preview · 2019-04-24 · tax cuts and jobs act: how. will you be affected? preview. mark reynolds,...

TRANSCRIPT

Tax Cuts and Jobs Act:How Will You Be Affected?

Preview

Mark Reynolds, CFP® Mark Reynolds and Associates

123 Main Street, Suite 100San Diego, CA 92128Phone: 800-123-4567Fax: 800-123-4567www.markreynoldsandassociates.com

Preview

Contents

Federal Income Tax Fundamentals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 Three Terms That Describe Our Federal Income Tax System . . . . . . . . . . . . . 3 Who Is Paying All Our Taxes? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 Tax Laws Change Periodically . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 Federal Income Taxation at a Glance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Tax Cuts and Jobs Act . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Provisions Affecting Individuals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 Marginal Tax Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 2019 Tax Tables, by Filing Status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7–8 Comparison of 2017 and 2019 Marginal Tax Brackets . . . . . . . . . . . . . . . . . . 9 Rates for Long-Term Capital Gains and Qualified Dividends . . . . . . . . . . . . 10 Alternative Minimum Tax for Individuals . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 AMT Phaseout Thresholds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11 What Is the “Kiddie Tax”? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11 Standard Deduction and Personal Exemptions . . . . . . . . . . . . . . . . . . . . . . . . 12 Limits on Itemized Deductions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 Child Tax Credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Other Changes Worth Noting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15 No More “Undoing” of a Roth IRA Conversion . . . . . . . . . . . . . . . . . . . . . . 15 Enhancement of 529 Savings Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16 Health Insurance Mandate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17 Estate and Gift Tax Exclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17 Alimony . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17 Moving Expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Provisions Affecting Business Owners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18 Corporate Tax Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18 Pass-Through Business Income Deduction . . . . . . . . . . . . . . . . . . . . . . . . . . 18 Treatment of Foreign Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18 “Bonus” Depreciation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19 Internal Revenue Code (IRC) Section 179 Expensing . . . . . . . . . . . . . . . . . . 19

Tax Cuts and Jobs Act NGS-019-07-000020

This material was written and prepared by Broadridge Advisor Solutions.

Copyright by Broadridge Investor Communication Solutions, Inc. All rights reserved. No part of this publication may be copied or distributed, transmitted, transcribed, stored in a retrieval system, transferred in any form or by any means—electronic, mechanical, magnetic, manual, or otherwise—or disclosed to third parties without the express written permission of Broadridge Advisor Solutions, 15050 Avenue of Science, Suite 200, San Diego, CA 92128-3419, U.S.A.

The information contained in this workbook is not written or intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security.

Broadridge assumes no responsibility for statements made in this publication including, but not limited to, typographical errors or omissions, or statements regarding legal, tax, securities, and financial matters. Qualified legal, tax, securities, and financial advisors should always be consulted before acting on any information concerning these fields.

Preview

© 2019 Broadridge Investor Communication Solutions, Inc. 3Tax Cuts and Jobs Act V19N2

Three Terms That Describe Our Federal Income Tax SystemProgressive . The United States has a progressive tax system . Generally, the more

taxable income you have, the higher the tax rate that will apply to your next dollar

of income . For example, in 2019, a single filer is subject to a 10% tax rate on the

first $9,700 of taxable income, a 12% tax rate on taxable income above $9,700 up

to $39,475 — and the rate continues to step up until it reaches a top marginal rate of

37%, which applies to taxable income over $510,300 . (See tax tables on pages 7–8.)

Voluntary . The federal income tax system is a voluntary system — that

simply means we’re responsible for calculating our own taxes, reporting our taxes

appropriately to the government, and paying any taxes due .

Pay-as-you-go . Federal income taxes are generally paid throughout the year . If you

are an employee for someone else, federal income tax is withheld from your paycheck

automatically . If you’re self-employed or don’t pay enough federal income tax

withholding, you typically have to make quarterly estimated tax payments . If you don’t

prepay enough federal income tax, you may be subject to an underpayment penalty .

Who Is Paying All Our Taxes? In 2015, the top 50% of taxpayers (based on reported adjusted gross

income, or AGI), were responsible for paying just over 97% of total

federal income taxes .

It might surprise you to learn that the wealthiest 10% of filers paid

about 71% of federal income taxes, and the top 5% accounted for about

60% of the total . This table shows where your 2015 AGI would have

placed you among filers that year, as well as the average effective tax rate

paid (total tax paid divided by total AGI) .

Federal Income Tax Fundamentals

Top Filers Adjusted Gross Income Average (by percentile) Threshold Tax Rate

0.001% $59,380,503 23.93%

0.01% $11,930,649 25.69%

0.1% $2,220,264 27.44%

1% $480,930 27.10%

5% $195,778 23.68%

10% $138,031 21.37%

20% $93,212 18.81%

30% $68,632 17.37%

40% $51,571 16.42%

50% $39,275 15.71%

Source: IRS Statistics of Income Bulletin, Winter 2018 (2015 data, most recent available)

Percent of Total Federal Income Tax Paid

for the Year

Top 10% of filers

Bottom 90% of filers

29%

71%

Preview

Tax Laws Change PeriodicallyHere’s a quick breakdown of some of the major tax legislation that has passed over

the last 11 years or so .

Taxes Aren’t Constant

U.S. tax laws change with relative frequency, which adds a layer of uncertainty when making financial decisions.

Federal Income Tax Fundamentals

LegislationPresidential

Administration Highlights

Tax Cuts and Jobs Act Donald Trump • Reduced 5 of the 7 income tax brackets for individuals (effective through 2025)• Reduced corporate income tax rate to 21% (permanent change)

Protecting Americans from Tax Hikes (PATH) Act of 2015

Barack Obama • Renewed most tax extenders• Child tax credit and earned income tax credit permanently expanded

Tax Increase Prevention Act of 2014

Barack Obama • Creation of ABLE accounts• Addressed multiple expiring provisions

American Taxpayer Relief Act of 2012

Barack Obama • Most 2001 and 2003 tax cuts made permanent, and expiring provisions were extended• AMT relief

Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010

Barack Obama • Extended multiple expiring provisions• AMT adjustments• Estate tax changes• Temporary payroll tax reduction

Patient Protection and Affordable Care Act of 2010

Barack Obama • Health-care premium subsidies and credits• Net investment income tax• Additional Medicare payroll contribution tax

Small Business Jobs Act of 2010

Barack Obama • New business loan programs, tax breaks, and credit enhancements

American Recovery and Reinvestment Act of 2009

Barack Obama • AMT provisions• Extension of business tax incentives• Making Work Pay Credit and American Opportunity Tax Credit

Emergency Economic Stabilization Act of 2008

George W. Bush • Energy incentives• AMT provisions• Tax extenders

Economic Stimulus Act of 2008

George W. Bush • One-time tax rebates• Business tax incentives

4 © 2019 Broadridge Investor Communication Solutions, Inc.

