presented by: jerry leemkuil field manager association risk management services federated insurance...

TRANSCRIPT

Presented by: Jerry LeemkuilField Manager Association Risk

Management ServicesFederated Insurance

Presented by: Jerry LeemkuilField Manager Association Risk

Management ServicesFederated Insurance

I am going to make it easy on you. Our Congress developed a flowchart for us to understand how the bill will be written and implemented.

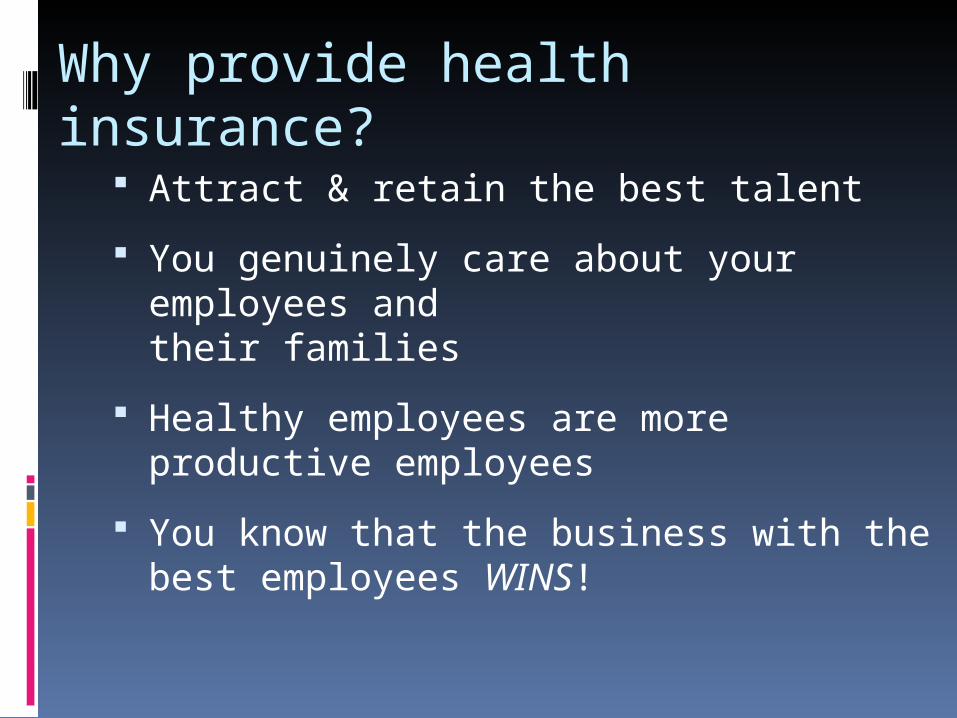

Why provide health insurance?

Attract & retain the best talent

You genuinely care about your employees and their families

Healthy employees are more productive employees

You know that the business with the best employees WINS!

Why else?

Contributions to the employee’s premiums are tax deductible

Employee premiums are not subject to Federal Income Tax, State Income Tax, Social Security, Medicare, Unemployment Tax, or Work Comp

Agenda What is PPACA (or ACA or

“ObamaCare”) What is “The Marketplace” or Exchange “Affordable” and “Valuable” Large Group versus Small Group Subsidies Available with ACA Will Premiums Rise?

Taxes associated with PPACA Health Insurance Options What is Federated doing to Respond?

What is ACA?

What is ACA?• Individual Mandate - 2014• Dependents until age 26• No annual or lifetime limits on care• No Preexisting Conditions - 2014• Expansion of Medicaid - 2014• Taxes on Health Care Industry - 2014• Health Insurance Exchange - 2014• Subsidies - 2014• New Medical Plans – Bronze, Silver,

Gold, and Platinum - 2014

Individual Requirement

Have health insurance on January 1, 2014 or pay a penalty

Open enrollment period October – December

Penalties

2014 - $95 per adult and $47.50 per child (up to $285 for a family) or 1.0% of family income, whichever is greater

2015 - $325 per adult and $162.50 per child (up to $975 for a family) or 2.0% of family income, whichever is greater

2016 - $695 per adult and $347.50 per child (up to $2,085 for a family) or 2.5% of family income, whichever is greater

