primer - vinod kotharivinodkothari.com/wp-content/uploads/2017/03/primer_on... · primer on...

TRANSCRIPT

Primer on External Commercial Borrowings (ECBs)

Vinita Nair [email protected]

Vignesh Iyer [email protected]

Arundhuthi Bose [email protected]

M/s Vinod Kothari & Company

As updated on July 12, 2016

Primer

Check at:

http://india-financing.com/staff-publications.html

for more write ups.

Copyright: This write up is the property of Vinod Kothari & Company and no part of it can be copied, reproduced or distributed in any manner. Disclaimer: The following questions are framed by us, and do not represent or necessarily match with views of regulatory authorities. The questions/answers are purely academic, and are not based on facts/circumstances of any particular case. Neither are they intended to be relied upon for any particular transaction or situation. Please do consult your counsel before deciding to rely on the following. For contacting authors of the primer below, kindly use email.

Primer on External Commercial Borrowings (ECBs)

1. How does ECB compare with domestic borrowings in terms of costs? 4

2. What is the key difference between ECB and FDI? 4

3. What all instruments of borrowings /debt instruments are covered by the

definition of “ECBs”? 5

4. What is the key difference between automatic route and approval route for

ECBs? 6

5. What is the recent amendment made in ECB? 6

6. What impact will the revised framework have on the ECBs already availed under

the erstwhile framework? 6

7. What will be the nature of ECB that can be availed? 7

8. What are the End-use restrictions in case of ECB? 8

9. Is ECB allowed for working capital or general corporate purposes? 10

10. Is ECB allowed for capital expenditure? 10

11. What is the definition of infrastructure under extant ECB guidelines? 11

12. Can ECB be availed for acquisition of shares under the Government’s

disinvestment programme of PSUs? 12

13. Can ECB be availed by Holding Companies/ Core Investment Companies? 12

14. Can ECB be availed for repaying rupee loans taken by the company? 13

15. Is it only that Corporates are allowed to accept ECBs or can Non-Corporate

Bodies also accept ECBs? 16

16. Who are the Borrowers eligible to avail ECB? 16

17. Can Entities engaged in manufacturing sector avail ECBs? 17

18. Can Corporate engaged in services sector avail ECBs under automatic route: 18

19. Can NBFCs avail of ECBs? 18

20. Can HFCs avail ECBs? 19

21. Can Infrastructure Finance Companies (IFCs) avail ECBs? 20

22. Can builders/real estate companies avail ECBs? 21

23. What needs to be done for a builder to avail ECBs through the National Housing

Bank? 22

24. Who can be the lender for an ECB? 23

25. Is it possible for a foreign equity holder to provide ECBs to the company in which

such equity holder holds investment? 24

26. What is the meaning of the debt/equity ratio in case of foreign equity holders? 25

27. Whether availing of operating lease by an Indian Entity an ECB? 25

28. Can an Operating Leasing or Asset Renting entity avail ECBs? 27

Primer on External Commercial Borrowings (ECBs)

29. Is a financial lease also treated as ECB? 27

30. Can securitisation be treated as ECB? 27

31. What is the procedure for getting ECBs under automatic route? 27

32. What is the procedure for getting ECBs under approval route? 28

33. Is it necessary that ECBs must be full hedged? 29

34. What are the restrictions on all-in cost of ECBs? What all is included in all-in

costs? 29

35. What are the maturity restrictions on ECBs? 30

36. The maturity restrictions talk about minimum maturity – is there anything on

maximum maturity? 31

37. What is Take-out Finance and who are allowed to avail the facility of take-out

finance? 31

38. What are the options available for repayment of ECBs? 32

39. What are the reporting requirements in case of conversion of ECB into equity? 32

40. Is prepayment allowed in case of ECB? 33

41. Can ECB be refinanced by raising a fresh ECB or be rescheduled? 33

42. What procedure needs to be followed in case of change in the terms and

conditions of the ECB? 33

43. Can Corporate, which have violated the extant ECB policy and are under

investigation by the Reserve Bank, avail of ECB? 37

44. If I go for ECBs, should I hedge myself, or leave it unhedged? 37

45. How about accounting for forex losses in ECBs? 37

Primer on External Commercial Borrowings (ECBs)

1. How does ECB compare with domestic borrowings in terms of costs?

The evaluation of cost of domestic borrowings versus ECBs must be done after a

careful comparison of the ECB cost, adding together the cost of hedging or the

cost due to foreign exchange losses. The decision primarily depends on the

prevailing interest rate gaps between – INR loans and forex loans. There are

situations when the gap is quite large, and even after considering the cost of

hedge, an ECB may make sense. However, ECB option is not necessarily cheaper.

Hence, please do consult your financial advisors to advise you on the cost

comparison.

If you leave ECB costs unhedged, you may be taking a substantial risk on forex

losses. There is a currency risk involved in ECBs. A depreciating rupee will prove

burdensome at the time of repayment of loan. Unless you have a natural hedge,

there may be periods where this may cause a significant strain on your

financials.

2. What is the key difference between ECB and FDI?

Parameters ECB FDI Meaning ECBs are commercial loans raised by

eligible resident entities from recognised non-resident entities and should conform to parameters such as minimum maturity, permitted and non-permitted end-uses, maximum all-in-cost ceiling, etc, as stipulated in the RBI Master Circular on External Commercial Borrowings and trade credits, issued from time to time, with a minimum average maturity of 3 /5 / 10 years.

FDI‘ means investment by non-resident entity/ person resident outside India in the capital of an Indian company under Schedule 1 of Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations 2000

Governed

by

ECBs are governed and included in the following three Regulations framed under FEMA:

Foreign Exchange Management Act, 1999

Foreign Exchange Management (Borrowing or Lending in Foreign Exchange) Regulations, 2000, dated May 3, 2000 as amended from time to time.

Foreign Exchange Management

Consolidated FDI Policy, 2012 and Foreign Exchange Management Act, 1999 & Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations 2000 dated May 3, 2000 as amended from time to time.

Primer on External Commercial Borrowings (ECBs)

Parameters ECB FDI (Transfer or Issue of any Foreign Security) Regulations, 2004 dated July 7, 2004 as amended from time to time.

Foreign Exchange Management (Guarantees) Regulations, 2000 dated May 3, 2000 as amended from time to time.

as provided under RBI Master Directions.1 End-use

restrictions

Refer Question No. 8 In case of Issue of shares by Indian Companies under FCCB/ADR/GDRs there is a ban on deployment/investment of such funds in real estate or the stock market.

Instruments Refer Question No. 3 Equity shares, fully, compulsorily and mandatorily convertible debentures and fully, compulsorily and mandatorily convertible preference shares.

3. What all instruments of borrowings /debt instruments are covered by the definition of “ECBs”?

Commercial loans in the form of bank loans, buyers’ credit2, suppliers’ credit3,

securitized instruments.

Foreign Currency Convertible Bonds

Financial Lease

Non- convertible, optionally convertible or partially convertible Preference

Shares.

Foreign Currency Exchangeable Bond.4

1 https://www.rbi.org.in/Scripts/BS_ViewMasterDirections.aspx?id=10204

2 Buyer’s Credit refers to loans for payment of imports in to India arranged by the importer from a bank or financial institution for original maturity of minimum three years.

3 Supplier’s Credit refers to credit for imports into India extended by the overseas supplier. 4 means a bond expressed in foreign currency issued by an Issuing Company and subscribed to by a

person who is a resident outside India, in foreign currency and exchangeable into equity share of another company, to be called the Offered Company. The principal and interest of the FCEB is payable in foreign currency. The FCEB may be denominated in any freely convertible foreign currency.

Primer on External Commercial Borrowings (ECBs)

4. What is the key difference between automatic route and approval route for ECBs?

Automatic Route applies to the borrowings made by a person resident in India

in accordance with the provisions of the Automatic Route Scheme as specified in

Schedule I of the Foreign Exchange Management (Borrowing or Lending in

Foreign Exchange) Regulations, 2000 as amended from time to time.

Approval Route applies to the foreign currency loans raised of the nature or for

the purposes as specified in Schedule II of the Foreign Exchange Management

(Borrowing or Lending in Foreign Exchange) Regulations, 2000 as amended

from time to time by the person resident in India and who satisfies the eligibility

and other conditions specified in that Schedule.

