private equity buyers — who, what and why - marshberry · the private equity (pe) industry as...

TRANSCRIPT

n VALUE CREATION in Private Equity

n THE SECRET SAUCE: Private Equity’s Growing Interest in Insurance Distribution

n PRIVATE EQUITY in Today’s Market

N o v e m b e r| 2 0 1 6

www.MarshBerry.com

helping clients learn, improve and realize their value

Private Equity Buyers — Who, What and

Why?How do PE firms differ from other buyers and how can you try to position yourself to attract their interest?

CONGRATULATIONS TO OUR PEER EXCHANGE NETWORK PARTNERS

To learn more about MarshBerry’s Peer Exchange NetworksContact Tommy McDonald at [email protected] or by calling 440.392.6700.

Selected by

as their 2016 BEST AGENCIES TO WORK FOR!

E A S T R E G I O N • S I L V E R W I N N E R

M I D W E S T R E G I O N • S I L V E R W I N N E R

S O U T H E A S T R E G I O N • S I L V E R W I N N E R

S O U T H E A S T R E G I O N • B R O N Z E W I N N E RMARSHBERRY

Marsh, Berry & Company, Inc. and its affiliates are not affiliated with Insurance Journal.

n PG. 4 Private Equity Buyers — Who, What and Why?

n PG. 6 Metric of the Month • Private Equity in Today's Market

n PG. 8 Value Creation in Private Equity

n PG. 10 The Secret Sauce: Private Equity’s Growing Interest in Insurance Distribution

n PG. 12 On the Horizon

TABLE OF CONTENTS

CONTRIBUTING AUTHORSSTEVE BOLLAND, Managing Director

MEGAN BOSMA, Senior Vice President

GEORGE BUCUR, Senior Consultant

JONATHAN HULL, Financial Analyst

CHAD MORGAN, Vice President

Let’s talk.

Engage with MarshBerry

28601 Chagrin Blvd., Ste. 400, Woodmere, OH 44122

www.marshberry.com

@marshberryinc

facebook.com/MarshBerry

linkedin.com/company/marshberry

November Spotlight

Changing Focus by Private Equity in the Insurance Industry through the yearsHistorically, the insurance industry was viewed by the private equity (PE) industry as being a low return industry with limited opportunities. This changed in the early 1990s with two events: Hurricane Andrew caused property catastrophe rates to spike to levels not seen before, and the advent of the first statistically-based catastrophe models. These models showed that high levels of reinsurance rates should be extremely profitable. The PE industry then invested heavily into the catastrophe reinsurance market.

Reinsurance pricing has fluctuated up and down since that time, with PE capital flowing in and out, depending on the cycle. Today, in a low part of the cycle, the only real PE funds in this part of the market are the “hedge fund” firms looking for “non-correlating” investments, and those looking for low risk insurance classes where they can invest the reinsurance company’s “float” through their investment funds.

In the early 2000s, other PE firms assisted in the privatizations of several publicly traded insurance brokers, and helped with financial backing to allow for further acquisitions. These turned out to be very successful and acted as a magnet for other PE firms to find similar transactions. In the absence of suitable candidates, they created their own by hiring experienced management teams who then grew through acquisition.

We are now seeing these firms, in many instances, selling to other PE firms, who intend to continue the process.

4 November 2016 | CounterPoint

Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440.354.3230

by Steven Bolland, Managing Director212.972.4880 [email protected]

Private Equity Buyers — Who, What and

Why?

How do PE firms differ from other buyers and how can you try to position yourself to attract their interest?

5CounterPoint | November 2016

The buy-sell environment in the insurance distribution industry has changed a lot in the past decade.

We believe the biggest reason for this may be the emergence of private equity (PE) firms into the space. In fact, last year, nearly half of all agency transactions in the U.S. involved PE firms in one way or another. This is up from almost nothing, historically. In our expertise, pricing has never been higher — with PE firms being aggressive buyers. How can they afford to pay these prices? What has happened to change things, and what should you know about these firms? In the face of such a “sea of change” in the marketplace you may want to find out more about these firms and how they operate. Chances are, even if you are not looking to sell currently, a number of your closest competitors may soon be under their control — one way or another!

The insurance distribution space is very diverse and contains thousands of firms. It is a market segment ripe for consolidation, with opportunities of all different sizes. But from a PE firms point of view, perhaps the most important factor is that insurance distribution firms have recurring income. This enables PE firms to use leverage in acquisitions — thus reducing their capital investment.

