presented by : mohsen ben hassine 2011 1. 1. definitions and basic properties 2. dependence 3....

TRANSCRIPT

INTRODUCTIONTO COPULAS

Presented by : Mohsen Ben Hassine

20111

Outline

1. Definitions and Basic Properties2. Dependence3. Important copulas4. Methods of Constructing Copulas5. Choice of Models

2

1. Definitions and Basic Properties

• The Word Copula is a Latin noun that means ''A link, tie, bond'‘• Appeared for the first time (Sklar 1959)• Non-linear dependence• Be able to measure dependence for heavy tail distributions

3

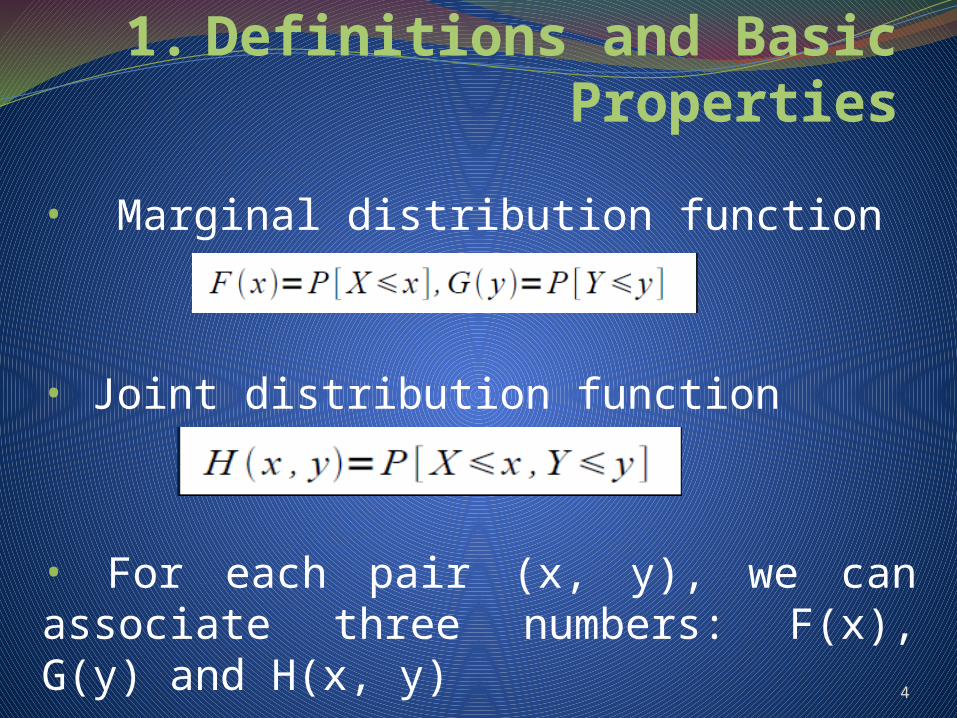

1. Definitions and Basic Properties

• Marginal distribution function

• Joint distribution function

• For each pair (x, y), we can associate three numbers: F(x), G(y) and H(x, y)

4

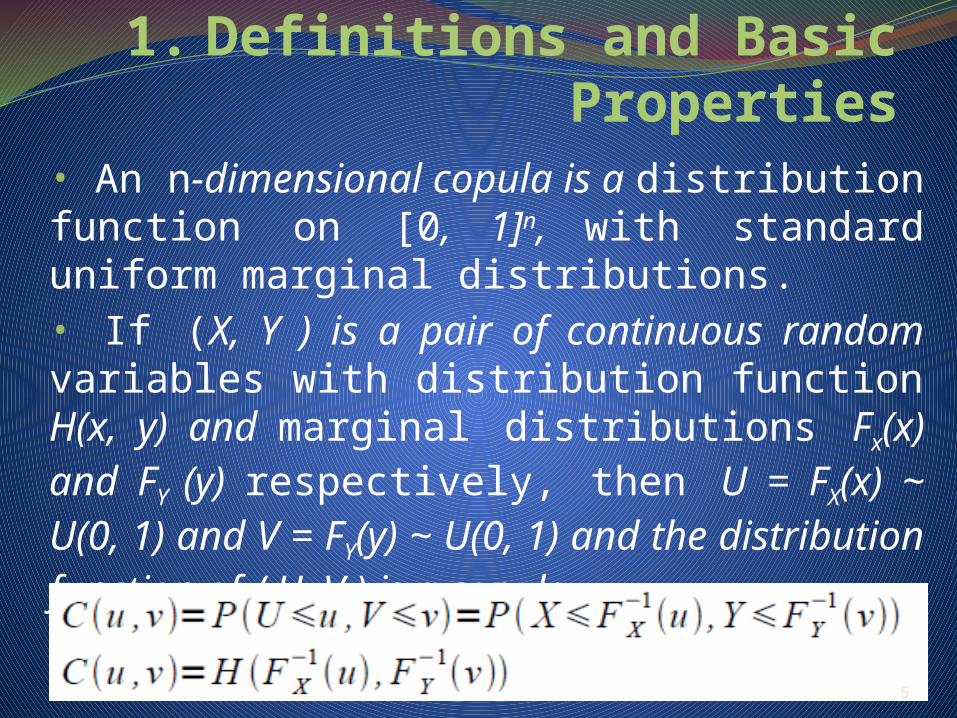

1. Definitions and Basic Properties

• An n-dimensional copula is a distribution function on [0, 1]n, with standard uniform marginal distributions.• If (X, Y ) is a pair of continuous random variables with distribution function H(x, y) and marginal distributions Fx(x) and FY (y) respectively, then U = FX(x) ~ U(0, 1) and V = FY(y) ~ U(0, 1) and the distribution function of (U, V ) is a copula.

