private equity investments -...

TRANSCRIPT

Author: Gunnar Freyr Gunnarsson

Study nr: 402785

Advisor: Peter Løchte Jørgensen

Private equity investments How do private equity funds create value within their portfolio firms

Aarhus School of Business, University of Aarhus

Department of Business Studies

June 2011

Abstract The purpose of this thesis is to explore private equity as a phenomenon by looking at

what it is, how it is structured and to investigate what activities private equity firms

can practice in order to generate value within their portfolio companies.

The thesis is split into 4 main chapters. The first part focuses on the literature around

the two main theories discussed, the optimization of the capital structure and the

agency theory. The second chapter is based on general discussions on private equity

to give the reader an insight into this asset class. The major part is dedicated to

analysis of activities that private equity firms can undertake to generate value in their

investments. In order to combine theories and reality, the third chapter is devoted to

analysis of two quite recent private equity investments, the takeover of ISS A/S and

TDC A/S. An attempt is made to evaluate the influence of the takeover by the private

equity firms by analyzing changes in the companies’ capital structure and operations.

The last chapter focuses on how private equity investments can be exited. This is an

important angle of the process as it can have a material effect on the final value of the

investments. The central subject of the chapter is an investigation of the very recent

IPO of Pandora A/S.

Based on the analysis made in this thesis it is my opinion that private equity as an

object in the financial literature has made an important contribution the development

of theories around corporate finance. Although the value generating activities

discussed cannot be confined only to private equity firms, it is clear that their

expertise in applying debt as a governance tool and implement clear and focused

strategy is vital for the value generating process in general. And with hands-on

management style, they are able to decrease the agency cost and at the same time

increase the unity between owners and employees that results in improved efficiency.

Table of contents

1. Introduction ................................................................................................................ 1 1.1 Motivation .......................................................................................................................... 3 1.2 Methodology and structure of the thesis ................................................................. 3 1.3 Limitations ......................................................................................................................... 5

2. Literature Review ...................................................................................................... 6 2.1 Private equity & Capital structure ............................................................................. 6 2.2 Private equity & Agency theory .................................................................................. 8

3. Private Equity .......................................................................................................... 11 3.1 Definition ......................................................................................................................... 11 3.2 Structure ........................................................................................................................... 13 3.3 Investment Process (Fundraising – structuring the finance) ......................... 15 3.3.1 Debt forms ................................................................................................................................ 16 3.3.2 Existing debt ............................................................................................................................ 17 3.3.3 Senior debt ................................................................................................................................ 17 3.3.4 Mezzanine debt ....................................................................................................................... 18

3.4 Types of buyouts ............................................................................................................ 18 3.4.1 LBO ............................................................................................................................................... 18 3.4.2 MBO .............................................................................................................................................. 19 3.4.3 MBI ............................................................................................................................................... 19 3.4.4 BIMBO ......................................................................................................................................... 19 3.4.5 PIPE .............................................................................................................................................. 19

3.5 Value drivers of PE funds ............................................................................................ 20 3.5.1 Value capturing ....................................................................................................................... 21 3.5.1.1 Financial arbitrage ........................................................................................................................ 21

3.5.2 Value creation .......................................................................................................................... 22 3.5.2.1 Primary levers ................................................................................................................................ 22 3.5.2.2 Secondary levers ........................................................................................................................... 28

4. Case comparison ..................................................................................................... 31 4.1 EQT Partners & Goldman Sachs Capital Partners takeover of ISS ................ 34 4.2 Nordic Telephone Company ApS (NTC) takeover of TDC ................................. 42

5. Exit strategies for PE investments .................................................................... 50 5.1 Initial public offering (IPO) ........................................................................................ 51

5.2 The case of Pandora ...................................................................................................... 54

6. Conclusion ................................................................................................................. 58

Bibliography ..................................................................................................................... 61

Appendix ........................................................................................................................... 68 1. ISS assets development ...................................................................................................... 68 2. ISS return on assets and profit margin ......................................................................... 68 3. ISS summarized financials ................................................................................................ 69 4. Net debt to EBITDA with possible results of an IPO ................................................. 69 5. ISS v/s Peers EBITDA margin .......................................................................................... 70 6. ISS profit margin v/s sales growth ................................................................................. 70 7. Development in asset base TDC v/s Peers .................................................................. 71 8. IPOs volume 2000-‐2010 .................................................................................................... 71 9. Pandora´s operational development 2009-‐2010 ..................................................... 72 10. Questionnaire and answers from Torben Ballegaard Sørensen ....................... 72

Table of figures

Figure 1: PE investments in volume 2000-2009 ............................................................ 1

Figure 2: Thesis structure ............................................................................................... 3

Figure 3: Simplified categorization of financial assets ................................................ 12

Figure 4: Average Private Equity investment size 2007-2009 .................................... 12

Figure 5: Private equity fund lifecycle (own creation) ................................................ 14

Figure 6: Cash flows in private equity ......................................................................... 16

Figure 7: Typical capital structure in LBOs ................................................................. 17

Figure 8: Factors behind value generation in LBOs (own creation) ............................ 21

Figure 9: Cash flows and their market values for two different firms with different

capital structures .......................................................................................................... 23

Figure 10: Debt to equity and cost of financial distress ............................................... 25

Figure 11: Tax shield and financial distress costs ........................................................ 26

Figure 12: Debt to equity ratio of ISS and its peers ..................................................... 37

Figure 13: ISS and peers interest coverage ratio .......................................................... 37

Figure 14: Net debt to EBITDA ISS v/s Peers ............................................................. 38

Figure 15: Return on assets .......................................................................................... 40

Figure 16: Asset turnover (ATO) and Profit margin (PM) .......................................... 40

Figure 17: ISS operating margin v/s profit margin ...................................................... 41

Figure 18: Financing and use in TDC takeover ........................................................... 43

Figure 19: TDC debt to equity ratio v/s peers .............................................................. 44

Figure 20: TDC Interest coverage ratio v/s Peers ........................................................ 44

Figure 21: TDC net debt to EBITDA v/s peers and its EBITDA margin .................... 45

Figure 22: TDC revenue and revenue growth .............................................................. 46

Figure 23: Return on assets (ROA) – TDC v/s Peers .................................................. 47

Figure 24: TDC´s asset turnover and profit margin ..................................................... 47

Figure 25: TDC revenue and EBITDA margin v/s peers ............................................. 48

Figure 26: Enterprise value and EV/EBITDA for TDC and peers .............................. 49

Figure 27: Exit strategies of leveraged buyouts 2000-2005 ........................................ 50

Figure 28: Proceeds from Pandora´s IPO .................................................................... 56

Figure 29: Artificial net equity value changes in Pandora ........................................... 57

Acronyms and definitions

PE: Private equity

LBO: Leveraged buyout

RLBO: Reverse leveraged buyout

MBO: Management Buyout

MBI: Management buy-in

BIMBO: Buy-in management buyout

PIPE: Private investment in public company

IPO: Initial public offering

GP: General partner

LP: Limited partner

FIH Erhvervsbank (FIH): FIH is Danish Bank specializing in lending to Danish

corporates

Kaupthing Bank: Was an international Icelandic bank, headquartered in Reykjavík,

Iceland. Following a major banking and financial crisis in Iceland in October 2008 it

was taken over by the Financial Supervisory authority and is now in liquidation.