5. What is the recent amendment made in ECB?

The recent amendments made in the revised ECB framework encompass various elements some of which are:-

Inclusion of financial lease as a forms of borrowings Relaxing rules for NBFCs Segmenting the Minimum Average Maturity (MAM) in three tracks - Track I,

Track II, Track III A more liberal approach, with fewer restrictions on end uses, higher all-in-cost

ceiling, etc. for long term foreign currency borrowings as the extended term makes repayments more sustainable and also minimizes roll-over risks for the borrower;

A more liberal regime for INR denominated ECBs where the currency risk is borne by the lender;

Expansion of the list of overseas lenders to include long-term lenders, such as, Insurance Companies, Pension Funds, Sovereign Wealth Funds;

Only a small negative list of end-use restrictions applicable in case of long-term ECB and INR denominated ECB;

Alignment of the list of infrastructure entities eligible for ECB with the Harmonised List of the Government of India.

6. What impact will the revised framework have on the ECBs already availed under the erstwhile framework?

Entities raising ECB under extant framework can raise the said loans by March 31, 2016, provided the agreement in respect of the loan is already signed by the date the new framework comes into effect.

Primer on External Commercial Borrowings (ECBs)

For raising of ECB under the following carve outs, the borrowers will, however, have time up to March 31, 2016 to sign the loan agreement and obtain the Loan Registration Number (LRN) from the Reserve Bank by this date:

i. ECB facility for working capital by airlines companies; ii. ECB facility for consistent foreign exchange earners under the USD 10

billion Scheme; and iii. ECB facility for low cost affordable housing projects (low cost affordable

housing projects as defined in the extant Foreign Direct Investment policy)

7. What will be the nature of ECB that can be availed?

The nature of ECB that can be availed along with the minimum average maturity will be as under:

Particulars Track I Track II Track III Nature of ECB

Medium term foreign currency denominated ECB with Minimum Average Maturity (MAM) of 3/5 years.

Long term foreign currency denominated ECB with MAM of 10 years.

Indian Rupee denominated ECB with MAM of 3/5 years.

Minimum Average Maturity

i. 3 years or more for ECB upto USD 50 million or its equivalent. ii. 5 years or more for ECB beyond USD 50 million or its equivalent.

For FCCBs/FCEBs

the MAM will be 5

years irrespective

of the amount

borrowed5

For Infrastructure

10 years or more irrespective of the amount.

i. 3 years or more for ECB upto USD 50 million or its equivalent. ii. 5 years or more for ECB beyond USD 50 million or its equivalent.

5 https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10314&Mode=0

Primer on External Commercial Borrowings (ECBs)

Particulars Track I Track II Track III sector/ NBFC-

IFC/NBFC-

AFC/CICs/Holding

Companies

8. What are the End-use restrictions in case of ECB?

Particulars Track I Track II Track III Permitted end use

1. ECB proceeds can be utilised for capital expenditure in the form of: i. Import of capital goods including payment towards import of services, technical know-how and license fees, provided the same are part of these capital goods; ii. Local sourcing of capital goods; iii. New project; iv. Modernisation /expansion of existing units; v. Overseas direct investment in Joint ventures (JV)/ Wholly owned subsidiaries (WOS); vi. Acquisition of shares of public sector undertakings at any stage of disinvestment under the disinvestment programme of the Government of India; vii. Refinancing of existing trade credit raised for import of capital goods; viii. Payment of capital goods already shipped / imported but unpaid; ix. Refinancing of existing ECB provided the residual maturity is not reduced.

2. SIDBI can raise ECB only for the purpose of on lending to the borrowers in the Micro, Small and Medium Enterprises (MSME sector), where MSME sector is as defined under the

1. The ECB proceeds can be used for all purposes excluding the following: i. Real estate activities ii. Investing in capital market iii. Using the proceeds for equity investment domestically; iv. On-lending to other entities with any of the above objectives; v. Purchase of land.

2. Holding companies can also use ECB proceeds for providing loans to their infrastructure SPVs.

NBFCs can use ECB proceeds for: a. On-lending to the infrastructure sector; b. providing hypothecated loans to domestic entities for acquisition of capital goods/equipments; and

c. providing capital goods/equipment to domestic entities by way of lease and hire-purchases

2. Developers of SEZs/ NMIZs can raise ECB only for providing infrastructure facilities within SEZ/ NMIZ.

3. NBFCs-MFI, other eligible MFIs, NGOs

Primer on External Commercial Borrowings (ECBs)

Particulars Track I Track II Track III MSME Development Act, 2006, as amended from time to time. #

3. Units of SEZs can raise ECB only for their own requirements. #

4. Shipping and airlines companies can raise ECB only for import of vessels and aircrafts respectively. #

5. ECB proceeds can be used for general corporate purpose (including working capital) provided the ECB is raised from the direct / indirect equity holder or from a group company for a minimum average maturity of 5 years.

6. ECBs for the following purposes will be considered under the approval route#: i. Import of second hand goods as per the Director General of Foreign Trade (DGFT) guidelines; ii. On-lending by Exim Bank.

7. ECBs raised by Holding Companies

and CICs shall be used only for on-

lending to infrastructure Special Purpose

Vehicles (SPVs).#6

8. ECBs raised by NBFC-IFCs and NBFC-

HFCs is to be used only for the purpose

of financing infrastructure.7

and not for profit companies registered under the Companies Act, 1956/2013 can raise ECB only for on-lending to self-help groups or for micro-credit or for bonafide micro finance activity including capacity building. 4. For other eligible entities under this track, the ECB proceeds can be used for all purposes excluding the following: i. Real estate activities ii. Investing in capital market iii. Using the proceeds for equity investment domestically; iv. On-lending to other entities with any of the above objectives; v. Purchase of land

# The respective conditions will be applicable for all three tracks.

6 https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10314&Mode=0

7 https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10314&Mode=0

Primer on External Commercial Borrowings (ECBs)

9. Is ECB allowed for working capital or general corporate purposes?

Under the revised ECB framework, ECBs raised under Track I can used for

general corporate purpose (including working capital) provided the ECB is raised from the direct / indirect equity holder or from a group company for a minimum average maturity of 5 years.

Civil Aviation sector is allowed to obtain ECB for working capital, subject to the

approval from the Reserve Bank of India. The maximum ECB permissible to be

used for working capital is equal to the overall ECB ceiling, being USD one

billion for the entire civil aviation sector and USD 300 million for an individual

airline company. The ECB needs to be raised within 12 months from April 24,

2012 (date of issue of circular), however, RBI vide A. P. (DIR Series) Circular No.

116 dated June 25, 2013 has extended the scheme of availing ECB till December

31, 2013. Further, RBI vide A.P ( DIR Series) Circular No. 113 dated March 26,

2014 had extended the scheme of availing ECB till March 31, 2015. However, the

borrowing is subject to the restriction that such ECB liability needs to be

extinguished only out of the foreign exchange earnings of the borrowing

company.

Airline companies registered under the Companies Act, 1956 and possessing

scheduled operator permit license from DGCA (Director General for Civil

Aviation) for passenger transportation are eligible to avail ECB for working

capital, with a minimum average maturity of 3 years, depending on their cash

flow, foreign exchange earnings and the capability to service the debt.

Under the revised ECB framework, these entities can raise ECB under the

aforesaid carve-out upto March 31, 2016 by signing loan agreement and

obtaining Loan Registration Number (LRN) from RBI by this date.

10. Is ECB allowed for capital expenditure?

ECB proceeds raised under Track I needs to be utilized for capital expenditure in

the form of :

i. Import of capital goods including payment towards import of services,

technical know-how and license fees, provided the same are part of these

capital goods;

ii. Local sourcing of capital goods;

iii. New project;

Primer on External Commercial Borrowings (ECBs)

iv. Modernisation /expansion of existing units;

v. Overseas direct investment in Joint ventures (JV)/ Wholly owned subsidiaries

(WOS);

vi. Acquisition of shares of public sector undertakings at any stage of

disinvestment under the disinvestment programme of the Government of

India;

vii. Refinancing of existing trade credit raised for import of capital goods;

viii. Payment of capital goods already shipped / imported but unpaid;

ix. Refinancing of existing ECB provided the residual maturity is not reduced.

Proceeds raised under Track II and III also can be utilized for capex purpose.

11. What is the definition of infrastructure under extant ECB guidelines?

For the purpose of raising ECB the definition of infrastructure will be as

provided under Harmonised Master List of Infrastructure sub-sectors and

Institutional Mechanism for its updation approved by Government of India

vide Notification F. No. 13/06/2009-INF dated March 27, 2012(as amended /

updated from time to time).

