print ver 17 june 2011 investor presentation final · investor presentation ... wind jackets...

TRANSCRIPT

Investor PresentationKvaerner Executive ManagementOslo Konserthus, Lille salen17 June 2011

17.06.2011© Kvaerner 20112

Copyright and disclaimer

© Kvaerner 20112

DisclaimerThis presentation has been prepared by Kværner ASA to provide an overview of certain aspects of the operations and strategy of the Company. This presentation speaks as of 17th June 2011, and there may have been changes in matters which affect Kværner ASA subsequent to the date of this presentation. Neither the issue nor delivery of this presentation shall under any circumstance create any implication that the information contained herein is correct as of any time subsequent to the date hereof or that the affairs of Kværner ASA have not since changed, and Kværner ASA does not intend, and does not assume any obligation, to update or correct any information included in this presentation

This presentation includes and is based, inter alia, on forward-looking information and statements that are subject to risks and uncertainties that could cause actual results to differ. These statements and this presentation are based on current expectations, estimates and projections about global economic conditions, the economic conditions of the regions and industries that are major markets for Kværner ASA and Kværner ASA’s (including subsidiaries and affiliates) lines of business. These expectations, estimates and projections are generally identifiable by statements containing words such as “expects”, “believes”, “estimates” or similar expressions. Important factors that could cause actual results to differ materially from those expectations include, among others, economic and market conditions in the geographic areas and industries that are or will be major markets for Kvaerner’s businesses, oil prices, market acceptance of new products and services, changes in governmental regulations, interest rates, fluctuations in currency exchange rates and such other factors as may be discussed from time to time in the presentation. Although Kværner ASA believes that its expectations and the presentation are based upon reasonable assumptions, no assurance can be given that those expectations will be achieved or that the actual results will be as set out in the presentation. Anyone considering taking actions based upon the content of this document is urged to base investment decisions upon such investigations as deemed necessary. No representation or warranty, expressed or implied, is made with respect to its accuracy, reliability or completeness, and Kværner ASA nor any of its directors, officers or employees accepts no liability whatsoever for any direct or consequential loss arising from use of this document or its contents.

This presentation does not constitute or form a part of, and should not be construed as, an offer or invitation to subscribe for or purchase any securities of the Company and neither this document nor anything contained herein shall form the basis of, or be relied on inconnection with, any offer or commitment whatsoever.

This communication is only being distributed to and is only directed at (i) persons who are outside the United Kingdom or (ii) to investment professionals falling within Article 19(5) of the U.K. Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) or (iii) high net worth entities falling within Article 49(2)(a) – (d) of the Order (the persons described in (i) through (iii) above together being referred to as “relevant persons”). Any person who is not a relevant person should not act or rely on this document or any of its contents.

Not for distribution or release in the United States or to US persons, Canada, Australia and Japan or any other jurisdiction where to do so might constitute a violation of the relevant laws or regulations of such jurisdiction.

CopyrightCopyright of all published material including photographs, drawings and images in this document remains vested in Kvaerner and third party contributors as appropriate. Accordingly, neither the whole nor any part of this document shall be reproduced in any form nor used in any manner without express prior permission and applicable acknowledgements. No trademark, copyright or other notice shall be altered or removed from any reproduction.

17.06.2011© Kvaerner 20113

Kvaerner - Investment Highlights

EXTENSIVE TRACK RECORD

Kvaerner is a “new” company with more than 40 years of experience from the world’s most demanding market

TAILORED TO MEET STRONG MARKET

With an unprecedented market growth ahead, Kvaerner is tailored to meet market trends as well as client demands

ALL SYSTEMS ARE IN PLACE

Delivery models, systems and experience in place to deliver sound profits and manage growth

FINANCIAL MUSCLE Access to opportunities and credibility towards customers

A SOLID POSITION FOR GROWTH

Five business areas with leading positions in their niches and technologies ready to capture growth

17.06.2011© Kvaerner 20114

Kvaerner - Investment Highlights

EXTENSIVE TRACK RECORD

Kvaerner is a “new” company with more than 40 years of experience from the world’s most demanding market

TAILORED TO MEET STRONG MARKET

With an unprecedented market growth ahead, Kvaerner is tailored to meet market trends as well as client demands

ALL SYSTEMS ARE IN PLACE

Delivery models, systems and experience in place to deliver sound profits and manage growth

FINANCIAL MUSCLE Access to opportunities and credibility towards customers

A SOLID POSITION FOR GROWTH

Five business areas with leading positions in their niches and technologies ready to capture growth

17.06.2011© Kvaerner 20115

A strong name with a solid track record

AkerSolutions

ED&S / Field Development

1850 20001900 1950

Peter SteenstrupFirst CEO

Oluf A Onsum, founder

2008

AkerKvaerner

Field Development

Aker AkerMaritime

Kvaerner (Oil & Gas)

Kvaerner

EngineeringStordVerdal

EngineeringEgersundRosenberg

KvaernerGlobal EPC provider

Est1841

Davy/John Brown/Trafalgar

Norw. Contractors

Maritime Group

17.06.2011© Kvaerner 20116

With full focus on EPC field developments

More focused

Field development market poses unique challenges and opportunitiesMarket requirements for dedicated EPC contractors

More flexible

Meeting low cost requirements through strategic partnershipsMeeting local content requirements through local partnerships

Creating a focused global EPC company

17.06.2011© Kvaerner 20117

Fast track process to listing

January:P&C sold to Jacobs

Dec 2010:Reorganisation decided

March 2011:Kvaerner becomes a separate business area, and starts operating as a company 100 percent owned by Aker Solutions

July 2011: Listing

May 2011:AGM

After AGM:Kvaerner is owned 100 percent by Aker Solutions until the listing in 3Q

17.06.2011© Kvaerner 20118

CONCRETE

Concrete substructures

Global leader in Gravity based concrete structures

JACKETS

Large steel jackets for oil & gas installationsWind jackets

Eurpoean leader in steel jackets

NORTH SEA

TopsidesFloatersOnshore upstream facilities

Leading EPC contractor to the North Sea market

Kvaerner – a dedicated EPC company

UPSTREAM DOWNSTREAM & INDUSTRIAL

E&C AMERICASINTERNATIONAL

TopsidesFloatersOnshore upstream facilities

Spearhead for international expansion

Onshore facilitiesPower plantsSteel mills

A leading EPC contractor for the American market

17.06.2011© Kvaerner 20119

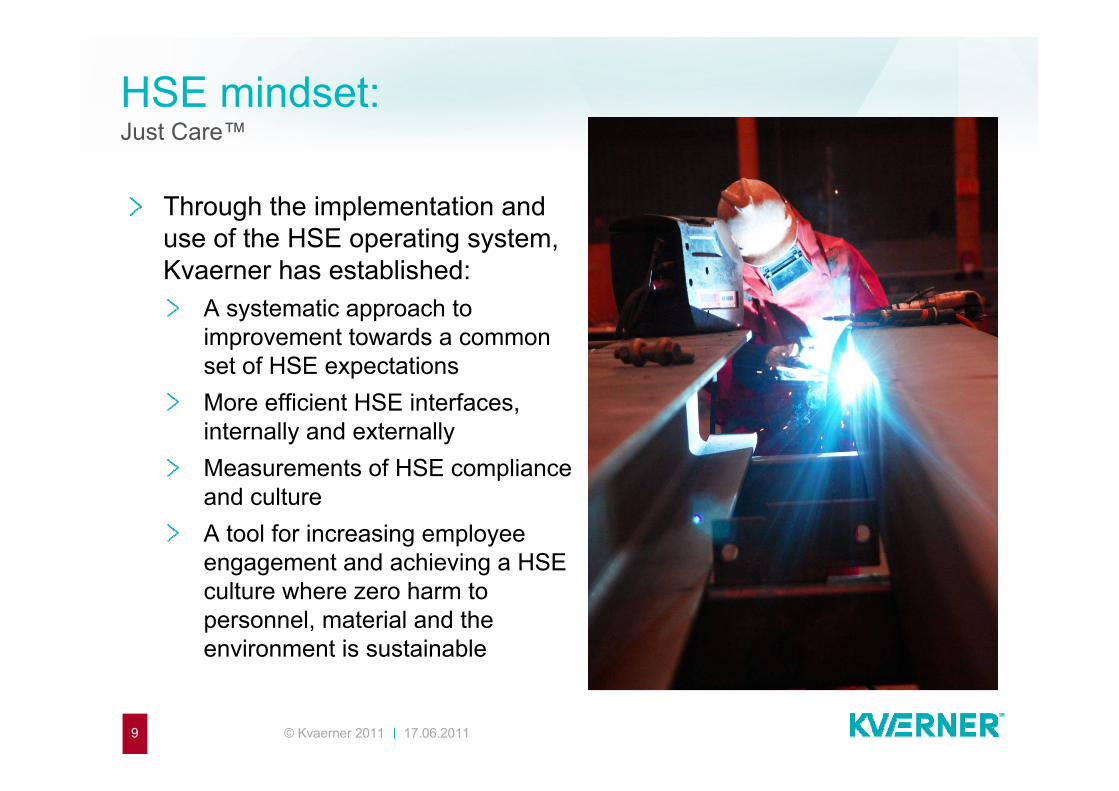

HSE mindset: Just Care™

Through the implementation and use of the HSE operating system, Kvaerner has established:

A systematic approach to improvement towards a common set of HSE expectationsMore efficient HSE interfaces, internally and externallyMeasurements of HSE compliance and cultureA tool for increasing employee engagement and achieving a HSE culture where zero harm to personnel, material and the environment is sustainable

17.06.2011© Kvaerner 201110

Experienced management teamLars EideNorth Sea Lars Eide has broad experience from a wide range of positions in Aker Solutions, most recently as President of Aker Stord, Project Director Gjøa EPCH and President of Aker Kværner Egersund. Mr. Eide holds a Masters Degree from the Norwegian University of Science and Technology.

