primary agent - july 2011 - pa edition

DESCRIPTION

Primary Agent - July 2011 - PA EditionTRANSCRIPT

PENNSYLVANIA

ALSO INTHISISSUE:_________________

Member profile: old and new media collide

7 tips for selecting an ad agency

G20662_C1s_July2011Primary 6/17/11 12:43 PM Page 3

Insurance for RestaurantsFamily Style, Pizza Shops, Take-Out, Fast Food, Donut Shops, Diners, Cafes, Bagel Stores, Franchises

Brokers Surplus Agency wants to quote your restaurants! We have a terrific BOP program that’s packed with the coverages you need.New Ventures eligible!Liquor liability coverage available!Contact us by phone or email today!(215) 443-9900Brokers Surplus AgencyP.O. Box 2849Warminster, PA 18974 Dennis Marsaglia, Ext. [email protected] Frisch, Ext. [email protected]

Insurance for RestaurantsFamily Style, Pizza Shops, Take-Out, Fast Food, Donut Shops,

Diners, Cafes, Bagel Stores, Franchises

Brokers Surplus Agency wants to quote your restaurants!

We have a terrific BOP program that’s packed with the coverages you need.New Ventures eligible!Liquor liability coverage available!

Contact us by phone or email today!(215) 443-9900

Brokers Surplus AgencyP.O. Box 2849

Warminster, PA 18974

Dennis Marsaglia, Ext. [email protected]

Evelyn Frisch, Ext. [email protected]

G20662_C2,C3,C4_Layout 1 6/17/11 1:36 PM Page 1

• Top 5 in Nation for Ease of Doing Business Deep Customer Connections• #1 Performing Company in Pennsylvania Insurance Agents & Brokers of PA• #1 Performing Company in New Hampshire Professional Insurance Agents of NH• Company of the Year in Maine Maine Insurance Agents Association

We’re honored that our Independent Agents have recognized our team’s exceptional customer service and ease of doing business:

hard work and a commitment to excellence.

To learn more about MMG,visit mmgins.com orcall us at 800-343-0533.

• Top 5 in Nation for Ease of Doing Business

Deep Customer Connections

• #1 Performing Company in Pennsylvania

Insurance Agents & Brokers of PA

• #1 Performing Company in New Hampshire

Professional Insurance Agents of NH

• Company of the Year in Maine

Maine Insurance Agents Association

We’re honored that our Independent Agents have recognized our team’s exceptional customer service and ease of doing business:

hard work and a commitment to excellence.

To learn more about MMG,

visit mmgins.com or

call us at 800-343-0533.

PennPRIME is the municipal entity specialist that can clearly illustrate ways to reduce risk. Formed, owned, and governed by our members, PennPRIME offers an array of products and services that are custom-tailored for Pennsylvania’s cities, townships, boroughs, and authorities. Composed of two insurance Trusts, PennPRIME provides comprehensive property, liability and workers’ compensation coverage as well as unique service programs like grants, training opportunities and sample loss control policies.Imagine a relationship with an organization with the leadership, advocacy, and Pennsylvania-specific expertise to take the burden of risk management off your client’s shoulders. Get into the swing of reducing your client’s risk. Imagine them as a client of PennPRIME…call today!

800.848.2040 • 717.236.9469 • www.pennprime.comPennPRIME is a service program of the Pennsylvania League of Cities and Municipalities

PennPRIME is the municipal entity specialist that can clearly illustrate ways to reduce risk. Formed, owned, and governed by our members, PennPRIME offers an array of products and services that are custom-tailored for Pennsylvania’s cities, townships, boroughs, and authorities.

Composed of two insurance Trusts, PennPRIME provides comprehensive property, liability and workers’ compensation coverage as well as unique service programs like grants, training opportunities and sample loss control policies.

Imagine a relationship with an organization with the leadership, advocacy, and Pennsylvania-specific expertise to take the burden of risk management off your client’s shoulders. Get into the swing of reducing your client’s risk. Imagine them as a client of PennPRIME…call today!

800.848.2040 • 717.236.9469 • www.pennprime.comPennPRIME is a service program of the Pennsylvania League of Cities and Municipalities

[ 1 ]

G20662_01-11_July2011 6/17/11 1:51 PM Page 1

The new marketing mix: Where will you meet your customers?

Tried and true marketing? Try tired and failing. The days of finding success from a cookie-cutter set of initiatives have long gone. Marketing savvy todaystems from an appreciation of flexibility and variety and an understanding that the customer knows best.

Page 12

Old and new media collide: How the Teeter Group found amarketing balance

When April Ressler purchased the Teeter Group in 2004, the agency was on a“maintenance” track. The three-person shop in Altoona, Pa. had a solid butstagnant book of business and an owner who was ready to retire. But Ressler saw growth potential.

Page 18

Tips for selecting a graphic design firm or advertising agency

The selection of an individual or firm to handle your marketing is one of the most important decisions a small company can make. Read on for seven tips to save time (and potential expense) when choosing a marketing partner.

Page 23

12

18

23

ContentsP R I M A R Y A G E N T M A G A Z I N E

Copyright 2011. All rights reserved. No material may be reproduced in whole or in part without written consent of the publisher. The information in this publication is general in nature and is not intended to serve as legal, accounting, financial,insurance, investment advisory or other professional advice as to any reader’s particular situation. Users are encouraged to consult withcompetent legal, financial, insurance, investment advisory and or other professional advisors concerning specific matters before makingany decisions and we disclaim any responsibility for any decisions or actions by readers. Statements of fact and opinion in PrimaryAgent are the responsibility of the authors alone and do not imply an opinion on the part of the officers or the members of the IA&B.Participation in IA&B events, activities and/or publications is available on a non-discriminatory basis and does not reflect IA&Bendorsement of the products and/or services.

Subscriptions: Non-member price: $2.25 per copy or $15 per year.

All communications for publications, including news, features, advertising copy, cuts, etc., must reach the editor by 1st of month two monthsprior to publication. Advertising rates furnished upon request.

Address inquiries to:Primary Agent EditorMechanicsburg, PA 17055-0763Phone (800) 998-9644 or (717) 795-9100 Fax (717) 795-8347

Periodical postage paid at Mechanicsburg, Pa. and additional entry post office.

Postmaster: Send address changes to above address.Primary Agent (ISSN 1543-3110), Permit # 638-620, Issue # 2011-7) is published monthly by IA&B Service Group Inc., a subsidiary of IA&B.

3 Glance at Events4 Chair of the Board’s Message5 Member FAQ6 State News8 Preventing Errors & Omissions10 Coverage Corner

17 IA&B Partners21 H.R. Headquarters25 Technology Update28 Advertisers Index28 Classified Ads28 Last & Least

In every issue

Mission StatementPrimary Agent delivers ideas to help InsuranceAgents & Brokers’ members negotiate their uniqueposition as guardians of trust between insuranceconsumers and companies while facing thechallenges of maintaining a small business. PrimaryAgent also supports IA&B’s mission to preserve andadvocate the American Agency System.

Get social with IA&B

G20662_01-11_July2011 6/17/11 1:51 PM Page 2

Date Topic Location

6 CISR: Commercial Casualty Course Reading, Pa.

7 CISR: Commercial Casualty Course State College, Pa.

12 CISR: Commercial Casualty Course Wilkes-Barre, Pa.

13 William T. Hold Seminar Lancaster, Pa.

14 William T. Hold Seminar Philadelphia, Pa.

19 CISR: Agency Operations Course Pittsburgh, Pa.

20 CISR: Agency Operations Course Altoona, Pa.

CISR: Commercial Casualty Course Lehigh Valley, Pa.

21 CISR: Commercial Casualty Course Mechanicsburg, Pa.

26 CISR: Commercial Casualty Course Hagerstown, Md.

Insuring Contractors Seminar Mechanicsburg, Pa.

27 CISR: Commercial Casualty Course Baltimore, Md.

Insuring Contractors Seminar Philadelphia, Pa.

Glance at EventsJ U L Y C A L E N D A R

On-Demand: Understanding the NFIP — Available anytime,anywhere you have Web access. Visit iabgroup.com/on-demand

SPEAK UP! YOUR JOB

DEPENDS ON IT!

SUPPORT AGENTPAC— your voice IN THE

STATE CAPITOL.

AgentPAC is your state political action committee and the collectivevoice of independent agents in the state capitol. Issues that affectyour job are at stake, and backing legislators aligned with IA&B’sgovernment affairs agenda depends on your support. Watch forGrassroots Action Alerts prompting you to contact your legislators onspecific issues, and consider donating to AgentPAC at a level thatspeaks (loudly) to policymakers that support our cause.

Your voice in the state capitol.

LEARN MORE AND CONTRIBUTE

ONLINE AT IABGROUP.COM/AGENTPAC.

G20662_01-11_July2011 6/17/11 1:51 PM Page 3

OfficersDavid Rosenkilde, CIC

Chair of the BoardReisterstown, Md.

