principles of accounts grade 10 weeks 1-5 - term 3

TRANSCRIPT

1

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 1 LESSON 1

TOPIC: SOURCE DOCUMENT – CASH RECEIPT

CONTENT

A Cash Receipt is a printed acknowledgement of the amount of cash received during a transaction involving the

transfer of cash or cash equivalent.

ACTIVITIES

1. Collect three (3) samples of cash receipts done by your parents or businesses in your community to show evidence of transactions done.

2. Collect three (3) samples of cash bills done by your parents or business in your community.

3. Prepare a cash receipt for an article of your choice that you have sold to a friend.

4. Prepare a cash bill for 5 stationery items to show your understanding of it.

UNIVERSAL SHOPPING PLAZA Leguan Island, Essequibo River.

Receipt # 1593 Date: 25 – 02 – 2021 Received from SHIVNARINE RAMPERSHAD . The sum of three thousand five hundred seventy dollars---------------------------------------------------. In full payment for One (1) Office Computer .

$3 570.00 R. Singh . Signature of Business Owner

$4 Revenue Stamps

2

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 1 LESSON 2

TOPIC: SOURCE DOCUMENT – CHEQUE

CONTENT

A Cheque is an order to the bank (drawee) to pay the payee a stated sum of money from the drawer’s account.

ACTIVITIES

1. Collect three (3) samples of cheques done by your parents or businesses in your community to show evidence of transactions done.

2. Prepare a cheque for an article of your choice that you have sold to a friend.

BANK OF INDUSTRY AND COMMERCE Leguan Island, Essequibo River.

Universal Shopping Plaza Serial #: 57689302 Leguan, Essequibo River. Date: .20 /.02 /2017. Pay to the order of: RABINDRANAUTH SINGH .

The sum of: Two thousand four hundred sixty dollars .

For: goods bought .

$2 460.00 D. Ramlall .

Signature Of Business Owner

120-908-1978

3

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 1 LESSON 3

TOPIC: BOOKS OF ORIGINAL ENTRY – THE CASH BOOK

CONTENT

The Cash Book

The Cash Book is used to record receipts and payments of cash and cheques of a business.

The Cash Book is a combination of the cash account and bank account of a business respectively put together.

The Purpose Of Cash Book

The advantages of having a Cash Book are:

1. Reduces the number of entries in the ledger.

2. Enables division of labour since another person can be entrusted to do the job of recording only cash

transactions.

3. Cross-reference to the Cash and Bank Accounts is made easier with the use of a separate book.

Contra Entries involve cash and bank only.

Let us examine the Two Column Cash Book now.

J. Smith General Ledger

Dr. Cash A/C Page 2 Cr.

Date Details Folio $ Date Details Folio $ 2020 12-01

Capital

GL 2

1000

2020 12-03

Rent

GL 3

100

12-05 Sales GL 5 980 12-06 A. Burton PL 31 220 12-09 G. Motta SL 41 650 12-10 Bank C 500 12-12 Sales GL 5 520 12-13 Motor Exp GL 7 350 12-15 Bank C 750 12-16 C. Lie PL 32 400 12-19 D. Frank SL 43 860 12-20 Pay GL 8 1 250 12-23 GNCB (loan) GL 10 3 550 12-24 Purchases GL 8 680 12-27 O. Khan SL 44 430 12-28 Office Exp GL 11 740

- 12-31 Balance c/d 5 670 8 730 8 730

2021 01-01

Balance

b/d

5 670

4

J. Smith General Ledger

Dr. Bank A/C Page 6 Cr.

Date Details Folio $ Date Details Folio $ 2020 12-02

F. Lai (loan)

GL 4

5 000

2020 12-04

B. Max

PL 30

650

12-07 N. Miller SL 40 620 12-08 Travelling GL 6 240 12-10 Cash C 500 12-11 F. Lai (loan) GL 4 1 000 12-14 P. Jones SL 42 480 12-15 Cash C 750 12-17 Sales GL 5 1 060 12-18 Purchases GL 8 520 12-21 Sales GL 5 960 12-22 Travelling GL 6 240 12-25 Sales GL 5 1 360 12-26 F. Lai (loan) GL 4 1000 12-29 E. Ram SL 45 730 12-30 Purchases GL 8 880

- 12-31 Balance c/d 5 430 10 710 10 710

2021 01-01

Balance

b/d

5 430

J. Smith

Dr. Two Column Cash Book Page 75 Cr.

Date Details Folio Cash Bank Date Details Folio Cash Bank 2020 12-01

Capital

GL 2

1000

2020 12-03

Rent

GL 3

100

12-02 F. Lai (loan) GL 4 5 000 12-04 B. Max PL 30 650 12-05 Sales GL 5 980 12-06 A. Burton PL 31 220 12-07 N. Miller SL 40 620 12-08 Travelling GL 6 240 12-09 G. Motta SL 41 640 12-10 Bank C 500 12-10 Cash C 500 12-11 F. Lai (loan) GL 4 1 000 12-12 Sales GL 5 520 12-13 Motor Expenses GL 7 350 12-14 P. Jones SL 42 480 12-15 Cash C 750 12-15 Bank C 750 12-16 C. Lie PL 32 470 12-17 Sales GL 5 1 060 12-18 Purchases GL 8 520 12-19 D. Frank SL 43 860 12-20 Pay GL 9 1 250 12-21 Sales GL 5 960 12-22 Travelling GL 6 240 12-23 GNCB (loan) GL 10 3 550 12-24 Purchases GL 8 680 12-25 Sales GL 5 1 360 12-26 F. Lai (loan) GL 4 1 000 12-27 O. Khan SL 44 430 12-28 Office Expenses GL 11 740 12-29 E. Ram SL 45 730 12-30 Purchases GL 8 880

12-31 Balance c/d 5 670 5 430 8 730 10 710 8 730 10 710

2021 01-01

Balance

b/d

5 670

5 430

5

ACTIVITY

Wallmart Stationery Plaza records all its cash transactions in a two column cash book. The Cash Book is balanced at the end of each month and balances are carried forward to the next month.

The information below relates to the months of September and October, 2020:

Sept 1 Balances: Bank $8 600, Cash $1 400.

4 Received cheque from B. Small $8 700.

9 Paid light bill by cheque $5 000.

12 Cash sales $12 000.

15 Cash purchases $5 000.

17 Received cheque from J. Murray $3 000.

20 Banked cash $8 000.

23 D. Persaud paid off her account by cash $9 000.

26 Paid G. Gibbon by cheque $1 300.

28 Paid wages by cheque $6 000.

Oct 2 Cash sales $3000.

5 Cash purchases $1 000.

11 Paid travelling by cash $1 500.

16 Received from H. Rally $4 500.

22 Banked cash $10 000.

26 Paid staff by cheque $8 000.

You are required to write up the cash book and balanced it off.

6

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 2 LESSON 1

TOPIC: BOOKS OF ORIGINAL ENTRY – THE CASH BOOK

CONTENT

Discount is a reduction given to us for buying goods in large quantities.

Trade Discount is a reduction given to us for buying goods in wholesale quantities.

Cash Discount is a reduction for making prompt payment with a specific period of time.

Discount Allowed is given to accounts receivable for making prompt payment to the business.

Discount Received is given to the business by its accounts payable for prompt payment done.

Bank Overdraft is a soft loan given to the business by the bank.

ACTIVITY

Write up the Cash Book of Super Stationery Store and balance it off for the month of December, 2020 and show the balances for the new month. Dec. 01 Cash balance b/f $3 500, bank overdraft b/f $5 000. Dec. 02 Cash purchases $820. Dec. 04 Singh who had an account balance of $8 000 paid in full by cheque after deducting 5% cash discount. Dec. 06 Paid rent by cheque $700. Dec. 08 Cash sales $2 020. Dec. 10 Paid M. Harripersaud by cash $1000 on account of $1 250 in full settlement. Dec. 12 Received a cheque of $4 000 from a friend, Sharma as a loan.

Dec. 14 Transferred $2 000 from bank to cash. Dec. 16 Bought goods by cheque $1 300. Dec. 18 Sold goods for cheque $2 460. Dec. 20 Paid Rampersaud $1 400 cash having deducted 10% cash discount. Dec. 22 Cash sales $1 990 paid directly into the bank account. Dec. 24 Cash received from Mc Intosh $960 on account of $1 000 in full settlement. Dec. 26 Dividends of $6 000 posted in the business bank account. Dec. 28 Cash withdrawn for personal use $2 000. Dec. 30 Bank charges as shown on bank statement $280.

7

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 2 LESSON 2

TOPICS: SOURCE DOCUMENT – PETTY CASH VOUCHER BOOKS OF ORIGINAL ENTRY –

PETTY CASH BOOK

CONTENT

A Petty Cash Voucher is usually a small form that is used to document a disbursement (payment) from a petty cash fund. Petty Cash Vouchers are also referred to as petty cash receipts and can be purchased from office supply stores. The Petty Cash Book is used to record small day to day expenditure of the business. The Imprest System is where the main cashier gives the petty cash cashier enough cash to meet the needs for the next period. Advantages of using the petty cash imprest system 1. A junior member of the accounts department, usually called the petty cashier can be given the task of

operating the system thus allowing the cashier to concentrate on other areas of work.