5

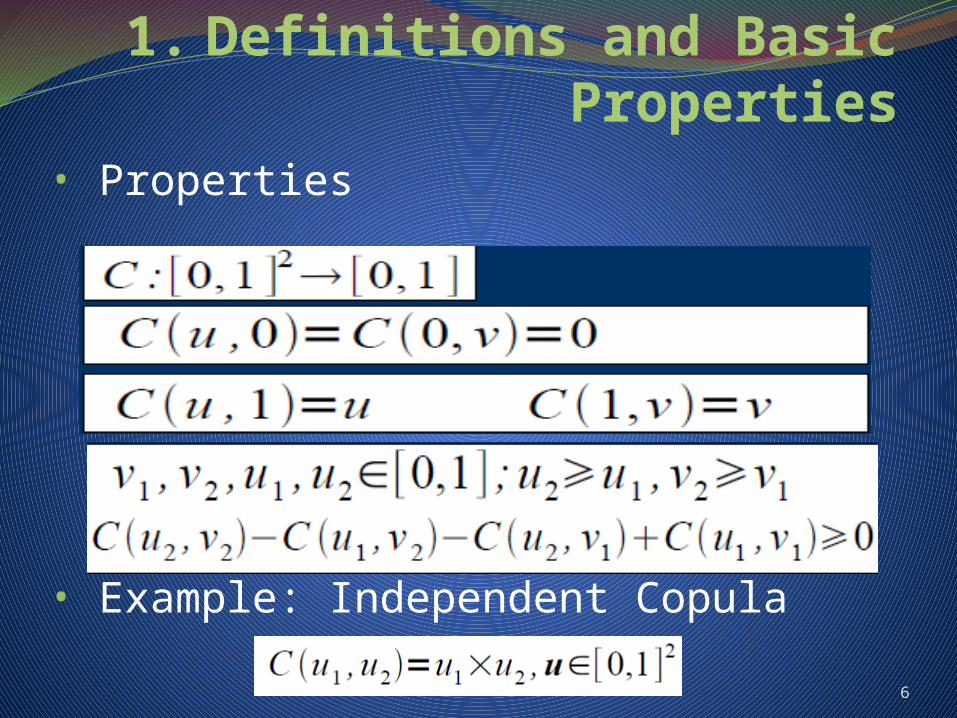

1. Definitions and Basic Properties

• Properties

• Example: Independent Copula

6

1. Definitions and Basic Properties

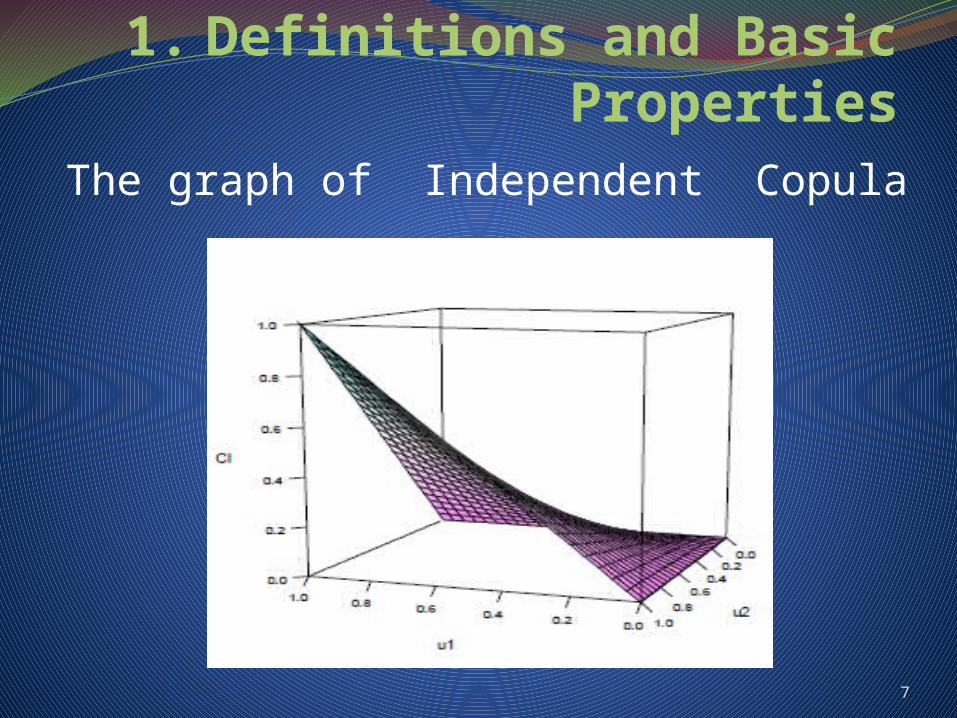

The graph of Independent Copula

7

1. Definitions and Basic Properties

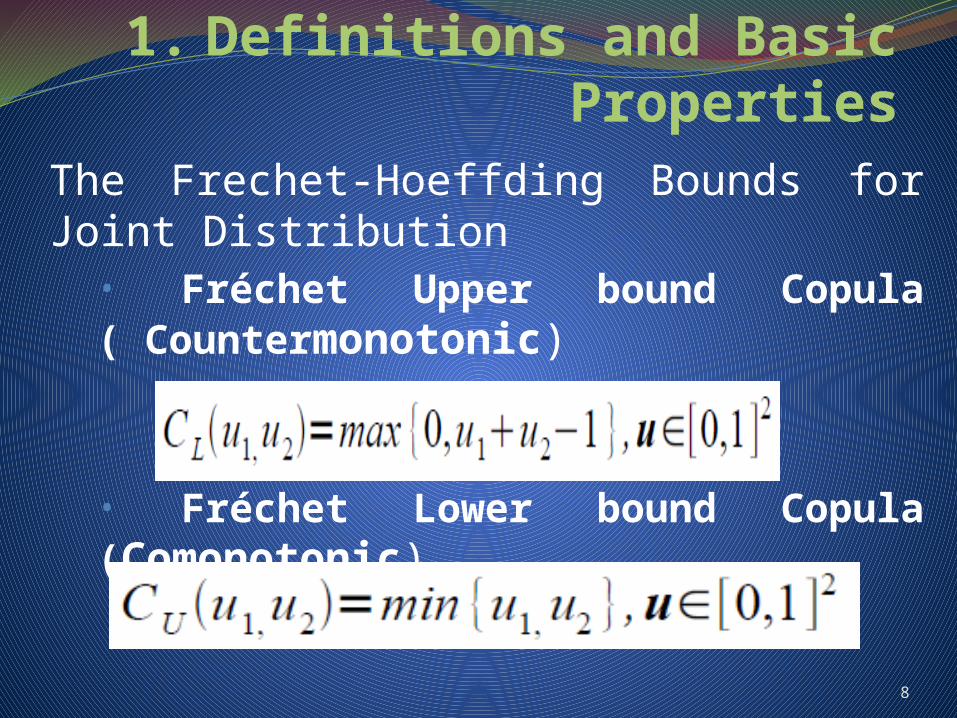