Investment grade: A rating that indicates that a corporate bond has a relatively low

risk of default

1

1. Introduction

Private equity (PE) activities have grown rapidly for last three decades. Investments

on behalf of PE funds and firms have received an enormous attention both in the

media and in the financial society. The Economist, for example, in 2004 described

private equity, mainly leveraged buyouts (LBOs), as the new king of capitalism (The

Economist, 2004). Some might say that the attention is questionable but in the light of

tremendous growth in amount and volume in this kind of activities the attention is

justifiable. Between 2003 and 2007 private equity investments totaled $832 billion,

which was equal to the size of Mexico and India´s GDP´s at that time (Cendrowski

et.al. 2008). The rise of the private equity market in the years after 2000 has been

attributed among other things to the comparatively low interest rates almost

worldwide, the rise of the hedge funds and the sovereign wealth funds. It has also

been attributed to the idea of the superior governance model of private equity relative

to the public companies (Jensen, Eclipse of the Public Corporation, 1989). Due to the

financial and economic shock in 2008 there has been a significant slowdown both in

investments in PE funds and also in the activity of the funds. Figure 1 shows the

evolution of European private equity investments since 2000 both in terms of volume

and companies financed. The investments in 2009 amounted 23,4 billion euros, down

57% from the year before (EVCA, 2010).

(Source: Figure 9, EVCA, 2010, p.17)

Figure 1: PE investments in volume 2000-2009

2

The increasing volume in this segment of the financial market for the last decades is

interesting and is worth further exploration. In this study I will go carefully through

what Private Equity is and try to detect the value generating activities the PE firms

use in order to maximize the gain for the stakeholders. In order to combine theory and

practice I will use as an example of two well-known private equity takeovers,

the EQT Partners and Goldman Sachs Capital Partners takeover of ISS and Nordic

Telephone Company ApS (NTC) takeover of TDC. The process in each case will be

compared with its peers and changes in the capital structure and operational

performance will be studied. The last chapter will discuss how PE firms are able to

exit from their investments, in order to put that in context I will investigate the recent

IPO of the Danish jewelry marker Pandora.

The aim of this thesis is to obtain comprehensive knowledge of Private Equity, how it

is structured and how firms in this field of investing manage to create value within

their portfolio companies. This is an exploratory thesis with the fundamental goal to

develop a better understanding of corporate finance and private equity investments by

analyzing the key factors in the value generating process. To be able to get a deeper

understanding of the PE market, an analysis is made on the key theories behind the

ideology of PE investments.

In a research by Berg & Gottschalg (2005) they point out six areas where PE funds

create value: financial arbitrage, financial engineering (The optimization of capital

structure), increasing operational effectiveness, increasing strategic distinctiveness,

reducing agency costs, mentoring (parenting advantage).

These points will be observed with a special attention on the PE funds approach to

reduce the agency cost and optimization of the capital structure

With this in mind the problem statement of this thesis will be:

• How do private equity firms create value in their portfolio companies?

o The effect of capital structure changes in value creation

In order to answer this question I will study other questions like: What is private

equity? How is it combined and who owns PE funds? What value generating activities

can the funds use? How does PE funds exit from their investments?

3

1.1 Motivation

The motivation for this thesis comes from a deep interest in this subject, which has

not been discussed much in my study. Private equity has a huge impact on global

trade and today especially in my home country Iceland, were currency restrictions, a

paralyzed stock market and an overbought bond market, have directed investors into

putting more focus on private equity investments. The Icelandic government is also

quite heavily dependent on one of the Danish private equity investment, Pandora. In

the autumn of 2008, the Central Bank of Iceland (CBI) lent the former owner of FIH

Erhvervsbank (FIH), Kaupthing Bank, 500 million Euros, with the assets of FIH as a

collateral. When Kaupthing Bank went bankrupt in October 2008, the CBI took over

the control of FIH. In September 2010, CBI sold FIH to Danish and Swedish investors

that paid less than half of the price in cash. The reminders of the price are based on

FIH´s operational efficiency and also on the final value of the private equity fund

Axcel III (owned by FIH). The fund´s biggest investment is 57,4% of the Pandora

shares.

With this in mind I decided to take on this subject to get more knowledge and

experience in this field.

1.2 Methodology and structure of the thesis

Figure 2 here below illustrates the thesis structure. It is basically in three parts, the

first part is surrounded by the theoretical discussions, the second part is dedicated to

private equity in general and the third part attempts to put the previous discussions in

context.

Figure 2: Thesis structure

Introduc*on, mo*va*on, structure and methodology

Theore*cal framework Agency

problem theory Capital structure

theory

Private Equity in general, and the investment

process

Prac*cal examples

• ISS • TDC

Exit strategies • The IPO of Pandora

Conclusion

4

In part one the theories relevant to private equity are identified and discussed by

reviewing the existing literature in this field. The main theories considered are the

ones that are related to the capital structure and the agency cost. The second part of

the thesis is dedicated to broad private equity discussions. It starts by going generally

through what the phenomenon is and how it is structured. Then the investment

process will be reviewed and different types of buyouts introduced. The main share of

this part is however consideration of the factors that are thought of being value

creating in private equity investments. Part three represents two quite recent private

equity investments, the takeover of ISS A/S and TDC A/S. The focus of this part is to

put previously discussed theoretical points in context by studying the development in

the companies´ capital structure and operational performance before and after the

private equity funds invested in them. The last chapter will focus on exit strategies for

PE investments and the important elements that have to be kept in mind at this stage

in the process. The very recent IPO of the Danish jewelry maker Pandora will be

investigated in in order to put discussions in this chapter into context.

The sources used for the thesis are more or less secondary and acknowledged

academic literature within the subject of corporate finance in general. The data used

for calculations in the case comparison were collected through the Orbis1 database,

which can be accessed on campus. Orbis is a database of financial information for

over 60 million companies around the world. The companies´ consolidated financial

statements were also used when that was needed.

In relation to the last chapter of the thesis, the discussion on Pandora, Torben

Ballegaard Sørensen, the former chairman of Pandora´s board and now Deputy

Chairman, was very helpful and kindly answered few questions for me about the IPO

process and his view on private equity firms contribution to value creation.

1 http://www.bvdinfo.com/Products/Company-Information/International/ORBIS.aspx 2 http://www.blackstone.com/ 3 http://carlyle.com/ 4 http://www.kkr.com/ 5 Closed end refers to the system of the fund. Investors cannot withdraw their amounts

5

1.3 Limitations

In order to keep focus in answering the problem statement questions, a number of

limitations should be put forward.

This thesis puts emphasis on discussions of the value creation of a private equity fund

acquiring a major stake in a LBO of a publicly listed company. Other kinds of

alternative investments such as venture capital are not explored. The discussion in this

thesis also focuses more on the relationship between the private equity fund and the

portfolio companies rather than detailed technical analysis of the function of the

private equity funds itself, that could be a subject of a whole another thesis.

Chapter 4 is used to put theories and discussions into perspective, the cases of TDC

and ISS are used as explanatory examples of how certain ratios changes in the process

of being taken over by a PE fund. In order to calculate the ratios, the financial

statements of the companies were used but they were not reformulated.

This thesis is explanatory and as such it does not claim to be an exhaustive analysis of

the private equity phenomenon, it rather tries to throw light onto private equity and

the value creating activities employed by the PE funds in the portfolio firm operations.

It is also worth pointing out that the phrases PE firms, PE company and PE funds will

be used interchangeably through the thesis

6

2. Literature Review

2.1 Private equity & Capital structure

Reviews of the theories of optimal capital structure always start with the revolutionary

work of Modigliani and Miller (MM) (1958, 1963). They proved that in perfect

capital markets, the choice between debt and equity financing has no material effects

on the value of the firm or on the cost of capital.