Robert B. Hall, CPCU, CLU, ChFC, ARM, ARM-PVice Chair of the BoardWest Chester, Pa.

Kathleen M. Glattly, ChFC, CLU, CPCUImmediate Past Chair of the BoardFactoryville, Pa.

MembersJoyce M. Bailey, CIC, CRM, CPIW

Newark, Del.

Norman F. Basso, CPCUYork, Pa.

Vincent D. “Chip” Boylan Jr., CPCURockville, Md.

Henry “Butch” Bradley, Jr.Crofton, Md.

Timothy P. BurrisThompsontown, Pa.

John T. “Chip” Colwell Jr., CICCorry, Pa.

N. Lee Dotson, CIC, AAIWilmington, Del.

John L. FrankenfieldTelford, Pa.

G. Greg Gunn, CICLemoyne, Pa.

Diana M. Hornung Hanby, ACSRWilmington, Del.

Jocelyn R. Howard-Sinopoli, CIC, CISRButler, Pa.

Robert S. Klinger, LUTCFGermantown, Md.

Michael F. McGroarty Sr.Pittsburgh, Pa.

Ann Gallen Moll, CICReading, Pa.

Scott C. Rogers, CPIA*York, Pa.

Susan A. Sallada, CIC**Ft. Washington, Pa.

David B. Wasson Sr., CICState College, Pa.

James M. Watkins*Dover, Del.

King W. “Kip” White, LUTCFFallston, Md.

* IIABA National Director** PIA National Director

Board of Directors

Improving the independent agent’s image

IA&B’s recent agency-principal survey and Member AgentPanel meetings pointed to the same conclusion: Theindependent agency system’s image needs a facelift.

Roger that.

Competition in the personal-lines market is fierce. And,thanks to direct writers’ hefty advertising expenditures andprice-based messaging, the public now views insurance as acommodity. Which, of course, equates to a lack ofunderstanding of an independent agent’s value.

Hence the desire of members — and the independent agencysystem, as a whole — to educate the public and adjustconsumers’ perceptions. Plans are in the works to chip awayat this on a large scale. At the same time, opportunities existon a micro level, opportunities for individual agencies todifferentiate themselves and show their value in theircommunities. This issue of Primary Agent magazine offersperspectives and tips on doing just that.

Read on, and then stay tuned to IA&B in the coming monthsto learn more about broader campaigns to support theindependent agency system.

Until next time,Dave

[ 4 ]

David B. Rosenkilde Sr., CIC

Chair of the Board’sM E S S A G E

G20662_01-11_July2011 6/17/11 1:51 PM Page 4

[ 4 ]

ANSWER:Indirectly, yes. Every producer has hisor her employer information on filewith the state regulator. While there isno direct requirement to report achange of employer, the statuterequires that a producer’s change ofaddress be reported to the regulator. InDelaware, Maryland and Pennsylvania,the timeframe to report a change ofaddress is 30 days.

All three state regulators haveinterpreted the statute to extend to thebusiness address, not just the mailingor residential address. While absent aseparate action the chance ofenforcement is likely slim (particularlysince most producers will update theinformation when they renew theirlicense), it is prudent to proceed withthe notification within the 30 daysallotted. In addition, since manyproducers choose their employer’saddress as their mailing address, theywould not receive any communicationsfrom the Department of Insurance(unless the mail is forwarded by theirformer employer).

How to proceed? The simplest way is probably to use theNational Insurance Producer Registry atwww.nipr.com, Address ChangeRequest feature. There should be nocharge for this service.

DO YOU HAVE A QUESTION? E-mail it to us at [email protected] use “Primary Agent FAQ” in the subject line of your message. You can also fax your question to (717) 795-8347. We look forward toanswering your questions!

QUESTION: Should a change of employer be reported to the Department of Insurance?

MemberFAQ

G20662_01-11_July2011 6/17/11 1:51 PM Page 5

State NewsPrimary Agent | July 2011

The value of independent agents is vastlymisunderstood. Not to mention under fireby a barrage of direct writers’ priceyadvertising campaigns.

IA&B member agents report that theirimage in the public’s eye is of topconcern. In fact, a recent study ofmember agency principals found that 64percent look to the association forassistance with branding and promotingthe independent agency system’s value.And agents echoed that feedback atrecent Member Agent Panel (MAP)meetings. (See box below.)

In response, the IA&B Board of Directorsnamed branding and marketing a toppriority for the association in the monthsand years ahead.

What does that mean for you? IA&B’sguidance on implementing a nationalbranding campaign, Trusted Choice, alongwith regional-level, supplemental publicrelations and marketing efforts – effortsbased upon member research.

Understanding Trusted ChoiceThis nationwide campaign, available to all IA&B members as of Sept. 1,combines national advertising exposurewith coordinated, individual efforts at the local level.

Trusted Choice is a member benefitspearheaded by the Big “I” nationalassociation, to which all IA&B membersbelong. Member agencies, as well asinsurance companies that sell throughindependent agents, fund the campaign.

The campaign provides members with national advertising exposure,including broadcast media buys (seesidebar for upcoming ad flights) and anextensive online and Facebook presence,that direct the public to an agency locator at www.trustedchoice.com. What’s more, members can utilizecustomizable advertisements, a library of consumer content and syndicatedwebsite content feed.

[ 7 ]

Educating the public on independent agents’ value is key. During the spring2011 MAP meetings, members used the following terms and phrases tohighlight their differentiation points. IA&B’s upcoming marketing andpublic relations efforts will capitalize on these messages.

Advocate

Choice of carriers

Choice of coverages

Claims assistance

Community involvement

Counseling

Customized

Expert

Guidance

Hands on and face-to-face

Knowledgeable

More than price

More than a policynumber

Personal relationship

Professional

Reversing the “dumbingdown” of buying

insurance

Service and advice

Trusted advisor

Understandingcomplexities

Polishing up the independent agent’s image

Research

G20662_01-11_July2011 6/17/11 1:51 PM Page 6

Certificates: newACORD 25 to be used by July,not MayAgencies not showing the 05/10version of ACORD 25 on their agencymanagement system have a two-month buffer. IA&B recently contactedACORD based on inconsistent reportson the effective date of the newcertificate form (05/10 ed. date).

ACORD explained that a form’spublication date and edition date donot always match.

The edition date (version printed onthe form) is selected before the formis filed, based on when ACORDestimates all states will have approvedthe form. The form is published afterall states have approved it. As a result,discrepancies can occur. In this case,the 05/10 version was not officiallypublished until July 2010, making July31, 2011 the deadline for use of thenew ACORD 25 (05/10).

Read more on certificates:www.iabgroup.com/pa/certificates

SimplifyingSurplus LinesbusinessPlacing some difficult risks is threesteps easier thanks to IA&B members'suggestions. The InsuranceDepartment updated its export list toinclude several risks submitted byIA&B on behalf of members.

Export list risks don't require adiligent search (submitting the risk tothree different admitted insurers andreceiving denials) before placing thebusiness with a Surplus Lines insurer.

Read more on surplus lines:www.iabgroup.com/pa/surplus_lines

Word to the wiseabout lifeinsurance andannuity salesMind your p’s and q’s — and otherdesignation alphabet soup — whenselling life insurance or annuities toseniors. The Pennsylvania InsuranceDepartment recently issued a noticeto remind producers what constitutesunfair financial planning practicesunder Pennsylvania law.

Prohibited activities include:

w Using a professional designationnot formally recognized infinancial planning or consulting

w Making any deceptive ormisleading statement about thebusiness of insurance

The law also places disclosurerequirements and fee limitations oninsurance producers engaging infinancial planning. Penalties forviolation range from loss of license to $5,000 fines.

Read the Insurance Department'snotice: http://www.pabulletin.com/secure/data/vol41/41-20/833.html

[ 7 ]

Tune in forTrusted Choice

July advertising schedule on TNT*

Dates Time # of30-secondspots

July 11-15 6 a.m.-2 p.m. 5July 11-17 8-11 p.m. 4July 11-17 12-3 a.m. 5July 16-17 6 a.m.-6 p.m. 2July 18-22 6 a.m.-2 p.m. 5July 18-22 5-7 p.m. 2July 18-24 8-11 p.m. 2July 18-24 12-3 a.m. 5July 23-24 6 a.m.-6 p.m. 2

* The September 2010 through August2011 cable advertising schedule includesspots on The History Channel, USA, FoxNews, The Discovery Channel, TNT andThe Weather Channel.

Tune in forTrusted Choice

July advertising schedule on TNT*

Dates Time # of30-secondspots

July 11-15 6 a.m.-2 p.m. 5July 11-17 8-11 p.m. 4July 11-17 12-3 a.m. 5July 16-17 6 a.m.-6 p.m. 2July 18-22 6 a.m.-2 p.m. 5July 18-22 5-7 p.m. 2July 18-24 8-11 p.m. 2July 18-24 12-3 a.m. 5July 23-24 6 a.m.-6 p.m. 2

* The September 2010 through August2011 cable advertising schedule includesspots on The History Channel, USA, FoxNews, The Discovery Channel, TNT andThe Weather Channel.