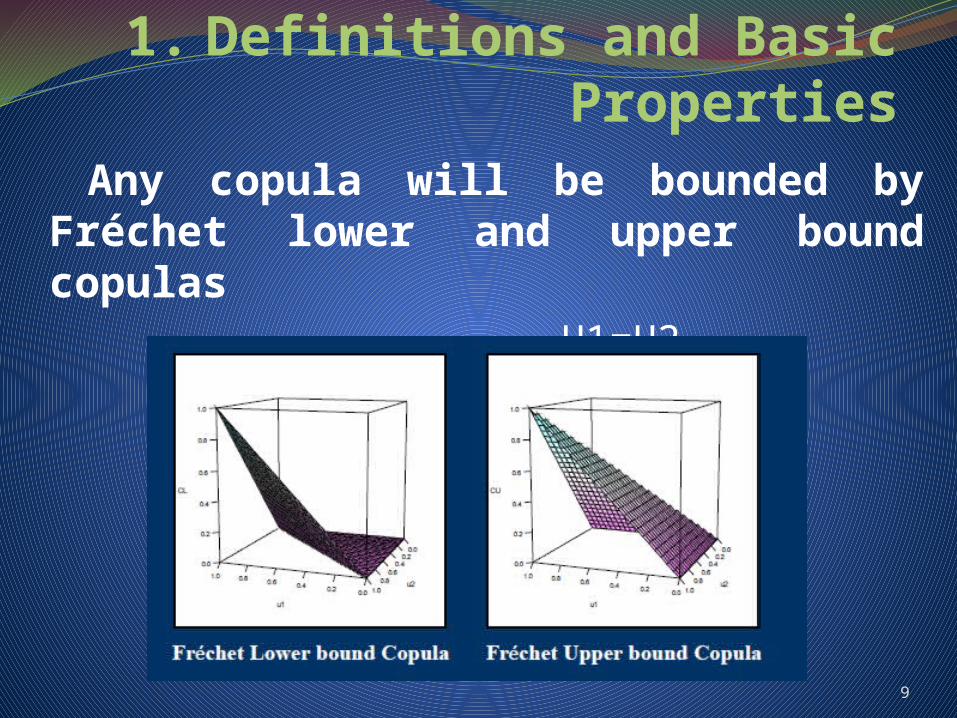

The Frechet-Hoeffding Bounds for Joint Distribution• Fréchet Upper bound Copula ( Countermonotonic)

• Fréchet Lower bound Copula (Comonotonic)

8

1. Definitions and Basic Properties

Any copula will be bounded by Fréchet lower and upper bound copulas U1=U2 U2=1-U1