Preview

Federal Income Tax Fundamentals

Federal Income Taxation at a GlanceThis is a simple illustration of how the federal income tax system works .

Not coincidentally, it reflects the order of calculations on IRS Form 1040 .

© 2019 Broadridge Investor Communication Solutions, Inc. 5

Gross income includes all your taxable income, such as wages and tips, dividends,

capital gains, interest income, and taxable pension and Social Security income .

You then subtract adjustments to income, such as deductible contributions to a

traditional IRA (with limitations), to compute your adjusted gross income .

You may subtract either the standard deduction or allowable itemized deductions

to arrive at your taxable income . Federal income tax is usually calculated from the

IRS tax table based on filing status and taxable income . Then any available credits,

such as the child tax credit, are subtracted to arrive at your income tax liability .

OR

Gross Income

Adjustments to Income

Standard Deduction

Adjusted Gross Income

Itemized Deductions

Taxable Income Calculate Tax

Available Credits

Income Tax Liability

Preview

What’s in a Name?

Although commonly referred to as the Tax Cuts and Jobs Act, the official title of the tax-reform package is more of a mouthful: “To provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018.”

Why? The tax-reform process was passed using a process known as reconciliation, and the Senate parliamentarian ruled that the version of the legislation with the short title violated a related Senate budget rule, because changing the title did not relate to fiscal or budget policy.

Tax Cuts and Jobs Act

On December 22, 2017, President Trump signed into law the Tax Cuts and

Jobs Act, a sweeping $1 .5 trillion tax-cut package that fundamentally changed

the individual and business tax landscape . While many of the provisions in the

legislation are permanent, others (including most of the tax cuts that apply to

individuals) are scheduled to expire after 2025 .

These were among the most significant changes made by the new legislation:

Changes in how taxes are calculated• New marginal tax brackets

• Revised tax thresholds for long-term capital gains and qualified dividends

• Alternative minimum tax (AMT)

• “Kiddie tax” rules

Major changes to deductions allowed• Higher standard deduction amounts

• No deduction for personal exemptions

• Limitations on itemized deductions

Other changes affecting individuals• Child tax credit rules

• Elimination of ability to “undo” a Roth IRA conversion

• Enhancement of 529 savings plans

• Repeal of Affordable Care Act individual responsibility payment

• Estate and gift tax rules

• Tax treatment of alimony

Changes affecting businesses• New flat 21% corporate tax rate

• Elimination of corporate alternative minimum tax

• Deduction for pass-through business income

• “Bonus” depreciation

• Internal Revenue Code Section 179 expensing

• Treatment of foreign income

6 © 2019 Broadridge Investor Communication Solutions, Inc.

Preview

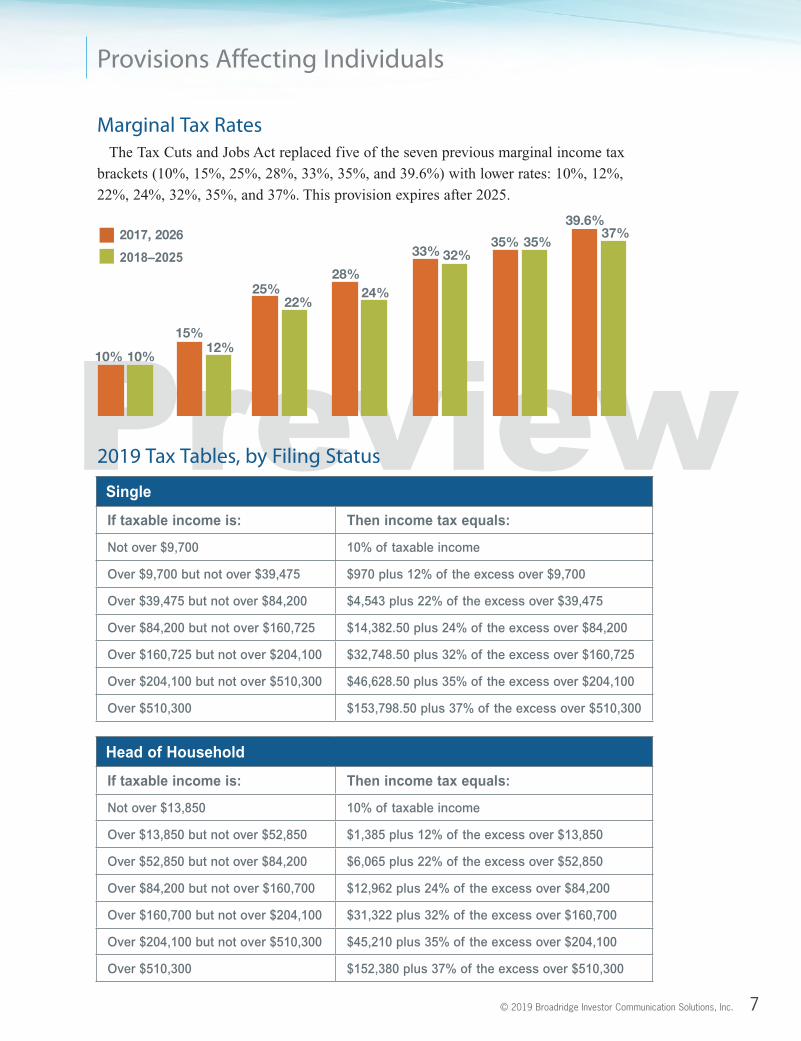

Marginal Tax RatesThe Tax Cuts and Jobs Act replaced five of the seven previous marginal income tax

brackets (10%, 15%, 25%, 28%, 33%, 35%, and 39 .6%) with lower rates: 10%, 12%,

22%, 24%, 32%, 35%, and 37% . This provision expires after 2025 .