Taking the next stepLook to IA&B for tips on leveragingTrusted Choice. The association willwalk members through utilization andsupplement the campaign withregional-level public relations andmarketing efforts. The goal? To educatethe public on who independent agentsare and what value they offer – themessages prioritized by members inIA&B’s research.

IA&B will supply additional informationin the coming months on how best toembrace Trusted Choice and how tosupport regional efforts to enhanceindependent agents’ image. In themeantime, learn more atwww.TrustedChoice.com/agents.

G20662_01-11REV.qxp:July2011 6/21/11 3:47 PM Page 7

[ 8 ] [ 9 ]

CURTIS M. PEARSALLCPCU, AIAF, CPIA

Curtis M. Pearsall, CPCU, AIAF,

CPIA, president of Pearsall

Associates Inc. and special

consultant to the Utica

National Errors & Omissions

Program, supplied this article.

education programs.

Primary Agent | July 2011

While Errors & Omissionsfrequency is generally downcompared to a couple ofyears ago, this is still an areacausing E&O claims. In fact,some E&O carriers believethis is so significant it has theability to generate enoughE&O claims to cause claimsfrequency to rise.

Many commercial andpersonal lines customershave been looking for pricingreductions in recent yearsbecause of the soft market.There has been atremendous amount ofinternal remarketing of thoseaccounts to your variouscarriers to address thesituation and ensure youretain the account. Forexample, if you marketed theaccount to five other carriers,there is significant potentialfor there to be differencesbetween the incumbentcarrier and the additionalmarkets. When you look tomove the account fromCompany A to Company B tosave the customer money onhis premium, it is critical your

agency identifies anycoverage differences andbrings them to thecustomer’s attention.

What could happen?Say you moved the accountto another carrier and thecoverage was not as broad insome areas. If the customersubsequently suffered anunderlying claim that wouldhave been covered byCompany A but was notcovered or not fully coveredby Company B, he very wellmay question your agencyabout why the coverage was moved. There is also a good chance of thecustomer saying that henever would have approvedyou moving the account if heknew he was giving upcoverage. This obviouslyspeaks to the need todocument these discussionswith your customers.

There are several areas ofpossible difference: sub-limits, the actual coveragegrant, specific endorsements,definitions for areas such as

“who is an insured,” what isexcluded on one policycompared to another, andthe rating of the carrier. Inaddition, advise the customerof a change in premiumpayment handling (agencybill to direct bill) as this couldcause some confusion andpotentially result incancellation of coverage.

The recommended approachis taking all the carriers youare considering and puttingthe details on a spreadsheet.Note all pertinent issues,limits, sub-limits, coveragegrants, etc. While this willtake time, it is crucial to noteall differences. Simplymoving the account and notadvising the customer of thedifferences could cause you aproblem down the road.Some agencies share thesespreadsheets with thecustomer and bring to hisattention the detail he needsto be aware of. Mostimportantly, the customersees the differences and canmake an educated decision.At minimum, the differences

THE MIRROR TEST – A SIGNIFICANT ERRORS &OMISSIONS HOTSPOT

PreventingE R R O R S A N D O M I S S I O N S

G20662_01-11_July2011 6/17/11 1:51 PM Page 8

[ 9 ]

between the expiring policy andcoverage from the other carriers youare considering should be brought tothe customer’s attention.

Get the customer’s written approval,regardless of his final decision. This will be key if an underlying claim occurs and your customer then finds out he didn’t have thecoverage he thought. It is fine if yourclient chose the lower price with thelesser coverage, but get in writing that he realized he was giving upsome coverage.

Important for all coveragesThe above scenario can occur even ifyou keep the account with the samecarrier. This is probably morecommon with Excess & Surplus Linesbusiness because E&S carriers are not required to give a conditionalrenewal notice if they want to add an exclusion on the renewal. Youshould still identify any differences on the renewal policy, bring it to thecustomer’s attention and get hissignoff. Due to the nature of E&S,it is best to do this review with thecustomer before you bind thecoverage in case the customersubsequently decides he doesn’t want the coverage. This will help your agency avoid the typicalminimum earned premium associatedwith E&S business.

This detailed comparison is importantfor all coverages. If you writeprofessional liability and/or Directors& Officers, you are aware that no twopolicies are the same. Thus, there areprobably more things to look at. E&Oclaims have occurred because anexclusion was in one policy but notthe other. It is best to identify thedifferences and bring them to thecustomer’s attention for theirapproval, regardless of how subtleyou believe the issues to be.

A detailed comparison is needed withthese lines of business. Consider askingthe respective carriers how theycompare with another carrier. Theymay have a comparison they can sharewith you or a checklist that identifiesmany of the issues you must watch for.In addition, there are firms that willperform these comparisons for you fora fee. They are extremely good at whatthey do and worth the cost.

For whatever the reason you wouldswitch the coverage from one carrierto another for a customer, make sureit passes the mirror test. Remember,too, to identify the differences, bringthem to the customer’s attention andget his written sign off.

in a five-minute phone call.

ArtisanContractors

coverage

800-334-5579www.gotapco.com

CGL Coverage Available:

* Available coverages and markets may varydependent upon risk characteristics.

Call. Quote. Bind.

“A”-ra e o -a i e carrier

Co e i ive rici g

a olic r aro

- e i a ci g available i o a e

Q ic cla a li g

10 cre i o o r er o alize A CO Zc i a ebi car i eac olic

i a a erCar a ACH a e acce e

The TAPCO Service Pledge

1,000 Strong More than 1,000 classes of P&C businesswritten under binding authority.

G20662_01-11REV.qxp:July2011 6/21/11 3:48 PM Page 9

CoverageC O R N E R

[ 10 ] [ 11 ]

JERRY M. MILTON, CIC

Jerry M. Milton teaches

and consults on industry

issues. The legal profession

recognizes him as an

expert on insurance

coverages. He is also the

education consultant for

IA&B, working with CISR,

CIC and continuing

education programs.

Primary Agent | July 2011

We live in a litigious society.You know that. Today, juriesand judges don’t think twiceabout handing out multi-million dollar awards whensomeone has been seriouslyinjured. You also know that.

There is no question that theownership and use of ourautos present us with thegreatest personal liabilityexposure. But our normaldaily activities can expose usto the potential of a largeliability claim that couldthreaten our personal assets.

One of the best ways tounderstand the need for aPersonal Umbrella policy isto review actual claimexamples. Listed below areactual personal liabilityclaims that illustrate the need for higher personalliability limits.

Loss #1:A babysitter left a 5-month-old infant unattended in awalker. The infant toppledthe walker, struck her headon the floor and suffered

brain damage. The parents ofthe infant sued the teenagebabysitter and her parents.The court awarded theparents $11,000,000.

Loss #2:A 28-year-old engineer doveinto a friend’s above-groundswimming pool, struck hishead on the bottom and, as aresult, became aquadriplegic. He sued boththe homeowner and the poolmanufacturer. The courtfound the homeowner to be60 percent responsible andthe pool manufacturer to be40 percent responsible, andawarded $10,000,000.

Loss #3:An 18-year-old collegestudent was struck byfraternity paddle duringinitiation. He sustained facialfractures and blindness in hisleft eye. The fellow fraternitymembers and their familieswere sued. The courtawarded $1,300,000.

Loss #4:The insured’s 18-year-old sonwas driving his parents’ carto the store with his 19-year-old girlfriend. He left theroadway and hit a tree. Theson told the police thatanother car cut him off, butthere were no witnesses, andthe girlfriend had norecollection of the accident.She was hospitalized for overa month with multiplefractures and internal injuriesand received extensivephysical therapy. ThePersonal Umbrella insurersettled with the girlfriend forthe policy limit.

Loss #5:The insured hosted a party athis home. Among the guestswas a family friend, who wasalso the insured’s financialadvisor. The friend broughthis wife, their 2-year-old childand their baby to the party.The insured gave them a jugof spring water to mixformula for the baby. The 2-year-old child also had adrink of the water. Shortlythereafter, both children

WHY DO I NEED A PERSONAL UMBRELLA?

G20662_01-11_July2011 6/17/11 1:51 PM Page 10

[ 10 ] [ 11 ]

became ill. The family left the party andtook the children to the hospital. Thehospital confiscated the water jug whichwas found to contain arsenic. An oldlabel was found wrapped around thehandle with the words “weed killer”printed on it. The insured hadmistakenly given the jug, which wassimilar to the ones containing springwater, to the family. The baby died and the 2 year old survived after being in critical condition several days. The Personal Umbrella liabilitylimit was paid.

Loss #6:A couple hosted a pool party for theirteenage children. They did not provideany alcohol, but it was brought by someof the guests and was available. Afterleaving the party, one of the guests wasseverely injured in an auto accident, andthe injury was attributed to hisconsumption of alcohol. This case wentto the Wisconsin Supreme Court whichdecided that anyone who sells orfurnishes alcohol to a minor isresponsible for the minor’s injuries aswell as any injuries caused by the minor.The opinion of the court was that thehomeowners should have prevented theconsumption of alcohol by minors ontheir premises. Both the Homeowners’and Personal Umbrella policiesresponded to this claim.