The expanded infrastructure sector and sub-sectors for the purpose of ECB

include:

(a) Energy which will include (i) electricity generation, (ii) electricity

transmission, (iii) electricity distribution, (iv) oil pipelines, (v)

oil/gas/liquefied natural gas (LNG) storage facility (includes strategic

storage of crude oil) and (vi) gas pipelines (includes city gas distribution

network);

(b) Communication which will include (i) mobile telephony services /

companies providing cellular services, (ii) fixed network

telecommunication (includes optic fibre / cable networks which provide

broadband / internet) and (iii) telecommunication towers;

(c) Transport which will include (i) railways (railway track, tunnel, viaduct,

bridges and includes supporting terminal infrastructure such as loading /

unloading terminals, stations and buildings), (ii) roads and bridges, (iii)

ports, (iv) inland waterways, (v) airport ( including Maintenance, Repairs

Primer on External Commercial Borrowings (ECBs)

and Overhaul8) and (vi) urban public transport (except rolling stock in

case of urban road transport);

(d) Water and sanitation which will include (i) water supply pipelines, (ii)

solid waste management, (iii) water treatment plants, (iv) sewage

projects (sewage collection, treatment and disposal system), (v) irrigation

(dams, channels, embankments, etc.) and (vi) storm water drainage

system;

(e) (i) mining, (ii) exploration and (iii) refining;

(f) Social and commercial infrastructure which will include (i) hospitals

(capital stock and includes medical colleges and para medical training

institutes), (ii) Hotel Sector which will include hotels with fixed capital

investment of Rs. 200 crore and above, convention centres with fixed

capital investment of Rs. 300 crore and above and three star or higher

category classified hotels located outside cities with population of more

than 1 million (fixed capital investment is excluding of land value), (iii)

common infrastructure for industrial parks, SEZs, tourism facilities, (iv)

fertilizer (capital investment), (v) post-harvest storage infrastructure for

agriculture and horticulture produce including cold storage, (vi) soil

testing laboratories and (vii) cold chain (includes cold room facility for

farm level pre-cooling, for preservation or storage or agriculture and

allied produce, marine products and meat.

(g) Through the notification RBI/2015-16/349 of A.P. (DIR Series) Circular

No.56, RBI inserted “Exploration, Mining and Refinery” sector in the list.

12. Can ECB be availed for acquisition of shares under the Government’s disinvestment programme of PSUs?

Yes, the same is a permitted end use under Track I, II and III.

13. Can ECB be availed by Holding Companies/ Core Investment Companies?

Under the revised ECB framework, Holding Companies and Core Investment Companies are permitted to raise ECB under Track-I and Track II. The ECB availed is subject to end use restrictions mentioned in Question 8. Also, for ECB raised by

8 Inserted vide AP (DIR Series) Circular No. 85 dated January 6, 2014

Primer on External Commercial Borrowings (ECBs)

these entities under Track-I, the MAM will be 5 years and with 100% hedging. The CICs and Holding Companies raising ECBs under Track –I also need to have a board approved risk management policy. The AD-I category bank needs to ensure the hedging requirement and file ECB-2 with regard to that. Moreover, the ECB raised under Track-I by them have to be used only for on-lending to infrastructure SPVs.

14. Can ECB be availed for repaying rupee loans taken by the company?

Permitted end use under Track II and Track III specify a negative list. The ECB

proceeds can be utilized for any purpose other than those specifically prohibited.

All ECB loan agreements entered into before December 02, 2015 may continue

with the disbursement schedules as already provided in the loan agreements

without requiring any further consent from the RBI or any AD Category I bank.

For raising of ECB under the following carve outs, the borrowers will, however,

have time up to March 31, 2016 to sign the loan agreement and obtain the LRN

from the Reserve Bank by this date:

o ECB facility for working capital by airlines companies (refinancing of the

outstanding working capital Rupee loan(s) availed of from the domestic

banking system);

o ECB facility for consistent foreign exchange earners under the USD 10 billion

Scheme (can raise ECBs for repayment of outstanding Rupee loans availed of

for capital expenditure from the domestic banking system and/ or fresh

Rupee capital expenditure subject to below mentioned certain terms and

conditions);

Indian Companies in the manufacturing and infrastructure sector

and as per A.P. (DIR Series) Circular No.78 dated January 21, 2013, Indian

Companies in the hotel sector (with a total project cost of INR 250

crore or more) who were consistent foreign exchange earners during

the past three financial years and not in default list/caution list of the

Reserve Bank of India can avail of ECBs, subject to overall limit of USD

10 billion and approval of the Reserve Bank of India, for repayment of

rupee loans availed of for capital expenditure from the domestic banking

systems which are still outstanding and/or fresh Rupee capital

expenditure. The maximum permissible ECB that could be availed of by

an individual company will be limited to 75 % of the average annual

export earnings realized during the past 3 financial years or 50% of the

average annual export earnings realised during past 3 financial years,

whichever is higher. However, the borrowing is subject to the restriction

that such ECB liability needs to be extinguished only out of the foreign

exchange earnings of the borrowing company.

Primer on External Commercial Borrowings (ECBs)

In furtherance to Circular no 78, RBI vide A.P. (DIR Series) Circular No.12

dated July 15, 2013 extended the benefit of USD 10 billion scheme to

Indian companies in the aforesaid sectors which have established Joint

Venture (JV) / Wholly Owned Subsidiary (WOS) / have acquired assets

overseas, subject to following conditions:

(a) ECB can be availed of for repayment of all term loans having average residual maturity of 5 years and above / credit facilities availed of by Indian companies from domestic banks for overseas investment in JV/WOS, in addition to ‘Capital Expenditure’;

(b) ECB can be availed of within the scheme based on the higher of 75 per cent of the average foreign exchange earnings realized during the past three financial years and / or 75 per cent of the assessment made about the average of foreign exchange earnings potential for the next three financial years of the Indian companies from the JV / WOS / assets abroad as certified by Statutory Auditors / Chartered Accountant / Certified Public Accountant / Category I Merchant Banker registered with SEBI / an Investment Banker outside India registered with the appropriate regulatory authority in the host country;

(c) ECB availed of under the scheme will have to be repaid out of forex earnings9 from the overseas JV / WOS / assets.

However, RBI vide RBI/2013-14/585 A.P. (DIR Series) Circular

No.129 dated May 9, 2014 has specified that eligible Indian companies

will NOT BE permitted to raise ECB from overseas branches /

subsidiaries of Indian banks for the purpose of refinance / repayment

of the Rupee loans raised from the domestic banking system in

respect of spectrum allocation, repayment of existing Rupee loans for

companies in infrastructure sector and Repayment of Rupee loans.

Former Provisions

Formerly, ECB availed under Automatic Route could not be utilised for

repayment of existing rupee loans. However, as per A.P. (Dir Series) Circular No.

54 dated November 26, 2012, successful bidders making the upfront payment for

9The past earnings in the form of dividend/repatriated profit/ other forex inflows like royalty, technical know-how, fee, etc from overseas JV/WOS/assets will be reckoned as foreign exchange earnings for the purpose of US$ 10 billion scheme.

Primer on External Commercial Borrowings (ECBs)

the award of 2G spectrum initially out of Rupee loans availed from the domestic

lenders could refinance such rupee loans with a long-term ECB, under the

Automatic Route subject to following conditions:

o the long term ECB shall be raised within a period of 18 months from the date

of sanction of such Rupee loans for the stated purpose from the domestic

lenders.

o the designated AD Category I bank has evidenced the payment of upfront fees

to GoI in the form of a receipt/challan from DoT; and

o the designated AD - Category I bank shall monitor the end-use of funds.

However, eligible borrowers in the Telecom Sector who were successful

bidders for spectrum allocation could avail rupee loan initially to make the

payment and refinance the same with a long-term ECB, subject to approval from

the Reserve Bank of India and fulfillment of following conditions:

o The ECB should be raised within 12 months from the date of payment of the

final installment to the Government; (ECB window for financing 3G spectrum

rupee loans, that are still outstanding in telecom operator’s books of

accounts, will be open upto March 31, 2014 – RBI vide A.P. (DIR Series)

Circular No.114 dated June 25, 2013.)

o The end-use of funds should be monitored by the designated AD-Category I

bank.

o No guarantee in any form will be given by the Banks in India.

o The borrower needs to comply with all other conditions relating to eligible

borrowers, recognized lenders, all-in-cost etc.

