privateers of the caribbean: the hedge funds-us-uk ... · pdf file2 privateers of the...

TRANSCRIPT

1

Privateers of the Caribbean:

The Hedge Funds-US-UK-Offshore Nexus

Jan Fichtner, Department of Political Science, Goethe University, Campus Westend – PEG,

Grüneburgplatz 1, 60323 Frankfurt, Germany. Website: http://www.jfichtner.net

Jan Fichtner is Lecturer in Political Science at Goethe University Frankfurt, Germany. His

current research focuses on different aspects of a Global Political Economy of hedge funds.

His work for publication includes the role of hedge funds as agents of financialization, the

impact of activist hedge fund on the German political economy, and the way growing income

inequality since the early 1980s has driven the rise of the hedge fund industry.

* * *

This is a pre-print version of the article that has been published in Competition & Change,

Vol. 18, No. 1, (2014), pp. 37-53. For full access use this link:

http://www.maneyonline.com/doi/full/10.1179/1024529413Z.00000000047

* * *

2

Privateers of the Caribbean:

The Hedge Funds-US-UK-Offshore Nexus

This paper argues that there is a nexus between private profit-oriented actors (privateers

and hedge funds) – being only lightly regulated by their home countries (Britain and

America) – and ‘offshore’ territories located in the Caribbean and elsewhere in the

Anglo-Saxon world. We argue that the ultimate reason for this nexus is the common

‘Lockean’ state/society complex of the UK and the US. The analysis of hedge funds as

privateers reveals that both benefit at the expense of others, while the geographic regions

in which they are based are virtually the same – London and New York/Boston.

Furthermore, this paper shows that the hedge fund ‘value chain’ is clearly dominated by

the US and the UK. Most hedge funds are based in Offshore Financial Centers (OFCs).

While this is a commonplace, by introducing the OFC-Intensity Ratio we show that the

most intensive OFCs are under the sovereignty of the US and the UK.

Keywords: Hedge funds, privateers, offshore, US, UK, differential gain

Introduction

In 1568 Sir Francis Drake landed on a group of islands in the Caribbean Sea south of Cuba.

Drake was one of the most infamous privateers of the era and at the same time an admiral of

Elizabeth I. Allegedly he named the archipelago after the indigenous word for crocodile – the

Cayman Islands. The Cayman Islands today, with a population of just 50,000 and a GDP of

$2 billion is the largest legal domicile for hedge funds in the world. Drake’s landing on the

Cayman Islands can be interpreted as one of the earliest historical precedents of a nexus

between private profit-oriented actors (first privateers and now hedge funds) that benefit at

the expense of other actors – while being only lightly regulated by their home countries (the

UK and the US) – and ‘offshore’ territories located in the Caribbean and elsewhere in the

Anglo-Saxon world. This paper argues that the ultimate reason for this nexus is the common

‘Lockean’ state/society complex (van der Pijl, 1998; 2006) of both the US and the UK.

A recent paper by Ertürk et al. (2010) has demonstrated that applying innovative analogies is

able to shed light on the opaque topic of hedge funds. Ertürk et al. criticize the frequently

used metaphorical characterizations of hedge funds as either traders/arbitrageurs or

3

speculators/gamblers. Instead, they offer the analogy of ‘nomadic war machine’ emphasizing

the highly mobile and opportunistic nature of hedge funds. They describe nomadic war

machine as ‘a marauding, rootless army – a self-organizing structure without state control that

exists for itself’ (ibid., p.18). This paper seeks to complement the analogy of hedge funds as

nomadic war machine by introducing the analogy of the privateer. Ertürk et al. acknowledge

that nomadic war machines are ‘often harnessed by the state in an attempt to do their

bidding’, but do not discuss the role of particular states. We argue that the genesis and demise

of privateers can only be explained by the role of specific states – first and foremost Britain

and the US. As a result, the position hedge funds occupy within the contemporary global

political economy can only be explained by analyzing the role of these two states.

This paper is organized in six sections. Following this introduction, section two introduces the

analogy of privateers. The theory of the ‘Lockean heartland’ is the concern of section three.

Section four argues that hedge funds pursue differential gains and that the entire hedge fund

value chain is clearly dominated by the US and the UK, respectively the offshore financial

centers (OFCs) under their sovereignty. Section five picks up the concept of ‘offshore’ and

argues that this phenomenon has been primarily driven (and/or tolerated) by the Lockean

heartland. In addition, this section introduces the OFC-Intensity Ratio, which reveals that

Lockean jurisdictions are clearly the most intensive OFCs by far. Finally, section six

concludes.

Privateers: Benefit at the Expense of Others

Privateers had the aim to enrich themselves at the expense of other maritime travelers. This

was mostly achieved by violent means, such as the forced appropriation of other vessels and

their merchandise (Starkey, 1990). Individual privateering ventures were financed by

merchants or other rich investors, which then received a predetermined share of the prize. In

eighteenth century Britain the prize was commonly divided in two parts, with the investors

receiving one half, and the crew receiving the other one. Although the aims and methods of

privateers have been similar to those of pirates, both activities had always been theoretically

distinct and became more clearly demarcated in the seventeenth century: ‘While the

privateersman assumed a place within the developing code of international maritime law …

the pirate’s indiscriminate and unauthorized business was increasingly outlawed’ (ibid., p.19).

4

The practice of privateering had its origin as early as the thirteenth century when English

kings regularly utilized private vessels of the ‘Cinque Ports’ for war purposes (Starkey, 1990).

A second origin was the long practiced arming of merchant ships in order to give them

protection against pirates. Finally, a third development strand of privateering was the ancient

right of reprisal. In the Middle Ages it was customary for individuals to make reprisals upon

the subjects of foreign rulers in order to recoup losses (Starkey, 2001). In 1295 England

became the first country to issue a letter of marque, which was aimed at Portugal (Thomson,

1994). The issuing of letters of marque and reprisal reached an apex in the sixteenth century

when Anglo-Spanish relations were in crisis. The boundary between official expeditions by

the Crown and privateering ventures was unclear, however; ‘privately motivated, but in the

ostensible service of the English Crown, these privateers severely blurred the line between

both state interest and private wealth accumulation’ (Mabee, 2009, p.149). The 1585 raid on

the West Indies by Drake was financed to one third by Elizabeth I and Drake acted as the

queen’s admiral. All fleets led by Drake in the 1580s and 1590s were of that hybrid character,

combining strategic purposes with prize-hunting. Other voyages remained essentially private

predatory ventures, in which the queen only invested (Andrews, 1964).