No penalty for a single gap in coverage of less than 3 months in a year

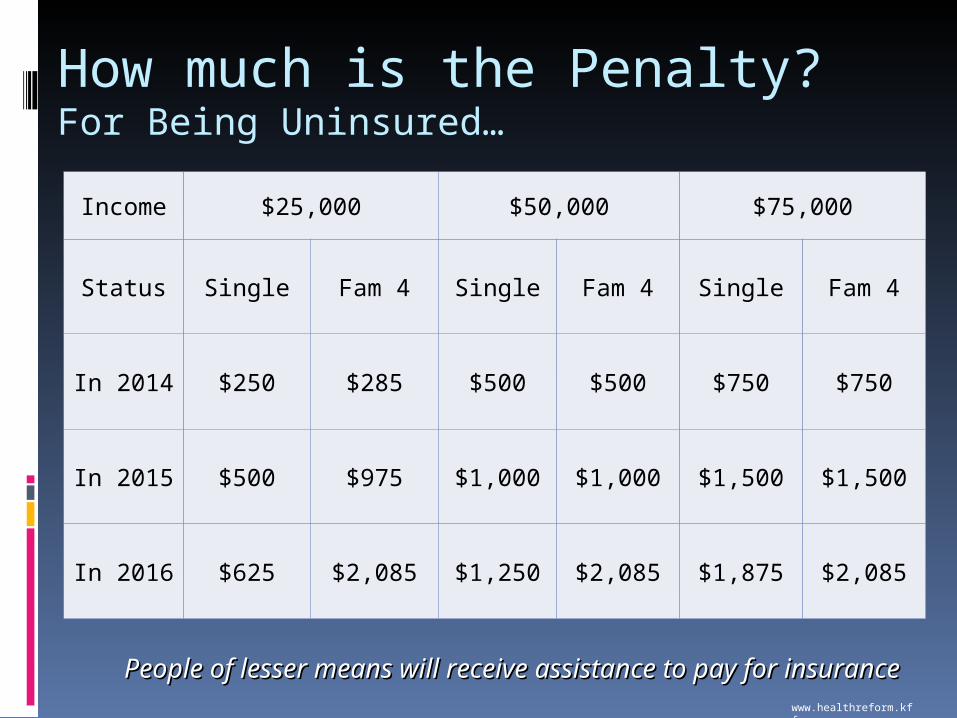

How much is the Penalty?For Being Uninsured…

Income $25,000 $50,000 $75,000

Status Single Fam 4 Single Fam 4 Single Fam 4

In 2014 $250 $285 $500 $500 $750 $750

In 2015 $500 $975 $1,000 $1,000 $1,500 $1,500

In 2016 $625 $2,085 $1,250 $2,085 $1,875 $2,085

People of lesser means will receive assistance to pay for insurancePeople of lesser means will receive assistance to pay for insurancewww.healthreform.kff.org

Small vs. Large Employers

“Affordable” Coverage

“Valuable” Coverage

Am I a Large Employer?

“Affordable” and “Valuable” “Affordable”

Less than 9.5% of W-2 wages

EE only-Dependents income is not part of this equation

“Valuable” Has Essential

Health Benefit (EHB)

Actuarial Value of at least 60% Bronze – 60% Silver – 70% Gold – 80% Platinum – 90%

For each month in 2013

A. Count the number of employees who worked 130

or more hours (these are Full Time EE’s)

B. Count the hours for employees who worked less

than 130 hours and divide by 120 = equivalent

FTE

Add A and B to determine FTEs for the month

ACA Impact on EmployersAm I a Large Employer?

For each month in 2013 (continued) Add the number of FTEs for each month in 2013

and divide by 12 = Average FTEs

If 51 or more – you are a large employer for all of

2014

What you are in 2014 depends on what you were in

2013

ACA Impact on EmployersAm I a Large Employer?

