problems with decision criteria transparencies for chapter 2

TRANSCRIPT

Problems With Decision Criteria

• Transparencies for chapter 2

The Payoff Matrix

The Simplest structure for a decision model consist of a set of possible course of actions, a list of possible outcomes that could occur and straight forward evaluation of each decision outcome pairs. Formulated as follows:

Payoff matrix aj : Course of action j i : Outcome variable yij : The value for the decision maker if taking action

aj and i occurs a1 a2 … aj ….. am

1

2

i

n

yij

Preptown Book Store

The manger of the bookstore at the Preptown college must decide how many copies to order of the book thought thinking

to order for the course Creative Thinking. The maximum enrollment is 70. So far 50 are enrolled and this could go up or down. The book will make $ 15 on every sold book. The course will not repeat and any book unsold book will be disposed at $ 5 loss. The manger must decide how much to order.

Payoff Matrix Considering only orders in units of 10 0 10 20 30 40 50 60 70 0 0 -50 -100 -150 –200 –250 –300 -350 10 0 150 100 50 0 -50 -100 -150 20 0 150 300 250 200 150 100 50 30 0 150 300 450 400 350 300 250 40 0 150 300 450 600 550 500 450 50 0 150 300 450 600 750 700 650 60 0 150 300 450 600 750 900 850 70 0 150 300 450 600 750 900 950

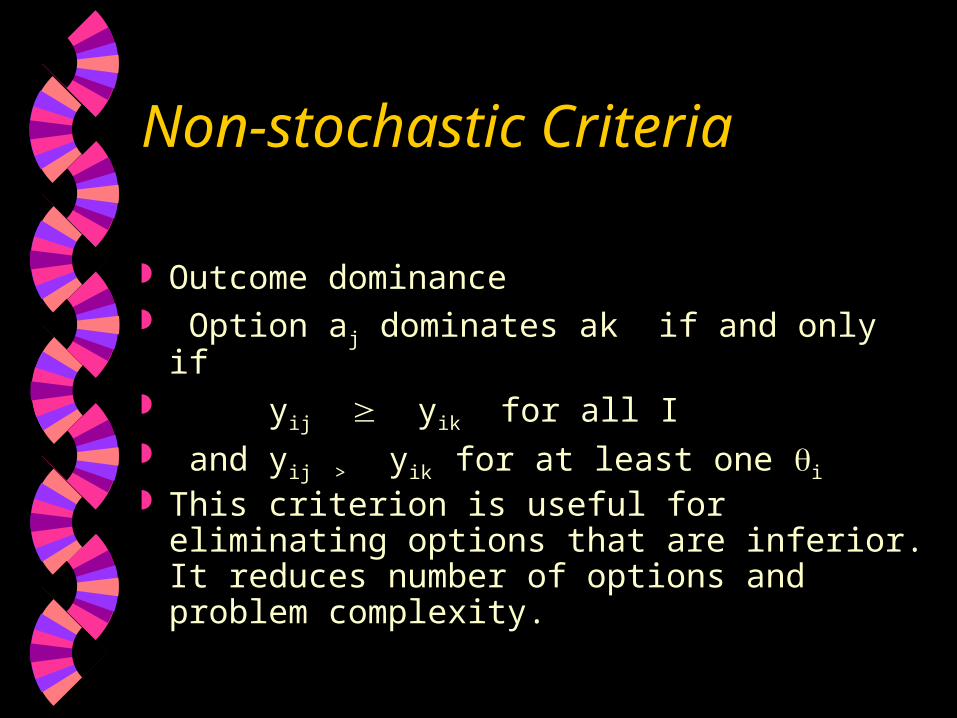

Non-stochastic Criteria

Outcome dominance Option aj dominates ak if and only if yij yik for all I and yij > yik for at least one i This criterion is useful for eliminating

options that are inferior. It reduces number of options and problem complexity.

Example for Outcome Dominance

Consider the following payoff matrix a1 a2 a3

1 6 3 8

2 5 4 2

3 7 6 3

a1 dominates a2

Maximin Criterion

Action aq is optimal in maximin criterion if and only if for each aj there exist a yij

* which is the minimum yij over all and yiq is the maximum of all yij

*

Example for Maximin Criterion

Examine the payoff matrix for the bookstore problem.