9

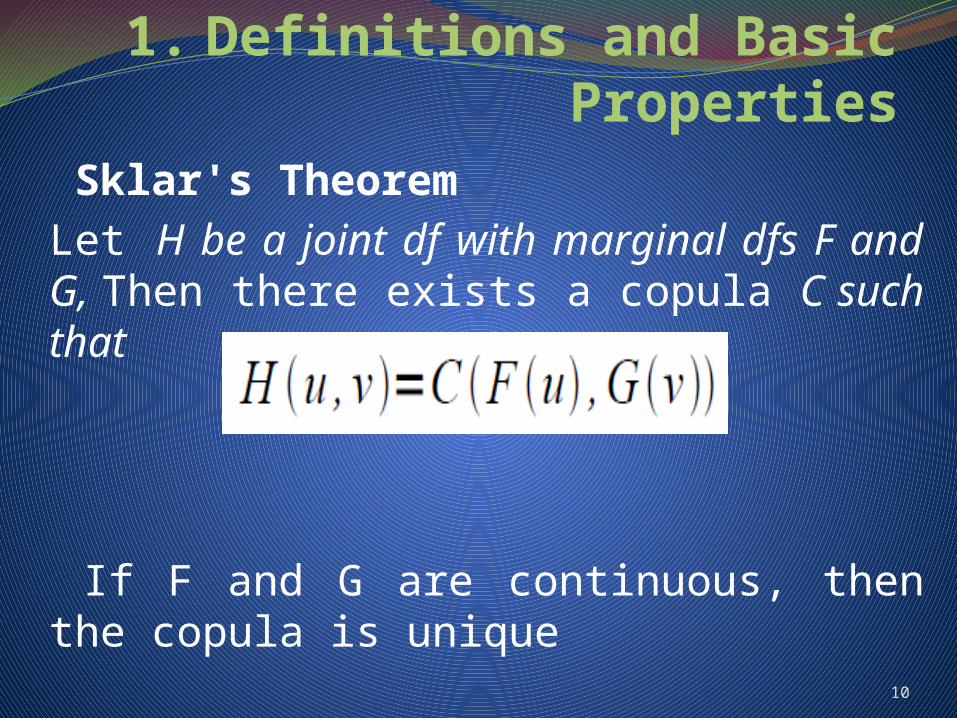

1. Definitions and Basic Properties

Sklar's TheoremLet H be a joint df with marginal dfs F and G, Then there exists a copula C such that