2. Small items of expenditure incurred by the organisation are entered into the petty cash book and only the totals at the end of period are posted to the appropriate accounts in the general ledger.

3. The imprest system enables the cash to be checked at any time since the amount paid out, represented by the petty cash vouchers and the cash in hand should equal the float at the beginning of the period.

8

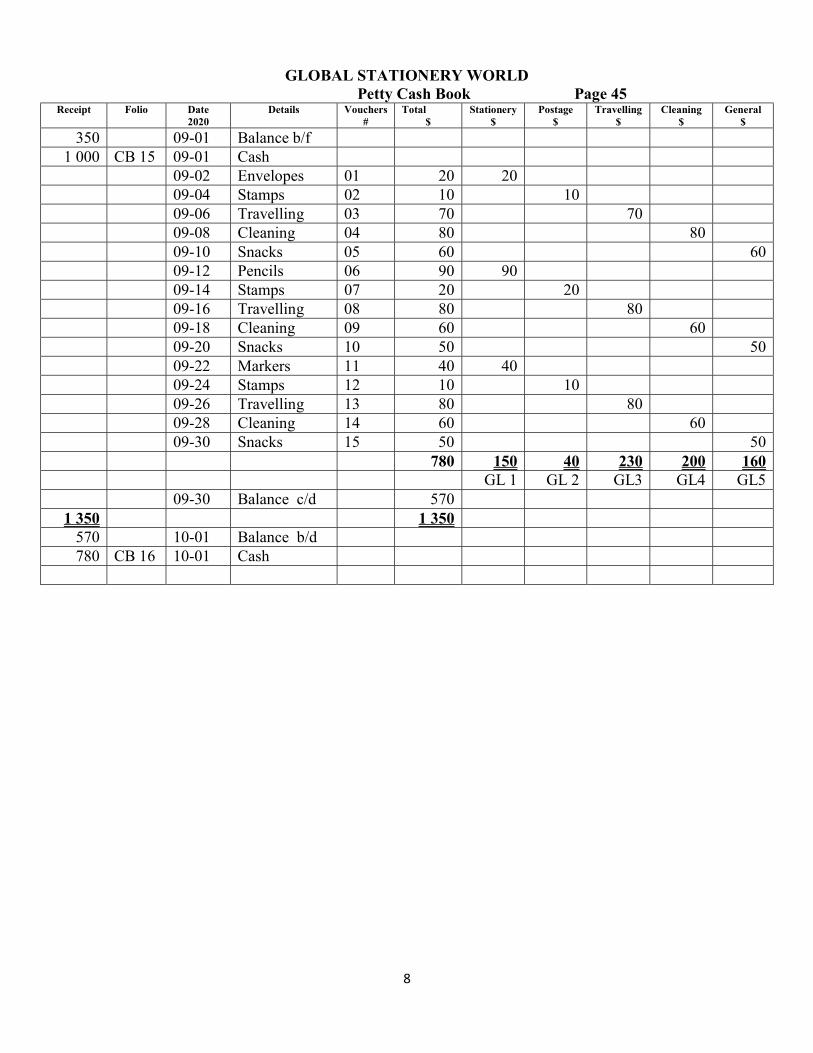

GLOBAL STATIONERY WORLD

Petty Cash Book Page 45 Receipt Folio Date

2020 Details Vouchers

# Total

$ Stationery

$ Postage

$ Travelling

$ Cleaning

$ General

$

350 09-01 Balance b/f 1 000 CB 15 09-01 Cash

09-02 Envelopes 01 20 20 09-04 Stamps 02 10 10 09-06 Travelling 03 70 70 09-08 Cleaning 04 80 80 09-10 Snacks 05 60 60 09-12 Pencils 06 90 90 09-14 Stamps 07 20 20 09-16 Travelling 08 80 80 09-18 Cleaning 09 60 60 09-20 Snacks 10 50 50 09-22 Markers 11 40 40 09-24 Stamps 12 10 10 09-26 Travelling 13 80 80 09-28 Cleaning 14 60 60 09-30 Snacks 15 50 50 780 150 40 230 200 160 GL 1 GL 2 GL3 GL4 GL5 09-30 Balance c/d 570

1 350 1 350 570 10-01 Balance b/d

780 CB 16 10-01 Cash

9

ACTIVITIES

Write up the Petty Cash Book with analysis columns for office expenses, motor expenses, cleaning expenses

and casual labour. The cash float is $600 and the amount spent is reimbursed on 30 June.

Show the balance carried down to 1 July, 2020.

June 1 H. Sangster – casual labour 13

June 2 Stationery 22

June 3 Unique Motors – motors repairs 30

June 4 Cleaning materials 16

June 6 Envelopes 14

June 8 Petrol 28

June 11 J. Hogan – casual labour 15

June 12 Paperclips 12

June 13 Mrs Bells – cleaner 27

June 14 Petrol 11

June 16 Stationery 31

June 18 Petrol 29

June 21 Motor Vehicle Taxation 50

June 22 T. Cooke – casual labour 21

June 23 Mrs Bells – cleaner 27

June 24 P. King – casual labour 19

June 27 Copy paper 27

June 28 Flat cars – motor repairs 21

June 29 Petrol 12

June 30 J. Young – casual labour 16

10

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 2 LESSON 3

TOPIC: SOURCE DOCUMENTS: CAPITAL PURCHASES INVOICE, CAPITAL SALES INVOICE,

LETTERS OF AGREEMENT / SETTLEMENT

CONTENT

CAPITAL PURCHASES INVOICE is a document issued to a business for purchasing a non-current asset, for

example: motor vehicle

CAPITAL SALES INVOICE is a document issued by the business for selling a non-current asset to a person,

for example: computer and accessories.

LETTERS OF AGREEMENT / SETTLEMENT is a document showing the arrangements or terms of

agreement or terms of settlement between the buyer and seller. It is a legal and binding agreement between the

parties involved.

ACTIVITIES 1. Prepare a Capital Purchases Invoice for a Motor Vehicle that cost $550 000 from Transpacific Motors Ltd that . you bought for your business on 15 – 10 – 2020. Make sure all components of the invoice are evident to show . your understanding. 2. Prepare a Capital Sales Invoice for an Office Desk with Chair that cost $140 000 that you sold to Computer . World on 23 – 11 – 2020. Make sure all components of the invoice are evident to show your understanding. 3. Draft a Letter Of Agreement showing a settlement of $3570 between yourself and a business of your choice to . show your understanding. Make it very simple as far as possible. Note: (i) Consult with your teacher. . (ii) Check the internet for sample and further guidance.

11

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 3 LESSON 1

TOPIC: BOOKS OF ORIGINAL ENTRY – THE GENERAL JOURNAL

CONTENT

The purchase of a non-current asset on credit 2019 – 07 – 05: Mr. A. Benjamin bought a motor car on credit from Auto Sales Ltd $10 500. Prepare the journal entry and post the entries into the respective accounts.

Mr. A. Benjamin The Journal

Date Particulars Folio Dr. Cr. 2019 - - $ $

07 – 05 Motor Vehicles a/c GL 1 10 500 Auto Sales Ltd a/c PL 2 10 500 Purchase of motor car on credit

Capital Purchases Invoice # 4352

General Journal is a day to day diary of the business.

General Journal records all other transactions that do not passed through the other books of original entry.

Ledgers

General Ledger

Uses of General Journal

1. Purchase & Sale Of Non-Current Assets On Credit

2. Writing Off Of Bad Debts

3. Other Items: Adjustments to any of the entries in the ledgers

4. Opening Entries – the entries needed to open a new set of books

5. Correction Of Errors

12

Mr. A. Benjamin General Ledger

Dr. Motor Vehicles A/C Page 1 Cr.

Purchases Ledger Dr. Auto Sales Ltd A/C Page 2 Cr.

ACTIVITIES 2020 – 06 – 04: Mrs. G. Williams bought furniture and fittings on credit from Ramroop Furniture Store costing $4 770. Prepare the journal entry and post the entries into the respective accounts. 2020 – 08 – 07: Mr. S. Mohamed bought an excavator from MACROP on credit for $8 250. Prepare the journal entry and post the entries into the respective accounts. 2020 – 10 – 09: Miss T. Whyte bought a computer and accessories on credit from Starr Computer World $6 940. Prepare the journal entry and post the entries into the respective accounts.

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 05 Auto Sales Ltd PL 2 10 500

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 05 Motor Vehicles GL 2 10 500

13

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 3 LESSON 2

TOPIC: BOOKS OF ORIGINAL ENTRY – THE GENERAL JOURNAL

CONTENT

The sale of a non-current asset on credit 2019 – 07 – 08: Mr. A. Benjamin sold office furniture on credit to B. F. Khan costing $3 060. Prepare the journal entry and post the entries into the respective accounts.