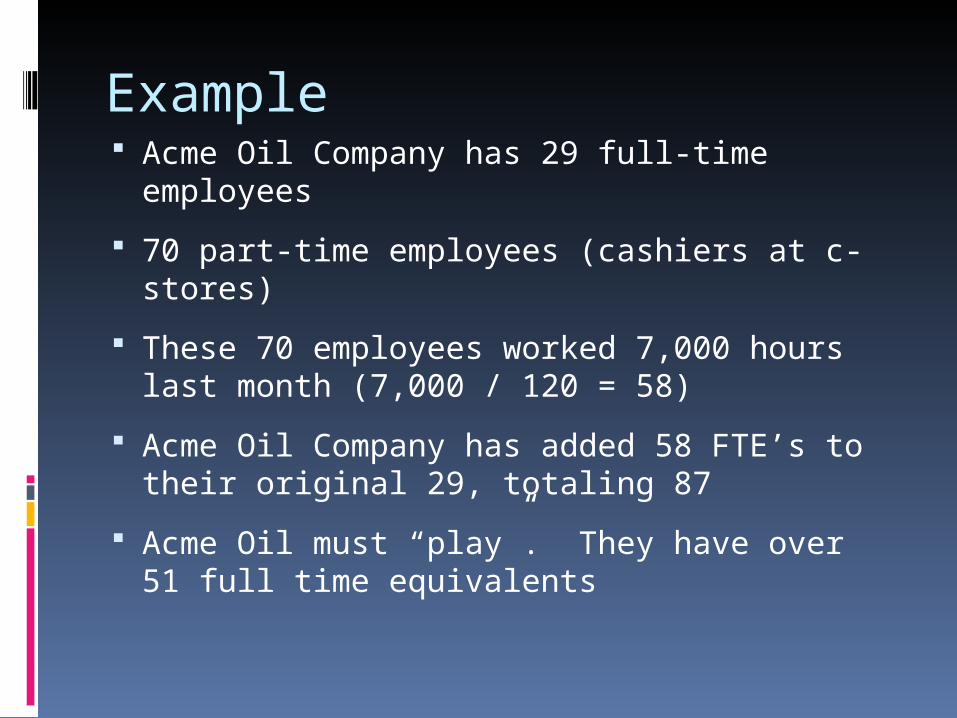

Example Acme Oil Company has 29 full-time

employees

70 part-time employees (cashiers at c-stores)

These 70 employees worked 7,000 hours last month (7,000 / 120 = 58)

Acme Oil Company has added 58 FTE’s to their original 29, totaling 87

Acme Oil must “play”. They have over 51 full time equivalents

Penalty* for Not Offering Insurance

True FTE x $166.67/mo = $2,000/yr

No penalty unless one or more employees obtains coverage through Public Exchange and receives a subsidy to purchase it.

* Delayed for large employers until 2015

Source: The Pay or Play Mandate for Large Employers, McKenna Long & Aldridge LLP

Employer MandateWhat if Coverage isn’t Good Enough? Coverage offered must be…

Affordable – cost the employee less than 9.5% of their income to participate.

Minimum value – actuarial value of 60% or more. Employer must then pay $250/mo = $3,000/yr

*for every “True” FTE that goes to the Exchange and obtains coverage with a tax credit subsidy.