Further, Indian Companies in the infrastructure sector (except companies

in the power sector) are permitted to utilise 25% of the fresh ECB raised by

them, towards refinancing of the Rupee loans availed from the domestic banking

system subject to the approval of the Reserve Bank of India and fulfillment of

following conditions:

o Atleast 75% of the fresh ECB proposed to be raised should be utilised for

capital expenditure towards new infrastructure project(s)

o In respect of the remaining 25%, the refinance needs to be utilized only for

repayment of the Rupee loan availed for ‘capital expenditure’ of earlier

completed infrastructure project(s); and

o The refinance needs to be utilised only for the Rupee loans which are

outstanding in the books of the financing bank concerned.

The term ‘Infrastructure Sector’ has the same meaning as given in the Harmonised

Master List of Infrastructure sub-sectors approved by Government of India vide

Primer on External Commercial Borrowings (ECBs)

Notification F. No. 13/06/2009-INF dated March 27, 2012 as amended / updated

from time to time. Companies in the power sector are permitted to utilize up to

40% of fresh ECB raised by them towards refinancing of the Rupee loan/s

availed from the domestic banking system subject to approval of the Reserve

Bank of India and fulfilment of the condition that atleast 60% of the fresh ECB

proposed to be raised should be utilized for fresh capital expenditure for

infrastructure project(s).

15. Is it only that Corporates are allowed to accept ECBs or can Non-Corporate Bodies also accept ECBs?

In case of Companies, only those who qualify as an eligible borrower are allowed

to accept ECB under the Automatic Route under the respective tracks allotted.

This means Corporate, including few in services sector, and Infrastructure

Finance Companies except financial intermediaries, such as banks, financial

institutions, Housing Finance Companies.

Non-Corporate like Trusts and Non-Profit making organizations are eligible to

raise ECB under Track III provided they are engaged in micro finance activities

and satisfy the following criteria:

(i) should have a satisfactory borrowing relationship for atleast three years with

an AD Cat I bank in India, and

(ii) should have a certificate of due diligence on ‘fit and proper’ status from the

AD Cat I bank..

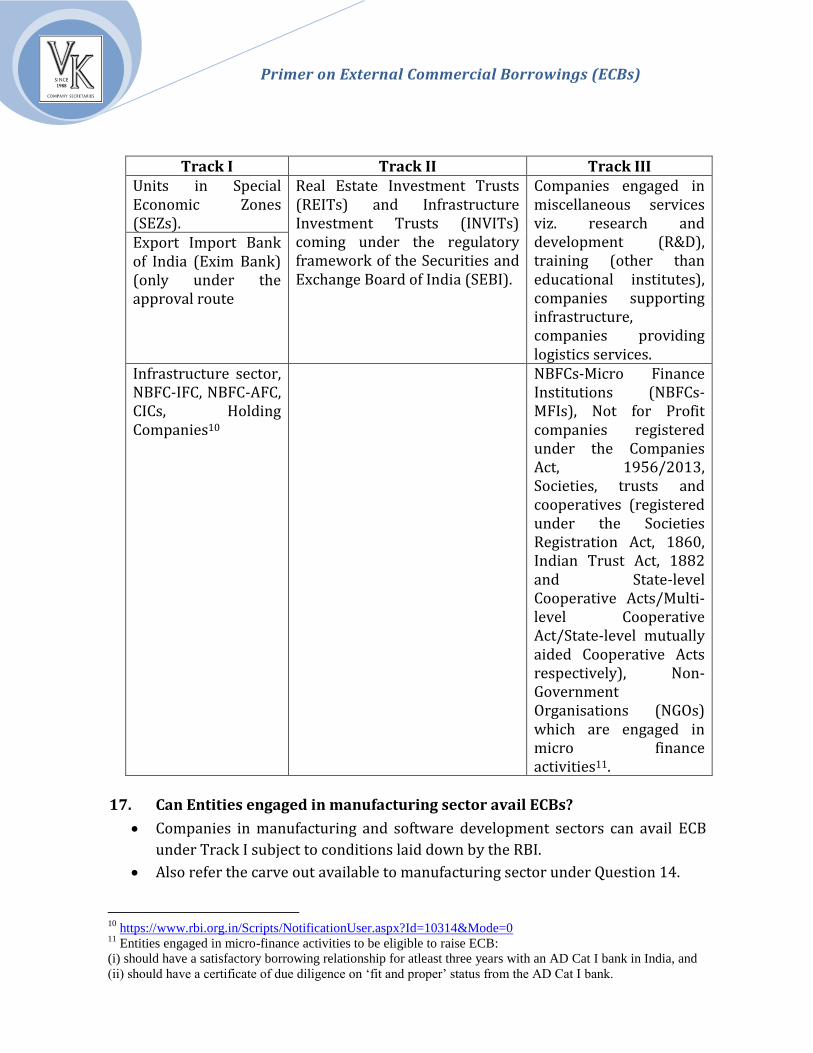

16. Who are the Borrowers eligible to avail ECB?

The list of entities eligible to raise ECB under the three tracks is set out in the

following table

Track I Track II Track III Companies in manufacturing, and software development sectors.

All entities listed under Track I All entities listed under Track I

Shipping and airlines companies.

Companies in infrastructure sector.

All Non-Banking Financial Companies (NBFCs)

Small Industries Development Bank of India (SIDBI).

Holding companies and Core Investment Companies (CICs)

Developers of Special Economic Zones (SEZs)/ National Manufacturing and Investment Zones (NMIZs).

Primer on External Commercial Borrowings (ECBs)

Track I Track II Track III Units in Special Economic Zones (SEZs).

Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (INVITs) coming under the regulatory framework of the Securities and Exchange Board of India (SEBI).

Companies engaged in miscellaneous services viz. research and development (R&D), training (other than educational institutes), companies supporting infrastructure, companies providing logistics services.

Export Import Bank of India (Exim Bank) (only under the approval route

Infrastructure sector, NBFC-IFC, NBFC-AFC, CICs, Holding Companies10

NBFCs-Micro Finance Institutions (NBFCs-MFIs), Not for Profit companies registered under the Companies Act, 1956/2013, Societies, trusts and cooperatives (registered under the Societies Registration Act, 1860, Indian Trust Act, 1882 and State-level Cooperative Acts/Multi-level Cooperative Act/State-level mutually aided Cooperative Acts respectively), Non-Government Organisations (NGOs) which are engaged in micro finance activities11.

17. Can Entities engaged in manufacturing sector avail ECBs?

Companies in manufacturing and software development sectors can avail ECB

under Track I subject to conditions laid down by the RBI.

Also refer the carve out available to manufacturing sector under Question 14.

10

https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10314&Mode=0 11

Entities engaged in micro-finance activities to be eligible to raise ECB:

(i) should have a satisfactory borrowing relationship for atleast three years with an AD Cat I bank in India, and

(ii) should have a certificate of due diligence on ‘fit and proper’ status from the AD Cat I bank.

Primer on External Commercial Borrowings (ECBs)

18. Can Corporate engaged in services sector avail ECBs under automatic route:

Companies in software development sector, Shipping and airline companies can

avail ECB under Track I, II and III.

Corporate engaged in miscellaneous services viz. research and development

(R&D), training (other than educational institutes), companies supporting

infrastructure and companies providing logistics services can avail ECB under

Track III.

Individual limit for service sector has been stipulated of USD200 million or

equivalent under automatic route. Corporate in the services sector can avail of

ECB beyond USD 200 million or its equivalent in a financial year under approval

route.

19. Can NBFCs avail of ECBs?

All NBFCs, under the purview of RBI,12 can avail ECBs under Track III for

following purpose:

o On-lending to the infrastructure sector;

o Providing hypothecated loans to domestic entities for acquisition of

capital goods/ equipments; and

o Providing capital goods/ equipment to domestic entities by way of lease

and hire-purchases.

Further, NBFCs-Micro Finance Institutions (NBFCs-MFIs), other eligible MFIs,

NGOs and not for profit companies registered under the Companies Act, 1956/

2013 are also eligible to raise ECB under Track III only for on-lending to self-

help groups or for micro-credit or for bonafide micro finance activity including

capacity building.

NBFC-IFC and NBFC-AFC can avail ECB under Track-I too, for the purpose of

investment in infrastructure sector only.

Position under erstwhile ECB framework:

NBFCs other than those specified below were not eligible to avail ECB.