The conditions that M&M referred to, as perfect capital markets were:

• Capital markets are frictionless

• Individuals can borrow and lend at the risk-free rate

• There are no costs to bankruptcy or to business disruption

• Firms issue only two types of claims: risk-free debt and risky equity

• All firms are assumed to be in the same risk class (operating risk)

• There are no taxes associated with security trading

• All cash flows are perpetuities (i.e. no growth)

• Operating cash flows are completely unaffected by changes in capital structure

Under these conditions, MM demonstrated the following result regarding the role of

capital structure in determining firm value:

MM Proposition I: In a perfect capital market, the total value of a firm is

equal to the market value of the total cash flow generated by its assets and

is not affected by its choice of capital structure (Berk & DeMarzo, 2007,

p.432).

Proposition II is derived from Proposition I and concerns the rate of return on equity:

MM Proposition II: The cost of capital of levered equity is equal to the

cost of capital of unlevered equity plus a premium that is proportional to

the market value debt-equity ratio (Berk & DeMarzo, 2007, p.438)

MM´s original work assumed a zero corporate tax rate. In 1963, they published a

second article, which included corporate tax effects. With corporate income taxes,

they conclude that leverage will increase a firm´s value, because interest on debt is a

7

tax-deductible expense, which lead to more of a leveraged firm´s operating income

flows through to investors. From it derives the conclusion that firms should use 100%

debt financing (Modigliani & Miller, 1963).

As one could imagine MM statements caused robust reaction from dozens of other

academics (e.g. Durand, 1959). Myers and Robichek (1966) concluded that the

assumptions behind Proposition I would not hold in the world assumed by MM. They

hypothesized that in the absence of taxes, the value of the firm would not change for

moderate amount of debt but would decline with high degree of leverage (Myers &

Robichek, 1966).

Jensen (1993) states that even though MM assumptions have been very productive in

helping the financial community to structure the logic of many valuation issues, “The

1980s control activities, however, have demonstrated that the MM theorems (while

logically sound) are empirically incorrect” (Jensen, 1993, p.878). Other researchers

have pointed out that evidence from e.g. LBOs have shown that leverage, payout

policy and ownership structure do matter when considering organizational efficiency

and therefore value (e.g. (Kaplan 1989) (Smith, 1990)). Brigham and Ehrhardt (2010)

supposed that Modigliani-Miller (MM) were theoretically right but in reality the cost

of bankruptcy exists and is directly proportional to the debt level of the firm.

Jensen (1986) discusses the importance of debt in the capital structure. From his point

of view debt can and should be used as a corporate governance tool. He argues that

managers are afraid of paying out the extra cash flow because the stock market

punishes dividend payments with stock reduction. In order to prevent the managers

from investing in projects with negative NPV, the firm should take on additional debt

that the extra cash flow would be used to pay down. He sees this use of debt as a

potential determinant of capital structure. Muscarella and Vetsuypens (1990)

reviewed reverse LBO´s and found that firms experience dramatic increase in

leverage at the LBO but the leverage ratios were gradually reduced over time.

Axelson et al. (2007) conducted an analysis of the financial structure in large buyouts.

They found no relation between leverage in their sample of buyouts and comparable

public firms. Their results suggest that capital structure in buyouts requires a different

explanation than in public firms.

8

Myers and Majluf (1984) recommend that firms should use debt financing rather than

equity financing when possible because of the information asymmetry costs. They

argue that when managers have superior information and go for an equity issue, the

stock price will fall but if the company issues safer debt such as bonds, the stock price

will not fall.

In relation to the discussions above about the different angles of the theories around

the capital structure it is interesting that in a survey by Graham and Harvey (2001),

they found that financial executives are not likely to follow the academically

proscribed factors and theories when determining capital structure. In light of this, it

will be exciting to see later on in this thesis if this is the case.

2.2 Private equity & Agency theory

The origin of the agency theory can be linked to the famous social philosopher and

economist Adam Smith. In 1776 he came up with this definition of the relationship

between owners of companies and their managers:

“The directors of such (joint-stock) companies, however, being the

managers rather of other people´s money than of their own, it cannot well

be expected, that they should watch over it with the same anxious vigilance

with which the partners in a private copartnery frequently watch over their

own. Like the stewards of a rich man, they are apt to consider attention to

small matters as not for their master´s honor, and very easily give

themselves a dispensation from having it. Negligence and profusion

therefore must always prevail, more or less, in the management of the

affairs of such company.”

(Quotation adapted from Jensen & Meckling, 1976)

Jensen and Meckling (1976) formalized this view from Adam Smith and in their

paper they conclude that the agent cannot at all times guarantee that he will make

optimal decisions from the owner´s point of view. According to Jensen and Meckling

agency costs of equity are defined as:

9

1. The monitoring expenditures by the principal

2. The bonding expenditures by the agent

3. The residual loss

Monitoring include efforts on behalf of the owner to control the behavior of the agent

to increase the alignment of interest between the agent and the owner. Among the

monitoring activities that the owner can use are budget restrictions, compensation

policies and operating rules (Jensen & Meckling, 1976). Jensen and Meckling

describe bonding as an action carried out by the agent “to expend resources (bonding

costs) to guarantee that he will not take certain actions which would harm the

principal or to ensure that the principal will be compensated if he does take such

actions” (Jensen & Meckling, 1976, p. 5). The costs related to bonding could be an

internal audit showing that the agent is acting in the interest of the principal. Residual

loss is defined as any reduction in welfare from the viewpoint of the owner that could

be related to the conflict between the agents decisions and the maximum gain for the

owner (Jensen & Meckling, 1976). Demsetz (1983) on the other hand concluded that

it would not be possible to expect any relation between ownership structure and

profitability (Demsetz, 1983).

According to Milgrom and Roberts (1992) one of the most important things in

relation to the Agency Theory is to align the interest between the owner (shareholder)

and the agent in order to reach the firm´s goals in an environment of uncertainty

(Milgrom & Roberts, 1992).

Jensen and Meckling (1976) distinguish between two approaches of the Agency

Theory, the normative and the positive. The normative aspect is mainly about how to

structure the contractual relation between the principal and the agent in order to

provide appropriate incentives for the agent to make choices that will maximize the

principal´s welfare. The positive theory is what Jensen and Meckling focus almost

entirely on. The aim of that approach is to identify a policy or behavior to merge debt

and equity holders’ interests with management and then to demonstrate how

information systems or outcome-based incentives solve the agency problem.

According to Renneboog & Simons (2005), the basics of the agency theory includes

three primary hypotheses regarding the motives of public to private transactions:

10

• Incentive realignment

• Control

• Free cash flow

The incentive realignment hypothesis states that the gains in stockholder wealth that

arise from going private are a result of offering more rewards for managers that

encourage them to act in line with the interests of the owners. The incentives could

e.g. take the form of increased ownership stake. The hypothesis of control argues that

successful implementation of supervision system by the management plays a critical

role for the shareholders wealth. The free cash flow hypothesis suggests that firms

should take on additional debt in order to force managers to pay out free cash flows.

The added leverage prevents managers from growing the firm beyond its optimal size

and at the expense of value creation (Renneboog & Simons, 2005).

Vinten (2007), on the contrary, points out that this kind of actions might lead to over-

monitoring by the large shareholder, which could reduce firm efficiency because of

poorer firm innovation. On top of that, huge debt burden might dampen the

managerial initiatives because the free cash flow now only serves the repayments on

the cost of investments in new firm activities (Vinten, 2007).