If F and G are continuous, then the copula is unique

10

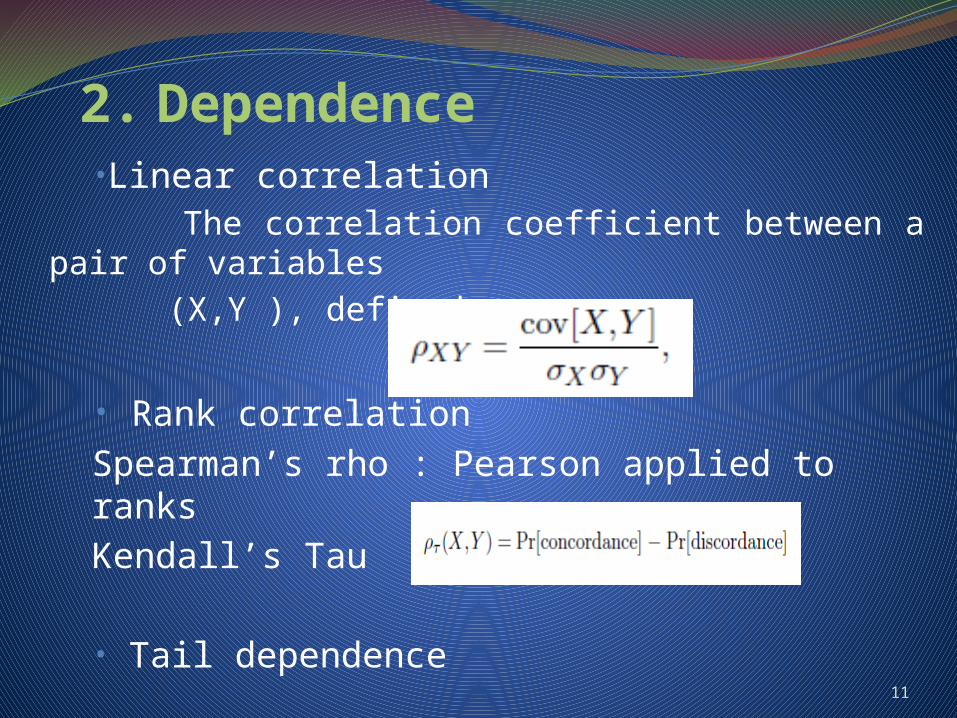

2. Dependence•Linear correlation

The correlation coefficient between a pair of variables (X,Y ), defined as

• Rank correlation Spearman’s rho : Pearson applied to ranksKendall’s Tau

• Tail dependence11

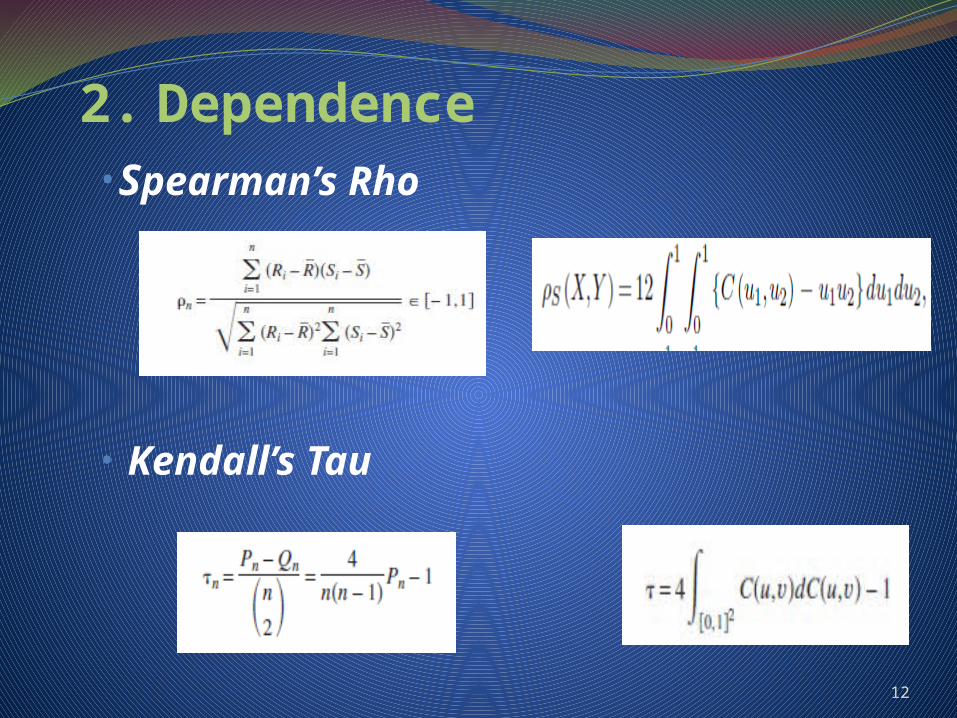

2. Dependence•Spearman’s Rho

• Kendall’s Tau

12

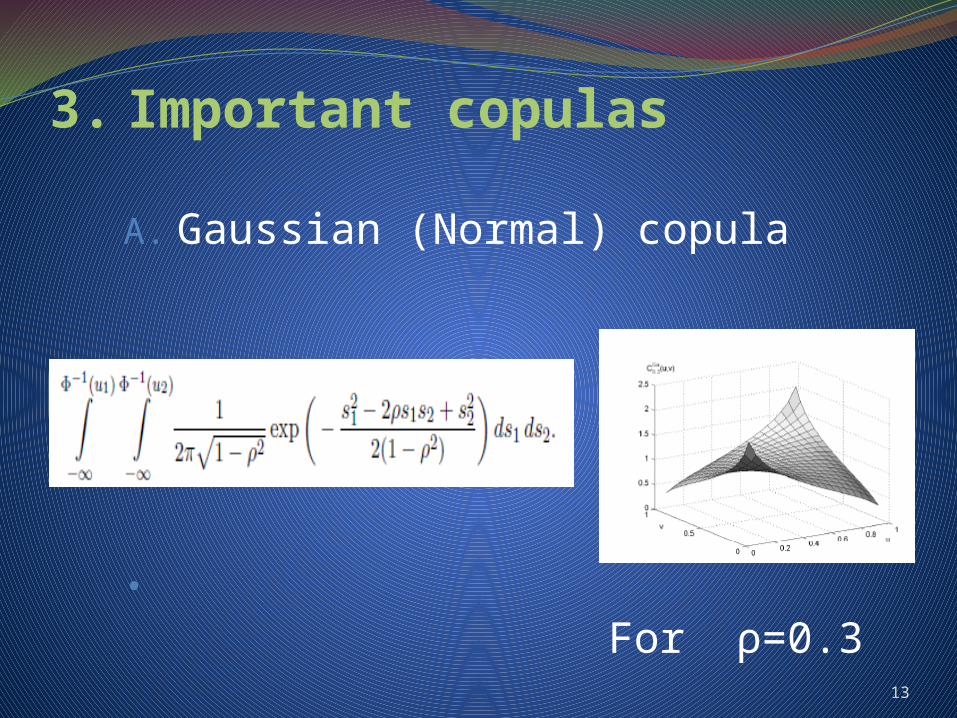

