principles of investment accounting - ohio apt of duties principles of investment accounting -...

TRANSCRIPT

Principles of Investment Accounting

Presented By

United American Capital Corporation

Ohio APT 41st Annual Conference - October 2014

Investment Accounting System

๏ Ensures full disclosure and accountability.

๏ Accurately describes all investments.

๏ Investment Reports are public records and promote “clean” audits.

2

Image courtesy of Pong / FreeDigitalPhotos.net

Principles of Investment Accounting - Presented by United American Capital Corporation

Separation of Duties

Principles of Investment Accounting - Presented by United American Capital Corporation

Investing Authority

Maintains official investment records

Balances with custodian and Investment Manager

State Auditor examines internal records

Registered Investment Advisor

Submits monthly/quarterly reports to Public Entity

Sends transaction advices to Public Entity

Custodian Bank

Issues monthly custody statements

Pays for purchases/delivers sold bonds on settlement date DVP

Brokers/Dealers

Sends trade confirmations to Public Entity and Investment Manager

Affirms trades with custodian

Delivers/Receives bonds vs. Payment (DVP)

3

Investment Reports

๏ Portfolio Inventory

๏ Transaction Activity • Purchases

• Sales

• Maturities

• Called Bonds

๏ Investment Income • Interest Received

• Realized Capital Gains/Losses

Principles of Investment Accounting - Presented by United American Capital Corporation 4

Image courtesy of sheelamohan / FreeDigitalPhotos.net

Components of the Inventory

๏ CUSIP: Letter and number combinations assigned to identify publicly traded securities. Each number is unique to the issue.

๏ Issuer: Entity issuing the bonds.

• Fannie Mae (FNMA), Freddie Mac (FHLMC), Federal Home Loan Bank (FHLB), Federal Farm Credit Bank (FFCB), and Farmer Mac (FAMCA), U.S. Treasury (UST), Municipalities, Corporations

๏ Investment Type: Callable bonds (fixed rate and step-ups), Non callable bonds (or bullets), Discount notes

Principles of Investment Accounting - Presented by United American Capital Corporation 5

Components of the Inventory

๏ Par Value: The value of a bond at maturity; its future value.

๏ Market Value: The liquidation value of each security as of a specific date; may be greater (or less) than your purchase cost due to changing interest rates.

๏ Book Value (Cost): The amount disbursed to purchase a security, including any accrued interest due to the seller on the settlement date.

Principles of Investment Accounting - Presented by United American Capital Corporation 6

Components of the Inventory

๏ Settlement Date: The date in which the securities are delivered versus payment. The legislation requires "delivery vs. payment" (DVP) and the use of a qualified safekeeping agent.

๏ Maturity Date: The future date in which the par amount is paid to the investor. The par value will be paid at maturity, regardless of original purchase cost.

Principles of Investment Accounting - Presented by United American Capital Corporation 7

Components of the Inventory

๏ Coupon (or Rate): The annual percentage amount paid to an investor, based upon the par value of the bond; the rate may be fixed or variable.

๏ Yield to Maturity: The rate of return anticipated on a bond if it is held to maturity. • If coupon < YTM, the bond was purchased at a

discount.

• If coupon > YTM, the bond was purchased at a premium.

• If coupon = YTM, the bond was purchased at par (100).

Principles of Investment Accounting - Presented by United American Capital Corporation 8