In a survey by Shleifer & Vishny (1997) they identify incentive contracts as a possible

solution for owners to get the managers to invest the investor´s capital in the most

optimal way. According to Lewellen et al (1985) negative returns are most common

for bidders in mergers and acquisitions activities where their managers hold little

equity, suggesting that agency problems can be enhanced with incentives.

Kaplan (1989) performed a study of 76 large public companies that went through

management buyout (MBO) between 1980 and 1986. He found that within 3 years

from the buyout, the companies increased their operating income and net cash flow.

He connected these operating changes to improved incentives rather than layoffs or

managerial exploitation of shareholders through inside information. These results

support that agency cost savings from better control and incentives lead to

improvement in the company´s performance. The results are in line with related

studies from Muscarella & Vetsuypens (1990) and Smith (1990).

11

Leslie & Oyer (2009) on the other hand raise question about whether incentives are

able to create value. Their study showed that companies owned by PE firms

implement much stonger incentives system for their top executives but they could not

find much evidence of these companies outperforming public firms in profitability or

operational efficiency (Leslie & Oyer, 2009).

3. Private Equity

In the following section a description of

the various aspects of private equity will

be provided in order to give the reader

insight to this particular asset class. First

there will a brief definition of private

equity, followed by a discussion of the

ownership structure and the investment

process, i.e. the fundraising and the

financing structure. Then different kinds

of buyouts will be introduced and the last

part of this chapter will then be dedicated to the value generating process of private

equity investments.

3.1 Definition

Investments in asset classes can roughly be divided between traditional and

alternative assets. The traditional ones are in most cases more liquid and easier to

understand than the alternatives one. Private equity investments are considered to be

alternative investments and suits investors that consider a longer investment horizon.

12

(Source: figure 1.2 Demaria, 2010, p.17)

Figure 3: Simplified categorization of financial assets

The concept of private equity contains different investment approaches such as

management buy-outs and buy-ins, venture capital, and development capital.

Furthermore, the investment strategies of different private equity companies differ

extremely according to their investment criteria, such as acquisition size, sector,

region, and purpose of the acquisition, which e.g. includes start-up, expansion,

buyouts and turnarounds. However, as can be seen in figure 4 the majority of funds

placed in private equity are invested in leveraged buyouts (LBOs), so referring to

private equity is often implicitly LBOs (Philippou & Zollo, 2005).

(Source: EVCA, 2010, p.19)

Figure 4: Average Private Equity investment size 2007-2009

Assets

Traditional

Bonds Stocks

Specialized products

Alternative

Hedge funds PRIVATE EQUITY

Real estate Commodities, Art, etc

13

In a leveraged buyout, a specialized investment firm using a relatively small portion

of equity and a relatively large portion of outside debt financing acquires a company.

The leveraged buyout investment companies today refer to themselves as private

equity firms. In a typical leveraged buyout transaction, the private equity firm buys

majority control of an existing or mature firm and brings in their own people in board

and even into the management team. This arrangement is different from venture

capital firms that typically invest in young or emerging companies, and typically do

not obtain majority control (Kaplan & Strömberg, 2008). The focus in this thesis will

be on private equity firms and the leveraged buyouts in which they invest.

Demaria (2010) supposed that because PE firms’ investment cycles are substantially

longer and the cycles are not correlated directly to the evolution of the stock exchange

index, investors in private equity were looking for diversification and return

enhancement. But as was also pointed out there is a close link to the markets, as exists

of investments are mainly trade sales or initial public offerings (IPOs). If markets are

in downturn, public companies will make fewer acquisitions or will negotiate lower

valuations and IPOs could turn out to be very negative. Private equity is also affected

by the interest rates because of the huge amount of debt borrowed in the buyout. The

higher the interest rates, the more difficult it is for a PE firm to transform a buyout

into a profit. (Demaria, 2010)

3.2 Structure

The classic private equity firm is organized as a partnership or limited liability

corporation. Jensen (1989) argued that private equity associations were more

decentralized than public companies with fairly few investment professionals. In a

survey of 7 PE firms he found that they had only on average 13 professionals with an

investment banking background (Jensen, 1989). This has changed a bit for last years

as the PE firms have become larger but they are though still relatively small in

relation to their investments. Among the biggest firms in the world today are

Blackstone2, Carlyle3 and KKR4.

2 http://www.blackstone.com/ 3 http://carlyle.com/ 4 http://www.kkr.com/

14

The Private equity firm raises capital through a private equity fund. These funds are

structured as “closed end”5 funds in which investors commit to providing a certain

amount of money into the fund. The PE firm serves as the general partner (GP) and

manages the fund, the investor is referred to as the limited partner (LP). The PE funds

are usually created for a 10-year life span, with option of an extension. These 10 years

are then subdivided into an investment period of 5 years and a divestment period of 5

years (Demaria, 2010).

Figure 5: Private equity fund lifecycle (own creation)

In the first period of the funds life cycle the fund managers structure the fund,

introduce the business plan and strategy for investors. The investors then commit

capital to the new established fund if they believe in the management ideas. When all

necessary observation such as due diligence has been made on the target firm and

participants have negotiated the price, a capital call is made, i.e. the investors are at

this time asked to lay out their committed capital. These capital calls can be made

more than once. For example, the agreement between the buyer and the seller can be

structured in that way that payments are made in separated parts over longer period.

After the investment process has taken place the strategic, organizational and

operational changes can be made to the target firm in the so-called holding period. At

this time in the cycle there is room for operational improvements and value creation

5 Closed end refers to the system of the fund. Investors cannot withdraw their amounts until the fund is terminated.

PE fund established

Fund raising by the GP -LP´s joins the fund

Searching period

Capital Call made by GP -

paid by LP

Investment period

Holding/Restructuring

period

Disinvestment period/Focus on

portfolio firm

Harvest/Exit

15

within the portfolio company. The latest stage is the harvest or the exit of the

investment. This marks the end of the LBO investment and is an important stage in

the process since the investors will ultimately realize the returns from their investment

(Berg & Gottschalg, 2005). The exits can be of different modes that will be further

discussed later in the thesis.

3.3 Investment Process (Fundraising – structuring the finance)

In their search for potential buyout targets, the GPs look for firms with strong, stable

cash flows, market leadership and a low leverage ratio relative to industry peers. A

rather famous phrase in the field of finance is “cash is king”, that is especially true in

the case of leverage buyouts, as the cash flow is used to service the debt raised in the

deal (Cendrowski, Martin, Petro, & Wadecki, 2008).

One of the most important topics for the PE fund is the fundraising. If this stage turns

out to be unsuccessful it can have serious consequences on the investment and in

some instances might prevent the fund from going further in the investment process.

The limited partners (LPs) put up the majority of the equity part but the GP also

contribute some capital. Good track record is vital in this perspective. Funds that have

been able to generate good returns in the past have definitely competitive advantage

to others (Demaria, 2010). One might describe this as the situation when a Danish guy,

Peter L, is going to invite a stand-up comedian to his party. He knows that he can get

Casper Christiansen but his Icelandic friend also told him about a famous Icelandic

comedian named Laddi that would come for free to escape the situation in Iceland.

Peter knows that his safest bet would be the Danish performer but he is also expensive,

so it is tempting to try the Icelandic one. Although Peter is tempted his safest choice

would be the Danish performer. This example shows that although one is tempted to

go for a new PE fund, he might still invest in a fund managed by a tried-and-true GP.