* Delayed for large employers until 2015

Source: The Pay or Play Mandate for Large Employers, McKenna Long & Aldridge LLP

Large Employer Small Employer

Employer Mandate (Play or Pay Penalty) Yes Delayed No

Discrimination Testing Yes Likely Delayed Yes

Metal Tier Plan No – Meet MEC Yes

Compressed Age Rating No Yes

Compressed Gender Rating No Yes

Eliminate Pre-existing Condition Exclusion Yes Yes

Essential Health Benefits No Yes

$2,000 Deductible Constraint No Yes

$6,350 OOP Max Constraint Yes Yes

Underwriting Restriction (CAF) No Yes

Waiting Period Limited to 90 Days Yes Yes

Contrasting Impact on Large and Small Employers

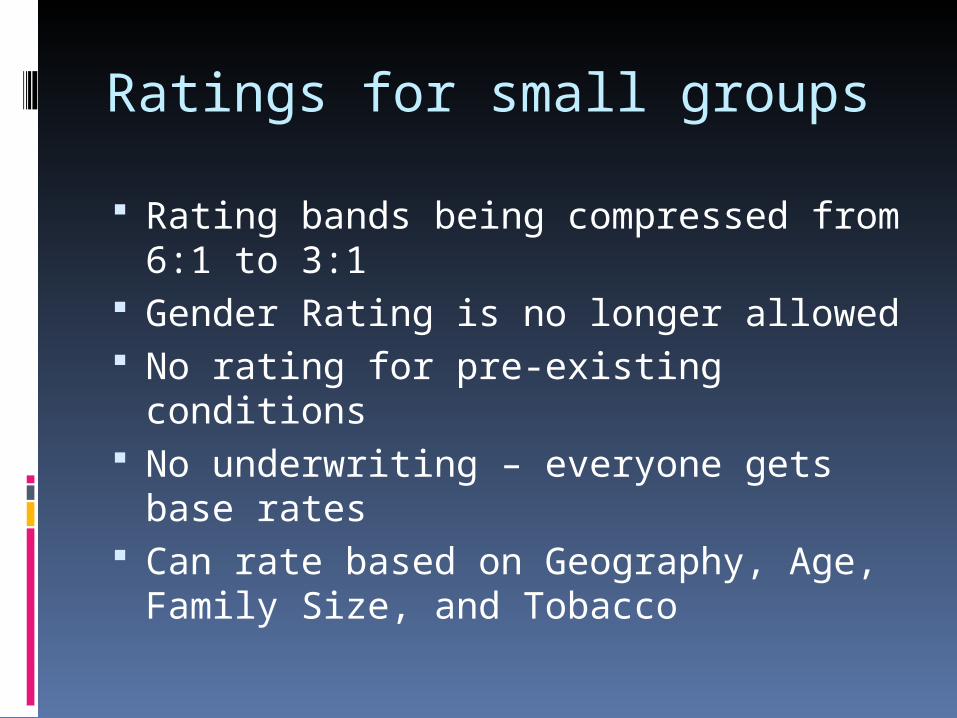

Ratings for small groups

Rating bands being compressed from 6:1 to 3:1

Gender Rating is no longer allowed No rating for pre-existing conditions No underwriting – everyone gets

base rates Can rate based on Geography, Age,

Family Size, and Tobacco

Rating for large groups

Can rate for medical history Allowed to underwrite - can pay less

or more than base rates Can rate based on Geography, Age,

Family Size, and Tobacco

Premium Tax Credit - Subsidy Tax Credits for people who earn up

to 4 times the Federal Poverty Level If an employer offers a plan to its

employees that is affordable and valuable, no subsidy will be provided to the employee

Medicaid & Subsidy ThresholdIn 2012 Dollars

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

1 Person 2 Person 3 Person 4 Person

400%

100%$44,680

$11,170

Eligibility will be based on household incomeEligibility will be based on household incomeSource:hhs.gov

$23,050$19,090$15,130

$60,520

$76,360

$92,200

Health Insurance Exchange Utah opted to not expand Medicaid Utah opted to let the Federal

Government put together its exchange

Enrollment opens on October 1, 2013 Website - HealthCare.gov

Will Premiums Increase?

Health Insurance Industry Fee (HIT Tax) $8 Billion in 2014

Increases year over year to $14.3 Billion in 2018

Following 2018 increases by premium growth

rate of industry

Estimated to be equivalent to 2.5% of premium in

2014

This “fee” is not tax deductible. Insurers must

pay the “fee” out of After-Tax Income. At 35% Corporate Tax Rate “Fee” equates to 3.85%