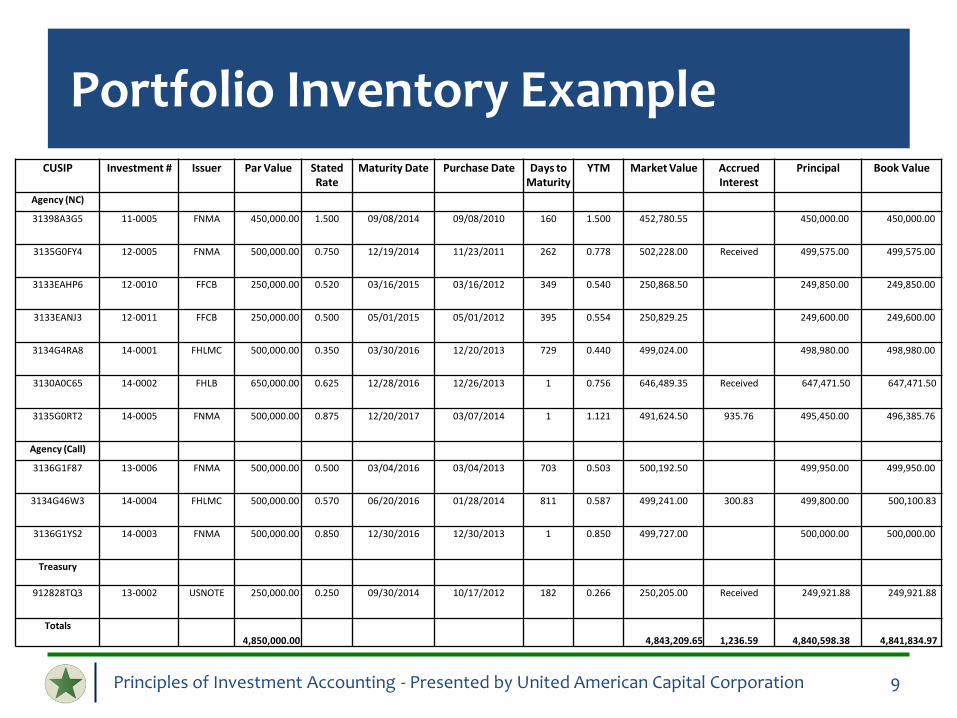

Portfolio Inventory Example

Principles of Investment Accounting - Presented by United American Capital Corporation

CUSIP Investment # Issuer Par Value Stated Rate

Maturity Date Purchase Date Days to Maturity

YTM Market Value Accrued Interest

Principal Book Value

Agency (NC)

31398A3G5 11-0005 FNMA 450,000.00 1.500 09/08/2014 09/08/2010 160 1.500 452,780.55

450,000.00 450,000.00

3135G0FY4 12-0005 FNMA 500,000.00 0.750 12/19/2014 11/23/2011 262 0.778 502,228.00 Received 499,575.00 499,575.00

3133EAHP6 12-0010 FFCB 250,000.00 0.520 03/16/2015 03/16/2012 349 0.540 250,868.50 249,850.00 249,850.00

3133EANJ3 12-0011 FFCB 250,000.00 0.500 05/01/2015 05/01/2012 395 0.554 250,829.25 249,600.00 249,600.00

3134G4RA8 14-0001 FHLMC 500,000.00 0.350 03/30/2016 12/20/2013 729 0.440 499,024.00 498,980.00 498,980.00

3130A0C65 14-0002 FHLB 650,000.00 0.625 12/28/2016 12/26/2013 1 0.756 646,489.35 Received 647,471.50 647,471.50

3135G0RT2 14-0005 FNMA 500,000.00 0.875 12/20/2017 03/07/2014 1 1.121 491,624.50 935.76 495,450.00 496,385.76

Agency (Call)

3136G1F87 13-0006 FNMA 500,000.00 0.500 03/04/2016 03/04/2013 703 0.503 500,192.50 499,950.00 499,950.00

3134G46W3 14-0004 FHLMC 500,000.00 0.570 06/20/2016 01/28/2014 811 0.587 499,241.00 300.83 499,800.00 500,100.83

3136G1YS2 14-0003 FNMA 500,000.00 0.850 12/30/2016 12/30/2013 1 0.850 499,727.00 500,000.00 500,000.00

Treasury

912828TQ3 13-0002 USNOTE 250,000.00 0.250 09/30/2014 10/17/2012 182 0.266 250,205.00 Received 249,921.88 249,921.88