After the fundraising process, than the GP takes full control of the fund and starts to

invest. The limited partners (LPs) have nothing to say in all the investment process,

which is also important because of their limited liability. A golden rule of private

equity fund is that those who are responsible for the investment process should be

members of the full-time executive team (Fraser-Sampson, 2007).

16

Incentives and fees

Figure 6 provides a view of the cash flow in private equity funds. The General partner

(GP) gets paid a management fee from the fund for the service he provides. The fee is

generally 1,5% to 2,5% per year depending on the fund size. This fee is calculated on

the fund size during the investment period, and usually on the net asset value of the

portfolio once the investment period has ended. In order to align the interest between

limited partners and the management team, a fee in form of carried interest is paid to

the management team. That fee is based on the performance of the fund and is around

20%. However, as the investors carry more risk than management team, than before

anything else is paid out of the fund, the investors are first compensated with a so-

called hurdle rate, which is between 5 and 15% (Demaria, 2010).

(Source: Figure 3.6 Demaria, 2010, p.55)

Figure 6: Cash flows in private equity investments

3.3.1 Debt forms

The use of debt financing is what most obviously distinguishes buyouts from other

transactions such as venture investments. Buyouts are often structurally very complex,

with many different layers of debt, were often the key buyout skills lay. The buyout is

typically financed with 60-90% debt, which explains the term leveraged buyout

(Kaplan & Strömberg, 2008). One of the key barriers to entry for new buyout firms is

to obtain as good terms from banks as the established players (Fraser-Sampson, 2007).

17

The typical debt structure almost always includes a portion of senior and secured

loans that are provided by a bank and also layers of junior and mezzanine debt.

(Source: Spliid, 2007, p.31)

Figure 7: Typical capital structure in LBOs

3.3.2 Existing debt

This part is often overlooked when observing PE activities. These are the debts that

are already present in the firm for the working capital purposes. Companies with high

levels of operating debt are less attractive as buyout targets. But on the other hand,

firms with low levels of debt and even a cash stack will be highly attractive. Buyout

firms typically seek to reduce the level of operating debt within a business once they

have acquired it. Operating debt finances the working capital cycle, so lowering the

stock levels can reduce the debt, also fewer debtor days or the opposite, by adding

more creditor days. Firms with a low operating debt might persuade a bank to issue

more debt in the acquisition so that equity can be released back to the buyout fund as

part of recapitalization (Fraser-Sampson, 2007).

3.3.3 Senior debt

Senior debt is a first priority debt in repayment in any liquidation of the company. It

has a greater seniority in the issuer´s capital structure than subordinated debt and is

often secured by collateral (Fraser-Sampson, 2007). Senior debts are issued in various

loan types (tranches) according to risk/return profile, repayments conditions and

maturity. For example as shown in figure 7, tranche A is the safest type of debt,

featuring a fixed amortization plan. Tranche B and C are lower-grade loans, based on

bullet payment structure. Debt tranches with bullet payments allow target companies

to take on higher debt multiples, as the payments will be made at the end of the loan

Financing Senior loans > > Mezzanine loans > > Equity and shareholders loans

Percent of capital structure 45-65 10 to 20 25-40

Expected return Euribor + 1,75-3,25% Euribor + 9-13% 15-30% (IRR)Leverage 4-5 x EBITDA 5-6 x EBITDA > 6 x EBITDA

A: Amortization 7 years Bullet loanB: Bullet loan 8 yearsC: Bullet loan 9 years

Typical capital structure in LBOs

Repayment profile

18

period, so there is a kind of payment relief in the beginning. But it does not come

without a cost, since the bullet loans carry higher interest rates. (Spliid, 2007)

3.3.4 Mezzanine debt

Mezzanine financing represents capital with a level of risk, which is positioned in the

gap between senior debt and equity. This kind of financing is junior to senior debt and

takes the form of subordinated notes from the private placement market or high yield

bonds from the public market. Due to its popularity, special mezzanine financing

funds have been raised to operate in this space (Fraser-Sampson, 2007).

Mezzanine finance is by nature cash flow lending but sometimes the lenders are

secured with operating assets in case of insolvency. This kind of debt obviously bear

higher interest rate then are paid on senior debt. Often it includes some form of equity

“kicker” in order to allow the mezzanine investor to participate in the upside of the

equity value and to compensate them for the risk taken. The existence of this kind of

financing allows PE firms to secure a gap in the financing of the deal at a price that is

less than pure equity and allows them to keep full majority control of their businesses

(Cendrowski, Martin, Petro, & Wadecki, 2008).

3.4 Types of buyouts

There is a great deal of overlap in the definitions of different buyouts. The discussion

so far has been centered on leveraged buyouts (LBOs) but certainly there are more

types. This section will try to distinguish further between these forms and definitions

of them.

3.4.1 LBO

Leveraged buyout can be defined as an acquisition of a company by an investor or

group of investors with a significant amount of the price paid by borrowed money.

The cash flow generated in the acquired firm or procedures from asset sale is then

used to pay down the massive debt. The assets of the acquired company are though

almost always used as collateral for the debt structure (Demaria, 2010). In the 1980´s

leveraged buyouts first arose as an important phenomenon due to its increased activity.

Famously, Jensen (1989) predicted that the leveraged buyouts would become the

19

dominant corporate organizational form in the future. He argued that the structure of

the PE firms were superior to those of the typical public corporations because of their

combined form of highly leveraged capital structures, concentrated ownership,

incentive systems and efficient organizations with a low overhead costs (Jensen,

1989). In a sense it can be said that all buyouts are leverage buyouts (LBOs) since all

buyouts involve use of some debt, just at different quantity.

3.4.2 MBO

Management buyout (MBO) in its purest form involves the executive team who are

managing a particular business activity, buying it out from the parent company. This

form of buyouts was especially popular in the early to mid 1990s. This method

requires the management team to put its own money into the deal but with a reward of

an equity stake. With larger funds and bigger deals, this method has become less

common (Fraser-Sampson, 2007).

3.4.3 MBI

Management buy-in developed from the MBO and is similar method apart from the

way in which the deal initially comes together. The key difference is that instead of

the management team of a business getting together to buy it, a team is put together to

buy another company operating in the same sector. Pure MBIs are rare and often fall

into the BIMBO category (Fraser-Sampson, 2007).

3.4.4 BIMBO

Buy-in management buyout occurs where outside executives join the existing

executive team to buyout a company. Much of the buyout activity falls into this

category if one applies the definition strictly. An example of this could be a former

CEO that returns to advice and help in the acquisition process (Fraser-Sampson,

2007).

3.4.5 PIPE

Private investment in public equity is a category of deals that occurs when a particular

investment instrument is created within á public company that may offer a private

equity-type return. Typically, while the company´s equity is quoted the instrument

20

itself is not. An example of this could be a private investments firm or mutual fund

that purchases firm´s equity at discount to current market value for the purpose of

raising the firm´s capital. This is called traditional PIPE and the stock equity could be

either preferred or common. Structured PIPE refers to the issue of convertible debt for

the same purpose (Fraser-Sampson, 2007).

3.5 Value drivers of PE funds

Demaria (2010) recommends that when value creation in firms is analyzed one should

put emphasis on the structure, execution and the exit of the deal. The reason behind

investments in PE funds it that they are believed to have the X factor to generate value

within their investments beyond others.

This section will discuss the various value generating activities that PE funds

undertake in their investments. Berg & Gottschalg (2005) and Renneboog & Simmons

(2005) made a comprehensive contribution to the literature in this field of PE

investments and this section will depart from their studies.