Jan Arve Haugan*Chief Executive Officer (from 1 August 2011)Jan Arve Haugan has since 2009 been CEO of Qatar AluminiumLtd (Qatalum) - a 50/50 Joint Venture between Qatar Petroleum and Hydro Aluminium - one of the largest primary aluminum plants ever built in one phase. He holds a Master of Science in Construction Management from the University of Colorado at Boulder, USA.

Jim MillerE&C Americas Jim Miller joined Aker Philadelphia Shipyard as President and CEO in June 2008. Before that, he was President of Aker Solutions Process & Construction (P&C) Americas. Mr. Miller graduated from the University of Edinboro in Pennsylvania with a BA.

Jan ØyriBusiness Support (from 1 September 2011)Jan Øyri has more than 15 years of experience with organisationaland production processes and management development from companies like NCC, Elkem, Mesta and Norsk Hydro. Mr Øyri has significant tenure as an Officer with the Norwegian Army and hasattended Norwegian Military Academy and the Norwegian Army Staff College.

Bjørn GundersenConcrete Bjørn Gundersen has over 30 years experience from the oil and gas industry. He has extensive experience through project managementpositions for major world class offshore oil and gas projects, as well as corporate business executive management positions, in Norway as well as internationally. Mr. Gundersen holds a degree in civil engineering from the Regional College of Stavanger.

Jan-Tore ElverhaugProject Support Jan-Tore Elverhaug has more than 30 years experience from the offshore industry and has been part of the management in Kværner Engineering and Aker Solutions, including EVP for Field Development and President of Aker Stord. He is a Petroleum Engineer from the Regional College of Stavanger in and holds a business degree from the Norwegian School of Management.

Nina Udnes Tronstad JacketsNina Udnes Tronstad has since joining Aker Solutions in 2007 been president of Aker Verdal. Prior to joining Aker Solutions, Ms Udnes Tronstad held various technical and management positions in Statoil, both upstream, midstream and downstream. Ms. Udnes Tronstad holds a degree in chemical engineering from the Norwegian University of Science and Technology.

Eiliv GjesdalChief Financial Officer Eiliv Gjesdal joined Aker Solutions in 2002 and has extensive experience from finance and control functions. Mr. Gjesdal holds a MSc in Economics and Business Administration from NHH in Bergen, Norway, and is a state authorised public accountant in Norway.

* Per Harald Kongelf will act as Interim CEO until 1 August 2011

17.06.2011© Kvaerner 201111

Directors with long tenure from the industry

Bruno WeymullerDirectorBruno Weymuller served as Strategy Director of the Total Group from 2000 to 2008. He started his career with positions within the French Ministry of Industry, the Energy Directorate as well as the Prime Minister‘s office. Mr. Weymuller has held various executive positions in Elf Aquitaine (Total) from 1981 to 2008. Mr. Weymuller is an alumnus of the Ecole Polytechnique and the Ecole des Mines (Paris) and also holds an MSc from MI.T

Kjell Inge RøkkeChairman Kjell Inge Røkke is an entrepreneur and industrialist, and has been a driving force in the development of Aker since the 1990s. Mr. Røkke owns 67.8 % of Aker ASA through privately held companies organised under TRG. He holds the positions as chairman of Aker ASA, Aker BioMarine ASA and Detnorske Oljeselskap ASA, and board member of Aker Solutions ASA.

Vibeke Hammer MadsenDirectorVibeke Hammer Madsen is the CEO of HSH (The Federation of Norwegian Commercial and Service Enterprises) since 2002. Prior to this, she was a partner in the PA Consulting Group. From 1993 to 1999 she was a vice president holding various positions in Statoil. Ms. Hammer Madsen holds a number of board positions, was board member of Aker Solutions from 2008 until May 2011. Ms. Hammer Madsen is a graduate of the Norwegian School of Radiography.

Lone Fønss SchrøderDirectorLone Fønss Schrøder has broad international experience acquired during 21 years in senior management, including board positions at A.P. Møller-Maersk A/S. She is a chairperson for the audit committee at Volvo, a non-executive director of Volvo PV in Sweden and NKT A/S in Denmark, as well as non-executive director and member of the audit committees of Aker Solutions ASA, Vattenfall AB and Svenska Handelsbanken AB. Ms. FønssSchrøder has a law degree from the University of Copenhagen and a Master of Economics from CBS.

Employee elected Directors:Rune RafdalStåle Knoff JohansenBernt Harald Kilnes

Tore TorvundDirectorTore Torvund holds the position as EVP of REC Silicon since 2009. Mr. Torvund has senior executive experience of more than 20 years in the oil and gas industry, including as EVP of E&P Norway at StatoilHydro, and EVP of Oil and Energy at Norsk Hydro. He has held several management positions related to drilling operations, field development and technologyprojects. Mr. Torvund holds an M.Sc in Petroleum Engineering from the Norwegian University of Science and Technology.

17.06.2011© Kvaerner 201112 © Kvaerner 20111212

Tailored to meet market requirements

12

Local delivery models where Kvaerner provides project management, yard management and risk expertise

Local content requirementsA major part of new field developments are located in closed markets

New frontiersA significant part of new resources to be found in remote areas, deepwater and/or harsh environment

The “easy” oil is gone, and so is easy contracting. Focus on relevant technologies such as GBS and advanced floaters

Low-cost competitionMature areas facing increased competition from low-cost players

Proactively seeking low-cost manufacturing capability through strategic partnerships

Contract risk managementCustomers increasingly favoring EPC contracts with less reimbursable elements

Creating a focused EPC player with strong risk management capabilities

17.06.2011© Kvaerner 201113

Kvaerner - Investment Highlights

EXTENSIVE TRACK RECORD

Kvaerner is a “new” company with more than 40 years of experience from the world’s most demanding market

TAILORED TO MEET STRONG MARKET

With an unprecedented market growth ahead, Kvaerner is tailored to meet market trends as well as client demands

ALL SYSTEMS ARE IN PLACE

Delivery models, systems and experience in place to deliver sound profits and manage growth

FINANCIAL MUSCLE Access to opportunities and credibility towards customers

A SOLID POSITION FOR GROWTH

Five business areas with leading positions in their niches and technologies ready to capture growth

17.06.2011© Kvaerner 201114

10 000

20 000

30 000

40 000

50 000

60 000

2000 2005 2010 2015 2020

CAGR 2010-15: 18%

Global Offshore Oil and Gas EPCUSD million

Unprecedented market outlook

Oil price outlook fuelling EPC market

Increasing production in frontier areas requires strong field development capabilities