Totals

4,850,000.00 4,843,209.65

1,236.59 4,840,598.38 4,841,834.97

9

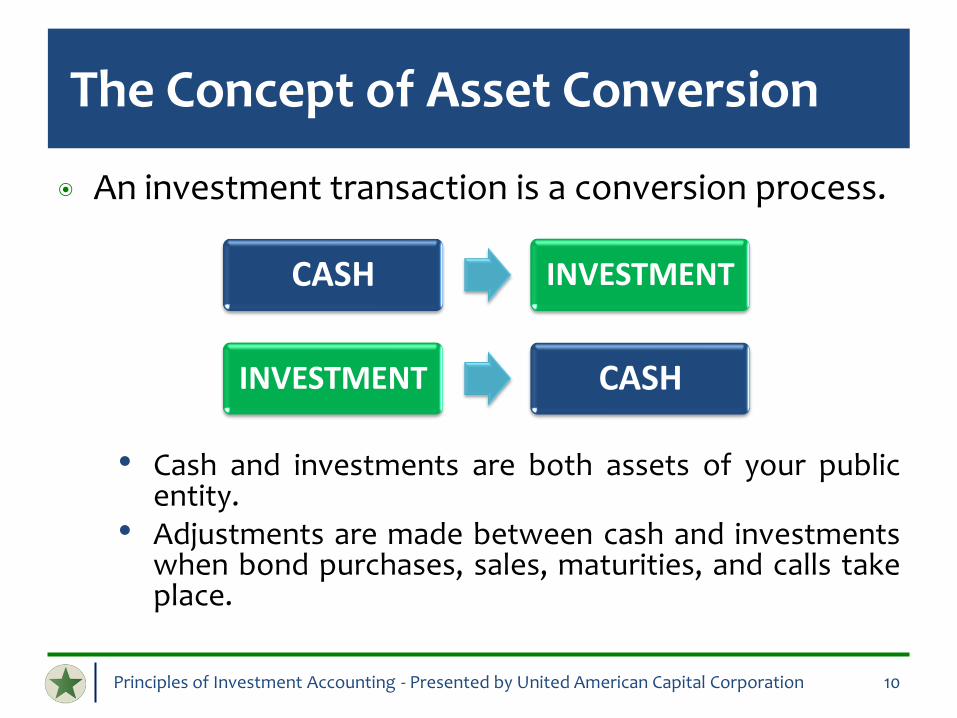

The Concept of Asset Conversion

๏ An investment transaction is a conversion process.

• Cash and investments are both assets of your public entity.

• Adjustments are made between cash and investments when bond purchases, sales, maturities, and calls take place.

Principles of Investment Accounting - Presented by United American Capital Corporation

CASH INVESTMENT

INVESTMENT CASH

10

The Concept of Asset Conversion

๏ The total asset value of the public entity increases when the investment pays interest (or when capital gains are realized).

Principles of Investment Accounting - Presented by United American Capital Corporation

Cash Increases Income is credited.