3. Important copulas

A. Gaussian (Normal) copula

• For ρ=0.3

13

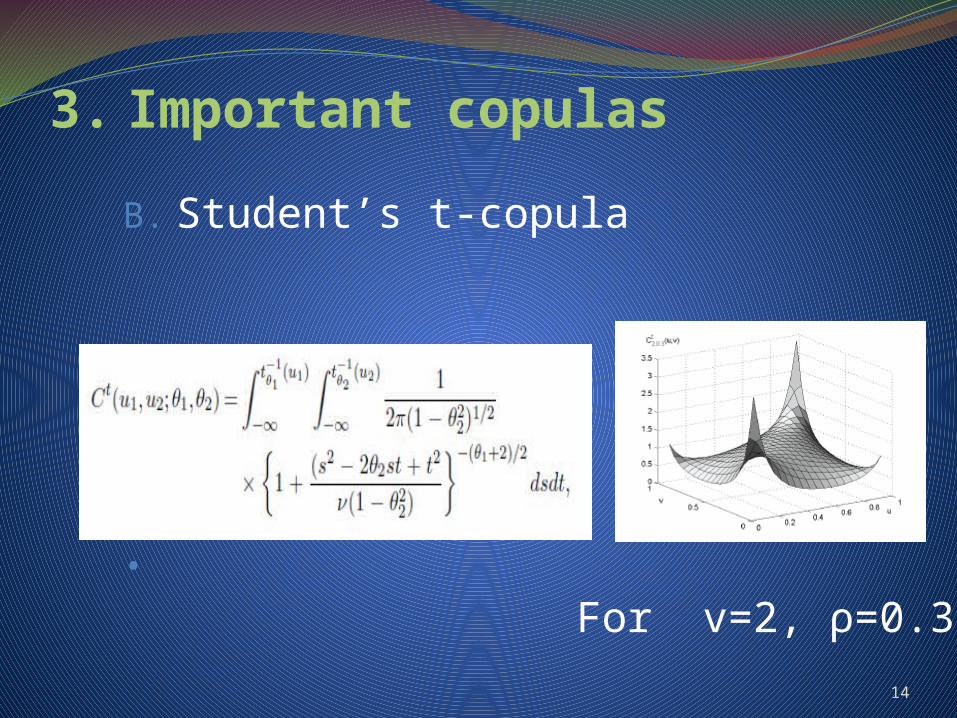

3. Important copulas

B. Student’s t-copula

• For v=2, ρ=0.3

14

3. Important copulas

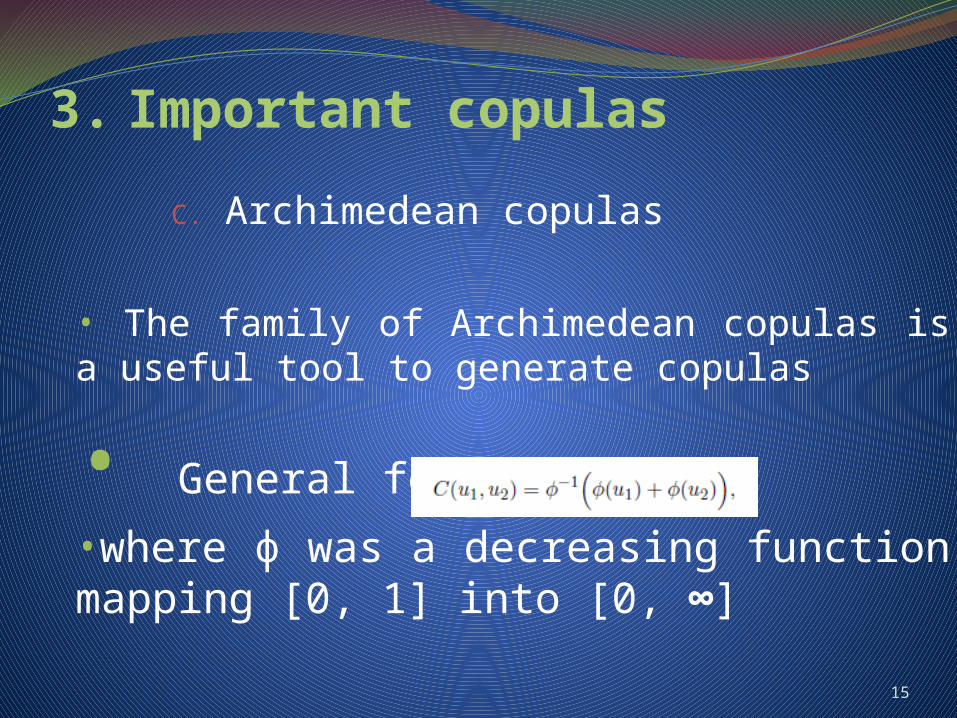

C. Archimedean copulas

• The family of Archimedean copulas is a useful tool to generate copulas

• General form :

•where ф was a decreasing function mapping [0, 1] into [0, ∞]