Mr. A. Benjamin

The Journal Date Particulars Folio Dr. Cr. 2019 - - $ $

07 – 08 B. F. Khan a/c SL 3 3 060 Office Furniture a/c GL 4 3 060 Sold office furniture on credit

Capital Sales Invoice # 2143

Mr. A. Benjamin Sales Ledger

Dr. B. F. Khan A/C Page 3 Cr.

General Ledger Dr. Office Furniture A/C Page 4 Cr.

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 08 Office Furniture GL 4 3 060

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 05 B. F. Khan SL 3 3 060

14

ACTIVITIES 2020 – 06 – 07: Mrs. G. Williams sold office equipment on credit to M. Fitzpatrick costing $2 740. Prepare the journal entry and post the entries into the respective accounts. 2020 – 08 – 10: Mr. S. Mohamed sold machinery to N. Singh on credit $5 190. Prepare the journal entry and post the entries into the respective accounts. 2020 – 10 – 13: Miss T. Whyte sold motor vehicle costing $7 000 to D. Murray on credit. Prepare the journal entry and post the entries into the respective accounts.

15

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 3 LESSON 3

TOPIC: BOOKS OF ORIGINAL ENTRY – THE GENERAL JOURNAL

CONTENT

Writing off of Bad Debts 2019 – 07 – 10: A debt of $220 owing to Mr. A. Benjamin by J. Oddy was written off as a bad debt. Prepare the journal entry and post the entries into the respective accounts.

Mr. A. Benjamin The Journal

Date Particulars Folio Dr. Cr. 2019 - - $ $

07 – 10 Bad Debts a/c GL 5 220 J. Oddy a/c SL 21 220 Debt written off as bad.

See letter in file O-691.

Mr. A. Benjamin General Ledger

Dr. Bad Debts A/C Page 5 Cr.

Mr. A. Benjamin

Sales Ledger Dr. J. Oddy A/C Page 21 Cr.

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 10 J.Oddy SL 21 220

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 01 Balance b/d 220 07 – 10 Bad Debts GL 5 220

16

ACTIVITIES 2020 – 06 – 09: A debt of $510 owing to Mrs. G. Williams was written off as bad for K. Rampershad. Prepare the journal entry and post the entries into the respective accounts. 2020 – 08 – 12: W. Spencer owed Mr. S. Mohamed $1 350. He was unable to pay off his debt and it was written off as bad. Prepare the journal entry and post the entries into the respective accounts. 2020 – 10 – 15: Miss T. Whyte was owed $820 by G. Munialall. He was unable to pay his debt and it was written off as bad. Prepare the journal entry and post the entries into the respective accounts.

17

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 4 LESSON 1

TOPIC: BOOKS OF ORIGINAL ENTRY – THE GENERAL JOURNAL

CONTENT

Other Items 2019 – 07 – 13: V. Smith, a debtor owed Mr. A. Benjamin $2 460. She was unable to pay her debt. Mr. A. Benjamin took an office table and a pair of chairs from her and cancelled her debt. Prepare the journal entry and post the entries into the respective accounts.

Mr. A. Benjamin The Journal

Date Particulars Folio Dr. Cr. 2019 - - $ $

07 – 13 Office Furniture a/c GL 6 2 460 V. Smith a/c SL 22 2 460 Accepted office table and chairs in

full settlement of debt. See letter dated 13/07/2019.

Mr. A. Benjamin General Ledger

Dr. Office Furniture A/C Page 6 Cr.

Mr. A. Benjamin Sales Ledger

Dr. V. Smith A/C Page 21 Cr.

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 13 V. Smith SL 22 2 460

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 01 Balance b/d 2 460 07 – 13 Office Furniture GL 6 2 460

18

ACTIVITIES 2020 – 06 – 09: A. Small, a debtor owed $1130 to Mrs. G. Williams. He was unable to pay off his debt and offered a motor vehicle in full settlement of his debt. His offered was accepted by Mrs. G. Williams. Prepare the journal entry and post the entries into the respective accounts. 2020 – 08 – 12: C. Ramkissoon, a debtor owed Mr. S. Mohamed $2 660. She was unable to pay off her debt and offered office equipment in full settlement of it. Mr. S. Mohamed accepted the offer given to him. Prepare the journal entry and post the entries into the respective accounts. 2020 – 10 – 15: Miss T. Whyte was owed $3 030 by M. Nandram, a debtor. She was unable to pay her debt and agreed to offer fixtures and fittings in full settlement of her debt. The offer was accepted by Miss T. Whyte. Prepare the journal entry and post the entries into the respective accounts.

19

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 4 LESSON 2

TOPIC: BOOKS OF ORIGINAL ENTRY – THE GENERAL JOURNAL

CONTENT

Other Items 2019 – 07 – 16: Mrs. P. Harper, a creditor took over Mr. A. Benjamin’s business, to whom a debt of $2740 is to be paid. Prepare the journal entry and post the entries into the respective accounts.

The Journal

Date Particulars Folio Dr. Cr. 2019 - - $ $

07 – 16 A. Benjamin SL 7 2 740 P. Harper SL 8 2 740 Transfer of indebtedness as per

letter ref A/0192

Dr. A. Benjamin A/C Page 7 Cr.

Dr. P. Harper A/C Page 21 Cr.

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 16 P. Harper SL 8 2 740 07- 16 Balance b/d 2 740

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 16 A. Benjamin SL 7 2 740

20

ACTIVITIES 2020 – 06 – 13: S. Dhanessar, a creditor took over Mrs. G. Williams business to whom a debt of $1 830 is to be paid. Prepare the journal entry and post the entries into the respective accounts. 2020 – 08 – 15: Mr. S. Mohamed’s business is taken over by E. Yakob, a creditor to whom a debt of $2 610 is to be paid. Prepare the journal entry and post the entries into the respective accounts. 2020 – 10 – 18: A creditor, J. Hodge took over Miss T. Whyte’s business to whom a debt of $3 390 is to be paid. Prepare the journal entry and post the entries into the respective accounts.

21

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 4 LESSON 3

TOPIC: BOOKS OF ORIGINAL ENTRY – THE GENERAL JOURNAL

CONTENT

Other Items 2019 – 07 – 19: Mr. A. Benjamin returned office furniture costing $5 000 he bought from Unique Office Supplies because they were found to be suitable in his office. Prepare the journal entry and post the entries into the respective accounts.

Mr. A. Benjamin The Journal

Date Particulars Folio Dr. Cr. 2019 - - $ $

07 – 19 Unique Office Supplies PL 9 5 000 Office Furniture GL 10 5 000 Returned faulty office furniture.

Full allowance given. See letter dated 19/07/2019.

Mr. A. Benjamin Purchases Ledger

Dr. Unique Office Supplies A/C Page 9 Cr.

General Ledger Dr. Office Furniture A/C Page 10 Cr.

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 19 Office Furniture GL 10 5 000 07- 01 Balance b/d 5 000

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2019 $ 2019 $

07 – 19 Unique Office Supplies PL 9 5 000

22

ACTIVITIES 2020 – 06 – 15: Mrs. G. Williams returned office equipment previously bought from Computer Trading Plus costing $8 250 and full allowance was given to her. Prepare the journal entry and post the entries into the respective accounts. 2020 – 08 – 17: Furniture and fittings costing $10 630 was returned to Singh Furniture World by Mr. S. Mohamed who found them to be damaged, full allowance given. Prepare the journal entry and post the entries into the respective accounts. 2020 – 10 – 20: A motor vehicle costing 9 500 was returned to Auto Spares Ltd, it was not functioning to capacity and full allowance was granted to Miss T. Whyte for it. Prepare the journal entry and post the entries into the respective accounts.

23

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 5 LESSON 1

TOPIC: BOOKS OF ORIGINAL ENTRY – THE GENERAL JOURNAL

CONTENT

Opening Entries

K. Small, after being in business for the last 5 years without keeping proper records, now decides to keep a

double entry set of books.

On 1 July, 2020 he establishes that that his assets and liabilities are as follows:

Assets: Motor Van $48 400, Furniture & Fittings $7 000, Inventory $3 900, Accounts receivable: B. Blake $950,

. E. Gibbson $450, Bank $5 080, Cash $3 230.

Liabilities: Accounts payable: M. Lee $1 290, C. Shaw $4 950.

K. Small The General Journal Page 1

Date Details Folio Dr Cr 2020 - - $ $

07 – 01 Motor Van GL 10 48 400 Furniture & Fittings GL 11 7 800 Inventory GL 12 3 600 Accounts receivable: B. Blake SL 25 1950 E. Gibbson SL 26 1340 Bank CB 33 5 080 Cash CB 33 3 230 Accounts payable: M. Lee PL 41 2 790 C. Shaw PL 42 4 910 Capital GL 13 63 700 Assets and Liabilities at this date

entered to open the books.

71 400 71 400

24

K.Small

General Ledger

DR. Motor Van A/C Page 10 CR.

DR. Furniture & Fittings A/C Page 11 CR.

DR. Inventory A/C Page 12 CR.

DR. Capital A/C Page 13 CR.

Sales Ledger

DR. B. Blake A/C Page 25 CR.