Combine this with today’s low interest rates, and the bank’s willingness to lend in the financing of these deals, and you have a recipe for high rates of return for investors. The reality is, PE firms want significant returns in a short period of time. Leverage, and a seemingly unlimited supply of additional acquisition targets, can provide just that. In a typical PE firm investment, their expectation is that through the combination of organic growth and additional agency purchases, there is the ability to make a return of over three times their capital investment in a few short years — and that is a return rate, we believe, not available in many other industries at this time.

To see how the math works, we should first consider how PE actually works. Understanding how these firms operate and what matters to them will help frame a discussion about

what they’re looking for in a deal. Then, we’ll address what we believe today’s influx of PE actually means for the industry, now and in the future.

Understanding How Private Equity WorksWe hear a lot about PE these days, but how do these firms actually work and what does that mean for insurance agencies in today’s M&A environment? Understanding what motivates PE firms to buy is important. But let’s back up and first address how a typical PE fund is structured. Typically, PE funds are set up as limited partnerships that are run by general partners (GP) who operate the fund. Investors in the fund are called limited partners (LP), and they are passive investors. That means, they provide capital but are not engaged in operating the fund in any way. When LP investors “buy in” to a PE fund, both parties enter into a Limited Partnership Agreement (LPA) that outlines terms and conditions.

What is important to know about PE funds is that there is a timespan. These funds don’t last forever. Typically, a fund’s life span is about ten years. During that time, the fund goes through various stages. First comes organizing and forming the PE fund. Next is fundraising, followed by deal sourcing and investment, which is where LPs come into the picture. GPs manage the portfolio and supervise the operation of the investments. Finally, the PE fund “ages out” as the fund sells off and exits all the investments they have made. The ultimate goal is to provide above market returns to the PE investors.

The typical PE fund pays to the GP a management fee to operate the fund, which is commonly two percent of the capital committed annually. These fees cover the firm’s salaries, deal sourcing, legal, data and research, marketing and operational expenses. Although attractive, such fees are not the reason why PE firms can pay very high salaries and attract the top talent. The “kicker” is that GPs can have the opportunity to receive a performance fee (e.g. about 20 percent of the excess gross profit for the fund) — a huge bonus for high performance! This is also the “carried interest” you hear discussed in the news; the

What is important to know about PE funds is

that there is a timespan. These funds

don’t last forever.

Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440.354.3230

6 November 2016 | CounterPoint

issue being that this is taxed as capital gains and not ordinary income — a huge benefit for PE firms! However, sometimes this can be limited by having a distribution waterfall, which could limit the fee to the amount of the profit that is in excess of an agreed return hurdle (say 8%, for example). So, the interest of the PE firm becomes ensuring top performance.

No two PE funds are the same. Each has a strategy and buys companies for different reasons. Also, limitations may be placed on the fund by conditions within the LPA, such as:

n Limitation on industry types into the fund

n Limitations on the company size and/or investment size, being invested in

n Diversification of investments into the fund

When a PE firm announces that they have “raised” a new fund, this does not mean that they have been given the money and have it in their bank account. Investors have provided a “commitment” to provide the money when asked (on a cash call). Money is “drawn down” as investments are found and investments are required to be made. Consequently, the clock starts ticking on their investment return on the “paid in capital”, and the firms track their cumulative distribution to the LPs and the residual value which is the market value of the remaining equity that the limited partners have in the fund.

Private Equity Dynamics: Investing in SuccessPE firms operate in a highly competitive environment; they are constantly competing to raise new funds. Fund raising happens approximately every 3 to 5 years as the old fund becomes fully invested. A PE firm may have several funds in operation at any one time, each in a different stage of development.

Firms compete for new funds based on their investment returns. In the past, investors had great difficulty obtaining meaningful comparisons of accurate investment performance data. Making apples-to-apples comparisons of investment performance was difficult, as firms reported information in different manners. So in 1987 the Global Investment Performance Standards (GIPS) was set-up to require that specific ratios be present when PE firms present their performance to prospective investors.