NBFCs categorized as Non-Banking Financial Company-Micro Finance

Institutions’ (NBFC-MFIs), by the Reserve Bank, could avail ECBs under

Automatic Route.

12

https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10314&Mode=0

Primer on External Commercial Borrowings (ECBs)

NBFCs could obtain ECB under the approval route, with minimum average

maturity of 5 years, from multilateral financial institutions, reputable regional

financial institutions, official export credit agencies and international banks to

finance import of infrastructure equipment for leasing to infrastructure projects.

NBFCs categorized as IFCs by the Reserve Bank, were permitted to avail of ECBs,

including the outstanding ECBs, upto 75% of their owned funds, under the

automatic route as per A.P. (DIR Series) Circular No. 69 dated January 7, 2013.

NBFC-IFCs desirous of availing ECBs beyond 75 % of their owned funds would

require the approval of the Reserve Bank and, therefore, be considered under

the approval route. However, the same was subject to fulfillment of compliance

norms as stipulated by the Reserve Bank via DNBS circular dated February, 2010

and hedging of the currency risk in full.

NBFCs categorized as Asset Finance Companies ( AFCs) by the Reserve Bank

had been allowed vide A.P. (DIR Series) Circular No. 6 dated July8, 2013 to avail of

ECB subject to following conditions:

(i) NBFC-AFCs are allowed to avail of ECB under the automatic route from all

recognised lenders as per the extant ECB guidelines with minimum

average maturity period of five years in order to finance the import of

infrastructure equipment for leasing to infrastructure projects;

(ii) in cases, where the NBFC-AFCs avail of ECB in the form of Foreign

Currency Bonds from international capital markets, such ECBs will be

permitted to be raised only from those international capital markets that

are subject to regulations prescribed by the host country regulator in a

Financial Action Task Force (FATF) member country compliant with

FATF guidelines;

(iii) such ECBs (including outstanding ECBs) under the automatic route can be

availed upto 75 per cent of owned funds of NBFC-AFCs, subject to a

maximum of USD 200 million or its equivalent per financial year;

(iv) ECBs by AFCs above 75 per cent of their owned funds will be considered

under approval route by Reserve Bank; and

(v) the currency risk of such ECBs is required to be hedged in full.

20. Can HFCs avail ECBs?

All ECB loan agreements entered into before December 02, 2015 may continue

with the disbursement schedules as already provided in the loan agreements

without requiring any further consent from the RBI or any AD Category I bank.

For raising of ECB under ECB facility for low cost affordable housing projects

Primer on External Commercial Borrowings (ECBs)

(low cost affordable housing projects as defined in the extant Foreign Direct

Investment policy), the borrowers will, however, have time up to March 31,

2016 to sign the loan agreement and obtain the LRN from the Reserve Bank by

this date:

o HFCs can avail ECB subject to conditions that:-The HFC should be registered

with the National Housing Bank (NHB) and operating in accordance with the

regulatory directions and guidelines issued by NHB;

o The minimum Net Owned Funds (NOF) for the past three financial years shall

not be less than INR 300 crore;

o Borrowing through the ECB should be within the HFC's overall borrowing

limit of 16 times their Net Owned Funds (NOF);

o The net non-performing assets (NNPA) shall not exceed 2.5 % of the net

advances;

o The maximum loan amount sanctioned to the individual buyer will be capped

at INR 25 lakh subject to the condition that the cost of the individual housing

unit shall not exceed INR 30 lakh; and

o The ECB shall be swapped into Rupees for the entire maturity on fully

hedged basis.

HFCs while making the applications, shall

o submit a certificate from NHB, the nodal agency, that the availment of ECB is

for financing prospective owners of individual units for the low cost

affordable housing;

o ensure that cost of such individual units does not exceed Rs. 30 lakh and loan

amount does not exceed Rs. 25 lakh;

o ensure that the units financed are having maximum carpet area of 60 square

metres; and

o ensure that the interest rate spread charged by the HFCs to the ultimate

buyer is reasonable.

NHB shall ensure that interest rate spread for HFCs for on-lending to prospective

owners’ of individual units under the low cost affordable housing scheme is

reasonable.

The ECB to be availed will be subject to an aggregate limit of USD 1(one) billion

fixed for ECB under the low cost affordable housing scheme which includes ECBs

to be raised by developers/builders and NHB/specified HFCs, for each of the

financial year 2013-14, 2014-15 and 2015-16.

21. Can Infrastructure Finance Companies (IFCs) avail ECBs?

Primer on External Commercial Borrowings (ECBs)

IFCs can avail of ECBs under the Track I, Track II and Track III of the automatic

route.

Additionally, NBFC-IFC can also avail of facility of credit enhancement by eligible

non-resident entities (viz. Multilateral financial institutions (such as, IFC, ADB,

etc.) / regional financial institutions and Government owned (either wholly or

partially) financial institutions, direct/ indirect equity holder) to domestic debt

raised through issue of capital market instruments, such as Rupee denominated

bonds and debentures.

o NBFC-IFCs proposing to avail of the credit enhancement facility should

comply with the eligibility criteria and prudential norms laid down in

the circular DNBS.PD.CC No.168/03.02.089/2009-10 dated February 12,

2010 and in case the novated loan is designated in foreign currency, the

IFC should hedge the entire foreign currency exposure; and

o The reporting arrangements as applicable to the ECBs would be

applicable to the novated loans.

22. Can builders/real estate companies avail ECBs?

All ECB loan agreements entered into before December 02, 2015 may continue

with the disbursement schedules as already provided in the loan agreements

without requiring any further consent from the RBI or any AD Category I bank.

For raising of ECB under ECB facility for low cost affordable housing projects

(low cost affordable housing projects as defined in the extant Foreign Direct

Investment policy), the borrowers will, however, have time up to March 31,

2016 to sign the loan agreement and obtain the LRN from the Reserve Bank by

this date:

Only Developers/Builders registered as companies may raise ECB for low cost

affordable housing projects, qualifying as an eligible borrower, can avail of ECB

(not through issue of FCCBs) under the Approval Route.

They should have minimum 3 years’ experience in undertaking residential

projects, have good track record in terms of quality and delivery and the project

and all necessary clearances from various bodies including Revenue Department

with respect to land usage/environment clearance, etc., are available on record.

They should also not have defaulted in any of their financial commitments to

banks/ financial institutions or any other agencies and the project should not be

a matter of litigation.

Primer on External Commercial Borrowings (ECBs)

Builders/ developers meeting the eligibility criteria shall have to apply to the

National Housing Bank (NHB) in the prescribed format.

NHB shall act as the nodal agency for deciding a project’s eligibility as a low cost

affordable housing project, and on being satisfied, forward the application to the

Reserve Bank for consideration under the approval route.

Once NHB decides to forward an application for consideration of RBI, the

prospective borrower (builder/developer) will be advised by the NHB to

approach RBI for availing ECB through his Authorised Dealer in the prescribed

format.

The ECB availed of by developers and builders shall be swapped into Rupees for

the entire maturity on fully hedged basis

The ECB to be availed will be subject to an aggregate limit of USD 1(one) billion

fixed for ECB under the low cost affordable housing scheme which includes ECBs

to be raised by developers/builders and NHB/specified HFCs, for each of the

financial year 2013-14, 2014-15 and 2015-16.

23. What needs to be done for a builder to avail ECBs through the National Housing Bank?

If a builder/developer is not able to raise ECB directly as discussed above,

National Housing Bank shall be permitted to avail of ECB, under approval route,

for on-lending to such developers who satisfy the following eligibility criteria,

subject to the interest rate spread set by the Reserve Bank:

i) Developers/builders undertaking low cost affordable housing projects

should be a company registered under the Companies Act, 1956;

ii) Such developers/builders should have minimum 3years’ experience in

undertaking residential projects, and should have good track record in terms

of quality and delivery;

iii) The developers/builders should not have defaulted in any of their financial

commitments to banks/ financial institutions or any other agencies;

iv) The project should not be a matter of litigation;

v) The project should be in conformity with the provisions of master plan/

development plan of the area. The layout should conform to the land use

stipulated by the town and country planning department for housing

projects; and

vi) All necessary clearances from various bodies including Revenue Department

with respect to land usage/environment clearance, etc., are available on

record.

Primer on External Commercial Borrowings (ECBs)

The ECB to be availed will be subject to an aggregate limit of USD 1(one) billion

fixed for ECB under the low cost affordable housing scheme which includes ECBs

to be raised by developers/builders and NHB/specified HFCs, for each of the

financial year 2013-14, 2014-15 and 2015-16.

