SUSTAINABLECOMPETITIVE ADVANTAGE

TRACK RECORD OFSTRONG RETURNS

Importantly, however, the performance of industry leading companies is still subject to market conditions. To assist in navigating this, the Investment Manager will rely on the industry knowledge, skill and experience of the Investment Committee and Portfolio Consultants to determine which industry leaders to invest in and over which time horizon.

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

29

Prior to investing, you should consider the risks involved in investing in the Fund and whether the Fund is appropriate for your objectives and financial circumstances. You should read this PDS in its entirety to gain an understanding of the risks associated with an investment in the Fund.

This PDS contains forward-looking statements based on certain assumptions that are inherently uncertain. Actual events and results of the Fund’s operations could differ materially from those anticipated. Some of the risks may be mitigated by the use of safeguards and appropriate systems and actions, but some are outside the control of the Responsible Entity and cannot be mitigated.

The Responsible Entity does not forecast or guarantee any rate of return in terms of income or capital or investment performance of the Fund. The value of the Units will ref lect the performance of the investments made by the Fund and current market conditions. There can be no certainty that the Fund will generate returns or distributions to the satisfaction of Unitholders.

The Fund should not be seen as a predictable, low risk investment. The Fund’s investments are expected to be concentrated in listed securities, and the Fund is therefore considered to have a higher risk profile than cash assets.

Investors can undertake several steps to help minimise the impact of risk. First, seek professional advice suited to your personal investment objectives, financial situation, and particular needs. Second, only make investments with a risk level and time frame recommended by your professional advisor.

This section describes the areas the Responsible Entity believes to be the major risks associated with an investment in the Fund. These risks have been separated into specific investment risks and general investment risks.

It is not possible to identify every risk associated with investing in the Fund. Prospective investors should note that this is not an exhaustive list of the risks associated with the Fund.

6.1 RISKS SPECIFIC TO THE FUND

(A) INVESTMENT SELECTION AND STRATEGY RISK

The Fund’s performance depends on the investment decisions made.

The Investment Manager may make investment decisions that result in low returns or loss of capital invested. This risk may be mitigated to some extent by the resources available to the Investment Manager and the recommendations it receives from the Investment Committee.

The success and profitability of the Fund will largely depend on the Investment Manager’s ability to manage the portfolio in a manner that complies with the Fund’s objectives, strategies, policies, guidelines, and permitted investments. If the Investment Manager fails to do so, the Fund may not perform well. There are risks inherent in the investment strategy that the Investment Manager will employ for the Fund.

(B) EQUITY RISK

The price of securities listed on securities exchanges can change considerably over time, and the market value of your investment is expected to increase and decrease with the value of the portfolio. Unitholders in the Fund are exposed to equity risk both through their holdings in the underlying investments in which the Fund will invest and through market f luctuations in the price of their Units. As with most investments, performance is not guaranteed. These risks may result in loss of income and principal invested.

The Fund may also invest at an unfavourable point of the investment cycle. The Investment Manager may invest funds at higher prices than those available soon after and may redeem investments at lower prices than those that were recently available or that may have been available soon thereafter.

6. RISKS

30

In the future, the sale of large parcels of Units may cause a decline in the price at which the Units trade. This may mean that the Fund may not trade in line with the underlying value of the portfolio. No assurances can be made that the performance of the Units will not be adversely affected by any such market f luctuations or factors. None of the Fund, the Responsible Entity, the Investment Manager or any other person guarantees the performance of the Units.

(C) COMPANY SPECIFIC RISK

Investments by the Fund in a company’s securities will be subject to many of the risks to which that particular company is itself exposed. These risks may impact the value of the securities of that company, and may include factors such as changes in management, actions of competitors and regulators, changes in technology and market trends.

(D) CONCENTRATION RISK

Generally, the more diversified a portfolio, the lower the risk that an adverse event pertaining to one security or sector has a material impact on the overall portfolio. Focusing investments in a small number of securities issuers, industries or countries increases the risk. Funds that invest in a relatively small number of securities issuers are more susceptible to risks associated with a single economic, political, or regulatory occurrence than more diversified funds might be.

(E) EXPERIENCE OF THE RESPONSIBLE ENTITY AND INVESTMENT MANAGER RISK

The Investment Manager was recently incorporated and has limited performance history.