Attractive marginal economics driving investments in mature areas

Global Oil and Gas EPCUSD million

20 000

40 000

60 000

80 000

100 000

120 000

140 000

2000 2005 2010 2015 2020

CAGR 2010-15: 15%

Source: Rystad Dcube April 2011

17.06.2011© Kvaerner 201115

5 000

10 000

15 000

20 000

25 000

30 000

2000 2005 2010 2015 2020

5 000

10 000

15 000

20 000

25 000

30 000

2000 2005 2010 2015 2020

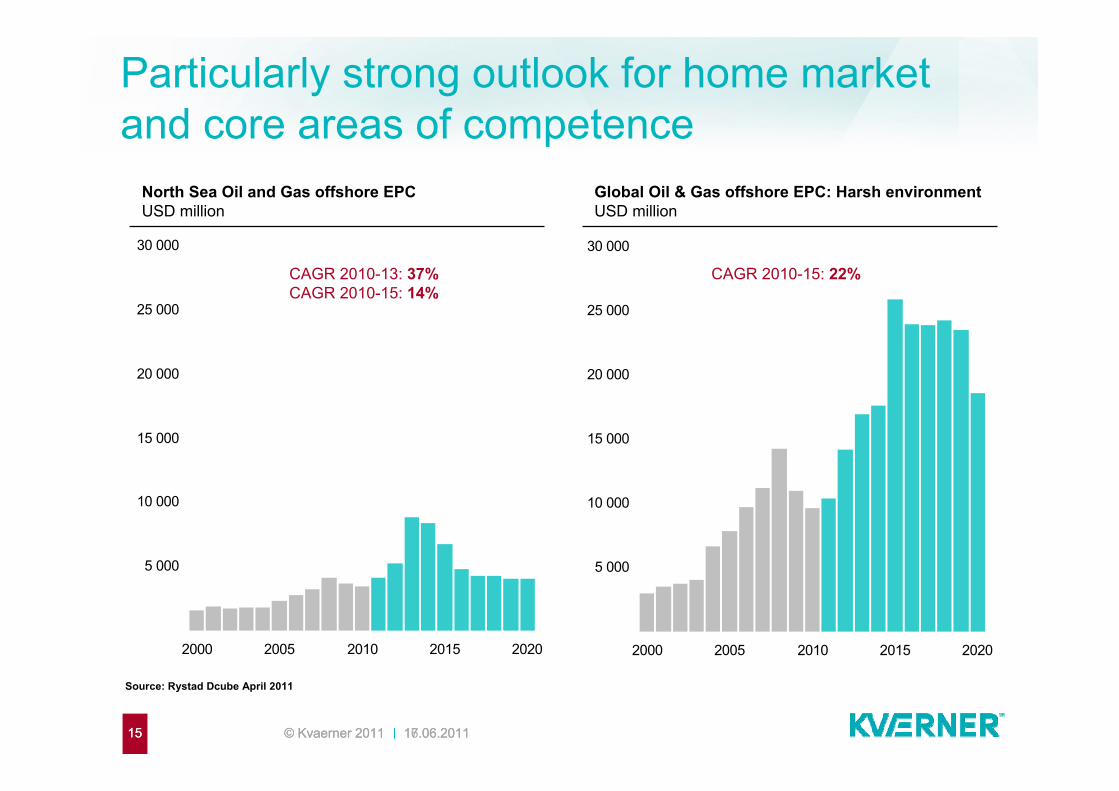

North Sea Oil and Gas offshore EPCUSD million

16.06.2011© Kvaerner 201115

Particularly strong outlook for home market and core areas of competence

Source: Rystad Dcube April 2011

CAGR 2010-13: 37%CAGR 2010-15: 14%

CAGR 2010-15: 22%

Global Oil & Gas offshore EPC: Harsh environmentUSD million

17.06.2011© Kvaerner 201116

A strategy for growth

Improve flexible engineering modelFurther develop Kvaerner’s flexible engineering delivery model: Adding enhanced in-house capabilities and subcontracted resources and entering into new joint ventures and partnerships arrangements in addition to existing agreements

Refine delivery modelIncreasing competitiveness through strengthening Kvaerner’s in-house capabilities, entering into partnerships, and further develop value added fabrication partnerships and regional delivery models.

Export knowledge and competenceLeveraging the knowledge and competence from home markets to grow internationally; with a particular focus on demanding projects

Capture expected market activityCapturing growth and defending market positions in home markets1

2

3

4

Kvaerner’s mission is to successfully plan and execute the world’s most demanding EPC projects and to become a top league global EPC company

17.06.2011© Kvaerner 201117

Kvaerner - Investment Highlights

EXTENSIVE TRACK RECORD

Kvaerner is a “new” company with more than 40 years of experience from the world’s most demanding market

TAILORED TO MEET STRONG MARKET

With an unprecedented market growth ahead, Kvaerner is tailored to meet market trends as well as client demands

ALL SYSTEMS ARE IN PLACE

Delivery models, systems and experience in place to deliver sound profits and manage growth

FINANCIAL MUSCLE Access to opportunities and credibility towards customers

A SOLID POSITION FOR GROWTH

Five business areas with leading positions in their niches and technologies ready to capture growth

17.06.2011© Kvaerner 201118

The EPC value chain

Analysis of development concepts

An appropriate development concept is selected

The chosen concept is further developed

Facility owner issues an invitation to tender

Definition and corresponding cost estimates

Project requirements are identified

Design elements are chosen and integrated

Encompasses the detailed engineering phase

Procurement of materials, labor and sub-contractors

Construction management and construction

On-site or at a yard

Module based construction

Services aimed at installing and commissioning the facility

Can be done by the facility owner or by the EPC contractor

CONCEPT FEED ENGINEERING (E) PROCUREMENT (P) CONSTRUCTION (C) COMMISSIONING

NOK ~10 - 20 million NOK ~30 - 60 million NOK ~4,000 - 8,000 million NOK ~200 - 300 million

~ 10 percent ~ 50 percent ~ 40 percentEstimate figures for illustrative purposes for a typical platform devlopment.

17.06.2011© Kvaerner 201119

A flexible delivery model

CONCEPT FEED ENGINEERING (E) PROCUREMENT (P) CONSTRUCTION (C) COMMISSIONING

ELDFISK (Topsides)

GUDRUN (Jacket)

SAKHALIN (GBS)

HEBRON (GBS)

BROWSE (TLP)

Aker Solutions as subcontractor

+ +

Aker Solutions as subcontractor COOEC as subcontractor

Potential agreement; for illustrative purposes

17.06.2011© Kvaerner 201120

Engineering capacity and capability

~700 Kvaerner engineersSelf sufficient on Jacket and ConcreteProject management resources as well as fabrication/late phase engineering resources

Cooperation with Aker SolutionsSubcontractor agreement for ongoing projectsResources dedicated for ongoing bids

Cooperation with other external engineering partners

Current projects and target prospects

Engineering strategy

Kvaerner to be involved in FEED phase for EPC phase positioningSelf sufficient on Jacket and ConcreteKvaerner in front, with engineering subcontractor/partner/JVPartner in front with Kvaerner involvement

Grow organically and through acquisitions

17.06.2011© Kvaerner 201121

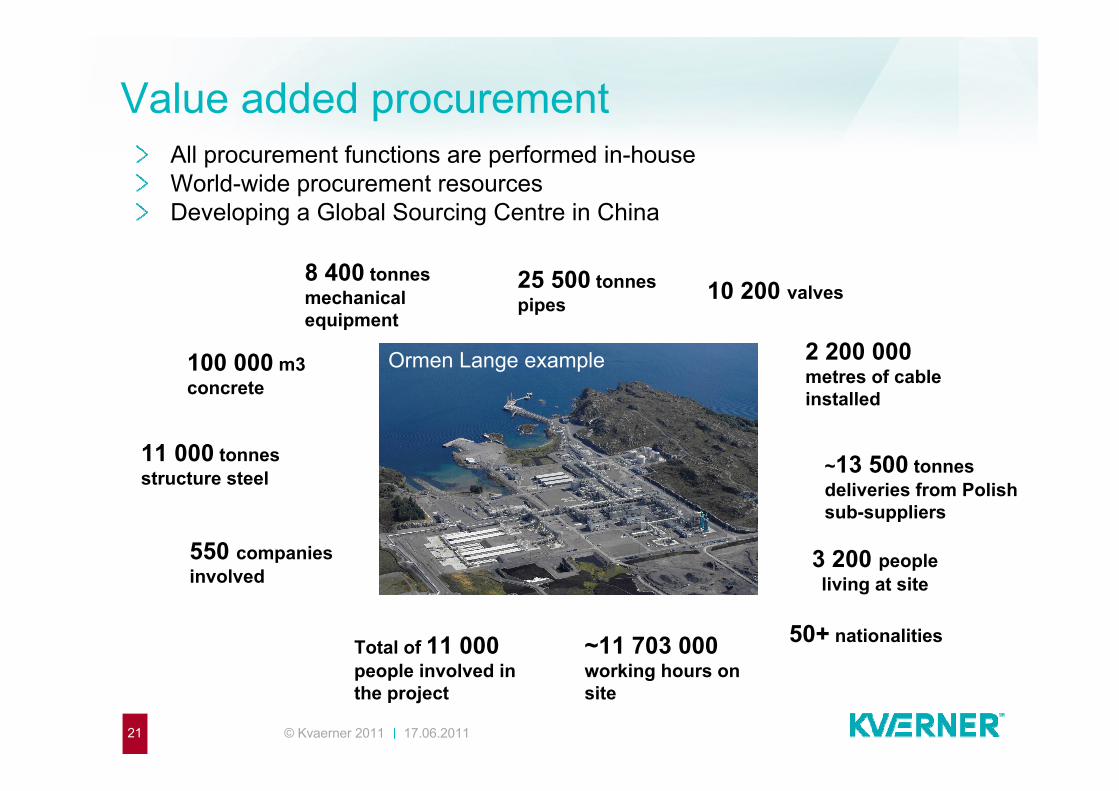

Value added procurementAll procurement functions are performed in-houseWorld-wide procurement resourcesDeveloping a Global Sourcing Centre in China

100 000 m3 concrete

11 000 tonnesstructure steel

8 400 tonnesmechanical equipment

25 500 tonnespipes 10 200 valves

2 200 000 metres of cable installed

50+ nationalities

550 companies involved

~11 703 000working hours on site

~13 500 tonnesdeliveries from Polish sub-suppliers

Total of 11 000 people involved in the project

3 200 people living at site

Ormen Lange example

17.06.2011© Kvaerner 201122

High quality, cost-effective fabrication

Value fabrication partner

High quality local content Value fabrication

Specialised yards An expanding network of qualified partners

COOEC (China)

Prefabrication suppliers in Poland

Fabrication on siteHigh quality local contentHigh quality local content, in important

marketsConcrete, e.g. Sakhalin, Russia

Concrete, e.g. Hebron, Canada

E&C Americas, e.g. Gulf LNG, USA

Specialised in-house yards~ 1 000 experienced operatorsMore than 2 000 highly experienced

engineers and operatorsStord, Norway

Verdal, Norway

17.06.2011© Kvaerner 201123

EPC contract formats

Contractual structures and risk (Figures are illustrative)

Field development contract format(Project example)

Contractor risk

Owner risk0 %

100 %0 %

100 %

Costreimbursement

Lump sum

Measurement

Target

Cost/target(reimbursable)

Measurement(rate based)

Lump sum

Measurement(norms/rate based)

Target(reimbursable)

Procurement

EngineeringConstructionProject management

17.06.2011© Kvaerner 201124

World class references

KRISTIN HPHT GAS PLATFORMThe first HPHT (high pressure, high temperature) floating production gas platform. Delivered in 2005.