Another famous privateer of this era was Sir Walter Raleigh, who founded the first English

colony in North America in 1584. In 1592 his ships brought back a huge treasure on a

captured Spanish ship: ‘The “Madre De Dios” alone provided privateers with half a normal

year’s takings’ (ibid., p.125). Indeed the main motivation for privateering – ‘the setting out of

privately owned vessels licensed by the state to appropriate the seaborne property of enemy

subjects’ (Starkey, 1988, p.50) – was to make profit. Andrews (1964) has found that between

1589 and 1591 approximately 270 English privateering voyages were undertaken. His rough

estimate is that the average profit on the fixed capital was 60%. Such a high profitability was

hard to achieve in most other industries, hence many investors moved to privateering. Drake

even became one of the richest men of England, as his raids on the Spanish treasure fleet were

very profitable: ‘Drake extorted large ransoms from two Spanish colonial cities by threatening

to burn them to the ground. His sack of Peru netted him and his backers £2.5 million and

repaid his backers, including Elizabeth, “47 for 1”’ (Thomson, 1994, p. 23). Privateers such as

Drake and Raleigh played a decisive role in the genesis of Britain’s maritime power in the

5

sixteenth century. The prizes seized by privateers measured up to between 10% and 15% of

English imports in some years (Andrews, 1964).

The regulation of privateering became more formalized in the seventeenth century, as the

rapid growth of state navies and overseas trade compelled major maritime powers to codify

their relations. Due to Dutch pressure the Anglo-Dutch Marine Treaty of 1674 fixed the

deposited surety at 3,000 pound for a vessel with 150 men or more (Starkey, 2001). This

ensured that privateers acted in accordance with the newly drafted ‘instructions to privateers’

by the Lords of Admiralty. If the instructions were contravened (for example by attacking

neutral Dutch vessels) the surety was liable to prosecution by the High Court of Admiralty:

The instructions ‘constituted a code of practice intended to guide the behavior of the

privateersman at sea and to ensure the proper adjudication of prizes’ (Starkey, 2001, p.24).

Again largely due to Dutch pressure, Britain passed the Privateers Act in 1759 which

introduced some minor restrictions on privateers. This increased, though still mild form of

regulation had the purpose to make sure that individual cases in which privateers attacked

neutral shipping did not provoke important trading partners such as the Dutch. Thus, the aim

was to ensure that both privateers (and their investors) and the state benefited from preying on

the commerce of rival powers. Consequently, Starkey (2001, p.79) has characterized the

British privateering enterprise as a ‘tense amalgam of private interest and public service’.

Centers of Privateering

Privateering was practiced intensively in America too – before and after the independence

from Britain. Swanson (1989) has found that in the period of 1739–48 alone there were at

least 3,973 instances of prize actions by American privateers. Manhattan was the single most

important American port for privateering, while the whole region from New York to Boston

formed the epicenter of this predatory industry. American (and British) privateering

concentrated on the Caribbean, because most of the precious merchandise from the Spanish

and French colonies passed through the Caribbean Sea. This line of business was extremely

profitable: ‘Privateering offered American merchants the opportunity to earn substantial

profits since successful voyages yielded returns of 130–140%.’ (Swanson, 1985, p.382).

Privateering continued after independence from Britain and played an essential role for the

early maritime history of America (Swanson, 1989).

6

Several small islands under British sovereignty also played significant roles as bases for

privateering, for example Bermuda and the Channel Islands. Bermuda, settled in 1609 by the

private Virginia Company on behalf of the English Crown, was a centre of privateering in the

seventeenth and eighteenth centuries. Other important bases for privateering were the Channel

Islands of Jersey and Guernsey, which mostly concentrated their preying on French traffic.

Privateers from Jersey and Guernsey became such a threat to French shipping in the mid-

eighteenth century that France deployed nine frigates ‘specifically to suppress the activities of

“les mauvaises corsairs de Guernsey et Jersey”’(Raban, 1989, p.295). Thus, it seems

appropriate to refer to Bermuda and the Channel Islands in those days as British ‘offshore

privateering centers’.

Comparative data on the history of privateering are incomplete. It seems highly probable,

however, that Britain and America together formed the largest base of privateering from the

late sixteenth to the early nineteenth century. Other states, particularly the United (Dutch)

Provinces and France, also were home to substantial numbers of privateers (Lunsford, 2005).

Britain, however, seems to have been a significantly larger base for privateering. From 1689

to 1815 alone there were about 23,000 applications for letters of marque filed with the High

Court of Admiralty in London. Privateering represented a considerable net addition to the

economic and military power of Britain. Most of the economic benefits accumulated in

London – the largest British centre for privateering in the eighteenth century by far (Starkey,

2001).

The Demise of Privateering

The importance of privateers began to decline significantly in the early nineteenth century as

the effects of the Industrial Revolution began to make an impact. The Industrial Revolution

completely changed economic life and enabled a vast number of highly profitable new

investments. In contrast to many of these new business possibilities, privateering was not very

scalable; the number of target vessels was simply limited. Hence, privateering became much

less attractive – especially due to the fact that it inherently was a dangerous endeavor.

Furthermore, large business ventures such as the British East India Company also combined

the private use of violence with the aim to make profits, but could scale their activities to a

7

much greater extent (Robins, 2006). In addition, the Royal Navy had become the largest navy

in the world by far, and as such could perform the role of privateers in preying on enemy

seaborne commerce. As a result, Great Britain found it in her interest to internationally outlaw

privateering by signing the Declaration of Paris in 1856 (Thomson, 1994).

In essence, privateers were private profit-motivated actors authorized by their home states –

primarily Britain and America – to benefit at the expense of actors from foreign states. Hence,

privateering had a dual purpose; on the one hand it represented a very profitable private

business opportunity, on the other hand it was of strategic benefit to the state. Britain and

America relied much more than other states on the private profit-motivated preying on the

seaborne commerce of foreign powers. This paper argues that the ‘Lockean’ state/society of

both countries is likely to be a central factor.

The ‘Lockean Heartland’

According to van der Pijl (1998, p.64) the ‘Lockean’ state/society complex finally became

clearly recognizable in England in the late seventeenth century – although elements of this

state/society complex had existed long before: ‘The Glorious Revolution of 1688 sealed the

series of transformations by which the vestiges of royal absolutism and feudal forms of social

protection in England had been torn down.’ The two main results of the Glorious Revolution

were the constitutional limitation of state power and the protection of the genuinely ‘private’.