Provisions Affecting Individuals

2019 Tax Tables, by Filing Status

10% 10%

15%12%

25%22%

28%24%

35% 35%33% 32%

39.6%37%2017, 2026

2018–2025

Single

If taxable income is: Then income tax equals:

Not over $9,700 10% of taxable income

Over $9,700 but not over $39,475 $970 plus 12% of the excess over $9,700

Over $39,475 but not over $84,200 $4,543 plus 22% of the excess over $39,475

Over $84,200 but not over $160,725 $14,382.50 plus 24% of the excess over $84,200

Over $160,725 but not over $204,100 $32,748.50 plus 32% of the excess over $160,725

Over $204,100 but not over $510,300 $46,628.50 plus 35% of the excess over $204,100

Over $510,300 $153,798.50 plus 37% of the excess over $510,300

Head of Household

If taxable income is: Then income tax equals:

Not over $13,850 10% of taxable income

Over $13,850 but not over $52,850 $1,385 plus 12% of the excess over $13,850

Over $52,850 but not over $84,200 $6,065 plus 22% of the excess over $52,850

Over $84,200 but not over $160,700 $12,962 plus 24% of the excess over $84,200

Over $160,700 but not over $204,100 $31,322 plus 32% of the excess over $160,700

Over $204,100 but not over $510,300 $45,210 plus 35% of the excess over $204,100

Over $510,300 $152,380 plus 37% of the excess over $510,300

© 2019 Broadridge Investor Communication Solutions, Inc. 7

Preview

Provisions Affecting Individuals

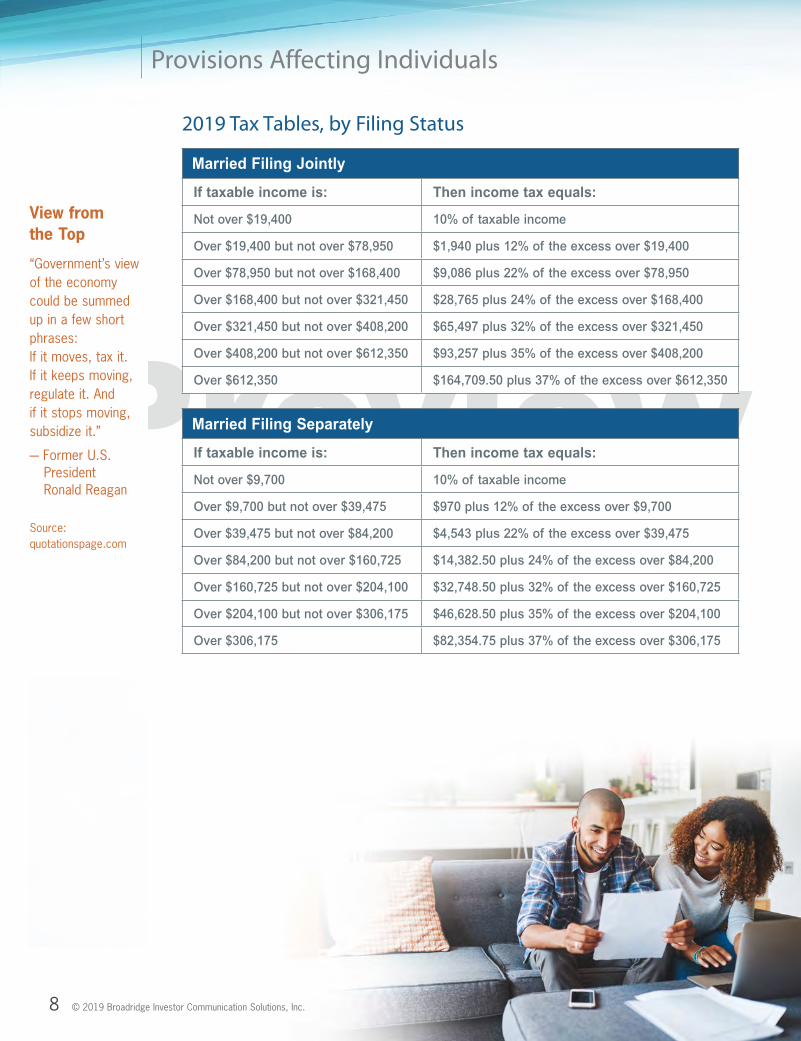

Married Filing Jointly

If taxable income is: Then income tax equals:

Not over $19,400 10% of taxable income

Over $19,400 but not over $78,950 $1,940 plus 12% of the excess over $19,400

Over $78,950 but not over $168,400 $9,086 plus 22% of the excess over $78,950

Over $168,400 but not over $321,450 $28,765 plus 24% of the excess over $168,400

Over $321,450 but not over $408,200 $65,497 plus 32% of the excess over $321,450

Over $408,200 but not over $612,350 $93,257 plus 35% of the excess over $408,200

Over $612,350 $164,709.50 plus 37% of the excess over $612,350

Married Filing Separately

If taxable income is: Then income tax equals:

Not over $9,700 10% of taxable income

Over $9,700 but not over $39,475 $970 plus 12% of the excess over $9,700

Over $39,475 but not over $84,200 $4,543 plus 22% of the excess over $39,475

Over $84,200 but not over $160,725 $14,382.50 plus 24% of the excess over $84,200

Over $160,725 but not over $204,100 $32,748.50 plus 32% of the excess over $160,725

Over $204,100 but not over $306,175 $46,628.50 plus 35% of the excess over $204,100

Over $306,175 $82,354.75 plus 37% of the excess over $306,175

2019 Tax Tables, by Filing Status

View from the Top

“Government’s view of the economy could be summed up in a few short phrases: If it moves, tax it. If it keeps moving, regulate it. And if it stops moving, subsidize it.”

– Former U.S. President Ronald Reagan

Source: quotationspage.com

8 © 2019 Broadridge Investor Communication Solutions, Inc.