The above losses show theconsequences of situations that canquickly exhaust the liability limits of theunderlying policies.

For less than the cost of a cup of coffeea day, most folks can purchase aPersonal Umbrella policy with a limit of $1,000,000, possibly $2,000,000 oreven $5,000,000.

Y’all take care!

Opening up opportunitywith personal umbrellasMember agent success story

When Nichole Leibensperger took advantage of IA&B members’access to RLI Personal Umbrella, part of the Market OptionProgram, sales took off. Within a matter of months, she became theorganization’s highest policy-count producer.

“The RLI rates are fabulous, and the product is great,” saysLeibensperger, owner of Sinking Spring, Pa.-based Chase InsuranceAssociates. She also touts the product’s stand-alone aspect — whichallows insureds to maintain their homeowners’ and auto coveragewith their current carrier(s) — and its ability to insure multipleinvestment properties.

Chase Insurance Associates has zoned in on real estate investmentclients, and RLI — along with IA&B service — have proved an ideal match.

“The staff has been excellent, and the product sells itself,” sharesLeibensperger. “Business has exploded.”

Editor’s note: Learn more about the RLI Personal Umbrella —and IA&B’s complete Market Option Program — by visitingwww.iabgroup.com and selecting “Insurance Products.” Orcontact IA&B’s Member Service Center at (800) 998-9644.

G20662_01-11_July2011 6/17/11 1:51 PM Page 11

MARKETING

The new marketing mix:Where will you meet your customers?

Tried and true marketing? Trytired and failing. The days offinding success from a cookie-cutter set of initiatives havelong gone. Marketing savvytoday stems from anappreciation of flexibility andvariety and an understandingthat the customer knows best.

G20662_12-17.qxp:July2011 6/21/11 3:50 PM Page 12

[ 13 ]

Primary Agent | July 2011

It wasn’t so long ago that the marketer’s quiver held ahandful of arrows. The skillful often chose somecombination of print advertising, radio, broadcasttelevision and cable spots, Yellow Pages ads, direct mail,

billboards, special events, telemarketing, press stories — andof course, word of mouth. These were the trusted marketingtools. You could count on them.

That was then; this is now, and everything has changed.More accurately, it is changing. Since most of us preferstability and predictability, we may see what is occurring assomething akin to a transition from the old to the new as welook for a new list of trusted tools to emerge. Unfortunately,it may be little more than wishful thinking.

This picture came into abrupt focus one morning when thetelephone rang. It was a vendor from a company placingvideo monitors displaying consumer ads in supermarkets.

“As you know, advertisers are trying new ways to get tocustomers, particularly since many of the traditionaltechniques are no longer effective,” said the salesperson,who was expressing the deepening dilemma facingcompanies today. Not only are there no silver bullets, but thebullet supply is running mighty low.

Although some may disagree, no one has a corner on the"right answers" today when it comes to marketing tactics.When someone asks if a particular tactic will produce thedesired results, there is only one acceptable answer: It alldepends on the product or service, the target demographic,the message and, particularly, how the target customerswant to be approached.

___________________________________________________________

If there is a message in all this, don’t expect anytactic to last. Everything is temporary. Technologywill constantly open the way to new opportunities.

___________________________________________________________

Recent CNN debates with Democratic and Republicancandidates are a good example of the profound changestaking place not only in political marketing, but the entiremarketing universe as well.

Perhaps the most dramatic event took place in July 2007when 3,300 people posted video questions on YouTube for a Democratic presidential candidates’ debate. It was the

________________________________

Not only are there no silver bullets, but the bullet supply is

running mighty low.

________________________________

I

G20662_12-17_July2011 6/17/11 2:08 PM Page 13

first-ever political reality-TVevent and what may come to bethought of as a marketingwatershed in politicalcampaigning. It may havehelped shape the answer to thisquestion: Is voter apathy thefault of the voters or is it areflection of feeling ignored?

The event sent the message that the public wants “realpeople” to question thecandidates. No longer will weaccept professional talkingheads interposing themselvesbetween candidate andquestioner. Even more to the point, the politicos looked painfully uncomfortablethat evening as they struggled to come up with “make sense” answers.

While this is but one example of the many communicationchanges taking place today, it illustrates the sea changethat’s occurring.

To put it as clearly as possible,no marketer can say withcertainty how to reach aparticular audience as thingsstand today. If that isn’t enough,there is reason to doubt that theclouds of confusion soon willpart and the sunlight of certaintywill shine again.

This was driven home recentlywhile going over a proposal we were preparing for aprospective client. Although thiswas a modest-size regionalbusiness, we found we wererecommending a dazzling arrayof 11 different marketing tactics.

Here are some “thought-lines”when considering anorganization’s marketingstrategies:

1. All marketing tactics aretemporary. The time has cometo recognize that there are nopermanent solutions. One majorsoft drink company is changingthe design of its cans every 12weeks in an effort to grabattention, while wine bottles arequickly becoming works of art.

The e-mail blast frenzy lastedabout a year, about as long as it took to ramp up the spamfilters. The question today isalways, what’s next? WillGoogle’s cell phone deliveradvertising messages that workwith consumers? Shouldelectronic ads be games? And what about mini-social(and micro) networks? How will they fare in lettingcustomers speak with eachother about your company’sproducts and services?

If there is a message in all this,don’t expect any tactic to last.Everything is temporary.Technology constantly will openthe way to new opportunities.

2. All marketing is essentiallyexperimental. On top of thetemporary nature of marketingtactics, they are alsoexperimental.

“We’re waiting to see how allthis shakes out before we doanything,” says a companypresident. The words arehauntingly reminiscent of thosewho announced rather proudlythat they would wait to buy a

MARKETING

[ 14 ]

A major shift in

thinking about

marketing is

needed.... Marketers

are juggling up

to a dozen or

more [tactics] at the

same time.

G20662_12-17.qxp:July2011 6/21/11 3:53 PM Page 14

computer until they wereperfected. Today, these samepeople view their computers asdisposable. It all happened in justa few years.

Even though there are those,particularly some vendors and adagencies, that like to suggest thatthey have “the answer,” it’s clearthat all marketing is, to oneextent or another, experimental.There are no certainties, noguarantees. What works with onegroup of customers may not workwith another. And some thingsdon’t work at all.

3. Marketing requires anarray of tactics. A major shift inthinking about marketing isneeded. Rather than bouncingthree or four balls at one time,marketers are juggling up to adozen or more at the same time.The roster may include a blog, aseries of eBulletins delivered toparticular customer segments,several websites, advertisingsequences on Google and Yahoo,personalized direct mail, TV andradio spots, print newsletters,print advertising in selectedvenues, billboards and a mini-social network, to name but afew. The frustration is felt whensomeone says, “What abouttrying billboards?”

The marketing concept is findingways to connect as intimatelyand meaningfully as possiblewith individual customers,recognizing that not even threeor four venues can deliver yourmessage to your entire universeof customers and prospects.

4. Customers are the onlyexperts. Perhaps the mostpoignant moment of the CNN TV debate featuring thevideoed questions was the onefeaturing the woman who hadlost her hair as a result of breastcancer treatment. Nothing wasmore real than her questionabout healthcare.

_________________________________

Today’s customers think lessabout brands and more

about themselves.

_________________________________

Al Wittemen, the managingdirector for retail strategy forAdvantage Retail and a marketerfor 35 years, points out thattoday’s customers think lessabout brands and more aboutthemselves. Even though itshould be obvious, it’s ignoredmore often than not.

Wittemen uses prepared foods asan example of consumerbehavior. When the customercomes to the supermarket, thereis far less interest in picking out aparticular brand than there is inpicking out dinner for tonight. Inother words, “Shoppers are notnecessarily looking for highdrama. More often, they arelooking for relevant solutions totheir immediate needs,” he notes.

Why did an advertising agencyreplace a higher-end well-knownbrand (Xerox) copy machine witha lesser known one (Lexmark)?It’s simpler, faster and more

flexible. That’s exactly whatHonda, Hyundai and Kia are all about, too.

When customers are gettingready to make a purchase today,the first place they go is to theInternet, to look for what othershave to say.

Among his observationsregarding customer behavior,George Colony, the ForresterResearch CEO, says that while100-question surveys might helpmeasure customer satisfaction,there is one question that will dothe job: “Would you recommendthis product or service to a friendor colleague?”

It’s time to forget about the hypeand listen to the customers;they’re the experts.

The marketing mix today isn’tjust in flux; it’s fluid. If anyonethinks it’s time to wait on thesidelines until the parade ofpossibilities goes by, thecompetition will have run off with the customers._______________________________

John R. Graham is president ofGraham Communications, amarketing services and salesconsulting firm. He is the author ofThe New Magnet Marketing andBreak the Rules Selling, writes for avariety of business publications, andspeaks on business, marketing andsales issues. Contact him at 40 Oval Road, Quincy, Mass. 02170;617-328-0069;[email protected].