Locke had generally argued for the withdrawal of the state from social and economic life and

for self-regulation of civil society; his ideas were rooted in ‘the tradition of gentry self-

regulation that had been the backbone of the English social order since the Middle Ages’ (van

der Pijl, 2006, p.7). This long tradition could explain why privateering existed before the

Glorious Revolution. The true emergence of the Lockean state, however, is linked to the

Glorious Revolution: ‘The Lockean state, governed by a constitutional monarch controlled by

a parliament, is the true bourgeois political formation; a state that “serves” a largely self-

regulating “civil” society by protecting private property at home and aboard’ (van der Pijl,

2006, p.8). In the middle of the seventeenth century private corporations such as the Virginia

Company transferred tens of thousands of settlers from the English motherland to the colonies

in North America. The pattern of self-government they brought with them enabled the

subsequent transnationalisation of the Lockean state/society complex: ‘with the Lockean

8

pattern transmitted to the new areas of settlement, there emerged, on the foundations of

industrial/commercial centrality and predominance, a heartland of the global political

economy’ (van der Pijl, 1998, p.70).

A special role might be ascribed to the United Provinces, which were not part of the Lockean

heartland proper, but closely associated with it since the late seventeenth century: ‘A flow of

funds was set in motion that would give Dutch investors stakes in the English national debt,

the East India Company, and the Bank of England, which ranged between one-quarter and

one-third by the mid-eighteenth century. Holland thus became an ancillary of the Lockean

heartland’ (van der Pijl, 2006, p.8). However, the two most important states of the Lockean

heartland have always been Britain and America. The temporary rift between them from the

mid-eighteenth to the early nineteenth century is not contradicting the theory of the Lockean

heartland, as the break-away by America was entirely in the Lockean spirit (ibid., p.10):

Mercantilist prohibitions on the development of manufactures motivated the English-speaking

settlers to rebel against British imperial control. Yet, as early as the 1820s, the common heritage

prevailed when the two states jointly established their informal empire over Latin America after

that continent’s emancipation from Iberian overlordship.

The counter model to this Lockean state is the ‘Hobbesian’ state, which only became fully

developed with Napoleonic France in the early nineteenth century, but whose contours were

already visible in seventeenth century France: ‘concentric development from above, using the

state as a lever; a “revolutionary” ideology mobilizing the social base; and a foreign policy

backing up the claim of sovereign equality with a powerful military’ (ibid., p.12). In short,

‘the specificity of the Hobbesian configuration resides in the paramountcy of the state’ (van

der Pijl, 1998, p.81). The Hobbesian state generally has an explicit doctrine of national

interest, and a genuine state class that relies on a powerful administration to regulate society

and the economy. In contrast, the Lockean state as a general rule relies on self-regulating

markets. There is no genuine state class, but rather a governing class that rules on behalf and

in the interest of the leading capitalist class. Hence, the mode of expansion of the Lockean

state is transnational, whereas the mode of expansion of Hobbesian states is international.

The primary purpose of the Lockean state is to foster free (capitalist) enterprise that the civil

society pursues at home and abroad. Therefore, it is only logical that finally in 1911 the US

9

and the UK outlawed war as a means of conflict resolution between both countries. ‘Thus’,

writes van der Pijl (1998, p.73), ‘the Lockean states drew together politically, placing

themselves outside the Hobbesian universe of Realpolitik in their mutual relations.’ The

renunciation of war is only valid for the Lockean heartland internally, however. The

maintenance of a powerful military force is necessary to secure a persistent predominance of

the Lockean heartland over the global political economy; this is the major exception to the

general retreat of the state in the Lockean state/society complex. This retreat of the state is not

complete, of course. Rather, the aim is to confine ‘the state to guaranteeing the general

conditions for capital accumulation and the creation of markets where they did not exist, and

hence bringing more and more areas of social life under the discipline of capital’ (Apeldoorn

et al., 2012, p. 476).

In irregular intervals the predominance of the Lockean heartland over the global political

economy has been directly challenged by other states that rose to power – ‘Hobbesian

contender states’. The first true Hobbesian contender state was Napoleonic France. Later

Hobbesian contender states included Imperial Japan, Nazi Germany and the Soviet Union.

China could become the next contender (van der Pijl, 2012); as a Hobbesian state it steers and

regulates its economy tightly – particularly its financial markets. This is in contrast to the US

and the UK, where financial markets, including actors such as hedge funds, play a pivotal

role. Both countries, in accordance with their Lockean state/society complex, have liberalized

and deregulated financial markets since the 1970s. Hence, it is only logical that hedge funds –

pure financial markets actors – have developed there. In the following sections we argue that

there are striking similarities between privateers and hedge funds, and that there is a nexus

between them, the US and the UK, and ‘offshore’ territories under their sovereignty.

Arguably the ultimate reason for this nexus is the common Lockean state/society complex.

Hedge Funds: Pursuit of Differential Gains

The rise of hedge funds has been made possible by the liberalization and deregulation of

financial markets pursued by the US and the UK since the 1970s. However, hedge funds only

became significant in the early 1990s when the number of funds as well as their assets under

management (AUM) began to grow rapidly. The entire hedge fund industry had AUM of

close to $40 billion in 1990. In March 2013 hedge funds hit a new all-time high of $2,375

10

billion in AUM (HFR, 2013). Despite this rapid growth hedge funds still only constitute a

small proportion of the entire global financial stock. However, because of high leverage and

the fact that they are more active traders than virtually all other investors, hedge funds have

an impact that is much greater than this small proportion would suggest. In general, hedge

funds are private investment vehicles, which are only lightly regulated. They cater primarily

to wealthy individuals and institutional investors and employ alternative investment strategies

(Harmes, 2002). Two characteristic features of hedge funds are discussed in this section:

Their aim to generate absolute returns, and the fact that the whole hedge fund ‘value chain’ is

dominated by just two countries, the US and the UK.

Absolute or Differential Returns?

The hedge fund industry has generally claimed to be able to generate ‘absolute returns’ in

every market condition. Another aim of most hedge funds is to generate ‘alpha’, profits that

are not correlated to the returns on the major financial markets (‘beta’). One problem with

evaluating these claims is the fact that most statistics on the hedge fund industry are produced

by private companies. Hedge funds are not obliged to report their performance to regulators –

as the Lockean US and UK have so far refrained from any direct regulation. Chapman (2012)

has analyzed hedge fund returns vis-à-vis stock market returns between 1999 and 2011, he

also took into account estimated hedge fund fees and assumed prime broker fees (together

called hedge fund community, HFC). According to the calculations by Chapman, the HFC has

outperformed ‘the market’ in every single year except 2003 when stock markets rebounded

from the dot-com crash – with particularly high outperformance 1999–2002 and 2007–2008.

However, in 2008 even hedge funds could not decouple completely from the stock markets

(which lost 34%) and lost 14% (ibid.). Hence, the claim by the hedge fund industry to

consistently generate ‘absolute returns’ is refuted. It seems much more probable that what

hedge funds really do is to pursue differential returns.