The ECB availed of by developers and builders shall be swapped into Rupees for

the entire maturity on fully hedged basis.

24. Who can be the lender for an ECB?

Track I Track II Track III

International banks and

International capital markets

All entities listed under

Track I but for overseas

branches / subsidiaries

of Indian banks.

All entities listed under

Track I but for overseas

branches / subsidiaries of

Indian banks.

Export credit agencies,

Suppliers of equipment, &

Foreign equity holders.

In case of NBFCs-MFIs,

other eligible MFIs, not

for profit companies and

NGOs, ECB can also be

availed from overseas

organisations13 and

individuals14.

Multilateral financial

institutions (such as, IFC,

ADB, etc.) / regional financial

institutions and Government

owned (either wholly or

13

Overseas Organizations proposing to lend ECB would have to furnish to the AD bank of the borrower a

certificate of due diligence from an overseas bank, which, in turn, is subject to regulation of host-country

regulators and such host country adheres to the Financial Action Task Force (FATF) guidelines on anti-money

laundering (AML)/ combating the financing of terrorism (CFT). The certificate of due diligence should

comprise the following: (i) that the lender maintains an account with the bank at least for a period of two years,

(ii) that the lending entity is organised as per the local laws and held in good esteem by the business/local

community, and (iii) that there is no criminal action pending against it. 14

Individual lender has to obtain a certificate of due diligence from an overseas bank indicating that the lender

maintains an account with the bank for at least a period of two years. Other evidence /documents such as

audited statement of account and income tax return, which the overseas lender may furnish, need to be certified

and forwarded by the overseas bank. Individual lenders from countries which do not adhere to FATF guidelines

on AML / CFT are not eligible to extend ECB.

Primer on External Commercial Borrowings (ECBs)

partially) financial

institutions.

Overseas long term investors

such as:

a. prudentially regulated

financial entities;

b. Pension funds;

c. Insurance companies;

d. Sovereign Wealth Funds;

e. Financial institutions

located in International

Financial Services Centres in

India

Overseas branches /

subsidiaries of Indian

banks15

25. Is it possible for a foreign equity holder to provide ECBs to the company in which such equity holder holds investment?

Eligibility for a foreign equity holder to be a ‘Recognized Lender’

Particulars Under Automatic

Route

Under Approval Route

For ECB upto USD 5

million

Minimum paid-up equity of

25% held directly by the

lender.

Minimum paid-up equity of

25% held directly by the

lender.

For ECB more than USD

5 million

Minimum paid-up equity of

25% held directly by the

lender & ECB liability-

equity ratio# not exceeding

4:1

Minimum paid-up equity of

25% held directly by the

lender & ECB liability-

equity ratio# not exceeding

7:1

15

Participation of Indian banks, their overseas branches / subsidiaries will be subject of prudential norms issued

by the Department of Banking Regulation (DBR) of the Reserve Bank.

Primer on External Commercial Borrowings (ECBs)

#For computation of ECB liability- equity ratio refer Question No.26

As per A.P (DIR Series) Circular No.31 dated September 4, 2013 eligible borrowers

are permitted to avail of ECB under the approval route from their foreign equity

holder company with minimum average maturity of 7 years for general corporate

purposes subject to the following conditions:

i. Minimum paid-up equity of 25 per cent should be held directly by the lender;

ii. Such ECBs would not be used for any purpose not permitted under extant the

ECB guidelines (including on-lending to their group companies / step-down

subsidiaries in India); and

iii. Repayment of the principal shall commence only after completion of minimum

average maturity of 7 years. No prepayment will be allowed before maturity.

26. What is the meaning of the debt/equity ratio in case of foreign equity holders?

Debt/equity ratio in case of foreign equity shareholders means the ECB liability-

equity ratio.

ECB liability means the proposed borrowing + the outstanding borrowing from

the concerned foreign equity holder lender.

Equity means Paid up capital + free reserves (including the share premium

received in foreign currency from the concerned foreign equity holder lender)

27. Whether availing of operating lease by an Indian Entity an ECB?

As per A.P.(DIR Series)Circular No.24 dated March 1, 2002, authorised dealers

may allow remittance of payment of lease rentals, opening of letter of credit

towards security deposit etc. in respect of import of aircraft/ aircraft engine/

helicopter on operating lease basis, after verifying documents to show that

necessary approval from the appropriate authorities has been obtained.

Further, by way of A.P.(DIR Series)Circular No.13 dated September 27, 2005 ADs

may permit airline companies (other than a Public Sector company or a

Department/Undertaking of the Government of India/State Government/s) to

remit up to USD 1,000,000 (US Dollar one million only) per aircraft towards

security deposit (for payment of lease rentals) with lessor for import of aircraft /

aircraft engine / helicopter on operating lease without a standby letter of credit

or a guarantee from a reputed international bank abroad or a guarantee of an AD

Primer on External Commercial Borrowings (ECBs)

in India against the counter-guarantee of a reputed international bank abroad

subject to following conditions:,

o The AD is satisfied about the bona fides of the transaction.

o The airline company has obtained necessary approval from appropriate

authority like Ministry of Civil Aviation/Director General of Civil Aviation,

Government of India for importing the aircraft/helicopter on operating lease.

o Remittance is permitted as per the Policy on Advance Remittances approved

by the Board of Directors of the bank or with the specific approval of the

Board of Directors of the bank.

o The final maturity of the security deposit should not be beyond the date of

the last installment towards lease rental or date of return of the aircraft /

helicopter to the lessor, whichever is later. If required, the deposit amount

may be adjusted towards lease rentals. However, the balance security

deposit, if any, should be repatriated before expiry of the lease period.

In case of an airline company in the Public Sector or a Department/Undertaking of

the Government of India/State Government/s, ADs may permit remittance of

amount exceeding USD 1,00,000 (US Dollar one hundred thousand only) per

aircraft towards security deposit (for payment of lease rentals) with lessor subject

to conditions specified above and a specific waiver of bank guarantee from the

Ministry of Finance, Government of India.

As per A. P. (DIR Series) Circular No.62 dated April 20, 2009, AD Category – I banks

are allowed to convey ‘no objection’ from the Foreign Exchange Management Act

(FEMA), 1999 angle for issue of corporate guarantee in favour of the overseas

lessor, for operating lease in respect of import of aircraft / aircraft engine /

helicopter, after obtaining –

o Board Resolution for issue of corporate guarantee from the company issuing

such guarantees, specifying names of the officials authorised to execute such

guarantees on behalf of the company.

o Ensuring that the period of such corporate guarantee is co-terminus with the

lease period.

Further, the Reserve Bank videNotificationNo. FEMA 206 / 2010-RB. dated June 1,

2010 amended the Foreign Exchange Management (Guarantees) Regulations,

2000 and inserted a new clause to the effect that :

“a bank which is an authorised dealer may, subject to the directions issued by the

Reserve Bank in this behalf, permit a person resident in India to issue corporate

guarantee in favour of an overseas lessor for financing imports through operating

lease effected in conformity with the Foreign Trade Policy in force and under the

provisions of the Foreign Exchange Management (Current Account Transactions)

Primer on External Commercial Borrowings (ECBs)

Rules, 2000 framed by Government of India vide Notification No G.S.R. 381 (E)

dated May 3, 2000 and the directions issued by Reserve Bank under Foreign

Exchange Management Act, 1999 from time to time.”

28. Can an Operating Leasing or Asset Renting entity avail ECBs?

o Operating leasing or Asset Renting entity render the service of providing the

asset on operating lease. The lessor has the legal title as well as the economic

ownership.

o Being companies engaged in miscellaneous services viz. companies supporting

infrastructure, companies providing logistics services can avail ECB under

Track III.

29. Is a financial lease also treated as ECB?

Yes, financial lease16, is also treated as ECB. The revised ECB framework

incorporates or identifies financial lease as a form of ECB unlike earlier

framework.

30. Can securitisation be treated as ECB?

ECB includes commercial loans in the form of securitized instruments like

floating rate notes, fixed rate bonds etc.

Thus raising money by way of securitisation from non-resident investors will be

treated as ECB.

31. What is the procedure for getting ECBs under automatic route?

Eligible Borrower enters into a loan agreement with the recognised lender for

raising ECB under Automatic Route.

The Borrower is required to submit Form-83, in duplicate, certified by the

Company Secretary (CS) or Chartered Accountant (CA) to the designated AD

bank.