In order for PE funds to reach their goal they have to exploit the value creation

opportunities laying in their investments. Berg & Gottschalg (2005) introduced three-

dimensional framework to analyse the factors behind value creation in LBOs either

within the portfolio company or through the interaction between the portfolio

company and the PE fund.

In both studies by Berg & Gottschalg (2005) and Renneboog & Simons (2005) a

distinction is made between value capturing and value creation in PTP buyouts. Value

capturing refers to activities that increase the value without changing anything in the

underlying performance of the business e.g. financial arbitrage, breaking up of

companies or improvements in the macroeconomic environment. Value creation on

the other hand takes place in the holding period or during the PE ownership of the

company and refers to the improvement of performance of the portfolio companies.

These improvements can be further divided into primary (direct) value creation, e.g.

the ones that are easy to measure on the portfolio company´s performance or

operations, and secondary (indirect) value creation, which refers to events that are

21

harder to measure but have an influence on value generation, such as benefits of

reduced agency costs. Figure 8 gives an overview of the various factors behind value

generation in LBOs as discussed by Berg & Gottschalg (2005).

Figure 8: Factors behind value generation in LBOs (own creation)

3.5.1 Value capturing

3.5.1.1 Financial arbitrage

According to the classical world that Modigliani and Miller among others belong to,

arbitrage opportunities should not exist if markets are efficient. However, market

conditions such as information asymmetry distract this picture of the perfect market

(Berk & DeMarzo, 2007). It is therefore possible for PE funds to find an investment

opportunity where value can be generated between the buyout and the divestment

without operational changes within the portfolio company.

According to Berg & Gottschalg (2005) the financial arbitrage can be based on four

factors:

Value genera*on in buyouts

Value crea*on

Primary levers

Financial engineering

Op*mizing capital structure

Reducing corporate tax

Opera*onal effec*veness

Cost cuJng and margin

imporvements

Reducing capital requirements

Removing managerial inefficiencies

Strategic dis*nc*veness

Secondary levers

Reducing agency costs

Of free cash flow

Improving incen*ve alignment

Improving mentoring and controlling

Mentoring

Restoring entrepreneural

spirit

Advising and enabling

Value capturing

Financial arbitrage

Based on change in market valua*on

Based on private info about

porOolio firm

Through superior market

info

Through op*miza*on of corporate scope

22

• Changes in market valuation – An example of this is so called “Multiple

riding”, i.e. when investor takes company private because he expects the

valuation based on public multiples to rise.

• Private information - For example information asymmetries in management

buyouts (MBOs).

• Different expectations regarding the future performance of the business or the

industry

• Superior deal making capabilities – For example, clever firms that managed to

limit competition from other firms and are therefore able to get better deal.

Renneboog and Simmons (2005) explained value capturing with the undervaluation

hypothesis, which suggest that value generated in the public to private process is

based on the management ability to use their knowledge to develop alternative higher-

value use for the companies’ asset´s.

3.5.2 Value creation

3.5.2.1 Primary levers

Changes that are made to the capital structure or the organizational structure in the

portfolio company are referred to as value creation activities. The PE firm can

undertake various restructuring activities within the portfolio company in order to

generate value. Berg & Gottschalg (2005) divided the value creation into primary and

secondary levers where the primary refers to activities that can be directly linked to

improvements in financial, operational and strategic performance of the portfolio

company.

The literature in the field of value creation in buyouts has put a great deal of attention

to the financial engineering i.e. the optimization of the capital structure and the

minimization of cost of capital (Berg & Gottschalg, 2005). This section will try to

bring out the aspects that have been considered to influence the improvements in the

bottom line results of the portfolio companies.

23

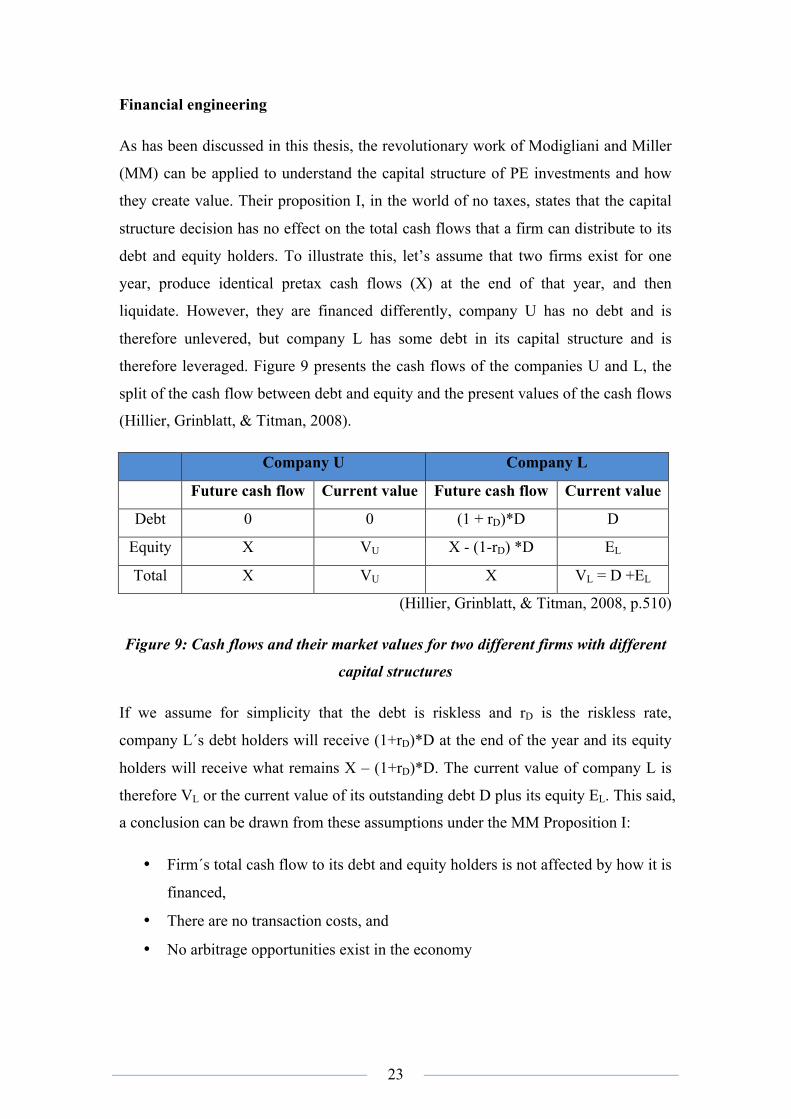

Financial engineering

As has been discussed in this thesis, the revolutionary work of Modigliani and Miller

(MM) can be applied to understand the capital structure of PE investments and how

they create value. Their proposition I, in the world of no taxes, states that the capital

structure decision has no effect on the total cash flows that a firm can distribute to its

debt and equity holders. To illustrate this, let’s assume that two firms exist for one

year, produce identical pretax cash flows (X) at the end of that year, and then

liquidate. However, they are financed differently, company U has no debt and is

therefore unlevered, but company L has some debt in its capital structure and is

therefore leveraged. Figure 9 presents the cash flows of the companies U and L, the

split of the cash flow between debt and equity and the present values of the cash flows

(Hillier, Grinblatt, & Titman, 2008).