Preview

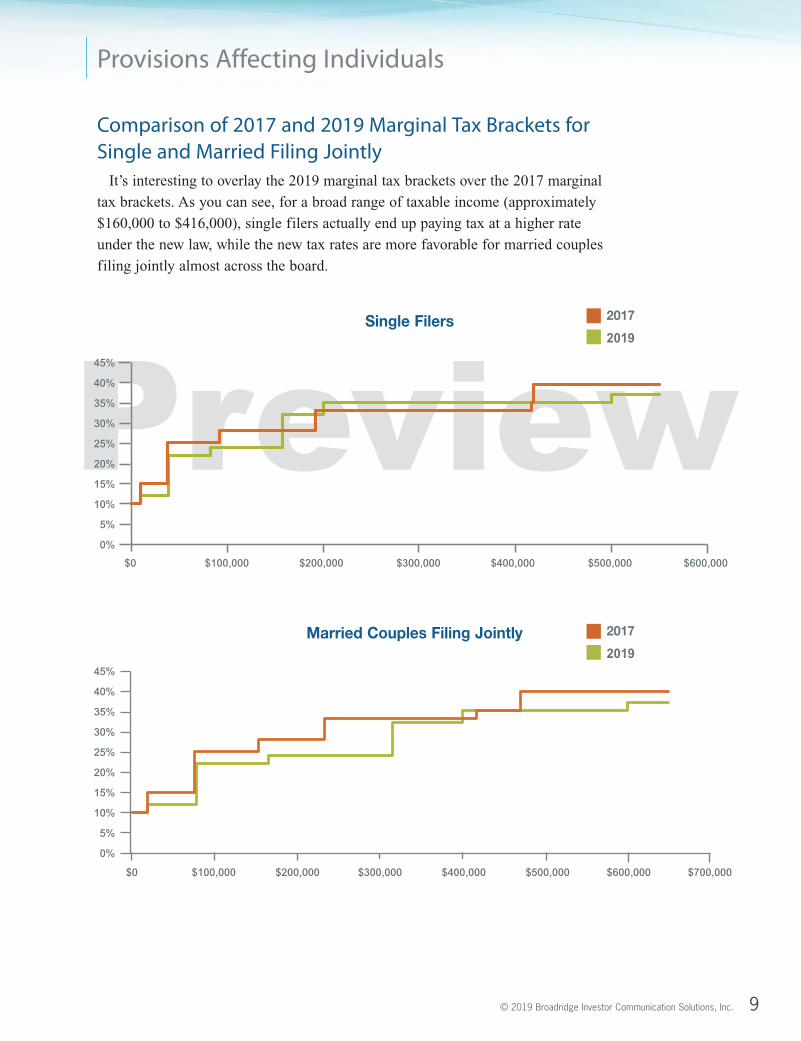

Comparison of 2017 and 2019 Marginal Tax Brackets for Single and Married Filing Jointly

It’s interesting to overlay the 2019 marginal tax brackets over the 2017 marginal

tax brackets . As you can see, for a broad range of taxable income (approximately

$160,000 to $416,000), single filers actually end up paying tax at a higher rate

under the new law, while the new tax rates are more favorable for married couples

filing jointly almost across the board .

Provisions Affecting Individuals

© 2019 Broadridge Investor Communication Solutions, Inc. 9

Married Couples Filing Jointly

Single Filers 2017

2019

2017

2019

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

$0 $100,000 $200,000 $300,000 $400,000 $500,000 $600,000

$0 $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 $700,000

Preview

10 © 2019 Broadridge Investor Communication Solutions, Inc.

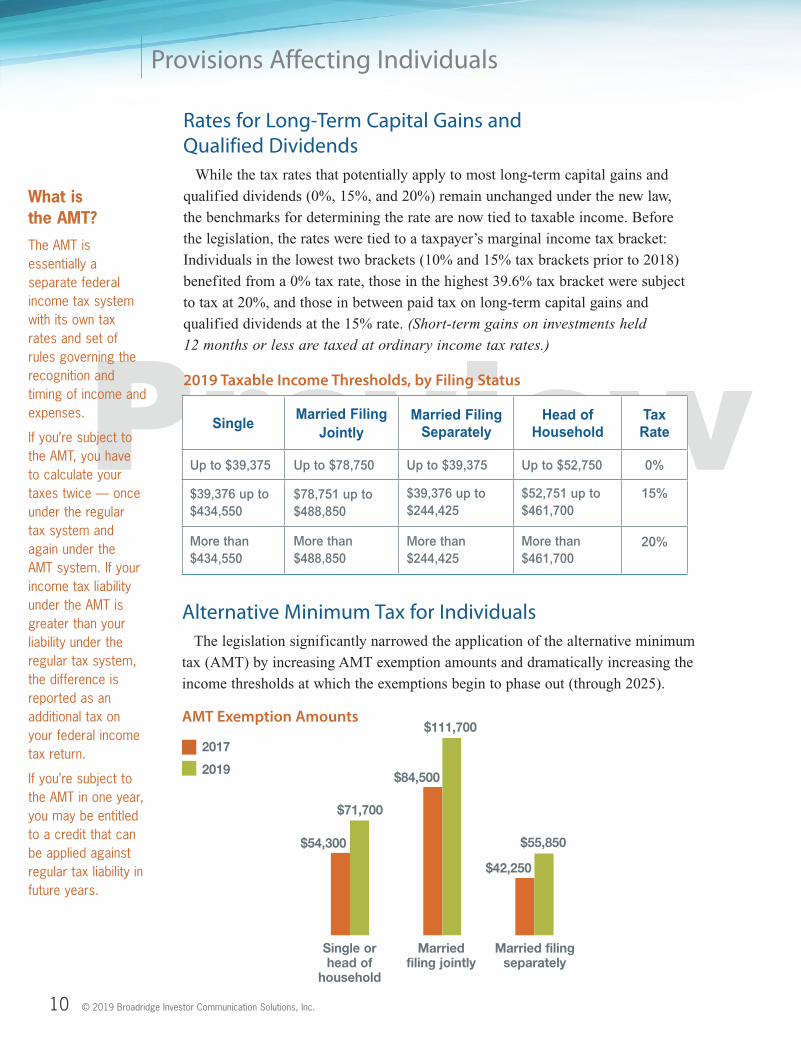

Rates for Long-Term Capital Gains and Qualified Dividends

While the tax rates that potentially apply to most long-term capital gains and

qualified dividends (0%, 15%, and 20%) remain unchanged under the new law,

the benchmarks for determining the rate are now tied to taxable income . Before

the legislation, the rates were tied to a taxpayer’s marginal income tax bracket:

Individuals in the lowest two brackets (10% and 15% tax brackets prior to 2018)

benefited from a 0% tax rate, those in the highest 39 .6% tax bracket were subject

to tax at 20%, and those in between paid tax on long-term capital gains and

qualified dividends at the 15% rate . (Short-term gains on investments held

12 months or less are taxed at ordinary income tax rates.)

2019 Taxable Income Thresholds, by Filing Status

Provisions Affecting Individuals

SingleMarried Filing

Jointly Married Filing

SeparatelyHead of

HouseholdTax Rate

Up to $39,375 Up to $78,750 Up to $39,375 Up to $52,750 0%

$39,376 up to $434,550

$78,751 up to $488,850

$39,376 up to $244,425

$52,751 up to $461,700

15%

More than $434,550

More than $488,850

More than $244,425

More than $461,700

20%

Alternative Minimum Tax for IndividualsThe legislation significantly narrowed the application of the alternative minimum

tax (AMT) by increasing AMT exemption amounts and dramatically increasing the

income thresholds at which the exemptions begin to phase out (through 2025) .

AMT Exemption Amounts

What is the AMT?

The AMT is essentially a separate federal income tax system with its own tax rates and set of rules governing the recognition and timing of income and expenses.

If you’re subject to the AMT, you have to calculate your taxes twice — once under the regular tax system and again under the AMT system. If your income tax liability under the AMT is greater than your liability under the regular tax system, the difference is reported as an additional tax on your federal income tax return.

If you’re subject to the AMT in one year, you may be entitled to a credit that can be applied against regular tax liability in future years.