A key ratio is the realization multiple which is also known as the distributions to paid-in (DPI) multiple. It is calculated

by dividing the cumulative distributions by paid-in capital. The realization multiple, in conjunction with the investment multiple, gives a potential private equity investor insight into how much of the fund’s return has actually been “realized,” or paid out, to investors. In our experience, this is also a reason why recapitalizations are so popular with PE firms, as they are effectively replacing their valuable capital with debt.

We believe that knowing how investors select PE funds and what metrics are watched to evaluate funds’ success will help you understand what qualities PE firms are looking for when they buy companies and, equally important, what they are looking to avoid.

The Math….Let’s keep this simple, as no two deals are alike (and different PE firms have different methodologies). Basically, if a PE firm has the ability to fund over half the transaction with debt (and we have seen levels far in excess of that) at very low rates, then it is easy to see how you can turn an agency making a 20% margin into an agency making a 40% margin. Combine this with the fact that they can expense the interest cost and amortization to effectively have a zero tax rate1, and you can see how they can be very effective competitors over the traditional agency buyers!

What does all this mean to you?1 Firstly, and most importantly, for a PE firm TIME IS

MONEY. They are judged (and rewarded) on not only by the amount of their returns to investors, but also by the speed with which they can do it. Average returns can severely impact their ability to raise new funds, and without new funds they are looking at a slow death.

2 Capital is precious to PE firms. If they can use debt or retained earnings to increase return rates, then that is much more preferable than investing additional capital. This is because the clock starts ticking anew on their investment return calculations as soon as a new cash call on their investors is made. Remember they are in a competition!

3 Growth – one way or another – is vital. A hold and consolidate strategy will not excite the average PE firm. If they are invested with you for over five years, chances are that something may have gone wrong.

1 Marsh, Berry & Co., Inc. and MarshBerry Capital, Inc. do not provide tax or legal advice. These professionals should be consulted before implementing changes to your tax or legal matters.

Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440.354.3230

7CounterPoint | November 2016

4 PE firms come in all sizes, and different firms invest in different stages in the “life cycle of a business.” Consequently, it is not unusual to see one PE firm invest in a company, grow that company and then sell to another PE firm, who believes that they can take it to the next level. This can happen more than once, and is becoming more common in the industry as the number of firms controlled by PE firms expands. Remember their holding period is short— and other PE firms have the ability to pay high prices.

ConclusionPE firms have found an attractive niche in the insurance distribution space, and can have many advantages over other types of buyer. We should expect this to continue into the future and perhaps even grow as more and more firms “discover” the attractions

of this space. An increase in interest rates would have an impact on their return rates, but would not become that significant until rates reached a level where the leverage “multiplier” factor is negated. A larger risk for the PE firms is the loss of the access to capital. We did see at the end of 2015 a temporary freeze by the banks on new lending, which caused an almost complete disruption in the closing of certain transactions. Without leverage, the math becomes much less attractive.

Does this mean that current pricing levels will continue? We see little reason to assume that it won’t, and with the “baby boomer” generation getting to retirement age, we believe the supply of potential acquisition targets is unlikely to slow down. And PE will be looking to take advantage. nSecurities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440.354.3230

Private Equityin Today’s MarketPrivate equity has grown to become an integral part of the merger and acquisition (M&A) market within the insurance distribution industry. As of August 31, 2016, private equity (PE), which for purposes of this publication includes PE-backed firms, accounted for 50.9% of announced transactions, which has increased from 44.4% over the same period from the previous year. The majority of PE transactions closing in 2016 came from four buyers, which accounted for 79 out of 141 transactions.1 Outside of the top buyers (listed right), the “Other Private Equity-Backed Brokers” accounted for 32 transactions, which are made up of 21 firms.

With a few exceptions, many of these firms have significantly increased their activity in the insurance distribution space within the past five years. Among the most active buyers, BroadStreet Partners, Inc. has been one of the top PE firms based on deal volume, accounting for 22 transactions as of August 31, 2016. HUB International, Limited and USI Insurance Services, LLC (USI) have consistently been among the leading acquirers dating back to 2007 when they were the target of leverage buyouts in take-private transactions. Since these take- private transactions, PE has become a primary source of capital in today’s M&A market for the insurance distribution space. n

2016 YEAR-TO-DATE PRIVATE EQUITY TRANSACTIONS

Source: SNL Financial, Insurance Journal, and other publicly available sources1MarshBerry estimates that only 15.0 to 30.0 percent of transactions are actually made public.