11

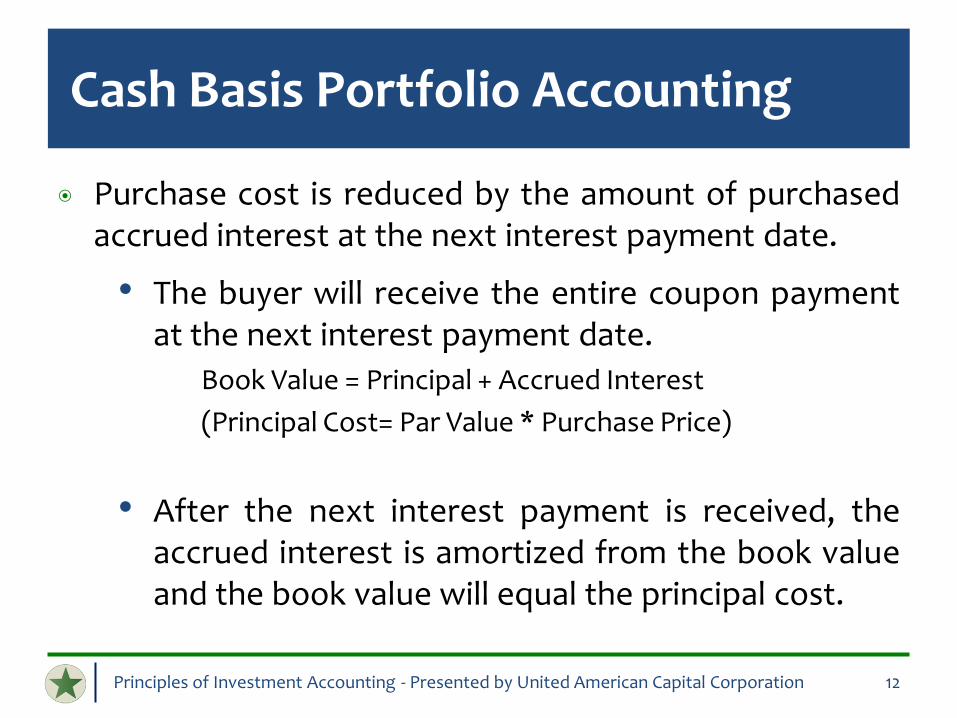

Cash Basis Portfolio Accounting

๏ Purchase cost is reduced by the amount of purchased accrued interest at the next interest payment date.

• The buyer will receive the entire coupon payment at the next interest payment date.

Book Value = Principal + Accrued Interest

(Principal Cost= Par Value * Purchase Price)

• After the next interest payment is received, the accrued interest is amortized from the book value and the book value will equal the principal cost.

Principles of Investment Accounting - Presented by United American Capital Corporation 12

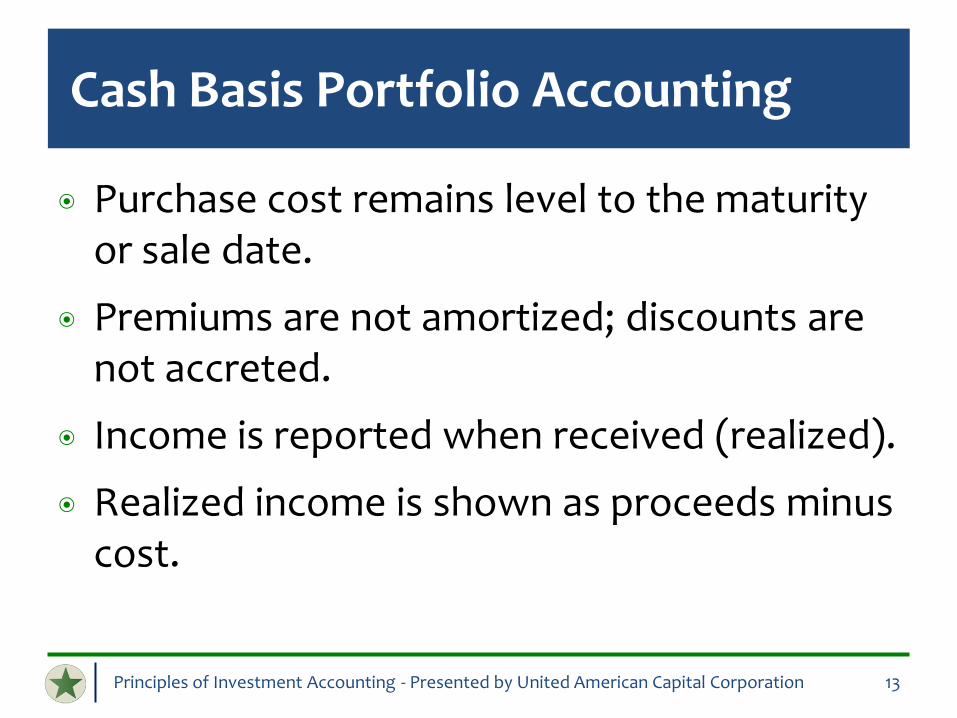

Cash Basis Portfolio Accounting

๏ Purchase cost remains level to the maturity or sale date.

๏ Premiums are not amortized; discounts are not accreted.

๏ Income is reported when received (realized).

๏ Realized income is shown as proceeds minus cost.