$71,700

$54,300 $55,850

$42,250

$111,700

$84,500

Single or head of

household

Married filing jointly

Married filing separately

2017

2019

Preview

Provisions Affecting Individuals

Only about 200,000 tax filers were expected to owe the AMT for the 2018 tax year, instead of the 5.2 million who could have been subject to the AMT under the old rules.

Source: Tax Policy Center, 2018

$80,450

$510,300

Married filing jointly

$160,900

$1,020,600

Single$120,700

$510,300

2017

2019

For 2019, taxpayers pay a tax rate of 26% on alternative minimum taxable income (AMTI) up to $194,800 ($97,400 if married filing separately) . The rate increases to 28% on AMTI above this amount .

What Is the “Kiddie Tax”?Special “kiddie tax” rules apply when a child has unearned income (for example,

investment income) . Prior to 2018, children subject to the kiddie tax were generally

taxed at their parents’ tax rate on any unearned income over a certain amount . In

2019, as a result of the Tax Cuts and Jobs Act, children subject to the kiddie tax

will generally be taxed using trust and estate marginal income tax brackets on any

unearned income over $2,200 (the first $1,100 is tax-free and the next $1,100 is taxed

at the child’s rate) .

Kiddie tax rules apply to: (1) those who are under age 18, (2) 18-year-olds whose

earned income doesn’t exceed one-half of their support, and (3) those ages 19 to

23 who are full-time students and whose earned income doesn’t exceed one-half of

their support .

2019 Trust and Estate Marginal Income Tax Brackets

AMT Phaseout Thresholds

If taxable income is: Then income tax equals:

Up to $2,600 10% of taxable income

Over $2,600 but not over $9,300 $260 plus 24% of the excess over $2,600

Over $9,300 but not over $12,750 $1,868 plus 35% of the excess over $9,300

Over $12,750 $3,075.50 plus 37% of the excess over $12,750

© 2019 Broadridge Investor Communication Solutions, Inc. 11

Married filing separately

Preview

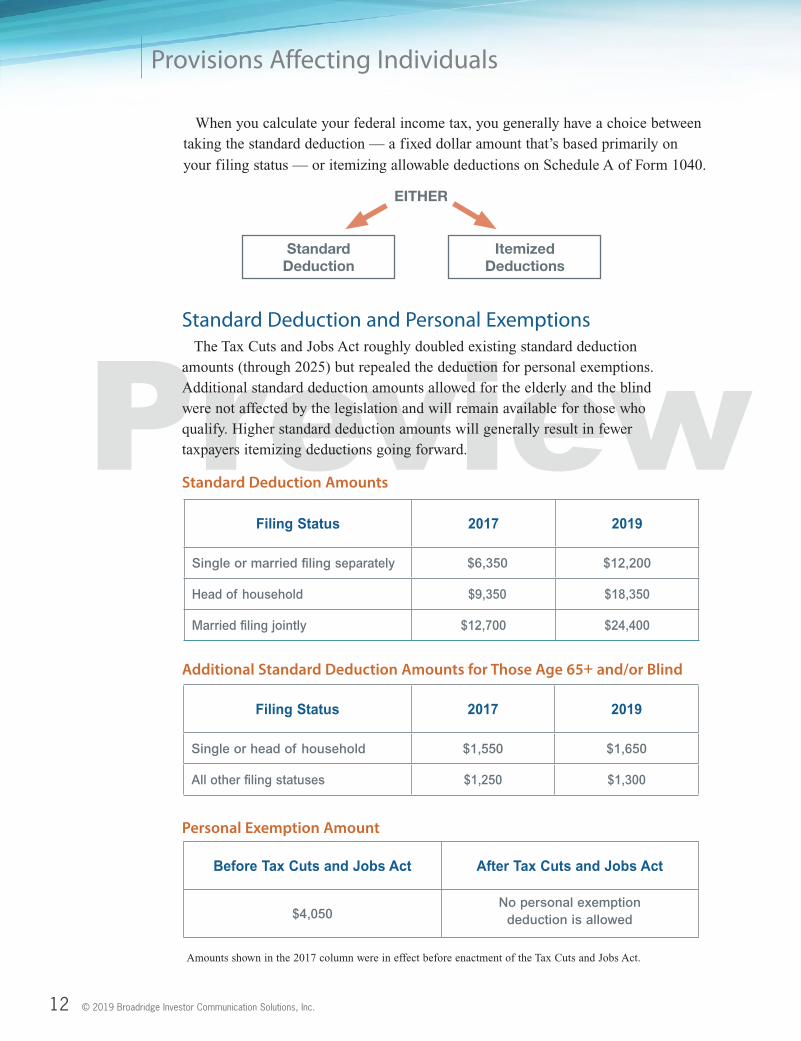

When you calculate your federal income tax, you generally have a choice between taking the standard deduction — a fixed dollar amount that’s based primarily on

your filing status — or itemizing allowable deductions on Schedule A of Form 1040 .

12 © 2019 Broadridge Investor Communication Solutions, Inc.

Provisions Affecting Individuals

Filing Status 2017 2019

Single or married filing separately $6,350 $12,200

Head of household $9,350 $18,350

Married filing jointly $12,700 $24,400

Filing Status 2017 2019

Single or head of household $1,550 $1,650

All other filing statuses $1,250 $1,300

Before Tax Cuts and Jobs Act After Tax Cuts and Jobs Act

$4,050No personal exemption

deduction is allowed

Amounts shown in the 2017 column were in effect before enactment of the Tax Cuts and Jobs Act .

Standard Deduction and Personal ExemptionsThe Tax Cuts and Jobs Act roughly doubled existing standard deduction

amounts (through 2025) but repealed the deduction for personal exemptions . Additional standard deduction amounts allowed for the elderly and the blind were not affected by the legislation and will remain available for those who qualify . Higher standard deduction amounts will generally result in fewer taxpayers itemizing deductions going forward .

Standard Deduction Amounts

Additional Standard Deduction Amounts for Those Age 65+ and/or Blind

Personal Exemption Amount

Standard Deduction

Itemized Deductions

EITHER

Preview

Provisions Affecting Individuals

Limits on Itemized DeductionsThe overall limit on itemized deductions that applied to higher-income taxpayers

(commonly known as the “Pease limitation”) has been repealed, and the following

changes are made to individual deductions . These provisions expire after 2025 .

Medical expenses . The adjusted gross income (AGI) threshold for deducting

unreimbursed medical expenses was retroactively reduced from 10% to 7 .5% for

tax years 2017 and 2018 only, but it returned to 10% for 2019 .

State and local taxes . Individuals are able to claim an itemized deduction of

up to $10,000 ($5,000 if married and filing a separate return) for state and local

property taxes and state and local income taxes (or sales taxes in lieu of income) .