DR. E. Gibbson A/C Page 26 CR.

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2020 - - $

07 – 01 Balance J 1 48 400

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2020 - - $

07 – 01 Balance J 1 7 800

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2020 - - $

07 – 01 Balance J 1 3 600

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2020 - - $ 07 – 01 Balance J 1 63 700

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2020 - - $

07 – 01 Balance J 1 1 950

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2020 - - $

07 – 01 Balance J 1 1 340

25

K.Small

Purchases Ledger

DR. M. Lee A/C Page 41 CR.

DR. C. Shaw A/C Page 42 CR.

DR. Cash Book Page 33 CR.

ACTIVITIES 1. Miss S. Hardat’s financial position at 1 January, 2020 was as follows:

$ Bank 2 910 Cash 1 600 Equipment 20 500 Premises 25 000 Accounts payable: R. Smith 1 890 D. Thomas 1 610 Accounts receivable: J. Carnegie 1 540 Loan from: J. Higgins 6 000

(a) Show the opening entries needed to open a double entry set of books for Miss S. Hardat.

(b) Open up the necessary accounts in Miss S. Hardat’s ledgers.

2. The following information relates to Mr. B. Jagdeo who commenced business on 1 July, 2020. Machinery $60 000, Office Furniture $40 000, Inventory $15 000, Bank $8 000, Cash $3 000. Accounts Payable $10 500, Loan from NBIC $20 000.

Show the opening entries in the General Journal and post in the Ledger accounts.

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2020 - - $ 07 – 01 Balance J 1 2 790

DATE DETAILS FOLIO AMT DATE DETAILS FOLIO AMT 2020 - - $ 07 – 01 Balance J 1 4 910

DATE DETAILS FOLIO CASH BANK DATE DETAILS FOLIO CASH BANK

2020 - - $ $ 07-01 Balance J 1 3 230 5 080

26

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 5 LESSON 2

TOPIC: CONTROL ACCOUNTS – SALES LEDGER CONTROL ACCOUNT

CONTENT

The Sales Ledger Control Account is also known as the Accounts Receivable Control Account.

Sales Ledger Control Source Opening accounts receivable List of customers’ balances drawn up at the end of the previous period. Credit sales Total from sales day book (journal). Sales returns (Returns Inwards) Total of sales returns day book (journal). Cheques received Cash Book: bank column on received side. List extracted or total of a

special column which has been included in the cash book. Cash received Cash Book: cash column on received side. List extracted or total of a

special column which has been included in the cash book. Discount allowed Total of discount allowed column in the cash book. Closing accounts receivable List of customers’ balances drawn up at the end of the period.

F. Hollingsworth maintains control accounts for his business for the month of March, 2020.

The following information relates to his business:

2020 $ March 1 Sales ledger balance 4 560 March 31 Total of entries for the month: Sales Journal 10 870 Sales Returns Day Book 460 Cheques and cash received from customers 9 615 Discounts allowed 305 Sales ledger balance 5 050

Prepare the Accounts Receivable Control Account.

27

F. Hollingsworth General Ledger

Dr. Accounts Receivable Control Account Page 35 Cr. Date Details Folio Amt Date Details Folio Amt 2020 - - $ 2020 - - $

03 - 01 Balance b/f 4 560 03 - 31 Sales Returns SRDB 2 460 03 - 31 Sales SJ 1 10 870 03 - 31 Bank & Cash CB 3 9 615

03 - 31 Discounts allowed GL 4 305 03 - 31 Balance c/f 5 050 15 430 15 430

04 - 01 Balance b/f 5 050

ACTIVITIES 1. The following information was provided by Talco Enterprises and records on the books for the month

of July, 2020. 2020 $ July 1 Sales ledger debit balance 7 500 Sales ledger credit balance 45

July31 Total cheques from accounts receivable 9750 Total cash from accounts receivable 300 Credit sales for the month 9 075 Bad debts written off 525 Dishonoured cheques 53 Sales returns 180 Discount allowed 360 Sales ledger debit balance 6 721 Sales ledger credit balance 1 253

Prepare the Accounts Receivable Control Account.

2. Quality Stationery Mart, whose sales are all on credit, prepares Accounts Receivable Control Account at the end of every month.

At the end of September, 2020 Quality Stationery Mart provided the following information:

Opening balances 9 360 (Dr), 470 (Cr) Sales for the month 87 890 Sales returns 1 330 Receipts from customers 69 110 Discount allowed 1 200 Bad debts 1 320 Customer’s cheque returned 970 Closing balance 550 (Cr)

Prepare the Accounts Receivable Control Account.

28

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

PRINCIPLES OF ACCOUNTS

TERM 3

GRADE 10

WEEK 5 LESSON 3

TOPIC: CONTROL ACCOUNTS – PURCHASES LEDGER CONTROL ACCOUNT

CONTENT

The Purchases Ledger Control Account is also known as the Accounts Payable Control Account.

Purchases Ledger Control Source Opening accounts payable List of suppliers’ balances drawn up at the end of the previous period. Credit purchases Total from purchases day book (journal). Purchases returns(Returns Outwards) Total of purchases returns day book (journal). Cheques paid Cash Book: bank column on payments side. List extracted or total of a

special column which has been included in the cash book. Cash paid Cash Book: cash column on payments side. List extracted or total of a

special column which has been included in the cash book. Discount received Total of discount received column in the cash book. Closing accounts payable List of suppliers’ balances drawn up at the end of the period.

F. Hollingsworth maintains control accounts for his business for the month of March, 2020.

The following information relates to his business:

2020 $ March 1 Purchases ledger balance 3 890 March 31 Total of entries for the month: Purchases Journal 5 640 Purchases Returns Day Book 315 Cheques and cash paid to suppliers 5 230 Discounts received 110 Purchases ledger balance 3 875

Prepare the Accounts Payable Control Account.

29

F. Hollingsworth General Ledger

Dr. Accounts Payable Control Account Page 45 Cr. Date Details Folio Amt Date Details Folio Amt 2020 - - $ 2020 - - $

03 - 31 Purchases Returns PRDB 2 315 03 - 01 Balance b/f 3 890 03 - 31 Bank & Cash CB 3 5 230 03 - 31 Purchases PJ 1 5 640 03 - 31 Discounts received GL 5 110 03 - 31 Balance c/f 3 875

9 530 9 530 04 - 01 Balance b/f 3 875

ACTIVITIES

1. L. Somerset presented the following information for the month of October, 2020.

$ Accounts Payable Control Account credit balance b/d 25 400 Accounts Payable Control Account debit balance b/d 1 450 Credit purchases 123 900 Purchases returns 1 200 Cheques payments done 100 300 Discount received 2 500 Refund by cheque from accounts payable due to damaged item 1 180 Cheque returned by accounts payable – presented too late to the bank 3300 Set off credit amount between sales ledger and purchases ledger 620 Received from accounts payable due to overpayment 280

Prepare the Accounts Payable Control Account.

2. The following information relates to RDC Co. Ltd who maintains Accounts Payable Control Account for the month of December, 2020.

Opening balances 5 100 (Cr.), 310 (Dr.) Purchases for the month 63 720 Purchases returns 620 Cheques and Cash payments 59 970 Discount received 1 200 Prepayment by cheque to suppliers 3 450 Late payment charge 40 Closing balance 270 (Dr.)

Prepare the Accounts Payable Control Account.

1

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 6 LESSON 1

TOPIC: CONTROL SYSTEMS

CONTENT

BANK RECONCILIATION STATEMENT

Students need to have a comprehensive knowledge of the terms associated with this topic.

ACTIVITIES

Define the following terms and give examples where applicable.

Cash Book Open Cheque Updated Cash Book Crossed Cheque Bank Statement Dishonoured Cheque Bank Reconciliation Statement Stale Cheque Bank Balance Unpresented Cheque Bank Overdraft Uncredited Cheque / Bank Lodgment Bank Giro Credit Standing Order Bank Charges Credit Transfer ATM Debit Transfer

2

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 6 LESSON 2

TOPIC: CONTROL SYSTEMS

CONTENT

BANK RECONCILIATION STATEMENT

Treatment with Balances in the Cash Book and on the Bank Statement

T. Persaud

The Cash Book

Dr. Bank Column Only Cr.

Date Details Amount Date Details Amount 2020 $ 2020 $ 02-01 Balance b/f 1 740 02-01 A. Dailey 349 02-07 T. J. Masters 88 02-07 R. Mason 33 02-22 J. Ellis 73 02-22 G. Small 115 02-25 K. Wood 249 02-28 Balance c/d 1 831 02-27 M. Barrett 178 -

. 2 328 2 328 03-01 Balance c/d 1 831

T. Persaud

Bank Statement

Date Dr. Cr. Balance 2020 $ $ $ 02-01 Balance b/f 1 740 02-07 Cheque 88 1 828 02-11 A. Dailey 349 1 479 02-20 R. Mason 33 1 446 02-22 Cheque 73 1 519 02-28 Credit transfer: J. Walters 54 1 573 02-28 Bank Charges 22 1 551

3

You are required to:

1. Update the Cash Book.

2. Prepare the Bank Reconciliation Statement.

T. Persaud

The Cash Book

Dr. Bank Column Only Cr.