Company U Company L

Future cash flow Current value Future cash flow Current value

Debt 0 0 (1 + rD)*D D

Equity X VU X - (1-rD) *D EL

Total X VU X VL = D +EL

(Hillier, Grinblatt, & Titman, 2008, p.510)

Figure 9: Cash flows and their market values for two different firms with different

capital structures

If we assume for simplicity that the debt is riskless and rD is the riskless rate,

company L´s debt holders will receive (1+rD)*D at the end of the year and its equity

holders will receive what remains X – (1+rD)*D. The current value of company L is

therefore VL or the current value of its outstanding debt D plus its equity EL. This said,

a conclusion can be drawn from these assumptions under the MM Proposition I:

• Firm´s total cash flow to its debt and equity holders is not affected by how it is

financed,

• There are no transaction costs, and

• No arbitrage opportunities exist in the economy

24

Then the value of a company is maintained regardless of the nature of the claims

against it. Thus the value is determined on the left side of the balance sheet by real

assets, not by the company´s leverage ratio.

Proposition II states that cost of equity depends on three factors

• The required rate of return on the company´s assets (RA)

• The company´s cost of debt (RD), and

• The company´s debt to equity ratio (D/E)

The 1958 theory as has been discussed was highly hypothetical. But in 1963 they

introduced corporate tax, which moved their theory closer to reality. Cost of debt is

under these circumstances calculated on an after tax basis as interest payments are

now tax deductible.

Hence, under the assumptions behind Proposition I mentioned above plus an extra

assumption that no personal taxes exist, then the value of a levered firm with risk-free

perpetual debt is the value of an otherwise equivalent unlevered firm plus the present

value of the tax shield. Therefore the firm´s optimal capital structure will include

enough debt to completely eliminate the firm´s tax liabilities (Hillier, Grinblatt, &

Titman, 2008).

However, although markets may work semi-efficiently after MM assumptions, they

are certainly not perfect and costs of financial distress exist. Costs of financial distress

depend on the probability of default and the magnitude of the costs. Proposition II

argues that the expected return on equity of a levered firm increases linearly with the

debt to equity ratio, as long as debt is risk-free. Nevertheless, as figure 10 visualizes,

when debt increases so does the risk of financial distress and debt holders demand

higher return for the additional risk that they carry. The more debt present, the less

sensitive equity holders become to further borrowing, hence the slope of RE slows

down as the ratio debt to equity increases (Brealey & Myers, 2003).

25

(Source: figure 17.2 in Brealey & Myers, 2003, p.474)

Figure 10: Debt to equity and cost of financial distress

This may seem to contradict Proposition I, which argued that the capital

structure is irrelevant. But as can be seen on the figure there is a risk-return

trade-off. Any increase in the expected return is exactly offset by an increase in

risk and therefore in shareholder´s required rate of return. The required return

simply rises to match the increased risk.

The trade-off theory helps to understand the choice of capital structure. It

suggests that the debt to equity decision relies on a balance between the tax

shield and the cost of financial distress. This explains why target debt ratios may

vary from firm to firm as companies with safe, tangible assets and steady cash

flow can better handle higher debt ratios. The theory also helps to explain what

kind of companies’ goes private in LBO´s. Because of the leverage factor in the

LBO´s, the target companies for the takeovers are usually mature with

established markets, strong cash flow and low debt to equity ratio. That makes

sense according to the trade-off theory since they are exactly the kind of

companies that “should” have high debt ratios (Koller, Goedhart, & Wessels,

2010).

Figure 11 shows how the trade-off between the tax-benefits, improved discipline

and the costs of distress are relevant elements when determining the optimal

capital structure. At some point, the risk of financial distress increases rapidly

with additional borrowing and the cost of financial distress begin to take a

26

substantial bite out of the firm value. Thus, the benefits from debt may be more

than offset by the financial distress cost.

(Source: Exhibit 23.1 Koller, Goedhart, & Wessels, 2010, p.478)

Figure 11: Tax shield and financial distress costs

Berg & Gottschalg (2005) pointed out that PE firms in power of their extensive

knowledge and experience of capital markets are able to help their portfolio

companies to optimize their capital structure, for example by reducing the cost of debt.

PE firm with good track records and reputation usually has better access to capital and

often at better terms than firm that either is unknown or with bad reputation.

Renneboog & Simons (2005) discussed how value could be created for the

stockholders by transferring wealth from the bondholders. From their point of view it

is possible for companies to do so in three ways: by increasing risk in investments, by

increasing the dividend payments and by issuing debt with higher or equal seniority of

the outstanding ones. They also mention that although this wealth expropriation

theory has not gained convincing evidence in the empirical researches so far, then

some studies show that companies, which have gone through public-to-private

transactions, faced substantial debt downgrades by the rating agencies (Renneboog &

Simons, 2005).

Koller et al (2010) indicate that financial engineering can create value in three ways;

• With derivative instruments that transfer company risk to third parties, such as

forwards, swaps and options.

27

• Off-balance sheet financing that detaches funding from the company´s credit

risk and often exploit tax advantages, for example leases and securitization.

An example of securitization could be of a distressed company in the car

industry that managed to “pack” their receivables and sell to investors at better

terms than otherwise possible if the company either issued bonds or asked for

traditional bank loan.

• Hybrid financing that offers new risk-return financing combinations. For

example convertible debt, this kind of financing might be used when a great

distinction exists between management and lenders about company´s credit

risk. Creditor might be tempted to finance a company at more reasonable

terms because of the warrant included in the structure, so the debt part of the

structure is, for the lender, not the most attractive but rather the warrant

component (Koller, Goedhart, & Wessels, 2010).

Sub-conclusion

As has been discussed above, Modigliani and Miller (MM) assumed that when

corporate taxes are included and the interest on debt is deductible (tax shield), than

firm’s optimal capital structure should be 100% debt. That was built on the idea that

the value of the company increased with the amount of debt because of the

exploitation of the tax shield that improved the cash flow to investors. But as was then

pointed out, the existence of financial distress cost makes this picture biased and a

balance is needed to realize the benefits of the tax shield. According to Kaplan

(1989b) tax benefits play an important role for the value creation in buyouts. He

found that in 76 buyouts completed between 1980 and 1986 the value of the tax

benefits ranged 21% to 143% of the premium paid to shareholders (Kaplan S., 1989b).

Optimization of the capital structure and the exploitation of the tax shield do clearly

impact the bottom line results of the portfolio company, but whether these tax benefits

are confined to PE activities is highly questionable. It is very likely that in today’s

competitive environment the former owners have already exploited these tax benefits.

It can therefore be concluded that it is unlikely that PE funds are able to create much

additional value through tax benefits (Renneboog & Simons, 2005). It is more

difficult to conclude something about the wealth transfer hypothesis; the effect of this

value-creating factor is likely to be built on how the covenants behind the bond issues

28

are made. Renneboog & Simmons indicate that bondholders that suffer losses have

simply not been contractually well protected (Renneboog & Simons, 2005).

Operational effectiveness and strategic distinctiveness

As has been discussed earlier the structure of a PE investment can be split into 2 parts,

the second part can be referred to as the holding period where the PE firm can make

its impact on the portfolio firms operations. The PE firm can initiate dozens of things

that can improve the operational results of the portfolio company. Bull (1989)

conducted a study where he compared different accounting variables of companies

before and after LBO and found that the financial performance improved significantly

after the LBO. Berg & Gottschalg (2005) draw attention to number of activities that

PE firms implement in order to reduce cost and capital requirements, such as

tightened control on corporate spending, reduction in production cost, decreased

corporate overhead cost and improvements in working capital. They also point out

that sometimes during the LBO process, the PE firm use the opportunity to dispose of

incompetent management team to get rid of managerial inefficiency (Berg &

Gottschalg, 2005).