of premium in 2014

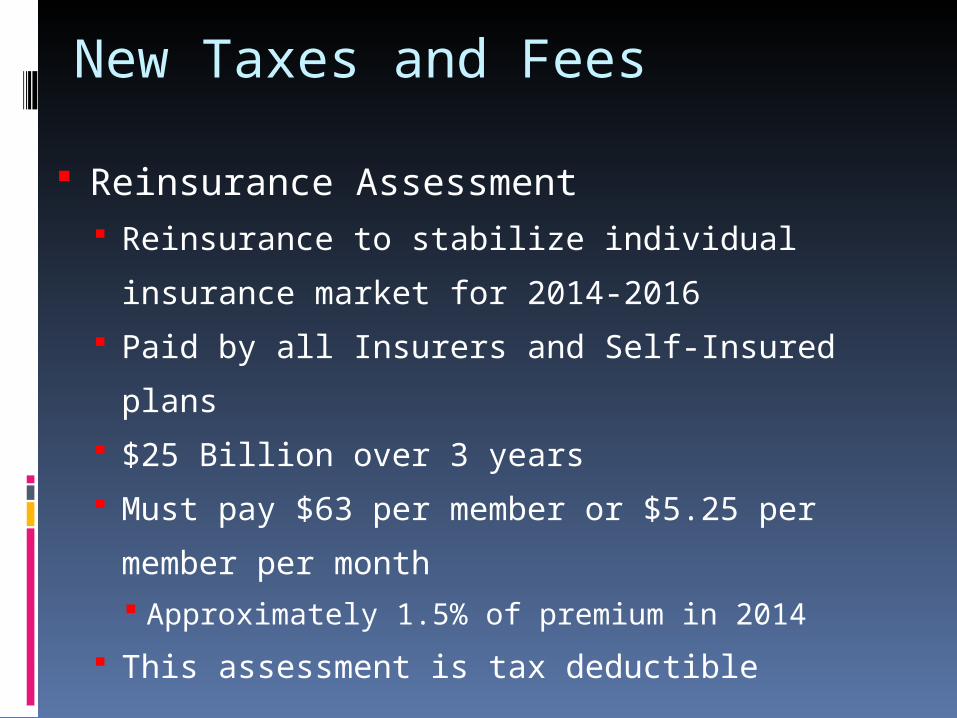

New Taxes and Fees

Reinsurance Assessment Reinsurance to stabilize individual insurance

market for 2014-2016

Paid by all Insurers and Self-Insured plans

$25 Billion over 3 years

Must pay $63 per member or $5.25 per

member per month Approximately 1.5% of premium in 2014

This assessment is tax deductible

New Taxes and Fees

Comparative Effectiveness Research Fee for

Patient Centered Outcome Research

Institute (PCORI)

Conduct Research to determine which

treatments work best

$1 per member per year, doubles to $2 in

2015

Paid by Insurer and also by HRA Plans

Equates to 0.3% of premium in 2014

New Taxes and Fees

HIT Tax

Reinsurance

PCORI

New Taxes and Fees Summary

2.5% before tax consideration

3.85% after tax consideration

1.5% of premium

0.3% of premium

4.3% to 5.65%

Premium rates must rise to fund these new taxes and fees.

New taxes and fees for pharmacology and medical services will also drive up costs and be passed through in premium.

Options for ACA

Stay on current rate change date (i.e. October 1, 2013 – October 1, 2014)

Comply with ACA on January 1, 2013 Drop Health Insurance and give

everyone a raise Change your plan year to December

1, 2013 (Delay for another year)