Principles of Investment Accounting - Presented by United American Capital Corporation 13

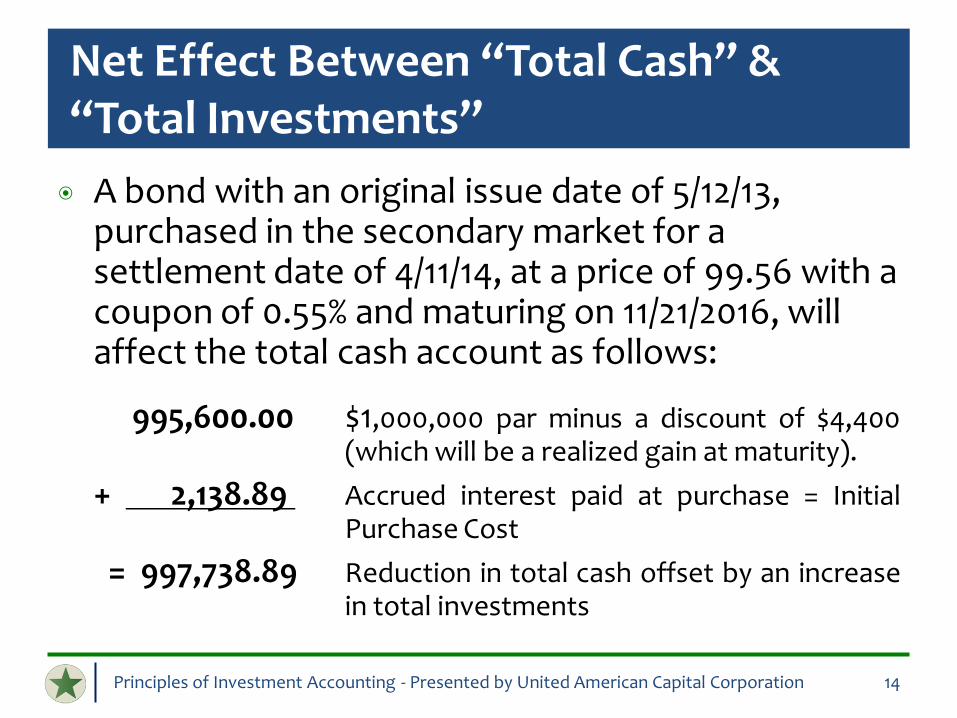

Net Effect Between “Total Cash” & “Total Investments”

๏ A bond with an original issue date of 5/12/13, purchased in the secondary market for a settlement date of 4/11/14, at a price of 99.56 with a coupon of 0.55% and maturing on 11/21/2016, will affect the total cash account as follows:

995,600.00 $1,000,000 par minus a discount of $4,400 (which will be a realized gain at maturity).

+ 2,138.89 Accrued interest paid at purchase = Initial Purchase Cost

= 997,738.89 Reduction in total cash offset by an increase in total investments

Principles of Investment Accounting - Presented by United American Capital Corporation 14

Net Effect Between “Total Cash” & “Total Investments”

๏ At the following interest payment date (05/21/2014), cash and investments are affected as follows:

Gross interest payment received minus accrued interest paid at purchase = net interest income (the “pay-in” amount):

$ 2,750.00 Interest received (credited by the custodian bank)

- 2,138.89 Accrued interest paid at settlement date (4/11/2014)

$ 611.11 Net interest income (Increase in cash offset by a decrease in investment cost)

Principles of Investment Accounting - Presented by United American Capital Corporation 15

Net Effect Between “Total Cash” & “Total Investments”