Financial markets are said to play an important role for the functioning of modern economies,

however, seen in isolation they represent a zero-sum game: ‘if a group of hedge funds is

betting heavily on a fall in energy prices or the convergence of Latin American interest rates,

somebody else must be betting just as heavily on the opposite outcome. Viewed globally, this

system of wagers is a giant zero-sum game’ (Mallaby, 2007, p.99). Or, in the words of

11

Chapman (2012), who focuses on the differential returns of the HFC: ‘the battle for alpha is a

zero sum game, so such HFC outperformance must be matched by equivalent losses by other

investors, such as pension funds, insurance funds and mutual funds.’ Thus, if financial

markets inherently represent a zero-sum game and hedge funds generate differential returns,

then hedge funds clearly benefit at the expense of other actors. As shown in section two, the

benefit at the expense of others has been an integral feature of privateers too. Hence, hedge

funds resemble privateers is this respect, except that they do not use violence of course –

which is not surprising given the vastly different levels of physical violence in society then

and today (Pinker, 2011). The other characteristic that defined privateers has been the

paramount role of Britain and America. Thus, now we turn to the centrality of the US and the

UK for the entire hedge fund ‘value chain’.

The Hedge Fund ‘Value Chain’

Hedge funds do not exist in isolation; they depend on a variety of other actors to function.

Hedge funds are connected to investors, fund administrators, hedge fund managers, prime

brokers and custodians. Together these institutions form the hedge fund ‘value chain’. Data

specifically pertaining to hedge fund custodians are not readily available. Custodians

primarily hold assets and do not provide many services to hedge funds beyond that. Hedge

fund administrators are more important. Hedge funds outsource accounting, investor services

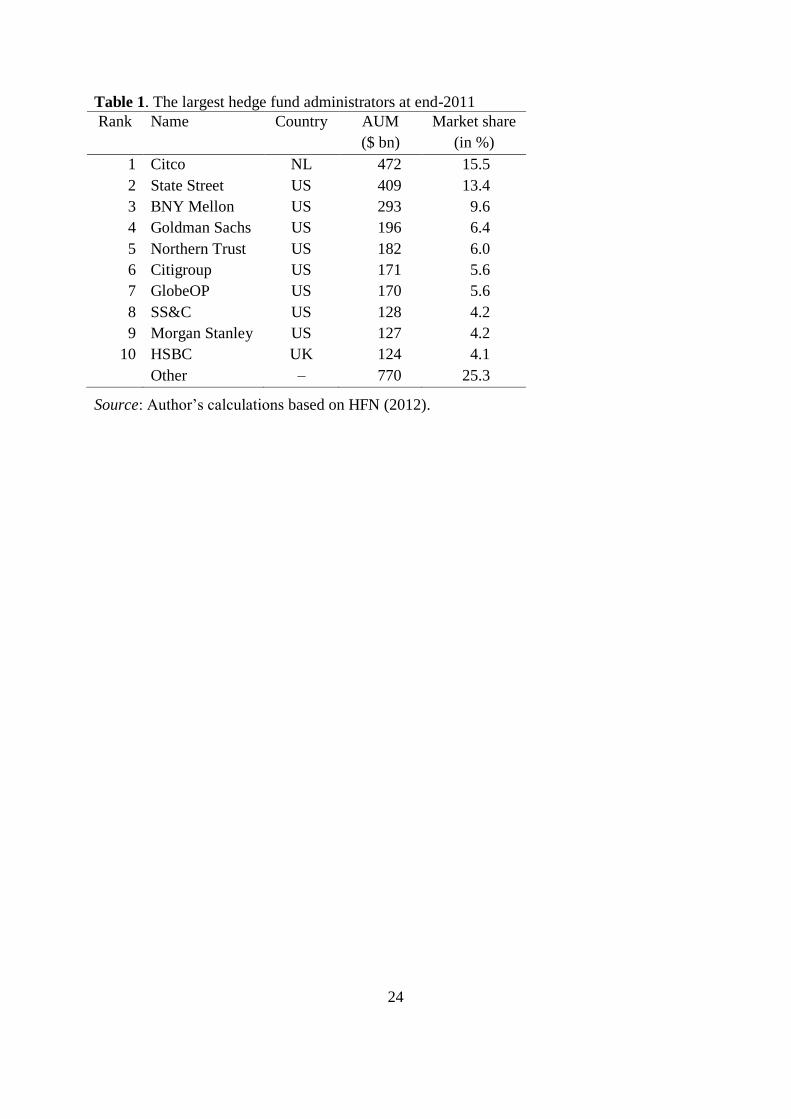

or risk analysis to administrators (TheCityUK, 2012). Table 1 shows the ten largest hedge

fund administrators at end-2011.

[Insert Table 1 here.]

In 2011 the largest hedge fund administrator of the world was Dutch. CITCO, which stands

for Curaçao International Trust Company, is based in Curaçao. This jurisdiction is an

‘autonomous country’ within the Kingdom of the Netherlands, but located in the Caribbean.

Curaçao is an OFC under Dutch sovereignty; this highlights the role of the Netherlands as an

ancillary to the Lockean heartland. Besides CITCO, the ranking of hedge fund administrators

is clearly dominated by the US. A still more important role than administrators is played by

hedge fund prime brokers. Prime brokers, which are part of large investment banks, are vital

partners to hedge funds; they execute trades, provide leverage or lend shares for short-selling.

12

Table 2 lists the top prime brokers in 2011.

[Insert Table 2 here.]

Hedge fund prime brokerage is dominated by US institutions. The top three prime brokers –

Goldman Sachs, Morgan Stanley and JPMorgan Chase – had 48.3% market share in 2011. All

five US institutions together had a market share of 56.9%. The considerable market shares of

Deutsche Bank, UBS and Credit Suisse could be misleading, however. Arguably the majority

of their prime brokerage services are carried out in the US and the UK, because all three have

bought American or British firms to enter this lucrative business.

At the end of 2011 about 70% of global hedge fund assets have been managed in the US.

Hedge fund managers based in the UK managed approximately 18% – virtually all of them

concentrated in London (TheCityUK, 2012). US based hedge fund managers are also

concentrated geographically. About 42% of hedge fund assets have been managed from New

York. The remaining roughly 28% of US-based hedge fund managers worked mainly in

Connecticut and Boston (IFSL, 2010). Hence, approximately 75-80% of all global hedge fund

managers are based in just two greater regions – the greater London area and the region

spanning from New York over Connecticut to Boston. Exactly these two regions were the

centers of British and American privateering. Hence, both hedge funds and privateers share

the characteristic of benefit at the expense of others, and, remarkably, both private profit

oriented actors have been based in the very same geographic regions of the ‘Lockean

heartland’. Furthermore, both have been financed by profit-motivated investors, both have

been very risky, and both have promised high returns. The remuneration schemes have been

quite similar too, with the privateers/hedge fund managers receiving a predetermined (high)

share of profits. Another similarity is that (in their heyday) both have been only lightly

regulated by the US and the UK.