[ 15 ]

Primary Agent | July 2011

G20662_12-17_July2011 6/17/11 2:08 PM Page 15

There are 175 reasons why agentssay they like to do business withMutual Benefit Group. Its people.

People they know by name. There’sSally, who has been underwritingbusiness in MBG’s Personal LinesDepartment for 47 years, and Elaine,who’s handled commercial accounts for33. Patsy has 42 years’ experience in theClaims Department; Joyce has beenprogramming computer applications for39 years. For 36 years, Shelby’s beenhandling payments and answeringquestions about billing.

Since 1908, Mutual Benefit has nurtureda relationship-driven corporate culturethat provides uncommon support for itsemployees, who in turn deliver anuncommon insurance experience toagents and policyholders alike. Thecompany enjoys a low employeeturnover rate of 6 percent. Seventy-threepercent of employees have been withthe company five years or more, 30 percent 15 years or more. MutualBenefit also makes a strong commitmentto professional development; in 2010,one-third of the company’s employeescompleted at least one company-reimbursed education course, with 13 earning a professional insurance credential.

In an industry where expertise is criticaland employee turnover is common,agents have commented on how muchthey appreciate knowing they will reachthe same personable, experiencedprofessional each time they call MutualBenefit. As one agent put it, “In today’sworld, it’s very unusual to see anybusiness have the same excellent staffcontinue to work for them for such anextended period of time as is the casewith Mutual Benefit. The people at MBG offer prompt, professional servicewhile never losing sight of adding a little friendly conversation along theway. I couldn’t imagine working in the insurance industry without Mutual Benefit Group.”

Selecting and retaining top-notchprofessionals is just one of the waysMutual Benefit exhibits its commitmentto its 250 independent agents and itsnearly 100,000 policyholders. Supportingthe independent agency system for over100 years has given Mutual Benefit aunique perspective on the importance offostering strong business ties withagents. We understand how critical it isto remain accessible to agents, and howimportant it is to listen to their needs inorder to respond in a way that benefitseveryone in the business relationship.

As the Insurance Agents and Brokersconducted their fourth CompanySatisfaction Index Survey in 2010, MutualBenefit Group for the fourth time in arow placed among the top threeinsurance carriers in its area ofoperation, ranking number two overallin commercial lines and tying fornumber three overall in personal lines.Mutual Benefit CEO Steve Sliver states,“The survey results reflect our staff’sone-of-a-kind commitment toaccessibility and responsiveness as theyprovide agents with the conscientiousservice, flexible underwriting, qualityproducts, exceptional claims handling,and technological systems that agentsdemand and deserve.”

As Mutual Benefit enters its secondcentury in the insurance industry with acorporate culture dedicated to buildingstrong relationships, it’s not surprisingthat “You Know Who we ARE(Accessible, Reliable, Experienced).” We reaffirm our commitment to a strong rapport with agents, a rapportthat elicits comments like this: “I treasure my relationship with Mutual Benefit and its many fine people.They always travel the high road.”

FEATURED PARTNERMutual Benefit Group

CHIEF EXECUTIVE OFFICERSteven C. Sliver, President and CEO

COMPANY LOCATIONHuntingdon, Pennsylvania

A.M. BEST RATING “A-” (Excellent)

WEB SITEwww.mutualbenefitgroup.com

Insurance Agents & Brokers proudly recognizesMutual Benefit Group as one of its Platinum Partners.IA&B Platinum Partners dedicate the highest level ofsponsorship to our organization.

Platinum Profile

G20662_12-17_July2011 6/17/11 2:08 PM Page 16

WHAT IS IA&BPARTNERS?The IA&B Partners

program gives company

and allied businesses

the opportunity to

demonstrate their

commitment of support

to independent agents

and receive maximum

market exposure. As an

IA&B Partner, you will

also realize the benefits

of IA&B membership to

help you succeed in

the insurance industry.

DO YOU SEEYOUR NAME?To become an IA&B Partner,

choose the sponsorship

package that matches your

commitment of support.

Contact the Member Sales

Center at (800) 998-9644,

(717) 795-9100 or visit us

online at www.iabgroup.com

to get started.

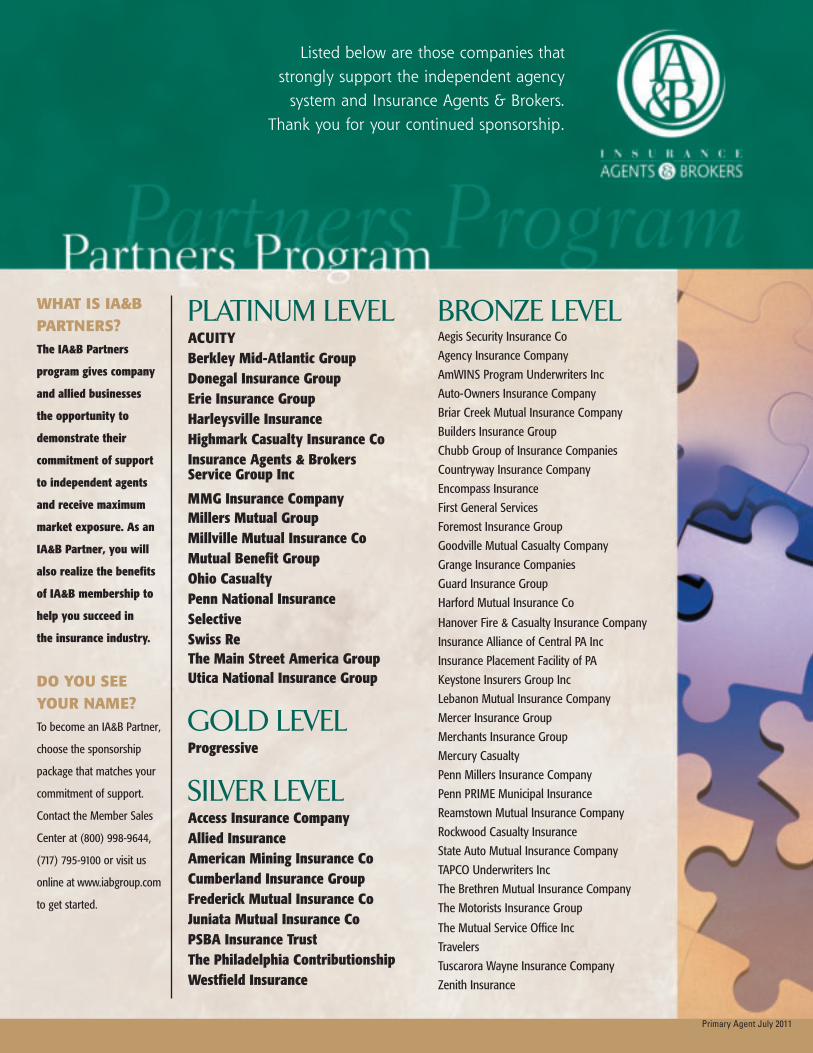

Listed below are those companies that strongly support the independent agencysystem and Insurance Agents & Brokers.

Thank you for your continued sponsorship.

PLATINUM LEVELACUITYBerkley Mid-Atlantic GroupDonegal Insurance GroupErie Insurance GroupHarleysville InsuranceHighmark Casualty Insurance CoInsurance Agents & BrokersService Group Inc

MMG Insurance CompanyMillers Mutual GroupMillville Mutual Insurance CoMutual Benefit GroupOhio CasualtyPenn National InsuranceSelective Swiss ReThe Main Street America GroupUtica National Insurance Group

GOLD LEVELProgressive

SILVER LEVELAccess Insurance Company Allied InsuranceAmerican Mining Insurance CoCumberland Insurance GroupFrederick Mutual Insurance CoJuniata Mutual Insurance CoPSBA Insurance TrustThe Philadelphia ContributionshipWestfield Insurance

BRONZE LEVELAegis Security Insurance Co

Agency Insurance Company

AmWINS Program Underwriters Inc

Auto-Owners Insurance Company

Briar Creek Mutual Insurance Company

Builders Insurance Group

Chubb Group of Insurance Companies

Countryway Insurance Company

Encompass Insurance

First General Services

Foremost Insurance Group

Goodville Mutual Casualty Company

Grange Insurance Companies

Guard Insurance Group

Harford Mutual Insurance Co

Hanover Fire & Casualty Insurance Company

Insurance Alliance of Central PA Inc

Insurance Placement Facility of PA

Keystone Insurers Group Inc

Lebanon Mutual Insurance Company

Mercer Insurance Group

Merchants Insurance Group

Mercury Casualty

Penn Millers Insurance Company

Penn PRIME Municipal Insurance

Reamstown Mutual Insurance Company

Rockwood Casualty Insurance

State Auto Mutual Insurance Company

TAPCO Underwriters Inc

The Brethren Mutual Insurance Company

The Motorists Insurance Group

The Mutual Service Office Inc

Travelers

Tuscarora Wayne Insurance Company

Zenith Insurance

Primary Agent July 2011

G20662_12-17_July2011 6/17/11 2:08 PM Page 17

MARKETING

Old and new media collideHow the Teeter Group found a marketing balance

When April Ressler purchased the Teeter Group in 2004, the agency was on a“maintenance” track. The three-person shop in Altoona, Pa. had a solid but stagnant book of business and an owner who was ready to retire.