GRANE PLATFORM JACKET17 500 tonnes fixed steel substructure for drilling, production, processing and accommodation facilities. Delivered in 2003.

SAKHALIN II GBSTwo concrete gravity based platforms for the Sakhalin II project offshore the Sakhalin island, East Russia. Delivered in 2005.

ORMEN LANGE The third largest gas field in Europe and one of Norway’s largest onshore plants. Delivered in 2007.

ADRIATIC LNG TERMINALThe world’s first offshore GBS based LNG re-gasification terminal, a strategic component of the Italian gas system. Delivered in 2009.

15 POWER PLANTS SINCE 2002New plants, as well as retrofits, environmental modifications, maintenance and upgrades to existing facilities

17.06.2011© Kvaerner 201125

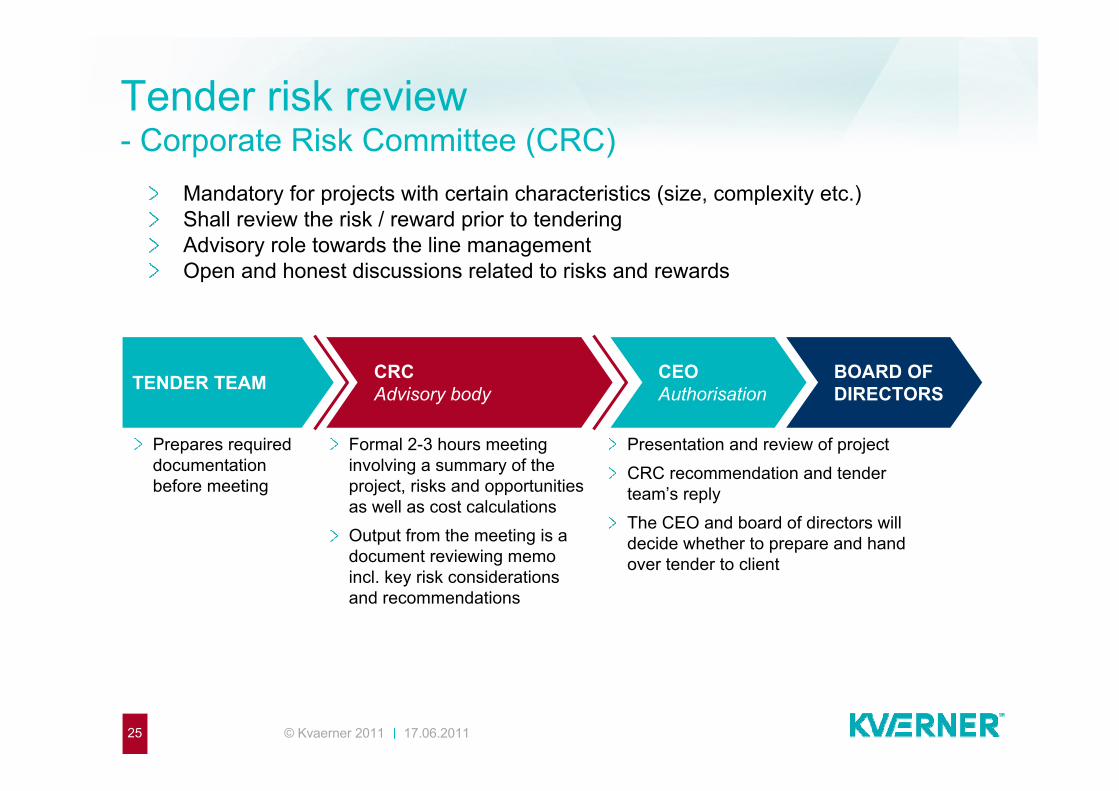

Tender risk review- Corporate Risk Committee (CRC)

Mandatory for projects with certain characteristics (size, complexity etc.)Shall review the risk / reward prior to tendering Advisory role towards the line managementOpen and honest discussions related to risks and rewards

TENDER TEAM CRCAdvisory body

CEOAuthorisation

BOARD OF DIRECTORS

Prepares required documentation before meeting

Formal 2-3 hours meeting involving a summary of the project, risks and opportunities as well as cost calculationsOutput from the meeting is a document reviewing memo incl. key risk considerations and recommendations

Presentation and review of projectCRC recommendation and tender team’s replyThe CEO and board of directors will decide whether to prepare and hand over tender to client

17.06.2011© Kvaerner 201126

Kvaerner - Investment Highlights

EXTENSIVE TRACK RECORD

Kvaerner is a “new” company with more than 40 years of experience from the world’s most demanding market

TAILORED TO MEET STRONG MARKET

With an unprecedented market growth ahead, Kvaerner is tailored to meet market trends as well as client demands

ALL SYSTEMS ARE IN PLACE

Delivery models, systems and experience in place to deliver sound profits and manage growth

FINANCIAL MUSCLE Access to opportunities and credibility towards customers

A SOLID POSITION FOR GROWTH

Five business areas with leading positions in their niches and technologies ready to capture growth

17.06.2011© Kvaerner 201127

Concrete substructures

Global leader in Gravity based concrete structures

Large steel jackets for oil & gas installationsWind jackets

Eurpoean leader in steel jackets

TopsidesFloatersOnshore upstream facilities

Leading EPC contractor to the North Sea market

Two segments - five business areasUPSTREAM DOWNSTREAM &

INDUSTRIAL

E&C AMERICAS

TopsidesFloatersOnshore upstream facilities

Spearhead for international expansion

Onshore facilitiesPower plantsSteel mills

A leading EPC contractor for the American market

CONCRETE JACKETS NORTH SEA INTERNATIONAL

17.06.2011© Kvaerner 201128

Income statement

(6.5)%2.4%3.7%8.8%12.5%EBITDA margin

NOK million Q1 2011 Q1 2010 2010 2009 2008Revenues 3 722 3 198 13 209 12 191 13 143

EBITDA 464 281 488 291 (852)Depreciation and amortisation (12) (13) (54) (85) (59)

EBIT 452 268 434 206 (911)Net financial items (1) (21) (30) (78) (23)

Profit before tax 451 247 404 128 (934)Tax (130) (77) (330) (76) 242

Net profit 321 170 74 52 (692)

17.06.2011© Kvaerner 201129

Historical financial highlights

2010: Increase in revenues and profitabilityIncreased revenues driven by Sakhalin and KashaganIncreased margins driven by project as well as pension plan adjustments

2009: Lower activity in all business areasThe H-6e drilling rigs completed early 2009 Lower activity in Jackets and Concrete

2008: Settlement on FriggFrigg decommissioning project and H-6e drilling rigs impacting profitability

Upstream Revenues and EBITDANOK million

Downstream & Industrials Revenues and EBITDANOK million

928

7 0509 1928 714

-1 018 -24

-2 0000

2 0004 0006 0008 000

10 000

2008 2009 201010.1%-0.3%-11.7%EBITDA-%

173

4 539 4 0495 274

-440315

-2 000

0

2 000

4 000

6 000

2008 2009 2010

-10.9%6.0%3.8%EBITDA-%

2010: Decrease in revenuesRevenue decrease due to completion of Cameron LNGLower margins as a result of the Longview and Hitachi

2009: Revenue increaseDriven by favourable phasing of projects

17.06.2011© Kvaerner 201130

Q1 2011: Upstream Review

Order backlog and order intakeNOK million

Revenues, EBITDA and EBITDA marginNOK million

MarketOperations

3 113 3 059

233 234 431 476

2 145 2 1951 739

290

1 000

2 000

3 000

4 000

Q1'10 Q2'10 Q3'10 Q4'10 Q1'11

13.8%1.7% 15.6%10.7%10.9%EBITDA-%

11 387 10 64812 735

10 376

14 273

1 342 9953 426

755

6 955

0

4 000

8 000

12 000

16 000

Q1'10 Q2'10 Q3'10 Q4'10 Q1'11

High activity on projects at the Norwegian yardsThe FEED and site preparation for the Hebron project progressing wellIncreased revenues and margins mainly driven by the Sakhalin and Kashagan projectsThe Kashagan HUC project has reached peak activity and the project is nearing completion

Award of Eldfisk 2/7 S, a NOK 5.5 billion EPC contract with ConocoPhillips to deliver the topside and bridges of the production platformKvaerner selected as one of two remaining players for key contracts for the Browse LNG development

Order backlog Order intakeRevenues EBITDA

17.06.2011© Kvaerner 201131

Q1 2011: Downstream & Industrial Review

Order backlog and order intakeNOK million

Revenues, EBITDA and EBITDA marginNOK million

MarketOperations

822 673

-64

1 068 1 0471 112

48

-137 -2863

-500

0

500

1 000

1 500

Q1'10 Q2'10 Q3'10 Q4'10 Q1'11

-34.8%-5.8% 0.4%-13.1%4.5%EBITDA-%

5 066 5 356 4 683

2 059 1 404298

1 053 819 531 1040

4 000

8 000

Q1'10 Q2'10 Q3'10 Q4'10 Q1'11

Low activity and weak margins, mainly due to Longview project

The Longview project towards completion in Q3’11 and Gulf LNG completion end 2011.