Date Details Amount Date Details Amount 2020 - $ 2020 - $ 02-28 Totals so far 2 328 02-28 Totals so far 497 02-28 J. Walters 54 02-28 Bank Charges 22

02-28 Balance c/d 1 863 2 382 2 382

03-01 Balance b/d 1 863

T. Persaud

Bank Reconciliation Statement

As at 28 – 02 – 2020

Balance as per Cash Book 1863 Add: Unpresented Cheque 115 1978 Less: Bank Lodgments (249 + 178) 427 Balance as per Bank Statement 1551

T. Persaud

Bank Reconciliation Statement

As at 28 – 02 – 2020

Balance as per Bank Statement 1551 Add: Bank Lodgments (249 + 178) 427 1978 Less: Unpresented Cheque 115 Balance as per Cash Book 1863

4

ACTIVITIES

The following are extracts of the Cash Book and Bank Statement of S. Dhanessar.

S. Dhanessar

The Cash Book

Dr. Bank Column Only Cr.

Date Details Amount Date Details Amount 2020 - $ 2020 - $ 05-01 Balance b/f 3 500 05-03 Rent 400 05-12 Sales 2 500 05-10 Salary 1 200 05-21 Winston 1 100 05-16 Thomas 700 05-27 Sales 1 800 05-26 James 800

-. 05-28 Sanjana 500 - 05-31 Balance c/d 5 300 8 900 8 900

06-01 Balance b/d 5 300

S Dhanessar

Bank Statement

Date Dr. Cr. Balance 2020 $ $ $ 05-01 Balance b/f 3 500 05-03 Cheque # 45001 400 3 100 05-10 Cheque # 45002 1 200 1 900 05-12 Cash 2 500 4 400 05-16 Cheque # 45003 700 3 700 05-21 Cheque # 73001 Winston 1 100 4 800 05-25 Insurance 680 4 120 05-27 Dividend 320 4 440 05-29 Bank Charges 20 4 420

You are required to:

1. Update the Cash Book.

2. Prepare the Bank Reconciliation Statement.

5

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 6 LESSON 3

TOPIC: CONTROL SYSTEMS

CONTENT

BANK RECONCILIATION STATEMENT

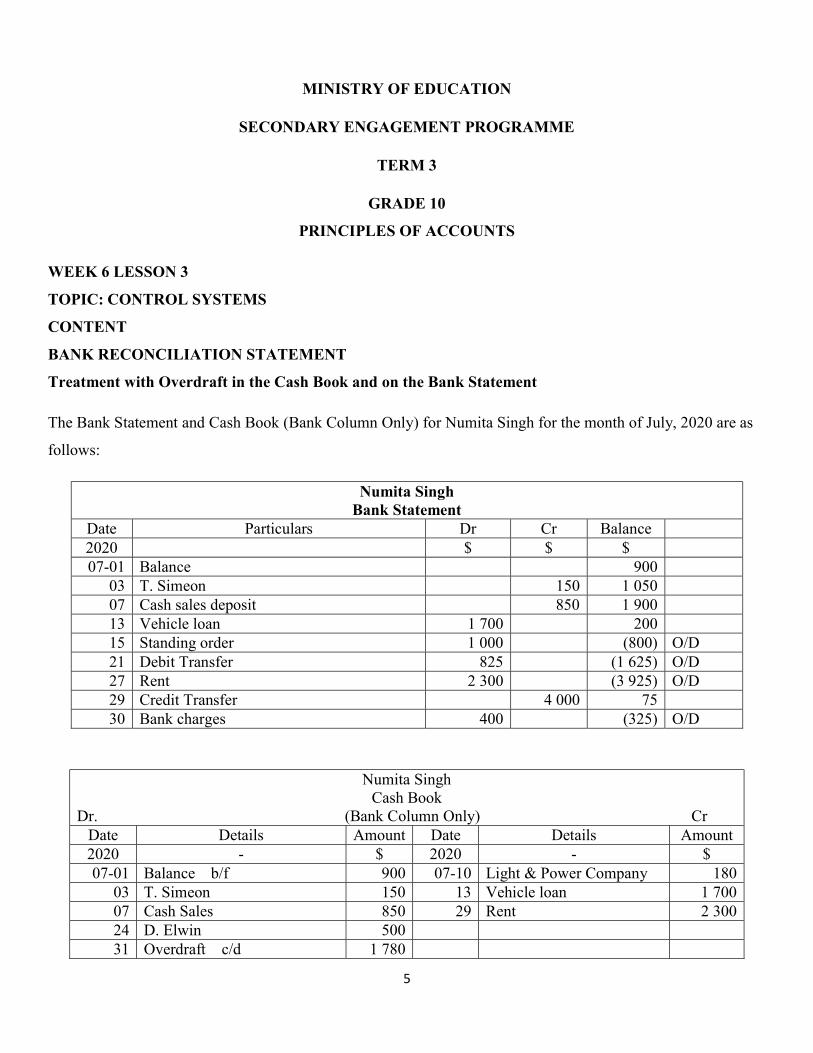

Treatment with Overdraft in the Cash Book and on the Bank Statement

The Bank Statement and Cash Book (Bank Column Only) for Numita Singh for the month of July, 2020 are as

follows:

Numita Singh Bank Statement

Date Particulars Dr Cr Balance 2020 $ $ $ 07-01 Balance 900

03 T. Simeon 150 1 050 07 Cash sales deposit 850 1 900 13 Vehicle loan 1 700 200 15 Standing order 1 000 (800) O/D 21 Debit Transfer 825 (1 625) O/D 27 Rent 2 300 (3 925) O/D 29 Credit Transfer 4 000 75 30 Bank charges 400 (325) O/D

Numita Singh Cash Book

Dr. (Bank Column Only) Cr Date Details Amount Date Details Amount 2020 - $ 2020 - $ 07-01 Balance b/f 900 07-10 Light & Power Company 180

03 T. Simeon 150 13 Vehicle loan 1 700 07 Cash Sales 850 29 Rent 2 300 24 D. Elwin 500 31 Overdraft c/d 1 780

6

4 180 4 180 08-01 Overdraft b/d 1 780

You are required to: 1. Update the Cash Book. 2. Prepare the Bank Reconciliation Statement

Numita Singh Adjusted Cash Book

Dr. (Bank Column Only) Cr Date Details Amount Date Details Amount 2020 - $ 2020 - $ 08-01 Credit Transfer 4 000 08-01 Overdraft b/d 1 780

01 Overdraft c/d 5 01 Standing Order 1 000 01 Debit Transfer 825 01 Bank Carges 400 4 005 4005

01 Overdraft b/d 5

Numita Singh Bank Reconciliation Statement

As at 31 – 07 – 2020 $ Overdraft as per Cash Book 5 Add: Bank Lodgment 500 505 Less: Unpresented Cheque 180 Overdraft as per Bank Statement 325

Numita Singh Bank Reconciliation Statement

As at 31 – 07 – 2020 Overdraft as per Bank Statement 325 Add: Unpresented Cheque 180 505 Less: Bank Lodgment 500 Overdraft as per Cash Book 5

7

ACTIVITIES

In July, 2020 Chintamani’s Cash Book (Bank Column Only) showed an overdraft of $3 400 which did not agree

with the overdraft on his Bank Statement. In checking his Cash Book with his Bank Statement,

Mr. Chintamani observed the following:

A cheque paid to A. Rambajue for $1 238 was correctly entered in the bank statement but recorded in the

cash book as $1 328.

Bank charges for the month of $100 were entered on the bank statement but recorded in the cash book.

The bank paid Chintamani’s insurance of $900 as instructed by standing order.

Deposits of $8 000 made to the bank account on July 29 did not appear on the bank statement.

Dividends of $2 100 from Star Co. Ltd. Was paid directly to Chintamani’s bank account.

Four cheques totaling $5 200 have not been presented to the bank for payment.

A cheque for $300 received from B. Smith on July 3 had been returned by the bank for insufficient funds.

You are required to:

1. Update the Cash Book.

2. Prepare the Bank Reconciliation Statement.

8

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 7 LESSON 1

TOPIC: ERRORS THAT DO NOT AFFECT THE TRIAL BALANCE AGREEMENT

CONTENT

ERRORS OF COMMISSION – where the correct amount is entered but in the wrong person’s account.

For example: 2020 – 08 – 13: B. F. Khan paid her account of $500 cash. It was correctly recorded in the Cash

Book but entered in B. F. Mohamed’s account by mistake.

Accounting Entries Explanation

Debit B. F. Mohamed’s Account To cancel out the error on the credit side of the account.

Credit B. F. Khan’s Account To enter the amount in the correct account.