G20662_18-28.qxp:July2011 6/21/11 3:54 PM Page 18

[ 19 ]

Primary Agent | July 2011

But Ressler – who had, and continues to oversee, abook of business with Bedford, Pa.-based Reed, Wertz& Roadman, Inc. — saw growth potential. Withinseven years she and her husband, the Teeter Group

office manager, expanded the agency’s staff complement,expertise and value. No doubt their progressive marketingstrategy is partially to thank.

One of the playersRessler began marketing the agency aggressively in 2004. Sherelied on billboard, newspaper and television advertising andfound success.

“We’re one of the players now,” she explains. “Customers thinkof us. They’ve heard of us.”

Then in 2010, Ressler met with her long-time partneredmarketing firm, Egan Advertising, as well as Artemis Group,her original website designer, and Magnetic MarketingUnlimited, a firm dedicated to social networking and onlinemarketing. She explained her desire to venture into Web-basedmarketing and then split her 2011 advertising budget in two —dedicating half to the traditional media that served her welland the other half to website revisions and Internet-driventactics that she knew had potential.

“My husband and I are in our 30s, and we research everythingonline,” she admits. “The younger generation goes on theInternet to read testimonials and consider their purchases.”

Recent surveys substantiate Ressler’s claim. According toAgents Council for Technology, 81 percent of Internet-usingadults use the Web to research their options — regardless ofwhether or not they plan to buy online.

Targeted efforts“Our intention is to get very specific in marketing to certainniches,” she says of the agency’s foray into the Internet, which includes a blog, refreshed website, Facebook presenceand YouTube channel. “We have specific products to get tospecific buyers.”

She began targeting the trucking industry by posting short,informational videos on YouTube. Three additional phases withtactics aimed at particular audiences are scheduled for 2011.

Additionally, in the coming months, Ressler and several staffmembers will rent a production studio in State College, Pa., tocreate a series of high-quality videos — one for each of theagency’s product offerings. These will be added to the agencywebsite and posted on YouTube.

“An upgraded website is important,” shares Ressler. “If acompany has an outdated website, consumers think thecompany is outdated, too.”

Ressler’s mixed marketing

plan works because she

understands her agency,

its customers and its

potential customers and

because she has firm

objectives in mind.

B

G20662_18-28_July2011 6/17/11 2:29 PM Page 19

Despite these efforts, Resslerremains loyal to traditionaladvertising. A few billboards,continued (albeit scaled back)radio and newspaper advertisingand another television commercial round out her 2011 marketing plan.

“We haven’t discounted other typesof marketing,” she explains. “It’sthe mix of all types that seems tobe helping us. We’re getting a lotof positive feedback, people arerecognizing us, and we’re closingmore accounts.”

Words of wisdomRessler’s mixed marketing planworks because she understandsher agency, its customers and its

potential customers and becauseshe has firm objectives in mind.

“Each agency has to do what feelsright to them,” shares Ressler. “Notevery agency has the same goals,and their marketing should reflectwhat they want to accomplish.”

A strictly commercial-lines agency, for example, likely wouldnot find value in launching aFacebook account. And an agencylooking to grow its 20-somethingclientele likely would not putextensive resources into printnewspaper advertisements.

Ressler also cites the importanceof finding reasonably priced yeteffective experts to help put thepieces into place.

“It comes down to partnering withgood people,” she says, referring tothe advertising and multi-mediavendors she utilizes. “Goodcompanies helping us through thisprocess have been key. We’re nottrying to do it all ourselves.”

Learn more about the Teeter Groupby visiting the agency’s website:teetergroup.com. Learn moreabout selecting a graphic designfirm or advertising agency on page 23. _______________________________

Karen Robison is public relationsdirector for IA&B.

MARKETING

[ 20 ]

IF YOU HAVE THE TOOLS,WE HAVE THE INSURANCE.

Residential Contractors with up to 5 employeescan find great deals on liability insurance atBrokers Surplus Agency. We represent Utica First Insurance, one of the largest writers of small contracting firms in the Northeast, and we cangive you a free quote on all your coverage needs!Call or email us today!

Contact: Dennis Marsaglia, Ext. [email protected] Frisch, Ext. [email protected]

Brokers Surplus Agency, P.O. Box 2849,Warminster, PA 18974 � Call (215) 443-9900

G20662_18-28.qxp:July2011 6/21/11 3:55 PM Page 20

Primary Agent | July 2011 H.R.H E A D Q U A R T E R S

[ 21 ]

JEFFREY W GERHARTCEBS, MBA

Jeffrey W. Gerhart, CEBS, MBA,

provided this article on behalf of

Mosteller & Associates, IA&B’s

contracted human resources

consulting firm.

IA&B members have access to

HR Solution©, a compilation of

products and services to help

them establish or improve their

human resources program.

Included are base-level

consultation services and

discounted professional services

from Mosteller & Associates.

But I pay all of mystaff a salary, so whywould I have to payany of them overtime?

Over the past few months,I’ve talked with a few agencyowners about commissionpayments to inside producerswho sell insurance. Thisdiscussion has raised myconcern about whether thereis understanding betweenpaying someone a salary and the Fair Labor StandardsAct (FLSA) classifications of exempt and non-exemptemployees.

Most of us equate payingsomeone hourly as non-exempt and having to payovertime. Paying a fixed,recurring salary to anemployee is generallyconsidered a higher levelposition that does not carryan overtime requirement. Butthat is a misunderstanding ofand misstatement of fact.

In part, exempt and non-exempt classifications have todo with whether an employeeis entitled to overtimecompensation as definedunder FSLA. Overtime is to be

paid to non-exemptemployees when they exceed40 hours of work in a seven-consecutive-day workweek, ata rate of one and one-halftheir regular rate. In general,unless meeting specificearnings and/or exemptioncriteria for executive,administrative, professional oroutside sales tests, employeesare protected under the actand entitled to receiveovertime pay.

The non-exempt status(meaning not exempt fromcoverage under FSLA) forovertime payment is withoutregard to whether theemployee is paid hourly or on a salaried basis. Saiddifferently, you may pay anon-exempt employee asalary, but you are still arerequired to pay overtime as it occurs.

I recently attended a seminarwhere a federal Wage & HourDivision investigatoraddressed the problemstypically encountered whenexamining employer paypractices. Many of the knownviolations are industry basedand drive investigations.

Others are based onemployers’ misunderstandingof regulations and requiredpayments. The investigatorindicated when it comes topaying commissions, bonusesand other recurring lump-sumpayments to non-exemptemployees, many employersdon’t understand the requiredovertime payment, let alonehow to calculate it.

Of particular concern toagency owners is whether theinside producer is properlyclassified as exempt or non-exempt from overtimecompensation. The exemptstatus earned through thesales exemption test isprimarily for outside sales,which likely applies to most ofyour producers. Inside salespositions, however, havedifficulty satisfying theexemption requirements.

What should I do?First, determine that yourpositions are classifiedcorrectly as exempt or non-exempt from overtimepayments. You can access HR Solution for guidelines toassess your FLSA status, aswell as hyperlinks to U.S.

PART I: FLSA AND THE PROBLEM WITH PAYINGNON-EXEMPT EMPLOYEES A SALARY

G20662_18-28_July2011 6/17/11 2:29 PM Page 21

[ 22 ]

Department of Labor Wage & Hour FactSheets. (See editor’s note at the end of this article.)

Second, determine whether your non-exempt positions work more than 40 hoursin any week. That may mean you need tointroduce time records for employees whoin the past did not complete them. You will need a way to know when more than40 hours are worked in a week.

Third, if you have non-exempt employeeson salary, re-evaluate whether to continuethat pay practice. Remember, non-exemptemployees, whether salaried or hourly, still are due overtime pay when exceeding40 hours of work in a week.

Fourth, document the types of recurringpayments beyond base pay that are givento non-exempt employees. Develop amethod by which overtime is determinedand the payment is calculated correctly.Work with your payroll resource to insurethe system works properly.

Editor’s note: The next issue of PrimaryAgent will illustrate a practical method forcalculating overtime for a non-exemptinside producer.

In the meantime, visit IA&B’s HR Solution to access guidance on classifying employees under the FLSA. Visitwww.iabgroup.com/HR to access (orregister to access) the program. Thenchoose “administrative guide,” “reviewsections of the administrative guide” and “employee classifications.”

Access to HR Solution is included with IA&B membership but is limited to thoseindividuals designated as agencyadministrators within the IA&B database. To add an agency administrator, contactIA&B’s Member Service Center at 800-998-9644, option 0.