Previously, there was no annual limit .

Home mortgage interest deduction . Individuals can deduct mortgage interest

on no more than $750,000 ($375,000 for married individuals filing separately) of

qualifying mortgage debt . For mortgage debt incurred on or before December 15,

2017, the prior $1 million limit will continue to apply .

Home equity interest deduction . Interest on home equity loans and home

equity lines of credit used to buy, build, or substantially improve your main home

or a second home remains deductible under the new rules . That’s because such debt

is considered acquisition debt and continues to be subject to the dollar limits on

qualified mortgage debt . However, interest on home equity loans and lines of credit

not used to buy, build, or substantially improve your main home or second home is

considered home equity debt and is no longer deductible under the new rules .

Charitable contributions . The top AGI limitation percentage that applies to

deducting certain cash gifts increases from 50% to 60% .

Casualty and theft losses . The deduction for personal casualty and theft

losses is eliminated, except for casualty losses suffered in a federally declared

disaster area .

Miscellaneous itemized deductions . Miscellaneous itemized deductions

that used to be subject to the 2% AGI threshold, including tax

preparation expenses and unreimbursed employee business

expenses, are no longer deductible .

© 2019 Broadridge Investor Communication Solutions, Inc. 13

In 1789, Founding Father Benjamin Franklin wrote what is considered to be his last great quote:

“But, in this world, nothing is certain except death and taxes.”

Source: Constitution Daily

Preview

Provisions Affecting Individuals

Stocks30%

14 © 2019 Broadridge Investor Communication Solutions, Inc.

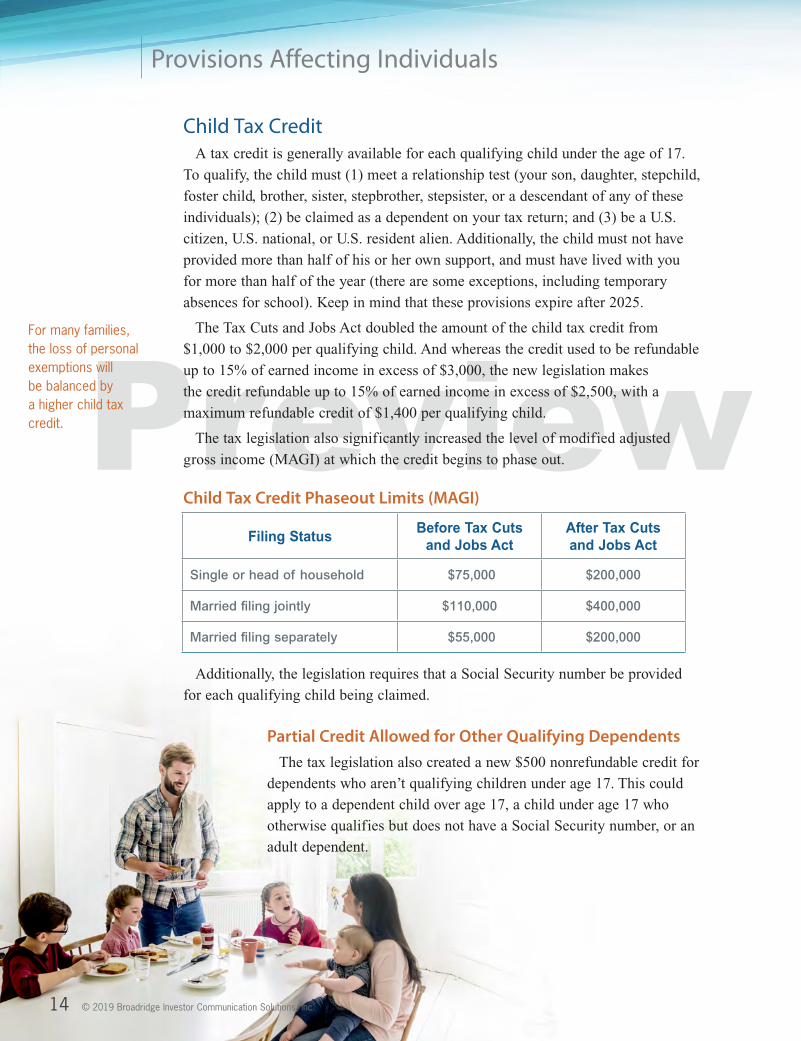

Child Tax CreditA tax credit is generally available for each qualifying child under the age of 17 .

To qualify, the child must (1) meet a relationship test (your son, daughter, stepchild,

foster child, brother, sister, stepbrother, stepsister, or a descendant of any of these

individuals); (2) be claimed as a dependent on your tax return; and (3) be a U .S .

citizen, U .S . national, or U .S . resident alien . Additionally, the child must not have

provided more than half of his or her own support, and must have lived with you

for more than half of the year (there are some exceptions, including temporary

absences for school) . Keep in mind that these provisions expire after 2025 .

The Tax Cuts and Jobs Act doubled the amount of the child tax credit from

$1,000 to $2,000 per qualifying child . And whereas the credit used to be refundable

up to 15% of earned income in excess of $3,000, the new legislation makes

the credit refundable up to 15% of earned income in excess of $2,500, with a

maximum refundable credit of $1,400 per qualifying child .

The tax legislation also significantly increased the level of modified adjusted

gross income (MAGI) at which the credit begins to phase out .

Child Tax Credit Phaseout Limits (MAGI)

Additionally, the legislation requires that a Social Security number be provided

for each qualifying child being claimed .

Partial Credit Allowed for Other Qualifying Dependents The tax legislation also created a new $500 nonrefundable credit for

dependents who aren’t qualifying children under age 17 . This could

apply to a dependent child over age 17, a child under age 17 who

otherwise qualifies but does not have a Social Security number, or an

adult dependent .

Filing StatusBefore Tax Cuts

and Jobs ActAfter Tax Cuts and Jobs Act

Single or head of household $75,000 $200,000

Married filing jointly $110,000 $400,000

Married filing separately $55,000 $200,000

For many families, the loss of personal exemptions will be balanced by a higher child tax credit.