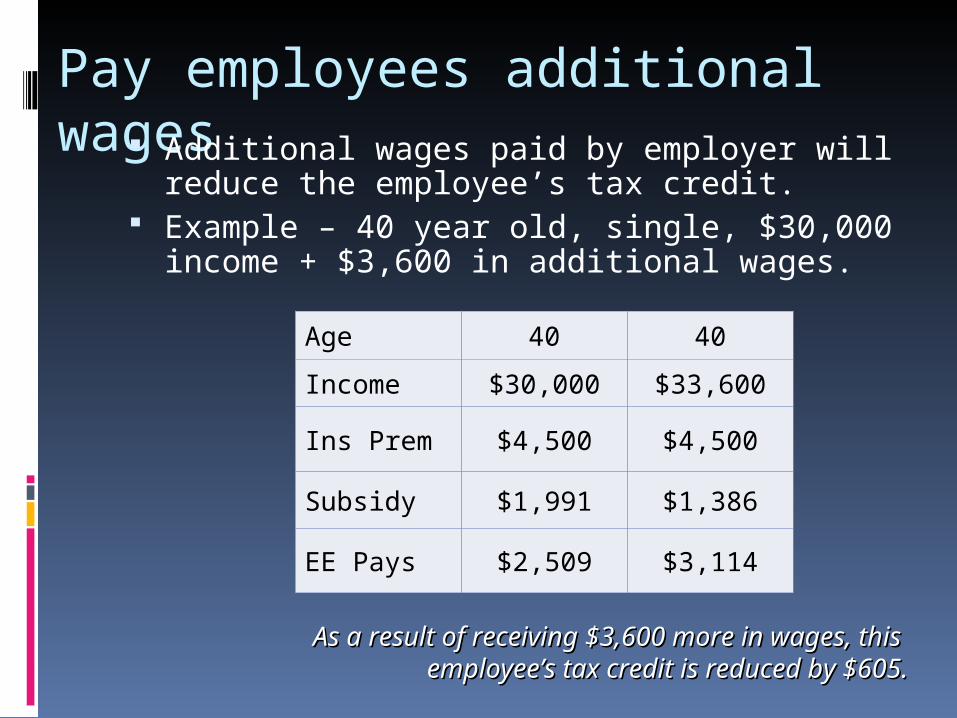

Pay employees additional wages Additional wages paid by employer will reduce

the employee’s tax credit. Example – 40 year old, single, $30,000 income

+ $3,600 in additional wages.

Age 40 40

Income $30,000 $33,600

Ins Prem $4,500 $4,500

Subsidy $1,991 $1,386

EE Pays $2,509 $3,114

As a result of receiving $3,600 more in wages, this As a result of receiving $3,600 more in wages, this employee’s tax credit is reduced by $605.employee’s tax credit is reduced by $605.

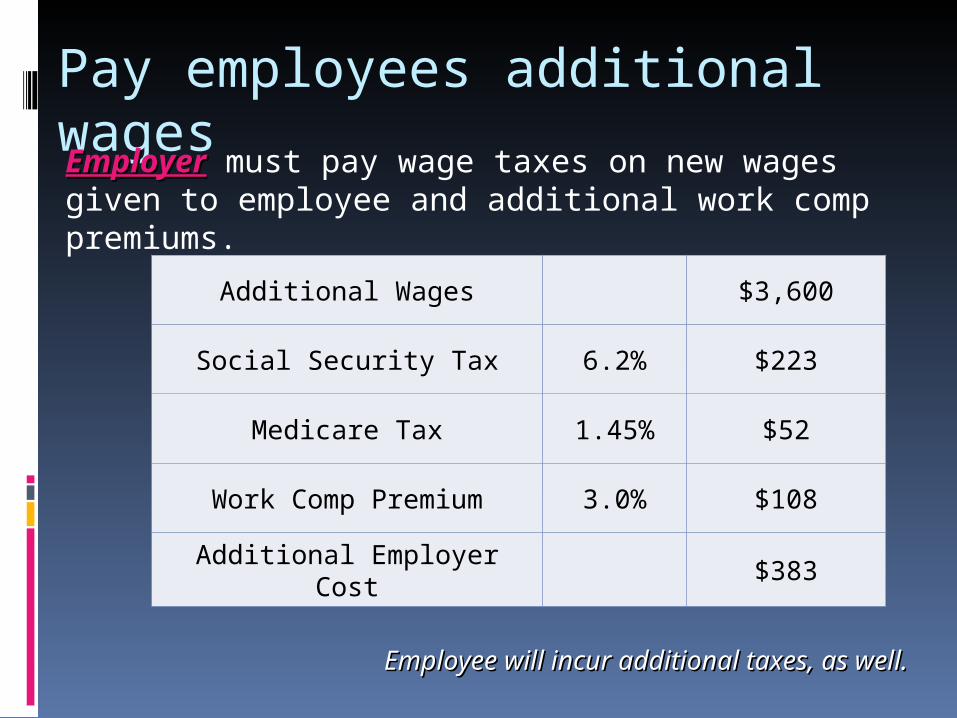

Pay employees additional wages

Additional Wages $3,600

Social Security Tax 6.2% $223

Medicare Tax 1.45% $52

Work Comp Premium 3.0% $108

Additional Employer Cost

$383

EmployerEmployer must pay wage taxes on new wages given to employee and additional work comp premiums.