Ledger Entries

Journal Entries

The Journal Date Particulars Dr Cr 2020 $ $ 08-31 B. F. Mohamed 500

B. F. Khan 500 Cash received, entered in wrong personal account, now corrected.

Dr. B. F. Mohamed A/C Cr Date Details Amount Date Details Amount 2020 - $ 2020 - $ 08-31 B. F. Khan: Error Corrected 500 08 -13 Cash 500

. Dr. B. F. Khan A/C Cr

Date Details Amount Date Details Amount 2020 - $ 2020 - $ 08-01 Balance b/d 500 08-31 Cash entered in error in 500

. B. F. Mohamed’s A/C

9

ACTIVITIES

2021 – 01 – 08: A receipt of $2 300 by cheque from M. Ramadan was recorded correctly in the Cash Book but

in error to the account of M. Ramteet.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 02 – 11: The sale of goods $2 500 to K. Martin had been entered in K. Marteen’s Account.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 03 – 15: Paid A. Teekaram $2 850 cash, however the amount was recorded in the account of P. Teekaram

by mistake.

You are required to show the correct entries in the journal and in the ledger accounts.

10

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 7 LESSON 2

TOPIC: ERRORS THAT DO NOT AFFECT THE TRIAL BALANCE AGREEMENT

CONTENT

ERRORS OF PRINCIPLE – where the correct amount is entered but in the wrong type of account, such as: a

non-current asset entered in an expense account.

For example: 2020 – 08 – 16: The purchase of a motor vehicle for $5 000 by cheque was recorded in error in

the motor expenses account.

Accounting Entries Explanation

Debit Motor Vehicles Account To enter the amount in the correct account.

Credit Motor Expenses Account To cancel out the error on the credit side of the account.

Ledger Entries

Journal Entries

The Journal Date Particulars Dr Cr 2020 $ $ 08-31 Motor Vehicles 5 000

Dr. Motor Expenses A/C Cr Date Details Amount Date Details Amount 2020 - $ 2020 - $ 08-16 Bank 5 000 08-31 Motor Vehicles: Error Corrected 5 000

. Dr. Motor Vehicles A/C Cr

Date Details Amount Date Details Amount 2020 - $ 2020 - $ 08-31 Bank: entered originally in 5 000

Motor Expenses

11

Motor Expenses 5 000 Correction of error whereby purchase of motor vehicle was

recorded

in motor expenses account

ACTIVITIES

2021 – 01 – 10: The sale of used computers valued at $40 000 cash was recorded correctly in the Cash Book

but in error to the account of Sales.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 02 – 13: The purchase of machinery for $10 500 had been entered in the Purchases Account.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 03 – 18: Bought office furniture on credit from Designer Style Furniture costing $27 310, however the

amount was recorded in the account of Office Expenses Account.

You are required to show the correct entries in the journal and in the ledger accounts.

12

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 7 LESSON 3

TOPIC: ERRORS THAT DO NOT AFFECT THE TRIAL BALANCE AGREEMENT

CONTENT

ERRORS OF ORIGINAL ENTRY – where an item is entered but both debit and credit entries are of the

same incorrect amount. .

For example: 2020 – 08 – 19: The sale of goods $1 530 to L. Henry on credit have been recorded as both a

debit and a credit of $1 350.

Ledger Entries

Journal Entries

The Journal Date Particulars Dr Cr 2020 $ $ 08-31 L. Henry 180

Sales 180 Correction of error: Sales of 1 530 had been incorrectly entered as $1350.

Dr. L. Henry A/C Cr Date Details Amount Date Details Amount 2020 - $ 2020 - $ 08-19 Sales 1 350 08-31 Sales: Error Corrected 180

Dr. Sales A/C Cr Date Details Amount Date Details Amount 2020 - $ 2020 - $

08-19 L. Henry 1 350 08-31 L. Henry: Error Corrected 180

13

ACTIVITIES

2021 – 01 – 12: The purchase of goods $2960 on credit from NDC Co. Ltd was recorded in both accounts as a

debit and a credit of $2 690.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 02 – 15: Credit sales $3 710 to A. Chintamani was recorded in both of the accounts as $3 170.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 03 – 21: Commission received $4 520 cash, however the amount was recorded in the account of

Commission Received and Cash as $4 250.

You are required to show the correct entries in the journal and in the ledger accounts.

14

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 8 LESSON 1

TOPIC: ERRORS THAT DO NOT AFFECT THE TRIAL BALANCE AGREEMENT

CONTENT

ERRORS OF OMISSION – where a transaction is completely left out from the books of the business.

For example: 2020 – 08 – 22: We purchased goods from F. Nedd for $2 880 but the transaction was not

recorded in the accounts. So there were nil debits and nil credits. We found the transaction on the last day

of the month after a careful observation.

Ledger Entries

Journal Entries

The Journal Date Particulars Dr Cr 2020 $ $ 08-31 Purchases 2 880

F. Nedd 2 880 Correction of error: Purchases omitted from books.

Dr. Purchases A/C Cr Date Details Amount Date Details Amount 2020 - $ 2020 - $ 08-31 F. Nedd: Error Corrected 2 880

. Dr. Nedd A/C Cr

Date Details Amount Date Details Amount 2020 - $ 2020 - $

08-31 Purchases: Error Corrected 2 880 .

15

ACTIVITIES

2021 – 01 – 14: Office fixtures costing $1 700 previously bought from Office Fixtures Limited were returned to

them as the wrong order but was not recorded in the accounts.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 02 – 17: The purchase of goods for $1 575 cash was completely omitted from the books.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 03 – 23: Rent received of $1 390 by cheque was not recorded in the books of the business.

You are required to show the correct entries in the journal and in the ledger accounts.

16

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 8 LESSON 2

TOPIC: ERRORS THAT DO NOT AFFECT THE TRIAL BALANCE AGREEMENT

CONTENT

COMPENSATING ERRORS – where two errors of equal amounts but on opposites sides of the accounts

cancel out each other.

For example: 2020 – 08 – 25: The purchases journal shows a balance $4 350 and the sales journal shows a

balance of $5 680. Both journals add up to $200 too much for the month.

If these were the only errors in the books, the trial balance will balance off but with the wrong amounts for

purchases and sales – 200 too much. So let us correct the accounts.

Ledger Entries

Journal Entries

The Journal Date Particulars Dr Cr 2020 $ $ 08-31 Sales Account 200

Purchases Account 200 Correction of compensating error: Totals of both purchases and sales journals incorrectly added up to $200 too much.

Dr. Purchases A/C Cr Date Details Amount Date Details Amount 2020 - $ 2020 - $ 08-25 Purchases 4 350 08-31 The Journal: Error Corrected 200

. Dr. Sales A/C Cr

Date Details Amount Date Details Amount 2020 - $ 2020 - $ 08-31 The Journal: Error Corrected 200 08-25 Sales 5 680

.

17

ACTIVITIES

2021 – 01 – 16: The Discount Allowed Account shows a balance of $2 840 and Discount Received Account

shows a balance of $3 950. Both of these accounts add up to $320 too much.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 02 – 20: The Purchase Returns Day Book and the Sales Returns Day Book showed a balance of $3 870

and $3 660 respectively. These two day books were added up $250 too much.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 03 – 25: The Staff Pay Account and the Commission Received Account showed a balance of $15 960

and $13 840 respectively. Both of these accounts were added up $500 too much

You are required to show the correct entries in the journal and in the ledger accounts.

18

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 8 LESSON 3

TOPIC: ERRORS THAT DO NOT AFFECT THE TRIAL BALANCE AGREEMENT

CONTENT

COMPLETE REVERSAL OF ENTRIES – where the correct amounts are entered in the correct accounts but

on the wrong side of each account.

For example: 2020 – 08 – 28: We paid a cheque for $2 130 to A. Sooklall. We entered it in the accounts as

follows.

Ledger Entries

Journal Entries

The Journal Date Particulars Dr Cr 2020 $ $ 08-31 A. Sooklall 4 260

Bank 4 260 Payment of $2 130 on 28 August, 2020 to A. Sooklall incorrectly credited to his account and debited to bank. Error now corrected.

Dr. Bank A/C Cr Date Details Amount Date Details Amount 2020 - $ 2020 - $ 08-28 A. Sooklall 2 130 08-31 A. Sooklall: Error Corrected 4 260

. Dr. A. Sooklall A/C Cr

Date Details Amount Date Details Amount 2020 - $ 2020 - $ 08-31 Bank: Error Corrected 4 260 08-28 Bank 2 130

.

19

ACTIVITIES

2021 – 01 – 20: Received cash from R. Persaud $2 020 entered on the credit side of the Cash Book and debit

side of R. Persaud’s Account.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 02 – 23: Cheque paid to D. Murray $3 440 was recorded on the debit side of the Cash Book and credit

side of D. Murray’s Account.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 03 – 28: A receipt of cash from E. Teekaram for $1 850 had been recorded on the credit side of the Cash

Book and debit side of E. Teekaram’s Account.

You are required to show the correct entries in the journal and in the ledger accounts.

20

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 9 LESSON 1

TOPIC: SUSPENSE ACCOUNT AND ERRORS

CONTENT

Suspense Account is an account where any difference in the trial balance is entered prior to looking for the error(s).

Casting means adding up figures.

Overcasting means adding up figures beyond the original amount.