Arbitrational award on the Hitachi project

Awarded the V&M pipe mill installation project by V&M Star LP Fostering strategic partnerships to jointly pursue North American power projectsPositive markets within most segments and high bidding activity

Order backlog Order intakeRevenues EBITDA

(1) The CAD 400 million contract with TransCanada for a gas firedpower plant was removed from the backlog in Q4’10.

17.06.2011© Kvaerner 201132

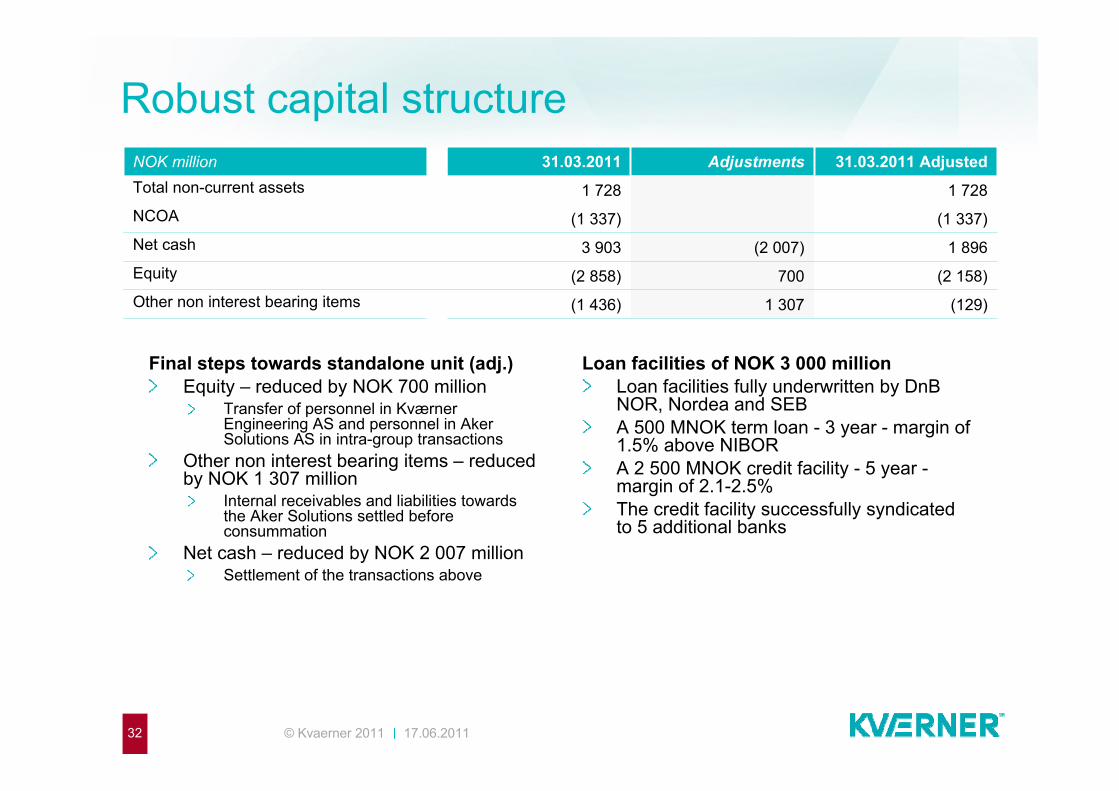

Robust capital structure

Final steps towards standalone unit (adj.)Equity – reduced by NOK 700 million

Transfer of personnel in KværnerEngineering AS and personnel in Aker Solutions AS in intra-group transactions

Other non interest bearing items – reducedby NOK 1 307 million

Internal receivables and liabilities towards the Aker Solutions settled before consummation

Net cash – reduced by NOK 2 007 millionSettlement of the transactions above

Loan facilities of NOK 3 000 million Loan facilities fully underwritten by DnBNOR, Nordea and SEBA 500 MNOK term loan - 3 year - margin of 1.5% above NIBOR A 2 500 MNOK credit facility - 5 year -margin of 2.1-2.5%The credit facility successfully syndicated to 5 additional banks

(129)

(2 158)

1 896

(1 337)

1 728

31.03.2011 AdjustedNOK million 31.03.2011 AdjustmentsTotal non-current assets 1 728NCOA (1 337)Net cash 3 903 (2 007)Equity (2 858) 700Other non interest bearing items (1 436) 1 307

17.06.2011© Kvaerner 201133

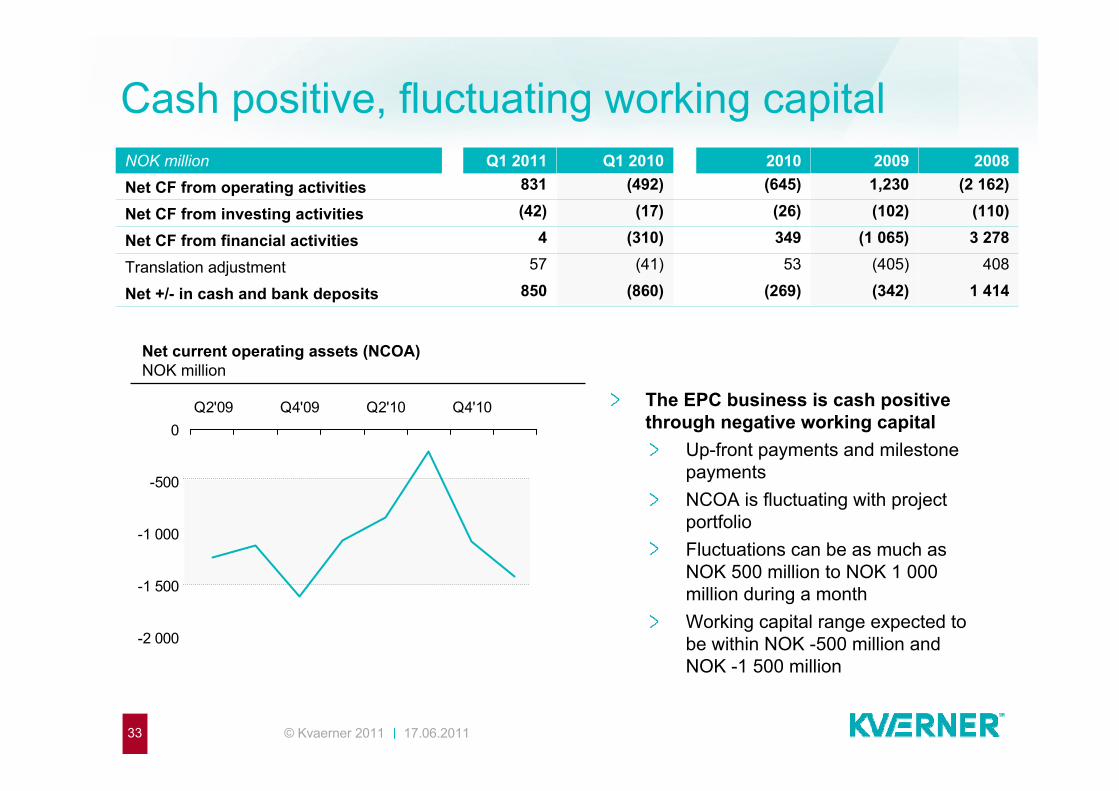

Cash positive, fluctuating working capital

The EPC business is cash positive through negative working capital

Up-front payments and milestone paymentsNCOA is fluctuating with project portfolioFluctuations can be as much as NOK 500 million to NOK 1 000 million during a monthWorking capital range expected to be within NOK -500 million and NOK -1 500 million

Net current operating assets (NCOA)NOK million

-2 000

-1 500

-1 000

-500

0Q2'09 Q4'09 Q2'10 Q4'10

200820092010Q1 2010Q1 2011NOK million

1 414(342)(269)(860)850Net +/- in cash and bank deposits

408(405)53(41)57Translation adjustment

3 278(1 065)349(310)4Net CF from financial activities

(2 162)1,230(645)(492)831Net CF from operating activities(110)(102)(26)(17)(42)Net CF from investing activities

17.06.2011© Kvaerner 201134

CAPEX and Investments

CAPEXNOK million

31

4

56

52 6

5

-20

0

20

40

60

80

100

2008 2009 2010

Other investmentsNOK million

Buildings and sitesMachinery, equipment and software Under construction (including transfers)

22

54

19-4 -3-4-20

0

20

40

60

80

100

2008 2009 2010Other investmentsAcquisition of subsidiary, net of cash acquiredProceeds from sale of PP&E

Investment plansHistorical capex review 2010: General maintenance

Capex related to maintenance2009: Mainly related to North Sea

A new barge for load-out and construction at StordIn addition to maintenance at Stord and E&C Americas

2008: Investments at StordNew building and barge

Maintenance capexExpected at NOK 30 - 50 million per year

Verdal 2011-2012: NOK 100-150 millionImproved capacity, paint shop and misc.