METRIC OF THE MONTH

Dealmaker’s Dialogue

Value Creation

8 November 2016 | CounterPoint

The question of how private equity (PE) funds actually create value in a transaction has been much debated inside and outside the PE industry.

in Private Equityby Chad Morgan, Vice President, Insurance Services Division 949.234.9653 | [email protected]

The PE governance model depends on some economic advantages it may have over the public equity governance model. These potential advantages, include:

1 the ability to re-engineer the private firm to generate superior returns,

2 a better alignment of interests between PE firm owners and the managers of the firms they control, and

3 the ability to access credit markets on favorable terms.

Do PE firms have superior ability to re-engineer companies and, therefore, generate superior returns?

Some of the more notable PE organizations have developed in-house, high-end consulting capabilities supported frequently by seasoned industry veterans (former CEOs, CFOs, senior advisers), and have a proven ability to execute deals on a global basis – two key ingredients that contribute to the track record of PE value creation.

Another important factor in value creation is the alignment of economic interests between PE owners and the managers of the companies they control. Alignment can crystallize management efforts to achieve ambitious milestones set by PE owners. For example, results-driven management pay packages, along with various contractual clauses, can help ensure that managers receive proper incentives to reach their targets, and that they will not be left behind after the PE house exits their investment (e.g. drag-along / tag-along rights).

Figure 1

1. Management (Mgmt.) equity receives 5% of the terminal equity value: .05×[$16m – ($8.4m + $4.0m) 2. PE Fund equity receive 95% of the terminal equity value: .95×[$16m – ($8.4m + $4.0m)3. Preference shares are paid a 12% annual dividend: $4.75m×(1+.12)^5 = $8.4m4. Senior debt is partially retired with operational cash flows. Debt holders receive $4.0m*The total does not exactly equal $16m due to roundingLBO = Leveraged Buy-OutSource: MarshBerry example for illustrative purposes only. Individual results may vary.