The last remaining component of the hedge fund ‘value chain’ is the legal domicile of the

hedge funds. The vast majority is legally domiciled in jurisdictions that offer low taxation and

lax regulation – so-called OFCs. In 2010 the most popular legal domicile for hedge funds has

been the Cayman Islands, which accounted for 52% of assets under management (AUM) by

13

hedge funds. This was followed by the US state of Delaware with 22% of AUM. Place three,

four and five have been occupied by the British Virgin Islands, Jersey and Bermuda with

11%, 5% and 4%, respectively (Jaecklin et al., 2011). The Cayman Islands, the British Virgin

Islands and Bermuda are ‘British Overseas Territories’, which means that they enjoy certain

autonomy in internal affairs such as tax legislation, but ultimately remain under British

sovereignty (Hendry and Dickson, 2011). The same holds for Jersey, a so-called ‘Crown

Dependency’. Hence, in 2010 nearly 95% of the AUM by the global hedge fund industry have

been domiciled in OFCs that are under the sovereignty of the US and the UK. In fact, we will

argue below that it is hard to conceive the phenomenon of ‘offshore’ without the pivotal role

of these two Lockean states.

‘Offshore’ as an Anglo-American Phenomenon

The phenomenon of ‘offshore’ is less about geography than about a withdrawal of public

regulation and control, primarily over finance: ‘Acting “offshore” means operating not

literally off the coast of institutionally structured countries but beyond the control of any

public institution’ (Deneault 2010, p.94). In the very core, then, ‘offshore’ is about a

bifurcation of state sovereignty:

‘Offshore consists of a set of juridical realms marking differential degrees of intensity, by which

states apply regulations, including taxation. Offshore is legal enclaves distinguished from their

“on-shore” brethren, not necessarily because of their location, but because they define a territory

or a realm of activities in which states choose to withhold some or all of their regulations and

taxation. In that sense, offshore signals a profound fissure in the life of the state system: it

denotes nothing less than the bifurcation of the juridical space of sovereignty into mutually

dependent relative spaces’ (Palan 1998, p.635).

This section argues that the Lockean heartland time and again has fostered or tolerated the

phenomenon of ‘offshore’. This is perfectly in line with the Lockean state/society

configuration, in which the state withdraws itself from the economy (except in times of

crisis); it is also in line with privateering, where ‘offshore’ deeds were permitted which never

would have been allowed onshore.

The first wave of offshore legislation developed in the late nineteenth century. As early as the

14

1880s the US states of New Jersey and Delaware began to draft legislation specifically to

attract corporations from other states (Palan, 2002). The aim, however, was not to shift

production to these emerging offshore centers, but only the legal personality of the

corporation to benefit from lower taxation. The Netherlands, an ancillary of the Lockean

heartland, played an important role by inventing the holding company in 1893 (Palan et al.,

2010). This ‘innovation’ was of paramount importance as it allowed corporations to shift

some of their profits to OFCs. In a series of decisions between 1876 and 1929 British courts

created the ‘virtual’ residency of foreign corporations in Britain, allowing them to incorporate

in Britain without paying taxes (ibid.). This British legislation is emblematic for the Lockean

state/society complex in which state interference is subordinate to civil society self-regulation.

Other countries, such as Switzerland or Liechtenstein also developed as OFCs. But in most

situations, they followed the lead of the Lockean heartland, and the US and the UK have been

the decisive veto players that could have halted the further development of offshore. During

World War II both Lockean states restricted the freedom of private enterprise, because the

challenge by the two Hobbesian contender states of Nazi Germany and Imperial Japan

required the mobilization of all economic resources. After the war the trend towards

‘offshore’ continued.

The most important instance for the rise of offshore clearly has been the development of the

Eurodollar market in the City of London since the late 1950s. In essence, British authorities

tolerated the ‘regulatory vacuum’ in which non-resident institutions conducted financial

transactions in foreign currencies (primarily US dollars) in the City of London (Burn, 1999).

True to the Lockean state configuration, there has been no clear-cut distinction between the

state and business actors and ‘careers flowed effortlessly from the City to the Bank and back

again (ibid., p.252). Palan et al. (2010, p.132) summarize this momentous development:

‘Because the transactions took place in London, they could not be regulated by any other

regulatory authority and so occurred nowhere – or rather, in a new and unregulated space

called the Euromarket, or the offshore financial market’.

During the 1960s jurisdictions such as the Cayman Islands, Bermuda and Jersey began to

become OFCs – with the latter two sharing a long tradition of having been ‘offshore

privateering centers’ in the seventeenth and eighteenth centuries. This has mostly been

15

accomplished by the government of the jurisdiction working in tandem with law and

accounting firms from the US and the UK. Jersey, Guernsey and the Isle of Man are ‘Crown

Dependencies’. The Cayman Islands, the British Virgin Islands, Bermuda and other territories

are ‘British Overseas Territories’. Hendry and Dickinson (2011, p.12) characterize their

position in international law as follows: ‘The overseas territories are plainly not independent

sovereign states. Their external relations remain the responsibility of the UK, the sovereign

power. Accordingly, the UK is responsible for each of the territories under international law.’

In fact, legally the territories could still be called ‘colonies’ of the UK (ibid.). In a bizarre

twist, however, the territories are not constitutionally parts of the UK, but are under direct

authority of the Crown. The Queen also appoints the governor of each territory. Even though

the British Overseas Territories have their own judicial systems and enact most of their laws

themselves, the final instance of appeal is the Privy Council of Her Majesty. That the UK has

ultimate sovereignty over all these territories has been demonstrated conspicuously when in

2009 London suspended local government in Turks and Caicos Islands due to evidence for

widespread corruption (Reuters, 2009).