Investment plansInvestments to be considered case-by-case

17.06.2011© Kvaerner 201135

Dividend capacity and growth possibilitiesCash conversionSimplified illustration

Dividend

Grow

th capital

Tax

Maintenance

CA

PE

X

Financial item

s

EBIT

DA

Dividend policyBetween 30 and 50 per cent of net profit

Maintenance capexBetween NOK 30 to 50 million per year

Tax rateTax rate in Norway(28 percent) and the tax rate in the US (approx. 40 percent)

High cash conversion provides both dividend capacity and growth possibilities30%-50% of net profits to be distributed as dividends Revenue recognition as well as project phasing may cause certain fluctuationsStrong cash flow from operations of NOK 831 million in Q1-2011

17.06.2011© Kvaerner 201136

Quarterly key figures

Q1 2011Q4 2010Q3 2010Q2 2010Q1 2010NOK million

15 6767 049

12.5%

464

3 722Q1 2011

3.7%3.0%(1.2)%8.8%EBITDA margin

NOK million Q1 2010 Q2 2010 Q3 2010 Q4 2010Revenues 3 198 2 848 3 237 3 932EBITDA 281 (35) 97 145

Order intake 1 634 2 034 4 237 1 282

Order backlog 16 462 16 007 17 419 12 435

17.06.2011© Kvaerner 201137

Kvaerner - Investment Highlights

EXTENSIVE TRACK RECORD

Kvaerner is a “new” company with more than 40 years of experience from the world’s most demanding market

TAILORED TO MEET STRONG MARKET

With an unprecedented market growth ahead, Kvaerner is tailored to meet market trends as well as client demands

ALL SYSTEMS ARE IN PLACE

Delivery models, systems and experience in place to deliver sound profits and manage growth

FINANCIAL MUSCLE Access to opportunities and credibility towards customers

A SOLID POSITION FOR GROWTH

Five business areas with leading positions in their niches and technologies ready to capture growth

E&C Americas Business AreaJim Miller, EVP E&C Americas

17.06.2011© Kvaerner 201139

E&C Americas

Overview – two different legal entitiesUnion Construction Houston EPC Centre

77%*

23%*

~250 employeesRevenues (2010): NOK 3 317 million

~160 employeesRevenues (2010): NOK 1 007 million

General contracting and maintenance services for Power, Steel and Petrochemical Industries

Key current projects include the newly awarded Vallourec & Mannesman mechanical, equipment and piping project as well as current pipe mill building; and First Energy Fremont Generating Station

EPC & project management for the oil & gas industry including offshore topsides, LNG & gas processing, chemical, petrochemical, refining, power, utilities and infrastructure

Key current projects include Gulf LNG Energy, Medicine Bow Fuels Coal-to-Liquids Project (FEED)

17.06.2011© Kvaerner 201140

E&C Americas

Reference projects – Union Construction

Product/Service: Construction of Pipe MillGeography: Youngstown, OH, USASize: Approx. 1 000 000 sq.ftAwarded: 2011Delivered: OngoingClient: Vallourec & Mannesmann

Product/service: JV EPC Gas Fired Combined Cycle Power Plant Geography: Halton Hills, ON, Canada Size: 683 MWAwarded: 2007Delivered: 2010Client: TransCanada Energy, Ltd.

Product/service: Construction Gas Fired Combined Cycle Power Plant Geography: Fremont, OH, USA Size: 585 MWAwarded: 2008Delivered: 2011 Client: First Energy

V&M Pipe Mill TransCanada – Generating Station First Energy – Generating Station

17.06.2011© Kvaerner 201141

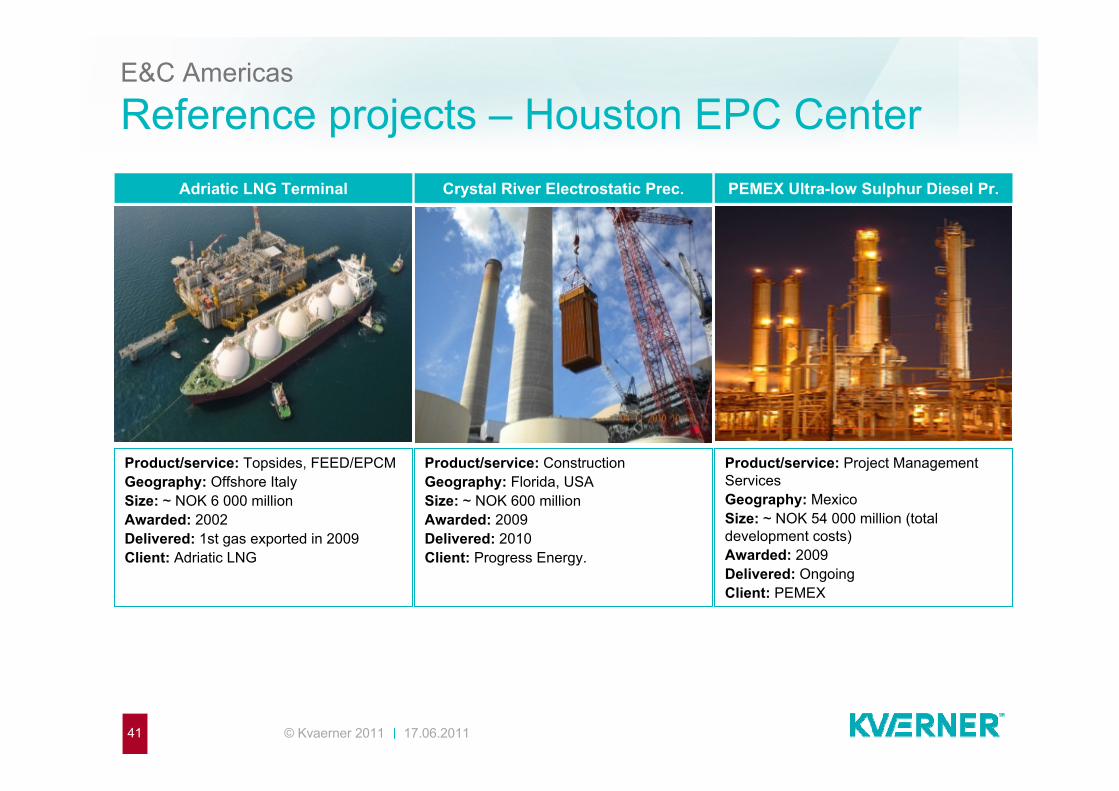

E&C Americas

Reference projects – Houston EPC Center

Product/service: ConstructionGeography: Florida, USASize: ~ NOK 600 millionAwarded: 2009Delivered: 2010Client: Progress Energy.

Product/service: Project Management Services Geography: MexicoSize: ~ NOK 54 000 million (total development costs)Awarded: 2009Delivered: OngoingClient: PEMEX

Product/service: Topsides, FEED/EPCM Geography: Offshore ItalySize: ~ NOK 6 000 millionAwarded: 2002Delivered: 1st gas exported in 2009Client: Adriatic LNG

Adriatic LNG Terminal Crystal River Electrostatic Prec. PEMEX Ultra-low Sulphur Diesel Pr.

17.06.2011© Kvaerner 201142

E&C Americas

Business Area StrategyHouston EPC CentreUnion Construction

Selected expansion by following clients into new markets such as Brazil, Middle East, China and Mexico

Develop regional Kvaerner delivery model and increase focus on and leveraging of strategic partnerships such as the LNG partnership with IHI

Develop position within natural gas liquefaction as well as coal/gas-to-liquids and leverage Kvaerner Group competencies as an entry strategy for the offshore market

Maintain and further develop key relationships with the major oil & gas, petrochemical companies and midstream operators

Selected expansion of core competencies in Western United States and Canada

Develop strategic alliances in core businesses to secure quality projects with strong partners. Increased training to improve execution and commercial outcome

As markets recover, capitalize on position in power, steel and petrochemical markets. Cultivate emerging alternative energy markets

Maintain position as a leading general construction and maintenance services provider to power and steel industries

Penetrate new geographical markets

Refine delivery model

Develop new products and market niches

Capture expected market activity

1

2

3

4

17.06.2011© Kvaerner 201143

E&C Americas

Operational structure and delivery model

Houston EPC Centre

Union Construction

Japan (Tokyo)

Partner (US LNG market (IHI))

India (Mumbai)

Partner (AKSO Engineering)

Mexico (Mexico City) Kvaerner

USA (Houston) Kvaerner (EPC Center)

USA (PA, IN)Canada (ON)

Kvaerner

China (Beijing)

Kvaerner (Sourcing) Partner (Aker Solutions)

17.06.2011© Kvaerner 201144

E&C Americas

Market outlook – Union Construction

Strong outlook for gas-fired power plants

Attractive outlook for USD 1bn steelworks maintenance market. Major US steel producers planning several upgrades

Aging infrastructure and postponed maintenance creates strong momentum for the general maintenance market going forward

Gas fired power plants to contribute significantly to electricity generationElectricity generation capacity additions by fuel type, 2010-2035 (gigawatts)

Source: IEA, Annual Energy Outlook 2011

17.06.2011© Kvaerner 201145

E&C Americas

Market outlook – Houston EPC Centre

Strong domestic energy demand outlook and energy price expectations encouraging investments in oil and gas sector

US shale gas play expected to increase demand for natural gas based projects such as liquefaction, NGL refining, downstream petrochemical and power

Expected strong demand for Kvaerner’s offering within coal-to-liquids and gas-to-liquids

Shale gas to potentially create demand for liquefaction capacityUS Dry Gas - trillion cubic feet per year

Source: IEA, Annual Energy Outlook 2011

17.06.2011© Kvaerner 201146

E&C Americas

ProspectsHouston EPC CentreProject Operator Location

Coal to Ammonia/Power Paradeep Phosphate India

Gas to Liquids Cenovus Energy Canada (Alb)

Waste Oil Recovery/Recycle Puralube Mexico

Project Management Services for Refinery Expansion PEMEX Chile

Gas to Chemicals Methanex/Petrobras USA (Tx)

Alaska Gas Treatment Plant ExxonMobil/Transcanada Taiwan / USA (La)

Industrial Gasification and Liquefaction Medicine Bow Fuels Project USA (Wy)

Union ConstructionProject Operator Location

Master Agreement Ontario Power Gen Ontario, Canada

Coker Piping Pkg 516 BP Indiana, USA

Coke Battery Arcelor Mittal Indiana, USA

Continuous Annealing Line U.S.Steel Kobe/Protec Ohio, USA

Combined Cycle Power Plant MacQuarie Cook Energy California, USA

Combined Cycle Power Plant NRG Energy California, USA

Flue Gas Desulfurization Units NIPSCO Indiana, USA

The list is not exhaustive or indicative of Kvaerner’s priorities.