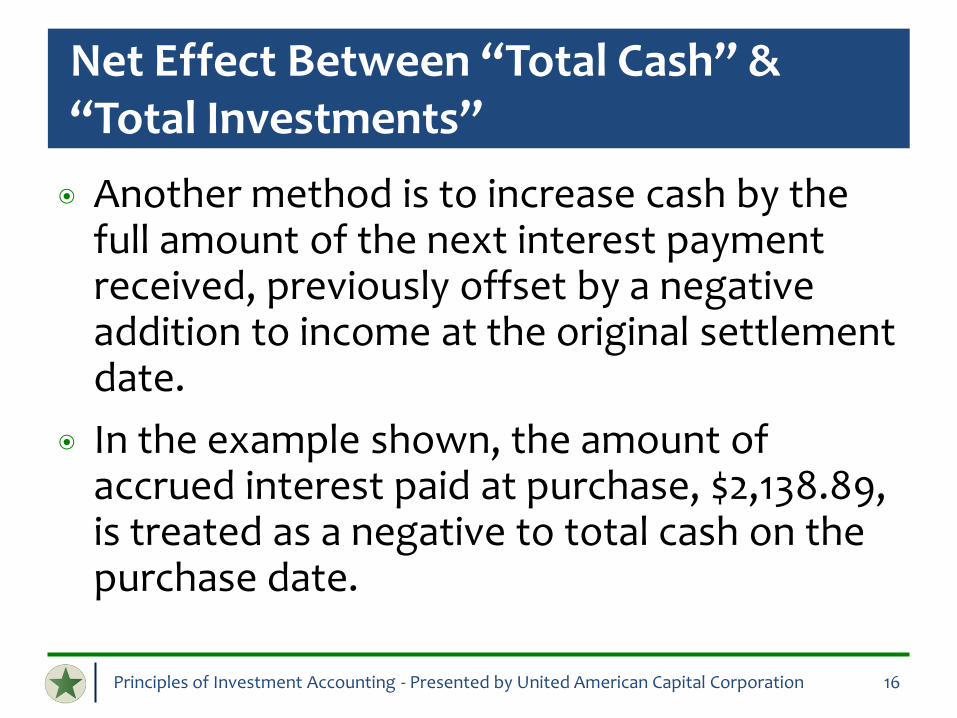

๏ Another method is to increase cash by the full amount of the next interest payment received, previously offset by a negative addition to income at the original settlement date.

๏ In the example shown, the amount of accrued interest paid at purchase, $2,138.89, is treated as a negative to total cash on the purchase date.

Principles of Investment Accounting - Presented by United American Capital Corporation 16

Net Effect Between “Total Cash” & “Total Investments”

๏ A straight interest payment (after the amortization has taken place) is paid-in totally, as an increase in the cash account.

• This amount is recognized even if the amount of interest paid has been totally credited to the money market sweep account within the custody account.

• From an accounting perspective, cash is debited and interest income is credited.

Principles of Investment Accounting - Presented by United American Capital Corporation 17

Accrual Portfolio Accounting

๏ Purchase cost is adjusted daily (“adjusted book value”).

๏ Premiums are amortized over the life of the security.

๏ Discounts accrete over the life of the security.

๏ Interest accrues daily.

๏ Capital gains/losses are based upon adjusted book value.

Principles of Investment Accounting - Presented by United American Capital Corporation 18

Reconciliation Process

๏ Components of the Reconciliation Process:

• Internal Records (the official books subject to audit)

• Custodian Bank – safekeeping of investment assets, purchase cost, income, trade activity

• Investment Advisor (if used) – inventory of assets and individual purchase cost, income, list of transactions

• Additional Records – broker/dealer trade confirms

Principles of Investment Accounting - Presented by United American Capital Corporation 19

Reconciliation Process

๏ A “pay-in” is made by the Public Entity evidencing a receipt of funds.

๏ A pay-in will occur when interest is received and/or capital gains are realized.

๏ It is recommended that a pay-in occurs when a receipt of funds occurs (credited) at the custodian bank. • Periodic pay-ins during the month are acceptable

provided that such transactions are reconciled prior to the pay-in to ensure that the Public Entity’s records balance with the custodian.

Principles of Investment Accounting - Presented by United American Capital Corporation 20

Reconciliation Process

๏ On cash basis accounting, a negative pay-in may occur at maturity if the purchase premium of a bond exceeds the final interest payment amount.

๏ Additionally, in the case of callable securities where a premium has been paid, a lower yield will be realized if the bond is called prior to maturity.

Principles of Investment Accounting - Presented by United American Capital Corporation 21

Common Reconciliation Errors

Principles of Investment Accounting - Presented by United American Capital Corporation

Using market value rather than book value (c0st)

Failing to account for purchased accrued interest

Not recognizing a discount at maturity

Not amortizing a premium paid

Not maintaining supporting documentation

Not recognizing income when received

22

Questions

Principles of Investment Accounting - Presented by United American Capital Corporation 23

Image courtesy of anankkml/FreeDigitalPhotos.net