This peculiar pseudo-independent status of the British Overseas Territories and Crown

Dependencies, having semi-autonomy in areas such as fiscal policy, but maintaining close ties

in foreign affairs and defense, is perfectly suited for the development of offshore. OFCs need

political, economic and fiscal stability, and of course a stable currency. London, however,

also played a vital role: ‘Indeed, the development of many of these jurisdictions as offshore

financial centers was encouraged and facilitated by UK authorities, especially the Bank of

England’ (Picciotto, 1999, p.67). This development of offshore is perfectly in line with the

nature of the Lockean state, which withdraws itself from social and economic life, but is still

needed to secure property rights and contracts. Or in the words of Palan (1998, p.627),

offshore ‘is a case of having your cake and eating it: maintaining the state system as organizer

and mediator of conflict and tension, yet removing the threat of regulation and taxation

attendant with the state – all done in the name of and by the state system itself.’ In essence,

the Lockean heartland creates a transnational space that allows capital to minimize taxation

and regulation and to flow freely between formally autonomous territories.

16

Measuring OFC-Intensity

In order to verify the exact role of the Lockean heartland for the phenomenon of offshore we

empirically compare the size of OFCs to their GDP. The result is the ‘OFC-Intensity Ratio’,

which is a rough indicator of the intensity with which each jurisdiction acts as an OFC. There

is no definition of the term OFC that is universally agreed upon. As a working definition we

follow Zoromé (2007) because his definition is well suited for empirical research. For Zoromé

(ibid., p.7) ‘an OFC is a country or jurisdiction that provides financial services to nonresidents

on a scale that is incommensurate with the size and the financing of its domestic economy.’

We approximate the size of OFCs using data from both the IMF and the Bank of International

Settlements (BIS). Since data on OFCs is not complete and suffers from serious

underreporting by some jurisdictions it makes sense to use both the CPIS (Coordinated

Portfolio Investment Survey) data from the IMF and the LBS (Locational Banking Statistics)

from the BIS in order to approximate the amount of foreign assets booked in OFCs. CPIS is a

voluntary survey conducted by the IMF, in which data on portfolio investment by non-

residents is collected (IMF, 2013). The LBS measure international loans and deposits of

banks in the reporting jurisdictions (BIS, 2013). We combine the CPIS or the LBS values and

divide this sum of foreign assets by GDP – for which we use the value at official exchange

rate provided by the CIA World Factbook (CIA, 2013). In total, 201 jurisdictions have been

analyzed; Table 3 displays the top 30 jurisdictions ranked according to their OFC-Intensity

Ratio in 2011.

[Insert Table 3 here.]

It is remarkable that the British Overseas Territory Cayman Islands is by far the most

intensive OFC with an OFC-Intensity Ratio of 1,566 (this extreme value mostly explains the

large difference between the mean of 14.53 and median of 0.31). This means that the foreign

assets booked in the Cayman Islands are over 1,566 times larger than GDP. Second placed

Marshall Islands are located in the Pacific and became formally independent in 1986, but are

since then ‘in free association’ with the US. The remaining top ten is dominated by

jurisdictions that are under British sovereignty or that are (formally independent) Common-

wealth realms, such as The Bahamas. Hence, in terms of OFC-intensity the jurisdictions that

are formally or informally dependent on Britain clearly play in their own league.

17

Just for illustration we have included the US state of Delaware. Delaware is the second

smallest state with a population of only 900,000. Despite its small size Delaware is the legal

domicile of more than half of all publicly listed US corporations. Corporations with a

‘Delaware-based tax strategy in place are able to reduce their state tax burden between 15%

and 24% when compared to other firms’, write Dyreng et al. (2012). Delaware has been

considered an abusive tax haven by the government of Brazil (ibid.). Deneault (2010, p.87)

concurs: ‘Delaware behaves like any other tax haven. It guarantees banking secrecy and

minimal or zero tax rates to foreign investors.’ There are no official statistics regarding the

amount of external assets booked in Delaware. However, three different sources report that

estimates put the value of external assets deposited in Delaware at $5 trillion (Hossli, 2009;

Hämmerli, 2009; Deneault, 2010). Using this estimate, Delaware would be the ninth most

intensive OFC, just after Anguilla.

No real economic ‘value’ is created in OFCs, virtually no foreign corporations run production

or research and development activities there. Even the number of people employed in finance

is minuscule when compared to the huge number of foreign corporations registered in most

OFCs. The raison d'être of OFCs is by and large the fact that they enable foreign actors to

evade taxes and avoid regulation of their home jurisdictions. Hence, the essence of OFCs is

benefit at the expense of others – just like this is the very essence of hedge funds, and like it

was of privateers before them.

In the aftermath of the global financial crisis the G20 have launched an initiative to regulate

OFCs. A study by Johannesen and Zucman (2013, p.25), however, finds that ‘the least

compliant havens have attracted new clients, while the most compliant ones have lost some,

leaving roughly unchanged the total amount of wealth managed offshore.’ Thus, this initiative

has been a farce, a symbolic measure to appease electorates (Rixen, 2013). The same is true

for the initiative to regulate hedge funds. France and Germany had long demanded a

regulation of hedge funds. The US and the UK, however, are the two decisive veto players in

this field. Because the global financial crisis had highly politicized this topic, the US and the

UK acquiesced to Franco-German demands (and also to growing domestic pressure) and

increased the regulation of hedge funds slightly. Similar to the G20 initiative on tax havens,

18

however, this has to be seen as a largely symbolic measure that is not fundamentally

infringing Lockean principles.

Conclusion

The purpose of this paper has been to facilitate the heterodox analysis of hedge funds. The

analysis of hedge funds as privateers reveals that there is a long Anglo-American (or

Lockean) tradition of setting up business ventures that have the purpose to benefit at the

expense of others (with or without using violence). Both privateers and hedge funds have

been financed by investors, both have been very risky, and both have promised high returns.

The remuneration schemes have been quite similar too, with the privateers/hedge fund

managers receiving a predetermined (high) share of profits. Remarkably, the vast majority of

hedge fund managers today is based in exactly the same two greater regions that have been

the principal centers for privateering – London and the region from New York to Boston. In

addition, this paper shows that the entire hedge fund ‘value chain’ is clearly dominated by the

US and the UK. Obviously, no analogy is perfect and there are of course significant

differences between privateers and hedge funds – which is to be expected as both activities

are separated by centuries. The point of this paper is that there are striking similarities, and

that these similarities are not coincidental, but arguably stem from the common Lockean

state/society complex of the US and the UK.

The fact that the majority of hedge funds is legally domiciled in OFCs is well documented.

The contribution of this paper, however, is to demonstrate that the OFCs mostly used by

hedge funds (Cayman Islands, Delaware, British Virgin Islands, Jersey and Bermuda) are

under the sovereignty of the US and the UK; moreover, the introduction of the OFC-Intensity

Ratio clearly shows that the most intensive OFCs of the world are British or American

dependencies. In fact, the Cayman Islands is by far the most intensive OFC with an OFC-

Intensity Ratio of 1,566; this means that the foreign assets booked in the Cayman Islands are

1,566 times as large as the GDP of this archipelago. The phenomenon of ‘offshore’ – seen as

a bifurcation of state sovereignty into different juridical spaces marked by lower degrees of

regulation and taxation to the benefit of wealthy individuals and large corporations,

particularly finance – can well be explained by the theory of the Lockean heartland. Van der

Pijl (1998; 2006) has introduced the concept of the Lockean state/society complex; the

19

Lockean state generally is subordinate to the interests of the financial and business elite.