AMPLIFIED INVESTMENT RETURN USING A SIMPLIFIED LBO SCENARIO

Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440.354.3230

9CounterPoint | November 2016

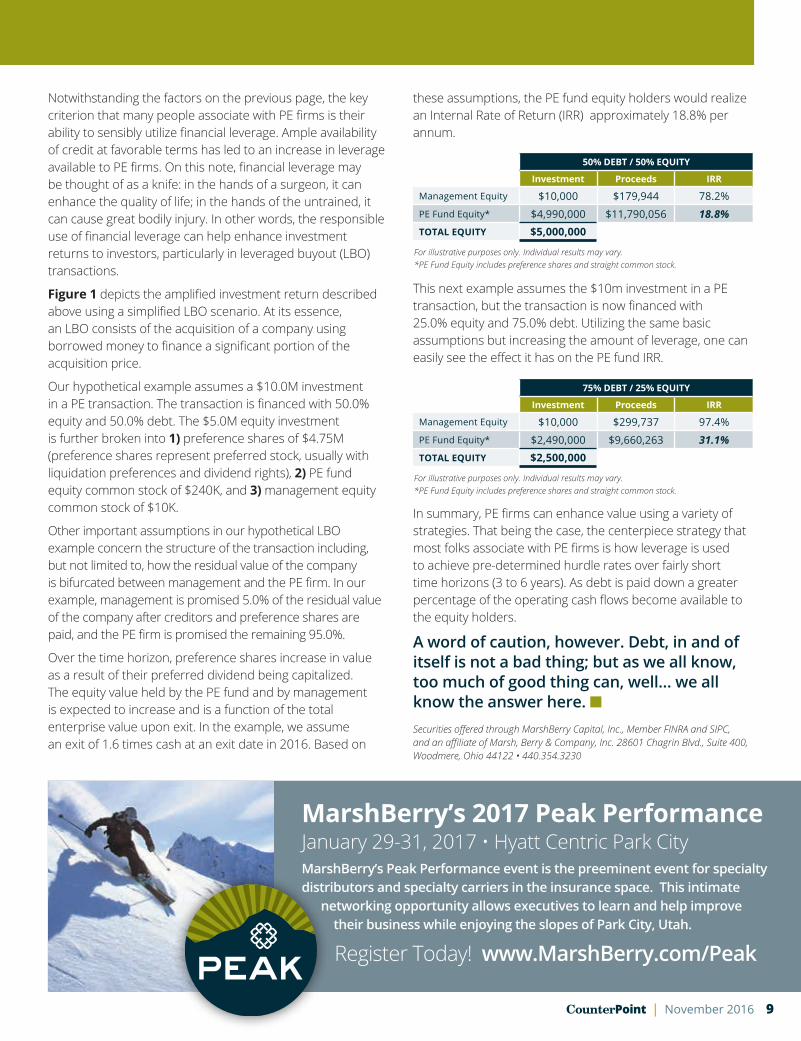

Notwithstanding the factors on the previous page, the key criterion that many people associate with PE firms is their ability to sensibly utilize financial leverage. Ample availability of credit at favorable terms has led to an increase in leverage available to PE firms. On this note, financial leverage may be thought of as a knife: in the hands of a surgeon, it can enhance the quality of life; in the hands of the untrained, it can cause great bodily injury. In other words, the responsible use of financial leverage can help enhance investment returns to investors, particularly in leveraged buyout (LBO) transactions.

Figure 1 depicts the amplified investment return described above using a simplified LBO scenario. At its essence, an LBO consists of the acquisition of a company using borrowed money to finance a significant portion of the acquisition price.

Our hypothetical example assumes a $10.0M investment in a PE transaction. The transaction is financed with 50.0% equity and 50.0% debt. The $5.0M equity investment is further broken into 1) preference shares of $4.75M (preference shares represent preferred stock, usually with liquidation preferences and dividend rights), 2) PE fund equity common stock of $240K, and 3) management equity common stock of $10K.

Other important assumptions in our hypothetical LBO example concern the structure of the transaction including, but not limited to, how the residual value of the company is bifurcated between management and the PE firm. In our example, management is promised 5.0% of the residual value of the company after creditors and preference shares are paid, and the PE firm is promised the remaining 95.0%.

Over the time horizon, preference shares increase in value as a result of their preferred dividend being capitalized. The equity value held by the PE fund and by management is expected to increase and is a function of the total enterprise value upon exit. In the example, we assume an exit of 1.6 times cash at an exit date in 2016. Based on

MarshBerry’s 2017 Peak Performance January 29-31, 2017 • Hyatt Centric Park CityMarshBerry’s Peak Performance event is the preeminent event for specialty distributors and specialty carriers in the insurance space. This intimate networking opportunity allows executives to learn and help improve their business while enjoying the slopes of Park City, Utah.

Register Today! www.MarshBerry.com/Peak

these assumptions, the PE fund equity holders would realize an Internal Rate of Return (IRR) approximately 18.8% per annum.

This next example assumes the $10m investment in a PE transaction, but the transaction is now financed with 25.0% equity and 75.0% debt. Utilizing the same basic assumptions but increasing the amount of leverage, one can easily see the effect it has on the PE fund IRR.

In summary, PE firms can enhance value using a variety of strategies. That being the case, the centerpiece strategy that most folks associate with PE firms is how leverage is used to achieve pre-determined hurdle rates over fairly short time horizons (3 to 6 years). As debt is paid down a greater percentage of the operating cash flows become available to the equity holders.

A word of caution, however. Debt, in and of itself is not a bad thing; but as we all know, too much of good thing can, well… we all know the answer here. n Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440.354.3230

For illustrative purposes only. Individual results may vary.*PE Fund Equity includes preference shares and straight common stock.

50% DEBT / 50% EQUITY

Investment Proceeds IRR

Management Equity $10,000 $179,944 78.2%PE Fund Equity* $4,990,000 $11,790,056 18.8%TOTAL EQUITY $5,000,000

For illustrative purposes only. Individual results may vary.*PE Fund Equity includes preference shares and straight common stock.

75% DEBT / 25% EQUITY

Investment Proceeds IRR

Management Equity $10,000 $299,737 97.4%PE Fund Equity* $2,490,000 $9,660,263 31.1%TOTAL EQUITY $2,500,000

10 November 2016 | CounterPoint

For the Record

by George Bucur, Senior Consultant440.392.6543 | [email protected]

Private Equity’s Growing Interest in Insurance Distribution

TheSecret Sauce:

With historically low investment returns in public financial markets, investors seek alternative investment opportunities. Evidence suggests that private equity (PE) funds are an increasingly popular alternative to historical investment strategies. This phenomenon is spreading across many industries. According to a March 29, 2016 article by Forbes titled “Competition Requires Private Equity Funds to Get Creative in Deal Making,” PE carried over $1.3 trillion of uninvested dry powder, or the current amount of capital available to private equity investors, in 2015. With prominence in many other industries, it is surprising PE has not been drawn to the insurance distribution industry sooner as an attractive investment opportunity.