When it comes toUmbrella or EquipmentBreakdown CoverageWe have fast, competitive quotesfor you, with the service you deserve.• Designed for Condos, Co-ops, Townhouses,

Apartments, HOAs, PUDs, HabitationalAccounts, and Lessor Risk Only Exposures

• Limits from $1 Million to $50 MIllion• Coverage Includes Excess, G.L., D&O, & Auto• Minimum premiums as low as $350

For additional information or quotes call:

888.548.2465And ask for a New Business Underwriter or [email protected]

Visit our website atwww.umbrellaprogram.com

JGSService is our specialty; protecting you is our mission®

®

I N S U R A N C E

A subsidiary of

H.R. HEADQUARTERS

G20662_18-28.qxp:July2011 6/21/11 3:55 PM Page 22

MARKETING

[ 23 ]

Often, the choiceinvolves a trade-offbetween quality and price — or at

least between experience andprice. Some full-serviceadvertising agencies andgraphic design firms are gearedto work with deep-pocketcorporations and will bebeyond a small company’sbudget. Many, however,provide excellent service atmore reasonable rates.

The following proven steps canhelp you determine if an adagency or design firm canserve your needs while fittingwithin your budget.

1. Ask other small-business owners forrecommendations. If an adagency or graphics firm hasperformed well for others ata reasonable rate, it’s likelythe company will do thesame for you. When askingfor recommendations, see ifyou can look at what theagency did. Examinematerials such as ads,brochures, websites, direct-mail pieces, etc. Talk withthe business owner to seehow well the marketingmaterial performed for him,in terms of revenue or newcustomers generated. Askhow easy the agency was towork with. Ask aboutcharges. And see if therewere any specific individualsat the agency who did agreat job.

2. Before meeting withagencies, prepare bygathering all informationthey’ll need to makesuggestions. These include:your present marketingmaterials, your goals andtimelines, your vision of theimage you would like yourcompany to have, yourbudget, etc. This informationwill be necessary for anagency to make realisticsuggestions and priceprojections.

______________________________

A one-person shop maydo even better work foryou than a large agency.______________________________

3. Ask to see samples ofwork done for previous orexisting clients. The workshould resonate with you. Ifnot, you should move toyour next interview because

Tips for selectinga graphic designfirm or advertisingagency

The selection of an individualor firm to handle yourmarketing is one of the mostimportant decisions a smallcompany can make. Read onfor seven tips to save time (andpotential expense) whenchoosing a marketing partner.

O

G20662_18-28.qxp:July2011 6/21/11 3:56 PM Page 23

[ 24 ]

it’s often hard for an agency torevamp the style of work itdoes, just as it’s difficult for anartist to draw or paint in a styleother than what they’vedeveloped over the years. If youdon’t like the way the agency’sads look, or if their design styledoesn’t seem like it would fitwith the image you want, keepan open mind. But don’t expectthat they’ll be able to changejust to suit you.

4. Ask about fees. It’s often hardfor a creative person or agencyto give an exact amount for howmuch a brochure, logo, adcampaign or other types of workwill cost. But you’ll need toknow a ballpark figure todetermine if you can afford towork with them. When talkingabout fees, don’t assume that anagency will come in at the lowend of an estimate.

5. Visit the agency’s offices. You’ll be able to tell a lot about an agency by how theirspace feels. It is orderly or is it a mess? Does the staff seem dedicated? Do they have samples of their work on display?

Tip: At least once, walk throughthe offices near the end of theday. People’s true colors comeout when they’ve been hard at itfor eight hours or more.

6. Ask about the people whowill be doing the work onyour account. Meeting withthe sales manager of a large adagency doesn’t really give youmuch information about thepeople who will be creating onyour behalf. Agencies range in

size from independententrepreneurs to large, full-service agencies employinghundreds of writers, designersand account representatives. No

matter how large, however,individuals within the agenciesundertake creative decisionsand create the final product. Forthis reason, a one-person shopmay do even better work foryou than a large agency.

The proprietor of a one-man orone-woman agency, forexample, may formerly havebeen a creative director at alarger agency. He or she mayhave experience and ability farbeyond what you could expectto end up with at a largeragency. Because of your small-company budget, a large agencycould assign your work to arelatively inexperienced person.

7. Does the person who will bedoing your work understandand share the vision youhave of your marketinggoals? This is probably themost important factor in theselection process.

Final note: When starting workwith an agency, don’t get lockedinto a long-term contract. Startslowly and commit gradually. Ifyou’re looking for a new logo, forinstance, ask to see sketchesbefore paying a significant deposit.If you’re working with thecompany to create a brochure, ask to see layout samples and copy ideas before too much time (and expense) goes into the creation.

Source: National Federation of IndependentBusiness, www.nfib.com

The work should

resonate with you.

If not, you should move

to your next interview

because it’s often hard

for an agency to revamp

the style of work it does.

MARKETING

G20662_18-28.qxp:July2011 6/21/11 3:56 PM Page 24

[ 25 ]

Primary Agent | July 2011 TechnologyU P D A T E

DANIELLE JOHNSON

Danielle Johnson is the vice

president, director of information

technology at InsurBanc, which

IIABA and the W.R. Berkley

Corporation established to assist

independent agencies,

businesses and consumers with

their specific banking needs.

Danielle prepared this article for

ACT, and she can be reached at

This article reflects the views

of the author and should not

be construed as an official

statement by ACT.

What is cybercrime?Like traditional crime,cybercrime covers a broadscope of criminal activity andcan occur anytime andanyplace. What makes itdifferent is that the crime is committed using acomputer and the Internet.You may recognize some of its most common formssuch as identity theft,computer viruses and

phishing and, at a corporatelevel, computer hacking ofcustomer databases.

Most people are aware ofthese and protect themselvesand their PCs with anti-spyware and anti-virussoftware such as Norton orMcAfee programs. As anagency owner, you should bealert to the fact thatcybercrime is becoming more

and more sophisticated andnot only targets consumersand large corporations, butsmall to medium sizedbusinesses as well. Singleprograms against theseintrusions are not enough.

An alarming cybercrime nowaffecting small to mediumsized businesses is “corporateaccount takeover.” Thisinvolves cyber criminalspenetrating the computernetwork of a business andspreading malicious software,such as a “keylogger” whichrecords the words typed, Webbrowsing history, passwordsand other private information.This in turn allows themaccess to programs using yourlog-in credentials.

If they steal your passwordand breach your onlinebanking system, the cybercriminal can begin an onlinesession to initiate fundstransfers, by ACH or wiretransfer, to their accomplices.The accomplices withdraw themoney almost immediately.

COMBAT CYBERCRIME AND PROTECT YOURAGENCY WITH SIMPLE SECURITY STEPS

G20662_18-28_July2011 6/17/11 2:29 PM Page 25

Take the first steps to prevent fraud at youragency: Become aware of the latestcybercrimes and how they can access abusiness’s computer network. An agencyshould also employ the most up-to-dateonline security practices on a pro-active basis.

Agencies can also take the opportunity topresent these online security practices to theirclients, as many are also instituting Internet-based online programs at their businesses.

Online security practicesWhile no tools or automated software is 100percent effective, the best solutions to protectyour agency are to be well informed and usecommon sense. Using a multiple vendor,multi-layer approach to system design cansignificantly reduce your chances of being avictim of cybercrime. To assess the risksassociated with a cyber intrusion of youragency’s online systems and critical clientdata, ask yourself the following questions:

1. Does your agency have a hardware-based firewall at the network level?

2. Does the network firewall include anti-virus, anti-spyware and anti-spamservices along with content filtering and intrusion prevention, detection andreal-time reporting?

3. At the individual PC level, does eachcomputer have centrally updated andmonitored anti-virus, anti-spyware andanti-spam software loaded?

4. Are your computers set up toautomatically update your operatingsystem and applications for the latestavailable security and critical updates?

5. Do you consider your browser securitysetting to determine how much or howlittle information the browser can acceptfrom, or transmit to, a website?

TECHNOLOGY UPDATE

[ 26 ]

Common online fraud definitions

Malware refers to software programs designed to damage ordo other unwanted actions on a computer system. Commonexamples of malware include spyware, keyloggers and viruses.

Spyware is a type of malware installed on your computerwithout your knowledge. It collects small to large pieces ofpersonal information including Internet surfing habits. It canredirect Web browser activity and change computer settings.Spyware is typically hidden from the user and can be difficult todetect once installed without proper anti-spyware tools.

Keyloggers, as with spyware, are installed on your computerwithout your knowledge. It is the action of tracking (or logging)the keys struck on a keyboard, typically in a hidden manner so thatthe person using the keyboard is unaware that their actions arebeing monitored. Keystroke logging can record the words typed,Web browsing history, passwords and other private information.This is extremely dangerous in all aspects of computer usage.

Viruses are an ever changing and constant threat to all systems.Based on their digital makeup, they can deliver malicious contentto your data and systems in an effort to either collect data, destroydata or turn your systems into a machine that spreads the virus orother malware.