The minimums for the course of actions for a1 through a8 are:

0 -50 -100 -150 -200 -250 -300 -350 The maximum of these minimums is 0

and therefore the optimal course of action is a1.

Problem with Maxmin

Looking at the worst scenarios can be misleading as in the following matrix (Conservative criterion)

a1 a2

1 31 32

2 10,000 33

The optimal under maxmin is a2 which is misleading

Maxmax Criterion

Action aq is optimal under maxmax criterion if and only if there exist p such that

ypq yij for all i and j.

Example for Maxmax Criterion

Consider the preptown store . The maximax criterion selects a8.

Maximax criterion is risky and can result in huge losses.

Example for Maxima

This example demonstrates that maximax is risky.

a1 a2 1 9 10

2 8 -50,000

Maximax will select a2

Minimax Regret Criterion

This criterion advocated by Savage Regret rij = Max (yij) – yij

j

a1 a2 Regret matrix

1 8 9 1 0

2 12 10 0 2

Minimax Regret

aq is optimal in minimax regret sense iff

rq* rj

* for all j

where rj* = max rij

Minmax Regret

To apply minimax regret perform the following steps:

• Compute the regret matrix

• For each aj compute the maximum regret

• Select aj with the minimum maximum regret.

Minimax regret

Minimax regret violates the coherence principle. The following example demonstrate that.

a1 a2 Regret matrix

1 8 2 0 6

2 0 4 4 0 a1 is the optimal using minmax regret

Minmax and Coherence ( cont.)

Payoff Matrix Regret Matrix

a1 a2 a3 a1 a2 a3

1 8 2 1 0 6 7

2 0 4 7 7 3 0

a2 is optimal when a3 is added. This is rank reversal. Any criterion that reverses the rank of alternatives is incoherent.

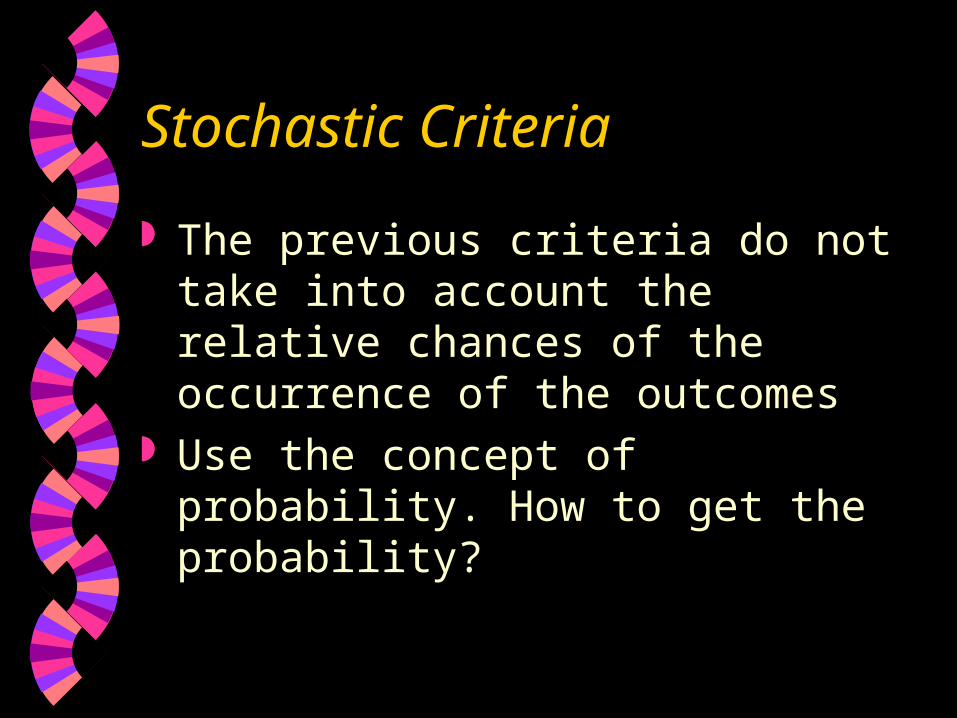

Stochastic Criteria

The previous criteria do not take into account the relative chances of the occurrence of the outcomes

Use the concept of probability. How to get the probability?