Undercasting means adding up figures below the original amount.

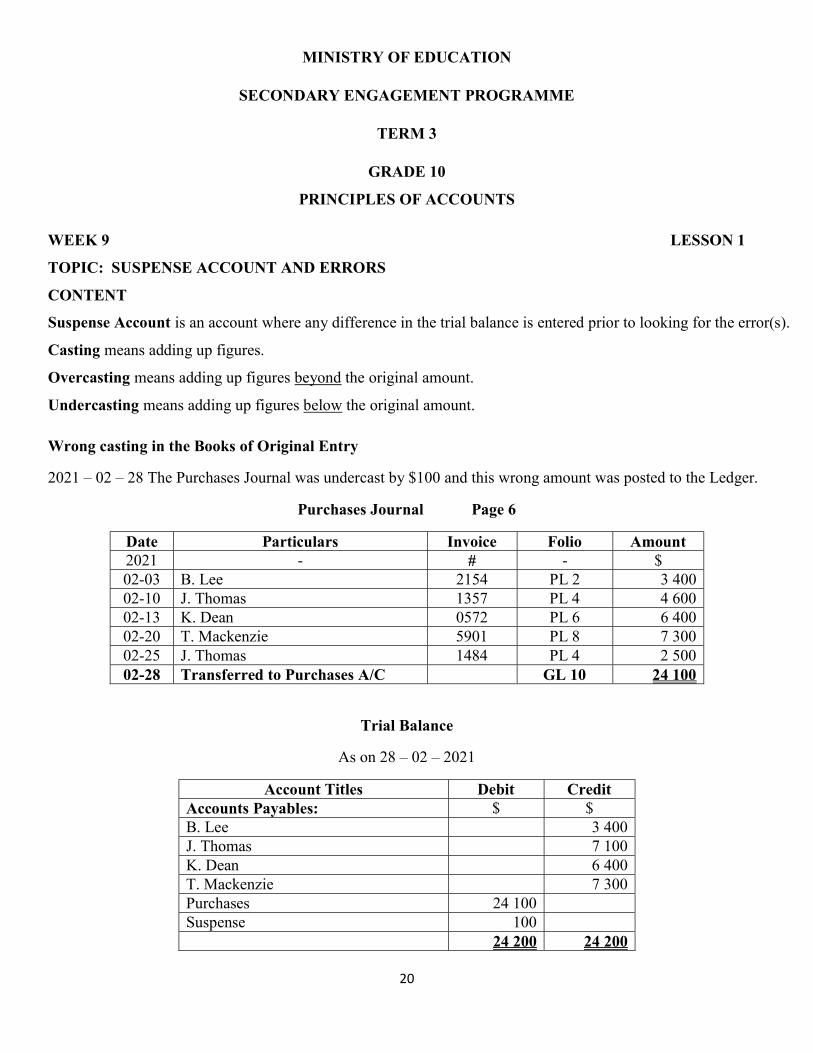

Wrong casting in the Books of Original Entry

2021 – 02 – 28 The Purchases Journal was undercast by $100 and this wrong amount was posted to the Ledger.

Purchases Journal Page 6

Date Particulars Invoice Folio Amount 2021 - # - $ 02-03 B. Lee 2154 PL 2 3 400 02-10 J. Thomas 1357 PL 4 4 600 02-13 K. Dean 0572 PL 6 6 400 02-20 T. Mackenzie 5901 PL 8 7 300 02-25 J. Thomas 1484 PL 4 2 500 02-28 Transferred to Purchases A/C GL 10 24 100

Trial Balance

As on 28 – 02 – 2021

Account Titles Debit Credit Accounts Payables: $ $ B. Lee 3 400 J. Thomas 7 100 K. Dean 6 400 T. Mackenzie 7 300 Purchases 24 100 Suspense 100

24 200 24 200

21

Correction

Dr. Purchases A/C $100

Cr. Suspense A/C $100

Ledger Entries

Journal Entries

The Journal Date Particulars Dr Cr 2021 - $ $ 02-28 Purchases 100

Suspense 100 Correction of undercasting of purchases $100.

ACTIVITIES

2021 – 01 – 31: The Sales Journal was undercast by $450. Sales Journal Total $35 350.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 02 – 28: The Purchases Returns Day Book ($2 170) was overcast by 240.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 03 – 30: The Sales Returns Day Book ($2 240) was overcast by 325.

You are required to show the correct entries in the journal and in the ledger accounts.

Dr. Suspense A/C Cr Date Details Amount Date Details Amount 2021 - $ 2021 - $ 02-28 Difference as per Trial Balance 100 02-28 Purchases 100

. Dr. Purchases A/C Cr

Date Details Amount Date Details Amount 2020 - $ - $ 02-28 Purchases Journal 24 100 02-28 Suspense 100

22

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 9 LESSON 2

TOPIC: SUSPENSE ACCOUNT AND ERRORS

CONTENT

Incomplete Double Entries

2021 – 02 – 28 Purchase of stationery for $1 360 by cash was only recorded in the Cash Book.

Correction

Dr. Stationery A/C $1 360

Cr. Suspense A/C $1 360

Ledger Entries

Journal Entries

The Journal Date Particulars Dr Cr 2021 - $ $ 02-28 Stationery 1 360

Suspense 1 360 Correction of error: Transaction not recorded in Stationery A/C

Dr. Suspense A/C Cr Date Details Amount Date Details Amount 2021 - $ 2021 - $ 02-28 Difference as per Trial Balance 1 360 02-28 Stationery 1 360

. Dr. Stationery A/C Cr

Date Details Amount Date Details Amount 2020 - $ - $ 02-28 Suspense 1 360

.

23

ACTIVITIES

2021 – 01 – 31: Rent received by cheque $2 550 was only recorded in the Cash Book.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 02 – 28: Paid travelling expenses by cash $1 840 was only entered in the Cash Book.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 03 – 30: Commission revenue earned $3 390 by cheque was only recorded in the Cash Book.

You are required to show the correct entries in the journal and in the ledger accounts.

24

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 9 LESSON 3

TOPIC: SUSPENSE ACCOUNT AND ERRORS

CONTENT

Double Entries Completed but with Different Amounts

2021 – 02 – 28 Sale of office equipment $2 640 on credit to C. Rampertab was correctly recorded in his account

but entered in the office equipment account as $2 460.

Correction

Dr. Suspense A/C $180

Cr. Office Equipment A/C $180

Ledger Entries

Journal Entries

The Journal Date Particulars Dr Cr 2021 - $ $ 02-28 Suspense 180

Office Equipment 180 Correction of error: Office Equipment Account wrongly undercast by

$180.

Dr. Suspense A/C Cr Date Details Amount Date Details Amount 2021 - $ 2021 - $ 02-28 Office Equipment 180 02-28 Difference as per Trial Balance 180

. Dr. Office Equipment A/C Cr

Date Details Amount Date Details Amount 2020 - $ - $

02-28 Suspense 180 .

25

ACTIVITIES

2021 – 01 – 31: Sold office furniture $3 830 for cheque. It was correctly recorded in the Cash Book but entered

in the Office Furniture Account as $3 350.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 02 – 28: Bought an excavator on credit from Auto Sales Ltd for $9 470. It was correctly recorded in the

account of Auto Sales Ltd but entered in the Machinery Account as $6 470.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 03 – 30: Sold furniture and fittings for cash $7 260. It was correctly recorded in the Cash Book but

entered in the Furniture and Fittings Account as $7 560.

You are required to show the correct entries in the journal and in the ledger accounts.

26

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 10 LESSON 1

TOPIC: SUSPENSE ACCOUNT AND ERRORS

CONTENT

Posting to the Same Side in Both Accounts

2021 – 02 – 28 Receipt of cheque $2 320 from L. Samaroo was correctly recorded in the Cash Book but

wrongly debited to L. Samaroo’s account (when it ought to be credited).

Correction

Dr. Suspense A/C $4 640

Cr. L. Samaroo A/C $4 640

Ledger Entries

Journal Entries

The Journal Date Particulars Dr Cr 2021 - $ $ 02-28 Suspense 4 640

L. Samaroo 4 640 Correction of error: Account of L. Samaroo wrongly debited instead of credited.

Dr. Suspense A/C Cr Date Details Amount Date Details Amount 2021 - $ 2021 - $ 02-28 L. Samaroo 4 640 02-28 Difference as per Trial Balance 4 640

. Dr. L. Samaroo A/C Cr

Date Details Amount Date Details Amount 2020 - $ - $

02-28 Suspense 4 640 .

27

ACTIVITIES

2021 – 01 – 31: Bought goods on credit from H. Muhammed costing $1 700 was correctly recorded in the

Purchases Journal but wrongly debited to H. Muhammed’s account (when it ought to be credited).

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 02 – 28: Paid J. Williams $2 250 cash, however both accounts were credited in the books of the business.

You are required to show the correct entries in the journal and in the ledger accounts.

2021 – 03 – 30: Sold goods on credit to C. Persaud worth $1 960 was correctly recorded in the Sales account

but wrongly credited to C. Persaud’s account (when it ought to be debited).