In the last couple of years the importance of strategic distinction has become more

prominent as a part of the value creation instruments for PE firms. Their vision often

leads to a strategic change such as, new market entrance, changes in production or

pricing or asset sales. These activities can help the portfolio company to improve their

focus on the financial performance and increase its value (Berg & Gottschalg, 2005).

3.5.2.2 Secondary levers

Berg & Gottschalg defined the secondary levers as: “levers of value creation (that) do

not have a direct impact on financial performance, but influence value creation

through primary levers” (Berg & Gottschalg, 2005, p.24). In this context, the focus of

this section will be on how the PE firms can use their knowledge and experience to

reduce the agency costs within their portfolio company in order to increase their value.

29

Agency cost

Many researchers have identified the reduction of agency costs as a key value driver

in buyouts. Agency cost reflects the conflict of interest between management, owners

and other stakeholders in the firm. The cost results in a loss of efficiency that reduces

the advantage of debt (Brigham & Gapenski, 1990). The root of the agency problem

as has been discussed earlier, is the separation of ownership and control, where the

manager becomes an agent for the owner (Shleifer & Vishny, 1997).

Berg & Gottschalg (2005) specify a few factors that LBOs can influence in order to

reduce the agency cost. For example by increasing debt, the waste of free cash flow

can be limited. Jensen (1989) concluded that debt is a powerful tool for change and

can be used to directly force managers to put all their effort in running the company

efficiently in order to reduce debt. Jensen stated that managers tend to spend the

additional cash flow in projects with negative NPV instead of distributing it to the

shareholders. He argues that companies that take on additional debt keep their spirit

going since they need to refocus on their strategy and structure so they can meet the

debt payments (Jensen, Eclipse of the Public Corporation, 1989). But as has been

discussed and Berg & Gottschalg (2005) draw attention to, the existence of financial

distress costs makes things more complex. High leverage can both cause managers to

drop projects with positive NPV because of risk aversion and caused companies to

overlook good investment opportunities because of stretched budget (Berg &

Gottschalg, 2005).

Incentive alignment and mentoring

The alignment between the management and the shareholders (owners) plays a crucial

role in successful buyouts. Jensen (1989) indicates that PE firms are efficient in

linking management bonuses to cash flow and debt retirement. In many buyouts, the

management team is encouraged to take on equity stake in the company in order to

align their interest with the owners. The argument for this method of reducing the

agency cost is to set the management focus on future strategic performance.

Management tolerance for inefficiency within the firm will also be on the bottom of

the scale and they feel that they are fighting for their own benefits (Muscarella &

30

Vetsuypens, 1990). This is in line with Smith (1990) who conducted a study on 58

Management Buyouts (MBOs) of public companies during the period of 1977 to 1986.

His findings revealed that there exists a positive relationship between management

ownership and the performance of the firm.

Berg & Gottschalg (2005) on the other hand pointed out the contrary, that financial

performance could decline when management ownership soars. This is due to the fact

that increased equity stakes might be of that size that it affected the management’s

personal budget dramatically, which could make them more risk-averse.

One of the characteristics of PE firms is that highly skilled and experienced

professionals with deep knowledge of the financial markets often manage them. How

the PE firm manages to be a mentor for their portfolio companies plays an important

role in whether the buyout will be successful or not. Among the advantages that the

PE firms have are:

• Huge network of financial within the industry and financial institutions that

can be used to get more favorable borrowing terms and also to appoint

experienced board members,

• Experience in running businesses with stretched budget and the awareness of

the importance of selecting top management team to improve the portfolio

companies’ efficiency ((Berg & Gottschalg, 2005) (Jensen, Eclipse of the

Public Corporation, 1989)).

Sub-conclusion

This section has discussed the various factors PE firms can use in order to create

value within the portfolio companies. The debate on private equity has often solely

been about the capital structure changes that are adherent to LBOs. But as has been

reviewed there are other things such as reduction of the agency cost by implementing

incentive systems and strategic changes that have become more and more important

for the value generating process.

31

4. Case comparison

In order to put the theories and discussions revealed in this thesis into perspective it is

interesting to make a connection to the real world. This section will therefore attempt

to do so by exploring two recent PE investment cases, the EQT Partners and Goldman

Sachs Capital Partners takeover of ISS and Nordic Telephone Company ApS (NTC)

takeover of TDC. The intention is to compare changes in the companies´ capital

structure and operational performance with their peer group.

The construction of this section will follow Koller et al. (2010), Penman (2010) and

Vinten (2007) thoughts on multiple analyses. There are a few things that have to be

kept in mind when a multiple comparison analysis is made. First it is important to

build a peer group of comparable firms that have operations similar to the target firm,

secondly, relevant measures within the companies have to be identified to calculate

the multiples and at last it is recommended, to use an average of the multiples used for

the comparison (Penman, 2010). The focus in this part will be on developments of

different ratios of growth, operational performance and capital structure. The peer

group used to compare with ISS was quite difficult to identify since none of their

competitors operate in more than one of ISS´s business areas. I decided to follow

credit analysis from Standard & Poor’s (2006) that defined Compass Group6 ,

Sodexo7, and Rentokil Initial8, as ISS´s core competitors although they differ in size,

revenue and product offering. It was easier to identify a peer group for TDC A/S as it

was possible to get a list of peers from the Orbus database. I decided to focus on well-

known Nordic/European competitors, Deutsche Telecom, France Telecom, Telecom

Italia, Telenor, Teliasonera, Swisscom and Belgacom.

6 Compass Group is a British catering and support services company with more than 380.000 employees and market share in 50 countries. http://www.compass-group.com/ 7 Sodexo is a French catering, health care and sports & leisure company with 380.000 employees and market share in 80 countries. http://www.sodexo.com/group_en/default2.asp 8 Rentokil Initial is a British service company with over 78.000 employees and market share in 50 countries. http://www.rentokil-initial.com/

32

Operational performance

The following ratios will be used to observe the changes in operational performance

of the companies:

!"#$%& !" !""#$" !"# = !"# !"#$%&!"#$% !""#$" Equation 1

Return on assets is a profitability ratio that measures the net income generated per

dollar of the company´s assets. The ratio is useful in comparing companies within the

same industry and can give indication of how effectively companies are using their

assets. There are especially two factors that affect ROA, the profit margin (PM) and

asset turnover (ATO) (Penman, 2010).

!"#$%& !"#$%& (!") = !"# !"#$%&!"#"$%" Equation 2

!""#$ !"#$%&'# (!"#) =

!"# !"#$! !"#$% !""#$"

Equation 3

Profit margin (PM) illustrates how much of the income from sales is kept as income

after subtraction of costs and asset turnover (ATO) measures the ability of assets to

generate sales (Penman, 2010). The limitations of these measures are that they do not

separate the effects of operating and investing decisions from the effects of financing

decisions.

The last profitability measure that will be reviewed is the EBITDA margin. Since

EBITDA excludes non-cash flow items such as depreciation, it removes the effect of

financial structuring and can therefore be defined as a pure cash flow measure. It is

stated that the buyout industry invented this measure in the late 1980s as they were

looking for a measure that could specifically indicate the ability of a company to

service certain level of debt (Fraser-Sampson, 2007).

!"#$%& !"#$%& =

!"#$%&!"#$% !"#"$%"

Equation 4

33

Growth ratios

Company´s ability to deliver growth is critical in relation to value creation. But

growth can only create value when a company´s new projects or acquisitions generate

returns that are above the cost of capital. The main components of growth can be split

into overall market expansion in the market segments, market share performance9 and

mergers & acquisitions10 (Koller, Goedhart, & Wessels, 2010). The following ratios