Probability Distributions

Review Probability Expected Value Mode Variance Possible application

Model Outcome

aq is optimal in modal outcome sense iff exist p such that :

P(p) P(i) for all i

and ypq ypj for all j

Modal Outcome

This criterion look at the most likely outcome and then select the course of action that has the maximum payoff with respect to this outcome.

p( ) a1 a2 a3

1

2

3

0,2

0.7

0.3

18 15 19

20 22 19

40 30 20

Modal Outcome

The following counter example shows that the model criterion could be misleading

p( ) a1 a2 a3

1

2

3

0,24

0.25

0.51

0 99 98

0 99 99

21 20 20

Modal Outcome

Linley presented an example to show modal outcome is incoherent.

p( ) a1 a2

1

2

3

2/9

4/9

5 3

5 3

8 9

3/9

Modal Outcome

Linley presented an example to show modal outcome is incoherent. Justify?

p( ) a1 a2

1 &2

3

5/9 5 3

8 9

4/9

Expected Value

EV(aj) = yijP(i )

Action aq is optimal in expected value sense iff :

E(aq) ≥ E(aj) for all j

i

Expected Value Example

p( ) a1 a2 a3

1

23

0.2

0.7

0.1

18 15 19

20 22 19

40 30 20

EV(Aj) 21.6 21.4 19.1

a1 is the optimal in expected value sense

Expected Regret

Compute the regret matrix Compute expected regret Select the option that minimizes expected

regret. The solution that maximizes expected

value is the same as the one that minimizes expected regret. Proof on page 29 text.

Expected Regret Example

p( ) a1 a2 a3

1

23

0.2

0.7

0.1

1 4 0

2 0 3

0 10 20

ER(aj) 1.6 1.8 4.1

a1 is the optimal in minimizing expected regret

Modal Outcome

This criterion look at the most likely outcome and the select the course of action that has the maximum payoff with respect to this outcome.

p( ) a1 a2 a3

1

2

3

0,2

0.7

0.3

18 15 19

20 22 19

40 30 20

Payoff Distribution Analysis

Payoff matrix versus payoff distribution For each action there is a payoff for each

state of nature (outcome) . Let us denote the payoff vector for aj by Yj and its probability distribution by pj( ). The payoff vector with its probability distribution is called the payoff distribution

Payoff Formulation of DP

The DP problem can be formulated as follows:

Given a set of payoff distributions Yj

(Options), select the best payoff distribution among them. Best, in what sense?

Expected value sense, medial payoff sense, modal payoff sense, etc.

Modal Payoff Versus Modal Outcome

p( ) a1 a2 1

23

0.3

0.3

0.4

10 20

10 20

15 10

This example shows modal payoff not the same as modal outcome. How see page 31 Bunn book “ Applied Decision Analysis”

Risk Analysis

Risk is the Likelihood of greater losses. It is the probability of undesirable event occurring.

In financial analysis risk is taken to be the dispersion of payoff distribution. (variance).

In insurance industry risk refers to the maximum amount of money which can lost under a particular policy. It is referred to as the expected value of a detritus proposal.

Measures of Risk

Variance : focuses on dispersion

Semi-variance: Focuses on the largest possible values greater than a certain value c.

dyyfyyv i )()( 22

=

iSv2

=dyyfyy

c

)()( 2

Measures of Risk

Critical probability: Same as semi-variance but risk is measured in terms of probability.

P( y≤ c ) = = F(c) Why we need all these

measures?

dyyfc

)(

Generalization of Risk Measures

Fishburn generalizes the last two measures of risks by making the power . If = 2 it becomes the semi-variance. If = 0 it becomes the critical value and so on. The use of critical value is more applicable in practice.

Mean -Variance Dominance Option aj dominates option ai iff E(aj) E(ai) and V(aj) ≤ V(ai) with one of

them an inequality.• Option j E(aj) V(aj)

• 1 7 1• 2 8 2• 3 9 2• 4 7

1.5• 5 10 3

Option 3 dominates options 2, option 1 dominates option 4. The efficient set:

ES = { Options 1, 3 and 5}