The Investment Manager will draw upon consultants and advisors who have extensive experience in the identification, acquisition, management, and disposal of a diverse range of asset classes.

Specifically, the Investment Manager will use the Investment Committee comprised of highly experienced industry professionals, who understand how issuers of securities can effectively position themselves to deliver sustainable earnings growth and returns on capital.

The Investment Manager has also engaged experienced research professionals, Ben Chan and Adam Alexander, to provide industry consulting services as required, in the capacity of Portfolio Consultants. The Investment Manager may engage with other industry consultants as required.

The Responsible Entity acts as the responsible entity for the Fund, the Fort Street Real Estate Capital Funds I, II & III, US Masters Residential Property Fund, Emerging Markets Masters Fund, New Energy Solar, Evans & Partners Global Disruption Fund and Cordish Dixon Private Equity Funds I, II, III and IV.

There can be no guarantee that the Responsible Entity and Investment Manager will be able to achieve the Fund’s objectives or that the Investment Manager will be able to locate appropriate investment opportunities.

(F) KEY PERSONNEL RISK

There is a risk of departure of key staff or consultants with particular expertise in the sector, whether they are the staff or Directors of the Responsible Entity, the Investment Manager, members of the Investment Committee, the Portfolio Consultants or independent advisors or consultants. This may have an adverse impact on the value of the Fund.

(G) GEARING AND INTEREST RATE RISK

While there is no current intention to do so, if the Fund is geared, the level of gearing, the costs of borrowing and the applicable interest rates will impact returns.

If utilised, gearing may amplify the Fund’s gains if the market value of the portfolio appreciates, however, it may also amplify losses if the market value of the portfolio declines. Any loans secured by the portfolio could result in the lender forcing the liquidation of investments at a loss or not at a time of the Investment Manager’s choosing.

PRODUCT DISCLOSURE STATEMENT | APRIL 2018

31

The cost of borrowing may reduce the returns of the Fund.

Should the Fund obtain borrowings, changes in interest rates may have a positive or negative impact directly on the Fund’s income. Changes in interest rates may also affect the market more broadly, and positively or negatively affect the value of the Fund’s underlying assets.

(H) NO OPERATING OR PERFORMANCE HISTORY OF THE FUND

The Fund has no financial, operating, or performance history and no track record which can be used by investors to make any form of assessment of the ability of the Fund to achieve the investment objectives set out in the PDS. The information in this PDS about the investment objectives of the Fund does not constitute or include forecasts, projections, or the result of any simulation of future performance. There is a risk that the Fund’s investment objectives will not be achieved.

(I) LIQUIDITY RISK

The Units and the portfolio are each subject to liquidity risk:

i. Units: The Fund is to be listed on the ASX, however there can be no guarantee that there will be a liquid market for Units. Investors should be aware that this may limit their ability to realise a return or recover their capital.

ii. Portfolio: The Fund is exposed to liquidity risk in relation to the underlying investments within its portfolio.

(J) LONG TIME HORIZON

Investing in capital growth focused investments requires a longer term commitment than to other asset classes, and this may mean that realisation of value through capital growth may be similarly timed. In addition, a longer time horizon increases the risk of exposure to market volatility.

(K) SUBSTANTIAL UNCOMMITTED FUNDS

Subject to market conditions, proceeds of the Offer may be retained in cash until appropriate investment opportunities arise or higher cash balances may be held than targeted from time to time. Given the low interest rate environment, the likely income to be generated by the Fund from cash investments may be significantly lower than that which might be received from investment in equities.

(L) RELATED PARTY TRANSACTION RISK

The Responsible Entity will transact with related parties. There are a number of related party transactions described in this PDS. See Section 12.4 for further information.

Conf licts of interest may arise in these circumstances where there is a risk that the interests of one party or the Unitholders may diverge from the interests of the other party. The Responsible Entity has a conf lict of interest and related party transaction policy for the Fund to assist in managing this risk.

3232

(M) DISTRIBUTION POLICY RISK

The Responsible Entity intends to target a cash distribution of 5% per annum based on the NAV at or around the beginning of the relevant distribution period, paid semi-annually. The nature of the Fund’s investments in equity securities means that it is unlikely that the actual income of the Fund will be exactly 5% per annum.

There may be circumstances where the Target Distribution is not paid, or is paid from capital of the Fund. Payments out of capital will reduce a Unitholder’s cost base. See Section 10 for further information.