Preview

© 2019 Broadridge Investor Communication Solutions, Inc. 15

Other Changes Worth Noting

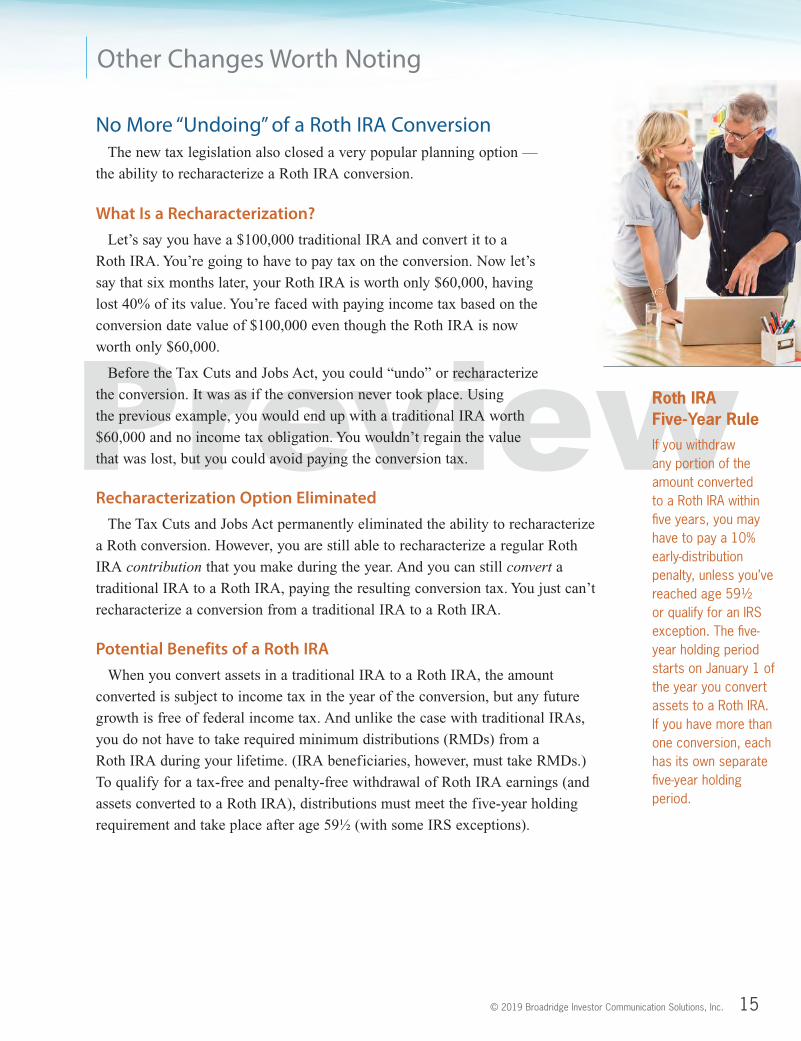

No More “Undoing” of a Roth IRA ConversionThe new tax legislation also closed a very popular planning option —

the ability to recharacterize a Roth IRA conversion .

What Is a Recharacterization? Let’s say you have a $100,000 traditional IRA and convert it to a

Roth IRA . You’re going to have to pay tax on the conversion . Now let’s

say that six months later, your Roth IRA is worth only $60,000, having

lost 40% of its value . You’re faced with paying income tax based on the

conversion date value of $100,000 even though the Roth IRA is now

worth only $60,000 .

Before the Tax Cuts and Jobs Act, you could “undo” or recharacterize

the conversion . It was as if the conversion never took place . Using

the previous example, you would end up with a traditional IRA worth

$60,000 and no income tax obligation . You wouldn’t regain the value

that was lost, but you could avoid paying the conversion tax .

Recharacterization Option Eliminated The Tax Cuts and Jobs Act permanently eliminated the ability to recharacterize

a Roth conversion . However, you are still able to recharacterize a regular Roth

IRA contribution that you make during the year . And you can still convert a

traditional IRA to a Roth IRA, paying the resulting conversion tax . You just can’t

recharacterize a conversion from a traditional IRA to a Roth IRA .

Potential Benefits of a Roth IRAWhen you convert assets in a traditional IRA to a Roth IRA, the amount

converted is subject to income tax in the year of the conversion, but any future

growth is free of federal income tax . And unlike the case with traditional IRAs,

you do not have to take required minimum distributions (RMDs) from a

Roth IRA during your lifetime . (IRA beneficiaries, however, must take RMDs .)

To qualify for a tax-free and penalty-free withdrawal of Roth IRA earnings (and

assets converted to a Roth IRA), distributions must meet the five-year holding

requirement and take place after age 59½ (with some IRS exceptions) .

Roth IRA Five-Year RuleIf you withdraw any portion of the amount converted to a Roth IRA within five years, you may have to pay a 10% early-distribution penalty, unless you’ve reached age 59½ or qualify for an IRS exception. The five-year holding period starts on January 1 of the year you convert assets to a Roth IRA. If you have more than one conversion, each has its own separate five-year holding period.

Preview

16 © 2019 Broadridge Investor Communication Solutions, Inc.

Enhancement of 529 Savings PlansThe Tax Cuts and Jobs Act changed some of the rules that govern 529 savings

plans — tax-advantaged state- or college-sponsored savings vehicles that were origi-

nally intended to help pay for college . Withdrawals from 529 plans are free of federal

income tax when used to pay qualified higher-education expenses, including tuition,

fees, and room and board . Withdrawals not used for qualified education expenses are

subject to federal and state income taxes and a 10% federal income tax penalty .

Qualified K-12 Expenses The new legislation expanded the definition of a 529 plan “qualified education

expense” to include K-12 tuition expenses . As of 2018, annual withdrawals of

up to $10,000 per student can be made from a 529 savings plan account to pay

tuition expenses at an elementary or secondary public, private, or religious school

(excluding home schooling) . Such withdrawals are now tax-free at the federal level,

but state tax rules may differ .

Transfers to ABLE Accounts The tax legislation also allows 529 account owners to roll over (transfer) funds

from a 529 plan to an ABLE plan without federal tax consequences . This provision

will expire at the end of 2025 unless a future Congress extends the law .

An ABLE plan is a tax-advantaged account that can be used to save for disability-

related expenses for individuals who become blind or disabled before age 26 . ABLE

plans allow funds to accumulate tax deferred, like 529 plans, and withdrawals are

tax-free when used to pay the beneficiary’s qualified disability expenses, which

may include (but are not limited to) housing, transportation, health care and related

services, personal assistance, and employment training and support .

ABLE accounts have annual and lifetime contribution limits . Contributions from

all donors combined during the year cannot exceed the annual gift tax exclusion

($15,000 in 2019) . Each state sets its own lifetime limit, which is also the state’s

maximum for its 529 savings plan contributions .

Investors should consider the investment objectives, risks, charges, and expenses associated with 529 plans and ABLE plans carefully before investing. Specific information is available in each plan’s official statement. Participating in a 529 plan or ABLE plan may involve investment risk, including possible loss of principal. There is no guarantee that any investment strategy will be successful, or that plan investments will perform well enough to cover college or disability-related costs as anticipated. As with other investments, there are generally fees and expenses associated with participation in a 529 savings plan. Before investing, consider whether your state offers residents favorable state tax benefits for 529 plan or ABLE plan participation, and whether those benefits are contingent on joining the in-state plan. Other state benefits for 529 plans may include financial aid, scholarship funds, and protection from creditors.