Hence, the Lockean state partly withdraws itself from the economy, leaving the protection of

private property and contracts as its most important purpose – except for periods when the

predominance of the Lockean heartland was seriously threatened by Hobbesian contender

states, such as Napoleonic France or Nazi Germany (or in times of severe economic crises).

The Lockean heartland is currently not challenged by a contender state. Thus, we might

compare the initiatives by the G20 and the OECD to regulate OFCs and hedge funds to the

Anglo-Dutch Marine Treaty of 1674 and the Privateers Act of 1759, which introduced some

minor regulations for privateering but did not constrain their activity in any fundamental way.

The abolition of privateering in 1856 suggests that the Lockean heartland will only agree to a

rigorous regulation of ‘offshore’ and hedge funds once they lose their important roles for the

pursuit of differential gains by wealthy individuals and large corporations – at least for the

near future such a development seems highly unlikely. The only other conceivable

development that could lead to a strict regulation of these two phenomena would be a serious

challenge to the predominance of the Lockean heartland by China. While not impossible, such

a development currently seems improbable. China could potentially become a genuine

Hobbesian contender state in the middle of the twenty-first century. Unlike earlier contender

states, however, China has intense economic and financial relations with the Lockean

heartland. And the plan to make the renminbi an international reserve currency inside the

global political economy still dominated by the Lockean heartland will arguably lead to a

gradual loss of control over domestic financial markets for Beijing. In addition, currently

planned relaxations of private capital outflows could even lead to an alignment of the interests

of Chinese investors with the Lockean heartland in the long term (Bloomberg, 2013) – not

entirely unlike the inflows of private Dutch capital into England in the early eighteenth

century.

Privateering had a dual purpose for the Lockean states of Britain and America; on the one

hand it represented a very profitable business opportunity, on the other hand it was of

strategic benefit to the state as it weakened rival powers. Modern global finance is more

complex than historical privateering. Hence, it has been beyond the scope of this paper to

discuss the strategic purpose of hedge funds for the Lockean heartland – which certainly is

20

less clear-cut than that of privateers. Inter alia such a strategic role of hedge funds could lie in

the opening of non-Lockean economies to Lockean principles, practices and capital. Potential

examples include activist hedge funds that force listed corporations in Europe and Japan to

maximize shareholder value as well as episodes such as the Asian crisis, in which hedge funds

arguably contributed to a spread and intensification of the crisis – which, in turn, entailed a

certain opening of ‘East Asian capitalism’ to Lockean practices and capital. Hedge funds

could also potentially play a role in financing the US trade deficit by earning higher returns

abroad than foreign investors earn in the US. Thus, the strategic purposes of hedge funds to

the Lockean heartland seem to be a promising avenue for future research.

References

Andrews, K. (1964) Elizabethan Privateering: English Privateering during the Spanish War,

1585–1603 (Cambridge: Cambridge University Press).

Apeldoorn, B., de Graaff, N. & Overbeek, H. (2012) The Reconfiguration of the Global

State–Capital Nexus, Globalizations 9(4), pp. 471–486.

Bloomberg (2013) China Studies Plan for Retail Investment Abroad,

http://www.bloomberg.com/news/2013-01-24/china-studies-plan-for-retail-investment-

abroad-securities-says.html.

BIS (2013) Locational Banking Statistics, http://www.bis.org/statistics/bankstats.htm.

Burn, G. (1999) The State, the City and the Euromarkets, Review of International Political

Economy 6(2), pp. 225–261.

Chapman, J. (2012) Hedge fund gains are other funds’ losses, Financial Times,

http://www.ft.com/cms/s/0/9c8fb776-7e49-11e1-b009-00144feab49a.html.

CIA (2013), The World Factbook, https://www.cia.gov/library/publications/the-world-

factbook/.

Deneault, A. (2010) Offshore: Tax Havens and the Rule of Crime (New York: The New

Press).

Dyreng, S., Lindsey, B. & Thornock, J. (2012) Exploring the Role Delaware Plays as a Tax

Haven, Centre for Business Taxation Working Paper WP 12/12 (Oxford: Oxford University).

Ertürk, I., Leaver, A. & Williams, K. (2010) Hedge Funds as ‘War Machine’: Making the

Positions Work, New Political Economy 15(1), pp. 9–28.

21

Hämmerli, A. (2009) Steueroasen geben dem Druck nach, Manager-Magazin,

http://www.manager-magazin.de/finanzen/artikel/0,2828,616620,00.html.

Harmes, A. (2002) The Trouble with Hedge Funds, Review of Policy Research 19(1), pp.

156–176.

Hendry, I., Dickinson, S. (2011) British Overseas Territories Law (Oxford: Hart).

HFN (2012) HFN Q4 2011 Administrator Survey,

https://www.hedgefund.net/AdminSurvey/hfresults.aspx?Quarter=4&Year=2011.

HFR (2013) Hedge Fund Assets Track HFRI To Record In 1Q13,

https://www.hedgefundresearch.com/pdf/pr_20130419.pdf.

Hossli, P. (2009) Steueroasen in Delaware, Weltwoche,

http://www.weltwoche.ch/ausgaben/2009-11/artikel-2009-11-usa-steueroasen.html.

IMF (2013) Coordinated Portfolio Investment Survey, http://cpis.imf.org/.

IFSL (2010) Hedge Funds 2010, http://www.thecityuk.com/assets/Uploads/Hedge-funds-

2010.pdf.

Jaecklin, S., Gamper, F. & Shah, A. (2011) Domiciles of Alternative Investment Funds,

www.alfi.lu/sites/alfi.lu/files/files/Publications_Statements/Press_releases/Oliver-Wyman-

presentation-written-21-11-11.pdf.

Johannesen, N., Zucman, G. (2013) The End of Bank Secrecy? An Evaluation of the G20 Tax

Haven Crackdown, http://www.parisschoolofeconomics.eu/docs/zucman-

gabriel/revised_jan2013.pdf.

Lack, S. (2010) The Hedge Fund Mirage (Hoboken, NJ: John Wiley&Sons).

Lunsford, V. (2005) Piracy and Privateering in the Golden Age Netherlands (Basingstoke:

Palgrave Macmillan).