The designated AD, after providing requisite details in Part F of the Form-83, will

forward one copy to the Director, Balance of Payments Statistics Division,

Department of Statistics and Information Management (DSIM), Reserve Bank of

16

Financial lease is a lease where the lessee is the owner, while the lessor has only the legal title and not the economic ownership.

Primer on External Commercial Borrowings (ECBs)

India, Bandra-Kurla Complex, Mumbai – 400 051, within 7 days from the date of

signing loan agreement between borrower and lender for allotment of LRN.

The borrower can draw-down the loan only after obtaining the LRN from DSIM,

Reserve Bank.

The Borrowers are then required to submit ECB - 2 Return certified by the

designated AD bank on monthly basis so as to reach DSIM, Reserve Bank within

7 working days from the close of month to which it relates.

32. What is the procedure for getting ECBs under approval route?

The Applicants are required to submit an application in Form ECB through the

designated AD to the Chief General Manager-In-Charge, Foreign Exchange

Department, Central Office, ECB Division, Reserve Bank of India, Mumbai-

400 001, along with following documents ( as relevant) certified by AD:-

o A copy of offer letter from the overseas lender/supplier furnishing complete

details of the terms and conditions of proposed ECB.

o A copy of the import contract, proforma/commercial invoice/bill of lading.

After obtaining the Approval, the Borrower is required to submit Form-83, in

duplicate, certified by the Company Secretary (CS) or Chartered Accountant (CA)

to the designated AD bank.

The designated AD, after providing requisite details in Part F of the Form-83, will

forward one copy to the Director, Balance of Payments Statistics Division,

Department of Statistics and Information Management (DSIM), Reserve Bank of

India, Bandra-Kurla Complex, Mumbai – 400 051, within 7 days from the date of

signing loan agreement between borrower and lender for allotment of LRN.

The borrower can draw-down the loan only after obtaining the LRN from DSIM,

Reserve Bank.

The Borrowers are then required to submit ECB - 2 Return certified by the

designated AD bank on monthly basis so as to reach DSIM, Reserve Bank within

7 working days from the close of month to which it relates.

Also, vide the A.P. (DIR Series) Circular No. 8017, dated 30th June, 2016 it has

been clarified that with a view to rationalizing and expediting the process of

giving approval, ECB proposals received in the Reserve Bank above a certain

threshold limit (refixed from time to time), be placed before the Empowered

17

https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10472&Mode=0

Primer on External Commercial Borrowings (ECBs)

Committee. The Reserve Bank will take a final decision in the cases taking into

account the recommendation of the Empowered Committee.

33. Is it necessary that ECBs must be full hedged?

The forex exposure of following borrowers needs to be fully hedged:-.

o In case of ECB availed by NBFCs categorized as IFCs and HFCs, the currency

risk needs to be fully hedged.

o If IFCs has availed of credit enhancement facility and the same gets invoked,

then in case the novated loan is designated in foreign currency, the IFCs

should hedge the entire foreign currency exposure.

o Infrastructure companies, CICs and Holding Companies also need to hedge

their currency risk, if ECB is raised under Track-I.

o ECB availed by the HFCs.

In case of other borrowers, hedging of ECB can be optional.

The entities raising ECB under the provisions of Tracks I and II are required to

follow the guidelines issued, if any, by the concerned sectoral or prudential

regulator with regard to hedging.

34. What are the restrictions on all-in cost of ECBs? What all is included in all-in costs?

The all-in-cost requirements for the three tracks will be as under:

Track I Track II Track III

1. For ECB with minimum average

maturity period of 3 to 5 years -

300 basis points per annum over 6

month LIBOR18* or applicable

bench mark for the respective

currency.

2. For ECB with average maturity

period of more than 5 years – 450

basis points per annum over 6

month LIBOR or applicable bench

mark for the respective currency.

The maximum spread over the

bench mark will be 500 basis

points per annum.

The all-in-cost

should be in line

with the market

conditions.

18

LIBOR means London Interbank Offered Rate being a benchmark giving an indication of the average rate at

which a LIBOR contributor bank can obtain unsecured funding in the London interbank market for a given

period, in a given currency. Libor rates are calculated for ten currencies and 15 borrowing periods ranging from

overnight to one year and are published daily at 11:30 am (London time) by Thomson Reuters.

Primer on External Commercial Borrowings (ECBs)

Penal interest, if any, for default or

breach of covenants should not be

more than 2 per cent over and above

the contracted rate of interest.

Remaining conditions will be as

given under Track I

All-in cost includes rate of interest and other fees and expenses in foreign

currency, guarantee fees whether paid in foreign currency or INR.

However, commitment fee, pre-payment fee, fees payable in Indian Rupees and

payment of withholding tax in Indian Rupees are excluded for calculating the all-

in-cost.

Cost of hedging is also not included in all-in cost ceiling.

In the case of fixed rate loans, the swap cost plus spread should be equivalent of

the floating rate plus the applicable spread.

35. What are the maturity restrictions on ECBs?

The minimum average maturities* for the three tracks are as follows:

Track I Track II Track II i. 3 years for ECB upto USD 50 million or its equivalent. ii. 5 years for ECB beyond USD 50 million or its equivalent. iii. 5 years for FCCB/FCEB irrespective of the amount raised. iv. 5 years for infrastructure companies, NBFC-IFC, NBFC-AFC, CIC, Holding Companies if raised under Track-I

10 years irrespective of the amount.

Same as under Track I.

* Computation of average maturity period may be viewed at Annex VI - Calculation

of Average Maturity- An Illustration. In case of domestic debt raised through issue of capital market instruments, such

as debentures and bonds, by all borrowers eligible to raise ECB under the

automatic route subject to fulfillment of certain conditions Viz. the underlying

debt instruments should have a minimum average maturity of three years and

Primer on External Commercial Borrowings (ECBs)

Prepayment and call/put options would be permissible for such capital

market instruments only after an average maturity period of 3 years.

36. The maturity restrictions talk about minimum maturity – is there anything on maximum maturity?

Under the extant norms on ECB provided by the Reserve Bank, there are no

restrictions pertaining to maximum maturity of ECB.

37. What is Take-out Finance and who are allowed to avail the facility of take-out finance?

Keeping in view the special funding needs of the infrastructure sector, take-out

financing arrangement through ECB, under the approval route, has been

permitted for refinancing of Rupee loans availed of from the domestic banks by

eligible borrowers in the sea port and airport, roads including bridges and

power sectors for the development of new projects, subject to the following

conditions:

o The corporate developing the infrastructure project should have a tripartite

agreement with domestic banks and overseas recognized lenders for either

a conditional or unconditional take-out of the loan within three years of the

scheduled Commercial Operation Date (COD). The scheduled date of

occurrence of the take-out should be clearly mentioned in the agreement.

o The loan should have a minimum average maturity period of seven years.

o The domestic bank financing the infrastructure project should comply with

the extant prudential norms relating to take-out financing.

o The fee payable, if any, to the overseas lender until the take-out shall not

exceed 100 bps per annum.

o On take-out, the residual loan agreed to be taken out by the overseas lender

would be considered as ECB and the loan should be designated in a

convertible foreign currency and all the extant norms relating to ECB should

be complied with.

o Domestic banks / Financial Institutions will not be permitted to guarantee the

take-out finance.

o The domestic bank will not be allowed to carry any obligation on its balance

sheet after the occurrence of the take-out event.

o Reporting arrangement as prescribed under the ECB policy should be adhered

to.

Primer on External Commercial Borrowings (ECBs)

However, RBI vide RBI/2013-14/585 A.P. (DIR Series) Circular No.129 dated May

9, 2014 have specified that eligible Indian companies will not be permitted to

raise ECB from overseas branches / subsidiaries of Indian banks for the purpose

of refinance / repayment of the Rupee loans raised from the domestic banking

system in respect of take-out financing scheme.

38. What are the options available for repayment of ECBs?

The ECB can be repaid as per the repayment schedule submitted while obtaining

the LRN.

The Designated AD bank has general permission to make remittances of

installments of principal, interest and other charges in conformity with the ECB

guidelines.

Alternatively, Conversion of ECB into equity is permitted subject to the following

conditions:-

o The activity of the company is covered under the Automatic Route for Foreign Direct Investment or Government (FIPB) approval for foreign equity participation has been obtained by the company, wherever applicable.

o The foreign equity holding after such conversion of debt into equity is within the sectoral cap, if any, as specified under the Consolidated FDI Policy issued by DIPP from time to time.

o Pricing of shares is as per the pricing guidelines issued under FEMA, 1999 in the case of listed/ unlisted companies.