Employee will incur additional taxes, as well.Employee will incur additional taxes, as well.

Pay employees additional wages

Additional Wages $3,600

Social Security Tax 6.2% $223

Medicare Tax 1.45% $52

State Income Tax 5.0% $180

Federal Income Tax 15.0% $540

Additional Employee Cost

$995

Employee must pay wage taxes on new wages along with Federal and State income taxes at marginal tax rates.

Pay employees additional wages

New Wages $3,600

Reduction in Tax Credit $605

Additional Employer Taxes/Costs

$383

Additional Employee Taxes/Costs

$995

Net Purchasing Power of Wages

$1,983

In this example, over half of the increase inIn this example, over half of the increase inwages given to the employee has been eroded!!wages given to the employee has been eroded!!

Let’s review our example:

Should I consider delaying ACA?

Have less than 50 full time equivalent employees

Deductible is currently over $2,000 Healthy group Young group You want rates locked (certainty) to

see how 2014 plays out

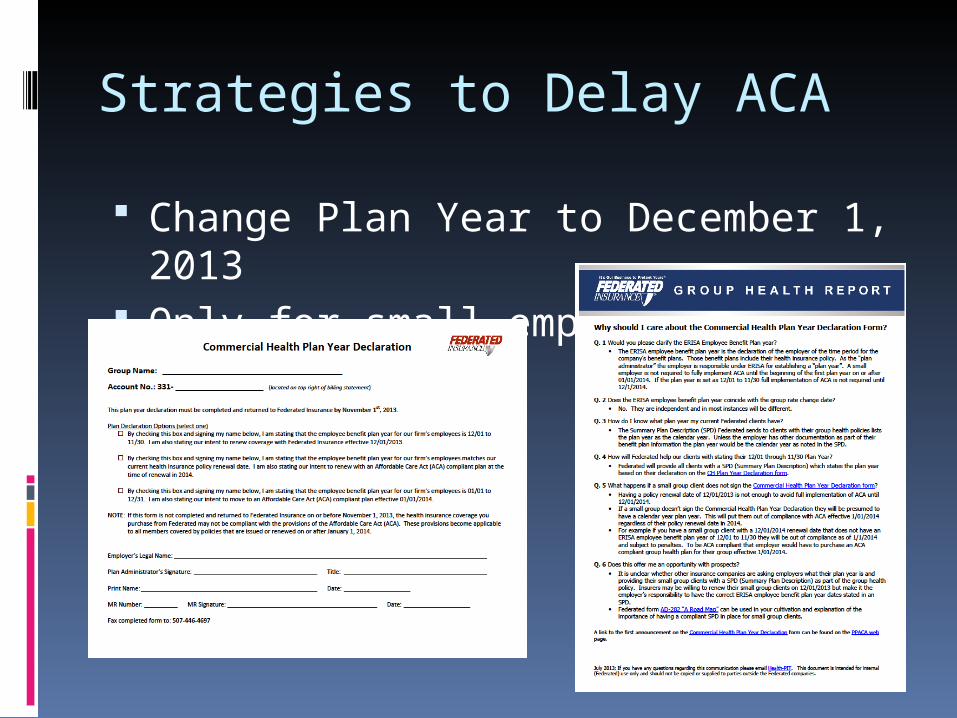

Strategies to Delay ACA

Change Plan Year to December 1, 2013

Only for small employers

ACA – Federated’s Response Substantial investment into the

development of Federated’s “Private Exchange”

Local Marketing Representatives equipped with tools for effective one-on-one discussions offering solutions for business owners. Marketing Representatives are receiving ongoing training from Federated on the latest developments regarding ACA

One “take-away” for you today…

Employee Notices are required to be provided to

all employees by 10/1/2013

Employer Requirements 3 written notices required:

Existence of the Marketplace (aka public exchange) including contact information and a description of services provided by the Marketplace

Must inform the employee they may be eligible for a premium tax credit through the Marketplace

The notice must tell the employee if they purchase health insurance through the Marketplace, they may lose the employer contribution to any health benefits plan and all or portion of such contribution may be excludable from income for Federal Income tax purposes