Mabee, B. (2009) Pirates, Privateers and the Political Economy of Private Violence, Global

Change, Peace & Security 21(2), pp. 139–152.

Mallaby, S. (2007) Hands off Hedge Funds, Foreign Affairs 86(1), pp. 91–101.

Palan, R. (1998) Trying to Have Your Cake and Eating It: How and Why the State System

Has Created Offshore, International Studies Quarterly 42(4), pp. 625–643.

Palan, R. (2002) Tax Havens and the Commercialization of State Sovereignty, International

Organization 56(1), pp. 151–176.

Palan, R., Murphy, R. & Chavagneux, C. (2010) Tax Havens: How Globalization Really

Works (Ithaca: Cornell University Press).

22

Picciotto, S. (1999) Offshore: The State as Legal Fiction, in M. Hampton and J. Abbott (eds.)

Offshore Finance Centers and Tax Havens: The Rise of Global Capital (West Lafayette:

Purdue University Press), 43–79.

Pinker, S. (2011) The Better Angels of Our Nature: Why Violence Has Declined (New York:

Penguin).

van der Pijl, K. (1998) Transnational Classes and International Relations (London:

Routledge).

van der Pijl, K. (2006) Global Rivalries: From the Cold War to Iraq (London: Pluto Press).

van der Pijl, K. (2012) Is the East Still Red? The Contender State and Class Struggles

in China, Globalizations 9(4), pp. 503–516.

Raban, P. (1989) Channel Island Privateering, 1739–1763, International Journal of Maritime

History 1(2), pp. 287–299.

Reuters (2009) Britain Suspends Government in Turks and Caicos Islands,

http://www.reuters.com/article/2009/08/14/us-britain-turkscaicos-

idUSTRE57D3LN20090814.

Rixen, T. (2013) Why reregulation after the crisis is feeble: Shadow banking, offshore

financial centers, and jurisdictional competition, Regulation & Governance, forthcoming.

Robins, N. (2006) The Corporation that Changed the World: How the East India Company

Shaped the Modern Multinational (London: Pluto Press).

Starkey, D. (1988) The Economic and Military Significance of British Privateering, 1702-83,

Journal of Transport History 9(1), pp. 50–59.

Starkey, D. (1990) British Privateering Enterprise in the Eighteenth Century (Exeter:

University of Exeter Press).

Starkey, D. (2001) The Origins and Regulation of Eighteenth-Century British Privateering, in

C.R. Penell, ed., Bandits at Sea: A Pirates Reader (New York: NYU Press).

Swanson, C. (1985) American Privateering and Imperial Warfare, 1739–1748, The William

and Mary Quarterly 42(3), pp. 357–382.

Swanson, C. (1989) Privateering in Early America, International Journal of Maritime History

1(2), pp. 253–278.

TheCityUK (2012) Hedge Funds 2012,

www.thecityuk.com/assets/Reports/Financial_Markets_Series/Hedge-Funds-2012.pdf.

23

Thomson, J. (1994) Mercenaries, Pirates, and Sovereigns: State-Building and Extraterritorial

Violence in Early Modern Europe (Princeton: Princeton University Press).

Zoromé, A. (2007) Concept of Offshore Financial Centers: In Search of an Operational

Definition. IMF Working Paper WP/07/87 (Washington, DC: IMF).

24

Table 1. The largest hedge fund administrators at end-2011

Rank Name Country AUM

($ bn)

Market share

(in %)

1 Citco NL 472 15.5

2 State Street US 409 13.4

3 BNY Mellon US 293 9.6

4 Goldman Sachs US 196 6.4

5 Northern Trust US 182 6.0

6 Citigroup US 171 5.6

7 GlobeOP US 170 5.6

8 SS&C US 128 4.2

9 Morgan Stanley US 127 4.2

10 HSBC UK 124 4.1

Other – 770 25.3

Source: Author’s calculations based on HFN (2012).

25

Table 2. The largest hedge fund prime brokers in 2011

Rank Prime broker name Country Market share

(in %)

1 Goldman Sachs US 17.4

2 Morgan Stanley US 16.4

3 JPMorgan Chase US 14.5

4 Deutsche Bank Germany 9.0

5 UBS Switzerland 8.4

6 Credit Suisse Switzerland 8.3

7 Citigroup US 5.0

8 Bank of America US 3.6

Other – 17.4

Source: TheCityUK (2012).

26

Table 3. The OFC-Intensity Ratio for the top 30 ‘offshore’ jurisdictions in 2011

Rank Country CPIS + LBS

($ bn)

GDP

($ bn)

OFC-

Intensity

Ratio

1 Cayman Islands (UK) 3524.29 2.25 1566.35

2 Marshall Islands (US) 39.65 0.17 227.90

3 Brit. Virgin Islands (UK) 173.23 1.10 158.20

4 Guernsey (UK) 358.17 2.74 130.63

5 Jersey (UK) 547.12 5.10 107.28

6 Bermuda (UK) 534.21 5.77 92.66

7 St. Kitts and Nevis (CR) 61.08 0.72 85.43

8 Anguilla (UK) 13.61 0.18 77.78

9 Bahamas, The (CR) 563.40 7.79 72.34

10 Antigua & Barbuda (CR) 80.74 1.12 72.22

11 Luxembourg 3339.57 59.20 56.41

12 Isle of Man (UK) 111.23 4.08 27.29

13 Curaçao (NL) 112.09 5.08 22.06

14 Liberia 31.31 1.55 20.26

15 Samoa 8.85 0.64 13.80

16 Gibraltar (UK) 14.72 1.11 13.31

17 Mauritius 144.41 11.26 12.83

18 Ireland 2354.75 217.28 10.84

19 Barbados (CR) 39.51 3.69 10.72

20 Belize (CR) 11.88 1.45 8.20

21 Seychelles 7.90 1.06 7.45

22 Hong Kong (China) 1266.55 248.61 5.95

23 Liechtenstein 27.91 4.83 5.78

24 Malta 49.92 8.89 5.62

25 Panama 134.29 26.78 5.01

26 Cyprus 99.57 24.69 4.03

27 St. Vincent & Grenadines (CR) 2.66 0.69 3.86

28 Netherlands 2933.28 836.07 3.51

29 Bahrain 73.10 22.95 3.19

30 Turks and Caicos (UK) 1.74 0.55 3.17

– Delaware (US) ~5000.00 65.76 ~76.00

Note: LBS data for 3, 7, 8, and 10 is only available aggregated to ‘West Indies UK’; LBS data

has been allocated to these four jurisdictions according to their GDP. CR stands for

‘Commonwealth Realm’.

Source: Author’s calculations based on IMF (2013), BIS (2013) and CIA (2013).