Reporting requirements on conversion of ECB, to the Reserve Bank (Refer

Question No. 39.

39. What are the reporting requirements in case of conversion of ECB into equity?

In case of full conversion of outstanding ECB into equity:

o Form FC-GPR needs to be filed with the regional office concerned of the

Reserve Bank.

o Form ECB - 2 needs to be submitted to the DSIM, RBI within 7 working days

from the close of month to which it relates.

o The words “ECB wholly converted to equity” should be clearly indicated on

top of the Form ECB - 2.

o Once reported, filing of Form ECB - 2 in the subsequent months is not

necessary.

In case of partial conversion of outstanding ECB into equity:

Primer on External Commercial Borrowings (ECBs)

o The converted portion needs to be reported in Form FC-GPR to the Regional

Office.

o Form ECB - 2 needs to be filed for the unconverted portion, clearly

indicating “ECB partially converted to equity” on the top of the Form ECB - 2.

o In subsequent months, the outstanding portion of ECB should be reported in

Form ECB - 2 to DSIM.

40. Is prepayment allowed in case of ECB?

Prepayment of ECB may be allowed by AD Cat I banks subject to compliance with the stipulated minimum average maturity as applicable to the contracted loan under these guidelines. 41. Can ECB be refinanced by raising a fresh ECB or be rescheduled?

The designated AD Cat I bank may allow refinancing of existing ECB by raising fresh

ECB provided the residual maturity is not reduced and all-in-cost of fresh ECB is lower

than the existing ECB. Raising of fresh ECB to part refinance the existing ECB is also

permitted subject to same conditions.

42. What procedure needs to be followed in case of change in the terms and conditions of the ECB?

Particulars Approval needed from

Condition specified

Changes/Modifications in the drawdown/ repayment schedule19

Designated AD Category-I banks. (availed both under the approval and the automatic route)

Average Maturity period as declared while obtaining the LRN is maintained.

Changes/Modifications in the drawdown schedule resulting in the original average

Designated AD Category-I banks. (availed both under the approval and

no changes/ modifications in the repayment schedule of the ECB. such reduced average maturity

19 The changes in the drawdown/repayment schedule should be promptly reported to the DSIM,

RBI in Form-83. However, any elongation/rollover in the repayment on expiry of the original maturity of the ECB would require the prior approval of the Reserve Bank.

Primer on External Commercial Borrowings (ECBs)

maturity period undergoing change.

the automatic route)

period complies with the stipulated minimum average maturity period. Change in all-in-cost is only due to the change in the average maturity period. ECB guidelines are complied with and the monthly ECB - 2 returns in respect of the LRN have been submitted to DSIM.

20Re-schedulement of ECB due to changes in drawdown/repayment schedule

Designated AD Category-I banks. (availed both under the approval and the automatic route)

Changes, if any, in all-in-cost (AIC) is only on account of the change in average maturity period (AMP) due to re-schedulement of ECB and post re-schedulement, the AIC and the AMP are in conformity with applicable guidelines. There should not be any increase in the rate of interest and no additional cost (in foreign currency / Indian Rupees) should be involved. The re-schedulement is allowed only once, before the maturity of the ECB If the lender is an overseas branch of a domestic bank, the prudential norms applicable on account of re-schedulement should be complied with. The changes on accountof re-schedulement should be reported to DSIM through revised Form 83. The ECB should be in compliance with all applicable guidelines related to eligible borrower, recognised lender, AIC, AMP, end-uses, etc. The borrower should not be in

20 Inserted vide RBI/2013-14/584A.P. (DIR Series) Circular No. 128 dated 09/05/2014.

Primer on External Commercial Borrowings (ECBs)

the default / caution list of RBI and should not be under the investigation of Directorate of Enforcement.

Changes in the currency of borrowing

Designated AD Category-I banks. (availed both under the approval and the automatic route)

All other terms and conditions of the ECB should remain unchanged. The proposed currency should be freely convertible. The changes should be promptly reported to DSIM, Reserve Bank of India in Form-83.

Change of the AD Bank. Designated AD Category-I banks.

Subject to No-Objection Certificate (NoC) from the existing designated AD bank and after due-diligence. The changes should be promptly reported to DSIM, Reserve Bank of India in Form-83.

Changes in the name of the Borrower Company

Designated AD Category-I banks.

Subject to production of documents evidencing the change in the name from the Registrar of Companies. The changes should be promptly reported to DSIM, Reserve Bank of India in Form-83.

Change in the recognized lender

Designated AD Category-I banks.21

Subject to the AD ensuring that the new lender is a recognized lender as per the extant ECB norms

There is no change in other terms and conditions of the ECB.

ECB is in compliance with the extant guidelines.

The changes should be promptly reported to DSIM, Reserve Bank of India in Form-83.

Cancellation of LRN The Designated AD Subject to ensuring that no draw

21 When the original lender is an international bank or a multilateral financial institution (such

as IFC, ADB, CDC, etc.) or a regional financial institution or a Government owned development financial institution or an export credit agency or supplier of equipment and the new lender also belongs to any one of the above mentioned categories

Primer on External Commercial Borrowings (ECBs)

Category-I bank may directly approach DSIM for cancellation of LRN for ECBs availed, both under the automatic and approval routes

down for the said LRN has taken place.

The monthly ECB - 2 returns till date in respect of the LRN have been submitted to DSIM.

Change in the end-use of ECB proceeds22

The designated AD Category-I bank may approve requests for ECB availed under the automatic route

Subject to ensuring that the proposed end-use is permissible under the automatic route as per the extant ECB guidelines.

ECB is in compliance with the extant guidelines.

The monthly ECB - 2 returns till date in respect of the LRN have been submitted to DSIM.

The changes should be promptly reported to DSIM, Reserve Bank of India in Form-83.

Reduction in amount of ECB

The Designated AD Category-I bank may approve requests for ECB availed under the automatic route

Subject to ensuring that the consent of the lender for reduction in loan amount has been obtained.

The average maturity period of the ECB is maintained.

The monthly ECB - 2 returns till date in respect of the LRN have been submitted to DSIM.

There are no changes in other terms and conditions of the ECB.

The changes should be promptly reported to DSIM, Reserve Bank of India in Form-83.

Reduction in the all-in-cost of ECB

Designated AD Category-I banks. (availed both under the approval and the automatic route)

Subject to ensuring that the consent of the lender has been obtained.

There are no changes in other terms and conditions of the ECB.

The monthly ECB - 2 returns till

22 Change in the end-use of ECBs availed under the approval route will continue to be referred

to the Foreign Exchange Department, Central Office, Reserve Bank of India

Primer on External Commercial Borrowings (ECBs)

date in respect of the LRN have been submitted to DSIM.

43. Can Corporate, which have violated the extant ECB policy and are under

investigation by the Reserve Bank, avail of ECB?

As per A.P. (DIR Series) Circular No. 87 dated March 5, 2013 all entities are

permitted to avail of ECBs under the automatic route as per the current norms,

notwithstanding the pending investigations / adjudications / appeals by the law

enforcing agencies, without prejudice to the outcome of such investigations /

adjudications / appeals.

Accordingly, in case of all applications where the borrowing entity has indicated

about the pending investigations / adjudications / appeals, Authorised Dealers

while approving the proposal shall intimate the concerned agencies by

endorsing the copy of the approval letter.

The same procedure will be followed by the Reserve Bank of India also while

approving such proposals.

44. If I go for ECBs, should I hedge myself, or leave it unhedged?

This is substantially dependent on (a) whether you have a natural hedge in your

operations and revenues; and (b) what view would you like to take on the

movements in foreign exchange over time. Since ECBs are a long-term exposure,

the long-term movement of exchanges rates tends to kill the interest rate

differentials in a pair of currencies. However, this fundamental argument, called

interest rate parity theory, is currently affected by a whole lot of macroeconomic

factors.

45. How about accounting for forex losses in ECBs?

The Ministry of Corporate Affairs, vide Notification No. G.S.R. 225(E) dated 31st

March, 2009 issued Companies (Accounting Standards) Amendment Rules, 2009

thereby inserting paragraph 46 in Accounting Standard (AS) 11 relating to “The

Effects of Changes in Foreign Exchange Rates”.

By virtue of the same,