Concrete Business AreaDag Nikolai Jensen, VP Business Development

17.06.2011© Kvaerner 201148

Concrete

Overview

World leader for floating and gravity-based concrete substructures for offshore oil and gas installations globally

Impressive track record with ~80* percent market share over 40 years

Approximately 150 employees based in Oslo

Proven execution model with experienced Oslo project management and local delivery model

* Estimate by Kvaerner

17.06.2011© Kvaerner 201149

Concrete

Reference projects

Product/service: Arctic GBS Geography: Sakhalin/RussiaSize: 63 000m3Awarded: 2003Delivered: 2005Client: SEIC (Shell)

Product/service: LNG Terminal Geography: Venice/ItalySize: 95 000 m3Awarded: 2004Delivered: 1st gas exported in 2009 Client: Adriatic LNG (ExxonMobil)

Product/service: Arctic GBS Geography: Sakhalin/Russia Size: 50 000m3Awarded: 2009Delivered: Ongoing, 2012 est.Client: ENL (ExxonMobil)

Sakhalin 2 LUN A & PAB Adriatic LNG Sakhalin 1 A-D

Key customers are ExxonMobil and Shell/SEICKey current projects are Sakhalin and the Hebron FEED for ExxonMobil

17.06.2011© Kvaerner 201150

Concrete

An impressive track record

First EPCI delivery was Beryl A Condeep in 197540 years of international Concrete experienceLead contractor in more than 20 major Concrete projects worldwidePioneered the development of high strength concrete for offshore applicationsIntroduced skirt piling for soft soil conditionsConcrete GBS for offshore platforms

Concrete GBS for LNG facilitiesConcrete hulls for floating platforms

17.06.2011© Kvaerner 201151

Concrete

The GBS offers many advantages

Integrated oil storageSignificant local contentRobustness to meet arctic environmentSupports large topside weightMinimum maintenanceLow lifecycle costInstallation independent of heavy lift vessel availability

17.06.2011© Kvaerner 201152

Concrete

Business Area Strategy

Penetrate new geographical marketsOngoing evaluation of Australia and Southeast Asia as potential future markets on an opportunistic basis. Develop execution model for GBS deliveries to North West Russia as well as for arctic Canada – both countries with demands for maximizing local content

Refine delivery modelEstablish local presence in key markets such as Canada and potentially Russia. Planned limited investments to secure relevant construction sites and enhance local execution capabilities

Develop new products and market nichesFurther develop GBS concept for LNG liquefaction plants for arctic gas rich areas, such as North West Russia, and promote minimum arctic wellhead platform concepts

Capture expected market activityMaintain position as #1 provider of concrete substructures for offshore oil and gas installations by strengthening ability to handle parallel projects

1

2

3

4

17.06.2011© Kvaerner 201153

Concrete

Operational structure and delivery model

Kvaerner project office(Newfoundland)

JV Partner (Peter Kiewit & Sons (PKS))

Current markets

Potential markets

Norway (Oslo)

Kvaerner Partner (Aker Solutions)

(Local external)

Russia (Sakhalin)

Kvaerner project office

Canada (St. Johns)

17.06.2011© Kvaerner 201154

Concrete

Market outlook

Concrete GBS experiencing a renaissance due to the structure’s suitability for Arctic and LNG based GBS developmentsKey markets include arctic environment areas such as Canada and RussiaKvaerner is market leader for Concrete with a 80%* historical market share for Condeep and floating concrete substructuresThe developments of Sakhalin 1 and Hebron GBS (ExxonMobil client for both) provides the foundation for developing increased capacity and growth towards 2020

* Estimate by Kvaerner

Concrete GlobalUSD million

0

100

200

300

400

500

600

700

800

900

1 000

2000 2005 2010 2015 2020

Canada Russia RoW

Source: Dcube April 2011

17.06.2011© Kvaerner 201155

Concrete

Prospects

North West CanadaConocoPhillips

Project Operator Location

Petchora LNG Alltech North West Russia

Hebron ExxonMobil Eastern Canada/Newfoundland

Piltun South Gazprom/Shell Sakhalin

Scarborough ExxonMobil Australia

White Rose Husky Eastern Canada/Newfoundland

Kammennomyskoye GazpromdobychaYamburg North West Russia

Yamal Novatek North West Russia

Dolginskoye Gazpeomneft North West Russia

Amuligak

Natuna ExxonMobil South East Asia

The list is not exhaustive or indicative of Kvaerner’s priorities.

Jackets Business AreaNina Udnes Tronstad, EVP Jackets

17.06.2011© Kvaerner 201157

Jackets

Overview

North Sea market leader for larger steel jackets for offshore oil and gas installations

Yard at Verdal with significant acreage and approximately 650 permanent employees

Strong track record with 34 oil & gas jackets delivered since 1975. New initiative within wind turbine jackets

Strong capabilities on design, soil and foundation, materials and supply chain management

In-house and integrated specialized engineering capacity, providing a truly seamless solution to the client

17.06.2011© Kvaerner 201158

Jackets

Reference projects – some examples

Product/service: Grane PDQ / EPC JacketGeography: Norway Size: 17,650 t; 150m Awarded: 2000Delivered: 2003Client: Hydro

Product/service: Valhall Re-Dev/EPC Jacket Geography: NorwaySize: 6,700 t; 106m Awarded: 2007Delivered: 2009Client: BP

Product/service: Buzzard WHP QU & P / 3 EPC jacketsGeography: UK Size: 4,600 t / 4,000 t / 5,600 t; 121mAwarded: 2003Delivered: 2005Client: Nexen UK

Grane PDQ Valhall redevelopment Buzzard Jackets

Current jacket projects include Gudrun, two jackets for Ekofisk, two steel jackets for the Clair Ridgedevelopment and a series of 49 wind jackets (Nordsee Ost) Key customers are Statoil, ConocoPhillips, the Clair Ridge Partnership and RWE Innogy

17.06.2011© Kvaerner 201159

Jackets

Business area strategy

Penetrate new geographical marketsEvaluate expansion into new markets through local fabrication partners. Australia and South East Asia high on agenda

Refine delivery modelPursue potential European fabrication partnerships to expand fabrication capacity and where partner locations are closer to the market

Develop new products and market nichesFurther strengthen the European wind jacket market position through standardization of design, competence on foundation and efficient installation concepts

Capture expected market activityRetain position as leading provider of large and complex steel substructures for oil and gas platforms through parallel construction of large steel jackets

1

2

3

4

17.06.2011© Kvaerner 201160

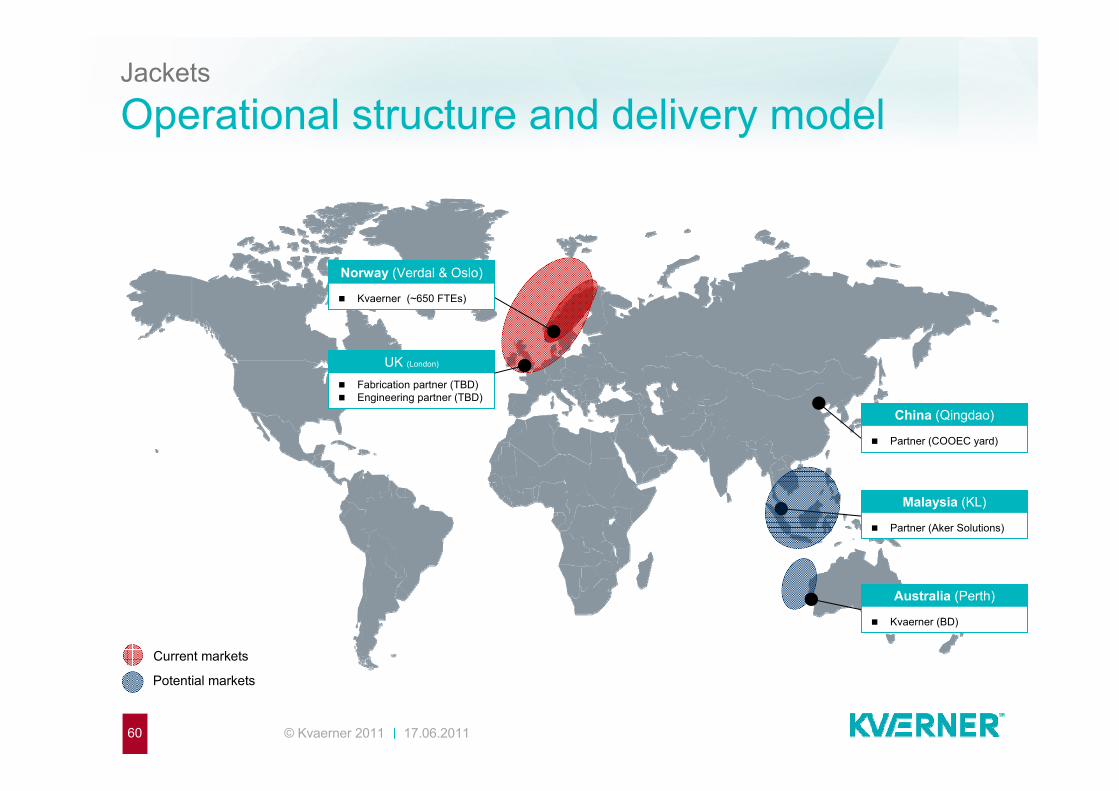

Jackets

Operational structure and delivery model

Fabrication partner (TBD) Engineering partner (TBD)