15

3. Important copulas

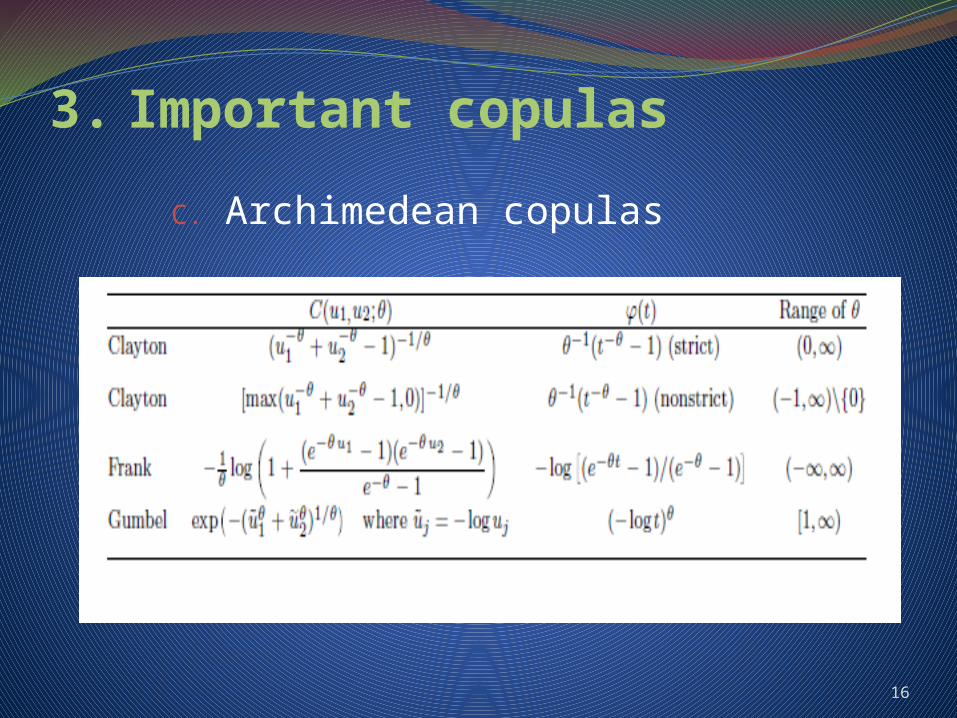

C. Archimedean copulas

•

16

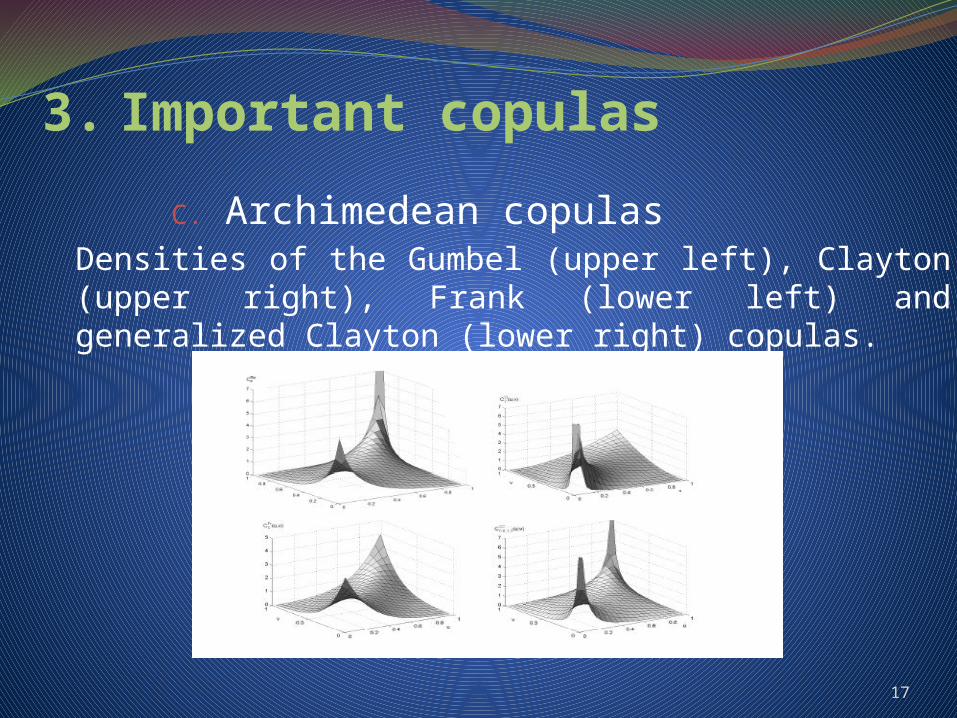

3. Important copulas

C. Archimedean copulasDensities of the Gumbel (upper left), Clayton (upper right), Frank (lower left) and generalized Clayton (lower right) copulas.

17

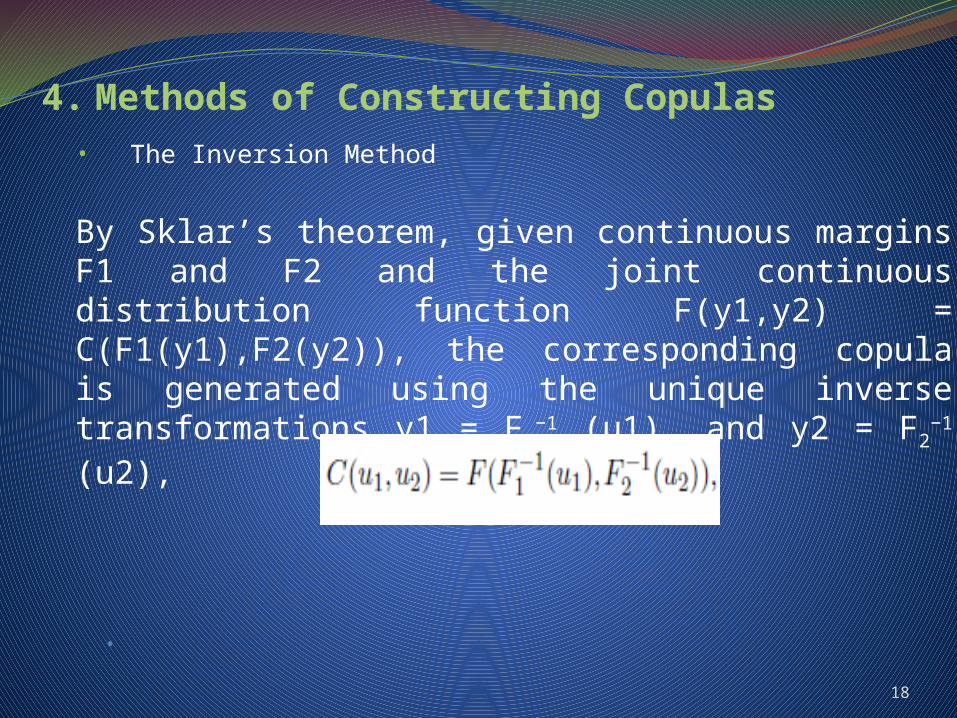

4. Methods of Constructing Copulas• The Inversion Method

By Sklar’s theorem, given continuous margins F1 and F2 and the joint continuous distribution function F(y1,y2) = C(F1(y1),F2(y2)), the corresponding copula is generated using the unique inverse transformations y1 = F1

−1 (u1), and y2 = F2−1 (u2),

• 18

4. Methods of Constructing Copulas

• The Inversion Method (example)