According to MarshBerry’s proprietary tracking of announced insurance distribution transactions, PE firms were involved in 212 transactions1 (46.5% of total) in 2015. When you compare this to the one transaction PE was involved with just 10 years ago in 2006, it is evident PE’s interest in the distribution sector is growing.

Evidence suggests that private equity funds are an increasingly popular alternative to historical investment strategies.

THE GROWTH OF PRIVATE EQUITY IN INSURANCE DISTRIBUTION

Sources: SNL Financial, Insurance Journal, other publicly available sources and MarshBerry proprietary databases

1 MarshBerry estimates that only 15.0 to 30.0 percent of transactions are actually made public.Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440.354.3230

11CounterPoint | November 2016

So what’s the secret sauce? Let’s look at the three ingredients:

1 Positive Cash Flows Capital expenditures are typically a minimal expense for insurance distributors. When coupled with high client retention rates that can easily exceed 85%, this helps to promote positive cash flows.

2 Fragmented Distribution Marketplace With tens of thousands of insurance distributors in the United States, many led by owners nearing retirement age, the market is ripe for consolidation. Buyers are presented with the opportunity to implement a consolidation strategy to form and/or grow operations. Sellers have the opportunity to de-risk through ownership liquidation.

3 Leverage (i.e. cheap debt) Fiscal policy has loosened on a global scale over the past eight years since the financial crisis. This prolonged capital infusion into public markets has pushed interest rates to historically low levels. Given the leveraged buyout (LBO) operating structure of many private equity firms, the availability of “easy money” allows for heightened debt levels. This accomplishes two somewhat related benefits for PE firms. First, it allows for improved investment returns as debt can be used in place of equity (i.e. a set return on an investment will be higher with a lower equity base). Second, PE firms can decide to be more aggressive when making offers to acquire firms (i.e. debt from banks supplements the equity needs of an investment).

Then, mixing well… Mixing it all together with a large number of diversified insurance distributors, PE is able to execute on acquisition strategies by borrowing debt at historically low interest rates. The cash flow from those acquisition targets is then used to pay off interest on the debt.

The combination of these factors can lead to one appetizing investment, which appears to be getting more notice among private equity investors in today’s low investment return environment. nSecurities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 • 440.354.3230

Peer Exchange Network NewsMarshBerry Employee Engagement SurveyHow do employees perceive your policies, practices, and management? Do you have a gauge on employee morale? What does your staff see as the greatest needs for improvement?

Unlock the answers to these questions and much more with the MarshBerry Employee Engagement Survey.

The online survey is given to employees to provide a holistic portrait of how well an organization is functioning internally. It gives employees a forum to voice their opinions honestly and confidentially in order to spark change.

Survey results are benchmarked against other organizations in the MarshBerry database as well as your own historical survey results. Use of the Employee Engagement Survey is available to network partners at no extra cost beyond the annual dues.

To initiate your organization’s employee engagement survey, email [email protected] today!

Interested in learning more about our Peer Exchange Networks? Contact Tommy McDonald today at [email protected]

ALL THE DATA YOU NEED TO HELP

GROW YOUR BUSINESS

360marshberry

info

rmation intellig

ence

understanding

insi

ght

REGISTER TODAYwww.MarshBerry.com/360 or 800.426.2774

Early Bird Pricing $450 by February 24, 2017

JANUARY 20171.29-31 Peak Performance

Park City, UT

MAY 2017S A V E T H E D A T E S ! 2017 MarshBerry 3605.09 New Orleans, Harrah’s New Orleans5.11 New York, Convene at 237 Park Avenue5.23 Chicago, Swissotel Chicago5.25 Las Vegas, The Cosmopolitan of Las Vegas

Registration opening this fall!

Log on to www.MarshBerry.com

to register for events and to view all MarshBerry

news and events.

WE WANT TO HEAR FROM YOU!We want to make sure we’re providing the content you want to read and want feedback on the articles we’re publishing. Send an email to us at [email protected] to share your thoughts!

MARSHBERRY28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122

ON THE HORIZON