“Phishing” is the act of obtaining personal information orspreading malware using e-mails, calls, text messages or pop-upmessages from what appear to be friends or legitimate banks,retailers, government agencies or other organizations.

G20662_18-28.qxp:July2011 6/21/11 3:57 PM Page 26

6. Does your agency have a security policy in place thatincludes such policies as disaster recovery, use/storage ofpasswords, use of social media on work computers, etc.?

7. Does your agency back up critical files in case of an issuethat disables your systems?

8. Has your agency identified an individual to review securitypolicies and practices on an ongoing basis?

9. Are you aware of the laws governing the protection ofpersonal information in your state?

10. Do you have cybercrime insurance to protect your data and liability exposure in the event of an intrusion?

11. Does your agency have a training program to educateemployees on best practices to avoid becoming a victim?

12. Does your online banking system provide multiple layers of security tools to prevent intrusions into the system such as token-based authentication? Agency principalsshould consider the types of transactions they conduct within online banking and check with their bankinginstitution for available security enhancements.

These are just some of the basic steps an agency can implementto assess and protect itself from cybercrime. Your agency should have a network security assessment and reviewconducted by a certified information technology firm thatspecializes in network security. This evaluation will help you toidentify the next steps in securing your network and data fromunauthorized access and distribution.

If your agency becomes a victimIf you discover, or even suspect, your agency has fallen victim to corporate identity theft, you should proceed as follows:

w Immediately cease all online activity and contact your IT administrator.

w Remove the affected computer from the network and any other computer stations involved.

w Contact your financial institution to disable online access to the accounts and close affected accounts. You can then open new accounts and reset passwords.

w Consult your counsel and your state’s data breachnotification law and regulations to ascertain the process you need to follow.*

w Notify other business partners that may have been affected,such as your insurance carriers.

w File a report with the police department.

All of the security tips presented here are simply guidelines to aidagencies in not becoming a target for cyber criminals. However,none can be guaranteed 100 percent effective.

Editor’s note: For more on security and identity theft, access the member resources at www.iabgroup.com. Simply select “Technology” from the left-hand menu and then“Other resources.”

*Read more about data breach notification and other privacyrequirements by visiting IA&B’s state-specific resources:

Pennsylvania: www.iabgroup.com/pa/privacy

Maryland: www.iabgroup.com/md/privacy

Delaware: www.iabgroup.com/de/privacy

[ 27 ]

G20662_18-28_July2011 6/17/11 2:29 PM Page 27

Atlantic Specialty Lines Inc . . . . . . . . . . . . . . . .20

Brokers Surplus Agency . . . . . . . . . . . . . .IFC, 20

Commonwealth Ins Co . . . . . . . . . . . . . . . . . .IBC

Guard Insurance Group . . . . . . . . . . . . . . . . . .27

Harford Mutual Ins Co . . . . . . . . . . . . . . . . . . . .5

IA&B Agent PAC . . . . . . . . . . . . . . . . . . . . . . . . . .3

IA&B Partners Program . . . . . . . . . . . . . . . . . . .17

Interstate Insurance Mngmnt. . . . . . . . . . . . .OBC

MMG Insurance Company . . . . . . . . . . . . . . . . .1

PennPRIME . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

Preferred Property Program . . . . . . . . . . . . . . .22

TAPCO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

The Philadelphia Contributionship . . . . . . . . .22

Ad Index

ClassifiedA D V E R T I S E M E N T S

DISCOVER THE BENEFITSOF A PARTNERSHIP

WITH FAYETTEINSURANCE ASSOCIATES

Uniontown, PA 15401Website: www.fayins.comEmail: [email protected]

SOUTHEAST PA PRODUCERS & AGENCIES

Professional agency since 1926 locatedin Feasterville, Bucks County, Pa. Call for confidential information and a review of our services. Contact Ray Reinard at (215) 375-8600, Ext. 119.

If you would like to place a

Classified Advertisement, simply

fax your ad on company letterhead

to (717) 795-8347, and we will take

care of the rest.

[ 28 ]

When Garrett Dalton, a Connecticut correctionalofficer, claimed a job-site injury, no one batted an eye.He collected thousands of dollars in workers’compensation. But soon after, his Hannah Montanainfatuation got the best of him.

Say what?

Dalton donned a dress, wig and heels to balance an eggon a spoon and run a 40-yard dash, among othereyebrow-raising antics, as part of a radio station contestto score Hannah Montana tickets. His cross-dressingstint garnered local TV news coverage though, andsomeone who saw the report alerted authorities.

Besides losing the radio station’s contest, Dalton wascharged with workers’ compensation fraud.

Sources: 11 dumbest insurance fraud cases, InsuranceNetworking News; ‘Hannah Montana’ high heel run landsofficer in hot water, Associated Press

----------------------------------------------------------------———————-------The Last & Least column is dedicated to the industry’s oddities —from creative claims and kooky coverages, to (tasteful) jokes andstrange stories. Submit yours to [email protected], subject line: Last & Least. The editor will happily protect sources’ anonymityupon request.

Whenworkers’compfraud is a drag

G20662_18-28_July2011 6/17/11 2:29 PM Page 28

“No bond, no job. No job,no commission.”

We know times in the construction business are tough andthat even the best of clientsare having problems. That’swhy when your client needs abond Commonwealth Surety should bethe first call you make. With our “A” Rated Treasury Listed bonds wecan provide the bond you never thought you could get. Why shoparound, get buried with paperwork and hear excuses? If we can’t writethe bond nobody can! We specialize in bonding those “less than perfect” clients, without cash collateral or Letters of Credit, and we’ll getyou that “YES” that you want to hear in 24 hours or less. We’ve beenwriting bonds for small and midsized companies for over 20 years. No bond is too big or too small. And by the way, we’ll even write thatbond for your perfect clients. Call now and get results not excuses.TOLL FREE: 1-800-886-7760FAX TOLL FREE: 1-800-566-7761The place for the hard-to-place Bonds

“No bond, no job. No job,no commission.”

We know times in the construction business are tough andthat even the best of clientsare having problems. That’swhy when your client needs abond Commonwealth Surety should bethe first call you make. With our “A” Rated Treasury Listed bonds wecan provide the bond you never thought you could get. Why shoparound, get buried with paperwork and hear excuses? If we can’t writethe bond nobody can! We specialize in bonding those “less than perfect” clients, without cash collateral or Letters of Credit, and we’ll getyou that “YES” that you want to hear in 24 hours or less. We’ve beenwriting bonds for small and midsized companies for over 20 years. No bond is too big or too small. And by the way, we’ll even write thatbond for your perfect clients. Call now and get results not excuses.TOLL FREE: 1-800-886-7760FAX TOLL FREE: 1-800-566-7761

The place for the hard-to-place Bonds

G20662_C2,C3,C4_Layout 1 6/17/11 1:36 PM Page 2

That’sw With our “A” Rated Treasury Listed bonds wec Why shopa If we can’t writet We specialize in bonding those “less than p We’ve beenw N And by the way, we’ll even write thatb Call now and get results not excuses.

That’s

w

With our “A” Rated Treasury Listed bonds wec Why shopa If we can’t writet We specialize in bonding those “less than p

We’ve beenw N And by the way, we’ll even write thatb Call now and get results not excuses.

www.interstate-insurance.com

HHoot t PP

htthA

PPrrosp

thhtth

pects

s

ewweehtthsAoyyolllliilwwiosillign�oorrotirwrednuruOorpreporpeht

sttsaehrehtthaesttscepsspoosrropruorevveoccoyttyilliiilbaiiaatbouoyplehnacsretneilcruoyroffonoitceto

,pp,uuproffos

.egarrania.stn

sretnInneeddiisseeRR••

�oors'etatsaallaaiiccrreemmmmooCCl,laaiittnn

atiseht'nodoSepsorpgn�oor

n arevveocgn�d effeooRlairtsudnIdnn

ehtelihwekirts…eta!toherastce

dulcnisegasre

:e

sepytllA•ustimiL•aeyeviF•tsneveS•

decorpgn�oorfosnoilliM1$otp

ecneirepxetsapsratimilyrot

xaFrollaC

tohgnidulcniserud

olelbatpeccadnae

itacilpparuoyx

.cte,selgnihs,rr,att

deriuqeryrotsihss

!yadotnoi

d

&ainavvalysnnePnIuoBrehoneM7032-1•8787-552-418

xE•

ainigriVtssteW&50951APPA,nwotsnhoJ•dravel

0106-552-418:XAFA•7920-254-008

xaFrollaCdnudecneirepkciuQ•

itacilpparuoyx•gnitirwred

ecorPsmialCk

!yadotnoiuoranruTtsaF•

gnisse

dnu

dnalyraMnI•daoRnerraWWa111-1•4471-826-014

-etatsretni.www

03012DM,ellivsyekcoC•B1etiuS4196-826-014:XAFA•9777-957-008

moc.ecnarusni-

G20662_C2,C3,C4_Layout 1 6/17/11 1:36 PM Page 3