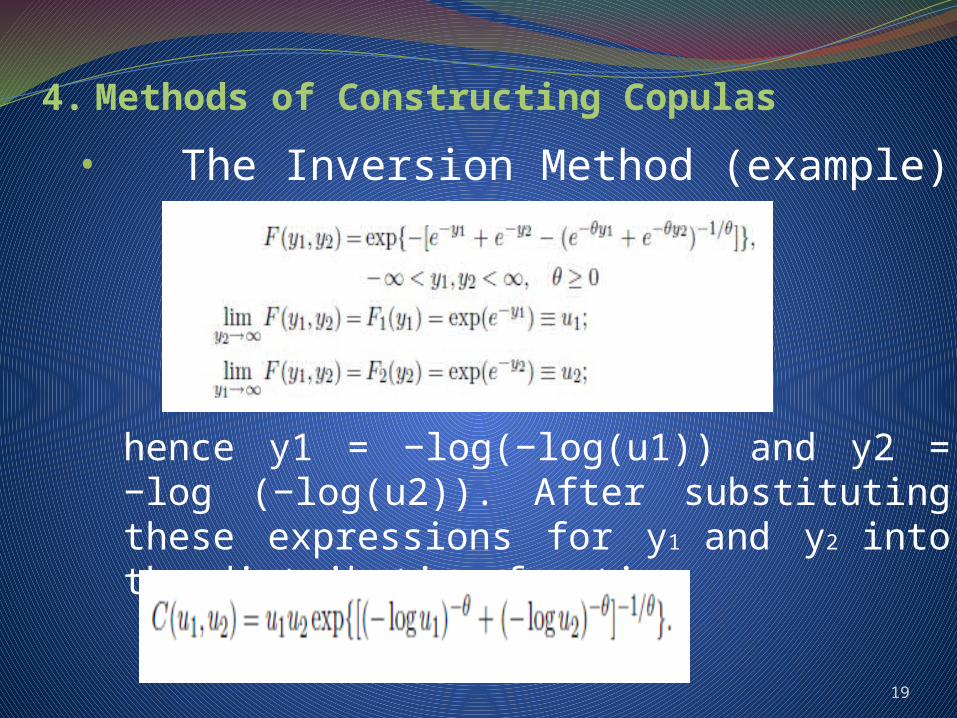

hence y1 = −log(−log(u1)) and y2 = −log (−log(u2)). After substituting these expressions for y1 and y2 into the distribution function

19

4. Methods of Constructing Copulas

• Other Methods

•Algebraic MethodsSome derivations of copulas begin with a relationship between marginals based on independence. Then this relationship is modified by introducing a dependence parameter and the corresponding copula is obtained.•Mixtures and Convex Sums

Given a copula C, its lower and upper bounds CL and CU, and the product copula Cp, a new copula can be constructed using a convex sum

20

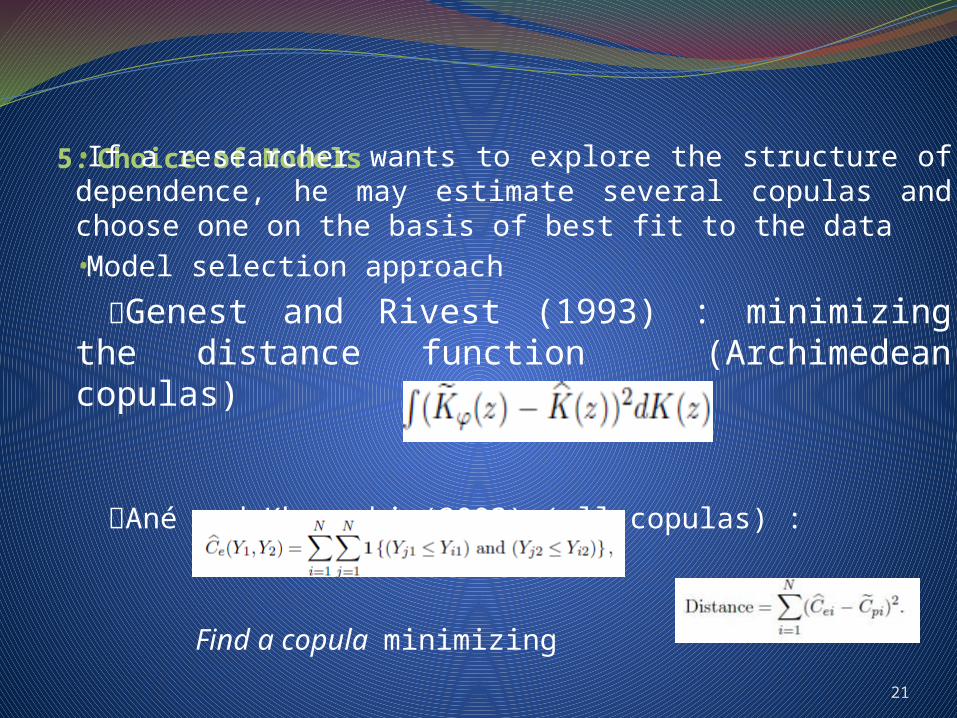

5. Choice of Models•If a researcher wants to explore the structure of dependence, he may estimate several copulas and choose one on the basis of best fit to the data•Model selection approach

Genest and Rivest (1993) : minimizing the distance function (Archimedean copulas)

Ané and Kharoubi (2003) (all copulas) :

Find a copula minimizing21

References•Everything you always wanted to know about copula, christian genest and anne-catherine favre, journal of hydrologic engineering © asce / july/august 2007

•Copula modeling: an introduction for practitioners ,pravin k. trivedi and david m. zimmer, foundations and trends in econometrics 2007

•Coping with copulas, thorsten schmidt, forthcoming in risk books "copulas - from theory to applications in finance“, 2006

•An introduction to copulas, Roger B. Nelsen, springer series in statistics 2006

•Understanding relationships using copulas, edward w. frees and emiliano a. valdez, north american actuarial journal, volume 2, number 1, 1998

22