Other Changes Worth Noting

For a list of 529 plans offered, by state, and a comparison tool, visit collegesavings.org.

For a list of ABLE plans offered, by state, and a comparison tool, visit ablenrc.org.

Preview

Other Changes Worth Noting

© 2019 Broadridge Investor Communication Solutions, Inc. 17

Health Insurance Mandate The Affordable Care Act individual responsibility payment — the penalty for

failing to have adequate health insurance coverage — has been permanently repealed

starting in 2019 . The federal individual mandate was put in place to help ensure

that younger, healthier people joined the insurance pool, which helped stabilize the

individual insurance marketplace and kept premium costs manageable .

Estate and Gift Tax ExclusionThe federal estate and gift tax lifetime exclusion amount was doubled for tax

years 2018 through 2025 (indexed annually for inflation), after which it returns to

2017 levels . The individual exclusion amount increased from $5 .49 million in 2017

to $11 .18 million in 2018 . In 2019, it rose to $11 .4 million, which enables some

married couples to exempt up to $22 .8 million . There was no change to the 40%

federal estate tax rate that applies to taxable amounts over the exclusion amount .

AlimonyFor divorce or separation agreements implemented after December 31, 2018 (or

modified after that date to specifically apply this provision), alimony and separate

maintenance payments are not deductible by the paying spouse and are not included

in the income of the recipient . This is a permanent change .

Moving ExpensesPrior to enactment of the tax law, a taxpayer could claim a deduction for moving

expenses incurred when starting a new job if the location was at least 50 miles

farther from the taxpayer’s residence than the former place of work . Through

2025, the deduction for a job-related move has been suspended, except for

members of the Armed Services on active duty .

Annual Gift Tax Exclusion

Due to inflation, the annual exclusion for gifts increased to $15,000 (up from $14,000 in 2017). This was the first increase in the exclusion amount in five years.

The annual gift tax exclusion enables you to transfer up to $15,000 per person, per year, to any number of individuals free of federal gift tax.

Preview

18 © 2019 Broadridge Investor Communication Solutions, Inc.

Corporate Tax RatesInstead of the previous graduated corporate tax structure with four rate brackets

(15%, 25%, 34%, and 35%), the Tax Cuts and Jobs Act permanently established

a single flat corporate rate of 21%, effective as of 2018 . The new legislation also

permanently repealed the corporate alternative minimum tax (AMT) .

Pass-Through Business Income Deduction

Individuals who receive business income from pass-through entities (e .g ., sole

proprietors, partners) generally report that business income on their individual

income tax returns, paying tax at individual rates .

For tax years 2018 through 2025, a new deduction is available equal to

20% of qualified business income from partnerships, S corporations, and sole

proprietorships .

For those with taxable incomes exceeding certain thresholds, the deduction may

be limited or phased out altogether, depending on two broad factors:

• The deduction is generally limited to the greater of 50% of W-2 wages reported by the business, or 25% of W-2 wages plus 2.5% of the value of qualifying depreciable property held and used by the business to produce income.

• The deduction is not allowed for certain businesses that involve the performance of services in fields including health, law, accounting, actuarial science, performing arts, consulting, athletics, and financial services.

For those with taxable incomes in 2019 not exceeding $160,700 ($321,400 if

married filing jointly), neither of the two factors above will apply (in other words,

the full deduction amount can be claimed) . Those with taxable incomes between

$160,700 and $210,700 (or between $321,400 and $421,400 if married filing jointly)

may be able to claim a partial deduction .

Provisions Affecting Business Owners

Treatment of Foreign IncomeThe legislation fundamentally changed the way multinational companies are taxed,

making a shift from worldwide taxation of income to a more territorial approach .

Under the new rules, qualifying dividends from foreign subsidiaries to domestic

C corporations are effectively exempt from U .S . tax .

The law also forces many corporations to pay U .S . tax on prior-year foreign earnings

that have accumulated outside the United States in foreign subsidiaries . After the one-

time “deemed repatriation” payment is made, foreign earnings can be brought back to

the United States with no additional tax liability .

Congress estimated that by reducing the corporate tax rate to 21%, the IRS will collect $1.35 trillion less from companies through 2027.

Ending the corporate AMT is likely to save companies $40 billion over the next decade.

Source: The Wall Street Journal, February 11, 2018

Preview

Provisions Affecting Business Owners

“Bonus” DepreciationThe cost of tangible property used in a trade or business, or held for the production

of income, generally must be recovered over time through annual depreciation

deductions . Even before the Tax Cuts and Jobs Act, special rules allowed an up-front

additional “bonus” amount to be deducted for most qualified property acquired and

placed in service before 2020 . For property placed in service in 2017, the additional

first-year depreciation amount was 50% of the adjusted basis of the property (40%

for property placed in service in 2018, 30% if placed in service in 2019) .

The Tax Cuts and Jobs Act extended and expanded first-year additional (“bonus”)

depreciation rules . Bonus depreciation is extended to cover qualified property

placed in service before January 1, 2027 . For qualified property that’s both acquired

and placed in service after September 27, 2017, 100% of the adjusted basis of the

property can be deducted in the year the property is first placed in service . The

first-year 100% bonus depreciation amount is reduced by 20% each year starting

in 2023 . The first-year bonus depreciation amount for most qualified property falls

to 80% in 2023, 60% in 2024, 40% in 2025, and 20% in 2026, until it is eliminated

altogether beginning in 2027 .

For qualified property acquired before September 28, 2017, prior bonus

depreciation limits apply . If placed in service in 2017, a 50% limit applies; the limit

drops to 40% if the property was placed in service in 2018, and to 30% if placed in

service in 2019 .

The timelines and percentages are slightly different for certain aircraft and property with longer production periods.

Internal Revenue Code (IRC) Section 179 Expensing Under IRC Section 179, small businesses may elect to expense the cost

of qualified property, rather than recover such costs through depreciation

deductions . The Tax Cuts and Jobs Act increased the maximum amount that

can be expensed in 2019 to $1,020,000, and the threshold at which

the maximum deduction begins to phase out to $2,550,000 . Both the

$1,020,000 and $2,550,000 amounts are indexed annually for inflation .

The new law also expands the range of property eligible for expensing .

The new tax law is complex and includes many other changes. It would be wise to consult a tax professional before taking any specific action regarding your taxes.

© Broadridge Investor Communication Solutions, Inc. 19

Your consultation is scheduled for:

_________________________________Date Time

What to BringPlease bring the following documents to your consultation:

1.

2.

3.

4.

5.

Preview