Current markets

Potential markets

Norway (Verdal & Oslo)

Kvaerner (~650 FTEs)

UK (London)

China (Qingdao)

Partner (COOEC yard)

Malaysia (KL)

Partner (Aker Solutions)

Australia (Perth)

Kvaerner (BD)

17.06.2011© Kvaerner 201161

Jackets

Market outlook

A local / regional market as transportation is costly as well as undesirableTarget markets include North Sea, Australia and South East Asia, representing approximately 30 % of the global market 2011-2020 Solid growth expected in home market, for which there is a limited number of suppliersKvaerner enjoys a historical market share of ~70-80%* Wind substructures provides further growth opportunity

0

200

400600

800

1000

1200

2000 2005 2010 2015 2020

Jackets for Oil and Gas – North SeaUSD million

Jackets for Oil and Gas – Key marketsUSD million

Source: Dcube April 2011

0200400600800

1000120014001600

2000 2005 2010 2015 2020North Sea Australia South East Asia

17.06.2011© Kvaerner 201162

Jackets

Prospects

NCSDet NorskeDraupne

NCSStatoilDagny

UKCSTalisman UKMontrose

NCSTotalHild

Oil & Gas ProspectsProject Operator Location

Golden Eagle Nexen UK UKCS

Luno Lundin NCS

Hejre Dong DK DKCS

Mariner Statoil UKCS

Bressay Statoil UKCS

Australia TBD

South East Asia TBD

Wind ProspectsProject Operator Location

Nordsee Ost Ext RWE Innogy Germany

Nordsee Innogy One RWE Innogy Germany

Dogger Bank Forewind consortium UK

The list is not exhaustive or indicative of Kvaerner’s priorities.

North Sea Business AreaLars Eide, EVP North Sea

17.06.2011© Kvaerner 201164

North Sea

Overview

Leading market position for North Sea topsides and assembly of floating and fixed offshore platforms

Solid track record of more than 25 major project deliveries over the last 25 years

Leading market position for complete onshore upstream facilities in Norway

Approximately 1 500 employees at Stord yard, specialised in project management, assembly and testing

Close engineering cooperation with Aker Solutions and other partners

17.06.2011© Kvaerner 201165

North Sea

Reference projects – some examples

2010: Gjøa2005: Kristin2001: Snorre B2000: Åsgard B1997: Heidrun1997: Njord1992: Snorre A TLP

Floating facilities

Current projects include the recently awarded EPC contract for the topside and bridges for Eldfisk 2/7Sas well as Skarv – final preparation for offshore hook-up

Topsides* Drlling rigs Onshore FPSO

* For fixed platforms

2003: Valhall drilling2000: Grane2000: Eldfisk1999: Siri1999: Oseberg Sør1996: Sleipner West1995: Troll gas1989: Gullfaks C1988: Oseberg A1986: Gullfaks A

2009: Aker Barents2009: Aker Spitsbergen

2011: Kollsnes upgrade2011: Test Centre Mongstad2007: Ormen Lange onshore terminal2007: Snøhvit LNG2005: Kårstø

2011: Skarv1999: Åsgard FPSO1999: Jotun FPSO1998: Laminaria1997: Norne FPSO

17.06.2011© Kvaerner 201166

North Sea

Business area strategy

Penetrate new geographical marketsCapture major share of expected Barents Sea development projects

Refine delivery modelEnter into additional engineering partnerships and further develop fabrication partnerships to meet low-cost competition

Develop new products and market nichesDevelop products for potentially large new markets, such as wind converter platforms, as well as prepare for the large decommissioning market to materialize

Capture expected market activityRetain leading position in the North Sea and capture major share of the expected upswing in the field development market as well as Norwegian onshore market

1

2

3

4

17.06.2011© Kvaerner 201167

North Sea

Operational structure and delivery model

Norway (Stord & Oslo)

Kvaerner (~1 500 FTEs) Partner (Aker Solutions)

Europe Engineering Partners

China (Beijing & Qingdao)

Kvaerner (Sourcing) Partner (COOEC yard)

Poland Partner (Single- and

multidisciplineconstruction partners)

Current markets, on- and offshore

Potential market entry

17.06.2011© Kvaerner 201168

01000200030004000500060007000

2000 2005 2010 2015 2020North Sea Norwegian Sea Barents Sea

North Sea

Offshore market outlook

Primary market is defined as offshore facilities larger than 4 000 tons in the North Sea, the Norwegian Sea and Barents regionKvaerner is the dominant player, but experiencing increased competition from far-east yards Steady flow of offshore new-build prospects in a five to ten year perspective is expectedKey projects for topsides in the North Sea the next years include Ekofisk, Eldfisk, Hejre, Luno, Mariner and HildKey projects for floaters in the North Sea and Barents Sea going forward include Luva, Snorre, Ormen Lange and Skrugard

TopsidesUSD million

FloatersUSD million

Source: Dcube April 2011

0

1000

2000

3000

4000

5000

2000 2005 2010 2015 2020North Sea Norwegian Sea Barents Sea

17.06.2011© Kvaerner 201169

North Sea

Onshore upstream facilities market outlook

The market is defined by traditional onshore upstream projects and other projects in conjunction with existing plantsThe market is a mature market with a mix of brown- and greenfield projects, both modifications and some new buildsKvaerner is the dominant player in NorwaySteady flow of medium-sized modification projects and some large-scale projects coming upStatoil is looking for suppliers that know their plants, to obtain synergies across the phases FEED, plant construction, modification and maintenance

17.06.2011© Kvaerner 201170

North Sea

Prospects

NorwayStatoilSnøhvit Phase II

North SeaStatoilDagny

Norwegian SeaStatoilLuva

UKStatoilBressay

UKStatoilMariner

Prospects offshore North SeaProject Operator Location

Hejre Dong Denmark

Hild Total North Sea

Luno Lundin North Sea

Ormen Lange Shell Norwegian Sea

Victoria Total Norwegian Sea

Snorre Statoil North Sea

Skrugard Statoil Barents Sea

Prospects Onshore NorwayProject Operator Location

Kollsnes Statoil Norway

Mongstad CO2 Statoil Norway

The list is not exhaustive or indicative of Kvaerner’s priorities.

International Business AreaPer Harald Kongelf, Interim CEO

17.06.2011© Kvaerner 201172

International

Overview

Provides key technologies and experience to international upstream EPC projects

Focus on demanding and complex solutions

Delivery model enables local content for closed and semi-closed markets

Current focus areas are Australia and Caspian region

Kashagan HUC is nearing completion, current key project is the Browse FEED study for two tension leg platforms in Australia

17.06.2011© Kvaerner 201173

International

Browse Full Field Development Schematic

Two TLPs

17.06.2011© Kvaerner 201174

International

Business area strategy

Penetrate new geographical marketsCurrent focus areas are the markets in Australia and Caspian region and opportunistically in GoM, whereas entry strategies for closed markets such as Russia, West-Africa and Brazil are under consideration

Refine delivery modelIncrease project delivery capabilities through engineering and yard partnerships

Develop new products and market nichesTarget key markets for which Kvaerner offers unique competencies and capabilities, e.g. harsh environment and deepwater

Capture expected market activityCurrent focus is on the expected demand for floaters in open markets such as Australia, in addition to the Caspian yard initiative triggered by the strong outlook for the Caspian field development market and the local presence required to participate

1

2

3

4

17.06.2011© Kvaerner 201175

International

Business area strategy

Norway (Oslo)

Head Office

UK (London)

JV Partner (K-WAC) BD activities Middle East

China (Beijing, Shanghai, Qingdao)

Kvaerner (Sourcing) Partner (COOEC yard)

Australia (Perth)

Kvaerner (BD, proj. mgmt)

Kazakhstan (Aktau) Kvaerner (Caspian BV)

(Contracting) Partner (NCE)

USA (Houston) Kvaerner (EPC Center)

Current markets

Potential markets

Saudia Arabia Kvaerner (repr. office)

17.06.2011© Kvaerner 201176

0

10 000

20 000

30 000

40 000

50 000

60 000

2000 2005 2010 2015 2020Floaters Topsides

International

Offshore market outlook

Focus areas include the Caspian as well as floaters for deepwater regions such as Australia and GoMThe market outlook in the Caspian is expected to be strong with a booming market in the years 2015 – 2019Spending related to Floaters and Topsides is expected to increase sharply in the coming years

Floaters and Topsides GlobalUSD million

Caspian Offshore EPCUSD million

Source: Dcube

0

1 000

2 000

3 000

4 000

5 000

6 000

2000 2005 2010 2015 2020