You are required to show the correct entries in the journal and in the ledger accounts.

28

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 10 LESSON 2

TOPIC: SUSPENSE ACCOUNT AND ERRORS

CONTENT

Effects of Correction of Errors on Profit

The table helps you to understand the effect of expenses and revenues on profit:

# Error Effects Action 1. Expenses + Profit - Profit + 2. Expenses - Profit + Profit - 3. Revenues + Profit + Profit - 4. Revenues - Profit - Profit +

Expenses and profit have a negative relationship. Errors that result in an increase in expenses will decrease the

profit and vice versa.

On the contrary, revenues and profit have a positive relationship. Errors that increase revenues also increase

profit. Similarly, errors that decrease revenues also decrease profit.

29

The following is the Profit and Loss Account of BBM Co. Ltd for the year ended 31 – 12 – 2020.

BBM Co. Ltd

Profit and Loss Account

For the year ended 31 – 12 – 2020.

$ $ Gross Profit 45 000 Add: Revenues Earned Rent Received 3 800 Commission Revenue 6 000 Total Revenues Earned 9 800 Total Income 54 800 Less: Expenses Insurance 820 Staff Pay 12 000 Office Expenses 460 Rates 1 200 Commission paid 1 000 Stationery 520 Total Expenses 16 000 Net profit 38 800

After the Profit and Loss Account has been prepared, the following errors were discovered:

1. Closing inventory was overcast by $2 000.

2. Insurance on purchase of goods $1 200 was omitted from the books.

3. Sales returns were overcast by $400.

4. Included in staff pay was a sum of $350 taken out by the proprietor for his own use.

5. Rental revenue per month was $400.

6. Commission expense of $300 was erroneously recorded as commission revenue.

You are required to:

(A) prepare a statement showing the corrected gross profit to be posted to the Profit and Loss Account.

(B) prepare a corrected Profit and Loss Account for the year ended 31 – 12 – 2020

30

BBM Co. Ltd

Statement of Adjusted Gross Profit

$ $ Gross Profit before correction of errors 45 000 Add: Overcast of sales returns 400 45 400 Less: Closing inventory overcast 2 000 Insurance on purchase of goods 1 200 3 200 Adjusted Gross Profit 42 200

BBM Co. Ltd

Profit and Loss Account

For the year ended 31 – 12 – 2020.

$ $ Gross Profit 42 200 Add: Revenues Earned Rent Received 4 800 Commission Revenue 5 700 Total Revenues Earned 10 500 Total Income 52 700 Less: Expenses Insurance 820 Staff Pay 11 650 Office Expenses 460 Rates 1 200 Commission paid 1 300 Stationery 520 Total Expenses 15 950 Net profit 36 750

Correction of Errors:

Staff Pay $12 000 - $350 (Drawings) = $11 650

Rent Received $400 x 12 months = $4 800

Commission Revenue $6 000 - $300 = $5 700

Commission Paid $1 000 + $300 = $1 300

ACTIVITIES:

31

The Profit and Loss Account of Mr. K. Fitzpatrick for the year ended 30 – 06 – 2019 was made available to you.

Mr. K. Fitzpatrick Profit and Loss Account

for the year ended 30 – 06 – 2019

$ $ Gross Profit 42 600 Add: Revenues Earned Rent Received 8 200 Commission Revenue 4 800 Total Revenues Earned 13 000 Total Income 55 600 Less: Expenses Commission paid 3 200 Electricity Charges 1 500 Advertising 1 100 Insurance 800 Office Expenses 380 Staff Pay 14 400 Total Expenses 21 380 Net profit 34 220

After the Profit and Loss Account has been prepared, the following errors were discovered:

1. Sales returns were overcast by $200.

2. Commission expense for the sum of $1 400 was wrongly recorded as commission revenue.

3. Closing inventory was undercast by $2 200.

4. Advertising of $400 was recorded in the staff pay account.

5. Purchases Day Book was undercast by $700.

You are required to:

(A) prepare a statement showing the corrected gross profit to be posted to the Profit and Loss Account.

(B) prepare a corrected Profit and Loss Account for the year ended 30 – 06 – 2019.

32

MINISTRY OF EDUCATION

SECONDARY ENGAGEMENT PROGRAMME

TERM 3

GRADE 10

PRINCIPLES OF ACCOUNTS

WEEK 10 LESSON 2

TOPIC: SUSPENSE ACCOUNT AND ERRORS

CONTENT

Errors that affect the Statement of Financial Position (Balance Sheet)

Errors such as incorrect valuation of assets, treatment of revenue expenditure as capital expenditure and vice

versa not only affect the Profit and Loss Account but also the Statement of Financial Position (Balance Sheet).

33

The following is the Statement of Financial Position (Balance Sheet) of J. Smith Enterprise as at 30 – 06 – 2020.

J. Smith Enterprise Statement of Financial Position (Balance Sheet)

As at 30 – 06 – 2020

$ $ $ NON-CURRENT ASSETS Premises 100 000 Motor Vehicles 25 000 Office Equipment 10 000 135 000 CURRENT ASSETS Closing Inventory 12 000 Accounts Receivable 8 000 Cash 1 000 21 000 LESS: CURRENT LIABILITIES Accounts Payable 7 000 Overdraft 3 000 10 000 Net Current Assets 11 000 146 000 LESS: NON-CURRENT LIABILITIES Mortgages 18 000 128 000 FINANCED BY: Opening Capital 90 000 Add: Net Profit 40 000 130 000 Less: Drawings 2 000 128 000

After the Statement of Financial Position (Balance Sheet) has been prepared, the following errors were

discovered:

1. Purchase of a computer for $3 800 for office use from Computer World was not recorded in the books.

2. Closing inventory was undercast by $1 500.

3. A cheques for $4 200 received from accounts receivable, T. Donald was not entered in the books.

4. Repairs to motor vehicles $3 000 was recorded in motor vehicles account.

5. Accrued expense of 450 was completely omitted from the books.

34

You are required to:

(A) prepare a statement showing the actual net profit after the correction of errors.

(B) redraft the Statement of Financial Position (Balance Sheet) after the correction of errors.

J. Smith Enterprise

Statement of Adjusted Net Profit

$ $ Net Profit before correction of errors 40 000 Add: Closing inventory undercast 1 500 41 500 Less: Repairs wrongly entered to motor vehicle account 3 000 Accrued expenses not recorded 450 3 450 Adjusted Net Profit 38 050

J. Smith Enterprise Statement of Financial Position (Balance Sheet)

As at 30 – 06 – 2020

$ $ $ NON-CURRENT ASSETS Premises 100 000 Motor Vehicles 22 000 Office Equipment 13 800 135 800 CURRENT ASSETS Closing Inventory 13 500 Accounts Receivable 3 800 Bank 1 200 Cash 1 000 19 500 LESS: CURRENT LIABILITIES Accounts Payable 10 800 Accrued Expenses 450 11 250 Net Current Assets 8 250 144 050 LESS: NON-CURRENT LIABILITIES Mortgages 18 000 126 050 FINANCED BY: Owner’s Equity 90 000 Add: Net Profit 38 050 128 050 Less: Drawings 2 000 126 050

35

Effect of Correction of Errors

Motor Vehicles $25 000 - $3 000 = $22 000 Office Equipment $10 000 + $3 800 = $13 800 Closing Inventory $12 000+$1 500 = $13 500 Accounts Receivable $8 000 - $4 200 = $3 800 Bank $3 000 - $4 200 = $1 200 Creditors $7 000 + $3 800 = $10 800

Note: The business paid off its bank overdraft and now has a bank balance.

ACTIVITIES:

The Statement of Financial Position (Balance Sheet) was taken from the books of C. Duncan.

C. Duncan

Statement of Financial Position (Balance Sheet)

As at 31 – 03 – 2020

$ $ $ NON-CURRENT ASSETS Motor Vehicles 55 000 Office Equipment 5 500 60 500 CURRENT ASSETS Closing Inventory 13 000 Accounts Receivable 14 000 Cash 600 27 600 LESS: CURRENT LIABILITIES Accounts Payable 9 000 Bank Overdraft 2 600 11 600 Working Capital 16 000 76 500 FINANCED BY: Owner’s Equity 50 000 Add: Net Profit 28 000 78 000 Less: Drawings 1 500 76 500

36

After the Statement of Financial Position (Balance Sheet) has been prepared, the following errors were found:

1. Goods taken for personal use $500 was not entered in the books.

2. Inventory $3 000 which was kept in the store room was not included as part of closing inventory.

3. A cheque $10 000 brought in by the proprietor for business use had not been recorded in the books.

4. Cash $5 000 from accounts receivable, W. Warren out of that $3 000 was used to pay accounts payable,

O. Doobay. No entries were done.

5. Accounts receivable, N. Thompson paid us by cheque $2 300. This transaction was not recorded in the

books of the business.

You are required to:

(A) prepare a statement showing the actual net profit after the correction of errors.

(B) redraft the Statement of Financial Position (Balance Sheet) after the correction of errors.